Embed Size (px)

Citation preview

4th Annual

Developing European Gas Supply Infrastructure

Market development, economics and strategy

4 easy ways to register:Visit: www.events.platts.comCall: +44-(0)-20-7176-6300

Fax: +44-(0)-20-7176-8512Email: [email protected]

AAtttteennddiinngg tthhee ccoonnffeerreennccee wwiillll eennaabbllee ddeelleeggaatteess ttoo::

� EEvvaalluuaattee the current macro-environment – Is overcapacityset to continue? How will this impact projects, prices andpolices moving forward?

� AAsssseessss the current challenges ahead for EU gas policies,meeting sustainability goals and opening new routes forsecure supplies

� RReecceeiivvee the latest industry case studies and operationalupdates from current and planned infrastructure projects,while highlighting key project challenges and successes

� DDiissccoovveerr how pricing patterns are changing – Will spotprevail long-term?

� IIddeennttiiffyy the current investment climate available to securenew supplies to Europe

� HHeeaarr how the internal market is progressing

� LLeeaarrnn whether gas purchasing blocks are the new solution

27-28 October 2010Marriott BrusselsBrussels, Belgium

Register by 10 September 2010 and save $200

Executive Sponsor Exhibitor ExhibitorLanyard and Name Badge Sponsor

Principal media partners

”“ Platts is the world's most

trusted and valued source

of global energy information

and intelligence

Supporting organisations

Platts is the world’s most

trusted and valued source

of global energy information

and intelligence

The European gas industry has been on a rollercoaster ride. Last year European gas demand fell on the back ofeconomic recession, access to growing global LNG production was boosted by the opening of new terminalsincluding South Hook and Dragon LNG in the UK, and interest in unconventional gas production spread from theUS to Poland and Germany. Spot gas prices fell to half the level of oil-indexed gas causing long-term contractsto be renegotiated. While prices have bounced back in recent months, the key questions remain: How long willthe gas market glut continue and can new infrastructure be developed in this changing market?

Platts 4th Annual Developing European Gas Supply Infrastructure conference will tackle all these issuesand many more. It will provide a focused outlook on Europe’s developing gas market, ranging from security ofsupply and the wave of pipeline project development, from the Baltic to the Black Sea, to pricing dynamics andpolicy direction. Building upon its highly successful history, the conference will once again bring togetherEurope’s leading gas utilities, regulators, traders, pipeline developers and observers and offers offers unrivalledbusiness and networking opportunities.

Key topics to be covered include:� Adapting to overcapacity, remaining competitive – Understanding the current and future macro

environment� Challenges ahead for EU gas policies: Meeting sustainability goals and opening new routes for secure

supplies� From vision to implementation: Developing an efficient demand delivering European gas supply

infrastructure� Trading, pricing and European hub development update� Looking ahead: Where next for the European gas market?

Early Bird Discount – Register by 10 September 2010 and SAVE $200 off your registration feeTeam Discount – Register 3 or more attendees simultaneously and SAVE $459 per personFor more information please contact Stacey Knox, telephone ++4444--((00))--2200--77117766--66330000 or emailccoonnff__rreeggiissttrraattiioonnss@@ppllaattttss..ccoomm

Supporting media partners

"Very good, an excellent and up to date overview of the most relevant issues in the area."E-control

Programme

Visit: www.events.platts.com • Call: +44-(0)-20-7176-6300 • Email: [email protected]

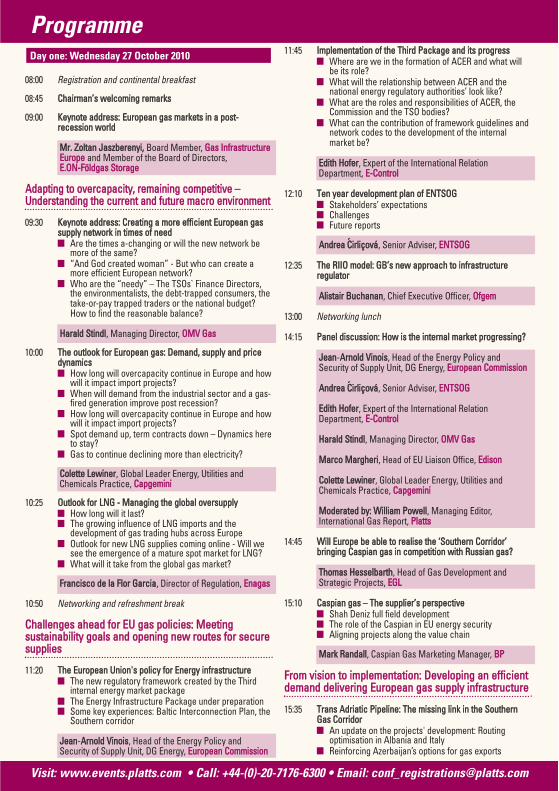

008:00 Registration and continental breakfast

08:45 CChhaaiirrmmaann’’ss wweellccoommiinngg rreemmaarrkkss

09:00 KKeeyynnoottee aaddddrreessss:: EEuurrooppeeaann ggaass mmaarrkkeettss iinn aa ppoosstt--rreecceessssiioonn wwoorrlldd

MMrr.. ZZoollttaann JJaasszzbbeerreennyyii,, Board Member, GGaass IInnffrraassttrruuccttuurreeEEuurrooppee and Member of the Board of Directors, EE..OONN--FFööllddggaass SSttoorraaggee

AAddaappttiinngg ttoo oovveerrccaappaacciittyy,, rreemmaaiinniinngg ccoommppeettiittiivvee ––UUnnddeerrssttaannddiinngg tthhee ccuurrrreenntt aanndd ffuuttuurree mmaaccrroo eennvviirroonnmmeenntt

09:30 KKeeyynnoottee aaddddrreessss:: CCrreeaattiinngg aa mmoorree eeffffiicciieenntt EEuurrooppeeaann ggaassssuuppppllyy nneettwwoorrkk iinn ttiimmeess ooff nneeeedd� Are the times a-changing or will the new network be

more of the same?� “And God created woman” - But who can create a

more efficient European network?� Who are the “needy” – The TSOs` Finance Directors,

the environmentalists, the debt-trapped consumers, thetake-or-pay trapped traders or the national budget?How to find the reasonable balance?

HHaarraalldd SSttiinnddll, Managing Director, OOMMVV GGaass

10:00 TThhee oouuttllooookk ffoorr EEuurrooppeeaann ggaass:: DDeemmaanndd,, ssuuppppllyy aanndd pprriicceeddyynnaammiiccss � How long will overcapacity continue in Europe and how

will it impact import projects?� When will demand from the industrial sector and a gas-

fired generation improve post recession? � How long will overcapacity continue in Europe and how

will it impact import projects?� Spot demand up, term contracts down – Dynamics here

to stay?� Gas to continue declining more than electricity?

CCoolleettttee LLeewwiinneerr, Global Leader Energy, Utilities andChemicals Practice, CCaappggeemmiinnii

10:25 OOuuttllooookk ffoorr LLNNGG -- MMaannaaggiinngg tthhee gglloobbaall oovveerrssuuppppllyy� How long will it last?� The growing influence of LNG imports and the

development of gas trading hubs across Europe� Outlook for new LNG supplies coming online - Will we

see the emergence of a mature spot market for LNG?� What will it take from the global gas market?

FFrraanncciissccoo ddee llaa FFlloorr GGaarrcciiaa, Director of Regulation, EEnnaaggaass

10:50 Networking and refreshment break

CChhaalllleennggeess aahheeaadd ffoorr EEUU ggaass ppoolliicciieess:: MMeeeettiinnggssuussttaaiinnaabbiilliittyy ggooaallss aanndd ooppeenniinngg nneeww rroouutteess ffoorr sseeccuurreessuupppplliieess

11:20 TThhee EEuurrooppeeaann UUnniioonn''ss ppoolliiccyy ffoorr EEnneerrggyy iinnffrraassttrruuccttuurree� The new regulatory framework created by the Third

internal energy market package� The Energy Infrastructure Package under preparation� Some key experiences: Baltic Interconnection Plan, the

Southern corridor

JJeeaann-AArrnnoolldd VViinnooiiss, Head of the Energy Policy andSecurity of Supply Unit, DG Energy, EEuurrooppeeaann CCoommmmiissssiioonn

11:45 IImmpplleemmeennttaattiioonn ooff tthhee TThhiirrdd PPaacckkaaggee aanndd iittss pprrooggrreessss� Where are we in the formation of ACER and what will

be its role? � What will the relationship between ACER and the

national energy regulatory authorities’ look like? � What are the roles and responsibilities of ACER, the

Commission and the TSO bodies? � What can the contribution of framework guidelines and

network codes to the development of the internalmarket be?

EEddiitthh HHooffeerr, Expert of the International RelationDepartment, EE--CCoonnttrrooll

12:10 TTeenn yyeeaarr ddeevveellooppmmeenntt ppllaann ooff EENNTTSSOOGG � Stakeholders’ expectations� Challenges� Future reports

AAnnddrreeaa ´́CCiirrlliiççoovváá, Senior Adviser, EENNTTSSOOGG

12:35 TThhee RRIIIIOO mmooddeell:: GGBB’’ss nneeww aapppprrooaacchh ttoo iinnffrraassttrruuccttuurreerreegguullaattoorr

AAlliissttaaiirr BBuucchhaannaann, Chief Executive Officer, OOffggeemm

13:00 Networking lunch

14:15 PPaanneell ddiissccuussssiioonn:: HHooww iiss tthhee iinntteerrnnaall mmaarrkkeett pprrooggrreessssiinngg??

JJeeaann-AArrnnoolldd VViinnooiiss, Head of the Energy Policy andSecurity of Supply Unit, DG Energy, EEuurrooppeeaann CCoommmmiissssiioonn

AAnnddrreeaa ´́CCiirrlliiççoovváá, Senior Adviser, EENNTTSSOOGG

EEddiitthh HHooffeerr, Expert of the International RelationDepartment, EE--CCoonnttrrooll

HHaarraalldd SSttiinnddll, Managing Director, OOMMVV GGaass

MMaarrccoo MMaarrgghheerrii, Head of EU Liaison Office, EEddiissoonn

CCoolleettttee LLeewwiinneerr, Global Leader Energy, Utilities andChemicals Practice, CCaappggeemmiinnii

MMooddeerraatteedd bbyy:: WWiilllliiaamm PPoowweellll, Managing Editor,International Gas Report, PPllaattttss

14:45 WWiillll EEuurrooppee bbee aabbllee ttoo rreeaalliissee tthhee ‘‘SSoouutthheerrnn CCoorrrriiddoorr’’bbrriinnggiinngg CCaassppiiaann ggaass iinn ccoommppeettiittiioonn wwiitthh RRuussssiiaann ggaass??

TThhoommaass HHeesssseellbbaarrtthh, Head of Gas Development andStrategic Projects, EEGGLL

15:10 CCaassppiiaann ggaass –– TThhee ssuupppplliieerr’’ss ppeerrssppeeccttiivvee� Shah Deniz full field development� The role of the Caspian in EU energy security� Aligning projects along the value chain

MMaarrkk RRaannddaallll, Caspian Gas Marketing Manager, BBPP

FFrroomm vviissiioonn ttoo iimmpplleemmeennttaattiioonn:: DDeevveellooppiinngg aann eeffffiicciieennttddeemmaanndd ddeelliivveerriinngg EEuurrooppeeaann ggaass ssuuppppllyy iinnffrraassttrruuccttuurree

15:35 TTrraannss AAddrriiaattiicc PPiippeelliinnee:: TThhee mmiissssiinngg lliinnkk iinn tthhee SSoouutthheerrnnGGaass CCoorrrriiddoorr� An update on the projects' development: Routing

optimisation in Albania and Italy � Reinforcing Azerbaijan’s options for gas exports

Day one: Wednesday 27 October 2010

Register by 10 September 2010 and SAVE $200

to Europe� TAP’s status within the EU

MMaarriijjaa SSaavvoovvaa VVeellkkoosskkii,, Commercial Manager, TTrraannssAAddrriiaattiicc PPiippeelliinnee ((TTAAPP))

16:00 Networking and refreshment break

16:30 NNoorrdd SSttrreeaamm:: SSeeccuurree ggaass ssuuppppllyy ffoorr EEuurrooppee -- CCuurrrreenntt ssttaattuussooff tthhee ppiippeelliinnee pprroojjeecctt tthhrroouugghh tthhee BBaallttiicc SSeeaa

SSeebbaassttiiaann SSaassss,, Head of EU Representation, NNoorrdd SSttrreeaamm

16:55 WWhhiittee SSttrreeaamm,, aann EEUU pprriioorriittyy pprroojjeecctt aanndd aann eesssseennttiiaallccoommppoonneenntt ooff tthhee ‘‘SSoouutthheerrnn CCoorrrriiddoorr’’� Synergy with other Southern Corridor projects� Technical challenges� Economic, legal, commercial and environmental aspects� Current status of the White Stream project

RRoobbeerrttoo PPiirraannii,, Chairman, WWhhiittee SSttrreeaamm PPiippeelliinneeCCoonnssoorrttiiuumm

17:20 LLNNGG vveerrssuuss ppiippeelliinnee ggaass iinn SSppaaiinn:: AA nneeww sscceennaarriioo� Interconnection between France and Spain� Medgaz pipeline� Security of supply – A European common vision� Spain - A new gas entry point into the EU

EErrnneessttoo PPaarrrriillllaa, Gas Operations Manager, IIbbeerrddrroollaa GGeenneerraacciióónn

17:45 TTuurrkkeeyy aass tthhee ffoouurrtthh ggaattee ffoorr EEuurrooppee –– AAnnaattoolliiaann ggaass ssuuppppllyyccoorrrriiddoorr � Turkey as the fourth gas supply corridor for Europe: Role

of Turkish NOCs in Turkish hinterland� Highlights of BOTAS Gas Master Plan 2010-2030:

Transformation of the local champion to a regional player� Zoom to the elements of fourth gate: Upstream

prospects, projects, infrastructures, Anatolian hub,storages, market, etc.

LLeevveenntt ÖÖzzggüüll,, Strategy and Business Development Managerand Head of Gas Master Plan Commission, BBOOTTAASS

18:10 Networking reception

08:00 Registration and continental breakfast

08:45 CChhaaiirrmmaann’’ss wweellccoommiinngg rreemmaarrkkss aanndd rreevviieeww ooff ddaayy oonnee

TTrraaddiinngg,, pprriicciinngg aanndd EEuurrooppeeaann hhuubb ddeevveellooppmmeenntt uuppddaattee

09:00 KKeeyynnoottee aaddddrreessss:: TThhee vviittaall rroollee ooff vviirrttuuaall hhuubbss iinn EEuurrooppee’’ssggaass ssuuppppllyy iinnffrraassttrruuccttuurree� A trader’s perspective on the development of European

gas hubs so far� How can hubs help to enable truly pan-European gas

trading?� Where do we go next?

GGaarreetthh GGrriiffffiitthhss, Chief Commercial Officer, EE..OONN EEnneerrggyyTTrraaddiinngg

09:30 GGaass pprriiccee oouuttllooookk –– WWiillll ssppoott pprreevvaaiill oovveerr lloonngg--tteerrmm??� A temporary movement or long-term shift to spot for

utilities?

� Will oil indexed price formation continue to dominate LTcontracts?

� Pipeline and LNG in competition� Arbitrage opportunities available� Gas prices to harmonise?

WWiilllliiaamm PPoowweellll, Managing Editor, International Gas Report,PPllaattttss

09:55 TThhee uunncceerrttaaiinn ffuuttuurree ooff ggaass ttrraaddiinngg rreegguullaattiioonn� Relevance of DG Energy’s tailor-made regime and of DG

Market’s Market Abuse Directive: New regulation onmarket integrity and transparency for all gas marketsparticipants

� Transparency of trade and fundamental gas data: Whatkind of transparency do we need?

� New financial market legislation, e.g. for mandatory CCPclearing: Do we need to centrally clear every trade?

KKaarrll-PPeetteerr HHoorrssttmmaannnn, Head of Markets Regulation, RRWWEE SSuuppppllyy aanndd TTrraaddiinngg

10:20 GGaass bbaallaanncciinngg –– TThhee qquueesstt ffoorr mmaarrkkeett bbaasseedd rruulleess� Roles and responsibilities for TSOs and network users� Trading and its role in system balancing � Developing rules that encourage the wholesale market

NNiiggeell SSiissmmaann, Senior Adviser, EENNTTSSOOGG

10:45 Networking and refreshment break

11:15 AArree ggaass ppuurrcchhaassiinngg bblloocckkss tthhee nneeww ssoolluuttiioonn??� Understanding the difficulties in buying Caspian gas� How would block purchasing work in practice?

LLeeiigghh HHaanncchheerr, Counsel, AAlllleenn && OOvveerryy

LLooookkiinngg aahheeaadd:: WWhheerree nneexxtt ffoorr tthhee EEuurrooppeeaann ggaassmmaarrkkeett??

11:40 TThhee ffiinnaanncciiaall ccrriissiiss aanndd iittss aaffffeecctt oonn EEuurrooppeeaann ggaass ssuuppppllyypprroojjeeccttss –– AA bbrreeaatthhiinngg ssppaaccee oorr aa ddaammaaggiinngg vvaaccuuuumm ffoorriinnvveessttmmeenntt??� What are investors looking for?� Attracting commercial lenders� Contracting methods and potential pitfalls� Reducing costs

LLáásszzllóó VVaarrrróó, Senior Vice President, Strategy Development,MMOOLL

12:05 DDeevveellooppiinngg nnaattuurraall ggaass mmaarrkkeett iinn CCeennttrraall EEuurrooppee� New sources of supply� Interconnections development� Role of Polish transmission system

PPiioottrr KKuu´́ss, Director of Brussels Office, GGAAZZ--SSYYSSTTEEMM

12:30 IIssssuueess ooff iinnvveessttmmeenntt iinn ccrroossss bboorrddeerr ccaappaacciittyy

MMiikkee YYoouunngg, Business Development Manager, GasTransportation, CCeennttrriiccaa EEnneerrggyy

12:55 AAnnaallyyssiinngg tthhee mmaarrkkeett ffoorr ssttoorraaggee ddeevveellooppmmeenntt iinn EEuurrooppee

JJaann IInnggwweerrsseenn, Vice President - Infrastructure andRegulatory Affairs, DDOONNGG EEnneerrggyy MMaarrkkeettss

13:20 End of conference

Day two: Thursday 28 October 2010

Sponsorship opportunities

To find out more information on the opportunities available please contact Michelle ThorbyPhone: +44-(0)-20-7176-6229 E-mail: [email protected]

Sponsorship of Platts 4th Annual DevelopingEuropean Gas Supply Infrastructure conferenceoffers you an unparalleled opportunity to be associatedwith the Platts’ brand and it will demonstrate yourorganisation’s strengths and capabilities to anaudience of senior industry decision makers. Thisopportunity will enable you to:

• Build lasting relationships with senior decisionmakers

• Enhance your visibility through Platts’ multi-channelmarketing platforms

• Showcase your business activities while beingassociated with the world’s leading provider ofenergy information

Hotel informationMarriott BrusselsRue Auguste Orts 3-7/Grand PlaceBrussels, 1000BelgiumTel: +32-2-516-92-00

A limited number of rooms have been reserved for Platts 4th AnnualDeveloping European Gas Supply Infrastructure conference participantsat the Marriott Brussels Hotel at the preferential rates listed below. Thediscounted rates are for the nights of 26 and 27 October 2010 only and willbe honoured until 5th October 2010.

Room rates:� Single or double occupancy ee199*This rate is inclusive of VAT and exclusive of breakfast

Reservations

� To book a room, please contact the hotel directly by either • Telephone +32-2-505-2500• Email [email protected] • Fax +32-2-505-2473

Be sure to mention that you are attending the Platts conference in order to receive the preferential rates. Pleaserefer to the event website for further details and booking code.

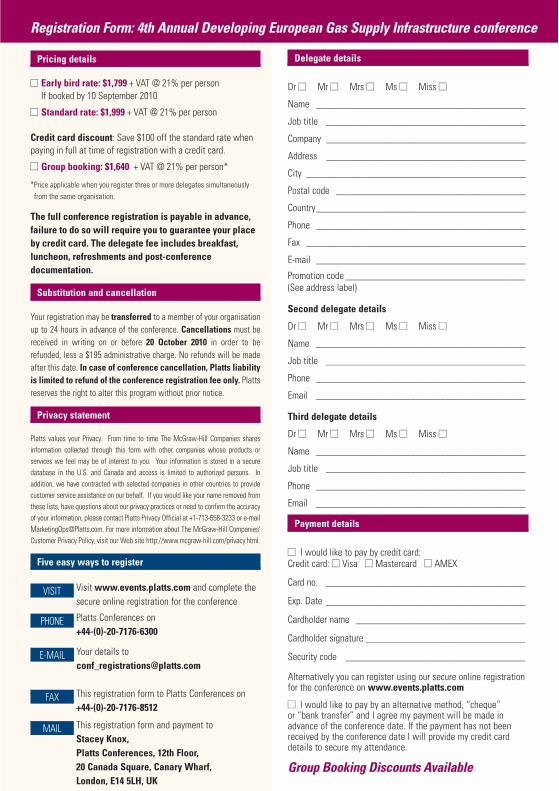

Pricing details

�� Early bird rate: $1,799 + VAT @ 21% per person If booked by 10 September 2010

�� Standard rate: $1,999 + VAT @ 21% per person

Credit card discount: Save $100 off the standard rate whenpaying in full at time of registration with a credit card.

�� Group booking: $1,640 + VAT @ 21% per person*

*Price applicable when you register three or more delegates simultaneouslyfrom the same organisation.

The full conference registration is payable in advance,failure to do so will require you to guarantee your placeby credit card. The delegate fee includes breakfast,luncheon, refreshments and post-conferencedocumentation.

Substitution and cancellation

Your registration may be transferred to a member of your organisationup to 24 hours in advance of the conference. Cancellations must bereceived in writing on or before 20 October 2010 in order to berefunded, less a $195 administrative charge. No refunds will be madeafter this date. In case of conference cancellation, Platts liabilityis limited to refund of the conference registration fee only. Plattsreserves the right to alter this program without prior notice.

Privacy statement

Platts values your Privacy. From time to time The McGraw-Hill Companies sharesinformation collected through this form with other companies whose products orservices we feel may be of interest to you. Your information is stored in a securedatabase in the U.S. and Canada and access is limited to authorized persons. Inaddition, we have contracted with selected companies in other countries to providecustomer service assistance on our behalf. If you would like your name removed fromthese lists, have questions about our privacy practices or need to confirm the accuracyof your information, please contact Platts Privacy Official at +1-713-658-3233 or [email protected]. For more information about The McGraw-Hill Companies'Customer Privacy Policy, visit our Web site http://www.mcgraw-hill.com/privacy.html.

Five easy ways to register

Visit www.events.platts.com and complete thesecure online registration for the conference

Platts Conferences on +44-(0)-20-7176-6300

Your details to [email protected]

This registration form to Platts Conferences on+44-(0)-20-7176-8512

This registration form and payment to Stacey Knox, Platts Conferences, 12th Floor,20 Canada Square, Canary Wharf, London, E14 5LH, UK

FAX

PHONE

VISIT

Delegate details

Dr �� Mr �� Mrs �� Ms �� Miss ��

Name __________________________________________

Job title ________________________________________

Company ________________________________________

Address ________________________________________

City ____________________________________________

Postal code ______________________________________

Country__________________________________________

Phone __________________________________________

Fax ____________________________________________

E-mail __________________________________________

Promotion code ____________________________________(See address label)

Second delegate details

Dr �� Mr �� Mrs �� Ms �� Miss ��

Name __________________________________________

Job title ________________________________________

Phone __________________________________________

Email __________________________________________

Third delegate details

Dr �� Mr �� Mrs �� Ms �� Miss ��

Name __________________________________________

Job title ________________________________________

Phone __________________________________________

Email __________________________________________

Payment details

�� I would like to pay by credit card: Credit card: �� Visa �� Mastercard �� AMEX

Card no. ________________________________________

Exp. Date ________________________________________

Cardholder name __________________________________

Cardholder signature ________________________________

Security code ____________________________________

Alternatively you can register using our secure online registrationfor the conference on www.events.platts.com

�� I would like to pay by an alternative method, “cheque” or “bank transfer” and I agree my payment will be made inadvance of the conference date. If the payment has not beenreceived by the conference date I will provide my credit carddetails to secure my attendance.

Group Booking Discounts Available

Registration Form: 4th Annual Developing European Gas Supply Infrastructure conference

If undelivered please return to:

PlattsConferences & Events 20 Canada SquareCanary WharfLondon, E14 5LHUK