Embed Size (px)

Citation preview

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

What We Are Striving To Accomplish

1. To understand how value is measured and how capital is managed across the multiple units of firms

2. To understand how international business and investments are funded and how their cash flow is managed

3. To understand the three primary currency exposures that confront the multinational firm

4. To understand how accounting practices differ across countries, and how these differences may alter the competitiveness of firms in international markets

5. To understand the problems faced by many U.S.-based multinational firms, who experience taxation liabilities at home and in foreign countries

6. To examine the mechanics of financing import-export operations

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

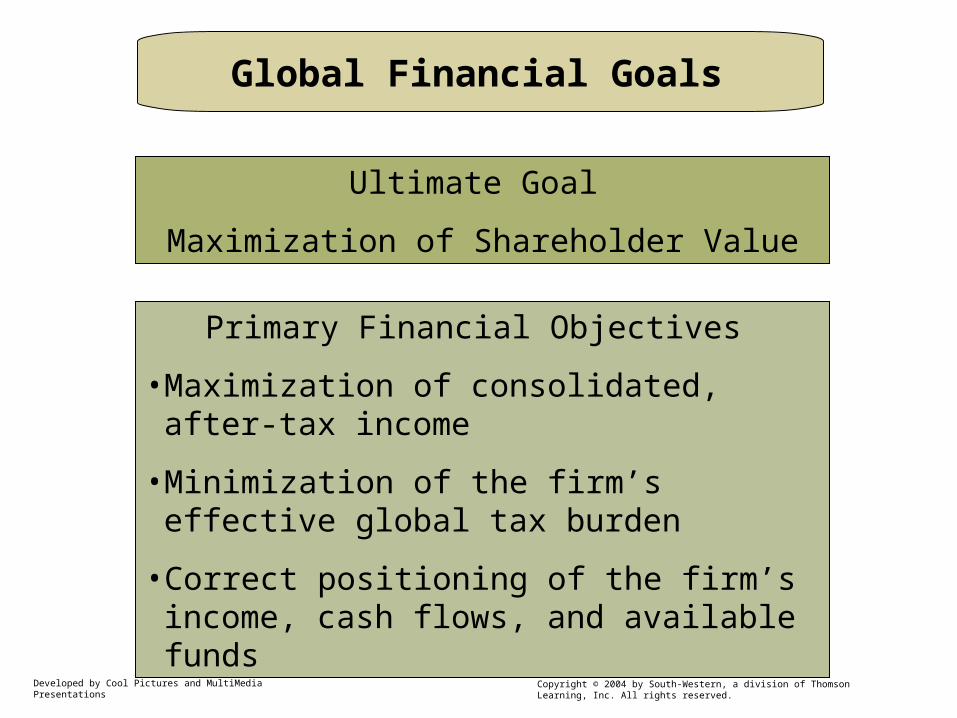

Global Financial Goals

Ultimate Goal

Maximization of Shareholder Value

Primary Financial Objectives

• Maximization of consolidated, after-tax income

• Minimization of the firm’s effective global tax burden

• Correct positioning of the firm’s income, cash flows, and available funds

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

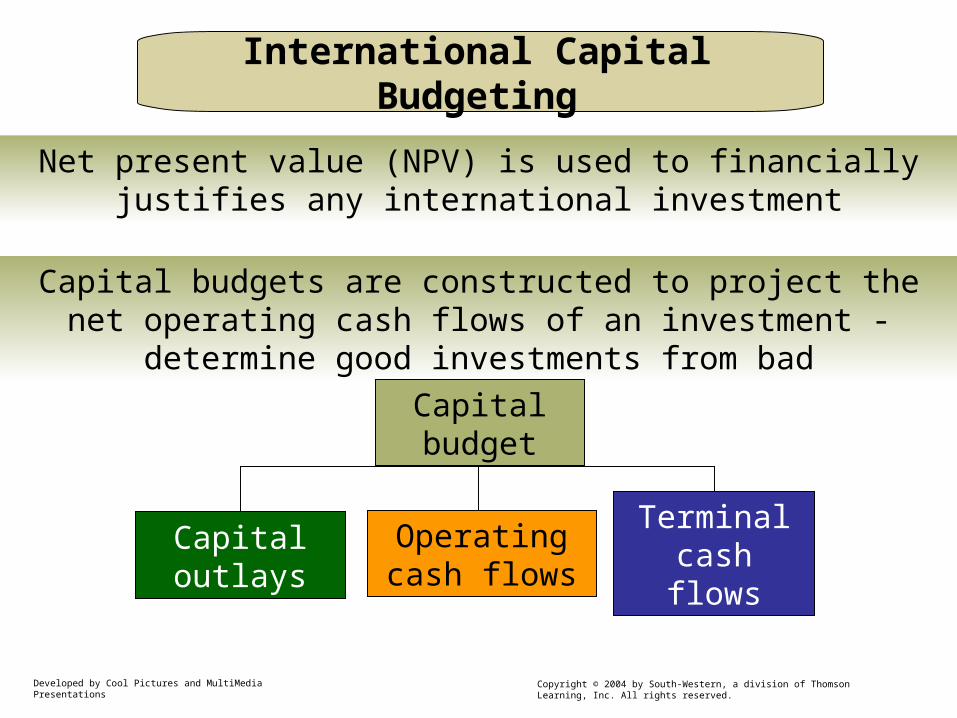

International Capital Budgeting

Net present value (NPV) is used to financially justifies any international investment

Capital budgets are constructed to project the net operating cash flows of an investment - determine good investments from bad

Capital budget

Capital outlays

Operating cash flows

Terminal cash flows

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

Capital Structure

Refers to the way a firm is funded

Debt-equity structure of the parent firm or competitive firms in the host country determines the ratio of debt and equity used in international investments.

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

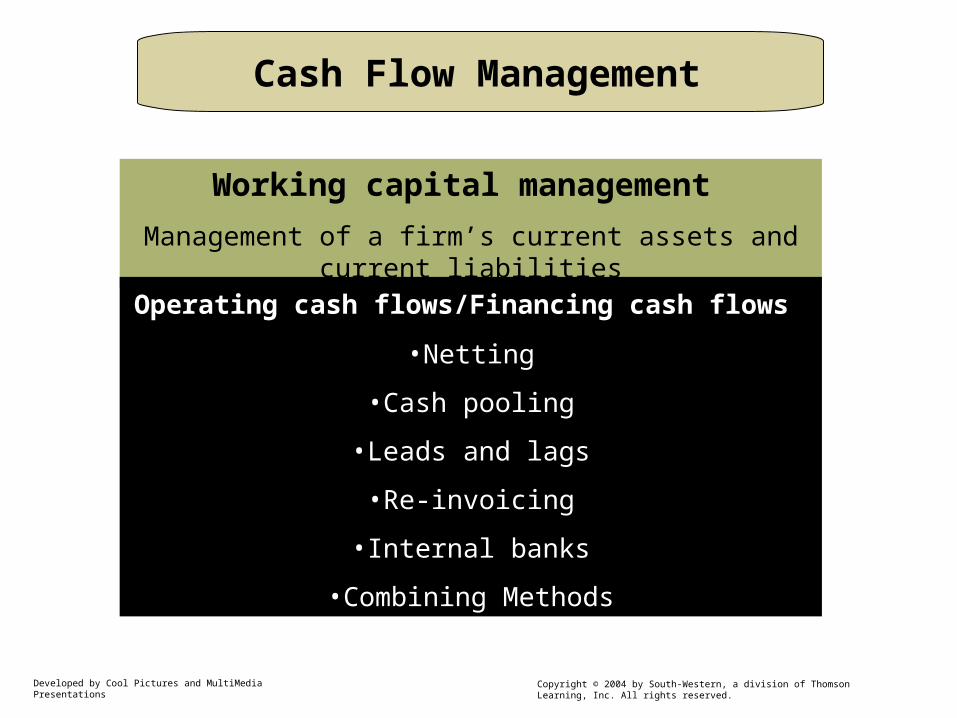

Cash Flow Management

Working capital management

Management of a firm’s current assets and current liabilities

Operating cash flows/Financing cash flows

•Netting

•Cash pooling

•Leads and lags

•Re-invoicing

•Internal banks

•Combining Methods

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

Foreign Exchange Exposure

Transaction exposure

Economic exposure

Translation exposure

Foreign Currency Exposure

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

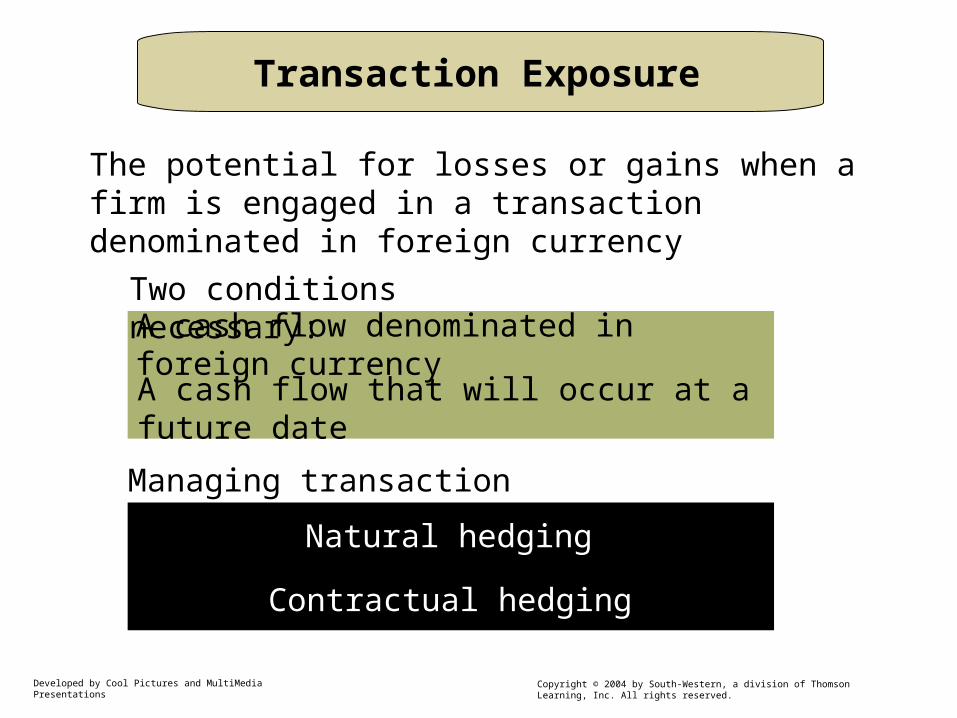

Transaction Exposure

The potential for losses or gains when a firm is engaged in a transaction denominated in foreign currency

Two conditions necessary:

A cash flow denominated in foreign currency

A cash flow that will occur at a future date

Managing transaction exposure

Natural hedging

Contractual hedging

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

Economic and Translation Exposure

Economic or operating exposureEconomic or operating exposure - the potential for long-term effects on a firm’s value as the result of changing currency values

Managing it:Managing it:Diversification of operations

Diversification of financing

Translation or accounting exposureTranslation or accounting exposure - the potential effect on a firm’s financial statements of a change in currency values

Financial Accounting Standards Board statement No. 52 is used in United States to properly translate foreign financial statements

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

International Accounting

The range in differences in national accounting practices (accounting diversity) can lead to:

•poor or improper business decision making

•difficulties in raising capital in different or foreign markets

•difficulty in monitoring competitive factors across firms, industries, and nations

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

Worldwide Accounting Standards

International Accounting Standards Committee (IASC)

•represented by nine countries worldwide

•seeks to create high-quality, understandable and enforceable accounting standards internationally

United States corporations and accounting firms have resisted change to ISC instead relying on Generally Accepted Accounting Principles (GAAP). Due to the Enron debacle and breakup of Andersen accounting firm, that position in under closer scrutiny now.

FASB

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

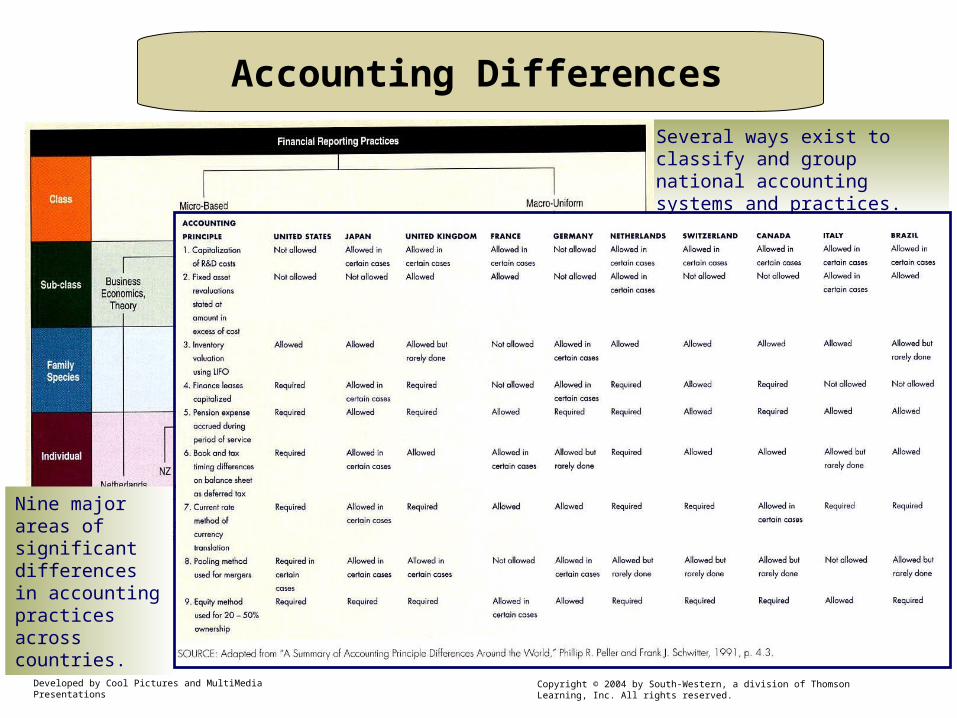

Several ways exist to classify and group national accounting systems and practices.

Accounting Differences

Nine major areas of significant differences in accounting practices across countries.

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

International Taxation

Tax treaties establish each country’s jurisdiction boundaries to avoid double taxation of international income.

International taxation can be approached as residential, territorial or a combination of the two.

Taxes are classified as:

• direct - taxes applied directly to income

• indirect - taxes applies to nonincome items, such as value-added taxes, excise taxes, tariffs, etc.

Developed by Cool Pictures and MultiMedia Presentations Copyright © 2004 by South-Western, a division of Thomson Learning, Inc. All rights reserved.

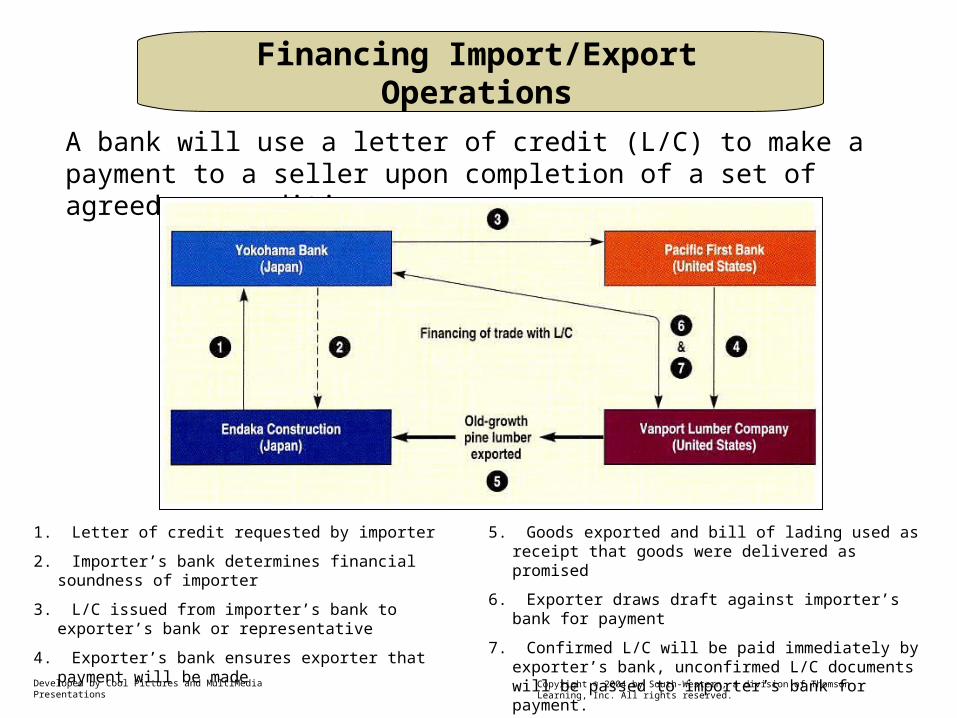

Financing Import/Export Operations

A bank will use a letter of credit (L/C) to make a payment to a seller upon completion of a set of agreed-on conditions.

1. Letter of credit requested by importer

2. Importer’s bank determines financial soundness of importer

3. L/C issued from importer’s bank to exporter’s bank or representative

4. Exporter’s bank ensures exporter that payment will be made

5. Goods exported and bill of lading used as receipt that goods were delivered as promised

6. Exporter draws draft against importer’s bank for payment

7. Confirmed L/C will be paid immediately by exporter’s bank, unconfirmed L/C documents will be passed to importer’s bank for payment.