Embed Size (px)

Citation preview

21 March 2017 Credit Research

Credit Flash – HG TMT

UniCredit Research page 1 See last pages for disclaimer.

Deutsche Telekom – Credit update ■ We keep our marketweight recommendation on Deutsche

Telekom’s (DT) bonds. Our fundamental analysis justifies their relatively tight valuations. DT bonds trade tight versus direct BBB rating peers in the sector and in line with single A rated peers. DT’s financial flexibility could be stretched by the final results/allocations of the broadcast incentive auction in the US, but DT should be capable of deleveraging quickly via potential disposals if need be. We do not expect DT to reduce its exposure to the US significantly in 2017, even if it participates with T-Mobile US (TMUS, Ba3s/BBp/--) in the consolidation of the US telecoms/media market. However, TMUS’s participation in the consolidation might lead to a deconsolidation of TMUS from DT’s accounts, which we would view as largely credit positive.

■ US spectrum auction: We assume DT might spend around USD 5-8bn in the currently ongoing US broadcast incentive auction. In the short term, this investment could drive DT’s reported leverage above 2.5x. With regard to the ongoing 600MHz US spectrum auction, DT stated that group leverage may overshoot leverage for one or two quarters but that, on a yoy basis, it will be very stringent with its leverage comfort zone of 2.0-2.5x (2.3x at FYE16).

■ Rating: We expect credit profile/rating development at DT to continue to be stable. Rating agencies have, in general, indicated that the US spectrum auction will not cause rating pressure if spectrum costs are not higher than anticipated. We are a bit skeptical regarding Moody’s, which may want DT to offset the negative impact of the US spectrum auction via disposal proceeds.

■ M&A: 1. We assume DT will not reduce its exposure to the US in the short term – not even in case it participates in the consolidation of this sector. In our view, Softbank (Sprint) and DT (TMUS) will likely discuss a potential merger of Sprint and TMUS in the US mobile market in 2017. We would view such a merger as credit positive for DT for several reasons: i) Reported group leverage would likely moderately decline as a result of the deconsolidation. ii) Group off-balance operating lease obligations would likely be reduced by around 70%. iii) If TMUS were to repay its debt obligations to DT, this would further reduce DT’s leverage. iv) DT would have a significant stake in the newly combined Sprint/TMUS entity, and this could be used to finance potential acquisitions in Europe. 2. A potential disposal of DT’s 12% stake in BT Group appears less likely following the most recent comments by DT’s management and after some uncertainty appears to be removed. 3. A disposal of T-Mobile NL is likely to resurface once DT has finalized the turnaround of this business. 4. We think DT might make use of its first right of refusal regarding the government’s 5% stake in OTE, which was transferred to the Hellenic Republic Asset Development Fund (HRADF).

■ Operating performance: If DT loses its growth driver TMUS double-digit revenue/EBITDA growth via strong subscriber growth in FY16) in the medium term, DT’s performance domestically and in Europe will become even more important. It appears as though domestic EBITDA stabilized in FY16, and DT might experience modest domestic EBITDA growth in FY17. The domestic fixed-line business seems to have benefitted from the company’s vectoring roll-out. In the domestic mobile market, prices are impacted mainly by regulatory measures (and in the low-price segment via mobile virtual network operators [Drillisch and United Internet]). In the high/mid-price market, DT’s “more for more” strategy seems to be working. In Europe, DT might experience stabilization in FY17 and growth in FY18.

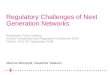

Recommendation Marketweight Major bond issues Mat Cpn Z-spread DT 04/23 0.625 32/29 DT 01/24 0.875 44/39 DT 01/27 1.375 64/61 DT 04/28 1.500 72/70 CDS-Spreads CDS CDS 1Y 12/16 CDS 3Y 26/30 CDS 5Y 50/53 CDS 7Y 63/66 CDS 10Y 73/77 Ratings L-T S-T Outlook Moody's Baa1 P-2 STABLE S&P BBB+ A-2 STABLE Fitch BBB+ F2 STABLE Company website www.telekom.com Financial calendar 2017 11 May: 1Q17 results 31 May: AGM 03 Aug.: 2Q17 09 Nov.: 3Q17 Relative Value

Source: iBoxx, UniCredit Research

Author Stephan Haber, CFA (UniCredit Bank) +49 89 378-15192 [email protected] Bloomberg UCGR Internet www.research.unicredit.eu

0

20

40

60

80

100

120

0 5 10 15 20

bp

mDur

PROXBB_CASH TELNO_CASH TELIAS_CASHSCMNVX_CASH DT_CASH ORAFP_CASH

0

20

40

60

80

100

120

140

0 2 4 6 8 10 12 14 16

bp

mDur

TELIAS_CASH DT_CASH ORAFP_CASH KPN_CASHVOD_CASH BRITEL_CASH TKAAV_CASH TELEFO_CASH

21 March 2017 Credit Research

Credit Flash – Deutsche Telekom

UniCredit Research page 2 See last pages for disclaimer.

Operating performance 4Q16 results Deutsche Telekom (DT) released solid 4Q16 results, which were mixed in terms of

consensus expectations*. Group revenues were above consensus, driven by stronger-than-expected growth in the US, which was partly offset by weaker top-line performance at T-Systems. Group EBITDA was slightly below expectations as the segments Europe and T-Systems reported clearly weaker-than-expected results. DT provided a healthy outlook for FY17, in line with its medium-term guidance. In terms of revenues (up organically yoy by 9.0% versus 6.5% in 3Q16, 3.9% in 2Q16 and 4.7% in 1Q16), DT Group again generated strong reported yoy growth in the US (+25.6%) – in contrast to moderate top-line declines in Germany (−0.7% yoy) and Europe (−2.4%) – and a strong decline at Systems-Solutions (−9.1% yoy). Regarding adjusted group EBITDA (organically up yoy by 1.8% versus 7.3% in 3Q16), the US business again showed strong yoy growth (12.0%), while T-Systems faced the strongest decline (−72%), alongside Europe (−9.8 yoy). Germany returned to positive EBITDA growth (+2.8% yoy). The group-adjusted EBITDA margin was down yoy to 26.9%, from 28.8% in 4Q15. FCF (before dividends) was down by more than 10% yoy to EUR 893mn (consensus of EUR 938mn). However, net debt increased qoq to EUR 50.0bn, from EUR 48.5bn, mainly due to spectrum investments (EUR 0.4bn) and FX effects (EUR +1.1bn). DT’s reported net debt/adj. EBITDA ratio remained stable qoq, at 2.3x (the company’s own threshold is 2.5x).

DT: 4Q16 RESULTS (ACTUAL VERSUS CONSENSUS EXPECTATIONS*)

Actual Actual Actual Actual Actual Actual Actual Consensus* Act. vs. cons. in EUR mn 4Q15 1Q16 2Q16 3Q16 4Q16 yoy in % qoq in % 4Q16 4Q16 Net revenues

Germany 5,321 5,136 5,076 5,208 5,284 -0.7% 1.5% 5,280 0.1%

Europe 3,334 3,018 3,020 3,140 3,253 -2.4% 3.6% 3,235 0.6%

United States 7,518 7,816 8,195 8,282 9,443 25.6% 14.0% 9,083 4.0%

T-Systems 1,520 1,545 1,402 1,349 1,382 -9.1% 2.4% 1,467 -5.8%

Group 17,859 17,630 17,817 18,105 19,543 9.4% 7.9% 19,216 1.7%

EBITDA (adjusted)

Germany 2,086 2,180 2,225 2,250 2,145 2.8% -4.7% 2,113 1.5%

Europe 1,075 986 1,038 1,100 970 -9.8% -11.8% 1,020 -4.9%

United States 2,075 1,908 2,172 2,156 2,325 12.0% 7.8% 2,308 0.7%

T-Systems 216 206 175 141 60 -72.2% -57.4% 177 -66.1%

Group 5,143 5,163 5,457 5,535 5,265 2.4% -4.9% 5,315 -0.9%

Adjusted EBITDA margin 28.8% 29.3% 30.6% 30.6% 26.9% 27.7%

FCF before dividends 998 822 1,320 1,904 893 -10.5% -53.1% 938 -4.8%

Net debt 47,570 47,603 48,692 48,484 49,959 5.0% 3.0% 49,219 1.5%

*consensus collected by DT Source: company data, UniCredit Research

Company outlook reiterated For FY17, DT provided an outlook that is in line with its medium-term guidance, which was confirmed. For FY17, it expects revenue growth to be ongoing (no concrete guidance, FY16: +5.6%) and adjusted EBITDA to grow by around 4% yoy to around EUR 22.2bn (FY16: +7.6% to EUR 21.4bn). FCF should increase by 12% to EUR 5.5bn (+8.6% to EUR 4.9bn in FY16). At its AGM, DT plans to propose a dividend of EUR 0.60 per share, which reflects roughly 10% yoy growth, which is in accordance with the group’s aim to increase dividends in line with FCF growth.

21 March 2017 Credit Research

Credit Flash – Deutsche Telekom

UniCredit Research page 3 See last pages for disclaimer.

COMPANY GUIDANCE AND CONSENSUS FORECAST1

Company guidance Revenues Adjusted EBITDA FCF2 14-18 CAGR 1-2% 2-4% *+~10% Guidance 2016 Increase ~EUR 21.2bn ~EUR 4.9bn Performance FY16 5.6% EUR 21.4bn (+7.6%) EUR 4.9bn (+8.6%) Guidance 2017 Increase ~EUR 22.2bn (+4%) ~EUR 5.5bn (+12%) Consensus forecast Revenues Adjusted EBITDA FCF2 FY17 consensus estimate in EUR bn 77.0 23.1 5.4 FY17 expected growth by consensus 5.4% 8.1% 9.4% FY18 consensus estimates in EUR bn 78.7 24.4 6.5 FY18 expected growth by consensus 2.1% 5.5% 20.2%

1) Consensus as collected by DT. 2) before dividend and spectrum payments Source: DT, UniCredit Research

Dividend policy For 2017, DT’s board of management has proposed a dividend of EUR 0.60 per share for

FY16 (in total EUR 2.8bn versus), versus EUR 0.55 per share in FY15 (in total EUR 2.6bn). Of this, EUR 1.0bn was paid in the form of a (voluntary) scrip dividend in FY16. The portion to be paid in the form of the scrip dividend amounted to 38% in 2013; 45% in 2014; 49% in 2015; and 41% in 2016. DT’s dividend policy stipulates that relative growth of FCF be taken into account when dividend payments are proposed. The 9% dividend increase for FY16 is in line with a 10% FCF increase in FY16. DT will continue to offer a scrip dividend for FY16, payable in 2017, which will likely reduce the cash impact of its dividends.

Update on potential M&A activities General M&A rules DT aims to become the leading European telecommunications provider. The basis for

achieving this goal is the utilization of a strong, fully integrated network that is fully controlled by DT. Hence, DT aims to have 100% control where it is active and aims to have only fully integrated networks. If one or both targets are not achievable in one country (e.g. the Netherlands), then the asset might be viewed as a “non-core” asset. However, just because an asset is deemed "non-core” according to the terms of DT’s overall strategy does not mean it is for sale. An asset will only be sold if selling it would add to shareholder value more so than if the asset were left to develop on its own. These simple M&A guidelines might explain DT’s stance towards potential acquisitions and disposals. Regarding its US operations, we note that DT aims to become a leading European telecoms provider and not a leading US telecoms provider. Moreover, DT is a mobile-only provider in the US. So far, the US assets are currently performing very well, i.e. DT can develop the (shareholder) value of these assets on its own. However, DT is open to participating with its asset in the consolidation of the US telecoms market, which is expected to generate additional shareholder value.

T-Mobile US During DT’s 4Q16-results conference call, CEO Timotheus Höttges stated that he thinks the new Republican-controlled government in the US is more open and less prone to implementing regulations regarding consolidation in the telecommunications industry than the former Democratic-controlled government. This also seems to be reflected in the comments from the new head of the Federal Communications Commission, Ajit Pai. However, it is not possible to draw any concrete conclusions from that regarding specific consolidation scenarios. Moreover, given DT’s participation in the broadcast-incentive auction, DT is not allowed to speculate publicly on these topics.

During its 3Q16-results conference call, DT’s management indicated that it remains open-minded regarding opportunities to benefit from possible consolidation in the US market.

21 March 2017 Credit Research

Credit Flash – Deutsche Telekom

UniCredit Research page 4 See last pages for disclaimer.

DT reiterated that a mobile-mobile merger could hugely benefit consumers, as such a newly created company would be able to be much more aggressive on the consumer side. Such a merger could also create significant synergies.

In December 2016, the CEO of SoftBank Group, Masayoshi Son, met with then US President-elect Donald Trump, who went on to state that Softbank had “agreed to invest USD 50bn in start-ups and new companies in the US and to create 50,000 new jobs”. Citing a person familiar with the matter, an article published by Bloomberg stated that the money to fund these investments should come from SoftBank’s announced USD 100bn technology fund. Mr. Trump’s statement spurred speculation that these investments could pave the way for a merger between Softbank’s 83% owned US mobile operator, Sprint Corporation, with T-Mobile US (TMUS). We note that, under the Obama administration, a merger between the two US mobile operators was deemed unlikely given potential resistance to the merger by the FCC, which regulates telecoms firms in the US. We note that an article published Bloomberg and citing a person familiar with the matter stated that the USD 50bn investment by SoftBank is not intended for mergers and acquisitions, such as that which would involve TMUS. However, such an investment commitment might improve the relationship between Mr. Son and Mr. Trump.

Therefore, we think that Softbank and DT will initiate discussions with the new US administration regarding a potential merger between Sprint and TMUS in 2017, also in light of the proposed acquisition of Time Warner by AT&T, which would already increase market concentration. Such a merger would offer DT the opportunity to retract from its US investments over time and to improve its European footprint.

How would DT’s credit profile develop if DT were to exchange/merge its stake in TMUS into a Sprint/TMUS JV with Softbank (without receiving any cash portion)? We assume that DT would have to deconsolidate TMUS. Therefore, DT Group’s net debt (EUR 50.0bn at FYE16) would decline by around USD 22.3bn (EUR 20.8bn), and DT Group’s EBITDA (EUR 21.4bn at FYE 2016) would decline by EUR 8.6bn. Hence, the reported-net-debt-to-EBITDA ratio would decline from 2.34x to 2.28x. Furthermore, we note that a significant part (>50%) of the group’s off-balance-sheet operating lease liabilities – the nominal value of future minimum lease payments of EUR 16.5bn would be significantly reduced, by USD 9.0bn or EUR 8.4bn – belong to TMUS, i.e. group off-balance-sheet liabilities would disproportionately be reduced. Hence, we assume that a deconsolidation of TMUS would position DT more adequately within the BBB+ rating category.

We note that DT has significantly increased its exposure to TMUS: from around USD 5.6bn in 1Q16 (when it started to soften its self-imposed self-financing rule for TMUS) to USD 17.1bn by March 2017. Hence, if DT were able to reduce its financing exposure to TMUS in case of a consolidation, it would further reduce DT’s leverage. If DT were to receive a cash payment for part of its TMUS stake in an M&A transaction, this would also reduce the overall leverage of the remaining DT Group. For example, we assume that DT would still own more than 25% (around 36% if no cash payment is made) in a newly combined Sprint/TMUS JV with an expected EV of more than USD 135bn (market capitalization expected: USD >85). Hence, DT’s stake in a newly combined JV would offer DT potential financial flexibility to make acquisitions in Europe.

We note that the broadcast incentive auction might prove expensive for TMUS (estimated payments of USD 5-8bn in 2017). Hence, in the short term, DT’s exposure to TMUS could lead DT’s reported leverage to increase above 2.5x (according to our calculations, 2.6x). With regard to the ongoing 600MHz US spectrum auction, DT stated that group leverage may overshoot leverage for one or two quarters but that, on a yoy basis, it will be very stringent with its leverage comfort zone of 2.0-2.5x.

21 March 2017 Credit Research

Credit Flash – Deutsche Telekom

UniCredit Research page 5 See last pages for disclaimer.

DT'S FUNDING SUPPORT FOR TMUS

Volume in USD bn Description 5.6 Unsecured HY bond (disbursed) 4.0 Unsecured HY bond purchase commitment (undrawn) 2.5 RCF, thereof USD 1.5bn secured (undrawn) 4.0 Secured term loan

3.5 Unsecured senior notes (USD 1bn 4.0% due 2022, USD 1.25bn 5.125% due 2025 and USD 1.25bn 5.375% due 2027)

-2.5 Repayment of notes held by DT 17.1 Total

Source: company info, UniCredit Research

Reduced structural subordination

Moody’s views it as positive that DT supports TMUS’s financing needs, as this reduces structural subordination issues. In our view, as DT is increasing its exposure to TMUS, it might become more complicated to dispose of TMUS. If DT’s stake in TMUS were to be significantly diluted in a potential consolidation transaction in the US telecoms/media market, DT may end up with a high investment in an uncontrolled (ownership below 50%) high-yield asset. Moreover, in our view, DT’s increased exposure to TMUS indicates that it does not plan to withdraw from TMUS in the short term. It currently looks more likely that DT will keep its exposure to the US telecoms market, even if TMUS participates in the consolidation of the US telecoms/media market. Hence, if rating agencies expect DT to reduce its indebtedness quickly after the impact of the broadcast incentive auction in the US becomes known, disposal proceeds will need to come from assets other than TMUS, in our view. So far, DT has indicated that it aims to reduce leverage due to the US auction via growth at TMUS. It needs to be seen if that will be sufficient to satisfy rating agencies (mainly Moody’s).

DT’s 12% stake in BT Group With regard to press speculation that DT could be interested in selling its stake in BT (to finance higher investment in the US), Mr. Höttges stated that recent developments have removed a lot of uncertainty regarding BT, for example that BT retained Champion League rights and the agreement regarding the legal separation of Openreach. Hence, DT’s basic assessment is that the business itself is strong and well positioned. DT indicated that it sees a lot of potential for cooperation between DT and BT, which DT views as a good asset/investment and as having a lot of good fundamental substance. DT is very much looking to support BT wherever BT wants DT’s support. Moreover, DT is currently not able to consider a sale of BT stock due to a lock-up period (see below). DT pointed out that it is very satisfied with the operating performance of BT/EE. However, there are three points of concern: 1. the Brexit situation; 2. pension funding, due to lower interest rates, and 3. legal separation (this concern has largely been removed by the recent agreement between BT and UK regulator Ofcom).

We note that DT is required to observe a lock-up period for its 12% stake in BT for 18 months from the closing of the BT/EE merger, which occurred at the end of January 2016. Hence, DT will look at its 12% BT stake in mid-2017 and at how the network separation has developed. Given DT’s comments (mentioned above), we think DT is rather unlikely to sell its 12% stake in BT in the short term.

T-Mobile NL More generally (although within the context of its business unit in the Netherland’s), Mr. Höttges stated, during DT’s 3Q16-results conference call, that “there is nothing sacrosanct in our portfolio”. He went on to say that, if a business unit is not performing well and is not accretive to DT’s profitability and free-cash-flow generation, the situation will need to be analyzed in order to determine how it can best be solved. In this regard, it is not important if an asset is core or non-core. The question is how to create value (for shareholders). In the Netherland’s, DT was lucky to have bought fixed-line assets (due to remedies to the Vodafone/Ziggo transaction – acquiring fixed-line infrastructure assets and 150k customers from Vodafone).

21 March 2017 Credit Research

Credit Flash – Deutsche Telekom

UniCredit Research page 6 See last pages for disclaimer.

This will help its Netherland’s unit fight fixed-mobile converged offers from its competitors. Moreover, DT has improved profitability in the Netherlands via cost-reduction measures. It is our impression that DT is currently developing its Netherland unit to dispose of it at a decent value at some point – as a mobile-only strategy (considering the scale of recent fixed-line asset purchases as the small/negligible) might not create value in the medium term.

Mobile-tower business An article published by Reuters in early July 2016 and citing two sources close to the matter reported that DT was preparing to sell its mobile-tower business for an estimated purchase price of EUR 4-5bn to free up funds for investing in its European networks. We note that DT had bundled its German tower operations into a separate company a few years ago. It appears as though DT has looked into the potential disposal of this unit, while it remains unclear if the full control of this unit might not prove advantageous, going forward, to managing a 5G roll-out.

OTE Recently, the Greek government transferred of a 5.0% stake in OTE to the Hellenic Republic Asset Development Fund (HRADF). The Greek parliament already approved an amendment to a shareholders agreement between the Greek state and DT. The state will retain a 5.0% stake in OTE, while DT will have the “right of first of refusal” when it comes to the sale of the 5.0% stake in OTE held by HRADF. We note that the current market value of this stake is around EUR 210mn.

M&A summary To summarize, DT’s management seems to be very open-minded regarding its asset portfolio. The main driver of DT’s portfolio management is value creation. In this regard, it is not helpful to divide assets into core or non-core assets. Moreover, we think that DT will use its asset portfolio to manage its leverage if necessary.

Government-related issuer/entity DT is around 32% owned directly/indirectly (via KfW) by the German government. Therefore,

DT, in general qualifies as government-related issuer (GRI) at Moody’s and as government-related entity (GRE) at S&P. However, only DT’s Baa1 rating at Moody’s benefits from a one-notch uplift derived from the government's support expectations. S&P does not factor in any support from the German government into its BBB+ rating on DT. This is because S&P considers that there is a low likelihood that the Federal Republic of Germany would provide timely and sufficient extraordinary government support to DT in the event of financial distress. We note that Moody’s one notch GRI-related rating uplift would be at risk, if the German government reduces its stake in DT significantly below 20%.

Recently, the economic magazine Wirtschaftswoche reported that the German finance ministry (BMI) has stated in a report that the German government sticks to its plan to gradually reduce its stake in DT. A spokesman of the German finance ministry immediately denied the intention to reduce its holding in DT and clarified that the Wirtschaftswoche referred to a standard formulation that it is a long-term goal to reduce state holdings such as the one of DT. This standard formulation probably exists since DT’s IPO in 1996. We note that the direct holding of the BMI in DT (14.5%) was stable in terms of the nominal number of DT shares since the end of 2005 and that the indirect holding of the KfW (17.5%) was stable since the end of 2006 and increased sometime in May probably as the KfW participated in DT’s scrip dividend payments. Hence, we view it unlikely that the German government and/or the BMI intends to reduce the stake of the German government in DT any time soon, as there is no (financial) reason to do so given the balanced German state budget.

We note that there will general elections in Germany in autumn 2017. Some politicians from parties with no governmental responsibility already came up with statements which require the privatization of the Governments stake in DT to finance the broadband network built out (in rural areas) in Germany. We do not take these statements serious, as long as they are not taken up by one of the major parties in Germany.

UniCredit Research page 7 See last pages for disclaimer.

21 March 2017 Credit Research

Credit Flash – Deutsche Telekom

Deutsche Telekom AG Analyst: Stephan Haber, CFA (UniCredit Bank), +49 89 378-15192 Corporate Ratings Rating Outlook Credit Profile Trend Recommendation Index Mcap Baa1/BBB+/BBB+ STABLE/STABLE/STABLE Stable Marketweight iBoxx/--/iTraxx S26 EUR 75.2bn

Company description: Deutsche Telekom AG (DT), headquartered in Bonn, Germany, is the leading domestic telecoms operator and among the leading international providers of wireless services. As of 31 December 2016, DT had 165mn mobile customers (155.4mn at FYE 2015), 28.5mn fixed-network lines (29.0mn at FYE 2015) and 18.5mn broadband lines (excluding wholesale; 17.8mn at FYE 2015). DT operates in regional divisions: 1. In Germany, the "T" brand offered services via 12.9mn broadband lines as of FYE 2016 (12.6mn as of FYE 2015), 19.8mn fixed-network lines at FYE 2016 (20.2mn at FYE 2015) and to 41.8mn mobile subscribers at FYE 2016 (25.2mn post and 16.6mn pre-paid). 2. In the US, (T-Mobile US) it provided wireless services to 71.5mn customers at FYE 2016 (62.3mn at FYE 2015). 3. In Europe, it had key mobile operations in GR, RO, HU, PL, CZ, HR, NL, SK and AT and a mobile customer base of 51.7mn at FYE 2016 (52,7mn FYE 2015). Additionally, it had 8.7mn fixed-network-line customers (8.8mn at FYE 2015). 4. Systems Solutions (T-Systems) provides information and communication technology solutions to corporate clients. DT employed 218,341 employees worldwide as of 31 December 2016. Its shareholder structure as of 31 December 2016 was as follows: German government, 32.0%, of which 14.5% directly and 17.5% indirectly through KfW; Blackrock, 4.6%; rest, free float.

Moody's (01/17): The stable outlook on the ratings reflects the expectation that DT will benefit from improving operating cash flow and operate its business at the low to mid-point of the 2.0-2.5x net debt/EBITDA comfort zone (as reported by the company), which is equivalent to Moody's-adjusted net debt/EBITDA of below 2.8x. In addition, Moody’s assumes that DT will maintain an RCF/adjusted net debt ratio of around 20%. Up: If the adjusted RCF/debt ratio exceeds 25% on a sustainable basis, this could pressure an upgrade. Down: The adjusted RCF/debt ratio dropping below 18% on a sustainable basis and the adjusted net debt/EBITDA ratio exceeding 2.8x could provide pressure for a downgrade. S&P (08/16): The stable outlook assumes resilient operating performance in DT’s domestic operations and strong growth in the US, and that the company sticks to its financial policy (reported leverage of 2.0-2.5x). Down: S&P could take a negative rating action if DT's adjusted-debt-to-EBITDA ratio exceeded or remained at 3.5x and if, at the same time, the adjusted-FFO-to-debt ratio declined to less than 23% for more than just a temporary period. In particular, this could result from higher-than-anticipated debt-funded spectrum costs in the US. Fitch (02/17): Although a temporary spike in debt due to 600MHz US spectrum auction purchases may be consistent with the current rating (provided that DT continues its deleveraging efforts), substantial overspending will further stretch leverage, putting pressure on the rating. DT's leverage is already high for its rating level: around 3.4x FFO-adjusted net leverage and 3.0x net debt/EBITDA (under Fitch's definition) at FYE 2015. The impact of US investment on DT's credit profile may be exacerbated by a strong USD (vs. EUR).

NET REVENUES PER SEGMENT

ADJUSTED EBITDA PER SEGMENT

Strengths/Opportunities – Market leader in domestic telecom services; well positioned in several CEE

markets and having mobile only operations in the NL and Austria; owning a 12% stake in BT Group

– Strong diversification offers flexibility to generate financial resources from portfolio disposals

– Relatively strong and stable FCF generation (despite lower FCF generation in 2013-15 due to growth investments); potential disposals (e.g. 12% in BT, T-Mobile US, T-Mobile-NL, domestic mobile-tower business)

– Solid liquidity profile – Strong rating commitment (although widely ranging, from A- to BBB flat)

Weaknesses/Threats – Challenging environment for its domestic business due to strong

competition (e.g. from cable operators) – High capex due to investments (e.g. LTE/FTTH network expansion) in

eastern Europe, Germany and the US – Relatively weak market position for T-Mobile USA compared to its two

major competitors – Potential M&A activities and shareholder-remuneration policy – Europe segment suffers from the difficult macroeconomic and competitive

environment in eastern Europe

MAJOR BOND ISSUES

ISIN Ticker/Issue Issue Rating Amount (EUR mn) Comment XS0875796541 DT 2.125% 18/01/21 Baa1/BBB+/BBB+ 1,250 XS0525787874 DT 4.25% 13/07/22 Baa1/BBB+/BBB+ 1,250 XS1382792197 DT 0.625% 03/04/23 Baa1/BBB+/BBB+ 1,750 XS1382791975 DT 1.5% 03/04/28 Baa1/BBB+/BBB+ 1,500

Company-specific information: As of 31 December 2016, DT had standardized bilateral credit agreements with 22 banks for a total of EUR 12.9bn. As of 31 December 2016, DT had access to undrawn, bilateral and

committed credit facilities of EUR 12.4bn. According to Moody's, the RCFs do not contain any covenants.

Source: rating agencies, company data, iBoxx, UniCredit Research

-15%

-10%

-5%

0%

5%

10%

15%

20%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Germany UnitedStates

Europe SystemsSolutions

GHS

in E

UR

mn

FY15 FY16 Diff. yoy

-30%

-20%

-10%

0%

10%

20%

30%

40%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Germany United States Europe SystemsSolutions

in E

UR

mn

FY15 FY16 Diff. yoy

UniCredit Research page 8 See last pages for disclaimer.

21 March 2017 Credit Research

Credit Flash – Deutsche Telekom

FINANCIAL STATISTICS

EUR mn 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Sales 62,516 61,666 64,602 62,421 58,653 58,169 60,132 62,658 71,225 77,263 EBIT margin adj. 15.0% 16.0% 16.3% 15.5% 15.2% 14.4% 14.3% 13.7% 12.2% 13.8% EBITDA rep. 16,897 18,015 19,906 17,313 20,022 18,147 15,834 17,821 18,388 22,544 EBITDA margin adj. 33.0% 33.8% 34.1% 33.3% 37.2% 35.8% 34.1% 33.5% 33.3% 32.9% Net income 1,078 2,024 873 1,760 670 -4,757 1,204 3,244 3,502 3,104 Funds from operations 16,177 15,212 15,677 15,183 14,813 14,681 13,587 13,461 15,557 17,043 Operating cash flow 13,714 15,368 15,795 14,731 13,925 13,577 13,017 13,393 14,997 15,533 Free cash flow rep. (after capex) 5,699 6,661 6,593 4,880 5,519 5,145 6,447 1,549 384 1,893 Dividend payment -3,762 -3,963 -4,287 -4,003 -3,521 -3,400 -2,243 -1,290 -1,256 -1,596 Retained cash flow 12,415 11,249 11,390 11,180 11,292 11,281 11,344 12,171 14,301 15,447 Acquisitions/disposals 21 -3,288 -592 -935 1,081 1,542 1,873 -339 -764 1,096 Share buybacks/issues 24 3 2 -400 -3 0 1,391 -86 16 0 Total debt rep. 42,906 46,594 51,191 50,546 48,318 44,614 51,599 55,227 62,380 64,650 Net debt rep. 40,706 43,568 46,169 47,738 44,569 40,588 43,629 47,704 55,483 56,903 Adj. for pensions 5,346 5,152 6,202 6,383 6,104 7,292 6,997 8,450 8,016 8,442 Adj. for operating leases and others 12,458 11,265 12,008 8,724 9,723 9,547 9,664 9,499 8,765 6,670* Net debt adj. 58,510 59,985 64,379 62,845 60,396 57,427 60,290 65,653 72,264 72,015

DEBT LEVERAGE

DEBT MATURITY PROFILE AS OF 31 DECEMBER 2016*

*including refinancing activities in January 2017 and excluding called T-Mobile US debt in February 2017

CREDIT METRICS

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 EBIT net interest cover adj. 2.7 2.8 2.8 2.8 2.7 2.8 2.8 2.6 3.7 4.3 EBIT gross interest cover adj. 2.5 2.5 2.6 2.5 2.5 2.5 2.6 2.4 3.3 3.9 EBITDA net interest cover adj. 5.9 5.8 5.9 6.0 6.6 7.0 6.6 6.4 10.0 10.2 EBITDA gross interest cover adj. 5.5 5.2 5.4 5.5 6.1 6.3 6.1 5.8 9.1 9.4 FFO adj./net debt adj. 27.6% 25.4% 24.4% 24.2% 27.5% 28.1% 25.4% 23.4% 24.5% 27.2% FFO adj./total debt adj. 26.6% 24.1% 22.6% 23.1% 25.9% 26.3% 22.4% 21.0% 22.4% 24.5% RCF adj./net debt adj. 21.2% 18.8% 17.7% 17.8% 21.7% 22.2% 21.7% 21.4% 22.8% 25.0% RCF adj./total debt adj. 20.4% 17.9% 16.4% 17.0% 20.4% 20.7% 19.2% 19.2% 20.8% 22.5% Net debt adj./EBITDA adj. 2.8 2.9 2.9 3.0 2.8 2.8 2.9 3.1 3.0 2.8 Total debt adj./EBITDA adj. 2.9 3.0 3.2 3.2 2.9 3.0 3.3 3.5 3.3 3.1 FFO adj./net interest adj. 4.6 4.3 4.2 4.4 5.1 5.4 4.9 4.7 7.5 7.9 FFO adj./gross interest adj. 4.3 3.8 3.9 4.0 4.7 4.9 4.6 4.2 6.8 7.2 Total debt adj./total capital. adj. 57.3% 59.4% 62.3% 60.4% 61.6% 66.8% 68.0% 68.7% 68.1% 67.2% Net debt adj./net capital. adj. 56.4% 58.2% 60.6% 59.4% 60.2% 65.3% 65.3% 66.4% 66.1% 65.0% Equity/total assets 37.5% 35.0% 32.8% 33.7% 32.6% 28.3% 27.1% 25.7% 25.7% 26.2%

*In 4Q16, DT’s operating segment in the US changed its operating leases assessment for cell sites regarding the exercise of extension options. For new leases, the exercising of extension options is not deemed reasonably certain beyond the non-cancelable basic lease term of between five and ten years against the background of the altered market situation and new technical framework. This change had resulted in a decrease of EUR 5.3bn in the expected future minimum lease payments from operating leases in the US as of FYE 2016. Source: company data, UniCredit Research

2.5

2.6

2.7

2.8

2.9

3.0

3.1

3.2

0%

5%

10%

15%

20%

25%

30%

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

FFO adj./net debt adj. Net debt adj. / EBITDA adj. (RS)

0

5,000

10,000

15,000

20,000

25,000

Liqu

idity

as

ofFY

E16 20

17

2018

2019

2020

2021

2022

2023

2024

2025

>202

5

Cash Undrawn, committed linesFinancial debt DT Financial debt TMUSFinancial debt OTE DT issued in Jan 2017TMUS issued in March 2017

21 March 2017 Credit Research

Credit Flash – Deutsche Telekom

UniCredit Research page 9 .

Disclaimer Our recommendations are based on information obtained from, or are based upon public information sources that we consider to be reliable but for the completeness and accuracy of which we assume no liability. All estimates and opinions and projections and forecasts included in the report represent the independent judgment of the analysts as of the date of the issue unless stated otherwise. This report may contain links to websites of third parties, the content of which is not controlled by UniCredit Bank. No liability is assumed for the content of these third-party websites. We reserve the right to modify the views expressed herein at any time without notice. Moreover, we reserve the right not to update this information or to discontinue it altogether without notice. This analysis is for information purposes only and (i) does not constitute or form part of any offer for sale or subscription of or solicitation of any offer to buy or subscribe for any financial, money market or investment instrument or any security, (ii) is neither intended as such an offer for sale or subscription of or solicitation of an offer to buy or subscribe for any financial, money market or investment instrument or any security nor (iii) as an advertisement thereof. The investment possibilities discussed in this report may not be suitable for certain investors depending on their specific investment objectives and time horizon or in the context of their overall financial situation. The investments discussed may fluctuate in price or value. Investors may get back less than they invested. Changes in rates of exchange may have an adverse effect on the value of investments. Furthermore, past performance is not necessarily indicative of future results. In particular, the risks associated with an investment in the financial, money market or investment instrument or security under discussion are not explained in their entirety. This information is given without any warranty on an "as is" basis and should not be regarded as a substitute for obtaining individual advice. Investors must make their own determination of the appropriateness of an investment in any instruments referred to herein based on the merits and risks involved, their own investment strategy and their legal, fiscal and financial position. As this document does not qualify as an investment recommendation or as a direct investment recommendation, neither this document nor any part of it shall form the basis of, or be relied on in connection with or act as an inducement to enter into, any contract or commitment whatsoever. Investors are urged to contact their bank's investment advisor for individual explanations and advice. Neither UniCredit Bank AG, UniCredit Bank AG London Branch, UniCredit Bank AG Milan Branch, UniCredit Bank Austria AG, UniCredit Bulbank, Zagrebačka banka d.d., UniCredit Bank Czech Republic and Slovakia, Bank Pekao, ZAO UniCredit Bank Russia, UniCredit Bank Czech Republic and Slovakia Slovakia Branch, UniCredit Bank Romania, UniCredit Bank AG New York Branch nor any of their respective directors, officers or employees nor any other person accepts any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection therewith. This analysis is being distributed by electronic and ordinary mail to professional investors, who are expected to make their own investment decisions without undue reliance on this publication, and may not be redistributed, reproduced or published in whole or in part for any purpose. Responsibility for the content of this publication lies with: UniCredit Group and its subsidiaries are subject to regulation by the European Central Bank a) UniCredit Bank AG (UniCredit Bank), Arabellastraße 12, 81925 Munich , Germany, (also responsible for the distribution pursuant to §34b WpHG). The company belongs to UniCredit Group. Regulatory authority: “BaFin“ – Bundesanstalt für Finanzdienstleistungsaufsicht, Marie-Curie-Str. 24-28 , 60439 Frankfurt, Germany. b) UniCredit Bank AG London Branch (UniCredit Bank London), Moor House, 120 London Wall, London EC2Y 5ET, United Kingdom. Regulatory authority: “BaFin“ – Bundesanstalt für Finanzdienstleistungsaufsicht, Marie-Curie-Str. 24-28, 60439 Frankfurt, Germany and subject to limited regulation by the Financial Conduct Authority, 25 The North Colonnade, Canary Wharf, London E14 5HS, United Kingdom and Prudential Regulation Authority 20 Moorgate, London, EC2R 6DA, United Kingdom. Further details regarding our regulatory status are available on request.

POTENTIAL CONFLICTS OF INTERESTS Deutsche Telekom 8a Key 1a: UniCredit Bank AG and/or any related legal person owns at least 2% of the capital stock of the analyzed company. Key 1b: The analyzed company owns at least 2% of the capital stock of UniCredit Bank AG and/or any related legal person. Key 2: UniCredit Bank AG and/or any related legal person has been lead manager or co-lead manager over the previous 12 months of any publicly disclosed offer of financial instruments of the analyzed company, or in any related derivatives. Key 3: UniCredit Bank AG and/or any related legal person administers the securities issued by the analyzed company on the stock exchange or on the market by quoting bid and ask prices (i.e. acts as a market maker or liquidity provider in the securities of the analyzed company or in any related derivatives). Key 5: The analyzed company and UniCredit Bank AG and/or any related legal person have concluded an agreement on the preparation of analyses. Key 6a: Employees or members of the Board of Directors of UniCredit Bank AG and/or any other employee that works for UniCredit Research (i.e. the joint research department of the UniCredit Group) and/or members of the Group Board (pursuant to relevant domestic law) are members of the Board of Directors of the analyzed company. Members of the Board of Directors of the analyzed company hold office in the Board of Directors of UniCredit Bank AG (pursuant to relevant domestic law). The application of this Key 6a is limited to persons who, although not involved in the preparation of the analysis, had or could reasonably be expected to have access to the analysis prior to its dissemination to customers or the public. Key 6b: The analyst is on the Supervisory Board/Board of Directors of the company they cover. Key 8a: UniCredit Bank AG and/or any related legal person hold a net long position exceeding 0.5% of the total issued share capital of the issuer. Key 8b: UniCredit Bank AG and/or any related legal person hold a net short position exceeding 0.5% of the total issued share capital of the issuer. UniCredit S.p.A. acts as a Specialist or a Primary Dealer in government bonds issued by the Italian or Greek Treasury, and as market maker in government bonds issued by the Spain or Portuguese Treasury. Main tasks of the Specialist are to participate with continuity and efficiency to the governments' securities auctions, to contribute to the efficiency of the secondary market through market making activity and quoting requirements and to contribute to the management of public debt and to the debt issuance policy choices, also through advisory and UniCredit Bank AG research activities. UniCredit S.p.A. Registered Office in Rome: Via Alessandro Specchi, 16 - 00186 Roma Head Office in Milan: Piazza Gae Aulenti 3 - Tower A - 20154 Milano, Registered in the Register of Banking Groups and Parent Company of the UniCredit Banking Group, with. cod. 02008.1; Cod. ABI 02008.1 - Competent Authority: Commissione Nazionale per le Società e la Borsa (CONSOB)”. UniCredit Bank AG acts as a Specialist or Primary Dealer in government bonds issued by the German or Austrian Treasury. Main tasks of the Specialist are to participate with continuity and efficiency to the governments' securities auctions, to contribute to the efficiency of the secondary market through market making activity and quoting requirements and to contribute to the management of public debt and to the debt issuance policy choices, also through advisory and research activities.

RECOMMENDATIONS, RATINGS AND EVALUATION METHODOLOGY Company Date Rec. Company Date Rec. Company Date Rec. DT 26/01/2017 Marketweight DT 04/05/2016 Marketweight DT 21/07/2016 Underweight Overview of our ratings You will find the history of rating regarding recommendation changes as well as an overview of the breakdown in absolute and relative terms of our investment ratings on our website www.disclaimer.unicreditmib.eu/credit-research-rd/Recommendations_CR_e.pdf. Note on the evaluation basis for interest-bearing securities: Recommendations relative to an index: For high grade names the recommendations are relative to the "iBoxx EUR Benchmark" index family, for sub investment grade names the recommendations are relative to the "iBoxx EUR High Yield" index family. Marketweight (MW): We recommend having the same portfolio exposure in the name as the respective iBoxx index. We expect that the average total return of the instruments of the issuer is equal to the total return of the index. Overweight (OW) : We recommend having a higher portfolio exposure in the name as the respective iBoxx index. We expect that the average total return of the instruments of the issuer is greater than the total return of the index. Underweight (UW): We recommend having a lower portfolio exposure in the name as the respective iBoxx index. We expect that the average total return of the instruments of the issuer is less than the total return of the index. Outright recommendations:

21 March 2017 Credit Research

Credit Flash – Deutsche Telekom

UniCredit Research page 10 .

Hold (H): We recommend holding the respective instrument for investors who already have exposure. We expect that the total return of the instruments of the issuer is equal to the yield. Buy (B): We recommend buying the respective instrument for investors who already have exposure. We expect that the total return of the instruments of the issuer is greater than the yield. Sell (S): We recommend selling the respective instrument for investors who already have exposure. We expect that the total return of the instruments of the issuer is less than the yield. We employ three further categorizations for interest-bearing securities in our coverage: Restricted (R): A recommendation and/or financial forecast is not disclosed owing to compliance or other regulatory considerations such as a blackout period or a conflict of interest. Coverage in transition (T): Due to changes in the research team, the disclosure of a recommendation and/or financial information are temporarily suspended. The interest-bearing security remains in the research universe and disclosures of relevant information will be resumed in due course. Not rated (NR): Suspension of coverage. Trading recommendations for fixed-interest securities mostly focus on the credit spread (yield difference between the fixed-interest security and the relevant government bond or swap rate) and on the rating views and methodologies of recognized agencies (S&P, Moody’s, Fitch). Depending on the type of investor, investment ratings may refer to a short period or to a 6 to 9-month horizon. Please note that the provision of securities services may be subject to restrictions in certain jurisdictions. You are required to acquaint yourself with local laws and restrictions on the usage and the availability of any services described herein. The information is not intended for distribution to or use by any person or entity in any jurisdiction where such distribution would be contrary to the applicable law or provisions. If not otherwise stated daily price data refers to pre-day closing levels and iBoxx bond index characteristics refer to the previous month-end index characteristics.

Coverage Policy A list of the companies covered by UniCredit Bank is available upon request. Frequency of reports and updates It is intended that each of these companies be covered at least once a year, in the event of key operations and/or changes in the recommendation.

SIGNIFICANT FINANCIAL INTEREST UniCredit Bank AG and/or other related legal persons with them regularly trade shares of the analyzed company. UniCredit Bank AG and/or other related legal persons may hold significant open derivative positions on the stocks of the company which are not delta-neutral. UniCredit Bank AG and/or other related legal persons have a significant financial interest relating to the analyzed company or may have such at any future point of time. Due to the fact that UniCredit Bank AG and/or any related legal person are entitled, subject to applicable law, to perform such actions at any future point in time which may lead to the existence of a significant financial interest, it should be assumed for the purposes of this information that UniCredit Bank AG and/or any related legal person will in fact perform such actions which may lead to the existence of a significant financial interest relating to the analyzed company. Analyses may refer to one or several companies and to the securities issued by them. In some cases, the analyzed companies have actively supplied information for this analysis.

INVESTMENT SERVICES The analyzed company and UniCredit Bank AG and/or any related legal person concluded an agreement on the provision of investment services in the previous 12 months, in return for which the Bank and/or such related legal person received a consideration or promise of consideration or intends to do so. Due to the fact that UniCredit Bank AG and/or any related legal person are entitled to conclude, subject to applicable law, an agreement on the provision of investment services with the analyzed company at any future point in time and may receive a consideration or promise of consideration, it should be assumed for the purposes of this information that UniCredit Bank AG and/or any related legal person will in fact conclude such agreements and will in fact receive such consideration or promise of consideration.

ANALYST DECLARATION The author’s remuneration has not been, and will not be, geared to the recommendations or views expressed in this study, neither directly nor indirectly.

ORGANIZATIONAL AND ADMINISTRATIVE ARRANGEMENTS TO AVOID AND PREVENT CONFLICTS OF INTEREST To prevent or remedy conflicts of interest, UniCredit Bank AG, UniCredit Bank AG London Branch, UniCredit Bank AG Milan Branch, UniCredit Bank Austria AG, UniCredit Bulbank, Zagrebačka banka d.d., UniCredit Bank Czech Republic and Slovakia, Bank Pekao, ZAO UniCredit Bank Russia, UniCredit Bank Czech Republic and Slovakia Slovakia Branch, UniCredit Bank Romania, UniCredit Bank AG New York Branch have established the organizational arrangements required from a legal and supervisory aspect, adherence to which is monitored by its compliance department. Conflicts of interest arising are managed by legal and physical and non-physical barriers (collectively referred to as “Chinese Walls”) designed to restrict the flow of information between one area/department of UniCredit Bank AG, UniCredit Bank AG London Branch, UniCredit Bank AG Milan Branch, UniCredit Bank Austria AG, UniCredit Bulbank, Zagrebačka banka d.d., UniCredit Bank Czech Republic and Slovakia, Bank Pekao, ZAO UniCredit Bank Russia, UniCredit Bank Czech Republic and Slovakia Slovakia Branch, UniCredit Bank Romania, UniCredit Bank AG New York Branch, and another. In particular, Investment Banking units, including corporate finance, capital market activities, financial advisory and other capital raising activities, are segregated by physical and non-physical boundaries from Markets Units, as well as the research department. In the case of equities execution by UniCredit Bank AG Milan Branch, other than as a matter of client facilitation or delta hedging of OTC and listed derivative positions, there is no proprietary trading. Disclosure of publicly available conflicts of interest and other material interests is made in the research. Analysts are supervised and managed on a day-to-day basis by line managers who do not have responsibility for Investment Banking activities, including corporate finance activities, or other activities other than the sale of securities to clients.

ADDITIONAL REQUIRED DISCLOSURES UNDER THE LAWS AND REGULATIONS OF JURISDICTIONS INDICATED You will find a list of further additional required disclosures under the laws and regulations of the jurisdictions indicated on our website www.cib-unicredit.com/research-disclaimer. Notice to Austrian investors: This analysis is only for distribution to professional clients (Professionelle Kunden) as defined in article 58 of the Securities Supervision Act. Notice to investors in Bosnia and Herzegovina: This report is intended only for clients of UniCredit in Bosnia and Herzegovina who are institutional investors (Institucionalni investitori) in accordance with Article 2 of the Law on Securities Market of the Federation of Bosnia and Herzegovina and Article 2 of the Law on Securities Markets of the Republic of Srpska, respectively, and may not be used by or distributed to any other person. This document does not constitute or form part of any offer for sale or subscription for or solicitation of any offer to buy or subscribe for any securities and neither this document nor any part of it shall form the basis of, or be relied on in connection with or act as an inducement to enter into, any contract or commitment whatsoever. Notice to Brazilian investors: The individual analyst(s) responsible for issuing this report represent(s) that: (a) the recommendations herein reflect exclusively the personal views of the analysts and have been prepared in an independent manner, including in relation to UniCredit Group; and (b) except for the potential conflicts of interest listed under the heading “Potential Conflicts of Interest” above, the analysts are not in a position that may impact on the impartiality of this report or that may constitute a conflict of interest, including but not limited to the following: (i) the analysts do not have a relationship of any nature with any person who works for any of the companies that are the object of this report; (ii) the analysts and their respective spouses or partners do not hold, either directly or indirectly, on their behalf or for the account of third parties, securities issued by any of the companies that are the object of this report; (iii) the analysts and their respective spouses or partners are not involved, directly or indirectly, in the acquisition, sale and/or trading in the market of the securities issued by any of the companies that are the object of this report; (iv) the analysts and their respective spouses or partners do not have any financial interest in the companies that are the object of this report; and (v) the compensation of the analysts is not, directly or indirectly, affected by UniCredit’s revenues arising out of its businesses and financial transactions. UniCredit represents that: except for the potential conflicts of interest listed under the heading “Potential Conflicts of Interest” above, UniCredit, its controlled companies, controlling companies or companies under common control (the “UniCredit Group”) are not in a condition that may impact on the impartiality of this report or that may constitute a conflict of interest, including but not limited to the following: (i) the UniCredit Group does not hold material equity interests in the companies that are the object of this report; (ii) the companies that are the object of this report do not hold material equity interests in the UniCredit Group; (iii) the UniCredit Group does not have material financial or commercial interests in the companies or the securities that are the object of this report; (iv) the UniCredit Group is not involved in the acquisition, sale and/or trading of the securities that are the object of this report; and (v) the UniCredit Group does not receive compensation for services rendered to the companies that are the object of this report or to any related parties of such companies. Notice to Canadian investors: This communication has been prepared by UniCredit Bank AG, which does not have a registered business presence in Canada. This communication is a general discussion of the merits and risks of a security or securities only, and is not in any way meant to be tailored to the needs and circumstances of any recipient. The contents of this communication are for information purposes only, therefore should not be construed as advice and do not constitute an offer to sell, nor a solicitation to buy any securities. Notice to Cyprus investors: This document is directed only at clients of UniCredit Bank who are persons falling within the Second Appendix (Section 2, Professional Clients) of the law for the Provision of Investment Services, the Exercise of Investment Activities, the Operation of Regulated Markets and other Related Matters, Law 144(I)/2007 and persons to whom it may otherwise lawfully be communicated who possess the experience, knowledge and expertise to make their own investment decisions and properly assess the risks that they incur (all such persons together being referred to as “relevant persons”). This document must not be acted on or relied on by persons who are not relevant persons or relevant persons who have requested to be treated as retail clients. Any investment or investment activity to which this communication related is available only to

21 March 2017 Credit Research

Credit Flash – Deutsche Telekom

UniCredit Research page 11 .

relevant persons and will be engaged in only with relevant persons. This document does not constitute an offer or solicitation to any person to whom it is unlawful to make such an offer or solicitation. Notice to Hong Kong investors: This report is for distribution only to “professional investors” within the meaning of Schedule 1 to the Securities and Futures Ordinance (Chapter 571, Laws of Hong Kong) and any rules made thereunder, and may not be reproduced, or used by or further distributed to any other person, in whole or in part, for any purpose. This report does not constitute or form part of an offer or solicitation of any offer to buy or sell any securities, nor should it or any part of it form the basis of, or be relied upon in connection with, any contract or commitment whatsoever. By accepting this report, the recipient represents and warrants that it is entitled to receive such report in accordance with, and on the basis of, the restrictions set out in this “Disclaimer” section, and agrees to be bound by those restrictions. Notice to investors in Ivory Coast: The information contained in the present report have been obtained by Unicredit Bank AG from sources believed to be reliable, however, no express or implied representation or warranty is made by Unicredit Bank AG or any other person as to the completeness or accuracy of such information. All opinions and estimates contained in the present report constitute a judgement of Unicredit Bank AG as of the date of the present report and are subject to change without notice. They are provided in good faith but without assuming legal responsibility. This report is not an offer to sell or solicitation of an offer to buy or invest in securities. Past performance is not an indicator of future performance and future returns cannot be guaranteed, and there is a risk of loss of the initial capital invested. No matter contained in this document may be reproduced or copied by any means without the prior consent of Unicredit Bank AG. Notice to New Zealand investors: This report is intended for distribution only to persons who are “wholesale clients” within the meaning of the Financial Advisers Act 2008 (“FAA”) and by receiving this report you represent and agree that (i) you are a “wholesale client” under the FAA (ii) you will not distribute this report to any other person, including (in particular) any person who is not a “wholesale client” under the FAA. This report does not constitute or form part of, in relation to any of the securities or products covered by this report, either (i) an offer of securities for subscription or sale under the Securities Act 1978 or (ii) an offer of financial products for issue or sale under the Financial Markets Conduct Act 2013. Notice to Omani investors: This communication has been prepared by UniCredit Bank AG. UniCredit Bank AG does not have a registered business presence in Oman and does not undertake banking business or provide financial services in Oman and no advice in relation to, or subscription for, any securities, products or financial services may or will be consummated within Oman. The contents of this communication are for the information purposes of sophisticated clients, who are aware of the risks associated with investments in foreign securities and neither constitutes an offer of securities in Oman as contemplated by the Commercial Companies Law of Oman (Royal Decree 4/74) or the Capital Market Law of Oman (Royal Decree 80/98), nor does it constitute an offer to sell, or the solicitation of any offer to buy non-Omani securities in Oman as contemplated by Article 139 of the Executive Regulations to the Capital Market Law (issued vide CMA Decision 1/2009). This communication has not been approved by and UniCredit Bank AG is not regulated by either the Central Bank of Oman or Oman’s Capital Market Authority. Notice to Pakistani investors: Investment information, comments and recommendations stated herein are not within the scope of investment advisory activities as defined in sub-section I, Section 2 of the Securities and Exchange Ordinance, 1969 of Pakistan. Investment advisory services are provided in accordance with a contract of engagement on investment advisory services concluded with brokerage houses, portfolio management companies, non-deposit banks and the clients. The distribution of this report is intended only for informational purposes for the use of professional investors and the information and opinions contained herein, or any part of it shall not form the basis of, or be relied on in connection with or act as an inducement to enter into, any contract or commitment whatsoever. Notice to Polish Investors: This document is intended solely for professional clients as defined in Art. 3.39b of the Trading in Financial Instruments Act of 29 July 2005 (as amended). The publisher and distributor of the document certifies that it has acted with due care and diligence in preparing it, however, assumes no liability for its completeness and accuracy. This document is not an advertisement. It should not be used in substitution for the exercise of independent judgment. Notice to Serbian investors: This analysis is only for distribution to professional clients (profesionalni klijenti) as defined in article 172 of the Law on Capital Markets. Notice to UK investors: This communication is directed only at clients of UniCredit Bank who (i) have professional experience in matters relating to investments or (ii) are persons falling within Article 49(2)(a) to (d) (“high net worth companies, unincorporated associations, etc.”) of the United Kingdom Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 or (iii) to whom it may otherwise lawfully be communicated (all such persons together being referred to as “relevant persons”). This communication must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this communication relates is available only to relevant persons and will be engaged in only with relevant persons. CR e 17/3

21 March 2017 Credit Research

Credit Flash – Deutsche Telekom

UniCredit Research page 12 .

UniCredit Research* Erik F. Nielsen Group Chief Economist Global Head of CIB Research +44 207 826-1765 [email protected]

Dr. Ingo Heimig Head of Research Operations +49 89 378-13952 [email protected]

Credit Research

Luis Maglanoc, CFA, Head +49 89 378-12708 [email protected]

Credit Strategy & Structured Credit Research

Dr. Philip Gisdakis, Head Credit Strategy +49 89 378-13228 [email protected]

Dr. Christian Weber, CFA, Deputy Head Credit Strategy +49 89 378-12250 [email protected]

Dr. Tim Brunne Quantitative Credit Strategy +49 89 378-13521 [email protected]

Holger Kapitza Credit Strategy & Structured Credit +49 89 378-28745 [email protected]

Dr. Stefan Kolek EEMEA Corporate Credits & Strategy +49 89 378-12495 [email protected]

Manuel Trojovsky Credit Strategy & Structured Credit +49 89 378-14145 [email protected]

Financials Credit Research

Franz Rudolf, CEFA, Head Covered Bonds +49 89 378-12449 [email protected]

Valentina Stadler, Deputy Head Sub-Sovereigns & Agencies +49 89 378-16296 [email protected]

Dr. Tilo Höpker Banks +49 89 378-12960 [email protected]

Luis Maglanoc, CFA Regulatory & Accounting Service +49 89 378-12708 [email protected]

Natalie Tehrani Monfared Regulatory & Accounting Service +49 89 378-12242 [email protected]

Dr. Michael Teig Banks +49 89 378-12429 [email protected]

Robert Vielhaber Sub-Sovereigns & Agencies, Green Bonds +49 89 378-12004 [email protected]

Corporate Credit Research

Stephan Haber, CFA, Co-Head Telecoms, Technology +49 89 378-15192 [email protected]

Dr. Sven Kreitmair, CFA, Co-Head Automotive & Mobility +49 89 378-13246 [email protected]

Jana Arndt, CFA Industrials +49 89 378-13211 [email protected]

Christian Aust, CFA Industrials +49 89 378-12806 [email protected]

Mehmet Dere Oil & Gas, EEMEA Energy, Consumer +49 89 378-11294 [email protected]

Michael Gerstner Utilities, Hybrids +49 89 378-15449 [email protected]

Jonathan Schroer, CFA Media/Cable, Logistics, Business Services +49 89 378-13212 [email protected]

Dr. Silke Stegemann, CEFA Health Care & Pharma, Food & Beverage, Personal & Household Goods +49 89 378-18202 [email protected]

Publication Address

UniCredit Research Corporate & Investment Banking UniCredit Bank AG Arabellastrasse 12 D-81925 Munich [email protected]

Bloomberg UCCR Internet www.research.unicredit.eu

*UniCredit Research is the joint research department of UniCredit Bank AG (UniCredit Bank), UniCredit Bank AG London Branch (UniCredit Bank London), UniCredit Bank AG Milan Branch (UniCredit Bank Milan), UniCredit Bank New York (UniCredit Bank NY), UniCredit Bank Austria AG (Bank Austria), UniCredit Bulbank, Zagrebačka banka d.d., UniCredit Bank Czech Republic and Slovakia, Bank Pekao, ZAO UniCredit Bank Russia (UniCredit Russia), UniCredit Bank Romania. 17/1