Embed Size (px)

Citation preview

NONPROFIT MANAGEMENT & LEADERSHIP, vol. 18, no. 4, Summer 2008 © 2008 Wiley Periodicals, Inc. 435Published online in Wiley InterScience (www.interscience.wiley.com). DOI: 10.1002/nml.197

Determinants of Compensation:A Study of Pay, Performance,and Gender Differences forFundraising Professionals

Debra J. Mesch, Patrick M. RooneyThis study examines the determinants of compensation forfundraising professionals by addressing the following researchquestions: (1) Is there a significant pay-performance relation-ship? (2) What are the factors that affect bonus and salary? (3) Is there a gender-pay gap for individuals who are in the roleof fundraisers? Data were collected over a four-year period froma national sample of fundraising professionals employed acrossall industry classifications. Amount of money raised was the primary performance variable of interest. Bivariate tests for differences between males and females, as well as two-stagesimultaneous regressions, were used to determine the effects offundraising performance on the pay of fundraisers. Results indi-cated a significant and positive pay-performance linkage acrossall fundraising positions, particularly for chief development offi-cers, as well as a consistent gender-pay gap across fundraisingpositions.

ALTHOUGH THERE HAS BEEN some theoretical work on compen-sation in nonprofits (for example, Hallock, 2000; Ruhm andBorkoski, 2003; Steinberg, 1990; Weisbrod, 1988), we have

little understanding of the actual determinants of compensation innonprofits from an empirical point of view (Hallock, 2000). One rea-son for the lack of empirical testing is that given the constraints andcharacteristics of the nonprofit sector, examining pay is problematic(Hallock, 2000). However, without a body of research that specifically

Note: We thank our research assistants, Brian Denton and Yuan Ding, master’sdegree students in economics, for their assistance in the empirical analysis. We also thank an anonymous reviewer for the suggestion of using two-stage simul-taneous regressions. Finally, we are indebted to Partha Deb of Hunter College forinsights and suggestions in solving the technical problems associated with usinginstrumental variables and two-stage simultaneous regressions.

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 435

Nonprofit Management & Leadership DOI: 10.1002/nml

436 ME S C H, RO O N E Y

focuses on compensation in the nonprofits, it is difficult to deter-mine whether incentive systems that are found to be successful inthe private sector will have their intended effects in the nonprofitarena.

There are several reasons that the lack of empirical research andvalidation of compensation systems in the nonprofit sector is trou-bling. First, compensation packages have exploded for many chiefexecutives in the nonprofit sector (Schwinn and Wilhelm, 2003).Salaries paid in 2003 to the top executives of the nation’s largest non-profits rose by twice the inflation rate, and the salaries of CEOs ofthe largest charities and foundations more than doubled from 1997to 2002; in fact, they received higher percentage raises than did theircounterparts in the corporate world (Schwinn and Wilhelm, 2003).Second, although use of performance-based compensation plans isa relatively new practice in nonprofits, such practices are becomingmore prevalent and are expected to increase in the future (Alvarado,1996; Bailey and Risher, 1996; Deckop and Cirka, 2000). Some stud-ies have found that 25 percent of nonprofits offer managers theopportunity to earn cash compensation—usually tied to achievementof performance measures (Rocco, 1991, 1992). Third, managementpay in the nonprofit world is becoming more highly scrutinized.New legislation requires nonprofits to document how much they paytheir top management as well as require that boards justify and out-line the compensation determination process (Preston, 2004). “If thesalaries are found to be higher than expected and higher than thosefound in similar charities,” fines could be levied and boards couldbe required to return the amount overpaid (Hallock, 2002a, p. 378).

Our study uses compensation survey data from a large nationalmembership association—the Association of Fundraising Profes-sionals (AFP)—a professional society responsible for generating phil-anthropic support for a wide variety of nonprofits. Its mission is toadvance philanthropy by enabling people and organizations to prac-tice ethical and effective fundraising—activities that include educa-tion, training, mentoring, research, credentialing and advocacy.

Membership associations may be defined as “mutual benefitorganizations, incorporated to serve their members’ interests”(Tschirhart, 2006, p. 523), formally organized and usually not rec-ompensed for their participation (Knoke, 1986). Although mem-bership associations make up a significant component of thenonprofit sector—consisting of 33 percent of the nonprofits regis-tered in the United States (Tschirhart, 2006)—there is a paucity ofresearch on this sector and virtually no examination of executive payin this type of nonprofit.

Purpose of the StudyThe purpose of our study is to address the following research ques-tions: (1) What are the significant determinants of compensation for

Compensationpackages haveexploded formany chief

executives in thenonprofit sector.

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 436

DE T E R M I N A N T S O F CO M P E N S AT I O N 437

Nonprofit Management & Leadership DOI: 10.1002/nml

individuals who are employed as fundraising professionals in non-profits? More specifically, does performance have a significant effecton compensation for these professionals? (2) What are the key deter-minants of bonus and salary for these individuals? (3) Is there agender-pay gap for individuals who are in the role of fundraisers fornonprofits?

First, we test to see whether there is a relationship betweenfundraiser performance and compensation. We selected fundraisingprofessionals because of the implicit relationship between their rolein the organization and performance (that is, “contributions raised”)to better test the pay-performance relationship. Performance can beappropriately rewarded only if it can be accurately measured anddirectly related to employee efforts. Presumably we would expect tosee a more direct linkage between job content or job responsibilitiesand performance for individuals who are in the role of fundrais-ing rather than other types of positions in nonprofits. In fact, fundraisinghas been described as a profession that is mission driven, offering cleargoals, advancement based on results, and work performance that isquantifiable (Tifft, 1992). In our study, we use “money raised,” aquantifiable measure of performance that directly relates to the effortsof fundraisers and is a measure of success. Furthermore, fundraisingprofessionals are unique to the nonprofit sector and traditionally notfound in for-profit firms. Few studies have been conducted that lookat determinants of compensation for these individuals.

Second, we disaggregate compensation into bonus and salary inorder to examine the pay-performance relationship more fully. Is thepay-performance relationship for fundraisers significant for bonus,for salary, or both? Studies comparing for-profit and nonprofit orga-nizations have found that nonprofits paid greater base salaries, lowerbonuses, and lower total compensation than for-profits, ceterisparibus (Roomkin and Weisbrod, 1999; Weisbrod, 1983). However,for fundraisers, where the measure of performance is objective andmeasurable (as is primarily the case in for-profit firms), there may bea more contingent relationship between performance and bonusbecause it is a reliable way to reward achievement of goals. Unlikeother pay-performance studies, under these conditions we may actu-ally find a relationship between performance and bonuses.

It is important to note that there is nothing illegal about beingpaid for performance as a fundraiser—and, in fact, this may be a wayto motivate employees to increase performance (Harrison, 1995).According to ethical guidelines, fundraisers are allowed to acceptperformance-based compensation (Sczudlo, 2003). Although wewould expect to see a stronger relationship between pay and perfor-mance for fundraisers than perhaps other individuals, we need tobear in mind the ethical standards facing fundraisers in nonprofitsand the importance of upholding the public trust. “In fact, nowhereis ethical behavior more essential, or its absence more damaging, thanin philanthropic fundraising” (Sczudlo, 2003, p. 30). As such,

There is nothingillegal about

being paid forperformance as afundraiser—and

this may be a wayto motivate

employees toincrease

performance

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 437

the pay-for-performance relationship for fundraisers may be some-what suppressed, where a “commission” or percentage-based pay forperformance is prohibited.

Third, we focus on issues of gender equity in the fundraisingworkforce. Over the past decade, there has been an increase in thememberships of the top three professional organizations representingfundraisers, to the point now where the majority of professionalsare women (Conry, 1998). Furthermore, more women than men areentering this profession as paid employees where women occupy allfundraising job categories across all types of nonprofit organizations(Conry, 1998). Conry (1991) refers to this phenomenon as “the fem-inization of fundraising” and cautions that this could have negativeimplications on the salaries, prestige, and status of a previouslymale-dominated occupation in which fundraising is seen as“women’s work.”

Much research has been conducted on the gender-pay gap in theprivate sector (for example, Bertrand and Hallock, 2001; Blau andFerber, 1992; Chauvin and Ash, 1994; Gerhart, 1990; Groshen, 1991;Harris, Gilbreath, and Sunday, 2002; Mohan and Ruggiero, 2003;Rose and Hartmann, 2004; Wood, Corcoran, and Courant, 1993),indicating that women are paid significantly less than men, evenwhen controlling for the industry, firm size, occupation, human cap-ital, performance, and organizational structural factors that are tra-ditionally associated with pay differentials. Although the nonprofitsector is dominated by women, very little research addresses wagedifferences between men and women (Hallock, 2000; Steinberg andJacobs, 1994). In our study, we investigate whether this finding per-sists in the nonprofit sector, in a profession where there is a quan-tifiable measure of performance as well as a preponderance of womenrecently entering the profession.

Compensation in Nonprofit OrganizationsMuch has been written regarding the theoretical reasons for differ-ences between compensation in the for-profit and nonprofit sectorand why compensation systems found in for-profit firms may notgeneralize to nonprofits (see Ballou and Weisbrod, 2003; Hallock,2000; Leete, 2001; Preston, 1989; Steinberg, 1990; Weisbrod, 1986,1988; Young and Steinberg, 1995 for discussion of this literature). Aprimary difference is that nonprofits operate under the “nondistribu-tion constraint” (Hansmann, 1980), thereby prohibiting distributionof profits to owners, and thus restricting organizations as to the type ofcompensation practices as well as the form of compensation thatcan be offered to its managers and employees. Given the nondistrib-ution constraint, “performance pay in nonprofits has historically notbeen very significant,” even though nonprofits are not precludedlegally from engaging in this practice (Hallock, 2000, p. 259). Severalrecent studies, however, have found a strong, positive link between

438 ME S C H, RO O N E Y

Nonprofit Management & Leadership DOI: 10.1002/nml

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 438

the assets of a nonprofit and the pay of its top manager (for example,Brickley and Van Horn, 2002; Hallock, 2002a). Gray and Benson(2003) found that when resource efficiency was used as an indicatorof performance, nonprofit executive compensation was based, at leastin part, on organizational performance, although client satisfactionhad no effect. A recent study by Carroll, Hughes, and Luksetich(2005) found a positive relationship between executive compensa-tion and performance when performance was measured as revenueper dollar of noncompensation expenditure. However, this analysisrevealed that compensation and performance were simultaneouslydetermined.

The nondistribution constraint in the nonprofit sector leads to a“sorting” of managers among the two sectors where “managers withthe least aversion to risk and the weakest preference for leading anorganization that has goals other than profit maximization” are moreattracted to the for-profit rather than the nonprofit sector (Roomkinand Weisbrod, 1999, p. 778). Given that the nondistribution con-straint restricts managerial discretion—particularly regarding com-pensation decisions—managers, as well as other employees, may sortthemselves according to the type of organization that they find mostcompatible with their preferences. That is, individuals may be will-ing to “donate” their paid labor to a nonprofit cause that they careabout by accepting less compensation (Frank, 1996).

A second significant difference between compensation in the for-profit and nonprofit sectors has to do with the way in which perfor-mance is measured. Unlike for-profit firms where the bottom-lineperformance is focused on making a profit and demonstration ofresults, nonprofits conduct business in pursuit of a social mission,where ideal information on performance is often unobtainable, costly,abstract, and not easily quantified (Weisbrod, 1988). Finding appro-priate performance metrics to satisfy stakeholders, as well as deter-mining which performance indicators should be tied to pay, is muchmore difficult (Hallock, 2000; Handy and Katz, 1998; Steinberg,1990). Consequently, nonprofit boards often rely on more indirect andimperfect measures of performance, such as activity or process mea-sures (Weisbrod, 1988). As such, nonprofits must choose betweenrewarding what is easily measured—even though this may not rewardthe desired outcomes—incurring costs by devising better measures orby not rewarding performance at all (Weisbrod, 1988).

However, in comparison to other types of positions in nonprof-its, fundraising actually is results oriented, and outcomes can be mea-sured (Duronio and Loessin, 1991). This is not to imply thatorganizations providing fundraisers with specific goals are engagingin unethical behavior—or that they will be more ethical and pro-ductive if the focus is on process rather than on the results achieved.Instead, the role of fundraisers requires an understanding of the bal-ance between “concern for results with concern for how results areachieved” (Durnio and Loessin, 1991, p. 129). In fact, fundraisers

DE T E R M I N A N T S O F CO M P E N S AT I O N 439

Nonprofit Management & Leadership DOI: 10.1002/nml

Several recentstudies have founda strong, positivelink between the

assets of anonprofit and the

pay of its topmanager.

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 439

who do not have specific, measurable goals and are not judged bywhat they accomplish may leave more room for unethical behaviorthan if evaluated on actual performance (Duronio and Loessin,1991). However, it has been suggested that “incentive contracts forfundraisers may lead to a perception among donors that their con-tributions are being diverted away from the organization’s major pur-pose and toward fundraiser compensation” (Carroll, Hughes, andLuksetich, 2005, p. 20).

Gender and PayResearch efforts over the past three decades “have attempted to disen-tangle factors that account for the gender-pay gap” (Renner, Rives, andBowlin, 2002, p. 332), and a great deal of theoretical work has beendeveloped in explaining the reasons that these differences occur (forexample, Blau, 1998; Blau and Ferber, 1992; Blau, Ferber, and Winkler,1998; Weichselbaumer, 2004). Reports in the popular press give anaccount of surveys that indicate senior female executives as well asother top positions of our nation’s nonprofits are routinely paid lessthan men in similar jobs: as high as a 50 percent gender differentialexists for CEOs (Lewin, 2001; Lipman, 2002). The pay gap is greatestamong the largest nonprofits (Lipman, 2002; GuideStar, 2005), per-sisting even across comparable job titles and responsibilities (Williams,2003), controlling for organization size (GuideStar, 2005).

Recent empirical research on nonprofits has found similar results.Although a few studies have found that CEO gender was not signifi-cantly related to compensation of nonprofits (for example, Oster, 1998;Preston, 1989), the majority of studies have found just the opposite(for example, Hallock, 2002b; Gibelman, 2000; Gray and Benson,2003; Werner, Konopaske, and Gemeinhardt, 2000; Williams, 2003;Ye and Manzo, 2004). Given that the nonprofit labor force is domi-nated by women, these results are even more troubling. According tothe Bureau of Labor Statistics, more than two-thirds of nonprofit work-ers are women, compared with about 43 percent of the employed civil-ian labor force as a whole (Johnston and Rudney, 1987).

MethodsIn terms of fundraising professionals, Conry (1998) summarizes sev-eral surveys that conclude female fundraisers have not made equalprogress in compensation rates. These findings indicate that (1)although overall salaries are climbing for fundraisers, women’s payconsistently lags behind that of men, and (2) women holding seniormanagement positions in fundraising are still a fraction of their over-all numbers as a group. These surveys, however, did not control forthe human capital factors traditionally associated with compensa-tion. The purpose of our study is to test whether a pay gap exists,controlling for organizational and human capital variables.

440 ME S C H, RO O N E Y

Nonprofit Management & Leadership DOI: 10.1002/nml

The pay gap[between malesand females in

top positions] isgreatest among

the largestnonprofits.

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 440

Sample and DataA national cross-sectional sample consisting of 2,439 fundraising pro-fessionals across all subsectors of the nonprofit field was collectedthrough the AFP’s Compensation and Benefits Survey that wasadministered once a year for four years. The sample consists of pro-fessionals who are members of the AFP and are currently employedin fundraising roles in a nonprofit organization. AFP was founded in1960 and has approximately twenty-six thousand members in 171chapters throughout the world.

The respondents are employed in the following types of non-profits: 27 percent are from education, 5 percent from religious orga-nizations, 9 percent from social services, 23 percent from arts andculture, 20 percent from health, and 11 percent are other; 68 percentare employed full time, 26 percent more than half time, and 2 per-cent less than half time; 43 percent are in positions as chief develop-ment officer (CDO), 23 percent deputy director, 20 percent staff, and8 percent consultant. Mean age of respondents is forty-four; 69 per-cent of the sample is female, 94 percent white; 24 percent have abachelor’s degree, and 49 percent have postgraduate education. Theaverage number of years employed as a fundraising professional is14. Most of the respondents (58 percent) have one or more profes-sional certificates. The average salary in the sample was $70,000 andranged as high as $850,000. Bonuses tended to be a small share ofcompensation, averaging only 1.2 percent, but they went as high as25 percent. Most (81 percent) responding organizations did not paya bonus. While the average fundraising experience overall is 14 years,the average with the current particular nonprofit is only 4.5 years, sug-gesting considerable churning among fundraisers. This turnover maybe a way that fundraisers, particularly women, seek pay equity giventhat pay raises occur with job changes. While 24 percent have a con-tract, only 3 percent received a signing bonus at the time of hire.

Four years of survey data were obtained for the period from 2002to 2005 from AFP. Each year, AFP conducts a compensation and ben-efits survey of all its members. The survey asks questions about con-tributions raised, the organization’s operating budget, bonus andsalary information, and demographic information.

Dependent VariableThe dependent variable was compensation. CEO compensation wasoperationalized in two ways: base salary and bonus only (over atwelve-month period). These measures represent total cash providedto the incumbent and are widely used in the executive compensationliterature. In theory, base salary is used to represent a fixed compo-nent of total compensation, whereas bonuses vary according to somemeasure of performance (Gomez-Mejia, 1994). To adjust for the widerange of salaries and more closely approximate a normal distribution,we use logSalary as the measure of salary in the analysis. Bonus isexpressed as the percentage of total compensation.

DE T E R M I N A N T S O F CO M P E N S AT I O N 441

Nonprofit Management & Leadership DOI: 10.1002/nml

The dependentvariable was

compensation.

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 441

Independent VariablePerformance was operationalized as the amount of money raised bythe organization in contributed gifts from all sources in a particularfiscal year. We use logMoney in the analysis.

Control VariablesThe control variables were as follows:

Type of organization. Organizations were coded as (1) educational,(2) religious, (3) consulting firm, partnership, or sole entrepre-neurship, (4) health, (5) social service, (6) arts and culture, (7)other.

Geographic scope. This was coded as (1) international, (2) national,(3) state, provincial, regional, or (4) local.

Organizational size. Organizational size was (1) operating budgetcoded as the log(Budget) for the fiscal year and (2) number offundraising support staff.

Region. The location of the organization was coded as (1) UnitedStates or (2) other.

Size of the metropolitan area was a categorical variable indicating pop-ulation of the metropolitan area, coded as (1) 0 to 500,000, (2)500,000 to 1 million, (3) 1 million to 3 million, or (4) more than3 million.

Position in the organization was coded as (1) chief development offi-cer, (2) deputy director, (3) staff, or (4) consultant.

Experience was coded as the number of years employed as a fundrais-ing professional as well as experience squared, and number of yearswith current employer.

Contract was whether the fundraising professional was under anemployment contract.

Signing bonus was whether the fundraising professional had a sign-ing bonus when hired.

Recruiter was whether the fundraising professional worked with anexecutive recruiter to secure their position.

Age was coded as age and age squared.Gender was coded as 1 � female.Race was white, black, or other. Black was coded � 1 if the respon-

dent self-identified s as black. “Other” was coded � 1 if therespondent indicated that they were a member of a nonblackminority group.

Education was (1) high school, (2) some college, (3) baccalaureatedegree, or (4) more than the baccalaureate.

Certification was coded as having at least one of the following pro-fessional certifications: Certified Fundraising Executive (CFRE),Advanced Certified Fundraising Executive (ACFRE), or Fellow forthe Association of Healthcare Philanthropy (FAHP), or other.

Year was coded as year of the survey. Year 1 is the comparison measure.

442 ME S C H, RO O N E Y

Nonprofit Management & Leadership DOI: 10.1002/nml

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 442

Analysis and ResultsThe Carroll, Hughes, and Luksetich (2005) study raises the questionof the causality between pay and performance: Do employees workharder when they are paid more, or do harder-working employees getpaid more? Given this issue of simultaneity and endogeneity, the esti-mation process is less clear-cut than might be desired. To account forthis, we use a two-stage simultaneous estimation process (2SLS).

Model Used for AnalysisWe first estimate compensation using pooled time-series cross-sectional ordinary least squares (OLS) to find the impact of produc-tivity and other variables on salary and bonus among differentfundraising positions. We have an unbalanced panel with unmatchedsurvey respondents each year. Therefore, in order to maximize thepower of the regressions, we include all respondents in each year foreach position and control for year-specific effects, which would cap-ture differences in the overall macroeconomic effects in a given year.

In order to estimate the effects of performance on pay, we needto find a measure of performance or productivity that is exogenousor independent of compensation. To do this, we estimate productiv-ity (money raised) based on the size of the development budget andthe development staff, as well as the other independent variables weused to estimate compensation. We use the size of the developmentbudget and the development staff as instrumental variables to esti-mate productivity (money raised), because these variables arearguably related to the amounts raised but unrelated directly to com-pensation. In the second stage, we use the independently estimatedvalue of productivity (money raised) as an independent variable toestimate the pay-for-performance relationship and the effects of theother independent variables on compensation.

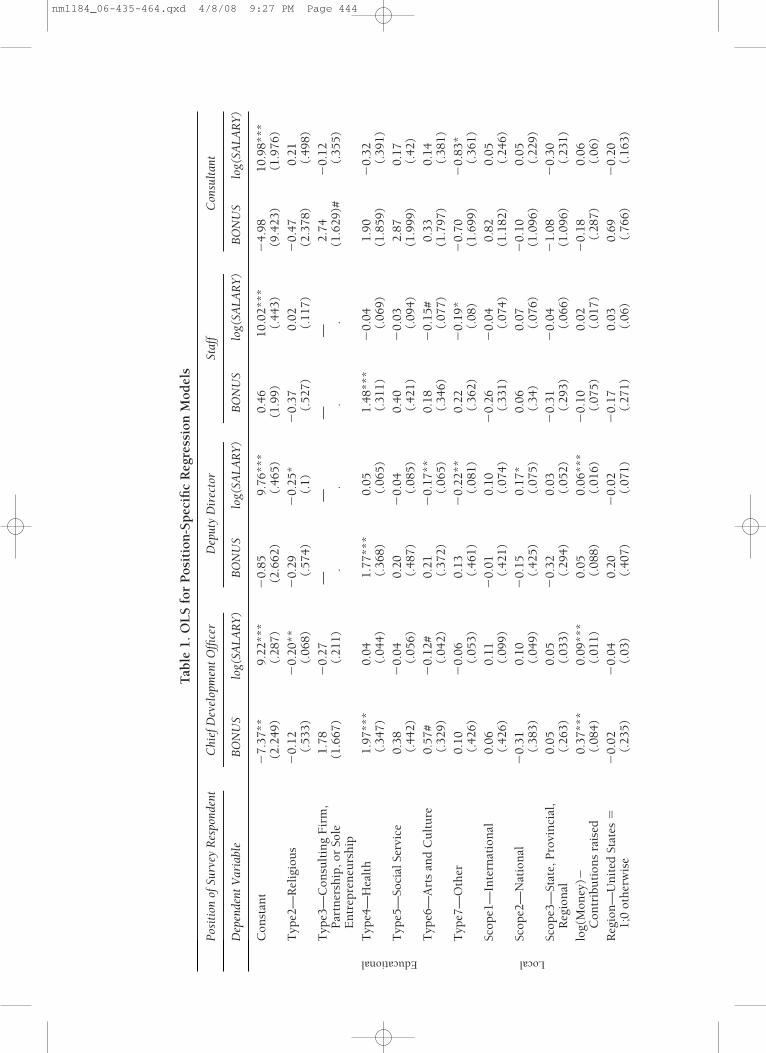

We first examine the relationship between pay and performancefor fundraising professionals and refer to the pooled OLS regressionresults in Table 1. Looking first at the results for each position only(see Table 1), we find that a 10 percent increase in funds raised bythe organization is significantly associated with a 0.9 percent raise insalary, as well as a significant increase in bonuses for the CDOs. Inaddition, deputy directors earned approximately a 0.6 percentincrease in salary for a 10 percent increase in funds raised. Dollarsraised is not significantly related to either of the compensation vari-ables for staff or consultant, which might be a reflection of either theindirect effects of these positions or the less precise meaning of con-sultants.

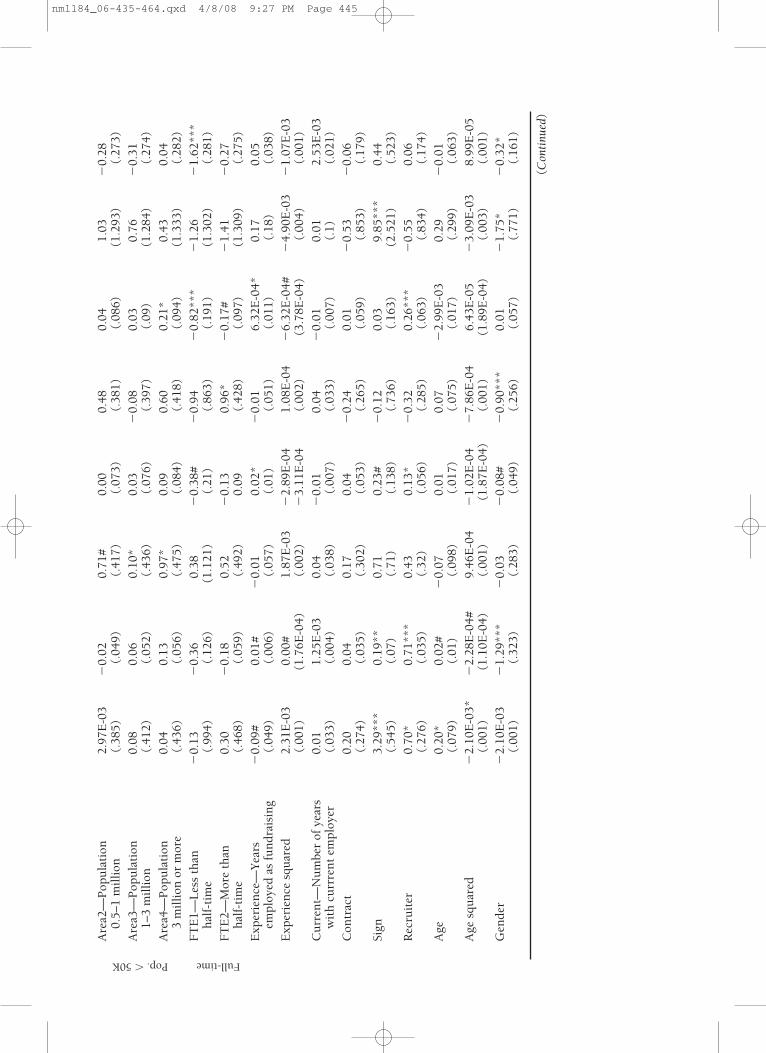

In Table 2, we provide the estimates of our measure of produc-tivity (money raised) using LnBudget and Staff (size) as instrumentalvariables that are independent of compensation but valid explanatoryvariables for productivity. We find that both LnBudget and Staff arehighly significant variables in explaining productivity (money raised)

DE T E R M I N A N T S O F CO M P E N S AT I O N 443

Nonprofit Management & Leadership DOI: 10.1002/nml

Do employeeswork harder

when they arepaid more, or doharder-workingemployees get

paid more?

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 443

Tab

le 1

. OL

S fo

r P

osit

ion

-Sp

ecifi

c R

egre

ssio

n M

odel

s

Posi

tion

of S

urve

y R

espo

nden

tC

hief

Dev

elop

men

t Offi

cer

Dep

uty

Dir

ecto

rSt

aff

Con

sult

ant

Dep

ende

nt V

aria

ble

BO

NU

Slo

g(SA

LAR

Y)

BO

NU

Slo

g(SA

LAR

Y)

BO

NU

Slo

g(SA

LAR

Y)

BO

NU

Slo

g(SA

LAR

Y)

Con

stan

t�

7.37

**9.

22**

*�

0.85

9.76

***

0.46

10.0

2***

�4.

9810

.98*

**(2

.249

)(.

287)

(2.6

62)

(.46

5)(1

.99)

(.44

3)(9

.423

)(1

.976

)T

ype2

—R

elig

iou

s�

0.12

�0.

20**

�0.

29�

0.25

*�

0.37

0.02

�0.

470.

21(.

533)

(.06

8)(.

574)

(.1)

(.52

7)(.

117)

(2.3

78)

(.49

8)T

ype3

—C

onsu

ltin

g F

irm

,1.

78�

0.27

——

——

2.74

�0.

12P

artn

ersh

ip, o

r So

le

(1.6

67)

(.21

1).

..

.(1

.629

)#(.

355)

E

ntr

epre

neu

rsh

ipT

ype4

—H

ealt

h1.

97**

*0.

041.

77**

*0.

051.

48**

*�

0.04

1.90

�0.

32

(.34

7)(.

044)

(.36

8)(.

065)

(.31

1)(.

069)

(1.8

59)

(.39

1)T

ype5

—So

cial

Ser

vice

0.38

�0.

040.

20�

0.04

0.40

�0.

032.

870.

17(.

442)

(.05

6)(.

487)

(.08

5)(.

421)

(.09

4)(1

.999

)(.

42)

Typ

e6—

Art

s an

d C

ult

ure

0.57

#�

0.12

#0.

21�

0.17

**0.

18�

0.15

#0.

330.

14(.

329)

(.04

2)(.

372)

(.06

5)(.

346)

(.07

7)(1

.797

)(.

381)

Typ

e7—

Oth

er0.

10�

0.06

0.13

�0.

22**

0.22

�0.

19*

�0.

70�

0.83

*(.

426)

(.05

3)(.

461)

(.08

1)(.

362)

(.08

)(1

.699

)(.

361)

Scop

e1—

Inte

rnat

ion

al0.

060.

11�

0.01

0.10

�0.

26�

0.04

0.82

0.05

(.42

6)(.

099)

(.42

1)(.

074)

(.33

1)(.

074)

(1.1

82)

(.24

6)Sc

ope2

—N

atio

nal

�0.

310.

10�

0.15

0.17

*0.

060.

07�

0.10

0.05

(.38

3)(.

049)

(.42

5)(.

075)

(.34

)(.

076)

(1.0

96)

(.22

9)Sc

ope3

—St

ate,

Pro

vin

cial

, 0.

050.

05�

0.32

0.03

�0.

31�

0.04

�1.

08�

0.30

Reg

ion

al

(.26

3)(.

033)

(.29

4)(.

052)

(.29

3)(.

066)

(1.0

96)

(.23

1)lo

g(M

oney

)�0.

37**

*0.

09**

*0.

050.

06**

*�

0.10

0.02

�0.

180.

06

Con

trib

uti

ons

rais

ed

(.08

4)(.

011)

(.08

8)(.

016)

(.07

5)(.

017)

(.28

7)(.

06)

Reg

ion

—U

nit

ed S

tate

s �

�0.

02�

0.04

0.20

�0.

02�

0.17

0.03

0.69

�0.

20

1;0

oth

erw

ise

(.23

5)(.

03)

(.40

7)(.

071)

(.27

1)(.

06)

(.76

6)(.

163)

Educational Local

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 444

Are

a2—

Pop

ula

tion

2.

97E

-03

�0.

020.

71#

0.00

0.48

0.04

1.03

�0.

28

0.5–

1 m

illi

on

(.38

5)(.

049)

(.41

7)(.

073)

(.38

1)(.

086)

(1.2

93)

(.27

3)A

rea3

—P

opu

lati

on

0.08

0.06

0.10

*0.

03�

0.08

0.03

0.76

�0.

311–

3 m

illi

on

(.41

2)(.

052)

(.43

6)(.

076)

(.39

7)(.

09)

(1.2

84)

(.27

4)A

rea4

—P

opu

lati

on

0.04

0.13

0.97

*0.

090.

600.

21*

0.43

0.04

3 m

illi

on o

r m

ore

(.43

6)(.

056)

(.47

5)(.

084)

(.41

8)(.

094)

(1.3

33)

(.28

2)F

TE

1—L

ess

than

�

0.13

�0.

360.

38�

0.38

#�

0.94

�0.

82**

*�

1.26

�1.

62**

*h

alf-

tim

e (.

994)

(.12

6)(1

.121

)(.

21)

(.86

3)(.

191)

(1.3

02)

(.28

1)F

TE

2—M

ore

than

0.

30�

0.18

0.52

�0.

130.

96*

�0.

17#

�1.

41�

0.27

hal

f-ti

me

(.46

8)(.

059)

(.49

2)0.

09(.

428)

(.09

7)(1

.309

)(.

275)

Exp

erie

nce

—Y

ears

�

0.09

#0.

01#

�0.

010.

02*

�0.

016.

32E

-04*

0.17

0.05

empl

oyed

as

fun

drai

sin

g (.

049)

(.00

6)(.

057)

(.01

)(.

051)

(.01

1)(.

18)

(.03

8)E

xper

ien

ce s

quar

ed2.

31E

-03

0.00

#1.

87E

-03

�2.

89E

-04

1.08

E-0

4�

6.32

E-0

4#�

4.90

E-0

3�

1.07

E-0

3(.

001)

(1.7

6E-0

4)(.

002)

�3.

11E

-04

(.00

2)(3

.78E

-04)

(.00

4)(.

001)

Cu

rren

t—N

um

ber

of y

ears

0.01

1.25

E-0

30.

04�

0.01

0.04

�0.

010.

012.

53E

-03

wit

h c

urr

ren

t em

ploy

er(.

033)

(.00

4)(.

038)

(.00

7)(.

033)

(.00

7)(.

1)(.

021)

Con

trac

t0.

200.

040.

170.

04�

0.24

0.01

�0.

53�

0.06

(.27

4)(.

035)

(.30

2)(.

053)

(.26

5)(.

059)

(.85

3)(.

179)

Sign

3.29

***

0.19

**0.

710.

23#

�0.

120.

039.

85**

*0.

44(.

545)

(.07

)(.

71)

(.13

8)(.

736)

(.16

3)(2

.521

)(.

523)

Rec

ruit

er0.

70*

0.71

***

0.43

0.13

*�

0.32

0.26

***

�0.

550.

06(.

276)

(.03

5)(.

32)

(.05

6)(.

285)

(.06

3)(.

834)

(.17

4)A

ge0.

20*

0.02

#�

0.07

0.01

0.07

�2.

99E

-03

0.29

�0.

01(.

079)

(.01

)(.

098)

(.01

7)(.

075)

(.01

7)(.

299)

(.06

3)A

ge s

quar

ed�

2.10

E-0

3*�

2.28

E-0

4#9.

46E

-04

�1.

02E

-04

�7.

86E

-04

6.43

E-0

5�

3.09

E-0

38.

99E

-05

(.00

1)(1

.10E

-04)

(.00

1)(1

.87E

-04)

(.00

1)(1

.89E

-04)

(.00

3)(.

001)

Gen

der

�2.

10E

-03

�1.

29**

*�

0.03

�0.

08#

�0.

90**

*0.

01�

1.75

*�

0.32

*(.

001)

(.32

3)(.

283)

(.04

9)(.

256)

(.05

7)(.

771)

(.16

1)

Pop. �50K Full-time

(Con

tinu

ed)

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 445

Bla

ck0.

37�

0.03

0.37

�0.

080.

59�

0.07

�0.

831.

13(.

734)

(.09

7)(.

799)

(.13

9)(.

722)

(.16

)(3

.549

)(.

737)

Oth

er�

0.65

0.08

�0.

58�

0.04

�0.

06�

0.04

1.54

0.26

(.61

2)(.

078)

(.61

6)(.

107)

(.57

9)(.

132)

(2.0

22)

(.42

)So

me

Col

lege

0.22

�3.

82E

-04

0.81

0.11

�0.

270.

25#

�0.

080.

11(.

463)

(.05

9)(.

618)

(.10

8)(.

632)

(.14

)(1

.994

)(.

415)

Bac

cala

ure

ate

Deg

ree

0.18

0.06

�0.

28�

0.04

�0.

490.

29*

�0.

01�

0.38

(.46

8)(.

06)

(.60

1)(.

106)

(.61

2)(.

135)

(1.7

95)

(.37

3)P

ost

seco

nda

ry0.

440.

18*

0.39

�0.

120.

550.

27#

0.78

�0.

35(.

552)

(.07

)(.

532)

(.09

3)(.

642)

(.14

2)(1

.698

)(.

353)

Cer

tifi

cati

on—

at le

ast

one:

0.85

*0.

040.

420.

030.

11�

0.06

0.43

�0.

23C

FR

E, A

CF

RE

, FA

HP

, Oth

er(.

408)

(.05

2)(.

369)

(.06

5)(.

389)

(.08

6)(1

.261

)(.

262)

Yea

r 2

�1.

51*

�0.

01�

0.42

�0.

40**

*1.

03*

�0.

151.

190.

31(.

612)

(.07

8)(.

62)

(.10

9)(.

522)

(.11

6)(2

.186

)(.

456)

Yea

r 3

�2.

83**

*0.

22*

�0.

59�

0.06

�0.

070.

201.

360.

32(.

761)

(.09

7)(.

803)

(.14

2)(.

694)

(.15

4)(2

.274

)(.

474)

Yea

r 4

�2.

65**

*�

0.05

�0.

12�

0.10

�0.

120.

06�

0.15

0.28

(.53

8)(.

068)

(.51

4)(.

09)

(.46

2)(.

101)

(1.7

89)

(.06

)Sa

mpl

e si

ze10

8010

7457

156

653

152

220

319

7A

dju

sted

R2

0.12

010.

3338

0.07

770.

2671

0.07

860.

1829

0.04

880.

2740

Tab

le 1

. (C

onti

nued

)

Posi

tion

of S

urve

y R

espo

nden

tC

hief

Dev

elop

men

t Offi

cer

Dep

uty

Dir

ecto

rSt

aff

Con

sult

ant

Dep

ende

nt V

aria

ble

BO

NU

Slo

g(SA

LAR

Y)

BO

NU

Slo

g(SA

LAR

Y)

BO

NU

Slo

g(SA

LAR

Y)

BO

NU

Slo

g(SA

LAR

Y)

White High school

Stan

dard

err

ors

in p

aren

thes

es.

Not

e: #

p�

0.1.

* p

�0.

05.

** p

�0.

01.

***

p�

0.00

1.

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 446

Tab

le 2

. Fir

st S

tage

Reg

ress

ion

for

Pos

itio

n-S

pec

ific

Reg

ress

ion

Mod

els

Posi

tion

of S

urve

y R

espo

nden

tC

hief

Dev

elop

men

t Offi

cer

Dep

uty

Dir

ecto

rSt

aff

Con

sult

ant

Fir

st-s

tage

reg

ress

ion

For

bon

usF

or ls

alar

yF

or b

onus

For

lsal

ary

Bon

usls

alar

yB

onus

lsal

ary

Dep

ende

nt V

aria

ble

lmon

eylm

oney

lmon

eylm

oney

lmon

eylm

oney

lmon

eylm

oney

Con

stan

t10

.26*

**10

.33*

**12

.52*

**12

.35*

**8.

01**

*7.

51**

*7.

66**

*7.

71**

*(.

697)

(.70

3)(1

.063

)(1

.061

)(.

966)

(.98

5)(1

.369

)(1

.411

)

Typ

e2—

Rel

igio

us

0.77

***

0.77

***

0.65

*0.

64**

0.09

0.11

2.11

***

2.09

***

(.16

8)(.

168)

(.24

)(.

24)

(.24

4)(.

244)

(.4)

(.41

)

Typ

e3—

Con

sult

ing

Fir

m,

4.05

***

4.05

***

——

——

2.59

***

2.58

***

Par

tner

ship

, or

Sole

(.

513)

(.51

2).

..

.(2

.737

)(.

288)

En

trep

ren

eurs

hip

Typ

e4—

Hea

lth

�0.

19#

�0.

19#

0.02

0.08

�0.

15�

0.17

�0.

93**

�0.

95*

(.11

)(.

11)

(.15

2)(.

152)

(.14

6)#

(.14

7)(.

279)

(.28

9)

Typ

e5—

Soci

al S

ervi

ce�

0.06

�0.

050.

47*

0.48

*0.

350.

320.

160.

16(.

14)

(.14

)(.

206)

(.20

6)(.

197)

(.19

8)(.

305)

(.31

5)

Typ

e6—

Art

s an

d C

ult

ure

�0.

04�

0.03

�0.

14�

0.15

�1.

12�

0.10

�0.

41�

0.42

(.10

4)(.

104)

(.15

6)(.

156)

(.16

2)(.

164)

(.27

8)(.

29)

Typ

e7—

Oth

er0.

180.

19�

0.03

�0.

020.

120.

110.

180.

16(.

134)

(.13

4)(.

194)

(.19

4)(.

169)

(.16

9)(.

277)

(.28

7)

Scop

e1—

Inte

rnat

ion

al0.

26#

0.26

#0.

190.

230.

39*

0.42

**�

0.07

�0.

08(.

136)

(.13

6)(.

179)

(.17

8)(.

157)

(.15

8)(.

181)

(.18

5)

Scop

e2—

Nat

ion

al0.

23#

0.22

#0.

60*

0.68

***

0.32

*0.

36*

�0.

27�

0.28

(.12

2)(.

122)

(.17

6)(.

176)

(.16

)(.

161)

(.16

7)(.

171)

Scop

e3—

Stat

e,

0.14

#0.

14#

0.06

0.09

0.15

0.17

�0.

02�

0.23

Pro

vin

cial

, Reg

ion

al(.

083)

(.08

3)(.

122)

(.12

2)(.

137)

(.13

8)(.

165)

(.17

)

Educational Local

(Con

tinu

ed)

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 447

Reg

ion

—U

nit

ed S

tate

s�

0.11

0.10

�0.

06�

0.05

0.16

0.16

�0.

17�

0.17

1;0

oth

erw

ise

(.07

4)(.

074)

(.16

8)(.

167)

(.12

9)(.

129)

(.11

2)(.

118)

Are

a2—

Pop

ula

tion

0.

23#

0.24

*0.

110.

120.

44*

0.47

*�

0.17

�0.

150.

5-1

mil

lion

(.12

2)(.

123)

(.17

3)(.

174)

(.17

9)(.

184)

(.20

2)(.

21)

Are

a3—

Pop

ula

tion

0.

32*

0.33

*0.

220.

200.

51**

0.55

**�

0.01

�0.

011-

3 m

illi

on(.

13)

(.13

)(.

18)

(.18

1)(.

186)

(.19

)(.

2)(.

211)

Are

a4—

Pop

ula

tion

0.

60**

*0.

62**

*0.

60**

0.58

**0.

87**

*0.

89**

*�

0.12

�0.

113

mil

lion

or

mor

e(.

137)

(.13

8)(.

196)

(.19

7)(.

196)

(.19

7)(.

204)

(.20

5)

FT

E1—

Les

s �

0.83

**�

0.83

**�

1.62

***

�1.

69**

0.27

0.31

�0.

11�

0.14

***

than

hal

f-ti

me

(.31

9)(.

319)

(.45

5)(.

487)

(.39

9)(.

399)

(.02

)(.

206)

FT

E2—

Mor

e �

0.61

***

�0.

62**

*�

0.59

**�

0.56

**�

0.27

�0.

35#

0.02

0.01

than

hal

f-ti

me

(.14

7)(.

147)

(.20

1)(.

202)

(.19

6)(.

201)

(.19

8)(.

205)

Exp

erie

nce

—Y

ears

0.

05**

*0.

05**

*0.

10**

*0.

09**

*0.

05*

0.05

*�

0.04

�0.

04em

ploy

ed a

s fu

ndr

aisi

ng

(.01

5)(.

015)

(.02

3)(.

023)

(.02

4)(.

024)

(.02

8)(.

029)

prof

esss

ion

al

Exp

erie

nce

squ

ared

�1.

12E

-03*

�1.

08E

-03*

�2.

11E

-03*

*�

1.90

E-0

3*�

1.42

E-0

3#�

1.52

E-0

3#6.

54E

-04

6.71

E-0

4(4

.39E

-04)

(4.3

9E-0

4)(.

001)

�(.

001)

(.00

1)(.

001)

(.00

1)(.

001)

Cu

rren

t—N

um

ber

of y

ears

�0.

02�

0.02

�0.

01�

0.01

3.82

E-0

30.

014.

83E

-03

4.42

E-0

3w

ith

cu

rrre

nt

empl

oyer

(.01

1)(.

011)

(.01

6)(.

016)

(.01

5)(.

015)

(.01

5)(.

015)

Con

trac

t0.

010.

02�

0.12

�0.

140.

030.

02�

0.08

�0.

08(.

087)

(.08

7)(.

125)

(.12

6)(.

125)

(.12

7)(.

128)

(.13

1)

Sign

0.46

**0.

43*

0.10

0.09

�0.

10�

0.09

�0.

11�

0.10

(.16

9)(.

171)

(.32

4)(.

322)

(.33

9)(.

34)

(.41

9)(.

427)

Rec

ruit

er0.

120.

110.

090.

110.

110.

120.

170.

17(.

087)

(.87

3)(.

133)

0.13

(.13

4)0.

13(.

124)

0.13

Age

3.98

E-0

31.

54E

-03

�0.

08#

�0.

07#

0.08

0.09

�0.

08#

�0.

08#

(.02

5)(.

025)

(.04

)(.

04)

(.03

5)(.

036)

(.04

5)(.

046)

Age

squ

ared

�1.

04E

-04

�8.

24E

-05

7.79

E-0

4#7.

03E

-04

�7.

51E

-04#

�8.

73E

-04

8.35

E-0

4#8.

49E

-04#

(2.6

9E-0

4)(2

.71E

-04)

(4.4

0E-0

4)(4

.39E

-04)

(3.9

2E-0

4)(3

.99E

-04)

(4.6

5E-0

4)(4

.80E

-04)

Gen

der

�0.

21**

�0.

22**

�0.

17�

0.16

�0.

13�

0.13

�0.

14�

0.13

(.07

9)(.

08)

(.11

7)(.

116)

(.12

)(.

121)

(.11

3)(4

.80E

-04)

Pop. � 50K Full-timeT

able

2. (

Con

tin

ued

)

Posi

tion

of S

urve

y R

espo

nden

tC

hief

Dev

elop

men

t Offi

cer

Dep

uty

Dir

ecto

rSt

aff

Con

sult

ant

Fir

st-s

tage

reg

ress

ion

For

bon

usF

or ls

alar

yF

or b

onus

For

lsal

ary

Bon

usls

alar

yB

onus

lsal

ary

Dep

ende

nt V

aria

ble

lmon

eylm

oney

lmon

eylm

oney

lmon

eylm

oney

lmon

eylm

oney

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 448

Bla

ck0.

340.

32�

0.64

#�

0.65

*0.

490.

500.

230.

26(.

233)

(.24

3)(.

33)

(.32

9)(.

332)

(.33

2)(.

52)

(.53

)

Oth

er0.

42*

0.42

*�

0.09

�0.

11�

0.07

0.01

�0.

80**

�0.

80**

(.19

6)(.

196)

(.25

3)(.

252)

(.26

6)(.

274)

(.29

3)(.

298)

Som

e C

olle

ge�

1.42

E-0

3�

0.01

�0.

08�

0.08

0.38

0.39

0.09

0.08

(.14

8)(.

149)

(.25

3)(.

253)

(.29

8)(.

298)

(.29

3)(.

302)

Bac

cala

ure

ate

Deg

ree

0.08

0.09

�0.

099.

15E

-02

0.04

0.05

0.16

0.15

(.15

)(.

151)

(.24

7)(.

248)

(.28

9)(.

289)

(.26

3)(.

268)

Pos

t se

con

dary

0.13

0.13

0.05

0.07

�0.

07�

0.09

0.02

0.01

(.17

9)(.

179)

(.21

8)(.

218)

(.30

2)(.

302)

(.25

)(.

255)

Cer

tifi

cati

on—

at le

ast

one:

0.15

0.18

0.01

0.01

0.22

0.22

0.13

0.13

CF

RE

, AC

FR

E, F

AH

P, O

ther

(.12

7)(.

127)

(.15

3)(.

154)

(.18

3)(.

184)

(.18

9)(.

192)

Yea

r 2

0.48

*0.

47*

0.12

0.12

***

0.33

*0.

36�

0.21

�0.

21(.

198)

(.19

9)(.

255)

(.25

5)(.

243)

(.24

4)(.

331)

(.34

)

Yea

r 3

0.45

#0.

43#

�0.

11�

0.16

�0.

91*

�0.

83*

0.10

0.11

(.24

3)(.

243)

(.33

1)(.

334)

(.32

1)(.

323)

(.33

9)(.

347)

Yea

r 4

�0.

22�

0.24

�0.

67**

�0.

68**

�0.

91**

*�

0.87

***

0.24

0.25

(.17

1)(.

171)

(.21

6)(.

215)

(.21

5)(.

216)

(.26

7)(.

274)

lbu

dget

0.15

***

0.15

***

0.16

***

0.17

***

0.23

***

0.24

***

0.59

***

0.59

***

(.02

5)(.

025)

(.03

2)(.

323)

(.03

3)(.

033)

(.04

7)(.

048)

staf

f0.

06**

*0.

06**

*0.

05**

*0.

05**

*0.

04**

*0.

04**

*0.

04**

*0.

05**

*(.

004)

(.00

4)(.

004)

(.00

4)(.

003)

(.00

3)(.

005)

(.00

6)

Sam

ple

size

1055

1049

563

558

511

501

197

191

Par

tial

R2

of I

V0.

2740

0.27

480.

2841

0.28

590.

4163

0.42

280.

6796

0.67

36

White High School

Stan

dard

err

ors

in p

aren

thes

es.

Not

e:#

p �

0.1

.*

p �

0.0

5.**

p �

0.0

1.**

* p

� 0

.001

.

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 449

450 ME S C H, RO O N E Y

Nonprofit Management & Leadership DOI: 10.1002/nml

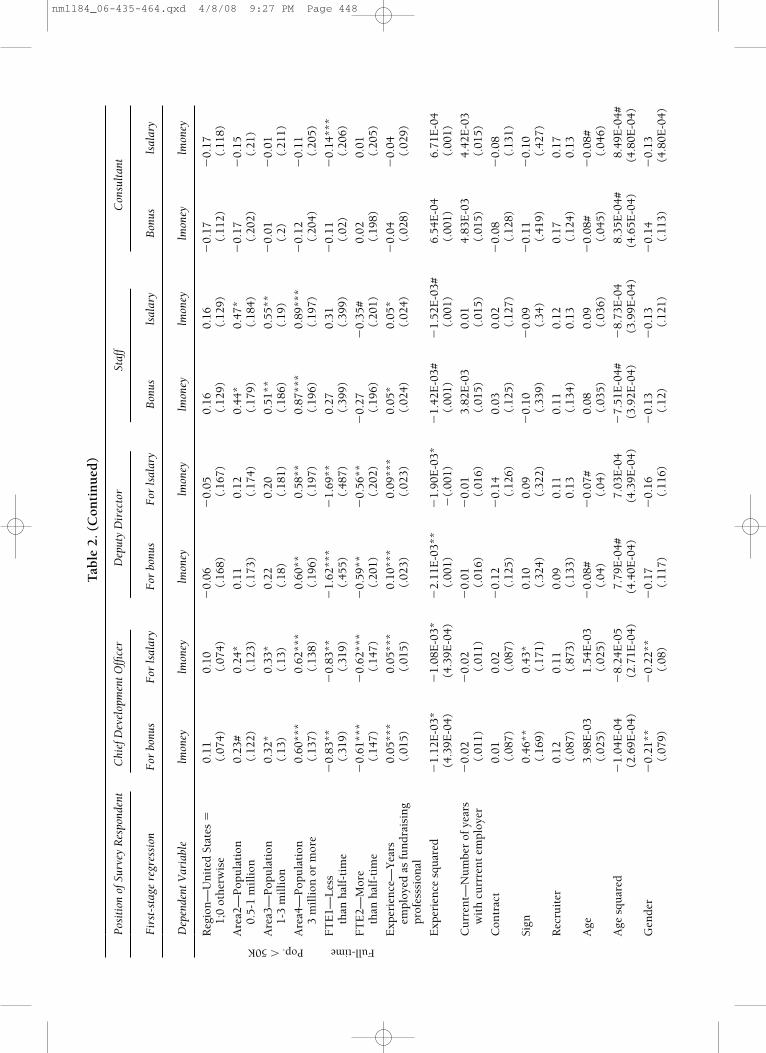

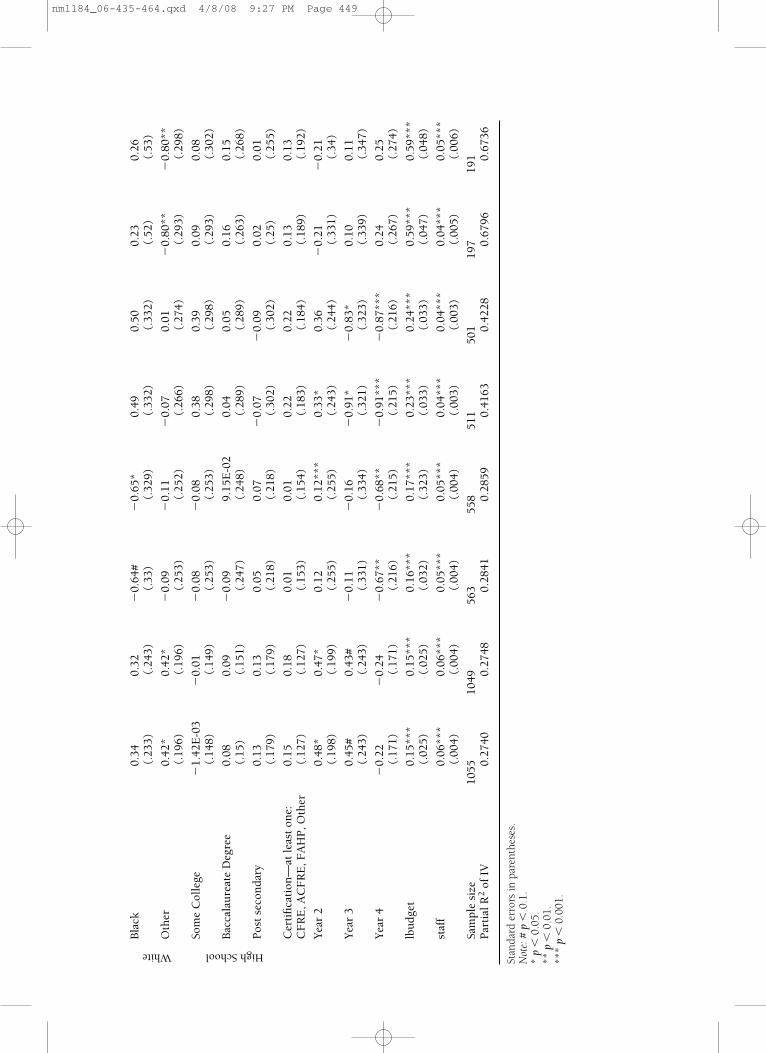

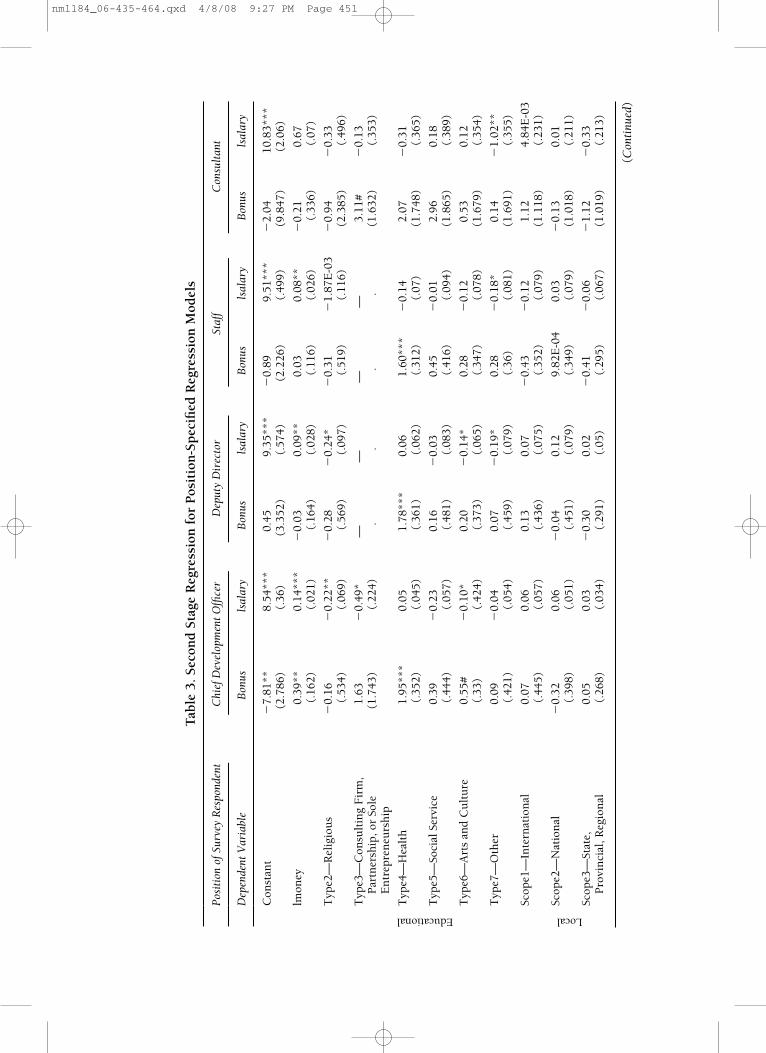

across all types of fundraising positions. Given this and the theoret-ical distinction between their roles in explaining productivity directlybut that they are arguably independent from explaining compensa-tion directly, we determine that they are valid instrumental variables.Therefore, we include them in the second stage of our analysis.

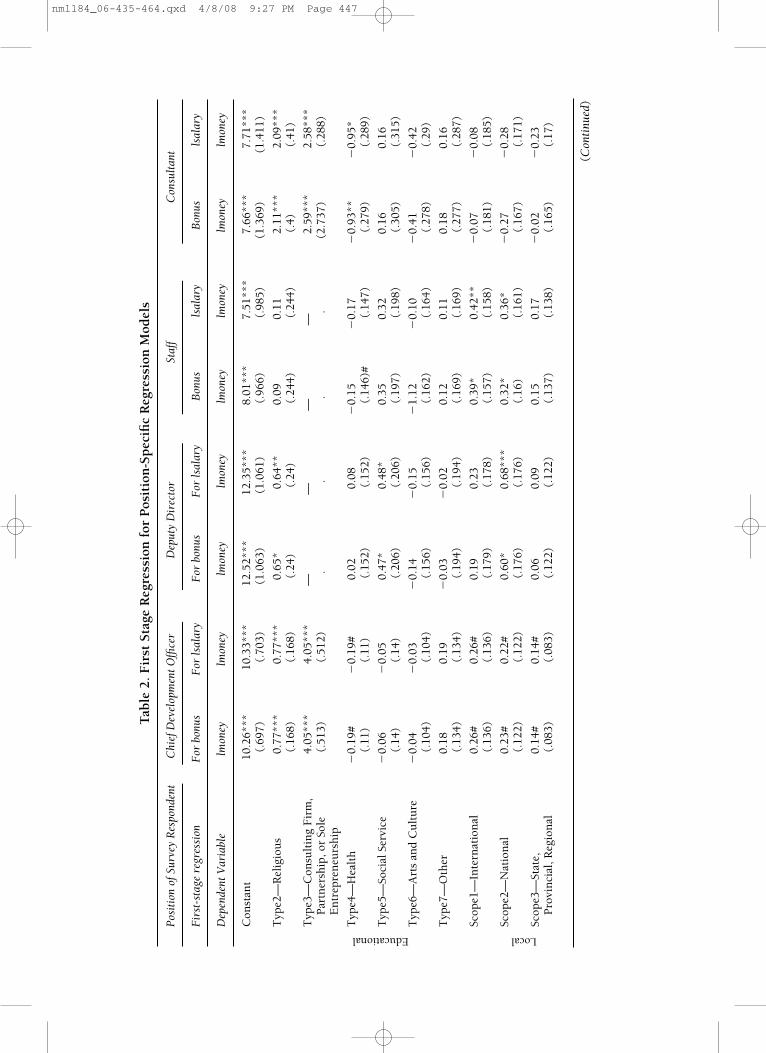

Table 3 presents the results of our 2SLS simultaneous estimates.In this estimate, we find that productivity (LnMoney) has a positiveand significant effect on the salary of each type of fundraising posi-tion. The strongest effect is for chief development officers, for whoma 10 percent increase in money raised is associated with a 1.4 percentincrease in salary. Fundraising productivity (LMoney raised) is notassociated with a significant increase in bonuses—except for CDOs.This may not be too surprising: if any position would have a variablecompensation component, it would be the CDO, who is chieflyresponsible for all aspects of fundraising at the organization. For thedeputy directors, a 10 percent increase in productivity is associatedwith a 0.9 percent increase in salary. Staff experienced a similarchange (0.8 percent); there was not a significant association betweenpay and performance for consultants.

Our results indicate a statistically significant relationshipbetween pay and performance for most fundraising positions. Con-trolling for differences in mission, geographic scope, geographicalpopulation, size of the nonprofit, and so forth, as well as severalhuman capital variables, we find evidence supportive of the notionof pay for performance among fundraisers.

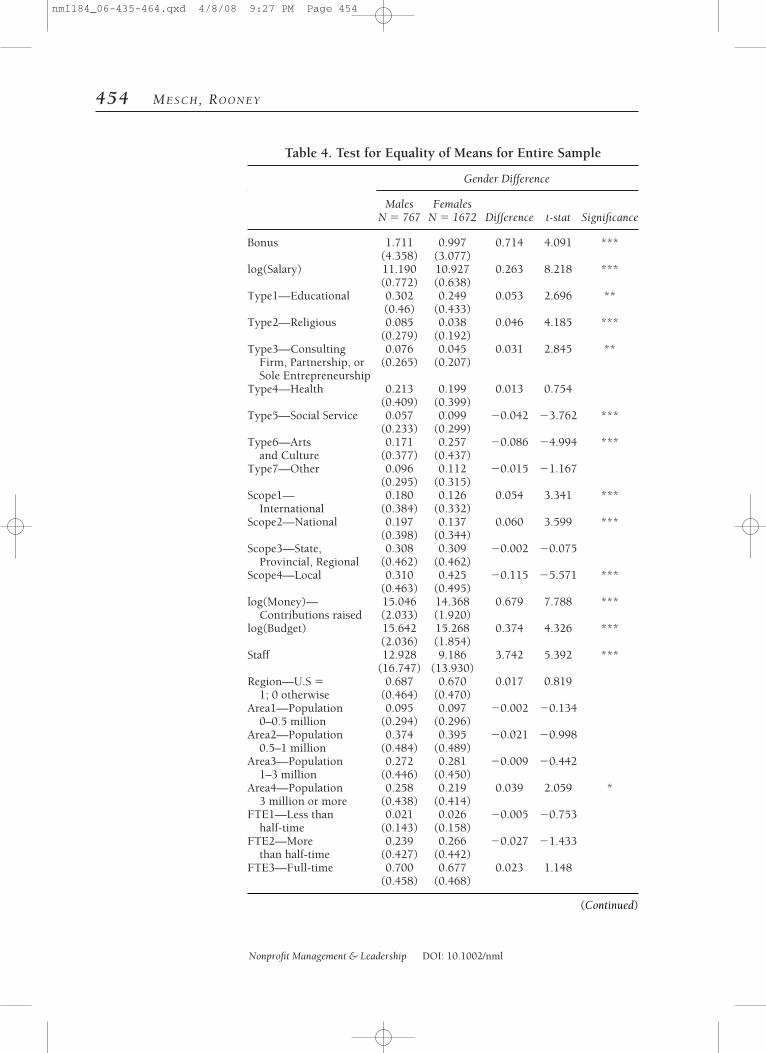

Are There Gender Differences in Compensation?We performed a series of t tests for differences between the meansfor men (n � 767) and women (n � 1,672) fundraisers. Noteworthyresults presented in Table 4 indicate that men have significantlyhigher average salaries and larger shares of income from bonuses.(Men’s bonuses are, on average, over 70 percent higher than those ofwomen.) Men are more likely than women to serve in educational,religious, and consulting organizations, whereas women are morelikely to serve in social services and arts and cultural nonprofits. Geo-graphically men are more likely to work in international and nationalnonprofits, and women are more likely to work in local nonprofits.Men raised significantly more money and worked for organizationswith larger development staffs and budgets. Men also had signifi-cantly more overall experience as fundraisers (four more years) buthad similar tenures with the current employer. Men were slightlyolder (3.6 years) and were almost twice as likely as females to havebeen hired through a recruiter. Men were more likely to have signif-icantly more education than women. Hence, if it were not possibleto refine our analysis further, we might conclude that men are paidmore than women, but they perhaps had earned higher compensa-tion because, on average, they raise more money, work in larger, morecomplex organizations, and have more education than women.

Fundraisingproductivity isnot associated

with a significantincrease in

bonuses—exceptfor chief

developmentofficers.

We find evidencesupportive of thenotion of pay for

performanceamong

fundraisers.

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 450

Tab

le 3

. Sec

ond

Sta

ge R

egre

ssio

n f

or P

osit

ion

-Sp

ecifi

ed R

egre

ssio

n M

odel

s

Posi

tion

of S

urve

y R

espo

nden

tC

hief

Dev

elop

men

t Offi

cer

Dep

uty

Dir

ecto

rSt

aff

Con

sult

ant

Dep

ende

nt V

aria

ble

Bon

usls

alar

yB

onus

lsal

ary

Bon

usls

alar

yB

onus

lsal

ary

Con

stan

t�

7.81

**8.

54**

*0.

459.

35**

*�

0.89

9.51

***

�2.

0410

.83*

**(2

.786

)(.

36)

(3.3

52)

(.57

4)(2

.226

)(.

499)

(9.8

47)

(2.0

6)

lmon

ey0.

39**

0.14

***

�0.

030.

09**

0.03

0.08

**�

0.21

0.67

(.16

2)(.

021)

(.16

4)(.

028)

(.11

6)(.

026)

(.33

6)(.

07)

Typ

e2—

Rel

igio

us

�0.

16�

0.22

**�

0.28

�0.

24*

�0.

31�

1.87

E-0

3�

0.94

�0.

33(.

534)

(.06

9)(.

569)

(.09

7)(.

519)

(.11

6)(2

.385

)(.

496)

Typ

e3—

Con

sult

ing

Fir

m,

1.63

�0.

49*

——

——

3.11

#�

0.13

Par

tner

ship

, or

Sole

(1

.743

)(.

224)

..

..

(1.6

32)

(.35

3)E

ntr

epre

neu

rsh

ip

Typ

e4—

Hea

lth

1.95

***

0.05

1.78

***

0.06

1.60

***

�0.

142.

07�

0.31

(.35

2)(.

045)

(.36

1)(.

062)

(.31

2)(.

07)

(1.7

48)

(.36

5)

Typ

e5—

Soci

al S

ervi

ce0.

39�

0.23

0.16

�0.

030.

45�

0.01

2.96

0.18

(.44

4)(.

057)

(.48

1)(.

083)

(.41

6)(.

094)

(1.8

65)

(.38

9)

Typ

e6—

Art

s an

d C

ult

ure

0.55

#�

0.10

*0.

20�

0.14

*0.

28�

0.12

0.53

0.12

(.33

)(.

424)

(.37

3)(.

065)

(.34

7)(.

078)

(1.6

79)

(.35

4)

Typ

e7—

Oth

er0.

09�

0.04

0.07

�0.

19*

0.28

�0.

18*

0.14

�1.

02**

(.42

1)(.

054)

(.45

9)(.

079)

(.36

)(.

081)

(1.6

91)

(.35

5)

Scop

e1—

Inte

rnat

ion

al0.

070.

060.

130.

07�

0.43

�0.

121.

124.

84E

-03

(.44

5)(.

057)

(.43

6)(.

075)

(.35

2)(.

079)

(1.1

18)

(.23

1)

Scop

e2—

Nat

ion

al�

0.32

0.06

�0.

040.

129.

82E

-04

0.03

�0.

130.

01(.

398)

(.05

1)(.

451)

(.07

9)(.

349)

(.07

9)(1

.018

)(.

211)

Scop

e3—

Stat

e,

0.05

0.03

�0.

300.

02�

0.41

�0.

06�

1.12

�0.

33P

rovi

nci

al, R

egio

nal

(.26

8)(.

034)

(.29

1)(.

05)

(.29

5)(.

067)

(1.0

19)

(.21

3)

Educational Local

(Con

tinu

ed)

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 451

Reg

ion

—U

nit

er S

tate

s �

�0.

46�

0.04

0.21

�0.

01�

0.16

0.02

0.51

�0.

231;

0 ot

her

wis

e(.

236)

(.03

)(.

397)

(.06

8)(.

274)

(.06

1)(.

703)

(.14

9)

Are

a2—

Pop

ula

tion

0.5

–1 m

illi

on0.

03�

0.04

0.76

#0.

010.

320.

001.

24�

0.14

(.39

2)(.

504)

(.41

5)(.

072)

(.39

1)(.

09)

(1.2

31)

(.25

9)

Are

a3—

Pop

ula

tion

1–3

mil

lion

0.10

0.02

1.04

*0.

04�

0.27

�0.

031.

06�

0.23

(.42

)(.

054)

(.41

5)(.

075)

(.40

8)(.

094)

(1.2

12)

(.25

7)

Are

a4—

Pop

ula

tion

0.

07(0

.08)

1.07

*0.

090.

310.

120.

430.

133

mil

lion

or

mor

e(.

454)

(.09

)(.

492)

(.08

5)(.

445)

(.10

2)(1

.246

)(.

262)

FT

E1—

Les

s th

an h

alf-

tim

e�

0.03

�0.

34**

0.23

�0.

30�

0.95

�0.

81**

*�

1.48

�1.

71**

*(1

.024

)(.

131)

(1.1

26)

(.20

7)(.

849)

(.19

)(1

.201

)(.

258)

FT

E2—

Mor

e th

an h

alf-

tim

e0.

31�

0.14

*0.

45�

0.10

1.01

*�

0.14

�1.

60�

0.25

(.48

1)(.

062)

(.49

2)(0

.08)

(.42

2)(.

097)

(1.2

23)

(.25

5)

Exp

erie

nce

—Y

ears

em

ploy

ed�

0.09

#0.

01�

0.01

0.02

1.65

E-0

30.

02*

0.22

0.05

as f

un

drai

sin

g pr

ofes

ssio

nal

(.00

2)(.

006)

(.06

)(.

01)

(.05

2)(.

012)

(.16

9)(.

035)

Exp

erie

nce

squ

ared

2.31

E-0

3#9.

71E

-05

2.20

E-0

30.

00�

6.32

E-0

4�

5.40

E-0

4�

6.18

E-0

3�

1.02

E-0

3(.

001)

(1.8

0E-0

4)(.

002)

(3.0

8E-0

4)(.

002)

(3.9

4E-0

4)(.

004)

(.00

1)

Cu

rren

t—N

um

ber

of y

ears

�0.

012.

84E

-03

0.04

�4.

35E

-03

0.04

�0.

01�

5.00

E-0

33.

30E

-03

wit

h c

urr

ren

t em

ploy

er(.

034)

(.00

4)(.

12)

(.00

6)(.

033)

(.00

7)(.

007)

(.01

9)

Con

trac

t0.

130.

03�

0.06

0.05

�0.

25�

1.75

E-0

3�

0.01

�0.

10(.

275)

(.03

5)(.

3)(.

052)

(.05

6)(.

061)

(.09

2)(.

166)

Sign

3.26

***

0.15

*0.

730.

22#

�0.

220.

01�

0.26

***

0.29

(.54

9)(.

071)

(.77

1)(.

132)

(.72

5)(.

162)

(.79

7)(.

535)

Rec

ruit

er0.

69*

0.12

**0.

480.

12*

�0.

390.

23**

*�

0.61

0.07

(.27

7)(.

036)

(.31

8)0.

05(.

287)

(.06

5)(.

759)

(.15

7)

Pop. �50K Full-Time

Tab

le 3

. (C

onti

nu

ed)

Posi

tion

of S

urve

y R

espo

nden

tC

hief

Dev

elop

men

t Offi

cer

Dep

uty

Dir

ecto

rSt

aff

Con

sult

ant

Dep

ende

nt V

aria

ble

Bon

usls

alar

yB

onus

lsal

ary

Bon

usls

alar

yB

onus

lsal

ary

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 452

Age

0.22

**0.

02#

�0.

080.

010.

06�

0.01

0.18

�0.

01(.

079)

(.01

)(.

097)

(.01

7)(.

076)

(.01

7)(.

286)

(.05

9)

Age

squ

ared

�2.

24E

-03*

*�

2.17

E-0

4*1.

03E

-03

�1.

01E

-04

�6.

52E

-04

1.57

E-0

4�

2.04

E-0

34.

08E

-05

(.00

1)(1

.10E

-04)

(.00

1)(1

.81E

-04)

(.00

1)(1

.93E

-04)

(.00

3)(.

001)

Gen

der

�0.

19�

0.11

**�

0.06

�0.

08#

�0.

86**

0.03

�1.

67*

�0.

36*

(.25

7)(.

331)

(.27

9)(.

048)

(.26

)(.

058)

(.70

7)(.

147)

Bla

ck0.

42�

0.04

0.29

�0.

050.

48�

0.08

�0.

851.

24#

(.74

3)(.

099)

(.78

9)(.

135)

(.71

)(.

158)

(3.2

31)

(.66

6)

Oth

er�

0.70

0.05

�0.

61�

0.04

�0.

07�

0.04

1.39

0.28

(.62

3)(.

08)

(.60

2)(.

103)

(.56

9)(.

131)

(1.8

69)

(.38

5)

Som

e C

olle

ge0.

250.

020.

820.

11�

0.48

0.21

�0.

030.

08(.

471)

(.06

1)(.

603)

(.10

3)(.

641)

(.14

3)(1

.825

)(.

377)

Bac

cala

ure

ate

Deg

ree

0.14

0.07

�0.

26�

0.05

�0.

710.

27#

�0.

07�

0.40

(.47

6)(.

061)

(.58

8)(.

101)

(.61

9)(.

138)

(1.6

34)

(.33

7)

Pos

t se

con

dary

0.40

0.19

**0.

40�

0.13

0.38

0.23

0.94

�0.

37(.

567)

(.07

3)(.

519)

(.08

9)(.

643)

(.14

4)(1

.551

)(.

32)

Cer

tifi

cati

on-a

t le

ast

one:

0.84

#0.

030.

430.

030.

03�

0.08

0.58

�0.

20C

FR

E, A

CF

RE

, FA

HP

, Oth

er(.

404)

(.05

2)(.

363)

(.06

3)(.

393)

(.08

8)(1

.163

)(.

239)

Yea

r 2

�1.

61*

�0.

05�

0.41

�0.

42**

*0.

98#

�0.

20#

0.37

0.30

(.62

8)(.

081)

(.60

7)(.

104)

(.52

4)(.

118)

(2.0

44)

(.42

4)

Yea

r 3

�2.

90**

*0.

18#

�0.

58�

0.07

0.06

0.24

0.78

0.19

(.77

4)(.

099)

(.78

5)(.

136)

(.69

1)(.

155)

(2.1

07)

(.43

6)

Yea

r 4

�2.

68**

*�

0.06

�0.

15�

0.09

0.08

0.11

*�

0.79

0.18

(.53

5)(.

069)

(.50

3)(.

086)

(.47

1)(.

105)

(1.6

59)

(.34

4)

Sam

ple

Size

1055

1049

563

558

511

501

197

191

White High School

Stan

dard

err

ors

in p

aren

thes

es.

Not

e: #

p�

0.1.

* p

�0.

05.

** p

�0.

01.

***

p�

0.00

1

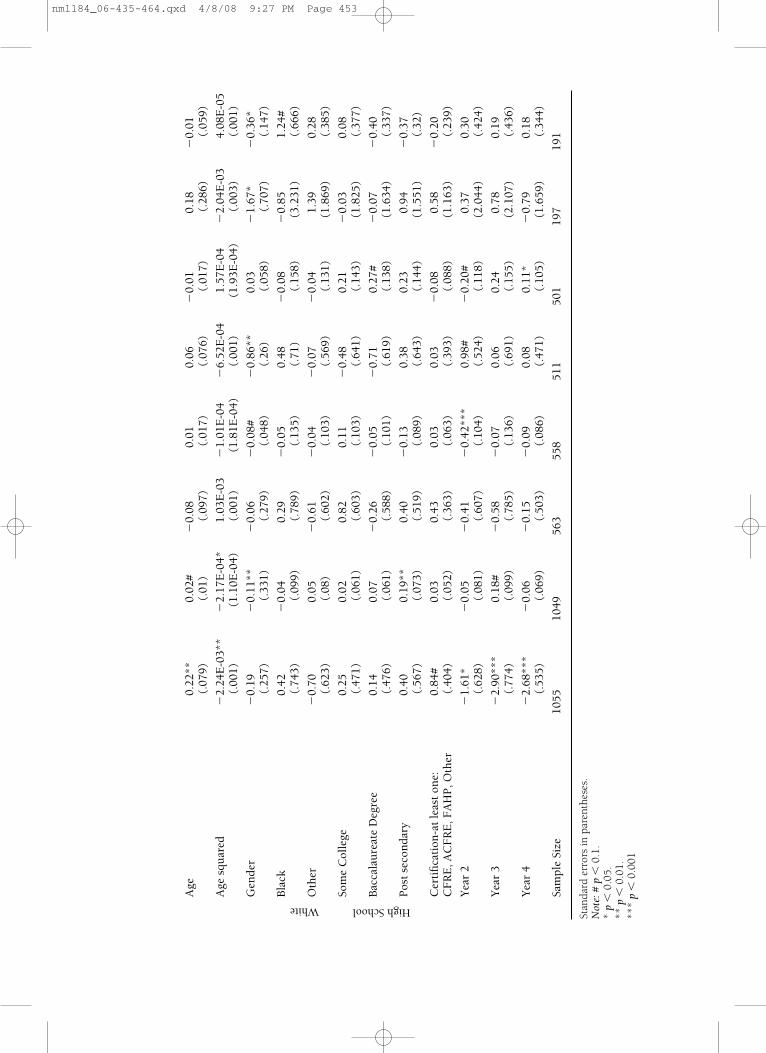

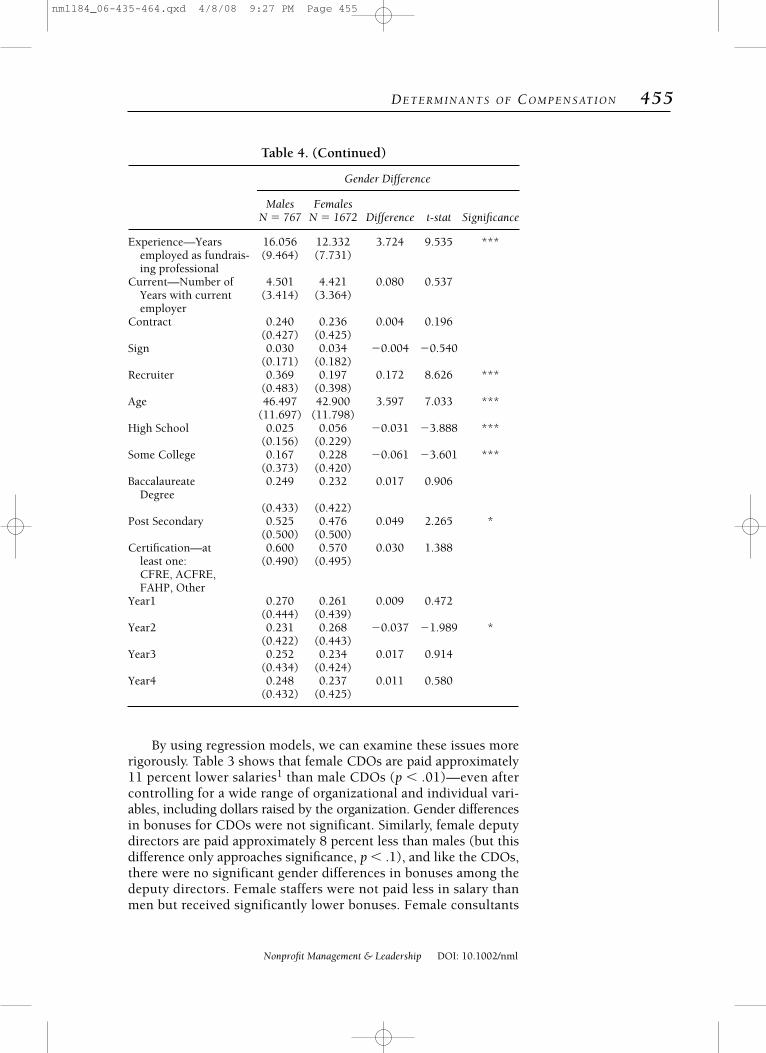

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 453

454 ME S C H, RO O N E Y

Nonprofit Management & Leadership DOI: 10.1002/nml

Table 4. Test for Equality of Means for Entire Sample

Gender Difference

Males FemalesN � 767 N � 1672 Difference t-stat Significance

Bonus 1.711 0.997 0.714 4.091 ***(4.358) (3.077)

log(Salary) 11.190 10.927 0.263 8.218 ***(0.772) (0.638)

Type1—Educational 0.302 0.249 0.053 2.696 **(0.46) (0.433)

Type2—Religious 0.085 0.038 0.046 4.185 ***(0.279) (0.192)

Type3—Consulting 0.076 0.045 0.031 2.845 **Firm, Partnership, or (0.265) (0.207)Sole Entrepreneurship

Type4—Health 0.213 0.199 0.013 0.754(0.409) (0.399)

Type5—Social Service 0.057 0.099 �0.042 �3.762 ***(0.233) (0.299)

Type6—Arts 0.171 0.257 �0.086 �4.994 ***and Culture (0.377) (0.437)

Type7—Other 0.096 0.112 �0.015 �1.167(0.295) (0.315)

Scope1— 0.180 0.126 0.054 3.341 ***International (0.384) (0.332)

Scope2—National 0.197 0.137 0.060 3.599 ***(0.398) (0.344)

Scope3—State, 0.308 0.309 �0.002 �0.075Provincial, Regional (0.462) (0.462)

Scope4—Local 0.310 0.425 �0.115 �5.571 ***(0.463) (0.495)

log(Money)— 15.046 14.368 0.679 7.788 ***Contributions raised (2.033) (1.920)

log(Budget) 15.642 15.268 0.374 4.326 ***(2.036) (1.854)

Staff 12.928 9.186 3.742 5.392 ***(16.747) (13.930)

Region—U.S � 0.687 0.670 0.017 0.8191; 0 otherwise (0.464) (0.470)

Area1—Population 0.095 0.097 �0.002 �0.1340–0.5 million (0.294) (0.296)

Area2—Population 0.374 0.395 �0.021 �0.9980.5–1 million (0.484) (0.489)

Area3—Population 0.272 0.281 �0.009 �0.4421–3 million (0.446) (0.450)

Area4—Population 0.258 0.219 0.039 2.059 *3 million or more (0.438) (0.414)

FTE1—Less than 0.021 0.026 �0.005 �0.753half-time (0.143) (0.158)

FTE2—More 0.239 0.266 �0.027 �1.433than half-time (0.427) (0.442)

FTE3—Full-time 0.700 0.677 0.023 1.148(0.458) (0.468)

(Continued)

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 454

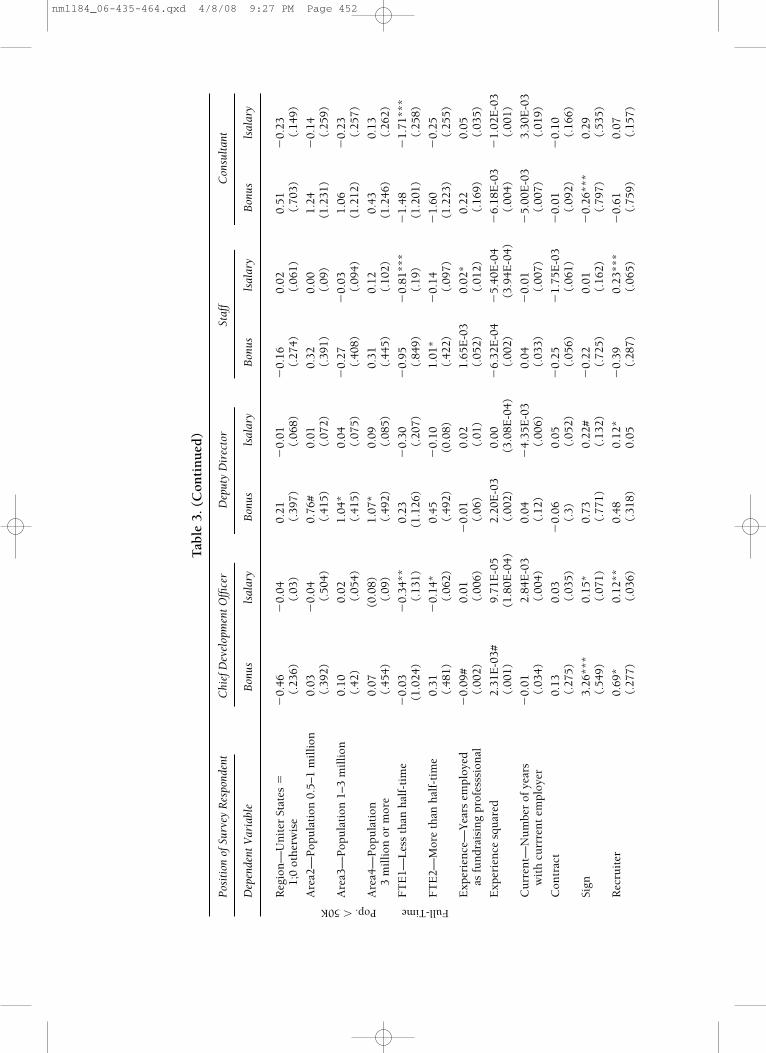

By using regression models, we can examine these issues morerigorously. Table 3 shows that female CDOs are paid approximately11 percent lower salaries1 than male CDOs (p � .01)—even aftercontrolling for a wide range of organizational and individual vari-ables, including dollars raised by the organization. Gender differencesin bonuses for CDOs were not significant. Similarly, female deputydirectors are paid approximately 8 percent less than males (but thisdifference only approaches significance, p � .1), and like the CDOs,there were no significant gender differences in bonuses among thedeputy directors. Female staffers were not paid less in salary thanmen but received significantly lower bonuses. Female consultants

DE T E R M I N A N T S O F CO M P E N S AT I O N 455

Nonprofit Management & Leadership DOI: 10.1002/nml

Experience—Years 16.056 12.332 3.724 9.535 ***employed as fundrais- (9.464) (7.731)ing professional

Current—Number of 4.501 4.421 0.080 0.537Years with current (3.414) (3.364)employer

Contract 0.240 0.236 0.004 0.196(0.427) (0.425)

Sign 0.030 0.034 �0.004 �0.540(0.171) (0.182)

Recruiter 0.369 0.197 0.172 8.626 ***(0.483) (0.398)

Age 46.497 42.900 3.597 7.033 ***(11.697) (11.798)

High School 0.025 0.056 �0.031 �3.888 ***(0.156) (0.229)

Some College 0.167 0.228 �0.061 �3.601 ***(0.373) (0.420)

Baccalaureate 0.249 0.232 0.017 0.906Degree

(0.433) (0.422)Post Secondary 0.525 0.476 0.049 2.265 *

(0.500) (0.500)Certification—at 0.600 0.570 0.030 1.388

least one: (0.490) (0.495)CFRE, ACFRE, FAHP, Other

Year1 0.270 0.261 0.009 0.472(0.444) (0.439)

Year2 0.231 0.268 �0.037 �1.989 *(0.422) (0.443)

Year3 0.252 0.234 0.017 0.914(0.434) (0.424)

Year4 0.248 0.237 0.011 0.580(0.432) (0.425)

Table 4. (Continued)

Gender Difference

Males FemalesN � 767 N � 1672 Difference t-stat Significance

nml184_06-435-464.qxd 4/8/08 9:27 PM Page 455

received approximately 36 percent lower salaries than male consul-tants and were given significantly lower bonuses as well.

Other Determinants of Bonus and SalaryThe following is a description of other factors that affect bonus andsalary for fundraising professionals. To simplify our presentation, wediscus only those in our final estimation of the 2SLS process in Table 3and the results that are statistically significant.

Mission of the Nonprofit. We used education as the referencegroup for this set of variables. We found that CDOs in religious non-profits earn approximately 22 percent lower salaries compared toeducation, and deputy directors earn approximately 24 percent less.Health care fundraisers earn approximately the same salaries as theirpeers in education, but health care fundraisers earn significantlyhigher bonuses than their counterparts in education. CDOs in artsand culture nonprofits earn approximately 10 percent less and deputydirectors earn approximately 14 percent less than their educationalcounterparts. Deputy directors, staff, and consultants in other sub-sectors earn substantially less than those in education. CDOs in con-sulting firms earn less than their educational peers, but there are notenough consultants in the deputy directors and staff categories to iso-late an independent effect. Perhaps most surprising is that fundrais-ers in social services do not earn significantly different salaries orbonuses than their counterparts in education.

Population of Base City. After controlling for all other factors, wefound no significant differences in the base salaries of fundraisers inany city size. However, deputy directors in various city sizes werepaid significantly higher bonuses than those living in the smallesttowns (population less than fifty thousand).