-

8/2/2019 Determinant of Interest Rates

1/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-1McGraw-Hill/Irwin

Chapter TwoDeterminants of

Interest Rates

-

8/2/2019 Determinant of Interest Rates

2/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-2McGraw-Hill/Irwin

Interest Rate Fundamentals

Nominal interest rates - the interest

rate actually observed in financial

markets

directly affect the value (price) of most

securities traded in the market

affect the relationship between spot and

forward FX rates

-

8/2/2019 Determinant of Interest Rates

3/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-3McGraw-Hill/Irwin

Time Value of Money and Interest Rates

Assumes the basic notion that a dollar

received today is worth more than a dollar

received at some future date

Compound interest

interest earned on an investment is reinvested

Simple interestinterest earned on an investment is not

reinvested

-

8/2/2019 Determinant of Interest Rates

4/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-4McGraw-Hill/Irwin

Calculation of Simple Interest

Value = Principal + Interest (year 1) + Interest (year 2)

Example:$1,000 to invest for a period of two years at 12

percent

Value = $1,000 + $1,000(.12) + $1,000(.12)

= $1,000 + $1,000(.12)(2)

= $1,240

-

8/2/2019 Determinant of Interest Rates

5/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-5McGraw-Hill/Irwin

Value of Compound Interest

Value = Principal + Interest + Compounded interest0 1 2

Invest Receive interest Receive interest=

$ 1,000 $ 1,000 x .12= $120 $ 1,000 x .12= $120+ $120 x .12=

14.4

= $134.40

Value of investment= Value of investment=$1,000+$120 $1000+

$120

+$134.4= $1,254.40

-

8/2/2019 Determinant of Interest Rates

6/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-6McGraw-Hill/Irwin

Present Value of a Lump Sum

PV function converts cash flows receivedover a future investment

horizon into an

equivalent (present) value by discounting

future cash flows back to present usingcurrent market interest

rate

lump sum payment~ single cash payment received

at the beginning or end of some investment horizon.

Annuity~ a series of equal cash flows received at

fixed intervals over the entire investment horizon.

-

8/2/2019 Determinant of Interest Rates

7/342007, The McGraw-Hill Companies, All Rights Reserved

Present Value of a Lump Sum

TODAY Yr. 6

? $10,000HOW MUCH ARE YOU GOING TO INVEST TODAY

(YEAR 0) TO BE ABLE TO GET $10,000 AT YEAR 6?

PVs decrease as interest rates increaseAs interest rates

increase, fewer funds need to be invested at

the beginning of an investment horizon to receive a stated

amount at the end of the investment horizon.

2-7McGraw-Hill/Irwin

-

8/2/2019 Determinant of Interest Rates

8/342007, The McGraw-Hill Companies, All Rights

Reserved2-8McGraw-Hill/Irwin

Calculating Present Value (PV) of a Lump

Sum

PV = FVn(1/(1 + i/m))nm = FVn(PVIFi/m,nm)

where:

PV = present valueFV = future value (lump sum) received in n

years

i = simple annual interest rate earned

n = number of years in investment horizon

m = number of compounding periods in a yeari/m = periodic rate

earned on investments

nm = total number of compounding periods

PVIF = present value interest factor of a lump sum

-

8/2/2019 Determinant of Interest Rates

9/342007, The McGraw-Hill Companies, All Rights

Reserved2-9McGraw-Hill/Irwin

Calculating Present Value of a Lump Sum

You are offered a security investment that pays$10,000 at the

end of 6 years in exchange for a fixedpayment today.

PV = FVn(1/(1 + i/m))nm

at 8% interest - = $10,000(0.630170) = $6,301.70

at 12% interest - = $10,000(0.506631) = $5,066.31

at 16% interest - = $10,000(0.410442) = $4,104.42

-

8/2/2019 Determinant of Interest Rates

10/342007, The McGraw-Hill Companies, All Rights Reserved

Present Value (PV) of an Annuity

TODAY 1 2 3 4

? $10,000 $10,000 $10,000 $10,000

HOW MUCH WILL YOU INVEST TODAY TO BE

ABLE TO RECEIVE $10,000 AT END/AT THE

BEGINNING OF EVERY YEAR?PV ANNUITY

LAST DAY OF EVERY YEAR

FIRST DAY OF EVERY YEAR

2-10McGraw-Hill/Irwin

-

8/2/2019 Determinant of Interest Rates

11/342007, The McGraw-Hill Companies, All Rights

Reserved2-11McGraw-Hill/Irwin

Calculation of Present Value (PV) of an

Annuity

nm

PV = PMT (1/(1 + i/m))t = PMT(PVIFAi/m,nm)t = 1

where:PV = present value

PMT = periodic annuity payment received

during investment horizon

i/m = periodic rate earned on investmentsnm = total number of

compounding periods

PVIFA = present value interest factor of an annuity

-

8/2/2019 Determinant of Interest Rates

12/342007, The McGraw-Hill Companies, All Rights Reserved

Calculation of Present Value (PV) of an

Annuity (LAST DAY)

2-12McGraw-Hill/Irwin

PV= PMT(PVIFAi/m,nm)

-

8/2/2019 Determinant of Interest Rates

13/34

-

8/2/2019 Determinant of Interest Rates

14/342007, The McGraw-Hill Companies, All Rights Reserved

Calculation of Present Value of an Annuity

(FIRST DAY)

If the investment pays on the FIRST day of

every quarter for the next six years (2%,

24)PV = PMT(PVIFAi/m,nm)(1 + i/m)

at 8% interest - = $10,000(18.913926)(1.02)

=$10,000(19.29220452)= $192,922.04

2-14McGraw-Hill/Irwin

-

8/2/2019 Determinant of Interest Rates

15/342007, The McGraw-Hill Companies, All Rights

Reserved2-15McGraw-Hill/Irwin

Future Values

Translate cash flows received during

an investment period to a terminal

(future) value at the end of aninvestment horizon

HOW MUCH WILL YOUR

INVESTMENT TODAY/ EVERY YEARBE WORTH IN THE FUTURE?

-

8/2/2019 Determinant of Interest Rates

16/342007, The McGraw-Hill Companies, All Rights Reserved

Future Values

FV increases with both the time horizon and

the interest rate

As interest rates increase, a stated amount of fundsinvested at

the beginning of an investment horizon

accumulates to a larger amount at the end of the

investment horizon.

LUMP SUM ANNUITY

LAST DAY

FIRST DAY 2-16McGraw-Hill/Irwin

-

8/2/2019 Determinant of Interest Rates

17/342007, The McGraw-Hill Companies, All Rights

Reserved2-17McGraw-Hill/Irwin

Future Value of a Lump Sum

TODAY Year 6

$10,000 ?

HOW MUCH WILL YOUR $10,000

INVESTMENT TODAY BE WORTH AT THE

END OF THE 6TH YEAR?

FVn = PV(1 + i/m)nm = PV(FVIF i/m, nm)

-

8/2/2019 Determinant of Interest Rates

18/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-18McGraw-Hill/Irwin

Calculation of Future Value of a Lump Sum

You invest $10,000 today in exchange for a fixed

payment at the end of six years

FVn = PV(1 + i/m)nm = PV(FVIF i/m, nm)

at 8% interest = $10,000(1.586874) = $15,868.74

at 12% interest = $10,000(1.973823) = $19,738.23

at 16% interest = $10,000(2.436396) = $24,363.96

at 16% interest compounded semiannually (8%,12)

= $10,000(2.518170) = $25,181.70

-

8/2/2019 Determinant of Interest Rates

19/34

2007, The McGraw-Hill Companies, All Rights Reserved

Future Value of an Annuity (LAST&FIRST

DAY)

TODAY 1 2 3 4

$10,000 $10,000 $10,000 $10,000 ?

HOW MUCH WILL YOUR YEARLY CASH

INVESTMENT BE WORTH AT THE END OF THE

FOURTH YEAR?(nm-1)

FVn = PMT (1 + i/m)t = PMT(FVIFAi/m, mn) (t = 0)

2-19McGraw-Hill/Irwin

-

8/2/2019 Determinant of Interest Rates

20/34

2007, The McGraw-Hill Companies, All Rights Reserved

Future Value of an Annuity (LAST DAY)

2-20McGraw-Hill/Irwin

FVn = PMT (1 + i/m)t = PMT(FVIFAi/m, mn)

-

8/2/2019 Determinant of Interest Rates

21/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-21McGraw-Hill/Irwin

Calculation of the Future Value of an Annuity

You invest $10,000 on the last day of every year

for the next six years,

at 8% interest = $10,000(7.335929) = $73,359.29

If the investment pays you $10,000 on the last dayof every

quarter for the next six years,

FV = $10,000(30.421862) = $304,218.62

If the annuity is paid on the first day of eachquarter,

FV=PMT(FVIFAi/m, mn)(1+ i/m)

FV = $10,000(30.421862)(1.02)= $10,000(31.030300) =

$310,303.00

-

8/2/2019 Determinant of Interest Rates

22/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-22McGraw-Hill/Irwin

Relation between Interest Rates and

Present and Future Values

Present

Value

(PV)

Interest Rate

Future

Value

(FV)

Interest Rate

As interest rates increase, fewer funds need

to be invested at the beginning of an

investment horizon to receive a stated

amount at the end of the investment horizon.

As interest rates increase, a stated amount of fundsinvested at

the beginning of an investment horizon

accumulates to a larger amount at the end of the

investment horizon.

-

8/2/2019 Determinant of Interest Rates

23/34

-

8/2/2019 Determinant of Interest Rates

24/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-24McGraw-Hill/Irwin

Loanable Funds Theory

A theory of interest rate

determination that views equilibriuminterest rates in financial

markets as aresult of the supply and demand forloanable funds

-

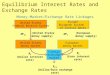

8/2/2019 Determinant of Interest Rates

25/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-25McGraw-Hill/Irwin

Supply of Loanable Funds

Interest

Rate

Quantity of Loanable Funds

Supplied and Demanded

Demand Supply

-

8/2/2019 Determinant of Interest Rates

26/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-26McGraw-Hill/Irwin

Funds Supplied and Demanded by Various

Groups (in billions of dollars)

Funds Supplied Funds Demanded Net

Households $34,860.7 $15,197.4 $19,663.3

Business - nonfinancial 12,679.2 30,779.2 -12,100.0

Business - financial 31,547.9 45061.3 -13,513.4

Government units 12,574.5 6,695.2 5,879.3

Foreign participants 8,426.7 2,355.9 6,070.8

-

8/2/2019 Determinant of Interest Rates

27/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-27McGraw-Hill/Irwin

Determination of Equilibrium Interest

Rates

Interest

Rate

Quantity of Loanable Funds

Supplied and Demanded

D S

IH

i

IL

E

Q

-

8/2/2019 Determinant of Interest Rates

28/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-28McGraw-Hill/Irwin

Effect on Interest rates from a Shift in the

Demand Curve for or Supply curve of

Loanable Funds

Increased supply of loanable funds

Quantity of

Funds Supplied

Interest

Rate DDSS

SS*

E

E*

Q*

i*

Q**

i**

Increased demand for loanable funds

Quantity of

Funds Demanded

DDDD* SS

EE*

i*

i**

Q* Q**

More funds are supplied as interest rates increase

(the reward for supplying funds is higher).

The quantity of loanable funds demanded is

higher as interest falls (the cost of borrowing

funds is lower).

-

8/2/2019 Determinant of Interest Rates

29/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-29McGraw-Hill/Irwin

Factors Affecting Nominal Interest

Rates

Inflation-the continual increase in price level

Real Interest Rate- interest rate that would exist on a

default

free security if no inflation were expected.

Default Risk-risk that security issuer will default

Liquidity Risk- risk that a security can be sold at a

predictable price with low transaction costs on short notice

Special Provisions-additional terms written in the contract.

Term to Maturity-the change in required interest rates as

the

maturity of a security changes.

-

8/2/2019 Determinant of Interest Rates

30/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-30McGraw-Hill/Irwin

Inflation and Interest Rates: The

Fisher Effect

The interest rate should compensate an investor

for both (1) expected inflation and (2) the

opportunity cost of foregone consumption(the real rate

component)

HIGH RISK, HIGH RETURNS

i = RIR + Expected(IP)

or RIR = iExpected(IP)

Example: 3.49% - 1.60% = 1.89%

-

8/2/2019 Determinant of Interest Rates

31/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-31McGraw-Hill/Irwin

Default Risk and Interest Rates

The risk that a securitys issuer will default

on that security by being late on or missing

an interest or principal payment

DRPj = ijt - iTt

Ijt= non-Treasury issueriTt= Treasury issuer

-

8/2/2019 Determinant of Interest Rates

32/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-32McGraw-Hill/Irwin

Term Structure of Interest Rates

Unbiased Expectations Theory- at a given point in time the

yield curve reflects the markets current expectations of

future

short-term rates.

e.g. 4-year bond vs 4 successive 1-year bond

Liquidity Premium Theory- investors will hold long-term

maturities only if they are offered at a premium to

compensate

for future uncertainty in a securities value, which

increases

with an assets maturity.

Market Segmentation Theory-individual investors and FIs

have specific maturity preferences, and to get them to hold

securities with maturities other than their preferred requires

a

higher interest rate. (BANK vs INSURANCE COMPANY)

-

8/2/2019 Determinant of Interest Rates

33/34

2007, The McGraw-Hill Companies, All Rights

Reserved2-33McGraw-Hill/Irwin

Forecasting Interest Rates

Forward rate is an expected or implied rate

on a security that is to be originated at some

point in the future using the unbiased

expectations theory

-

8/2/2019 Determinant of Interest Rates

34/34

ENDNext meeting:

Examples and illustrations/ quiz bowl