Embed Size (px)

DESCRIPTION

Incentives are intended to ignite the sales staff's enthusiasm to sell more and better. They are used in nearly all industries - but the complex relationships and interdependencies involved in their application are often ignored.Here the Sales Strategies Group from Detecon's Strategy & Marketing Competence Practice presents a practical overview of the opportunities, challenges, and solutions which incentives can offer.Our analysis is based on the 'Incentive Framework' developed by Detecon. This provides a complete catalog of all the corporate and individual factors which influence incentives, and the relationships between them.

Citation preview

> Opinion Paper

www.detecon.com

Sales Incentives From the Jam Session to the Symphony

2009 / 03

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 2 Detecon International GmbH

Table of Contents

1 Executive Summary ............................................................................................ 4 2 From the Soloist to the Orchestra ....................................................................... 5 3 Enthusiasm is Measurable .................................................................................. 6

3.1 Targets and Possible Forms of Incentives .................................................. 6 3.2 The Full Gamut of Incentives ...................................................................... 7 3.3 Measurability ............................................................................................... 8 3.4 Variable Target Systems ............................................................................. 8

4 From the Concept to the Realization of the Incentives........................................ 9 4.1 Factors Influencing the Incentive Procedure ............................................... 9 4.1.1 Corporate influencing factors – the orchestra ........................................... 10 4.1.2 Individual influencing factors ..................................................................... 11 4.2 Abuse of Incentive Measures .................................................................... 11 4.3 Return on Incentives (ROI)........................................................................ 12 4.4 Special Features of the Distribution Channels .......................................... 14 4.4.1 Direct sales (via own employees, sales organizations)............................. 14 4.4.2 Indirect sales (sales via sales partners, e.g., supplied dealers) ................ 14 4.4.3 Direct and indirect sales in comparison..................................................... 14 4.5 Implementation of Incentive Measures and Systems................................ 15 4.6 Case Study: Indirect Sales on Emerging Markets..................................... 16 4.7 Case Study: Direct Sales on Mature Markets ........................................... 18

5 The Task of Sales Management ....................................................................... 20 6 Recommended Reading ................................................................................... 21 7 The Authors....................................................................................................... 22 8 The Company.................................................................................................... 24

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 3 Detecon International GmbH

Table of Figures

Figure 1: Detecon’s Incentive Framework................................................................................ 4

Figure 2: Decision Tree of Incentives....................................................................................... 7

Figure 3: Incentive Framework with Influencing Factors.......................................................... 9

Figure 4: Influencing Variables for Calculating the Effects of Incentives ............................... 12

Figure 5: Calculating Return on Incentives ............................................................................ 13

Figure 6: Implementation of Incentives .................................................................................. 15

Figure 7: Classic Distribution Channel Breakdown on an Emerging Market ......................... 16

Figure 8: Incentive Structure on an Emerging Market ........................................................... 17

Figure 9: Example of a Distribution Channel Structure on a Mature Market ......................... 18

Figure 10: Example of an Incentive Structure on a Mature Market ....................................... 19

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 4 Detecon International GmbH

1 Executive Summary

Incentives are intended to arouse the recipients’ enthusiasm so that they will sell more successfully. Virtually all industries make use of incentives – but the complexity of this tool in the interaction of dependencies and the related effects is frequently not fully appreciated. The bank crisis of 2008 makes this clear in a vivid manner. In today’s atmosphere of political discussions about extravagant manager bonuses or the irresponsible granting of loans to real estate customers, a consideration of incentives appears to be called for. However, the goal of this paper is not to evaluate the economic events now going on, but to take a look at incentives per se.

So Detecon describes the possibilities, the challenges, and the possible forms for incentives in a practice-oriented approach. The basis for this paper is the “Incentive Framework” developed by Detecon which considers the corporate and individual influencing factors from a holistic standpoint.

KnowledgeTypology Motivation

Internal External

The Company Environment

The Individual

Detecon’s Incentive Framework

Holistic incentives along the value chain

Profitability

Quality

Figure 1: Detecon’s Incentive Framework

If developed and implemented holistically, incentives make a major contribution to the achievement of tactical and strategic sales targets – in both direct and indirect distribution channels. Clear measurability is required if the success of incentive measures is to be evaluated.

The most important performance indicator here is the return on incentives (ROI). This ratio is calculated by comparing the additional profit generated by an incentive with the expenditures for the incentive itself. Successful incentives have a return on incentive ratio of as much as 120%.

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 5 Detecon International GmbH

2 From the Soloist to the Orchestra

The more complex a market, the more demanding the sales management. The days are long gone when a product could be sold in large quantities via a single distribution channel. The interaction of sales partners at widely varying levels and the many sides of direct sales are today standard. Whereas in the past it was possible to fall back on a few very good soloists, it is now necessary to manage a large number of capable players and direct them in a specific direction.

The challenge today is not, “What new distribution channel can I add to increase my sales?”, but rather, “How can I optimize the interaction of the channels without losing sight of the profitability of each individual one?”

When it comes to sales, companies must be where the customers are; that is why they try to cover as many channels and locations as possible. But the number of visiting customers (footfall) and the buying rate (conversion rate) can be increased long-term only “in the orchestra” of the entire company and across all stages of added value. For example, incentives given for the acquisition of new customers in sales can lead to a resource bottleneck in the downstream departments Customer Care or Billing if the measures have not been coordinated. Empirical studies document the effectiveness of the holistic procedure and reveal substantially higher return on incentives when such approaches serve as the foundation for the programs.

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 6 Detecon International GmbH

3 Enthusiasm is Measurable

Even though the word “incentive” is frequently associated with pleasure trips, incentives as a means of managing sales can be understood in a substantially broader sense:

An incentive is anything which motivates a person or team to do something aimed at a specific goal – in terms of sales, to sell something.

A major difference from other types of motivation is that the work to obtain the promised incentive can be done within a specific time period. Rewards, in contrast, can be given independently of actions aimed at specific goals or on the basis of unforeseeable or subjective factors. In that case, they do not motivate anyone, and may even have the opposite effect. The content of any incentive is characterized by two determinants: why an employee receives something (targets) and what he or she receives.

3.1 Targets and Possible Forms of Incentives

An incentive defines both: the performance and the related reward. The performance can be managed by the following measures:

Targets which must be achieved;

Competitions in which the aim is to be better than anyone else;

Mixed forms: e.g., competitions which presume the achievement of a target.

Whereas target incentives measure the performance in terms of the degree of achievement of a target which has been defined in absolute terms, it is the relative performance in comparison with the other participants which counts in competitions. The point in the latter case is to be better than anyone else.

If competitions are to have a motivational effect, each person’s own performance must be transparent – just like that of every other participant. The information required for this purpose is generally confidential, which makes it difficult to carry out competitions in an environment with strict rights of co-determination and for indirect sales in general.

One possible solution is the combination of target and competition incentives: the best performances are determined on the basis of the degree of achievement of the targets. This combination has an advantage for the company in that the number of winners of the competition is limited (e.g., the best 10) and costs can be calculated more exactly.

The majority of incentives are managed by means of targets or the degree of achievement of targets. The precise definition of the target values is a prerequisite for ensuring that the targets are set correctly and consequently are motivational. The SMART method provides an ideal approach:

S Specific: Targets must be defined precisely. This includes a clear definition of the measurement value, e.g., whether cancellations are deducted from turnover.

Incentive

The word incentive comes from the Latin root incendere, meaning to “arouse enthusiasm” or “inflame”.

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 7 Detecon International GmbH

M Measurable: Targets must be measurable. These measurements must be dependable and be conducted at regular intervals.

A Achievable: Targets should be achievable. Goals which are beyond reach discourage anyone.

R Relevant: Targets must be meaningful. A target which does not interest anyone is discouraging, despite an incentive. A discernible relationship between one’s own work and the corporate goals increases the perception of meaningfulness.

T Timely: An incentive needs a concrete time frame. This includes a starting and a finishing point as well as the point in time of the reward and feedback.

3.2 The Full Gamut of Incentives

The more specifically an incentive measure can be utilized, the more useful it is for sales management. Since there is such a broad range of possible measures, the decision tree in Figure 2 will aid in the selection of the right incentive on the basis of four relevant variables: the target, the target group, the time frame, and the nature of the incentive.

Catalogue of Incentives (extract)

YesProfit

No

Sales Force

Sales Partner

No

Short term

Long term

Yes

No

No

Check Time Frame

Financial

Social

Yes

No

Yes Competition

Yes Event: e.g. feast

Financial

Social

No

Yes Variable Salary

Yes Bestseller Club

Yes

Short termYes Financial

No

Yes Add. equipmentYes

Goal Target Group Time Remuneration Type of Incentive

Figure 2: Decision Tree of Incentives

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 8 Detecon International GmbH

Common incentives include:

Variable salary components, bonuses dependent on performance, commissions, especially for sales employees

High-value non-cash rewards: e.g., vouchers, consumables, entertainment electronics, accessories, etc.

Trips and unusual experiences: the more expensive the same trip is when booked privately, the greater the incentive

Intangible rewards: e.g., “Employee of the Month”, meetings with the management, public praise, winning of competitions

3.3 Measurability

If an incentive is to function properly, the degree of target achievement must be clearly measurable. Performance which can only be estimated and not truly measured cannot be motivated with incentives. Sales figures, for example, can be measured directly, but customer loyalty can be determined only indirectly.

The measurement variables and points in time must be defined very precisely so that there is as little room for interpretation as possible. Furthermore, they must not be changed for the duration of the incentive program. The participants must be able to depend on the reliability of the general conditions.

3.4 Variable Target Systems

In variable target systems, the overachievement of a target can compensate for the failure to meet other targets. However, the motivation to achieve the difficult targets as well is somewhat limited in this case. Moreover, a large number of detailed targets does not motivate anyone if the failure to achieve them individually does not have perceptible consequences.

In both cases, the corporate strategy plays an important role. It is the guide for weighting the individual targets and determining the extent to which overachievement of targets can compensate underachievement in other areas.

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 9 Detecon International GmbH

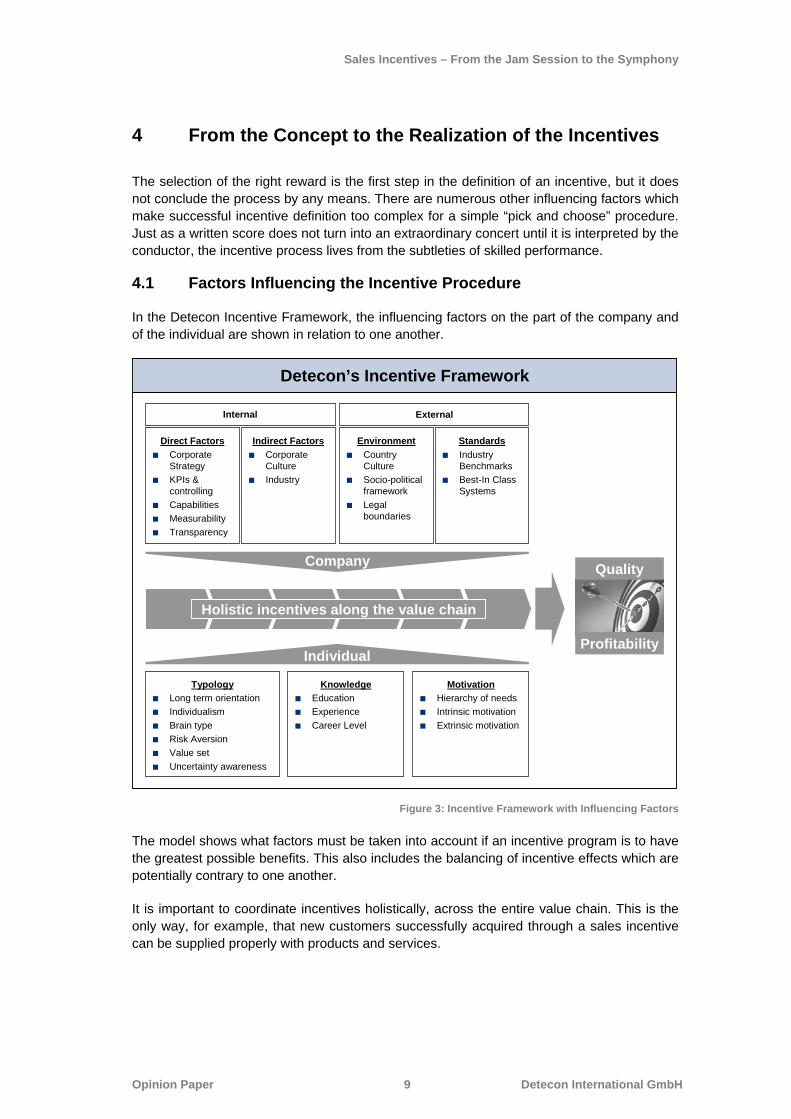

4 From the Concept to the Realization of the Incentives

The selection of the right reward is the first step in the definition of an incentive, but it does not conclude the process by any means. There are numerous other influencing factors which make successful incentive definition too complex for a simple “pick and choose” procedure. Just as a written score does not turn into an extraordinary concert until it is interpreted by the conductor, the incentive process lives from the subtleties of skilled performance.

4.1 Factors Influencing the Incentive Procedure

In the Detecon Incentive Framework, the influencing factors on the part of the company and of the individual are shown in relation to one another.

Detecon’s Incentive Framework

Individual

KnowledgeEducationExperienceCareer Level

TypologyLong term orientationIndividualismBrain typeRisk AversionValue setUncertainty awareness

MotivationHierarchy of needsIntrinsic motivationExtrinsic motivation

Internal External

Direct FactorsCorporate StrategyKPIs & controllingCapabilities MeasurabilityTransparency

Indirect FactorsCorporate CultureIndustry

EnvironmentCountry CultureSocio-political frameworkLegal boundaries

StandardsIndustry Benchmarks Best-In Class Systems

Company

Holistic incentives along the value chain

Profitability

Quality

Figure 3: Incentive Framework with Influencing Factors

The model shows what factors must be taken into account if an incentive program is to have the greatest possible benefits. This also includes the balancing of incentive effects which are potentially contrary to one another.

It is important to coordinate incentives holistically, across the entire value chain. This is the only way, for example, that new customers successfully acquired through a sales incentive can be supplied properly with products and services.

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 10 Detecon International GmbH

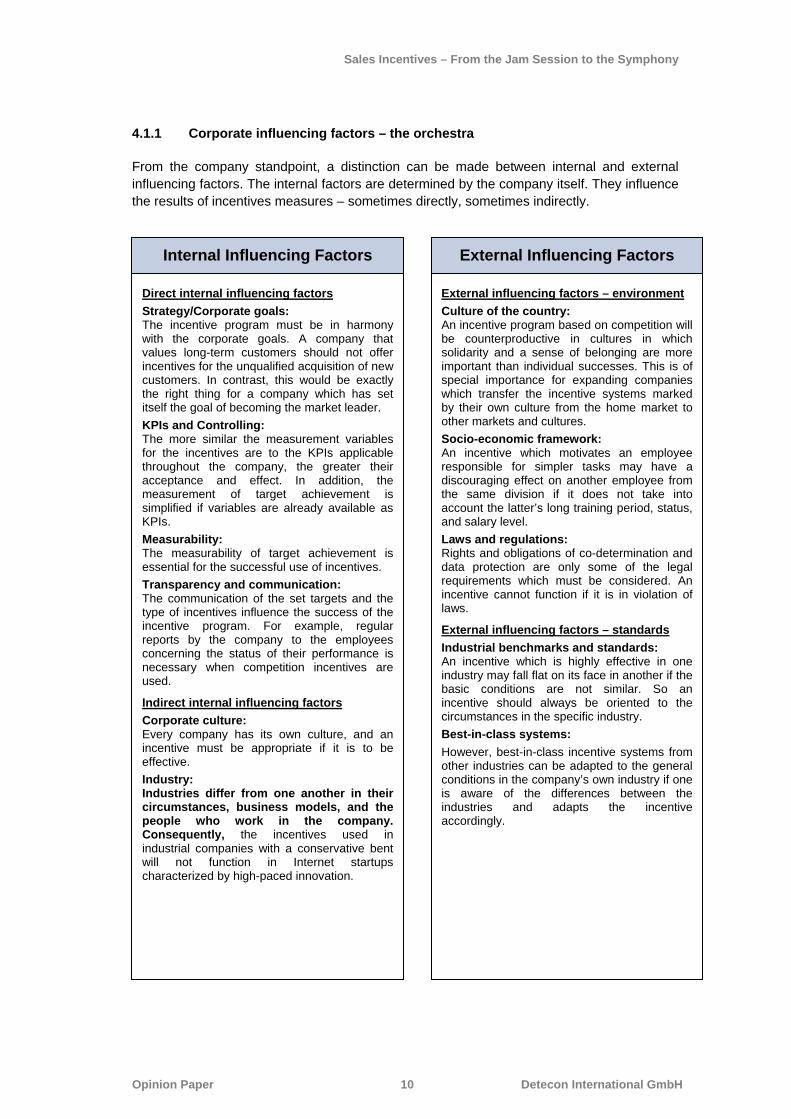

4.1.1 Corporate influencing factors – the orchestra

From the company standpoint, a distinction can be made between internal and external influencing factors. The internal factors are determined by the company itself. They influence the results of incentives measures – sometimes directly, sometimes indirectly.

Direct internal influencing factors Strategy/Corporate goals: The incentive program must be in harmony with the corporate goals. A company that values long-term customers should not offer incentives for the unqualified acquisition of new customers. In contrast, this would be exactly the right thing for a company which has set itself the goal of becoming the market leader. KPIs and Controlling: The more similar the measurement variables for the incentives are to the KPIs applicable throughout the company, the greater their acceptance and effect. In addition, the measurement of target achievement is simplified if variables are already available as KPIs. Measurability: The measurability of target achievement is essential for the successful use of incentives. Transparency and communication: The communication of the set targets and the type of incentives influence the success of the incentive program. For example, regular reports by the company to the employees concerning the status of their performance is necessary when competition incentives are used.

Indirect internal influencing factors Corporate culture: Every company has its own culture, and an incentive must be appropriate if it is to be effective. Industry: Industries differ from one another in their circumstances, business models, and the people who work in the company. Consequently, the incentives used in industrial companies with a conservative bent will not function in Internet startups characterized by high-paced innovation.

Internal Influencing Factors

External influencing factors – environment Culture of the country: An incentive program based on competition will be counterproductive in cultures in which solidarity and a sense of belonging are more important than individual successes. This is of special importance for expanding companies which transfer the incentive systems marked by their own culture from the home market to other markets and cultures. Socio-economic framework: An incentive which motivates an employee responsible for simpler tasks may have a discouraging effect on another employee from the same division if it does not take into account the latter’s long training period, status, and salary level. Laws and regulations: Rights and obligations of co-determination and data protection are only some of the legal requirements which must be considered. An incentive cannot function if it is in violation of laws.

External influencing factors – standards Industrial benchmarks and standards: An incentive which is highly effective in one industry may fall flat on its face in another if the basic conditions are not similar. So an incentive should always be oriented to the circumstances in the specific industry. Best-in-class systems: However, best-in-class incentive systems from other industries can be adapted to the general conditions in the company’s own industry if one is aware of the differences between the industries and adapts the incentive accordingly.

External Influencing Factors

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 11 Detecon International GmbH

4.1.2 Individual influencing factors

People are different: what is boring for one and a sporting challenge for another may seem threatening to a third person. Nevertheless, not every single employee can be given an individual motivation program tailored to his or her exact needs. But being aware of personal differences contributes to a willingness to empathize with individuals to a certain degree and thereby to increase the effect of incentives.

4.2 Abuse of Incentive Measures

An intrinsically motivated person is active on his or her own accord. Extrinsic motivation is the persuasion of people to do something because of an outside factor, e.g., money. The situation may also arise in which a higher reward is sought without producing the required performance. That is why the borders between the “testing of the gray areas” and out-and-out fraud are fluid.

The playful testing of limits is more likely to be found where there is still adequate intrinsic motivation, but the company has a pronounced competitive culture. Conscious abuse is most likely to occur when the employees’ identification with the company is weak. But both situations lead to results which do not correspond to the company’s intentions. Besides the higher costs, negative effects with respect to third parties are noticed above all.

A clear form of the incentive system helps to prevent abuse. The more precisely targets are defined, the better they can be measured, and the more exact the instructions, the less room there is for employees to abuse the system. But beyond this, there should be clarity about the reasonableness of the means chosen. Doing away with incentives to prevent their abuse reduces the motivation of all of the employees. So the opportunity costs from lost sales could be much higher. Slight abuse should be punished consistently, while serious abuse should be punished with the appropriate severity.

Typology: Although no two people are alike, only a small number of characteristics are important for a general incentive program. They include the time orientation, the degree of individuality, and the attitude towards risk along with the capability to motivate oneself (intrinsic motivation). Knowledge / Skills / Influencing possibilities: Incentives do not motivate anyone who is incapable of achieving the targets set for him or her. The question here is not one of how high the targets are set, but whether the person is fundamentally capable of carrying out the task. Demands exceeding someone’s capabilities owing to a lack of knowledge or skills lead to a lack of motivation to take on further challenges and reduced receptivity to future incentives.

Motivation: Incentives are supposed to motivate. So the common motivation theories can serve as a basis for successful incentive programs. They include arguments explaining why money as the sole motivator does not have a sustained effect and why factors such as public recognition and attention are often more suitable.

Individual Influencing Factors

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 12 Detecon International GmbH

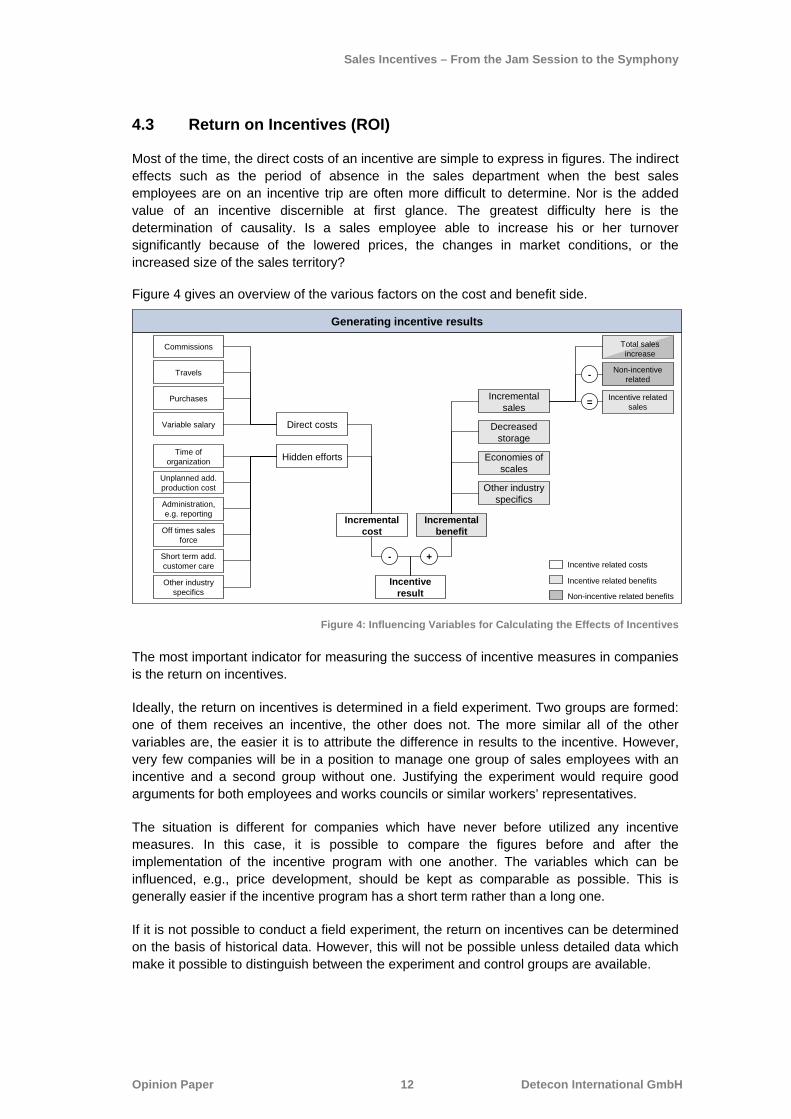

4.3 Return on Incentives (ROI)

Most of the time, the direct costs of an incentive are simple to express in figures. The indirect effects such as the period of absence in the sales department when the best sales employees are on an incentive trip are often more difficult to determine. Nor is the added value of an incentive discernible at first glance. The greatest difficulty here is the determination of causality. Is a sales employee able to increase his or her turnover significantly because of the lowered prices, the changes in market conditions, or the increased size of the sales territory?

Figure 4 gives an overview of the various factors on the cost and benefit side.

Generating incentive results

Incentive result

Direct costs

Hidden efforts

Travels

Purchases

Variable salary

Commissions

Time of organization

Unplanned add. production cost

Administration, e.g. reporting

Off times sales force

Incremental cost

Incremental benefit

Decreased storage

Incremental sales

Economies of scales

Non-incentive related

Incentive related sales

+-

=

-

Short term add. customer care

Other industry specifics

Other industry specifics

Total sales increase

Incentive related benefits

Non-incentive related benefits

Incentive related costs

Figure 4: Influencing Variables for Calculating the Effects of Incentives

The most important indicator for measuring the success of incentive measures in companies is the return on incentives.

Ideally, the return on incentives is determined in a field experiment. Two groups are formed: one of them receives an incentive, the other does not. The more similar all of the other variables are, the easier it is to attribute the difference in results to the incentive. However, very few companies will be in a position to manage one group of sales employees with an incentive and a second group without one. Justifying the experiment would require good arguments for both employees and works councils or similar workers’ representatives.

The situation is different for companies which have never before utilized any incentive measures. In this case, it is possible to compare the figures before and after the implementation of the incentive program with one another. The variables which can be influenced, e.g., price development, should be kept as comparable as possible. This is generally easier if the incentive program has a short term rather than a long one.

If it is not possible to conduct a field experiment, the return on incentives can be determined on the basis of historical data. However, this will not be possible unless detailed data which make it possible to distinguish between the experiment and control groups are available.

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 13 Detecon International GmbH

The principles for the calculation of a return on incentives is shown in Figure 5. The return on incentives compares additional profits realized through an incentive program with the costs of the program. The results show whether the additional profits are higher than the additional costs. A value less than one reveals that an incentive program did not result in enough additional profit to cover the costs of the program.

ROI = Incremental Profits

Incremental Cost ROI =

Incremental Profits

Incremental Cost

before after

IncrementalCost

ROI > 1: Profitable (Incremental profits > incremental costs)ROI < 1: Unprofitable (Incremental profits < incremental costs)

Source: The Incentive Research Foundation, Detecon Research

Return on Incentives

before after

IncrementalProfits

Profit Cost

Figure 5: Calculating Return on Incentives

Studies in the telecommunications sector show return on incentives of as much as 120% for successful incentive programs.

The determination of the return on incentives is highly dependent on the quality of the data. The more precise the data, the more confidently the additional profit can be attributed to the incentive and considered in relation to the costs.

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 14 Detecon International GmbH

4.4 Special Features of the Distribution Channels

4.4.1 Direct sales (via own employees, sales organizations)

Owing to its direct influence on the employees, the sales management is responsible for achievement of the corporate goals to a high degree. It is responsible, for example, if too few transactions are concluded with current customers and too many transactions with new customers.

4.4.2 Indirect sales (sales via sales partners, e.g., supplied dealers)

Creating incentives for sales management is more complex for indirect sales operations than for direct sales. Due to the specific structures, there are fewer incentive instruments which can be used. Less information about competing products is available for the decision about which group of persons should have incentives and how influence should be exercised.

The value of one’s own incentives in ratio to those of other parties can only be estimated. If a store is regarded as an indirect sales partner, for example, the direct competitors are not the only ones clamoring for the seller’s attention. Products from other industries sold in the same store must also be considered.

An added difficulty is that two different groups of people must be considered: the contact person who has the commercial responsibility for the sales partner and the actual salesperson. Direct access to the salesperson is consequently the exception rather than the rule. A sales manager will make the commercial contact person very happy by granting a higher margin – but it is questionable whether this will lead to greater commitment on the part of the salesperson and subsequently to higher sales figures.

Since the relationship between performance and monetary award is not directly recognizable for the salesperson, the significance of the emotional reward becomes greater. As a consequence, it is important to gain his or her enthusiasm for the products. The means to achieve this include demonstration products and training sessions as well as giveaways and opportunities for unusual experiences.

However, the agreement of the employer and the reasonableness of the means must be assured in every case. In 2006, many companies returned tickets to World Cup matches which they had received as incentives. This conduct shows how narrow (and individual) the line can be between a motivating gesture and attempted coercion.

4.4.3 Direct and indirect sales in comparison

The effects of the company’s influencing factors vary in their intensity for direct and indirect sales. In contrast, the influence of the individual factors is independent of the channel. Whereas the internal factors have more noticeable effects on direct sales, the external factors affect indirect sales more strongly. The main reasons are the availability of information and the comparison values in the evaluation of incentives.

The sales partner knows the conditions that exist on the market. If there are two comparable products, he will tend to recommend the one for which he has a better margin. So an important factor for satisfying an indirect sales partner is the external comparison.

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 15 Detecon International GmbH

Whereas the sales partner compares the incentives of two producers, the employee from direct sales is competing with his or her colleagues. The internal comparison with team colleagues is more important for his or her individual motivation than external reference figures. The internal factors of transparency and communication play a great role for internal sales. For example, motivation and satisfaction are raised by establishing and communicating clear rules for incentives (e.g., only a target achievement greater than 100% will qualify someone to take part in a trip).

When defining an incentive, the sales management must take all factors into account so as to address direct and indirect channels. Yet direct and indirect channels on growing or saturated markets each have specific advantages which should be considered in setting up the incentive program.

Whereas the sales costs dependent on turnover are extremely variable in indirect sales, the variable share of the sales costs in direct sales is lower. This is why direct selling on markets with strongly fluctuating turnover figures is more cost-intensive because the costs remain stable even when turnover is lower. On the other hand, the costs of direct selling remain relatively stable even when turnover figure rise sharply.

On saturated markets with cut-throat competition, indirect sales have the advantage that customers with a demand for impartial advice by sales partners can be served. The incentives for the sales partner must as a minimum be at the level of the competition. The incentives in direct sales, on the other hand, compete with the competition only in the war of talents.

4.5 Implementation of Incentive Measures and Systems

Any incentive is only as good as its implementation. That starts with the definition of the targets and target groups, continues with determining the details and setting the target values in each case as well as the prediction of costs and returns, and goes on to the actual implementation.

Implementation

CelebrateDo itCommunicateSet up the programSet the individual goals

Figure 6: Implementation of Incentives

Communication plays an essential role during implementation. Just as the violinist must know his cue, the sales employees must know what they have to do – but also when any further processing will be counterproductive. If they know the background of the incentives, they will have a better understanding of how their targets have been determined and can plan their own work more effectively.

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 16 Detecon International GmbH

Communication also includes regular feedback and reports concerning the extent to which individual sales employees have already reached their targets, which targets need more effort if they are to be achieved, and which targets may be given a lower priority for the time being because the level of achievement is already high. The foundation of the communication is effective measurement procedures: a reporting system that does not produce results until months after the conclusion of an incentive measure is not helpful.

Another aspect of the implementation is the formal acknowledgement of the success. American companies emphasize this much more strongly than German enterprises, for example. This is a consequence of differences in the legal situation as well as in the cultures. But regardless of the culture people come from: celebrating a success and being publically praised for it motivates a person to do even more. In Asian cultures, the group praise for the achievement of a team or corporate goal is more important, while in Western cultures the individual performance takes priority.

4.6 Case Study: Indirect Sales on Emerging Markets

The majority of the sales to end customers on emerging markets are handled via indirect distribution channels. An overview of the classic breakdown of common distribution channels is shown in Figure 7.

Direct and Indirect Sales of emerging GSM operators

Distributors

Direct Channels Indirect Channels

Shops Franchise Shops DealersCorporate sales

Dealers

Figure 7: Classic Distribution Channel Breakdown on an Emerging Market

As a rule, the structures of the indirect distribution channels display characteristics which are also reflected in the incentive program models:

Individual dealers have direct contracts with the network operators and operate either shops franchised by the operator or retail stores with their own branding.

There are frequently distributors between the dealers and the operator. Their task is to provide the logistics and infrastructure for the dealers. Consequently, the distributor also handles the incentive program / commissioning.

Another characteristic usually found on emerging markets is an overproportional share of distributors, frequently resulting in a lack of transparency in the incentive models and making it difficult to compare them.

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 17 Detecon International GmbH

A major point of attack for new players on such a market is the development of an incentive system featuring transparent KPIs which

is attractive for the distributors or indirect channels,

increases the loyalty of the participants in the distribution channel,

does not cause the incentive costs for the operator to rise overproportionately, and

avoids any opportunistic conduct on the part of the dealers.

The structure of an incentive or commission model described below has been developed and successfully implemented for the market entry of a mobile operator on an emerging market which already had a number of established competitors:

Nr. of cards are allocated to dealers based on a performance based quota system.

Revenues per indirect

dealer= Commission per product-unit # of product-unitsx

Competitive principle of quota allocation

Performance basedSIM sales target achievementRecharge card sales achievementE-Top up target achievement

Fixed quotaDependent on initial contract conditions

A high upfront commission

Upfront After salesComponent to guarantee “ good behavior” in qualitative aspects

Quality based amountbased on mystery shopping regarding

Price loyaltyBrand supportthrough shops

Commissionbased on airtime usage

Fixed amount

Concept

Components

Incentive Structure Emerging Markets

Figure 8: Incentive Structure on an Emerging Market

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 18 Detecon International GmbH

The components are explained briefly in the following:

Upfront commission: A high “upfront” incentive in comparison with the competition guarantees the dealers’ loyalty, especially for the new entry of an operator on the market.

After-sales quality: The compliance with price agreements, brand loyalty, service quality, and similar factors of the dealers can be measured with the help of mystery shopping. An assessment of the service quality is taken into account as a part of the incentive for the sold products.

A fixed incentive amount is, as a rule, based on the agreement between the operator and distributor association and on the degree of target achievement of the previous month.

The acquisition of customers with a high value contribution can be encouraged by coupling the incentive proportionately to the airtime usage as well, creating a negative sanction for the strict orientation to new customer contracts via the commissioning.

Performance-based incentives are oriented to the degree of target achievement of the individual dealer with respect to the sold products. On emerging markets, these are usually pre-paid or post-paid SIM card sales and top-up volumes within a specified observed period.

An incentive structure of this type supports in particular the focus on the quality parameters important for the network operator and encourages the sustained development of customers with a higher value contribution for the company.

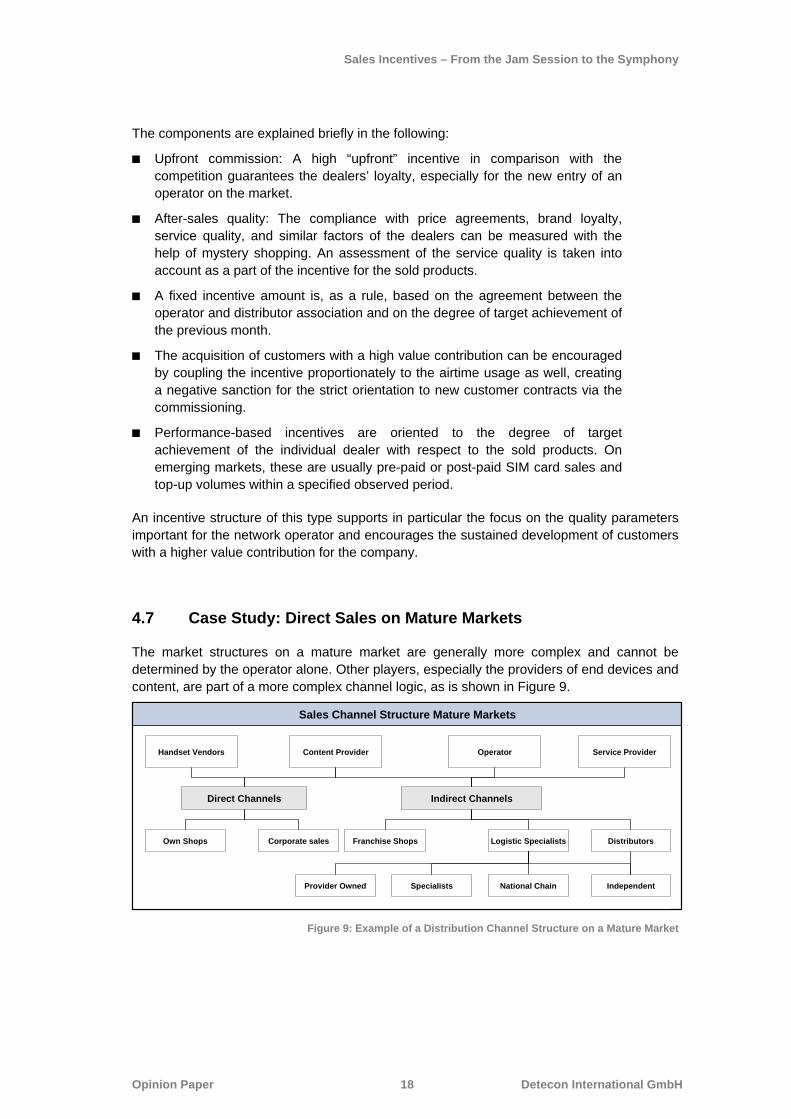

4.7 Case Study: Direct Sales on Mature Markets

The market structures on a mature market are generally more complex and cannot be determined by the operator alone. Other players, especially the providers of end devices and content, are part of a more complex channel logic, as is shown in Figure 9.

Sales Channel Structure Mature Markets

Logistic Specialists

Direct Channels Indirect Channels

Own Shops Franchise Shops DistributorsCorporate sales

Handset Vendors Content Provider Operator Service Provider

Logistic Specialists

Direct Channels Indirect Channels

Own Shops Franchise Shops DistributorsCorporate sales

National Chain

Handset Vendors Content Provider Operator Service Provider

IndependentSpecialistsProvider Owned

Figure 9: Example of a Distribution Channel Structure on a Mature Market

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 19 Detecon International GmbH

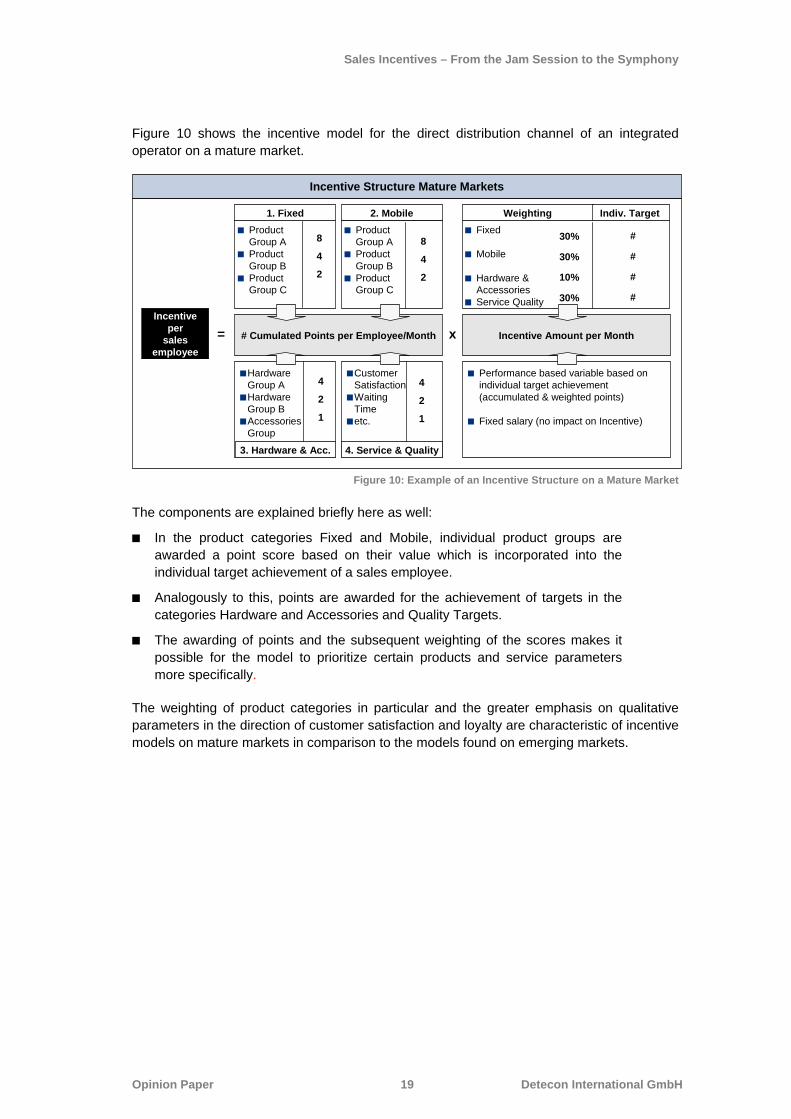

Figure 10 shows the incentive model for the direct distribution channel of an integrated operator on a mature market.

Figure 10: Example of an Incentive Structure on a Mature Market

The components are explained briefly here as well:

In the product categories Fixed and Mobile, individual product groups are awarded a point score based on their value which is incorporated into the individual target achievement of a sales employee.

Analogously to this, points are awarded for the achievement of targets in the categories Hardware and Accessories and Quality Targets.

The awarding of points and the subsequent weighting of the scores makes it possible for the model to prioritize certain products and service parameters more specifically.

The weighting of product categories in particular and the greater emphasis on qualitative parameters in the direction of customer satisfaction and loyalty are characteristic of incentive models on mature markets in comparison to the models found on emerging markets.

Fixed

Mobile

Hardware & AccessoriesService Quality

Incentive per

sales employee

= # Cumulated Points per Employee/Month Incentive Amount per Monthx

Weighting

Performance based variable based on individual target achievement(accumulated & weighted points)

Fixed salary (no impact on Incentive)

ProductGroup AProductGroup BProduct Group C

1. Fixed 2. MobileProductGroup AProduct Group BProductGroup C

CustomerSatisfactionWaiting Timeetc.

HardwareGroup AHardwareGroup BAccessoriesGroup

3. Hardware & Acc. 4. Service & Quality

8

4

2

8

4

2

4

2

1

4

2

1

30%

30%

10%

30%

#

#

#

#

Indiv. Target

Incentive Structure Mature Markets

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 20 Detecon International GmbH

5 The Task of Sales Management

.Within the company, the sales management realizes the requirements from the corporate strategy as specific incentives and ensures a balance in the overall picture by adjusting the individual channels.

When incentives with a specific direction are offered, short-term turnover targets as well as the strategic orientation of the company can be taken into account and realized. By heeding the individual needs of the sales employees, sales management can achieve a holistic treatment of all of the factors influencing sales. The approach of an indiscriminate distribution to everyone is avoided and sales are promoted where action is meaningful and has a positive influence on achievement of the corporate goals. At the same time, less efficient product-channel combinations are minimized, thereby increasing profitability.

This procedure is initially applicable to all market situations. However, differences in the various market and product phases must be taken into account by sales management. The consistency and understandability of the measures are important for the participants in every market phase. The measurability and correct calculation of the return on incentives are other major success factors.

The fact that an orchestra is made up of a large number of talented individuals does not by itself automatically lead to a magnificent performance. The jam session does not turn into a symphony until a conductor comes along to handle the coordination. Successful sales people also need coordination. Playing together successfully comes to fruition only in the combination of conductor and orchestra, sales management and sales force.

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 21 Detecon International GmbH

6 Recommended Reading

Gerstenberger, Rico; Plogmann, Stefan; Stanat, Thomas; Willand, Sebastian; Zülz, Corinna: Motivation und Motivationstheorien

Gopalakrishna, Srinath: Measuring the RETURN-ON-INCENTIVE of Sales Incentive Program, 2004

Häusel, Dr. Hans-Georg: Brain Script. Warum Kunden kaufen, 2004

ITA-Group: Using Audience Segmentation and Targeted Strategies to Boost the RETURN-ON-INCENTIVE of Performance Management Programs, 2007

Kehr, Dr. Hugo M.: Motivation und Volition: Zwischen impliziten Motiven und expliziten Zielen, 2001

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 22 Detecon International GmbH

7 The Authors

Rena Wickenheiser is a Senior Consultant working in Detecon’s Competence Practice Strategy and Marketing at the Bonn office. After earning her degree in psychology and an MBA, she worked in a number of positions in sales and project management in various companies. She joined Detecon in 2007. Thanks to her practical experience from numerous sales projects, she has a broad knowledge base for both the analysis of and the drafting of concepts for sales organizations and processes.

Telephone: +49 228 700 2577 or

Daniel Oliver Augsten is a Senior Consultant working in Detecon’s Sales Strategy Group. He has had more than eight years of experience in the ICT industry, including several years in various positions in marketing and sales in the mobile network sector. He has been involved in national and international projects at Detecon since 2004. His focus is on the sales and marketing strategy development for Tier 1 fixed and mobile network operators as well as on the establishment and operation of marketing and sales organizations on emerging markets.

Telephone: +49 228 700 2521 or

Holger Biermann is a Senior Consultant working in Detecon’s Sales Strategy Group. He has had more than eleven years of experience in the ICT industry, including several years in various positions in marketing and sales in the mobile network sector. He has been involved in national and international projects at Detecon since 2007. The focus of his work is on the development of sales and marketing strategies, the establishment and optimization of sales structures and processes, and investigations of economic efficiency.

Telephone: +49 228 700 2567 or

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 23 Detecon International GmbH

Martin Beiten is a Business Analyst in Detecon’s Competence Practice Strategy and Marketing at the Bonn office where he works for the Sales Strategy Group. He has concluded various national and international projects at Detecon since 2007. He has experience in sales for managed services, mobile payment, and fixed-mobile convergence products and services. The focal point of his work is on the analysis of markets and the development of competitive strategies.

Telephone: +49 228 700 2529 or

Sales Incentives – From the Jam Session to the Symphony

Opinion Paper 24 Detecon International GmbH

8 The Company

Detecon International GmbH

Detecon International is a leading worldwide company for integrated management and technology consulting founded in 2002 from the merger of consulting firms DETECON and Diebold. Based on its comprehensive expertise in information and communication technology (ICT), Detecon provides consulting services to customers from all key industries. The company's focus is on the development of new business models, optimization of existing strategies and increase of corporate efficiency through strategy, organization and process improvements. This combined with Detecon's exceptional technological expertise enables us to provide consulting services along our customers' entire value-added chain.. The industry know-how of our consultants and the knowledge we have gained from successful management and ICT projects in over 100 countries forms the foundation of our services. Detecon is a subsidiary of T-Systems, the business customers brand of Deutsche Telekom.

Integrated Management and Technology Competence

We possess an excellent capability to translate our technological expertise and comprehensive industry and procedural knowledge into concrete strategies and solutions. From analysis to design and implementation, we use integrated, systematic and customer-oriented consulting approaches. These entail, among other things, the evaluation of core competencies, modular design of services, value-oriented client management and the development of efficient structures in order to be able to distinguish oneself on the market with innovative products. All of this makes companies in the global era more flexible and faster – at lower costs.

Detecon offers both horizontal services that are oriented towards all industries and can entail architecture, marketing or purchasing strategies, for example, as well as vertical consulting services that presuppose extensive industry knowledge. Detecon's particular strength in the ICT industry is documented by numerous domestic and international projects for telecommunications providers, mobile operators and regulatory authorities that focused on the development of networks and markets, evaluation of technologies and standards or support during the merger and acquisition process.

Detecon International GmbH Oberkasselerstr. 2

53227 Bonn Telefon: +49 228 700 0

E-Mail: [email protected] Internet: www.detecon.com