Embed Size (px)

Citation preview

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 1/13

JAIN IRRIGATION SYSTEMS LIMITED(JISL)

Reiterating- BUY

October 7,October 7,October 7,October 7, 2011201120112011

Analyst Analyst Analyst AnalystRajivRajivRajivRajiv BharatiBharatiBharatiBharati

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 2/13

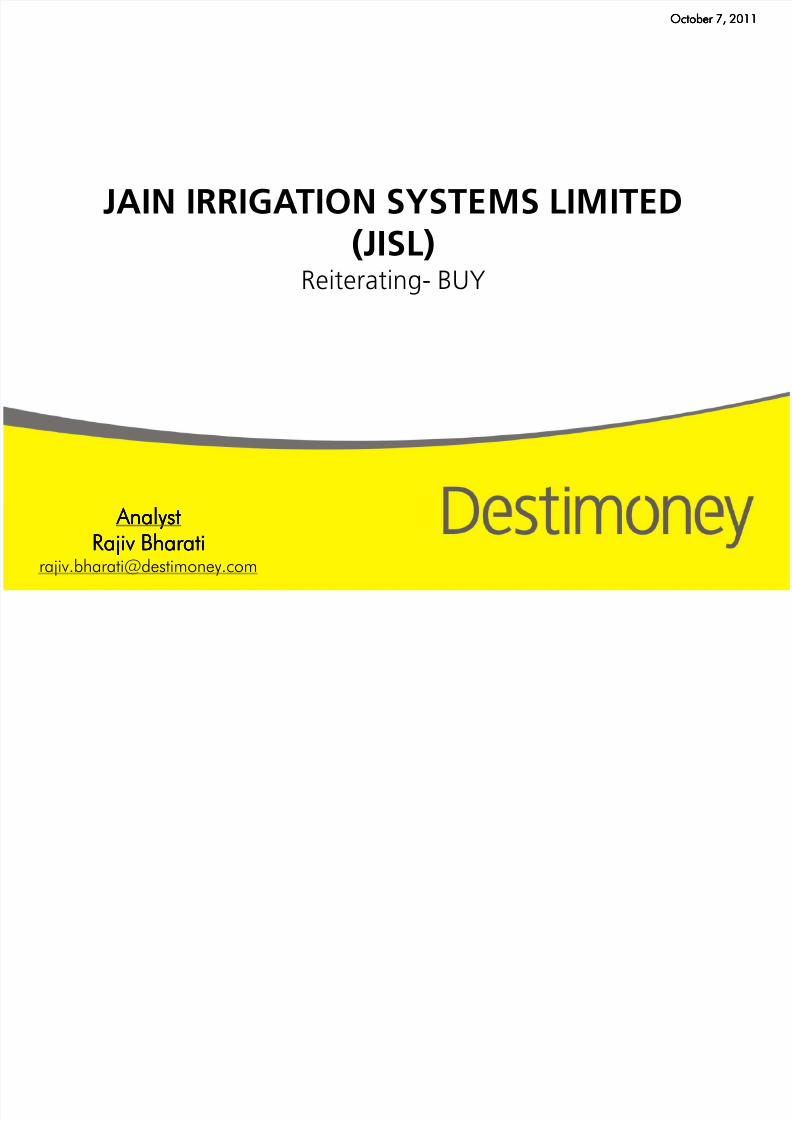

JISL – Reiterating BUY with a target upside of 20% BUYBUYTARGET :TARGET : ` ` 162162

CMP :CMP : ` ` 135135

Key Data

Ticker (Bloomberg) JI

NSE Code JISLJALEQS

BSE Code 500219

Sector Agriculture

Industry

Face Value (`) 2

Book Value per share 41

Dividend Yield (%) 0.7%

52 Week Range (`) 128.5-246.8

Market Cap. (` mn.) 51,568

Irrigation & Food Processing

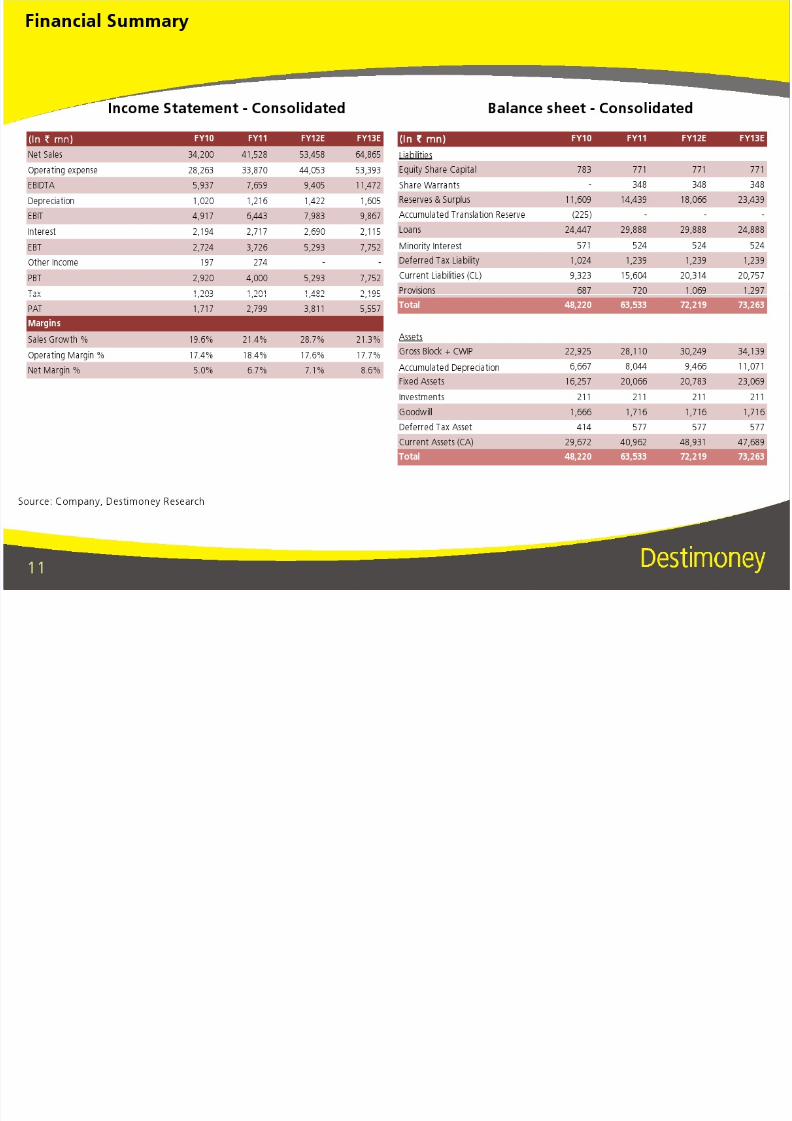

(In ` mn)(In ` mn)(In ` mn)(In ` mn) FY10 FY11 FY12E FY13E

Net Sales 34,200 41,528 53,458 64,865

EBITDA 5937 7659 9405 11472

EBITDA Margin 17.4% 18.4% 17.6% 17.7%

EPS (`) 6.5 7.4 9.5 14.1

EV/Sales 2.1 1.7 1.3 1.1

EV/EBITDA 12.0 9.3 7.6 6.2

P/E (x) 20.8 18.4 14.2 9.6

Price Performance CY08 CY09 CY10 YTD

Absolute -46% 154% 21% -35%

Relative 6% 78% 3% -15%

2

Source: Company, Bloomberg, Destimoney Research

Promoter31%

MF/UTI2%

FIIs55%

BodiesCorporate

5%

Individuals

6%

Others1% 55

70

85

100

115

Oct-10 Jan-11 Mar-11 Jun-11 Sep-11

NIFTY JISL

Shareholding Pattern (as of Jun 30, 2011) Relative Stock Performance (Oct'10=100)

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 3/13

NBFC model not as treacherous at it sounds

JISL’s decision to address the problem of rising gross receivables due to delay in receipt of subsidy from govt

by setting up an NBFC is a potent solution with a few regulatory and execution related riders.

Securitization of the loans given to farmers is eligible to be considered as Priority Sector Lending and hence

will reduce the cost of funds for the NBFC which will percolate to farmers in the form of reduced interestburden.

Stretched balance sheets of competitors will also inspire them to follow suite if the model gathers

momentum.

3

Acceptance o up ront scount on t e MIS equ pments to negate t e nterest to e pa y t e armer n

case of delay in release of subsidy by the govt is a major determinant in the success of the above solution.

During Q1FY12, MIS grew at a robust 30% YoY while Agro processing segment grew by 86% on the back

of strong Fruit Pulp processing. Operating margins for MIS shrunk by 100 bps at 30.3% while Agro

Processing segment witnessed 300 bps margin at a YoY level.

Proposed ` 7bn QIP to fund the future capex plans remains an overhang as the stock is trading way belowthe managements’ comfort level to float the issue.

We feel business at large is still robust and NBFC model will iron out the current short term cash flow

worries as well. Hence, we reiterate BUY on JISL with a target price of ` `̀ ` 162 per share.

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 4/13

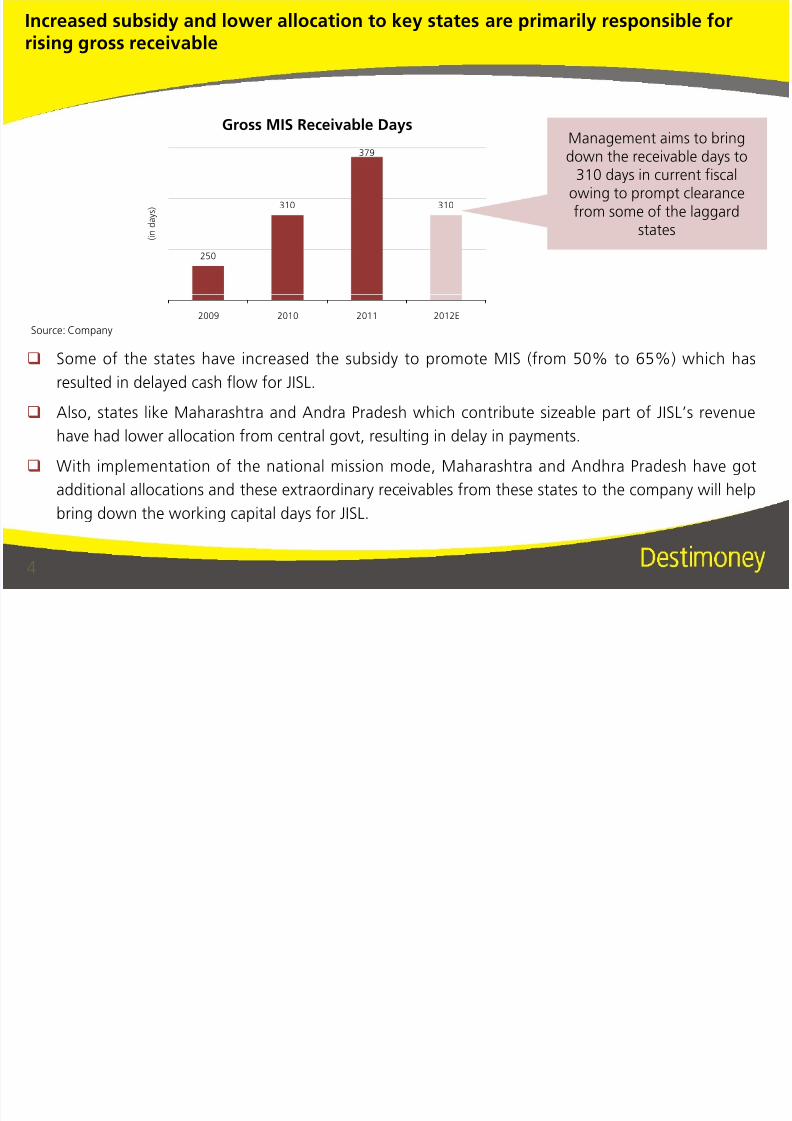

Increased subsidy and lower allocation to key states are primarily responsible forrising gross receivable

250

310

379

310

( i n d a y s )

Gross MIS Receivable DaysManagement aims to bringdown the receivable days to

310 days in current fiscalowing to prompt clearance

from some of the laggardstates

4

Some of the states have increased the subsidy to promote MIS (from 50% to 65%) which has

resulted in delayed cash flow for JISL.

Also, states like Maharashtra and Andra Pradesh which contribute sizeable part of JISL’s revenuehave had lower allocation from central govt, resulting in delay in payments.

With implementation of the national mission mode, Maharashtra and Andhra Pradesh have got

additional allocations and these extraordinary receivables from these states to the company will help

bring down the working capital days for JISL.

2009 2010 2011 2012E

Source: Company

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 5/13

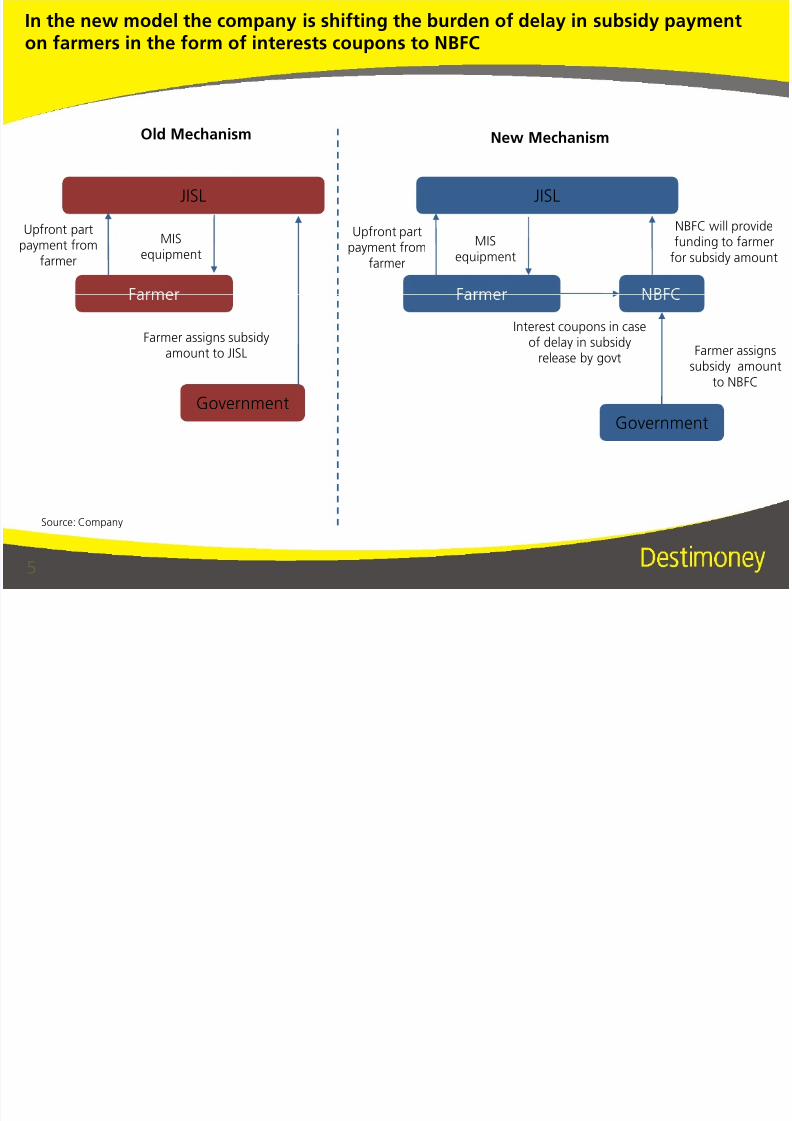

In the new model the company is shifting the burden of delay in subsidy paymenton farmers in the form of interests coupons to NBFC

JISL

MISequipment

Upfront partpayment from

farmer

JISL

NBFC will providefunding to farmer

for subsidy amount

Old Mechanism New Mechanism

MISequipment

Upfront partpayment from

farmer

5

Government

Farmer assigns subsidyamount to JISL

Government

Farmer assignssubsidy amount

to NBFC

Interest coupons in caseof delay in subsidy

release by govt

Source: Company

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 6/13

New mechanism is expected to become operational by the close of FY12

Management expects license from RBI to float the NBFC to come by Q3FY12.

The structure of the NBFC would be

Year 1: Equity base ` 800 mn – JISL (max 49%), IFC(10% ), Promoters (balance)

Year 2 onwards: Equity base ` 2,000 mn – JISL (40%), IFC(10% ), Promoters (20%), Others

(30%)

6

oug opera ng marg ns are expec e o come un er pressure ue o e up ron scoun

offered by JISL to negate the interest cost to the farmer, but we expect reduction in interest burden

on JISL will compensate for the same.

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 7/13

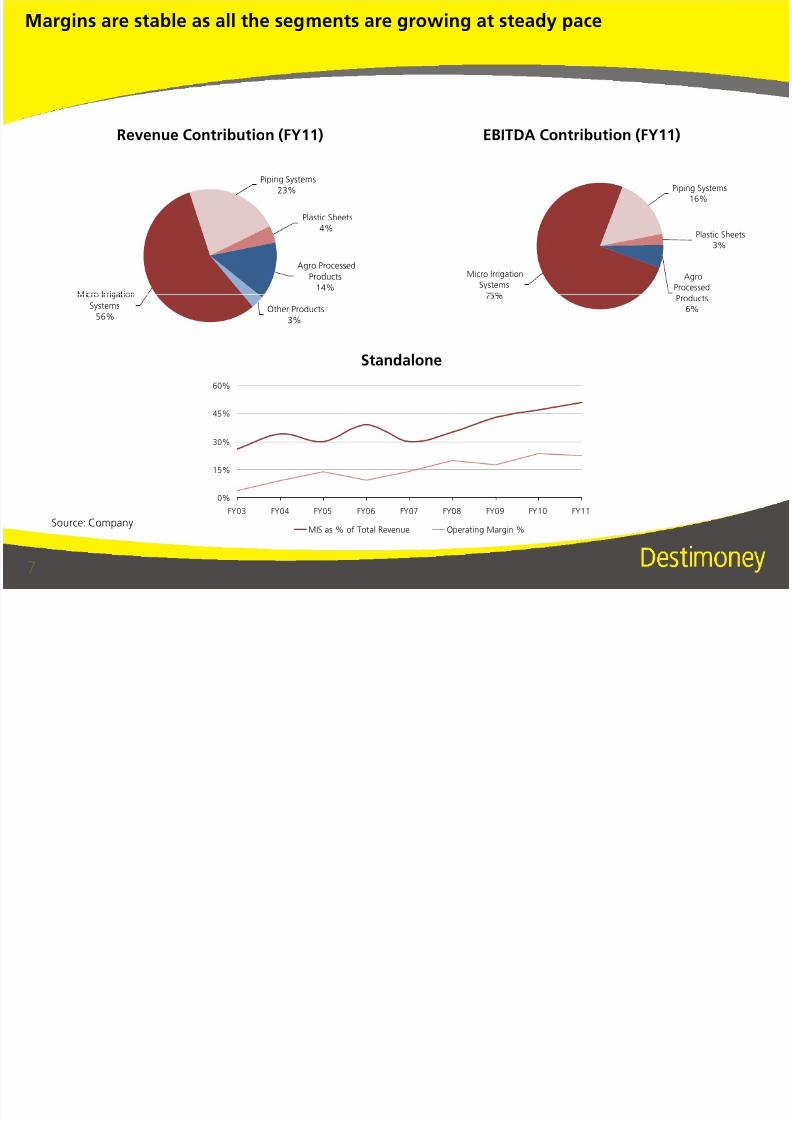

Margins are stable as all the segments are growing at steady pace

Revenue Contribution (FY11) EBITDA Contribution (FY11)

Piping Systems

23%

Plastic Sheets

4%

Agro Processed

Products

14%

Piping Systems

16%

Plastic Sheets

3%

Agro

Processed

Micro Irrigation

Systems

7

0%

15%

30%

45%

60%

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11

MIS as % of Total Revenue Operating Margin %

Other Products3%

Systems

56%

Products

6%

Standalone

Source: Company

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 8/13

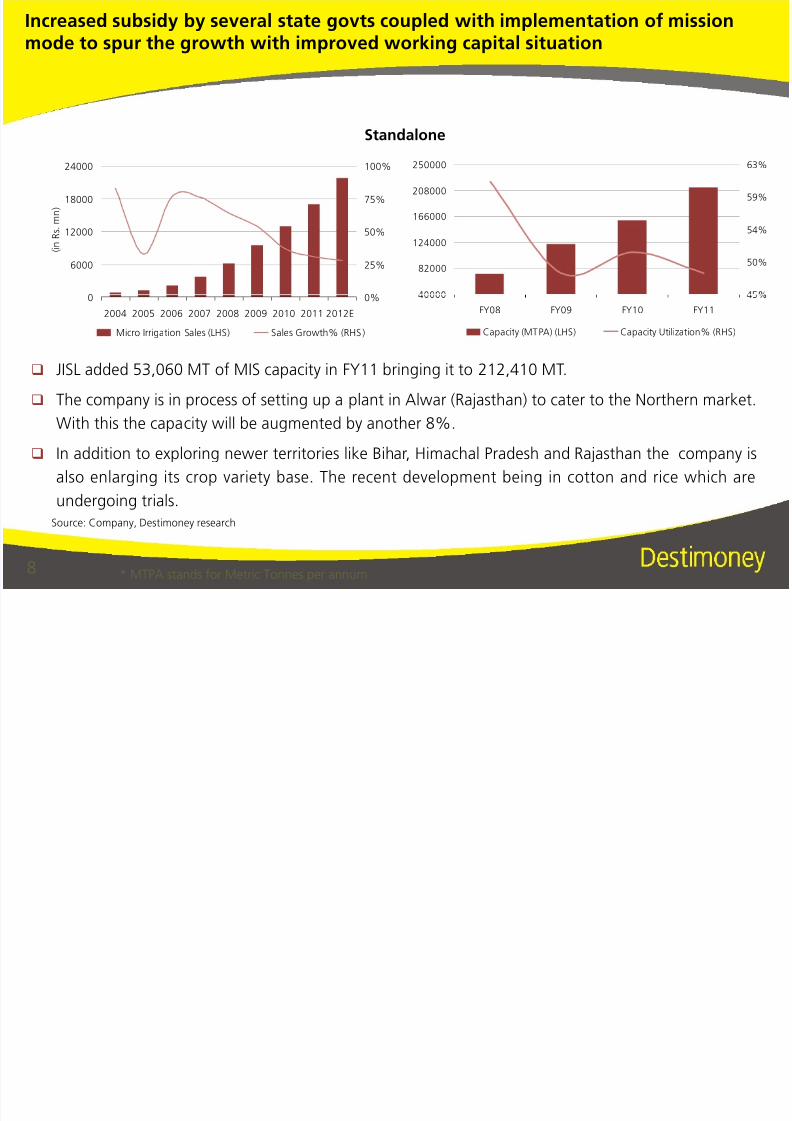

Increased subsidy by several state govts coupled with implementation of missionmode to spur the growth with improved working capital situation

6000

12000

18000

24000

( i n R s . m n )

25%

50%

75%

100%

82000

124000

166000

208000

250000

50%

54%

59%

63%

Standalone

8

JISL added 53,060 MT of MIS capacity in FY11 bringing it to 212,410 MT.

The company is in process of setting up a plant in Alwar (Rajasthan) to cater to the Northern market.

With this the capacity will be augmented by another 8%.

In addition to exploring newer territories like Bihar, Himachal Pradesh and Rajasthan the company is

also enlarging its crop variety base. The recent development being in cotton and rice which are

undergoing trials.

0

2004 2005 2006 2007 2008 2009 2010 2011 2012E

0%

Micro Irrigation Sales (LHS) Sales Growth% (RHS)

FY08 FY09 FY10 FY11

Capacity (MTPA) (LHS) Capacity Utilization% (RHS)

* MTPA stands for Metric Tonnes per annum

Source: Company, Destimoney research

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 9/13

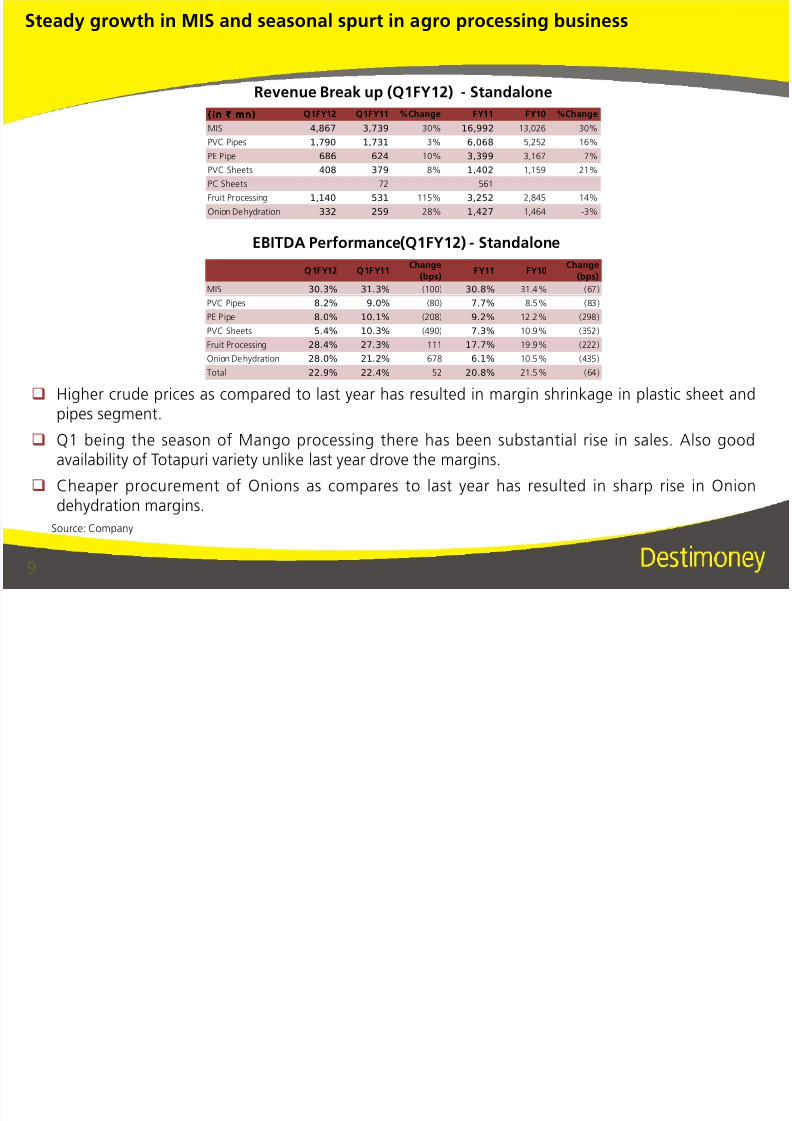

EBITDA Performance(Q1FY12) - Standalone

Revenue Break up (Q1FY12) - Standalone

Steady growth in MIS and seasonal spurt in agro processing business

(In ` mn)(In ` mn)(In ` mn)(In ` mn) Q1FY12 Q1FY11 %Change FY11 FY10 %Change

MIS 4,867 3,739 30% 16,992 13,026 30%

PVC Pipes 1,790 1,731 3% 6,068 5,252 16%

PE P ipe 686 624 10% 3,399 3,167 7%

PVC Sheets 408 379 8% 1,402 1,159 21%

PC Sheets 72 561

Fruit Processing 1,140 531 115% 3,252 2,845 14%

Onion Dehydration 332 259 28% 1,427 1,464 -3%

Q1FY12 Q1FY11Change

(bps)FY11 FY10

Change

(bps)

MIS 30.3% 31.3% (100) 30.8% 31.4% (67)

9

Source: Company

Higher crude prices as compared to last year has resulted in margin shrinkage in plastic sheet and

pipes segment. Q1 being the season of Mango processing there has been substantial rise in sales. Also good

availability of Totapuri variety unlike last year drove the margins.

Cheaper procurement of Onions as compares to last year has resulted in sharp rise in Oniondehydration margins.

PVC Pipes 8.2% 9.0% (80) 7.7% 8.5% (83)

PE P ipe 8.0% 10.1% (208) 9.2% 12.2% (298)

PVC Sheets 5.4% 10.3% (490) 7.3% 10.9% (352)

Fruit Processing 28.4% 27.3% 111 17.7% 19.9% (222)

Onion Dehydration 28.0% 21.2% 678 6.1% 10.5% (435)

Total 22.9% 22.4% 52 20.8% 21.5% (64)

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 10/13

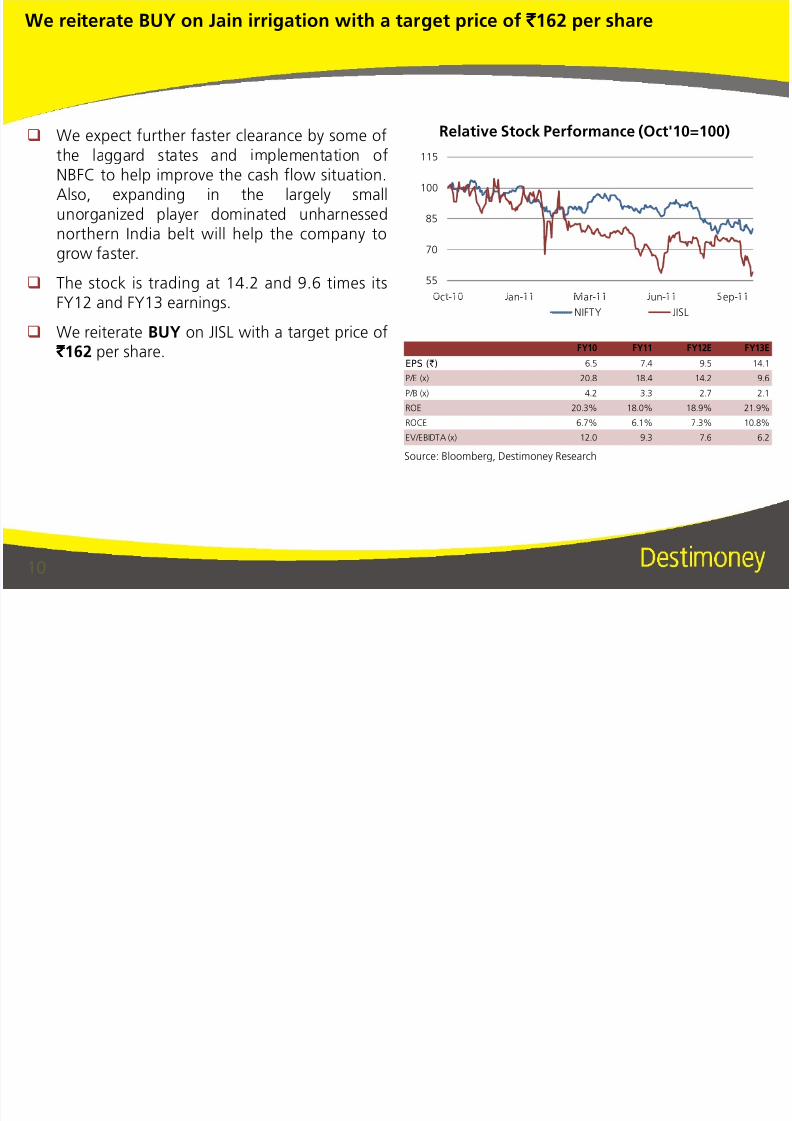

We reiterate BUY on Jain irrigation with a target price of ` `̀ ` 162 per share

We expect further faster clearance by some ofthe laggard states and implementation ofNBFC to help improve the cash flow situation.Also, expanding in the largely small

unorganized player dominated unharnessednorthern India belt will help the company togrow faster.

The stock is trading at 14.2 and 9.6 times its 55

70

85

100

115

Relative Stock Performance (Oct'10=100)

10

FY12 and FY13 earnings. We reiterate BUY on JISL with a target price of

` `̀ ` 162 per share.

Source: Bloomberg, Destimoney Research

FY10 FY11 FY12E FY13E

EPS (`) 6.5 7.4 9.5 14.1

P/E (x) 20.8 18.4 14.2 9.6

P/B (x) 4.2 3.3 2.7 2.1

ROE 20.3% 18.0% 18.9% 21.9%

ROCE 6.7% 6.1% 7.3% 10.8%

EV/EBIDTA (x) 12.0 9.3 7.6 6.2

c - an- ar- un- ep-

NIFTY JISL

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 11/13

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 12/13

Key risks

Any delay in securing NBFC license and floating the NBFC will act negatively to the already

deteriorated cash flow.

QIP issue at current levels will cause greater dilution of equity.

The business propels on the subsidy provided by GoI. Any cut in the subsidy by GoI will have a direct

impact on JISL’s business

Piping and sheets business are very sensitive to polymer prices

12

Whole business is pivoted around micro irrigation technology and hence the company is vulnerableto the technology becoming obsolete or it may lose out to a cheaper technology providing the same

benefits

Convincing the farmers to switch from traditional irrigation to MIS usage is time consuming. Most

farmers are averse to be the first mover and tend to wait for their peers to switch first.

There is a slight possibility of various countries banning imports into their countries which might

impact the business of JISL.

8/3/2019 Des Ti Money Research JISL Reiterating BUY

http://slidepdf.com/reader/full/des-ti-money-research-jisl-reiterating-buy 13/13

![Tata Trusts and Jain Irrigation Systems Ltd. (JISL) Collaborate on High Tech And Sustainable Agribusiness Development [Company Update]](https://img.pdfslide.us/doc/110x75/577c812a1a28abe054abbe66/tata-trusts-and-jain-irrigation-systems-ltd-jisl-collaborate-on-high-tech.jpg)