Embed Size (px)

Citation preview

March 2014

Growth Through Risk Management

Deriving the Economic Impact of Derivatives

March 2014

Growth Through Risk Management

Apanard (Penny) Prabha, Keith Savard, and Heather Wickramarachi

Research SupportStephen Lin, Donald Markwardt, and Nan Zhang

Project DirectorsRoss DeVol and Perry Wong

Deriving the Economic Impact of Derivatives

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Praesent pharetra vestibulum lacus eget consequat. In vel varius metus. Curabitur ut fringilla est. Sed hendrerit mollis facilisis.

—Lorem Ipsum

ACKNOWLEDGMENTS

This project evolved from discussions with various stakeholders of the Milken Institute who encouraged us to examine derivatives markets in the aftermath of the financial crisis and Great Recession. It was made possible through the support of the CME Group. The views expressed in the report, however, are solely those of the Milken Institute.

The Milken Institute would like to give special thanks to the research department of the CME Group for their valuable suggestions, feedback, and overall leadership throughout the research process. The authors appreciate the indispensable efforts of Milken Institute Managing Director Mindy Silverstein in securing the resources required to convert a methodological outline into a final product. Additionally, we appreciate the encouragement provided by Milken Institute CEO Michael Klowden in this undertaking.

The Milken Institute Research team is grateful for the advice, counsel, and expertise provided by reviewers Richard Sandor, chairman and CEO of Environmental Financial Products LLC; Ross Levine, Willis H. Booth Chair in Banking and Finance at the Haas School of Business, University of California at Berkeley; and James Barth, the Lowder Eminent Scholar in Finance at Auburn University. All are Senior Fellows of the Milken Institute. Richard Sandor is a true financial innovator known as the “father of financial futures.” Ross Levine is among the most highly regarded researchers in the operations of financial systems and functioning of the economy. Jim Barth is an expert in financial institutions and capital markets, both domestic and global, with special emphasis on regulatory issues. Our colleagues’ insights significantly improved the quality and clarity of this report.

ABOUT THE MILKEN INSTITUTE

A nonprofit, nonpartisan economic think tank, the Milken Institute works to improve lives around the world by advancing innovative economic and policy solutions that create jobs, widen access to capital, and enhance health. We produce rigorous, independent economic research—and maximize its impact by convening global leaders from the worlds of business, finance, government, and philanthropy. By fostering collaboration between the public and private sectors, we transform great ideas into action.

©2013 Milken Institute This work is made available under the terms of the Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Unported License, available at creativecommons.org/licenses/by-nc-nd/3.0/

Executive Summary ...................................................................................... 1

Key Findings ...................................................................................................................... 1

An Empirical Foundation .................................................................................................. 2

Derivatives: A Market Mainstay Amid Globalization ....................................................... 4

Why Use Derivatives? ....................................................................................................... 5

Regulatory Reform and the Future .................................................................................. 6

Introduction ................................................................................................... 9

1. History ...................................................................................................... 13

1.1 Integration and Oversight in the Modern Era ........................................................... 14

2. Global Growth and Recent Trends ....................................................... 19

2.1 Volatility and Technology .......................................................................................... 22

2.2 The Exchange-Traded Market .................................................................................. 25

2.3 The OTC Market ......................................................................................................... 27

2.4 Different Environments, Different Strengths .......................................................... 30

3. Risk, Price, and Cost ............................................................................... 33

3.1 Managing Risk ...........................................................................................................33

3.2 Price Discovery .........................................................................................................40

3.3 Liquidity and Lower Costs ........................................................................................ 42

4. Measuring Derivatives’ Impact Empirically ....................................... 45

4.1 Bolstering Bank Lending .........................................................................................48

4.2 Augmenting the Value of Non-Financial Firms ....................................................... 55

4.3 Overall Impact on the U.S. Economy ........................................................................ 59

4.4 What Futures Do for the Economy ...........................................................................63

5. A New Framework .................................................................................. 69

5.1 Clearing and Capital .................................................................................................. 69

5.2 Costs Will Influence Use ........................................................................................... 71

5.3 Extraterritoriality and Regulatory Arbitrage .......................................................... 71

References and Appendixes ....................................................................... 73

About the Authors ..................................................................................... 104

Contents

1

Executive SummaryThis study is being released at a time when the global economy is still struggling to heal itself, with the help of central banks, from a crisis that ravaged the financial system. Prior to the calamity that began six years ago, derivatives use grew at an astounding rate as a broad array of businesses and investors sought to reap their benefits. During the period of the crisis and its aftermath, over-the-counter (OTC) derivatives—credit derivatives in particular—were severely criticized as a factor in raising counterparty risk and contributing to a near-shutdown of the financial system. Consequently, significant regulatory change has been instituted with the aim of increasing transparency and reducing systemic risk.

It is time for a fact-based assessment of the role derivative products play in commerce. If these financial instruments are so harmful, as some parties believe, why do so many banks and non-financial firms use them in the course of everyday business? What has been lost in the drama surrounding derivatives is an understanding of the positive impact, primarily through risk mitigation, that most of these instruments have had on U.S. economic growth over the past decade.

KEY FINDINGS

» Banks’ use of derivatives, by permitting greater extension of credit to the private sector, increased U.S. quarterly real GDP by about $2.7 billion each quarter from Q1 2003 to Q3 2012.

» Derivatives use by non-financial firms increased U.S. quarterly real GDP by about $1 billion during the same period by improving their ability to undertake capital investments.

» Combined, derivatives expanded U.S. real GDP by about $3.7 billion each quarter. The total increase in economic activity was 1.1 percent ($149.5 billion) between 2003 and 2012.

» By the end of 2012, employment had been boosted by 530,400 (0.6 percent) and industrial production 2.1 percent.

Derivatives’ role during the financial crisis and subsequent anemic recovery is also examined. Derivatives are shown to have an even larger positive impact relative to the pre-crisis period. This is not surprising given that firms use derivatives to minimize cash-flow volatility associated with underlying risk.

This first-of-its-kind study of derivatives’ quantitative impact on economic growth is built on a solid and robust methodological foundation, an extensive literature survey, and careful attention to data gathering and empirical analysis. Several methodological challenges were overcome in attempting to discern the effects of derivatives use on overall U.S. economic performance.

2 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

Case studies of the airline, energy, and food-processing industries provide detail and context for the macroeconomic analysis. As reported in 10-K filings, many firms in these industries saved hundreds of millions of dollars in costs or enjoyed other net gains through derivatives use during the course of a fiscal year. Their choice of instrument varies from forwards to futures and options as well as swaps. Companies that use these derivatives report their impact on pricing, output, supply chains, and other factors.

Considering the scale of the derivatives market, while the notional value (the value of the contracts’ underlying assets) of OTC derivatives amounted to $633 trillion (nine times global GDP) at year-end 2012, the gross market value (fair value or amount at risk) and gross credit exposure after netting (sum of positive and negative fair values across counterparties) were orders of magnitude less. This is relevant in assessing potential systemic risk under the new regulatory requirements and in making comparisons with traditional exchange-traded derivatives, which are often mistakenly viewed as dwarfed by OTC instruments.

AN EMPIRICAL FOUNDATION

In order to fully appreciate the study’s findings, it is important to understand how they were derived. The use of derivatives by banks and non-financial firms has an indirect impact on economic growth via various channels. To encompass that overall impact, the analysis is divided into two steps.

The first is estimating the influence of bank use on lending and the effects of non-financial firm use on firm value. The second step links those results to the macroeconomy. Although derivatives influence the U.S. economy in other ways, our quantitative assessment focuses especially on credit extension and firm value. Small and medium-sized enterprises rely on bank credit to expand capacity, and the nation’s economic health depends on the health of that sector.

%€Interest RatesForeign Exchange

Lending Support

Banks use derivatives contracts to hedge risk stemming primarily from the movements of interest rates and currency values. A stronger financial position promotes a higher volume of lending, which spurs the growth of industries across the economy.

3EXECUTIVE SUMMARY

Our statistical analysis demonstrates that banks’ derivatives use allows for a larger volume of commercial and industrial loans, holding other factors constant, increasing business investment. Additionally, it confirms that investors assign higher valuations to non-financial firms using derivative products, and those valuations boost their willingness and ability to expand operations.

In estimating the broad macroeconomic effect, we used two alternate approaches. One is based on a pure measure of statistical association which uses current and past values of variables in a system to determine their relationships. A key advantage is that a limited number of variables are necessary to perform the estimation. The second approach uses a structural model of the economy. This provides a separate estimate of the resulting changes in real GDP growth and includes further detail on investment, industrial production, employment, wages and incomes, and consumption, in addition to many other variables. Nevertheless, the approaches yield consistent results, warranting a high level of confidence.

This study examines the benefits of exchange-traded derivatives. The use of futures contracts has a positive association in all statistical formulations, suggesting that they help banks and non-financial firms manage risk, enabling banks to extend more loans and firms to invest more capital. Indeed, while the estimated relationships of the futures use variable do not pass conventional tests of significance, they make futures’ economic benefits clear to users, policymakers, and other stakeholders.

A Value Play

Our research shows that companies that use derivatives tend to have an edge in firm value over those that don’t. Further, this increase in firm value has a significant positive impact on overall economic growth.

4 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

DERIVATIVES: A MARKET MAINSTAY AMID GLOBALIZATION

Derivatives are financial instruments in the form of contracts, the value of which is derived from the value of an underlying asset. The trading of derivatives is done in two types of markets: organized exchanges and over the counter. An important feature of derivatives exchanges is the interposition of a clearinghouse that serves as a counterparty to reduce the default risk of parties engaged in the contract. Derivatives traded through the OTC market are privately negotiated and customized to the specifications of the counterparties involved.

Rudimentary exchange-based derivatives trading was recorded as early as the 1500s, but only recently have we seen a rapid increase in the creation of such exchanges around the world. While the major derivatives exchanges are located in mature economies (e.g., CME Group, Deutsche Borse AG, NYSE Euronext), the development of the global marketplace indicates expanding opportunities and demand in emerging economies. Based on turnover data (gross value of new deals during a given period), about two-thirds of derivatives are traded on exchanges in advanced countries, while they are traded almost equally on OTC and exchange markets in emerging economies.

Derivatives markets are populated by four main types of contracts: forwards, futures, options, and swaps. The general concepts are similar, with their value derived from the price of an underlying asset. Differences include some of the functions and features of the contracts as well as the markets where the various types of derivatives are traded. The largest derivatives market by notional amounts is swaps and the second-largest is forwards.

In recent decades, volatility in stocks and interest rates, along with the globalization of capital markets, has spurred demand for financial instruments to unbundle risks. From that perspective, interest rate derivatives are the most widely traded among global OTC derivatives, accounting for 77 percent of notional amounts outstanding in 2012. They first became popular in the late 1970s and early 1980s, when corporations were grappling with wide fluctuations in rates. Foreign exchange derivatives are the second-largest category. Rapid globalization has added exchange rate risk to the concerns of many businesses and investors.

One newer type of derivative used in risk mitigation is the credit default swap (CDS). This is a contract that allows the buyer to hedge the credit risk of debt securities contingent upon a credit event that befalls the issuer, such as a bankruptcy or payment default. Over the past 10 years, the CDS market grew at a tremendous pace, reflecting in part strong housing sales and the expansion of mortgage-backed securities prior to 2008. Although recognized as a useful hedging tool, credit default swaps have also come under a dark cloud for their misuse.

The U.S. Financial Crisis Inquiry Commission (FCIC) identified OTC derivatives—in particular, CDSs— as one of eight major factors that contributed to the financial crisis and subsequent Great Recession. One principal factor identified by the FCIC was the leverage—use of borrowed funds for making investments—that permeated the financial system. Many mistakenly assign disruptions caused by overleverage to the “D-word,” derivatives.

The absence of regulatory oversight played a considerable role in the buildup of the one-way protection writing position that AIG established in the CDS market, which was concentrated in insuring against default of mortgage-backed securities. If a clearing regime (posting of collateral based on daily marking to market)

5EXECUTIVE SUMMARY

had been implemented, AIG’s losses would not have been permitted to accumulate, and what became a financial crisis might have been much less damaging. In short, history might have been quite different.

WHY USE DERIVATIVES?

Investors generally use derivatives for three purposes: risk management, price discovery, and reduction of transaction costs. In a traditional banking model, a maturity mismatch between assets and liabilities subjects banks to interest rate risk. Derivatives mitigate this risk, which often contributes to capital adequacy, profitability, and lowering the probability of bank failure. In addition, banks make markets in derivatives to meet the risk management needs of financial and non-financial firm customers. In the process, they generate fees and other revenue from this trading as well as lower their cost of funding.

For non-financial firms, derivatives can assist in risk management associated with cash flow volatility arising from adverse changes in interest rates, exchange rates and commodity and equity prices. The tax code also offers incentives for hedging cash-flow volatility and income. A hedging strategy involving derivatives might alleviate underinvestment caused by insufficient cash flow and risk aversion.

The information that can be extracted from derivatives, such as price discovery, is another important benefit. In “complete” markets (when agents can buy insurance contracts to protect against any future state of the world), trading on derivative exchanges should reveal no new information to market participants. However, the lack of completeness means that informed traders could prefer to own futures or options in lieu of the

$1INCREASE

PER BARRELMILLION

$

INCREASE IN OPERATING COSTS

JET FUEL

A Lift for Airlines

Fuel is often a carrier’s largest operating expense, and a particularly volatile one as well. In 2011, United calculated that every $1 increase per barrel added $95 million in costs. Airlines use derivatives on similar fuels to hedge against adverse price shifts, which may allow them to increase their investment in physical capital, add flights, and prevent out-of-control costs from impacting consumers.

6 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

underlying assets, and this might reveal new information about price. Most studies done on developed nations show that the futures market leads the spot market and therefore serves as the focal point for price discovery.

Another positive identified with derivatives is reduced transaction costs through narrower bid-ask spreads. Spot markets with derivatives often have more liquidity and lower trading fees than markets without. If investors want exposure to the S&P 500, for instance, but wish to avoid the expense of purchasing all the underlying securities, they can trade index options and futures for the same result with less cost.

REGULATORY REFORM AND THE FUTURE

Derivatives’ outlook is veiled by regulatory changes taking place in the United States and other major markets. The Dodd-Frank Wall Street Reform and Consumer Protection Act (commonly known as Dodd-Frank) was signed into law in July 2010, five months before the release of the Financial Crisis Inquiry Report. It focused on addressing the lack of transparency as well as the absence of capital and collateral requirements in some derivatives markets, primarily OTC-related. Title VII of Dodd-Frank, also called the Wall Street Transparency and Accountability Act, granted the Commodity Futures Trading Commission (CFTC) and the Securities and Exchange Commission (SEC) authority to regulate swap derivatives. The SEC was designated to have specific authority over “security-based swaps.” Other titles under Dodd-Frank addressed broader issues of interconnectedness among firms and concentrations of risk in derivatives markets.

Whether Dodd-Frank’s remedies will succeed remains for history to judge. Many of the measures linked with changes to OTC derivatives and the requirement to use “swap execution facilities” have been put in place only recently. Even if the adjustment is less than smooth, the past suggests that derivatives will continue to play a pivotal role in economic and financial activities. Their continued contribution to economic growth will depend on the markets becoming more transparent and liquid, enabling end users to generate competitive returns while effectively hedging risk.

The authors hope that the results of this study will provide a more balanced view of these instruments and further their use in ways that promote economic expansion and contribute to overall financial stability.

9

IntroductionIn undertaking this research, the authors were aware that financial derivatives have been analyzed and discussed ad nauseam in recent years. Ironically, derivatives have been frequently maligned by those who confuse them with other financial instruments. This has not stopped derivatives from being erroneously portrayed as the creations of Ph.D.-trained financial engineer types, used by Wall Street bankers to entice investors seeking leverage as well as by businesses looking to enhance profits and/or reduce risk.

Derivatives, particularly over-the-counter (OTC) instruments, are blamed for any number of financial maladies, including the recent global financial crisis. They have been tagged with catchy phrases like “financial weapons of mass destruction” by none other than Warren Buffett. Nevertheless, Buffett’s Berkshire Hathaway has benefited substantially from the use of derivatives, by the company’s own admission.

This is not to say that there have been no problems with some types of derivatives. Most recently, credit default swaps (CDS) have come under scrutiny, as the history chapter in this study shows. However, the fact that derivatives have been with us for many centuries is a testament to the contribution they have made in promoting commerce and benefiting businesses of all forms and sizes. Direct benefits are manifest in risk mitigation, price discovery, and liquidity enhancement. Derivatives assist in completing markets,1 providing firms and individuals with financial flexibility as well as investment opportunity. By reducing risk they also reduce costs, which generally means that borrowing and lending (as illustrated in the home mortgage industry) can occur at lower expense than would otherwise be the case.

While the qualitative benefits of derivatives are well-known and taught in university finance programs, a tremendous amount of deep-seated skepticism remains. This study breaks new ground by rigorously quantifying, for the first time in a publicly available study, derivatives’ positive impact on economic growth. Primarily, we focus on their role in facilitating credit availability through banks. We also look at the effects derivatives have had on non-financial firms. That portion of the analysis offers broader insight into the use of various types of derivatives and their ability to enhance firm value.

Regarding the future, the transformed regulatory environment in the United States and other global financial centers poses the question of whether the evolving product mix and costs of derivatives will allow them to step up their contribution to economic growth. The emphasis on increased transparency and reduced counterparty risk, among other aims, should dampen fears of systemic risk that had been associated with unsupervised OTC derivatives activity. The authors hope that, in some small way, the results of this study will provide a more balanced view of these instruments and further their use in ways that promote economic expansion and contribute to overall financial stability.

1. In economics, a complete market (or complete system of markets) is one in which the complete set of possible gambles on future states-of-the-world can be constructed with existing assets without friction.

10 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

The paper proceeds as follows: Section 1 details the historical development and importance of derivatives and derivatives markets. Here, the authors demonstrate how these products have promoted commerce and highlight their evolution as the global financial system has expanded in scale and complexity.

Section 2 assesses the growth of the global derivatives market and all types of derivatives contracts. We discuss the varied features and distinctions among derivatives traded over the counter and on exchanges while highlighting emerging trends in the expansion of exchanges worldwide. Since the topic has received so much media attention, the analysis sheds light on public misunderstandings that stem from the varied ways of measuring derivatives’ value, the roles of derivatives and structured products during the global financial crisis, and the growth of these instruments in relation to other financial markets.

In Section 3, the authors look at the channels through which derivatives impact the real economy, focusing on risk management, price discovery, and transaction costs. Risk management is of critical importance, with financial exposure stemming from adverse changes in interest rates, foreign exchange rates, and commodity and equity prices. We address the way banks and non-financial firms mitigate risk through exchange-traded and OTC derivatives and how this remedy theoretically influences firm value and credit supply.

The main focus of this study lies in Section 4, where the authors empirically assess the impact of derivatives use by banks and non-financial firms on credit supply and firm value,2 respectively, and how these effects influence the real economy. Although other studies have assessed the impact on bank lending and firm value, none has extended the analysis to the effect on economic growth.

This assessment is divided into four parts. Parts 1 and 2 quantitatively estimate the relationships between, on the one hand, banks’ derivatives use and credit extension, and, on the other, non-financial firms’ derivatives use and firm value. Part 3 investigates the impact of firm value and bank lending on economic growth. Coupled with the estimates derived from Parts 1 and 2, it enables us to assess derivatives’ overall impact on the U.S. economy. Part 4 extends the analysis to the use of futures contracts and economic growth.

Section 5 concludes our study with an evaluation of the future of exchange-traded and OTC derivatives. Regulatory changes, along with accompanying administrative rules born of the financial crisis, will likely have a significant impact on the market structure of derivatives in the coming years. The focus on reducing systemic, and by extension counterparty, risk could result in a material migration from OTC markets to exchanges. However, the speed and degree of this adjustment is still to be determined and will depend inter alia on how rules concerning end users are interpreted and how they influence the costs of the instruments. This section highlights these and other major trends likely to emerge and offers perspective on how they might affect economic growth.

2. Firm value is defined in terms of the market-to-book value ratio.

Besides the rapid development of digital technology and its use in finance, the growth in OTC derivatives in the 1990s and early 2000s was spurred by a lax, perhaps at times controversial, regulatory environment.

13

The financial instruments we know as derivatives have played a vital role in economic activities dating back as far as Antiquity. From helping to secure the supply of commodities to facilitating trade and providing hedges against a variety of risks, derivatives use has evolved along with changes in commerce, the forms of financial assets, and their regulation. Trading activities and the platforms on which they take place also have undergone significant change, but with new regulation, instead of market preferences, sometimes leading to the transformation. In addition, technology has had a prominent role in the modern history of derivatives trading, particularly in facilitating access to these markets for non-financial businesses.

The first known use of derivatives dates to 2000 B.C., when merchants, in what is now called the Kingdom of Bahrain, engaged in consignment transactions for goods destined for India. A few hundred years later, the 48th law in the Code of Hammurabi established a contractual relation in the form of a put option.

Ancient Greece and Rome also played roles in the history of derivatives. According to the writings of Aristotle, around 580 B.C. a philosopher and mathematician named Thales purchased options on olive presses and made a fortune from an unusually large harvest by leasing out the presses at a substantial premium. In the Roman Empire for many years, laws did not recognize the transferability of contract rights and obligations, impeding derivatives use. However, commercial realities forced change, resulting in the use of contracts for future deliveries. Roman law would go so far as to enforce the intentions of contracting parties, even if they were speculative (Swan, 2000).

Derivatives continued to facilitate merchandise and commodities trade during the Middle Ages. Much of the activity at the height of the period took place in Italy, where merchants engaged in commerce spanning the Mediterranean Sea and beyond. A form of commodity forward contracts—known as Commandas—developed along with the bill of exchange. As commercial trade expanded, the exchange business grew. Professional money changers emerged, along with the trading of these bills.

As this activity multiplied, centralized markets for goods sprang up. An early version was the periodic fair, which was supervised by church institutions. Markets became specialized to respond to the trading needs of varied merchant groups. For their part, derivatives largely remained, in today’s terminology, “over the counter” but with the counters closely aligned with the individual markets. Periodic medieval markets lost their importance in trade over time, leading to permanent trading places located at the junction of port sites and land routes (Swan, 2000).

The exodus from the Middle Ages coincided with the spread of derivatives to other parts of Europe and as far as Japan. Around 1600, forward and options contracts on commodities, shipments, and securities were

1. History

14 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

traded in Amsterdam. This was followed a few decades later by forward contracting on tulip bulbs during the infamous Tulip Mania. A standardized futures contract for rice could be found in Osaka, Japan, around 1650, although it is not known whether the contracts were marked to market on a daily basis and/or had credit guarantees.

The early part of the 17th century saw the first recorded short-selling attack stemming from the abuse of options. The attack was directed at the Dutch East India Co., which was created as a joint stock company in the Netherlands in 1602. Participants in this early attack were successful, but subsequent similar efforts were less so, resulting in a number of bankruptcies. One of the outcomes of this episode was a ban on short selling in 1610, which apparently was not effectively enforced (Gelderblom and Jonker, 2009).

Although derivatives trading in a regulated exchange can be traced back to the 12th century, the first formal exchange for trading derivatives was the Royal Exchange in London, founded in 1565. The rise of England as a maritime power is one factor cited as supporting the development of derivatives trade in the country. In addition, English law recognized the transferability and negotiability of bills of exchange. Settlement was also facilitated through contracts for difference, in which a losing party could compensate the winning party for the difference between the delivery price and the spot price at the termination of the agreement.

The trading of derivatives in 18th century England also brought us the term “bubble.” When the South Sea joint stock company was established in 1711, its exclusive trade with Spain’s South American colonies was widely expected to generate enormous profits. This led to the formation of ancillary companies called bubbles. In 1720, the English Parliament passed the Bubble Act, prohibiting all joint stock companies not authorized by royal charter. The law triggered a wave of turmoil in financial markets, resulting in a crash (Swan, 2000). According to a subsequent investigation, the breakdown was attributed to those who dealt in options— mainly call options known as “refusals.” The legal consequences were that, after long debate, Parliament passed the Sir John Barnard’s Act, which banned options in shares as well as short selling (Weber, 2008).

1.1 INTEGRATION AND OVERSIGHT IN THE MODERN ERA

An ocean away and more than a century later, the first formal commodities exchange was established in the United States in 1848. In addition to tackling the problem of credit risk, the Chicago Board of Trade (CBOT) provided a centralized location to negotiate forward contracts. Under its aegis, the first exchange-traded derivatives contracts were listed in 1865, and in 1925 the first futures clearinghouse formed. In 2007, the CBOT merged with the Chicago Mercantile Exchange to become the CME Group.

The recent history of derivatives is characterized by their broad integration into commerce and finance, as evidenced by the creation of new products along with the platforms and tools for delivering them. Besides the rapid development of digital technology and its use in finance, the growth in OTC derivatives in the 1990s and early 2000s was spurred by a lax, perhaps at times controversial, regulatory environment. Derivatives also benefited from advances in finance at the academic level. In 1973, for instance, Fischer Black and Myron Scholes put forth their Nobel Prize-winning option pricing formula.

15HISTORY

The final decades of the 20th century witnessed new types of derivatives trading on currencies, bond and interest rate futures, as well as options on share indexes. The Chicago Mercantile Exchange created one of the first futures contracts that were not on physical commodities. The first currency futures were launched in 1970 at the International Commercial Exchange in New York while the Bretton Woods system was still in effect. Five years later, the interest rate futures contract based on Ginnie Mae mortgages was traded for the first time on the CBOT (Girish, 2010).

This was followed in 1977 by the U.S. Treasury bond futures contract, which became the highest-volume contract at the time. The flurry of activity continued with the creation of the Chicago Mercantile Exchange’s Eurodollar contract in 1982 and the first stock index futures contract by the Kansas City Board of Trade. The Chicago Mercantile Exchange quickly followed with its highly successful contract on the S&P 500 index.

While most derivatives were traded on exchanges up until this period, the 1980s marked the beginning of the era of swaps and other OTC derivatives. With a new generation of corporate financial managers well-versed in the use of derivatives, these instruments became essential for hedging, and in some cases speculating on, interest rate, exchange rate, and commodity risks. As corporations’ financial risks became more complex, so did the derivatives to deal with them. By 1991, the notional amount of OTC derivatives trading had surpassed that of exchange-traded derivatives (Whaley, 2006).

The rapid growth in OTC derivatives was fueled in part by the emergence of credit derivatives in the mid-1990s. The first CDSs were created by the J.P. Morgan investment bank (now JPMorgan Chase), which led the industry away from relationship banking toward credit trading. By engaging in such activities, bankers and others were striving for higher returns while shedding buy-and-hold risk.

Despite all the positives associated with derivatives in the 1990s, a number of high-profile incidents raised concerns among some regulators and others. In 1994, firms with deep financial experience such as Procter & Gamble and Metallgesellschaft suffered large losses on derivatives trading—primarily using swaps. Orange County, Calif., one of the wealthiest counties in the United States, declared bankruptcy, allegedly due to derivatives trading involving leveraged repurchase agreements. The following year, the United Kingdom’s Barings Bank declared bankruptcy because of speculation on futures by a rogue trader in its Singapore office (Chance, 1995).

These incidents did lead to minor changes in the way derivatives were sold, but for the most part firms were responsible for tightening controls internally. Following the 1998 collapse of Long-Term Capital Management (LTCM), a giant hedge fund, the Report of the President’s Working Group on Financial Markets recommended that the Securities and Exchange Commission (SEC), Commodity Futures Trading Commission (CFTC), and U.S. Treasury receive expanded authority. This would have required counterparties in OTC derivatives transactions to provide credit risk information and keep records on concentrations, trading strategies, and risk models. Federal Reserve Chairman Alan Greenspan declined to endorse these proposals but deferred to those regulators with supervisory authority, who took no discernible action.

16 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

On the heels of these events, 12 international banks formed the Counterparty Risk Management Policy Group (CRMPG) to examine the practices that brought about the LTCM crisis. Recommendations for self-regulatory practices were put forth to prevent a recurrence. There was mention of detailing certain large exposure information on a consolidated group basis. However, the major thrust of the CRMPG report was to oppose new regulation.

In late 2000, Congress passed and President Bill Clinton signed the Commodity Futures Modernization Act (CFMA), satisfying calls for deregulation amid market volatility. The law removed OTC derivatives transactions, including those related to energy, from all requirements of exchange trading and clearing under the Commodity Exchange Act (CEA) so long as counterparties to swaps were “eligible contract participants.” Except for issues related to fraud, the SEC was barred from OTC derivatives oversight. Moreover, the CFMA expressly preempted state gaming and anti-bucket shop laws, which would have barred the otherwise unregulated speculative activity granted under the act. In effect, almost no law applied to this market (Greenberger, 2010).

In the aftermath of the CFMA’s passage, derivatives growth skyrocketed. Although this boom was generally viewed as positive in helping to mitigate risk and enhance commerce, regulators and swap dealers themselves expressed reservations about operational shortcomings of OTC markets. In 2005, Timothy Geithner, then president of the Federal Reserve Bank of New York, assembled representatives of the world’s 14 largest banks to discuss his concern about substantial backlogs in the documentation of credit derivatives. He requested that banks clear up 80 percent of the backlog within a year and asked them to form a clearinghouse for complex derivatives contracts.

The CRMPG issued two reports, the first in July 2005, which aired clear concerns about the viability of the credit derivatives market. In particular, that report highlighted problems of identifying CDS counterparties because of poor documentation. The second report, released in July 2008, acknowledged difficulties with the credit derivatives settlement process and urged “swift action to create a clearinghouse for OTC derivatives, starting with CDS” (Greenberger, 2010).

For critics of OTC derivatives and credit derivatives in particular, the global financial crisis beginning in 2008 was seen as validating their views while presenting an opportunity to fundamentally alter the operational structure of derivatives markets through sweeping legislation. The facile labeling of these instruments as financial WMD added to the momentum for change. The final report of the National Commission on the Causes of the Financial and Economic Crisis in the United States took a more balanced view of derivatives’ role in the collapse. While acknowledging that OTC derivatives contributed “significantly to this crisis,” the report went on to point out that these instruments were but one of eight major factors involved.

The Dodd-Frank Wall Street Reform and Consumer Protection Act (commonly known as Dodd-Frank)—which was signed into law in July 2010, five months before the release of the Financial Crisis Inquiry Report—clearly reflected the overall negative political and public sentiment toward derivatives. Particular emphasis was placed on dealing with a lack of transparency and a buildup of losses on trading positions, as well as the absence of capital and collateral requirements in some derivatives markets, primarily OTC-related. Title VII of Dodd-Frank, also called the Wall Street Transparency and Accountability Act, granted the CFTC and SEC

17HISTORY

authority to regulate swap derivatives. The SEC was designated to have specific authority over “security-based swaps.” Other titles under Dodd-Frank addressed broader issues of interconnectedness among firms and concentrations of risk in derivatives markets.

Whether Dodd-Frank’s remedies, including a push toward cleared (listed) derivatives, will succeed remains to be seen. Many of the measures linked with changes to OTC derivatives and the requirement to use “swap execution facilities” have been put in place only recently. Even if the adjustment is less than smooth, the past suggests that derivatives will continue to play a pivotal role in economic and financial activities.

Given the expansion of international trade and financial activities, participants are likely to face increasing risks, and derivatives markets are expected to contribute to economic development by making these risks manageable.

19

2. Global Growth and Recent TrendsDerivatives are financial instruments in the form of contracts between two parties to engage in a transaction at a future time. The value of the contract is derived from the value of an underlying asset (e.g., equity, bond, or commodity) or market variable (e.g., interest rate, exchange rate, stock index, or credit risk). The notional amounts of a derivative contract refer to the principal value of the underlying asset.

Derivatives are traded in two types of markets: organized exchanges and over-the-counter (OTC). An important feature of derivatives exchanges is the interposition of a clearinghouse that serves as a counterparty to reduce the default risk of parties engaged in the contract. Exchange markets also trade standardized financial derivatives (e.g., futures and options contracts). Derivatives traded through the OTC market, on the other hand, are privately negotiated and customized to the specifications of the counterparties involved. OTC derivatives are executed bilaterally, and in most cases with derivatives dealers (such as global commercial and investment banks), who either find a counterparty or serve as a counterparty themselves. In contrast to past practice, Dodd-Frank requires with some exceptions that OTC derivatives be cleared by a derivatives clearing organization (DCO), and that the transactions trade on swap execution facilities (SEFs) or designated contract markets (DCMs) (see Part 5 for regulation of OTC derivatives under Dodd-Frank). European regulators and some Asian nations are taking a similar approach. However, it is unclear whether all of the G-20 will concur.

The four main types of derivatives contracts are forwards, futures, options, and swaps. The general concepts are similar, with their value derived from the price of an underlying asset. Differences include some of the functions and features of the contracts as well as the markets where the various types of derivative are traded.

Forwards and futures contracts are agreements between two parties to engage in a financial transaction at a specified price and quantity and at a future (forward) date. Forwards, however, are customized through negotiation. Since such contracts are bilaterally agreed upon and settled, the participants are exposed to counterparty risk.

A futures contract has several features designed to overcome this risk. Futures are traded on organized exchanges and represent a standardized agreement to deliver or receive a specific amount of a financial instrument at a specific price and date. Trading on organized exchanges enhances transparency as prices and other trade-related information are publicly displayed, while a central clearinghouse reduces counterparty credit risk. In part, this risk is mitigated because a clearinghouse requires contributions (in the form of collateral or margin) from their counterparties and collects mark-to-market collateral upon changes in the value of contracts. Most financial futures contracts in the United States are traded through the CME Group.

20 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

An option is a contract that grants owners the right but not the obligation to purchase (a call option) or sell (a put option) a financial instrument for a specific price within a defined time period. It functions by having the purchaser/owner pay the seller/writer an option premium for the right to buy or sell. The purchaser’s potential loss is limited to the price of the premium, curbing the downside. In contrast, the seller of an option receives the premium in return for risk exposure. Options are traded on organized exchanges and OTC derivatives markets, though standardized options are traded solely on organized exchanges.

A swap is a financial contract to exchange a set of payments one party owns for a set of payments owned by another party. The type most commonly traded is the interest-rate swap, which has increased in importance as financial institutions seek to manage interest-rate risk. Such transactions involve the exchange of one set of fixed-rate interest payments for a set of variable-rate interest payments. Similar to forwards, swaps are traded on the OTC market and subject to default/counterparty risk. However, all swaps not subject to enumerated exceptions are now required under Dodd-Frank to be cleared by a DCO and executed on an SEF. These reforms are aimed at reducing counterparty risk associated with bilaterally traded OTC derivatives, which policymakers and many commentators identified as a factor that magnified the global financial crisis in 2008 (see Box 1).

21GLOBAL GROWTH AND RECENT TRENDS

Financial derivatives are recognized as a useful tool for hedging risk. However, the collapse of American International Group Inc., followed by its $85-billion bailout in September 2008, illustrates that the misuse of financial instruments, along with an absence of regulatory oversight, can pose serious dangers for the financial system.

In the years leading up to the crisis, AIG had been active in the credit derivatives business, including trading (CDSs). The giant insurer’s CDS portfolio was written on complex collateralized debt obligations (CDOs) with underlying residential mortgage-backed securities (MBSs) whose asset pools included subprime loans. In this regard, AIG offered insurance in the form of CDSs to investors to protect against default or decline in MBS values, in exchange for a fee or premium.

AIG’s financial problems emerged after the U.S. residential market started to deteriorate in late 2006 and early 2007. Defaults by mortgage borrowers led to massive write-downs in AIG’s portfolio. The downgrades of AIG’s long-term debt by the major credit rating agencies, which triggered additional cash collateral obligations, led to a severe liquidity shortage at the company. Finally, the government stepped in and committed more than $180 billion to repair AIG’s liquidity situation amid fears that an abrupt collapse would trigger massive losses throughout the global financial system.

Accordingly, the U.S. Financial Crisis Inquiry Commission (FCIC) identified OTC derivatives as one of the eight major factors that contributed to the crisis. Its Final Report (2011, p. 50) notes that a “key OTC derivative in the financial crisis was the credit default swap.”

Some scholars and critics presented dissenting views on the role derivatives played as described by the FCIC. For example, Peery (2012, p. 21) points out that “members of the Crisis Commission… could not tell the difference between the derivatives that many companies

in the mainstream use every day to manage risk on the one hand, and derivatives that enabled big players like Lehman Brothers and American International Group Inc. (AIG) to pursue excessive risk taking, on the other hand.”

Regarding the distinction between the functions of derivatives and their misuse, Peter Wallison of the American Enterprise Institute (2011, pp. 5-6) argued:

“The only company known to have failed because of its CDS obligations was AIG (American International Group), and that firm appears to have been an outlier. Blaming CDS for the financial crisis because one company did not manage its risks properly is like blaming lending generally when a bank fails. Like everything else, derivatives can be misused, but there is no evidence that the ‘interconnections’ among financial institutions alleged have caused the crisis were significantly enhanced by CDS or derivatives generally.”

Nonetheless, the fact that AIG was not required to put aside adequate capital reserves and could take huge positions in the OTC derivatives market proved highly dangerous. According to René Stulz (2009, p. 64), “The AIG situation is unusual, however, because it was mostly a protection writer. Financial institutions more typically are both protection writers and protection buyers.”

In addition, several observers noted that if these OTC derivatives transactions had been cleared, the losses would have been much smaller and the massive bailout would have been less likely. This is because a clearinghouse requires the transacting parties to post initial margin (collateral) and make margin payments in response to changes in values of the contracts from daily mark-to-market. Therefore, in the case of AIG, the margin calls would have come sooner and been more frequent (see IMF, 2010, p.99. Also see Pirrong, 2011, for discussion on the economic function of central counterparties).

Credit derivatives, risk, and the 2007-2009 financial crisisB

OX 1

21GLOBAL GROWTH AND RECENT TRENDS

22 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

2.1 VOLATILITY AND TECHNOLOGY

The derivatives markets were small until the 1970s. Since then, their growth has been driven by both demand and supply factors. In the 1970s and ’80s, economic conditions such as rising volatility in stocks, interest rates, and exchange rates, along with the globalization of the capital markets, spurred demand for instruments to hedge risk. Supply factors, such as advancing technology and financial engineering, which aided the design of sophisticated derivatives, played an important role (in particular, the Black-Scholes [1973] formula to price options was widely acknowledged as an important factor).1

In the past two decades, the global derivatives markets have grown dramatically, despite experiencing a slowdown after the onset of the global financial crisis in 2008. The size of the market cited in the news media often refers to the notional amounts outstanding of contracts. Based on statistics from the Bank for International Settlements (BIS), the OTC derivatives market grew by a factor of eight, from $80 trillion to $633 trillion annually, between 1998 and 2012. The exchange-traded market expanded considerably as well over that period, from $14 trillion to $54 trillion, or about four times (Figure 1).

The global derivatives market (notional amounts outstanding)

FIG

UR

E

1

Source: Bank for International Settlements, June 2013.

$ trillions OTC derivatives

Exchange-traded derivatives

June 19

98

June 19

99

June 20

00

June 20

01

June 20

02

June 20

03

June 20

04

June 20

05

June 20

06

June 20

07

June 20

08

June 20

09

June 20

10

June 20

11

June 20

12

June 19

98

June 19

99

June 20

00

June 20

01

June 20

02

June 20

03

June 20

04

June 20

05

June 20

06

June 20

07

June 20

08

June 20

09

June 20

10

June 20

11

June 20

12

0

100

200

300

400

500

600

700

800

$ trillions

0102030405060

8090

70

100

1. According to Merton (1998), “The most influential development in terms of impact on finance practice was the Black-Scholes model for option pricing... This success in turn increased the speed of adoption for quantitative financial models to help value options and assess risk exposures” (pp. 323-324).

23GLOBAL GROWTH AND RECENT TRENDS

Among the four types of derivatives, swaps are the largest market by notional amount. The second-largest is forwards (see Figure 2). Both swaps and forwards are traded on OTC markets, while futures and standardized options are traded on organized exchanges. As discussed in detail in Part 2.4, simply comparing notional amounts outstanding between exchanges and OTC derivatives markets can be misleading. For instance, an offsetting OTC trade actually adds to the notional amount outstanding, while offsetting exchange-traded transactions are netted out. In other words, OTC trading data captures gross positions, while exchange data represents net positions. Therefore, the growth of derivative types as presented in Figure 2 should be compared within the markets where the instruments are traded.

Notional amounts, by instrument

FIG

UR

E

2

Note: Unallocated excluded.

Source: Bank for International Settlements, June 2013.

$ trillions

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

0

100

200

300

400

500

600

700

800

Future (exch tr)

Options (exch tr)

Options (OTC)

Swaps (OTC)

Forwards (OTC)*

Credit derivatives (OTC)

Unallocated

* Includes forex swaps, equity-linked swaps, and commodity swaps. The amounts outstanding for these categories are small and BIS reports their data with forwards. Equity-linked forwards and swaps combined is 0.3% and commodity forwards and swaps is 0.3% of total contracts.

The development of derivatives can also be presented in terms of the risk category of the underlying assets (i.e., interest rate, foreign exchange, equity-linked, commodity, and credit derivatives), in addition to type of instrument (i.e., forwards, futures, options, and swaps) and market (i.e., exchange-traded and OTC). Appendix 1 provides data by market, risk category, and instrument.2

In terms of risk category of the underlying assets, interest rate derivatives are the most widely traded, accounting for about 77 percent of notional amounts outstanding of global OTC derivatives in 2012 (see Figure 3). They became popular in the late 1970s and early 1980s, when corporations were grappling with wide rate fluctuations and sought financial instruments to reduce the associated risk. Although some manufacturers were affected by rate movements, financial institutions, whose profit comes primarily from interest-sensitive liabilities, were even more exposed. They became the primary users of interest rate swaps, now the most commonly traded type of interest rate derivative.

2. Categorization based on Bank for International Settlements methodology.

24 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

OTC derivatives by risk categoryF

IGU

RE

3

Source: BIS, Milken Institute.

1998

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Unallocated CDS CommodityEquity-linked Foreign exchange Interest rate

OTC derivatives:$633 trillion (2012)

UnallocatedCDS

Commodity <1%Equity-linked 1%Foreign exchange

Interest rate

77%

7%4%

11%

Foreign exchange derivatives, at 11 percent of the notional amount of the global OTC total, are the second-largest category, much smaller than interest rate derivatives. In recent decades, foreign financial markets have become more accessible and international trade more open as technology reduced costs associated with cross-border transactions. The trend increases demand for foreign exchange derivatives to hedge currency risk, as global banks, institutional investors, and multinational corporations increase their exposure to exchange rate risk. The foreign exchange derivatives market expanded from the notional amount of $18 trillion in 1998 to $67 trillion in 2012. Activity in equity-linked and commodity derivatives is relatively small, with each accounting for about 1 percent of the broader market.

Credit derivatives are a new type, with the credit default swap its predominant form. This is a contract that allows the buyer to hedge the credit risk of debt securities contingent upon a credit event that befalls the issuer, such as a bankruptcy or payment default. With a CDS, a protection buyer makes periodic payments to a protection seller. Until the credit event occurs, the protection seller benefits from the premium payments it receives over the life of the CDS contract. If a credit event does occur, the seller is obligated to compensate the buyer equal to the price of debt securities specified in the contract.3 Most reference entities (debt issuers) are corporations, and the primary sellers and buyers of credit default swaps include globally active financial institutions.

3. Compensation upon settlement is discussed, for example, in Rajan (2007). The amount the protection seller has to pay the buyer depends on the type of settlements, including the treatment of recovery.

25GLOBAL GROWTH AND RECENT TRENDS

Over the past 10 years, the CDS market has grown at an astounding pace. The notional amount outstanding reached its peak of $58 trillion at year-end 2007, twice the size of a year earlier and a multiple of nine since 2004, according to BIS statistics. However, when compared to some other types of derivatives, the CDS market is small. The category has accounted for 3 percent to 5 percent of the total notional amount of OTC derivatives, except for a few years leading up to the financial crisis, when they jumped to 7 percent to 10 percent (see Figure 3).

One reason for CDS’ rapid growth was the heated activity in the housing market and the expansion of mortgage-backed securities. Many financial institutions that invested in mortgage-backed securities purchased CDS contracts to protect against default (see Box 1 on credit derivatives and the financial crisis). The CDS market declined amid the financial crisis and has not recovered to previous levels.

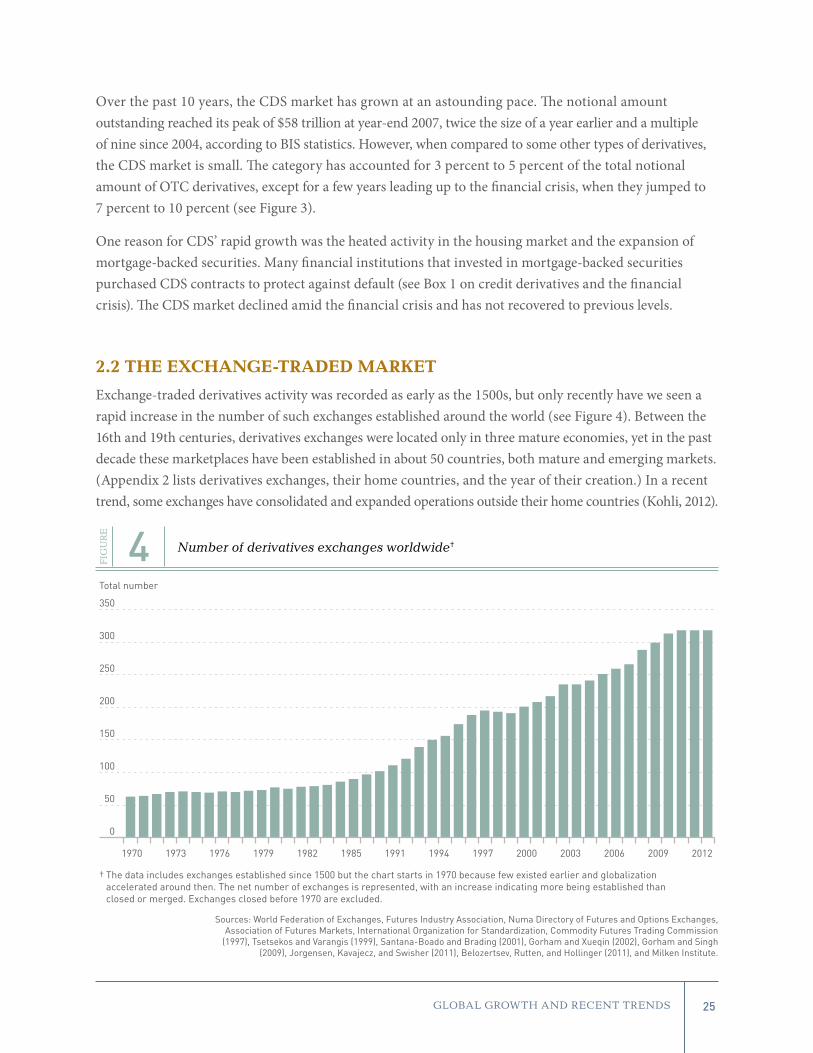

2.2 THE EXCHANGE-TRADED MARKET

Exchange-traded derivatives activity was recorded as early as the 1500s, but only recently have we seen a rapid increase in the number of such exchanges established around the world (see Figure 4). Between the 16th and 19th centuries, derivatives exchanges were located only in three mature economies, yet in the past decade these marketplaces have been established in about 50 countries, both mature and emerging markets. (Appendix 2 lists derivatives exchanges, their home countries, and the year of their creation.) In a recent trend, some exchanges have consolidated and expanded operations outside their home countries (Kohli, 2012).

Number of derivatives exchanges worldwide†

FIG

UR

E

4

Sources: World Federation of Exchanges, Futures Industry Association, Numa Directory of Futures and Options Exchanges, Association of Futures Markets, International Organization for Standardization, Commodity Futures Trading Commission

(1997), Tsetsekos and Varangis (1999), Santana-Boado and Brading (2001), Gorham and Xueqin (2002), Gorham and Singh (2009), Jorgensen, Kavajecz, and Swisher (2011), Belozertsev, Rutten, and Hollinger (2011), and Milken Institute.

0

50

1970 1973 1976 1979 1982 1985 1991 1994 1997 2000 2003 2006 2009 2012

100

150

200

250

300

350

Total number

The data includes exchanges established since 1500 but the chart starts in 1970 because few existed earlier and globalization accelerated around then. The net number of exchanges is represented, with an increase indicating more being established than closed or merged. Exchanges closed before 1970 are excluded.

†

26 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

Derivatives exchanges trade standardized contracts. Since the exchanges record transactions, activity can be tracked in a straightforward manner. The Futures Industry Association (FIA) and World Federation of Exchanges (WFE) collect futures and options trading information on their member exchanges.4 Their published surveys report the activity of listed derivatives in terms of trading volume (the number of contracts traded) and open interest (the number of contracts entered into but not fulfilled by delivery). Last year, 21.2 billion derivatives contracts were traded on organized exchanges worldwide, close to triple the volume a decade ago.5 The peak was reached in 2011, when more than 25 billion contracts were traded. Trading volume, reflecting the quantity of demand, is usually used as a measure of growth for exchanges. Those with higher volume are often recognized as being successful in offering properly designed contracts.

Regarding geographic distribution, Europe and North America dominate the exchange-traded derivatives market as measured by notional turnover and open interest—together holding more than 90 percent. Exchanges in the Asia-Pacific region account for a larger proportion of trading volume (see Figure 5) than notional amounts. These distributions, based on different units of measurement, reflect the smaller contracts traded on Asia-Pacific exchanges.

Derivatives traded on organized exchanges (2012), by region

FIG

UR

E

5

Sources: Data for the number of contracts traded and open interest is from the World Federation of Exchanges. Data for notional amounts outstanding is from BIS.

Americas EAME (Europe, Africa, Middle East) Asia Pacific

42%

22%

36%

Number of contracts traded 21.2 billion

29%

8%

63%

Open interest640 million contracts

52%

43%

5%

Notional amounts outstanding$54.4 trillion

4. Appendix 3 provides data sources for global derivatives activity.5. In 2003, the volume was 8.1 billion, according to the FIA’s annual survey. BIS also publishes the number of contracts outstanding and turnover of

exchange-traded derivatives.

27GLOBAL GROWTH AND RECENT TRENDS

Although the major derivatives exchanges are located in mature economies (e.g., CME Group, Deutsche Börse AG, ICE/NYSE), demand for such products is rising in emerging economies. Derivatives exchanges in Brazil, China, India, South Korea, and Russia have shown remarkable growth and are now ranked among the top tier (see Appendix 4). Many exchanges also pursue aggressive strategies to attract foreign trading firms through a combination of infrastructure and product development. Given the expansion of international trade and financial activities, participants are likely to face increasing risks, and derivatives markets are expected to contribute to economic development by making these risks manageable. (Parts 3 and 4 of this study examine the relationship between derivatives and economic performance for U.S. banks and non-financial firms.)

2.3 THE OTC MARKET

OTC derivatives are privately negotiated and traded between two parties without intermediation through an exchange (although OTC transactions may be cleared by a clearinghouse). Information on the trading of these individual contracts is held by dealers, who are either buyers or sellers of contracts. BIS and the International Swaps and Derivatives Association (ISDA) regularly survey global derivatives dealers and publish the results. Both surveys report notional amounts outstanding, reflecting the scale and growth of activity.

The notional amount outstanding, which stood at $633 trillion at the end of 2012, according to BIS, have drawn a great deal of attention and concern regarding possible risks tied to their scale. By this measure, the derivatives market is approximately 10 times larger than world GDP and several times larger than other global financial sectors. However, notional amounts outstanding, though a rough measure of derivatives activity, do not represent the actual amount exchanged in a transaction or, generally, the amount at risk (ISDA, 2008; OCC, 2012). The sums more closely related to the risks are gross market value and gross credit exposure (see Box 2 for definitions). As of 2012, their values are $25 trillion and $3.6 trillion, respectively, according to BIS statistics. In 1998, gross market value was $3 trillion (see Figure 6).

Growth of the global OTC derivatives market (by gross market value)

FIG

UR

E

6

Source: BIS, June 2013.

$ trillions

0

5

10

15

20

25

30

35

Jun. 1

998

Dec. 19

98

Jun. 1

999

Dec. 19

99

Jun. 2

000

Dec. 20

00

Jun. 2

001

Dec. 20

01

Jun. 2

002

Dec. 20

02

Jun. 2

003

Dec. 20

03

Jun. 2

004

Dec. 20

04

Jun. 2

005

Dec. 20

05

Jun. 2

006

Dec. 20

06

Jun. 2

007

Dec. 20

07

Jun. 2

008

Dec. 20

08

Jun. 2

009

Dec. 20

09

Jun. 2

010

Dec. 20

10

Jun. 2

011

Dec. 20

11

Jun. 2

012

Dec. 20

12

28 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

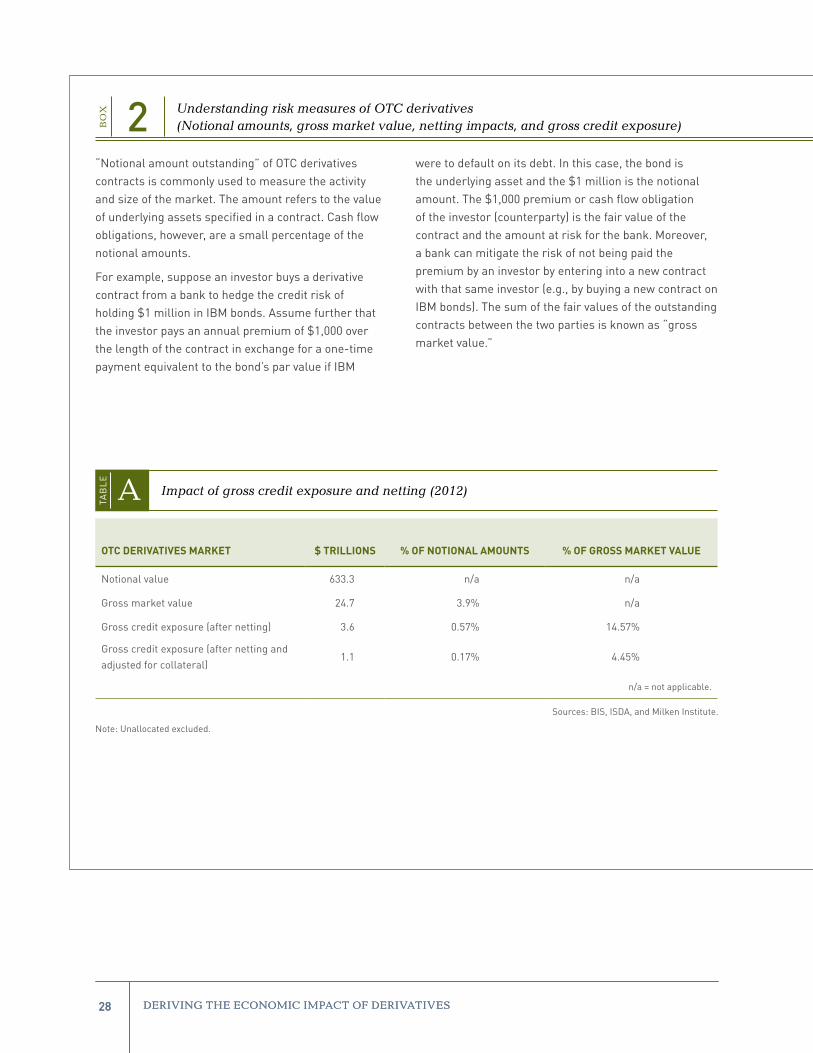

“Notional amount outstanding” of OTC derivatives contracts is commonly used to measure the activity and size of the market. The amount refers to the value of underlying assets specified in a contract. Cash flow obligations, however, are a small percentage of the notional amounts.

For example, suppose an investor buys a derivative contract from a bank to hedge the credit risk of holding $1 million in IBM bonds. Assume further that the investor pays an annual premium of $1,000 over the length of the contract in exchange for a one-time payment equivalent to the bond’s par value if IBM

were to default on its debt. In this case, the bond is the underlying asset and the $1 million is the notional amount. The $1,000 premium or cash flow obligation of the investor (counterparty) is the fair value of the contract and the amount at risk for the bank. Moreover, a bank can mitigate the risk of not being paid the premium by an investor by entering into a new contract with that same investor (e.g., by buying a new contract on IBM bonds). The sum of the fair values of the outstanding contracts between the two parties is known as “gross market value.”

Understanding risk measures of OTC derivatives(Notional amounts, gross market value, netting impacts, and gross credit exposure)B

OX 2

28 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

OTC DERIVATIVES MARKET $ TRILLIONS % OF NOTIONAL AMOUNTS % OF GROSS MARKET VALUE

Notional value 633.3 n/a n/a

Gross market value 24.7 3.9% n/a

Gross credit exposure (after netting) 3.6 0.57% 14.57%

Gross credit exposure (after netting and adjusted for collateral)

1.1 0.17% 4.45%

n/a = not applicable.

Sources: BIS, ISDA, and Milken Institute.

Note: Unallocated excluded.

Impact of gross credit exposure and netting (2012)ATAB

LE

29GLOBAL GROWTH AND RECENT TRENDS

BIS reports the gross market value of global OTC derivatives contracts along with the notional amount. In 2012, gross market value was $24.7 trillion, or 3.9 percent of the notional amount of $633 trillion.

In the United States, banks can benefit from netting and posting collateral from a master netting agreement in accordance with U.S. generally accepted accounting principles. Based on the IBM example, the bank has a positive fair value from the first contract and a negative fair value in the second contract. These cash flows can be netted out according to legally enforceable bilateral netting agreements. The sum of positive and negative fair values between the counterparties (i.e., the bank and the investor) after bilateral netting is known as “gross credit exposure.”

According to the ISDA, the gross credit exposure of global derivatives was $3.6 trillion, or 0.57 percent of the notional amount outstanding, in 2012 (see Figure A). Collateralization further reduces counterparty risk exposure. The benefits of netting and collateral posted further reduce credit exposure to 0.17 percent of the notional amount and 4.45 percent of the gross market value (see Table A).

Gross market value and gross credit exposure are considered more closely related to risk than the notional amount of derivatives (ISDA, 2008).

29GLOBAL GROWTH AND RECENT TRENDS

Sources: BIS, ISDA, and Milken Institute.

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

$ trillions

0

10

20

30

40

Gross market value

Gross credit exposure

Benefits of netting

Impact of netting and gross credit exposure, OTC marketA

FIG

UR

E

30 DERIVING THE ECONOMIC IMPACT OF DERIVATIVES

Studies also point out that the gross market value of derivatives is a more appropriate measure than notional amounts in comparing the size of the market with that of other financial sectors (and world GDP). As noted by Markose (2012, p. 6), “The gross market value gives an estimate of the economic risk in derivatives arising from the volatility of underlying reference/asset prices, leverage and hedge ratios, duration, liquidity, and counterparty risk.”

Figure 7 shows this comparison. Based on market value, the size of the OTC derivatives market appears smaller than other markets, although OTC derivatives activity has burgeoned in recent decades (see Figure 1). The size of the global bond market (both private and public) was $84 trillion, which made it the largest market, more than three times the scale of OTC derivatives as of 2012. The global stock market is double the size of the OTC derivatives market.

Size of global financial markets ($ trillions), by type

FIG

UR

E

7

Note: The size of the global bond market is based on total debt outstanding, global stock market is based on capitalization, and global OTC derivatives market on gross market value. All data is in the nominal term as of 2012. GDP is based on the IMF estimate.

Sources: BIS, Bloomberg, World Bank, and Milken Institute.

Bond

GDP

Stock

OTC derivatives(gross market value)

2012 1998

8730

7230

52

27

253

2.4 DIFFERENT ENVIRONMENTS, DIFFERENT STRENGTHS

Trading derivatives through organized exchanges is recognized as more transparent. Exchanges typically offer pre-trade price discovery. Furthermore, exchanges also distribute transaction prices, bids/offers, and other trading information in real time. With such information available to all market participants as well as regulators, trading on exchanges provides a high level of transparency. Information on bilateral OTC transactions, on the other hand, is opaque to outside parties.

Exchanges also use a central counterparty (CCP) to clear and settle trades. Clearinghouses also serve as counterparties and set and enforce margin requirements. They are obliged to honor the trade in the event of a party’s default; therefore, they reduce counterparty risk. In a traditional bilateral OTC transaction, the counterparties bear the risk of default by each. In the aftermath of the global financial crisis, some G-20 countries called for certain OTC derivatives to be cleared via CCPs as a way to reduce counterparty credit risk. (The risk can become systemic because losses from defaults can spread to

31GLOBAL GROWTH AND RECENT TRENDS

parties who entered into contracts with the counterparties of the defaulted contracts). Therefore, both exchange-traded and cleared OTC derivatives benefit from credit protections through the clearing and settling services provided by clearinghouses.

Nevertheless, the swift growth of the OTC derivatives market in the past reflects some of its advantages. For example, participants can trade customized, complex, or illiquid products. This ability to design deals makes OTC contracts suitable for corporations that seek to completely hedge the risk tied to specific assets in their portfolios.

In regard to the size of the two markets, it should be noted that the notional amounts outstanding for OTC derivatives are not comparable with those of exchange-traded derivatives in terms of exposure. Consider a generic example from an ISDA study (Pirrong, 2011, p. 7):

“A may sell a contract; B may buy an identical contract and then sell it; and C may buy this contract. In a bilateral OTC market, B’s offsetting positions remain open, and one (or even in some circumstances both) of its counterparties on these contract could lose from its default. In contrast, if all of these contracts are cleared through a CCP, B’s contract would be netted out and B’s contractual obligations would be extinguished. If B went bankrupt, neither A nor C could suffer a default loss (as long as the CCP remains solvent).”

In the OTC market, traders may enter into a new transaction to hedge out a previous one. In terms of recorded transactions, the notional amount of the new contract will be accumulated to past transactions, even though the net exposure is reduced. In this example, the total notional amounts of B’s two contracts with identical notional amounts will be counted double although their net risk is zero.

For exchange-traded derivatives, the existing contract is netted out by a CCP who takes the opposite position in the same contract for each trader. That leaves the notional amounts outstanding the same or smaller, and counterparty risk is extinguished. The positive net positions are then summed across traders. As noted by Kleist (2012, p. 48), “For exchange-traded contracts, it is perfectly reasonable to net in this way because, unlike OTC contracts, exchange-traded contracts have standardized size and settlement dates and the same counterparty, i.e., the [clearinghouse].”

To compare derivatives activity between OTC and exchange markets, turnover data is considered a more appropriate measure than notional amounts. Turnover is defined as the gross value of new deals during a given period and measured in terms of the nominal or notional amount of contracts. BIS’ Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity includes this data. A BIS study shows that when gauging derivatives activity based on turnover data, exchanges are two-thirds larger than OTC markets for a sample of advanced countries, while derivatives are traded in similar proportions in both markets for emerging countries (Mihaljek and Packer, 2010). However, using notional amounts outstanding, OTC derivatives were several times larger than those traded on exchanges—$633 trillion versus $54 trillion.

Most previous studies done on developed nations show that the futures market leads the spot market and therefore serves as the focal point for price discovery.

33

3. Risk, Price, and CostThis section examines the functions of derivatives and the costs and benefits associated with them. Our framework is meant to improve understanding of the reasons derivatives contracts are widely and increasingly used in financial markets. We focus on three major functions of derivatives: risk management, price discovery, and reducing transaction costs.

Their use impacts the overall economy, affecting firm value, investment opportunities, and credit availability. These effects will be assessed empirically in Part 4 of this study.

3.1 MANAGING RISK

Corporations are important players in derivatives markets. Non-financial firms typically use them to hedge market risk. Banks, while taking positions in derivatives to mitigate their own risk exposure, also make markets in these instruments to meet the risk management needs of their corporate customers. In return, they generate fee and other revenue from this trading and lower their cost of funding. We discuss how banks and non-financial firms use derivatives for risk management purposes in turn.