Embed Size (px)

Citation preview

Department of Education Internal Audit COMMUNITY SCHOOL FOR ADULTS CONSOLIDATED REVIEW REPORT FISCAL YEAR ENDED JUNE 30, 2012 ISSUE DATE: DECEMBER 27, 2012

CONFIDENTIAL This report is prepared solely for the internal use of the Board of Education and management of the Department of Education. Distribution requires prior approval from the Board or management.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

1

TABLE OF CONTENTS

I. EXECUTIVE SUMMARY Page

Summary 3 Background 3 Scope and Objectives 3-4

II. OBSERVATIONS AND RECOMMENDATIONS

Summary of Findings and Recommendations: General Observation 6 Non-Appropriated Local School Funds 7-12 Appropriated Funds Accounts 13-18 Accounting for Tuition Fees 19-21 Leave Accounting Records 22-23 Casual Hire Payroll Verification 24-25 Inventory Records 26

2

I. EXECUTIVE SUMMARY

Community School for Adults State of Hawaii

Department of Education June 30, 2012

3

SUMMARY

Internal Audit (IA) performed agreed upon procedures for six (6) of the 11 Community School for Adults to review the Non-Appropriated Local School Fund and Appropriated Federal and State Funds held in the Financial Management System (FMS) for school year 2011 – 2012 to determine its compliance with the Department of Education (DOE) policies and procedures. In addition, IA completed questionnaires with the remaining five (5) schools regarding the schools compliance with DOE’s policies and procedures.

BACKGROUND

Prior to July 2012, there were 11 Community School for Adults. Due to budget cuts, it was decided that the 11 community schools would transition to a two (2) administrative center structure. As part of the transition, Superintendent Kathryn S. Matayoshi requested IA to perform a limited review to provide a cut off point for the 11 school system. Each school receives appropriated cash collections for tuition fees, enrollment fees, General Educational Development (GED) testing, English as a Second Language (ESL) appraisal fees, and transcripts, which are deposited into the DOE’s central bank checking account. In addition, various schools receive non-appropriated cash collections for snack sales, donations, and graduation fees. These cash collections are deposited into the respective school’s non-appropriated local school bank checking account held outside the State Treasury. All of the community schools use the LACESTM system for student registration. The LACESTM system is a comprehensive program management system, providing educational and social services agencies with a framework for program and participant management and evaluation. LACESTM provides tools to track detailed personal data for all participants. This includes demographic, contact/address, residence, employment history, assessments, goals, hours, and comments for staff, classes, and students.

SCOPE AND OBJECTIVES

The agreed upon procedures for the six (6) schools for the year ended June 30, 2012 was conducted to determine the schools compliance with the DOE’s FMS User Guide and other DOE policies and procedures, with respect to the schools’ Non-Appropriated Local School Fund (LSF), appropriated funds accounts, accounting for tuition fees, leave accounting records, casual hire payroll verification, and inventory records. To gain an understanding of all 11 schools’ procedures in processing financial transactions and documenting the internal controls related to those procedures, IA interviewed appropriate personnel, reviewed the requirements of the DOE’s FMS User Guide and other DOE policies and procedures, and documented personnels’ understanding of the established accounting procedures and internal controls in place during the engagement period.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

4

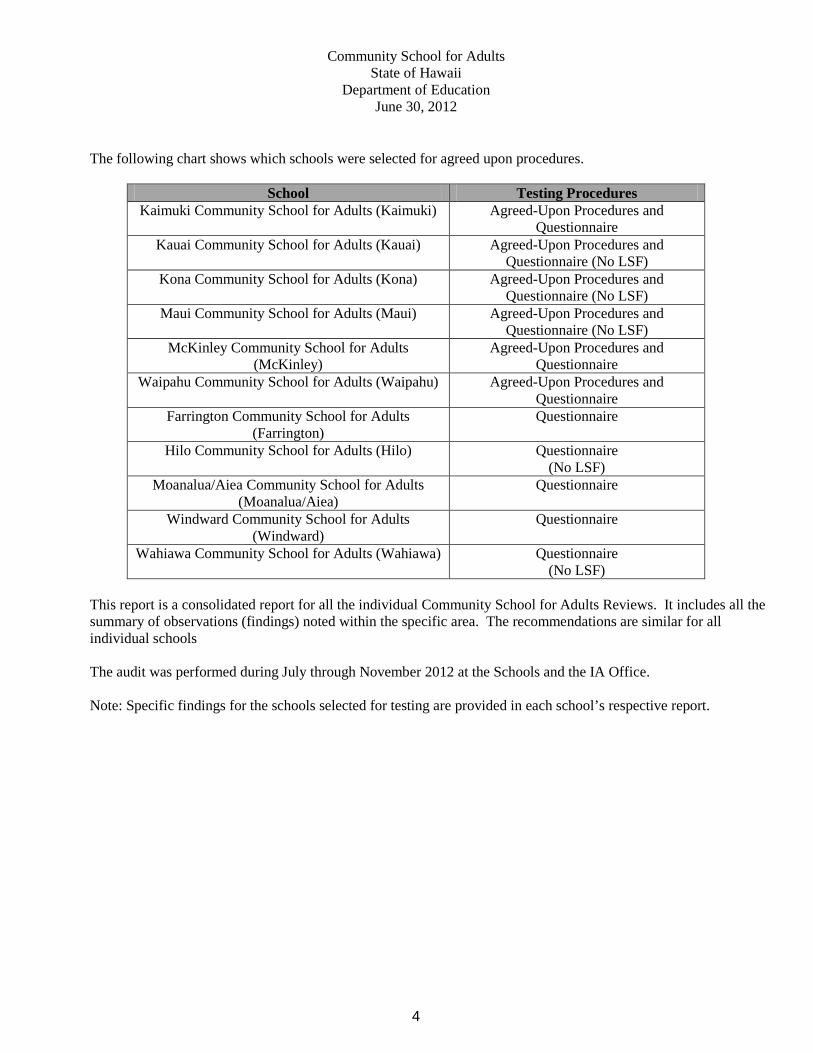

The following chart shows which schools were selected for agreed upon procedures.

School Testing Procedures Kaimuki Community School for Adults (Kaimuki) Agreed-Upon Procedures and

Questionnaire Kauai Community School for Adults (Kauai) Agreed-Upon Procedures and

Questionnaire (No LSF) Kona Community School for Adults (Kona) Agreed-Upon Procedures and

Questionnaire (No LSF) Maui Community School for Adults (Maui) Agreed-Upon Procedures and

Questionnaire (No LSF) McKinley Community School for Adults

(McKinley) Agreed-Upon Procedures and

Questionnaire Waipahu Community School for Adults (Waipahu) Agreed-Upon Procedures and

Questionnaire Farrington Community School for Adults

(Farrington) Questionnaire

Hilo Community School for Adults (Hilo) Questionnaire (No LSF)

Moanalua/Aiea Community School for Adults (Moanalua/Aiea)

Questionnaire

Windward Community School for Adults (Windward)

Questionnaire

Wahiawa Community School for Adults (Wahiawa) Questionnaire (No LSF)

This report is a consolidated report for all the individual Community School for Adults Reviews. It includes all the summary of observations (findings) noted within the specific area. The recommendations are similar for all individual schools The audit was performed during July through November 2012 at the Schools and the IA Office.

Note: Specific findings for the schools selected for testing are provided in each school’s respective report.

5

II. OBSERVATIONS AND RECOMMENDATIONS

Community School for Adults State of Hawaii

Department of Education June 30, 2012

6

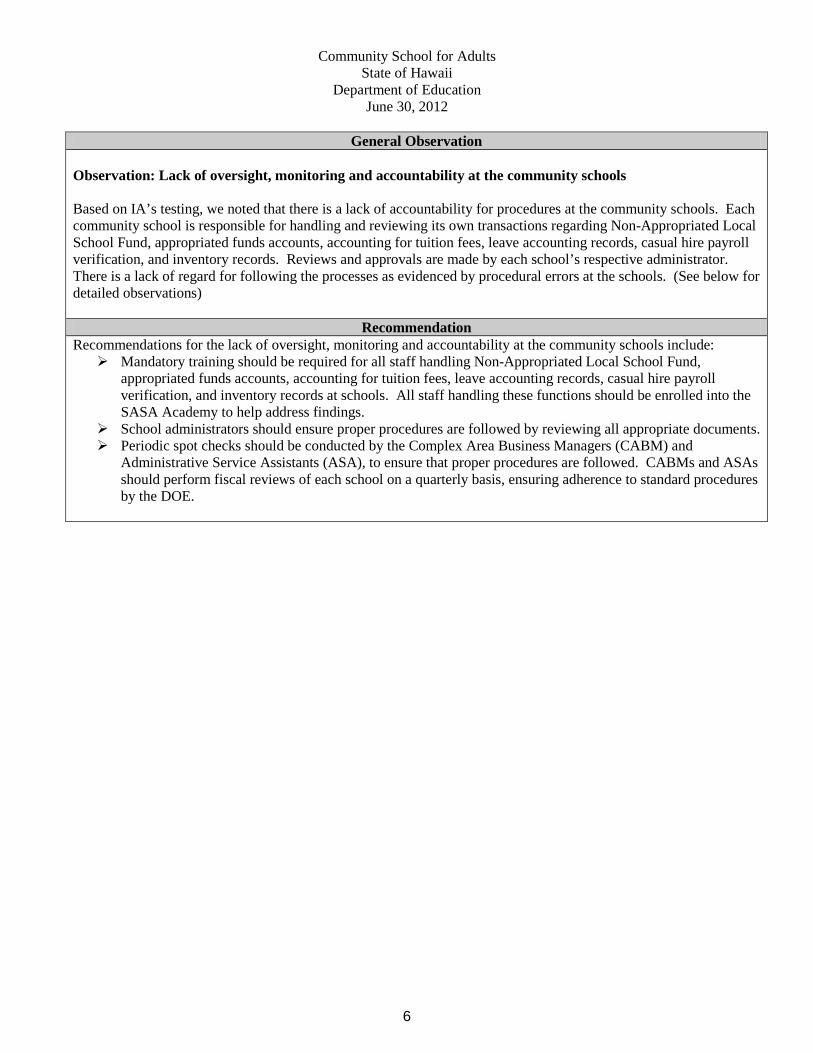

General Observation Observation: Lack of oversight, monitoring and accountability at the community schools Based on IA’s testing, we noted that there is a lack of accountability for procedures at the community schools. Each community school is responsible for handling and reviewing its own transactions regarding Non-Appropriated Local School Fund, appropriated funds accounts, accounting for tuition fees, leave accounting records, casual hire payroll verification, and inventory records. Reviews and approvals are made by each school’s respective administrator. There is a lack of regard for following the processes as evidenced by procedural errors at the schools. (See below for detailed observations)

Recommendation Recommendations for the lack of oversight, monitoring and accountability at the community schools include: Mandatory training should be required for all staff handling Non-Appropriated Local School Fund,

appropriated funds accounts, accounting for tuition fees, leave accounting records, casual hire payroll verification, and inventory records at schools. All staff handling these functions should be enrolled into the SASA Academy to help address findings.

School administrators should ensure proper procedures are followed by reviewing all appropriate documents. Periodic spot checks should be conducted by the Complex Area Business Managers (CABM) and

Administrative Service Assistants (ASA), to ensure that proper procedures are followed. CABMs and ASAs should perform fiscal reviews of each school on a quarterly basis, ensuring adherence to standard procedures by the DOE.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

7

Observations for Non-Appropriated Local School Funds Observation: Non-Appropriated Local School Funds procedures were not always followed at the schools Schools are required to follow the DOE’s FMS User Guide and other DOE policies and procedures for the local school fund transactions. IA noted that five (5) of the 11 schools did not have local school funds: Wahiawa, Hilo, Kona, Maui, and Kauai. The following table summarizes the observations of non-compliance noted during our review indicating that procedures were not always followed. Further detail on each of the procedures is provided in the Reference column.

Reference(s) Summary of Observations Noted Questionnaire Chapter 1 of the FMS User Guide states

that School administrative offices, District offices, and State offices use FMS to perform their daily tasks related to purchasing and accounting. The FMS User Guide should be used to assist the schools with FMS related tasks.

Chapter 7 of the FMS User Guide states that all pre-numbered forms are recorded and accounted for on a log “Inventory Record of Pre-numbered Forms,” Form No. 439 and secured so that they are inaccessible to unauthorized personnel.

Chapter 9 of the FMS User Guide states that the Principal should indicate that review of the bank reconciliation has been performed by signing or initialing and dating the bank statement.

Chapter 9 of the FMS User Guide states that the signatory card must be updated whenever there is a change in personnel listed on the signatory card.

Chapter 9 of the FMS User Guide states

that the deposit slip and check should be imprinted with the identity to the Non-Appropriated Local School Fund with school name and address.

One (1) out of 11 schools did not keep the FMS User Guide on file.

Three (3) out of 11 schools did not maintain an Inventory Record of Pre-Numbered Forms, Form 439 for all pre-numbered forms.

Two (2) out of 11 schools did not keep the official pre-numbered receipts, Form 239, “WIZ receipt” and the Inventory Record of Pre-numbered Forms, Form 439 in a secured place so that they are inaccessible to unauthorized personnel.

Three (3) of the six (6) LSF schools stated

that bank statements were not signed/dated by the Principal.

One (1) of the six (6) LSF schools did not

update bank account signatory cards on a timely basis for changes in authorized signers.

One (1) of the six (6) LSF schools did not

have an imprint of “Non-Appropriated Local School Fund” on the deposit slips and checks.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

8

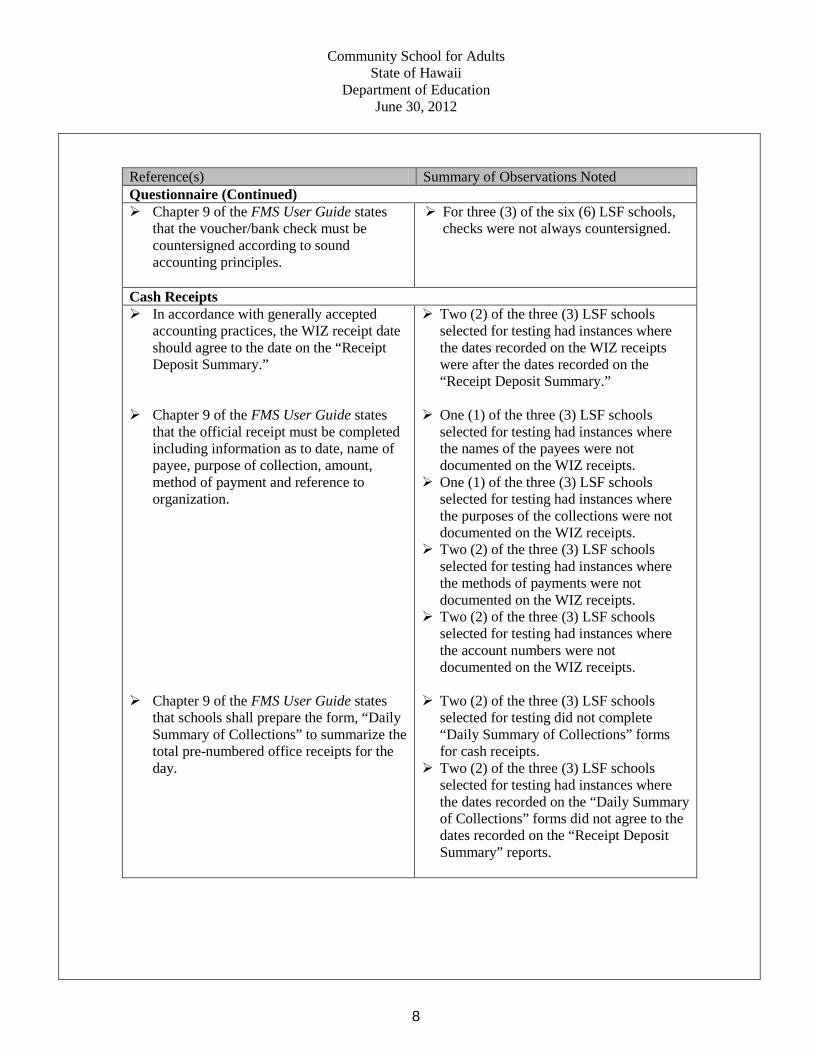

Reference(s) Summary of Observations Noted Questionnaire (Continued) Chapter 9 of the FMS User Guide states

that the voucher/bank check must be countersigned according to sound accounting principles.

For three (3) of the six (6) LSF schools, checks were not always countersigned.

Cash Receipts In accordance with generally accepted

accounting practices, the WIZ receipt date should agree to the date on the “Receipt Deposit Summary.”

Chapter 9 of the FMS User Guide states

that the official receipt must be completed including information as to date, name of payee, purpose of collection, amount, method of payment and reference to organization.

Chapter 9 of the FMS User Guide states that schools shall prepare the form, “Daily Summary of Collections” to summarize the total pre-numbered office receipts for the day.

Two (2) of the three (3) LSF schools selected for testing had instances where the dates recorded on the WIZ receipts were after the dates recorded on the “Receipt Deposit Summary.”

One (1) of the three (3) LSF schools selected for testing had instances where the names of the payees were not documented on the WIZ receipts.

One (1) of the three (3) LSF schools selected for testing had instances where the purposes of the collections were not documented on the WIZ receipts.

Two (2) of the three (3) LSF schools selected for testing had instances where the methods of payments were not documented on the WIZ receipts.

Two (2) of the three (3) LSF schools selected for testing had instances where the account numbers were not documented on the WIZ receipts.

Two (2) of the three (3) LSF schools selected for testing did not complete “Daily Summary of Collections” forms for cash receipts.

Two (2) of the three (3) LSF schools selected for testing had instances where the dates recorded on the “Daily Summary of Collections” forms did not agree to the dates recorded on the “Receipt Deposit Summary” reports.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

9

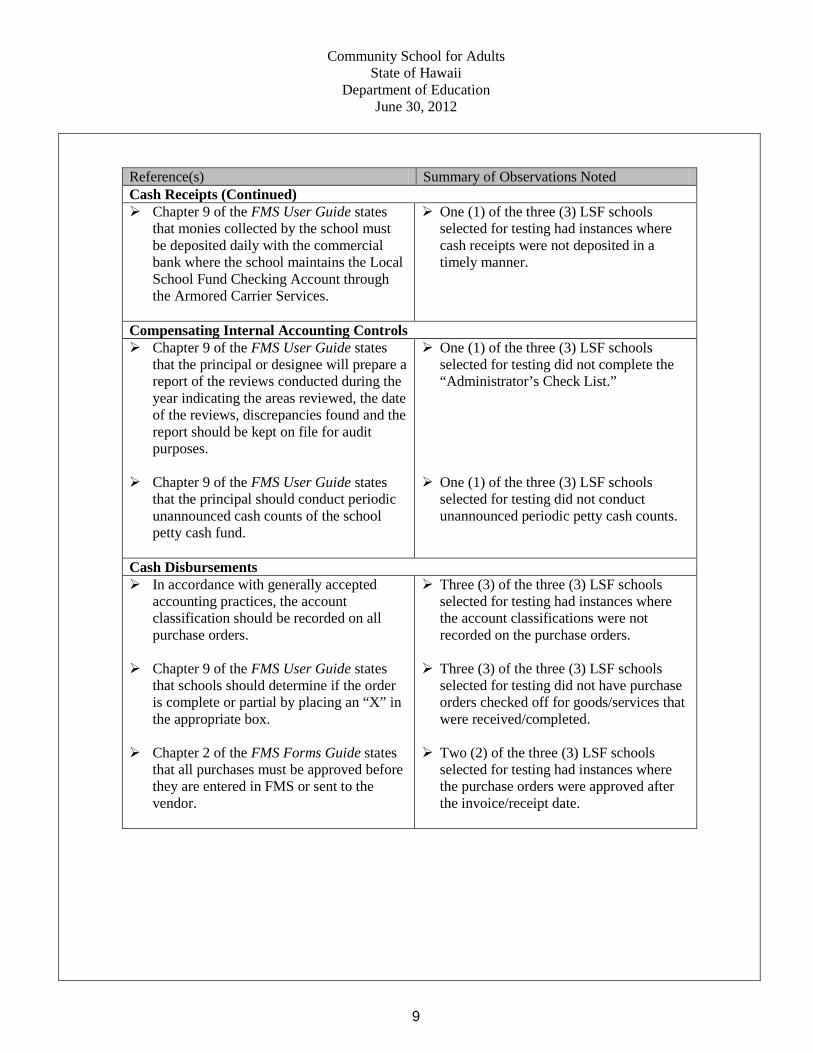

Reference(s) Summary of Observations Noted Cash Receipts (Continued) Chapter 9 of the FMS User Guide states

that monies collected by the school must be deposited daily with the commercial bank where the school maintains the Local School Fund Checking Account through the Armored Carrier Services.

One (1) of the three (3) LSF schools selected for testing had instances where cash receipts were not deposited in a timely manner.

Compensating Internal Accounting Controls Chapter 9 of the FMS User Guide states

that the principal or designee will prepare a report of the reviews conducted during the year indicating the areas reviewed, the date of the reviews, discrepancies found and the report should be kept on file for audit purposes.

Chapter 9 of the FMS User Guide states that the principal should conduct periodic unannounced cash counts of the school petty cash fund.

One (1) of the three (3) LSF schools selected for testing did not complete the “Administrator’s Check List.”

One (1) of the three (3) LSF schools

selected for testing did not conduct unannounced periodic petty cash counts.

Cash Disbursements In accordance with generally accepted

accounting practices, the account classification should be recorded on all purchase orders.

Chapter 9 of the FMS User Guide states

that schools should determine if the order is complete or partial by placing an “X” in the appropriate box.

Chapter 2 of the FMS Forms Guide states that all purchases must be approved before they are entered in FMS or sent to the vendor.

Three (3) of the three (3) LSF schools selected for testing had instances where the account classifications were not recorded on the purchase orders.

Three (3) of the three (3) LSF schools selected for testing did not have purchase orders checked off for goods/services that were received/completed.

Two (2) of the three (3) LSF schools

selected for testing had instances where the purchase orders were approved after the invoice/receipt date.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

10

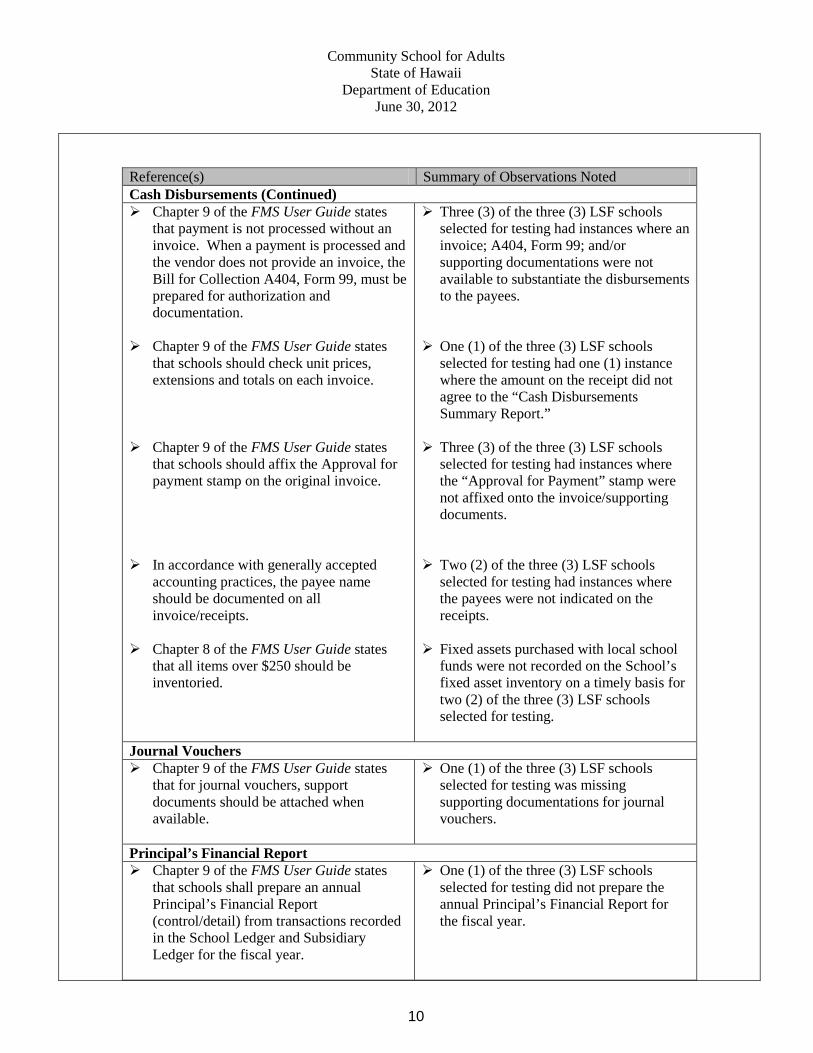

Reference(s) Summary of Observations Noted Cash Disbursements (Continued) Chapter 9 of the FMS User Guide states

that payment is not processed without an invoice. When a payment is processed and the vendor does not provide an invoice, the Bill for Collection A404, Form 99, must be prepared for authorization and documentation.

Chapter 9 of the FMS User Guide states that schools should check unit prices, extensions and totals on each invoice.

Chapter 9 of the FMS User Guide states that schools should affix the Approval for payment stamp on the original invoice.

In accordance with generally accepted

accounting practices, the payee name should be documented on all invoice/receipts.

Chapter 8 of the FMS User Guide states that all items over $250 should be inventoried.

Three (3) of the three (3) LSF schools selected for testing had instances where an invoice; A404, Form 99; and/or supporting documentations were not available to substantiate the disbursements to the payees.

One (1) of the three (3) LSF schools selected for testing had one (1) instance where the amount on the receipt did not agree to the “Cash Disbursements Summary Report.”

Three (3) of the three (3) LSF schools selected for testing had instances where the “Approval for Payment” stamp were not affixed onto the invoice/supporting documents.

Two (2) of the three (3) LSF schools selected for testing had instances where the payees were not indicated on the receipts.

Fixed assets purchased with local school

funds were not recorded on the School’s fixed asset inventory on a timely basis for two (2) of the three (3) LSF schools selected for testing.

Journal Vouchers Chapter 9 of the FMS User Guide states

that for journal vouchers, support documents should be attached when available.

One (1) of the three (3) LSF schools selected for testing was missing supporting documentations for journal vouchers.

Principal’s Financial Report Chapter 9 of the FMS User Guide states

that schools shall prepare an annual Principal’s Financial Report (control/detail) from transactions recorded in the School Ledger and Subsidiary Ledger for the fiscal year.

One (1) of the three (3) LSF schools selected for testing did not prepare the annual Principal’s Financial Report for the fiscal year.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

11

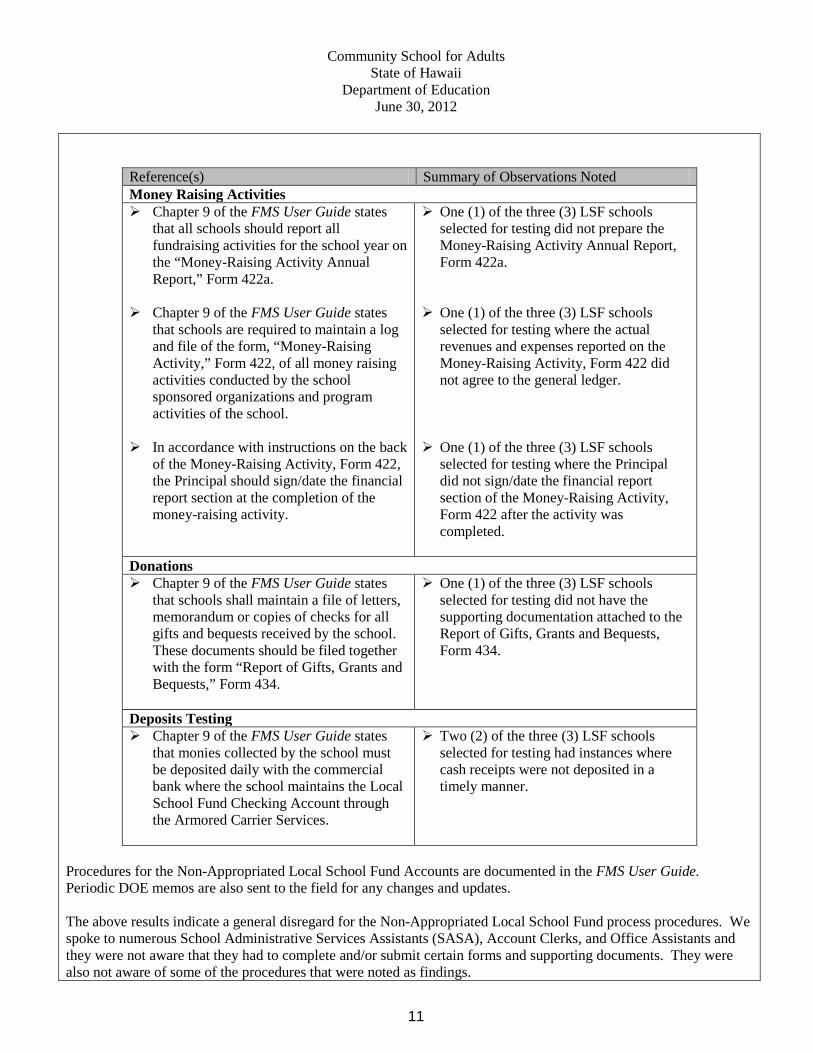

Reference(s) Summary of Observations Noted Money Raising Activities Chapter 9 of the FMS User Guide states

that all schools should report all fundraising activities for the school year on the “Money-Raising Activity Annual Report,” Form 422a.

Chapter 9 of the FMS User Guide states that schools are required to maintain a log and file of the form, “Money-Raising Activity,” Form 422, of all money raising activities conducted by the school sponsored organizations and program activities of the school.

In accordance with instructions on the back

of the Money-Raising Activity, Form 422, the Principal should sign/date the financial report section at the completion of the money-raising activity.

One (1) of the three (3) LSF schools selected for testing did not prepare the Money-Raising Activity Annual Report, Form 422a.

One (1) of the three (3) LSF schools selected for testing where the actual revenues and expenses reported on the Money-Raising Activity, Form 422 did not agree to the general ledger.

One (1) of the three (3) LSF schools selected for testing where the Principal did not sign/date the financial report section of the Money-Raising Activity, Form 422 after the activity was completed.

Donations Chapter 9 of the FMS User Guide states

that schools shall maintain a file of letters, memorandum or copies of checks for all gifts and bequests received by the school. These documents should be filed together with the form “Report of Gifts, Grants and Bequests,” Form 434.

One (1) of the three (3) LSF schools selected for testing did not have the supporting documentation attached to the Report of Gifts, Grants and Bequests, Form 434.

Deposits Testing Chapter 9 of the FMS User Guide states

that monies collected by the school must be deposited daily with the commercial bank where the school maintains the Local School Fund Checking Account through the Armored Carrier Services.

Two (2) of the three (3) LSF schools selected for testing had instances where cash receipts were not deposited in a timely manner.

Procedures for the Non-Appropriated Local School Fund Accounts are documented in the FMS User Guide. Periodic DOE memos are also sent to the field for any changes and updates. The above results indicate a general disregard for the Non-Appropriated Local School Fund process procedures. We spoke to numerous School Administrative Services Assistants (SASA), Account Clerks, and Office Assistants and they were not aware that they had to complete and/or submit certain forms and supporting documents. They were also not aware of some of the procedures that were noted as findings.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

12

Recommendation Recommendations for the observation regarding Non-Appropriated Local School Funds procedures were not always followed at the schools include: Mandatory training should be required for all staff handling Local School Funds at schools. All staff

handling Local School Funds should be enrolled into the SASA Academy to help address findings. School administrators should ensure proper procedures are followed by reviewing all appropriate documents. Periodic spot checks should be conducted by the CABMs and ASAs, to ensure that proper procedures are

followed. CABMs and ASAs should perform fiscal reviews of each school on a quarterly basis, ensuring adherence to standard procedures by the DOE.

IA should perform periodic Local School Fund audits for the Community School for Adults.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

13

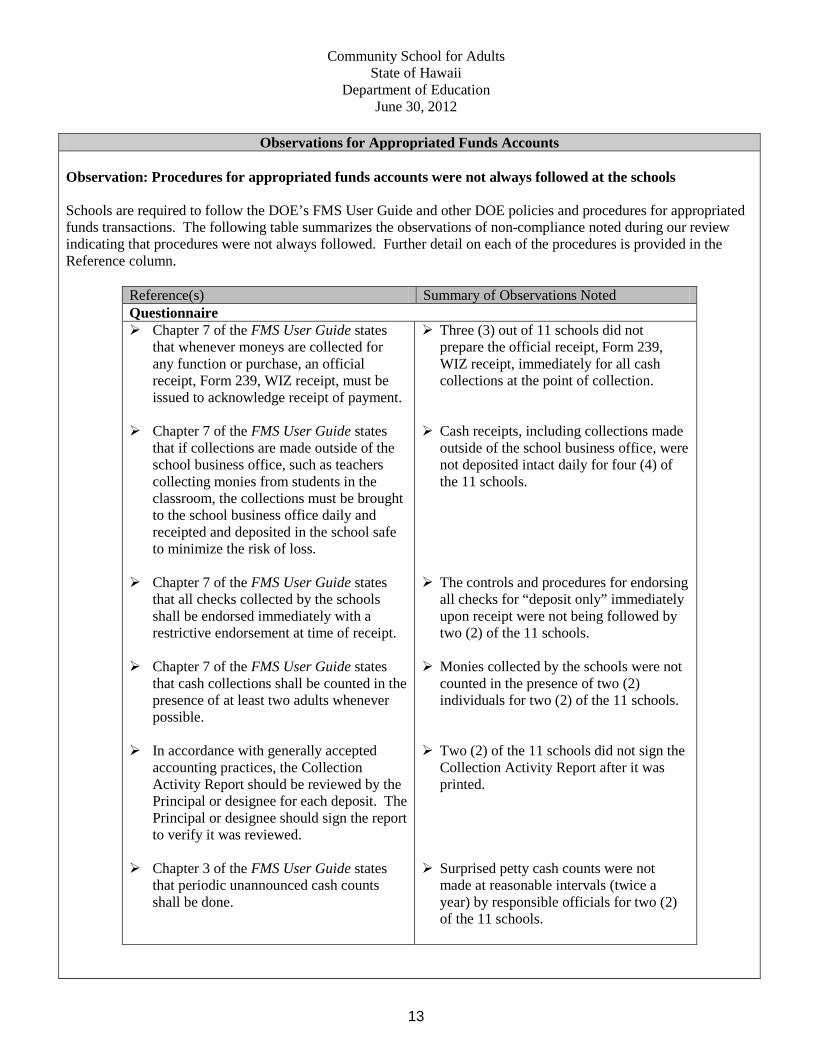

Observations for Appropriated Funds Accounts Observation: Procedures for appropriated funds accounts were not always followed at the schools Schools are required to follow the DOE’s FMS User Guide and other DOE policies and procedures for appropriated funds transactions. The following table summarizes the observations of non-compliance noted during our review indicating that procedures were not always followed. Further detail on each of the procedures is provided in the Reference column.

Reference(s) Summary of Observations Noted Questionnaire Chapter 7 of the FMS User Guide states

that whenever moneys are collected for any function or purchase, an official receipt, Form 239, WIZ receipt, must be issued to acknowledge receipt of payment.

Chapter 7 of the FMS User Guide states that if collections are made outside of the school business office, such as teachers collecting monies from students in the classroom, the collections must be brought to the school business office daily and receipted and deposited in the school safe to minimize the risk of loss.

Chapter 7 of the FMS User Guide states

that all checks collected by the schools shall be endorsed immediately with a restrictive endorsement at time of receipt.

Chapter 7 of the FMS User Guide states

that cash collections shall be counted in the presence of at least two adults whenever possible.

In accordance with generally accepted

accounting practices, the Collection Activity Report should be reviewed by the Principal or designee for each deposit. The Principal or designee should sign the report to verify it was reviewed.

Chapter 3 of the FMS User Guide states

that periodic unannounced cash counts shall be done.

Three (3) out of 11 schools did not prepare the official receipt, Form 239, WIZ receipt, immediately for all cash collections at the point of collection.

Cash receipts, including collections made outside of the school business office, were not deposited intact daily for four (4) of the 11 schools.

The controls and procedures for endorsing all checks for “deposit only” immediately upon receipt were not being followed by two (2) of the 11 schools.

Monies collected by the schools were not counted in the presence of two (2) individuals for two (2) of the 11 schools.

Two (2) of the 11 schools did not sign the Collection Activity Report after it was printed.

Surprised petty cash counts were not

made at reasonable intervals (twice a year) by responsible officials for two (2) of the 11 schools.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

14

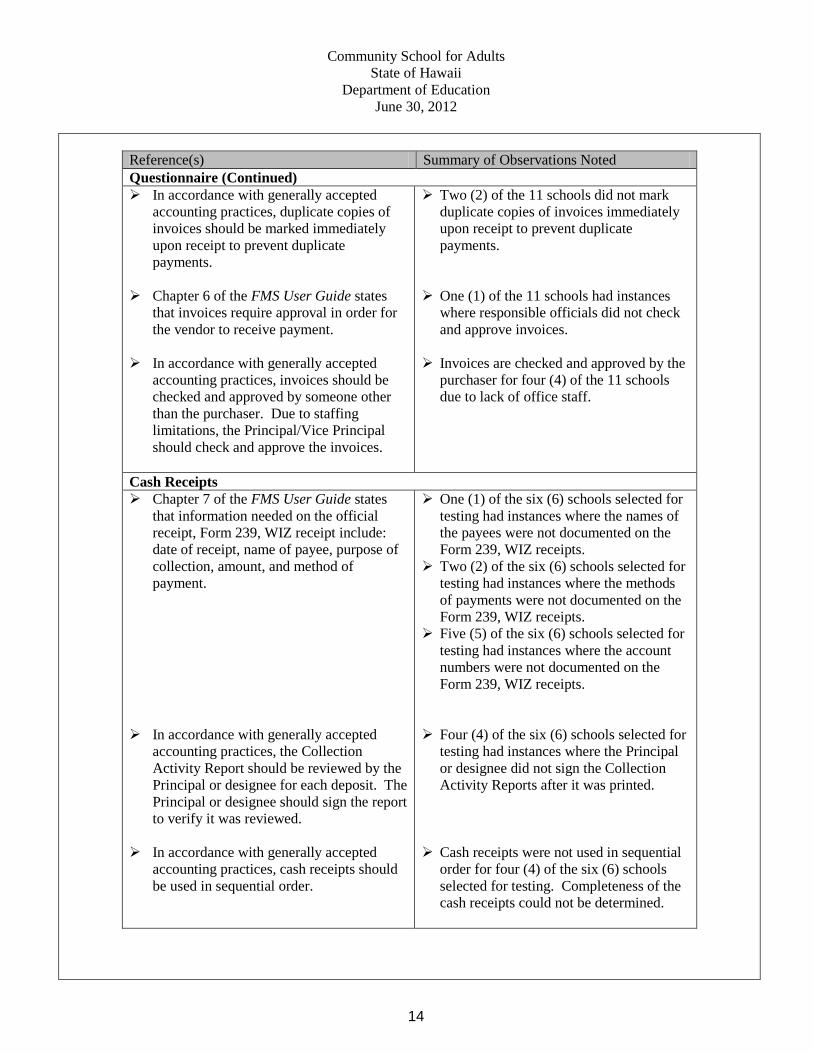

Reference(s) Summary of Observations Noted Questionnaire (Continued) In accordance with generally accepted

accounting practices, duplicate copies of invoices should be marked immediately upon receipt to prevent duplicate payments.

Chapter 6 of the FMS User Guide states

that invoices require approval in order for the vendor to receive payment.

In accordance with generally accepted

accounting practices, invoices should be checked and approved by someone other than the purchaser. Due to staffing limitations, the Principal/Vice Principal should check and approve the invoices.

Two (2) of the 11 schools did not mark duplicate copies of invoices immediately upon receipt to prevent duplicate payments.

One (1) of the 11 schools had instances where responsible officials did not check and approve invoices.

Invoices are checked and approved by the purchaser for four (4) of the 11 schools due to lack of office staff.

Cash Receipts Chapter 7 of the FMS User Guide states

that information needed on the official receipt, Form 239, WIZ receipt include: date of receipt, name of payee, purpose of collection, amount, and method of payment.

In accordance with generally accepted accounting practices, the Collection Activity Report should be reviewed by the Principal or designee for each deposit. The Principal or designee should sign the report to verify it was reviewed.

In accordance with generally accepted accounting practices, cash receipts should be used in sequential order.

One (1) of the six (6) schools selected for testing had instances where the names of the payees were not documented on the Form 239, WIZ receipts.

Two (2) of the six (6) schools selected for testing had instances where the methods of payments were not documented on the Form 239, WIZ receipts.

Five (5) of the six (6) schools selected for testing had instances where the account numbers were not documented on the Form 239, WIZ receipts.

Four (4) of the six (6) schools selected for testing had instances where the Principal or designee did not sign the Collection Activity Reports after it was printed.

Cash receipts were not used in sequential

order for four (4) of the six (6) schools selected for testing. Completeness of the cash receipts could not be determined.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

15

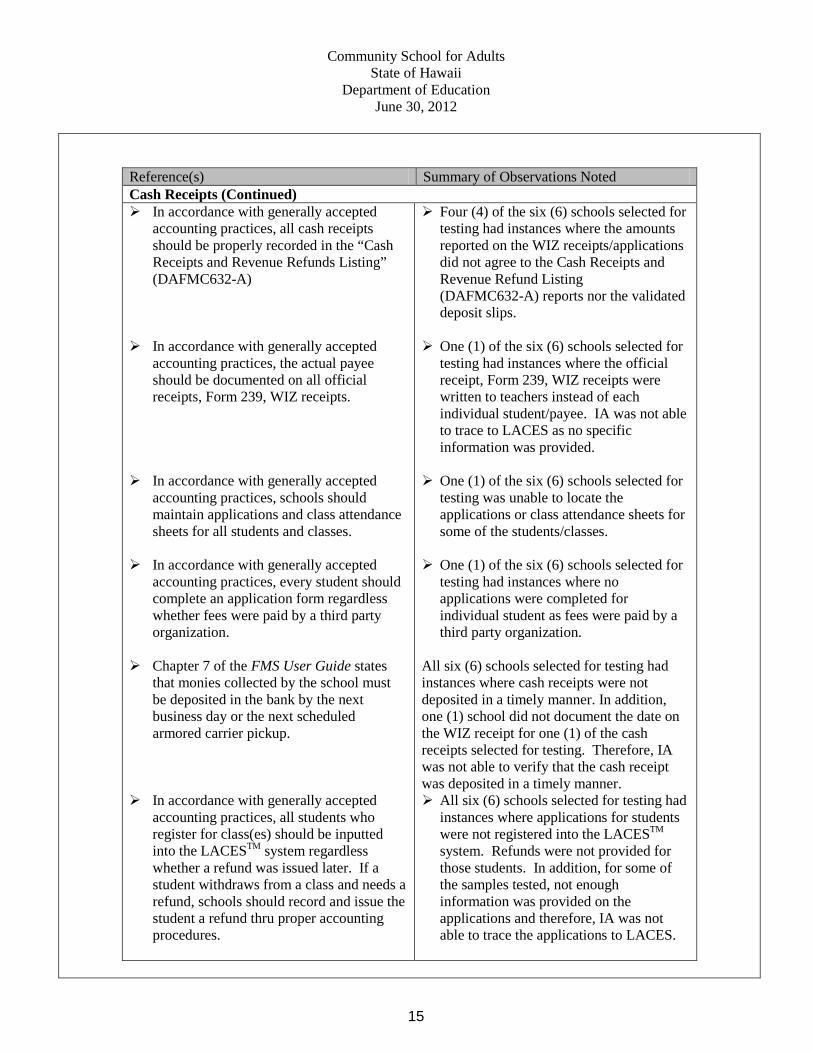

Reference(s) Summary of Observations Noted Cash Receipts (Continued) In accordance with generally accepted

accounting practices, all cash receipts should be properly recorded in the “Cash Receipts and Revenue Refunds Listing” (DAFMC632-A)

In accordance with generally accepted accounting practices, the actual payee should be documented on all official receipts, Form 239, WIZ receipts.

In accordance with generally accepted accounting practices, schools should maintain applications and class attendance sheets for all students and classes.

In accordance with generally accepted accounting practices, every student should complete an application form regardless whether fees were paid by a third party organization.

Chapter 7 of the FMS User Guide states

that monies collected by the school must be deposited in the bank by the next business day or the next scheduled armored carrier pickup.

In accordance with generally accepted

accounting practices, all students who register for class(es) should be inputted into the LACESTM system regardless whether a refund was issued later. If a student withdraws from a class and needs a refund, schools should record and issue the student a refund thru proper accounting procedures.

Four (4) of the six (6) schools selected for testing had instances where the amounts reported on the WIZ receipts/applications did not agree to the Cash Receipts and Revenue Refund Listing (DAFMC632-A) reports nor the validated deposit slips.

One (1) of the six (6) schools selected for testing had instances where the official receipt, Form 239, WIZ receipts were written to teachers instead of each individual student/payee. IA was not able to trace to LACES as no specific information was provided.

One (1) of the six (6) schools selected for testing was unable to locate the applications or class attendance sheets for some of the students/classes.

One (1) of the six (6) schools selected for

testing had instances where no applications were completed for individual student as fees were paid by a third party organization.

All six (6) schools selected for testing had instances where cash receipts were not deposited in a timely manner. In addition, one (1) school did not document the date on the WIZ receipt for one (1) of the cash receipts selected for testing. Therefore, IA was not able to verify that the cash receipt was deposited in a timely manner. All six (6) schools selected for testing had

instances where applications for students were not registered into the LACESTM system. Refunds were not provided for those students. In addition, for some of the samples tested, not enough information was provided on the applications and therefore, IA was not able to trace the applications to LACES.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

16

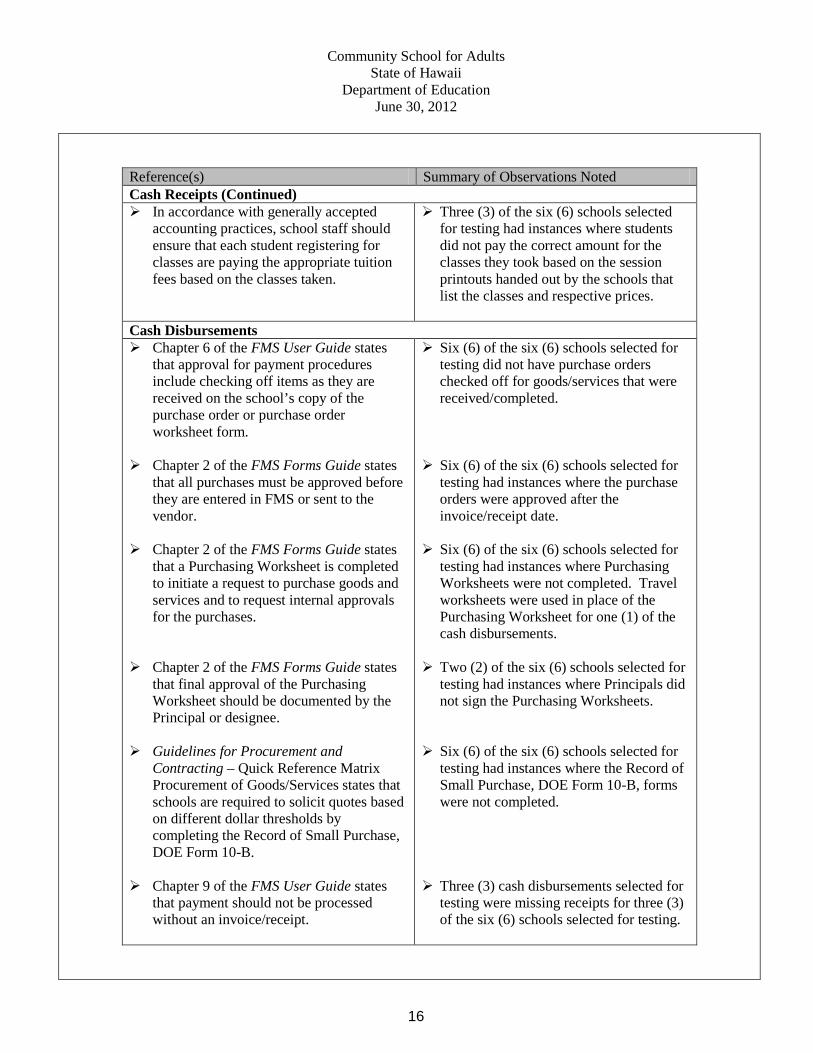

Reference(s) Summary of Observations Noted Cash Receipts (Continued) In accordance with generally accepted

accounting practices, school staff should ensure that each student registering for classes are paying the appropriate tuition fees based on the classes taken.

Three (3) of the six (6) schools selected for testing had instances where students did not pay the correct amount for the classes they took based on the session printouts handed out by the schools that list the classes and respective prices.

Cash Disbursements Chapter 6 of the FMS User Guide states

that approval for payment procedures include checking off items as they are received on the school’s copy of the purchase order or purchase order worksheet form.

Chapter 2 of the FMS Forms Guide states that all purchases must be approved before they are entered in FMS or sent to the vendor.

Chapter 2 of the FMS Forms Guide states

that a Purchasing Worksheet is completed to initiate a request to purchase goods and services and to request internal approvals for the purchases.

Chapter 2 of the FMS Forms Guide states that final approval of the Purchasing Worksheet should be documented by the Principal or designee.

Guidelines for Procurement and Contracting – Quick Reference Matrix Procurement of Goods/Services states that schools are required to solicit quotes based on different dollar thresholds by completing the Record of Small Purchase, DOE Form 10-B.

Chapter 9 of the FMS User Guide states

that payment should not be processed without an invoice/receipt.

Six (6) of the six (6) schools selected for testing did not have purchase orders checked off for goods/services that were received/completed.

Six (6) of the six (6) schools selected for

testing had instances where the purchase orders were approved after the invoice/receipt date.

Six (6) of the six (6) schools selected for

testing had instances where Purchasing Worksheets were not completed. Travel worksheets were used in place of the Purchasing Worksheet for one (1) of the cash disbursements.

Two (2) of the six (6) schools selected for

testing had instances where Principals did not sign the Purchasing Worksheets.

Six (6) of the six (6) schools selected for

testing had instances where the Record of Small Purchase, DOE Form 10-B, forms were not completed.

Three (3) cash disbursements selected for

testing were missing receipts for three (3) of the six (6) schools selected for testing.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

17

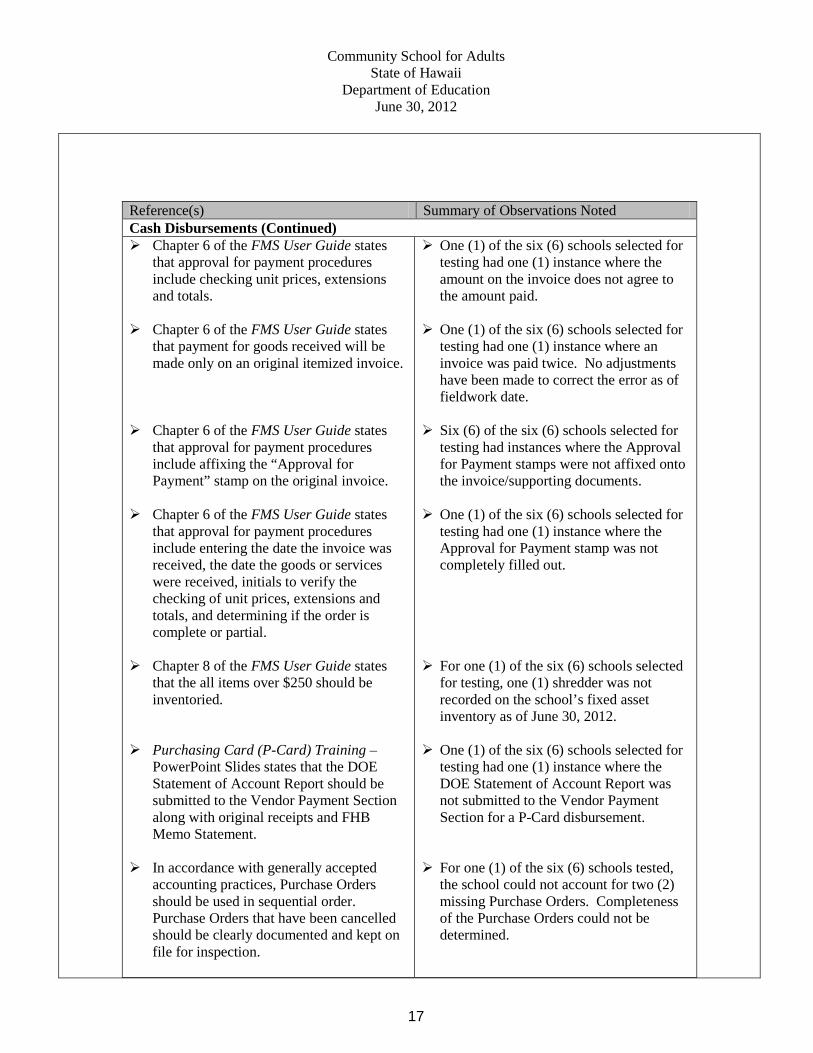

Reference(s) Summary of Observations Noted Cash Disbursements (Continued) Chapter 6 of the FMS User Guide states

that approval for payment procedures include checking unit prices, extensions and totals.

Chapter 6 of the FMS User Guide states that payment for goods received will be made only on an original itemized invoice.

Chapter 6 of the FMS User Guide states that approval for payment procedures include affixing the “Approval for Payment” stamp on the original invoice.

Chapter 6 of the FMS User Guide states that approval for payment procedures include entering the date the invoice was received, the date the goods or services were received, initials to verify the checking of unit prices, extensions and totals, and determining if the order is complete or partial.

Chapter 8 of the FMS User Guide states

that the all items over $250 should be inventoried.

Purchasing Card (P-Card) Training –

PowerPoint Slides states that the DOE Statement of Account Report should be submitted to the Vendor Payment Section along with original receipts and FHB Memo Statement.

In accordance with generally accepted accounting practices, Purchase Orders should be used in sequential order. Purchase Orders that have been cancelled should be clearly documented and kept on file for inspection.

One (1) of the six (6) schools selected for testing had one (1) instance where the amount on the invoice does not agree to the amount paid.

One (1) of the six (6) schools selected for testing had one (1) instance where an invoice was paid twice. No adjustments have been made to correct the error as of fieldwork date.

Six (6) of the six (6) schools selected for

testing had instances where the Approval for Payment stamps were not affixed onto the invoice/supporting documents.

One (1) of the six (6) schools selected for

testing had one (1) instance where the Approval for Payment stamp was not completely filled out.

For one (1) of the six (6) schools selected

for testing, one (1) shredder was not recorded on the school’s fixed asset inventory as of June 30, 2012.

One (1) of the six (6) schools selected for testing had one (1) instance where the DOE Statement of Account Report was not submitted to the Vendor Payment Section for a P-Card disbursement.

For one (1) of the six (6) schools tested,

the school could not account for two (2) missing Purchase Orders. Completeness of the Purchase Orders could not be determined.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

18

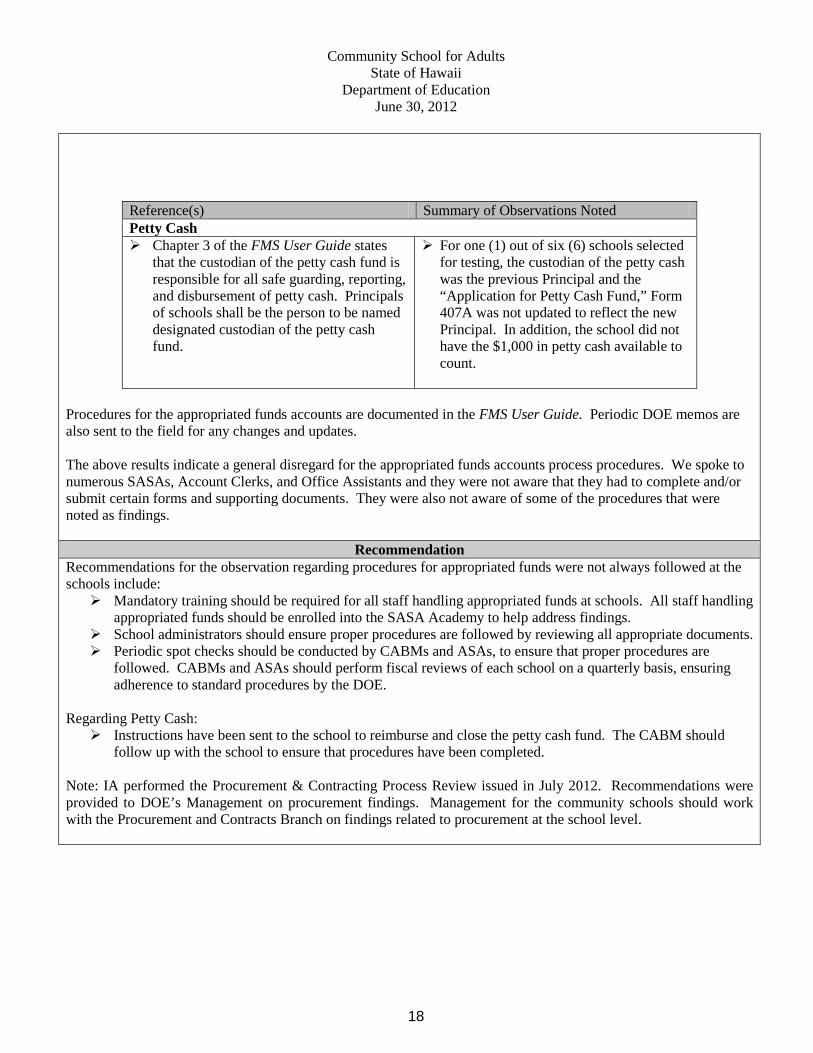

Reference(s) Summary of Observations Noted Petty Cash Chapter 3 of the FMS User Guide states

that the custodian of the petty cash fund is responsible for all safe guarding, reporting, and disbursement of petty cash. Principals of schools shall be the person to be named designated custodian of the petty cash fund.

For one (1) out of six (6) schools selected for testing, the custodian of the petty cash was the previous Principal and the “Application for Petty Cash Fund,” Form 407A was not updated to reflect the new Principal. In addition, the school did not have the $1,000 in petty cash available to count.

Procedures for the appropriated funds accounts are documented in the FMS User Guide. Periodic DOE memos are also sent to the field for any changes and updates. The above results indicate a general disregard for the appropriated funds accounts process procedures. We spoke to numerous SASAs, Account Clerks, and Office Assistants and they were not aware that they had to complete and/or submit certain forms and supporting documents. They were also not aware of some of the procedures that were noted as findings.

Recommendation Recommendations for the observation regarding procedures for appropriated funds were not always followed at the schools include: Mandatory training should be required for all staff handling appropriated funds at schools. All staff handling

appropriated funds should be enrolled into the SASA Academy to help address findings. School administrators should ensure proper procedures are followed by reviewing all appropriate documents. Periodic spot checks should be conducted by CABMs and ASAs, to ensure that proper procedures are

followed. CABMs and ASAs should perform fiscal reviews of each school on a quarterly basis, ensuring adherence to standard procedures by the DOE.

Regarding Petty Cash: Instructions have been sent to the school to reimburse and close the petty cash fund. The CABM should

follow up with the school to ensure that procedures have been completed. Note: IA performed the Procurement & Contracting Process Review issued in July 2012. Recommendations were provided to DOE’s Management on procurement findings. Management for the community schools should work with the Procurement and Contracts Branch on findings related to procurement at the school level.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

19

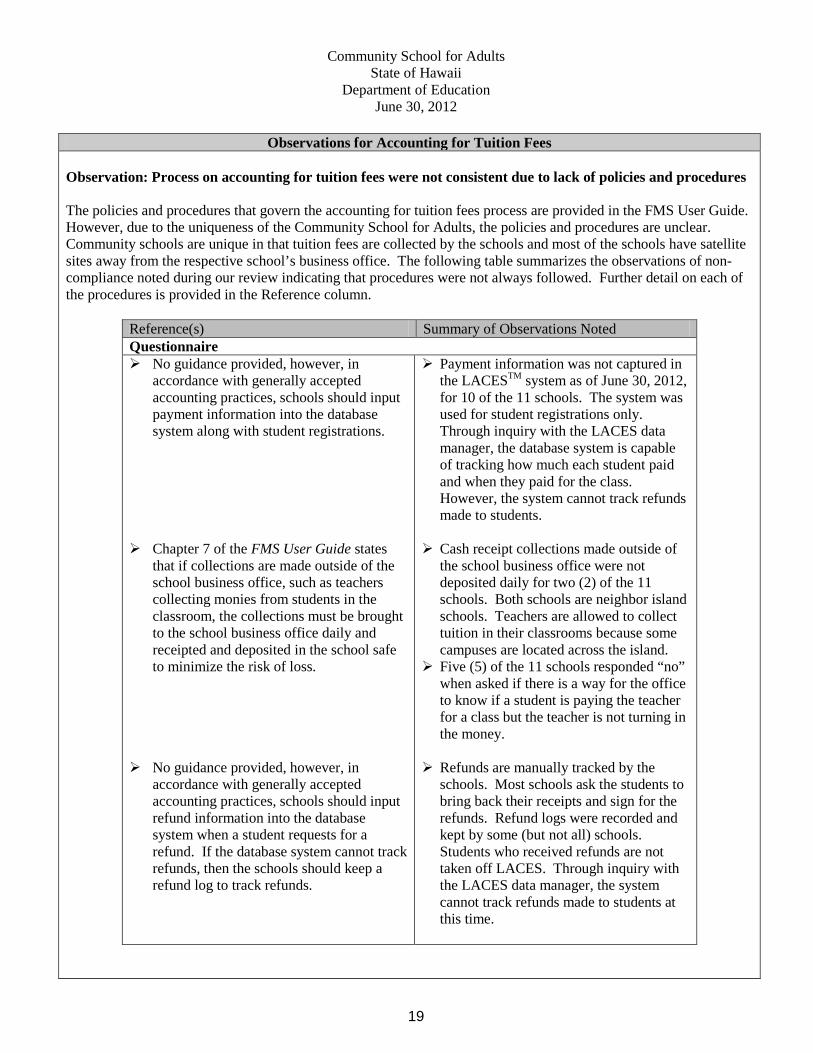

Observations for Accounting for Tuition Fees Observation: Process on accounting for tuition fees were not consistent due to lack of policies and procedures The policies and procedures that govern the accounting for tuition fees process are provided in the FMS User Guide. However, due to the uniqueness of the Community School for Adults, the policies and procedures are unclear. Community schools are unique in that tuition fees are collected by the schools and most of the schools have satellite sites away from the respective school’s business office. The following table summarizes the observations of non-compliance noted during our review indicating that procedures were not always followed. Further detail on each of the procedures is provided in the Reference column.

Reference(s) Summary of Observations Noted Questionnaire No guidance provided, however, in

accordance with generally accepted accounting practices, schools should input payment information into the database system along with student registrations.

Chapter 7 of the FMS User Guide states

that if collections are made outside of the school business office, such as teachers collecting monies from students in the classroom, the collections must be brought to the school business office daily and receipted and deposited in the school safe to minimize the risk of loss.

No guidance provided, however, in accordance with generally accepted accounting practices, schools should input refund information into the database system when a student requests for a refund. If the database system cannot track refunds, then the schools should keep a refund log to track refunds.

Payment information was not captured in the LACESTM system as of June 30, 2012, for 10 of the 11 schools. The system was used for student registrations only. Through inquiry with the LACES data manager, the database system is capable of tracking how much each student paid and when they paid for the class. However, the system cannot track refunds made to students.

Cash receipt collections made outside of the school business office were not deposited daily for two (2) of the 11 schools. Both schools are neighbor island schools. Teachers are allowed to collect tuition in their classrooms because some campuses are located across the island.

Five (5) of the 11 schools responded “no” when asked if there is a way for the office to know if a student is paying the teacher for a class but the teacher is not turning in the money.

Refunds are manually tracked by the schools. Most schools ask the students to bring back their receipts and sign for the refunds. Refund logs were recorded and kept by some (but not all) schools. Students who received refunds are not taken off LACES. Through inquiry with the LACES data manager, the system cannot track refunds made to students at this time.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

20

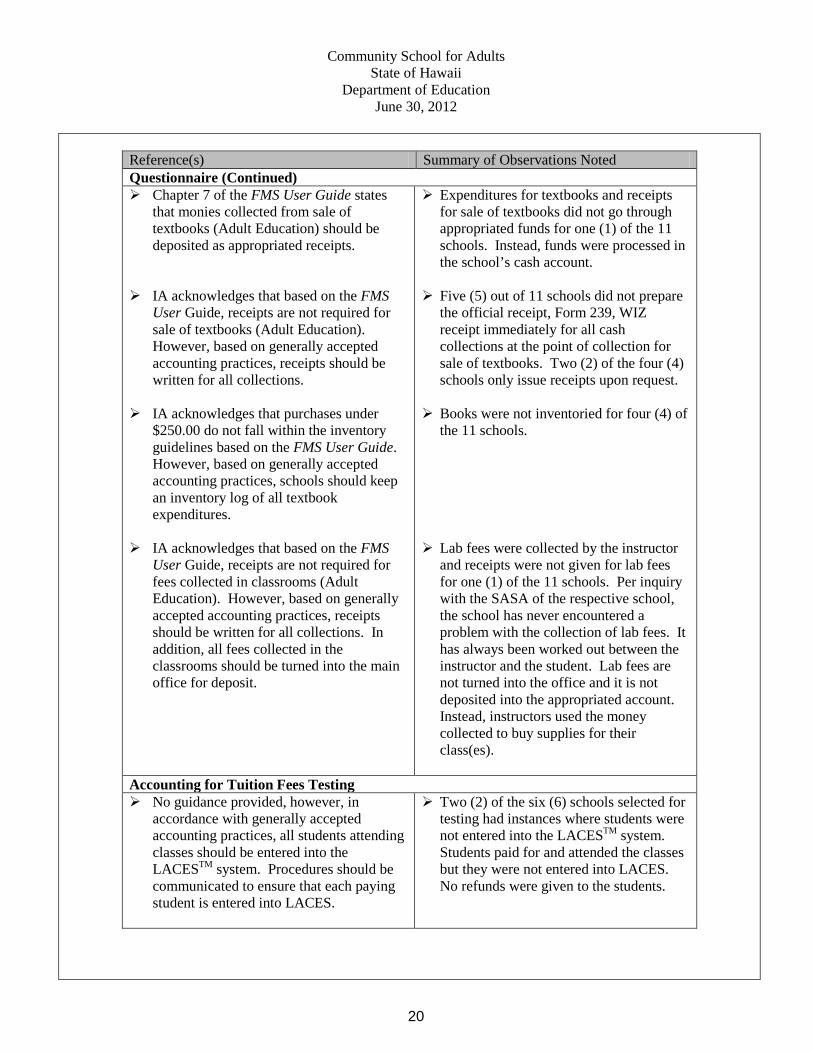

Reference(s) Summary of Observations Noted Questionnaire (Continued) Chapter 7 of the FMS User Guide states

that monies collected from sale of textbooks (Adult Education) should be deposited as appropriated receipts.

IA acknowledges that based on the FMS User Guide, receipts are not required for sale of textbooks (Adult Education). However, based on generally accepted accounting practices, receipts should be written for all collections.

IA acknowledges that purchases under $250.00 do not fall within the inventory guidelines based on the FMS User Guide. However, based on generally accepted accounting practices, schools should keep an inventory log of all textbook expenditures.

IA acknowledges that based on the FMS User Guide, receipts are not required for fees collected in classrooms (Adult Education). However, based on generally accepted accounting practices, receipts should be written for all collections. In addition, all fees collected in the classrooms should be turned into the main office for deposit.

Expenditures for textbooks and receipts for sale of textbooks did not go through appropriated funds for one (1) of the 11 schools. Instead, funds were processed in the school’s cash account.

Five (5) out of 11 schools did not prepare the official receipt, Form 239, WIZ receipt immediately for all cash collections at the point of collection for sale of textbooks. Two (2) of the four (4) schools only issue receipts upon request.

Books were not inventoried for four (4) of the 11 schools.

Lab fees were collected by the instructor

and receipts were not given for lab fees for one (1) of the 11 schools. Per inquiry with the SASA of the respective school, the school has never encountered a problem with the collection of lab fees. It has always been worked out between the instructor and the student. Lab fees are not turned into the office and it is not deposited into the appropriated account. Instead, instructors used the money collected to buy supplies for their class(es).

Accounting for Tuition Fees Testing No guidance provided, however, in

accordance with generally accepted accounting practices, all students attending classes should be entered into the LACESTM system. Procedures should be communicated to ensure that each paying student is entered into LACES.

Two (2) of the six (6) schools selected for testing had instances where students were not entered into the LACESTM system. Students paid for and attended the classes but they were not entered into LACES. No refunds were given to the students.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

21

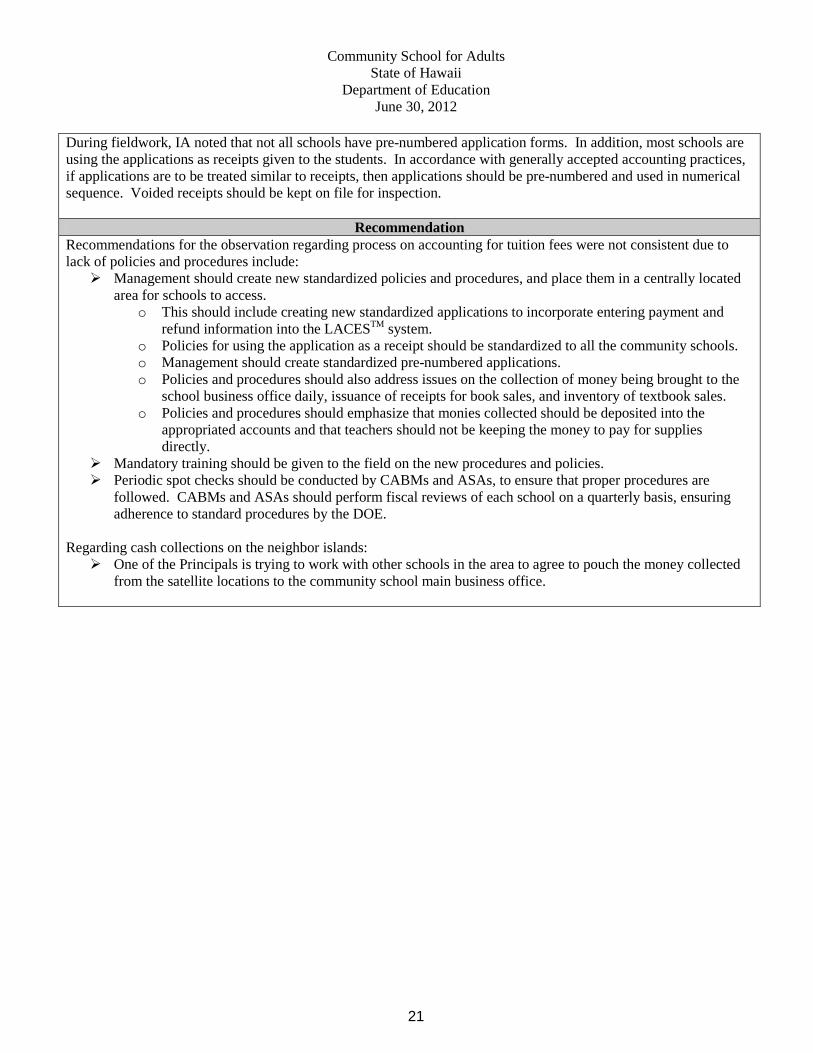

During fieldwork, IA noted that not all schools have pre-numbered application forms. In addition, most schools are using the applications as receipts given to the students. In accordance with generally accepted accounting practices, if applications are to be treated similar to receipts, then applications should be pre-numbered and used in numerical sequence. Voided receipts should be kept on file for inspection.

Recommendation Recommendations for the observation regarding process on accounting for tuition fees were not consistent due to lack of policies and procedures include: Management should create new standardized policies and procedures, and place them in a centrally located

area for schools to access. o This should include creating new standardized applications to incorporate entering payment and

refund information into the LACESTM system. o Policies for using the application as a receipt should be standardized to all the community schools. o Management should create standardized pre-numbered applications. o Policies and procedures should also address issues on the collection of money being brought to the

school business office daily, issuance of receipts for book sales, and inventory of textbook sales. o Policies and procedures should emphasize that monies collected should be deposited into the

appropriated accounts and that teachers should not be keeping the money to pay for supplies directly.

Mandatory training should be given to the field on the new procedures and policies. Periodic spot checks should be conducted by CABMs and ASAs, to ensure that proper procedures are

followed. CABMs and ASAs should perform fiscal reviews of each school on a quarterly basis, ensuring adherence to standard procedures by the DOE.

Regarding cash collections on the neighbor islands: One of the Principals is trying to work with other schools in the area to agree to pouch the money collected

from the satellite locations to the community school main business office.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

22

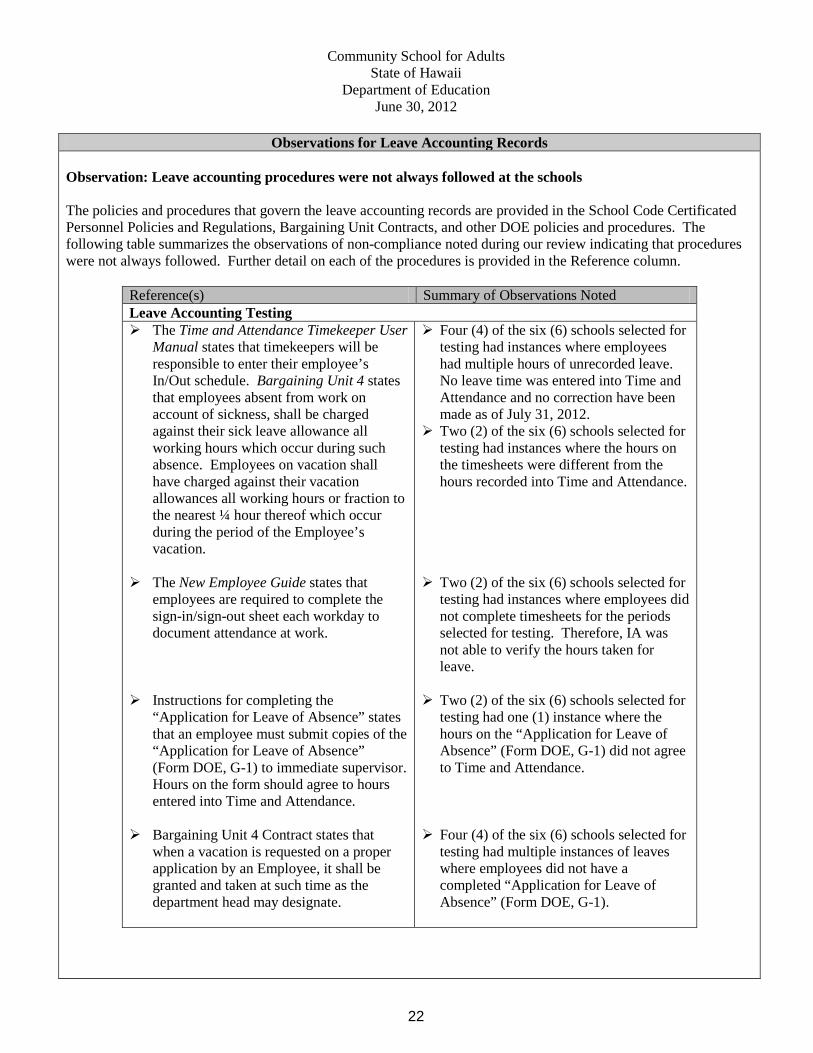

Observations for Leave Accounting Records Observation: Leave accounting procedures were not always followed at the schools The policies and procedures that govern the leave accounting records are provided in the School Code Certificated Personnel Policies and Regulations, Bargaining Unit Contracts, and other DOE policies and procedures. The following table summarizes the observations of non-compliance noted during our review indicating that procedures were not always followed. Further detail on each of the procedures is provided in the Reference column.

Reference(s) Summary of Observations Noted Leave Accounting Testing The Time and Attendance Timekeeper User

Manual states that timekeepers will be responsible to enter their employee’s In/Out schedule. Bargaining Unit 4 states that employees absent from work on account of sickness, shall be charged against their sick leave allowance all working hours which occur during such absence. Employees on vacation shall have charged against their vacation allowances all working hours or fraction to the nearest ¼ hour thereof which occur during the period of the Employee’s vacation.

The New Employee Guide states that employees are required to complete the sign-in/sign-out sheet each workday to document attendance at work.

Instructions for completing the

“Application for Leave of Absence” states that an employee must submit copies of the “Application for Leave of Absence” (Form DOE, G-1) to immediate supervisor. Hours on the form should agree to hours entered into Time and Attendance.

Bargaining Unit 4 Contract states that when a vacation is requested on a proper application by an Employee, it shall be granted and taken at such time as the department head may designate.

Four (4) of the six (6) schools selected for testing had instances where employees had multiple hours of unrecorded leave. No leave time was entered into Time and Attendance and no correction have been made as of July 31, 2012.

Two (2) of the six (6) schools selected for testing had instances where the hours on the timesheets were different from the hours recorded into Time and Attendance.

Two (2) of the six (6) schools selected for testing had instances where employees did not complete timesheets for the periods selected for testing. Therefore, IA was not able to verify the hours taken for leave.

Two (2) of the six (6) schools selected for testing had one (1) instance where the hours on the “Application for Leave of Absence” (Form DOE, G-1) did not agree to Time and Attendance.

Four (4) of the six (6) schools selected for

testing had multiple instances of leaves where employees did not have a completed “Application for Leave of Absence” (Form DOE, G-1).

Community School for Adults State of Hawaii

Department of Education June 30, 2012

23

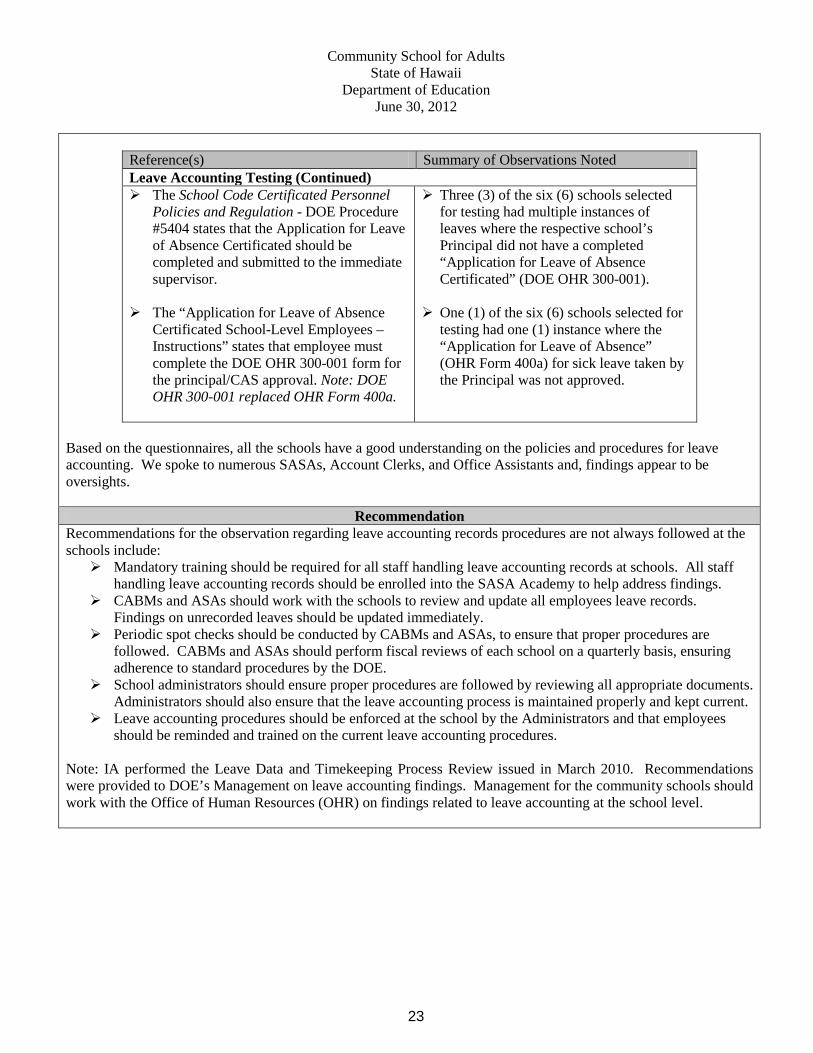

Reference(s) Summary of Observations Noted Leave Accounting Testing (Continued) The School Code Certificated Personnel

Policies and Regulation - DOE Procedure #5404 states that the Application for Leave of Absence Certificated should be completed and submitted to the immediate supervisor.

The “Application for Leave of Absence Certificated School-Level Employees – Instructions” states that employee must complete the DOE OHR 300-001 form for the principal/CAS approval. Note: DOE OHR 300-001 replaced OHR Form 400a.

Three (3) of the six (6) schools selected for testing had multiple instances of leaves where the respective school’s Principal did not have a completed “Application for Leave of Absence Certificated” (DOE OHR 300-001).

One (1) of the six (6) schools selected for testing had one (1) instance where the “Application for Leave of Absence” (OHR Form 400a) for sick leave taken by the Principal was not approved.

Based on the questionnaires, all the schools have a good understanding on the policies and procedures for leave accounting. We spoke to numerous SASAs, Account Clerks, and Office Assistants and, findings appear to be oversights.

Recommendation Recommendations for the observation regarding leave accounting records procedures are not always followed at the schools include: Mandatory training should be required for all staff handling leave accounting records at schools. All staff

handling leave accounting records should be enrolled into the SASA Academy to help address findings. CABMs and ASAs should work with the schools to review and update all employees leave records.

Findings on unrecorded leaves should be updated immediately. Periodic spot checks should be conducted by CABMs and ASAs, to ensure that proper procedures are

followed. CABMs and ASAs should perform fiscal reviews of each school on a quarterly basis, ensuring adherence to standard procedures by the DOE.

School administrators should ensure proper procedures are followed by reviewing all appropriate documents. Administrators should also ensure that the leave accounting process is maintained properly and kept current.

Leave accounting procedures should be enforced at the school by the Administrators and that employees should be reminded and trained on the current leave accounting procedures.

Note: IA performed the Leave Data and Timekeeping Process Review issued in March 2010. Recommendations were provided to DOE’s Management on leave accounting findings. Management for the community schools should work with the Office of Human Resources (OHR) on findings related to leave accounting at the school level.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

24

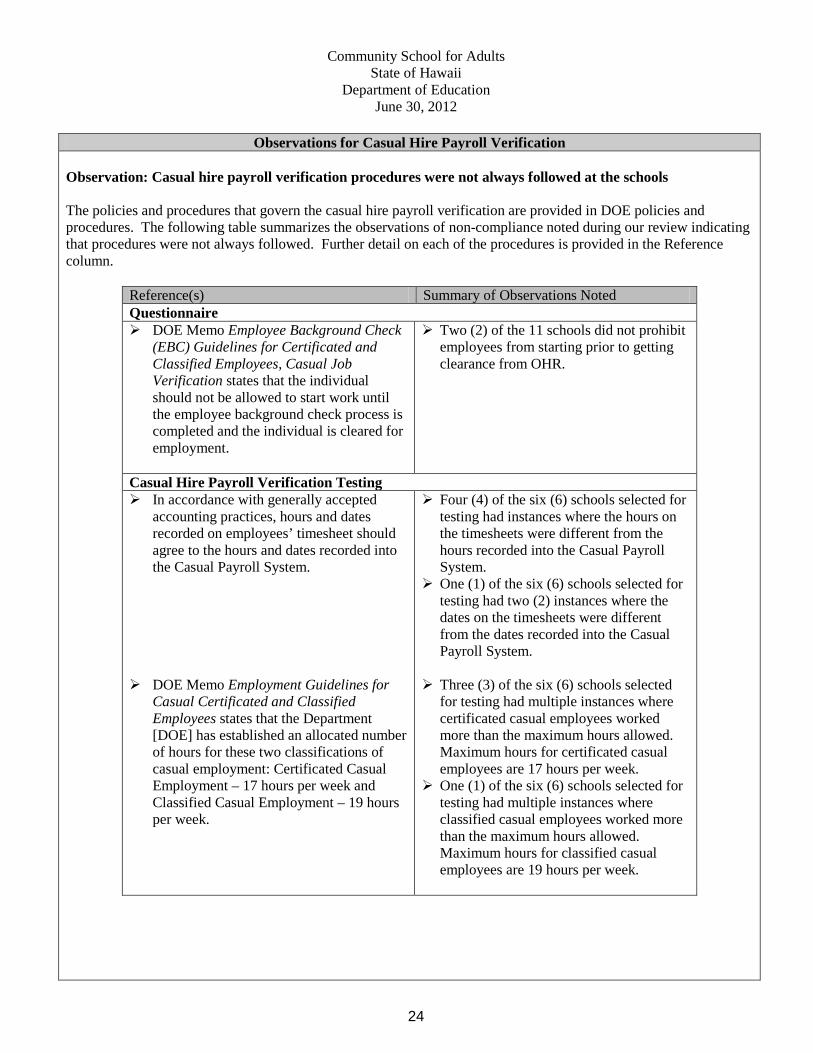

Observations for Casual Hire Payroll Verification Observation: Casual hire payroll verification procedures were not always followed at the schools The policies and procedures that govern the casual hire payroll verification are provided in DOE policies and procedures. The following table summarizes the observations of non-compliance noted during our review indicating that procedures were not always followed. Further detail on each of the procedures is provided in the Reference column.

Reference(s) Summary of Observations Noted Questionnaire DOE Memo Employee Background Check

(EBC) Guidelines for Certificated and Classified Employees, Casual Job Verification states that the individual should not be allowed to start work until the employee background check process is completed and the individual is cleared for employment.

Two (2) of the 11 schools did not prohibit employees from starting prior to getting clearance from OHR.

Casual Hire Payroll Verification Testing In accordance with generally accepted

accounting practices, hours and dates recorded on employees’ timesheet should agree to the hours and dates recorded into the Casual Payroll System.

DOE Memo Employment Guidelines for Casual Certificated and Classified Employees states that the Department [DOE] has established an allocated number of hours for these two classifications of casual employment: Certificated Casual Employment – 17 hours per week and Classified Casual Employment – 19 hours per week.

Four (4) of the six (6) schools selected for testing had instances where the hours on the timesheets were different from the hours recorded into the Casual Payroll System.

One (1) of the six (6) schools selected for testing had two (2) instances where the dates on the timesheets were different from the dates recorded into the Casual Payroll System.

Three (3) of the six (6) schools selected for testing had multiple instances where certificated casual employees worked more than the maximum hours allowed. Maximum hours for certificated casual employees are 17 hours per week.

One (1) of the six (6) schools selected for testing had multiple instances where classified casual employees worked more than the maximum hours allowed. Maximum hours for classified casual employees are 19 hours per week.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

25

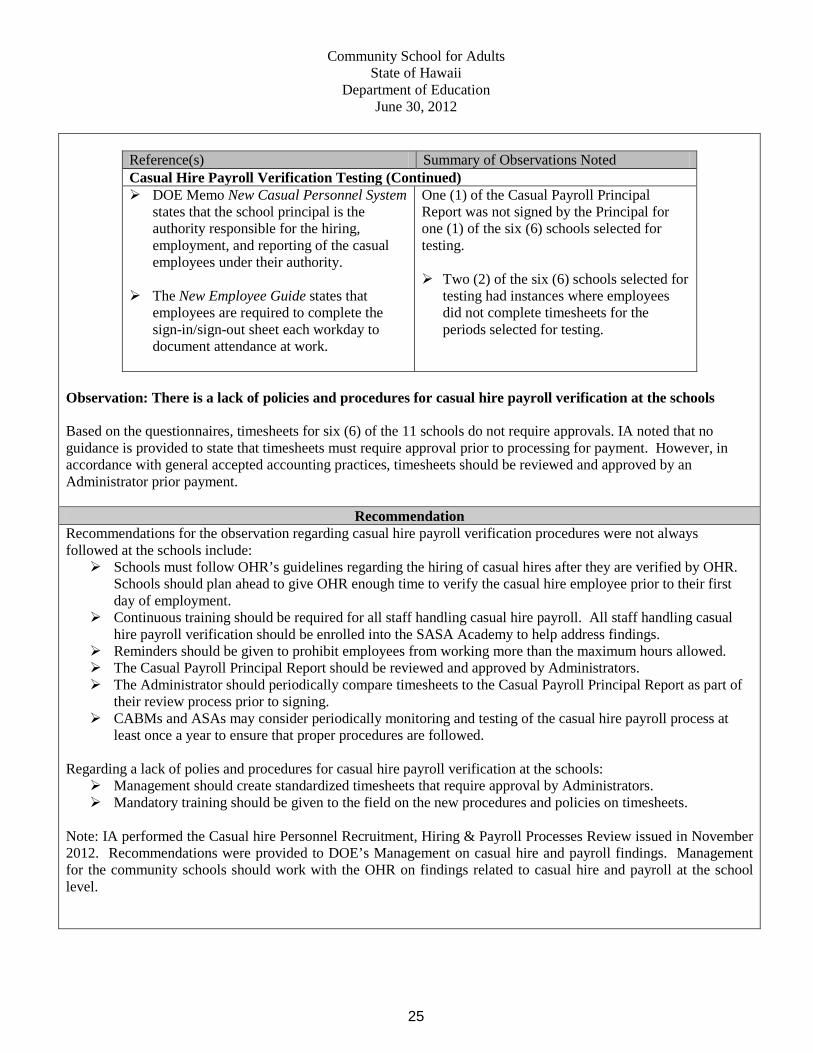

Reference(s) Summary of Observations Noted Casual Hire Payroll Verification Testing (Continued) DOE Memo New Casual Personnel System

states that the school principal is the authority responsible for the hiring, employment, and reporting of the casual employees under their authority.

The New Employee Guide states that employees are required to complete the sign-in/sign-out sheet each workday to document attendance at work.

One (1) of the Casual Payroll Principal Report was not signed by the Principal for one (1) of the six (6) schools selected for testing. Two (2) of the six (6) schools selected for

testing had instances where employees did not complete timesheets for the periods selected for testing.

Observation: There is a lack of policies and procedures for casual hire payroll verification at the schools Based on the questionnaires, timesheets for six (6) of the 11 schools do not require approvals. IA noted that no guidance is provided to state that timesheets must require approval prior to processing for payment. However, in accordance with general accepted accounting practices, timesheets should be reviewed and approved by an Administrator prior payment.

Recommendation Recommendations for the observation regarding casual hire payroll verification procedures were not always followed at the schools include: Schools must follow OHR’s guidelines regarding the hiring of casual hires after they are verified by OHR.

Schools should plan ahead to give OHR enough time to verify the casual hire employee prior to their first day of employment.

Continuous training should be required for all staff handling casual hire payroll. All staff handling casual hire payroll verification should be enrolled into the SASA Academy to help address findings.

Reminders should be given to prohibit employees from working more than the maximum hours allowed. The Casual Payroll Principal Report should be reviewed and approved by Administrators. The Administrator should periodically compare timesheets to the Casual Payroll Principal Report as part of

their review process prior to signing. CABMs and ASAs may consider periodically monitoring and testing of the casual hire payroll process at

least once a year to ensure that proper procedures are followed. Regarding a lack of polies and procedures for casual hire payroll verification at the schools: Management should create standardized timesheets that require approval by Administrators. Mandatory training should be given to the field on the new procedures and policies on timesheets.

Note: IA performed the Casual hire Personnel Recruitment, Hiring & Payroll Processes Review issued in November 2012. Recommendations were provided to DOE’s Management on casual hire and payroll findings. Management for the community schools should work with the OHR on findings related to casual hire and payroll at the school level.

Community School for Adults State of Hawaii

Department of Education June 30, 2012

26

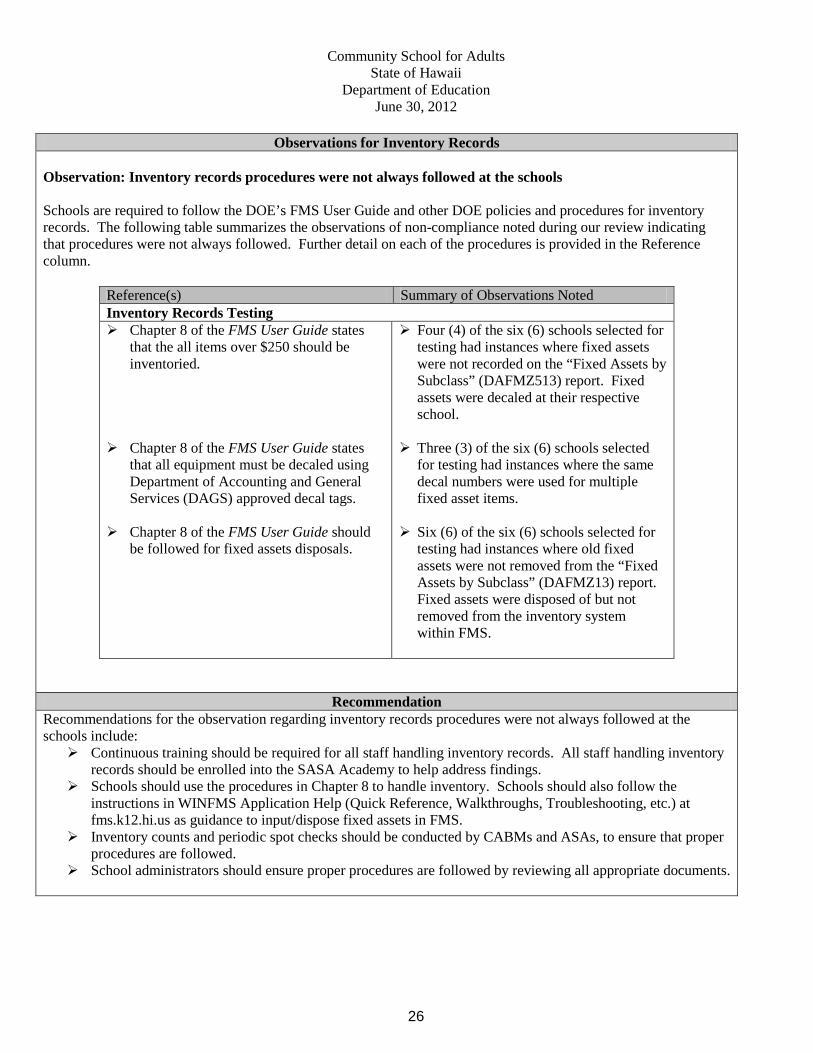

Observations for Inventory Records Observation: Inventory records procedures were not always followed at the schools Schools are required to follow the DOE’s FMS User Guide and other DOE policies and procedures for inventory records. The following table summarizes the observations of non-compliance noted during our review indicating that procedures were not always followed. Further detail on each of the procedures is provided in the Reference column.

Reference(s) Summary of Observations Noted Inventory Records Testing Chapter 8 of the FMS User Guide states

that the all items over $250 should be inventoried.

Chapter 8 of the FMS User Guide states that all equipment must be decaled using Department of Accounting and General Services (DAGS) approved decal tags.

Chapter 8 of the FMS User Guide should be followed for fixed assets disposals.

Four (4) of the six (6) schools selected for testing had instances where fixed assets were not recorded on the “Fixed Assets by Subclass” (DAFMZ513) report. Fixed assets were decaled at their respective school.

Three (3) of the six (6) schools selected for testing had instances where the same decal numbers were used for multiple fixed asset items.

Six (6) of the six (6) schools selected for

testing had instances where old fixed assets were not removed from the “Fixed Assets by Subclass” (DAFMZ13) report. Fixed assets were disposed of but not removed from the inventory system within FMS.

Recommendation Recommendations for the observation regarding inventory records procedures were not always followed at the schools include: Continuous training should be required for all staff handling inventory records. All staff handling inventory

records should be enrolled into the SASA Academy to help address findings. Schools should use the procedures in Chapter 8 to handle inventory. Schools should also follow the

instructions in WINFMS Application Help (Quick Reference, Walkthroughs, Troubleshooting, etc.) at fms.k12.hi.us as guidance to input/dispose fixed assets in FMS.

Inventory counts and periodic spot checks should be conducted by CABMs and ASAs, to ensure that proper procedures are followed.

School administrators should ensure proper procedures are followed by reviewing all appropriate documents.