Embed Size (px)

Citation preview

JOHANNES KEPLER UNIVERSITY LINZ Altenberger Str. 69 4040 Linz, Austria www.jku.at DVR 0093696

Submitted by

Michaela Trierweiler

Submitted at

Department of Business Informatics – Information Engineering

Supervisor

Assoz. Univ.-Prof. Mag. Dr. René Riedl

July 2019

EVALUATION THE USE OF BIG DATA ANALYTICS TO FACILITATE COMPLIANCE AND FRAUD PREVENTION An empirical study about usefulness and usage of big data analytics to prevent occupational fraud in German speaking companies

Master Thesis to obtain the academic degree of

Master of Science (MSc) in the Master’s Program

Business Informatics

08. July 2019 Michaela K. Trierweiler 2/103

STATUTORY DECLARATION

I hereby declare that the thesis submitted is my own unaided work, that I have not used sources other than those indicated, and that all direct and indirect sources are acknowledged as references. This printed thesis is identical to the electronic version submitted. Utting am Ammersee, 08.07.2019 Signature, Michaela Trierweiler

NOTE

This work contains parts in the German language when the content is related to direct cited references like laws and figures and when describing the empirical part in order to demonstrate the terms used for the online-survey without any bias. Headlines and terms within the result charts a with bi-lingual descriptions in German and English when terms are not common in both languages. This makes it possible to use the same figures regardless of a reader´s language and to keep just one version of them for the sake of consistency.

08. July 2019 Michaela K. Trierweiler 3/103

ABSTRACT

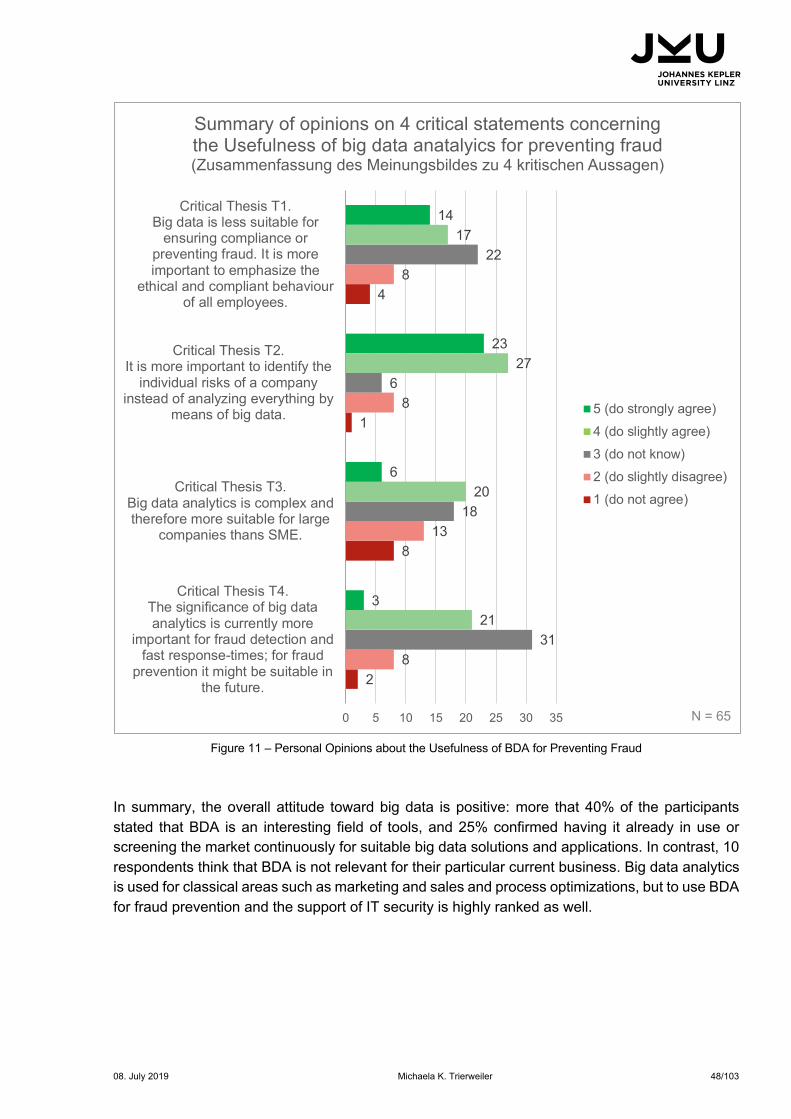

Motivation and Problem Statement: In the context of increasing digitalization and the worldwide increasing number of cases of occupational fraud – in combination with internet crime – this master’s thesis evaluates and discusses the question of how big data analytics methods are used to minimize any risk of losses by preventing fraud and ensuring compliance with appropriate countermeasures. Approach: As a study with practical impact or insights, the evaluation of the usefulness of big data analytics for compliance reasons and fraud prevention was conducted as a multi-step empirical study starting with expert interviews and combining the results with aspects found in literature and own experiences to spread an online survey among companies in the German-speaking area. The main participants were managing directors, compliance or fraud managers, or came from information technology-related departments. In total, 75% of the respondents came from research-relevant functions. Results: This study shows that information technology-based and analytical fraud prevention and detection measures are less widely distributed than traditional human-related or organizational measures and activities. But even small and medium enterprises can benefit from big data analytics as a countermeasure, and some small enterprises are already using big data techniques in the area of fraud risk management. However, significant skepticism about the value of big data methods to prevent fraud is recognizable, and there is uncertainty about the company’s capability to cope with big data analytics. The three most common obstacles to using big data techniques are limited information technology resources, the need for too-specific knowledge the company cannot afford, and the high complexity during implementation and daily usage. Classical and established technical countermeasures like access restrictions and regular software updates are viewed as more suitable and practicable for the companies’ risk and fraud management. Conclusions: Big data analytics, as part of information technology-based anti-fraud mechanisms, needs to be embedded within the governance, risk, and compliance strategy of a company. It is part of a mixture of different mechanisms and concepts containing technical, organizational, and people-related fraud prevention countermeasures and activities. The outcome of this research contributes to the future development of an anti-fraud framework in further research projects by providing insights from practitioners as a first-hand information base. Keywords: Big data, fraud prevention, compliance, corporate governance, analytics, IT-security, anti-fraud-management, MTO, GRC

08. July 2019 Michaela K. Trierweiler 4/103

Glossary 2FA two-factor authentication ACFE American Association of Certified Fraud Examiners; www.acfe.com aka also known as AI artificial intelligence AT ISO country code for Austria B2B business-to-business: business relationships with other companies B2C business-to-consumer: business relationships with private persons BDA big data analytics BI business intelligence Bitkom Bundesverband Informationswirtschaft, Telekommunikation und neue

Medien e. V.; www.bitkom.org ca. circa, approximatly CH ISO country code for Switzerland CIO chief information officer CISO chief information security officer COBIT Control Objectives for Information and Related Technology: international

framework for IT governance COSO The Committee of Sponsoring Organization of the Treadway Commission DACH a common acronym for Germany–Austria–Switzerland DE ISO country code for Germany DICO e.V. German Institution of Compliance/Deutsches Institut für Compliance e.V;

www.dico-ev.de DOA delegation of authority (EU-)GDPR The European General Data Protection Regulation (effective since May 26th,

2018) E&Y Ernst & Young (auditing firm) ERM enterprise risk management ERP enterprise resource planning systems EUR Euro (currency) FDA forensic data analytics GRC governance, risk, and compliance I-1, I-2, I-3 acronyms for the expert interview partners ICS | IKS internal control system | Internes Kontrollsystem IIA Austria Austrian Institution for internal Revision/Institut für Interne Revision

Österreich; https://www.internerevision.at IOT internet of things IP internet protocol KDD knowledge discovery in databases: a basic principle to extract information

out of existing data developed by Kononenko et al. in 2007

08. July 2019 Michaela K. Trierweiler 5/103

KPI key performance indicator KPMG KPMG (auditing firm) M&A merger and acquisition (process) Mio. million MTO man–technology–organization (based on the MTO concept of Strohm and

Ulich) NPO non-profit organization PDF portable document format PIR personal information record (related to GDPR) PwC Price Waterhouse Coopers (auditing firm) ROI return on investment RQ research question SAP/SAP HANA brands from SAP corporation, an ERP software developer SIU Special Investigation Unit SLR systematic literature review (based on the concepts of Kitchenham et al.) SME small and medium enterprises SOX compliance rules according to the Sarbanes-Oxley Act of 2002: relevant and

obligatory for stock-listed companies in the United States URL uniform resource locator

08. July 2019 Michaela K. Trierweiler 6/103

TABLE OF CONTENTS

Glossary ......................................................................................................................................... 4 1. Problem Definition and Theoretical Background ..................................................................... 8

1.1 Introduction ...................................................................................................................... 8 1.2 Problem Definition and Validation ................................................................................... 9

1.2.1 Context and Motivation ......................................................................................... 9 1.2.2 Scope of the Research and Use of the MTO Concept ....................................... 10 1.2.3 Fraud Theory: Types and Dimensions of Occupational Fraud ........................... 11 1.2.4 Anti-Fraud Management ..................................................................................... 16 1.2.5 Definition of BDA in the Context of this Research .............................................. 18 1.2.6 Fraud Prevention with Big Data .......................................................................... 21

1.3 Aim and Research Questions ........................................................................................ 23 2 Methodology ......................................................................................................................... 24

2.1 Research Process – Mixed Method Approach .............................................................. 24 2.2 Use of Terms ................................................................................................................. 25 2.3 Methods of Data Collection and Analysis ...................................................................... 26

2.3.1 Questioning Techniques ..................................................................................... 26 Interview ............................................................................................................. 26 Questionnaire/Survey ......................................................................................... 27

2.3.2 Analytical Methods ............................................................................................. 30 Qualitative Content Analysis .............................................................................. 30 Quantitative Content Analysis ............................................................................ 31

2.4 Literature Research ....................................................................................................... 33 2.5 Realization of Preliminary-Study – Expert Interviews .................................................... 34 2.6 Realization of Online Survey – Quantitative Research .................................................. 36

3 Results .................................................................................................................................. 39 3.1 Results of the Pre-Study and Implications for This Research ....................................... 39 3.2 Results of the Online Survey: Summary and Highlights ................................................ 41

3.2.1 Summary and Highlights: Participant Structure .................................................. 42 3.2.2 Summary and Highlights: Fraud Management Status ........................................ 43 3.2.3 Summary and Highlights: Use of Big Data ......................................................... 46

4 Discussion ............................................................................................................................. 49 4.1 Answer to Research Question 1: Summary of Established Fraud Prevention

Mechanisms and Activities ............................................................................................ 49 4.2 Answer to Research Question 2: The Value of Big Data for Fraud Prevention and

Compliance Mechanisms .............................................................................................. 52 4.3 Answer to Research Question 3: Carryover to SMEs ................................................... 57 4.4 Big Data in the Context of an MTO-Based Anti-Fraud Framework ............................... 57 4.5 Conclusion and Further Implications ............................................................................. 58

5 Summary ............................................................................................................................... 60

08. July 2019 Michaela K. Trierweiler 7/103

6 List of Tables ......................................................................................................................... 63 7 List of Figures ....................................................................................................................... 63 8 References ............................................................................................................................ 64 9 Appendices ........................................................................................................................... 71

9.1 Design and Structure of the Online Questionnaire ........................................................ 71 9.2 Online Survey, Examples of Addressing potential Participants ..................................... 82 9.3 Literature Search Strategy ............................................................................................. 84 9.4 Full Set of Result Charts of the Online Survey .............................................................. 85

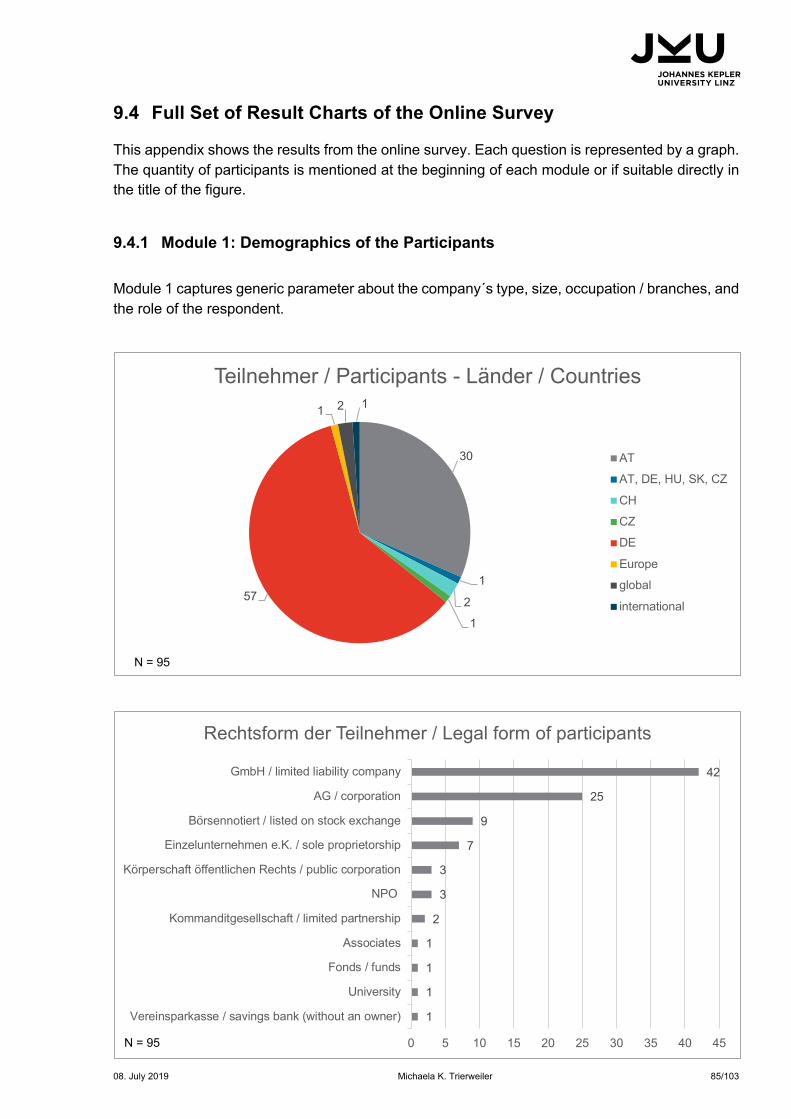

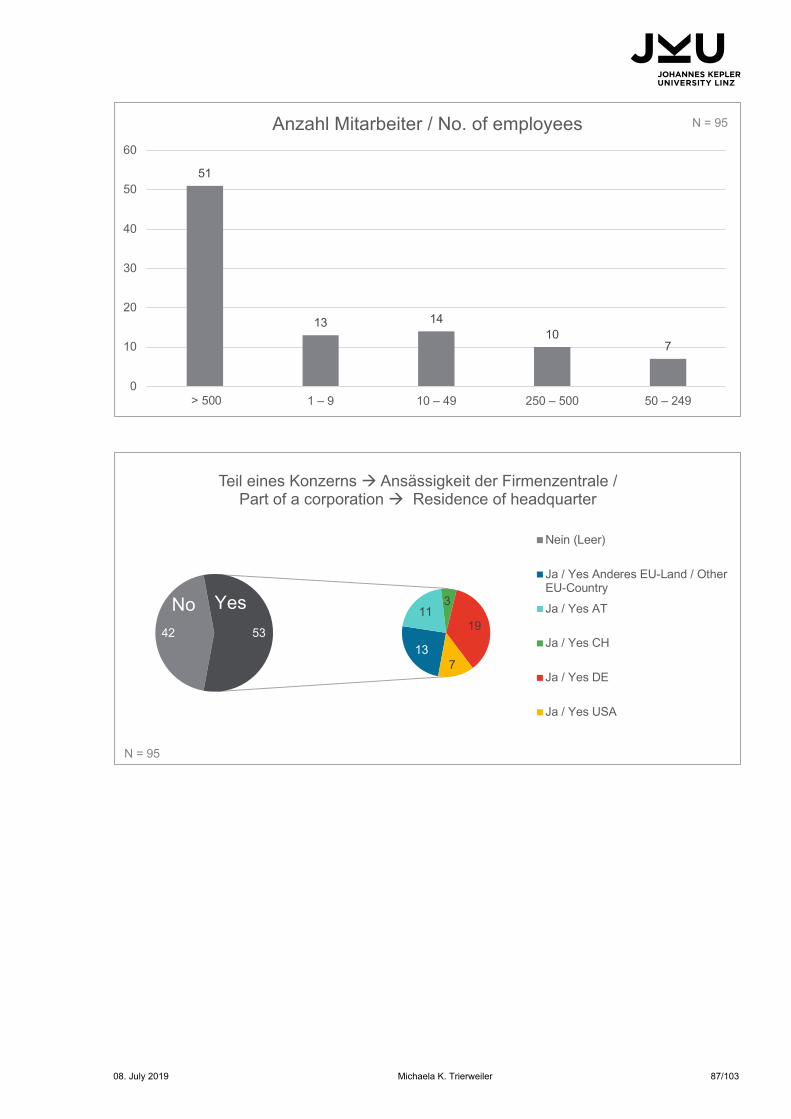

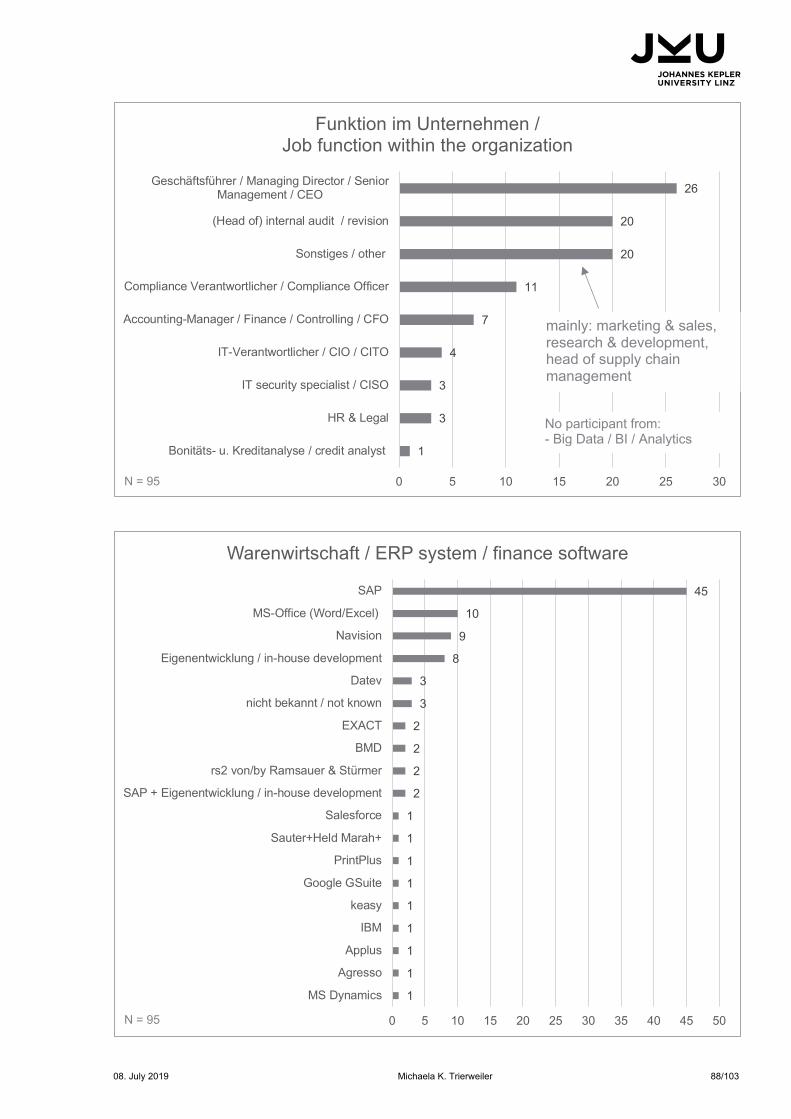

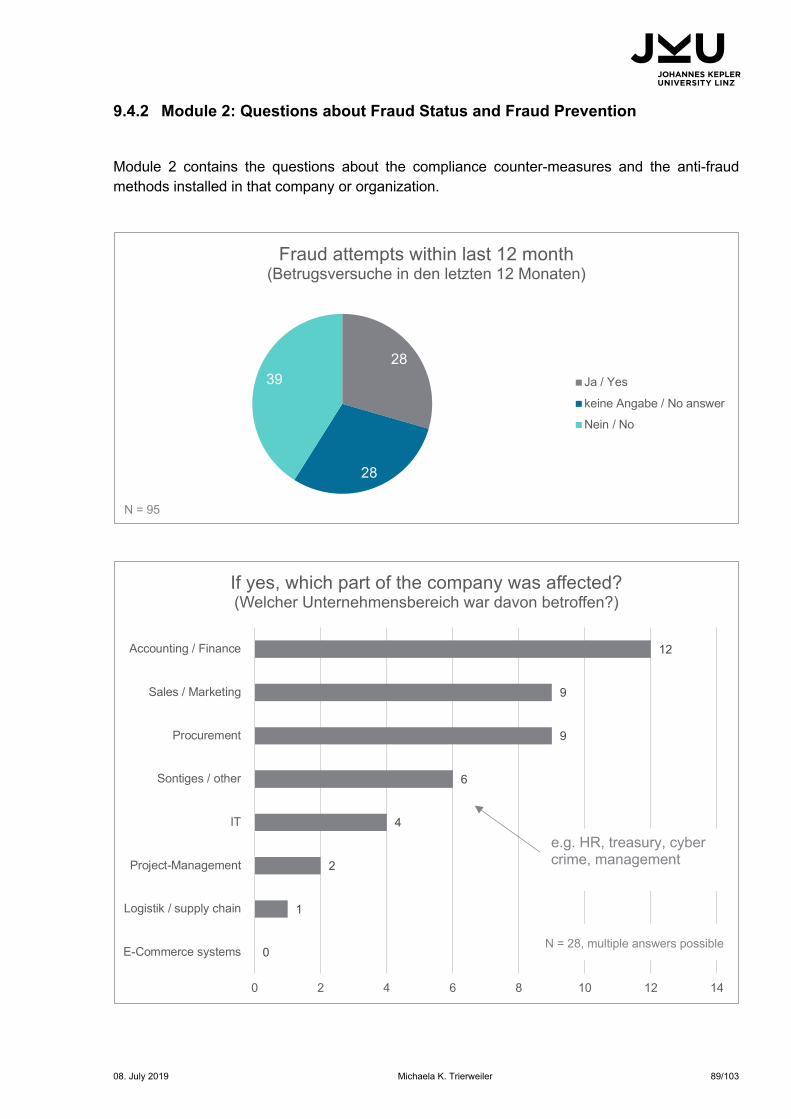

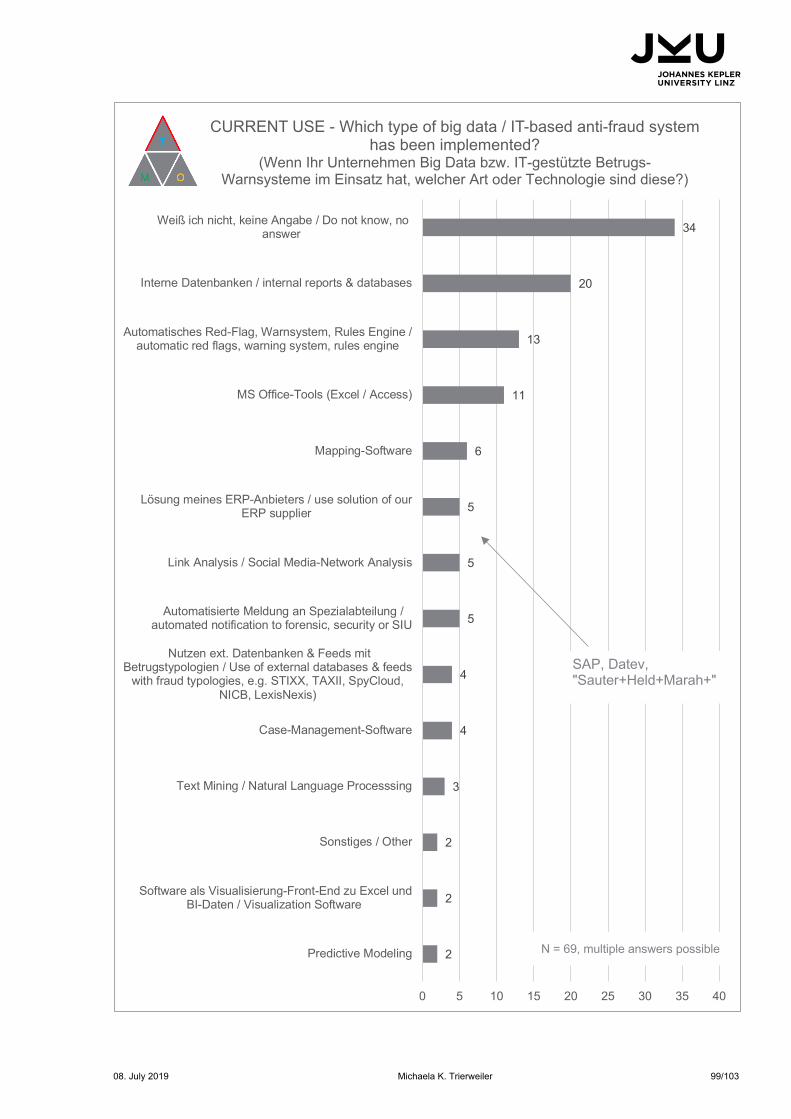

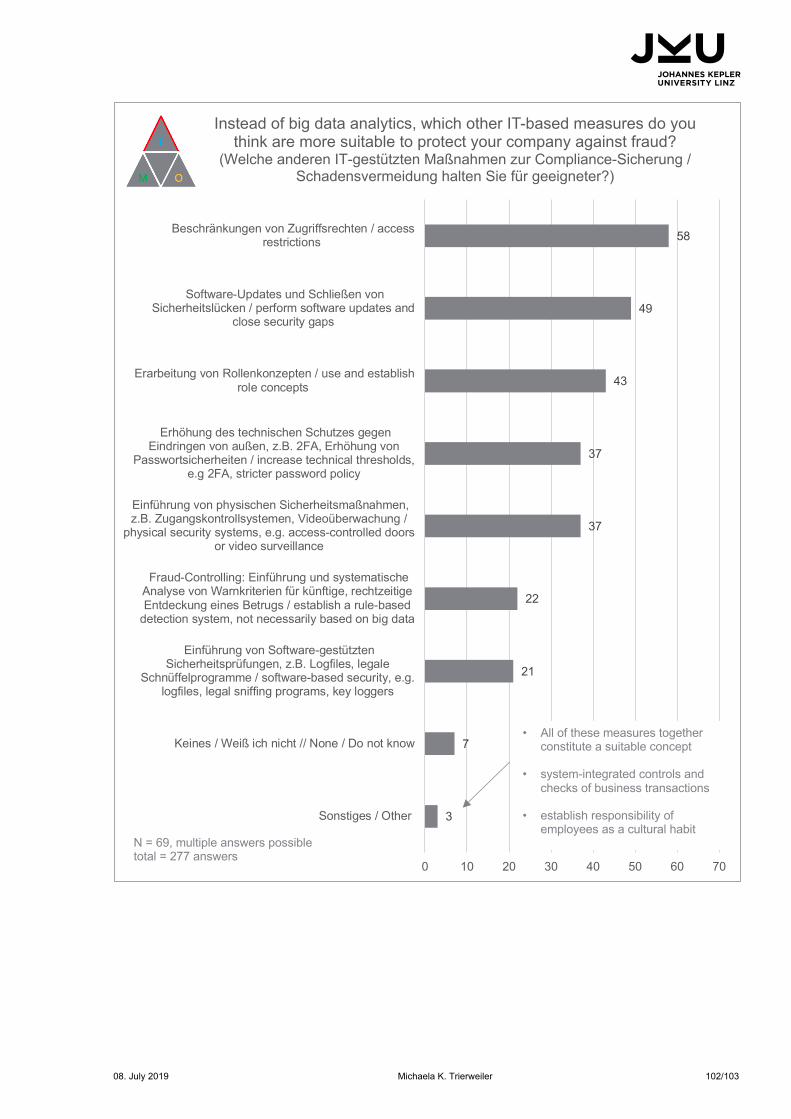

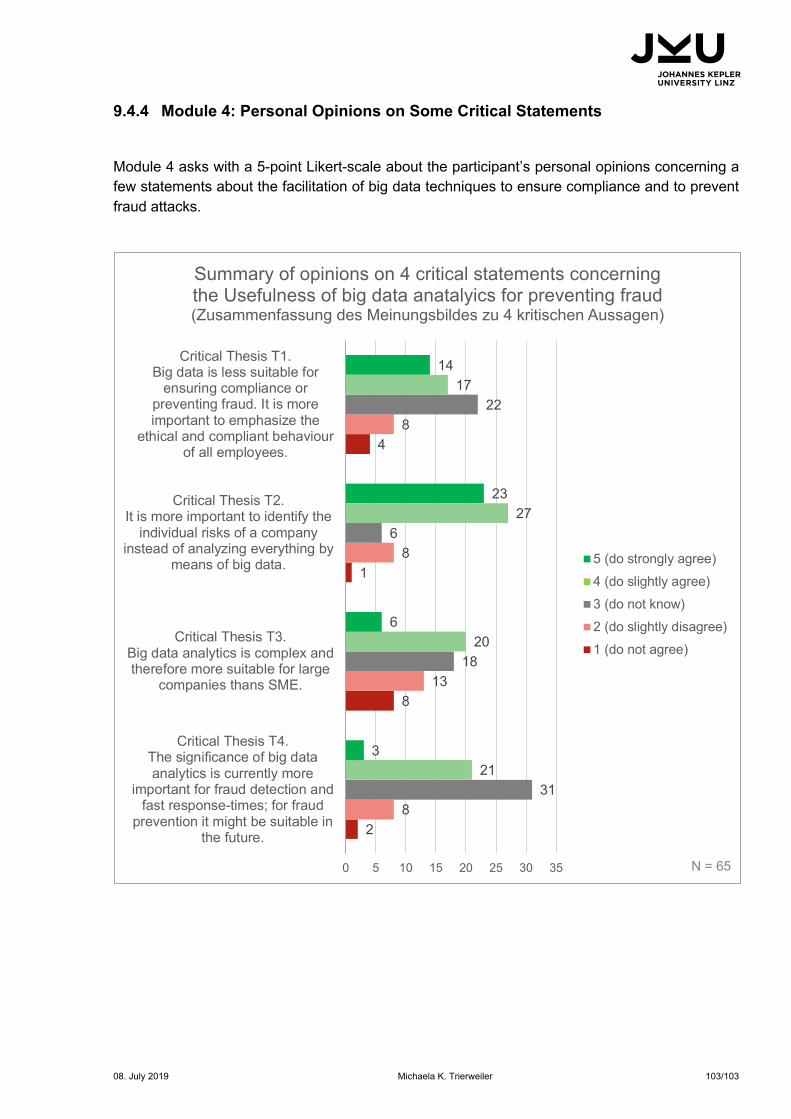

9.4.1 Module 1: Demographics of the Participants ...................................................... 85 9.4.2 Module 2: Questions about Fraud Status and Fraud Prevention ....................... 89 9.4.3 Module 3: Questions about the Use of Big Data Analytics ................................. 96 9.4.4 Module 4: Personal Opinions on Some Critical Statements ............................. 103

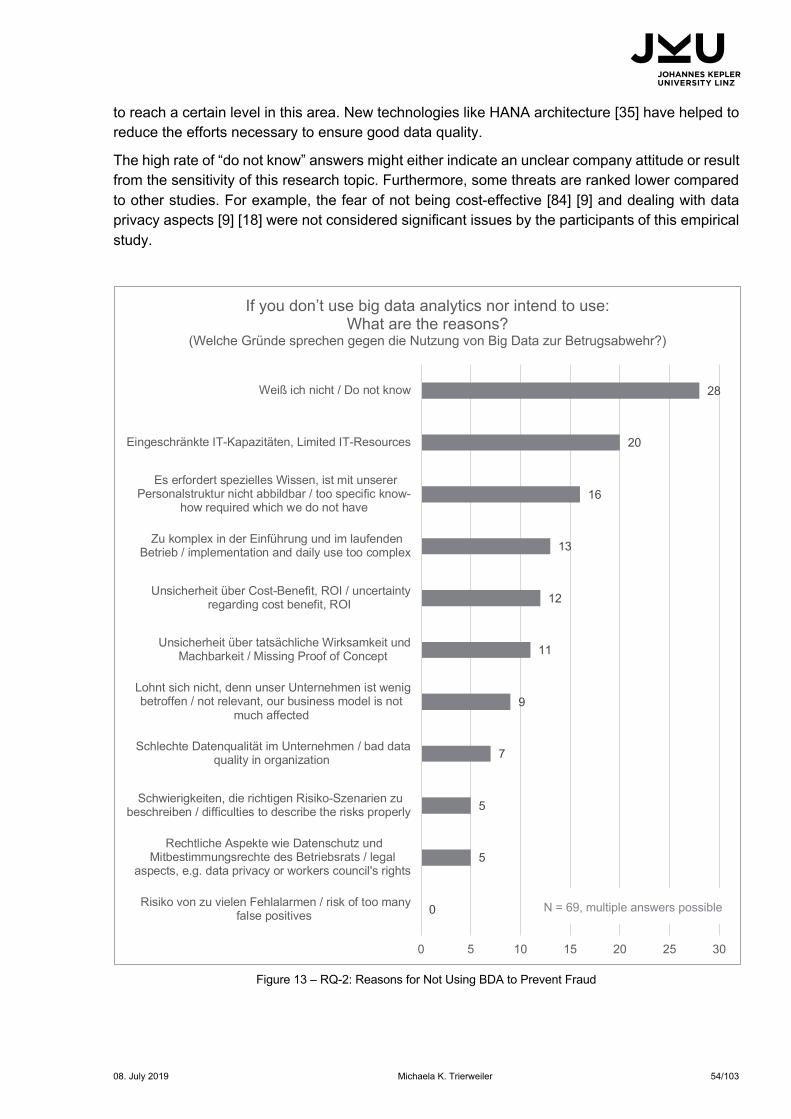

08. July 2019 Michaela K. Trierweiler 8/103

1. Problem Definition and Theoretical Background 1.1 Introduction

Compliant and ethical behavior should be natural in human and business interactions and therefore implicit in corporate structures and organizations as well. However, increasing – or at least more frequently detected – cases of occupational misbehavior, such as bribery, corruption, accounting fraud, credit card fraud, phishing, malware, and hacking attacks, paired with identity fraud [1] [2] [3] [4], suggest the opposite. New business models based on more technology, such as brokerage services are conducted remotely, often as cross-border transactions, and thus are becoming more anonymous. The identification of someone’s identity and trustworthiness is more and more difficult to capture. For instance, psychological barriers to committing fraud lower with the spatial distance of using internet shops and E-commerce platforms [5]. This development enables new kinds of fraud based on technology and forces organizations to adapt and upgrade their countermeasures.

In the private arena, people are presenting more and more personal details on social media platforms, e.g. by registering their profiles on various online platforms, by asking search engines for information, and by storing private data in digital clouds rather than locally. In consequence, people are presenting more and more behavior, attitudes, and preferences to the public and allowing the capture and storage of these data and information in large databases within the internet or cloud platforms.

Analytical methods for dealing with large amounts of data have developed during the last few years, as for data are assumed to be the new goldmine. Big data analytics (BDA) has reached a grade of maturity, and lots of analytical software is available. According to some recent studies or symposiums, BDA – often in the sense of predictive analytics – is mostly used for sales prediction and customer behavior analysis to fine-tune the marketing strategy and invent new products and services [6] [7] [8], or for other traditional business decisions by increasing transparency of existing data [9], simple to earn money with it. But BDA is only little implemented for risk management purposes [7] [9] [10]. Another field of use is the field of predictive maintenance for optimized machine services, the better synchronization of logistics, and to secure a higher quality during production processes [11].

However, it may also be possible to use BDA not to earn money but to prevent the loss of money. For instance, Heißner and Benecke think that intelligent big data technology used by experienced analysts is already capable of predicting a crime with its likelihood, the affected company’s division, and the place and time it is to happen [12]. Fraud data analytics could even help to identify fraudulent billing schemes committed via shell companies [13], to identify mobile phone fraud and identity theft [14], or even detect click fraud [15].

Establishing information technology (IT)-based anti-fraud-mechanisms is an investment a company must make, and if it works, the lever could be a big one: any coin not lost needs not to be earned with other customers. Not to ignore the damage on a company’s image and reliability once a fraud or hacking attack has been known to the public.

Obviously, there are hotspots of fraud areas like credit card fraud [16] and the banking sector where BDA techniques [14] are established to help to prevent fraud or at least detect a fraud attempt as early as possible, but how is big data used in other areas of business? How useful is BDA seen, and how far is it already implemented in different types of companies? How much is

08. July 2019 Michaela K. Trierweiler 9/103

BDA established to prevent fraud and what other measures and anti-fraud activities are implemented in the German speaking business environment?

This thesis addresses these questions by conducting an empirical study. The next sections provide more details on the context and motivation, the aim of this research, its scope, and the research questions. For readers not familiar with anti-fraud management, it provides some definitions and sums up the main concepts, and it defines BDA in the context of this research. The further parts of this paper treat the research methods used, bridge their application for this study, and present and discuss the results. Finally, a conclusion and outlook for future research approaches is provided.

1.2 Problem Definition and Validation

This chapter provides details on the context and motivation and explains the theoretical backgrounds on fraud theory and BDA that are relevant to this research.

1.2.1 Context and Motivation The topic of IT-based anti-fraud and more analytical approaches has risen in the past few years. Earlier literature about fraud prevention often came from Anglo-American experts who have long-term practical experience. These textbooks mostly concentrate on explaining some dedicated analytics methods or on special fraud types connected to the banking sector or the financial accounting area. This is not surprising, because occupational fraud mostly originates in accounting departments [17] and was investigated by financial accountants from the beginning in sensitive business functions to ensure correct tax payments to the government. Thus, well-known auditing firms1 have been engaged here for a long time and are increasing their business efforts in forensic and fraud detection services as a field of additional consultancy services. In parallel, more and more companies are installing functions like compliance officers and fraud prevention managers to deal with these threads, to ensure ethical business standards, and to follow legal authorities’ request to install such functions. People working in these capacities can exchange knowledge within certain circles and associations like the German Institution for Compliance (DICO e.V.), the Austrian Institution for Internal Revision (IIA Austria), and the American Association of Certified Fraud Examiners (ACFE). The ACFE has defined some standards regarding types of occupational fraud and how to deal with them.

In the present day, dealing with occupational fraud has become a much wider field than just looking into accounting fraud, bribery, or corruption because of the constantly increasing technology-based fraud attacks like credit card fraud and phishing attacks using identity theft and social engineering methods. Digitalization creates new opportunities but also introduces new risks related to data protection, data privacy compliance, and cyber breaches [18]. Companies need to arm themselves against more technologically skilled fraudsters and e-crime attacks. Small and medium enterprises (SMEs) with specialized knowledge are interesting to hackers because they are assumed not to be armed like larger companies [19]. According to the ACFE Report to Nation

1 Ernst & Young (E&Y), KPMG, Price Waterhouse Coopers (PwC), and Deloitte

08. July 2019 Michaela K. Trierweiler 10/103

2016, this gap in fraud prevention and detection leaves small companies unimmunized and at a high risk of significant damage to their limited resources [17].

If BDA is viewed in the sense of being part of IT-based anti-fraud mechanisms, it needs to be embedded within and connected to IT security and compliance efforts. Looking into use cases about companies’ investments in digitalization, an interview-based study from 2017 indicates with more than 50% mentions that there are significant interests in investments in the areas of security reporting and incident management, internet of things (IOT) security of cyber-physical systems, and, early warning systems and intrusion detection [20]. However, a KPMG study from 2016 indicates that this opportunity is not well noticed or used by companies, as only 3% of all fraud detections resulted from technical or analytical methods [10]. During my professional career, I was in contact with certain fraud prevention techniques several times and experienced the usefulness of such measures. However, I also recognized that most of them were more organizational countermeasures than technical ones.

The reasons that companies are not very interested in using technology or analytical methods to prevent fraud may include the complexity, the specific skills required, the questionable return on investment (ROI) [21], not enough pain (seeing themselves as not at risk), their underestimation of the situation and lack of awareness of legal consequences, or just having enough other counteractions already in place. Therefore, these reasons are one aspect discussed during this research. Another question connected to the situation is that different fraud types might require different countermeasures, and BDA in particular might only be useful in certain cases or certain industry segments.

1.2.2 Scope of the Research and Use of the MTO Concept This thesis discusses the state of implementation of IT-based anti-fraud systems, especially using BDA techniques, among German-speaking companies and organizations of different sizes and industry sectors. Anti-fraud management is part of compliance management; therefore, these terms are used synonymously in some parts of this work.

Companies must avoid fraud and work according to certain compliance standards, for instance the Sarbanes-Oxley Act of 2002 (SOX). In Austria and Germany, fraud is viewed as a criminal act and is punished with imprisonment. When using data to find a fraudster, the analysis might encounter personal information. This leads to the need to consider data privacy regulations like the European General Data Protection Regulation (EU-GDPR) or to involve workers’ councils [22] [23]. However, to discuss those different legal aspects would go far beyond the scope of this research work and was therefore left out. In practice, organizations must design procedures and governance structures to act in legal compliance when searching and analyzing data [24].

When establishing a powerful anti-fraud management system, a company must consider different aspects related to project management, stakeholder management, risk analysis, segregation of duty, and education. Besides these soft factors of organizational and human-related factors, a comprehensive anti-fraud management system is now also connected to IT security and data analytics aspects. This combination of soft factors and IT-related factors leads to my opinion that an anti-fraud management system is a sociotechnical system in the sense of Strohm and Ulich’s [25] man–technology–organization (MTO) concept, because to optimize anti-fraud management concepts in an enterprise means a joint optimization of the application of technology, the organization, and the people working there. Therefore, when this research touches on the different types of fraud prevention measures established in an organization, the MTO concept is used for

08. July 2019 Michaela K. Trierweiler 11/103

classification and better understanding of the participants of the empirical part of this research and for the readers of this thesis. This classification is mentioned verbal and indicated in the relevant result figures with a small thumbnail consisting of a triangle representing the three dimensions MTO. This research does not discuss or evaluate the reasons and motivations for people to commit fraud; these are given as background information in the theory part of this thesis.

1.2.3 Fraud Theory: Types and Dimensions of Occupational Fraud This section provides a short introduction to occupational fraud and describes the main aspects by giving some definitions and explaining the main types of fraud and what facilitates a fraudulent action.

Legally, fraud is part of the white-collar crime area, and the main elements of fraud are intention, deception, and damage to another party in the sense of financial loss. For example, §263 of the German Strafgesetzbuch defines fraud as follows and has even enlarged this element of crime with §263a for computational fraud by manipulating digital data [26] and mentions some specific fraud types in subsequent paragraphs:

“Wer in der Absicht, sich oder einem Dritten einen rechtswidrigen Vermögensvorteil zu verschaffen, das Vermögen eines anderen dadurch beschädigt, daß er durch Vorspiegelung falscher oder durch Entstellung oder Unterdrückung wahrer Tatsachen einen Irrtum erregt oder unterhält, wird mit Freiheitsstrafe bis zu fünf Jahren oder mit Geldstrafe bestraft.” [27]

The Austrian Strafgesetzbuch defines fraud similarly in §146 as shown below. It regulates several grades of severity in §147f and mentions especially fraud by abuse data processing in §148a:

“Wer mit dem Vorsatz, durch das Verhalten des Getäuschten sich oder einen Dritten unrechtmäßig zu bereichern, jemanden durch Täuschung über Tatsachen zu einer Handlung, Duldung oder Unterlassung verleitet, die diesen oder einen anderen am Vermögen schädigt, ist mit Freiheitsstrafe bis zu sechs Monaten oder mit Geldstrafe bis zu 360 Tagessätzen zu bestrafen.” [28]

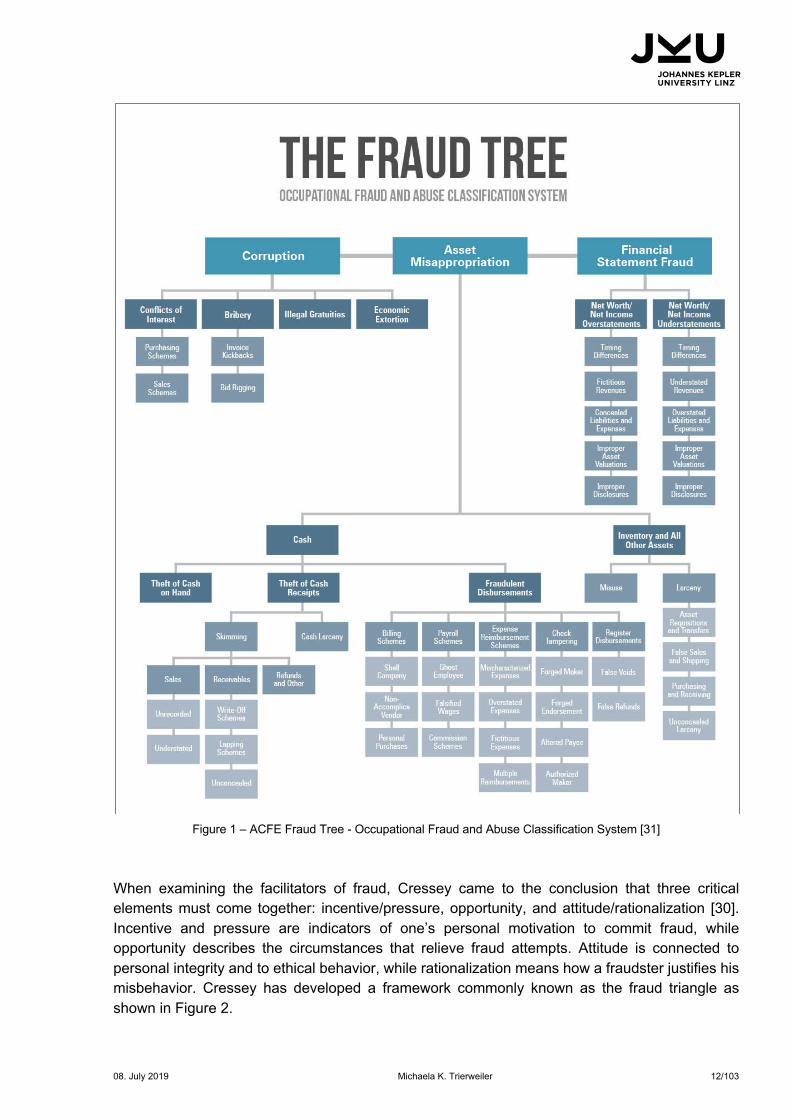

The bandwidth of white-collar crime is huge and includes delicts that harm a company directly, such as stealing paper or paying too much salary, as well as delicts that look good for a company at first glance, such as corruption to gain a large profitable deal [29]. For a better differentiation of the different kinds of fraud in business contexts, Joseph T. Wells, founder of the ACFE, developed in 2007 a classification system for occupational fraud – informally known as the “fraud tree” – that covers most kinds of misconduct of executives, managers, and employees of organizations [30]. This tree model was refined over the years and is now viewed as one of the state-of-the-art definition concepts. Common to all versions is the split into three main types: corruption, asset misappropriation, and financial statement fraud (aka accounting fraud). Figure 1 shows the current taxonomy tree available on the ACFE’s webpage.

All these types of fraud could be summarized under the definition of non-compliant behavior, meaning behavior that is corporately and social inadequate and therefore not wished for because it harms a company [29] or an individual. This generic perception that fraud is equal to divergent behavior gives the first indication of what fraud analytics must focus on: calculating and finding behavior and patterns that do not match against existing and defined standards.

08. July 2019 Michaela K. Trierweiler 12/103

Figure 1 – ACFE Fraud Tree - Occupational Fraud and Abuse Classification System [31]

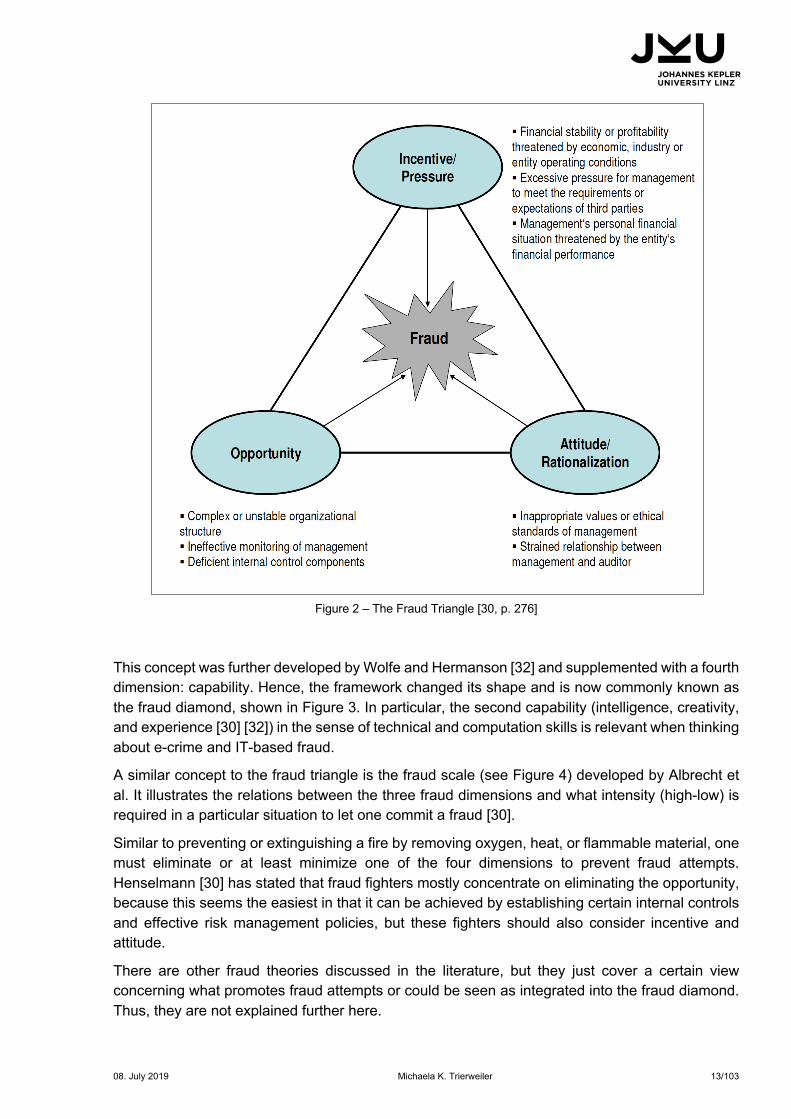

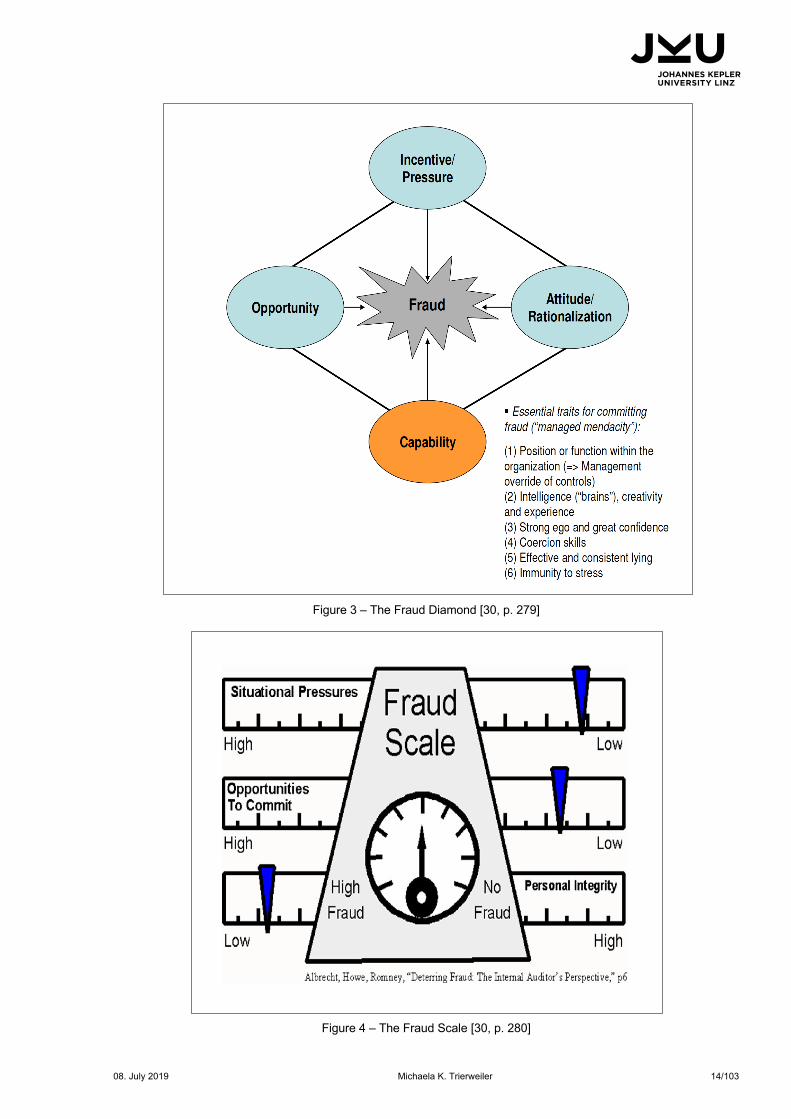

When examining the facilitators of fraud, Cressey came to the conclusion that three critical elements must come together: incentive/pressure, opportunity, and attitude/rationalization [30]. Incentive and pressure are indicators of one’s personal motivation to commit fraud, while opportunity describes the circumstances that relieve fraud attempts. Attitude is connected to personal integrity and to ethical behavior, while rationalization means how a fraudster justifies his misbehavior. Cressey has developed a framework commonly known as the fraud triangle as shown in Figure 2.

08. July 2019 Michaela K. Trierweiler 13/103

Figure 2 – The Fraud Triangle [30, p. 276]

This concept was further developed by Wolfe and Hermanson [32] and supplemented with a fourth dimension: capability. Hence, the framework changed its shape and is now commonly known as the fraud diamond, shown in Figure 3. In particular, the second capability (intelligence, creativity, and experience [30] [32]) in the sense of technical and computation skills is relevant when thinking about e-crime and IT-based fraud.

A similar concept to the fraud triangle is the fraud scale (see Figure 4) developed by Albrecht et al. It illustrates the relations between the three fraud dimensions and what intensity (high-low) is required in a particular situation to let one commit a fraud [30].

Similar to preventing or extinguishing a fire by removing oxygen, heat, or flammable material, one must eliminate or at least minimize one of the four dimensions to prevent fraud attempts. Henselmann [30] has stated that fraud fighters mostly concentrate on eliminating the opportunity, because this seems the easiest in that it can be achieved by establishing certain internal controls and effective risk management policies, but these fighters should also consider incentive and attitude.

There are other fraud theories discussed in the literature, but they just cover a certain view concerning what promotes fraud attempts or could be seen as integrated into the fraud diamond. Thus, they are not explained further here.

08. July 2019 Michaela K. Trierweiler 14/103

Figure 3 – The Fraud Diamond [30, p. 279]

Figure 4 – The Fraud Scale [30, p. 280]

08. July 2019 Michaela K. Trierweiler 15/103

Theses major concepts of fraud theory describe from an abstract point of view what kinds of countermeasures are relevant and useful to minimize fraud and gain moral behavior.

For instance, the banking and insurance sector is already full of IT-based anti-fraud mechanisms embedded in a holistic governance, risk, and compliance (GRC) concept to minimize risks. If the IT-based risk assessment is combined with fraud detection research and analytical tools, the threat analysis could be enriched with real key figures, and the efficiency of IT-based anti-fraud controls could be automated, evaluated, and continuously fine-tuned [33].

Fraud can be executed internally, externally, or in collaboration. Figure 5 provides an example of internal and external fraud detection streams in the banking sector. It reduces the opportunity to commit fraud because a strong control component is active, realized by a real-time warning system [33]:

§ On the left side – internal fraud attempt: An employee does a balance inquiry from a non-active customer account > The employee looks for the age of this customer > The employee changes the address and contact details > The system generates a first warning > The employee transfers money from this bank account > The system generates an alert and attempt is stopped

§ On the right side – extern fraud attempt: A user makes a money withdrawal from a cash-point machine > The same user makes another money withdrawal at a second cash terminal > The system generates a first warning > The user makes a third attempt at a money withdrawal > The system generates an alert and attempt is stopped > The user’s cash card is disabled, and no further withdrawals are possible

Figure 5 – Fraud Prevention in Real Time – Example from Banking Sector [33, p. 143]

The interaction and relation of the four dimensions of the fraud diamond indicate already the complexity of fraud prevention. This raises the need for collaboration between different departments within an enterprise and the need to use different types of mechanisms to establish an effectively working fraud-prevention system. Therefore, a successful anti-fraud management system is a combination of people-related, technology-related, and organization-related (MTO) items whose characteristics are individually tailored to a company’s size, structure, and industry sector. Some major concepts for anti-fraud management systems are described in the next section.

08. July 2019 Michaela K. Trierweiler 16/103

1.2.4 Anti-Fraud Management Although management and every employee are responsible for compliant and ethical behavior on an individual level, there are some basic concepts about corporate anti-fraud management systems, and these kinds of concepts are described in this section.

Basically, effective anti-fraud management is relevant for every organization for three primary reasons:

§ To act according to current law standards § To avoid direct financial loss § To avoid indirect financial loss via bad publicity and loss of confidence from suppliers and

customers

Different functions and departments within an organization could be responsible to care about anti-fraud management and continuously develop this system, including compliance managers, fraud officers, and risk management, IT security, corporate governance, internal audit, and forensic departments [34] [23]. A working fraud management framework should be integrated into the GRC framework of an organization , but with a specific viewpoint: controls are derived from the examined risks to avoid malicious or fraudulent acts. These controls are implemented within the scope of the operational fraud management [35] [36]. Fraud management consists of all measures that help to prevent, detect, and investigate fraud. Therefore, fraud management has a preventive component as well as proactive and reactive components and is integrated into a company´s compliance management structure [37].

Hofmann [38], for instance, has developed a framework to prevent fraud based on the KPMG three-layer model. The three layers, shown Figure 6, consist of the inter-company level, the intra-company relations, and the political-legal environment. In his work, Hofmann has only focused on the intra-company part, meaning establishing organizational countermeasures and cultural, ethical standards, and on the political-legal situation. However, he has also stated that anti-fraud strategies are located at the interface between the five disciplines of business administration, jurisprudence, ethics, psychology, and sociology. According to Hofmann, it is key to integrate fraud management into the corporate risk management structure, register the individual fraud risks by probability and potential damage, and classify them, for instance, by structure, staff, and style.

Besides all of these organizational and soft countermeasures, an effective fraud-prevention program is supported by software tools in order to be able to detect fraudulent actions and even recognize them in advance to prevent them, especially when thinking on the inter-company level and about digital and automated business transactions and relations. Embedded real-time components enable short reaction times in combination with information for a high-quality decision. The goal is to target fraudulent activities with high damage potential. However, the IT-based fraud detection must be directly connected to the business processes; otherwise, a detection engine would not deliver the right suspect items to investigate [33].

The real-time fraud prevention example from above indicates one major concept of a fraud countermeasure: the warning signal analysis (e.g., red flag analysis or mapping against blacklists). When using this analytical method, predefined risk factors and standards such as thresholds, blacklisted accounts, embargo lists, etc. are determined. Those datasets that match these predefined factors or have a certain deviation from the standard are marked with a red flag to demonstrate the need for further investigation. Based on these flags, appropriate samples are collected [23]. This kind of IT-based fraud prevention is already common in the banking sector and allows for monitoring of currently running financial transactions, including stopping a suspicious

08. July 2019 Michaela K. Trierweiler 17/103

transaction that needs to be checked and then released or rejected [39] [40]. In case of the need to identify a certain pattern within the analyzed data, which is more complex than just comparing against a predefined filter, hypothesis testing methods are suitable [23].

Figure 6 – Three Layer Model of Anti-Fraud-Management [38, p. 54]

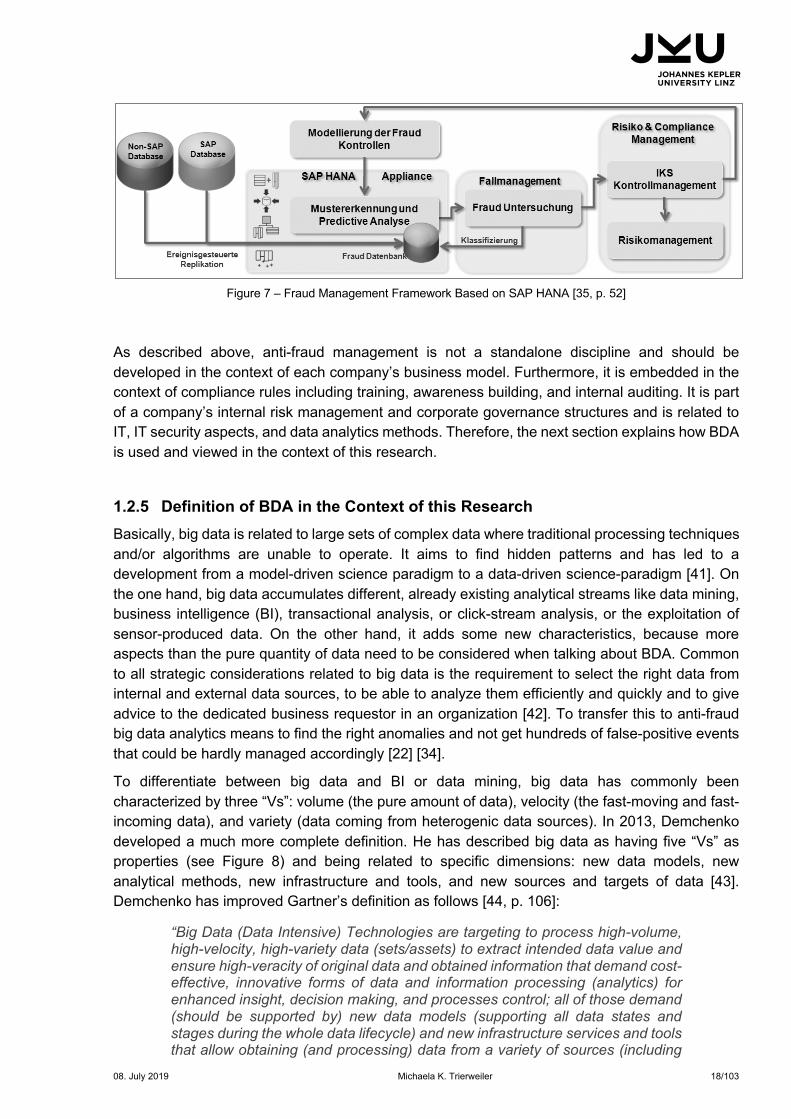

An example of a technical, more operational fraud management framework is the enterprise resource planning systems (ERP)-related framework from SAP using the HANA technology as shown in Figure 7. SAP HANA acts as a corporate-wide repository for all fraud-relevant objects that need to be investigated. The data of different and heterogeneous (SAP-based and non-SAP based) sources are replicated and consolidated there in a fraud database via cyclic or event-based processes. In HANA, all data relevant to an analysis (e.g., a pattern or predictive analysis) are combined from the different tables to create uniform views on the objects. Results from an analysis indicating a fraud activity create alerts to be reviewed by a case management team. For continuous improvement, findings from these investigated fraud cases are then fed back into the internal control systems (ICS/IKS) and added as new classifications into the fraud database.

08. July 2019 Michaela K. Trierweiler 18/103

Figure 7 – Fraud Management Framework Based on SAP HANA [35, p. 52]

As described above, anti-fraud management is not a standalone discipline and should be developed in the context of each company’s business model. Furthermore, it is embedded in the context of compliance rules including training, awareness building, and internal auditing. It is part of a company’s internal risk management and corporate governance structures and is related to IT, IT security aspects, and data analytics methods. Therefore, the next section explains how BDA is used and viewed in the context of this research.

1.2.5 Definition of BDA in the Context of this Research Basically, big data is related to large sets of complex data where traditional processing techniques and/or algorithms are unable to operate. It aims to find hidden patterns and has led to a development from a model-driven science paradigm to a data-driven science-paradigm [41]. On the one hand, big data accumulates different, already existing analytical streams like data mining, business intelligence (BI), transactional analysis, or click-stream analysis, or the exploitation of sensor-produced data. On the other hand, it adds some new characteristics, because more aspects than the pure quantity of data need to be considered when talking about BDA. Common to all strategic considerations related to big data is the requirement to select the right data from internal and external data sources, to be able to analyze them efficiently and quickly and to give advice to the dedicated business requestor in an organization [42]. To transfer this to anti-fraud big data analytics means to find the right anomalies and not get hundreds of false-positive events that could be hardly managed accordingly [22] [34].

To differentiate between big data and BI or data mining, big data has commonly been characterized by three “Vs”: volume (the pure amount of data), velocity (the fast-moving and fast-incoming data), and variety (data coming from heterogenic data sources). In 2013, Demchenko developed a much more complete definition. He has described big data as having five “Vs” as properties (see Figure 8) and being related to specific dimensions: new data models, new analytical methods, new infrastructure and tools, and new sources and targets of data [43]. Demchenko has improved Gartner’s definition as follows [44, p. 106]:

“Big Data (Data Intensive) Technologies are targeting to process high-volume, high-velocity, high-variety data (sets/assets) to extract intended data value and ensure high-veracity of original data and obtained information that demand cost-effective, innovative forms of data and information processing (analytics) for enhanced insight, decision making, and processes control; all of those demand (should be supported by) new data models (supporting all data states and stages during the whole data lifecycle) and new infrastructure services and tools that allow obtaining (and processing) data from a variety of sources (including

08. July 2019 Michaela K. Trierweiler 19/103

sensor networks) and delivering data in a variety of forms to different data and information consumers and devices.”

Figure 8 – The Five Vs of Big Data [43, p. 6]

Zacher from IDC has made similar arguments. He has stated that big data is neither a product nor a customer requirement but rather a concept and a procedure. Thus, big data collects different approaches and technologies with respect to data provision and data analysis offered by various suppliers [45]: meaning visualization of data and correlations, automation of analytical processes, ad-hoc usage of heterogenic data sources, as well as decision-support systems and predictive analytics methods [46].

Freiknecht has defined and compared BI, big data, and data mining by their behavior regarding the four aspects of data entry, data sources, data processing, and data output, as shown in Table 1 but has emphasized that a strict separation is more a theoretical distinction. In reality, the three complement each other [47]. Fels et al. have described big data as an evolutionary development out of BI in terms of both being decision-making supporting systems. The integration results from the fact that big data techniques are able to use structured data like a BI solution does, meaning that big data is able to work with structured data that have previously been stored in a BI data

08. July 2019 Michaela K. Trierweiler 20/103

warehouse. These data could be imported into the big data application, processed there, and exported into the data warehouse again [48].

Business Intelligence Big Data Analytics Data Mining

Data entry Unstructured Structured in data warehouse

Huge volume of data Very large volume Prepared, cleared data

Data sources ERP Systems HDFS, NoSQL, web

requests, streams Called from data

warehouse

Data processing

Selection, converting and transformed (KDD process)

Map-Reduce, YARN, Spark, etc. --

Storing in data warehouse and processing via data mining

Cluster analysis, classification, filtering, association analysis

Data output

Presentation of data from various perspectives

Key-value pairs, raw data Pattern and correlations

Newly gained information that serves decision-making

Table 1: Comparison of Definitions of BI, Big Data, and Data Mining [47, p. 18]

In this research, BDA is considered a concept of tools and activities that are part of a corporate governance, compliance, and/or IT security strategy, and thus especially as part of the technical, IT-based fraud countermeasures and forensic investigations. Ernst & Young (E&Y) has defined the term forensic data analytics (FDA) as “the collection and analysis of all types of data with the objective to manage legal, compliance and fraud risks” [18, p. 4]. A software tool used for auditing needs to deliver clear, plausible, correct, true, and coherent answers in a specific context to eligible/legitimate questions regarding the sense and usage of data and information. All relevant electronic data must be captured in a particular context and analyzed in a critical and rational way [49].

Hence, I gave the following explanation to all participants in this empirical study as the relevant definition for anti-fraud BDA:

The use of big data for regular (daily or even real-time) analysis of electronic data of critical processes and areas in an enterprise by automatized software tools that will give warning signals (the answer) on defined abnormalities (the specific context) to look into an issue; the use and combination of different and heterogenic data sources are of particular interest.

Moving one step further and analyzing non-predefined patterns, anti-fraud BDA affects the areas of machine learning and artificial intelligence. But neither machine learning nor artificial intelligence aspects were asked to the interview partners, because these areas go far beyond the scope of this study.

08. July 2019 Michaela K. Trierweiler 21/103

1.2.6 Fraud Prevention with Big Data According to the ACFE, the presence of anti-fraud controls is correlated to lower loss by fraud and quicker detection time, but proactive data monitoring/analysis was only the key for detection in approximately 37% of the investigated cases (third last) but reduced the median loss by more than 50% (second most) and increased the speed with which a fraud was detected [17] [21]. This reciprocal correlation indicates that BDA could play an effective role in upcoming fraud detection and prevention initiatives. In most cases, fraud is discovered long after it took place, so currently the main use of analytical methods is to minimize the harm and adjust the policies and rules to prevent a particular fraud from happening again [50] [35] . The main goal is to use big data analytical tools to analyze claims and transactions in real time, identifying large-scale patterns or detecting anomalous behavior from an individual user [50]. As part of a forensic process, FDA techniques in combination with human intelligence can help to better monitor, prevent, detect, investigate, and predict anomalies in daily business activities [18]. In that sense, anti-fraud BDA as an automated process is able to support continuous auditing purposes [23] but needs to investigate the full datasets that are available and legally allowed to be used. When using BDA or data mining techniques in anti-fraud systems, the most commonly used option is transaction monitoring systems, a specialized software that uses “IF-THEN” filters or fraud scorings to do real-time analytics but needs to handle complex algorithms [51] or machine learning approaches.

During the literature search for this empirical study, some summarizing literature was found in the form of textbooks from practitioners and gave a good overview and initial information. However, from a scientific point of view, it was necessary to find papers and primary studies about concrete usage of big data techniques to support fraud prevention. I have found two types of papers: some are about particular use cases of big data and algorithms in specific business areas or for dedicated applications, while others are more like SLRs and hence take a basic approach to summarizing existing methods. A selection of both groups was composed to deepen the theoretical background and is presented in Table 2. The following term-based summary is structured in terms of the technique, the type of method mentioned, and the reference to the scientific source where this big data method was discussed. The list is in alphabetical order for easier reading.

Big Data Analytics Technique Type Paper

(Artificial) neural networks Machine learning, supervised (classification and regression)

[52] [53] [51] [54] [55] [56]

A/B testing [53]

Apriori algorithm Data mining [51]

Artificial immune systems Machine learning, supervised (classification and regression)

[55]

Association rules [56]

AutoClass Clustering and outlier detection [54]

Bayesian (belief) networks Machine learning, supervised (classification and regression)

[52] [55] [56]

Benford’s law Frequency testing [57]

08. July 2019 Michaela K. Trierweiler 22/103

Break point analysis Clustering and outlier detection [55]

Cluster analysis or data segmentation

[53] [56]

Data mining [53]

Decision trees Machine learning, supervised (classification and regression)

[52] [51] [55] [56]

Evolutionary programming [51]

Fuzzy logic [51]

Genetic algorithms [53] [51] [56]

Gradient boosted trees Machine learning [58] [56]

Hadoop processing Sequence mining [51]

Hidden Markov model Machine learning, supervised (classification and regression)

[52] [51] [55]

K-means clustering Clustering and outlier detection [55]

K-nearest neighbor Machine learning, supervised (classification and regression)

[52] [51] [55]

Latent variable models [56]

Logistic regression | regularized regression

Machine learning, supervised (classification and regression)

[58] [55] [56]

Naïve Bayes Machine learning, supervised (classification and regression)

[52] [51] [55] [56]

Natural language processing [53]

Outlier detection methods Data mining [55]

Peer group analysis Clustering and outlier detection [55]

Principal component analysis [53]

Random forest (trees) Machine learning [52] [58] [51] [54]

Regression analysis [51]

Rotation forest [54]

Self-organizing maps Pattern matching, clustering, and outlier detection

[53] [54] [55]

Stacking-bagging technique [51]

Support vector machines Machine learning, supervised (classification and regression)

[52] [51] [54] [55] [56]

Transaction monitoring systems Data mining [51]

Table 2: Composition of Big Data Techniques for Fraud Prevention Found in the Literature

08. July 2019 Michaela K. Trierweiler 23/103

These specific kinds of algorithms are known to very few people in an organization, such as data scientists, and this information was not the basis for designing the questionnaire with respect to the target audience. With respect to future research, the conduction of a mapping study to cluster and describe the existing big data techniques is an option.

1.3 Aim and Research Questions

As described in the previous chapters, IT-based anti-fraud management is assumed to be complex and cost-intensive and therefore only manageable for large corporations. Smaller organizations might not see the value for their own businesses or may not have the structures to facilitate an IT-based anti-fraud system.

Furthermore, there are industries that face a higher risk of fraud than others, and these are technically better armed than other industries. However, fraud can affect any company negatively and cause damage.

This research wants to examine what countermeasures are installed to prevent fraud in different kinds of organizations and what role BDA plays here. In case big data is not used, this research is intended to determine the reasons for not using big data to prevent fraud and ensure compliance. Perhaps there are practices in some areas that could be transferred to other segments or sizes of companies. With the results and findings from this study, this research is intended to contribute to the development of an anti-fraud framework in future research projects.

Therefore, this study evaluates and discusses the current use and perception of usefulness of BDA methods to prevent fraud within German-speaking companies of different sizes and industry sectors by conducting an empirical study.

To determine what role BDA plays in that particular sense today, the following three research questions were defined:

RQ-1. Which countermeasures to prevent fraud are in place in different types of companies? Is there any proof that there are more technical and analytical anti-fraud measures in large companies than in SMEs, or is there even a focus in specific industry sectors?

RQ-2. What role does BDA play, and how common (distributed) is it currently? If it is not well distributed, why not? What are the reasons for not using BDA to prevent fraud?

RQ-3. If use cases are more common in large companies, are there benefits that could be carried over to SMEs?

08. July 2019 Michaela K. Trierweiler 24/103

2 Methodology This chapter describes the stages of the research process; the terms, techniques, and concepts used. Furthermore, it provides the details of the literature review and the setup for the expert interviews and the online survey, plus explains assumptions and limitations.

2.1 Research Process – Mixed Method Approach

My intention was to research with a practical impact and insight view. Therefore, an empirical study questioning experts and practitioners covering that field in daily business seemed like the best approach to find out how much big data is already used in different organizations to support compliance and fraud prevention.

The research was set up as a mixed-method design following the sequential process of an exploratory design with the qualitative study at the beginning of the study. The quantitative study was given priority with respect to the research questions. Therefore, the expert interviews as the qualitative part worked as a preliminary study [59, p. 81f] for two reasons:

• First, to gain a better understanding of what will be relevant for the quantitative survey (more simply, to find the right questions). When thinking about the legal consequences of committing fraud, this study touches on a highly sensitive topic; thus, it was important to elaborate beforehand what kind of questions could not be asked or needed to be softened by asking for compliance violation instead. Otherwise, I would have risked obtaining no really valuable and reliable answers to some survey questions. This approach minimized the risk of gaps. The interviews helped to construct the main research instrument better [60].

• Second, to be able to conduct a more focused literature research and select the right papers, studies, and textbooks.

The next figure illustrates this staggered approach and mixed-method concept following the qual à QUANT principle [59, p. 81]:

Figure 9 – Multi-Step Research Design (Exploratory Design Following the qual à QUANT Principle)

I. Literature Research

Basic researchabout fraudprevention and big data

Refine literatureresearch to find more fitting studies in a second review

II. Qualitative Analysis

Run three to five interviews withexperts from fraud-effected (large) enterprises to learnfrom theirexperience

III. Quantitative Analysis

Develop and runonline survey

Extract and analyze results of valid participants

IV. Conclusion

Discuss the results in the context of other related research and conclude further implications

08. July 2019 Michaela K. Trierweiler 25/103

The arrows show the sequence, but their parallelism indicates that the stages were not isolated; there has been overlapping and iterations during the research process as well. To approximate the topic, an initial generic literature search was performed. After that, a preliminary study with three guided interviews with experts from IT security and compliance was conducted to learn and capture the qualitative aspects of this research area directly from experienced practitioners. This helped to design and sharpen the focus of the main study and to select the best literature in a second, more systematic literature review. Based on the theory outcome and the feedback provided in the interviews, the main part of this work was designed as a questionnaire distributed as an online survey to German-speaking companies. This quantitative survey allowed for insight into the dissemination and use of big data for fraud prevention over different business areas or company sizes. Finally, the results were analyzed and discussed in the context of other related studies and research.

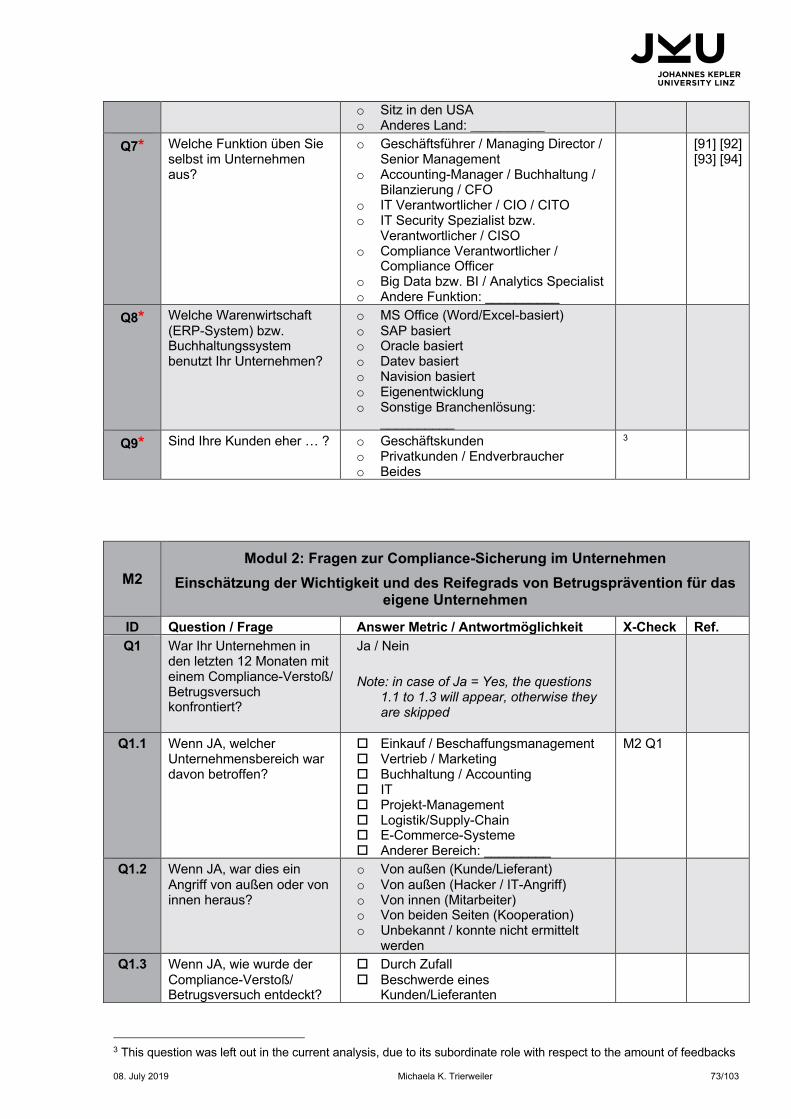

When combining qualitative and quantitative methods to gather data, a researcher must be careful when integrating the different answers, because both concepts use codices to structure the answers, but in a different usage. In qualitative research, the codices are developed ad hoc according to the existing data material. They have been used to classify answers and to find text passages more quickly to compare and interpret them. In quantitative research, however, the codes represent the countable facts [60]. This circumstance was considered by using the predefined questions plus additional derived clusters of information from the guided interviews as codes. These codes were used as questions and answer options (= countable code) for the online survey. For more details, see Appendix 9.1 where the questions for the survey, the answer options, and the references are provided.

2.2 Use of Terms

As seen in the previous theory sections, two wide and complex areas of interest – big data and fraud prevention – need to be linked. During the first literature review, I found some expressions used in parallel to describe similar concepts or measures. Therefore, I decided to use these for the second literature review and the selection of libraries as well.

In the context of this thesis paper, one will find in appropriate contexts a coequal meaning of the following terms:

• Fraud prevention | fraud detection | compliance | anti-fraud management

• BI | analytics | big data

Furthermore, these terms are used in parallel for more accommodating reading:

• Company | organization

• Questionnaire | (online) survey

• Expert interview | guided interview | semi-structured interview

08. July 2019 Michaela K. Trierweiler 26/103

2.3 Methods of Data Collection and Analysis

This section describes the theoretical backgrounds for the qualitative and quantitative research. It explains the chosen questioning techniques and why a specific method was used.

2.3.1 Questioning Techniques When using questioning techniques, stakeholders are asked about dedicated subjects or specific requirements by using oral or written words. If the individual can articulate these requirements properly, this is a valuable instrument for capturing someone’s ideas, knowledge, or experience to get insights into a specific topic [61, p. 105]. For this research work, the methods of guided (semi-structured) interview and online survey were selected as a suitable combination of questioning techniques.

Interview The interview is one of the open questioning techniques and is a well-proven method for gaining qualitative data. Qualitative data are written texts containing structured, non-randomized symbols (including pictures) [62]. To produce a text as the result of an interview, the interview needs to be recorded as video or audio, and a transcript needs to be made afterward to act as proper protocol [61]. An interview requires careful preparation: select the right interview partner, define how the interview is conducted (meaning face-to-face, written, or by telephone [63, p. 193]), and, consider how far the interrogator may influence the interviewee via the grade of explanations and steering during the interview [62]. Most of the interviews require some kind of structure, which is provided by the interview questions. In semi-structured interrogations, predefined questions and encouragement to answer provide the necessary guidance [62] [63]. In this case, the interview is classified by its method as a guided interview. If such a guided interview is done with a particular group of people that have specific knowledge important to the research, the interview is called an expert interview due to the dedicated target group [62]. Depending on the research focus, it may be necessary to have a specific target group with special expertise contribute. When focusing on the capturing of the experience, perceptions, ideas, and reflections of the interviewee concerning a certain research topic, the interview could be conducted as a problem-centered interview (in Anglo-American research, referred to as a “semi-structured interview” [64, p. 465]). All of these are subtypes of the guided interview form [65] [62].

Once the question guidelines and the target group are defined, the interview partners must be identified and asked to participate. During the interrogation, a confiding and frank conversation climate is helpful, and legal aspects like privacy and anonymity must be agreed upon before starting the interview and making any recording [65].

The main criteria for a good guided interview structure, are as follows [65] [64]:

• The guide must be clear and allow an overview

• The guide should focus on the specific topic and is adapted to this

• A natural speaking situation must be possible

• The guide should follow a certain logical structure and during the interview process shall steer but not restrict; allow open answers

08. July 2019 Michaela K. Trierweiler 27/103

A semi-structured interview should work as a tool that helps to capture the ideas of the interview partner. In the case of a problem-centered approach, the researcher, acting as interrogator, has made himself familiar with the area of interest [64] and potential answers in order to be able to conduct the interview on a par and lead the interview partner back in case there have been explanations of side effects due to the basically open structure of such an interview.

When preparing the questions for an interview that are mostly open questions, a few aspects need to be considered, such as who the interviewee is, what his/her knowledge base is, and whether or not explanations of terms are necessary. It is important not to combine several topics in the same question and to point out what kind of answer is expected (e.g., a keyword or a single information, a full list, or a narration). Furthermore, the importance of a question for the research should be highlighted to encourage the interviewee to answer [66].

Due to the fact that the researcher already has knowledge about the research topic and wants to examine and deepen his/her own expertise, semi-structured interviews are appropriate for pre-studies [64] and are used in that sense for this research (more details are described in Section 2.5).

Questionnaire/Survey A survey is a high structured interrogation with predefined questions and answers in a defined order. Using standardized questions should allow a maximum grade of objectivity to be achieved and is the basis for the reliability and validity of the rating [67]. Such a questionnaire allows for a count of the given answers related to quantitative aspects of one’s research. These kinds of closed questions require a known spectrum of answer options. In contrast, the open questions do not have any presetting; thus, they are not common in standardized surveys [67], because the analysis of the answers requires different techniques such as the “Qualitative Content Analysis,” according to Mayring. A mixture of both types is called the hybrid question, which has predefined answer options plus an “other” category with a field to enter free text [67]. In this study, closed and hybrid questions were used. The answer options were defined using feedback from the expert interviews and findings from the research literature.

Basically, five types of questions are distinguished according to their need for information: a) attitude; b) facts and knowledge; c) events, intentions, and behavior; d) social-statistical attributes; and d) network questions [67]. The first three of these types were used in this research.

When asking for the respondent’s attitude toward a specific item, the answers are typically captured using a rating scale. Rating scales should follow some principles [68]:

• When using verbalized scales, the scale labels need to be completely written to be unique and precise at the same time; they must be symmetrical or balanced by having the same amount of positive and negative answer options with similar distances between them.

• When using a neutral or middle answer option, consider its position, because depending on the question’s sensitivity or complexity, a real neutral answer could be given, or it just be used to avoid answering the question. Leaving out a middle category is not recommended, because otherwise the person is forced to give a false answer, which leads to a bias or noise in the results.

• The use of direct rating scales (e.g., in the form of a Likert scale) is helpful when asking for a grade of acceptance, and such scales are easy to understand and count.

• The display format should be horizontal to minimize primacy effects, which are tendencies to select answer options from the first half of the selection list.

08. July 2019 Michaela K. Trierweiler 28/103

Facts and knowledge can be captured with preset answer options [67], and the survey participant selects the best fitting answer(s) out of these. In an online survey, a radio-button selection typically allows only one answer, whereas a checkbox allows the selection of multiple answers.

Asking about events and behavior requires two-step questioning, because they are related to an occurrence in the past. First, the prevalence question asks for a yes-no answer regarding whether or not a certain event has happened. In the case of a “yes” answer, the subsequent related questions are displayed to capture the incidence rates [67] from the answer options of these questions, which could also be questions regarding facts and knowledge.

The main principles for the structure of a survey questionnaire are [63, p. 228ff] [67] [69] as follows:

• Start with warm-up questions that are interesting and easy to answer in order to create a positive atmosphere and avoid pure “yes-no” answers

• Place the research-important questions in the first part after the warm-up phase or in the middle where the interrogation partner is still cognitively fit

• Place sensitive questions in the middle or towards the end in case a participant drops off, because the previous answers will still be kept

• Demographically statistical questions should be placed at the end when the attention span is low; but at the beginning as a warm-up is also fine

• Cluster topics and questions with regard to content, creating modules that make it possible to answer questions related to each other in a row is user-friendly, enabling respondents to focus and avoid irritation garnered by hopping between topics

• Have a user-friendly layout and give clear instructions; be explanatory

• Create an appropriate landing page explaining the purpose of the survey and providing an introduction to the topic

• Use bridge passages between different modules to reduce complexity

• Thank the participants for their time and effort on the final page

Regarding the wording for a questionnaire, the research literature suggests the following [63, p. 231ff] [70] [71]:

• Use short and precise phrases as much as possible; if necessary, explain technical terms or give background information

• Do not use dialect speech, (double) negative phrasing, or ask two things in one question

• The answer options need to be as disjunct, complete, and precise as possible

• Avoid multidimensional answer options because of their complexity

• Use indirect questions rarely and only under particular conditions, such as when seeking sensitive answers that otherwise risk being skipped

• Do not use suggestive questions or make implicit assumptions

• Avoid hypothetical questions; they are too complex and require too much intellectual effort

• The answer options need to be in a logical order, and the list should be not too long

08. July 2019 Michaela K. Trierweiler 29/103

A questionnaire can be distributed via postal mail, but since the 1990s, it is more common to use the internet for standardized surveys. Already in 2012, a third of all market research interviews have been done via the internet [72]. Today, this is the common standard for performing surveys, using the always-on mentality of people (via their smartphones, tablet PCs, and laptops) in combination with the advantage of a survey database including data capturing and visualization options for the results. Therefore, the preferred method for this research was to develop and use an online survey.

Nevertheless, a few aspects need to be considered when conducting an online survey: First, who can be asked to participate via the internet? Who has access? And second, how should the sample group be selected [72]? For this research, the people in the target group are all business people with internet access and e-mail addresses and are thus basically reachable. The more difficult part was to find the right contact details to select the sample group. This was the case for two primary reasons: first, the sensitive and specific topic required respondents at the management or expert level in an organization. These people are often very busy, their contact details are not publicly listed on their companies’ webpages, and it was only one answer per company necessary to represent the company’s perception towards this research area. Second, the EU-GDPR neither allows one to send out mass e-mails to people with whom one has no relation nor allows one to collect contact details from unpublished sources. This means that a researcher must use personally known contacts or search the internet for publicly available contact details in order to compile a sample list. In this research, this limitation was addressed by using the following types of available contacts:

• Sending e-mails to personal contacts met during my professional career or in private environments (ca. 380)

• Sending e-mails to publicly available contacts on the research-relevant website www.dnwe.de (ca. 25)

• Asking research-relevant associations (i.e., Dico e.V., IIA Austria) to act as multipliers by asking their community members via newsletters to participate in my study

• Placing blog posts on social media channels (i.e., XING, Linked-In, and Facebook)

Following the principle “the more participants, the better accuracy,” a certain quantity of answers is needed. This means that it is necessary to reach as many relevant people as possible and convince them to contribute to minimizing the non-responses. Depending on the topic or target group, the usefulness of the survey topic or a personal benefit must be highlighted to motivate people to participate [63]. As an incentive to contribute to this research, every participant was invited to subscribe to receive a summary of the results, after this thesis paper is published. See Appendix 9.2 for examples of the circulation of the request for participants to join the survey.

08. July 2019 Michaela K. Trierweiler 30/103

2.3.2 Analytical Methods This section explains the theoretical aspects regarding the analysis of the collected data during the expert interviews and the online survey of this research.

Qualitative Content Analysis To produce an analyzable text as a result of an interview, the interview must be recorded in some way and afterward transcribed into a textual transcript that can be trawled through and coded. There are technical tools such as the QCAmap software [73] available to support a text analysis. Such tools are helpful when there are very long or multiple texts to be compared. However, for this research, the interviews worked as preliminary study. Therefore, just three experts were asked for their opinions and insights, and it was possible to analyze the transcripts without any specific tool. This manual approach, which uses a table structure where each question has been entered as a code, made it possible to concentrate on the content while reading through and summarizing based on Mayring’s concepts of qualitative content analysis.

There are seven basic types of interview transcription [73, p. 45ff]:

• The selective protocol as an economic procedure where the researcher defines selection criteria with respect to the research question and transcribes only the relevant parts.

• The comprehensive protocol is a tightening of the full material where the researcher summarizes reasonable passages. The researcher must be trained for this procedure.

• The clean read and smooth verbatim transcript type is done word for word, but decorative words or utterances are left out and dialect speech is converted into standard language. This allows for simple understanding but keeps the original wording and meaning.

• The pure verbatim protocol is done word for word including all utterances, dialect speech, etc.

• The International Phonetic Alphabet (IAP) is used when one wants to preserve as much as coloration of the oral language as possible. A special set of characters must be used, and the text is not easy to read.

• A protocol with special characters contains the wordings and a set of signs to describe nonverbal aspects and expressions; for example, laughter or low voice is notated.

• A protocol with comment column is an extensive form and allows the researcher to add all special perceptions beside the text. This method is used for transcription of focus group discussions when a moderator is present.

Although the interviews just served as a preliminary study to gain deeper insight into the research area and were not the main part of this research, the clean read and smooth verbatim transcript was chosen in order to create the most complete picture and possibly be able to use the transcripts in future research. A documentation of nonverbal expressions was neither necessary for the content nor possible, because two of the interviews were conducted by telephone.

Basically, content analysis is not a standardized instrument and needs to be adapted to each study. Hence, the “General content-analytical procedural model” from Mayring [73, p. 54] was adapted and shortened to the following stages:

• Definition of the material by using all three transcripts

• Consideration of the formal characteristics of the material by adding line numbers, anonymizing the interview partner, and handing over the transcript to get a formal approval to use the transcript

08. July 2019 Michaela K. Trierweiler 31/103

• Definition of the direction of analysis as a summary of the answers along with the questions that are acting as codices enriched with new codes found suitable when analyzing the text

• Determination of techniques of analysis and establishment of a concrete procedural model by documenting the outcome in a table.

• Analytical steps are taken by means of the category system: summary/inductive category formation, explication/context analysis, structuring/deductive, or mixed

• Interpretation of the results in relation to the main problem and issue by writing summaries and make notes regarding where the given information should be used during the next research steps (e.g., what could be added as a question or answer option in the online survey)

Three basic procedures of qualitative text analysis are defined as follows, but could also be mixed [73, p. 64f]:

• Summary: The object is to reduce the material in such a way that the essential contents and statements remain in order to create a comprehensive overview of the base through abstraction.

• Explication: The object is to provide additional material on individual doubtful text components to increase the understanding, explaining, and interpreting of the particular text passage.

• Structuring: The object is to filter out particular aspects of the material, to provide a cross-section through the material with defined abstraction criteria, or to assess the material according to certain other criteria.

First, the text passages were mapped to the codes (questions) and paraphrased, and parts of them were generalized and reduced. Second, some new useful codes were created and filled with aspects mentioned by the interviewee during the analysis. Since the aim was not to quantify or derive generalizations out of the experts’ answers, this concentration was just made to focus on dedicated aspects that could be integrated into the next stage of this research. In that sense [73, pp. 70–81], I used a mixture of the summary and structuring principle by using deductive (predefined categories) and inductive (new categories) elements.

Quantitative Content Analysis A successful analysis requires clever and precise data collecting plus careful and thoroughly cleaning and preparation of these data. This might sound trivial, but it is mostly time consuming and/or technically demanding, and error-prone [74].

The analytical process for quantitative data follows a much more sequential procedure than the one for qualitative analysis. Basically, it consists of the following 10 steps [59, p. 105ff]:

1. Preparation of the data 2. Entry of the data 3. Checking the data regarding completeness, errors, and plausibility 4. Formatting and preparing multi-answer options 5. Coding of the open questions respectively the given answers

08. July 2019 Michaela K. Trierweiler 32/103

6. Using basic counts and descriptive statistical methods 7. Analyzing contexts: correlations and differences between groups 8. Complex statistical analysis and modeling 9. Presentation, discussion, and evaluation of the results 10. Creating the research report

Kuckartz [59, p. 105ff] and Lück and Landrock [74] have explained the key aspects to be considered when conducting a quantitative data analysis. This is summarized and accumulated in the following:

• It is important to bring the raw data in a digital, computational form, or a data matrix. This makes it possible to use statistical software tools and to ensure liability for the upcoming steps. Ideally, there is a code plan that acts as mapping between the questions and the answer variables. Modern survey tools automatically declare the questions and answer options with variables and organize the raw data in data matrices.

• The characteristic of each variable could be a binary, number, integer, characters, alphanumerical, or signs. If a piece of data is not electronically captured during the survey like in an online questionnaire, it must be typed in correctly or scanned.