Embed Size (px)

Citation preview

WELCOME! Dial in to the conference line for the audio of the presentation:

Dial In #: 1.866.620.7326 Conf #: 5497824306 (Note: All participant lines are muted)

AGENDA (Note: Times are estimated)

9:00a Welcome – Nancy Ruoff9:05 Capital Asset Reporting – Jackie Craine9:45 SEFA Audit Finding Issue – Roger Basinger9:55 CAFR Due Dates – Fatima Gilbert10:00 Break (10 minutes)10:10 SMART/SHARP Updates:

Fiscal Year End Info Circular Overview – Nancy HauflerNegative Cash Fund Balance at Fiscal Year-End Policy – Kim FowlerACH Initiative Updates and Reminders – Kim FowlerBudget Date Change Requests and Template – Sunni Zentnere-Supplier – Sunni ZentnerMoving Expenses – Amanda EntressSMART/SHARP Project Update – Nancy Ruoff

11:25 Online Skype Conference Ends

To submit questions during the presentation:During the presentation, questions for the presenters may be e-mailed to: [email protected] the subject line “OCFO Presentation”. Questions will be reviewed/answered if possible during the Skype presentation. For all questions not answered during the presentation, or received following the presentation, responses will be sent later to the inquirer. The question and answer will also be sent to the broader group if applicable.

Department of Administration Excellent customer service, every time!

Capital Asset Reporting

Jackie Craine

Statewide Policy Manager

2

Department of Administration Excellent customer service, every time!

SHARP Updates

Agenda:

• Capital Asset Records

• Recording New Assets

• Asset Disposal

• Implementation of DA-87

• Asset Inventory

• Capital Asset Year-End Reminders

3

Department of Administration Excellent customer service, every time!

Taxable Fringe Benefits

4

Department of Administration Excellent customer service, every time!

Policy Manual 13,001 Capital Asset Records

The state agency owns all property purchased with State of Kansas

funds and all property received as gifts. Although title to property

purchased with funds from a grant or contract may not be vested in

the state agency, the state agency should exercise the responsibilities

of ownership for such property. Regardless of which state agency

organizational unit ordered the item, the fund cited, or the particular

budget expensed, the principle of state ownership prevails.

Property Management Officer: Each state agency should appoint an

individual to serve as the lead person regarding all asset management issues

within the state agency. This person is responsible for distributing all

statewide and agency-specific asset management policies throughout the

state agency and for conducting the agency's annual physical inventory.

Taxable Fringe Benefits

What is a Capital Asset?

Assets with a cost meeting the established

capitalization threshold and a useful life

exceeding one year.

• Tangible assets are physical assets such as vehicles,

equipment, machinery, furniture, and property (land and

buildings). Note: Land should be recorded separately from the

building because buildings are depreciated and land is not depreciated.

• Intangible assets are nonphysical, such as computer

software, easements, water rights, patents and

trademarks.

5

Department of Administration Excellent customer service, every time!

Description Capitalization Threshold

Equipment and Furnishings $5,000

Vehicles $5,000

Buildings and Improvements $100,000

Land $100,000

Land Improvements $100,000

Leasehold Improvements $100,000

Intangible - Software $250,000

Intangible - Other $250,000

6

Department of Administration Excellent customer service, every time!

The statewide capitalization thresholds for assets are as follows:

7

Taxable Fringe BenefitsDepartment of Administration Excellent customer service, every time!

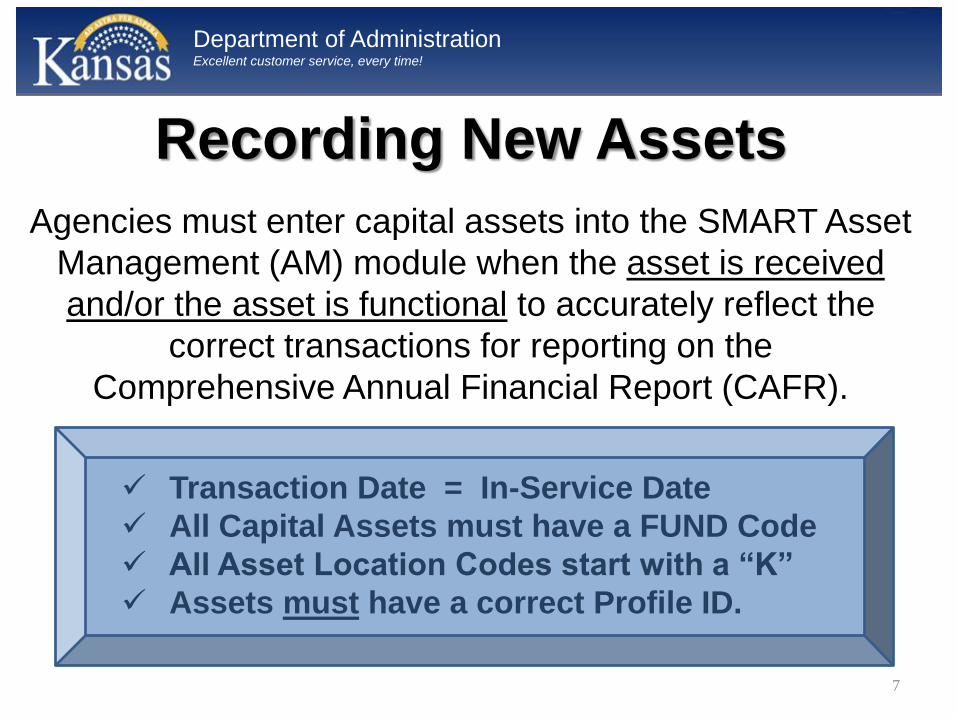

Recording New Assets

Agencies must enter capital assets into the SMART Asset

Management (AM) module when the asset is received

and/or the asset is functional to accurately reflect the

correct transactions for reporting on the

Comprehensive Annual Financial Report (CAFR).

✓ Transaction Date = In-Service Date

✓ All Capital Assets must have a FUND Code

✓ All Asset Location Codes start with a “K”

✓ Assets must have a correct Profile ID.

8

Department of Administration Excellent customer service, every time!

Asset Profile ID

The Profile ID is the most important field in Asset Management.

▪ Profile ID’s are templates that help reduce data entry when

adding an asset.

▪ Each Asset Profile is configured with an Asset Class, an Asset

Type, and an Asset Category.

▪ Profile ID’s drive the depreciation and accounting entry

generation of an asset for CAFR purposes.

Most Profile IDs are based on General Ledger Account Codes▪ Capital Assets have Profile ID’s ending in 54XX00, 54XX10, or 54XX20.

▪ Non-Capital Assets have Profile ID’s ending in 54XX90 or 54XX91.

▪ Construction-In-Progress (CIP) have unique CIP Profile IDs.

9

Department of Administration Excellent customer service, every time!

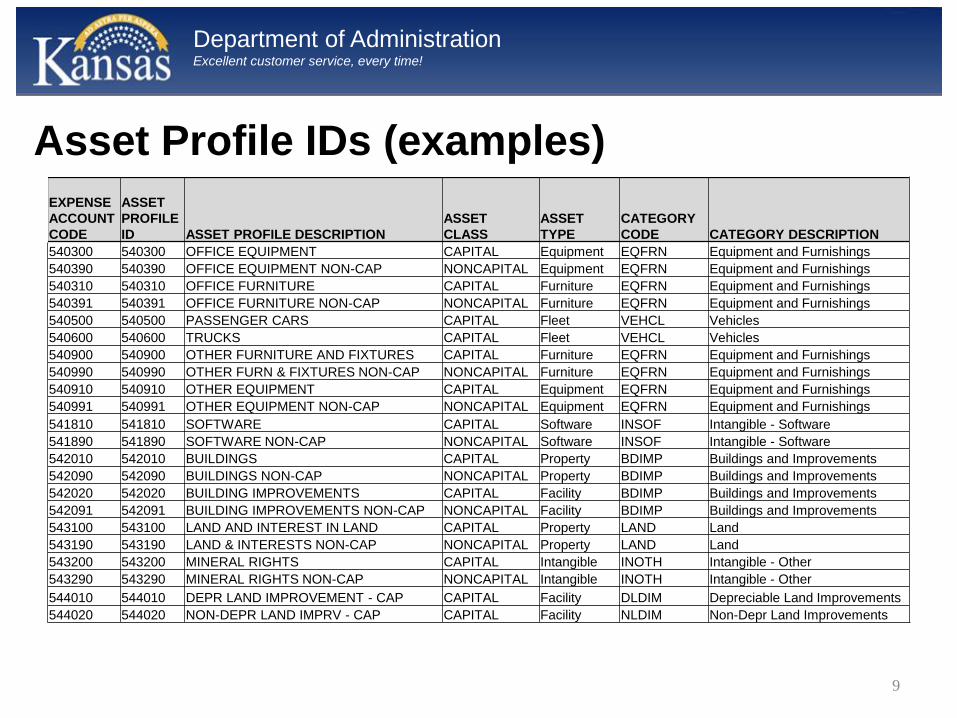

Asset Profile IDs (examples)

EXPENSE

ACCOUNT

CODE

ASSET

PROFILE

ID ASSET PROFILE DESCRIPTION

ASSET

CLASS

ASSET

TYPE

CATEGORY

CODE CATEGORY DESCRIPTION

540300 540300 OFFICE EQUIPMENT CAPITAL Equipment EQFRN Equipment and Furnishings

540390 540390 OFFICE EQUIPMENT NON-CAP NONCAPITAL Equipment EQFRN Equipment and Furnishings

540310 540310 OFFICE FURNITURE CAPITAL Furniture EQFRN Equipment and Furnishings

540391 540391 OFFICE FURNITURE NON-CAP NONCAPITAL Furniture EQFRN Equipment and Furnishings

540500 540500 PASSENGER CARS CAPITAL Fleet VEHCL Vehicles

540600 540600 TRUCKS CAPITAL Fleet VEHCL Vehicles

540900 540900 OTHER FURNITURE AND FIXTURES CAPITAL Furniture EQFRN Equipment and Furnishings

540990 540990 OTHER FURN & FIXTURES NON-CAP NONCAPITAL Furniture EQFRN Equipment and Furnishings

540910 540910 OTHER EQUIPMENT CAPITAL Equipment EQFRN Equipment and Furnishings

540991 540991 OTHER EQUIPMENT NON-CAP NONCAPITAL Equipment EQFRN Equipment and Furnishings

541810 541810 SOFTWARE CAPITAL Software INSOF Intangible - Software

541890 541890 SOFTWARE NON-CAP NONCAPITAL Software INSOF Intangible - Software

542010 542010 BUILDINGS CAPITAL Property BDIMP Buildings and Improvements

542090 542090 BUILDINGS NON-CAP NONCAPITAL Property BDIMP Buildings and Improvements

542020 542020 BUILDING IMPROVEMENTS CAPITAL Facility BDIMP Buildings and Improvements

542091 542091 BUILDING IMPROVEMENTS NON-CAP NONCAPITAL Facility BDIMP Buildings and Improvements

543100 543100 LAND AND INTEREST IN LAND CAPITAL Property LAND Land

543190 543190 LAND & INTERESTS NON-CAP NONCAPITAL Property LAND Land

543200 543200 MINERAL RIGHTS CAPITAL Intangible INOTH Intangible - Other

543290 543290 MINERAL RIGHTS NON-CAP NONCAPITAL Intangible INOTH Intangible - Other

544010 544010 DEPR LAND IMPROVEMENT - CAP CAPITAL Facility DLDIM Depreciable Land Improvements

544020 544020 NON-DEPR LAND IMPRV - CAP CAPITAL Facility NLDIM Non-Depr Land Improvements

10

Department of Administration Excellent customer service, every time!

Construction-In-Progress (CIP)

CIP assets that have an estimated cost that meets or

exceeds the statewide capitalization threshold but are not

complete should be recorded with a CIP profile ID.

Agencies should consider the cost of the entire project, rather than each

payment or vendor separately. When the asset is complete and usable, the

costs should be moved from CIP to the appropriate asset category.

PROFILE_ID ASSET PROFILE DESCRIPTION

ASSET

CLASS

ASSET

TYPE

CATEGORY

CODE

CIP_BDIMP CIP-Buildings and Improvements CAPITAL Other CBDIM

CIP_DLDIM CIP-Depreciable Land Improvements CAPITAL Other CDLDI

CIP_EQFRN CIP-Equipment and Furnishings CAPITAL Other CEQFN

CIP_INOTH CIP-Intangible Other CAPITAL Other CINOT

CIP_INSOF CIP-Intangible Software CAPITAL Other CINSF

CIP_LHDIM CIP-Leasehold Improvements CAPITAL Other CLHDI

CIP_NLDIM CIP-Non Depr Land Improvements CAPITAL Other CNLDI

11

Department of Administration Excellent customer service, every time!

Building Improvement vs. Repair

Building improvements are significant alterations,

renovations, or structural changes that increase the

usefulness of the asset, enhances its efficiency, or

prolongs its useful life.

Repair and/or service costs are expenses for routine

maintenance that sustains a building's original condition

rather than provide additional value.

VS.

Taxable Fringe Benefits

Acquisition Costs

Assets should be recorded at historical cost rather than current cost or market value.

Historical costs include:

• Cost of an asset less discounts/rebates

• Non-refundable sales tax

• Initial installation cost (excluding internal labor)

• Modifications

• Attachments

• Accessories or apparatus necessary to make the asset usable and render it into service

• Ancillary charges (such as freight and transportation charges, site preparation costs and professional fees)

Note: Incidental charges (such as extended warranties, maintenance agreements, training costs, additional parts or consumable items) are not considered part of the asset and should not be included in the cost of the asset.

12

Department of Administration Excellent customer service, every time!

Asset Disposal

13

Department of Administration Excellent customer service, every time!

State agency property must be

disposed of in accordance with

State Surplus Property policies

and procedures, and under the

direction of the agency

Property Management Officer.

Taxable Fringe Benefits

14

Department of Administration Excellent customer service, every time!

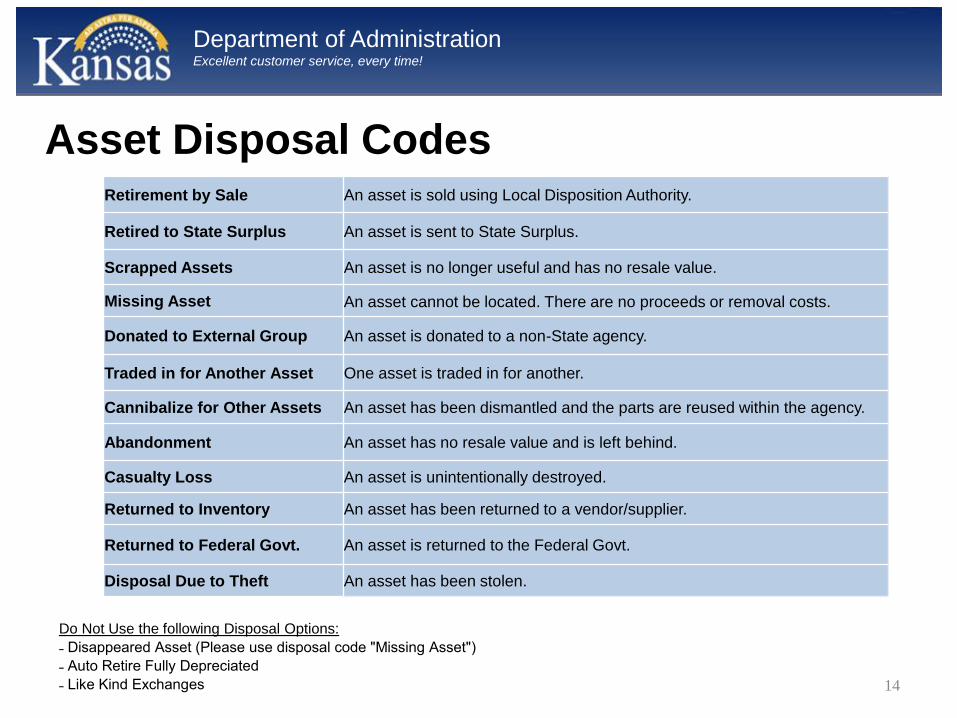

Do Not Use the following Disposal Options:

˗ Disappeared Asset (Please use disposal code "Missing Asset")

˗ Auto Retire Fully Depreciated

˗ Like Kind Exchanges

Asset Disposal CodesRetirement by Sale An asset is sold using Local Disposition Authority.

Retired to State Surplus An asset is sent to State Surplus.

Scrapped Assets An asset is no longer useful and has no resale value.

Missing Asset An asset cannot be located. There are no proceeds or removal costs.

Donated to External Group An asset is donated to a non-State agency.

Traded in for Another Asset One asset is traded in for another.

Cannibalize for Other Assets An asset has been dismantled and the parts are reused within the agency.

Abandonment An asset has no resale value and is left behind.

Casualty Loss An asset is unintentionally destroyed.

Returned to Inventory An asset has been returned to a vendor/supplier.

Returned to Federal Govt. An asset is returned to the Federal Govt.

Disposal Due to Theft An asset has been stolen.

15

State Surplus Property

Agency Offices Located Within Shawnee County: All agencies are

required to dispose of surplus property to the State Surplus Property

Program, regardless of value, unless Local Disposal Authority is pre-approved

by State Surplus.

Agency Offices Located Outside Shawnee County: The local head of each

state agency office located outside Shawnee County is designated by the

Secretary of Administration to dispose of surplus property in accordance with

KSA 75-6602(a) and (b).

✓ Agencies should remove assets from their records when the State

Surplus Property takes possession of the asset.

✓ All revenues received from the State Surplus Property for selling

an asset will be recorded as miscellaneous revenue in the CAFR.

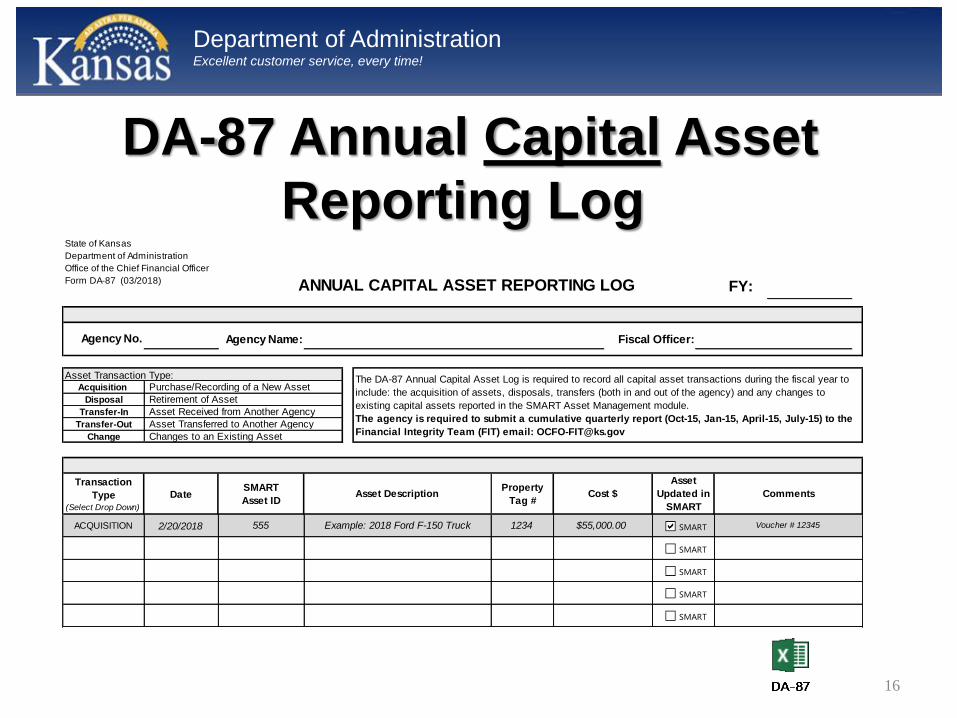

DA-87 Annual Capital Asset

Reporting Log

16

Department of Administration Excellent customer service, every time!

State of Kansas

Department of Administration

Office of the Chief Financial Officer

Form DA-87 (03/2018)

Agency No.

Acquisition

Disposal

Transfer-In

Transfer-Out

Change

Transaction

Type (Select Drop Down)

Date

ACQUISITION 2/20/2018 Voucher # 12345

Fiscal Officer:

Comments

FY:

Asset Description

Retirement of Asset

Asset

Updated in

SMART

Cost $

The DA-87 Annual Capital Asset Log is required to record all capital asset transactions during the fiscal year to

include: the acquisition of assets, disposals, transfers (both in and out of the agency) and any changes to

existing capital assets reported in the SMART Asset Management module.

The agency is required to submit a cumulative quarterly report (Oct-15, Jan-15, April-15, July-15) to the

Financial Integrity Team (FIT) email: [email protected]

Property

Tag #

ANNUAL CAPITAL ASSET REPORTING LOG

$55,000.00 Example: 2018 Ford F-150 Truck

SMART

Asset ID

555

Agency Name:

Asset Transaction Type: Purchase/Recording of a New Asset

Asset Received from Another Agency

Asset Transferred to Another Agency

Changes to an Existing Asset

1234 SMART

SMART

SMART

SMART

SMART

17

Department of Administration Excellent customer service, every time!

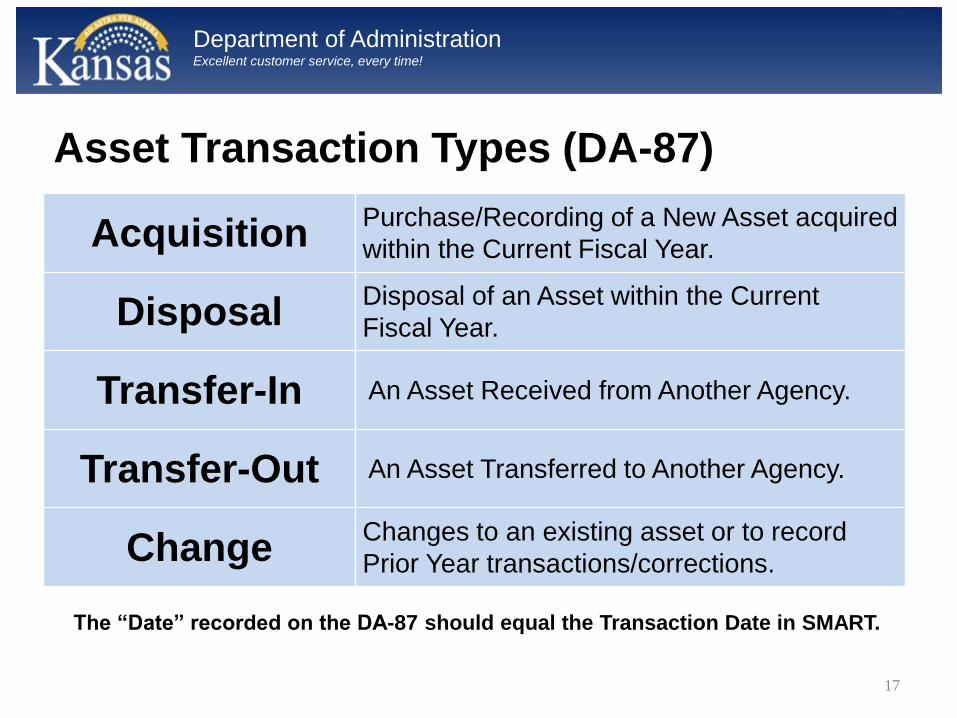

Acquisition Purchase/Recording of a New Asset acquired

within the Current Fiscal Year.

DisposalDisposal of an Asset within the Current

Fiscal Year.

Transfer-In An Asset Received from Another Agency.

Transfer-Out An Asset Transferred to Another Agency.

ChangeChanges to an existing asset or to record

Prior Year transactions/corrections.

Asset Transaction Types (DA-87)

The “Date” recorded on the DA-87 should equal the Transaction Date in SMART.

18

Department of Administration Excellent customer service, every time!

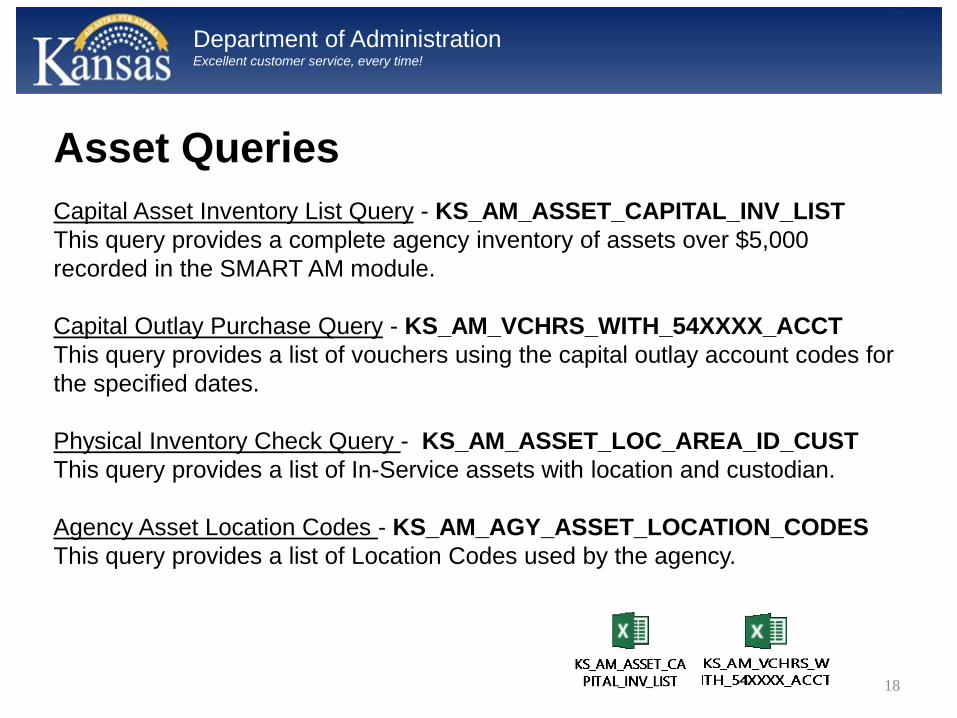

Asset Queries

Capital Asset Inventory List Query - KS_AM_ASSET_CAPITAL_INV_LIST

This query provides a complete agency inventory of assets over $5,000

recorded in the SMART AM module.

Capital Outlay Purchase Query - KS_AM_VCHRS_WITH_54XXXX_ACCT

This query provides a list of vouchers using the capital outlay account codes for

the specified dates.

Physical Inventory Check Query - KS_AM_ASSET_LOC_AREA_ID_CUST

This query provides a list of In-Service assets with location and custodian.

Agency Asset Location Codes - KS_AM_AGY_ASSET_LOCATION_CODES

This query provides a list of Location Codes used by the agency.

19

Department of Administration Excellent customer service, every time!

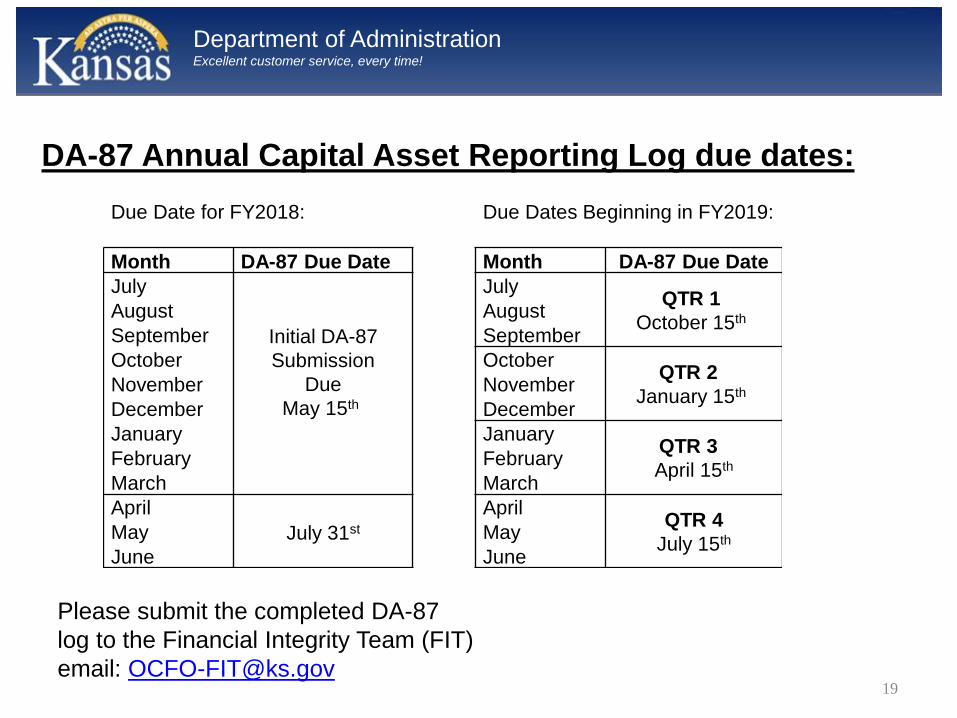

Due Date for FY2018: Due Dates Beginning in FY2019:

Month DA-87 Due Date Month DA-87 Due Date

July

Initial DA-87

Submission

Due

May 15th

JulyQTR 1

October 15thAugust August

September September

October OctoberQTR 2

January 15thNovember November

December December

January JanuaryQTR 3

April 15thFebruary February

March March

April

July 31st

AprilQTR 4

July 15thMay May

June June

DA-87 Annual Capital Asset Reporting Log due dates:

Please submit the completed DA-87

log to the Financial Integrity Team (FIT)

email: [email protected]

20

Department of Administration Excellent customer service, every time!

Inventories are required to verify the accuracy of property

records and the status of the assets recorded in the

SMART Asset Management module.

Physical inventories

are to be completed

ANNUALLYbefore

Fiscal Year-End Closing

21

Department of Administration Excellent customer service, every time!

DA-82 Capital Asset Supplemental Information

Certification of Fixed Asset Inspection

Due to OCFO Financial Integrity Team (FIT)

By August 1st of each year.

All capital assets are required to be recorded in the SMART

Asset Management (AM) module before fiscal year closing.

If an error or omission is found after year-end closing, in

addition to entering the correction in SMART AM, a detailed

explanation should be included with the DA-82 form.

22

Department of Administration Excellent customer service, every time!

Capital Asset Year-End Reminders

The following guidance is provided to assist in completing capital asset reporting:

✓ Capital asset physical inventories are to be completed annually. Inventories are recommended to be conducted

prior to June 15th to allow for corrections/additions to be recorded in the SMART AM module prior to SMART

Year-End deadlines.

✓ Verify correct Profile ID and Category Code are used for assets. Asset Profiles drive the depreciation and

accounting entry creation for CAFR purposes, it is crucial that the correct Asset Profile is used. SMART Job

Aid: Incorrect Asset Profiles and Corrections / Profile ID Section Job Aid

✓ Agencies should review Construction-In-Progress (CIP) before year-end closing to ensure all costs are included

in the asset module. CIP costs can be entered directly into AM as an addition/adjustment on the Cost

Adjust/Transfer page to add costs as expenditures are incurred. SMART Job Aid: CIP Assets

✓ Completed CIP assets need to be recategorized, the profile ID updated to a non-CIP profile, and other

requirements completed as further defined in the job aid. SMART Job Aid: CIP Assets (See Section: Steps to

Perform After CIP Asset is Complete)

✓ All assets that have been sent to state surplus, sold, or otherwise no longer in the agency’s possession should

be disposed of in the SMART AM module accordingly. SMART Job Aid: Retiring and Reinstating Assets

✓ Verify reported asset cost allocations, and update asset costs, if necessary. SMART Job Aid Adjustments and

Additions to Cost and/or Quantity

✓ For agencies utilizing integration, all outstanding Asset Integration Interface ID’s must be processed. SMART

Job Aid: Reviewing Transaction Loader Tables

Questions?

23

Department of Administration Excellent customer service, every time!

For Policy Questions:

Send an Email to: [email protected]

For SMART Processing Questions:

Submit a ManageEngine Service Desk ticket.

OCFO Policy Manuals:

http://admin.ks.gov/offices/chief-financial-officer/policy-manual

OCFO Forms:

http://admin.ks.gov/resources/document-center

SMART Job Aids can be located on the SMARTweb:

http://www.smartweb.ks.gov/training/asset-management

State Surplus Property Program website:

http://admin.ks.gov/offices/surplus-property/state-surplus

Contacts & Resources

Questions?

24

Department of Administration Excellent customer service, every time!

2017 & 2018 SEFAFindings, Issues, and Key Dates

Roger Basinger

Federal Reporting Team Lead

Department of Administration Excellent customer service, every time!

Inaccurate Reporting of Federal Expenditures (2017 SEFA Finding)

Condition/Context:

• On the 2017 SEFA audit there was a finding related to expenditures being reported inaccurately.

• The amount reported ($593,564) was over stated due to double reporting of expenditures by two different agencies on the DA-89 spreadsheets.

• The awarding agency reported the amount as an expenditure and the receiving agency reported the amount as a transfer in.

• This amount was corrected in the final SEFA for 2017.

26

Department of Administration Excellent customer service, every time!

Inaccurate Reporting of Federal Expenditures(2017 SEFA Finding)

Recommendation/Corrective Action:

• Auditors recommend the Department of Administration enhance review controls to verify expenditures are properly reported.

• Corrective action included contacting both agencies involved, a re-emphasis of DA-89 training, an expansion of SEFA review procedures, and reinforcing the DA-89 instructions.

27

Department of Administration Excellent customer service, every time!

Using Generic CFDA Numbers(2017 SEFA Issue: non-finding)

We had the following issue come up when completing the SEFA:

• Some agencies were reporting transfers in from other agencies under a generic CFDA number rather than the actual number.

• For example, an agency recording a transfer in from another agency under CFDA 10.000 when it should have been reported under CDFA 10.001.This causes the elimination report to not match up to the correct agency.

• Agencies transferring funds to another agency need to make sure that the agency has the correct CFDA number. Also, if an agency is unsure of the CFDA number they should ask the agency that is transferring the funds for the correct number.

• This has been an ongoing issue with the SEFA and is not new.

28

Department of Administration Excellent customer service, every time!

Warrant Cancellation(2017 SEFA Issue: non-finding)

The following was brought up to us by the auditors as a possible issue:

• A state agency had a warrant that was issued in June 2017 and then cancelled in July (after fiscal year end).

• The auditors (CLA) were concerned about whether the cancellation should have been included on the 2017 SEFA since the corrected amount crossed fiscal years.

• Although the amount in this case was not material, CLA worried that this may have occurred or may occur in the future with other agencies for larger amounts.

29

Department of Administration Excellent customer service, every time!

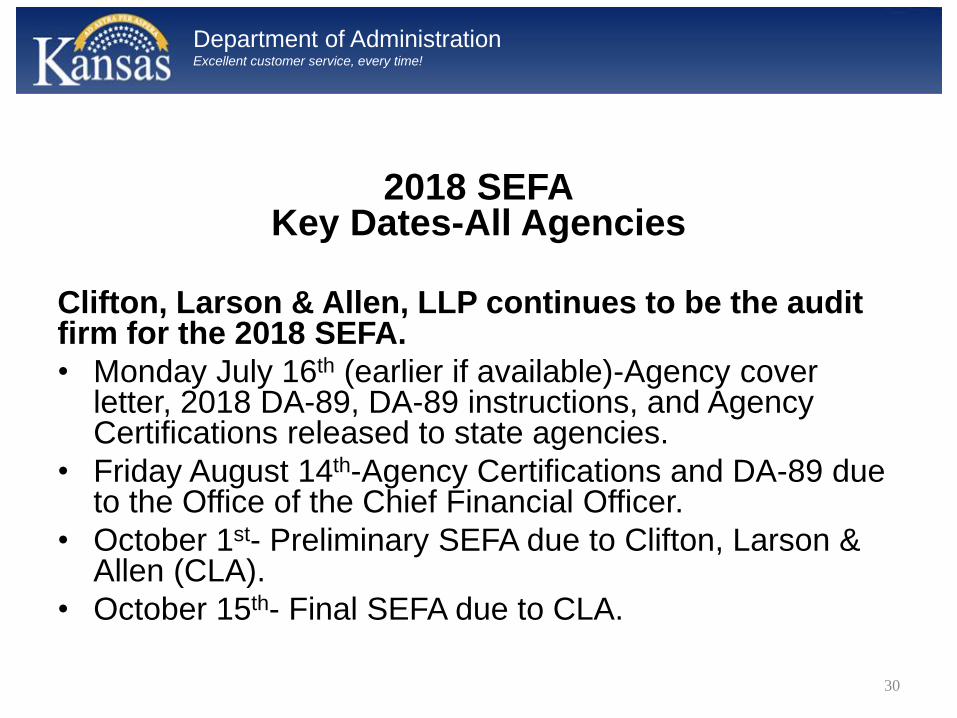

2018 SEFAKey Dates-All Agencies

Clifton, Larson & Allen, LLP continues to be the audit firm for the 2018 SEFA.

• Monday July 16th (earlier if available)-Agency cover letter, 2018 DA-89, DA-89 instructions, and Agency Certifications released to state agencies.

• Friday August 14th-Agency Certifications and DA-89 due to the Office of the Chief Financial Officer.

• October 1st- Preliminary SEFA due to Clifton, Larson & Allen (CLA).

• October 15th- Final SEFA due to CLA.

30

Department of Administration Excellent customer service, every time!

Questions?

31

Department of Administration Excellent customer service, every time!

CAFR DUE DATESFatima Gilbert

CAFR Accountant, Financial Integrity Team

32

Department of Administration Excellent customer service, every time!

FY 2018 CAFR Due Dates

33

Document Final Due Date

Legal liabilities 8/1/2018

Non-monetary transactions, federal grants, leases,

construction commitments and other liabilities 8/1/2018

DA-32(A) Accounts and Other Receivables 8/1/2018

DA-32 (B) Long Term Receivables 8/1/2018

DA-82 Capital Asset Supplemental Information 8/1/2018

Service Concession Arrangements for GASB 60 8/1/2018

Pollution Remediation for GASB 49 8/1/2018

Cash outside of the State Treasurer's Office 8/1/2018

DA-89 Schedule of Expenditures of Federal Awards

(SEFA) 8/14/2018

Draft Financial Reports 9/14/2018

Final Financial Reports 10/1/2018

KPERS Draft Financial Report 10/1/2018

KPERS Final Financial Report 10/15/2018

Department of Administration Excellent customer service, every time!

Questions?

34

Department of Administration Excellent customer service, every time!

Break (10 Minutes)

Upcoming: SMART/SHARP Updates

Department of Administration Excellent customer service, every time!

Statewide Payroll and

Accounting

SMART/SHARP Updates

36

Agenda• Fiscal Year End Info Circular Overview – Nancy Haufler

• Negative Cash Fund Balance at Fiscal Year End Policy – Kim

Fowler

• ACH Initiative Updates and Reminders – Kim Fowler

• Budget Date Change Requests and Template – Sunni Zentner

• e-Supplier – Sunni Zentner

• Moving Expenses – Amanda Entress

• SMART/SHARP Project Update – Nancy Ruoff

37

Fiscal Year End Info Circular

Overview

Nancy Haufler

SMART Processing Team Lead

38

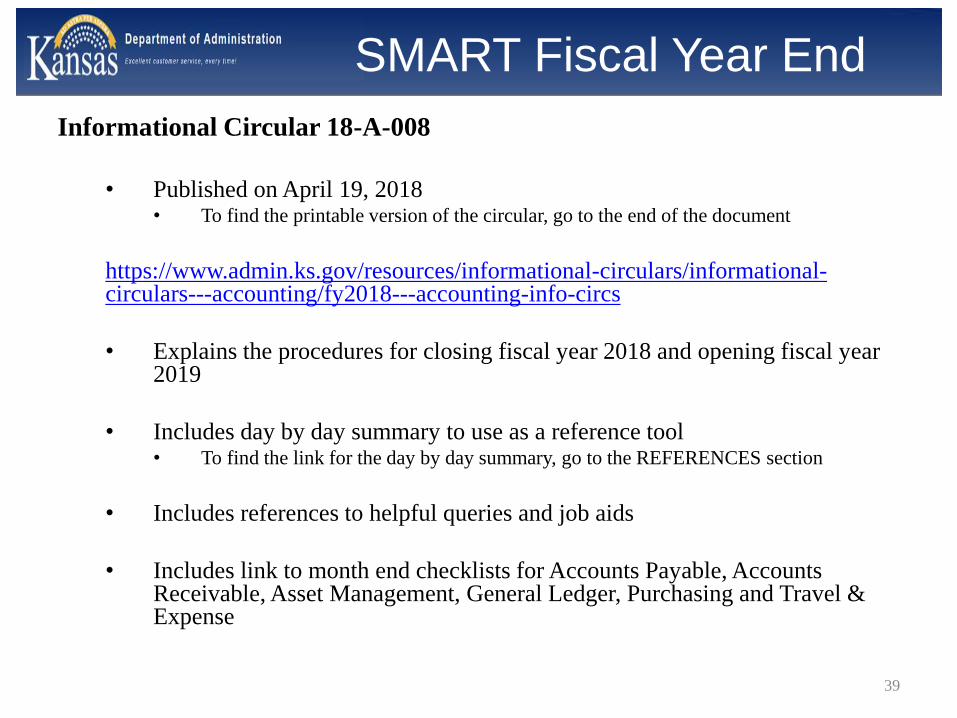

SMART Fiscal Year End

Informational Circular 18-A-008

• Published on April 19, 2018• To find the printable version of the circular, go to the end of the document

https://www.admin.ks.gov/resources/informational-circulars/informational-circulars---accounting/fy2018---accounting-info-circs

• Explains the procedures for closing fiscal year 2018 and opening fiscal year 2019

• Includes day by day summary to use as a reference tool• To find the link for the day by day summary, go to the REFERENCES section

• Includes references to helpful queries and job aids

• Includes link to month end checklists for Accounts Payable, Accounts Receivable, Asset Management, General Ledger, Purchasing and Travel & Expense

39

SMART Fiscal Year End

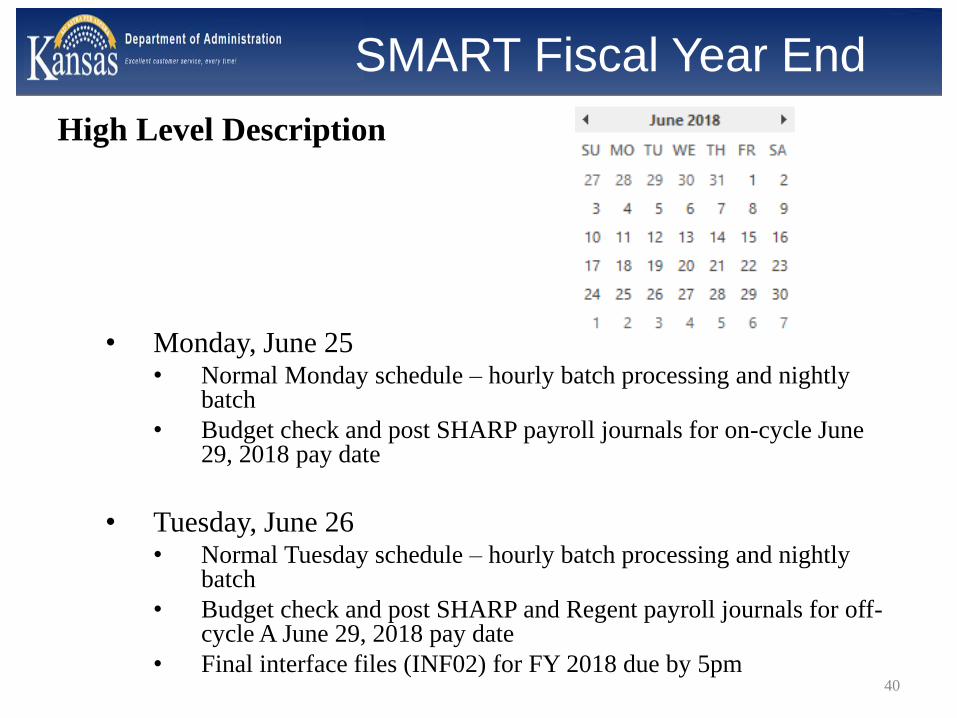

High Level Description

• Monday, June 25 • Normal Monday schedule – hourly batch processing and nightly

batch

• Budget check and post SHARP payroll journals for on-cycle June 29, 2018 pay date

• Tuesday, June 26 • Normal Tuesday schedule – hourly batch processing and nightly

batch

• Budget check and post SHARP and Regent payroll journals for off-cycle A June 29, 2018 pay date

• Final interface files (INF02) for FY 2018 due by 5pm40

SMART Fiscal Year End

High Level Description

• Wednesday, June 27• Last day for agencies to enter data in SMART for FY 2018

• Normal Wednesday schedule – hourly batch processing and nightly batch

• Review day by day summary for cutoff deadlines

• Thursday, June 28 and Friday, June 29 • Agencies will not have access to SMART

• SMART Team will be performing final clean-up and entering budget information for FY 2019

• Agency staff should be available to assist with questions

• Saturday, June 30• Agencies will not have access to SMART

• SMART Team will be performing final clean-up and entering budget information for FY 2019

41

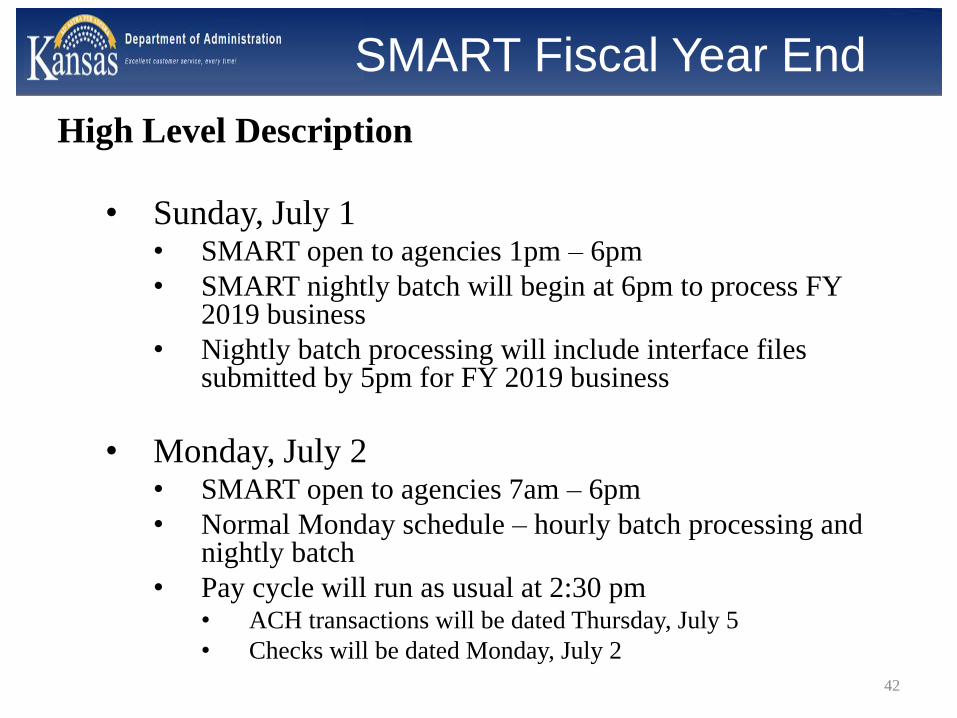

SMART Fiscal Year End

High Level Description

• Sunday, July 1• SMART open to agencies 1pm – 6pm

• SMART nightly batch will begin at 6pm to process FY 2019 business

• Nightly batch processing will include interface files submitted by 5pm for FY 2019 business

• Monday, July 2• SMART open to agencies 7am – 6pm

• Normal Monday schedule – hourly batch processing and nightly batch

• Pay cycle will run as usual at 2:30 pm• ACH transactions will be dated Thursday, July 5

• Checks will be dated Monday, July 2

42

SMART Fiscal Year End

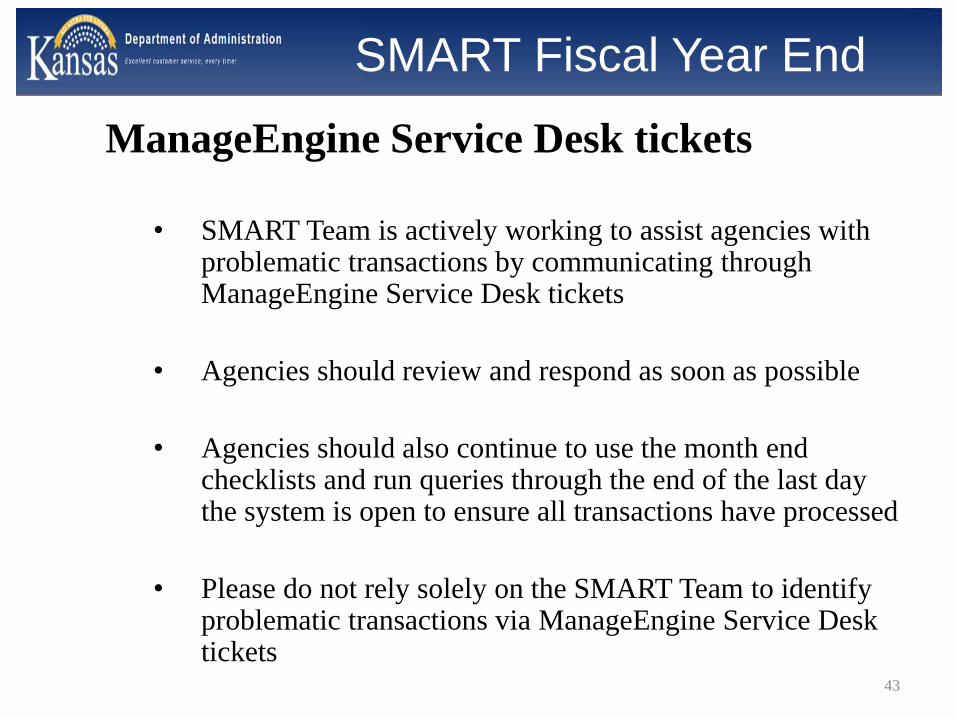

ManageEngine Service Desk tickets

• SMART Team is actively working to assist agencies with problematic transactions by communicating through ManageEngine Service Desk tickets

• Agencies should review and respond as soon as possible

• Agencies should also continue to use the month end checklists and run queries through the end of the last day the system is open to ensure all transactions have processed

• Please do not rely solely on the SMART Team to identify problematic transactions via ManageEngine Service Desk tickets

43

SMART Fiscal Year End

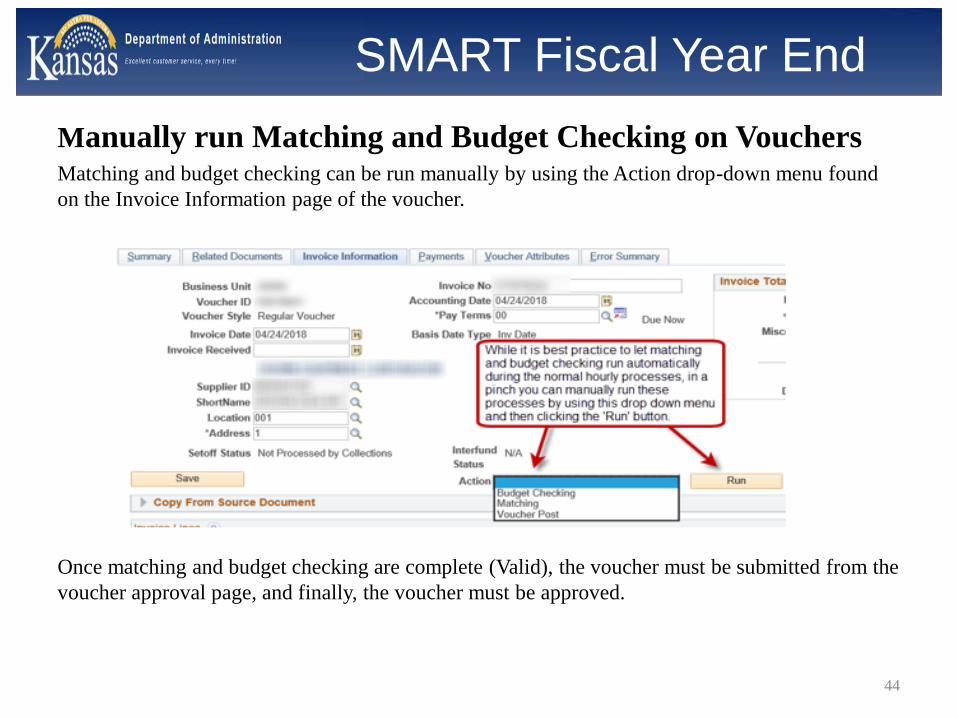

Manually run Matching and Budget Checking on VouchersMatching and budget checking can be run manually by using the Action drop-down menu found

on the Invoice Information page of the voucher.

Once matching and budget checking are complete (Valid), the voucher must be submitted from the

voucher approval page, and finally, the voucher must be approved.

44

SMART Fiscal Year End

Processing reminders

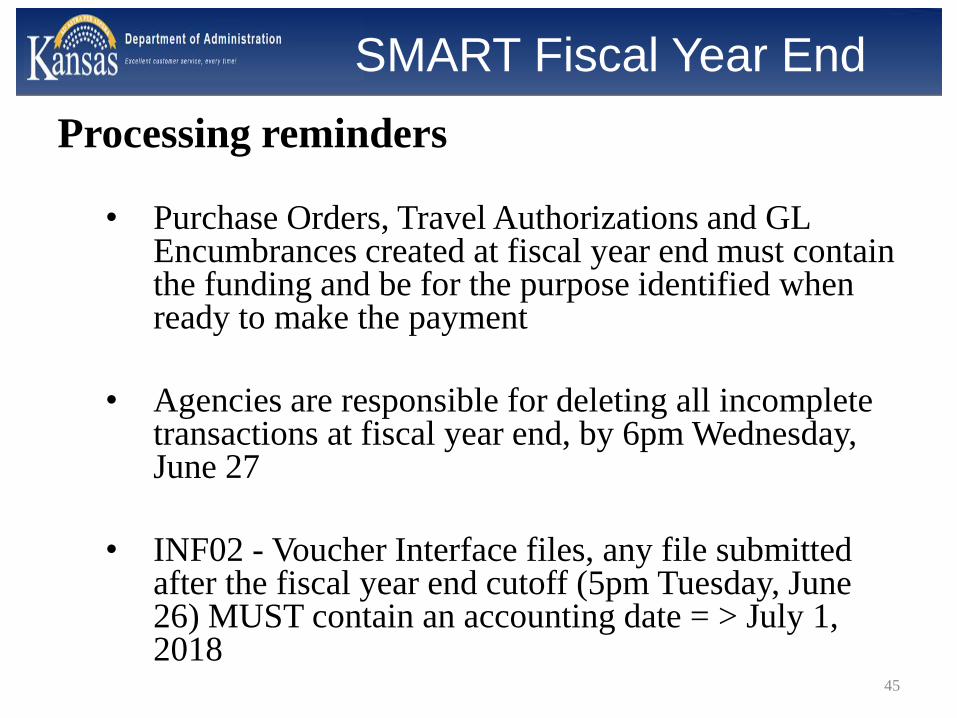

• Purchase Orders, Travel Authorizations and GL Encumbrances created at fiscal year end must contain the funding and be for the purpose identified when ready to make the payment

• Agencies are responsible for deleting all incomplete transactions at fiscal year end, by 6pm Wednesday, June 27

• INF02 - Voucher Interface files, any file submitted after the fiscal year end cutoff (5pm Tuesday, June 26) MUST contain an accounting date = > July 1, 2018

45

SMART Fiscal Year End

Processing reminders

• Refer to Policy Manual 14,002 Fiscal Year Closing of Obligations – General to determine appropriate processing period for each type of account code activity

• Remember the Accounts Receivable module is treated differently to accommodate receipts received through the last business day of the fiscal year Friday, June 29. Refer to details in the informational circular.

• SMART will be unavailable to users the morning of Friday, July 6 as the General Ledger closing entries are generated and processed. A SMART blast will be sent out once SMART is open for users.

46

Questions?

47

Negative Cash Fund Balance at

Fiscal Year End Policy

Kim Fowler

SMART Central Systems Responsibilities Team Lead

48

Negative Cash Fund Balance at Fiscal

Year End Policy

Negative Cash Fund Balance at Fiscal Year End

Policy Manual - Accounts Receivable Procedure 8,004 Federal Funds Fiscal Year End Negative Cash Balances

• Record an accounts receivable in SMART

• Document reimbursement has been requested

• JVs no longer used

49

Negative Cash Fund Balance at Fiscal

Year End Policy

Negative Cash Fund Balance at Fiscal Year End

Informational Circular 18-A-009Federal Funds Fiscal Year End Negative Cash Balances

Accounting Policy Questions:

Email Statewide Agency Audit Services Team at [email protected]

SMART Processing Questions:

Submit a ManageEngine Service Desk ticket

50

Negative Cash Fund Balance at Fiscal

Year End Policy

Negative Cash Fund Balance at Fiscal Year End

SMART Accounts Receivable job aids http://www.smartweb.ks.gov/training/accountsreceivable

• Accounts Receivable – Deposits:

• Accounts Receivable – Receivables:

51

ACH Initiative Updates and

Reminders

Kim Fowler

SMART Central Systems Responsibilities Team Lead

52

ACH Initiative Updates and Reminders

ACH Update and Reminders

May 2017 Informational Circular 17-A-013

• Travel and Expense payments mandatory ACH

• Increase ACH payment percentage in SMART

• Department of Administration takes Attachment A list

• Agencies work on the rest

• KS_AP_PAYMENT_CHK_COUNT

53

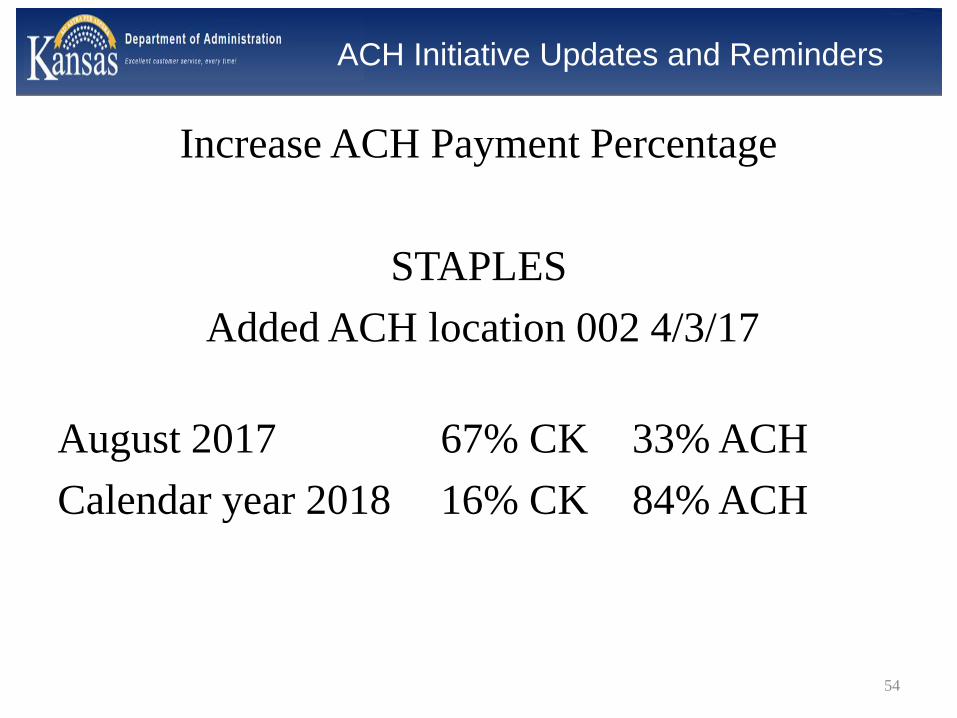

ACH Initiative Updates and Reminders

Increase ACH Payment Percentage

STAPLES

Added ACH location 002 4/3/17

August 2017 67% CK 33% ACH

Calendar year 2018 16% CK 84% ACH

54

ACH Initiative Updates and Reminders

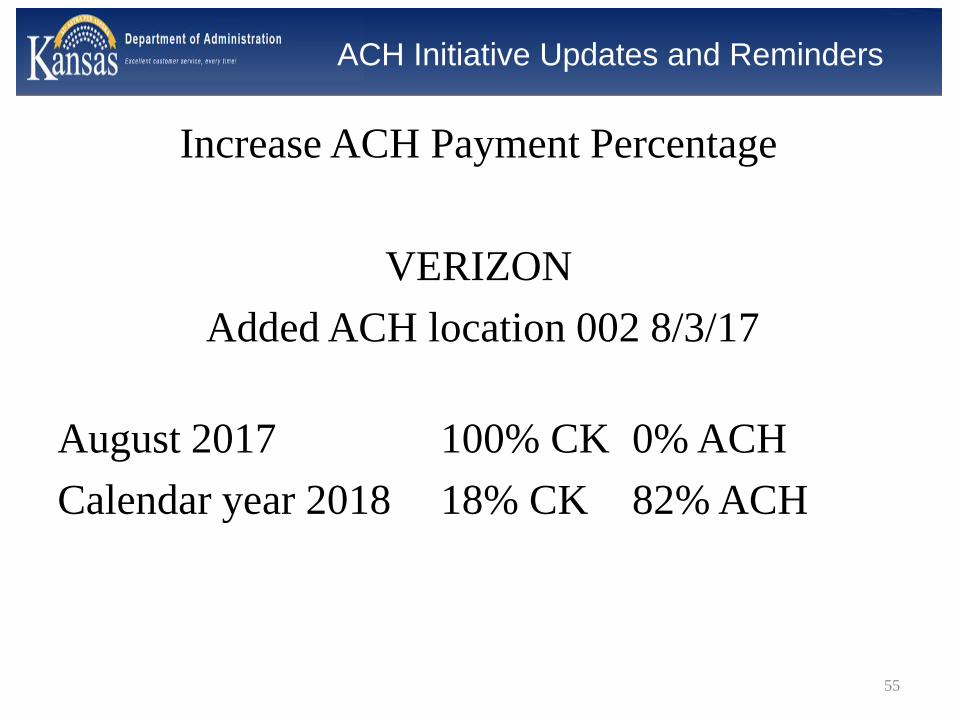

Increase ACH Payment Percentage

VERIZON

Added ACH location 002 8/3/17

August 2017 100% CK 0% ACH

Calendar year 2018 18% CK 82% ACH

55

ACH Initiative Updates and Reminders

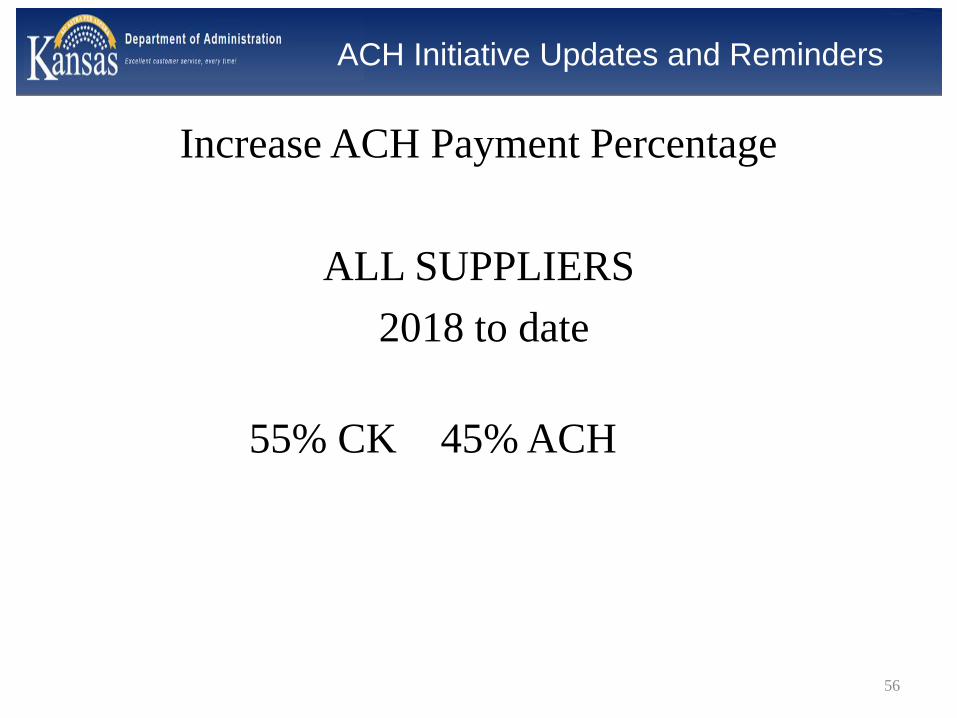

Increase ACH Payment Percentage

ALL SUPPLIERS

2018 to date

55% CK 45% ACH

56

ACH Initiative Updates and Reminders

Increase ACH Payment Percentage

Are we using the ACH payment location?

• Vouchers entered in SMART

• Change order on purchase orders created prior to

the addition of the ACH location

• Change the payment location on the payments tab

after the PO is associated with the voucher

• Vouchers interfaced into SMART

• Modify system to use ACH location57

ACH Initiative Updates and Reminders

ACH Department of Administration Progress

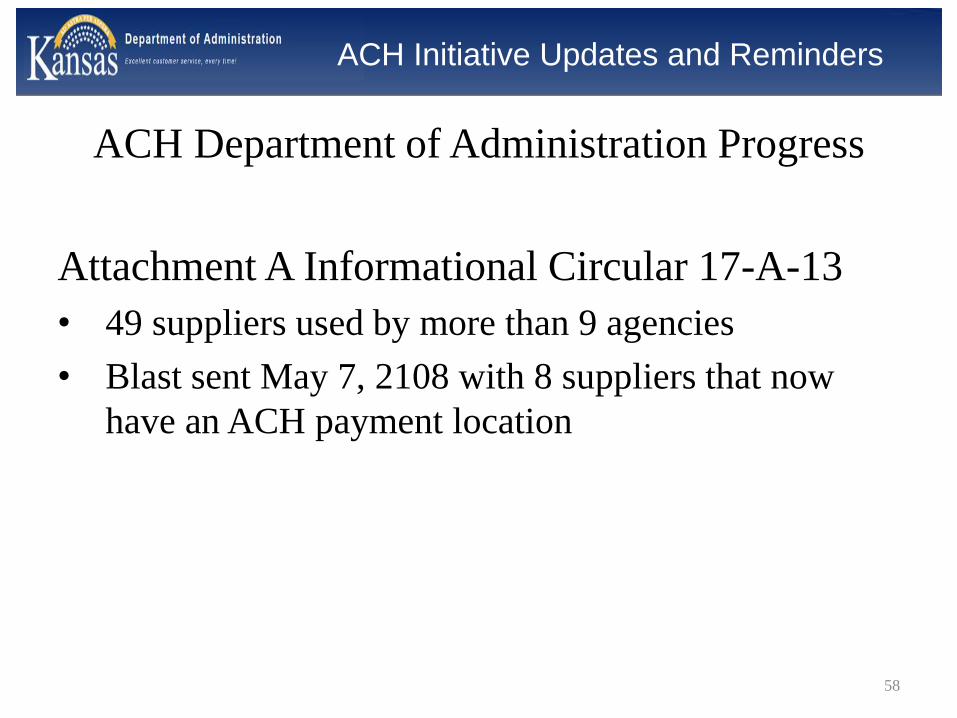

Attachment A Informational Circular 17-A-13

• 49 suppliers used by more than 9 agencies

• Blast sent May 7, 2108 with 8 suppliers that now

have an ACH payment location

58

ACH Initiative Updates and Reminders

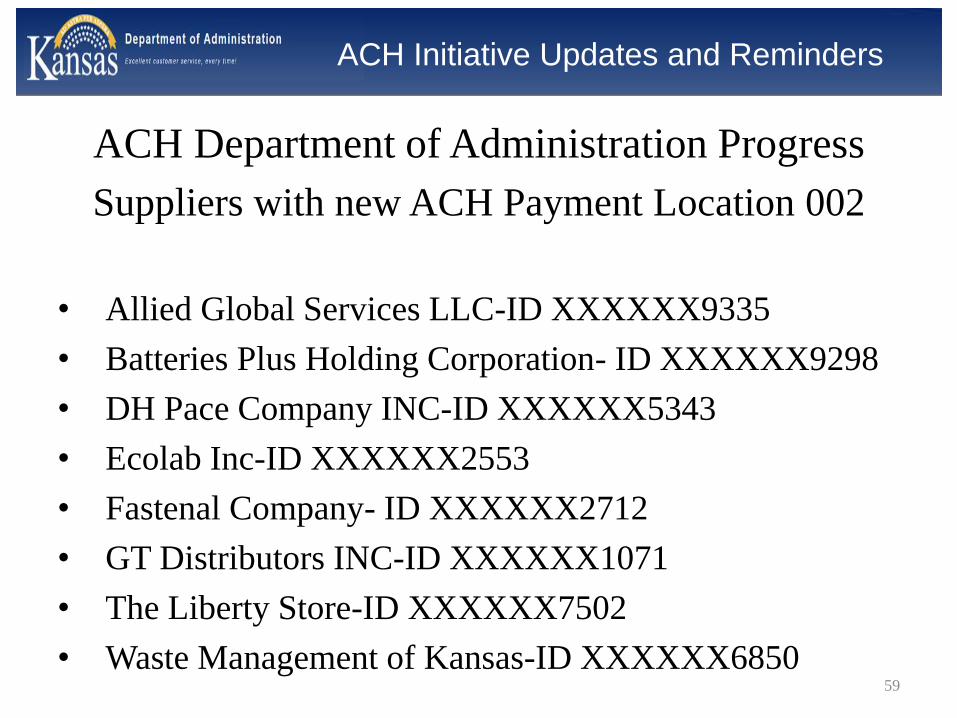

ACH Department of Administration Progress

Suppliers with new ACH Payment Location 002

• Allied Global Services LLC-ID XXXXXX9335

• Batteries Plus Holding Corporation- ID XXXXXX9298

• DH Pace Company INC-ID XXXXXX5343

• Ecolab Inc-ID XXXXXX2553

• Fastenal Company- ID XXXXXX2712

• GT Distributors INC-ID XXXXXX1071

• The Liberty Store-ID XXXXXX7502

• Waste Management of Kansas-ID XXXXXX685059

ACH Initiative Updates and Reminders

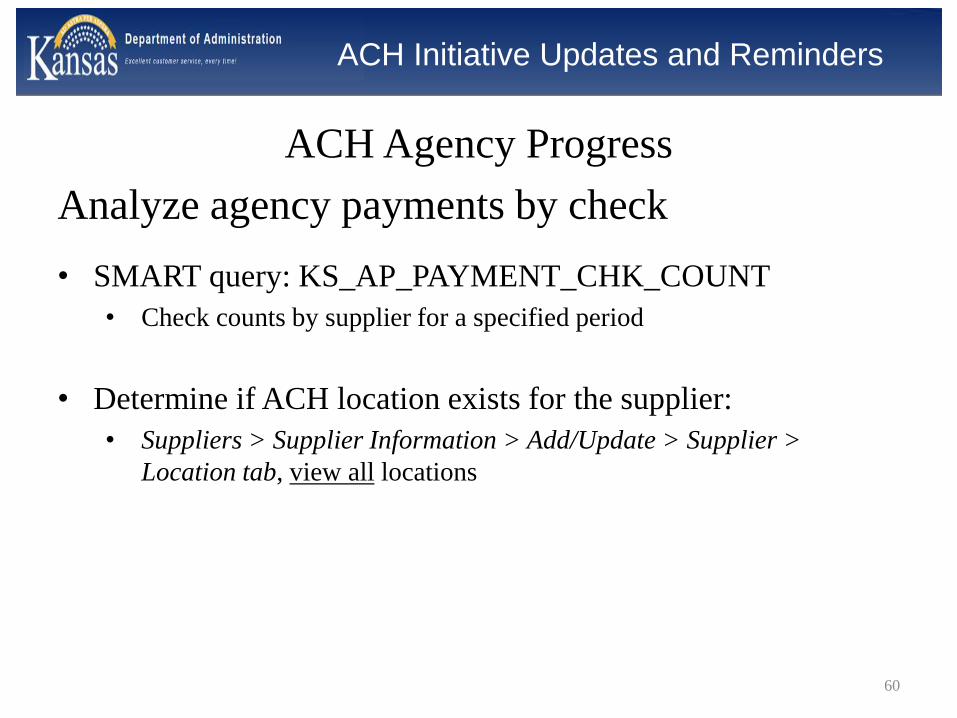

ACH Agency Progress

Analyze agency payments by check

• SMART query: KS_AP_PAYMENT_CHK_COUNT

• Check counts by supplier for a specified period

• Determine if ACH location exists for the supplier:

• Suppliers > Supplier Information > Add/Update > Supplier >

Location tab, view all locations

60

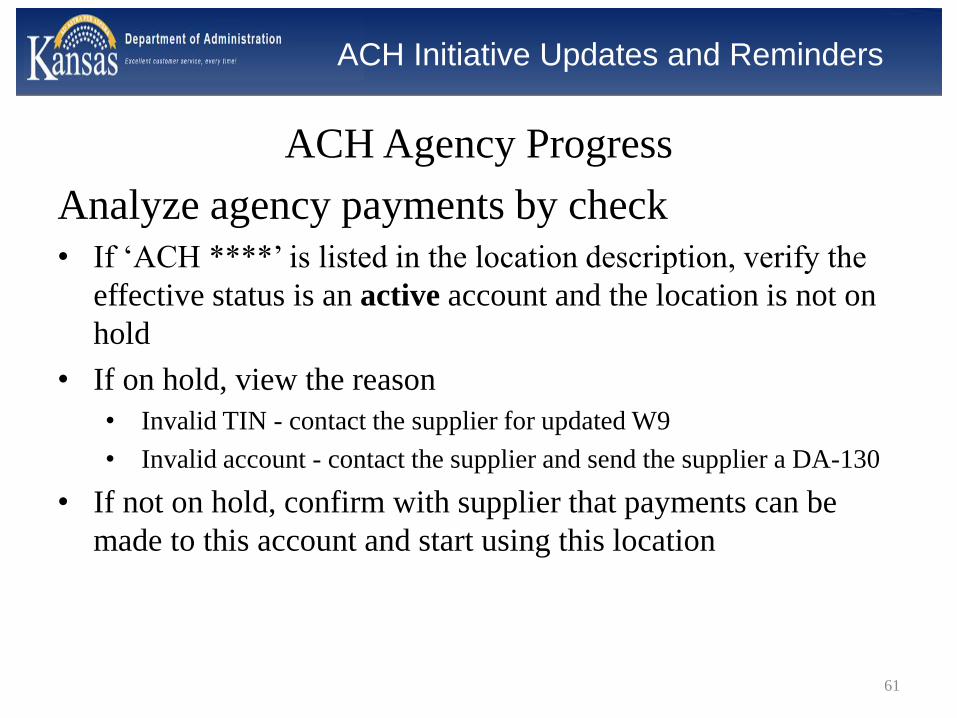

ACH Initiative Updates and Reminders

ACH Agency Progress

Analyze agency payments by check• If ‘ACH ****’ is listed in the location description, verify the

effective status is an active account and the location is not on

hold

• If on hold, view the reason

• Invalid TIN - contact the supplier for updated W9

• Invalid account - contact the supplier and send the supplier a DA-130

• If not on hold, confirm with supplier that payments can be

made to this account and start using this location

61

SMART ACH InitiaACH Initiative

Updates and Reminderstive

ACH Agency Progress

Work with suppliers to accept ACH payment• If SYSTEM CHECK is the only location description the

supplier does not have ACH account information in SMART

• Send the supplier a DA-130 form

62

ACH Initiative Updates and Reminders

ACH Agency Progress

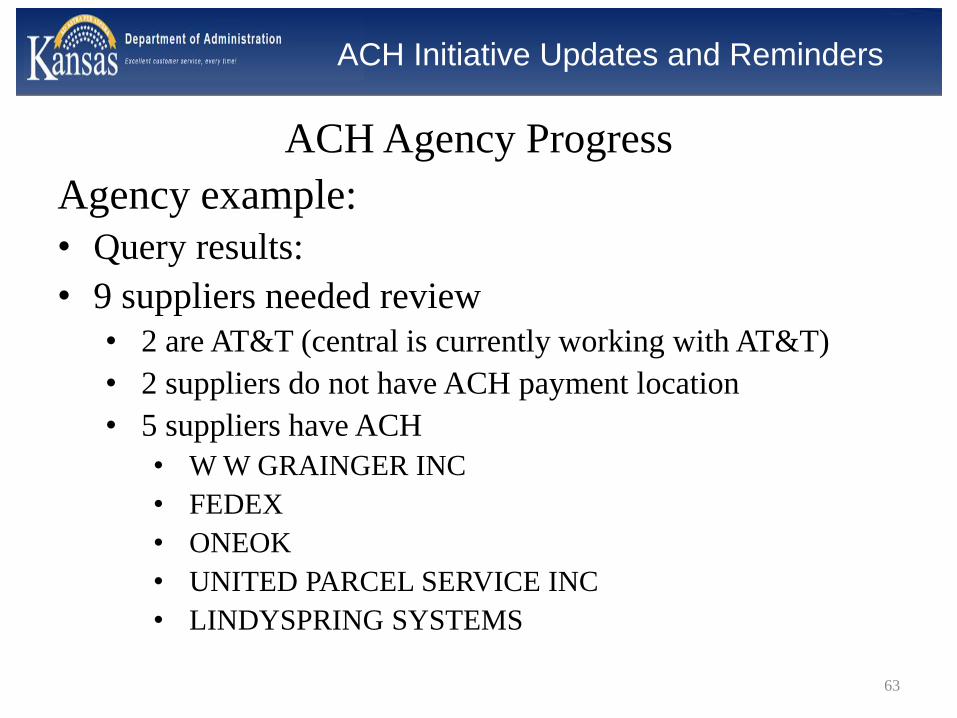

Agency example:

• Query results:

• 9 suppliers needed review

• 2 are AT&T (central is currently working with AT&T)

• 2 suppliers do not have ACH payment location

• 5 suppliers have ACH

• W W GRAINGER INC

• FEDEX

• ONEOK

• UNITED PARCEL SERVICE INC

• LINDYSPRING SYSTEMS

63

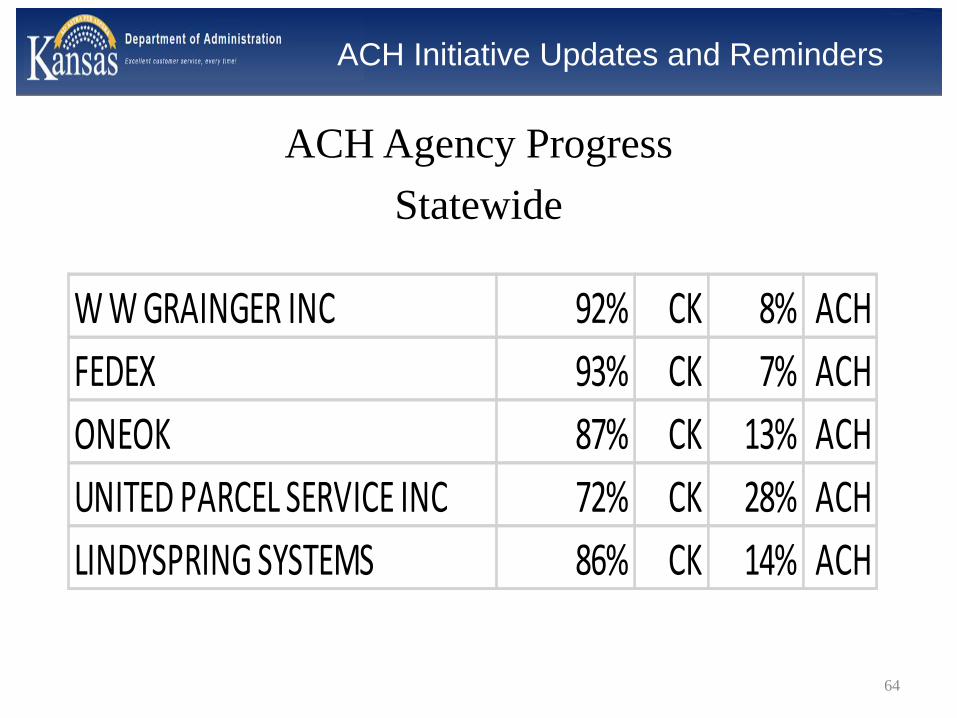

ACH Initiative Updates and Reminders

ACH Agency Progress

Statewide

64

W W GRAINGER INC 92% CK 8% ACH

FEDEX 93% CK 7% ACH

ONEOK 87% CK 13% ACH

UNITED PARCEL SERVICE INC 72% CK 28% ACH

LINDYSPRING SYSTEMS 86% CK 14% ACH

ACH Initiative Updates and Reminders

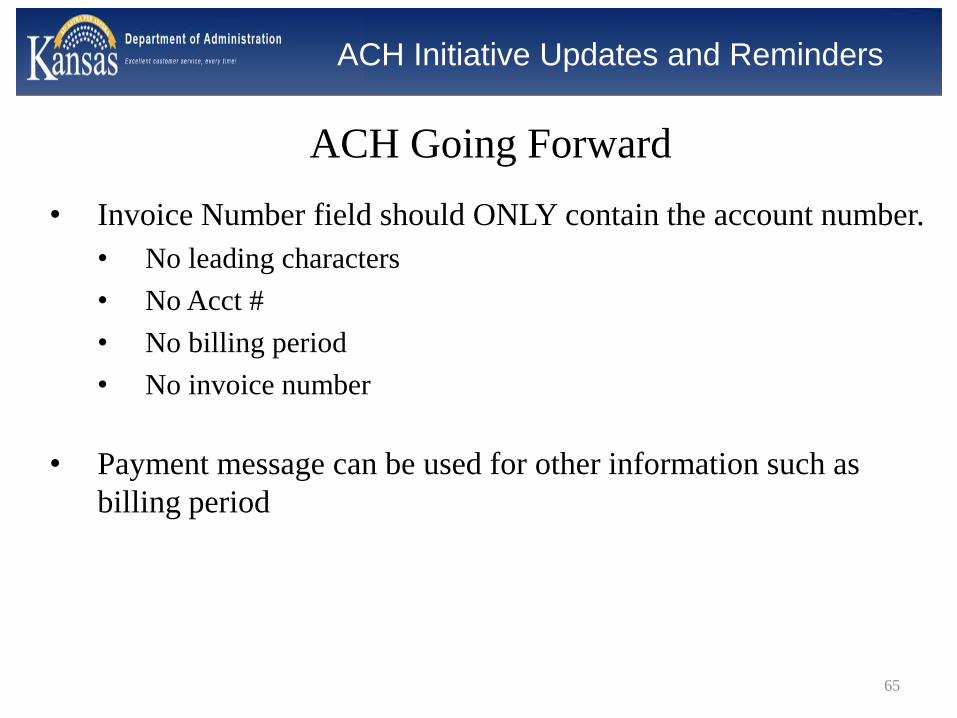

ACH Going Forward

• Invoice Number field should ONLY contain the account number.

• No leading characters

• No Acct #

• No billing period

• No invoice number

• Payment message can be used for other information such as

billing period

65

SMART Reminders

Kim Fowler

SMART Central Systems Responsibilities Team Lead

66

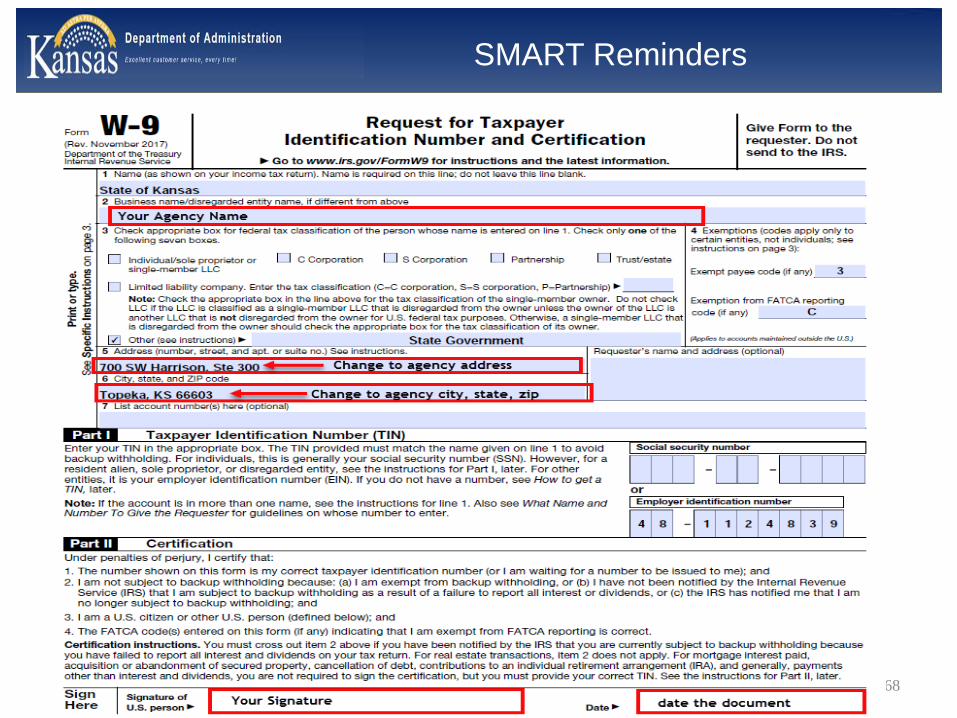

SMART Reminders

Please do not submit altered forms

Forms that have been altered will not be accepted

Example: Modified DA-130

67

SMART Reminders

68

Questions?

69

Budget Date Change Requests and

Template

Sunni Zentner, SMART Team Supervisor

70

Budget Date Change Requests and Template

The OCFO is analyzing agency budget date change

requests to determine if policy changes or

clarifications are needed regarding the use of prior

fiscal year encumbrances.

• Information was e-mailed to agencies through the

SMART Info distribution list on April 18, 2018

• A new form, GL-F026, must be completed and

attached to a ManageEngine Service Desk ticket

for budget date change requests

71

Budget Date Change Requests and Template

Links to documents:

• Budget Date Change Request Job Aid

• Budget Date Change Request Form (GL-F026)

72

Budget Date Change Requests and Template

When completing the Excel template:

• Because one form is used for multiple types of budget date change requests, the grayed lines are there as examples and to define the required fields for each type. Agency requests shall be filled in the white lines below.

• Multiple budget date change requests may be included on one form, as long as the type of request (for example, Requisition – GL Encumbrance) is the same for all lines.

• Additional entry lines may be inserted if there are multiple requisitions, funds, etc. included in the requests.

• The reason for the budget date change request must describe in detail why the current transaction is an appropriate use of the prior fiscal year funds.

73

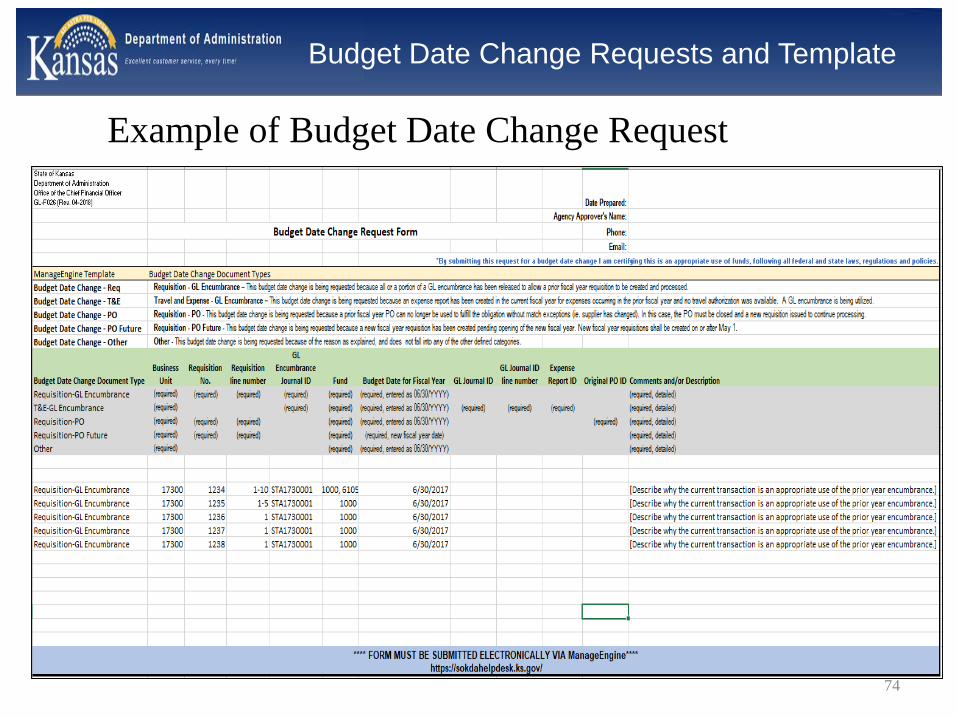

Budget Date Change Requests and Template

Example of Budget Date Change Request

74

Kansas eSupplier

Sunni Zentner, SMART Team Supervisor

75

Kansas eSupplier

Kansas eSupplier Module will be turned-on May 21

What is eSupplier?

• eSupplier is an external portal to SMART that came

delivered with the PeopleSoft Finance system, but

was not utilized until now

• State of Kansas will use eSupplier to:

• Allows bidders to self-register

• Allow suppliers to view invoice and payment

information from the system

76

Kansas eSupplier

• Office of Procurement and Contracts will send new bidders to Kansas eSupplier page to register

• Once registered, bidder users can view their contact information and update their purchasing category codes

• Once awarded an event, bidders become suppliers in SMART

• Supplier users will be able to view invoice and payment information

77

Phase I – May 21

Phased Approach

Kansas eSupplier

• Allow existing Kansas suppliers to register users

• Supplier users will be able to view invoices and payments

• Supplier users will be able to register as an administrator for the supplier account– The supplier (external) administrator will be able to

lock and unlock other supplier users within their organization, as well as reset passwords

78

Phase II – July 16

Phased Approach (continued)

Kansas eSupplier

What is agency’s role in using eSupplier?No changes:

• Continue to enter new suppliers into SMART, just as you do today

• Continue to verify and submit TM-21 forms for a supplier request for changes to contact information (via ManageEngine Service Desk)

• Continue to work with suppliers to convert payments from checks to ACH or update ACH information. DA-130 forms should continue to be verified and submitted to the SMART Team (via ManageEngineService Desk)

79

Kansas eSupplier

What about the current Vendor Payment Self-Service Search page on the Department of Administration’s web site?

Link: https://admin.ks.gov/offices/chief-financial-officer/central-responsibilities/vendor-payment-self-service/vpss-search

• This page will continue to be supported for now

• When Phase II is implemented on July 16, a notice will be displayed on this page to direct suppliers to register and begin using Kansas eSupplier

• When the decision is made to discontinue, agencies will be given plenty of warning and an appropriate notice will be posted to the page for any suppliers still using it

80

Kansas eSupplier

What do the pages look like?

• Kansas eSupplier landing page

81

Kansas eSupplier

82

Kansas eSupplier

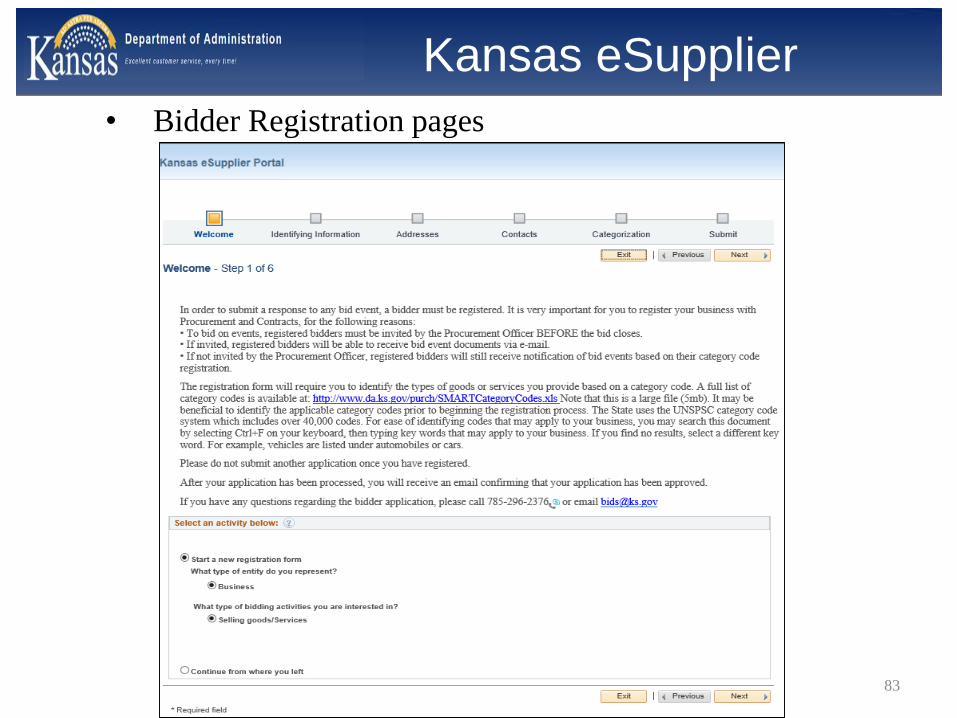

• Bidder Registration pages

83

Kansas eSupplier

84

Kansas eSupplier

85

Kansas eSupplier

86

Kansas eSupplier

87

Kansas eSupplier

88

Kansas eSupplier

89

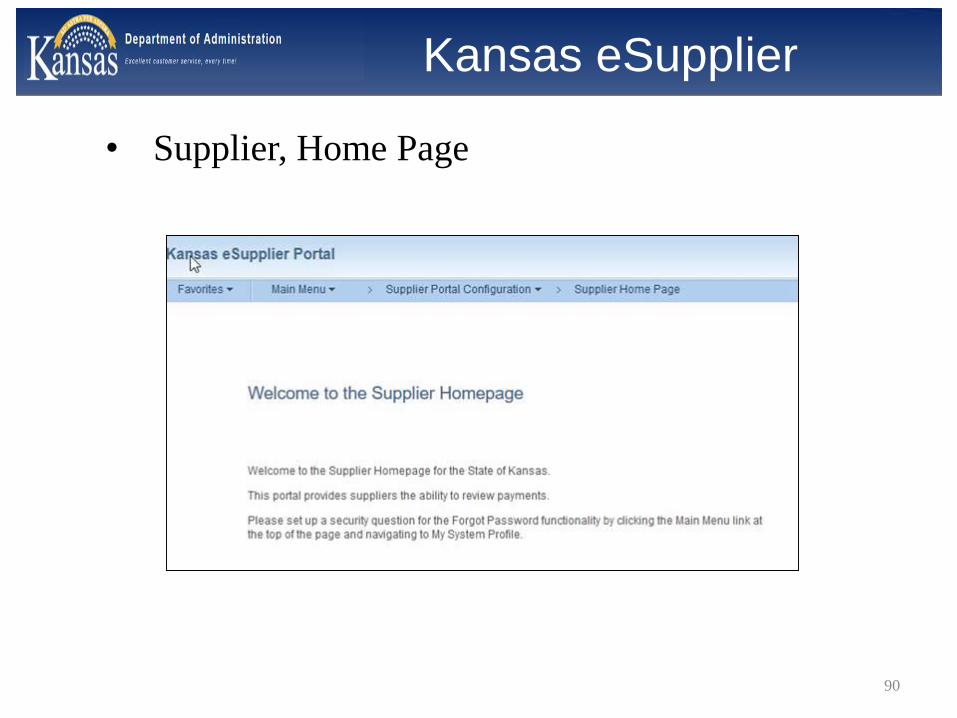

Kansas eSupplier

• Supplier, Home Page

90

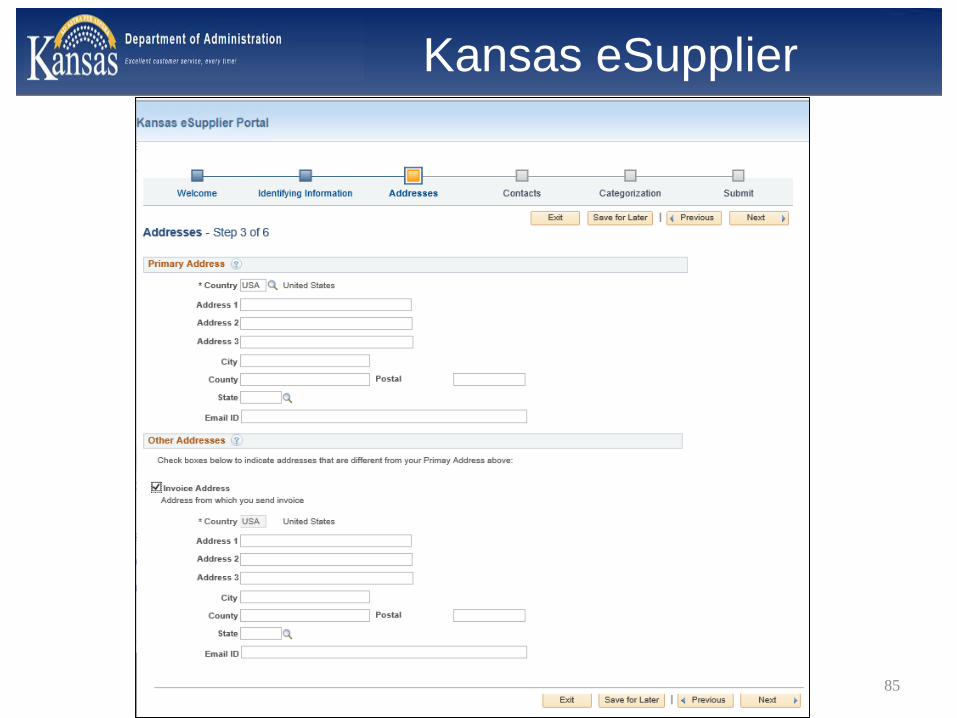

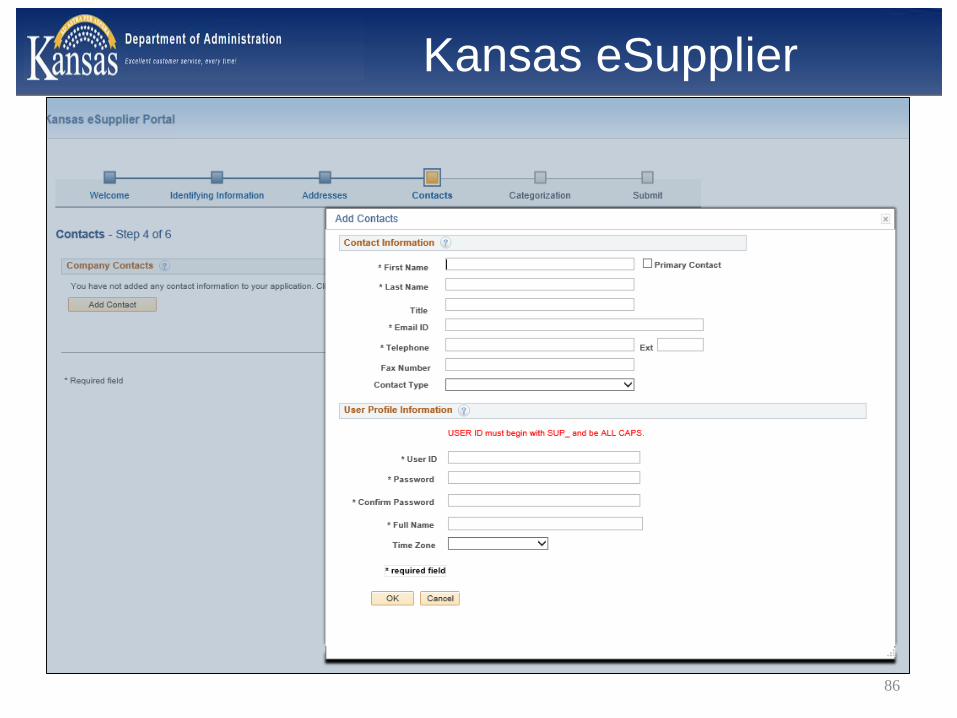

Kansas eSupplier

• Supplier, Addresses Page

91

Kansas eSupplier

• Supplier, Addresses Page

92

Kansas eSupplier

• Supplier invoice view

93

Kansas eSupplier

94

Kansas eSupplier

• Supplier payment view

• Modifications were made to include the paying

agency and the payment message

95

Kansas eSupplier

96

Kansas eSupplier

What is NOT included within the eSupplier pages?

• TIN

• Bank information

The risks associated with having the eSupplier portal

open are mitigated by limiting the data elements that

can be viewed as well as the limiting the

maintenance that the user can perform.

97

Questions?

98

Moving Expenses

Amanda Entress

SHARP Processing Team Lead

99

Moving Expenses

Taxation of Moving Expense Reimbursements:

The federal Tax Cuts and Job Act (H.R.1) enacted

in law on December 22, 2017 amends Internal

Revenue Code – Title 26, Section 132 (g)

suspending the existing exclusion for qualified

moving expense reimbursements from gross

income

100

What does this mean for State of Kansas Agencies and Employees?

• Effective January 1, 2018 all moving expenses reimbursed to an employee are considered taxable income to the employee and include applicable employer taxes (includes 2017 expenses reimbursed in 2018)

• Reimbursement amounts are also taxable at the State and Local level unless there is specific legislation to exempt the reimbursement from gross earnings

• All moving expenses must be reimbursed directly to the employee and paid through SHARP using the Moving Expense Taxable (MVT) earnings code (see Info Circ 18-P-019 at https://www.admin.ks.gov/resources/informational-circulars/informational-circulars---payroll/fy2018---payroll-info-circs

101

Moving Expenses

What does this mean for State of Kansas Agencies and

Employees?

• Moving related payments are no longer authorized to be paid directly to a

commercial carrier

• The amount to be paid for moving household and personal effects may not

in any case exceed the amount of the actual reimbursable moving expenses

verified by receipts and bill of lading

• Policy Manual 3,607 – Employee Moving Expense Reimbursement has

been updated and is available on the Department of Administration

website: http://admin.ks.gov/offices/chief-financial-officer/policy-manual

102

Moving Expenses

SMART/SHARP Project Update

Nancy Ruoff

Statewide Payroll and Accounting Manager

103

SHARP/SMART Project

SHARP/SMART Upgrade Project Goals:

• Modernize and enhance existing user experience

• Implement new functionality in targeted areas

• Apply security and system updates

104

SHARP/SMART Project

SHARP/SMART Upgrade Project Scope:

• Implement new PeopleSoft User Interface

• Upgrade to PeopleTools v8.56

• Upgrade to SHARP PUM 25/SMART PUM 26

105

SHARP/SMART Project

New PeopleSoft User Interface:

• Modernizes the ‘look and feel’ of SHARP/SMART for

all user interactions (i.e. Employee Self Service, Core

users)

• Provides multi-platform mobility for select pages

• Automatically modifies display of developed ‘FLUID’ pages

based on type of device being used (i.e. smartphone, tablet)

• Additional pages will be transitioned to ‘FLUID’ in the

future

106

SHARP/SMART Project

New PeopleSoft User Interface:

• Updates navigation to be more intuitive and reduce

‘clicks’ required to reach a specific page

• Uses navigation (nav) collections and ‘tiles’ to create logical

groupings of pages by business function

• Navigation collections work like a group of shortcuts

• The new User Interface does not change system

functionality

• It does not change ‘what’ you do when you reach a

SHARP/SMART page...

…but ‘how’ you get to the page to do your job107

SHARP/SMART Project

PeopleTools/PUM Upgrade:

• Applies up-to-date system and security patches, fixes,

and updates

• Provides the framework/opportunity for additional

future enhancements/functionality

• Limited new functionality (other than FLUID) will be

included in the scope of this upgrade

108

SHARP/SMART Project

SHARP/SMART Upgrade Project Schedule:

• Currently in Discovery and Fit/Gap phase of the

project

• Anticipated go-live in 1st Qtr, 2019

• Additional information will be provided as the

project progresses!

109

Questions?

110