Embed Size (px)

Citation preview

Denise Rouleau New England School of Acupuncture

Bob Cohen Attain LLC

Joe O’Brien Attain LLC

Cost TransfersClearly Allowable, Clearly Not Allowable,

Clearly Confusing?

FRA XIVMarch 12, 2013

Learning Objectives

What Are Cost Transfers?

Recent Findings

Challenge For Research Administrators

Typical Audit Questions/ Findings

What Federal Regulations Require

Cost Transfer Red Flags

What Have We Learned?

How To Manage Risk

Case Studies

What are Cost Transfers?

Lets begin with a definition…

A Cost Transfer is the transfer of an expenditure that initially posted

to one project and is then transferred to another project

What are Cost Transfers?

Salary expenditures

Labor, including salaries, wages, and benefits

Non-salary expenditures

Non-Labor, all costs other than salary (e.g., chemicals, lab supplies, equipment, travel, internal service provider charges)

Recent Findings

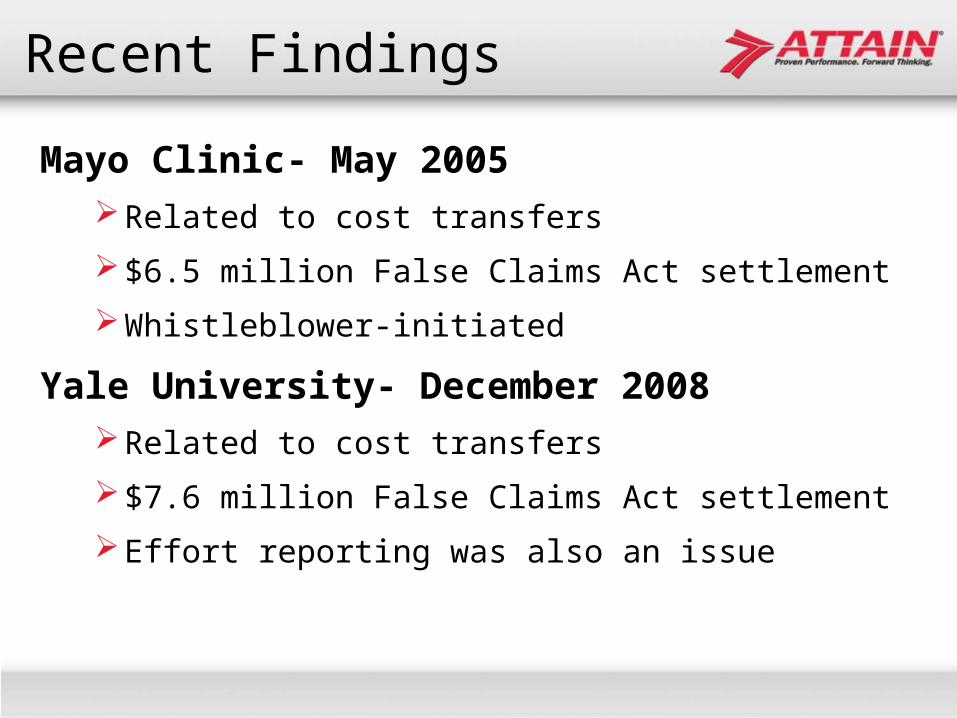

Mayo Clinic- May 2005Related to cost transfers

$6.5 million False Claims Act settlement

Whistleblower-initiated

Yale University- December 2008Related to cost transfers

$7.6 million False Claims Act settlement

Effort reporting was also an issue

Recent Findings

Univ. of California Santa Barbara – Sept 2012$500,000 of Cost Transfers Questioned by NSF

OIG$6.3M total Compliance Findings

Georgia Institute of Technology – June 2009Effort Reporting Controls and Transfers$16M in NSF Salaries, $49M in other Federal

Salaries

Recent Findings

Thomas Jefferson University – April 200711-year NIH review after designation as “High

Risk”6-year Integrity Agreement with HHS

California Institute of Technology – March 2007Salary transferred from Overspent NSF Award

Challenge for Research Administrators

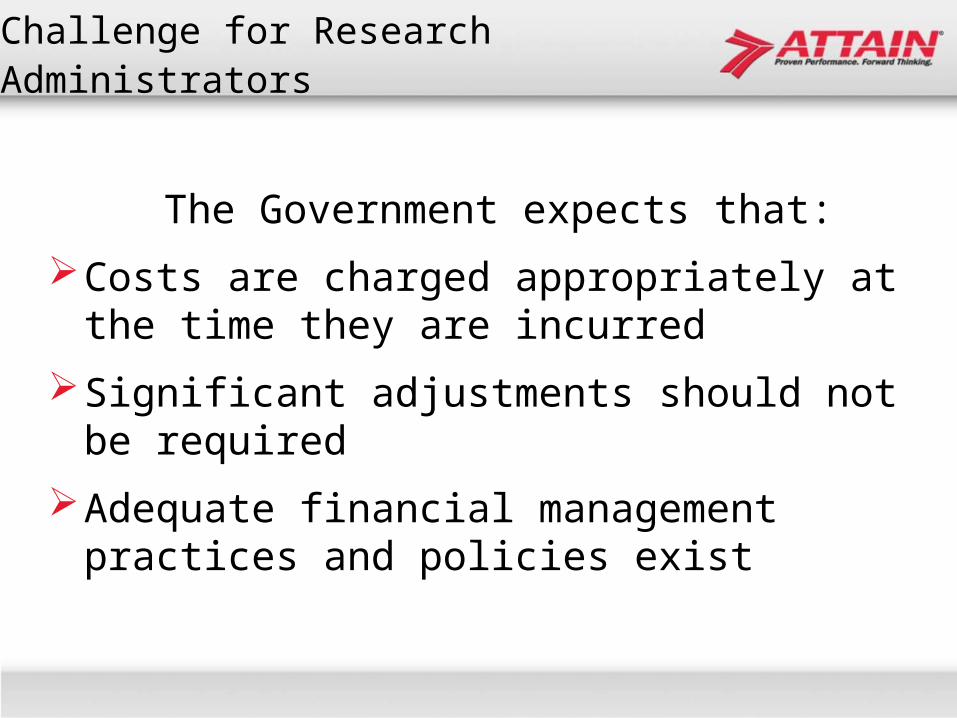

The Government expects that:

Costs are charged appropriately at the time they are incurred

Significant adjustments should not be required

Adequate financial management practices and policies exist

Challenge for Research Administrators

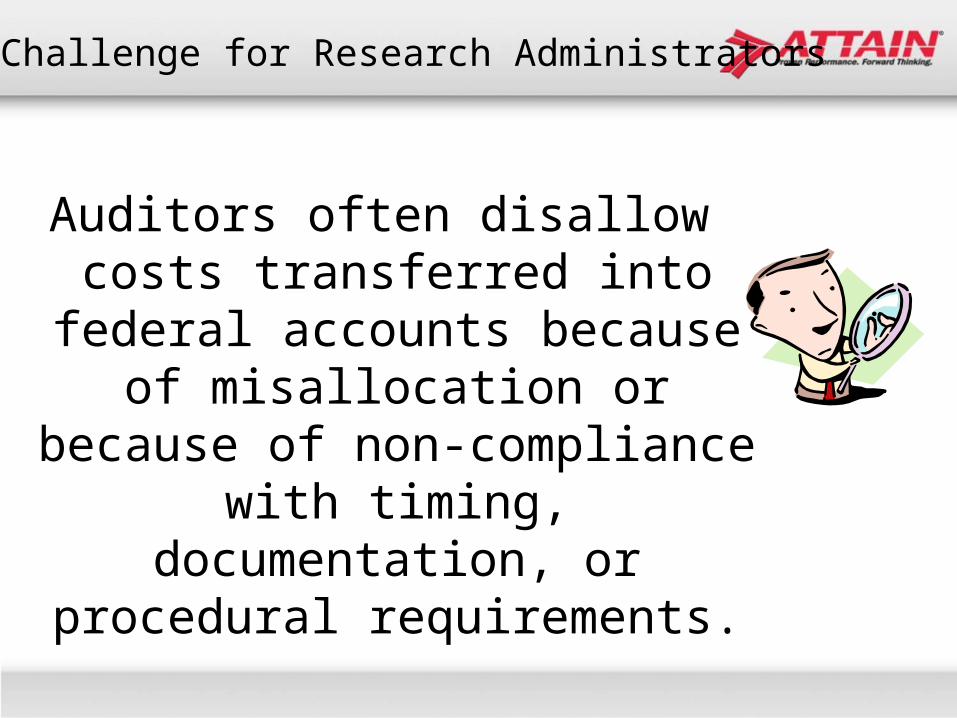

Auditors often disallow costs transferred into federal

accounts because of misallocation or because of non-compliance with timing,

documentation, or procedural requirements.

Challenge for Research Administrators

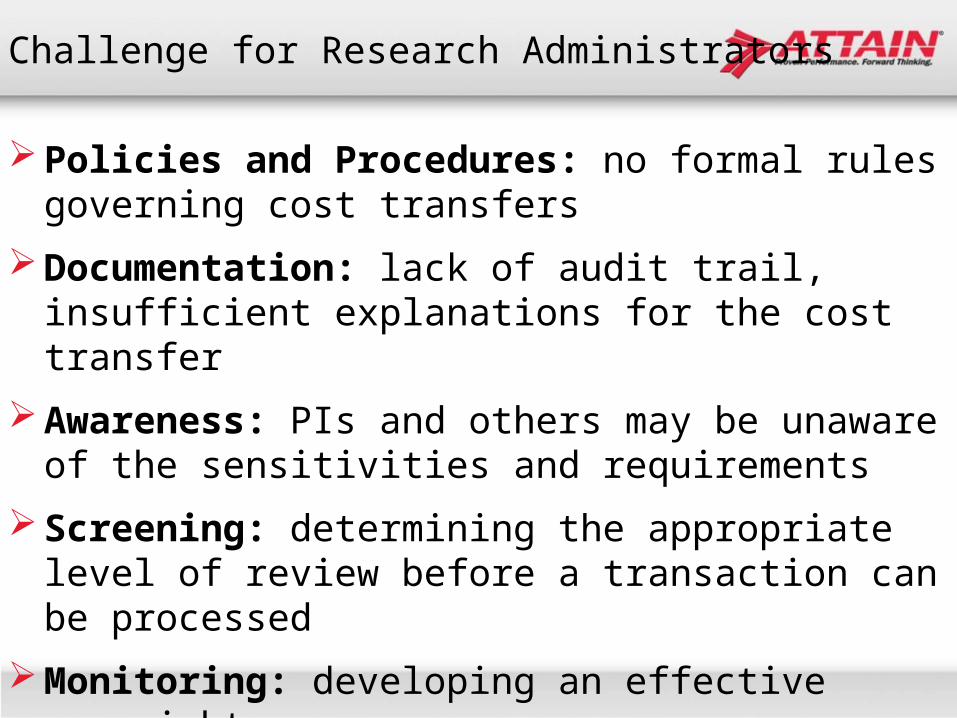

Policies and Procedures: no formal rules governing cost transfers

Documentation: lack of audit trail, insufficient explanations for the cost transfer

Awareness: PIs and others may be unaware of the sensitivities and requirements

Screening: determining the appropriate level of review before a transaction can be processed

Monitoring: developing an effective oversight program

Challenge for Research Administrators

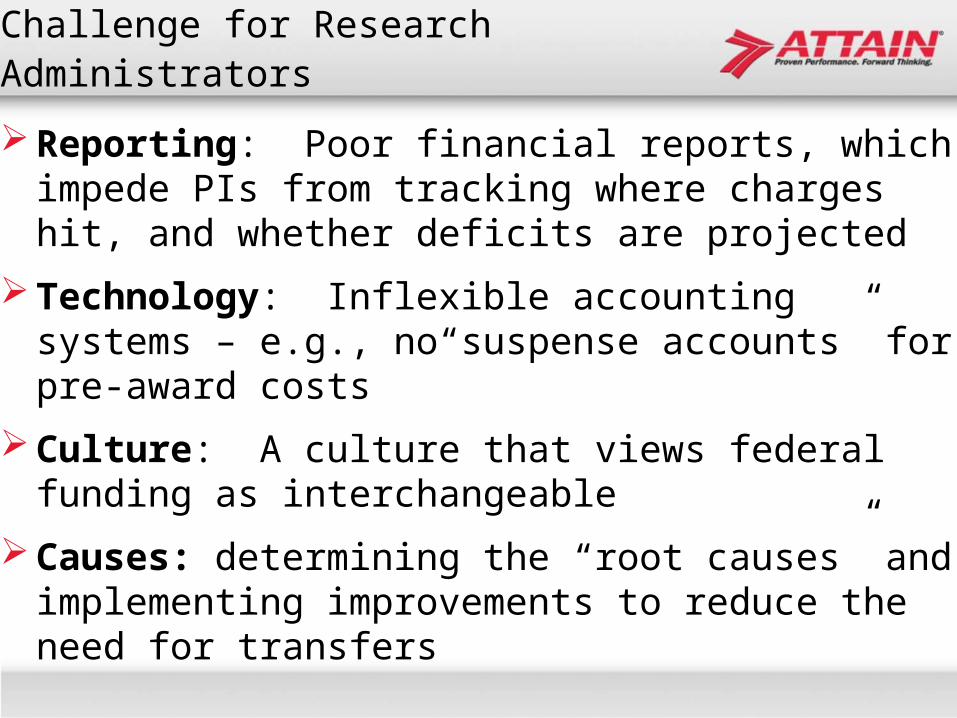

Reporting: Poor financial reports, which impede PIs from tracking where charges hit, and whether deficits are projected

Technology: Inflexible accounting systems – e.g., no“suspense accounts” for pre-award costs

Culture: A culture that views federal funding as interchangeable

Causes: determining the “root causes” and implementing improvements to reduce the need for transfers

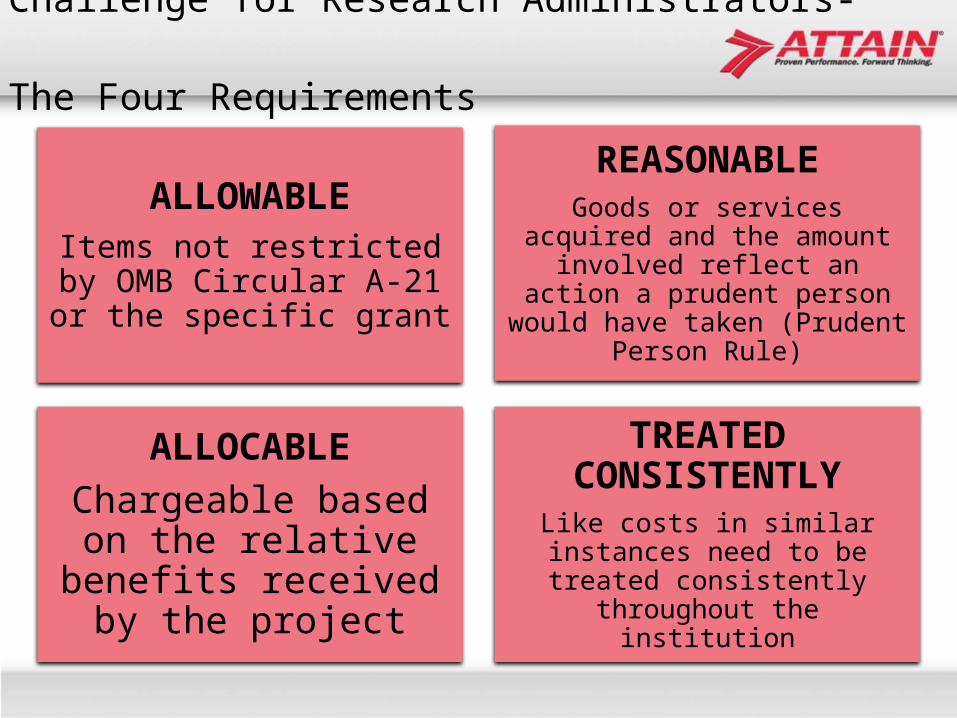

Challenge for Research Administrators- The Four Requirements

ALLOWABLEItems not restricted by

OMB Circular A-21 or the specific grant

REASONABLEGoods or services acquired and the amount involved

reflect an action a prudent person would have taken

(Prudent Person Rule)

ALLOCABLEChargeable based on the relative benefits

received by the project

TREATED CONSISTENTLY

Like costs in similar instances need to be treated

consistently throughout the institution

Typical Audit Questions/ Findings

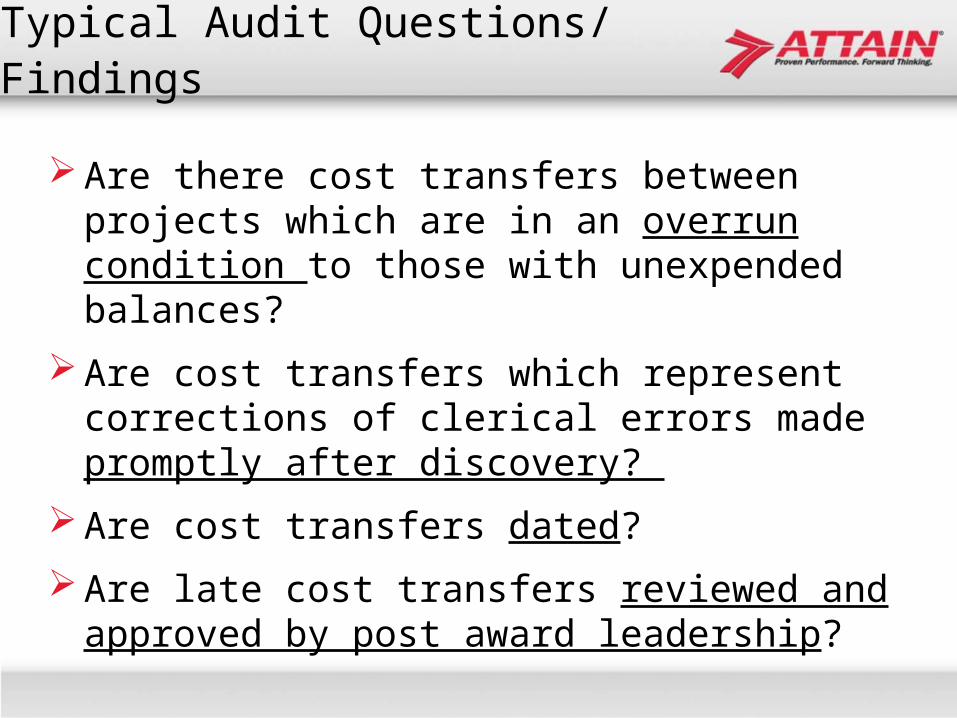

Are there cost transfers between projects which are in an overrun condition to those with unexpended balances?

Are cost transfers which represent corrections of clerical errors made promptly after discovery?

Are cost transfers dated?

Are late cost transfers reviewed and approved by post award leadership?

Typical Audit Questions/ Findings

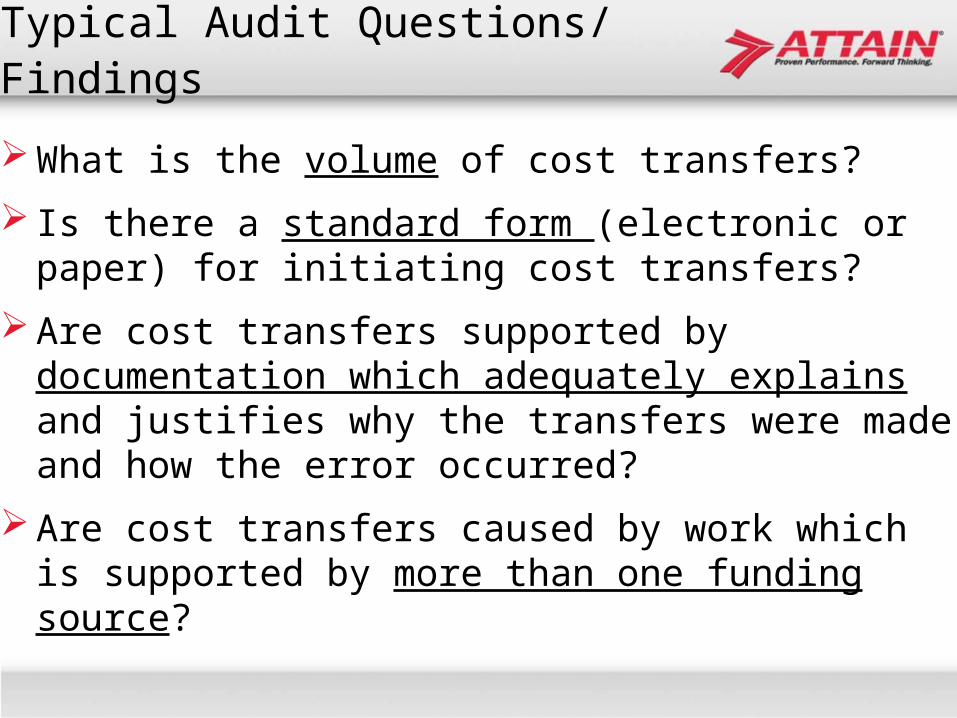

What is the volume of cost transfers?

Is there a standard form (electronic or paper) for initiating cost transfers?

Are cost transfers supported by documentation which adequately explains and justifies why the transfers were made and how the error occurred?

Are cost transfers caused by work which is supported by more than one funding source?

Typical Audit Questions/ Findings

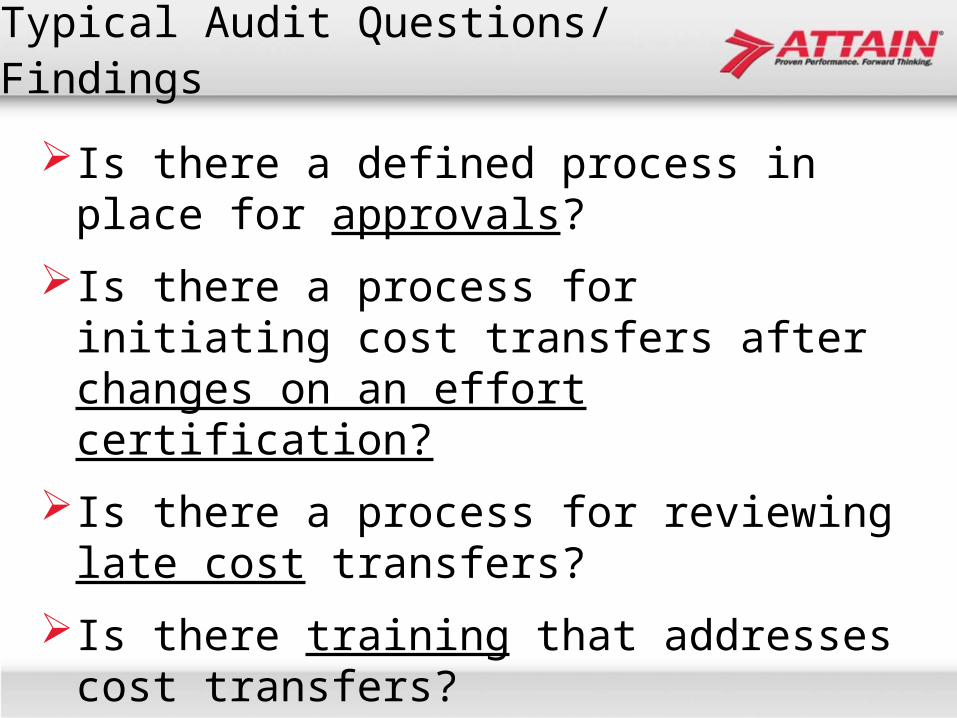

Is there a defined process in place for approvals?

Is there a process for initiating cost transfers after changes on an effort certification?

Is there a process for reviewing late cost transfers?

Is there training that addresses cost transfers?

Typical Audit Questions/ Findings

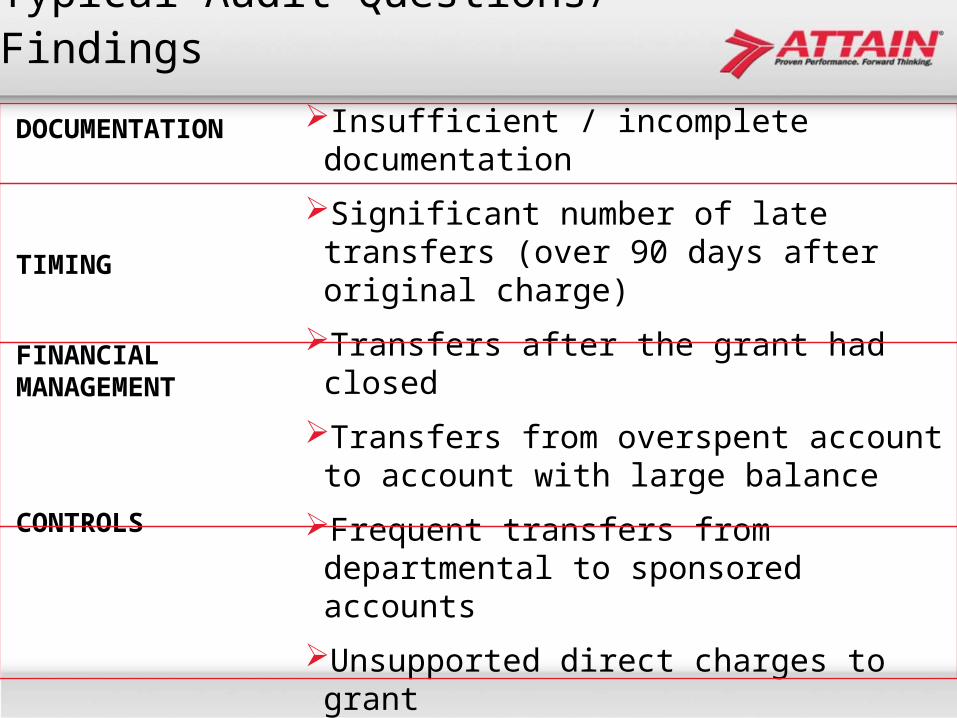

DOCUMENTATION

TIMING

FINANCIAL MANAGEMENT

CONTROLS

Insufficient / incomplete documentation

Significant number of late transfers (over 90 days after original charge)

Transfers after the grant had closed

Transfers from overspent account to account with large balance

Frequent transfers from departmental to sponsored accounts

Unsupported direct charges to grant

Accounting system unable to monitor and manage charges on grants

What Federal Regulations Require

NIH Grants Policy Statement:

Cost Transfers, Overruns, and Accelerated/ Delayed Expenditures:

“An explanation merely stating that the transfer was made "to correct error" or "to transfer to correct project" is not sufficient

Cost transfers should be accomplished “within 90 days”

What Federal Regulations Require

NIH Grants Policy Statement:

Cost Transfers, Overruns, and Accelerated/ Delayed Expenditures:

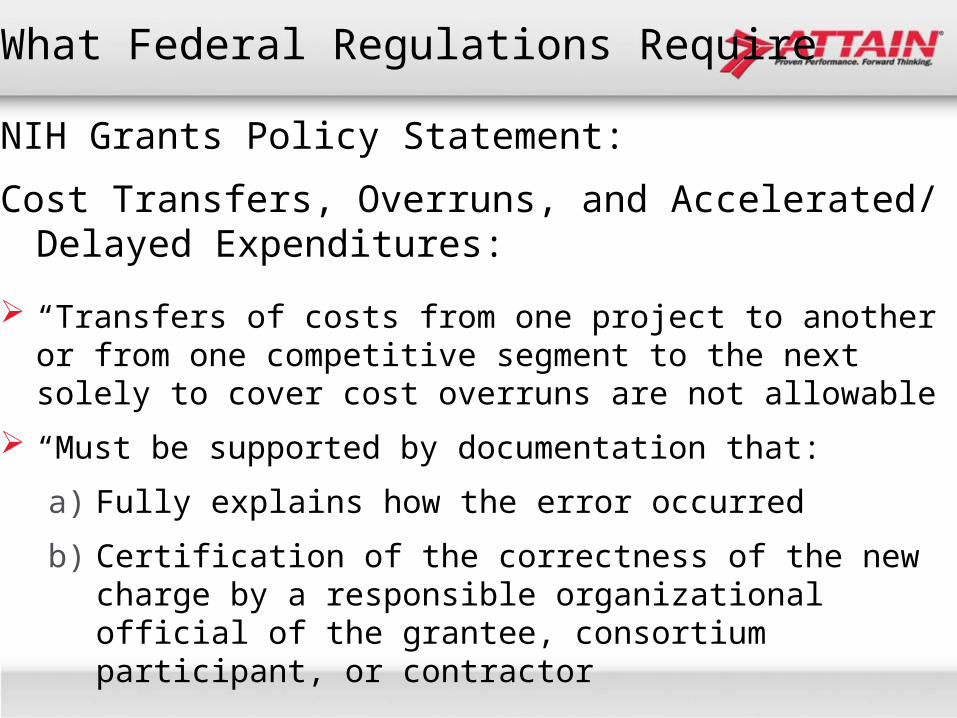

“Transfers of costs from one project to another or from one competitive segment to the next solely to cover cost overruns are not allowable”

“Must be supported by documentation that:

a) Fully explains how the error occurred

b) Certification of the correctness of the new charge by a responsible organizational official of the grantee, consortium participant, or contractor

What Federal Regulations Require

NIH Grants Policy Statement:

Cost Transfers, Overruns, and Accelerated / Delayed Expenditures:

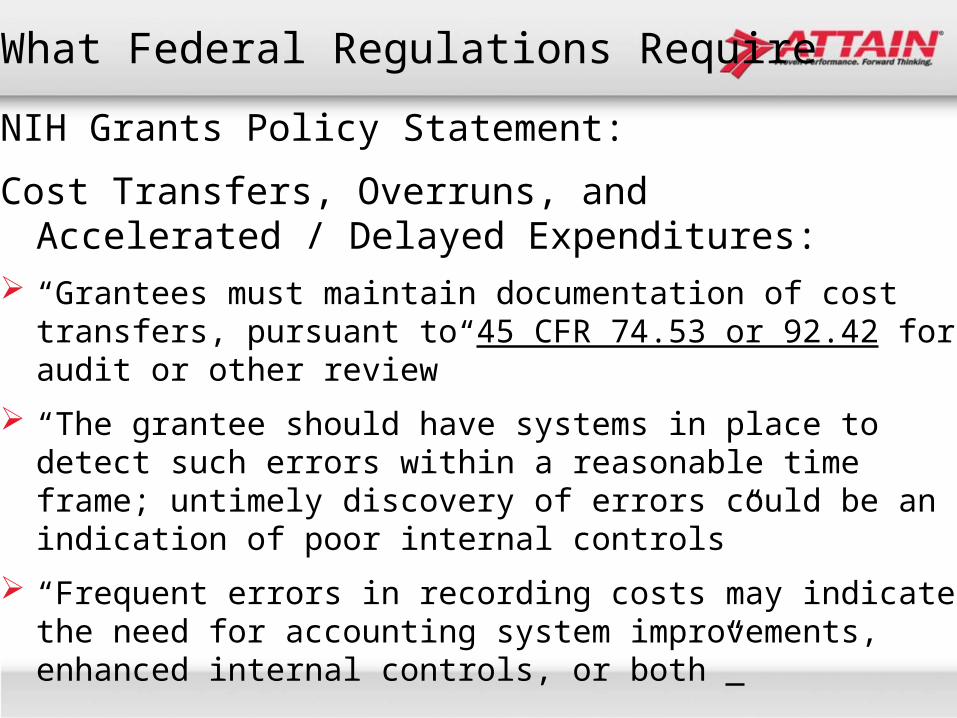

“Grantees must maintain documentation of cost transfers, pursuant to 45 CFR 74.53 or 92.42 for audit or other review”

“The grantee should have systems in place to detect such errors within a reasonable time frame; untimely discovery of errors could be an indication of poor internal controls”

“Frequent errors in recording costs may indicate the need for accounting system improvements, enhanced internal controls, or both”

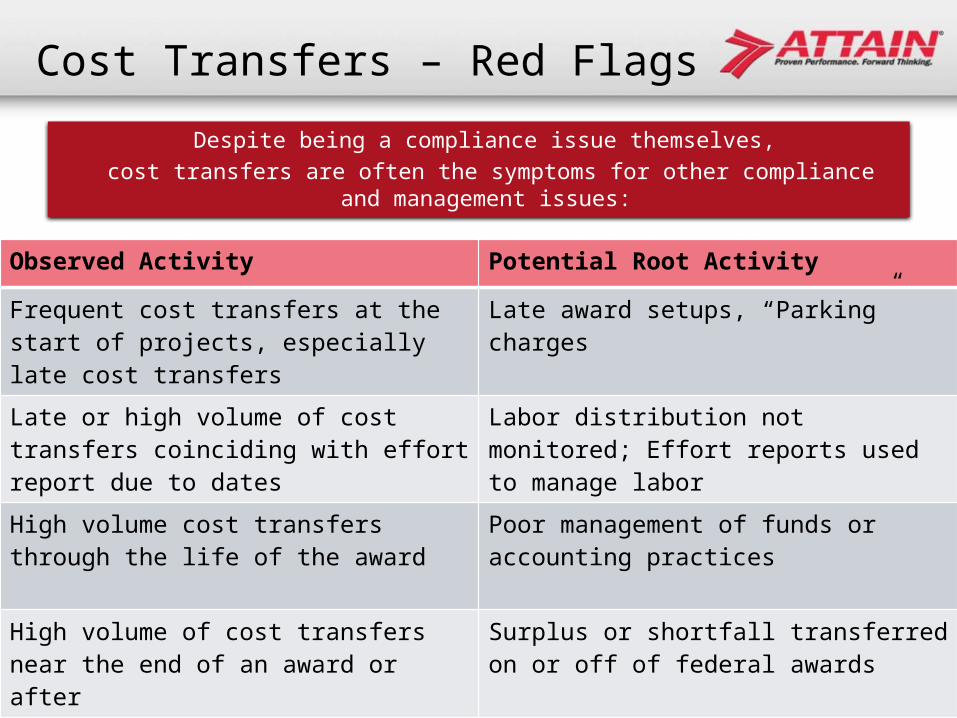

Cost Transfers – Red Flags

Observed Activity Potential Root Activity

Frequent cost transfers at the start of projects, especially late cost transfers

Late award setups, “Parking” charges

Late or high volume of cost transfers coinciding with effort report due to dates

Labor distribution not monitored; Effort reports used to manage labor

High volume cost transfers through the life of the award

Poor management of funds or accounting practices

High volume of cost transfers near the end of an award or after

Surplus or shortfall transferred on or off of federal awards

Despite being a compliance issue themselves, cost transfers are often the symptoms for other compliance

and management issues:

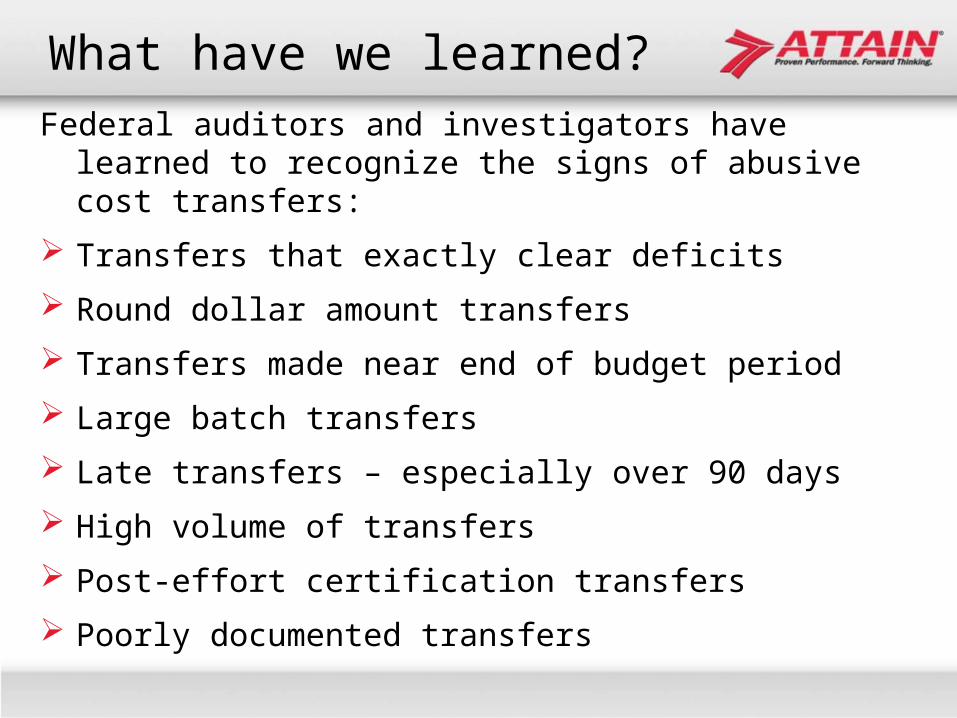

What have we learned?Federal auditors and investigators have learned to

recognize the signs of abusive cost transfers:

Transfers that exactly clear deficits

Round dollar amount transfers

Transfers made near end of budget period

Large batch transfers

Late transfers – especially over 90 days

High volume of transfers

Post-effort certification transfers

Poorly documented transfers

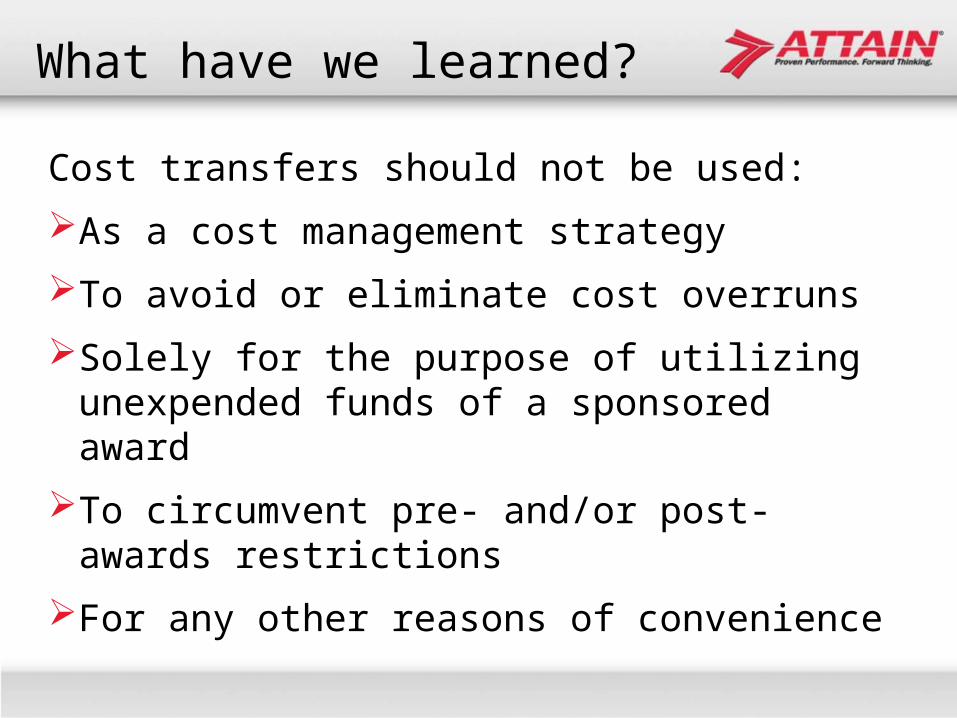

What have we learned?

Cost transfers should not be used:

As a cost management strategy

To avoid or eliminate cost overruns

Solely for the purpose of utilizing unexpended funds of a sponsored award

To circumvent pre- and/or post-awards restrictions

For any other reasons of convenience

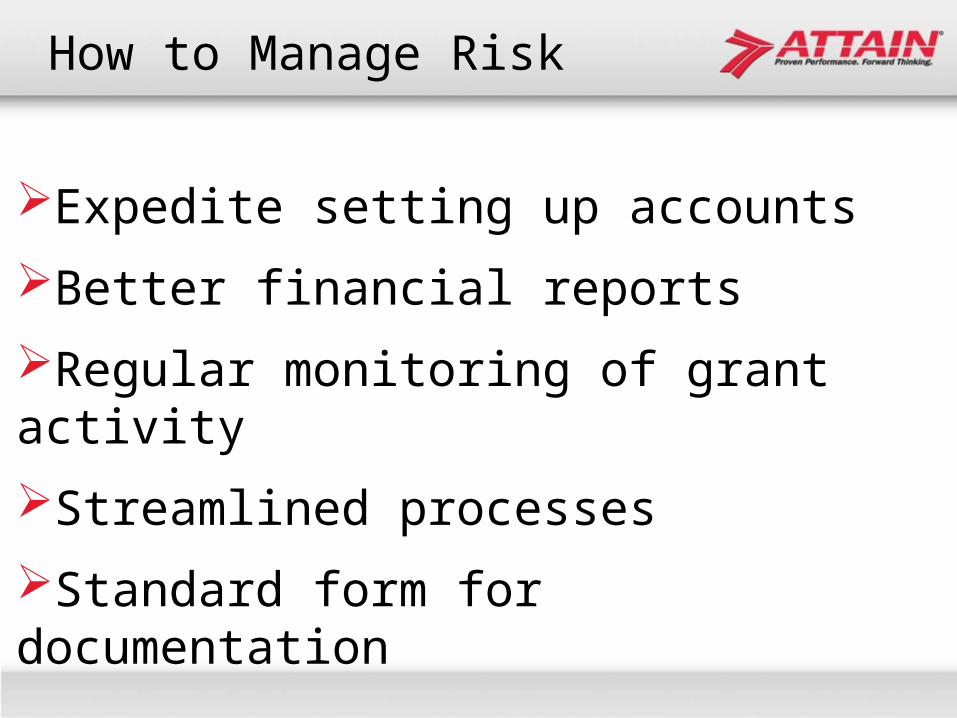

How to Manage Risk

PeopleReview Skills, Knowledge, SupportConduct TrainingReview Organizational Skills

ProcessClear policies and procedures Document requirements

TechnologyConfiguration/Control SettingsSystems IntegrationEvaluate Technology Alternatives

How to Manage Risk

Expedite setting up accounts

Better financial reports

Regular monitoring of grant activity

Streamlined processes

Standard form for documentation

How to Manage Risk

Plan expenditures to avoid cost transfers.

Charge costs to the correct award initially.

When costs are shared by more than one award, allocate appropriately.

Set up non-sponsored program accounts to hold costs to be allocated.

Set up advance accounts for costs incurred prior to receipt of notice of grant award.

How to Manage Risk Update funding sources for items such as

salaries and open purchase orders in a timely manner when award numbers change.

If a transfer corrects effort, recertify that month’s effort and attach documentation.

Obtain “no cost” extensions prior to the end date of the original project in order to complete work after the original award ends.

Plan and monitor costs monthly.

Process cost transfers in a timely manner.

How to Manage Risk

Document, document, document! Provide documentation to support the transfer and make the situation clear to an outside person, including:

A description of the error and how it occurred

A description of how the cost benefits the project it is being moved to

Certification of the transfer by a responsible organizational official

Use clear and concise language explaining the transfer.

Review documentation for late cost transfers justifying the request.

How to Manage RiskTop 10 List:

1. Do it right the first time—“fixing” it after-the-fact creates more work.

2. Talk with the people initiating the transactions—and by “talk” we don’t mean “email”.

3. Keep good supporting documentation—if you can’t prove it, it never happened.

4. Develop a routine—meet periodically rather than once or twice and letting things slip.

5. Be concise—the shorter the better.

How to Manage RiskTop 10 List:

6. Identify bottlenecks to offer solutions—not just to complain… anyone can do that.

7. Don’t wait for direction to come from the top—implement change at your level.

8. Suggest solutions—outline the issue, the obstacle, intended improvement, and explain how they can help.

9. Do things first that don’t cost money, show progress, then ask for more resources.

10. Be positive—no one responds to negativity.

Timing: Case Studies

Scenario: The grant administrator requests salary transfers for multiple individuals to/from sponsored projects, some dating back over 6 months.

Justification: “The main reason for this is that two of our accounts are out of money and the salaries need to be moved to avoid a cost over run”.

Would you approve? Why or why not?

Timing: Case Studies

Scenario: The grant administrator requests a salary transfer for John Smith for July from Grant 12345 to Grant 12346. The transfer request is submitted in August.

Justification: “The budget period for Grant 12345 ended on 6/30/11 and the next year of the fund, Grant 12346, had not been set up. In the future, we will request an advance account in a more timely fashion.”

Would you approve? Why or why not?

Wording: Case Studies

Scenario: The grant administrator requests that a cost of $1,000 be moved from Grant 12345 to Grant 12354. The expense occurred in May and the transfer is requested in June.

Justification: “ I incorrectly charged Grant 12345 instead of Grant 12354. This was a data-keying error that was discovered when reconciling our monthly financial reports.”

Would you approve? Why or why not?

Wording : Case Studies

Scenario: The grant administrator requests in July that expenses incurred during the period of January – June be moved to another sponsored project.

Justification: “Please process this cost transfer. Other priorities prevented me from reconciling my monthly financial reports and I am just noticing the error now.”

Would you approve? Why or why not?

Allocations : Case StudiesScenario: A freezer was purchased on Grant

12345. At the time of the purchase Grant 67891 was not set up and therefore not included on the original PO#. The grant administrator is requesting to move 50% of the freezer cost from Grant 12345 to Grant 67891.

Justification: “This freezer is used by two PI’s for sample storage. Each PI estimates 50% usage of this freezer. PI Davis stores blood samples for Grant 12345, PI Abrams stores cell tissue for Grant 67891.”

Would you approve this? Why or why not?

Other: Case Studies

Scenario: Lab supplies were charged to a private award and the grant administrator is now requesting to move to an NIH federal award.

Justification: “We’re requesting the P-card charges be move to Dr. Spock’s federal award because the items were in the approved budget (attached). The error was made because the P-card default had been setup on another PI’s private grant. We’ve updated our P-card default to a University account number.”

Would you approve this? Why or why not?

Other: Case Studies

Scenario: Travel expenses were charged to a department account and the grant administrator is now requesting to move to a private award. The individual for whom the travel was for had no effort on the grant.

Justification: “The travel expenses were charged to the department account in error. Please move these expenses to the private award because this is where they belong.”

Would you approve this? Why or why not?

Discussion

For Questions, Contact:

Bob Cohen [email protected]

Denise Rouleau [email protected]

Joe O’Brien [email protected]

![Goal Intent Attain[1]](https://img.pdfslide.us/doc/110x75/577d35691a28ab3a6b90617a/goal-intent-attain1.jpg)