Embed Size (px)

Citation preview

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

1

KEY HIGHLIGHTS

1. Real Money Gaming 2. Average revenue per paying user

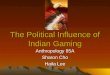

Mobile gaming expected to triple to a $5Bn+ market opportunity by 2025300Mn+ user base, growing with ease of access; spike in new adoption; leading companies actively shaping market

evolution with increased marketing spends

Unprecedented level of investor interest indicative of high expected growth in the industry

33% of all funding for gaming in India came in Q12021; gaming platforms winning at the back of variety in proposition

Consumer research insights point to market evolutionSix gamer personas defined by context i.e. occasion, group composition; limited correlation to demographics; rise of

women gamers, gaming increasingly being viewed as "productive" and "social", competition induces more spend

Monetization in non-RMG nascent but trending positivelyLarge dependence on ad revenues today (~43% of non-RMG1 spend) with low paying base (7-8% for non-RMG1); higher

ARPPU's2 expected to provide fillip to industry revenues

Familiarity in content, user generated content (e.g., esports), influencers serve as effective hooks to onboard new gamers, ease adoption and drive more engagement overall

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

2

Who plays where, key

trends shaping the

ecosystem

Insights from consumer

research

Action agenda for

companies

$5B+ market

opportunity at the back

of exponential growth

EVOLUTION OF

THE INDIAN

GAMING

ECOSYSTEM

DECODING THE

INDIAN GAMER

REALIZING THE

OPPORTUNITY

MARKET

OVERVIEW

INSPIRATIONS:

WHAT IT TAKES

TO WIN

Learnings from

exemplars

CO

NT

EN

TS

TA

BL

E o

f

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

3

CO

NT

EN

TS

TA

BL

E o

f

EVOLUTION OF

THE INDIAN

GAMING

ECOSYSTEM

DECODING THE

INDIAN GAMER

REALIZING THE

OPPORTUNITY

Who plays where, key

trends shaping the

ecosystem

Insights from consumer

research

Action agenda for

companies

INSPIRATIONS:

WHAT IT TAKES

TO WIN

Learnings from

exemplars

MARKET

OVERVIEW

$5B+ market

opportunity at the back

of exponential growth

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

4

KEY HIGHLIGHTS

Gaming a $1.8Bn sunrise sector in India: still relatively small (~1% of global) but growing very

fast (~38% CAGR)01

Market made up of a mix of genres: different evolution vs. markets like China wherein action and

adventure formats steeping in local connotations reign supreme05

Multiplayer games are seeing increased time spent and monetization because consumers like to

compete and spend time socially with their friends04

Monetization still nascent: paying base still low (7-8% for non-RMG1, 15-20% for RMG) but

trending positively and alongside higher ARPPU's2 expected to provide momentum to industry

revenues 03

Mobile-first trend within gaming continues strong: sizeable user base (300Mn+) with ~$1.5Bn

revenues and expected to reach $5Bn+ by 2025 - increased availability and adoption

turbocharging user base02

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

1. Real money gaming 2. Average revenue per paying user

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

5

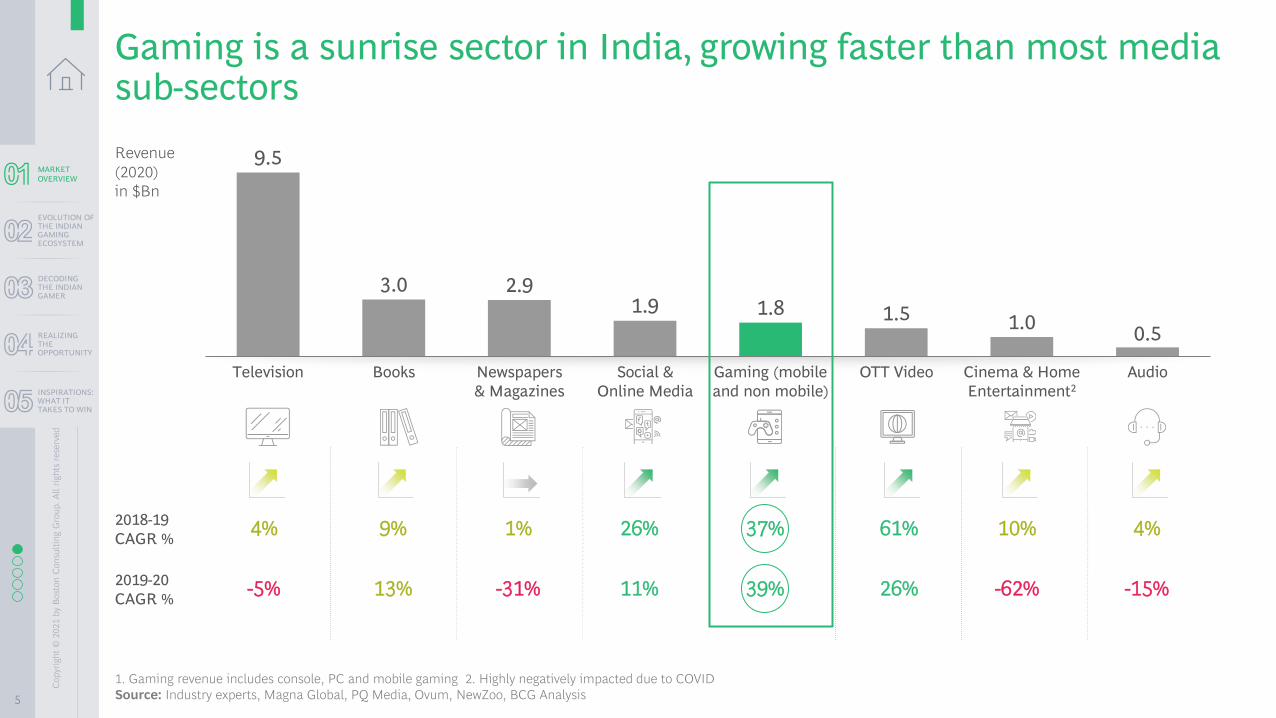

Gaming is a sunrise sector in India, growing faster than most media sub-sectors

1. Gaming revenue includes console, PC and mobile gaming 2. Highly negatively impacted due to COVID

Source: Industry experts, Magna Global, PQ Media, Ovum, NewZoo, BCG Analysis

9.5

3.0 2.91.9 1.8 1.5 1.0

0.5

AudioCinema & Home

Entertainment2

Television Books Newspapers

& Magazines

Social &

Online Media

Gaming (mobile

and non mobile)

OTT Video

2018-19

CAGR %4% 9% 1% 26% 61% 4%37% 10%

-5% 13% -31% 11% 26% -15%39% -62%2019-20

CAGR %

Revenue

(2020)

in $Bn

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

6

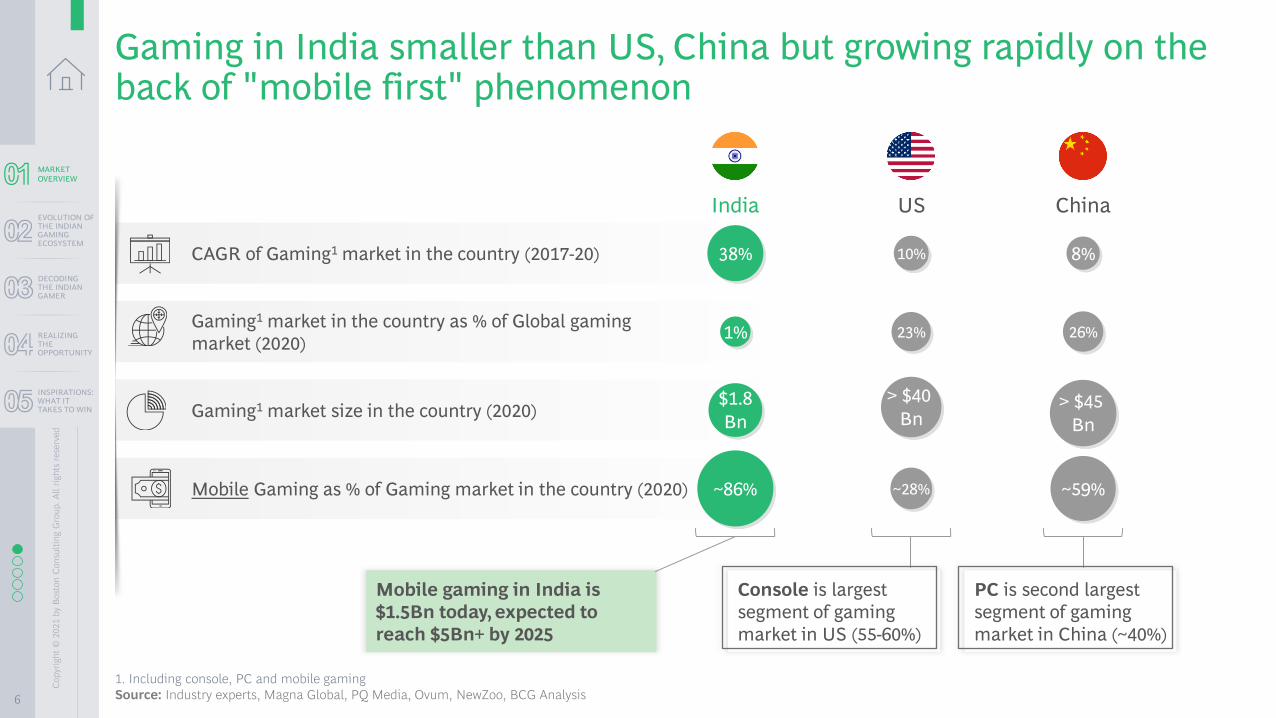

Mobile gaming in India is

$1.5Bn today, expected to

reach $5Bn+ by 2025

Gaming in India smaller than US, China but growing rapidly on the back of "mobile first" phenomenon

1. Including console, PC and mobile gaming

Source: Industry experts, Magna Global, PQ Media, Ovum, NewZoo, BCG Analysis

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Mobile Gaming as % of Gaming market in the country (2020)

CAGR of Gaming1 market in the country (2017-20)

Gaming1 market in the country as % of Global gaming

market (2020)

Gaming1 market size in the country (2020)

India

~86%

38%

1%

$1.8

Bn

US

~28%

10%

23%

> $40

Bn

China

~59%

8%

26%

> $45

Bn

Console is largest

segment of gaming

market in US (55-60%)

PC is second largest

segment of gaming

market in China (~40%)

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

7

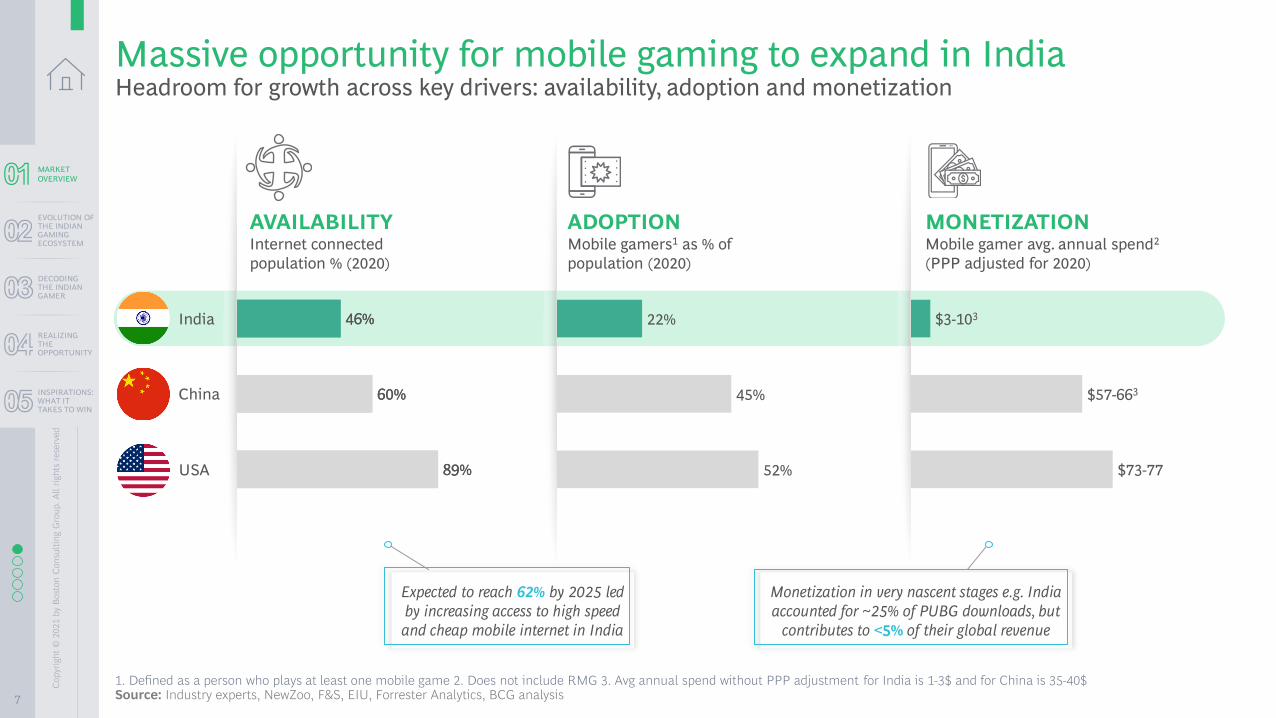

Massive opportunity for mobile gaming to expand in IndiaHeadroom for growth across key drivers: availability, adoption and monetization

1. Defined as a person who plays at least one mobile game 2. Does not include RMG 3. Avg annual spend without PPP adjustment for India is 1-3$ and for China is 35-40$Source: Industry experts, NewZoo, F&S, EIU, Forrester Analytics, BCG analysis

AVAILABILITYInternet connected

population % (2020)

ADOPTIONMobile gamers1 as % of

population (2020)

MONETIZATIONMobile gamer avg. annual spend2

(PPP adjusted for 2020)

46%

60%

89%

46%

60%

89% $73-77

$3-103

$57-663

22%

45%

52%

Expected to reach 62% by 2025 led

by increasing access to high speed

and cheap mobile internet in India

Monetization in very nascent stages e.g. India

accounted for ~25% of PUBG downloads, but

contributes to <5% of their global revenue

India

China

USA

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

8

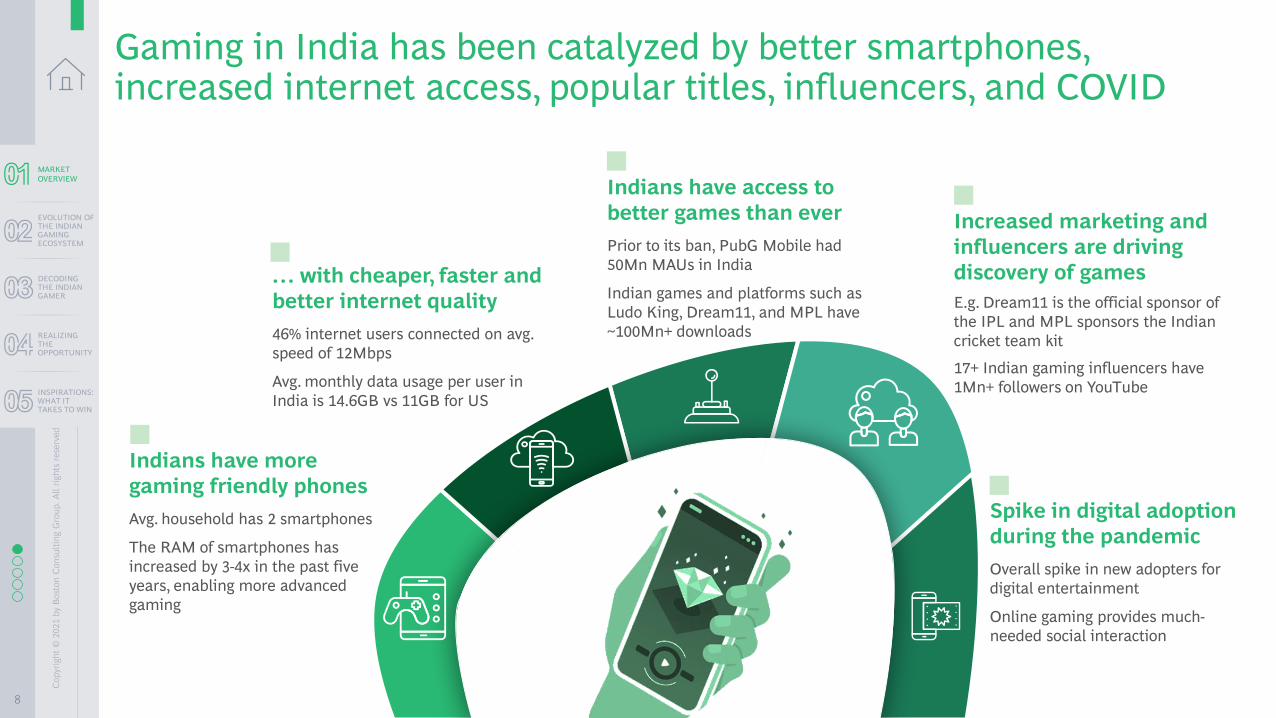

Gaming in India has been catalyzed by better smartphones, increased internet access, popular titles, influencers, and COVID

Indians have access to

better games than ever

Prior to its ban, PubG Mobile had

50Mn MAUs in India

Indian games and platforms such as

Ludo King, Dream11, and MPL have

~100Mn+ downloads

Indians have more

gaming friendly phones

Avg. household has 2 smartphones

The RAM of smartphones has

increased by 3-4x in the past five

years, enabling more advanced

gaming

… with cheaper, faster and

better internet quality

46% internet users connected on avg.

speed of 12Mbps

Avg. monthly data usage per user in

India is 14.6GB vs 11GB for US

Increased marketing and

influencers are driving

discovery of games

E.g. Dream11 is the official sponsor of

the IPL and MPL sponsors the Indian

cricket team kit

17+ Indian gaming influencers have

1Mn+ followers on YouTube

Spike in digital adoption

during the pandemic

Overall spike in new adopters for

digital entertainment

Online gaming provides much-

needed social interaction

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

9

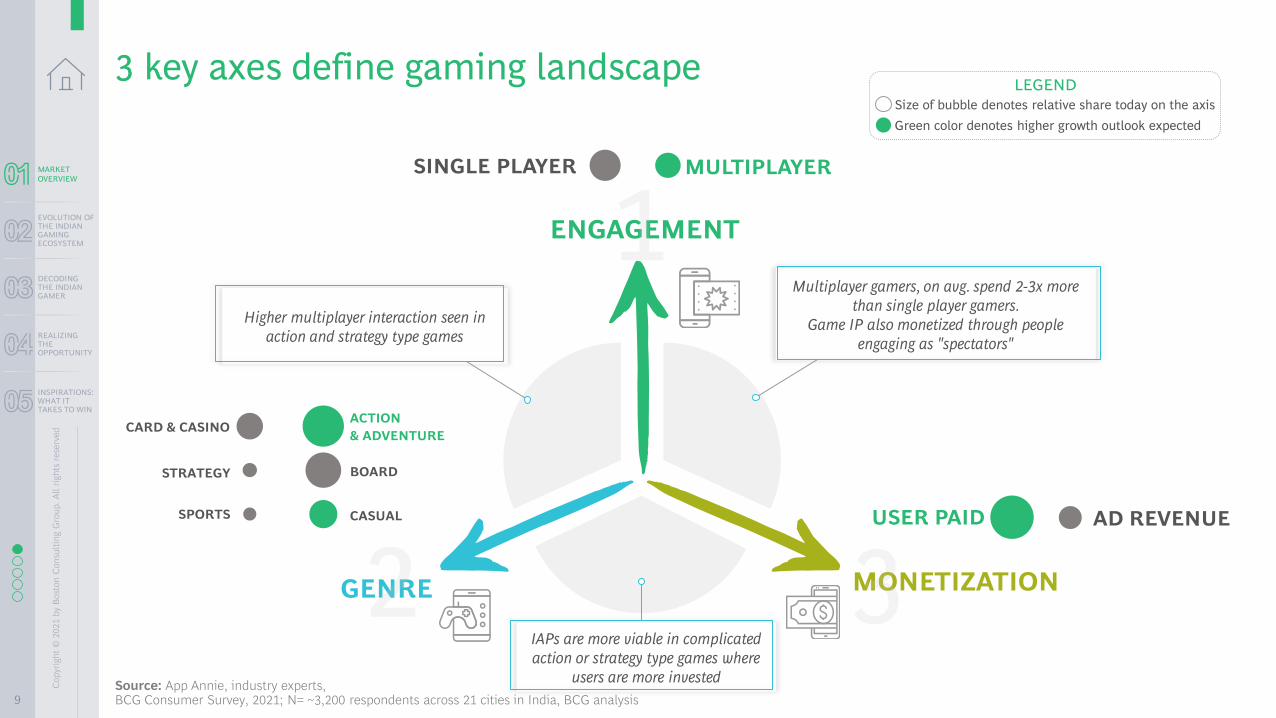

3 key axes define gaming landscapeLEGEND

Size of bubble denotes relative share today on the axis

Green color denotes higher growth outlook expected

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

GENRE

ENGAGEMENT

MONETIZATION

USER PAID AD REVENUE

MULTIPLAYERSINGLE PLAYER

ACTION

& ADVENTURE

SPORTS

BOARD

CASUAL

CARD & CASINO

STRATEGY

Higher multiplayer interaction seen in

action and strategy type games

Multiplayer gamers, on avg. spend 2-3x more

than single player gamers.

Game IP also monetized through people

engaging as "spectators"

IAPs are more viable in complicated

action or strategy type games where

users are more investedSource: App Annie, industry experts, BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India, BCG analysis

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

10

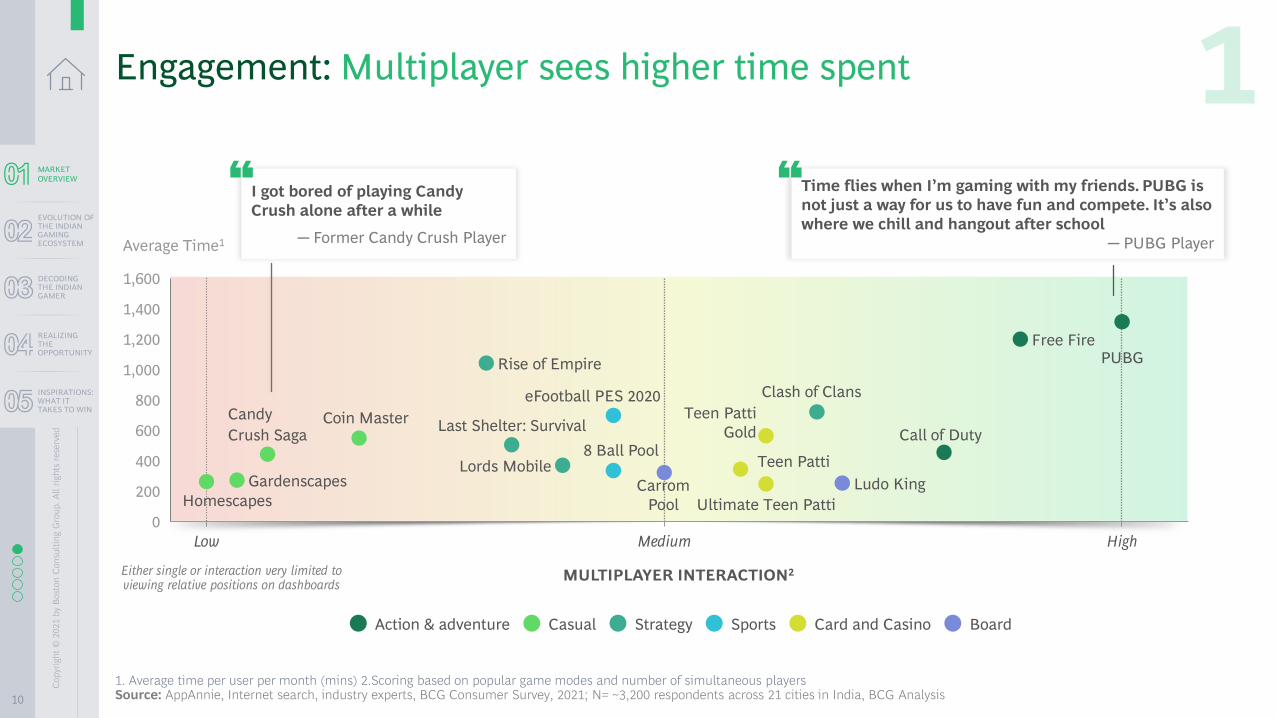

Engagement: Multiplayer sees higher time spent

1. Average time per user per month (mins) 2.Scoring based on popular game modes and number of simultaneous playersSource: AppAnnie, Internet search, industry experts, BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India, BCG Analysis

Low

0

Medium High

200

400

600

800

1,000

1,200

1,400

1,600

Clash of Clans

MULTIPLAYER INTERACTION2

Last Shelter: SurvivalCoin Master

Lords Mobile

Average Time1

Free Fire

Gardenscapes

Call of Duty

Candy

Crush Saga

Rise of Empire

Ultimate Teen Patti

Ludo King

Action & adventure Casual SportsStrategy BoardCard and Casino

Either single or interaction very limited to viewing relative positions on dashboards

Homescapes

8 Ball PoolTeen Patti

Teen Patti

Gold

PUBG

Carrom

Pool

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

I got bored of playing Candy

Crush alone after a while

─ Former Candy Crush Player

Time flies when I’m gaming with my friends. PUBG is

not just a way for us to have fun and compete. It’s also

where we chill and hangout after school

─ PUBG Player

eFootball PES 2020

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

11

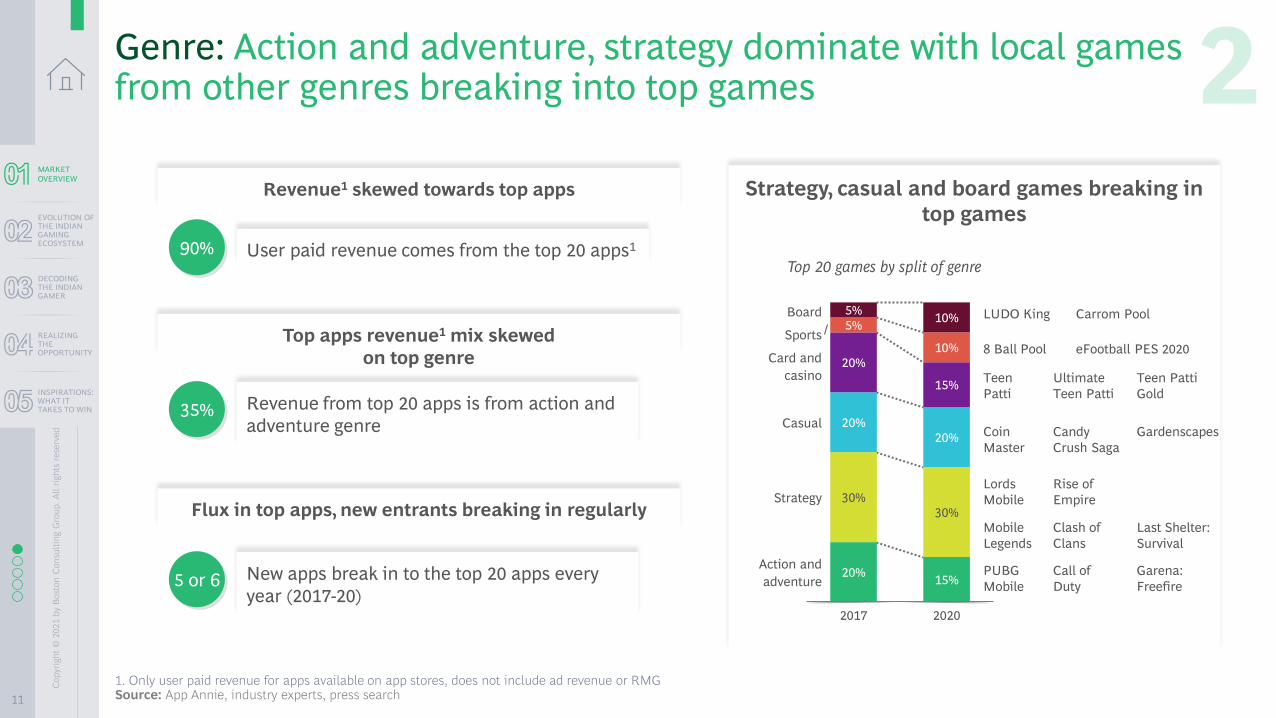

Strategy, casual and board games breaking in

top games

Revenue1 skewed towards top apps

Genre: Action and adventure, strategy dominate with local games from other genres breaking into top games

1. Only user paid revenue for apps available on app stores, does not include ad revenue or RMGSource: App Annie, industry experts, press search

KEY

INSIGHTS

20%15%

30%30%

20%20%

20%

15%

5%

10%

5%10%

Sports

20202017

Casual

Board

Card and

casino

Strategy

Action and

adventure

Top 20 games by split of genre

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM 90% User paid revenue comes from the top 20 apps1

Revenue from top 20 apps is from action and

adventure genre35%

New apps break in to the top 20 apps every

year (2017-20)5 or 6

Top apps revenue1 mix skewed

on top genre

Flux in top apps, new entrants breaking in regularly

Candy

Crush Saga

GardenscapesCoin

Master

Ultimate

Teen Patti

Teen

Patti

Teen Patti

Gold

8 Ball Pool eFootball PES 2020

LUDO King Carrom Pool

Lords

Mobile

Last Shelter:

Survival

Rise of

Empire

Mobile

Legends

Clash of

Clans

Garena:

Freefire

PUBG

Mobile

Call of

Duty

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

12

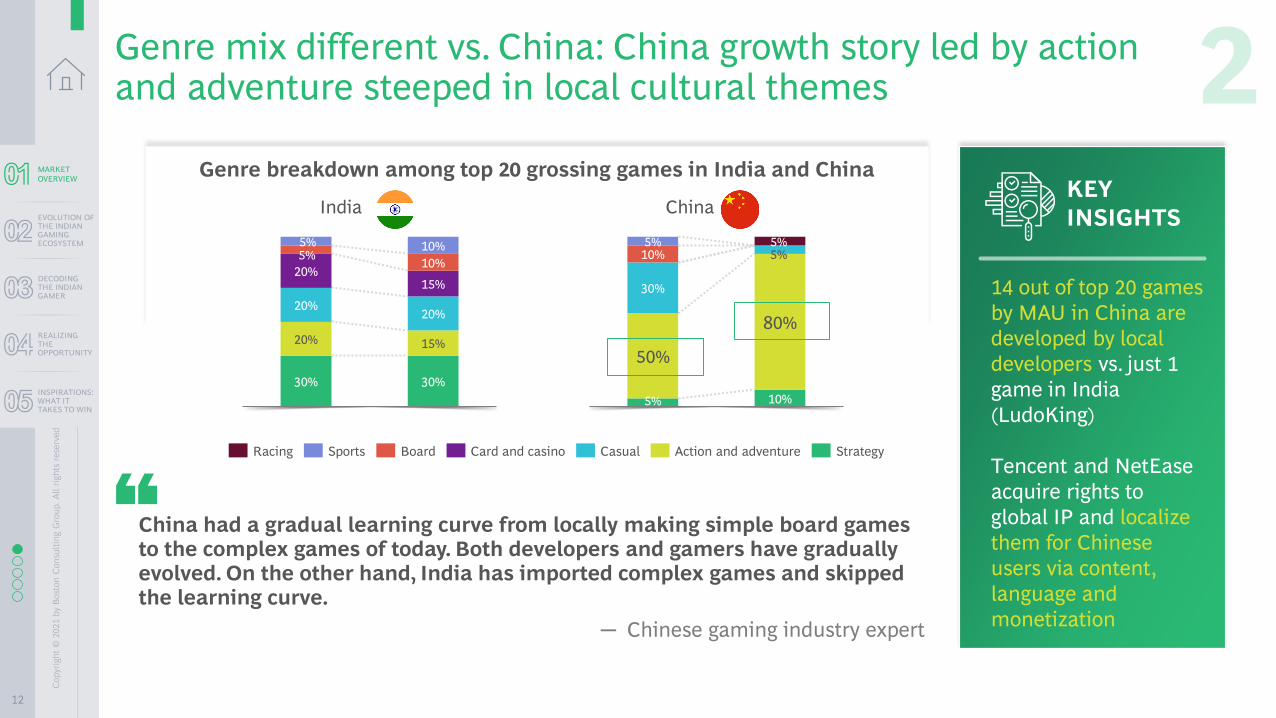

Genre breakdown among top 20 grossing games in India and China

Genre mix different vs. China: China growth story led by action and adventure steeped in local cultural themes

14 out of top 20 games

by MAU in China are

developed by local

developers vs. just 1

game in India

(LudoKing)

Tencent and NetEase

acquire rights to

global IP and localize

them for Chinese

users via content,

language and

monetization

KEY

INSIGHTS

10%

50%

80%

30%

10%

30% 30%

20% 15%

20%20%

20%15%

10%

10%

CasualRacing Card and casinoSports Board Action and adventure Strategy

5%5%

India China

China had a gradual learning curve from locally making simple board games to the complex games of today. Both developers and gamers have gradually evolved. On the other hand, India has imported complex games and skipped the learning curve.

─ Chinese gaming industry expert

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

5%

5% 5%5%

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

13

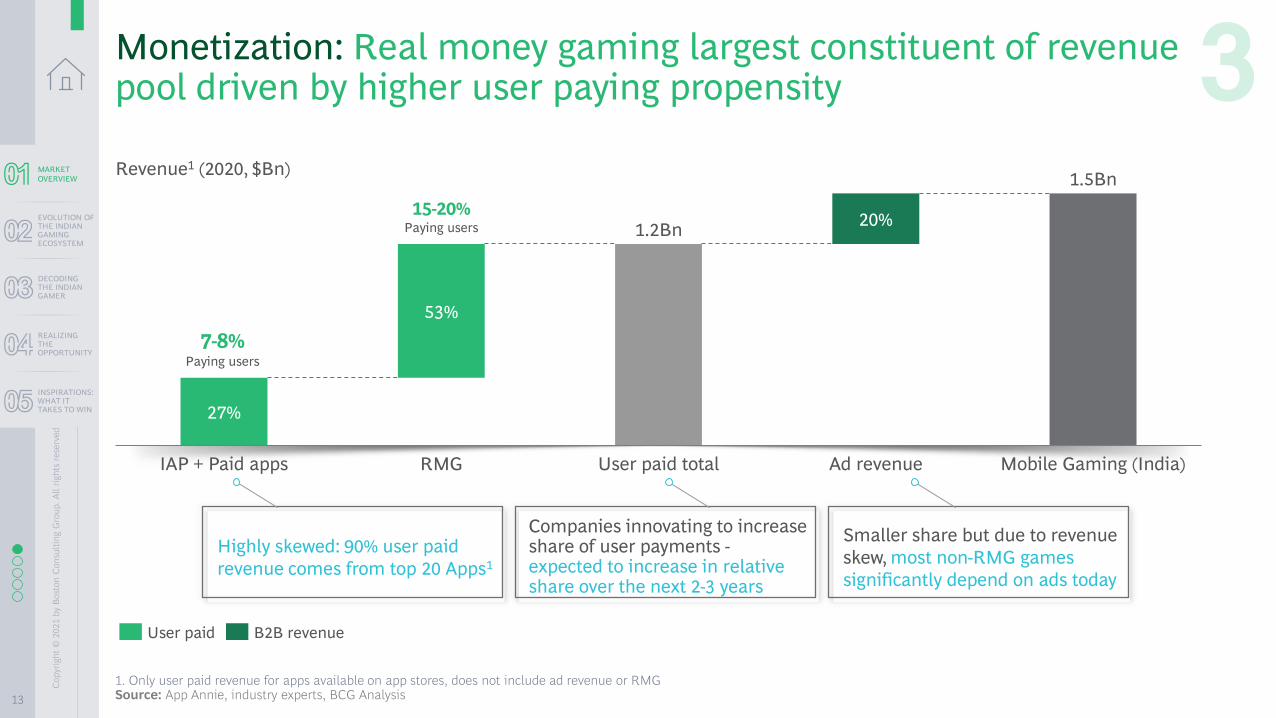

Monetization: Real money gaming largest constituent of revenue pool driven by higher user paying propensity

1.2Bn

1.5Bn

Ad revenue

20%

27%

IAP + Paid apps

53%

Mobile Gaming (India)User paid totalRMG

User paid B2B revenue

7-8%Paying users

15-20%Paying users

Highly skewed: 90% user paid

revenue comes from top 20 Apps1

Companies innovating to increase share of user payments -expected to increase in relative share over the next 2-3 years

Revenue1 (2020, $Bn)MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

1. Only user paid revenue for apps available on app stores, does not include ad revenue or RMGSource: App Annie, industry experts, BCG Analysis

Smaller share but due to revenue

skew, most non-RMG games

significantly depend on ads today

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

14

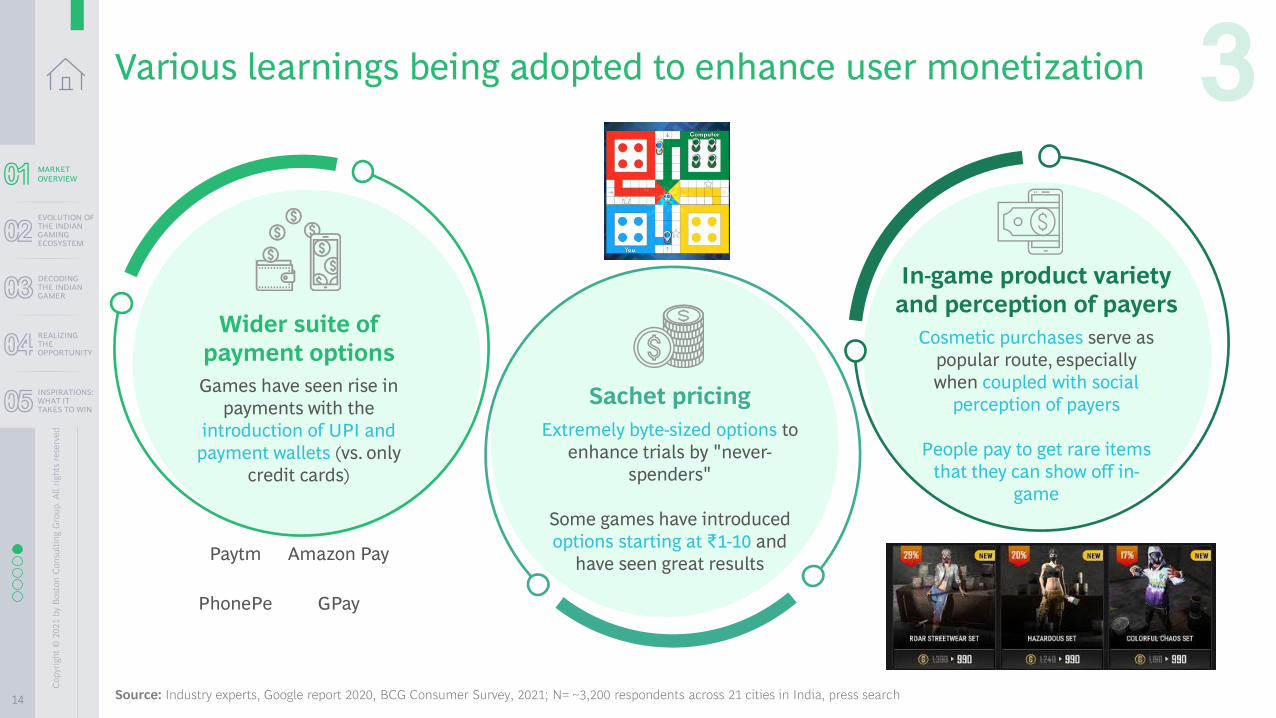

Various learnings being adopted to enhance user monetization

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Source: Industry experts, Google report 2020, BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India, press search

Games have seen rise in

payments with the

introduction of UPI and

payment wallets (vs. only

credit cards)

Wider suite of

payment options

Extremely byte-sized options to

enhance trials by "never-

spenders"

Some games have introduced

options starting at ₹1-10 and

have seen great results

Cosmetic purchases serve as

popular route, especially

when coupled with social

perception of payers

People pay to get rare items

that they can show off in-

game

In-game product variety

and perception of payers

Sachet pricing

Paytm Amazon Pay

PhonePe GPay

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

15

EVOLUTION OF

THE INDIAN

GAMING

ECOSYSTEM

DECODING THE

INDIAN GAMER

REALIZING THE

OPPORTUNITY

Who plays where, key

trends shaping the

ecosystem

Insights from consumer

research

Action agenda for

companies

MARKET

OVERVIEW

$5B+ market

opportunity at the back

of exponential growth

INSPIRATIONS:

WHAT IT TAKES

TO WIN

Learnings from

exemplars

CO

NT

EN

TS

TA

BL

E o

f

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

16

LEGEND: ARCHETYPES OF COMPANIES IN THE GAMING ECOSYSTEM

Mix of homegrown and global players competing in different plays across the value chain

AD NETWORKS

GAME TECH GAMING PLATFORMS

APP STORES

INDEPENDENT DEVELOPERS

STUDIOS AND PUBLISHERS DEVICES

PAYMENT

SOCIAL

OTHER IP OWNERS

Marketing Distribution Consumption

Source: Industry experts, press search

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM Enablers Content development Interfaces

GAMERS

ESPORTS TEAMS ESPORTS LEAGUES

1

2

3

4

5

6

7

8

9

10

11

12

UnityUNREAL

Engine

Lucasfilm Ltd FIFA

Lucid Labs

Frostwood

Interactive

Underdogs

Studio LLP

Xigma Games MPL: Mobile

Premier LeagueWINZO

Paytm

First GamesROBLOX STADIA

Gametion

Games 24

Seven

Ctro

Tencent

Games

Dream11

King Ubisoft

GameskraftKrafton Game

Union

Moonfrog

EPIC

Games

Steam

Google Play

Store

IOS App

Store

App

Bazaar

NODWIN

GamingESL India

Audience

Network by

InmobiGoogle

AdMobTSM Team Team Finatic

GPay Paytm

Vivo Samsung

Backbone Mi

YouTube

Gaming

Gaming

Discord

NON EXHAUSTIVE

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

17

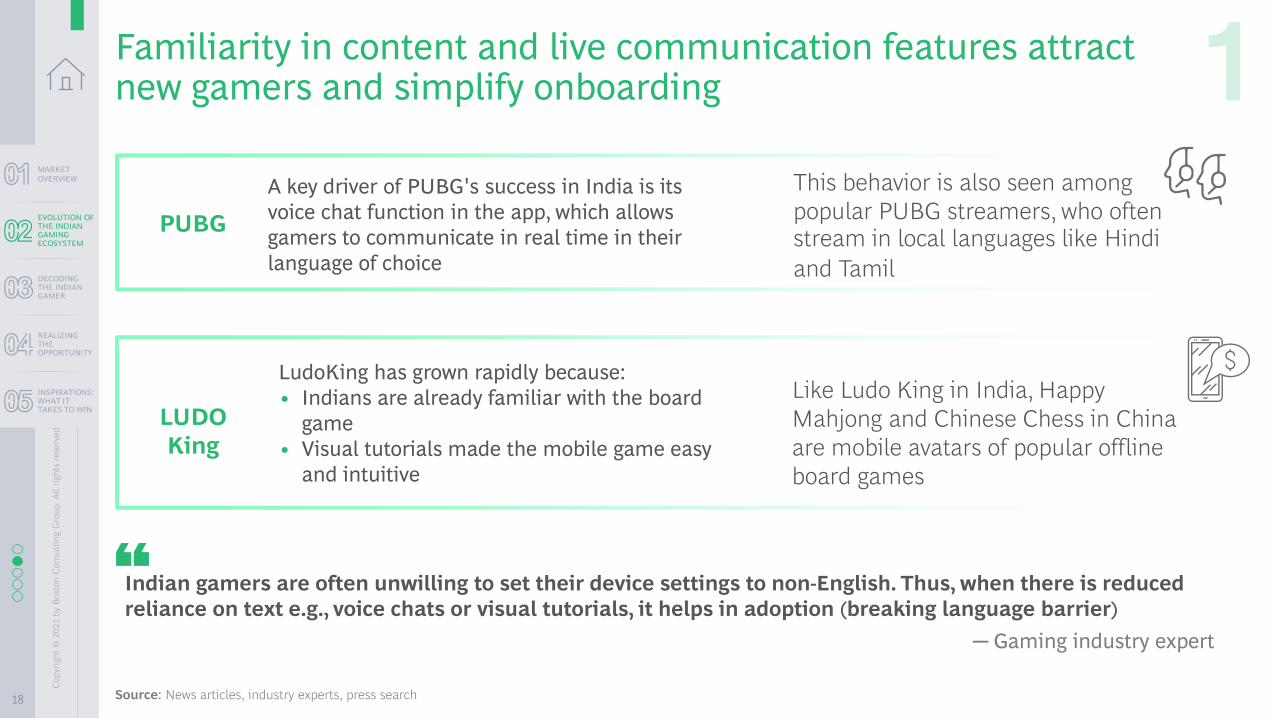

Increased focus on familiar content, along with visual and voice features are helping onboard

new gamers and driving higher engagement 01

Investors are actively scouting and shaping space: increased early-stage activity with new highs

in terms of $s invested (~33% of all gaming funding came in 2021Q1)05

Gaming platforms emerging - attracting user and investor attention: proposition of diverse

games as a one stop shop04

Influencer-driven user generated content, livestreaming and the nascent but growing ~$100Mn

esports industry are driving gaming adoption and higher engagement03

India emerging as talent hub - for India and for the world: larger talent pool with # gaming

companies having gone up >10x over last decade. Early investments by international studios

translating to talent proliferation now02

5 key trends in the Indian mobile gaming market

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

18

LudoKing has grown rapidly because:

• Indians are already familiar with the board

game

• Visual tutorials made the mobile game easy

and intuitive

Familiarity in content and live communication features attractnew gamers and simplify onboarding

Source: News articles, industry experts, press search

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

This behavior is also seen among

popular PUBG streamers, who often stream in local languages like Hindi

and Tamil

Indian gamers are often unwilling to set their device settings to non-English. Thus, when there is reduced

reliance on text e.g., voice chats or visual tutorials, it helps in adoption (breaking language barrier)

─ Gaming industry expert

Like Ludo King in India, Happy

Mahjong and Chinese Chess in China

are mobile avatars of popular offline

board games

A key driver of PUBG's success in India is its

voice chat function in the app, which allows

gamers to communicate in real time in their

language of choice

PUBG

LUDO

King

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

19

Talent begets talent: international studios have groomed Indian developers, who have in turn gone on to start their own companies

Source: App Annie, news articles, industry experts, press search

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

15,000+Game developers

in India

25

20202010

275+

+10x

Total number of gaming companies in India

International studios such as EA, Ubisoft and Zynga had set

up game development centers in India in the early 2010’s

Valued at $950Mn within 3 years of launch

Acquired for $360Mn by Swedish giant MTG

Acquired for $100Mn by Stillfront

Raised $2.5Mn from Lumikai, Leo Capital

Select examples of ex-Zynga founders

Raised $1Mn+ from Kae Capital, Graph Ventures

MPL

PLAYSIMPLE

Moonfrog

Bombay Play

Hypernova

Interactive

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

20

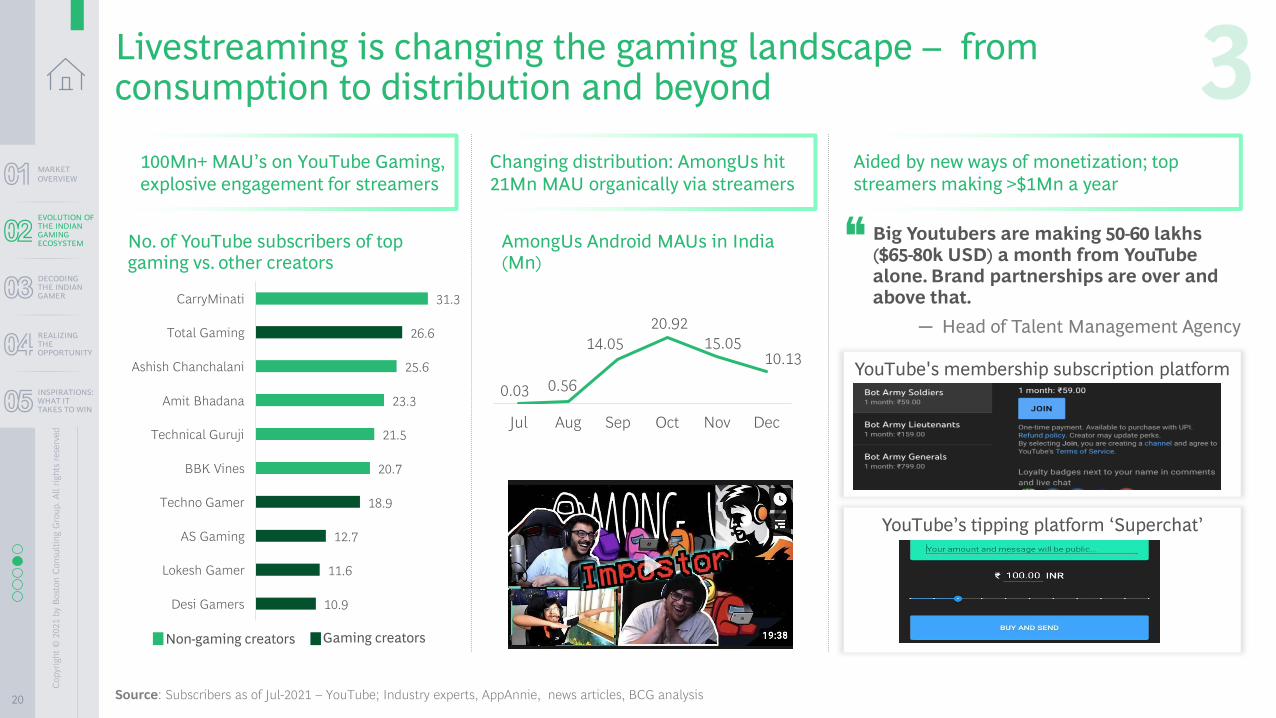

YouTube's membership subscription platform

Aided by new ways of monetization; top

streamers making >$1Mn a year

Livestreaming is changing the gaming landscape – from consumption to distribution and beyond

Source: Subscribers as of Jul-2021 – YouTube; Industry experts, AppAnnie, news articles, BCG analysis

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Big Youtubers are making 50-60 lakhs ($65-80k USD) a month from YouTube alone. Brand partnerships are over and above that.

─ Head of Talent Management Agency

YouTube’s tipping platform ‘Superchat’

100Mn+ MAU’s on YouTube Gaming,

explosive engagement for streamers

No. of YouTube subscribers of top gaming vs. other creators

0.03 0.56

14.05

20.92

15.0510.13

Jul Aug Sep Oct Nov Dec

AmongUs Android MAUs in India (Mn)

10.9

11.6

12.7

18.9

20.7

21.5

23.3

25.6

26.6

31.3

Desi Gamers

Lokesh Gamer

AS Gaming

Techno Gamer

BBK Vines

Technical Guruji

Amit Bhadana

Ashish Chanchalani

Total Gaming

CarryMinati

Non-gaming creators Gaming creators

Changing distribution: AmongUs hit

21Mn MAU organically via streamers

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

21

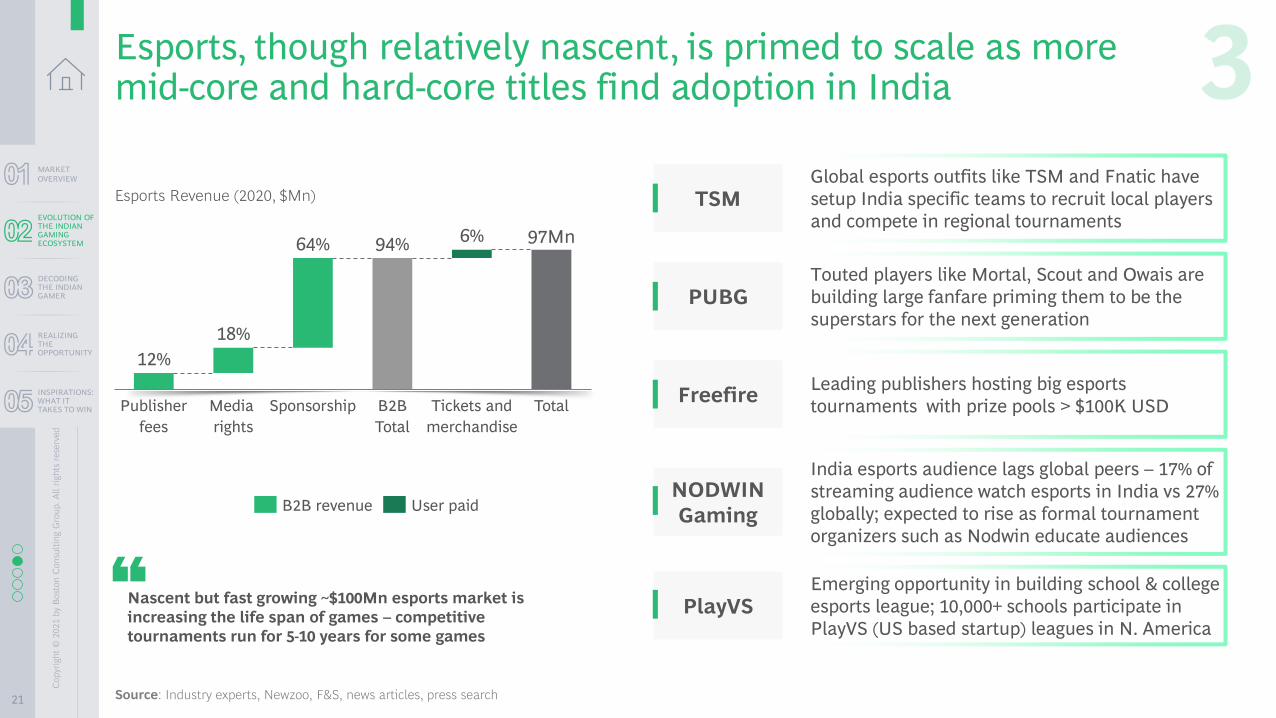

Esports, though relatively nascent, is primed to scale as moremid-core and hard-core titles find adoption in India

Source: Industry experts, Newzoo, F&S, news articles, press search

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

12%

94%

18%

64% 6%

Sponsorship B2B

Total

Publisher

fees

Tickets and

merchandise

Media

rights

Total

97Mn

User paidB2B revenue

Nascent but fast growing ~$100Mn esports market is

increasing the life span of games – competitive

tournaments run for 5-10 years for some games

Esports Revenue (2020, $Mn)Global esports outfits like TSM and Fnatic have

setup India specific teams to recruit local players

and compete in regional tournamentsTSM

Touted players like Mortal, Scout and Owais are

building large fanfare priming them to be the

superstars for the next generationPUBG

Leading publishers hosting big esports

tournaments with prize pools > $100K USDFreefire

India esports audience lags global peers – 17% of

streaming audience watch esports in India vs 27%

globally; expected to rise as formal tournament

organizers such as Nodwin educate audiences

NODWIN

Gaming

Emerging opportunity in building school & college

esports league; 10,000+ schools participate in

PlayVS (US based startup) leagues in N. AmericaPlayVS

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

22

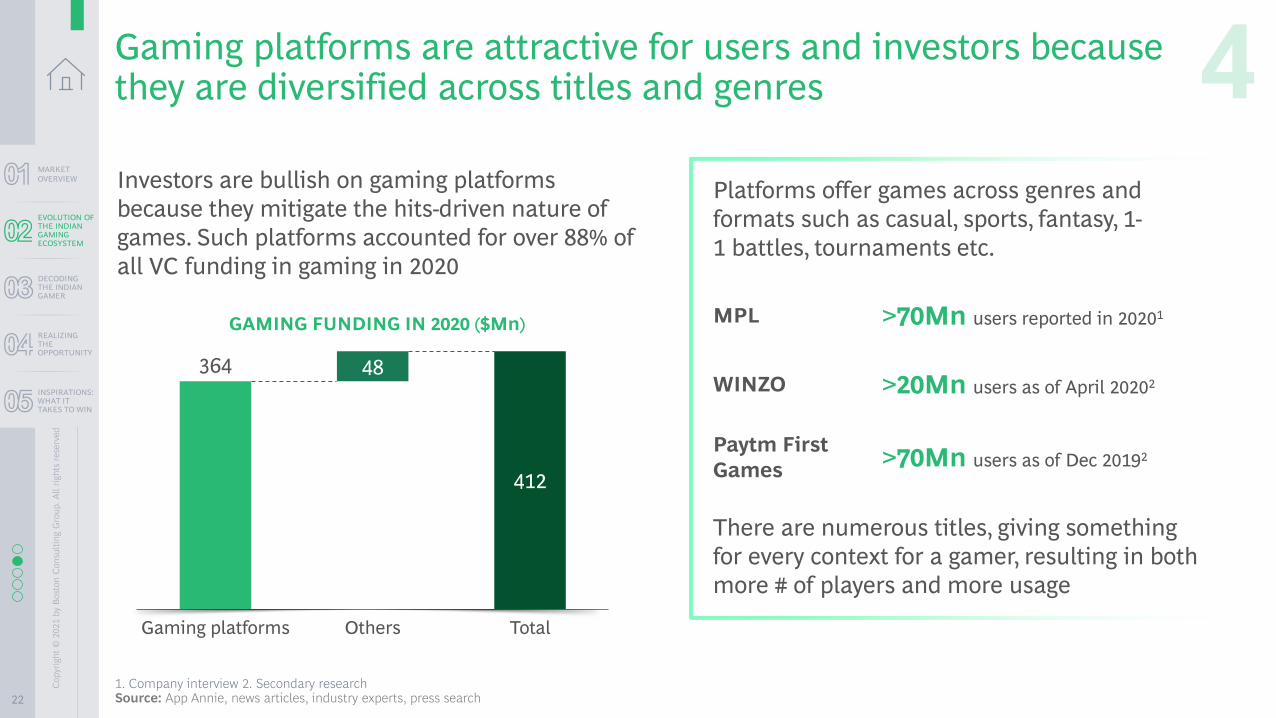

Gaming platforms are attractive for users and investors because they are diversified across titles and genres

1. Company interview 2. Secondary researchSource: App Annie, news articles, industry experts, press search

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

GAMING FUNDING IN 2020 ($Mn)

364

412

48

TotalGaming platforms Others

Investors are bullish on gaming platforms

because they mitigate the hits-driven nature of

games. Such platforms accounted for over 88% of

all VC funding in gaming in 2020

Platforms offer games across genres and

formats such as casual, sports, fantasy, 1-

1 battles, tournaments etc.

>70Mn users reported in 20201

>20Mn users as of April 20202

>70Mn users as of Dec 20192

There are numerous titles, giving something

for every context for a gamer, resulting in both

more # of players and more usage

MPL

WINZO

Paytm First

Games

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

23

Target Strategic Funding Amount Type of deal

Playsimple MTG $360Mn M&A

MoonfrogStillfront

Group$100Mn M&A

NODWIN Gaming Krafton $22.5Mn Strategic

LOCO Krafton $9Mn Strategic

Investor activity booming: gaming is the next big frontier in consumer

Source: Tracxn, Pitchbook, industry experts, press search

42 45 53 34

176 157 175

412

549

20172010-13 2014 2015 20192016 2018 2020 2021 Q1

+38%Total funding raised ($Mn)

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Active gaming investors and key investments Emerging strategic and M&A activity (2021)

*not exhaustive

MPL Moonfrog Rheo

Dream11 WINZO

LOCO Bombay Play eloelo

Get MEGA Mech Mocha

Playsimple Turnip

Sequoia

Capital India

Kalaari capital

Lumikai

Accel

Elevation

Octro

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

24

EVOLUTION OF

THE INDIAN

GAMING

ECOSYSTEM

REALIZING THE

OPPORTUNITY

Who plays where, key

trends shaping the

ecosystem

Action agenda for

companies

MARKET

OVERVIEW

$5B+ market

opportunity at the back

of exponential growth

INSPIRATIONS:

WHAT IT TAKES

TO WIN

Learnings from

exemplars

CO

NT

EN

TS

TA

BL

E o

f

Insights from consumer

research

DECODING THE

INDIAN GAMER

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

25

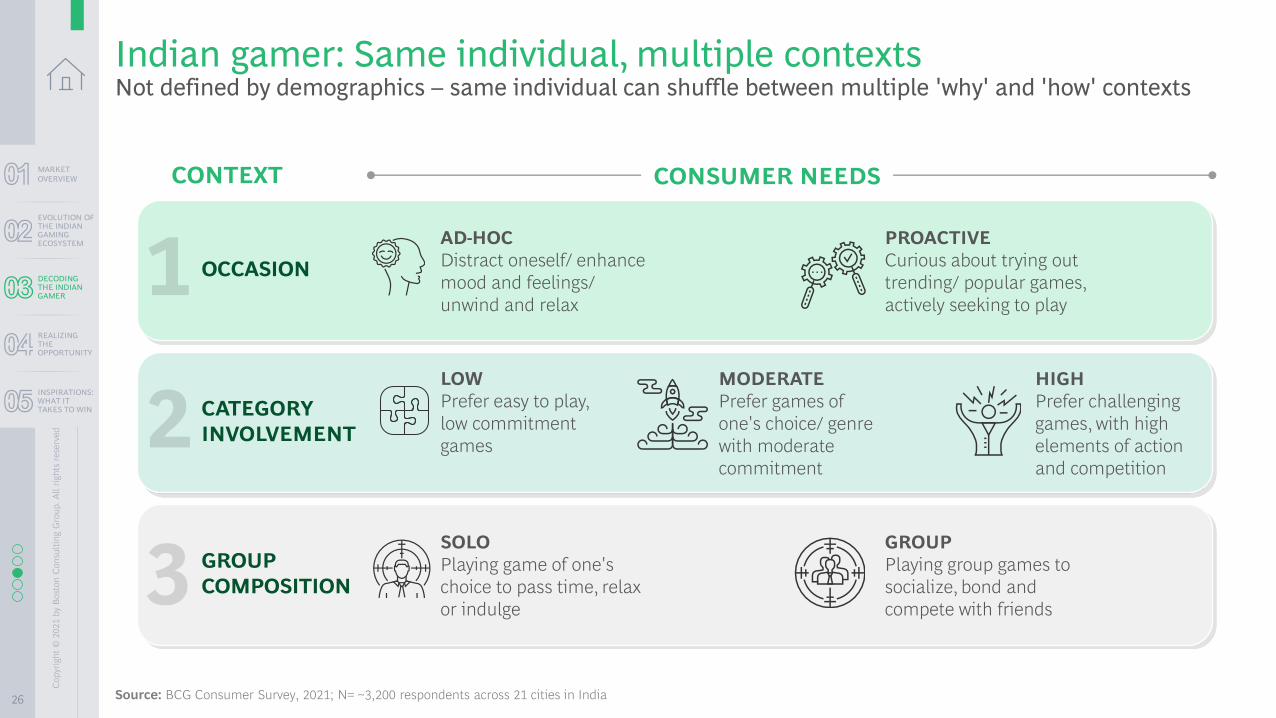

Many faces to one individualChoice of games context oriented with different drivers. Limited correlation of factors like

demographics to the gamer archetype01

Gaming is social; more players induces competition and loosened purse stringsClose to half the gamers prefer to play games with friends and family as a means of socializing; high

engagement gamer archetypes tend to spend more across monetization preferences04

Rise of women gamers Increasing adoption by women gamers albeit in low engagement archetypes (higher engagement

archetypes continue to be male dominated) – helps push overall maturity curve for gaming in India03

Game discovery continues to be an unmet need Discovery continues to be a pain point with gamers seeking more personalized game recommendations

(Gamers today discover games largely through word-of-mouth, app stores or social media)02

Gaming is no longer perceived as a 'waste of time'Gamers are seeing gaming in a positive light, and are likely to use gaming as a means of therapy as

well as for educational purposes 05

KEY CONSUMER INSIGHTS

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

26

GROUP

COMPOSITION

CATEGORY

INVOLVEMENT

OCCASION

CONTEXT

PROACTIVE

Curious about trying out

trending/ popular games,

actively seeking to play

AD-HOC

Distract oneself/ enhance

mood and feelings/

unwind and relax

LOW

Prefer easy to play,

low commitment

games

HIGH

Prefer challenging

games, with high

elements of action

and competition

MODERATE

Prefer games of

one's choice/ genre

with moderate

commitment

SOLO

Playing game of one's

choice to pass time, relax

or indulge

GROUP

Playing group games to

socialize, bond and

compete with friends

CONSUMER NEEDS

Indian gamer: Same individual, multiple contextsNot defined by demographics – same individual can shuffle between multiple 'why' and 'how' contexts

Source: BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

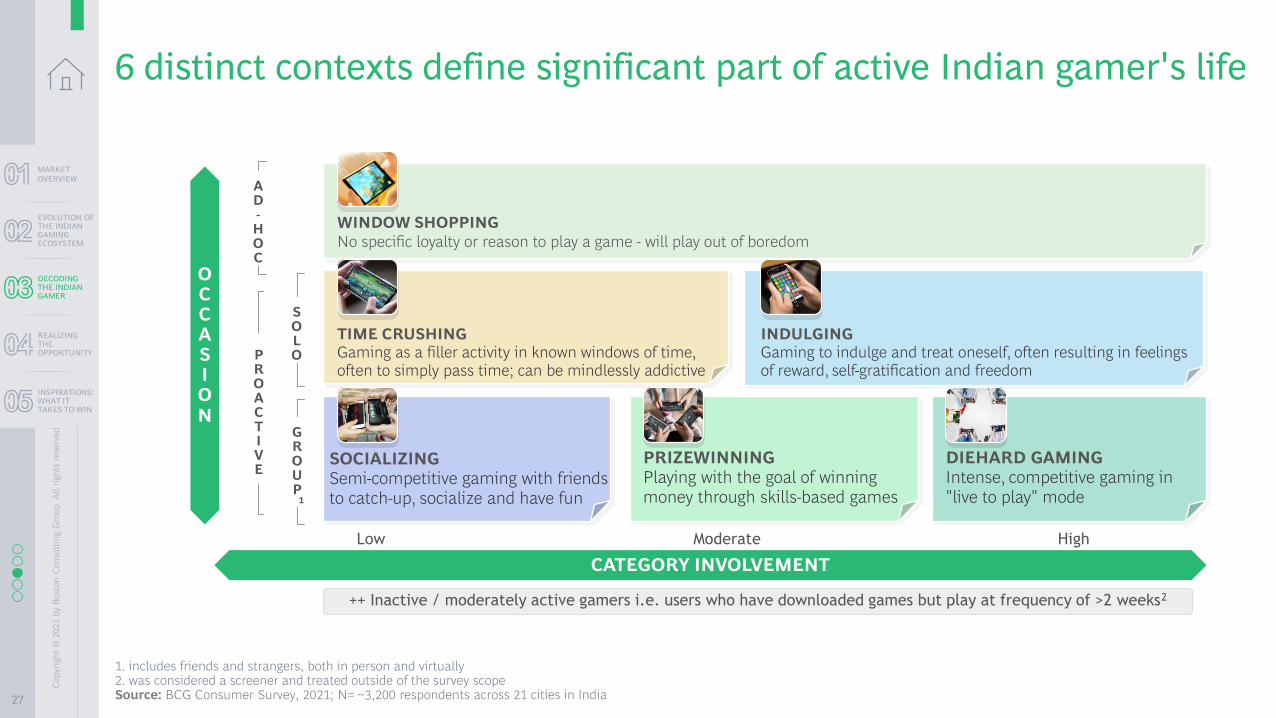

27

1. includes friends and strangers, both in person and virtually2. was considered a screener and treated outside of the survey scopeSource: BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India

TIME CRUSHINGGaming as a filler activity in known windows of time, often to simply pass time; can be mindlessly addictive

SOCIALIZING Semi-competitive gaming with friends to catch-up, socialize and have fun

INDULGINGGaming to indulge and treat oneself, often resulting in feelings of reward, self-gratification and freedom

DIEHARD GAMINGIntense, competitive gaming in "live to play" mode

PRIZEWINNINGPlaying with the goal of winning money through skills-based games

WINDOW SHOPPING

No specific loyalty or reason to play a game - will play out of boredom

ModerateLow High

OCCASION

CATEGORY INVOLVEMENT

SOLO

GROUP

1

PROACTIVE

AD-

HOC

++ Inactive / moderately active gamers i.e. users who have downloaded games but play at frequency of >2 weeks2

6 distinct contexts define significant part of active Indian gamer's life

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

28

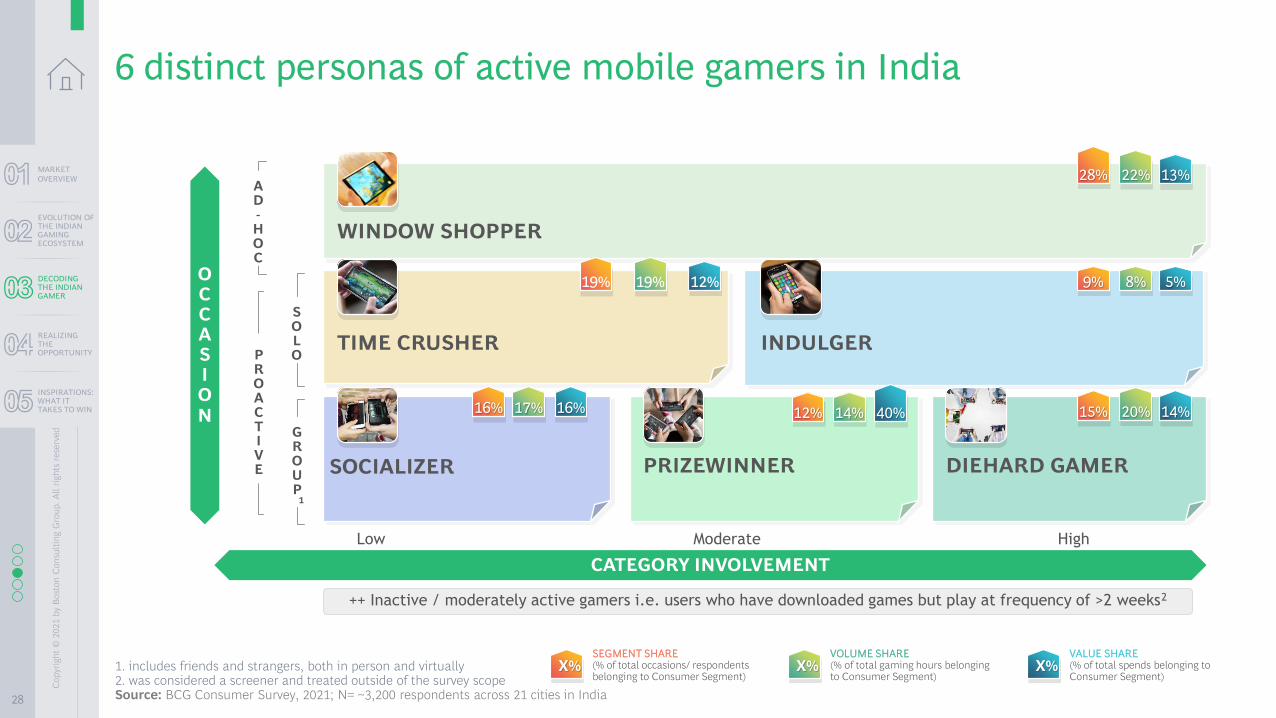

1. includes friends and strangers, both in person and virtually2. was considered a screener and treated outside of the survey scopeSource: BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India

SEGMENT SHARE(% of total occasions/ respondents belonging to Consumer Segment)

X%VOLUME SHARE (% of total gaming hours belonging to Consumer Segment)

X%VALUE SHARE (% of total spends belonging to Consumer Segment)

X%

TIME CRUSHER

SOCIALIZER

INDULGER

DIEHARD GAMERPRIZEWINNER

WINDOW SHOPPER

ModerateLow High

OCCASION

CATEGORY INVOLVEMENT

15% 20% 14%

9% 8% 5%

28% 22% 13%

19% 19% 12%

12% 14% 40%16% 17% 16%

SOLO

GROUP

1

PROACTIVE

AD-

HOC

++ Inactive / moderately active gamers i.e. users who have downloaded games but play at frequency of >2 weeks2

6 distinct personas of active mobile gamers in India

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

29

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

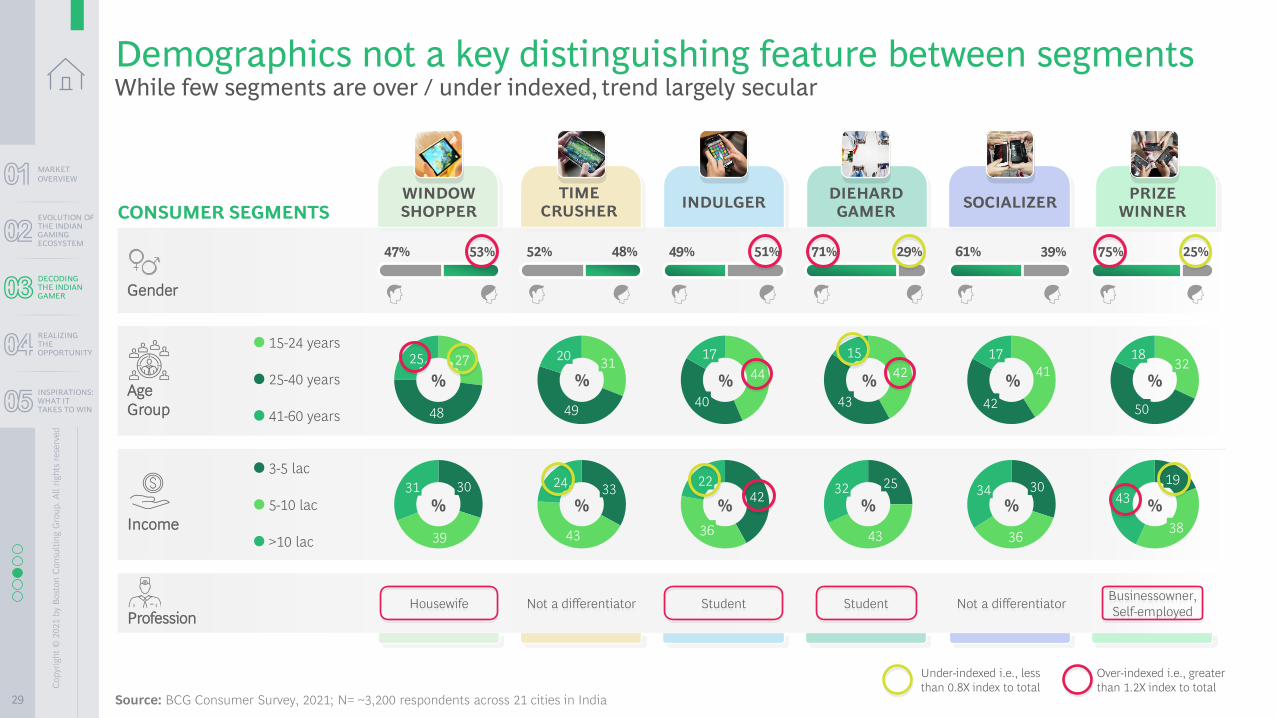

Demographics not a key distinguishing feature between segmentsWhile few segments are over / under indexed, trend largely secular

Over-indexed i.e., greater

than 1.2X index to total

Under-indexed i.e., less

than 0.8X index to total

Age

Group

25-40 years

15-24 years

41-60 years

CONSUMER SEGMENTSWINDOW SHOPPER

TIMECRUSHER

INDULGER DIEHARD GAMER

SOCIALIZER PRIZE

WINNER

Gender

53%47% 48%52% 51%49% 29%71% 39%61% 25%75%

41

42

17

49

3120

48

272544

40

17

42

43

1532

50

18

Income

Profession Not a differentiator Student Student

Businessowner,

Self-employed Housewife

39

3031

5-10 lac

3-5 lac

>10 lac 43

332442

36

22

43

2532

36

303443

19

38

%

%

%

%

%

%

%

%

%

%

%

%

Not a differentiator

Source: BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

30

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Source: BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India

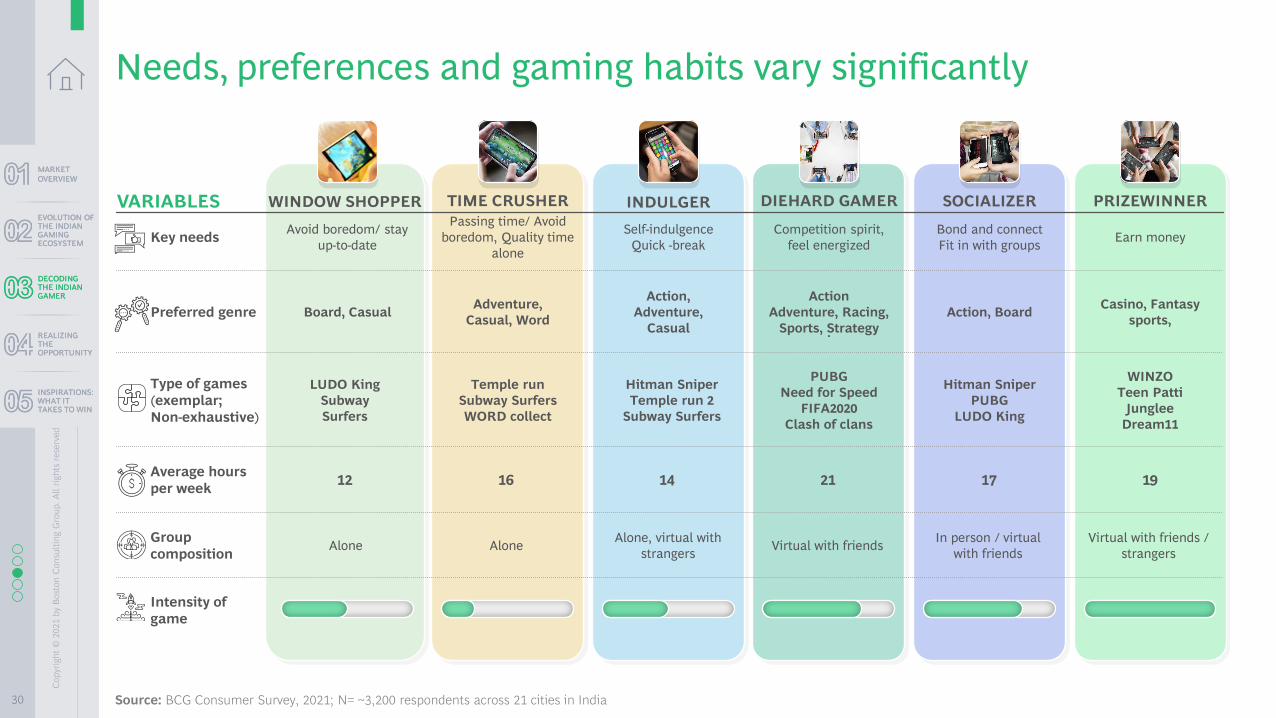

Needs, preferences and gaming habits vary significantly

VARIABLES WINDOW SHOPPER TIME CRUSHER INDULGER DIEHARD GAMER

.

SOCIALIZER PRIZEWINNER

.

Intensity of

game

Preferred genre Board, Casual Adventure,

Casual, Word

Action,

Adventure,

Casual

Action

Adventure, Racing,

Sports, Strategy

Action, BoardCasino, Fantasy

sports,

Group

compositionAloneAlone Virtual with friends

In person / virtual

with friends

Virtual with friends /

strangers

Alone, virtual with

strangers

Key needsAvoid boredom/ stay

up-to-date

Passing time/ Avoid

boredom, Quality time

alone

Self-indulgence

Quick -break

Competition spirit,

feel energized

Bond and connect

Fit in with groupsEarn money

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Average hours

per week12 16 14 21 17 19

Type of games

(exemplar;

Non-exhaustive)

LUDO King

Subway

Surfers

Temple run

Subway Surfers

WORD collect

Hitman Sniper

Temple run 2

Subway Surfers

PUBG

Need for Speed

FIFA2020

Clash of clans

Hitman Sniper

PUBG

LUDO King

WINZO

Teen Patti

Junglee

Dream11

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

31

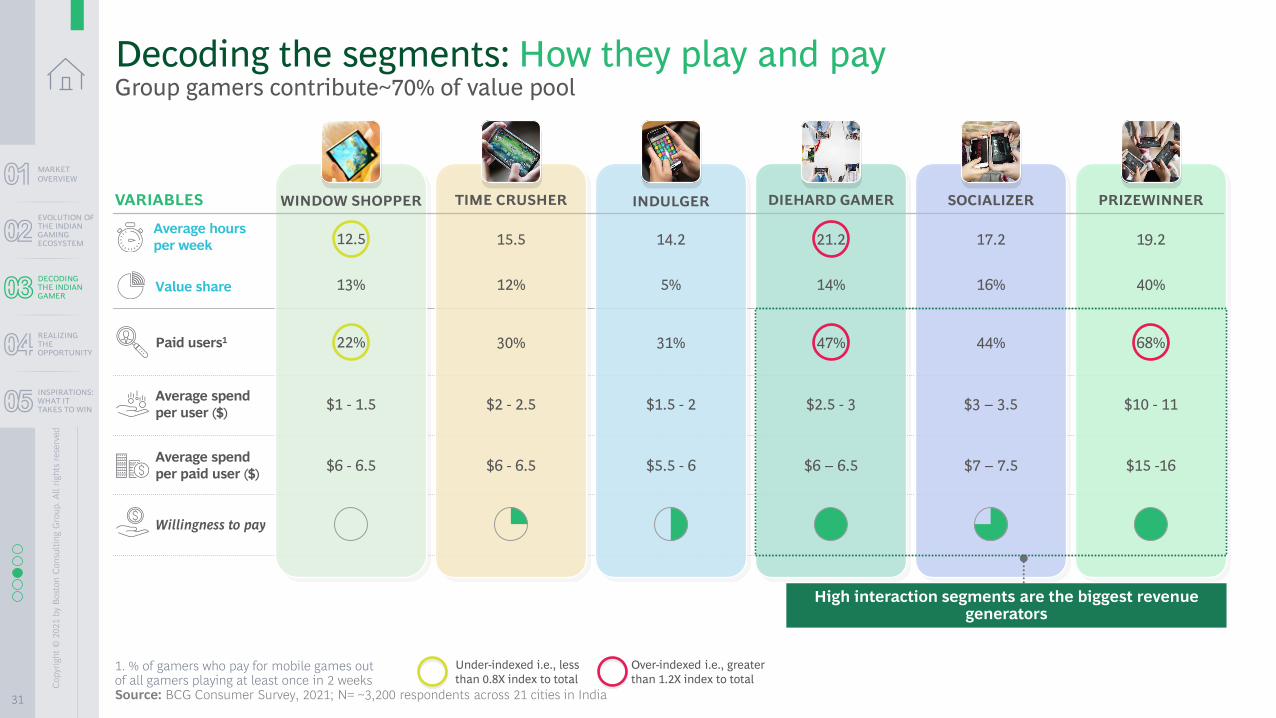

Paid users1

Willingness to pay

VARIABLES WINDOW SHOPPER TIME CRUSHER INDULGER DIEHARD GAMER SOCIALIZER PRIZEWINNER

22% 30% 31% 47% 44% 68%

Average spend

per user ($)

Average spend

per paid user ($)

Average hours

per week 12.5 15.5 14.2 21.2 17.2 19.2

Value share 12% 5% 16% 40%13% 14%

1. % of gamers who pay for mobile games out of all gamers playing at least once in 2 weeksSource: BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India

Decoding the segments: How they play and payGroup gamers contribute~70% of value pool

High interaction segments are the biggest revenue generators

Over-indexed i.e., greater

than 1.2X index to total

Under-indexed i.e., less

than 0.8X index to total

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

$1 - 1.5 $2 - 2.5 $1.5 - 2 $2.5 - 3 $3 – 3.5 $10 - 11

$6 - 6.5 $6 - 6.5 $5.5 - 6 $6 – 6.5 $7 – 7.5 $15 -16

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

32

PROFILE

MEDIA PROFILE

PREFERRED MODEL

AGE

GENDER

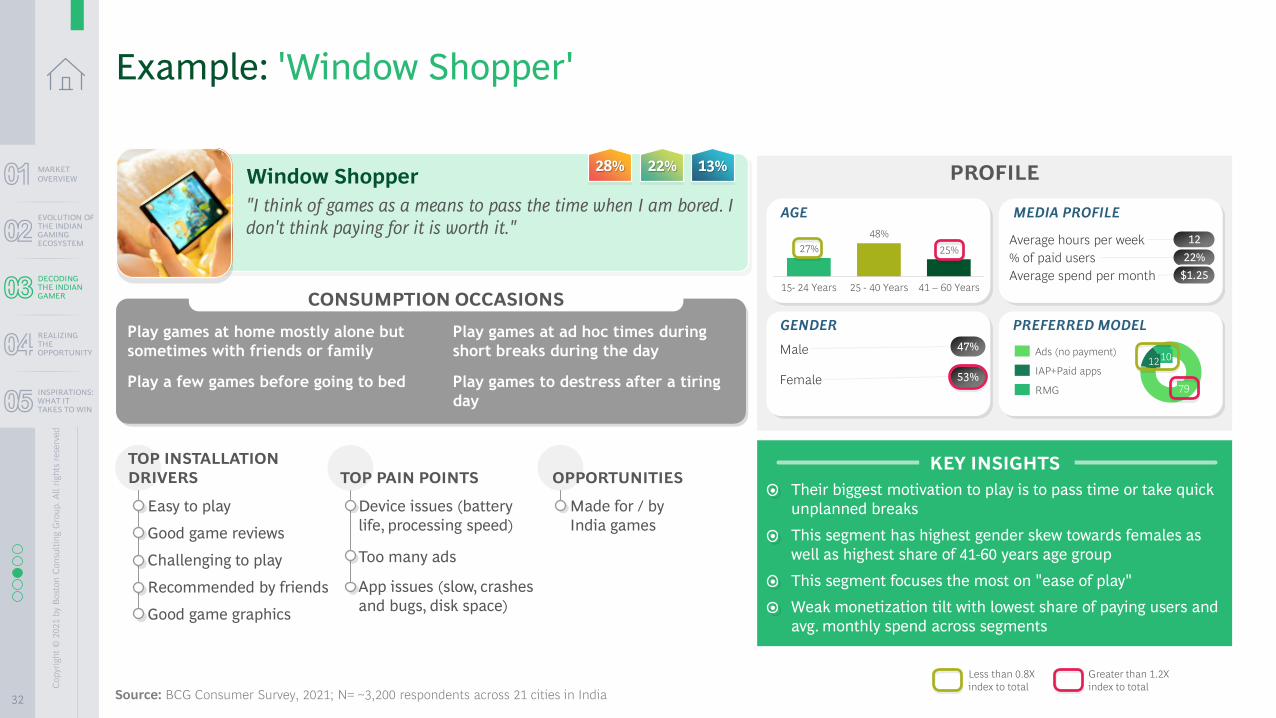

Example: 'Window Shopper'

KEY INSIGHTS

• Their biggest motivation to play is to pass time or take quick

unplanned breaks

Less than 0.8X

index to total

Greater than 1.2X

index to total

• This segment has highest gender skew towards females as

well as highest share of 41-60 years age group

• This segment focuses the most on "ease of play"

• Weak monetization tilt with lowest share of paying users and

avg. monthly spend across segments

Play games at home mostly alone but

sometimes with friends or family

Play a few games before going to bed

Window Shopper

"I think of games as a means to pass the time when I am bored. I

don't think paying for it is worth it."

TOP INSTALLATION

DRIVERS OPPORTUNITIES TOP PAIN POINTS

Easy to play

Good game reviews

Challenging to play

Recommended by friends

Good game graphics

Play games at ad hoc times during

short breaks during the day

Play games to destress after a tiring

day

CONSUMPTION OCCASIONS

28% 22% 13%

Device issues (battery

life, processing speed)

Too many ads

App issues (slow, crashes

and bugs, disk space)

Made for / by

India games

27%

48%

25%

41 – 60 Years15- 24 Years 25 - 40 Years

Male 47%

Female 53%

Average hours per week 12

% of paid users 22%

Average spend per month $1.25

79

1012Ads (no payment)

IAP+Paid apps

RMG

Source: BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

33

TOP INSTALLATION

DRIVERS OPPORTUNITIES TOP PAIN POINTS

PROFILE

MEDIA PROFILE

PREFERRED MODEL

PREFERRED COMPANY

PREFERRED PLACE

Example: 'Time Crusher' segment

• Their biggest motivation to play is to de-stress or to spend

some "me-time"

• This segment has the largest share of people preferring to

play alone

• Only segment to spend considerable amount of gaming time

during commute

17

15

68IAP+Paid apps

Ads (no payment)

RMG

Average hours per week 16

% of paid users 30%

Average spend per month $2.2577

23Alone

With others1

9

80

11At home

Commute

Other

Time Crusher

"Gaming helps me relax after a long day of work. It is a good

distraction on the long ride back home from work"

Easy to play

Good game reviews

Challenging to play

Recommended by friends

Good game graphics

Device issues (battery life,

processing speed)

Poor audio and video

App issues (slow, crashes

and bugs, disk space)

Made for / by India

games

Inclined towards games

recommended by

influencers

Play games alone at home or

sometimes online with friends/family

Play a few games before going to bed

Play games during commute or when

waiting for something

Play games to destress after a tiring

day or to connect with friends/family

CONSUMPTION OCCASIONS

Less than 0.8X

index to total

Greater than 1.2X

index to total

19% 19% 12%

KEY INSIGHTS

1. "With others" includes friends and strangers, both in person and virtuallySource: BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

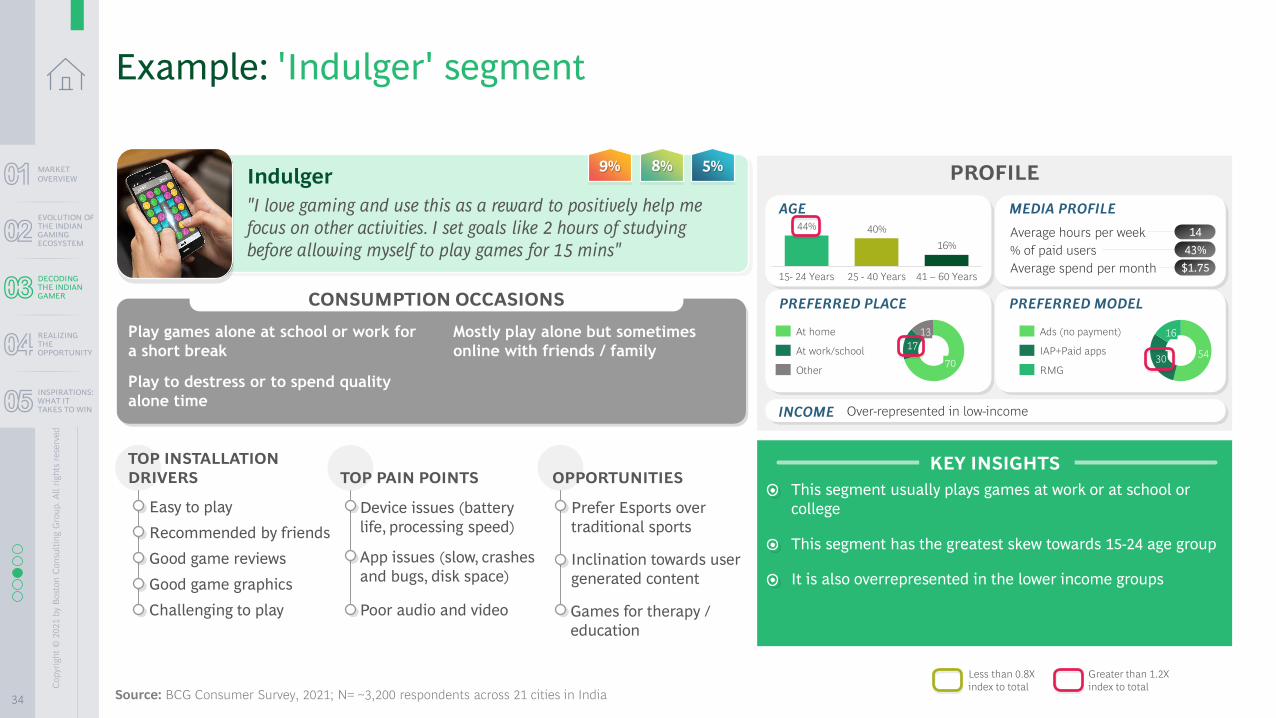

34

TOP INSTALLATION

DRIVERS OPPORTUNITIES TOP PAIN POINTS

PROFILE

KEY INSIGHTS

Example: 'Indulger' segment

• This segment usually plays games at work or at school or

college

• This segment has the greatest skew towards 15-24 age group

• It is also overrepresented in the lower income groups

Indulger

"I love gaming and use this as a reward to positively help me

focus on other activities. I set goals like 2 hours of studying

before allowing myself to play games for 15 mins"

Easy to play

Good game reviews

Challenging to play

Recommended by friends

Good game graphics

Device issues (battery

life, processing speed)

Poor audio and video

App issues (slow, crashes

and bugs, disk space)

Prefer Esports over

traditional sports

Inclination towards user

generated content

Play games alone at school or work for

a short break

Play to destress or to spend quality

alone time

Mostly play alone but sometimes

online with friends / family

CONSUMPTION OCCASIONS

Games for therapy /

education

MEDIA PROFILE

Average hours per week 14

% of paid users 43%

Average spend per month $1.75

X Axis

PREFERRED MODEL

5430

16Ads (no payment)

IAP+Paid apps

RMG

AGE44% 40%

16%

15- 24 Years 25 - 40 Years 41 – 60 Years

PREFERRED PLACE

17

70

13

Other

At home

At work/school

INCOME Over-represented in low-income

Less than 0.8X

index to total

Greater than 1.2X

index to total

9% 8% 5%

Source: BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

35

PROFILE

KEY INSIGHTS

MEDIA PROFILE

PREFERRED MODEL

AGE

PREFERRED PLACE

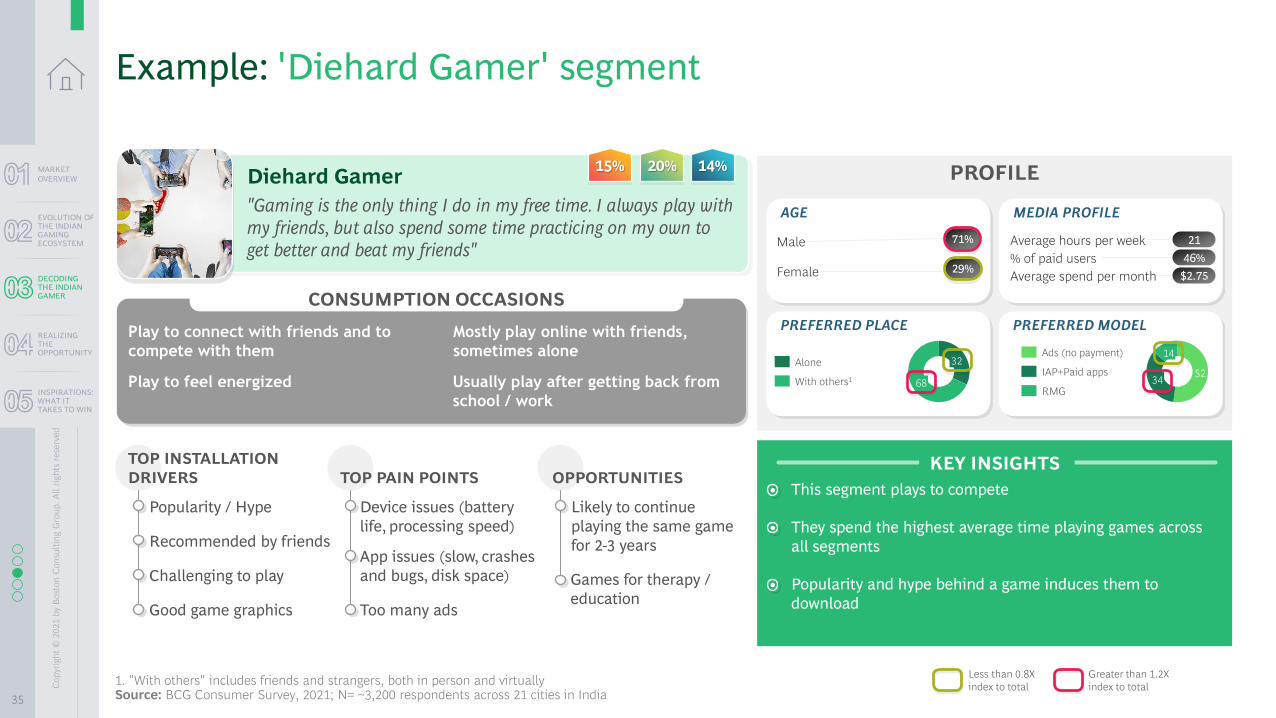

Example: 'Diehard Gamer' segment

• This segment plays to compete

• They spend the highest average time playing games across

all segments

• Popularity and hype behind a game induces them to

download

5234

14Ads (no payment)

IAP+Paid apps

RMG

Average hours per week 21

% of paid users 46%

Average spend per month $2.75

68

32Alone

With others1

Male 71%

Female 29%

Diehard Gamer

"Gaming is the only thing I do in my free time. I always play with

my friends, but also spend some time practicing on my own to

get better and beat my friends"

Popularity / Hype

Challenging to play

Recommended by friends

Good game graphics

Device issues (battery

life, processing speed)

Too many ads

App issues (slow, crashes

and bugs, disk space)

Likely to continue

playing the same game

for 2-3 years

Play to connect with friends and to

compete with them

Play to feel energized

Mostly play online with friends,

sometimes alone

CONSUMPTION OCCASIONS

Games for therapy /

education

Usually play after getting back from

school / work

Less than 0.8X

index to total

Greater than 1.2X

index to total

15% 20% 14%

TOP INSTALLATION

DRIVERS OPPORTUNITIES TOP PAIN POINTS

1. "With others" includes friends and strangers, both in person and virtuallySource: BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

36

PROFILE

KEY INSIGHTS

MEDIA PROFILE

PREFERRED MODEL

PREFERRED PLACE

PREFERRED COMPANY

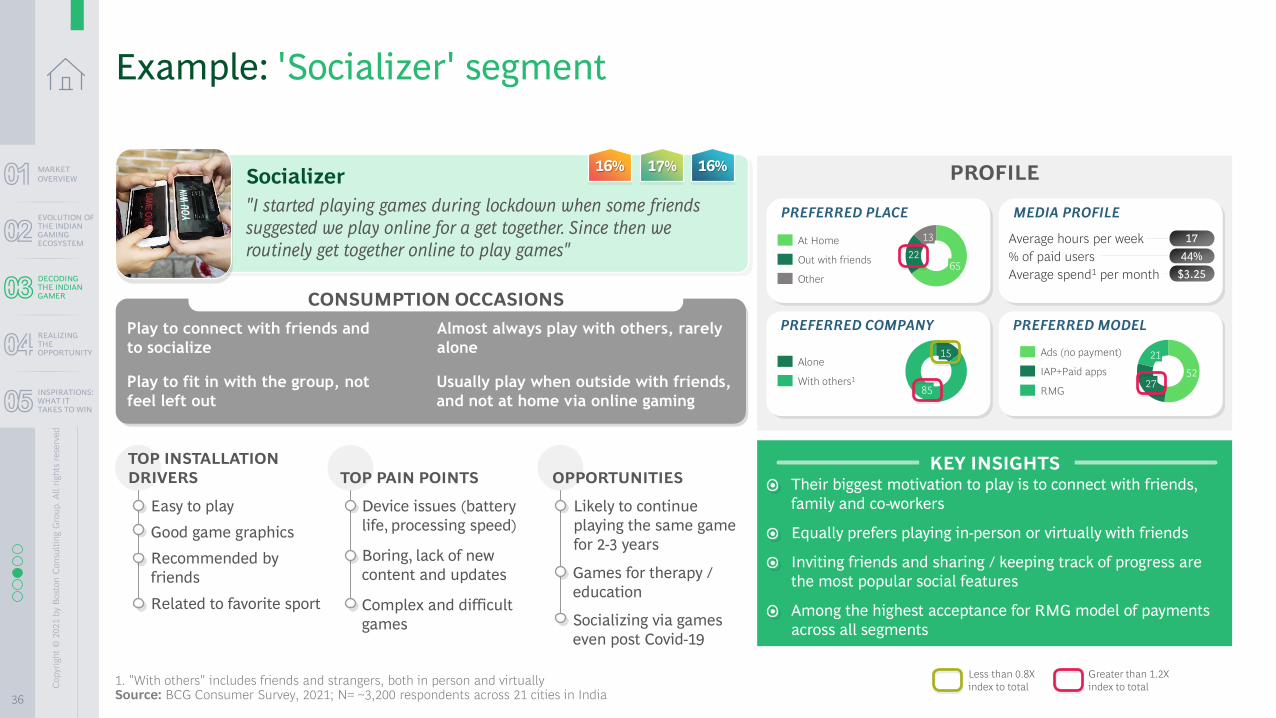

Example: 'Socializer' segment

• Their biggest motivation to play is to connect with friends,

family and co-workers

• Equally prefers playing in-person or virtually with friends

• Inviting friends and sharing / keeping track of progress are

the most popular social features

• Among the highest acceptance for RMG model of payments

across all segments

5227

21Ads (no payment)

IAP+Paid apps

RMG

Average hours per week 17

% of paid users 44%

Average spend1 per month $3.25

22

13

65

At Home

Other

Out with friends

15

85

Alone

With others1

Socializer

"I started playing games during lockdown when some friends

suggested we play online for a get together. Since then we

routinely get together online to play games"

Easy to play

Related to favorite sport

Recommended by

friends

Good game graphics

Device issues (battery

life, processing speed)

Complex and difficult

games

Boring, lack of new

content and updates

Likely to continue

playing the same game

for 2-3 years

Play to connect with friends and

to socialize

Play to fit in with the group, not

feel left out

Almost always play with others, rarely

alone

CONSUMPTION OCCASIONS

Games for therapy /

education

Usually play when outside with friends,

and not at home via online gaming

Socializing via games

even post Covid-19

Less than 0.8X

index to total

Greater than 1.2X

index to total

16% 17% 16%

TOP INSTALLATION

DRIVERS OPPORTUNITIES TOP PAIN POINTS

1. "With others" includes friends and strangers, both in person and virtuallySource: BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

37

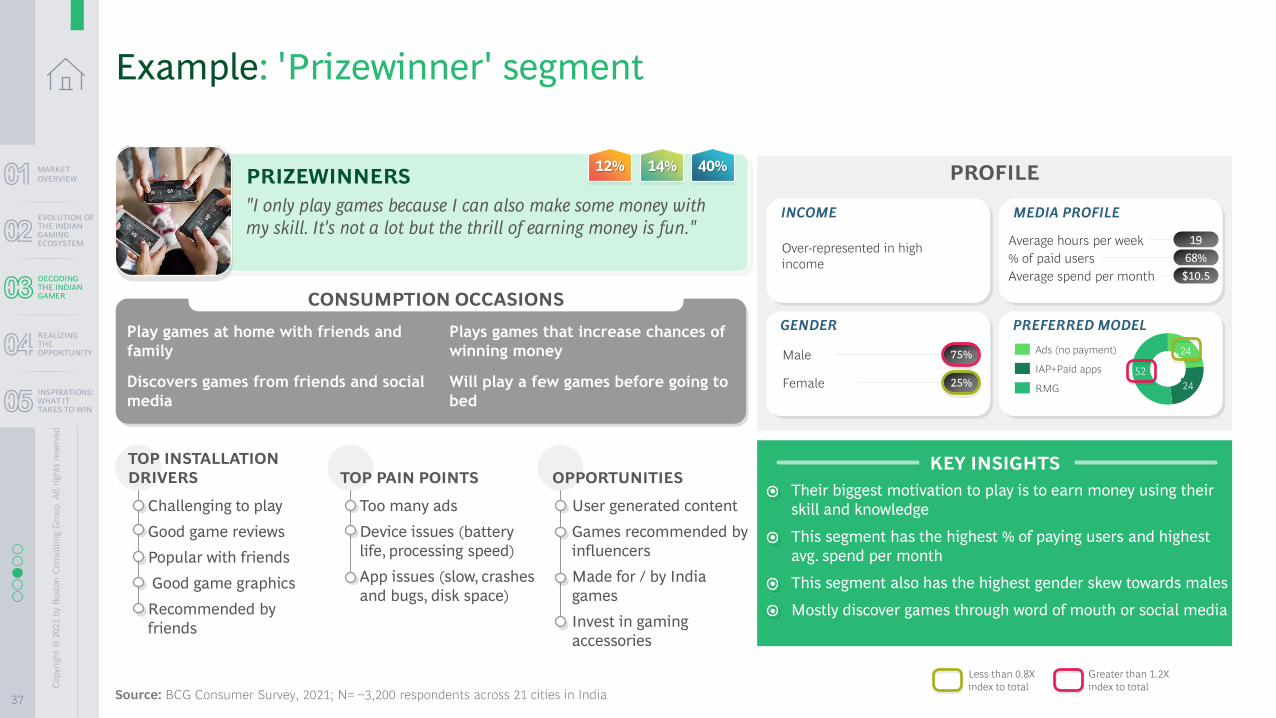

PROFILE

KEY INSIGHTS

MEDIA PROFILE

PREFERRED MODEL

INCOME

GENDER

Over-represented in high

income

Average hours per week 19

% of paid users 68%

Average spend per month $10.5

Male 75%

Female 25%

• Their biggest motivation to play is to earn money using their

skill and knowledge

• This segment has the highest % of paying users and highest

avg. spend per month

• This segment also has the highest gender skew towards males

• Mostly discover games through word of mouth or social media

52

24

24

Ads (no payment)

IAP+Paid apps

RMG

Example: 'Prizewinner' segment

PRIZEWINNERS

"I only play games because I can also make some money with

my skill. It's not a lot but the thrill of earning money is fun."

Challenging to play

Good game reviews

Popular with friends

Good game graphics

Recommended by

friends

User generated content

Games recommended by

influencers

Made for / by India

games

Invest in gaming

accessories

Too many ads

Device issues (battery

life, processing speed)

App issues (slow, crashes

and bugs, disk space)

Play games at home with friends and

family

Discovers games from friends and social

media

Plays games that increase chances of

winning money

Will play a few games before going to

bed

CONSUMPTION OCCASIONS

Less than 0.8X

index to total

Greater than 1.2X

index to total

12% 14% 40%

TOP INSTALLATION

DRIVERS OPPORTUNITIES TOP PAIN POINTS

Source: BCG Consumer Survey, 2021; N= ~3,200 respondents across 21 cities in India

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

38

CO

NT

EN

TS

TA

BL

E o

f

EVOLUTION OF

THE INDIAN

GAMING

ECOSYSTEM

DECODING THE

INDIAN GAMER

Who plays where, key

trends shaping the

ecosystem

Insights from consumer

research

INSPIRATIONS:

WHAT IT TAKES

TO WIN

Learnings from

exemplars

MARKET

OVERVIEW

$5B+ market

opportunity at the back

of exponential growth

REALIZING THE

OPPORTUNITY

Action agenda for

companies

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

39

6 imperatives to drive the next wave of growth

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

ENHANCE

DISCOVERY

AND ADOPTION

IMPROVE

USAGE AND

RETENTION

DRIVE

"ACCEPTABLE"

MONETIZATION

Game design and mechanics are effective in driving organic discovery and growth 2

Casual games, free to play games and influencers are good hooks to onboard first-

time gamers1

Genre diversification effective in increasing engagement and addressing churn3Contextual and interactive social experiences are key in driving adoption and

retention for gamers 4Ads and product placements can be blended seamlessly into the game without

being obtrusive to the gamer5Localized pricing strategies are extremely effective in converting users to payers6

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

40

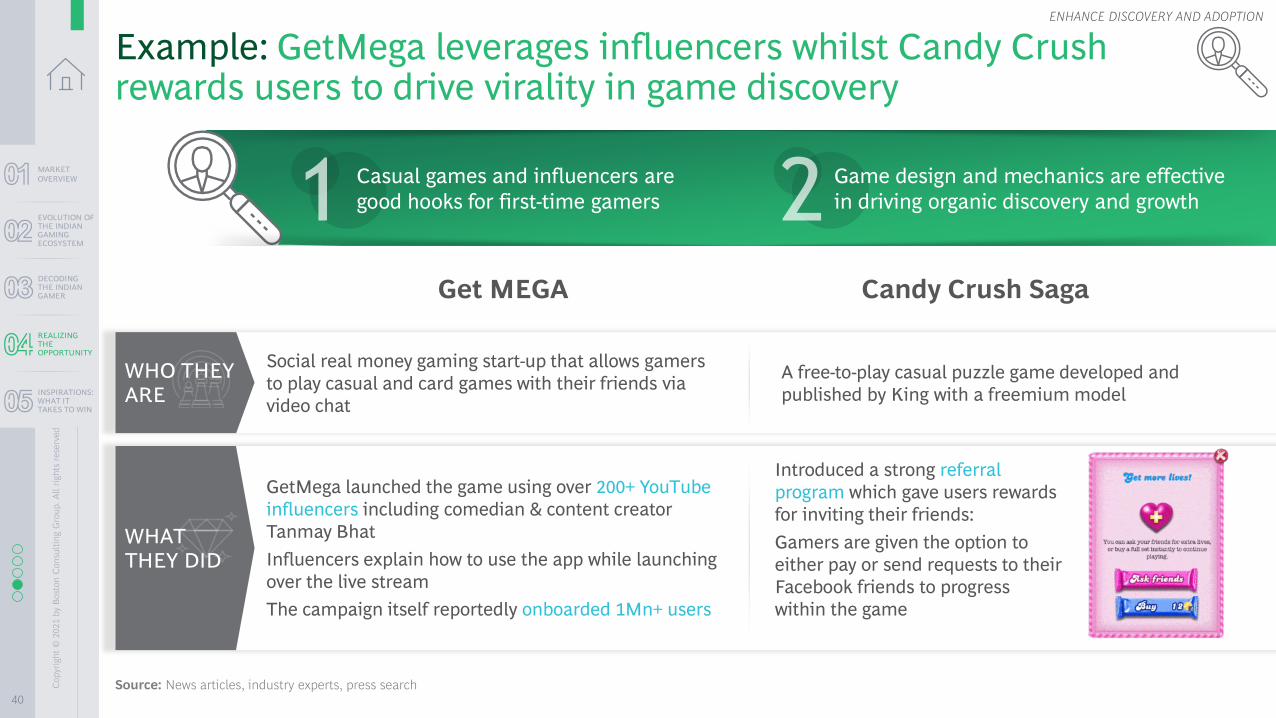

Example: GetMega leverages influencers whilst Candy Crush rewards users to drive virality in game discovery

ENHANCE DISCOVERY AND ADOPTION

Game design and mechanics are effective

in driving organic discovery and growth

Casual games and influencers are

good hooks for first-time gamers

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Social real money gaming start-up that allows gamers

to play casual and card games with their friends via

video chat

A free-to-play casual puzzle game developed and

published by King with a freemium model

WHO THEY ARE

Source: News articles, industry experts, press search

GetMega launched the game using over 200+ YouTube

influencers including comedian & content creator

Tanmay Bhat

Influencers explain how to use the app while launching

over the live stream

The campaign itself reportedly onboarded 1Mn+ users

Introduced a strong referral

program which gave users rewards

for inviting their friends:

Gamers are given the option to

either pay or send requests to their

Facebook friends to progress

within the game

WHAT THEY DID

Get MEGA Candy Crush Saga

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

41

WHAT THEY DID

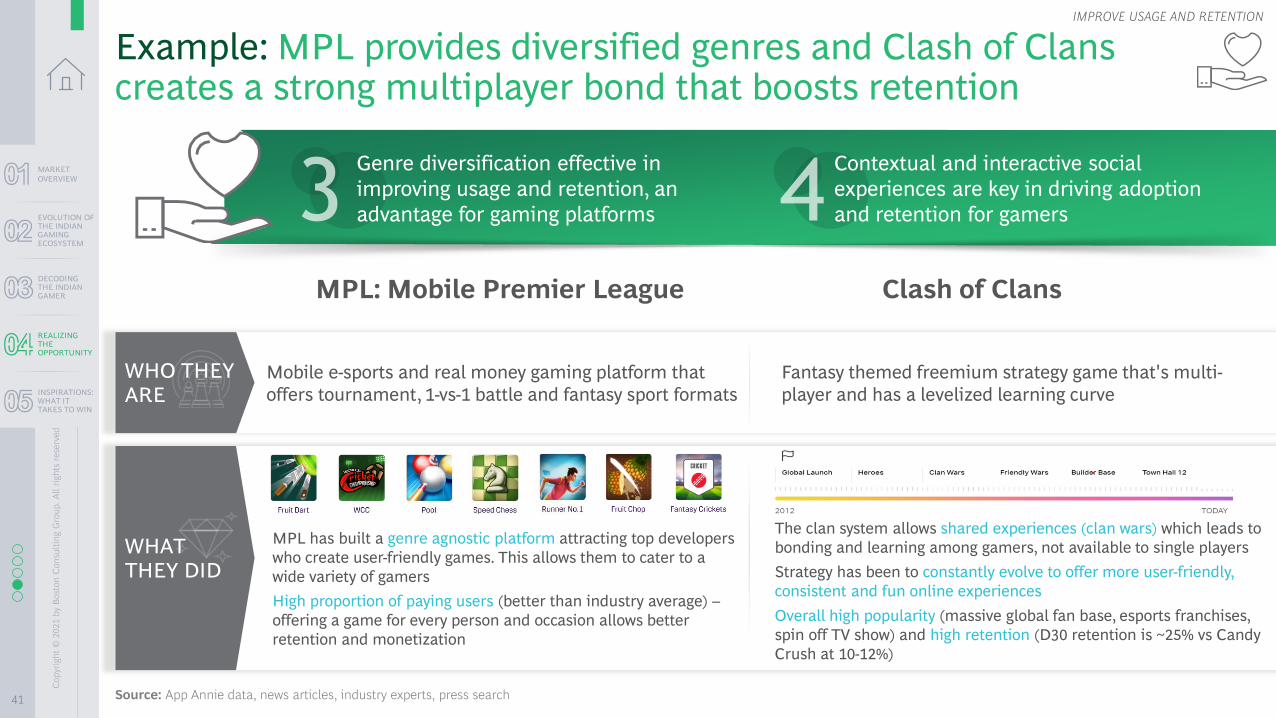

Example: MPL provides diversified genres and Clash of Clans creates a strong multiplayer bond that boosts retention

Contextual and interactive social

experiences are key in driving adoption

and retention for gamers

Genre diversification effective in

improving usage and retention, an

advantage for gaming platforms

WHO THEY ARE

Source: App Annie data, news articles, industry experts, press search

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Mobile e-sports and real money gaming platform that

offers tournament, 1-vs-1 battle and fantasy sport formats

Fantasy themed freemium strategy game that's multi-

player and has a levelized learning curve

MPL has built a genre agnostic platform attracting top developers

who create user-friendly games. This allows them to cater to a

wide variety of gamers

High proportion of paying users (better than industry average) –

offering a game for every person and occasion allows better

retention and monetization

The clan system allows shared experiences (clan wars) which leads to

bonding and learning among gamers, not available to single players

Strategy has been to constantly evolve to offer more user-friendly,

consistent and fun online experiences

Overall high popularity (massive global fan base, esports franchises,

spin off TV show) and high retention (D30 retention is ~25% vs Candy

Crush at 10-12%)

MPL: Mobile Premier League Clash of Clans

IMPROVE USAGE AND RETENTION

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

42

WHAT THEY DID

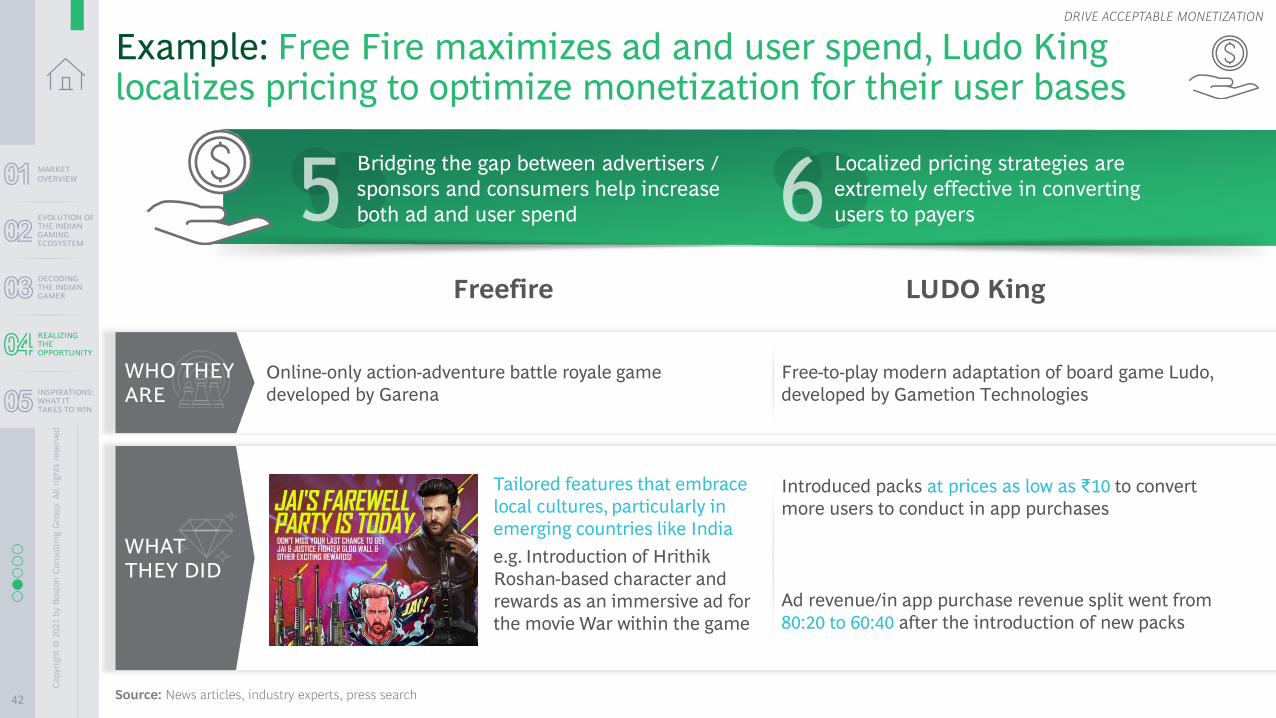

Example: Free Fire maximizes ad and user spend, Ludo King localizes pricing to optimize monetization for their user bases

Online-only action-adventure battle royale game

developed by Garena

Free-to-play modern adaptation of board game Ludo,

developed by Gametion Technologies

Tailored features that embrace

local cultures, particularly in

emerging countries like India

e.g. Introduction of Hrithik

Roshan-based character and

rewards as an immersive ad for

the movie War within the game

Introduced packs at prices as low as ₹10 to convert

more users to conduct in app purchases

Ad revenue/in app purchase revenue split went from

80:20 to 60:40 after the introduction of new packs

Localized pricing strategies are

extremely effective in converting

users to payers

Bridging the gap between advertisers /

sponsors and consumers help increase

both ad and user spend

WHO THEY ARE

Source: News articles, industry experts, press search

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Freefire LUDO King

DRIVE ACCEPTABLE MONETIZATION

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

43

CO

NT

EN

TS

TA

BL

E o

f

EVOLUTION OF

THE INDIAN

GAMING

ECOSYSTEM

DECODING THE

INDIAN GAMER

Who plays where, key

trends shaping the

ecosystem

Insights from consumer

research

MARKET

OVERVIEW

$5B+ market

opportunity at the back

of exponential growth

REALIZING THE

OPPORTUNITY

Action agenda for

companies

INSPIRATIONS:

WHAT IT TAKES

TO WIN

Learnings from

exemplars

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

44

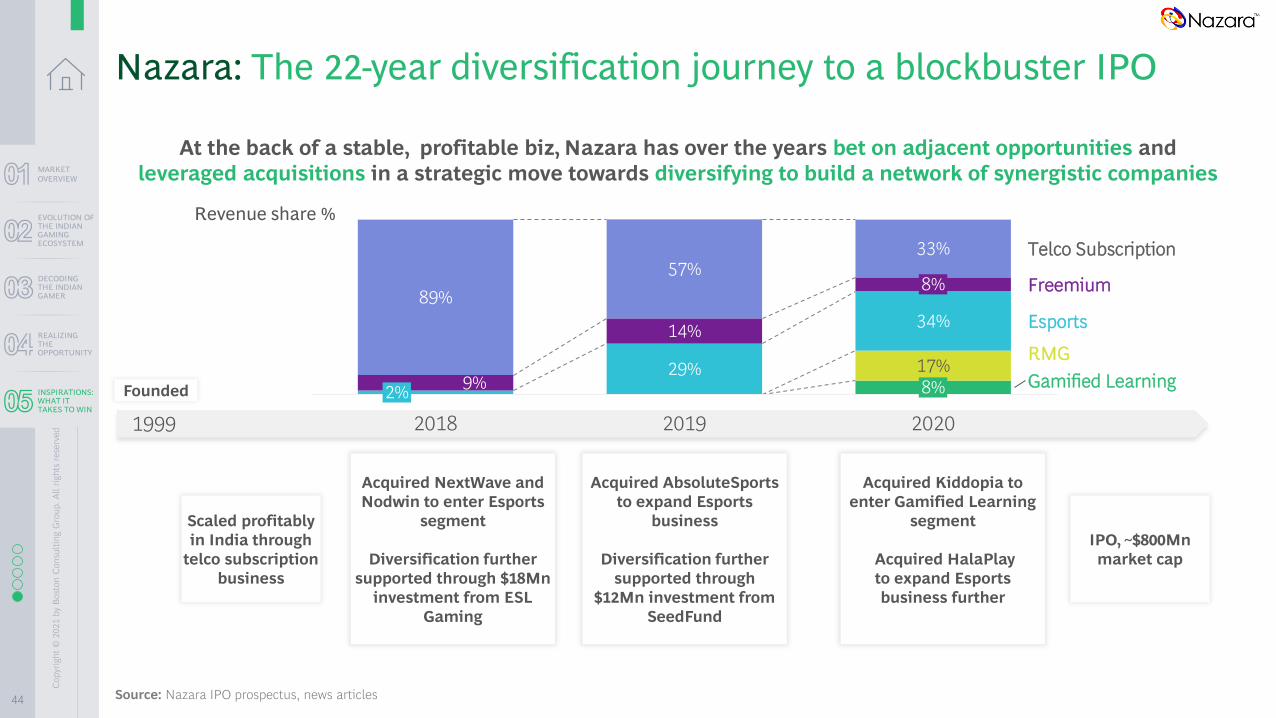

Nazara: The 22-year diversification journey to a blockbuster IPO

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Source: Nazara IPO prospectus, news articles

29%9%

14%

17%

89%

57%

34%

33%

20202019

2%

Esports

2018

8%

RMG

Telco Subscription

Freemium

Gamified Learning

8%

1999

Scaled profitably

in India through

telco subscription

business

Founded

Acquired NextWave and

Nodwin to enter Esports

segment

Diversification further

supported through $18Mn

investment from ESL

Gaming

Acquired AbsoluteSports

to expand Esports

business

Diversification further

supported through

$12Mn investment from

SeedFund

Acquired Kiddopia to

enter Gamified Learning

segment

Acquired HalaPlay

to expand Esports

business further

At the back of a stable, profitable biz, Nazara has over the years bet on adjacent opportunities and

leveraged acquisitions in a strategic move towards diversifying to build a network of synergistic companies

IPO, ~$800Mn

market cap

Revenue share %

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

45

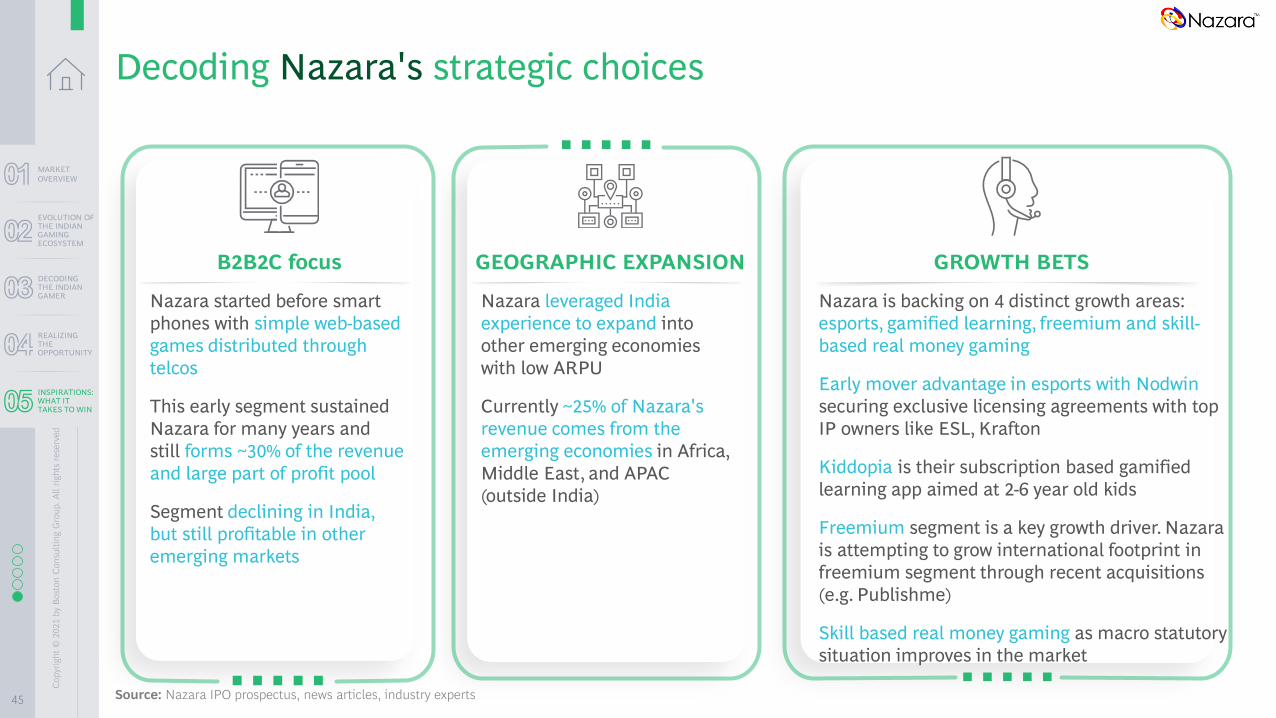

Decoding Nazara's strategic choices

Source: Nazara IPO prospectus, news articles, industry experts

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Nazara started before smart

phones with simple web-based

games distributed through

telcos

This early segment sustained

Nazara for many years and

still forms ~30% of the revenue

and large part of profit pool

Segment declining in India,

but still profitable in other

emerging markets

Nazara leveraged India

experience to expand into

other emerging economies

with low ARPU

Currently ~25% of Nazara's

revenue comes from the

emerging economies in Africa,

Middle East, and APAC

(outside India)

B2B2C focus GEOGRAPHIC EXPANSION

Nazara is backing on 4 distinct growth areas:

esports, gamified learning, freemium and skill-

based real money gaming

Early mover advantage in esports with Nodwin

securing exclusive licensing agreements with top

IP owners like ESL, Krafton

Kiddopia is their subscription based gamified

learning app aimed at 2-6 year old kids

Freemium segment is a key growth driver. Nazara

is attempting to grow international footprint in

freemium segment through recent acquisitions

(e.g. Publishme)

Skill based real money gaming as macro statutory

situation improves in the market

GROWTH BETS

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

46

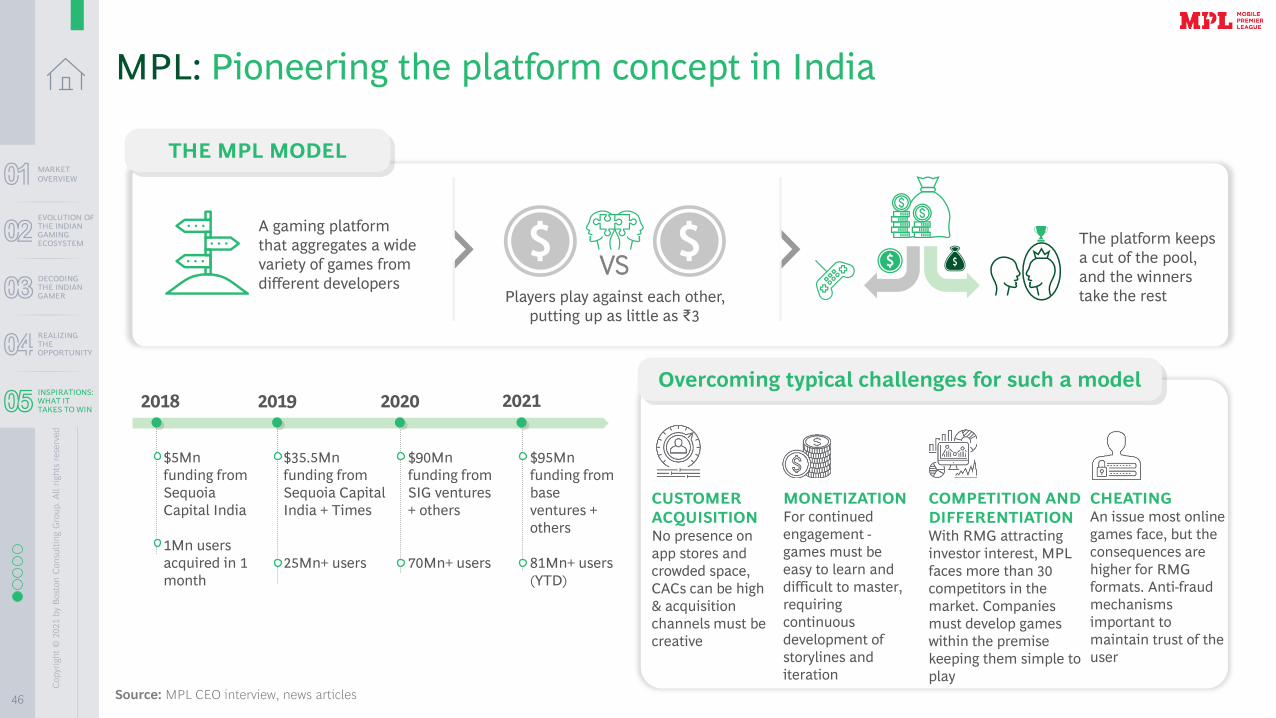

MPL: Pioneering the platform concept in India

Source: MPL CEO interview, news articles

THE MPL MODEL

2018 2019 2020 2021

$5Mn

funding from

Sequoia

Capital India

1Mn users

acquired in 1

month

$35.5Mn

funding from

Sequoia Capital

India + Times

25Mn+ users

$90Mn

funding from

SIG ventures

+ others

70Mn+ users

$95Mn

funding from

base

ventures +

others

81Mn+ users

(YTD)

A gaming platform

that aggregates a wide

variety of games from

different developers Players play against each other,

putting up as little as ₹3

The platform keeps

a cut of the pool,

and the winners

take the rest

VS

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

MONETIZATIONFor continued

engagement -

games must be

easy to learn and

difficult to master,

requiring

continuous

development of

storylines and

iteration

CUSTOMER

ACQUISITIONNo presence on

app stores and

crowded space,

CACs can be high

& acquisition

channels must be

creative

COMPETITION AND

DIFFERENTIATION With RMG attracting

investor interest, MPL

faces more than 30

competitors in the

market. Companies

must develop games

within the premise

keeping them simple to

play

CHEATINGAn issue most online

games face, but the

consequences are

higher for RMG

formats. Anti-fraud

mechanisms

important to

maintain trust of the

user

Overcoming typical challenges for such a model

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

47

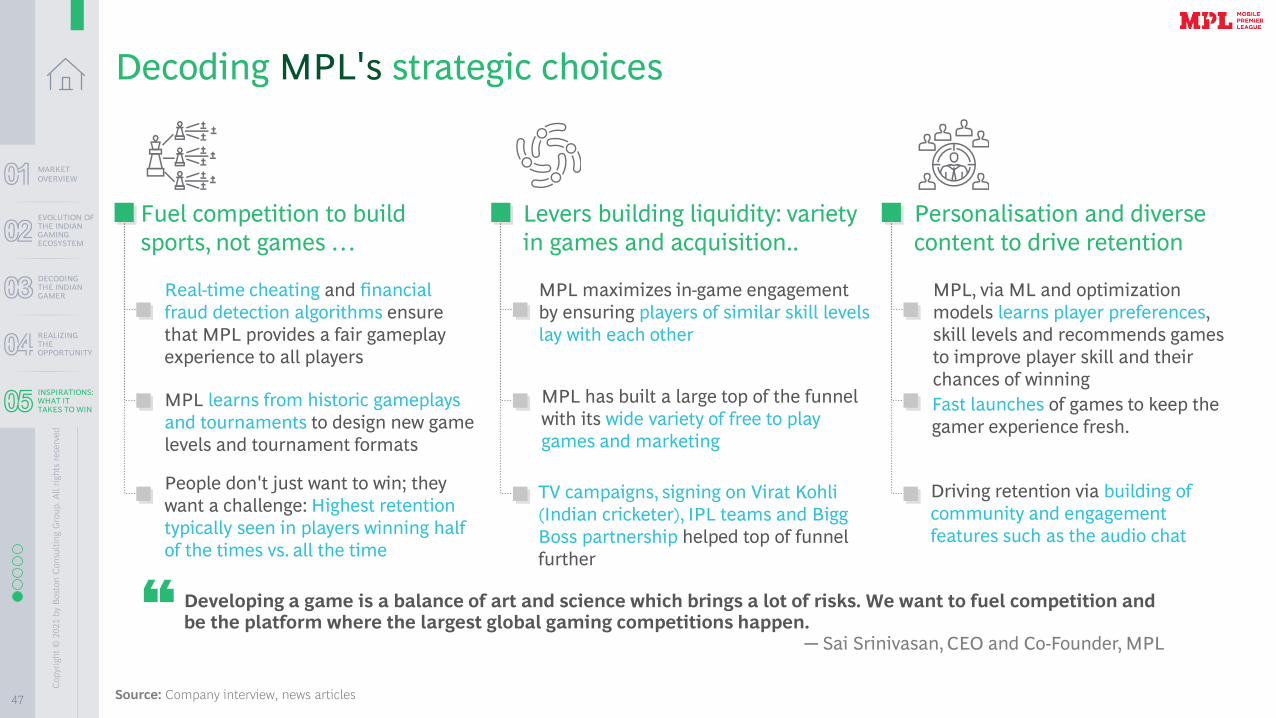

Decoding MPL's strategic choices

Source: Company interview, news articles

Levers building liquidity: variety

in games and acquisition..

Personalisation and diverse

content to drive retention

Fuel competition to build

sports, not games …

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

MPL maximizes in-game engagement

by ensuring players of similar skill levels

lay with each other

MPL has built a large top of the funnel

with its wide variety of free to play

games and marketing

TV campaigns, signing on Virat Kohli

(Indian cricketer), IPL teams and Bigg

Boss partnership helped top of funnel

further

MPL, via ML and optimization

models learns player preferences,

skill levels and recommends games

to improve player skill and their

chances of winning

Fast launches of games to keep the

gamer experience fresh.

Driving retention via building of

community and engagement

features such as the audio chat

Real-time cheating and financial

fraud detection algorithms ensure

that MPL provides a fair gameplay

experience to all players

MPL learns from historic gameplays

and tournaments to design new game

levels and tournament formats

People don't just want to win; they

want a challenge: Highest retention

typically seen in players winning half

of the times vs. all the time

Developing a game is a balance of art and science which brings a lot of risks. We want to fuel competition and be the platform where the largest global gaming competitions happen.

─ Sai Srinivasan, CEO and Co-Founder, MPL

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

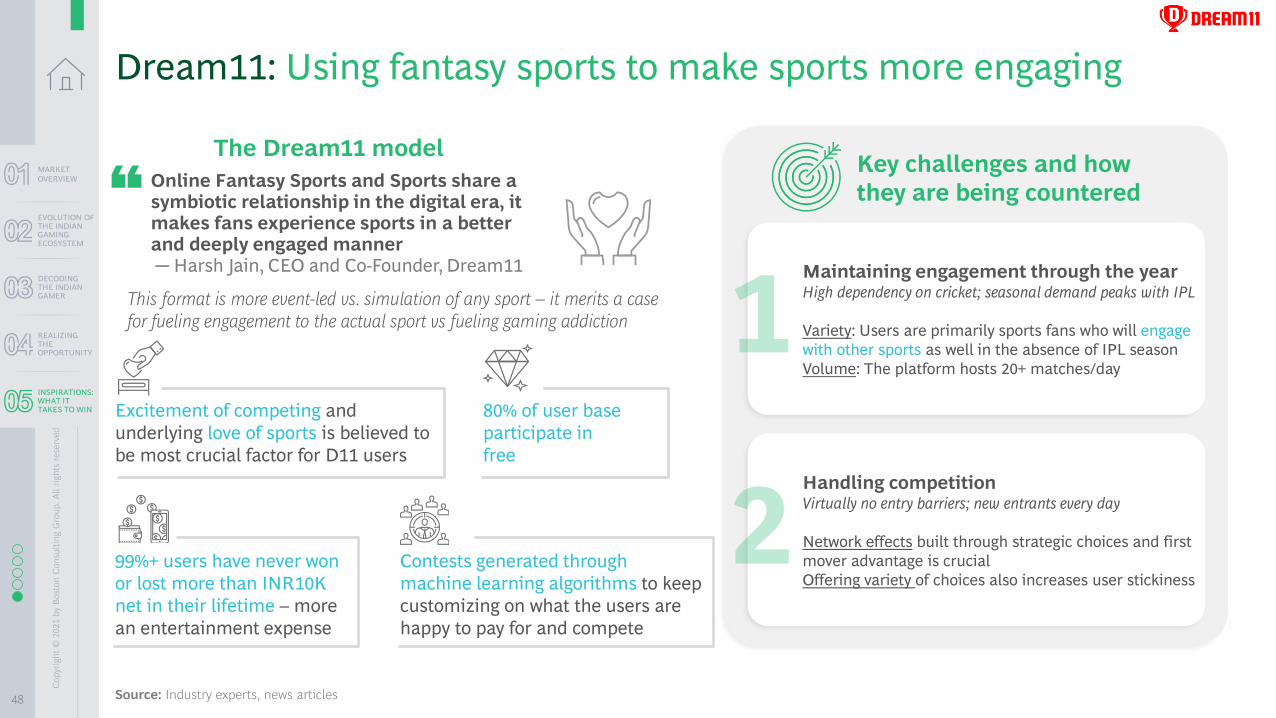

48 Source: Industry experts, news articles

Dream11: Using fantasy sports to make sports more engaging

The Dream11 modelKey challenges and how

they are being countered

Maintaining engagement through the yearHigh dependency on cricket; seasonal demand peaks with IPL

Variety: Users are primarily sports fans who will engage

with other sports as well in the absence of IPL season

Volume: The platform hosts 20+ matches/day

99%+ users have never won

or lost more than INR10K

net in their lifetime – more

an entertainment expense

Excitement of competing and

underlying love of sports is believed to

be most crucial factor for D11 users

80% of user base

participate in

free

Contests generated through

machine learning algorithms to keep

customizing on what the users are

happy to pay for and compete

Handling competitionVirtually no entry barriers; new entrants every day

Network effects built through strategic choices and first

mover advantage is crucial

Offering variety of choices also increases user stickiness

This format is more event-led vs. simulation of any sport – it merits a case

for fueling engagement to the actual sport vs fueling gaming addiction

Online Fantasy Sports and Sports share a symbiotic relationship in the digital era, it makes fans experience sports in a better and deeply engaged manner─ Harsh Jain, CEO and Co-Founder, Dream11

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

49 Source: Industry experts, news articles

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

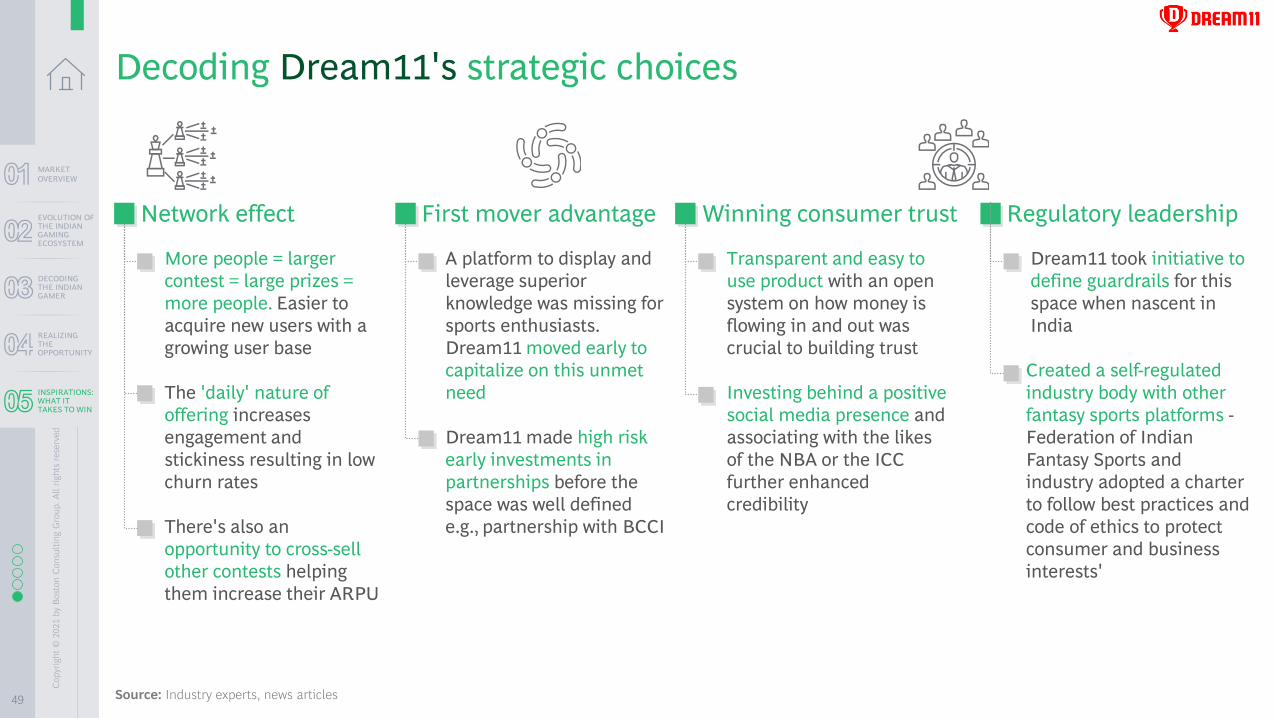

Decoding Dream11's strategic choices

More people = larger

contest = large prizes =

more people. Easier to

acquire new users with a

growing user base

The 'daily' nature of

offering increases

engagement and

stickiness resulting in low

churn rates

There's also an

opportunity to cross-sell

other contests helping

them increase their ARPU

Network effect

A platform to display and

leverage superior

knowledge was missing for

sports enthusiasts.

Dream11 moved early to

capitalize on this unmet

need

Dream11 made high risk

early investments in

partnerships before the

space was well defined

e.g., partnership with BCCI

First mover advantage

Transparent and easy to

use product with an open

system on how money is

flowing in and out was

crucial to building trust

Investing behind a positive

social media presence and

associating with the likes

of the NBA or the ICC

further enhanced

credibility

Winning consumer trust

Dream11 took initiative to

define guardrails for this

space when nascent in

India

Created a self-regulated

industry body with other

fantasy sports platforms -

Federation of Indian

Fantasy Sports and

industry adopted a charter

to follow best practices and

code of ethics to protect

consumer and business

interests'

Regulatory leadership

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

50

OVERVIEW

Launched as a fantasy game

platform in 2019

Currently offers three sets of

RMG games for users

Source: GK Leadership interview, Secondary resources

Gameskraft: One of India's fastest growing companies

COMPETITION AND

DIFFERENTIATION

Highly competitive

market with 30+

companies. Entry of global

companies adding to mix

GOVERNMENT

RESTRICTIONS

A few states like Andhra,

Telangana, Kerala have

banned RMG games

USER

RETENTION

Cost effective retention

of customers continues

to be a challenge

KEY CHALLENGES

FOR

GAMESKRAFT

Parent company of

RummyCulture and Gamezy

10+

Mn

registered

base,

1-1.5

Mn

MAUs and

growing

Players compete putting up as little as

₹1 + multiple tourneys types

GK keeps a cut of the pool money (rake

percentage), and winners take the rest

First product of GK. Launched in

October 2017

Real Money rummy platform.

Offers everyday and special

tournaments and table pool

matches

Fantasy cricket – T20, ODI and test matches

Card games like poker, rummy

Casual games like snake, carrom, chess, 8 Ball pool

MARKET

OVERVIEW

DECODING THE INDIAN GAMER

REALIZING THE OPPORTUNITY

INSPIRATIONS: WHAT IT TAKES TO WIN

EVOLUTION OF THE INDIAN GAMING ECOSYSTEM

RummyCulture

Gamezy

Co

pyr

igh

t ©

202

1 b

y B

ost

on

Co

nsu

ltin

g G

rou

p.

All r

igh

ts r

ese

rved

51

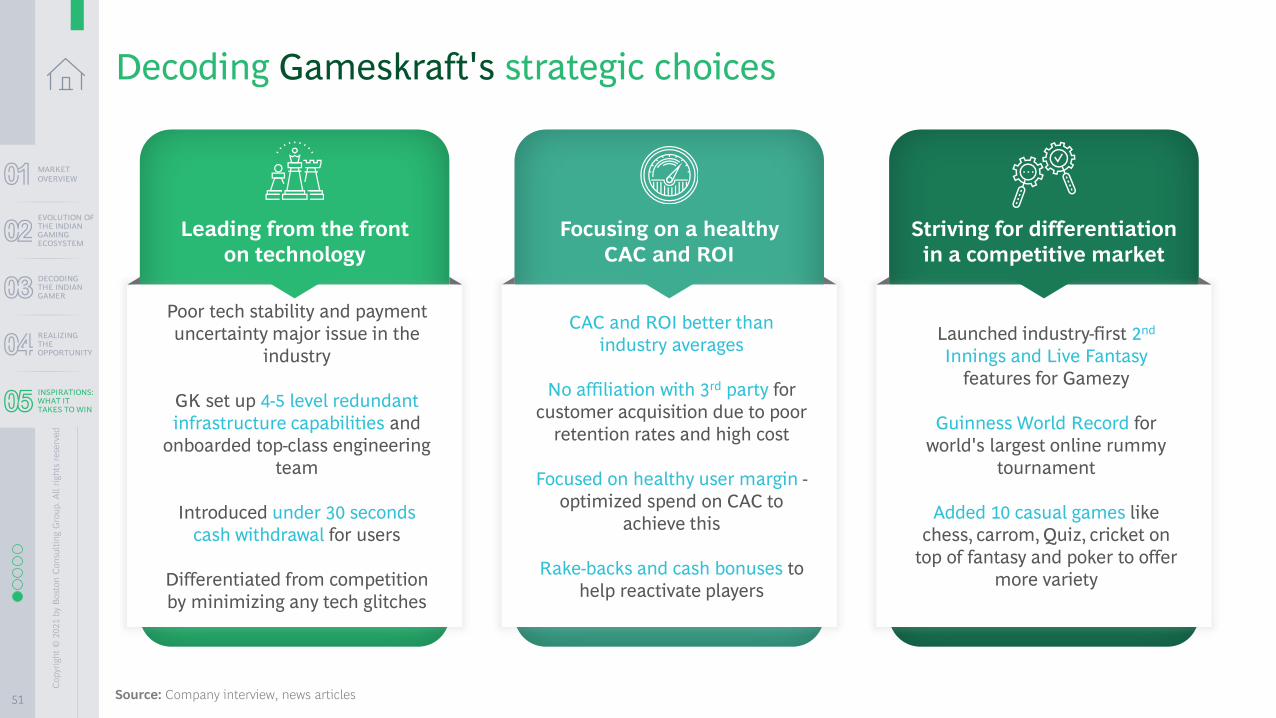

Striving for differentiation

in a competitive market

Focusing on a healthy

CAC and ROI

Leading from the front

on technology

Source: Company interview, news articles

Decoding Gameskraft's strategic choices

Launched industry-first 2nd

Innings and Live Fantasy

features for Gamezy

Guinness World Record for

world's largest online rummy

tournament

Added 10 casual games like

chess, carrom, Quiz, cricket on

top of fantasy and poker to offer

more variety

Poor tech stability and payment

uncertainty major issue in the

industry

GK set up 4-5 level redundant

infrastructure capabilities and

onboarded top-class engineering

team