Embed Size (px)

Citation preview

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 1/29

Demutualisation of Stock

Exchanges

SAPM | Section A | Group 2

Abhishek Sinha | Manish Yadav | Manu Gupt |Nishant Hingu | Roshan Tirkey | Vijay KumarSiddi

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 2/29

DEMUTUALIZATION –

ROLE &DEFINITION

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 3/29

Capital Markets and Exchanges

• Capital markets channel the savings of an economy intoinvestments

• Stock exchanges create an organized market whereissuers and investors are brought together

• Demutualization:• conversion of an exchange from a not-for-profit member

owned organization

• to a for-profit shareholder owned corporation

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 4/29

Organizational Structure differences

• Role and powers of the exchange’s Board of Directors

• Influence of external bodies and public interestrepresentatives

• Legal and regulatory frameworks

• Degree of oversight of each exchange by Govt.

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 5/29

Traditional Exchanges

• Mutual associations owned by their members• Co-operative governance: close identity between owners

and direct users of its trading services

• Democratic: one-member one-vote

• Ownership rights not freely tradeable or exchangeable• Forfeited on the cessation of membership

• Non-profit objective and prohibit the distribution ofsurpluses

• Seldom able to raise capital from anyone other than theirmembers

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 6/29

Demutualized Exchange “DE”

• Corporations with share capital which are listed publiclytraded

• 3 principal groups: owners, decision-makers, customers

• Shareholders vest decision-making power in board of

directors• Voting rights of shareholders are proportionate to their

economic interest in the corporation

• Owners with greater economic interests are more

capable of influencing decision making• Separate ownership rights from trading privileges

• Able to raise new capital from a variety of sources

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 7/29

Post-demutualization structure

• Remained private corporations• Public corporations by listing their stock

• Subsidiaries of publicly traded holding companies

• Some have limited the tradeablity of their shares post-

public listing• Most have imposed share ownership restrictions

• Appropriateness of each structure is dependent on thecircumstances

• However, most of the benefits are associated with thepublicly listed demutualized exchange with freely tradableshares

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 8/29

Process of Demutualization

• Process of continuing an organization from its mutualownership structure to a share ownership structure

• Obtaining the appropriate regulatory and governmentalconsents

• Converting membership rights into shares• Public issuance and listing of the exchange

• Immediate or eventual freely tradeable shares

• DE’s governance structure rests the ultimate control of

the exchange in the hands of its shareholders

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 9/29

Historical Evolution of Exchanges

• Stockholm Stock Exchange, was the first major exchangeto demutualize in 1993

• Singapore Exchange Limited (“SGX”) was Asia-Pacific'sfirst, in 2000

• LSE, Deutsche Borse and Euronext, NYSE, NASDAQ• 70% of the world’s stock market capitalization is of

publicly-listed exchanges

• 18% have demutualized but not listed their shares

• All of the largest stock exchanges have demutualizedand listed their shares in the last decade

• Similar pattern is for the largest derivatives exchanges

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 10/29

Reasons to Demutualize:RationalizedGovernance

• NSE model: Consensus decision making is slow• Exchange unable to respond quickly and decisively to

changes

• Floor community had significant power over decision

making• Whereas, Bulk Business driven by Institutional Investors,

expecting lowest cost and efficient execution of trades

• Cost and efficiency threatens profits of the floor

community and makes it difficult to implement changes

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 11/29

Reasons to Demutualize: RationalizedGovernance

• DE model: Bottom-line focussed, capable of actingdecisively and rapidly

• Management to take actions in the best interests of the

exchange and its shareholders

• Greater degree of transparency and accountancy toshareholders and thus better corporate governance

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 12/29

Reasons to Demutualize: InvestorParticipation

• Stakeholders: Participating organizations, listedcompanies, and institutional and retail investors

• A DE affords both institutional investors and retail

investors the opportunity to become shareholders

• A DE will have greater flexibility to accommodate theneeds of the now more powerful institutional investors

(who have high liquidity and block trading preferences)

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 13/29

Reasons to Demutualize: Competition fromATSs and Upstairs Trading

• Alternative trading systems (“ATSs”): ATSs are privately operated

computerized systems centralizing and matching buy and sell ordersand providing post-trade information

• Maintained by a third party who also serves a limited regulatoryfunction by imposing requirements on each subscriber

• Upstairs trading: Broker-dealers adopting internal systems toautomate the firm’s execution of customer orders

• When a stock exchange member matches customer orders againstother customer orders or against its own inventory position within thefirm, rather than exposing the order to auction on the exchange

• A DE will be more capable of remaining competitive in terms of price,variety and quality of their services than the exchanges organizedpursuant to the NSE model

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 14/29

Reasons to Demutualize: Globalization

• More mobile as issuers and investors are more readilyable to access foreign capital markets

• Locality and nationality has become less of a defining

characteristic of capital

• Exchanges that once were isolated find themselves inintense competition with global rivals

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 15/29

Reasons to Demutualize: Consolidation

• Strategic alliances and consolidations are impactingcapital markets and exchanges

• Mergers among stock and derivative exchanges havecreated super-exchanges

• Exchanges have to expand their capabilities• Consolidation process will be greatly facilitated by the DE

structure with publicly traded shares

• Greater incentive for exchanges to seek revenue and

cost-saving synergies• DEs makes for easier execution of such strategies

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 16/29

Reasons to Demutualize: Resources forCapital Investment

• Capital raised from an IPO or private investment and aheightened awareness of accountability to stakeholders

• DE should have both the incentive and the resources to

invest in the competitiveness of its information systemsconsiderable capital investment was required to buy-outthe interests of the traders and to modernize theinformation systems of exchanges

• Demutualization was an efficient and rational means ofinfusing additional capital inorder to finance bothactivities

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 17/29

REGULATION OF ADEMUTUALIZED EXCHANGE

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 18/29

The Need for Regulation

• Regulation is necessary to address the inefficienciesgenerated by economic activity

• 3 main objectives of securities regulation asexpressed by the International Organization ofSecurities Commissions (“IOSCO”) are:a. the protection of investors

b. the creation and maintenance of fair, efficient and transparent markets;and

c. the reduction of systemic risk

• Regulation aims toa. reduce the risk of failure of market intermediaries,

b. seeks to reduce the impact of that failure, and

c. isolates the risk to the failing institution

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 19/29

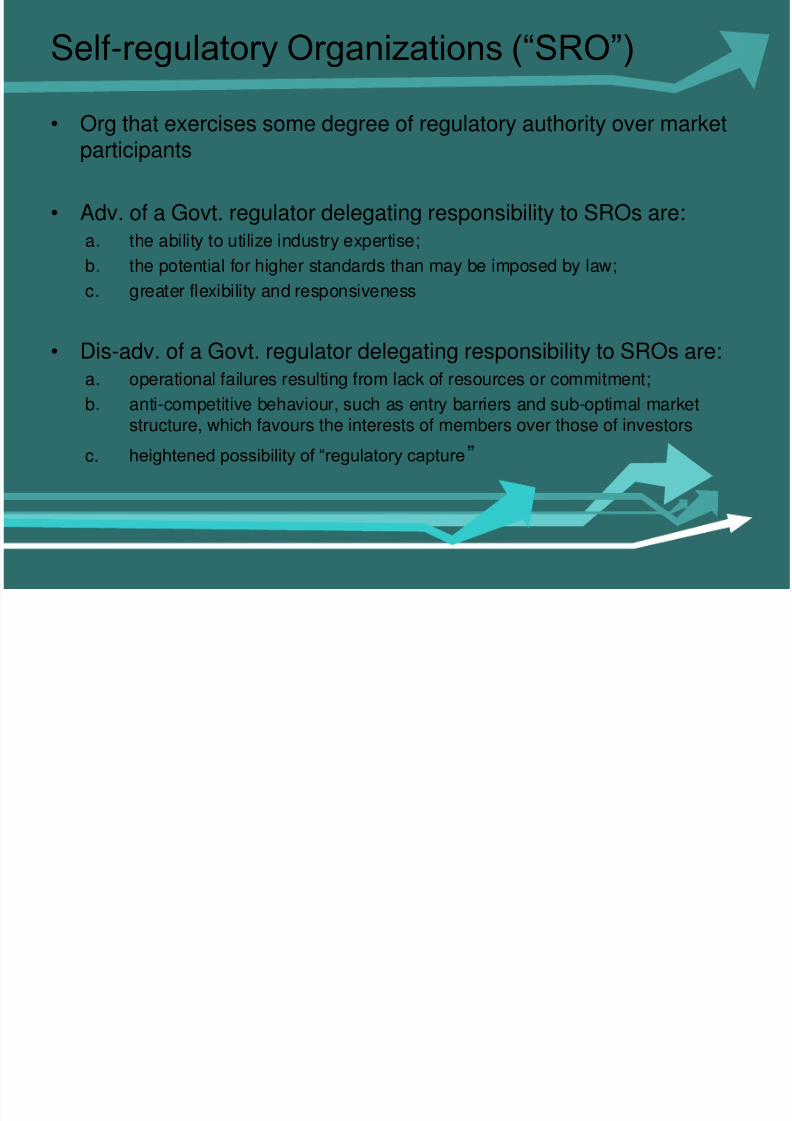

Self-regulatory Organizations (“SRO”)

• Org that exercises some degree of regulatory authority over marketparticipants

• Adv. of a Govt. regulator delegating responsibility to SROs are:

a. the ability to utilize industry expertise;

b. the potential for higher standards than may be imposed by law;

c. greater flexibility and responsiveness

• Dis-adv. of a Govt. regulator delegating responsibility to SROs are:

a. operational failures resulting from lack of resources or commitment;

b. anti-competitive behaviour, such as entry barriers and sub-optimal marketstructure, which favours the interests of members over those of investors

c. heightened possibility of “regulatory capture”

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 20/29

Demutualization, Self-regulation andConflicts of Interest

Issues

• Management will be too preoccupied with profits and business

• Duplicative costs of creating multiple SROs

• If for-profit exchange enters into new businesses, it increases itsopportunities for conflict

Response from DEs• Divided their business from their regulatory branch ensuring

independence of SROs

• Mechanisms to ensure sufficient disclosure by the SRO of theirregulatory duties

• Limits on the level of ownership of the exchange

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 21/29

DEMUTUALIZATION OFINDIAN STOCK EXCHANGES

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 22/29

Demutualization of Indian Stock Exchanges

• Stock exchanges formed as association of stock brokers

• Mutual organizations managed within a single city with ahuge dealer population

• Registered as section 25 companies

• Exchanges required funds only the extent of meeting itsexpenses

• Any surplus made by the exchange resulted in reducedaccess fees for members

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 23/29

SEBI’s Guidelines

• Issued guidelines on 13 November,2006 for investment in stock

exchanges in India

• Under the guidelines, shareholding of trading members has to bebrought down to 49% .This can be done by either-

• Offer for sales by prospectus by existing trading members havingownership shares

• Placement of shares of shareholders having trading rights to suchpersons or institutions as may be shortlisted by the exchange withthe approval of SEBI

• Issue of equity shares on private placement basis by the stock

exchange to any person or group of persons not having trading rightssubject to approval of SEBI

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 24/29

Limitations by SEBI

• No person shall directly or indirectly acquire or hold morethan 5% in the paid up capital

• Foreign investments up to 49% will be allowed inexchanges with a separate cap on FDI of 26% and FII of23%

• No FII shall seek and get representation on the Board of

Directors of stock exchanges

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 25/29

Demutualization of BSE

• Asia’s oldest stock exchange.131 Year old history

• Corporatized on May 19,2005

• Around 51% stake of 790 brokers were offloaded to 21investors(SBI,LIC,AB Group, Singapore Exchange,Deutsche Borse etc.)

• 19 investors have picked up 41% stake

• 10% stake was picked by Singapore Exchange anddeutsche Borse

• Share price of INR 200,• Total capital raised: INR 189 Crore

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 26/29

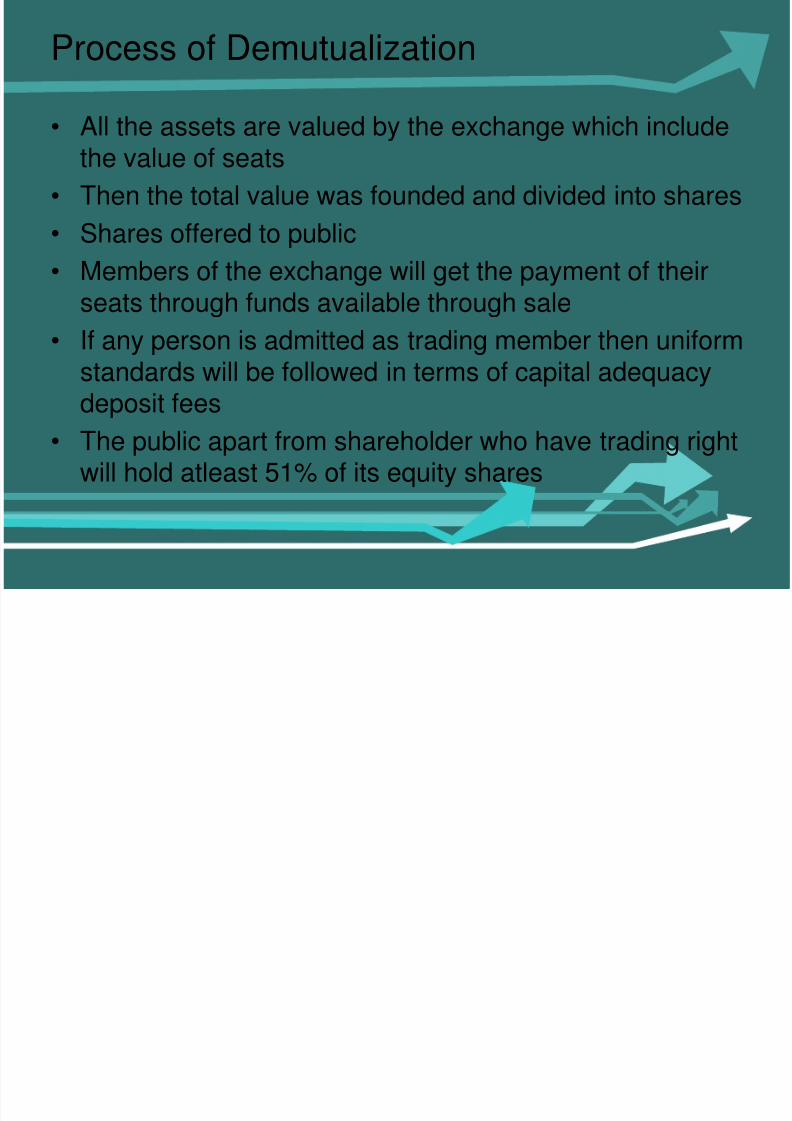

Process of Demutualization

• All the assets are valued by the exchange which includethe value of seats

• Then the total value was founded and divided into shares

• Shares offered to public

• Members of the exchange will get the payment of theirseats through funds available through sale

• If any person is admitted as trading member then uniformstandards will be followed in terms of capital adequacydeposit fees

• The public apart from shareholder who have trading rightwill hold atleast 51% of its equity shares

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 27/29

Demutualization of NSE

• Formed in November 1992 as a tax paying company

• Owned by a set of leading financial institutions i.e.

I. Industrial development Bank of India LimitedII. Industrial Finance corporation of India Limited

III. National Insurance Company Limited

IV. Infrastructure Development finance Company Limited

D t li ti f R i l St k

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 28/29

Demutualization of Regional StockExchanges

• Government asks for demutualization of regional stock exchanges in

2 ways:

Either by trading arms of BSE & NSE

or

No of regional stock exchanges join hands to make a separate platform

• 9 Exchanges recently signed an MOU with NSE to extend its tradingplatform on regional stock exchanges

• Out of 21 stock exchanges ,17 are now demutualized

• Stock exchanges still not demutualized are:

– Coimbatore Stock Exchange – Mangalore Stock Exchange

– Meerut Stock Exchange

– UP Stock Exchange

8/3/2019 Demutualisation of Stock Exchanges

http://slidepdf.com/reader/full/demutualisation-of-stock-exchanges 29/29