Embed Size (px)

Citation preview

Demandware Shopping Index | © 2015 Demandware, Inc. The shopping index is not indicative of Demand-ware’s operational performance or its reported financial metrics including GMV growth and comparable GMV growth. This document contains archival information which should not be considered current and may no longer be accurate. Approved for unlimited distribution.

DemandwareShopping Index2015 Q2

Analyzing the activity of over 200 million shoppers, this report

measures Digital Commerce growth, and the trends and sources

that are driving that growth.

As shoppers evolve their shopping patterns, it is critical for retailers

to change their approach to servicing shoppers and guiding their

experience. More than ever before, that experience must be

seamless across channels and devices.

Demandware Shopping Index

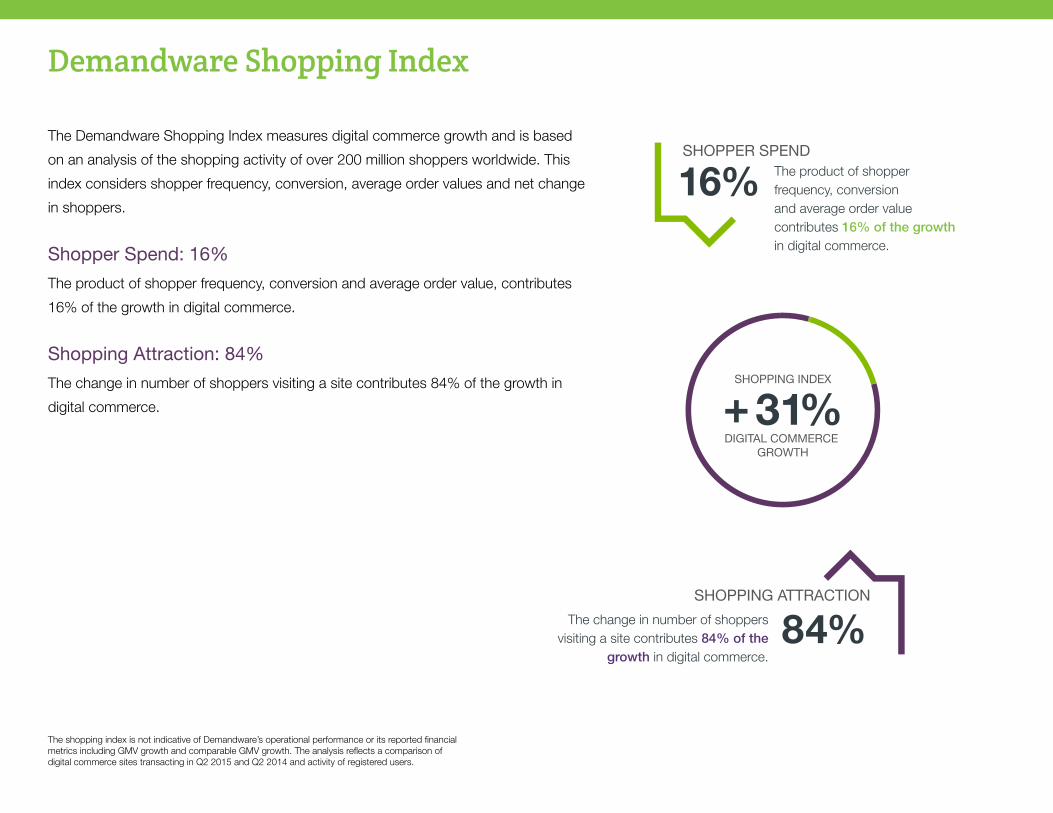

The Demandware Shopping Index measures digital commerce growth and is based

on an analysis of the shopping activity of over 200 million shoppers worldwide. This

index considers shopper frequency, conversion, average order values and net change

in shoppers.

Shopper Spend: 16%

The product of shopper frequency, conversion and average order value, contributes

16% of the growth in digital commerce.

Shopping Attraction: 84%

The change in number of shoppers visiting a site contributes 84% of the growth in

digital commerce.

The shopping index is not indicative of Demandware’s operational performance or its reported financial metrics including GMV growth and comparable GMV growth. The analysis reflects a comparison of digital commerce sites transacting in Q2 2015 and Q2 2014 and activity of registered users.

16%

84%

The product of shopper frequency, conversion and average order value contributes 16% of the growth in digital commerce.

The change in number of shoppers visiting a site contributes 84% of the

growth in digital commerce.

31%

Phones Prosper

The analysis reflects a comparison of digital commerce sites transacting in Q2 2015 and Q2 2014.

Phones are the driving force of digital commerce growth. Shoppers do much more

than browse; they are creating more baskets and ordering more than ever before, right

from the palm of their hand.

In fact, phones accounted for 94% of the year-over-year increase in traffic, 74% of the

increase in basket creation and 47% of the order growth.

What Really Matters

Clearly, the time to employ a mobile-first strategy is here. Retailers that force shoppers

to pinch and zoom through their shopping journey are not only deteriorating their

brand, they are missing a revenue opportunity.

Device Contribution on Digital Commerce Growth Metrics

Phone Tablet and Computer

Visits Baskets Orders

Phones Fuel Growth

Phones are quickly becoming the device of choice for shopping. Here are some of the key metrics on the soon-to-be most popular

shopping device.

The analysis reflects a comparison of digital commerce sites transacting in Q2 2015 and Q2 2014.

THE BATTLE BETWEEN OPERATING SYSTEMS LEVELS OFF

Device Trends

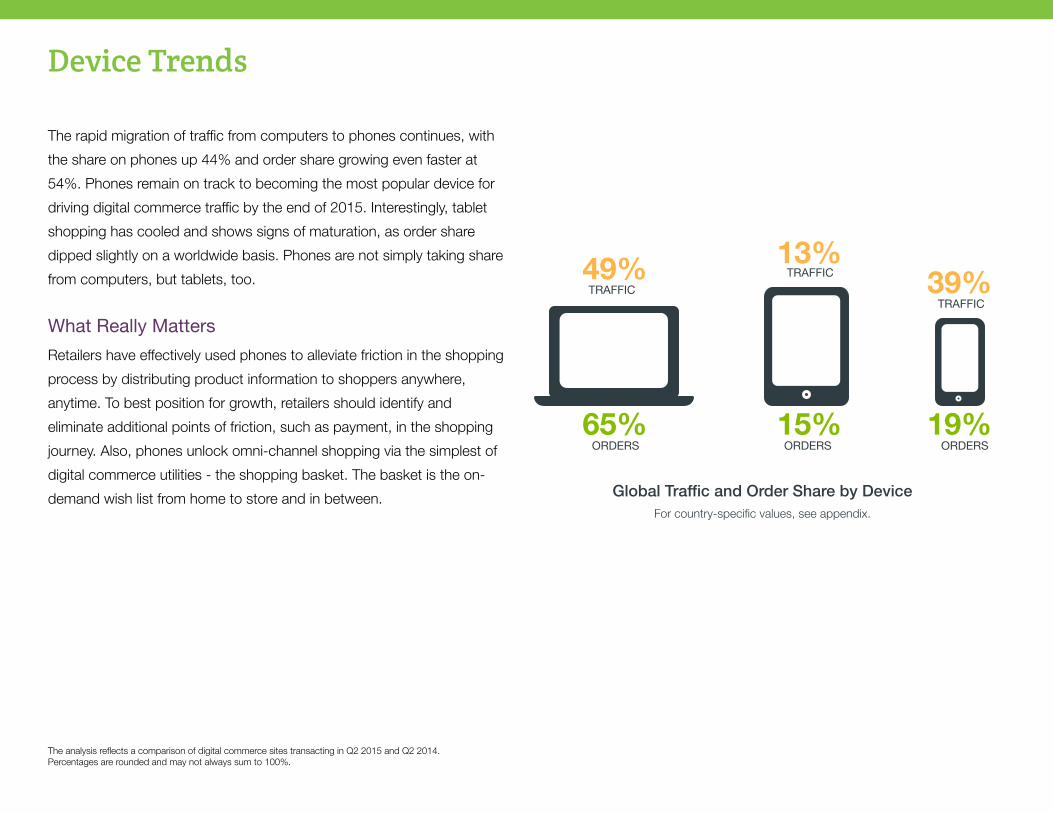

The rapid migration of traffic from computers to phones continues, with

the share on phones up 44% and order share growing even faster at

54%. Phones remain on track to becoming the most popular device for

driving digital commerce traffic by the end of 2015. Interestingly, tablet

shopping has cooled and shows signs of maturation, as order share

dipped slightly on a worldwide basis. Phones are not simply taking share

from computers, but tablets, too.

What Really Matters

Retailers have effectively used phones to alleviate friction in the shopping

process by distributing product information to shoppers anywhere,

anytime. To best position for growth, retailers should identify and

eliminate additional points of friction, such as payment, in the shopping

journey. Also, phones unlock omni-channel shopping via the simplest of

digital commerce utilities - the shopping basket. The basket is the on-

demand wish list from home to store and in between.

The analysis reflects a comparison of digital commerce sites transacting in Q2 2015 and Q2 2014. Percentages are rounded and may not always sum to 100%.

Global Traffic and Order Share by DeviceFor country-specific values, see appendix.

49%

65%

39%

19%

13%

15%

Time on Site

What were once idle moments, waiting for a train, sitting at the doctor’s office

or standing in line, are now filled with digital engagement. People spend

these brief, quiet moments with their phone in their hand and, as a result, we

continue to see a decrease in duration of shopping visits.

What Really Matters

As visit duration falls, it is vital that retailers use their time with shoppers

wisely. In particular, each shopper visit should pick up where the previous

visit left off– this means creating a more connected strategy for cross-

device shopping. Marketing can help get a jump on the shopper journey

by effectively personalizing vehicles like email messages, and ensuring

that landing pages accelerate the journey deep into the shopping and site

experience.

The analysis reflects a comparison of digital commerce sites transacting in Q2 2015 and Q2 2014.

AVERAGE TIME PER VISIT, Q2 2015 (GLOBAL)

AVERAGE TIME PER PHONE VISIT, Q2 2015 (GLOBAL)

9.4 mins, down 28%

8.5 mins, down 37%

For country-specific values, see appendix.

9.4

8.5

28%

37%

Shopping Activity

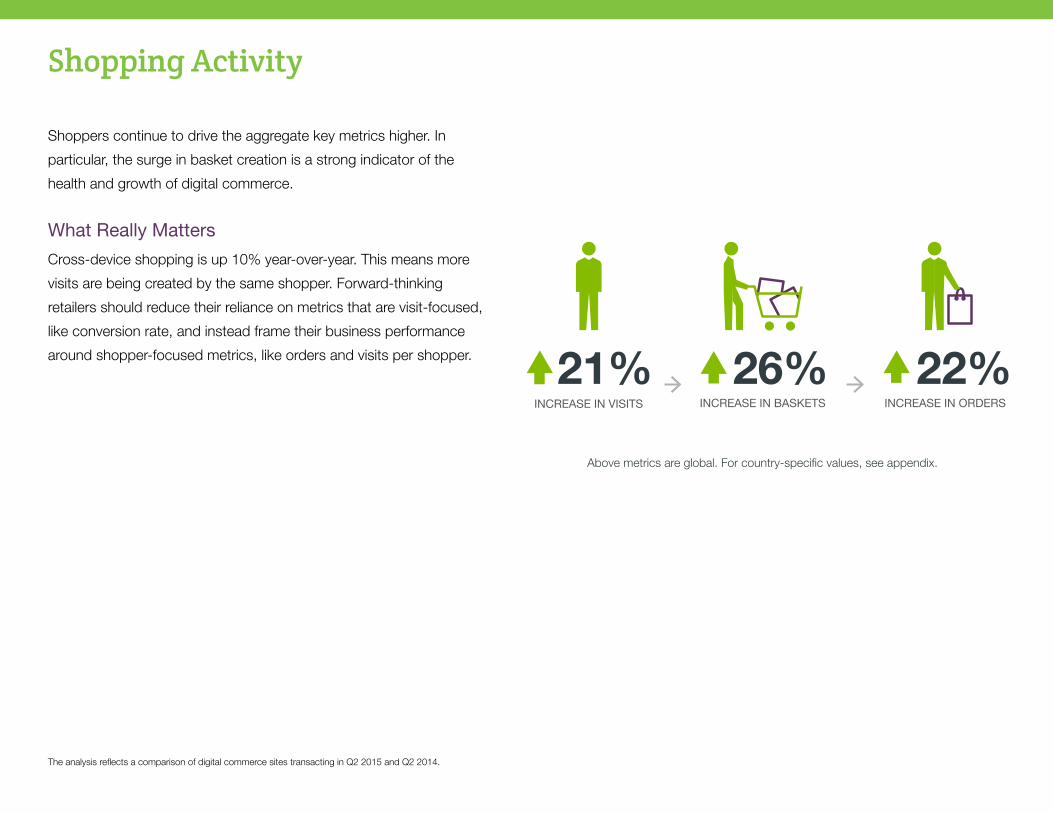

Shoppers continue to drive the aggregate key metrics higher. In

particular, the surge in basket creation is a strong indicator of the

health and growth of digital commerce.

What Really Matters

Cross-device shopping is up 10% year-over-year. This means more

visits are being created by the same shopper. Forward-thinking

retailers should reduce their reliance on metrics that are visit-focused,

like conversion rate, and instead frame their business performance

around shopper-focused metrics, like orders and visits per shopper.

The analysis reflects a comparison of digital commerce sites transacting in Q2 2015 and Q2 2014.

Above metrics are global. For country-specific values, see appendix.

21% 26% 22%

Order Value & Discounts

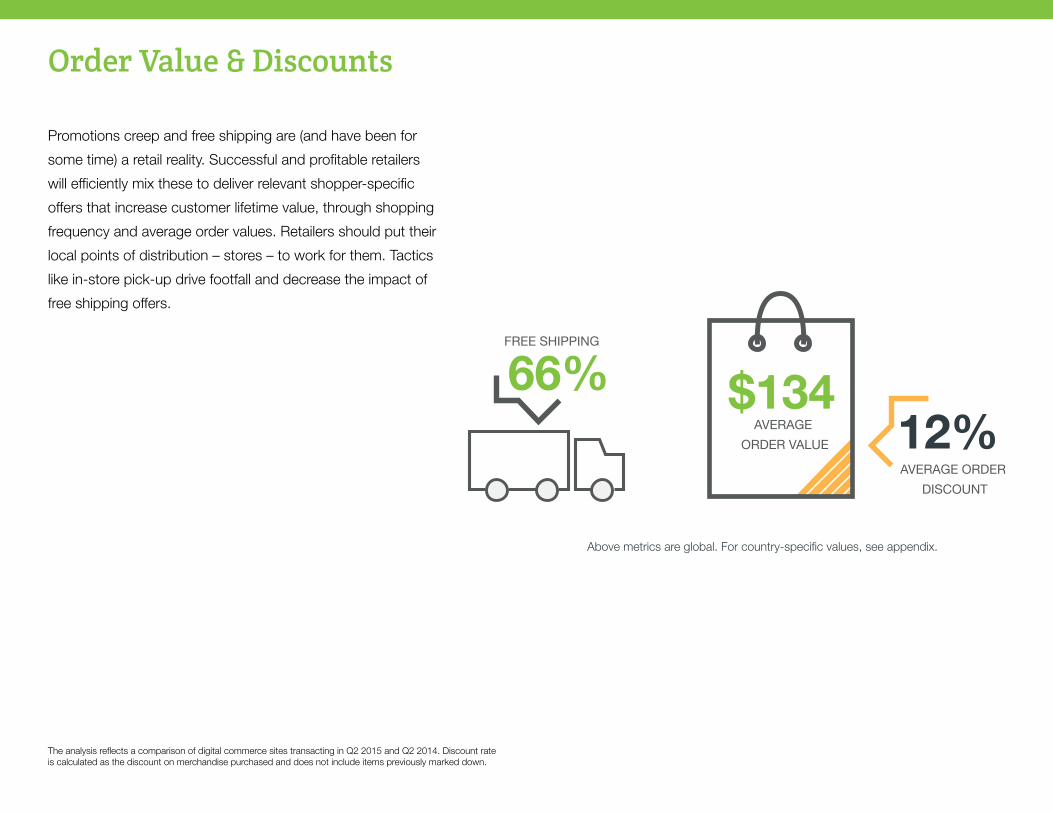

Promotions creep and free shipping are (and have been for

some time) a retail reality. Successful and profitable retailers

will efficiently mix these to deliver relevant shopper-specific

offers that increase customer lifetime value, through shopping

frequency and average order values. Retailers should put their

local points of distribution – stores – to work for them. Tactics

like in-store pick-up drive footfall and decrease the impact of

free shipping offers.

The analysis reflects a comparison of digital commerce sites transacting in Q2 2015 and Q2 2014. Discount rate is calculated as the discount on merchandise purchased and does not include items previously marked down.

Above metrics are global. For country-specific values, see appendix.

66% $13412%

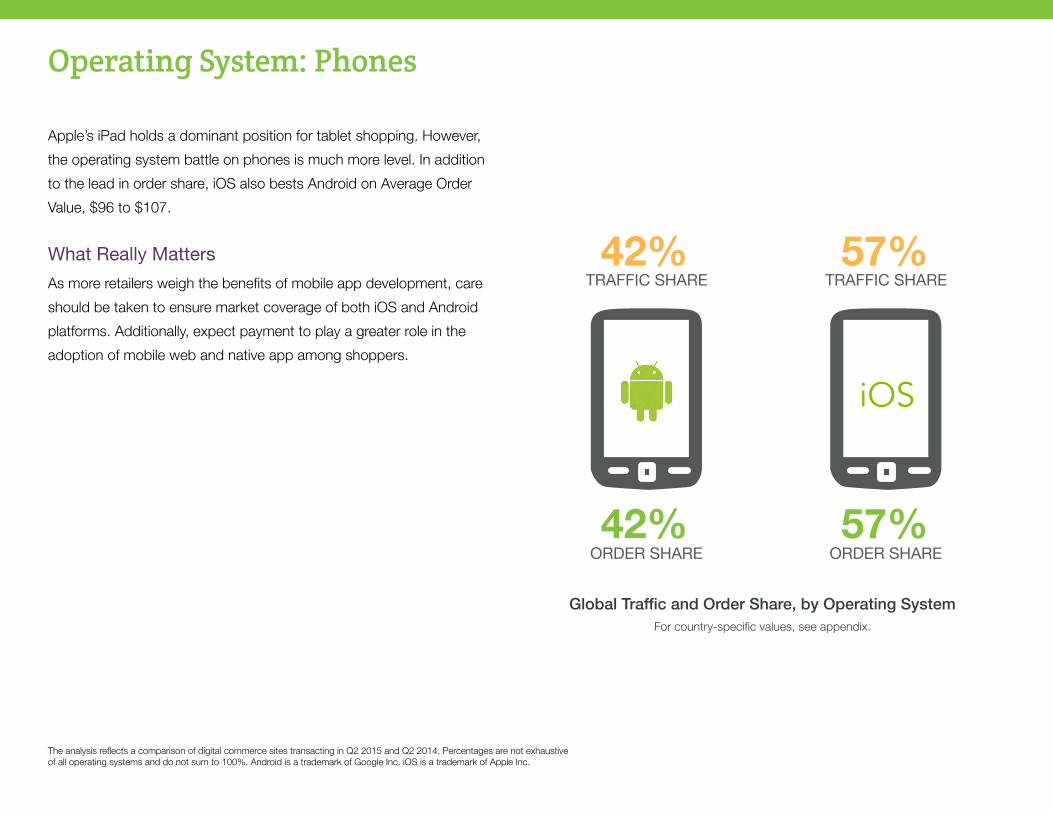

Operating System: Phones

Apple’s iPad holds a dominant position for tablet shopping. However,

the operating system battle on phones is much more level. In addition

to the lead in order share, iOS also bests Android on Average Order

Value, $96 to $107.

What Really Matters

As more retailers weigh the benefits of mobile app development, care

should be taken to ensure market coverage of both iOS and Android

platforms. Additionally, expect payment to play a greater role in the

adoption of mobile web and native app among shoppers.

The analysis reflects a comparison of digital commerce sites transacting in Q2 2015 and Q2 2014. Percentages are not exhaustive of all operating systems and do not sum to 100%. Android is a trademark of Google Inc. iOS is a trademark of Apple Inc.

Global Traffic and Order Share, by Operating SystemFor country-specific values, see appendix.

42%

42%

57%

57%

About the Shopping Index

This comprehensive report analyzes activity of over 200 million

shoppers worldwide to identify trends and opportunities for

retailers to elevate the shopper experience and grow revenue.

The Demandware Shopping Index measures the pace of digital

shopping growth, assigning a numerical value to crucial shopper

metrics.

As a leader in enterprise digital commerce with more than

1,300 global retail sites running on Demandware Commerce

and processing billions of dollars in gross merchandise value,

Demandware is uniquely positioned to offer actionable insights

into shopping behavior.

The Demandware Shopping Index is published quarterly. Data

footnotes are noted inline throughout the report to provide

additional clarity on the analysis.

The Shopping Index is not indicative of Demandware’s

operational performance or its reported financial metrics including

GMV growth and comparable GMV growth.

© 2015 Demandware, Inc. This document contains archival information which should not be considered current and may no longer be accurate. Approved for unlimited distribution.

Appendix

TrafficShare

2015 Q2 2014 Q2 YoY

Country Computer Tablet Phone Computer Tablet PhoneComputer -

YoYTablet -

YoYPhone -

YoY

Global 49% 13% 39% 59% 14% 27% -18% -10% 44%

USA 48% 10% 42% 58% 12% 30% -17% -13% 38%

UK 41% 21% 38% 51% 24% 25% -20% -10% 49%

Germany 57% 13% 31% 66% 14% 20% -14% -6% 51%

France 54% 11% 35% 68% 11% 21% -20% -4% 66%

Canada 49% 17% 34% 59% 16% 24% -18% 3% 41%

Vertical Computer Tablet Phone Computer Tablet PhoneComputer -

YoYTablet -

YoYPhone -

YoY

Active Apparel

52% 9% 39% 64% 10% 26% -18% -11% 48%

General Apparel

49% 12% 39% 61% 13% 27% -19% -6% 47%

Luxury Apparel

49% 12% 39% 56% 16% 28% -12% -25% 38%

Health & Beauty

45% 9% 46% 54% 11% 35% -16% -21% 33%

Home 50% 17% 33% 64% 18% 19% -21% -3% 75%

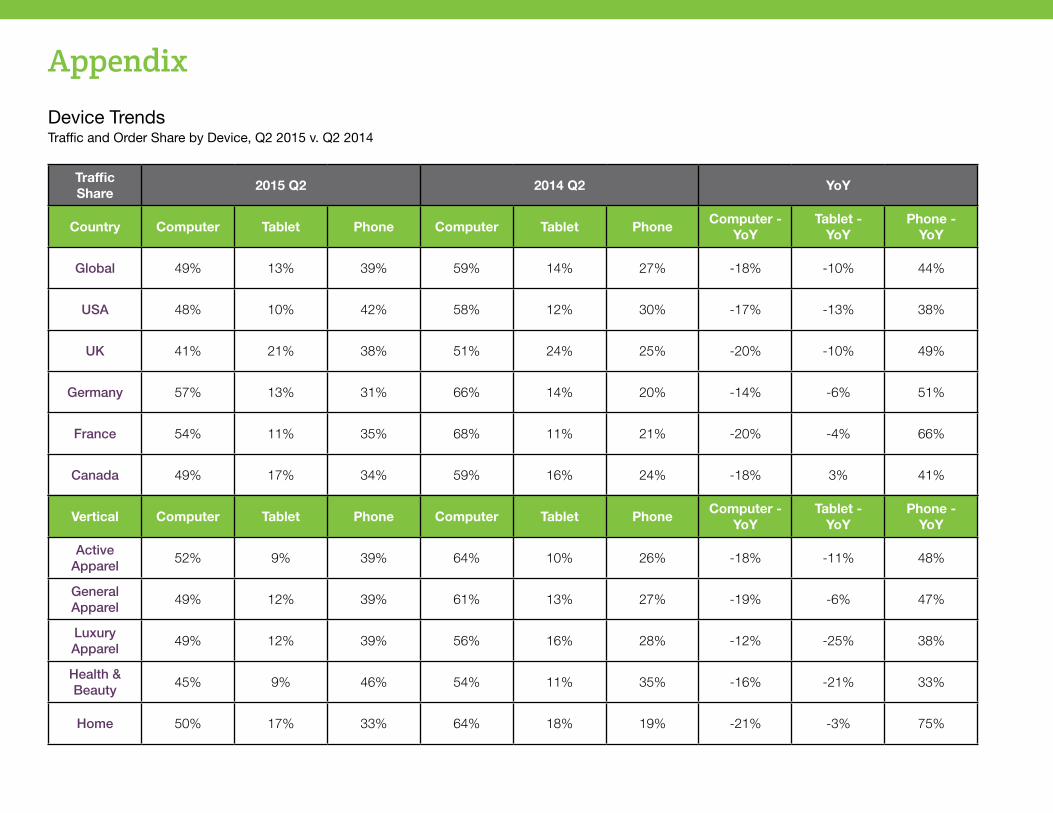

Device TrendsTraffic and Order Share by Device, Q2 2015 v. Q2 2014

Appendix

Order Share

2015 Q2 2014 Q2 YoY

Country Computer Tablet Phone Computer Tablet PhoneComputer -

YoYTablet -

YoYPhone -

YoY

Global 65% 15% 19% 72% 16% 12% -9% -2% 54%

USA 69% 12% 19% 74% 13% 12% -7% -8% 50%

UK 51% 24% 25% 59% 23% 18% -14% 1% 45%

Germany 72% 14% 14% 79% 13% 8% -8% 3% 73%

France 75% 11% 14% 80% 12% 8% -7% -5% 75%

Canada 68% 17% 15% 75% 16% 9% -9% 1% 71%

Vertical Computer Tablet Phone Computer Tablet PhoneComputer -

YoYTablet -

YoYPhone -

YoY

Active Apparel

70% 11% 18% 77% 12% 10% -9% -9% 76%

General Apparel

67% 15% 18% 73% 15% 12% -9% -2% 57%

Luxury Apparel

66% 15% 19% 71% 18% 11% -7% -15% 65%

Health & Beauty

71% 12% 17% 76% 14% 11% -6% -12% 54%

Home 59% 18% 23% 66% 17% 16% -11% 3% 41%

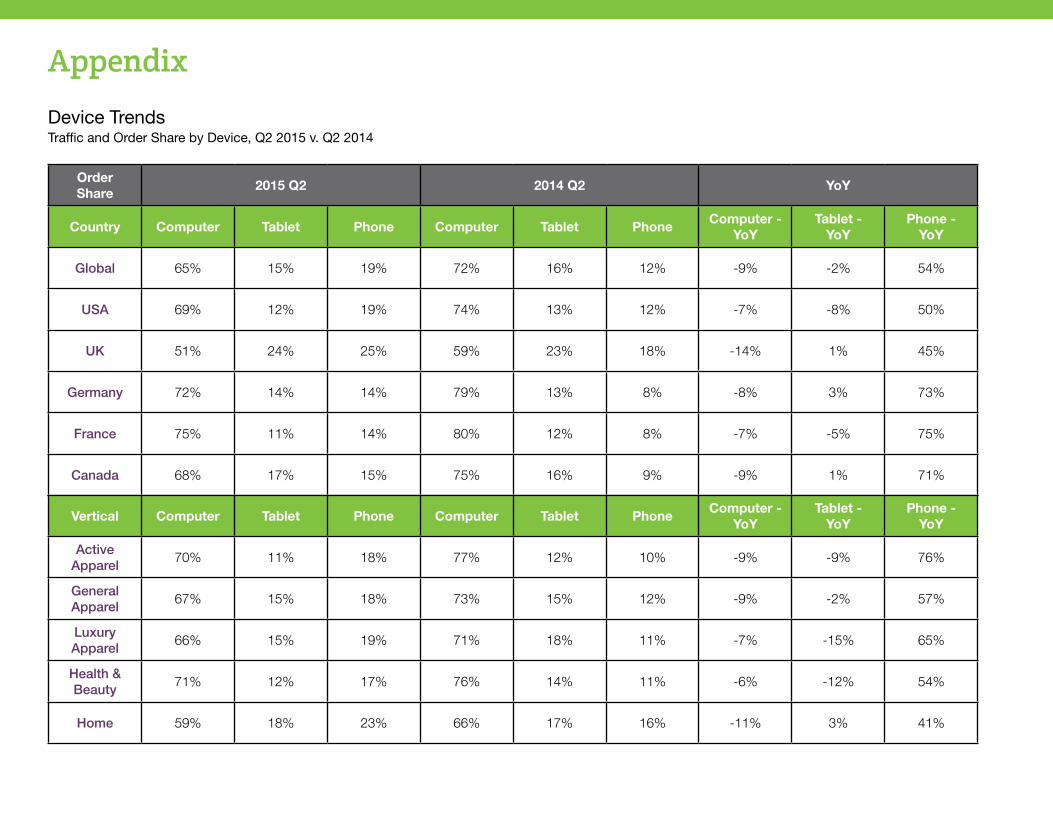

Device TrendsTraffic and Order Share by Device, Q2 2015 v. Q2 2014

Appendix

Time on Site, by deviceVisit Duration in Minutes, Q2 2015 v. Q2 2014

Country 2015 Q2 2014 Q2 YoY 2015 Q2 2014 Q2 YoY 2015 Q2 2014 Q2 YoY

Global 9.8 12.7 -23% 10.3 13.8 -25% 8.5 13.4 -37%

USA 9.3 13.4 -31% 9.9 13.0 -24% 8.5 13.5 -37%

UK 11.3 13.5 -16% 11.7 16.4 -29% 8.4 13.8 -39%

Germany 10.0 10.1 -1% 9.6 11.2 -14% 8.5 11.8 -28%

France 8.5 9.6 -11% 9.0 12.8 -30% 7.4 12.0 -38%

Canada 9.7 10.6 -8% 8.2 11.0 -25% 7.8 11.5 -32%

Vertical 2015 Q2 2014 Q2 YoY 2015 Q2 2014 Q2 YoY 2015 Q2 2014 Q2 YoY

Active Apparel

11.0 12.9 -15% 10.7 14.4 -26% 8.7 13.3 -35%

General Apparel

10.2 13.2 -23% 10.2 13.2 -23% 9.2 13.8 -33%

Luxury Apparel

8.7 12.5 -30% 10.0 14.7 -32% 7.9 13.3 -41%

Health & Beauty

7.6 9.9 -23% 8.3 11.5 -28% 6.7 10.7 -37%

Home 10.2 13.3 -23% 10.0 13.0 -23% 8.7 12.8 -32%

Appendix

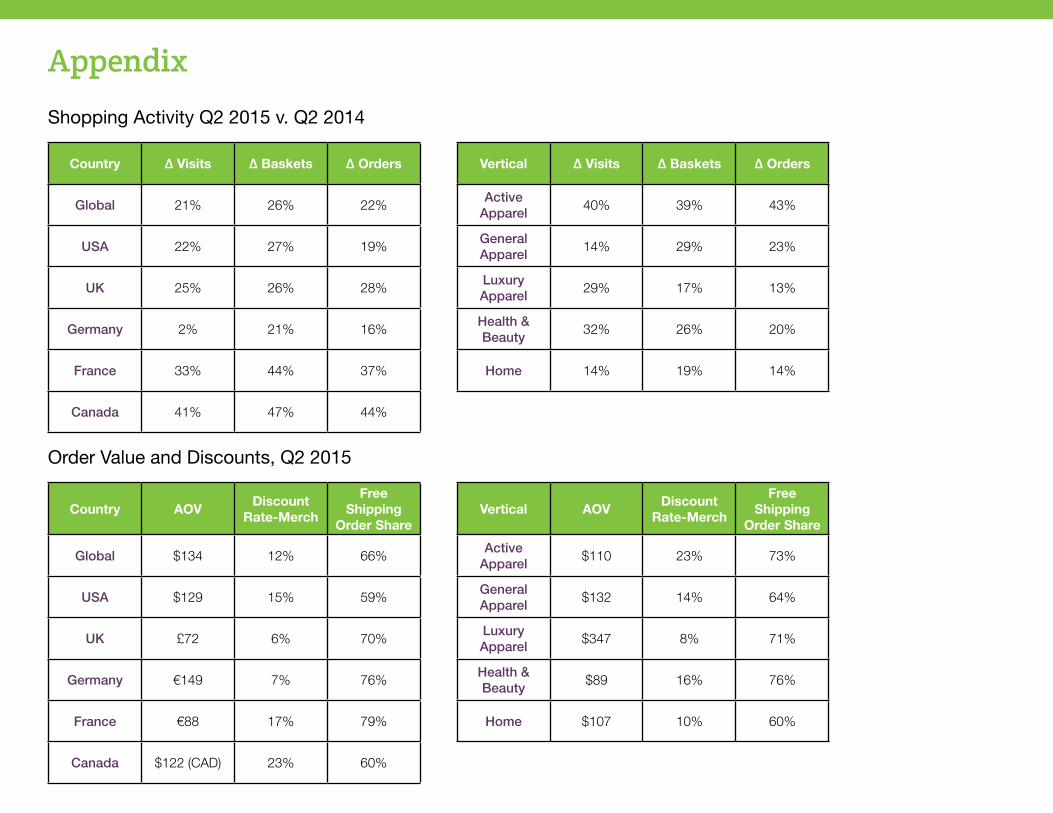

Shopping Activity Q2 2015 v. Q2 2014

Order Value and Discounts, Q2 2015

Country ∆ Visits ∆ Baskets ∆ Orders

Global 21% 26% 22%

USA 22% 27% 19%

UK 25% 26% 28%

Germany 2% 21% 16%

France 33% 44% 37%

Canada 41% 47% 44%

Country AOVDiscount

Rate-Merch

Free Shipping

Order Share

Global $134 12% 66%

USA $129 15% 59%

UK £72 6% 70%

Germany €149 7% 76%

France €88 17% 79%

Canada $122 (CAD) 23% 60%

Vertical ∆ Visits ∆ Baskets ∆ Orders

Active Apparel

40% 39% 43%

General Apparel

14% 29% 23%

Luxury Apparel

29% 17% 13%

Health & Beauty

32% 26% 20%

Home 14% 19% 14%

Vertical AOVDiscount

Rate-Merch

Free Shipping

Order Share

Active Apparel

$110 23% 73%

General Apparel

$132 14% 64%

Luxury Apparel

$347 8% 71%

Health & Beauty

$89 16% 76%

Home $107 10% 60%

Appendix

TrafficShare

2015 Q2 2014 Q2 YoY

Country Android iOS Android iOSAndroid -

YoYiOS - YoY

Global 42% 57% 44% 56% -3% 3%

USA 39% 61% 41% 59% -5% 4%

UK 39% 60% 38% 60% 2% 0%

Germany 58% 42% 60% 40% -3% 5%

France 48% 52% 52% 47% -8% 10%

Canada 36% 64% 33% 66% 9% -3%

Vertical Android iOS Android iOSAndroid -

YoYiOS - YoY

Active Apparel

49% 50% 54% 45% -9% 12%

General Apparel

42% 58% 43% 56% -3% 2%

Luxury Apparel

25% 75% 26% 74% -4% 2%

Health & Beauty

41% 59% 43% 56% -5% 4%

Home 45% 55% 42% 58% 8% -5%

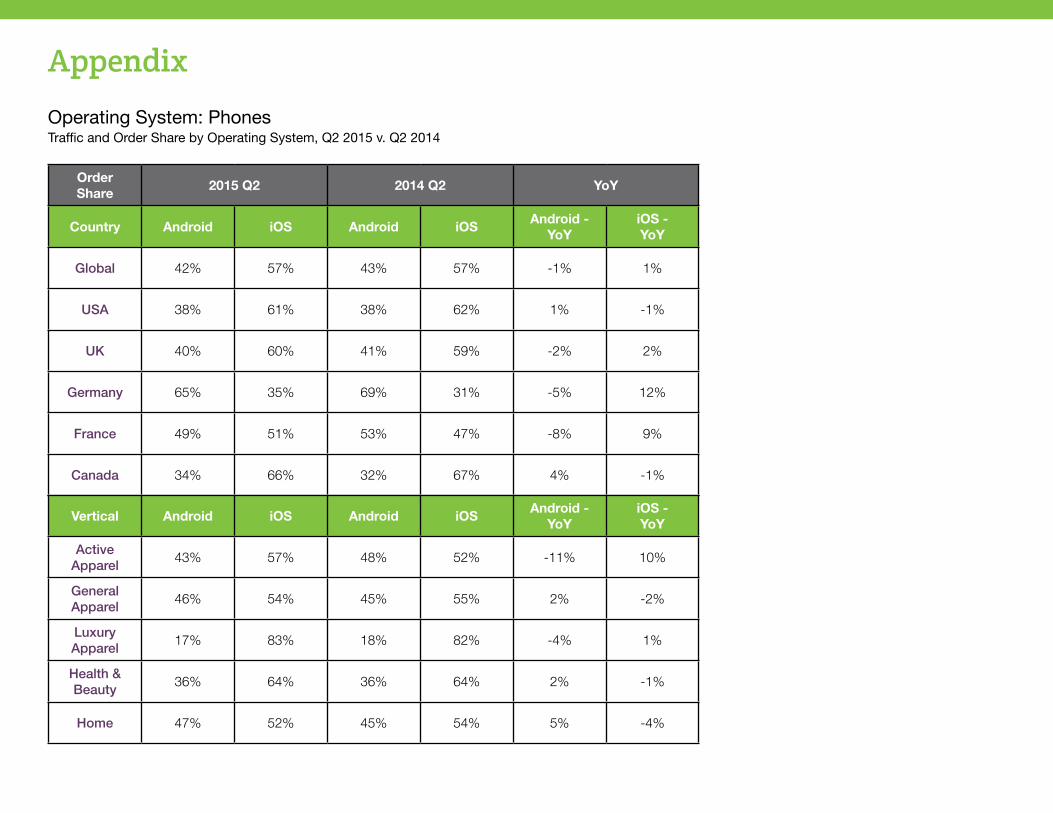

Operating System: PhonesTraffic and Order Share by Operating System, Q2 2015 v. Q2 2014

Appendix

Order Share

2015 Q2 2014 Q2 YoY

Country Android iOS Android iOSAndroid -

YoYiOS - YoY

Global 42% 57% 43% 57% -1% 1%

USA 38% 61% 38% 62% 1% -1%

UK 40% 60% 41% 59% -2% 2%

Germany 65% 35% 69% 31% -5% 12%

France 49% 51% 53% 47% -8% 9%

Canada 34% 66% 32% 67% 4% -1%

Vertical Android iOS Android iOSAndroid -

YoYiOS - YoY

Active Apparel

43% 57% 48% 52% -11% 10%

General Apparel

46% 54% 45% 55% 2% -2%

Luxury Apparel

17% 83% 18% 82% -4% 1%

Health & Beauty

36% 64% 36% 64% 2% -1%

Home 47% 52% 45% 54% 5% -4%

Operating System: PhonesTraffic and Order Share by Operating System, Q2 2015 v. Q2 2014

![INDEX [ptgmedia.pearsoncmg.com] · 2009-06-09 · Index 735 resources for, 714–715 SHOPPING CHART (F3), 369–376 Beliefnet conferences available through, 125 sidebar use on, 525](https://img.pdfslide.us/doc/110x75/5f0c81127e708231d435bbe8/index-2009-06-09-index-735-resources-for-714a715-shopping-chart-f3-369a376.jpg)