Embed Size (px)

Citation preview

DEMAND, SUPPLY, MARKET EQUILIBRIUM TRUE OR FALSE STATEMENTS 1. In a market in the state of oversupply the equilibrium will be established by an

increase in the actual price. 2. After levying consumption tax on the product, the consumer surplus will increase. 3. If the consumption tax on a product increases, its price will increase. That’s why

the supply will increase as well. 4. If the government subsidizes a product, the demand curve will shift to the right. PROBLEMS / EXERCISES 1. To encourage the broader use of public transport the local government plans to subsidize the purchase of season tickets. It aims to increase the demand by 10 percent on constant prices. The equation of the demand curve for season tickets is: Q=120.000-20p, the equation of the supply curve of seasons tickets is: Q=30p-80.000.

a) Determine the price and the quantity of the season tickets sold as well as the sum of the subsidy needed to achieve this goal!

b) Determine the new curves of demand and supply! c) Make a schedule of the market!

2, The equations of the demand and the supply curves in the market of potatoes are as follows: D=300-5p; S=10p-150.

a) Calculate the consumers’ surplus in case of market equilibrium! b) The state maximises the prise of the potatoes in 25 HUF. Calculate the market

equilibrium after this action! c) Determine the sum the state would have to pay (in terms of subsidies for

production) if the government to would like to give incentives for the producers to produce the demanded quantity of potatoes at the set maximal price!

d) Is the maximised price beneficial for the consumers, if the subsidy paid to the producers was financed from consumers’ tax payments?

3, The market of pumpkins can be characterised by the following curves: D=1500-5p, S=3p-500. After strong advertising (about the vitamin content of the product) the demand increased by 20 percent by constant prices.

a) Determine the new demand curve! b) Calculate the consumers’ surplus at the original situation and after the

demand has changed! c) Illustrate the market of the product!

4, We know the inverse demand and supply curves in the market of potatoes: P=300-1,5Q P=Q+50. The state decided to decrease the production by 40 percent with levying a tax.

a) Calculate the equilibrium price and quantity before levying the tax! b) Show the changes in the potato market after introducing the tax and calculate

the new price! c) How large is the tax and how much revenue the government can raise by the

introduction of this tax? d) Illustrate the changes in a frame of reference!

5, The market demand of strip leaves is: Q=1500-20p, and the supply is: Q=30p-500. The state aims to decrease the quantity by 10 percent for the sake of health promotion that is why it levies a tax on production.

a) Determine the amount of tax necessary to decrease the consumption by 10 percent!

b) Determine the equations of the new demand and supply curves, if the demand reacts on the new supply!

c) Calculate the resulted change in the consumer surplus!

6, The market of skates can be characterised with the following curves: D=1500-20p and S=30p-500. To foster the sport activity of young people, the local government wants to increase the sold quantity by 10 percent.

a) How large support do the parents and the sellers require if the price doesn’t change?

b) Determine the new demand and supply curves! c) Calculate the resulted change in the consumer surplus!

SOLUTIONS

1. a)p*=4.000; Q*=40.000; Q’=48.000 Consumer support: 32.000.000 Producer support: 12.800.000

b)D’=128.000-20p

2. a) Ft=2250 b) p=25; D=175; S=100; D>S excess demand c) support 7,5 Ft/kg , altogether 1312,5 Ft d) change in consumer surplus: ΔFt=812,5 Ft, support 1312,5, negative effect on

consumers

3. a) p*=250; Q*=250, Q’=300; D’=1550-5p b) Ft0=6.250; ΔFt=2.750 4. a) p*=150 and Q*=100

b) Q’=60; S’=p+150; p=210. c) tax 100 Ft/kg, government revenue 6000 Ft

5. a) tax 5,9 Ft/unit b) D doesn’t change; S’=30p-675 c) ΔFt=2327,5 6. a) p*=40; Q*=700; Q’=770; consumer support 2800; producer support 1771. b) D’=1570-20p; S’=30p-430 c) ΔFt=2.572,5

MARKET DEMAND TRUE OR FALSE STATEMENTS 1. The aggregate demand function is the vertical sum of the individual demand

curves. 2. The slope of the market demand curve of two consumers who have the same

individual demand equals the slope of their individual demand curves. PROBLEMS / EXERCISES 1, A rent-a-car company has three consumers: Kate, Sophie and Peter. Their individual demands are the following: Kate: q1=40-p Sophie: q2=60-p Peter: q3=30-0,5p

a) Illustrate the individual demand curves! b) Determine the market demand curve!

2, The individual demands of a product are the following: d1: p=10-0,1q d2: p=12-0,2q d3: p=20-0,2q d4: p=15-0,125q

a) Determine the market demand curve! b) The equation of the supply curve in the examined sector is S: Q=12P-15.

Determine the consumers’ surplus!

3, The consumers in the market of apple can be divided into three groups, their individual demand equations are give per person. Into the first group belong 20 people, their individual demand is: q=10-0,2p. The second group consists of 15 consumers, the individual demand is: q=20-0,4p. There are 5 people in the third group, whose individual demand equation is q=18-0,5p per person.

a) Determine the market demand equation! b) How will the market demand change if another (4th) group of 10 consumers

appears in the market with an inverse demand curve, p=60-5q per person? c) Calculate the equilibrium price and quantity in both cases if the market’s

supply is S: Q=140+2,5P?

4,The individual demand functions of three consumers in the banana market are: q1=100-2p; q2=180-5p; q3=200-4p.

e) Determine the market demand curve! f) How will the demand curve change if there is a 4th consumer in the market

whose inverse individual demand is: p=60-0,5p. g) Illustrate the demand curves!

5,Consumers of a product are divided into 2 groups. There are 50-50 people in both groups. People in the same group have the same equations of demand which are the following: d1: q=10-0,5p d2: q=5-0,3p. The supply in the examined sector is: S:Q=10P+200.

a) Calculate the consumers’ surplus! b) The demand increases by 10%, while the prices didn’t change. Determine the

new supply curve and the change of the consumers’ surplus if the supply adapts to the increased demand!

6, We know the individual demand curves of the 3 consumers of the jet-ski shop called Speedy Ltd. q1=90-p q2=120-3p q3=60-2p

a) Illustrate the market! b) Determine the market demand curve! c) How much is the market demand if the Ltd has the following supply curve:

S=-20+2p. Also determine the consumers’ surplus!

SOLUTIONS

1. If 40<P<60, D=90-1,5P. If P<40, D=130-2,5P. 2. a) If ≤10 D=380-28p; if 10<p≤12, D=280-18p; ha 12<p≤15, D=220-13p; if

15<p≤20, D=100-5p; if p>20, D=0. b) Consumers’ surplus=372,72.

3. a) If 36<P≤50, D=500-10P. If P≤36, D=590-12,5P

b) The market demand in case of 4 groups: If 50<P≤60, D=120-2P. If 36<P≤50, D=620-12P. If P≤36, D=710-14,5P c) Equilibrium: P=33,3, Q=223,8.

4. a) If p≥50, D=0, if 36≤p<50 D=300-6p, if p<36 D=480-11p

b) If 50<P≤60, D=120-2P. If 36<P≤50, D=420-8P. If P≤36, D=600-13P. 5. a) If 16,6<P≤20, D=500-25P. If P≤16,6, D=750-40P. Equilibrium: P=11, Q=310.

Consumers’ surplus: 1238,68 b) Q’=341, S’=10p+231

6. b) If P≤30, D=270-6p; if 30<P≤40, D=210-4p, if 40<P≤90, D=90-p; if p>90, D=0

c) Q*=56,6, Consumers’ Surplus=1338,8

OPTIMAL CHOICE OF THE CONSUMERS TRUE OR FALSE STATEMENTS

1. The consumer spends his income optimally, if the MRS equals the rate of the marginal utility.

2. The MRS shows the slope of the budget line. 3. At the optimum point of consumption the slope of the budget line equals the ratio

of prices. 4. If the price of a product is increases, while the income of the consumer does not

change, the optimum of consumption will stay unvaried.

5. In case of a linear indifference curve, the point of optimal consumption can’t be determined.

6. The hypothesis of the diminishing marginal utilities means, when the consumption is decreased we sacrifice less and less utility.

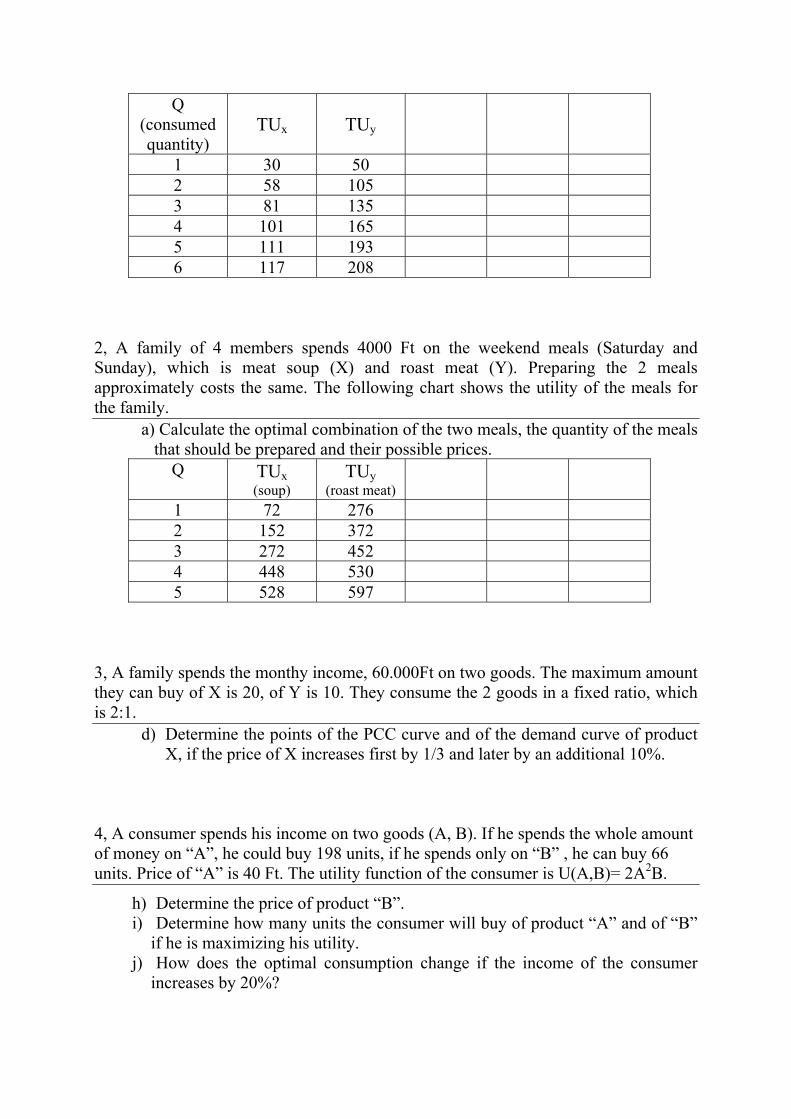

PROBLEMS / EXERCISES 1, A family spends the monthly income, 3400 Ft, on two goods: X and Y. The price of Y is 1,5 times higher than price of X. Determine the optimal consumption of the two goods according to the information given in the chart. The family members are on a diet, so they can take a maximum of 1700 calories. One unit of X gives 200 calories, while one unit of Y contains 300 calories.

a) Determine the optimal consumption of the two goods. b) Determine the prices of the goods.

Q (consumed quantity)

TUx TUy

1 30 50 2 58 105 3 81 135 4 101 165 5 111 193 6 117 208

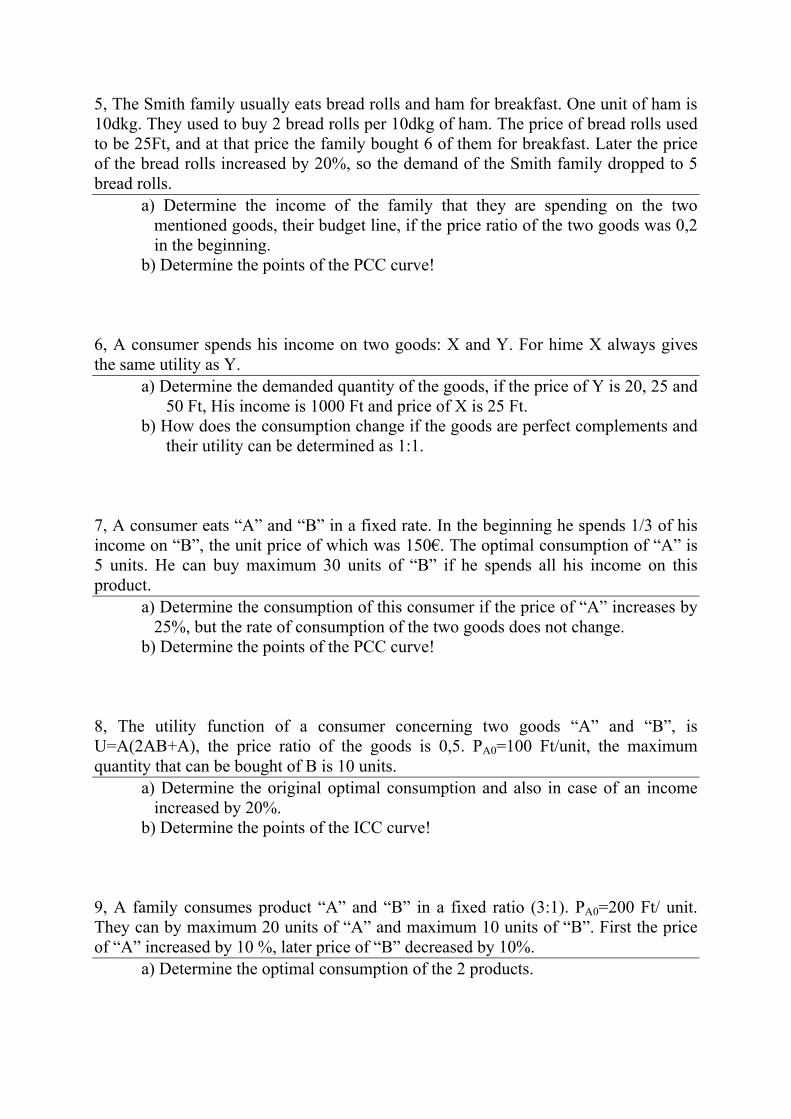

2, A family of 4 members spends 4000 Ft on the weekend meals (Saturday and Sunday), which is meat soup (X) and roast meat (Y). Preparing the 2 meals approximately costs the same. The following chart shows the utility of the meals for the family.

a) Calculate the optimal combination of the two meals, the quantity of the meals that should be prepared and their possible prices.

Q

TUx (soup)

TUy (roast meat)

1 72 276 2 152 372 3 272 452 4 448 530 5 528 597

3, A family spends the monthy income, 60.000Ft on two goods. The maximum amount they can buy of X is 20, of Y is 10. They consume the 2 goods in a fixed ratio, which is 2:1.

d) Determine the points of the PCC curve and of the demand curve of product X, if the price of X increases first by 1/3 and later by an additional 10%.

4, A consumer spends his income on two goods (A, B). If he spends the whole amount of money on “A”, he could buy 198 units, if he spends only on “B” , he can buy 66 units. Price of “A” is 40 Ft. The utility function of the consumer is U(A,B)= 2A2B.

h) Determine the price of product “B”. i) Determine how many units the consumer will buy of product “A” and of “B”

if he is maximizing his utility. j) How does the optimal consumption change if the income of the consumer

increases by 20%?

5, The Smith family usually eats bread rolls and ham for breakfast. One unit of ham is 10dkg. They used to buy 2 bread rolls per 10dkg of ham. The price of bread rolls used to be 25Ft, and at that price the family bought 6 of them for breakfast. Later the price of the bread rolls increased by 20%, so the demand of the Smith family dropped to 5 bread rolls.

a) Determine the income of the family that they are spending on the two mentioned goods, their budget line, if the price ratio of the two goods was 0,2 in the beginning.

b) Determine the points of the PCC curve!

6, A consumer spends his income on two goods: X and Y. For hime X always gives the same utility as Y.

a) Determine the demanded quantity of the goods, if the price of Y is 20, 25 and 50 Ft, His income is 1000 Ft and price of X is 25 Ft.

b) How does the consumption change if the goods are perfect complements and their utility can be determined as 1:1.

7, A consumer eats “A” and “B” in a fixed rate. In the beginning he spends 1/3 of his income on “B”, the unit price of which was 150€. The optimal consumption of “A” is 5 units. He can buy maximum 30 units of “B” if he spends all his income on this product.

a) Determine the consumption of this consumer if the price of “A” increases by 25%, but the rate of consumption of the two goods does not change.

b) Determine the points of the PCC curve! 8, The utility function of a consumer concerning two goods “A” and “B”, is U=A(2AB+A), the price ratio of the goods is 0,5. PA0=100 Ft/unit, the maximum quantity that can be bought of B is 10 units.

a) Determine the original optimal consumption and also in case of an income increased by 20%.

b) Determine the points of the ICC curve! 9, A family consumes product “A” and “B” in a fixed ratio (3:1). PA0=200 Ft/ unit. They can by maximum 20 units of “A” and maximum 10 units of “B”. First the price of “A” increased by 10 %, later price of “B” decreased by 10%.

a) Determine the optimal consumption of the 2 products.

10, Peter spends his money on hamburger (H) and ice cream (C). The price of one hamburger is 50$ and of an ice cream is 25$. The utility function of Peter is U= H*C.

a) Determine the optimal consumption. b) Determine the change in optimal consumption if the state imposes a tax of

20% on the price of hamburger.

SOLUTIONS

1. Px=400; Py=600

2. 2 soups and 3 roast meat, the price is P=200 or 5 soups and 3 roast meat, P=125

3. x0=5 y0=10 x1=8,57 y1=4,28 x2=8,1 y2=4,05

4. PB=120

A0=132 B0=22 A1=158,4 B1=26,4

5. I=525 PCC (6;3) and (5;3)

6. If X and Y has the same utility: at Py=20, he consumes only product Y (50 units) Py=25, any point of the budget line is optimal (consumption is 40 units) Py=50, he consumes only product X (40 units)

If the fixed rate is 1:1 Py=20, x=y=22,2 Py=25, x=y=20 Py=50, x=y=13,3

7. the fixed rate of consumption is B=2A, A=4,29 and B=8,57 the original consumption is B=10 and A=5

8. A0=14 B0=3 A1=16,6 B1=3,66

9. A0=12 B0=4 A1=11,32 B1=3,77 A2=11,76 B2=3,92

10. H0=6 C0=12 H1=5 C1=12

ELASTICITY TRUE OR FALSE STATEMENTS

1. The shorter the reaction time is, the higher the price elasticity of the product is. 2. If y is a complement to product x and price of product x is increasing, the cross-

price elasticity is negative. 3. The income elasticity of luxury goods is constant 4. If the real income of a consumer increases he can decrease consumption of every

goods.

5. The less substitute goods a product has, the more elastic the demand of this product is.

6. If a 2% increase in the price of a product causes less than 2% increase in the demand for it, the demand of this product is non-elastic.

PROBLEMS / EXERCISES 1, In the market of fruits there are 2 types of oranges: Cuban and Spanish orange. The inverse demand curve of the Cuban orange is: p=500-2Q. In January 200 Spanish orange was sold, while the price of the Cuban orange was 250 Ft. In February the price of Cuban orange decreased by 20%, so the sold quantity of the Spanish orangedecreased to 4/5 of January’s quantity.

a) Determine the price elasticity of the Cuban orange and the cross-price elasticity of the 2 types of oranges.

b) What kind of goods are they?

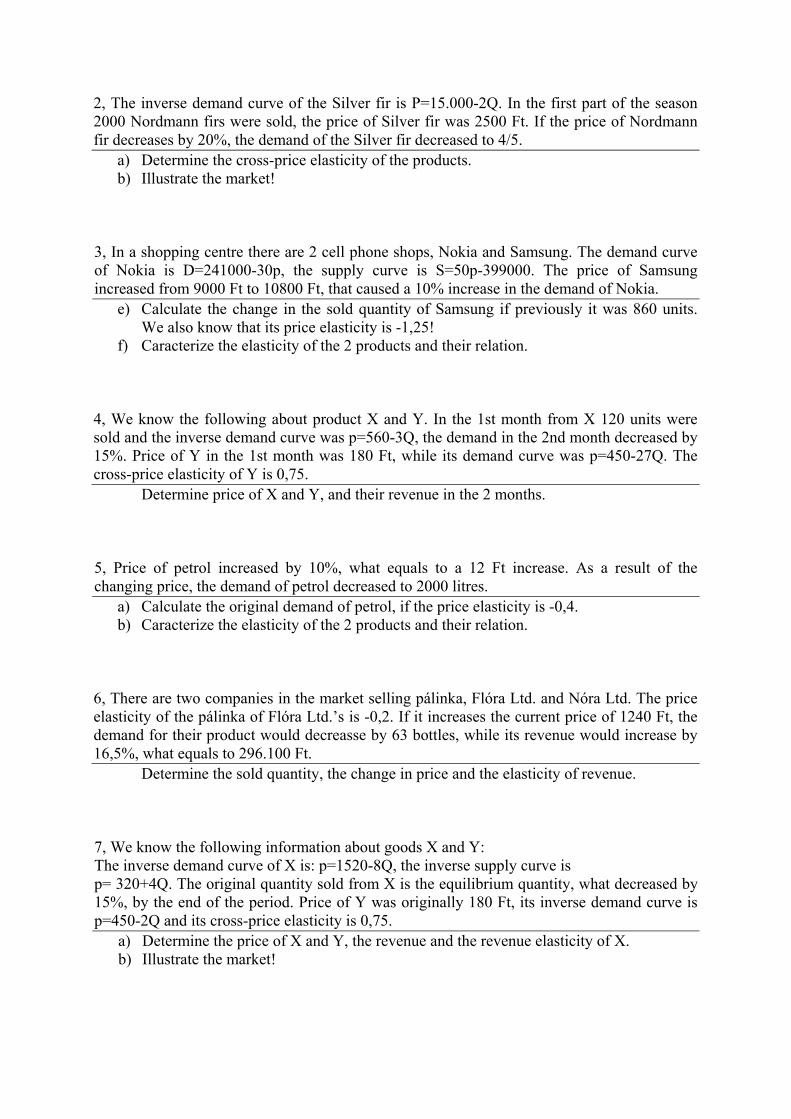

2, The inverse demand curve of the Silver fir is P=15.000-2Q. In the first part of the season 2000 Nordmann firs were sold, the price of Silver fir was 2500 Ft. If the price of Nordmann fir decreases by 20%, the demand of the Silver fir decreased to 4/5.

a) Determine the cross-price elasticity of the products. b) Illustrate the market!

3, In a shopping centre there are 2 cell phone shops, Nokia and Samsung. The demand curve of Nokia is D=241000-30p, the supply curve is S=50p-399000. The price of Samsung increased from 9000 Ft to 10800 Ft, that caused a 10% increase in the demand of Nokia.

e) Calculate the change in the sold quantity of Samsung if previously it was 860 units. We also know that its price elasticity is -1,25!

f) Caracterize the elasticity of the 2 products and their relation.

4, We know the following about product X and Y. In the 1st month from X 120 units were sold and the inverse demand curve was p=560-3Q, the demand in the 2nd month decreased by 15%. Price of Y in the 1st month was 180 Ft, while its demand curve was p=450-27Q. The cross-price elasticity of Y is 0,75.

Determine price of X and Y, and their revenue in the 2 months.

5, Price of petrol increased by 10%, what equals to a 12 Ft increase. As a result of the changing price, the demand of petrol decreased to 2000 litres.

a) Calculate the original demand of petrol, if the price elasticity is -0,4. b) Caracterize the elasticity of the 2 products and their relation.

6, There are two companies in the market selling pálinka, Flóra Ltd. and Nóra Ltd. The price elasticity of the pálinka of Flóra Ltd.’s is -0,2. If it increases the current price of 1240 Ft, the demand for their product would decreasse by 63 bottles, while its revenue would increase by 16,5%, what equals to 296.100 Ft.

Determine the sold quantity, the change in price and the elasticity of revenue. 7, We know the following information about goods X and Y: The inverse demand curve of X is: p=1520-8Q, the inverse supply curve is p= 320+4Q. The original quantity sold from X is the equilibrium quantity, what decreased by 15%, by the end of the period. Price of Y was originally 180 Ft, its inverse demand curve is p=450-2Q and its cross-price elasticity is 0,75.

a) Determine the price of X and Y, the revenue and the revenue elasticity of X. b) Illustrate the market!

SOLUTIONS

1. 1, −=CPCε , 1, =

CPSε . 2. 1, =

NPSε

3. QS1=645. 5,0, =SPNε , so it is a substitute product.

4. Px0=200, Px1=237,5. Py does not change. Qy0=10; Qy1=11,4.

Revenue of product X: 1st month: 24 000 Ft, 2nd month 24 225 Ft Revenue of product Y: 1st month 1 800Ft, 2nd month 2 052 Ft.

5. Q0=2083,33. εTR=0,56. 6. Q0=1447 units. Q1=1384 units. P1=1510 Ft. ε=0,76.

7. Px0=720, Px1=840, Py does not change. Qy0=135, Qy1=151,875. Revenue elasticity of X is: ε=0,049.

8. PP0=40; PP1=65, QR1=2625. S’=300P-12 500. 6,0 ,&−=

PPPε

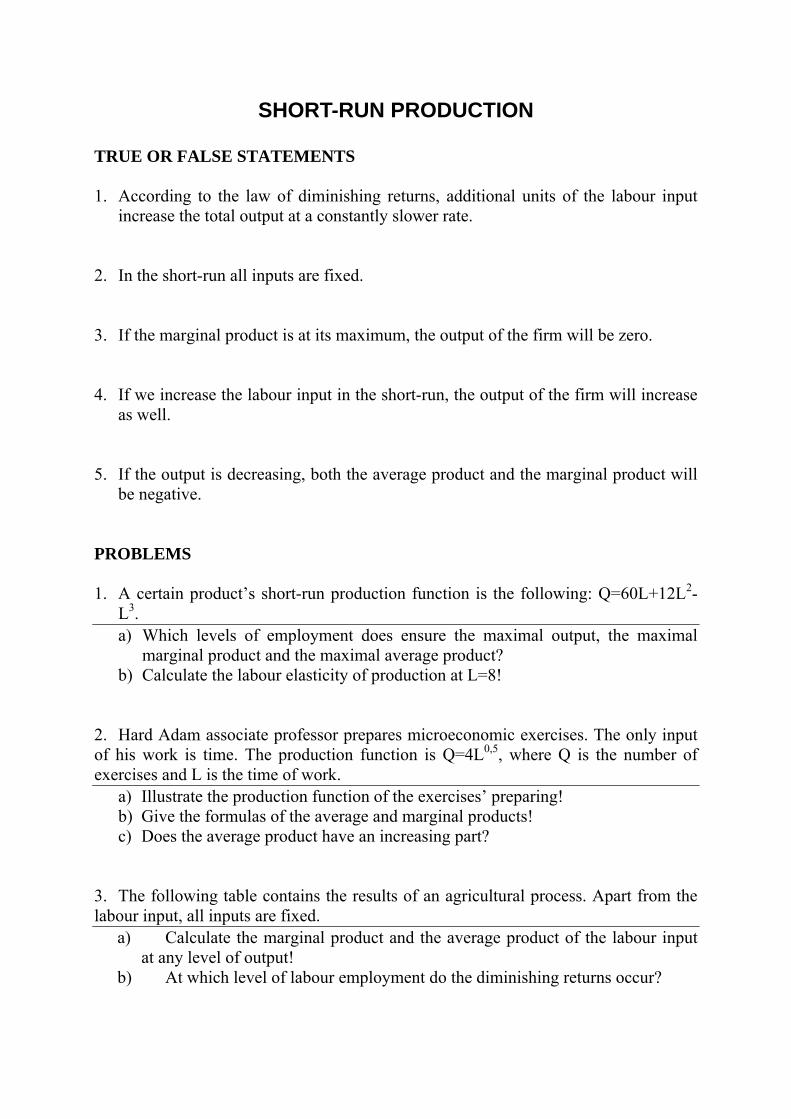

SHORT-RUN PRODUCTION TRUE OR FALSE STATEMENTS 1. According to the law of diminishing returns, additional units of the labour input

increase the total output at a constantly slower rate. 2. In the short-run all inputs are fixed. 3. If the marginal product is at its maximum, the output of the firm will be zero. 4. If we increase the labour input in the short-run, the output of the firm will increase

as well. 5. If the output is decreasing, both the average product and the marginal product will

be negative. PROBLEMS 1. A certain product’s short-run production function is the following: Q=60L+12L2-

L3. a) Which levels of employment does ensure the maximal output, the maximal

marginal product and the maximal average product? b) Calculate the labour elasticity of production at L=8!

2. Hard Adam associate professor prepares microeconomic exercises. The only input of his work is time. The production function is Q=4L0,5, where Q is the number of exercises and L is the time of work.

a) Illustrate the production function of the exercises’ preparing! b) Give the formulas of the average and marginal products! c) Does the average product have an increasing part?

3. The following table contains the results of an agricultural process. Apart from the labour input, all inputs are fixed.

a) Calculate the marginal product and the average product of the labour input at any level of output!

b) At which level of labour employment do the diminishing returns occur?

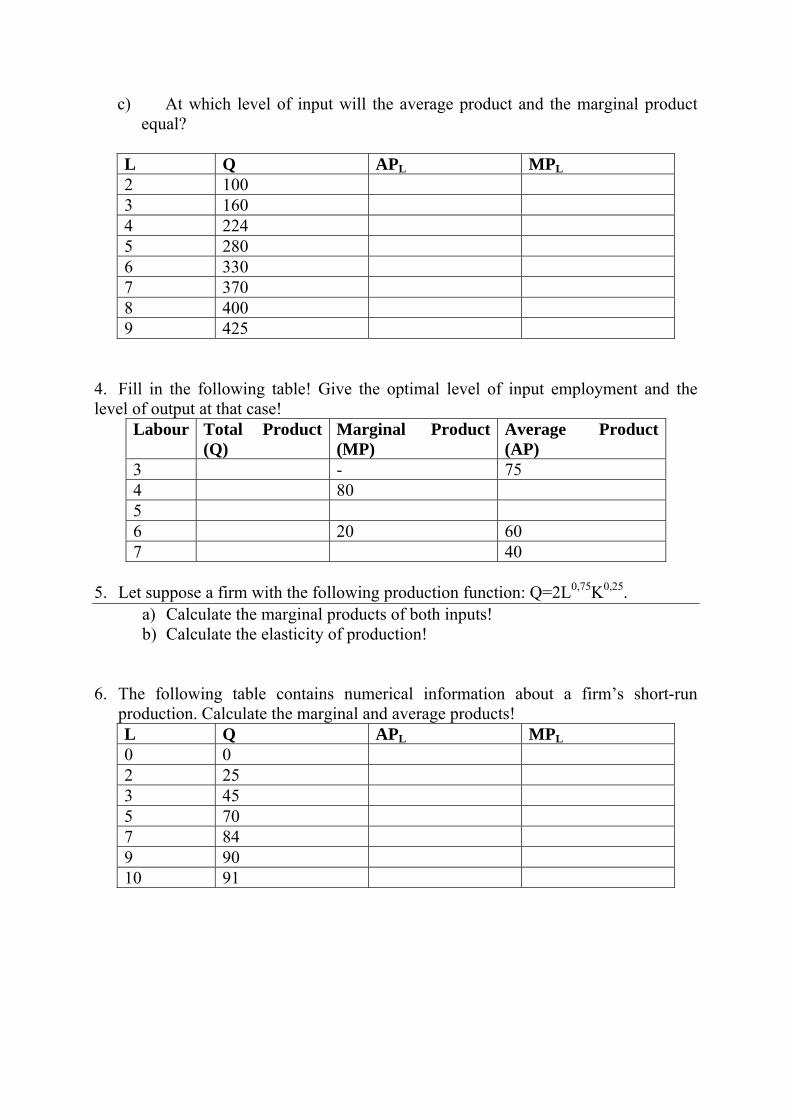

c) At which level of input will the average product and the marginal product equal?

L Q APL MPL 2 100 3 160 4 224 5 280 6 330 7 370 8 400 9 425

4. Fill in the following table! Give the optimal level of input employment and the level of output at that case!

Labour Total Product (Q)

Marginal Product (MP)

Average Product (AP)

3 - 75 4 80 5 6 20 60 7 40

5. Let suppose a firm with the following production function: Q=2L0,75K0,25.

a) Calculate the marginal products of both inputs! b) Calculate the elasticity of production!

6. The following table contains numerical information about a firm’s short-run production. Calculate the marginal and average products! L Q APL MPL 0 0 2 25 3 45 5 70 7 84 9 90 10 91

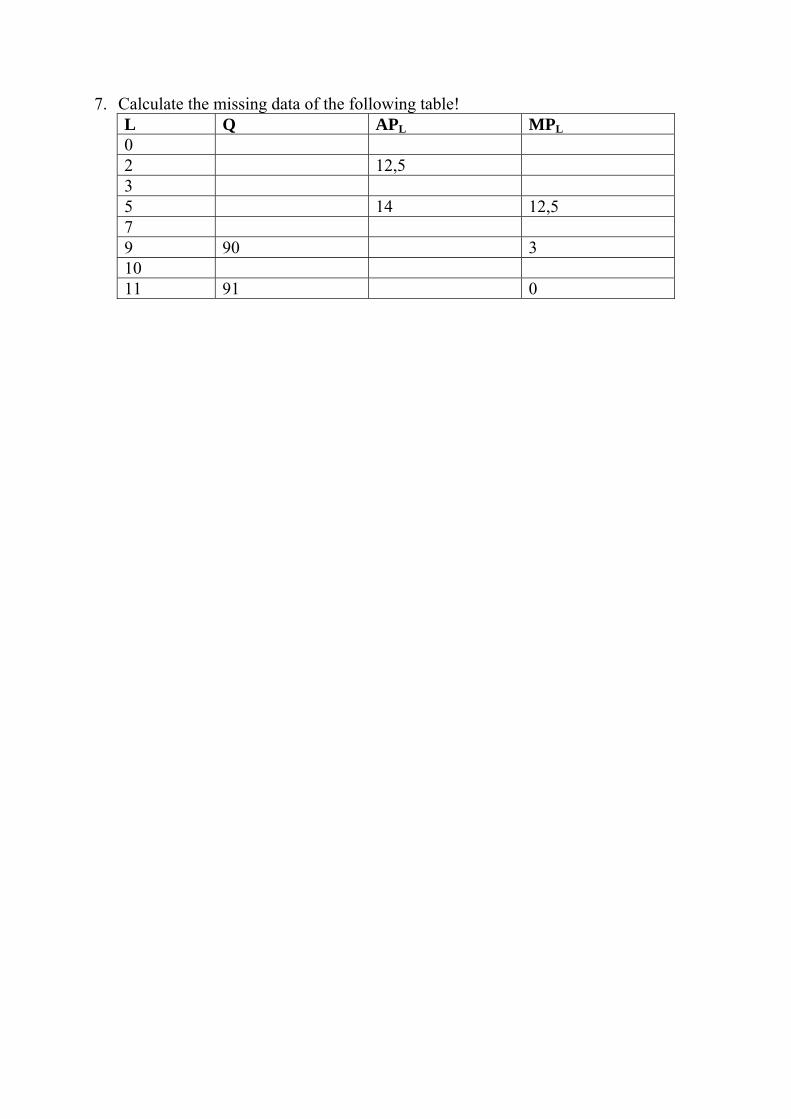

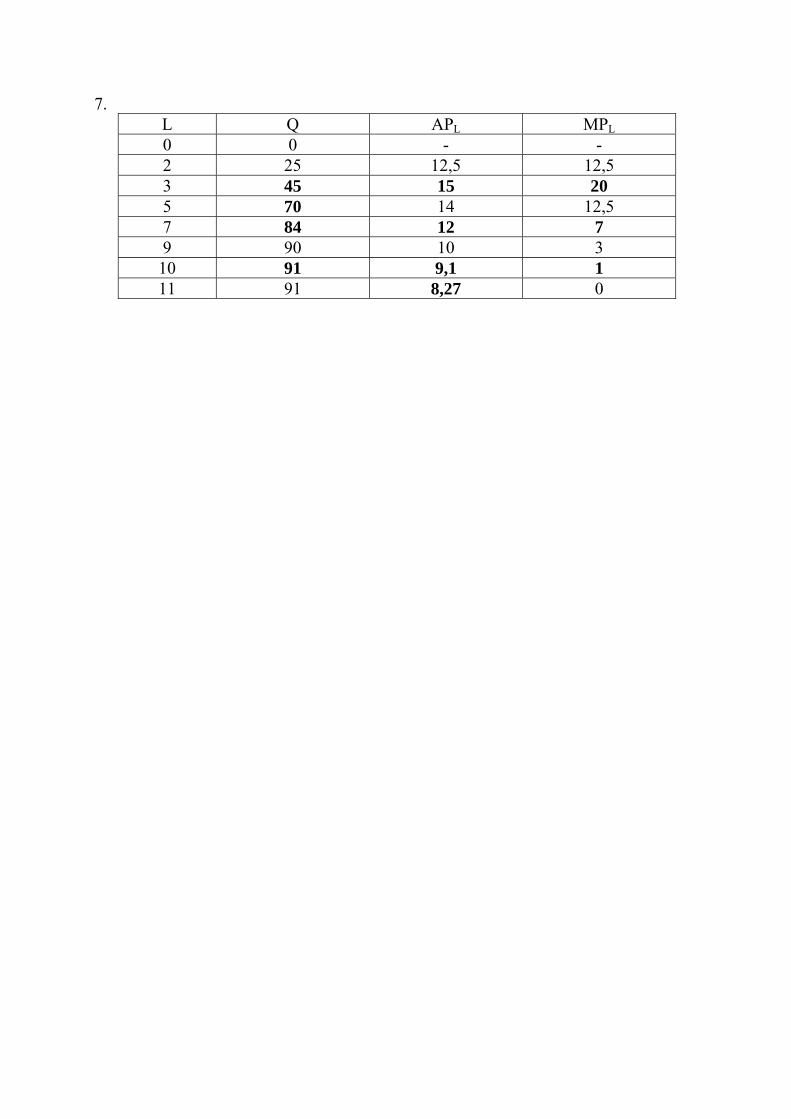

7. Calculate the missing data of the following table! L Q APL MPL 0 2 12,5 3 5 14 12,5 7 9 90 3 10 11 91 0

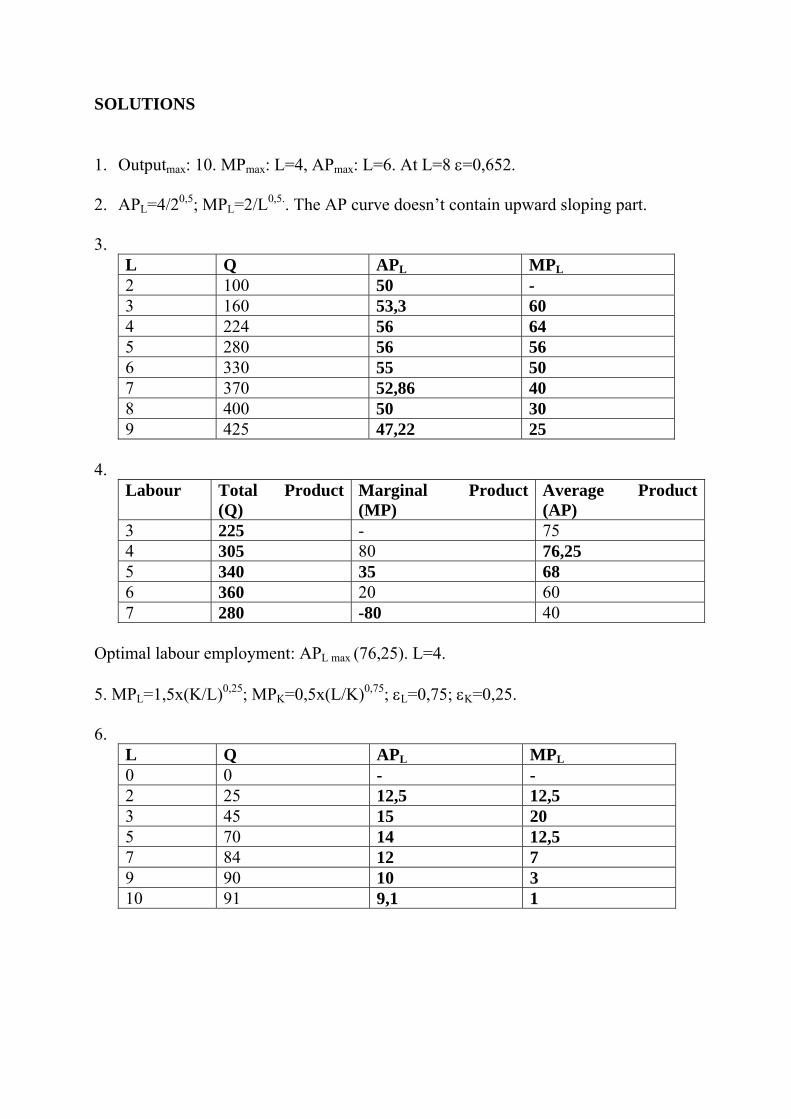

SOLUTIONS 1. Outputmax: 10. MPmax: L=4, APmax: L=6. At L=8 ε=0,652. 2. APL=4/20,5; MPL=2/L0,5.. The AP curve doesn’t contain upward sloping part. 3.

L Q APL MPL 2 100 50 - 3 160 53,3 60 4 224 56 64 5 280 56 56 6 330 55 50 7 370 52,86 40 8 400 50 30 9 425 47,22 25

4.

Labour Total Product (Q)

Marginal Product (MP)

Average Product (AP)

3 225 - 75 4 305 80 76,25 5 340 35 68 6 360 20 60 7 280 -80 40

Optimal labour employment: APL max (76,25). L=4. 5. MPL=1,5x(K/L)0,25; MPK=0,5x(L/K)0,75; εL=0,75; εK=0,25. 6.

L Q APL MPL 0 0 - - 2 25 12,5 12,5 3 45 15 20 5 70 14 12,5 7 84 12 7 9 90 10 3 10 91 9,1 1

7. L Q APL MPL 0 0 - - 2 25 12,5 12,5 3 45 15 20 5 70 14 12,5 7 84 12 7 9 90 10 3

10 91 9,1 1 11 91 8,27 0

LONG-RUN PRODUCTION TRUE OR FALSE STATEMENTS 1. It will be worth to increase the labour input at the expense of capital, if the

marginal product of the labour is larger than the marginal product of capital. 2. Isoquant curve shows all the combinations of capital and labour that can be used to

produce with a given total cost. 3. If the marginal product of a dollar’s worth of labour equals that of a dollar’s worth

of capital, allocation of inputs will be optimal. 4. The increase of an input’s price doesn’t change the slope of the isocost curve. PROBLEMS 1) A firm’s long-run production function is Q=3LK+300. The firm spends 3000 euro on the inputs. From this sum of money, it can apply maximum 10 workers (L). The price ratio of the inputs is PL/PK=1.

a) Calculate the optimal input allocation! b) How will the combination of the two inputs change, if the budget of the firm

increases by 20 percent? c) Calculate the output of both cases! d) Illustrate the isocost and isoquant curves and the optimal choices of the firm!

2) A company’s total cost is 2400 thousand Ft. Let suppose, that it can buy 4L or 8K inputs from this sum of money. The company’s production can be characterised with the following production function: Q=LK.

a) Determine the input allocation in this case! b) How will the use of inputs change, if the price of the labour increases by one

third? c) Calculate the output in both cases! d) Illustrate the isocost and isoquant curves and the optimal choices of the firm!

3) Let suppose, that only one combination (1:2) of L and K inputs can be used to produce a given product. The prices of the inputs are: PL=200, PK=100, the firm spends 10 000 euro on them.

a) Determine the input allocation in this case! b) How does the resource allocation change after a 10 percent price rise of the L

input? c) Illustrate the isocost and isoquant curves and the optimal choices of the firm!

4) Let suppose, that only one combination (1:2) of L and K inputs can be used to produce a given product. The prices of the inputs are: PL=200, PK=100, the firm spends 10 000 euro on them.

a. Determine the input allocation in this case! b. How will the resource allocation change, if the budget of the company

decreases by 20 percent? c. Illustrate the isocost and isoquant curves and the optimal choices of the firm!

SOLUTIONS

1. a) L0=5, K0=7,5. b) L1=6, K1=9. c) Q0=412,5, Q1=462.

2. a) L0=2, K0=4. b) L1=1,5, K1=4. c) Q0=8, Q1=10.

3. a) L0=25, K0=50. b) L1=23,8, K1=47,6.

4. L0=25, K0=50. b) L1=20, K1=40.

COSTS OF PRODUCTION TRUE OR FALSE STATEMENTS 1. A company will achieve economic profit, if its accounting profit is larger than the accounting cost. 2. Depreciation is a non-accountable implicit cost. 3. Marginal profit curve will reach its maximum, if the marginal cost curve is at its minimum. 4. The average variable cost curve cannot intersect the average fixed cost curve. 5. The average total cost curve is located below the average fixed cost curve till a certain output level, after that point it is located above it. 6. The average variable costs curve intersects the marginal cost curve where it is located above the average fixed cost curve. PROBLEMS 1. We know the annual data of a company: Accounting profit 12800 non-accountable implicit cost 8400 Explicit costs 8600 Economic costs 17400 Calculate the accounting and implicit cost and the economic and normal profit of the company! 2. The economic cost of a company in the last year was 7500 thousand forints. The implicit cost was 1350 thousand forints, 350 thousand forints of the latter was accountable. Economic profit was 560 thousand forints. Determine the accounting and explicit costs and the accounting and normal profits of the firm!

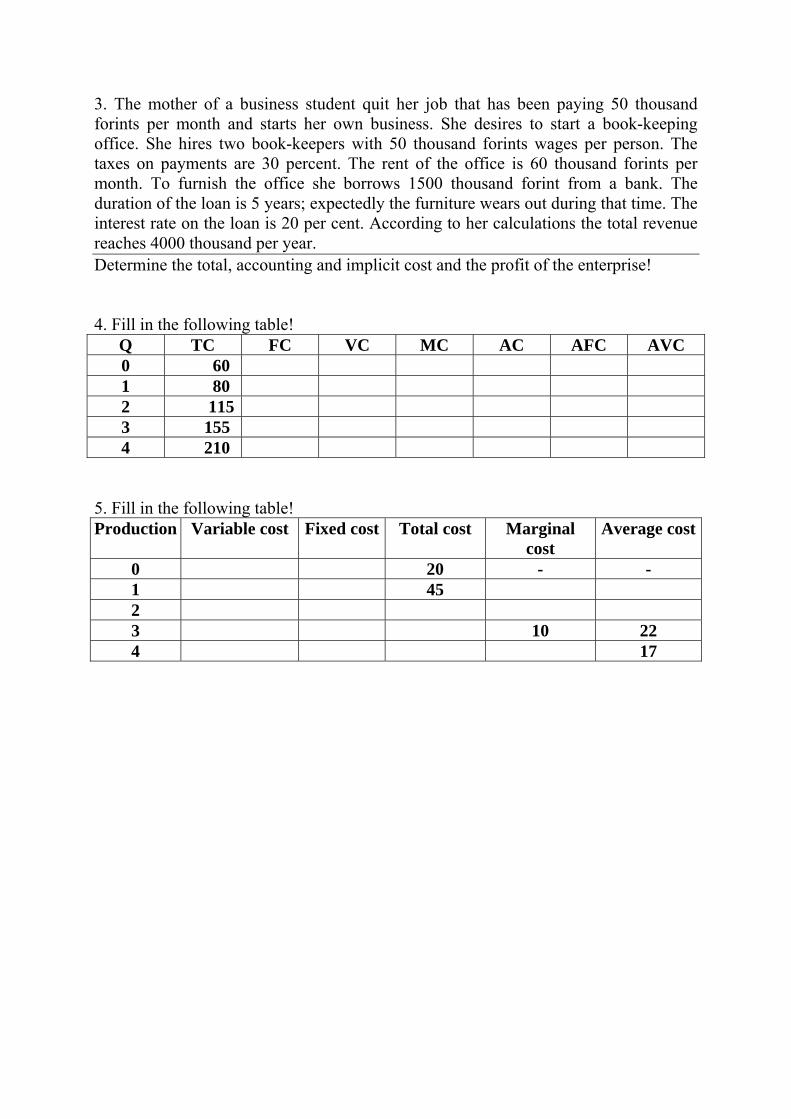

3. The mother of a business student quit her job that has been paying 50 thousand forints per month and starts her own business. She desires to start a book-keeping office. She hires two book-keepers with 50 thousand forints wages per person. The taxes on payments are 30 percent. The rent of the office is 60 thousand forints per month. To furnish the office she borrows 1500 thousand forint from a bank. The duration of the loan is 5 years; expectedly the furniture wears out during that time. The interest rate on the loan is 20 per cent. According to her calculations the total revenue reaches 4000 thousand per year. Determine the total, accounting and implicit cost and the profit of the enterprise! 4. Fill in the following table!

Q TC FC VC MC AC AFC AVC 0 60 1 80 2 115 3 155 4 210

5. Fill in the following table! Production Variable cost Fixed cost Total cost Marginal

cost Average cost

0 20 - - 1 45 2 3 10 22 4 17

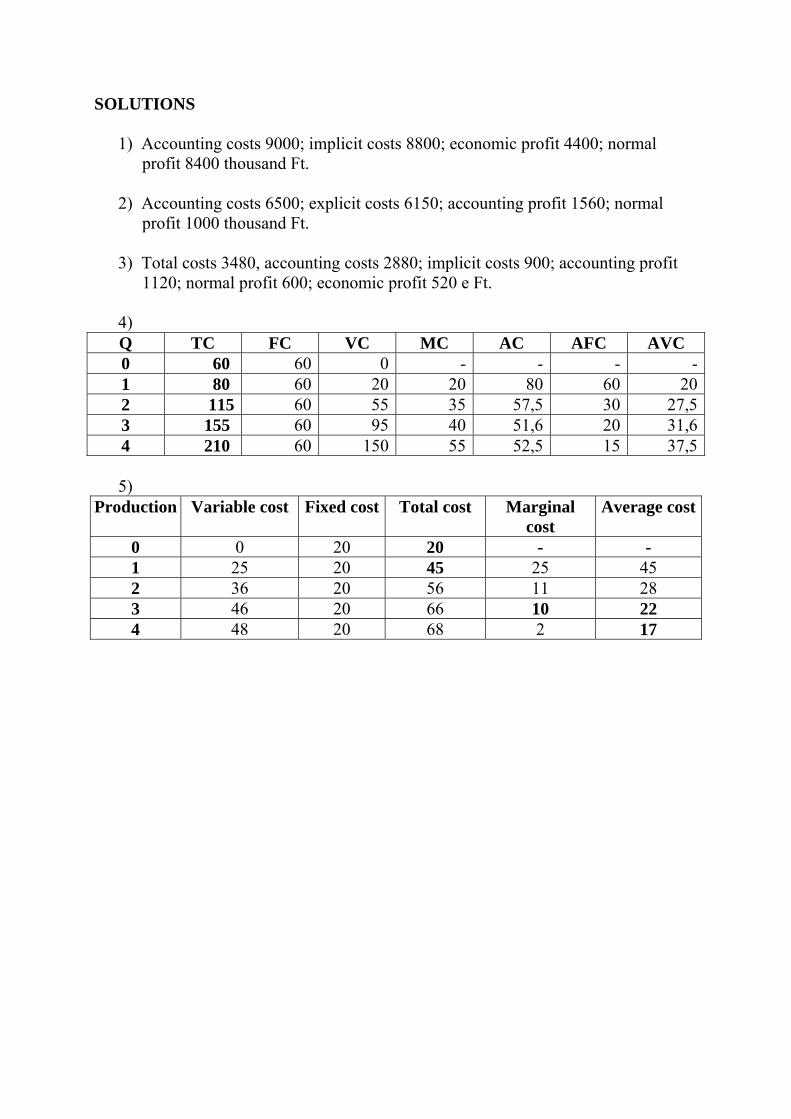

SOLUTIONS

1) Accounting costs 9000; implicit costs 8800; economic profit 4400; normal profit 8400 thousand Ft.

2) Accounting costs 6500; explicit costs 6150; accounting profit 1560; normal

profit 1000 thousand Ft.

3) Total costs 3480, accounting costs 2880; implicit costs 900; accounting profit 1120; normal profit 600; economic profit 520 e Ft.

4) Q TC FC VC MC AC AFC AVC 0 60 60 0 - - - -1 80 60 20 20 80 60 202 115 60 55 35 57,5 30 27,53 155 60 95 40 51,6 20 31,64 210 60 150 55 52,5 15 37,5

5)

Production Variable cost Fixed cost Total cost Marginal cost

Average cost

0 0 20 20 - - 1 25 20 45 25 45 2 36 20 56 11 28 3 46 20 66 10 22 4 48 20 68 2 17

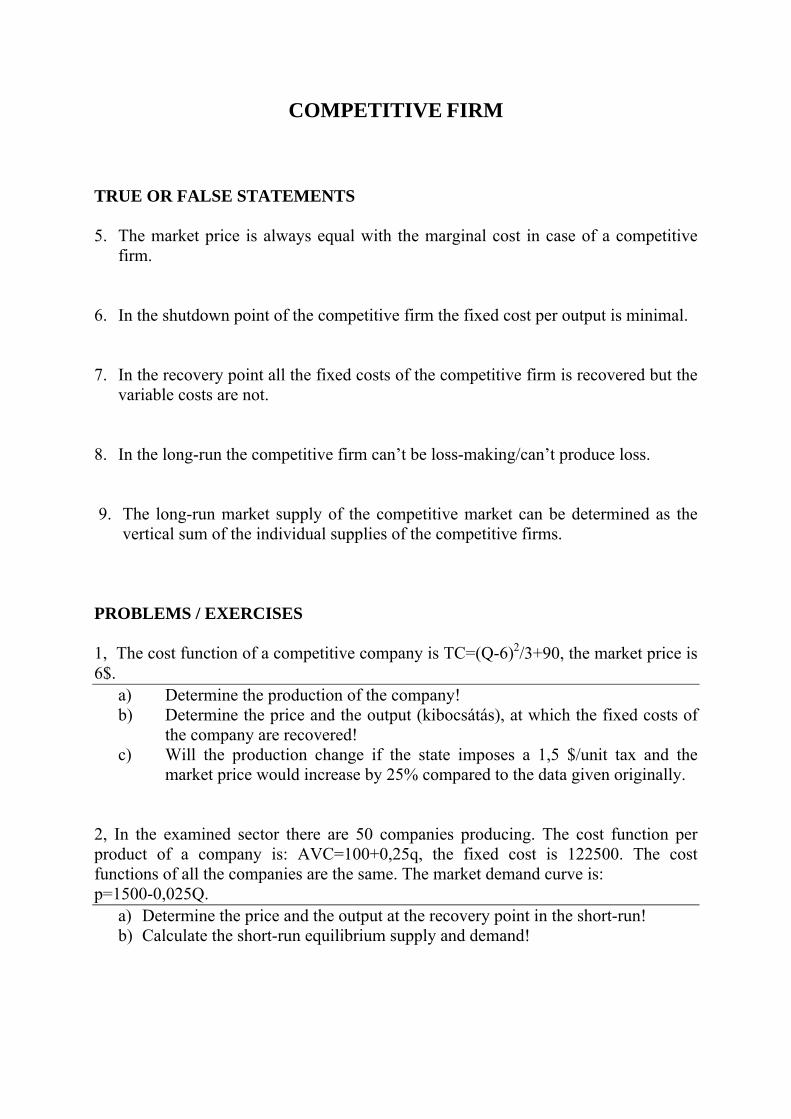

COMPETITIVE FIRM TRUE OR FALSE STATEMENTS 5. The market price is always equal with the marginal cost in case of a competitive

firm.

6. In the shutdown point of the competitive firm the fixed cost per output is minimal. 7. In the recovery point all the fixed costs of the competitive firm is recovered but the

variable costs are not. 8. In the long-run the competitive firm can’t be loss-making/can’t produce loss. 9. The long-run market supply of the competitive market can be determined as the

vertical sum of the individual supplies of the competitive firms. PROBLEMS / EXERCISES 1, The cost function of a competitive company is TC=(Q-6)2/3+90, the market price is 6$.

a) Determine the production of the company! b) Determine the price and the output (kibocsátás), at which the fixed costs of

the company are recovered! c) Will the production change if the state imposes a 1,5 $/unit tax and the

market price would increase by 25% compared to the data given originally. 2, In the examined sector there are 50 companies producing. The cost function per product of a company is: AVC=100+0,25q, the fixed cost is 122500. The cost functions of all the companies are the same. The market demand curve is: p=1500-0,025Q.

a) Determine the price and the output at the recovery point in the short-run! b) Calculate the short-run equilibrium supply and demand!

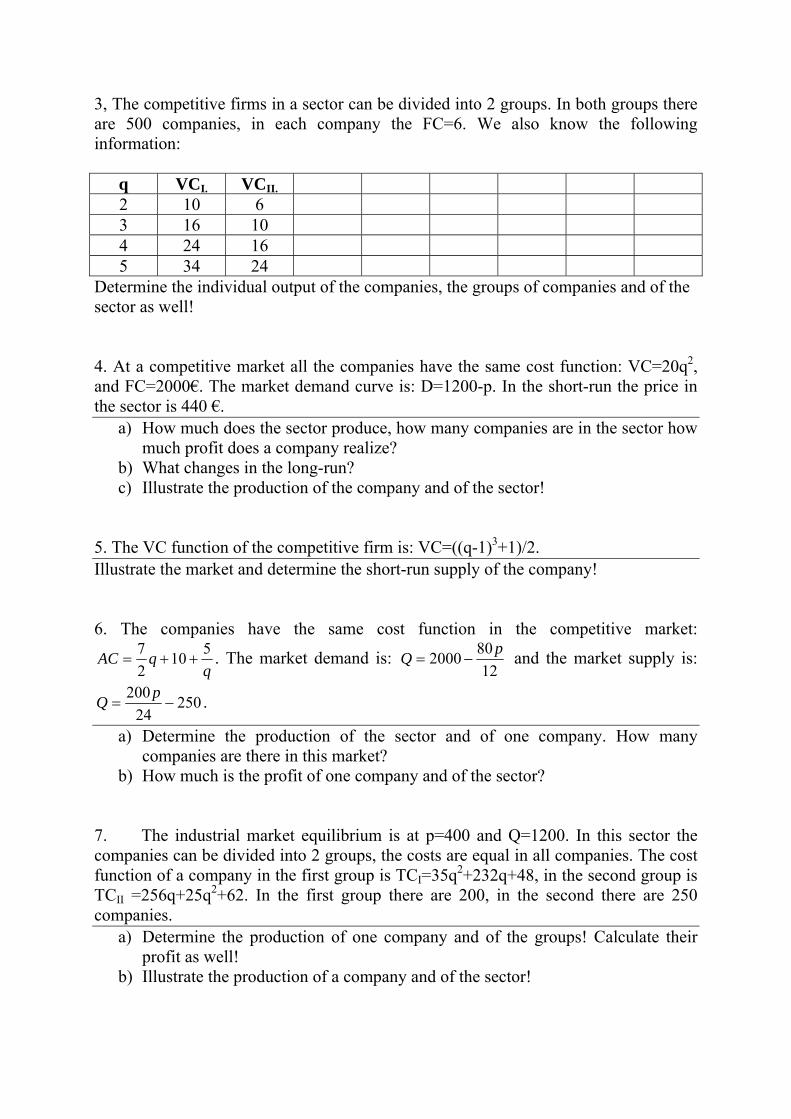

3, The competitive firms in a sector can be divided into 2 groups. In both groups there are 500 companies, in each company the FC=6. We also know the following information:

q VCI. VCII. 2 10 6 3 16 10 4 24 16 5 34 24

Determine the individual output of the companies, the groups of companies and of the sector as well! 4. At a competitive market all the companies have the same cost function: VC=20q2, and FC=2000€. The market demand curve is: D=1200-p. In the short-run the price in the sector is 440 €.

a) How much does the sector produce, how many companies are in the sector how much profit does a company realize?

b) What changes in the long-run? c) Illustrate the production of the company and of the sector!

5. The VC function of the competitive firm is: VC=((q-1)3+1)/2. Illustrate the market and determine the short-run supply of the company! 6. The companies have the same cost function in the competitive market:

qqAC 510

27

++= . The market demand is: 12

802000 pQ −= and the market supply is:

25024

200−=

pQ .

a) Determine the production of the sector and of one company. How many companies are there in this market?

b) How much is the profit of one company and of the sector? 7. The industrial market equilibrium is at p=400 and Q=1200. In this sector the companies can be divided into 2 groups, the costs are equal in all companies. The cost function of a company in the first group is TCI=35q2+232q+48, in the second group is TCII =256q+25q2+62. In the first group there are 200, in the second there are 250 companies.

a) Determine the production of one company and of the groups! Calculate their profit as well!

b) Illustrate the production of a company and of the sector!

8. In the examined sector the market equilibrium is at Q=1200 and P=400. The companies in this sector can be divided into 2 groups, having the same cost functions. The first group consists of 200 companies and their cost function is: TCI=35Q2+232Q-408,4. In the second group there are 250 companies having the following cost function: TCII=25Q2+256Q-672.

a) Determine the production of one company and of the groups! Calculate their profit as well!

b) Illustrate the production of a company and of the sector! 9. The cost function of a competitive firm is: TC=550Q-12Q2+Q3 . The company has filled out invoices up to 80% of the price. (80% of the costs are recorded in the accounts of the company)

a) Determine the long-run supply and the profit of the company.! b) Illustrate the functions!

10. In the examined sector the market equilibrium is at Q=1000 and P=140. In this sector the fixed cost of a company is 5 at an output of Q=2. The function of the variable cost is the following: VC=60Q+5Q2.

a) Calculate the production and the profit of the company in short-run! b) Determine the production in the long-run. How much is the price? c) Illustrate the functions!

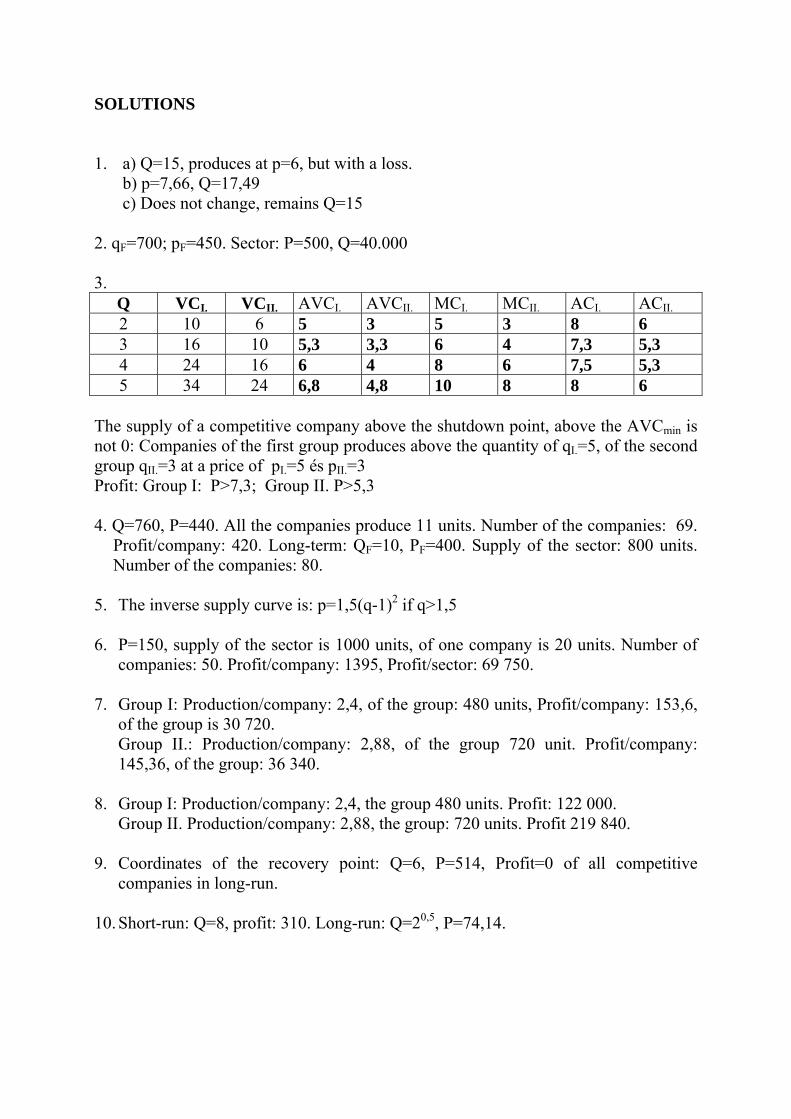

SOLUTIONS 1. a) Q=15, produces at p=6, but with a loss.

b) p=7,66, Q=17,49 c) Does not change, remains Q=15

2. qF=700; pF=450. Sector: P=500, Q=40.000 3.

Q VCI. VCII. AVCI. AVCII. MCI. MCII. ACI. ACII. 2 10 6 5 3 5 3 8 6 3 16 10 5,3 3,3 6 4 7,3 5,3 4 24 16 6 4 8 6 7,5 5,3 5 34 24 6,8 4,8 10 8 8 6

The supply of a competitive company above the shutdown point, above the AVCmin is not 0: Companies of the first group produces above the quantity of qI.=5, of the second group qII.=3 at a price of pI.=5 és pII.=3 Profit: Group I: P>7,3; Group II. P>5,3 4. Q=760, P=440. All the companies produce 11 units. Number of the companies: 69.

Profit/company: 420. Long-term: QF=10, PF=400. Supply of the sector: 800 units. Number of the companies: 80.

5. The inverse supply curve is: p=1,5(q-1)2 if q>1,5

6. P=150, supply of the sector is 1000 units, of one company is 20 units. Number of

companies: 50. Profit/company: 1395, Profit/sector: 69 750.

7. Group I: Production/company: 2,4, of the group: 480 units, Profit/company: 153,6, of the group is 30 720. Group II.: Production/company: 2,88, of the group 720 unit. Profit/company: 145,36, of the group: 36 340.

8. Group I: Production/company: 2,4, the group 480 units. Profit: 122 000.

Group II. Production/company: 2,88, the group: 720 units. Profit 219 840. 9. Coordinates of the recovery point: Q=6, P=514, Profit=0 of all competitive

companies in long-run. 10. Short-run: Q=8, profit: 310. Long-run: Q=20,5, P=74,14.

THE MONOPOLY TRUE OR FALSE STATEMENTS 1. If a competitive sector transforms into a monopoly, the consmer’s surplus

increases.

2. The monopoly can not produce losses neither in short-run, nor in long-run.

3. The Total Revenue of a monopoly can be increased by increasing the output.

4. The monopoly has no recovery point.

5. In case of the monopoly no shutdown point can be determined because it always produces economic profit..

EXERCISES 1. The demand curve of a sector is Q=100-0,1P. The cost function of the sector is: TC= 10.000+100Q+5Q2. a) Determine the price and the produced quantity in case of a monopoly and of pure

competition! b) Determine the profit of the monopoly and the deadweight loss caused by the

monopoly! c) Determine the consumers’ surplus and the producers’ surplus in case of the

monopoly and of pure competition!

2. The demand curve of a sector is Q= 50-0,5P. The average cost in the sector is AC=25. a) Calculate the price and the output of a monopoly! b) Calculate the price and the output of a competitive sector! c) Determine the profit of the monopoly! d) Determine the deadweight loss caused by the monopoly! e) In case of the monopolist production by how much will the consumers’ surplus

decrease compared to the pure competition? How much of the lost consumers’ surplus transformes into producers’ surplus?

f) Illustrate the market! 3. The demand curve of a sector is Q=768-2P, the marginal cost curve is linear. a) Determine the marginal cost equation of the sector , if in case of monopoly the

price is 351, in a competutuve market is 348. b) Calculate the change int he consumers’ surplus and in producers’ surplus! c) Illustrate the market! 4. The demand curve of a sector is Q=15-0,125P. The costs are increasing in a constant way. If the sector transformes into a monopoly, the consumers’ surplus decreases by 300 (compared to a pure competition). a) Determine the output in case of pure competition and of monopoly! Determine the

deadweight loss!

5. A student is collecting hip in the forest and sells it to a chemistry to increase his pocket-money. The demand of the hip is P=20-2Q. The Average Cost function of the student is AC=[2+(Q-2)3]/2Q. a) Determine the supply quantity and the supply price of the student! b) The owner of the forest permits the student to collect hip only if he pays a land use

fee. He can choose between two options: Pay 10$ once or 2$ after each kilograms collected. Which one would you use?

6. The monopoly produces the same type of product in two factories. The market demand curve is Q=77-P. The Marginal cost function of the first factory is MC1=q1-5; of the second is MC2=0,5q2-1. a) Determine the optimal output of the two factories! 7. The demand curve of the examined sector is Q=560-P, the cost can be determined by the following equation: AVC=60+Q. The minimum of AC curve is at 380$. a) Determine the production an the market price in a competitive market and in case

of a monopoly. b) Determine the profit and the producers’ surplus in each case!

SOLUTIONS 1. QTV=45; PTV=550. QM=30; PM=700. Consumers’ surplus M: 4500, TV: 10125. Producers’ surplus: M: 13500, TV:10125. Deadweight loss: 1125. 2. QM=18,75; PM=62,5. QTV=37,5; PTV=25. Profit of monopoly: 703,125. Deadweight loss: 351,5625. 703,125 of the lost consumers’ surplus transforms into producers’ surplus of the monopoly. 3. MC=5Q-12. Change in consumers’ surplus 207. Change in producers’ surplus: 108. 4. PM=80; PTV=40; QM=5; QTV=10. Deadweight loss: 100. 5. Q=3,79; P=12,42. Profit in case of the once payable fee 33,2, in case of fee/kg 35,8, So choose the fee/kg. 1. q1=14, q2=20. 7. QM=125, PM=560-Q=435, QTV=166,6, PTV=560-Q=393,3, MC=60+2Q. Profit of the monopoly 5650, of the competitive sector 2177,78. Consumers’ surplus of the monopoly 31250, of the competitive sector 27777,78.

THE INPUT MARKET TRUE OR FALSE STATEMENTS 1. A subsequent input increases the total cost by the price of that input. 2. According to the general condition of the optimal input employment PL has to be equal with VMPL. 3. If there is pure competition in the output market, MFCL=MRPL. 4. The individual labour supply curve shows the relation between the income and the free time. EXERCISES

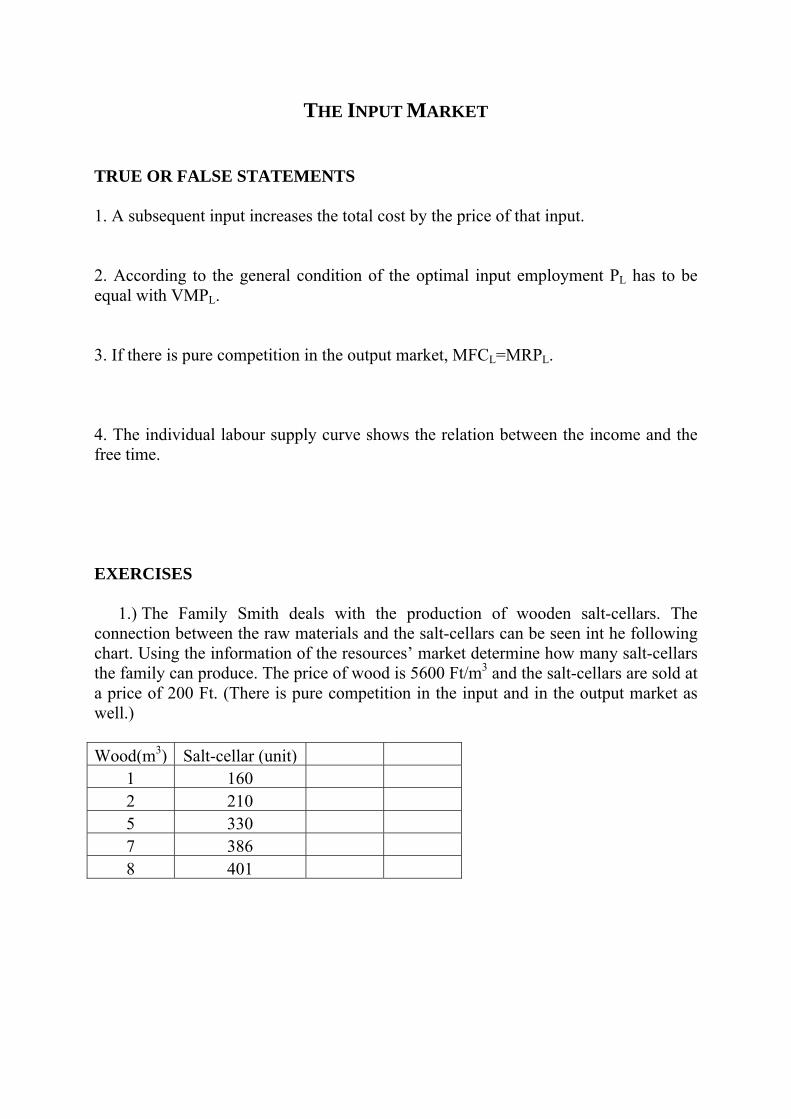

1.) The Family Smith deals with the production of wooden salt-cellars. The connection between the raw materials and the salt-cellars can be seen int he following chart. Using the information of the resources’ market determine how many salt-cellars the family can produce. The price of wood is 5600 Ft/m3 and the salt-cellars are sold at a price of 200 Ft. (There is pure competition in the input and in the output market as well.)

Wood(m3) Salt-cellar (unit)

1 160 2 210 5 330 7 386 8 401

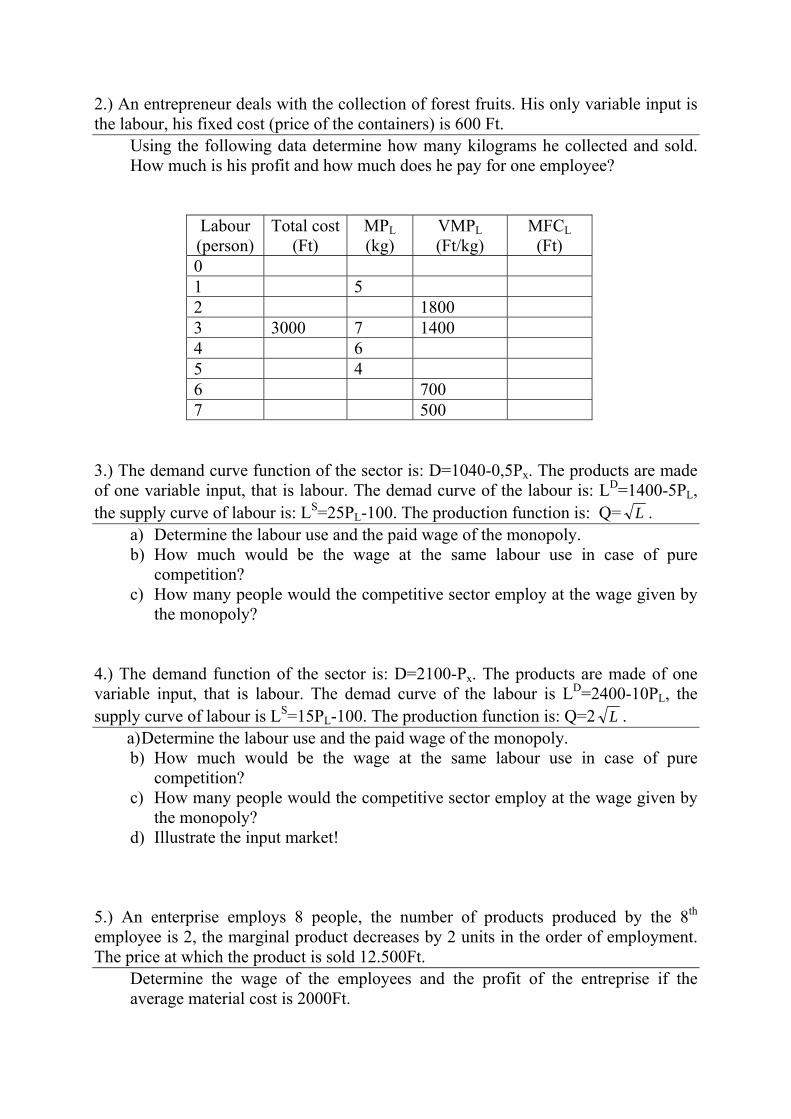

2.) An entrepreneur deals with the collection of forest fruits. His only variable input is the labour, his fixed cost (price of the containers) is 600 Ft.

Using the following data determine how many kilograms he collected and sold. How much is his profit and how much does he pay for one employee?

Labour (person)

Total cost (Ft)

MPL (kg)

VMPL (Ft/kg)

MFCL (Ft)

0 1 5 2 1800 3 3000 7 1400 4 6 5 4 6 700 7 500

3.) The demand curve function of the sector is: D=1040-0,5Px. The products are made of one variable input, that is labour. The demad curve of the labour is: LD=1400-5PL, the supply curve of labour is: LS=25PL-100. The production function is: Q= L .

a) Determine the labour use and the paid wage of the monopoly. b) How much would be the wage at the same labour use in case of pure

competition? c) How many people would the competitive sector employ at the wage given by

the monopoly? 4.) The demand function of the sector is: D=2100-Px. The products are made of one variable input, that is labour. The demad curve of the labour is LD=2400-10PL, the supply curve of labour is LS=15PL-100. The production function is: Q=2 L .

a) Determine the labour use and the paid wage of the monopoly. b) How much would be the wage at the same labour use in case of pure

competition? c) How many people would the competitive sector employ at the wage given by

the monopoly? d) Illustrate the input market!

5.) An enterprise employs 8 people, the number of products produced by the 8th employee is 2, the marginal product decreases by 2 units in the order of employment. The price at which the product is sold 12.500Ft.

Determine the wage of the employees and the profit of the entreprise if the average material cost is 2000Ft.

6.) The demand function of a sector is: xpQ 22000 −= . The cost curve of the sector

is: 1004002

2

++= QQTC .

a) Determine the wage in the competitive market, if the nth employee produces 20 units. b) How much is the wage int he monopoly, if all the characteristics of the employees are the same? c) Determine the number of employees in case of the monopoly!

7.) The demand function of a product is: pQ 22000 −= .

a) Determine the wage paid in the competitive market, if the supply curve int he sector is: p . The last employee produces 20 units. S +=1400

b) Calculate the change in the wage if there is a monopoly operating in the sector. The characteristics of the employees are the same, but the monopoly intends to reach the price 550$.

8.) We know the following data about a company that is competitive in the input and in the output market as well. Production function: QL=-L2+400L+1000. The only variable input of the company is the labour. The wage paid by the company is PL=10000 Ft/óra. The market price of its product is ára P=100 Ft. Determine the optimal input use in case of a competitive market.

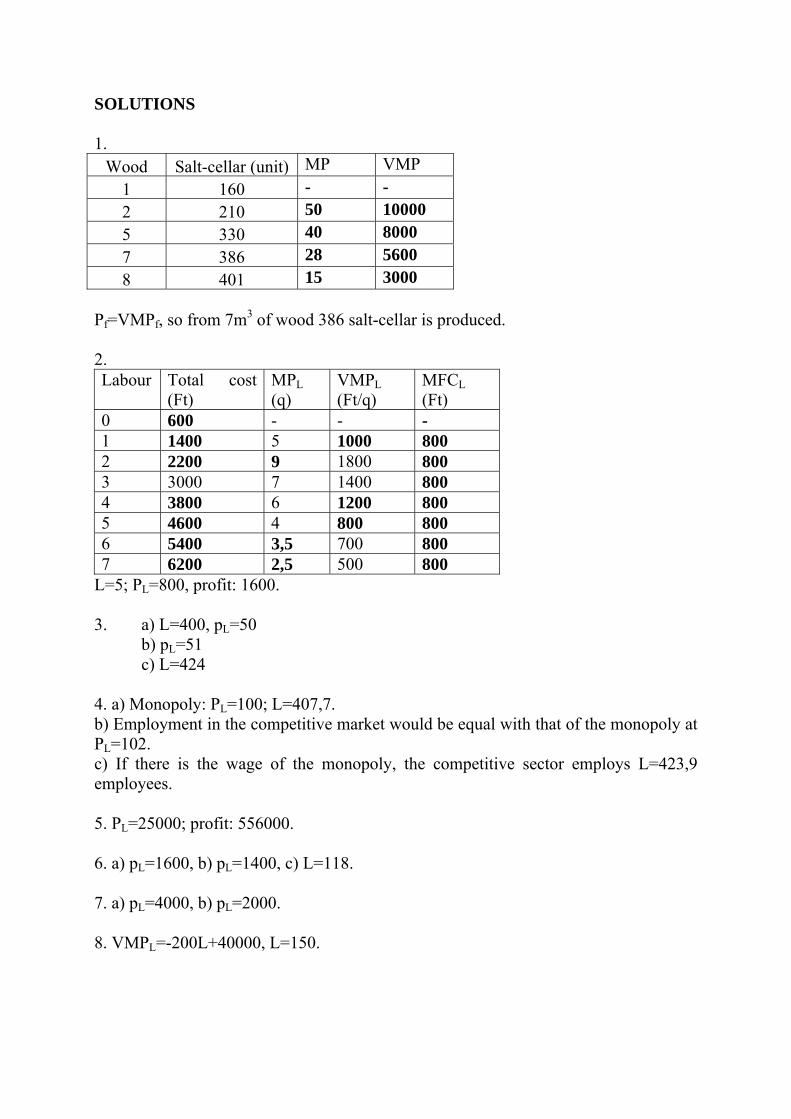

SOLUTIONS 1.

Wood Salt-cellar (unit) MP VMP 1 160 - - 2 210 50 10000 5 330 40 8000 7 386 28 5600 8 401 15 3000

Pf=VMPf, so from 7m3 of wood 386 salt-cellar is produced. 2. Labour Total cost

(Ft) MPL (q)

VMPL (Ft/q)

MFCL (Ft)

0 600 - - - 1 1400 5 1000 800 2 2200 9 1800 800 3 3000 7 1400 800 4 3800 6 1200 800 5 4600 4 800 800 6 5400 3,5 700 800 7 6200 2,5 500 800

L=5; PL=800, profit: 1600. 3. a) L=400, pL=50

b) pL=51 c) L=424

4. a) Monopoly: PL=100; L=407,7. b) Employment in the competitive market would be equal with that of the monopoly at PL=102. c) If there is the wage of the monopoly, the competitive sector employs L=423,9 employees. 5. PL=25000; profit: 556000. 6. a) pL=1600, b) pL=1400, c) L=118. 7. a) pL=4000, b) pL=2000. 8. VMPL=-200L+40000, L=150.

CAPITAL MARKETS TRUE OR FALSE STATEMENTS 1. The higher the interest rate is, the larger the present value of a future yield is. 2. The present value of perpetuity cannot be calculated. 3. The price of the land is an external factor. 4. A future investment’s present value is determined by the market price. 5. It is worth to invest, if the expected gross yield exceeds the investment cost. PROBLEMS 1. The Alumni of Miskolc Club decided to establish a foundation, to support the 5

best graduates with 100 thousand forint each. The interest rate is 8 percent. a.) What deposit before one year of graduation does enable to pay a one time

support? b.) What deposit before one year of graduation does enable to pay continually? c.) What equal deposits will be needed if the first payment is only after 5 years?

2. The Human Bank wants to establish a foundation in order to support well educated

economics students. The foundation plans to give the first subsidies, 100-100 thousand forints for 6 students, after 3 years. The interest rate is 6,5 percent. a.) What deposit from today does enable to pay the support continually after three

years? b.)What a sum of money is needed to a one time support?

3. An investment provides 1400 thousand forints per year for each of the next 4 years.

The initial cost of the investment is 4000 thousand. From this the owner’s own resource is 1000 thousand, the rest is bank loan for 4 years with 13 percent lending rate. The bank rate is 9 percent. a.) Can the owner pay back the loan? b.)What is the present value of the future profits? c.) What is the real cost of the investment?

4. You have to decide about a plant’s rent. The rent is 2 million forints. To pay, you have to borrow the money for 4 years with 15 percent lending rate. The plant’s gross yield can reach 2,6 million forints in the next five years, 75 percent from it is cost. a.) What is the cost of the investment? b.)Is it worth to rent, if the bank rate is 10 percent?

5. An entrepreneur wants to buy his previous workplace (a newsagent’s). The cost is

3 million forints. He wants to finance it from bank loan. He can choose a 3-year loan with 16 percent interest rate or he can pay back 1 million in every year (three times). In this case the lending rate is 20 percent. The expected yield is 1,5 million per year. Interest rate is 10 percent. a.) Which loan would you choose? b.)Is it worth to start the business?

6. An entrepreneur buys a mine and starts his mushroom growing business. The price

of the mine is 10 million forint, the entrepreneur has the money. The starting cost is 2 million, which will be a bank loan with 40 percent interest rate for 2 years. He has to pay back the money and the interest rate at the end of the second year. The revenue is 1,6 million in the first year, 2 million in the second, and 2,5 million after that. From the third year the entrepreneur has to spend 7 hundred forint per year. a) Can the entrepreneur pay back the bank loan, if the interest rate is 25 percent? b) Is it worth to invest?

7. The expected yield of an investment is 1,1 million forint in the first year, 1,2 in the

second. In the third and after that 1,25 million forint, but from the fourth year 20 percent of the gross yield has to be spent on modernisation of the machines. The price is 6 million forint. Two-third of the sum is missing, but available through a loan with 15 percent interest rate for 4 years. a.) Can the entrepreneur pay back, if the bank loan is 10 percent? b.)What is the present value of the future profits? c.) Which yield from the fourth year makes the interest rate equal to internal rate of

return? 8. An entrepreneur would like to rent a restaurant. The leasehold for 5 years is 5

million forint (he has to pay in advance). The entrepreneur has half of the money. The other part would be a bank loan. He can choose from two conditions: he can pay back in two equal terms in the end of the 2nd and the 3rd years with 15 percent interest rate, or he can pay back in one sum in the end of the 3rd year with 12 percent interest rate. The yield of the restaurant is expected to reach the one million per year in the next 7 years. Interest rate is 8 percent. a.) Which loan would you choose? b.)Is it worth to rent the restaurant?

9. The grandparents of a freshman give 600 thousand forints on condition that he is allowed to spend it only after graduating. He can deposit the money in a savings account with 7,5 percent interest rate. He can choose other investments, for example government securities with 6,5 percent interest rate, where 20 percent of the deposit will be tax allowance in the first year. An investment counsellor’s would pay back the loan in 160 thousand forint instalments in the next four years. a) Which solutions would you choose?

SOLUTIONS 1. a) One time support: 462,9 thousand Ft. b) Continual support: 6250 thousand Ft. c) 1065,6/year. 2. a) Continual support 8138,4 thousand Ft. b) One time support 496,7 thousand Ft. 3. a) He can pay back. b) PVyield: 4,536 million Ft. c) It is worth to invest (NPV=0,074). 4. a) 2,389 million forint. b) No (PVyield=2,06 million Ft). 5. a) The first loan is cheaper (PVloan1=3,51; PVloan2=3,8) b) It is worth to start (PVyield= 3,73 is larger than the costs of the business). 6. a) He can pay back (PVloan=2,5, PVyield

1-2=2,56). b) No (PVyield= 7,168, NPV=-5,3408). 7. a) He cannot pay back (PVloan=4,778, PVyield

1-4=3,614). b) 10,44. c) Required yield: 0,512/year. 8. The 2nd loan is cheaper (PVloan1=2,9; PVloan2=2,78). It is not worth to rent (the present value of the yields is 5,17, the costs 5,28. 9. The second. (PVA=600; PVB=684,24; PVC=535,89).