Embed Size (px)

Citation preview

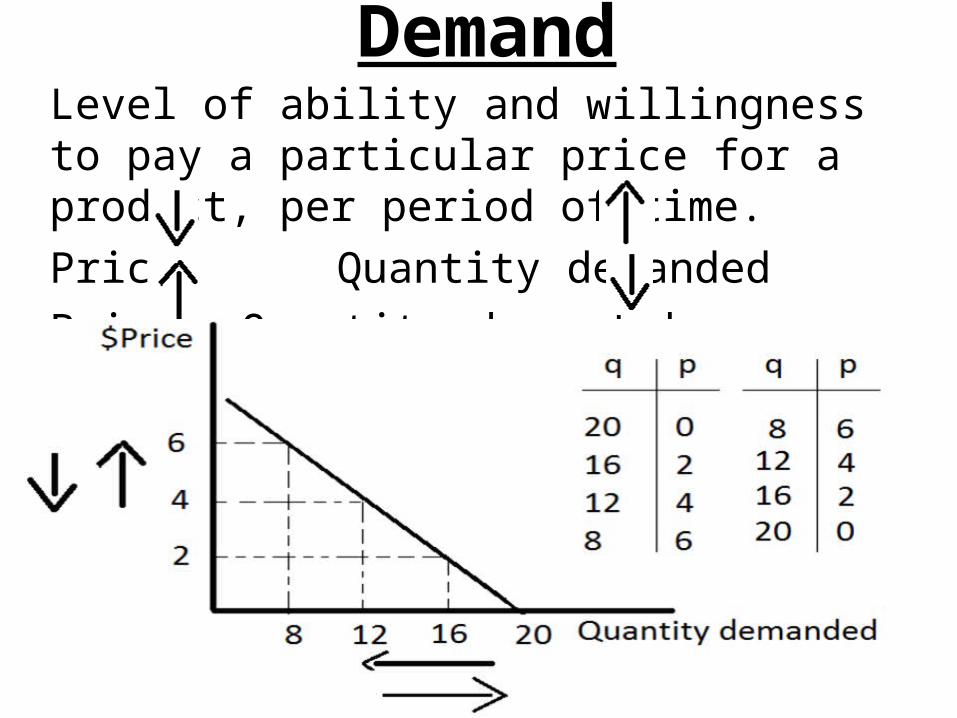

DemandLevel of ability and willingness to pay a particular price for a product, per period of time.Price Quantity demanded Price Quantity demanded

Determinants of the level of demand

Consumer income income demandPrice and availability of substitutes

number of substitutes v Price of a product

number of substitutes price of a product

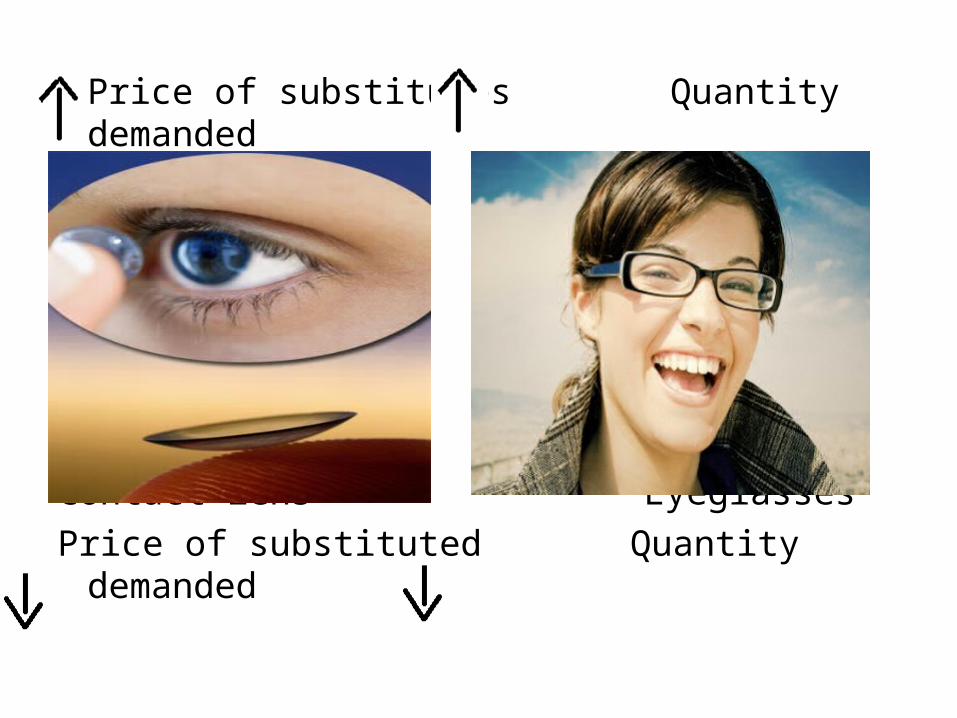

Price of substitutes Quantity demanded

Contact lens EyeglassesPrice of substituted Quantity demanded

Price and availability of complementsPrice of a product Q. demanded of complements

Printers Ink cartridgesPrice of a product Q. demanded of complements

Marketing Marketing (advertising) demand

Fashions, habits and tastesIf fashion changes, demand of certain products

will change.Utility (level of satisfaction)

Quality

It attracts certain clients, even at very high prices.

Speculation

Expectations and forecasts can also influence the level of demand.

People expect the prices to raise, so they start to buy a lot.

State of economyLevel of confidence in the economy is low, demand

Others Weather and

seasons

Religious beliefs

Age

Peer influence of pressure

Exceptions to the general law of demand

• Ostentatious consumption.- Expensive products to make customers fell good about themselves.

Nike trainers Vera wang wedding dresses Demand if price (Prestige and exclusivity is

important for customers)

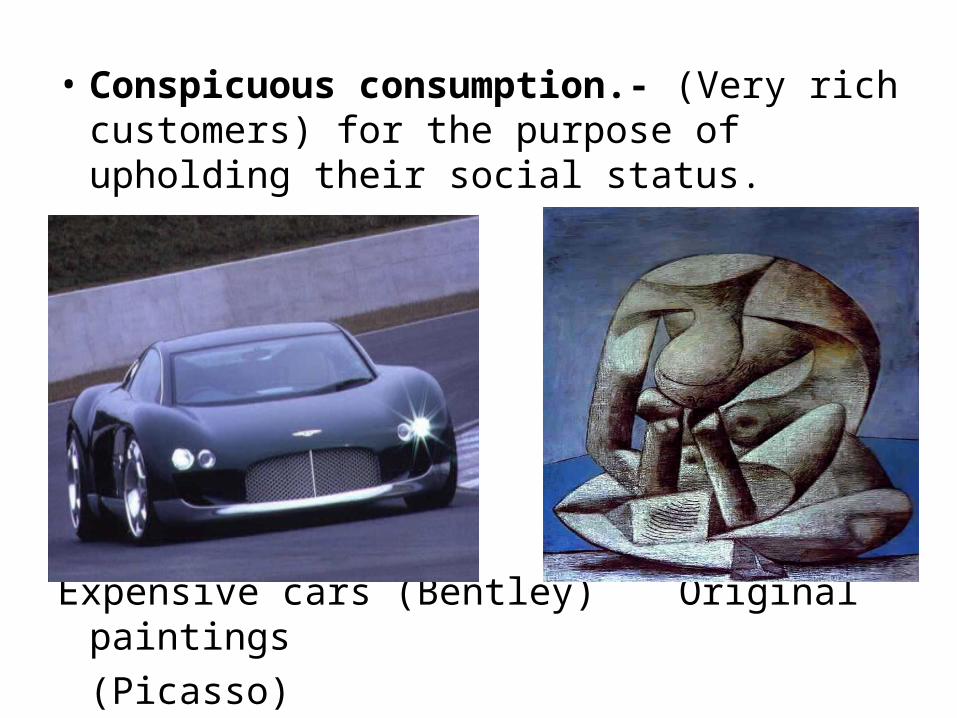

• Conspicuous consumption.- (Very rich customers) for the purpose of upholding their social status.

Expensive cars (Bentley)Original paintings(Picasso)

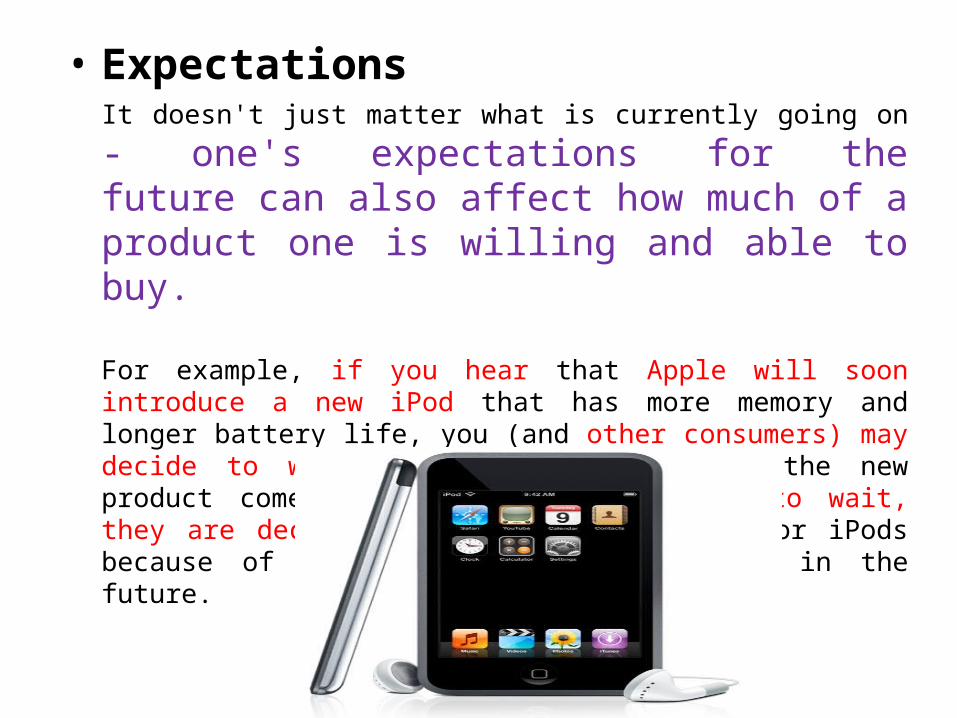

• ExpectationsIt doesn't just matter what is currently going on - one's expectations for the future can also affect how much of a product one is willing and able to buy.

For example, if you hear that Apple will soon introduce a new iPod that has more memory and longer battery life, you (and other consumers) may decide to wait to buy an iPod until the new product comes out. When people decide to wait, they are decreasing the current demand for iPods because of what they expect to happen in the future.

Similarly, if you expect the price of gasoline to go up tomorrow, you may fill up your car with gas now. So your demand for gas today increased because of what you expect to happen tomorrow.

This is similar to what happened after Hurricane Katrina hit in the fall of 2005. Rumors started that gas stations would run out of gas. As a result, many consumers decided to fill up their cars (and gas cans), leading to long lines and a big increase in the demand for gas. This was all based on the expectation of what would happen.

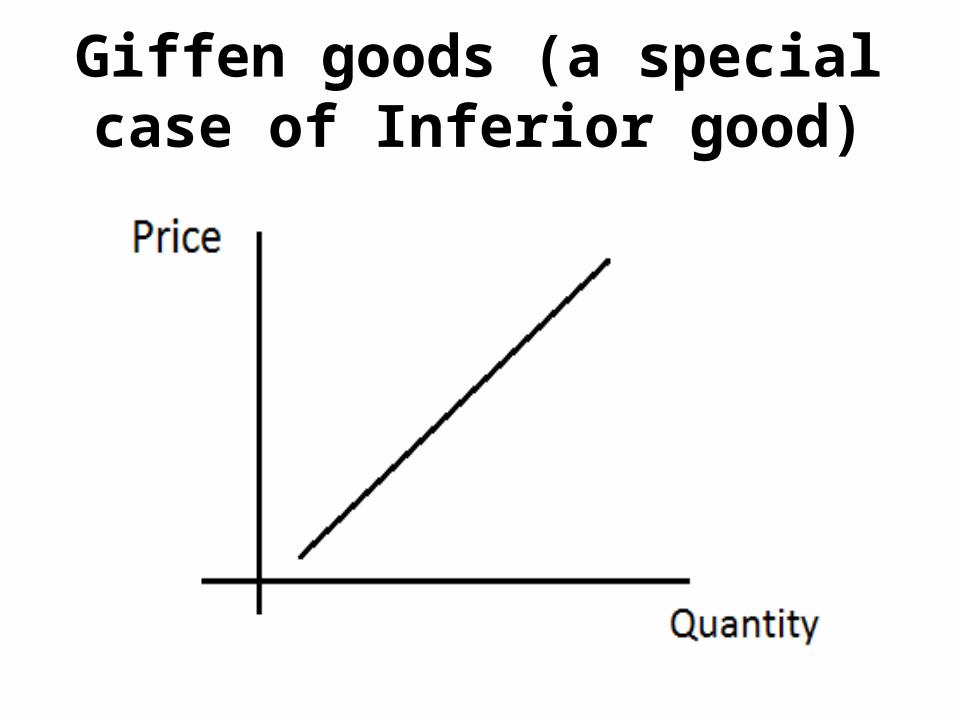

• Giffen goods.Price Quantity demandedPrice Quantity demanded

A rise in the price of bread (inferior good) makes so large a drain on the resources of the poorer labouring families. They are forced to curtail their consumption of meat and the more expensive food: and, bread being still the cheapest food which they can get and will take, they consume more, and not less of it.

Giffen goods (a special case of Inferior good)

Supply• Willingness and ability of firms to provide

products ate given price levels per period of time

• The higher the market price of a product, the more willing and able producers are to supply products in the market.

• Firms can make more profits when prices are higher or new firms will be attracted to enter the market when prices are higher

Price Quantity suppliedPrice Quantity supplied

Determinants of the level of supply

• Price of raw materialPrice of raw material Quantity supplied Price of raw material Quantity supplied • Barriers of entry Barriers of entry # producers Q supplied

Barriers of entry # producers Q supplied• Technology• advances technology Q. supplied cost prod advances technology Q. supplied cost prod

• Taxes Taxes Production costs Quantity supplied

Taxes Production costs Quantity supplied• Subsidies• subsidies Production costs Quantity supplied subsidies Production costs Quantity supplied• Price of related goods

Some goods are in competitive supply

“The product with the higher relative profitability will be produced and supplied in larger volumes”

In the case of join supply: Production of one product supply of another (join) product

• ClimateFavourable weather conditions, supply

Unfavourable weather conditions, supply Floods

• Time: Agricultural products take time to harvest

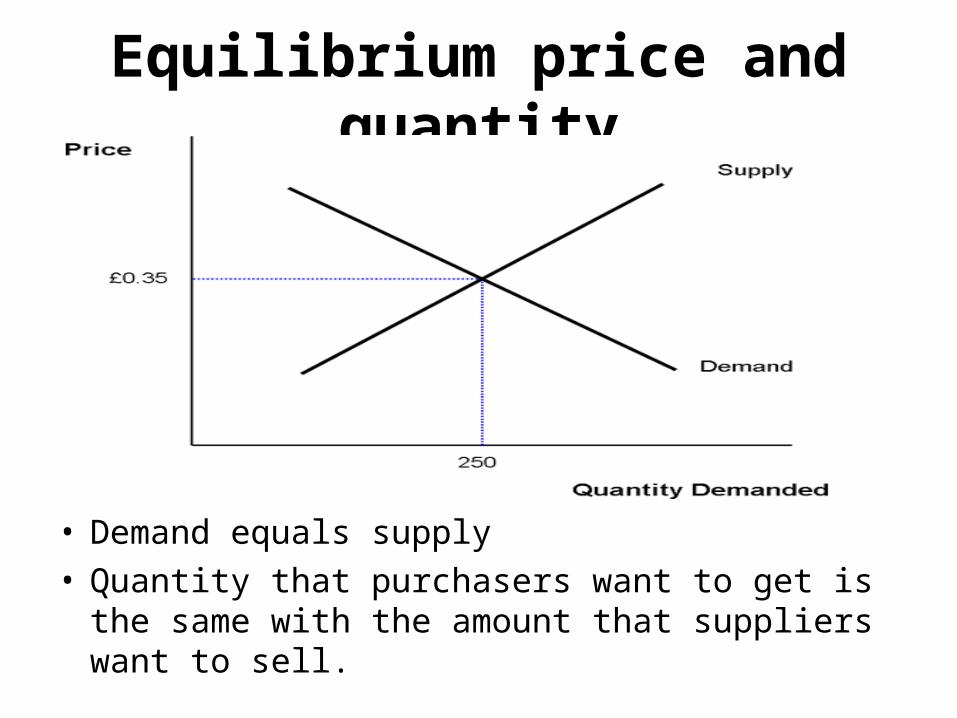

Equilibrium price and quantity

• Demand equals supply• Quantity that purchasers want to get is the same

with the amount that suppliers want to sell.

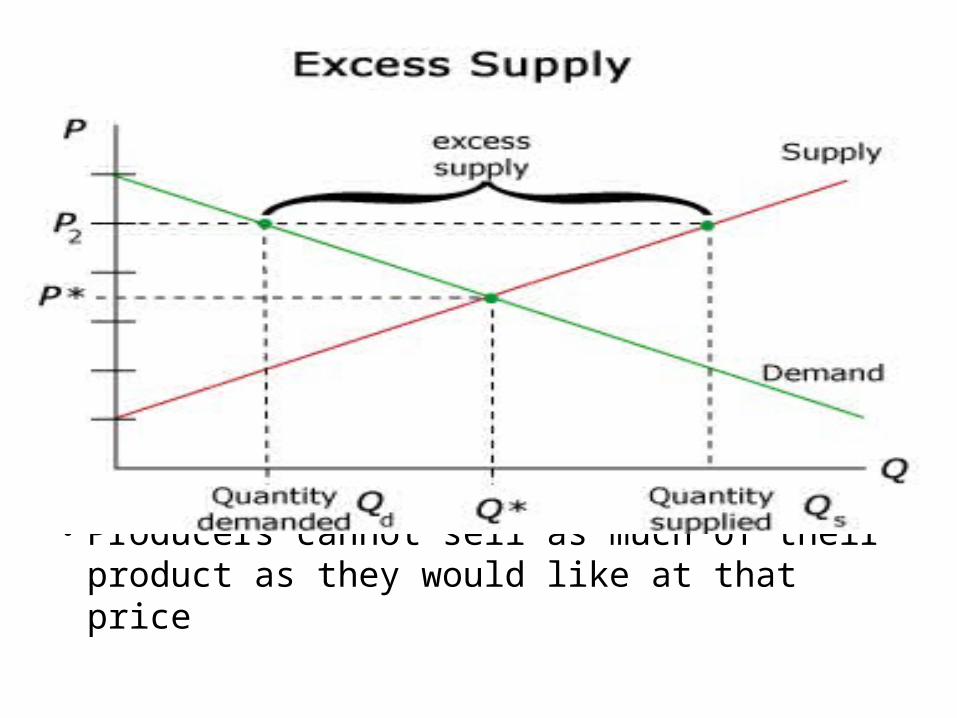

• Consumers want to purchase more units of a good than producers want to sell.

• Producers cannot sell as much of their product as they would like at that price