Embed Size (px)

Citation preview

Delivering value through transformationPractical Guide to New Singapore Financial Reporting Standards for 2014

Pra

ctic

al G

uid

e

Contents

Introduction 4

Developments in IFRS not yet adopted by ASC 5

1. New/revised standards and interpretations 6

FRS 27 (revised 2011) Separate Financial Statements and FRS 110 Consolidated 8 Financial Statements

FRS 28 (revised 2011) Investments in Associates and Joint Ventures and FRS 111 10 Joint Arrangements

FRS 112 Disclosure of Interests in Other Entities 12

Amendments to FRS 110 Consolidated Financial Statements, FRS 111 14 Joint Arrangements, FRS 112 Disclosure of Interests in Other Entities – Transition guidance

Amendments to FRS 110 Consolidated Financial Statements, FRS 112 Disclosure 15 of Interests in Other Entities and FRS 27 Separate Financial Statements – Exception from consolidation for ‘investment entities’

Amendments to FRS 32 Financial Instruments: Presentation 17 –Offsettingfinancialassetsandfinancialliabilities

Amendments to FRS 36 Impairment of Assets 18 –Recoverableamountdisclosuresfornon-financialassets

Amendments to FRS 39 Financial Instruments: Recognition and Measurement 19 – Novation of derivatives and continuation of hedge accounting

INT FRS 121 Levies 20

AmendmentstoFRS19(R)EmployeeBenefits 22 –DefinedBenefitPlans:EmployeeContributions

Improvements to FRSs 2012 24

Improvements to FRSs 2013 26

FRS 114 Regulatory Deferral 27

2. Differences between Singapore Financial Reporting Standards and 29 International Financial Reporting Standards

4

Pra

ctic

al G

uid

e

Introduction

ThispublicationisapracticalguidetothenewFRSstandardsandinterpretationsthatcomeintoeffect for 2014 year ends.

Agroupoffivenewandrevisedstandardswerepublishedandapplyfrom1January2014.FRS110,‘Consolidatedfinancialstatements’,changesthedefinitionofcontrol;FRS111,‘Jointarrangements’, reduces the types of joint arrangement to joint operations and joint ventures, andprohibitstheuseofproportionateconsolidation.FRS112,‘Disclosureofinterestsinotherentities’,bringstogetherinonestandardthedisclosurerequirementsthatapplytoinvestmentsinsubsidiaries,associates,jointventures,structuredentitiesandunconsolidatedstructuredentities.Aspartofthisoverhauloftheconsolidationstandards,FRS27(revised)nowdealsonlywithseparatefinancialstatements,andFRS28(revised)coversequityaccountingforjointventuresaswellasassociates.Thesenewstandardshavetobeimplementedtogether.Afurtheramendmenttothese standards sets out the accounting for investment entities and this comes into effect from 1January2014aswell.

Oneinterpretation–INTFRS121,‘Levies’,waspublishedin2013inrelationtoFRS37,‘Provisions,contingentliabilitiesandcontingentassets’.FRS37setsoutcriteriafortherecognitionofaliability,oneofwhichistherequirementfortheentitytohaveapresentobligationasaresultofapastevent(knownasanobligatingevent).Theinterpretationclarifiesthattheobligatingeventthatgivesrisetoaliabilitytopayalevyistheactivitydescribedintherelevantlegislationthattriggersthepaymentofthe levy and is effective 1 January 2014.

Afewnarrowscopeamendmentstoexistingstandardshavealsobeenissuedandareeffectiveforannualperiodsbeginningonorafter1January2014.Firstly,anamendmenttoFRS32,‘Financialinstruments:Presentation’regardingtheoffsettingoffinancialassetsandfinancialliabilities.Secondly,anamendmenttoFRS36,‘Impairmentofassets’regardingrecoverableamountdisclosuresfornon-financialassets.Finally,anamendmenttoFRS39,‘Financialinstruments:Recognition and measurement’ regarding the novation of derivatives and continuation of hedge accounting.

Inaddition,anamendmenttoFRS19,‘Employeebenefits’,concerningdefinedbenefitplansthatrequireemployeesorthirdpartiestocontributetowardsthecostsofbenefits,wasissuedinJanuary2014 and is effective annual periods on or after 1 July 2014.

The 2012 improvements project containing seven amendments and the 2013 improvements project containingthreeamendmentswereissuedinJanuary2014andFebruary2014respectivelyandalltheamendmentsareeffectiveforannualperiodsbeginningonorafter1July2014.

FRS114,‘Regulatorydeferralaccounts’,hasbeenissuedandiseffective1January2016. Earlyapplicationispermitted.FRS114permitsfirst–timeadopterstocontinuetorecogniseamountsrelatedtorateregulationinaccordancewiththeirpreviousGAAPrequirementswhen they adopt FRS.

Practical Guide 2014 5

Pra

ctic

al G

uid

e

Developments in IFRS not yet adopted by ASC

ThefollowingarethesignificantdevelopmentsinIFRSwhicharenotyetadoptedbyASC(asat30September2014).

• IFRS15,‘Revenuefromcontractswithcustomers’,wasissuedon28May2014bytheIASB.ThisstandardreplacesIAS18‘Revenue’,IAS11‘Constructioncontracts’andotherrevenue-relatedinterpretations.Itappliestoallcontractswithcustomers,exceptforleases,financialinstrumentsandinsurancecontracts.IFRS15providesasingle,principle-basedmodeltobeappliedtoallcontractswithcustomers.Itprovidesguidanceonwhetherrevenueshouldberecognisedatapointintimeorovertime,replacingthepreviousdistinctionbetweengoodsandservices.Thestandardintroducesnewguidanceonspecificcircumstanceswherecostshouldbecapitalisedandnewrequirementsfordisclosureofrevenueinthefinancialstatements. Thestandardiseffectiveforannualperiodsbeginningonorafter1January2017underIFRS.Moredetailscanbefoundinhttp://www.pwc.com/us/en/cfodirect/issues/revenue-recognition/index.jhtml.

• IFRS9,‘Financialinstruments’,wasissuedonJuly2014andincludesguidanceontheclassificationandmeasurementoffinancialassetsandfinancialliabilitiesandde-recognitionoffinancialinstruments.TheIASBhaspreviouslypublishedversionsofIFRS9thatintroducednewclassificationandmeasurementrequirements(in2009and2010)andanewhedgeaccountingmodel(in2013).TheJuly2014publicationrepresentsthefinalversionofthestandardandreplaces the earlier versions of IFRS 9 and completes the IASB’s project to replace IAS 39, ‘Financial Instruments: Recognition and Measurement’. The standard is effective for annual periodsbeginningonorafter1January2018underIFRS.Moredetailscanbefoundinhttp://www.pwc.com/us/en/cfodirect/issues/financial-instruments/index.jhtml.

Abbreviations used in the publication

ASC Accounting Standards CouncilFRS Singapore Financial Reporting StandardsIAS International Accounting StandardsIASB International Accounting Standards BoardIFRS International Financial Reporting StandardsINT FRS Interpretations of Financial Reporting Standard

6

Pra

ctic

al G

uid

e

New/revised standards and interpretations

Significantchangesin

Standards Scope and Measurement Presentation Details Definition andRecognition andDisclosures (Page)

Effective for annual periods beginning on or after 1 January 2014• FRS27(revised2011) 3 8 Separate Financial Statements

• FRS28(revised2011)Investments 3 10 in Associates and Joint Ventures

• FRS110ConsolidatedFinancialStatements 3 3 3 8

• FRS111JointArrangements 3 3 3 10

• FRS112DisclosureofInterestsin 3 3 12 Other Entities

• AmendmentstoFRSs110Consolidated 3 3 14 Financial Statements, FRS 111 Joint Arrangements and FRS 112 Disclosure of Interests in Other Entities

- Transitionguidance

• AmendmentstoFRS110Consolidated 3 3 3 15 Financial Statements, FRS 112 Disclosure

of Interests in Other Entities and FRS 27 Separate Financial Statements

- Exceptionfromconsolidationfor ‘investment entities’

• AmendmentstoFRS32Financial 3 17 instruments: Presentation

- Offsettingfinancialassetsand financialliabilities

• AmendmentstoFRS36Impairment 3 18 of Assets

- Recoverableamountdisclosuresfor non-financialassets

• AmendmentstoFRS39FinancialInstruments: 3 3 19 Recognition and Measurement

- Novationofderivativesandcontinuation of hedge accounting

• INTFRS121Levies 3 3 20

Practical Guide 2014 7

Pra

ctic

al G

uid

e

Significantchangesin

Standards Scope and Measurement Presentation Details Definition andRecognition andDisclosures (Page)

Effective for annual periods beginning on or after 1 July 2014• AmendmentstoFRS19(R)EmployeeBenefits 3 22

- DefinedBenefitPlans:EmployeeContributions

Effective for annual periods beginning on or after 1 July 2014

- Annual improvements 2012• AmendmentstoFRS102Share-basedPayment 3 24

• AmendmentstoFRS103BusinessCombinations 3 24

• AmendmentstoFRS108OperatingSegments 3 24

• AmendmentstoFRS16Property,Plant 3 25 andEquipment

• AmendmentstoFRS38IntangibleAssets 3 25

• AmendmentstoFRS24RelatedPartyDisclosures 3 25

- Annual improvements 2013• AmendmentstoFRS103BusinessCombinations 3 26

• AmendmentstoFRS113FairValueMeasurement 3 26

• AmendmentstoFRS40InvestmentProperty 3 26

Effective for annual periods beginning on or after 1 January 2016• FRS114RegulatoryDeferralAccounts 3 3 3 27

New/revised standards and interpretations

8

Pra

ctic

al G

uid

e

FRS 27 (revised 2011) Separate Financial Statements and FRS 110 Consolidated Financial Statements

TheASChasissuedFRS110,‘Consolidatedfinancialstatements’,aspartofthegroupoffivenewstandardsthataddressthescopeofthereportingentity.FRS110replacesalloftheguidanceoncontrolandconsolidationinFRS27,‘Consolidatedandseparatefinancialstatements’,andINTFRS12,‘Consolidation−specialpurposeentities’.FRS27isrenamed‘Separatefinancialstatements’;itcontinuestobeastandarddealingsolelywithseparatefinancialstatements.Theexistingguidanceforseparatefinancialstatementsisunchanged.

TherestofthepackageincludesFRS111,‘Jointarrangements’(seep10);FRS112,‘Disclosureofinterestsinotherentities’(seep12);andconsequentialamendmentstoFRS28,‘Investmentsin associates’.

Effective dateAnnualperiodsbeginningonorafter1January2014.Earlyadoptionispermitted.

What are the key provisions?FRS110changesthedefinitionofcontrolsothatthesamecriteriaareappliedtoallentitiestodeterminecontrol.Thisdefinitionissupportedbyextensiveapplicationguidancethataddressesthedifferentwaysinwhichareportingentity(investor)mightcontrolanotherentity(investee).Thechangeddefinitionandapplicationguidanceisnotexpectedtoresultinwidespreadchangeintheconsolidationdecisionsmadebyreportingentities,althoughsomeentitiescouldseesignificantchanges.

Allentitieswillneedtoconsiderthenewguidance.Thecoreprinciplethataconsolidatedentitypresentsaparentanditssubsidiariesasiftheyareasingleentityremainsunchanged,asdothemechanics of consolidation.

AccordingtoamendmentsmadetoFRS110,FRS112andFRS27,specificguidanceapplytoinvestment entities (see p15).

Thereviseddefinitionofcontrolfocusesontheneedtohavebothpowerandvariablereturnsbeforecontrolispresent.Poweristhecurrentabilitytodirecttheactivitiesthatsignificantlyinfluencereturns.Returnsmustvaryandcanbepositive,negativeorboth.

Thedeterminationofpowerisbasedoncurrentfactsandcircumstancesandiscontinuouslyassessed.Thefactthatcontrolisintendedtobetemporarydoesnotobviatetherequirementtoconsolidateanyinvesteeunderthecontroloftheinvestor.Votingrightsorcontractualrightsmaybeevidenceofpower,oracombinationofthetwomaygiveaninvestorpower.Powerdoesnothavetobeexercised.Aninvestorwithmorethanhalfthevotingrightswouldmeetthepowercriteriaintheabsenceofrestrictionsorothercircumstances.

Theapplicationguidanceincludesexamplesillustratingwhenaninvestormayhavecontrolwithlessthan half of the voting rights. When assessing if it controls the investee, an investor should consider potential voting rights, economic dependency and the size of its shareholding in comparison to otherholdings,togetherwithvotingpatternsatshareholdermeetings.Thislastconsiderationwillbringthenotionof‘defacto’controlfirmlywithintheconsolidationstandard.

Practical Guide 2014 9

Pra

ctic

al G

uid

e

FRS 110 also includes guidance on participating and protective rights. Participating rights give aninvestortheabilitytodirecttheactivitiesofaninvesteethatsignificantlyaffectthereturns.Protectiverights(oftenknownasvetorights)willonlygiveaninvestortheabilitytoblockcertaindecisionsoutsidetheordinarycourseofbusiness.

Thenewstandardincludesguidanceonagent/principalrelationships.Aninvestor(theagent)maybeengagedtoactonbehalfofasinglepartyoragroupofparties(the‘principals’).Certainpowerisdelegatedtotheagent−forexample,tomanageinvestments.Theinvestormayormaynothavecontroloverthepooledinvestmentfunds.FRS110includesanumberoffactorstoconsiderwhendeterminingwhethertheinvestorhascontrolorisactingasanagent.

ThereviseddefinitionofcontrolandassociatedguidancereplacesnotonlythedefinitionandguidanceinFRS27butalsothefourindicatorsofcontrolinINTFRS12.

Who is affected?FRS 110 has the potential to affect all reporting entities (investors) that control one or more investeesunderthereviseddefinitionofcontrol.Thedeterminationofcontrolandconsolidationdecisionsmaynotchangeformanyentities.However,thenewguidancewillneedtobeunderstoodandconsideredinthecontextofeachinvestor’sbusiness.

What do affected entities need to do?ManagementshouldconsiderwhetherFRS110willaffecttheircontroldecisionsandconsolidatedfinancialstatements.

TheASChasissuedFRS110,‘Consolidatedfinancialstatements’,aspartofthegroupoffivenewstandardsthataddressthescopeofthereportingentity.FRS110replacesalloftheguidanceoncontrolandconsolidationinFRS27,‘Consolidatedandseparatefinancialstatements’,andINTFRS12,‘Consolidation−specialpurposeentities’.FRS27isrenamed‘Separatefinancialstatements’;itcontinuestobeastandarddealingsolelywithseparatefinancialstatements.Theexistingguidanceforseparatefinancialstatementsisunchanged.

TherestofthepackageincludesFRS111,‘Jointarrangements’(seep10);FRS112,‘Disclosureofinterestsinotherentities’(seep12);andconsequentialamendmentstoFRS28,‘Investmentsin associates’.

Effective dateAnnualperiodsbeginningonorafter1January2014.Earlyadoptionispermitted.

10

Pra

ctic

al G

uid

e

FRS 28 (revised 2011) Investments in Associates and Joint Ventures and FRS 111 Joint Arrangements

TheASChasissuedthelongawaitedFRS111,‘Jointarrangements’,aspartofa‘package’offivenewstandardsthataddressthescopeofthereportingentity.

Changesinthedefinitionshavereducedthe‘types’ofjointarrangementstotwo:jointoperations and joint ventures. The existing policy choice of proportionate consolidation for jointlycontrolledentitieshasbeeneliminated.Equityaccountingismandatoryforparticipantsinjointventures.Entitiesthatparticipateinjointoperationswillfollowaccountingmuchlikethatforjoint assets or joint operations today.

Effective dateAnnualperiodsbeginningonorafter1January2014.Earlyadoptionispermitted.

What are the key provisions?

Underlying principlesAjointarrangementisdefinedasbeinganarrangementwheretwoormorepartiescontractuallyagreetosharecontrol.Jointcontrolexistsonlywhenthedecisionsaboutactivitiesthatsignificantlyaffectthereturnsofanarrangementrequiretheunanimousconsentofthepartiessharingcontrol.

Allpartiestoajointarrangementshouldrecognisetheirrightsandobligationsarisingfromthearrangement.Thefocusisnolongeronthelegalstructureofjointarrangements,butratheronhowrightsandobligationsaresharedbythepartiestothejointarrangement.Thestructureandform of the arrangement is only one of the factors to consider in assessing each party’s rights and obligations.Thetermsandconditionsagreedbytheparties(forexample,agreementsthatmaymodify the legal structure or form of the arrangement) and other relevant facts and circumstances shouldalsobeconsidered.

If the facts and circumstances change, a venturer needs to reassess:• whetherithasjointcontrol;and/or• thetypeofjointarrangementinwhichitisinvolved.

Types of joint arrangement and their measurementFRS111classifiesjointarrangementsaseitherjointoperationsorjointventures.The‘jointlycontrolledassets’classificationinFRS31,‘Interestsinjointventures’,hasbeenmergedintojointoperations,asbothtypesofarrangementsgenerallyresultinthesameaccountingoutcome.

A joint operation is a joint arrangement that gives parties to the arrangement direct rights to the assetsandobligationsfortheliabilities.Ajointoperatorwillrecognizeitsinterestbasedonitsinvolvementinthejointoperation(thatis,basedonitsdirectrightsandobligations)ratherthanonthe participation interest it has in the joint arrangement.

Ajointoperatorinajointoperationwillthereforerecogniseinitsownfinancialstatements:• itsassets,includingitsshareofanyassetsheldjointly;• itsliabilities,includingitsshareofanyliabilitiesincurredjointly;• itsrevenuefromthesaleofitsshareoftheoutputofthejointoperation;• itsshareoftherevenuefromthesaleoftheoutputbythejointoperation;and• itsexpenses,includingitsshareofanyexpensesincurredjointly.

Practical Guide 2014 11

Pra

ctic

al G

uid

e

A joint venture, in contrast, gives the parties rights to the net assets or outcome of the arrangement. Ajointventurerdoesnothaverightstoindividualassetsorobligationsforindividualliabilitiesofthejointventure.Instead,jointventurersshareinthenetassetsand,inturn,theoutcome(profitorloss)oftheactivityundertakenbythejointventure.JointventuresareaccountedforusingtheequitymethodinaccordancewithFRS28,‘Investmentsinassociates’.Entitiescannolongeraccountforan interest in a joint venture using the proportionate consolidation method.

Thestandardalsoprovidesguidanceforpartiesthatparticipateinjointarrangementsbutdonothave joint control.

Who is affected?Entitieswithexistingjointarrangementsorthatplantoenterintonewjointarrangementswillbeaffectedbythenewstandard.Theseentitieswillneedtoassesstheirarrangementstodeterminewhethertheyhaveinvestedinajointoperationorajointventureuponadoptionofthenewstandardor upon entering into the arrangement.

Entitiesthathavebeenaccountingfortheirinterestinajointventureusingproportionateconsolidationwillnolongerbeallowedtousethismethod;insteadtheywillaccountforthejointventureusingtheequitymethodoraccountfortheirshareofassetsandliabilitiesifitisassessedasajointoperation.Inaddition,theremaybesomeentitiesthatpreviouslyequity-accountedforinvestmentsthatmayneedtoaccountfortheirshareofassetsandliabilitiesnowthatthereislessfocus on the structure of the arrangement.

ThetransitionprovisionsofFRS111requireentitiestoapplythenewrulesatthebeginningoftheearliest period presented upon adoption. When transitioning from the proportionate consolidation methodtotheequitymethod,entitiesshouldrecognisetheirinitialinvestmentinthejointventureastheaggregateofthecarryingamountsthatwerepreviouslyproportionatelyconsolidated.Intransitioningfromtheequitymethodtoaccountingforassetsandliabilities,entitiesshouldrecognisetheirshareofeachoftheassetsandliabilitiesinthejointoperation,withspecificrulesdetailinghowtoaccountforanydifferencefromthepreviouscarryingamountoftheinvestment.

What do affected entities need to do?Managementofentitiesthatarepartytojointarrangementsshouldevaluatehowtherequirementsofthenewstandardwillaffectthewaytheyaccountfortheirexistingornewjointarrangements.Theaccountingmayhaveasignificantimpactonentities’financialresultsandfinancialposition,whichshouldbeclearlycommunicatedtostakeholdersassoonaspossible.

Managementshouldalsocarefullyconsidertheplannedtimingoftheiradoption.Iftheywishtoretainthecurrentaccountingforexistingarrangements,nowisthetimetoconsiderhowthetermsofthesearrangementscanbereworkedorrestructuredtoachievethis.

TheASChasissuedthelongawaitedFRS111,‘Jointarrangements’,aspartofa‘package’offivenewstandardsthataddressthescopeofthereportingentity.

Changesinthedefinitionshavereducedthe‘types’ofjointarrangementstotwo:jointoperations and joint ventures. The existing policy choice of proportionate consolidation for jointlycontrolledentitieshasbeeneliminated.Equityaccountingismandatoryforparticipantsinjointventures.Entitiesthatparticipateinjointoperationswillfollowaccountingmuchlikethatforjoint assets or joint operations today.

Effective dateAnnualperiodsbeginningonorafter1January2014.Earlyadoptionispermitted.

12

Pra

ctic

al G

uid

e

FRS 112 Disclosure of Interests in Other Entities

The ASC has issued FRS 112, ‘Disclosure of interests in other entities’, as part of the group of fivenewstandardsthataddressthescopeofthereportingentity.

FRS112setsouttherequireddisclosuresforentitiesreportingunderthetwonewstandards,FRS110,‘Consolidatedfinancialstatements’,andFRS111,‘Jointarrangements’;itreplacesthedisclosurerequirementscurrentlyfoundinFRS28,‘Investmentsinassociates’.FRS27isrenamed‘Separatefinancialstatements’andnowdealssolelywithseparatefinancialstatements.Theexistingguidanceanddisclosurerequirementsforseparatefinancialstatements are unchanged.

Effective dateAnnualperiodsbeginningonorafter1January2014.Earlyadoptionispermitted.

What are the key provisions?FRS112requiresentitiestodiscloseinformationthathelpsfinancialstatementreaderstoevaluatethenature,risksandfinancialeffectsassociatedwiththeentity’sinterestsinsubsidiaries,associates, joint arrangements and unconsolidated structured entities.

Tomeetthisobjective,disclosuresarerequiredinthefollowingareas.

Significant judgements and assumptionsSignificantjudgementsandassumptionsmadeindeterminingwhethertheentitycontrols,jointlycontrols,significantlyinfluencesorhassomeotherinterestsinotherentitiesinclude:• anassessmentofprincipal-agentrelationshipsinconsolidation;• determinationofthetypeofjointarrangement;and• anyoverrideofpresumptionsofsignificantinfluenceandcontrolwhenvotingrightsrangefrom

20% to 50%, and exceed 50%, respectively.

Interests in subsidiariesThisincludesinformationabout:• groupcomposition;• interestsofnon-controllinginterests(NCI)ingroupactivitiesandcashflows,andinformationabouteachsubsidiarythathasmaterialNCI,suchasname,principalplaceofbusinessandsummarisedfinancialinformation;

• significantrestrictionsonaccesstoassetsandobligationstosettleliabilities;• risksassociatedwithconsolidatedstructuredentities,suchasarrangementsthatcouldrequirethegrouptoprovidefinancialsupport;

• accountingforchangesintheownershipinterestinasubsidiarywithoutalossofcontrol−ascheduleoftheimpactonparentequityisrequired;

• accountingforthelossofcontrol–detailofanygain/lossrecognisedandthelineiteminthestatementofcomprehensiveincomeinwhichitisrecognised;and

• subsidiariesthatareconsolidatedusingdifferentyearends.

Practical Guide 2014 13

Pra

ctic

al G

uid

e

Interests in joint arrangements and associatesDetailed disclosures include:• thename,countryofincorporationandprincipalplaceofbusiness;• proportionofownershipinterestandmeasurementmethod;• summarisedfinancialinformation;• fairvalue(ifpublishedquotationsareavailable);• significantrestrictionsontheabilitytotransferfundsorrepayloans;• year-endsofjointarrangementsorassociatesifdifferentfromtheparent’s;and• unrecognisedshareoflosses,commitmentsandcontingentliabilities.

Interests in unconsolidated structured entitiesDetailed disclosures include:• thenature,purpose,size,activitiesandfinancingofthestructuredentity;• thepolicyfordeterminingstructuredentitiesthataresponsored;• asummaryofincomefromstructuredentities;• thecarryingamountofassetstransferredtostructuredentities;• therecognisedassetsandliabilitiesrelatingtostructuredentitiesandlineitemsinwhichthey arerecognised;

• themaximumlossarisingfromsuchinvolvement;and• informationonfinancialorothersupportprovidedtosuchentities,orcurrentintentionstoprovide

such support.

Who is affected?Allentitiesthathaveinterestsinsubsidiaries,associates,jointventuresorunconsolidatedstructuredentitiesarelikelytofaceincreaseddisclosurerequirements.

What do affected entities need to do?Managementshouldconsiderwhetheritneedstoimplementadditionalprocessestobeabletocompiletherequiredinformation.

The ASC has issued FRS 112, ‘Disclosure of interests in other entities’, as part of the group of fivenewstandardsthataddressthescopeofthereportingentity.

FRS112setsouttherequireddisclosuresforentitiesreportingunderthetwonewstandards,FRS110,‘Consolidatedfinancialstatements’,andFRS111,‘Jointarrangements’;itreplacesthedisclosurerequirementscurrentlyfoundinFRS28,‘Investmentsinassociates’.FRS27isrenamed‘Separatefinancialstatements’andnowdealssolelywithseparatefinancialstatements.Theexistingguidanceanddisclosurerequirementsforseparatefinancialstatements are unchanged.

Effective dateAnnualperiodsbeginningonorafter1January2014.Earlyadoptionispermitted.

14

Pra

ctic

al G

uid

e

Amendments to FRS 110 Consolidated Financial Statements, FRS 111 Joint Arrangements, FRS 112 Disclosure of Interests in Other Entities– Transition guidance

The ASC has issued ‘Amendments to FRS 110 Consolidated Financial Statements, FRS 111 JointArrangementsandFRS112DisclosureofInterestsinOtherEntities-Transitionguidance’.TheamendmentclarifiesthedateofinitialapplicationofFRS110andrequirementforcertaincomparative disclosures undere FRS 112.

Effective dateAnnualperiodsbeginningonorafter1January2014,retrospectivelyapplied.Earlyadoptionispermitted.

What is the issue?ThisamendmentclarifiesthatthedateofinitialapplicationisthefirstdayoftheannualperiodinwhichFRS110isadopted–forexample,1January2014foracalendar-yearentitythatadoptsFRS110in2014.EntitiesadoptingFRS110shouldassesscontrolatthedateofinitialapplication;thetreatmentofcomparativefiguresdependsonthisassessment.

TheamendmentalsorequirescertaincomparativedisclosuresunderFRS112upontransition.

The key changes in the amendment are:• iftheconsolidationconclusionunderFRS110differsfromFRS27/INTFRS12asatthedateofinitialapplication,theimmediatelyprecedingcomparativeperiod(thatis,2013foracalendar-yearentitythatadoptsFRS110in2014)isrestatedtobeconsistentwiththeaccountingconclusionunderFRS110,unlessimpracticable;

• anydifferencebetweenFRS110carryingamountsandpreviouscarryingamountsatthebeginningoftheimmediatelyprecedingannualperiodisadjustedtoequity;

• adjustmentstopreviousaccountingarenotrequiredforinvesteesthatwillbeconsolidatedunderbothFRS110andthepreviousguidanceinFRS27/INTFRS12asatthedateofinitialapplication,orinvesteesthatwillbeunconsolidatedunderbothsetsofguidanceasatthedateofinitialapplication;and

• comparativedisclosureswillberequiredforFRS112disclosuresinrelationtosubsidiaries,associates,andjointarrangements.However,thisislimitedonlytotheperiodthatimmediatelyproceedsthefirstannualperiodofFRS112application.Comparativedisclosuresarenotrequiredfor interests in unconsolidated structured entities.

Who is affected?Theamendmentwillaffectallreportingentities(investors)whoneedtoadoptFRSs110,111or112.

What do affected entities need to do?FRSpreparersshouldstartconsideringthetransitionamendment,andhowtheycanusetheexemptions granted to minimise implementation costs of FRSs 110, 111 and 112.

FRSpreparersshouldalsostartcollatingthecomparativedisclosureinformationrequiredbytheamendment.

Practical Guide 2014 15

Pra

ctic

al G

uid

e

Amendments to FRS 110 Consolidated Financial Statements, FRS 112 Disclosure of Interests in Other Entities and FRS 27 Separate Financial Statements– Exception from consolidation for ‘investment entities’

The ASC has issued an amendment to FRS 110 Consolidated Financial Statements, FRS 112 Disclosure of Interests in Other Entities and FRS 27 Separate Financial Statements’. This amendment applies to an ‘investment entity’. The amendment applies to an ‘investment entity’. Theamendmentdefinesaninvestmententity,introducesanexceptiontoconsolidationforinvestment entity and disclosures that an investment entity needs to make.

Effective dateAnnualperiodsbeginningonorafter1January2014,retrospectivelyapplied.Earlyadoptionispermitted.

What is the issue?

Definition of an investment Managementwillneedtomakeanassessmentofwhethertheentitymeetstheinvestmententitydefinition.

An investment entity is an entity that:• obtainsfundsfromoneormoreinvestorsforthepurposeofprovidingthoseinvestor(s)withinvestmentmanagementservices;

• commitstoitsinvestor(s)thatitsbusinesspurposeistoinvestfundssolelyforreturnsfromcapitalappreciation,investmentincomeorboth;and

• measuresandevaluatestheperformanceofsubstantiallyallofitsinvestmentsonafairvaluebasis.

Theamendmentsalsorequireasetoftypicalcharacteristicstobeconsidered.These,combinedwiththedefinition,areintendedtoallowforanappropriatebalancebetweencreatingaclearscopeandallowingjudgmentinassessingwhethereachentityisaninvestmententity.

The characteristics are: holding more than one investment, having more than one investor, having investorsthatarenotrelatedpartiesoftheentity,andhavingownershipinterestsintheformofequityorsimilarinterests.Theabsenceofoneormoreofthesecharacteristicsdoesnotpreventtheentityfromqualifyingasaninvestmententity.

Anentityisnotdisqualifiedfrombeinganinvestmententitybyperforminganyofthefollowingactivities:• provisionofinvestment-relatedservicestothirdpartiesandtoinvestors,evenwhensubstantial;

and• providingmanagementservicesandfinancialsupporttoinvestees,butonlywhenthesedonotrepresentseparatesubstantialbusinessactivityandarecarriedoutwiththeobjectiveofmaximising the investment return from investees.

The ASC has issued ‘Amendments to FRS 110 Consolidated Financial Statements, FRS 111 JointArrangementsandFRS112DisclosureofInterestsinOtherEntities-Transitionguidance’.TheamendmentclarifiesthedateofinitialapplicationofFRS110andrequirementforcertaincomparative disclosures undere FRS 112.

Effective dateAnnualperiodsbeginningonorafter1January2014,retrospectivelyapplied.Earlyadoptionispermitted.

16

Pra

ctic

al G

uid

e

Exception from consolidation and measurement of investees AnentitythatqualifiesasaninvestmententityisrequiredtoaccountforitssubsidiariesatfairvaluethroughprofitorlossinaccordancewithFRS39,‘Financialinstruments:recognitionandmeasurement’.Theonlyexceptionisforsubsidiariesthatprovideservicestotheentitythatarerelatedtotheentity’sinvestmentactivities,whichareconsolidated.

Accounting by a non-investment entity parent for the controlled investments of an investment entity subsidiaryAnentitymaybeaninvestmententitybutitsparentisnot.Forexample,aninvestmententityfundmaybecontrolledbyaninsurancecompanythatdoesnotqualifyasaninvestmententity.Thenon-investmententityparentisrequiredtoconsolidateallentitiesitcontrolsincludingthosecontrolledthroughaninvestmententity.Theinsurancegroupwillhavetoconsolidatethesubsidiariesoftheinvestmententity’sfundintheinsurancegroup’sfinancialstatements,eventhoughinthefund’sownfinancialstatementsitwillfairvalueitssubsidiaries.Therefore,whatisknownasthefairvalue‘roll-up’isnotpermittedtoanon-investmentparententity.

DisclosureRequireddisclosuresforanentitythatqualifiesasaninvestmententityincludethefollowing:• significantjudgementsandassumptionsmadeindeterminingthatanentitymeetsthedefinitionofaninvestmententity;

• reasonsforconcludingthatanentityisaninvestmententityeventhoughitdoesnothaveoneormoreofthetypicalcharacteristics;

• informationoneachunconsolidatedsubsidiary(name,countryofincorporation,proportionofownershipinterestheld);

• restrictionsonunconsolidatedsubsidiariestransferringfundstotheinvestmententity;• financialorothersupportprovidedtounconsolidatedsubsidiariesduringtheyear,wheretherewasn’tanycontractualobligationtodoso;and

• informationaboutany‘structuredentities’thattheinvestmententitycontrols(forexample,anycontractualarrangementstoprovideanyfinancialorothersupport).

Who is affected?Fundsorsimilarentitiesmaybeaffected.Somemayqualifyasinvestmententities,andsome may not.

What do affected entities need to do?Managementshouldlookcloselyattheguidancetodeterminewhetherornottheentityisaninvestment entity. For example, property funds that actively develop properties are unlikely to qualify,astheobjectiveisnotsolelycapitalappreciationorinvestmentincome.Ontheotherhand,alimitedlifefundsetuptobuyandsellorlistarangeofinfrastructuresubsidiariesmightqualifyasan investment entity.

Managementshouldstartcollatingcomparativeinformationasthechangeinaccountinghastobeapplied retrospectively in most cases.

Practical Guide 2014 17

Pra

ctic

al G

uid

e

Amendments to FRS 32 Financial Instruments: Presentation – Offsetting financial assets and financial liabilities

The ASC has issued ‘Amendment to FRS 32 Financial Instruments: Presentation – ‘Offsetting financialassetsandfinancialliabilities’. Thisamendmentclarifiessomeoftherequirementsforoffsettingfinancialassetsandfinancialliabilitiesonthestatementoffinancialposition.

Effective dateAnnualperiodsbeginningonorafter1January2014.Earlyadoptionispermitted.

What is the issue?

Key provisionsTheamendmentsdonotchangethecurrentoffsettingmodelinFRS32,whichrequiresanentitytooffsetafinancialassetandfinancialliabilityinthestatementoffinancialpositiononlywhentheentitycurrentlyhasalegallyenforceablerightofset-offandintendseithertosettletheassetandliabilityonanetbasisortorealisetheassetandsettletheliabilitysimultaneously.

Theamendmentsclarifythattherightofset-offmustbeavailabletoday–thatis,itisnotcontingentonafutureevent.Italsomustbelegallyenforceableforallcounterpartiesinthenormalcourseofbusiness,aswellasintheeventofdefault,insolvencyorbankruptcy.

The amendments also clarify that gross settlement mechanisms (such as through a clearing house) withfeaturesthatboth(i)eliminatecreditandliquidityriskand(ii)processreceivablesandpayablesinasinglesettlementprocess,areeffectivelyequivalenttonetsettlement;theywouldthereforesatisfy the FRS 32 criterion in these instances.

Masternettingagreementswherethelegalrightofoffsetisonlyenforceableontheoccurrenceof some future event, such as default of the counterparty, continue not to meet the offsetting requirements.

DisclosuresTheamendeddisclosureswillrequiremoreextensivedisclosuresthanarecurrentlyrequiredunderFRS.Thedisclosuresfocusonquantitativeinformationaboutrecognisedfinancialinstrumentsthatareoffsetinthestatementoffinancialposition,aswellasthoserecognisedfinancialinstrumentsthataresubjecttomasternettingorsimilararrangementsirrespectiveofwhethertheyareoffset.

Who is affected?Theseamendmentsprimarilyaffectfinancialinstitutions,astheywillberequiredtoprovideadditionaldisclosuresdescribedabove.However,otherentitiesthatholdfinancialinstrumentsthatmaybesubjecttooffsettingruleswillalsobeaffected.

What do affected entities need to do?Managementshouldbegingatheringtheinformationnecessarytopreparethenewdisclosurerequirements.ManagementwillalsoneedtoinvestigatewhethertheclarificationsoftheoffsettingprincipleinFRS32resultinanychangestowhattheyoffsetinthestatementoffinancialpositiontoday.Managementmayneedtoworkwiththeclearinghousestheyusetodeterminewhethertheirsettlementprocessescomplywiththenewrequirements.

18

Pra

ctic

al G

uid

e

Amendments to FRS 36 Impairment of Assets – Recoverable amount disclosures for non-financial assets

TheASChasissued‘AmendmentstoFRS36ImpairmentofAssets–Recoverableamountdisclosuresfornon-financialassets’.Thisamendmenthasmadesmallchangestothedisclosuresrequiredonrecoverableamountdeterminedbasedonfairvaluelesscostsofdisposal.

Effective dateAnnualperiodsbeginningonorafter1January2014.

What is the issue?ThisnarrowscopeamendmenthasmadesmallchangestothedisclosuresrequiredbyFRS36,Impairmentofassetswhenrecoverableamountisdeterminedbasedonfairvaluelesscosts of disposal.

TheASCmadeconsequentialamendmentstothedisclosurerequirementsofFRS36whenitissuedFRS113.Oneoftheamendmentswasdraftedmorewidelythanintended.Thislimitedscopeamendmentcorrectsthisandintroducesadditionaldisclosuresaboutfairvaluemeasurementswhentherehasbeenimpairmentorareversalofimpairment.

Key amendments TheASChasamendedFRS36asfollows:• toremovetherequirementtodiscloserecoverableamountwhenacashgeneratingunit(CGU)containsgoodwillorindefinitelivedintangibleassetsbuttherehasbeennoimpairment;

• torequiredisclosureoftherecoverableamountofanassetorCGUwhenanimpairmentlosshasbeenrecognisedorreversed;and

• torequiredetaileddisclosureofhowthefairvaluelesscostsofdisposalhasbeenmeasuredwhenanimpairmentlosshasbeenrecognisedorreversed.

Theamendmentswillimpactallpreparerswhorecogniseorreverseanimpairmentlossonnon-financialassets.

Who is affected?Theamendmentswillimpactallpreparerswhorecogniseorreverseanimpairmentlossonnon-financialassets.

What do affected entities need to do?Management should read the proposed amendments in their entirety to determine the impact.

Practical Guide 2014 19

Pra

ctic

al G

uid

e

Amendments to FRS 39 Financial Instruments: Recognition and Measurement – Novation of derivatives and continuation of hedge accounting

The ASC has issued ‘Amendments to FRS 39 Financial Instruments: Recognition and Measurement – Novation of derivatives and continuation of hedge accounting’. This amendment hasproviderelieffromdiscontinuinghedgeaccountingwhennovationofahedginginstrumenttoaCCPmeetsspecifiedcriteria.

Effective dateAnnualperiodsbeginningonorafter1January2014.Earlyadoptionispermitted.

What is the issue?Widespreadlegislativechangeshavebeenintroducedtoimprovetransparencyandregulatoryoversightofover-the-counter(OTC)derivatives.Asaresult,entitiesarenovatingderivativecontracts to central counterparties (CCPs) in an effort to reduce counterparty credit risk.

UnderFRS39,‘Financialinstruments:Recognitionandmeasurement’,anentityisrequiredtodiscontinuehedgeaccountingforaderivativethathasbeendesignatedasahedginginstrumentwherethederivativeisnovatedtoaCCP;thisisbecausetheoriginalderivativenolongerexists.ThenewderivativewiththeCCPisrecognisedatthetimeofthenovation.

TheASC,however,wasconcernedaboutthefinancialreportingeffectsthatwouldarisefromnovationsthatareaconsequenceoflawsorregulations.Asaresult,theASChasamendedFRS39toproviderelieffromdiscontinuinghedgeaccountingwhennovationofahedginginstrumenttoaCCPmeetsspecifiedcriteria.

Key amendmentsAccordingtotheamendments,therewillbenoexpirationorterminationofthehedginginstrumentif:• asaconsequenceoflawsorregulations,thepartiestothehedginginstrumentagreethataCCP,oranentity(orentities)actingasacounterpartyinordertoeffectclearingbyaCCP(‘theclearingcounterparty’),replacestheiroriginalcounterparty;and

• otherchanges,ifany,tothehedginginstrumentarelimitedtothosethatarenecessarytoeffect such replacement of the counterparty. These changes include changes in the contractual collateralrequirements,rightstooffsetreceivablesandpayablesbalances,andchargeslevied.

ThechangesarebroaderthanthoseproposedintheexposuredraftpublishedinFebruary2013,sincetheamendmentsrefertonovations‘asaconsequenceof’lawsorregulations,ratherthanthose‘requiredby’lawsorregulations.Thechangesalsoexpandthescopetoallowtheuseofclearingbrokers.

Who is affected?TheseamendmentsarebeneficialtoallentitiesapplyinghedgeaccountingthataresubjecttonovationofOTCderivatives,asdescribedabove.

TheASChasissued‘AmendmentstoFRS36ImpairmentofAssets–Recoverableamountdisclosuresfornon-financialassets’.Thisamendmenthasmadesmallchangestothedisclosuresrequiredonrecoverableamountdeterminedbasedonfairvaluelesscostsofdisposal.

Effective dateAnnualperiodsbeginningonorafter1January2014.

20

Pra

ctic

al G

uid

e

INT FRS 121 Levies

ASChasissuedINTFRS121Levies.INTFRS121setsouttheaccountingforanobligationto pay a levy that is not income tax. The interpretation could result in changes in the timing of recognitionofaliability,particularlyinconnectionwithleviesthataretriggeredbycircumstancesonaspecificdate.

Effective dateAnnualperiodsbeginningonorafter1January2014.

What is the issue?

Scope and objective Leviesareimposedbygovernmentsinaccordancewithlegislationandareoftenmeasuredbyreferencetoanentity’srevenues,assetsorliabilities(forexample,1%ofrevenue).

Theinterpretationaddressesdiversityinpracticearoundwhentheliabilitytopayalevyisrecognised.Practicediffersparticularlywhenalevyismeasuredbasedonfinancialdatarelatingtoaperiodbeforethedateonwhichtheobligationtopaythelevyarises.

INTFRS121addressestheaccountingforaliabilitytopayalevyrecognisedinaccordancewithFRS37,‘Provisions’,andtheliabilitytopayalevywhosetimingandamountiscertain.ItexcludesincometaxeswithinthescopeofFRS12,‘Incometaxes’.Itsapplicationtoliabilitiesarisingfromemissions trading schemes is optional.

Theinterpretationdoesnotaddresswhethertheliabilitytopayalevygivesrisetoanassetoranexpense.Entitieswillneedtoapplyotherstandardstodeterminetheaccountingfortheexpense.

Key provisionsINTFRS121addressesthefollowingissues:• Whatistheobligatingeventthatgivesrisetoaliabilitytopayalevy?

Theobligatingeventthatgivesrisetoaliabilitytopayalevyistheeventidentifiedbythelegislationthattriggerstheobligationtopaythelevy.

The fact that an entity is economically compelled to continue operating in a future period, or preparesitsfinancialstatementsunderthegoingconcernprinciple,doesnotcreateanobligationtopayalevythatwillarisefromoperatinginthefuture.

• Whenisaliabilitytopayalevyrecognised?

Aliabilitytopayalevyisrecognisedwhentheobligatingeventoccurs.Thismightariseatapointintime or progressively over time.

Theinterpretationalsorequiresthatanobligationtopayalevytriggeredbyaminimumthresholdisrecognisedwhenthethresholdisreached.

• Istheaccountingataninterimreportingdatethesameasatyearend?

Practical Guide 2014 21

Pra

ctic

al G

uid

e

Example 1

Levy A – 1% of current year revenues is due if the entity is operating on 1 January.

Aliabilityequalto1%ofthecurrentyearrevenuesisrecognisedprogressivelyasrevenueisgenerated.

Levy B – 1% of prior year revenues is due if the entity is operating on 1 January.

Aliabilityequalto1%oftheprioryearrevenuesisrecognisedinfullon1January.

Levy C–1%ofcurrentyearrevenuesisdueiftheentityisoperatingon31December. Aliabilityequalto1%ofthecurrentyearrevenuesisrecognisedinfullon31December.

Example 2

Levy D – 1% of current year revenues is due if the entity is operating on 1 January (same as LevyA)andifcurrentyearrevenueexceedsCU20m. Aliabilityequalto1%ofCU20misrecognisedinfullwhenthethresholdisreached.TheliabilityisthenincreasedprogressivelyasrevenueoverCU20misgenerated.

Thesamerecognitionprinciplesapplyininterimandannualfinancialstatements.Theobligationshouldnotbeanticipatedordeferredintheinterimfinancialreportifitwouldnotbeanticipatedordeferredinannualfinancialstatements.

Theinterpretationprovidesexamplesthatillustratetheaccountingfortheliabilitytopayalevy.

Who is affected?

INTFRS121willaffectentitiesthataresubjecttoleviesthatarenotincometaxeswithinthescopeofFRS12.Thesearecommoninmanycountriesandinmanyindustries–banking,retailandtransportation,tonameafew.

ASChasissuedINTFRS121Levies.INTFRS121setsouttheaccountingforanobligationto pay a levy that is not income tax. The interpretation could result in changes in the timing of recognitionofaliability,particularlyinconnectionwithleviesthataretriggeredbycircumstancesonaspecificdate.

Effective dateAnnualperiodsbeginningonorafter1January2014.

22

Pra

ctic

al G

uid

e

Amendments to FRS 19 (R) Employee Benefits – Defined Benefit Plans: Employee Contributions

TheASChasissued‘AmendmentstoFRS19EmployeeBenefits–DefinedBenefitPlansEmployeeContributions’.ThisamendmentclarifiestheapplicationofFRS19,‘EmployeeBenefits’(2011)–referredtoasFRS19R,toplansthatrequireemployeesorthirdpartiestocontributetowardsthecostofbenefits.Thisamendmentdoesnotaffecttheaccountingforvoluntarycontribution.

Effective dateAnnualperiodsbeginningonorafter1July2014.Earlyadoptionispermitted.

What is the issue?

Somepensionplansrequireemployeesorthirdpartiestocontributetotheplan.Thesecontributionsreducethecosttotheemployerofprovidingthebenefits.CommonpracticeunderthepreviousversionofFRS19wastodeductthecontributionsfromthecostofthebenefitsearnedintheyearinwhichthecontributionswerepaid.

FRS19R,whichisapplicabletoperiodscommencingonorafter1January2013,wasintendedtoclarifythetreatmentofcontributionsfromemployeesorthirdparties.However,therevisedguidanceisopentoarangeofpotentiallycomplexinterpretations,andcouldrequiremostentitiestochangethewayinwhichtheyaccountforthesecontributions.

The2011revisionstoFRS19distinguishedbetweenemployeecontributionsrelatedtoserviceandthosenotlinkedtoservice.Thecurrentamendmentfurtherdistinguishesbetweencontributionsthatarelinkedtoserviceonlyintheperiodinwhichtheyariseandthoselinkedtoserviceinmorethanoneperiod.Inourview,acontributionthatispayableoutofcurrentsalaryislinkedtoservice.

Theamendmentallowscontributionsthatarelinkedtoservice,anddonotvarywiththelengthofemployeeservice,tobedeductedfromthecostofbenefitsearnedintheperiodthattheserviceisprovided.

Theamendmentwillallow(butnotrequire)manyentitiestocontinueaccountingforemployeecontributionsusingtheirexistingaccountingpolicy,ratherthanspreadingthemovertheemployees’workinglives.

Contributionsthatarelinkedtoservice,andvaryaccordingtothelengthofemployeeservice,mustbespreadovertheserviceperiodusingthesameattributionmethodthatisappliedtothebenefits;thatmeanseitherinaccordancewiththeformulainthepensionplan,or,wheretheplanprovidesamateriallyhigherlevelofbenefitforserviceinlateryears,onastraightlinebasis.

Practical Guide 2014 23

Pra

ctic

al G

uid

e

Example 1

Aplanthatrequiresemployeestocontribute4%ofsalaryiftheyarebelowage40,and7%ofsalaryiftheyare40orabove,isanexampleofaplaninwhichemployeecontributionsarenotlinked to the length of service.

Thecontributionsarelinkedtoageandsalary,butarenotdependentonthelengthofservice.Sothecontributionswouldberecognisedasareductionofpensionexpenseintheyearinwhichtherelatedserviceisdelivered.

Thebenefitofemployeecontributionslinkedtothelengthofserviceisrecognisedinprofitorlossovertheemployee’sworkinglife.Itisnotclearhowthisshouldbedone,andavarietyofapproaches are likely to develop.

Contributionsthatarenotlinkedtoservicearereflectedinthemeasurementofthebenefitobligation.

Example 2

Aplanthatprovidesalumpsumbenefitonretirementof10%offinalsalaryforthefirsttenyearsofservice,plus20%offinalsalaryforeachsubsequentyearofservice,andrequiresemployeecontributionsequalto5%ofsalaryforthefirsttenyearsofserviceand8%thereafter,isaplaninwhichcontributionsarelinkedtothelengthofservice.

Thecontributionsvarywiththelengthofservice,aswellassalary,andsotheyhavetoberecognisedovertheworkinglife.Thebenefitearnedandtheemployeecontributionswouldberecognisedonastraightlinebasisovertheemployeesworkinglifeinthisexample.

Example 3

Apost-employmentmedicalinsuranceplan,wheretheemployeeisrequiredtomeetthefirstCU20permonthoftheinsurancepremium,isanarrangementinwhichthecontributionsarenotlinkedtoservice.Theexpectedfuturecontributionsfromtheemployee,whichwouldbepayableafterretirement,wouldbeincludedinthemeasurementofthebenefitobligation.

Who is affected?TheamendmenttoFRS19Rwillaffectanypost-employmentbenefitplanswhereemployeesorthirdpartiesarerequiredtomeetsomeofthecostoftheplan.

Theamendmentclarifiestheaccountingbyentitieswithplansthatrequirecontributionslinkedonlyto service in each period.

Entitieswithplansthatrequirecontributionsthatvarywithservicewillberequiredtorecognisethebenefitofthosecontributionsoveremployees’workinglives.Managementshouldconsiderhowitwillapplythatmodel.

TheASChasissued‘AmendmentstoFRS19EmployeeBenefits–DefinedBenefitPlansEmployeeContributions’.ThisamendmentclarifiestheapplicationofFRS19,‘EmployeeBenefits’(2011)–referredtoasFRS19R,toplansthatrequireemployeesorthirdpartiestocontributetowardsthecostofbenefits.Thisamendmentdoesnotaffecttheaccountingforvoluntarycontribution.

Effective dateAnnualperiodsbeginningonorafter1July2014.Earlyadoptionispermitted.

24

Pra

ctic

al G

uid

e

Standard/Interpretation

Amendment Effective date

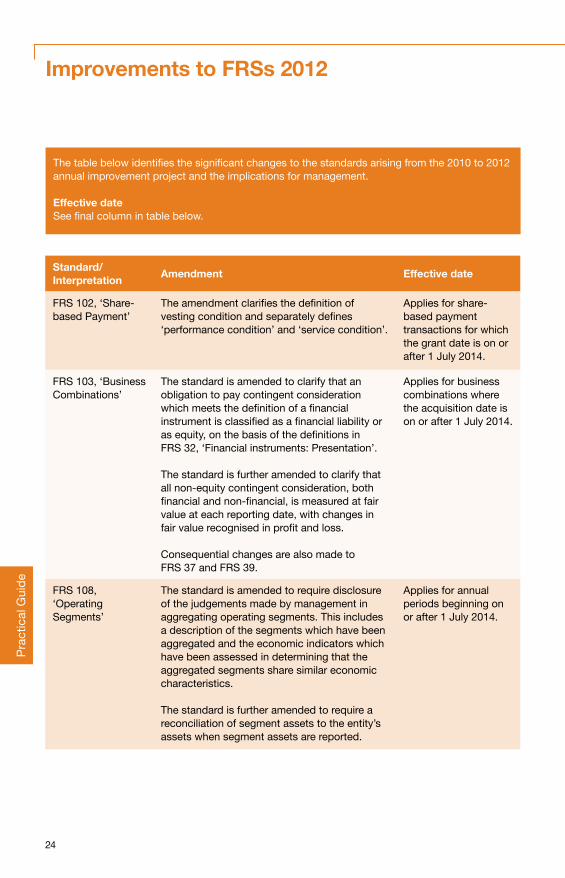

FRS102,‘Share-basedPayment’

Theamendmentclarifiesthedefinitionofvestingconditionandseparatelydefines‘performance condition’ and ‘service condition’.

Appliesforshare-basedpaymenttransactionsforwhichthe grant date is on or after 1 July 2014.

FRS 103, ‘Business Combinations’

The standard is amended to clarify that an obligationtopaycontingentconsiderationwhichmeetsthedefinitionofafinancialinstrumentisclassifiedasafinancialliabilityorasequity,onthebasisofthedefinitionsin FRS 32, ‘Financial instruments: Presentation’.

The standard is further amended to clarify that allnon-equitycontingentconsideration,bothfinancialandnon-financial,ismeasuredatfairvalueateachreportingdate,withchangesinfairvaluerecognisedinprofitandloss.

Consequentialchangesarealsomadeto FRS 37 and FRS 39.

Appliesforbusinesscombinationswheretheacquisitiondateison or after 1 July 2014.

FRS 108, ‘Operating Segments’

Thestandardisamendedtorequiredisclosureofthejudgementsmadebymanagementinaggregating operating segments. This includes adescriptionofthesegmentswhichhavebeenaggregatedandtheeconomicindicatorswhichhavebeenassessedindeterminingthattheaggregated segments share similar economic characteristics.

Thestandardisfurtheramendedtorequireareconciliation of segment assets to the entity’s assetswhensegmentassetsarereported.

Applies for annual periodsbeginningonor after 1 July 2014.

Improvements to FRSs 2012

Thetablebelowidentifiesthesignificantchangestothestandardsarisingfromthe2010to2012annual improvement project and the implications for management.

Effective dateSeefinalcolumnintablebelow.

Practical Guide 2014 25

Pra

ctic

al G

uid

e

Standard/Interpretation

Amendment Effective date

FRS 16, ‘Property, Plant and Equipment’and

FRS38,‘IntangibleAssets’

Bothstandardsareamendedtoclarifyhowthegross carrying amount and the accumulated depreciationaretreatedwhereanentityusesthe revaluation model.

The carrying amount of the asset is restated to the revalued amount.

Thesplitbetweengrosscarryingamountandaccumulated depreciation is treated in one of thefollowingways:

• eitherthegrosscarryingamountisrestatedinamannerconsistentwiththerevaluationof the carrying amount, and the accumulated depreciationisadjustedtoequalthedifferencebetweenthegrosscarryingamount and the carrying amount after taking intoaccountaccumulatedimpairmentlosses;or

• theaccumulateddepreciationiseliminatedagainst the gross carrying amount of the asset.

Applies for annual periodsbeginningonor after 1 July 2014.

FRS 24, ‘Related Party Disclosures’

The standard is amended to include, as a related party, an entity that provides key management personnel services to the reporting entity or to the parent of the reporting entity (‘the management entity’).

Thereportingentityisnotrequiredtodisclosethecompensationpaidbythemanagemententity to the management entity’s employees ordirectors,butitisrequiredtodisclosetheamountschargedtothereportingentitybythemanagement entity for services provided.

Applies for annual periodsbeginningon or after 1 July 2014.

Thetablebelowidentifiesthesignificantchangestothestandardsarisingfromthe2010to2012annual improvement project and the implications for management.

Effective dateSeefinalcolumnintablebelow.

26

Pra

ctic

al G

uid

e

Standard/Interpretation

Amendment Effective date

FRS 103, ‘Business Combinations’

The standard is amended to clarify that FRS 103 does not apply to the accounting for the formation of any joint arrangement under FRS 111.Theamendmentalsoclarifiesthatthescopeexemptiononlyappliesinthefinancialstatements of the joint arrangement itself.

Applies for annual periodsbeginningonor after 1 July 2014.

FRS 113, ‘Fair Value Measurement’

TheamendmentclarifiesthattheportfolioexceptioninFRS113,whichallowsanentitytomeasurethefairvalueofagroupoffinancialassetsandfinancialliabilitiesonanetbasis,appliestoallcontracts(includingnon-financialcontracts)withinthescopeofFRS39.

Applies for annual periodsbeginningon or after 1 July 2014. An entity shall apply the amendment prospectively from the beginningofthefirstannualperiodinwhichFRS 113 is applied.

FRS 40, ‘Investment Property’

The standard is amended to clarify that FRS 40 and FRS 103 are not mutually exclusive. The guidance in FRS 40 assists preparers todistinguishbetweeninvestmentpropertyandowner-occupiedproperty.Preparersalsoneed to refer to the guidance in FRS 103 todeterminewhethertheacquisitionofaninvestmentpropertyisabusinesscombination.

Applies for annual periodsbeginningonor after 1 July 2014.

Improvements to FRSs 2013

Thetablebelowidentifiesthesignificantchangestothestandardsarisingfromthe2011to2013annual improvement project and the implications for management.

Effective dateSeefinalcolumnintablebelow.

Practical Guide 2014 27

Pra

ctic

al G

uid

e

FRS 114 Regulatory Deferral

The ASC has issued FRS 114 ‘Regulatory Deferral’, an interim standard on the accounting for certainbalancesthatarisefromrate–regulatedactivities(‘regulatorydeferralaccounts’).

FRS114isonlyapplicabletoentitiesthatapplyFRS101asfirst-timeadoptersofFRS.Itpermits such entities, on adoption of FRS, to continue to apply their previous GAAP accounting policiesfortherecognition,measurement,impairmentandde-recognitionofregulatorydeferralaccounts. The interim standard also provides guidance on selecting and changing accounting policies(onfirst–timeadoptionorsubsequently)andonpresentationanddisclosure.

Thereiscurrentlynostandardthatspecificallyaddressesrate–regulatedactivities.TheobjectiveoftheinterimstandardistoallowentitiesadoptingFRStoavoidmajorchangesinaccountingpolicybeforecompletionofthebroaderIASBprojecttodevelopanIFRSonrate-regulatedactivities. A discussion paper on the project is expected later in 2014.

Effective dateAnnualperiodsbeginningonorafter1January2016.Earlyadoptionispermitted.

What are the key provisions?

ScopeFRS114onlyappliestofirst-timeadoptersofFRSthatapplyFRS101andconductrate–regulatedactivities.Rateregulationisaframeworkwherethepricethatanentitychargestoitscustomersforgoodsandservicesissubjecttooversightand/orapprovalbyanauthorisedbody.FRS114excludesentitiesthatareself–regulated(forexample,ifpricesareregulatedsolelybytheentity’sowngoverningbody).

Entities in the scope of FRS 114 are permitted to continue applying previous GAAP accounting policies for regulatory deferral accounts. Changes to existing policies are restricted. Any change mustmakethefinancialstatementsmorerelevantandnolessreliable,asdescribedbyFRS8.

Entities are not permitted to change accounting policies to start recognising regulatory deferral accountbalancesthatwerenotrecognisedunderpreviousGAAP.Entitiescan,however,recognisenewbalancesthatariseasaresultofachangeinaccountingpolicy(suchasonthefirst–timeadoptionofFRSorforchangestoFRS).Forexample,ifanewdeferralaccountarisesfromtheadoptionofnewFRSemployeebenefitsguidance,thenewaccountisaccountedforconsistentlywiththeentity’spreviousGAAPaccountingpolicies.

Recognition, measurement, impairment and de-recognitionAn entity is permitted to continue applying its previous GAAP accounting policies for the recognition andmeasurementofregulatorydeferralaccountsonfirst–timeadoption.Theinterimstandarddoesnotincludeanyfurtherguidanceonrecognition,measurement,impairmentandde-recognition.

PreviousGAAPaccountingpoliciesareonlyappliedtobalancesthatarenototherwisecoveredbyspecificFRSs.Thatis,otherspecificFRSsshouldbeappliedfirst,andonlyanyresidualbalanceisaccounted for under FRS 114.

Thetablebelowidentifiesthesignificantchangestothestandardsarisingfromthe2011to2013annual improvement project and the implications for management.

Effective dateSeefinalcolumnintablebelow.

28

Pra

ctic

al G

uid

e

Otherstandardsmightalsoneedtobeappliedtoregulatorydeferralaccountstoreflectthemappropriatelyinthefinancialstatements.Forexample,theentitywouldapplyitspreviousGAAPaccountingpolicytotheimpairmentofregulatorydeferralaccountbalances,butitwouldapplytheFRSimpairmentguidancetocashgeneratingunitsthatcontainsuchbalances.

JudgementwillberequiredtodeterminewhatotherstandardsmightbeapplicableandhowtheymightinteractwithpreviousGAAPaccountingpolicies.

PresentationBalancesarisingfromtheapplicationofFRS114arepresentedseparatelyinthebalancesheetandthe statement of comprehensive income.

Aseparatelineitemispresentedinthebalancesheetfortotalregulatorydeferraldebitbalancesandtotalregulatorydeferralcreditbalances,followingasub–totalofallotherassetsandliabilities.Thedistinctionbetweencurrentandnon–currentbalancesisnotpresentedonthebalancesheet,andoffsettingisnotpermitted,althoughthisinformationmightbedisclosedelsewhere.

Thetotalmovementinallregulatorydeferralaccountsissplitbetweenothercomprehensiveincome(OCI)andprofitandloss.Theamountrecordedinprofitandlossisseparatelypresentedasasinglelineitemafterasub–totalforprofitandloss.TheamountrecordedinOCIispresentedintwolineitems,basedonwhethertheamountrelatestoitemsthatwillorwillnotbesubsequentlyreclassifiedtoprofitandloss.MovementsareclassifiedinOCIwherethebalancesrelatetoitemsrecognised in OCI.

An entity that presents earnings per share (EPS) should present, in the income statement, EPS excluding and including the movement in the regulatory deferral accounts.

DisclosuresThedisclosurerequirementsaddressinformationaboutthenatureandriskoftheregulationandtheeffectonthefinancialstatements,including:• adescriptionofthenatureandextentofrateregulation;• howthefuturerecoveryorreversalofeachbalanceisaffectedbyrisksanduncertainties;• thebasisonwhichtheregulatorydeferralaccountbalancesarerecognisedandmeasured;and• areconciliationofthebalancesfromthebeginningtotheendoftheperiod.

Who is affected?FRS114willaffectfirst–timeadoptersofFRSthatcurrentlyrecognisebalancesarisingfromrateregulationunderpreviousGAAPaccountingpolicies.Thisiscommonintheutilitiesindustry,buttheinterimstandardmightaffectotherindustrieswherepricesareregulated.

What do affected entities need to do?Entitiesthatwillapplytheguidanceshouldbegintoconsidertheimplicationsinconnectionwiththeadoption of FRS.

Thebroaderprojectonrate–regulatedactivitiesisongoing.TheIASBisexpectedtoissueadiscussionpaperontheprojectlaterin2014toseekinitialviewsontheaccountingforrate–regulated activities.

Practical Guide 2014 29

Pra

ctic

al G

uid

e

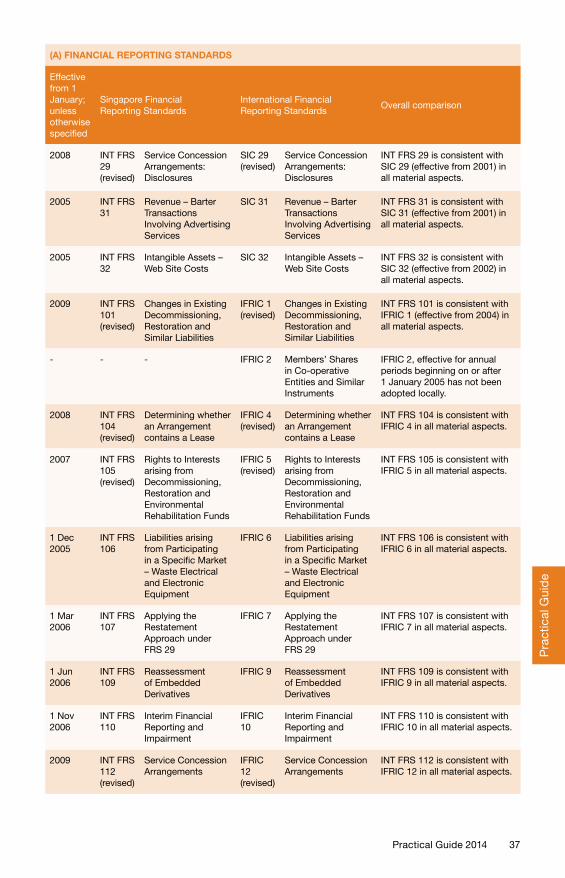

(A) FINANCIAL REPORTING STANDARDS

Effective from 1 January;unless otherwisespecified

Singapore Financial Reporting Standards

International Financial Reporting Standards

Overall comparison

2009 FRS 1 (revised)

Presentation of Financial Statements

IAS 1 (revised)

Presentation of Financial Statements

FRS1isconsistentwithIAS1inall material aspects.

2009 FRS 2 (revised)

Inventories IAS 2 (revised)

Inventories FRS2isconsistentwithIAS2inall material aspects.

2009 FRS 7 (revised)

Statement of Cash Flows

IAS 7 (revised)

Statement of Cash Flows

FRS7isconsistentwithIAS7 (effective from 1994) in all material aspects.

2009 FRS 8 (revised)

Accounting Policies, Changes in Accounting Estimates and Errors

IAS 8 (revised)

Accounting Policies, Changes in Accounting Estimates and Errors

FRS8isconsistentwithIAS8inall material aspects.

2007 FRS 10 (revised)

Events after the Reporting Period

IAS 10 (revised)

Events after the Reporting Period

FRS10isconsistentwithIAS10 in all material aspects.

2009 FRS 11 (revised)

Construction Contracts

IAS 11 (revised)

Construction Contracts

FRS11isconsistentwithIAS11 (effective from 1995) in all material aspects.

2007 FRS 12 (revised)

Income Taxes IAS 12 (revised)

Income Taxes FRS12isconsistentwithIAS12 (effective from 1998) in all material aspects, except for accounting for unremitted foreign income.

UnderRecommendedAccounting Practice (RAP) 8issuedbytheInstituteofCertifiedPublicAccountantsofSingapore (ICPAS), no deferred tax is accounted for temporary difference arising from foreign income not yet remitted to Singapore if:

Differences between Singapore Financial Reporting Standards and International Financial Reporting Standards

Asat30September2014

30

Pra

ctic

al G

uid

e

(A) FINANCIAL REPORTING STANDARDS

Effective from 1 January;unless otherwisespecified

Singapore Financial Reporting Standards

International Financial Reporting Standards

Overall comparison

(a) theentityisabletocontrolthe timing of the reversal of thetemporarydifference;and

(b) itisprobablethatthetemporary difference willnotreverseintheforeseeablefuture.

UnderIAS12,deferredtaxisrequiredtobeaccountedfortemporary difference arising from such unremitted foreign income.

2009 FRS 16 (revised)

Property, Plant and Equipment(PPE)

IAS 16 (revised)

Property, Plant and Equipment(PPE)

FRS16isconsistentwithIAS16in all material aspects, except thatFRS16givesthefollowingexemption:

“Foranenterprisewhichhad:revalueditsPPEbefore 1 January 1984 (in accordance withtheprevailingaccountingstandardatthetime);orperformedanyone-offrevaluationonitsPPEbetween1 January 1984 and 31December1996(bothdatesinclusive),therewillbenoneedfor the enterprise to revalue itsassetsinaccordancewithparagraph 29 of FRS 16.”

“One-offrevaluation”meansanyinstancewhereanitemofPPEwasrevaluedonlyoncebetween1January1984and31December1996(bothdatesinclusive).

Where an item of PPE has beenrevaluedmorethanonceduring this period, the company should:

(a) explainwhytheparticularitemofPPEshouldbeexempted;and

(b) obtaintheauditor’sconcurrence of the explanation.

IAS 16 does not include the aboveexemption.

Practical Guide 2014 31

Pra

ctic

al G

uid

e

(A) FINANCIAL REPORTING STANDARDS

Effective from 1 January;unless otherwisespecified

Singapore Financial Reporting Standards

International Financial Reporting Standards

Overall comparison

2007 FRS 17(revised)

Leases IAS 17 (revised)

Leases FRS17isconsistentwithIAS17 in all material aspects.

2005 FRS 18 Revenue IAS 18 Revenue FRS18isconsistentwithIAS18 (effective from 1995) in all material aspects except for revenuerecognitionofpre-solduncompleted properties.

INTFRS115prescribestheaccounting treatment for sale of uncompleted properties. Please refertosectionBbelowonInterpretations for details.

UnderIFRS,suchrevenueisgenerally recognised after the properties are completed and handedovertothebuyers.

2013 FRS 19(revised)

EmployeeBenefits IAS 19 (revised)

EmployeeBenefits FRS19isconsistentwithIAS19 in all material aspects.

2005 FRS 20 Accounting for Government Grants and Disclosure of Government Assistance

IAS 20 Accounting for Government Grants and Disclosure of Government Assistance

FRS20isconsistentwithIAS20 (effective from 1984) in all material aspects.

2006 FRS 21(revised)

The Effects of Changes in Foreign Exchange Rates

IAS 21 (revised)

The Effects of Changes in Foreign Exchange Rates

FRS21isconsistentwith IAS 21 in all material aspects.

2009 FRS 23(revised)

BorrowingCosts(revised)

IAS 23 (revised)

BorrowingCosts(revised)

FRS23isconsistentwith IAS 23 in all material aspects.

2011 FRS 24(revised)

Related Party Disclosures

IAS 24 (revised)

Related Party Disclosures

FRS24isconsistentwith IAS 24 in all material aspects.

2005 FRS 26 Accounting and ReportingbyRetirementBenefitPlans

IAS 26 Accounting and ReportingbyRetirementBenefitPlans

FRS26isconsistentwithIAS26 (effective from 1990) in all material aspects.

2014 FRS 27 (revised)

Separate Financial Statements

IAS 27 Separate Financial Statements

FRS27isconsistentwithIAS27 in all material aspects, except in:

• oneoftheconditionsfor exemption from consolidation. This dissimilarityisasidentifiedinFRS110;and

• effectivedates:IAS27(revised) is effective for annualperiodsbeginningonor after 1 January 2013.

32

Pra

ctic

al G

uid

e

(A) FINANCIAL REPORTING STANDARDS

Effective from 1 January;unless otherwisespecified

Singapore Financial Reporting Standards

International Financial Reporting Standards

Overall comparison

2014 FRS 28 (revised)

Investments in Associates and Joint Ventures

IAS 28 (revised)

Investments in Associates and Joint Ventures

FRS28isconsistentwithIAS28 in all material aspects, except in:

• oneoftheconditionsforexemptionfromequityaccounting. This dissimilarity isasidentifiedinFRS110;and

• effectivedates:IAS28(revised) is effective for annualperiodsbeginningonor after 1 January 2013.

2005 FRS 29 Financial Reporting inHyperinflationaryEconomies

IAS 29 Financial Reporting inHyperinflationaryEconomies

FRS29isconsistentwithIAS29 (effective from 1990) in all material aspects.

2005 FRS 31 Interests in Joint Ventures

IAS 31 Interests in Joint Ventures

FRS31isconsistentwithIAS31in all material aspects, except in one of the conditions for exemption from proportionate consolidationorequityaccounting. The dissimilarity is asidentifiedinFRS27.

NotethatIAS31isbeingreplacedbyIFRS11,whichis effective for annual periods beginningonorafter1January2013.

Correspondingly, FRS 31, is beingreplacedbyFRS111,whichiseffectiveforannualperiodsbeginningonorafter 1 January 2014.

2007 – for listed companies

2008 – for non-listedcompanies

FRS 32(revised)

Financial Instruments:Presentation

IAS 32 Financial Instruments:Presentation

FRS32isconsistentwithIAS32 (effective from 2007) in all material aspects.

2009 FRS 33(revised)

Earnings per Share IAS 33 (revised)

Earnings per Share FRS33isconsistentwithIAS33 in all material aspects.

2009 FRS 34(revised)

Interim Financial Reporting

IAS 34 (revised)

Interim Financial Reporting

FRS34isconsistentwithIAS34 in all material aspects.

2009 FRS 36(revised)

Impairment of Assets

IAS 36 (revised)

Impairment of Assets

FRS36isconsistentwithIAS36 in all material aspects.

Practical Guide 2014 33

Pra

ctic

al G

uid

e

(A) FINANCIAL REPORTING STANDARDS

Effective from 1 January;unless otherwisespecified

Singapore Financial Reporting Standards

International Financial Reporting Standards

Overall comparison

2006 FRS 37(revised)

Provisions, ContingentLiabilitiesand Contingent Assets

IAS 37 (revised)

Provisions, ContingentLiabilitiesand Contingent Assets

FRS37isconsistentwithIAS37 (effective from 1999) in all material aspects.

2009 FRS 38(revised)

IntangibleAssets IAS 38 (revised)

IntangibleAssets FRS38isconsistentwithIAS38 in all material aspects.

2007 FRS 39(revised)

Financial Instruments: Recognition and Measurement

IAS 39 (revised)

Financial Instruments: Recognition and Measurement

FRS39isconsistentwithIAS39 in all material aspects except for the effect of difference in transition dates.

2007 FRS 40(revised)

Investment property IAS 40 (revised)

Investment property FRS40isconsistentwithIAS40 (effective from 2005) in all material aspects.

2005 FRS 41 Agriculture IAS 41 Agriculture FRS41isconsistentwithIAS41 in all material aspects.

2005 – for listed companies

2006 – for other companies

FRS 102

Share-basedPayment

IFRS 2 Share-basedPayment

FRS102isconsistentwithIFRS 2 in all material aspects, except for their effective dates fornon-listedcompanies.Fornon-listedcompanies,FRS102is effective for annual periods beginningonorafter1January2006,whilstIFRS2iseffectiveforannualperiodsbeginningonor after 1 January 2005.

Additionally,IFRS2willapplyto:

(a) share-basedpaymenttransactionsthatweregranted on or after 7 November2002andhadnotyetvestedby1January2005;and

(b) share-basedpaymenttransactionsmadebefore7November2002,whichweresubsequentlymodified.

FRS102replaces“7November2002”with“22November2002”.

1 Jul 2009

FRS 103 (revised)

Business Combinations

IFRS 3 (revised)

Business Combinations

FRS103isconsistentwithIFRS3 in all material aspects.

2007 FRS 104(revised)

Insurance Contracts IFRS 4(revised)

Insurance Contracts FRS104isconsistentwithIFRS4 in all material aspects.

34

Pra

ctic

al G

uid

e

(A) FINANCIAL REPORTING STANDARDS

Effective from 1 January;unless otherwisespecified

Singapore Financial Reporting Standards

International Financial Reporting Standards

Overall comparison

2009 FRS 105 (revised)

Non-currentAssetsHeld-for-Saleand Discontinued Operations

IFRS 5 (revised)

Non-currentAssetsHeld-for-Saleand Discontinued Operations

FRS105isconsistentwithIFRS5 in all material aspects.

2009 FRS 106(revised

Exploration for and Evaluation of Mineral Resources

IFRS 6(revised)

Exploration for and Evaluation of Mineral Resources

FRS106isconsistentwithIFRS6 in all material aspects.

2007 – for listed companies

2008 – for non-listedcompanies

FRS 107

Financial Instruments: Disclosures

IFRS 7 Financial Instruments: Disclosures

FRS107isconsistentwithIFRS7 in all material aspects, except fortheireffectivedatesfornon-listed companies.

Fornon-listedcompanies,FRS 107 is effective for annual periodsbeginningonorafter1January2008,whilstIFRS7is effective for annual periods beginningonorafter1January2007.

2009 FRS 108

Operating Segments IFRS 8 Operating Segments FRS108isconsistentwithIFRS8 in all material aspects.

2013 FRS 113

Fair ValueMeasurement

IFRS 13 Fair ValueMeasurement

FRS113isconsistentwithIFRS13 in all material aspects.

2014 FRS 110

Consolidated Financial Statements

IFRS 10 Consolidated Financial Statements

FRS110isconsistentwithIFRS 10 in all material aspects, except in:

• oneoftheconditionsfor exemption from consolidation.

FRS110requirestheultimate holding company or any intermediate parent of a company that seeks exemption from consolidation to produce consolidated financialstatementsthatareavailableforpublicuse.Theseconsolidatedfinancialstatements need not comply withanyspecificaccountingframework.

IFRS10requirestheultimate holding company or any intermediate parent of a company that seeks exemption from consolidation to produce consolidated financialstatementsthatareavailableforpublicuseandcomplywithIFRS.

• effectivedates:IFRS10iseffective for annual periods beginningonorafter 1 January 2013.

Practical Guide 2014 35

Pra

ctic

al G

uid

e

(A) FINANCIAL REPORTING STANDARDS

Effective from 1 January;unless otherwisespecified

Singapore Financial Reporting Standards

International Financial Reporting Standards

Overall comparison

2014 FRS 111

Joint Arrangements IFRS 11 Joint Arrangements FRS111isconsistentwithIFRS 11 in all material aspects, except in:

• oneoftheconditionsforexemption from proportionate consolidationorequityaccounting. The dissimilarity isasidentifiedinFRS110.

• effectivedates:IFRS11iseffective for annual periods beginningonorafter 1 January 2013.

2014 FRS 112

Disclosure of Interests in Other Entities

IFRS 12 Disclosure of Interests in Other Entities

FRS112isconsistentwithIFRS12 in all material aspects except for the effective dates. IFRS 12 is effective for annual periods beginningonorafter1January2013.

2016 FRS 114

Regulatory Deferral Accounts

IFRS 14 Regulatory Deferral Accounts

FRS114isconsistentwithIFRS14 in all material aspects.

- - IFRS 15 Revenue from contractswithcustomers

IFRS 15 is effective for annual periodsbeginningonorafter 1 January 2017.

IFRS15hasnotbeenadoptedlocally.

- - IFRS 9 Financial Instruments

IFRS 9 is effective for annual periodsbeginningonorafter 1 January 2018.

IFRS9hasnotbeenadoptedlocally.

2005 INT FRS 7

Introduction of the Euro

SIC 7 Introduction of the Euro

INTFRS7isconsistentwithSIC 7 (effective from 1998) in all material aspects.

2005 INT FRS 10

Government Assistance – No specificRelationtoOperating Activities

SIC 10 Government Assistance – No SpecificRelationtoOperating Activities

INTFRS10isconsistentwithSIC 10 (effective from 1998) in all material aspects.

36

Pra

ctic

al G

uid

e

(A) FINANCIAL REPORTING STANDARDS

Effective from 1 January;unless otherwisespecified

Singapore Financial Reporting Standards

International Financial Reporting Standards

Overall comparison

2005 INT FRS 12

Consolidation – Special Purpose Entities

SIC 12 Consolidation – Special Purpose Entities

INTFRS12isconsistentwithSIC 12 (effective from 1999) in all material aspects.

NotethatSIC12hasbeenincorporated into IFRS 10, whichiseffectiveforannualperiodsbeginningonorafter 1 January 2013.

Correspondingly, INT FRS 12 hasbeenincorporatedintoFRS110,whichiseffectiveforannualperiodsbeginningonorafter 1 January 2014.

2005 INT FRS 13

Jointly Controlled Entities–Non-Monetary ContributionsbyVenturers

SIC 13 Jointly Controlled Entities–Non-Monetary ContributionsbyVenturers

INTFRS13isconsistentwithSIC 13 (effective from 1999) in all material aspects.

NotethatSIC13hasbeenincorporated into IAS 28 (revised),whichiseffectiveforannualperiodsbeginningonorafter 1 January 2013 and has beenadoptedlocally.

Correspondingly, INT FRS 13 hasbeenincorporatedintoFRS111,whichiseffectiveforannualperiodsbeginningonorafter 1 January 2014.

2005 INT FRS 15

Operating Leases – Incentives

SIC 15 Operating Leases – Incentives

INTFRS15isconsistentwithSIC 15 (effective from 1999) in all material aspects.

2005 INT FRS 21

Income Taxes – Recovery of RevaluedNon-DepreciableAssets

SIC 21 Income Taxes – Recovery of RevaluedNon-DepreciableAssets

INTFRS21isconsistentwithSIC 21 (effective from 2000) in all material aspects.

NotethatINTFRS21hasbeenincorporated into FRS 12, whichiseffectiveforannualperiodsbeginningonorafter 1 January 2012.

2005 INT FRS 25

Income Taxes – Changes in the Tax Status of an Enterprise or its Shareholders

SIC 25 Income Taxes – Changes in the Tax Status of an Enterprise or its Shareholders

INTFRS25isconsistentwithSIC 25 (effective from 2000) in all material aspects.

2005 INT FRS 27

Evaluating the SubstanceofTransactions Involving the Legal Form of a Lease

SIC 27 Evaluating the SubstanceofTransactions Involving the Legal Form of a Lease

INTFRS27isconsistentwithSIC 27 (effective from 2001) in all material aspects.

Practical Guide 2014 37

Pra

ctic

al G

uid

e

(A) FINANCIAL REPORTING STANDARDS

Effective from 1 January;unless otherwisespecified

Singapore Financial Reporting Standards

International Financial Reporting Standards

Overall comparison

2008 INT FRS 29(revised)

Service Concession Arrangements: Disclosures

SIC 29(revised)

Service Concession Arrangements: Disclosures

INTFRS29isconsistentwithSIC 29 (effective from 2001) in all material aspects.

2005 INT FRS 31

Revenue – Barter Transactions Involving Advertising Services

SIC 31 Revenue – Barter Transactions Involving Advertising Services

INTFRS31isconsistentwithSIC 31 (effective from 2001) in all material aspects.

2005 INT FRS 32

IntangibleAssets–WebSiteCosts

SIC 32 IntangibleAssets–WebSiteCosts

INTFRS32isconsistentwithSIC 32 (effective from 2002) in all material aspects.

2009 INT FRS 101(revised)

Changes in Existing Decommissioning, Restoration and SimilarLiabilities

IFRIC 1(revised)

Changes in Existing Decommissioning, Restoration and SimilarLiabilities

INTFRS101isconsistentwithIFRIC 1 (effective from 2004) in all material aspects.

- - - IFRIC 2 Members’SharesinCo-operativeEntities and Similar Instruments

IFRIC 2, effective for annual periodsbeginningonorafter1January2005hasnotbeenadopted locally.

2008 INT FRS 104(revised)

Determiningwhetheran Arrangement contains a Lease

IFRIC 4(revised)

Determiningwhetheran Arrangement contains a Lease

INTFRS104isconsistentwithIFRIC 4 in all material aspects.

2007 INT FRS 105(revised)

Rights to Interests arising from Decommissioning, Restoration and Environmental RehabilitationFunds

IFRIC 5(revised)

Rights to Interests arising from Decommissioning, Restoration and Environmental RehabilitationFunds

INTFRS105isconsistentwithIFRIC 5 in all material aspects.

1 Dec 2005

INT FRS 106

Liabilitiesarisingfrom Participating inaSpecificMarket– Waste Electrical and Electronic Equipment

IFRIC 6 Liabilitiesarisingfrom Participating inaSpecificMarket– Waste Electrical and Electronic Equipment

INTFRS106isconsistentwithIFRIC 6 in all material aspects.

1 Mar 2006

INT FRS 107

Applying the Restatement Approach under FRS 29

IFRIC 7 Applying the Restatement Approach under FRS 29

INTFRS107isconsistentwithIFRIC 7 in all material aspects.

1 Jun 2006

INT FRS 109

Reassessment ofEmbeddedDerivatives

IFRIC 9 Reassessment ofEmbeddedDerivatives

INTFRS109isconsistentwithIFRIC 9 in all material aspects.

1 Nov 2006

INT FRS 110

Interim Financial Reporting and Impairment

IFRIC 10

Interim Financial Reporting and Impairment

INTFRS110isconsistentwithIFRIC 10 in all material aspects.

2009 INT FRS 112(revised)

Service Concession Arrangements

IFRIC 12(revised)

Service Concession Arrangements

INTFRS112isconsistentwithIFRIC 12 in all material aspects.

38

Pra

ctic

al G

uid

e

(A) FINANCIAL REPORTING STANDARDS

Effective from 1 January;unless otherwisespecified

Singapore Financial Reporting Standards

International Financial Reporting Standards

Overall comparison

1 Jul 2008

INT FRS 113

Customer Loyalty Programmes

IFRIC 13

Customer Loyalty Programmes

INTFRS113isconsistentwithIFRIC 13 in all material aspects.

2008 INT FRS 114

FRS 19 –The LimitonaDefinedBenefitAsset,Minimum Funding Requirementsandtheir Interaction

IFRIC 14

FRS 19 –The LimitonaDefinedBenefitAsset,Minimum Funding Requirementsandtheir Interaction