Embed Size (px)

Citation preview

DELIVERING THE ANALYTICAL BROKER

NATIONAL PROPERTY PRACTICE

OUR MISSIONTO SUPPORT ALL OF OUR OFFICES AND CONSISTENTLY DELIVER THE BEST POSSIBLE PROPERTY INSURANCE SOLUTIONS FOR OUR CLIENTS ON A UNIFORM BASIS ACROSS OUR FIRM

Willis North America Inc.

Brookfield Place200 Liberty Street, 7th FloorNew York, New York 10281-1003United StatesTel: +1 212 915 8888

Willis Limited

The Willis Building51 Lime StreetLondon, EC3M 7DQUnited KingdomTel: +44 (0)20 3124 6000

www.willis.com

50790/02/15

PROPERTY CONTACTS

DAVID FINNIS National Property Practice [email protected] 302 3848

NORTHEAST REGIONAL MANAGERNEW YORK , NYPaul Richardson [email protected] 915 7939

SENIOR RESOURCE Kevin [email protected] 291 1541

ATLANTIC REGIONAL MANAGERRADNOR, PA Sue Winterode [email protected] 254 5697

SENIOR RESOURCESteve [email protected] 915 7959

BERMUDA Ivan [email protected] 1 278 0046

SOUTH REGIONAL MANAGERATLANTA , GANancy [email protected] 302 3852

LONDONGarret [email protected] 0 20 7558 9327

MIDWEST REGIONAL MANAGERCHICAGO, ILDick Forand [email protected] 288 7343

ANALYTICS/CAT MODELING Ben [email protected] 349 4010

WEST REGIONAL MANAGER DENVER, CO David [email protected] 996 6723

BOILER & MACHINERYEarl [email protected] 351 7532

CALIFORNIA REGIONAL MANAGERLOS ANGELES , CAFrank Beuthin [email protected] 607 6341

INFORMATION SYSTEMSNora [email protected] 872 3252

DELIVERING THE ANALYTICAL BROKERIn today’s world as the Analytical Property Broker, it is truly an exciting time as we continue to evolve in this area. One only needs to think back a decade ago to contrast and compare how we analyzed our clients’ risks/exposures versus the diagnostic process we utilize today.

In 2015, the diagnostic process includes the following:

Ȗ “CAT” perils modeling (RMS/AIR)

Ȗ Flood Zone Identification tools (RiskMeter)

Ȗ Satellite imagery location drill down capability (Pictometry)

Ȗ Risk Mapping with quick and sleek exhibits (SpatialKey)

Ȗ Benchmarking via a deep dive in data (WillPLACE)

Ȗ Desktop Value Appraisal (Marshall*Swift*Boeckh, now part of CoreLogic)

Our main message in 2015 … WATCH THIS SPACE! Willis is committed to take our value proposition in this critical area to the next level. Our clients expect us to have command of the insurance market … that is a given. Now we must be able to take that experience/knowledge and supplement it with the ability to be conversant with our full arsenal of analytic tools and models.

This is what our clients expect from their Analytical Property Broker … and our clients should notice that it is our ambition to exceed their expectations in this space.

Dave FinnisNational Property Practice Leader

RiskMeter Online

50790_BROCHURE_NPP_2015.FINAL.indd 1 3/25/2015 10:07:25 AM

ROLLOUT OF ANOTHER WAR - WILLIS ALL RISKThe last version of Willis All Risk (WAR) was released in November 2011; we are now releasing the 2015 version: WAR Policy - January 2015.doc

The revisions range from cosmetic to material changes in coverage.

Some examples of the material changes are: Ȗ New coverages, such as Downzoning and Special Time Element - Cancellation

Coverage Ȗ Aggregate limits for CAT perils of Earthquake and Flood are set up so that the

sublimit for each different area (e.g., Earthquake, California Earthquake, All Other High Hazard Earthquake) is a dedicated separate aggregate tower of capacity and does not erode the overall limit

Ȗ Added Historical Landmark Valuation Ȗ Minimized counties where Tier One Named Storm deductible applies or where

High Hazard Earthquake limits/deductibles apply

We continue to emphasize to our clients and underwriters the main spirit of WAR (in contrast to the acronym): a policy that is clear and strives to provide contract certainty while, at the same time, is broad in coverage and yet still acceptable to the underwriting community.

If you have questions or for additional information, please call one of the NPP WAR Committee members listed below:

Ben Phillips +1 650 349 4010 [email protected]

Adrine Weisbeck +1 763 302 7254 [email protected]

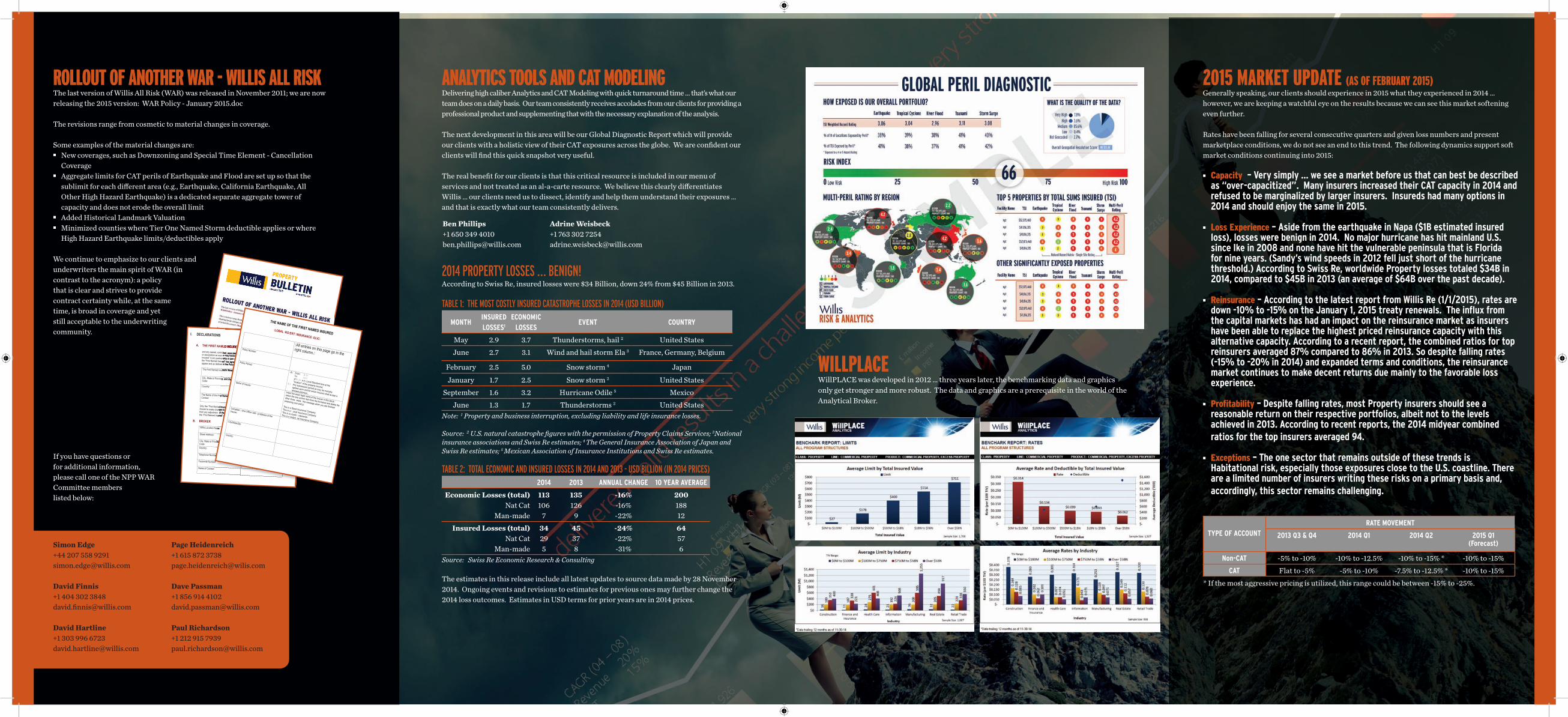

ANALYTICS TOOLS AND CAT MODELING Delivering high caliber Analytics and CAT Modeling with quick turnaround time … that’s what our team does on a daily basis. Our team consistently receives accolades from our clients for providing a professional product and supplementing that with the necessary explanation of the analysis.

The next development in this area will be our Global Diagnostic Report which will provide our clients with a holistic view of their CAT exposures across the globe. We are confident our clients will find this quick snapshot very useful.

The real benefit for our clients is that this critical resource is included in our menu of services and not treated as an al-a-carte resource. We believe this clearly differentiates Willis … our clients need us to dissect, identify and help them understand their exposures … and that is exactly what our team consistently delivers.

2014 PROPERTY LOSSES … BENIGN! According to Swiss Re, insured losses were $34 Billion, down 24% from $45 Billion in 2013.

TABLE 1: THE MOST COSTLY INSURED CATASTROPHE LOSSES IN 2014 (USD BILLION)

MONTHINSURED LOSSES1

ECONOMIC LOSSES

EVENT COUNTRY

May 2.9 3.7 Thunderstorms, hail 2 United StatesJune 2.7 3.1 Wind and hail storm Ela 3 France, Germany, Belgium

February 2.5 5.0 Snow storm 4 Japan

January 1.7 2.5 Snow storm 2 United StatesSeptember 1.6 3.2 Hurricane Odile 5 Mexico

June 1.3 1.7 Thunderstorms 2 United StatesNote: 1 Property and business interruption, excluding liability and life insurance losses.

Source: 2 U.S. natural catastrophe figures with the permission of Property Claims Services; 3National insurance associations and Swiss Re estimates; 4 The General Insurance Association of Japan and Swiss Re estimates; 5 Mexican Association of Insurance Institutions and Swiss Re estimates.

TABLE 2: TOTAL ECONOMIC AND INSURED LOSSES IN 2014 AND 2013 - USD BILLION (IN 2014 PRICES) 2014 2013 ANNUAL CHANGE 10 YEAR AVERAGE

Economic Losses (total) Nat Cat

Man-made

113106

7

135126

9

-16%-16%-22%

20018812

Insured Losses (total) Nat Cat

Man-made

34295

45378

-24%-22%-31%

64576

Source: Swiss Re Economic Research & Consulting

The estimates in this release include all latest updates to source data made by 28 November 2014. Ongoing events and revisions to estimates for previous ones may further change the 2014 loss outcomes. Estimates in USD terms for prior years are in 2014 prices.

2015 MARKET UPDATE (AS OF FEBRUARY 2015)Generally speaking, our clients should experience in 2015 what they experienced in 2014 … however, we are keeping a watchful eye on the results because we can see this market softening even further.

Rates have been falling for several consecutive quarters and given loss numbers and present marketplace conditions, we do not see an end to this trend. The following dynamics support soft market conditions continuing into 2015:

Ȗ Capacity – Very simply ... we see a market before us that can best be described as “over-capacitized”. Many insurers increased their CAT capacity in 2014 and refused to be marginalized by larger insurers. Insureds had many options in 2014 and should enjoy the same in 2015.

Ȗ Loss Experience – Aside from the earthquake in Napa ($1B estimated insured loss), losses were benign in 2014. No major hurricane has hit mainland U.S. since Ike in 2008 and none have hit the vulnerable peninsula that is Florida for nine years. (Sandy’s wind speeds in 2012 fell just short of the hurricane threshold.) According to Swiss Re, worldwide Property losses totaled $34B in 2014, compared to $45B in 2013 (an average of $64B over the past decade).

Ȗ Reinsurance – According to the latest report from Willis Re (1/1/2015), rates are down -10% to -15% on the January 1, 2015 treaty renewals. The influx from the capital markets has had an impact on the reinsurance market as insurers have been able to replace the highest priced reinsurance capacity with this alternative capacity. According to a recent report, the combined ratios for top reinsurers averaged 87% compared to 86% in 2013. So despite falling rates (-15% to -20% in 2014) and expanded terms and conditions, the reinsurance market continues to make decent returns due mainly to the favorable loss experience.

Ȗ Profitability – Despite falling rates, most Property insurers should see a reasonable return on their respective portfolios, albeit not to the levels achieved in 2013. According to recent reports, the 2014 midyear combined ratios for the top insurers averaged 94.

Ȗ Exceptions – The one sector that remains outside of these trends is Habitational risk, especially those exposures close to the U.S. coastline. There are a limited number of insurers writing these risks on a primary basis and, accordingly, this sector remains challenging.

TYPE OF ACCOUNTRATE MOVEMENT

2013 Q3 & Q4 2014 Q1 2014 Q2 2015 Q1(Forecast)

Non-CAT -5% to -10% -10% to -12.5% -10% to -15% * -10% to -15%CAT Flat to -5% -5% to -10% -7.5% to -12.5% * -10% to -15%

* If the most aggressive pricing is utilized, this range could be between -15% to -25%.

I. DECLARATIONS

A. THE FIRST NAMED INSURED and any owned, controlled, associated or affiliated subsidiary, company, corporation, organization, trust or association as now or may hereinafter be constitu ted or acquired; the interest of the “First Named Insured” in any partnership or joint venture, to the extent not otherwise insured; and any entity for which the “First Named Insured” has agreed to provide insurance, as their respective rights and interests appear and as defined in the Policy wording. The First Named Insured’s Street Address:

City, State or Province, and Zip/Postal Code:

Country:

The Name of the First Named Insured’s Contact:

Only the “First Named Insured” is authorized to cancel this policy and/or otherwise agree with this Insurer to make changes to the terms and conditions contained herein. Any return premium resulting from any adjustment of the premium or cancellation of the policy prior to expiration shall be returned to the “First Named Insured” unless otherwise instructed in writing by the “First Named Insured”. B. BROKER

Willis Location Name:

Street Address:

City, State or Province, and Zip/Postal Code: Country:

Telephone Number:

Facsimile Number:

Name of Contact:

THE NAME OF THE FIRST NAMED INSURED �LOBAL �RO�ERT� INSURANCE �OLIC�

�All entries on this page go in the right column.�

Policy Number:

Policy Period:

�A� From: �� � � To: � � � � at �� :� � a.m. Local Standard time at the

“location” of the property insured. �� � Any subsequent period as may be mutually

agreed upon and for which Insurers shall accept a

renewal premium.

Name of Insurer:

Insert the exact legal name of the Insurer in this block;

select the one correct item from the list below and delete the

other three. �elete this message when you are finished

preparing your policy�. This is a Stock Insurance Company This is a � utual Insurance Company This is a Lloyds � nderwriter This is a �ecipro cal Insurance Company

Complete � ome Office �ailin g Address of the

Insurer:

City/State/Zip:

Country:

Page Heidenreich+1 615 872 [email protected]

Dave Passman+1 856 914 [email protected]

Paul Richardson +1 212 915 7939 [email protected]

Simon Edge+44 207 558 9291 [email protected]

David Finnis +1 404 302 3848 [email protected]

David Hartline +1 303 996 6723 [email protected]

WILLPLACEWillPLACE was developed in 2012 … three years later, the benchmarking data and graphics only get stronger and more robust. The data and graphics are a prerequisite in the world of the Analytical Broker.

50790_BROCHURE_NPP_2015.FINAL.indd 2 3/25/2015 10:07:34 AM