Embed Size (px)

Citation preview

Delivering growth in the new steel horizon

24 September 2008

Michel Wurth – Member of Group Management Board

1

Disclaimer

•Forward-Looking Statements This document may contain forward-looking information and statements about

ArcelorMittal and its subsidiaries. These statements include financial projections and estimates and their underlying assumptions, statements regarding plans, objectives and expectations with respect to future operations, products and services, and statements regarding future performance. Forward-looking statements may be identified by the words “believe,” “expect,” “anticipate,” “target” or similar expressions. Although ArcelorMittal’s management believes that the expectations reflected in such forward-looking statements are reasonable, investors and holders of ArcelorMittal’s securities are cautioned that forward-looking information and statements are subject to numerous risks and uncertainties, many of which are difficult to predict and generally beyond the control of ArcelorMittal, that could cause actual results and developments to differ materially and adversely from those expressed in, or implied or projected by, the forward-looking information and statements. These risks and uncertainties include those discussed or identified in the filings with the Luxembourg Stock Market Authority for the Financial Markets (Commission de Surveillance du Secteur Financier) and the United States Securities and Exchange Commission (the “SEC”) made or to be made by ArcelorMittal or the entities to which it is successor (including Mittal Steel Company N.V. (“Mittal Steel”), including Mittal Steel’s Annual Report on Form 20-F filed with the SEC. ArcelorMittal undertakes no obligation to publicly update its forward-looking statements, whether as a result of new information, future events, or otherwise.

2

Agenda

• A global leader with a unique strategy• The new steel horizon• Delivering growth plan• Conclusion

3

A global leader with a unique strategy

4

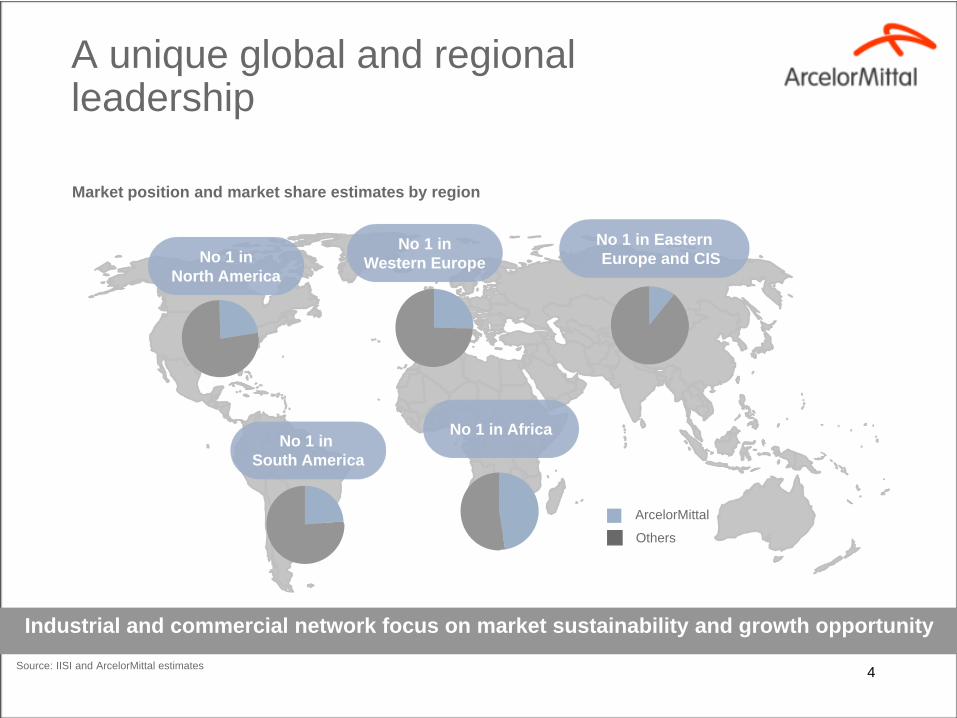

No 1 inNorth America

No 1 in South America

No 1 inWestern Europe

No 1 in EasternEurope and CIS

No 1 in Africa

A unique global and regional leadership

Market position and market share estimates by region

Source: IISI and ArcelorMittal estimates

Industrial and commercial network focus on market sustainability and growth opportunity

ArcelorMittal

Others

5

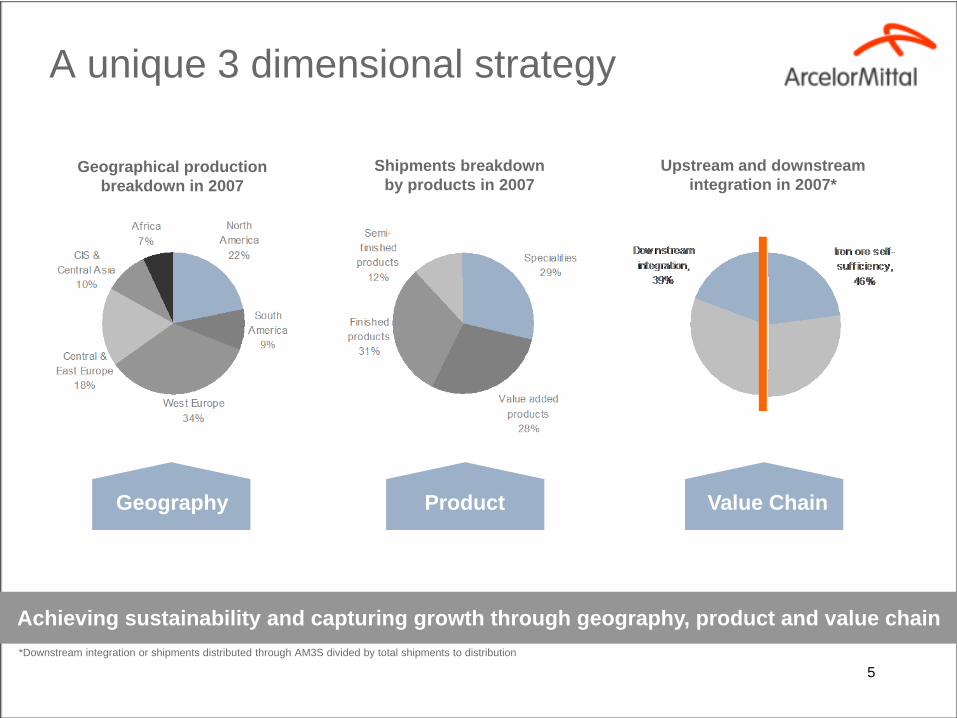

A unique 3 dimensional strategy

Achieving sustainability and capturing growth through geography, product and value chain*Downstream integration or shipments distributed through AM3S divided by total shipments to distribution

Geographical production breakdown in 2007

Shipments breakdown by products in 2007

Upstream and downstream integration in 2007*

ProductGeography Value Chain

6

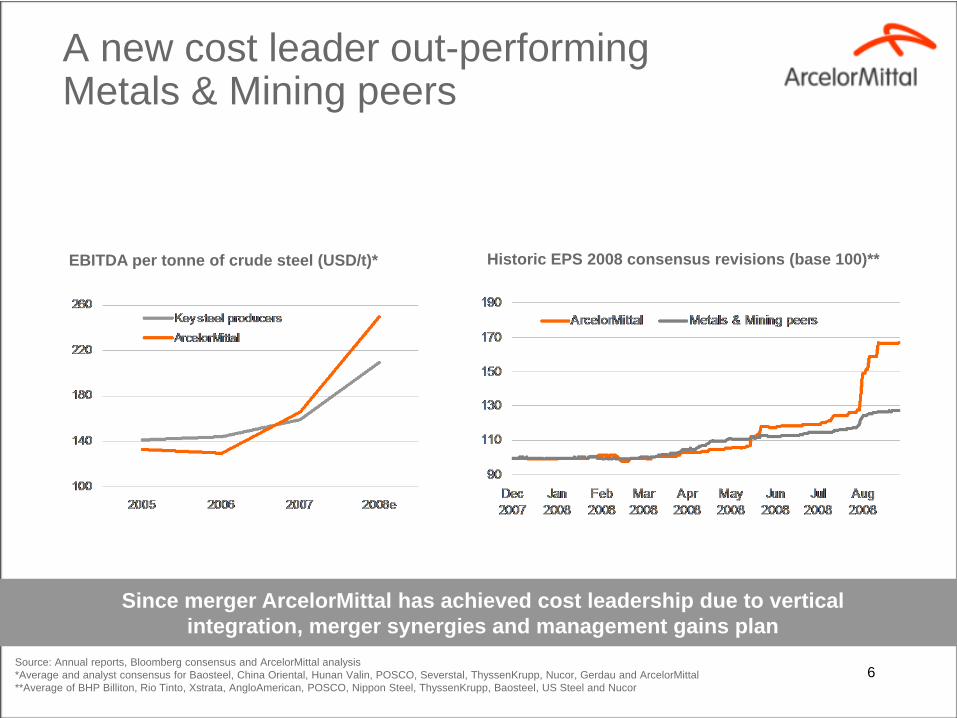

A new cost leader out-performing Metals & Mining peers

Since merger ArcelorMittal has achieved cost leadership due to vertical integration, merger synergies and management gains plan

EBITDA per tonne of crude steel (USD/t)*

Source: Annual reports, Bloomberg consensus and ArcelorMittal analysis*Average and analyst consensus for Baosteel, China Oriental, Hunan Valin, POSCO, Severstal, ThyssenKrupp, Nucor, Gerdau and ArcelorMittal**Average of BHP Billiton, Rio Tinto, Xstrata, AngloAmerican, POSCO, Nippon Steel, ThyssenKrupp, Baosteel, US Steel and Nucor

Historic EPS 2008 consensus revisions (base 100)**

7

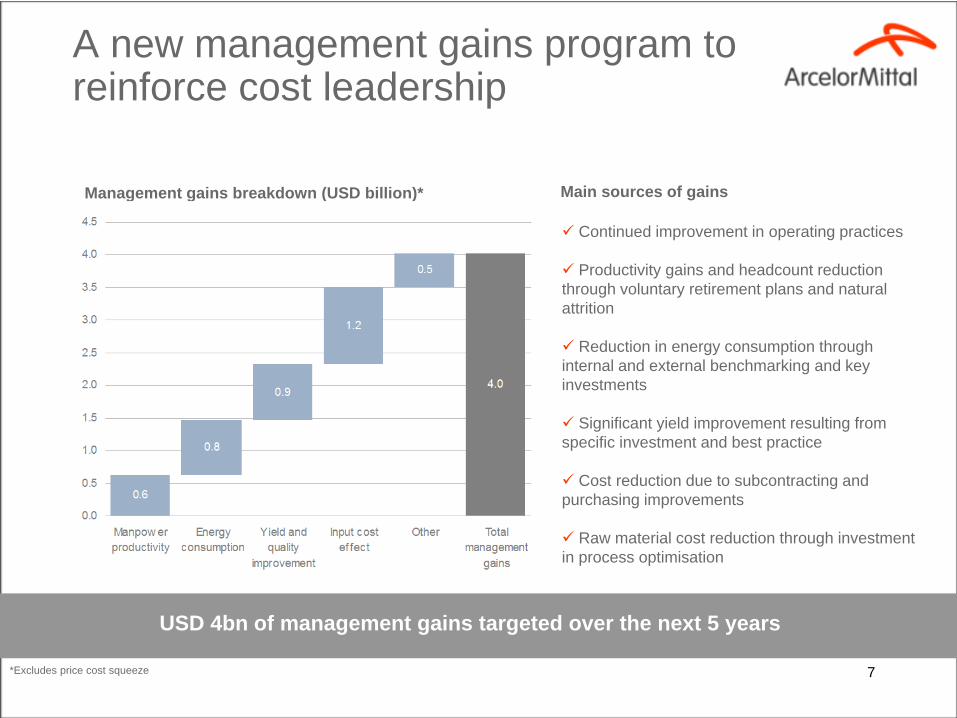

A new management gains program to reinforce cost leadership

36*Excludes price cost squeeze

Management gains breakdown (USD billion)*

Continued improvement in operating practices

Productivity gains and headcount reduction through voluntary retirement plans and natural attrition

Reduction in energy consumption through internal and external benchmarking and key investments

Significant yield improvement resulting from specific investment and best practice

Cost reduction due to subcontracting and purchasing improvements

Raw material cost reduction through investment in process optimisation

Main sources of gains

USD 4bn of management gains targeted over the next 5 years

8

The new steel horizon

9

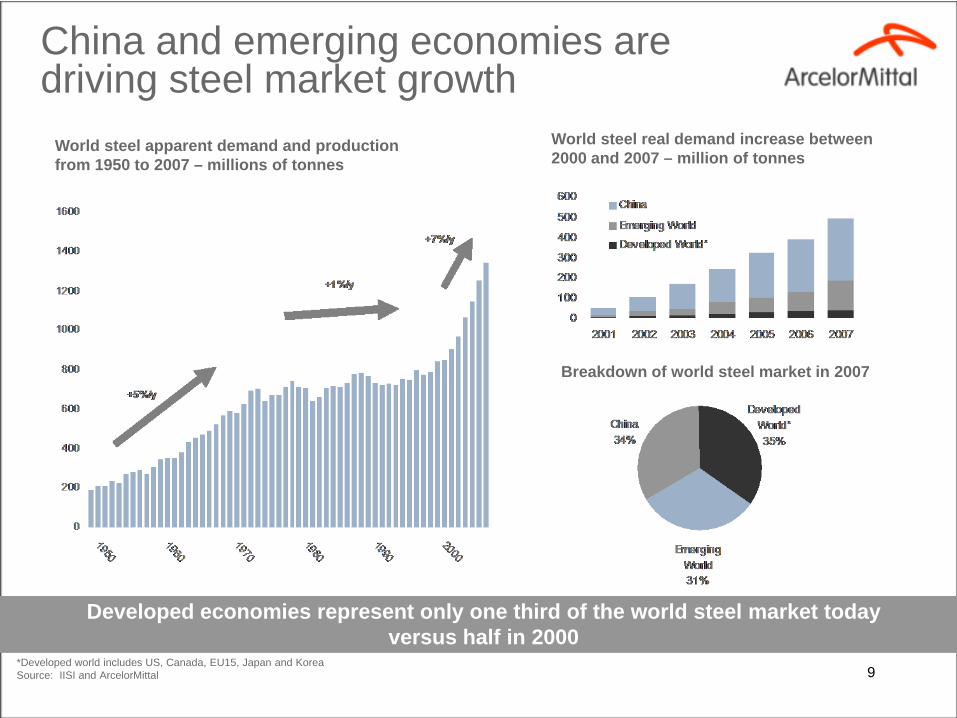

World steel apparent demand and production from 1950 to 2007 – millions of tonnes

China and emerging economies are driving steel market growth

Developed economies represent only one third of the world steel market today versus half in 2000

World steel real demand increase between 2000 and 2007 – million of tonnes

*Developed world includes US, Canada, EU15, Japan and KoreaSource: IISI and ArcelorMittal

Breakdown of world steel market in 2007

10

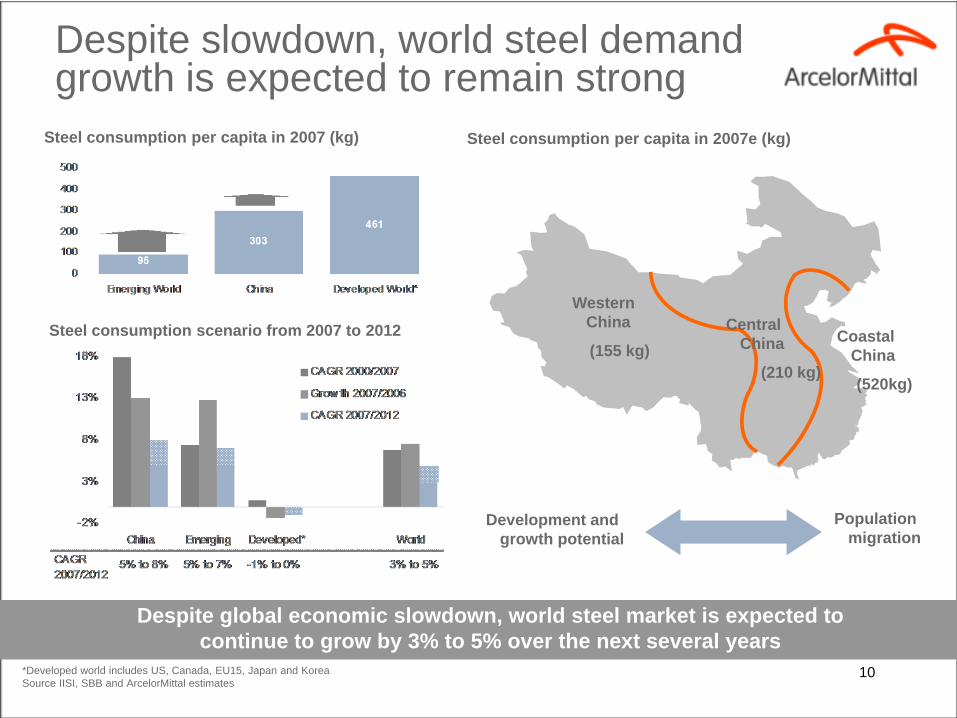

Despite slowdown, world steel demand growth is expected to remain strong

Despite global economic slowdown, world steel market is expected to continue to grow by 3% to 5% over the next several years

*Developed world includes US, Canada, EU15, Japan and KoreaSource IISI, SBB and ArcelorMittal estimates

Steel consumption scenario from 2007 to 2012

Steel consumption per capita in 2007e (kg)

Western China

(155 kg)Coastal

China

(520kg)

Central China

(210 kg)

Development and growth potential

Population migration

Steel consumption per capita in 2007 (kg)

11

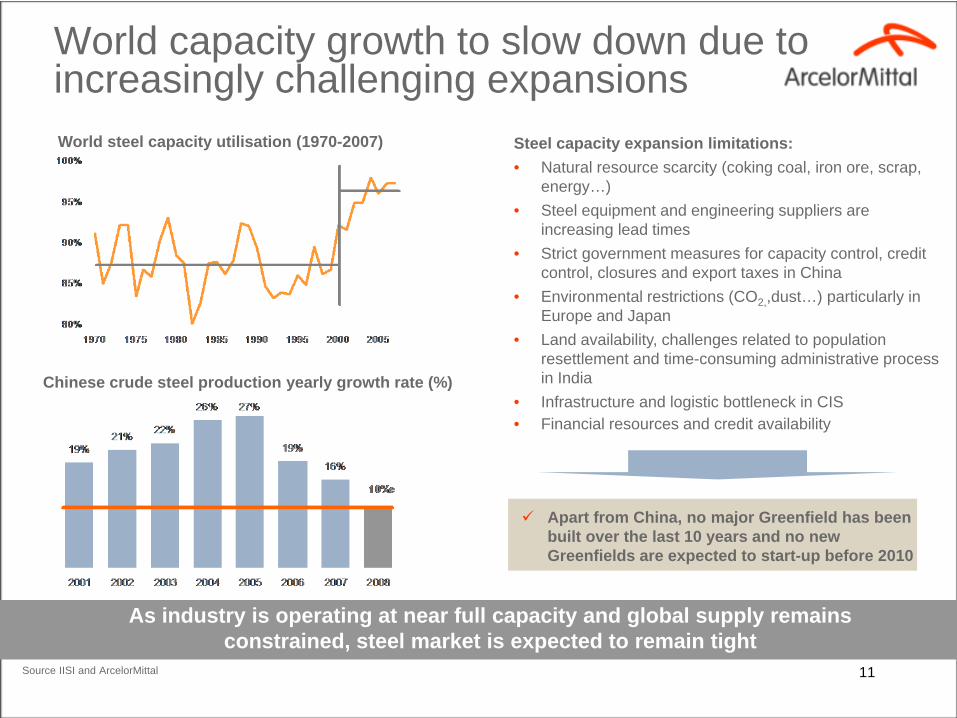

World capacity growth to slow down due to increasingly challenging expansions

As industry is operating at near full capacity and global supply remains constrained, steel market is expected to remain tight

Source IISI and ArcelorMittal

Steel capacity expansion limitations:• Natural resource scarcity (coking coal, iron ore, scrap,

energy…)• Steel equipment and engineering suppliers are

increasing lead times• Strict government measures for capacity control, credit

control, closures and export taxes in China• Environmental restrictions (CO2,,dust…) particularly in

Europe and Japan • Land availability, challenges related to population

resettlement and time-consuming administrative process in India

• Infrastructure and logistic bottleneck in CIS• Financial resources and credit availability

Apart from China, no major Greenfield has been built over the last 10 years and no new Greenfields are expected to start-up before 2010

Chinese crude steel production yearly growth rate (%)

World steel capacity utilisation (1970-2007)

12

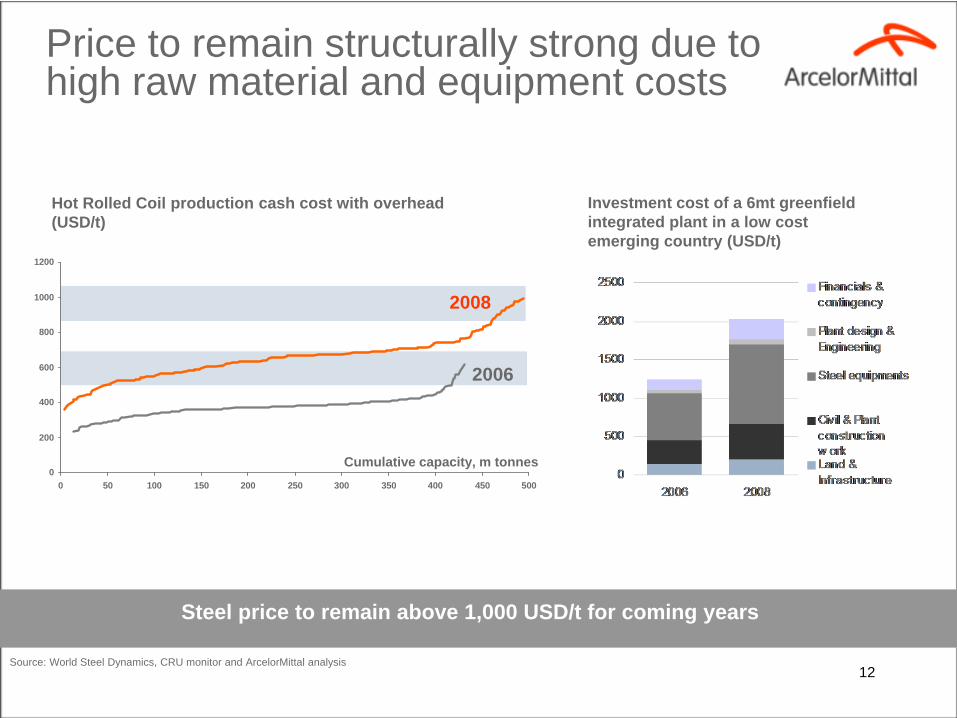

Hot Rolled Coil production cash cost with overhead (USD/t)

Source: World Steel Dynamics, CRU monitor and ArcelorMittal analysis

Steel price to remain above 1,000 USD/t for coming years

Price to remain structurally strong due to high raw material and equipment costs

0

200

400

600

800

1000

1200

0 50 100 150 200 250 300 350 400 450 500

Cumulative capacity, m tonnes

2008

2006

Investment cost of a 6mt greenfield integrated plant in a low cost emerging country (USD/t)

13

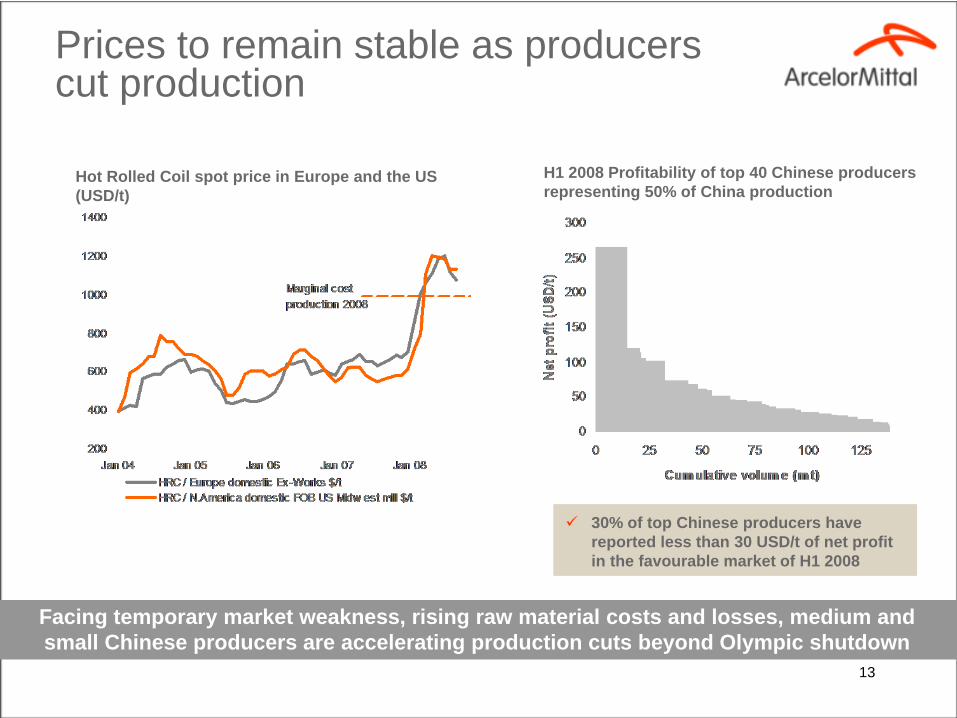

Prices to remain stable as producers cut production

Facing temporary market weakness, rising raw material costs and losses, medium and small Chinese producers are accelerating production cuts beyond Olympic shutdown

Hot Rolled Coil spot price in Europe and the US (USD/t)

H1 2008 Profitability of top 40 Chinese producers representing 50% of China production

30% of top Chinese producers have reported less than 30 USD/t of net profit in the favourable market of H1 2008

14

Delivering growth plan

15

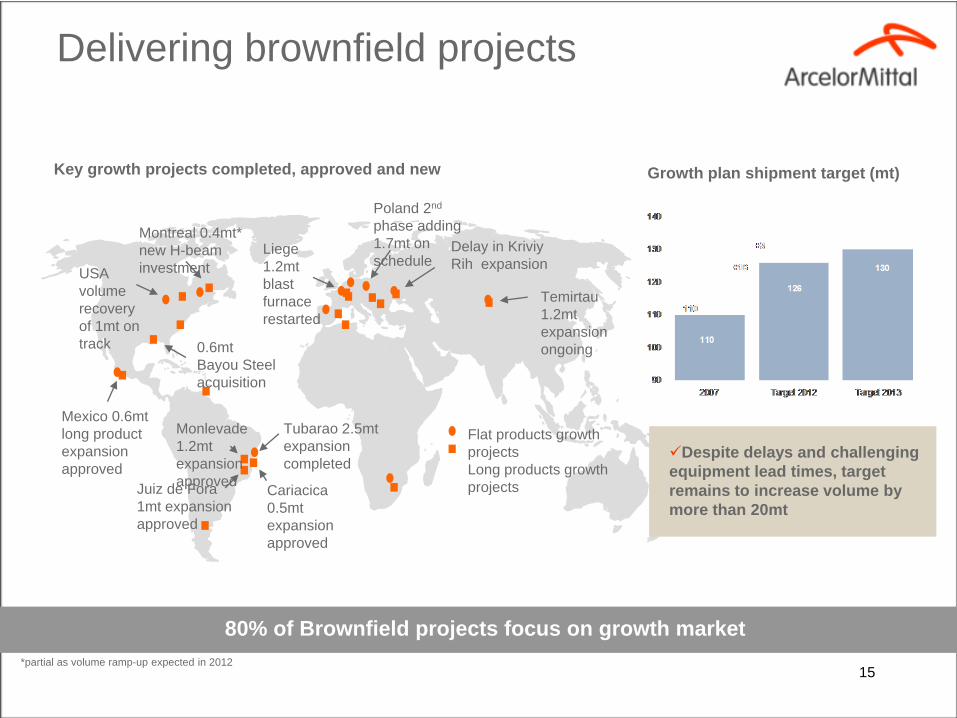

Key growth projects completed, approved and new

80% of Brownfield projects focus on growth market*partial as volume ramp-up expected in 2012

Flat products growth projectsLong products growth projects

Tubarao 2.5mt expansion completed

Liege 1.2mt blast furnace restarted

Monlevade 1.2mt expansion approved

USA volume recovery of 1mt on track

Mexico 0.6mt long product expansion approved

0.6mt Bayou Steel acquisition

Montreal 0.4mt* new H-beam investment

Poland 2nd

phase adding 1.7mt on schedule

Delay in Kriviy Rih expansion

Temirtau 1.2mt expansion ongoing

Juiz de Fora 1mt expansion approved

Cariacica 0.5mt expansion approved

Growth plan shipment target (mt)

Delivering brownfield projects

Despite delays and challenging equipment lead times, target remains to increase volume by more than 20mt

16

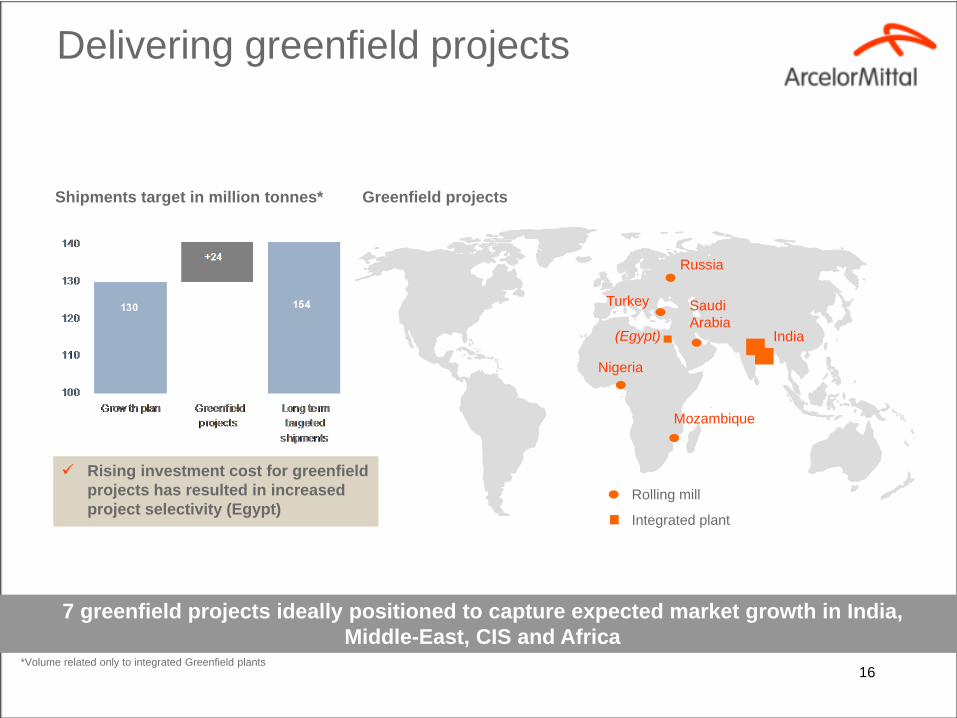

Delivering greenfield projects

Shipments target in million tonnes*

Rising investment cost for greenfield projects has resulted in increased project selectivity (Egypt)

Greenfield projects

India

Rolling mill

Integrated plant

Russia

Turkey Saudi Arabia

Nigeria

Mozambique

(Egypt)

7 greenfield projects ideally positioned to capture expected market growth in India, Middle-East, CIS and Africa

*Volume related only to integrated Greenfield plants

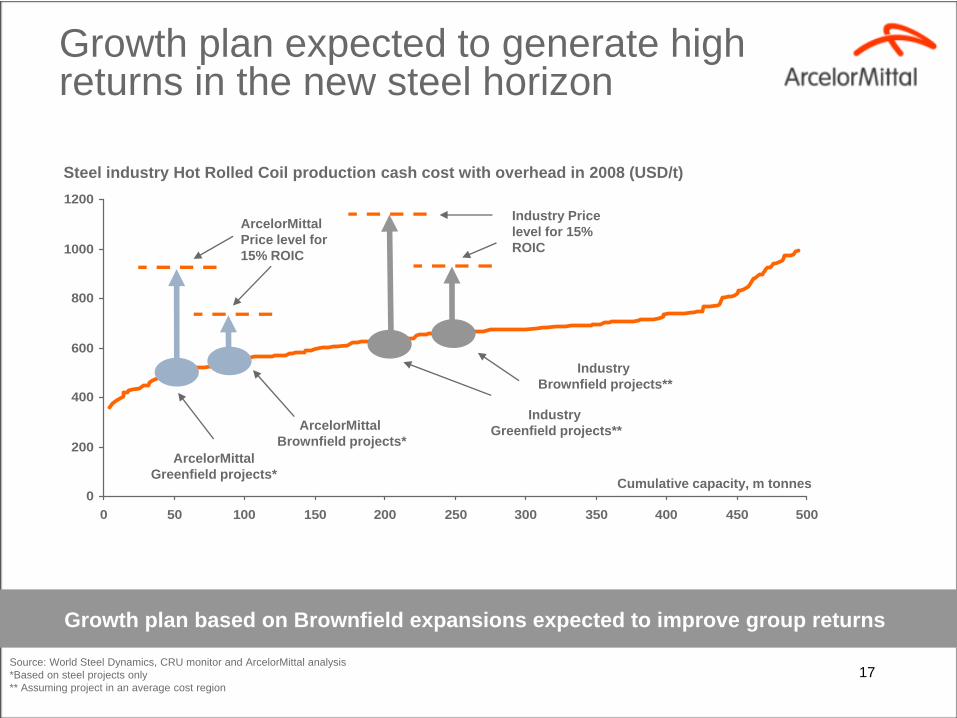

17Source: World Steel Dynamics, CRU monitor and ArcelorMittal analysis*Based on steel projects only** Assuming project in an average cost region

Growth plan based on Brownfield expansions expected to improve group returns

Growth plan expected to generate high returns in the new steel horizon

0

200

400

600

800

1000

1200

0 50 100 150 200 250 300 350 400 450 500

Cumulative capacity, m tonnes

ArcelorMittalGreenfield projects*

ArcelorMittal Brownfield projects*

ArcelorMittal Price level for 15% ROIC

Industry Price level for 15% ROIC

Industry Brownfield projects**

Industry Greenfield projects**

Steel industry Hot Rolled Coil production cash cost with overhead in 2008 (USD/t)

18

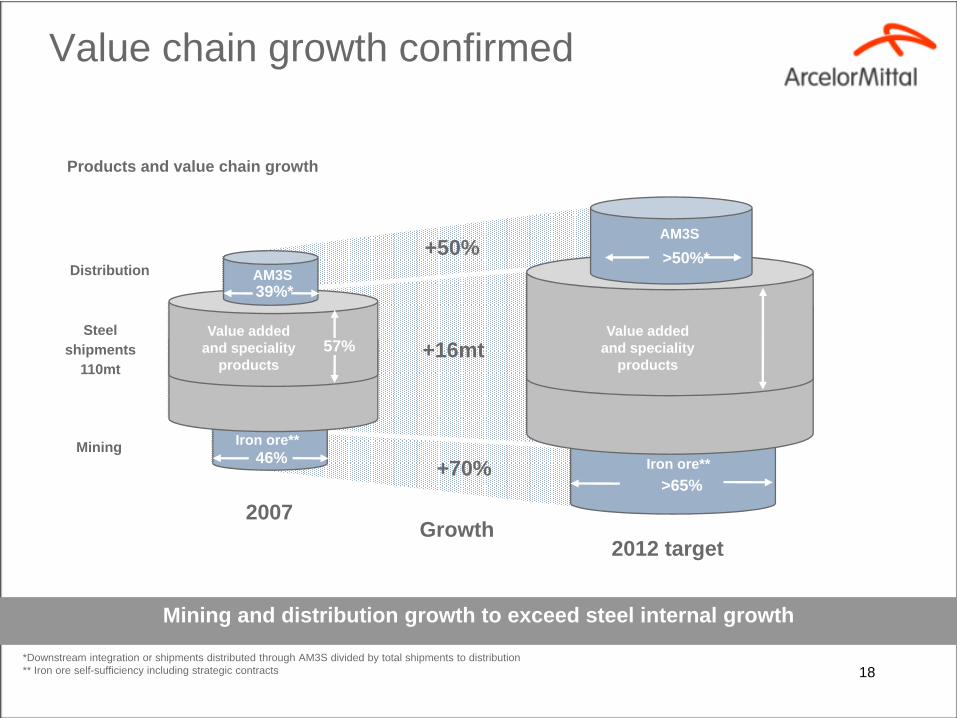

Value chain growth confirmed

Mining and distribution growth to exceed steel internal growth

*Downstream integration or shipments distributed through AM3S divided by total shipments to distribution** Iron ore self-sufficiency including strategic contracts

46%

39%*

57%Steel

shipments 110mt

2007

Value added and speciality

products

Distribution

Mining Iron ore**

AM3S Growth plan 2012*

>65%

>50%*

2012 target

+16mt

Iron ore**

+50%

+70%

AM3S

Value added and speciality

products

Products and value chain growth

Growth

19

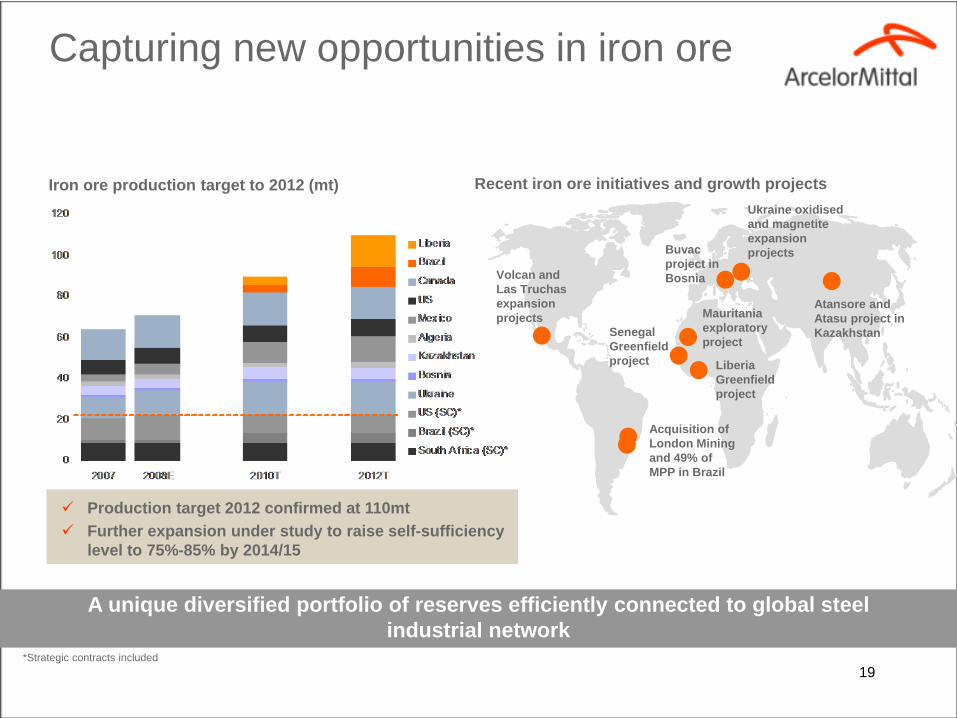

Capturing new opportunities in iron ore

*Strategic contracts included

Acquisition of London Mining and 49% of MPP in Brazil

Recent iron ore initiatives and growth projectsIron ore production target to 2012 (mt)

Production target 2012 confirmed at 110mtFurther expansion under study to raise self-sufficiency level to 75%-85% by 2014/15

Volcan and Las Truchas expansion projects

Ukraine oxidised and magnetite expansion projects

Atansore and Atasu project in Kazakhstan

Buvac project in Bosnia

Senegal Greenfield project Liberia

Greenfield project

Mauritania exploratory project

A unique diversified portfolio of reserves efficiently connected to global steel industrial network

20

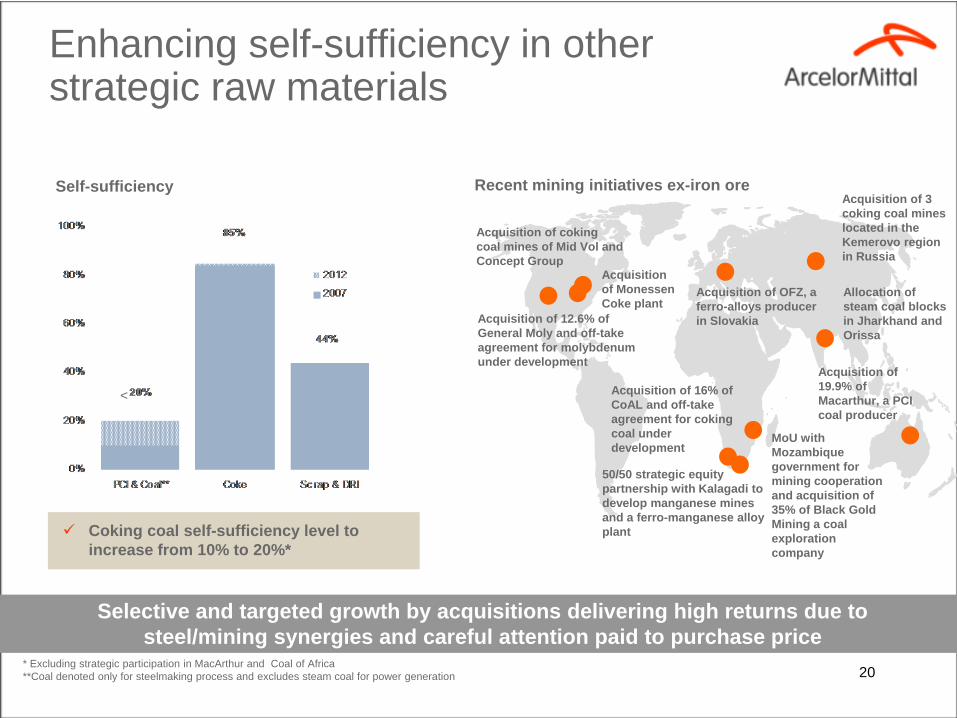

Enhancing self-sufficiency in other strategic raw materials

Allocation of steam coal blocks in Jharkhand and Orissa

MoU with Mozambique government for mining cooperation and acquisition of 35% of Black Gold Mining a coal exploration company

Acquisition of 12.6% of General Moly and off-take agreement for molybdenum under development

Acquisition of OFZ, a ferro-alloys producer in Slovakia

50/50 strategic equity partnership with Kalagadi to develop manganese mines and a ferro-manganese alloy plant

Acquisition of 3 coking coal mines located in the Kemerovo region in Russia

Recent mining initiatives ex-iron ore

Acquisition of 16% of CoAL and off-take agreement for coking coal under development

Acquisition of 19.9% of Macarthur, a PCI coal producer

Acquisition of coking coal mines of Mid Vol and Concept Group

Acquisition of Monessen Coke plant

Coking coal self-sufficiency level to increase from 10% to 20%*

Self-sufficiency

* Excluding strategic participation in MacArthur and Coal of Africa**Coal denoted only for steelmaking process and excludes steam coal for power generation

Selective and targeted growth by acquisitions delivering high returns due to steel/mining synergies and careful attention paid to purchase price

<

21

Conclusion

22

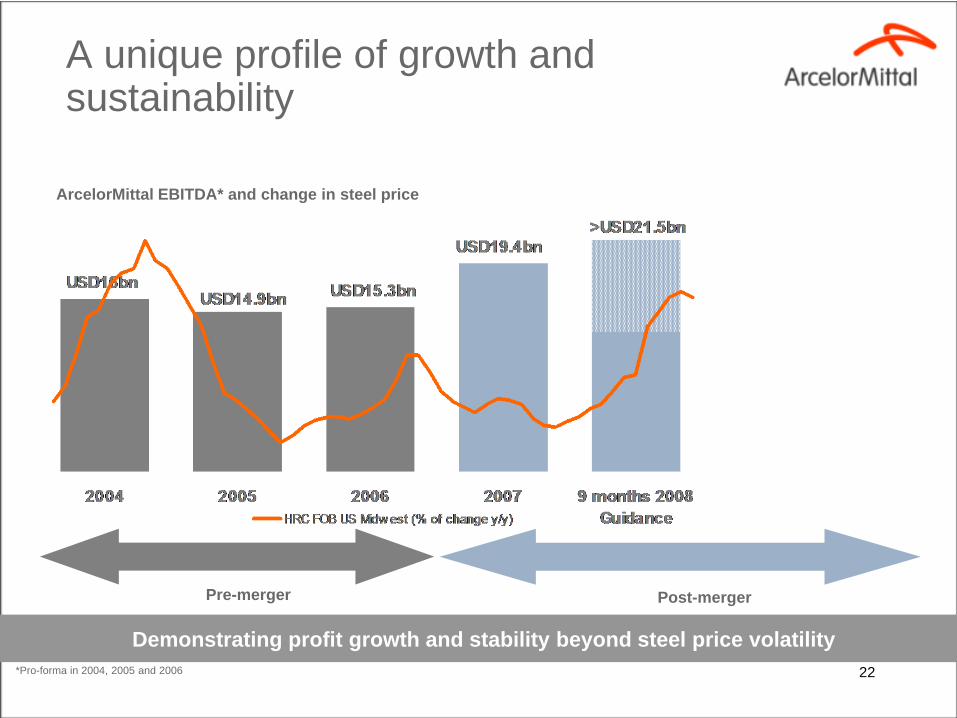

A unique profile of growth and sustainability

Pre-merger Post-merger

Demonstrating profit growth and stability beyond steel price volatility

ArcelorMittal EBITDA* and change in steel price

*Pro-forma in 2004, 2005 and 2006

23

Q&A