Embed Size (px)

Citation preview

Annual Report 2011

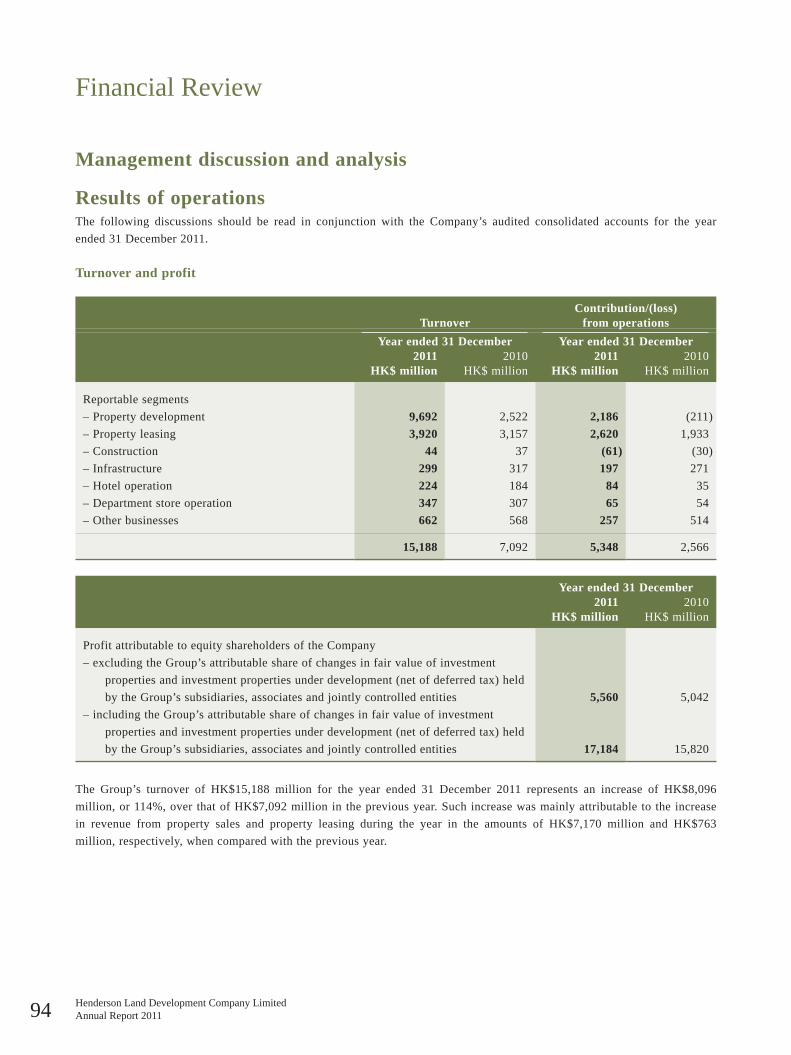

At the core of the Group’s commitment to a sustainable future, Henderson Land embraces innovation and continually aligns its operations to best practice. Henderson Land follows a strategy emphasizing sustainability, that is driving the progressive development of its business and ensuring its long term success.

(Cover Photo: Many of the Group’s signature buildings in Hong Kong and mainland China have been recognized for their green features. From left to right, The Gloucester, Mira Moon, Henderson Metropolitan, Two International Finance Centre, World Financial Centre, Arch of Triumph, Hill Paramount. The photo below shows the Winter Garden inside World Financial Centre.)

Two ifc, Hong KongPlatinum BEAM Rating (left)

Centro, ShanghaiLEED Gold Certification (right)

DELIVERING A

SUSTAINABLEFUTURE

Annual Report 2011

Xinjiang

Xizang

QinghaiGansu

Guizhou

GuangxiYunnan

Hainan

Taiwan

Fujian

Zhejiang

ShandongShanxi

Hebei

Beijing

Jilin

Ningxia

Inner Mongolia

Heilongjiang

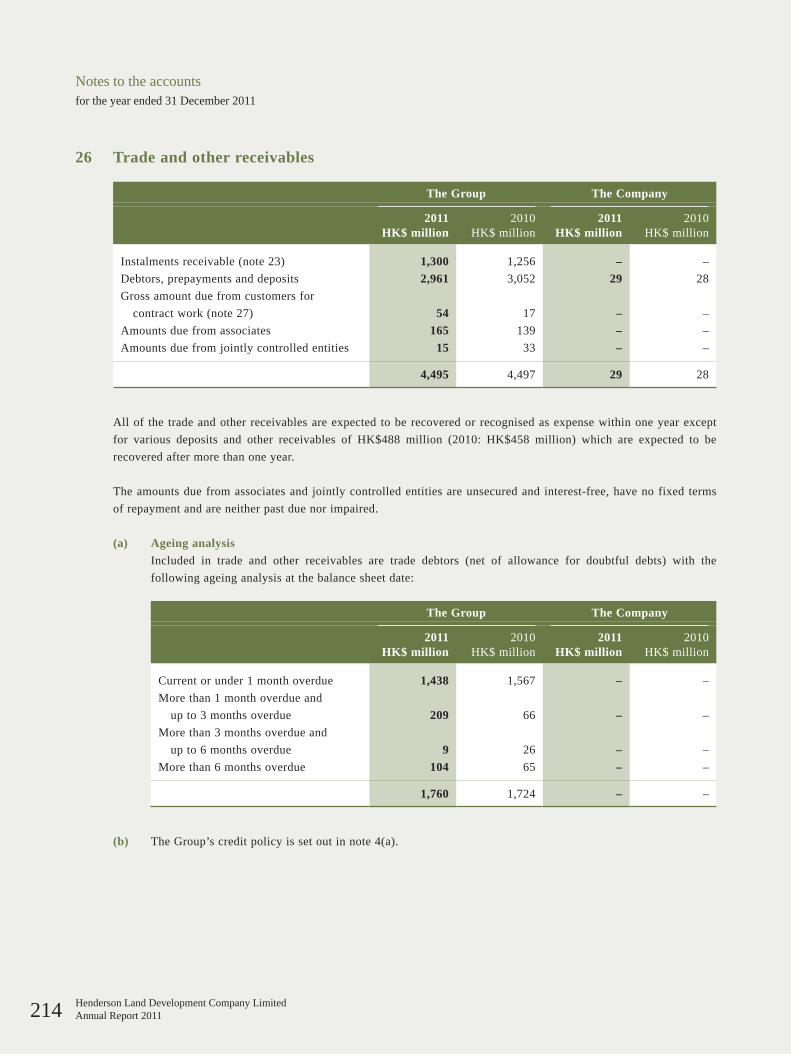

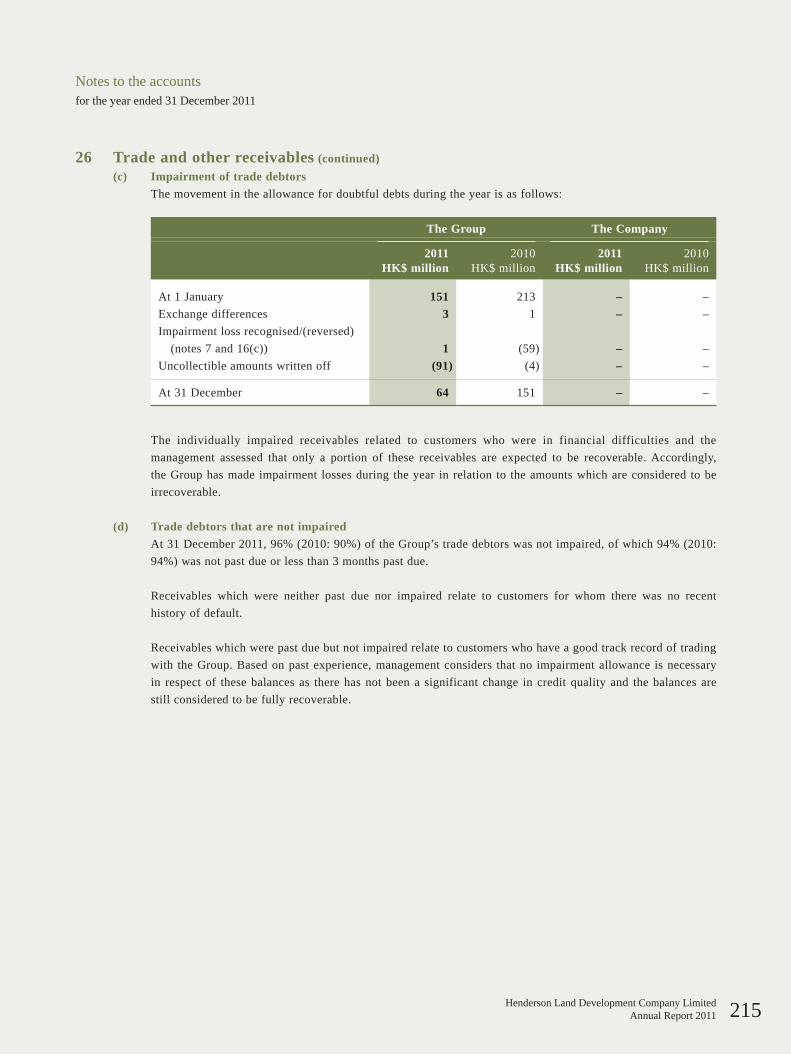

Jiangxi

Hubei

Henan

Anhui

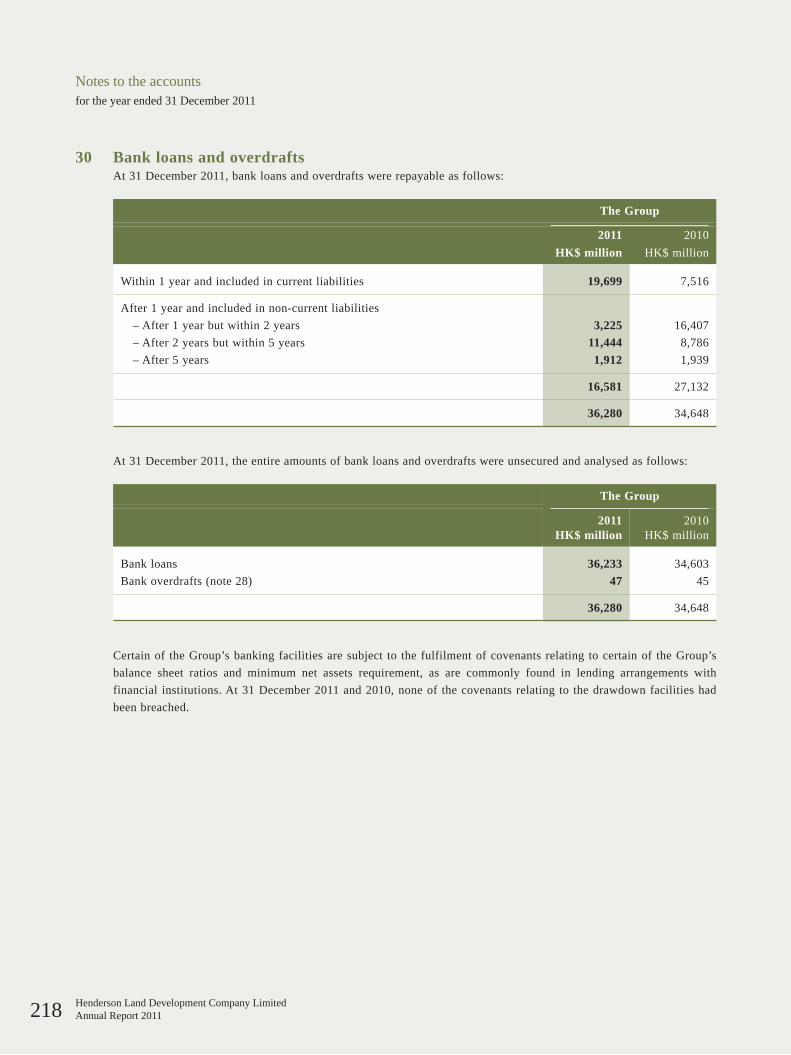

Sichuan

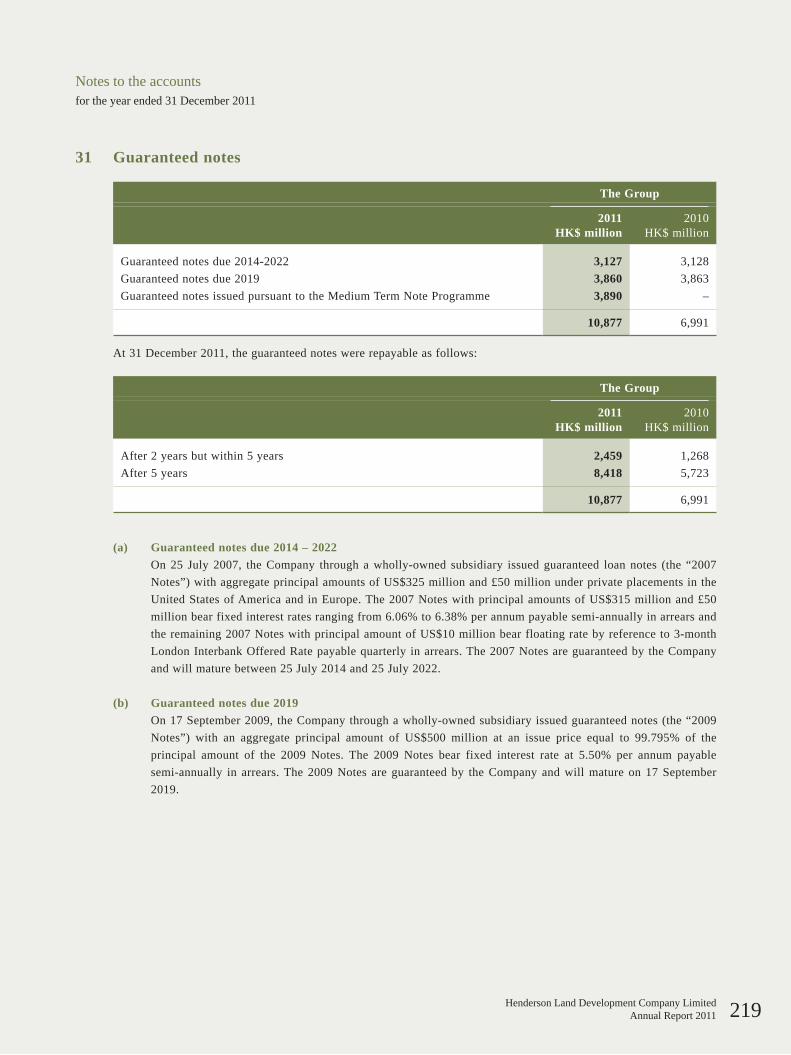

Chongqing

Shaanxi

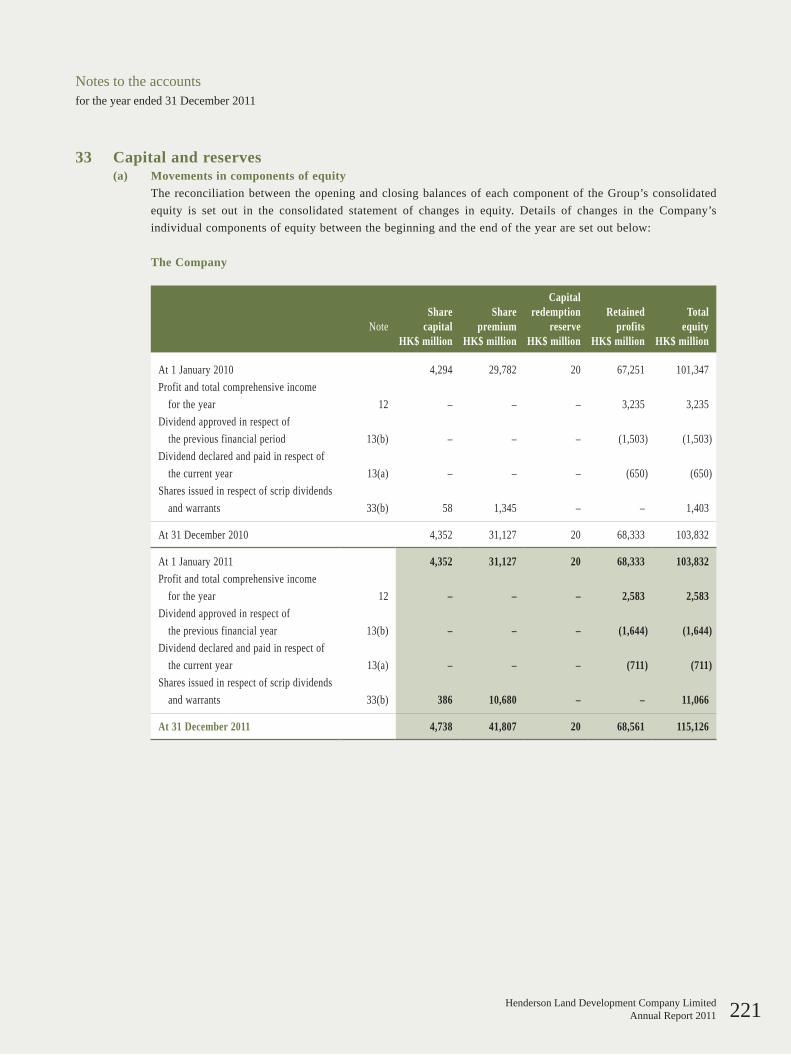

Hunan

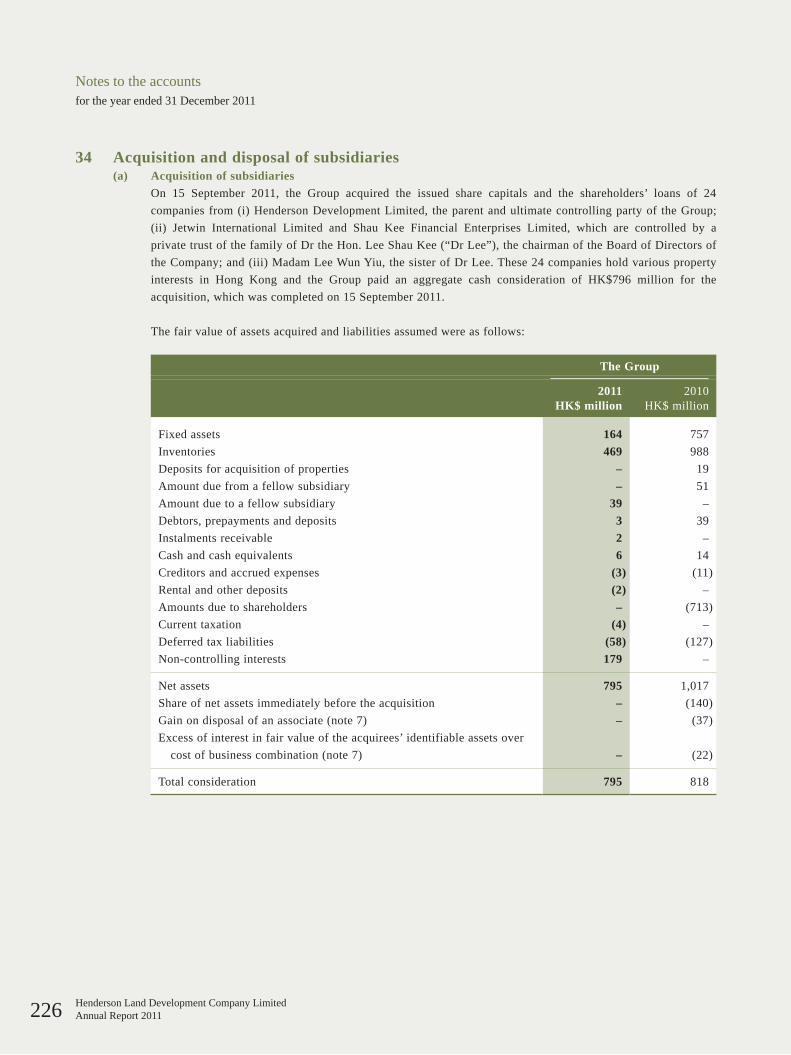

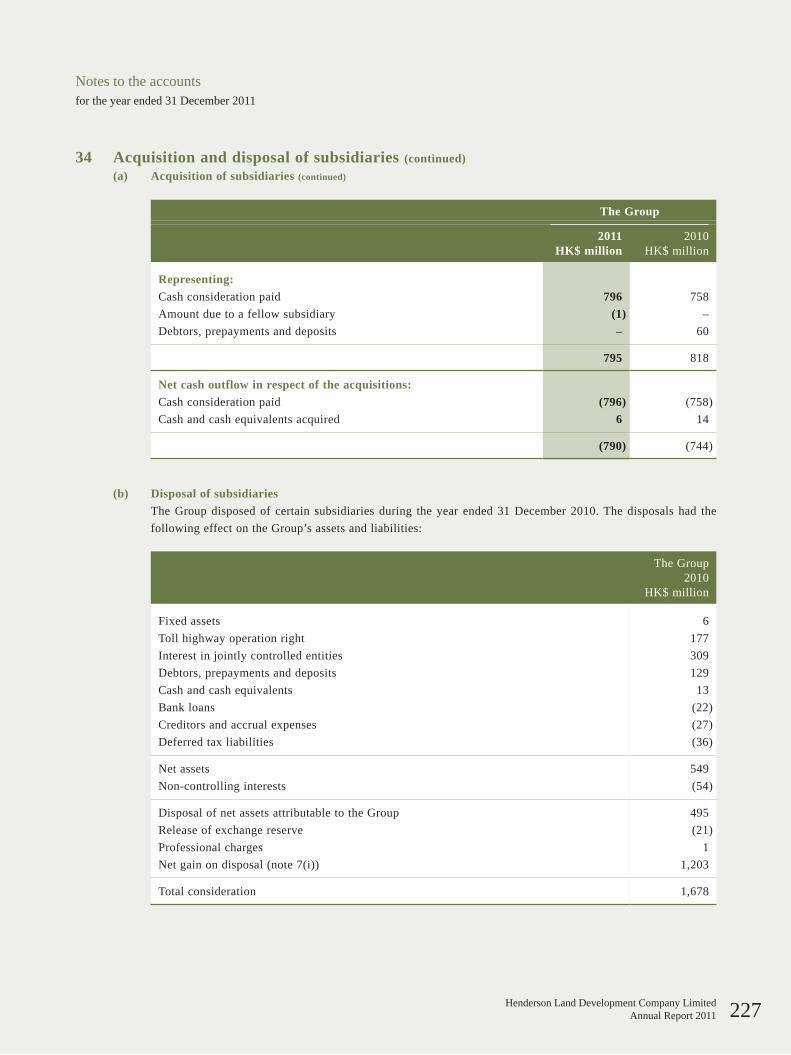

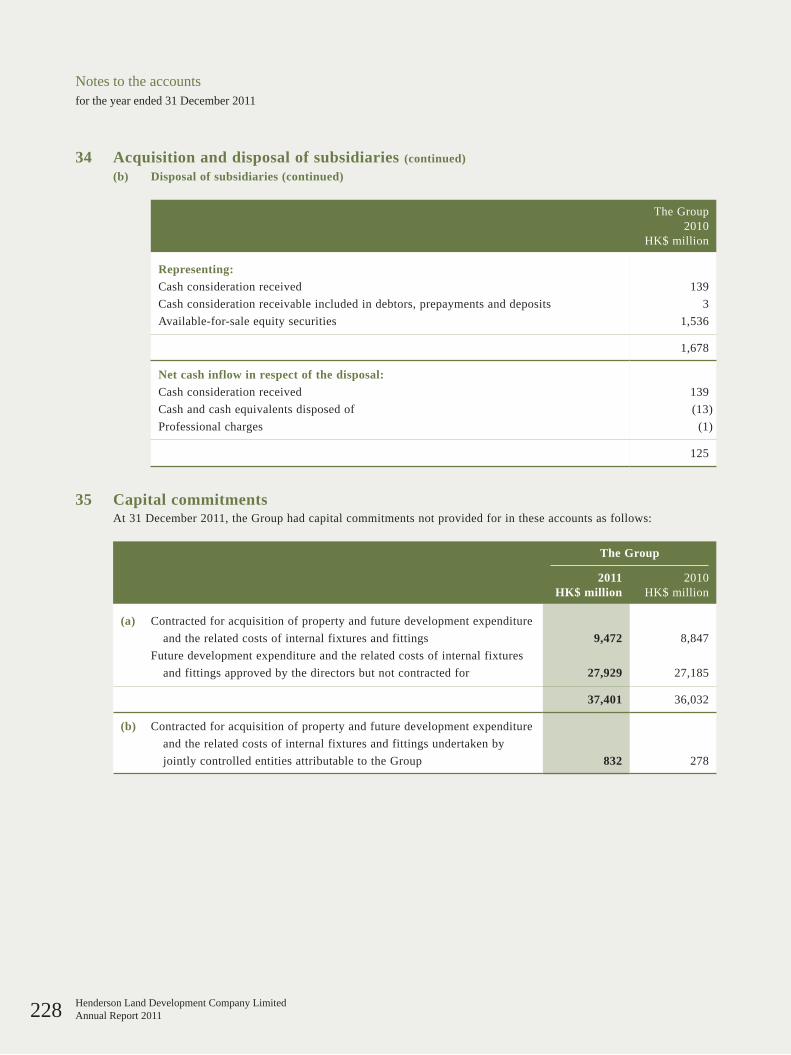

Shanghai

Jiangsu

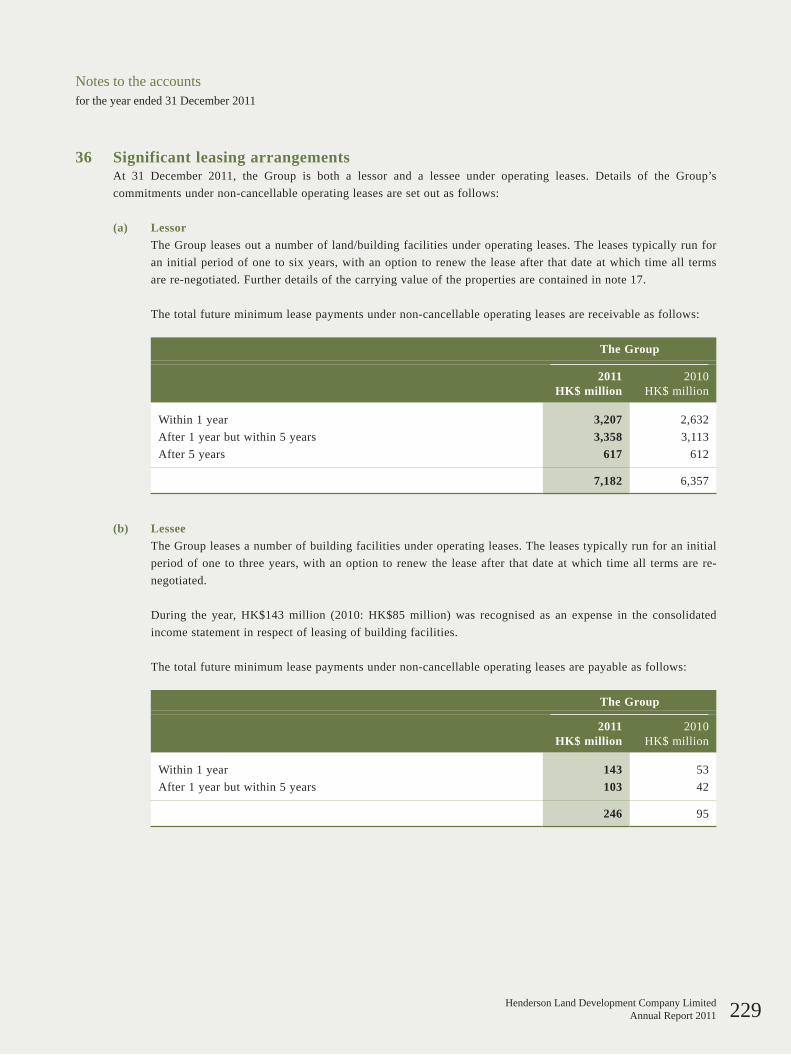

Liaoning

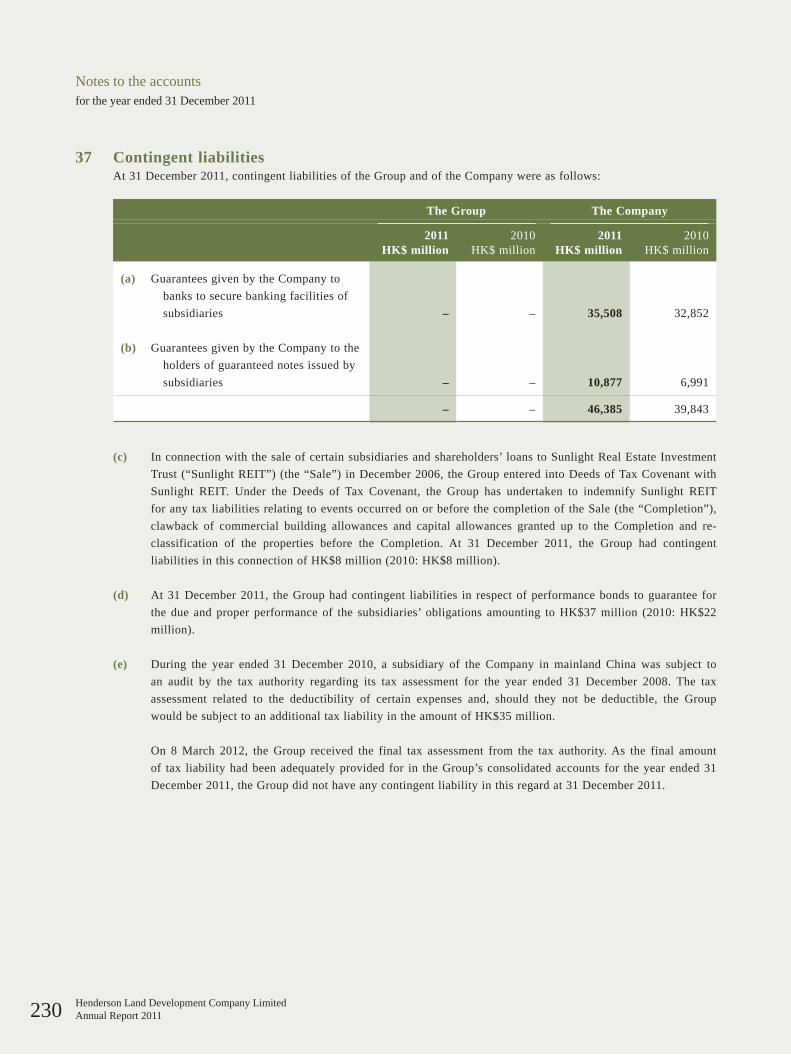

Guangdong

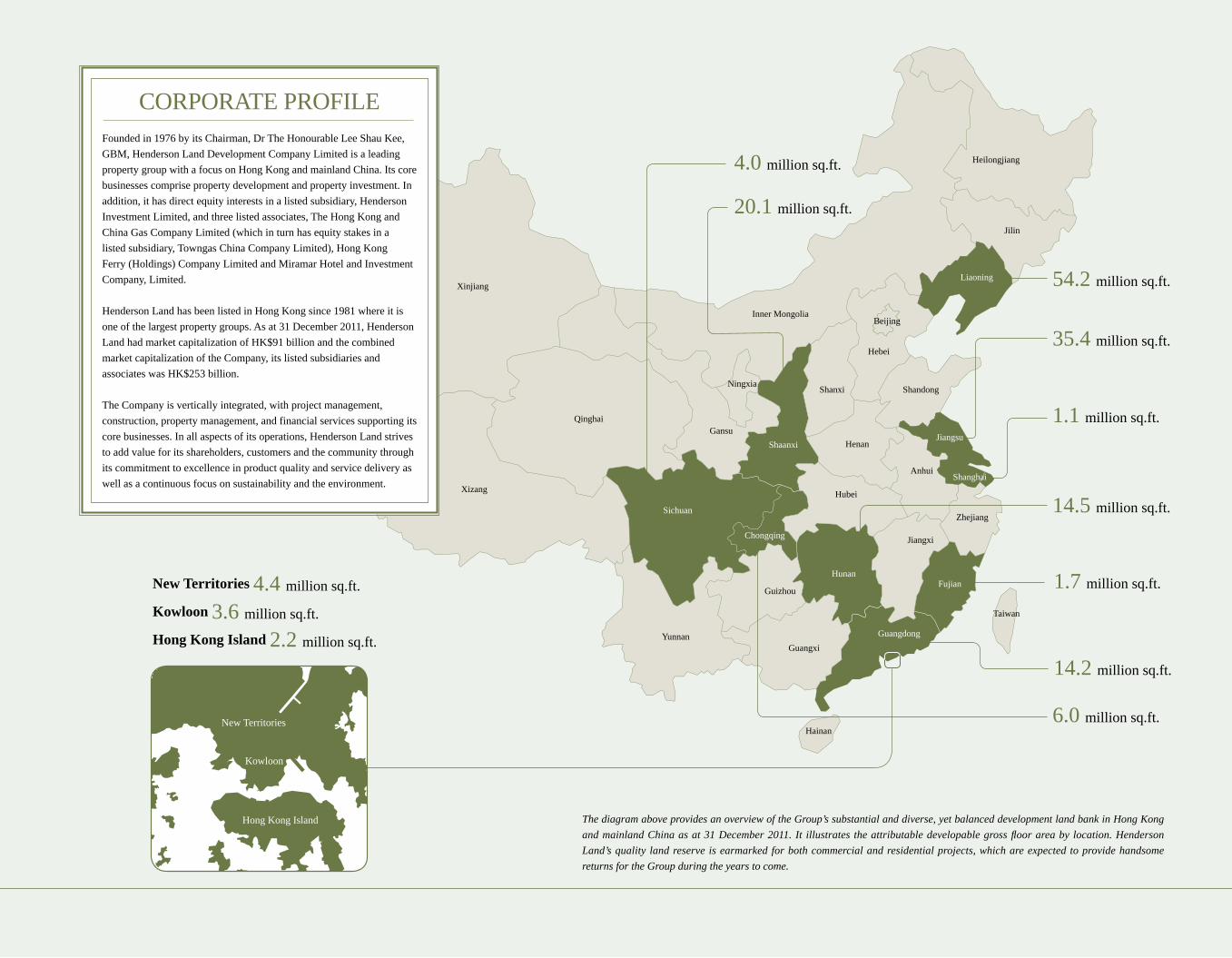

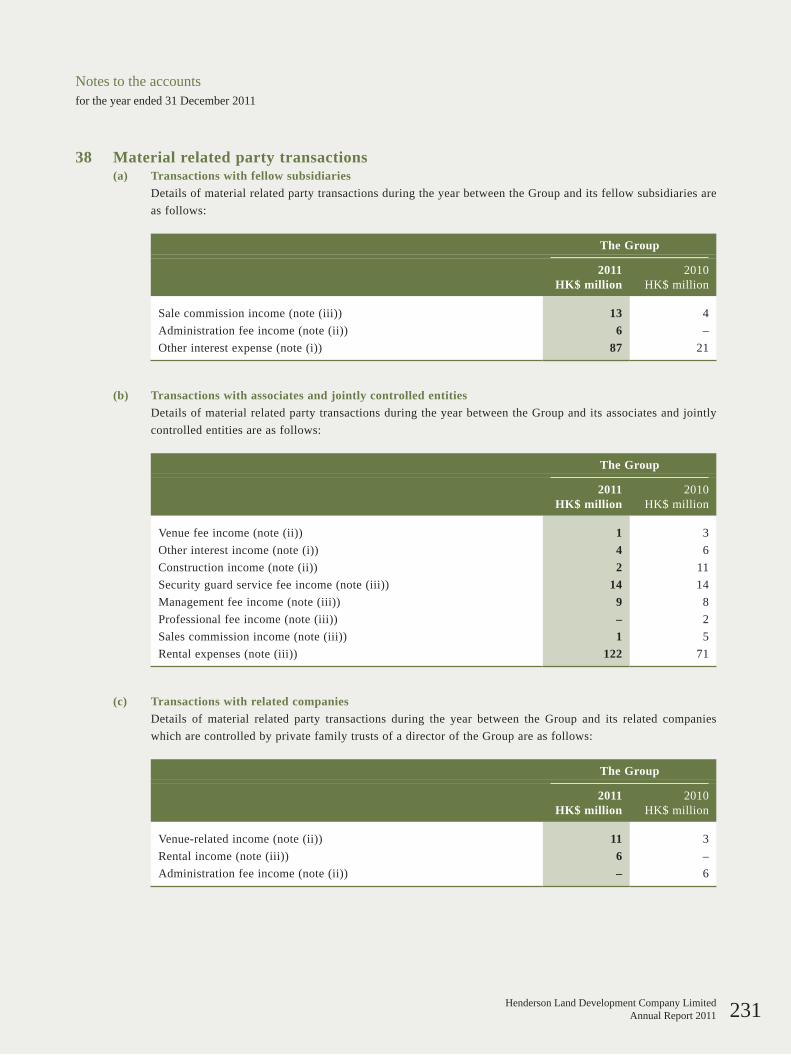

54.2 million sq.ft.

20.1 million sq.ft.

Kowloon 3.6 million sq.ft.

New Territories 4.4 million sq.ft.

Hong Kong Island 2.2 million sq.ft.

35.4 million sq.ft.

1.1 million sq.ft.

14.5 million sq.ft.

6.0 million sq.ft.

4.0 million sq.ft.

Hong Kong Island

Kowloon

New Territories

1.7 million sq.ft.

14.2 million sq.ft.

The diagram above provides an overview of the Group’s substantial and diverse, yet balanced development land bank in Hong Kong and mainland China as at 31 December 2011. It illustrates the attributable developable gross floor area by location. Henderson Land’s quality land reserve is earmarked for both commercial and residential projects, which are expected to provide handsome returns for the Group during the years to come.

CORPORATE PROFILEFounded in 1976 by its Chairman, Dr The Honourable Lee Shau Kee, GBM, Henderson Land Development Company Limited is a leading property group with a focus on Hong Kong and mainland China. Its core businesses comprise property development and property investment. In addition, it has direct equity interests in a listed subsidiary, Henderson Investment Limited, and three listed associates, The Hong Kong and China Gas Company Limited (which in turn has equity stakes in a listed subsidiary, Towngas China Company Limited), Hong Kong Ferry (Holdings) Company Limited and Miramar Hotel and Investment Company, Limited.

Henderson Land has been listed in Hong Kong since 1981 where it is one of the largest property groups. As at 31 December 2011, Henderson Land had market capitalization of HK$91 billion and the combined market capitalization of the Company, its listed subsidiaries and associates was HK$253 billion.

The Company is vertically integrated, with project management, construction, property management, and financial services supporting its core businesses. In all aspects of its operations, Henderson Land strives to add value for its shareholders, customers and the community through its commitment to excellence in product quality and service delivery as well as a continuous focus on sustainability and the environment.

Contents Insidefront CorporateProfile

2 Awards&Accolades

4 Group Structure

5 Highlightsof2011FinalResults

10 Chairman’sStatement

ReviewofOperations

Business in Hong Kong

36 Land Bank

44 PropertyDevelopment

52 PropertyInvestment

58 PropertyRelatedBusinesses

BusinessinMainlandChinaandMacau

62 Land Bank

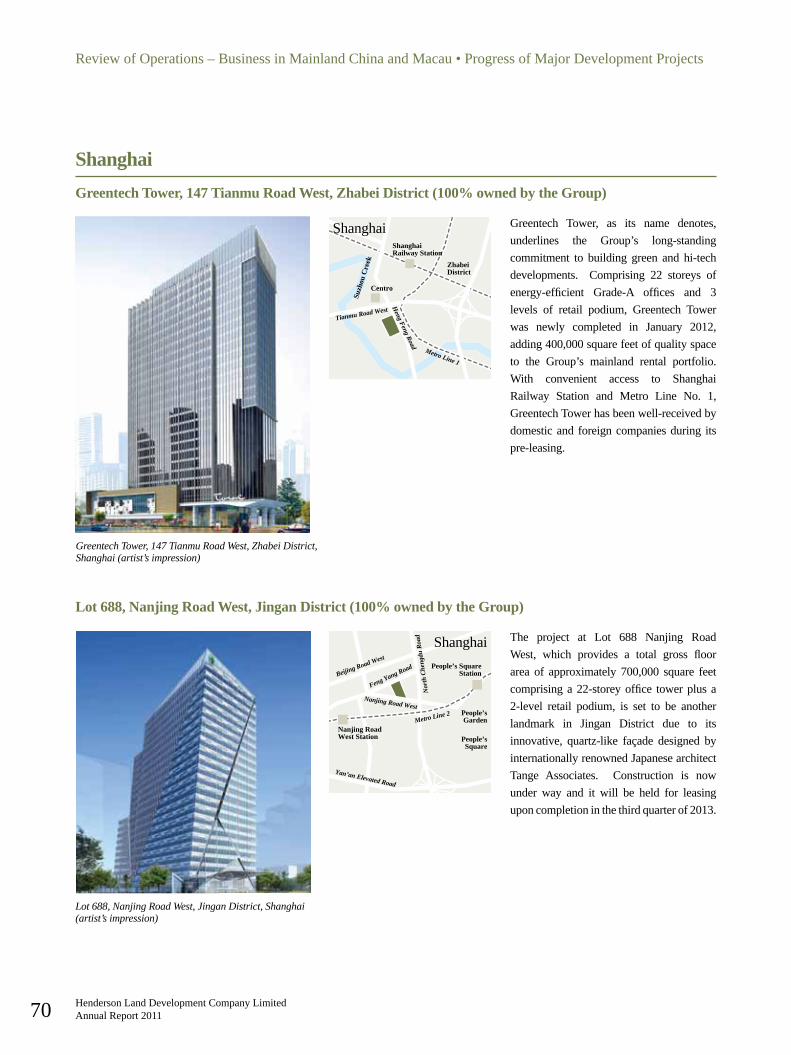

66 ProgressofMajorDevelopmentProjects

76 MajorInvestmentProperties

82 Subsidiary&AssociatedCompanies

94 FinancialReview

102 FiveYearFinancialSummary

106 SustainabilityandCSR

112 CorporateGovernanceReport

120 ReportoftheDirectors

138 BiographicalDetailsofDirectorsandSeniorManagement

146 ReportoftheIndependentAuditor

147 Accounts

242 CorporateInformation

245 NoticeofAnnualGeneralMeeting

248 FinancialCalendar

Forward-LookingStatementsThisannualreportcontainscertainstatementsthatareforward-lookingorwhichusecertainforward-looking terminologies. These forward-lookingstatements are based on the current beliefs,assumptions and expectations of the Board ofDirectorsoftheCompanyregardingtheindustryandmarketsinwhichitoperates.Theseforward-looking statements are subject to risks,uncertainties and other factors beyond the Company’s control which may cause actualresults or performance to differmaterially fromthose expressed or implied in such forward-lookingstatements.

Henderson Land Development Company LimitedAnnual Report 20112

Awards & Accolades

1. The 8th Top 10 Influential Brands in China China United Business News, China

Wisdom Engineering Association and 3 other research institutes / associations

Top 10 Influential Brands in China Real Estate Industry

2. Hang Seng Corporate Sustainability Index Series

Hang Seng Indexes Company Limited Constituent Company3. The 5th Annual Autodesk HK BIM

Awards 2011 Autodesk4. Caring Company 2010/11 Hong Kong Council of Social Services Henderson Land, Hong Kong & China Gas,

Hong Kong Ferry, Miramar, Hang Yick, Well Born & Goodwill

5. BCI Asia Top 10 Awards 2011 BCI Asia Top 10 Developers Awards 20116. The Excellence of Listed Enterprise

Awards 2011 CAPITAL WEEKLY7. 2011 International ARC Awards Mercomm, Inc. Gold Award (category: Financial Data -

Real Estate Development) Bronze Award (category: Interior Design -

Real Estate Development)8. Golden Brick Award for Real Estate

of China 21st Century Business Herald and the

Organizing Committee of Boao 21st Century Real Estate Forum

2011 Most Outstanding Architecture Award (39 Conduit Road)

9. metroBOX Greater China Excellent Brand Awards 2011

metroBOX, Yangcheng Metro News Greater China Excellent Brand for Luxury

Properties (Hill Paramount)10. HKCA Safety Award 2010 Hong Kong Construction Association HKCA Proactive Safety Contractors Award

2010 (E Man, Heng Shung & Grandic) HKCA Safety Merit Award 2010 (Heng Lai)11. The 2nd Hong Kong Outstanding

Corporate Citizenship Award Hong Kong Productivity Council Services Industry - Merit Award (Property

Management) Outstanding Corporate Volunteer Team -

Silver Award (Team of Care)12. 2010 Customer Relationship

Excellence Awards Asia Pacific Customer Service Consortium Corporate Health & Safety Achievement of

the Year 2010 (Property Management) Customer Loyalty Program of the Year 2010

(Property Management) Corporate Environmental & Social

Leadership of the Year 2010 (Property Management - Goodwill)

High Speed Customer Service of the Year 2010 (Property Management - Goodwill)

Merit - Integrated Support Team of the Year 2010 (Goodwill)

13. Excellence in Facility Management Award 2011

Hong Kong Institute of Facility Management

Excellence in Facility Management Award - Office Building (Manulife Financial Centre)

Excellence in Facility Management Award - Retail (Metro City Phase II)

14. Family-Friendly Employers Award Scheme 2011

Family Council Distinguished Family-Friendly Employer (The

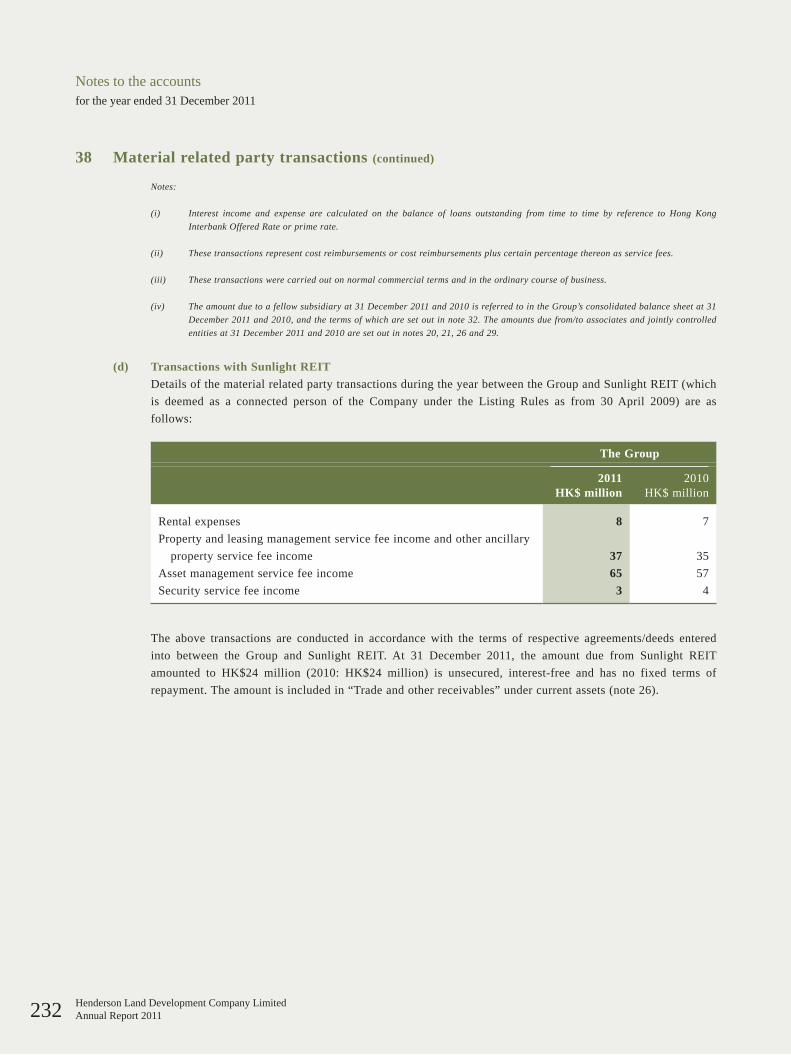

Hong Kong & China Gas Company Limited) Family-Friendly Employer (Hang Yick, Well

Born & Goodwill)15. World Top 1000 Chinese Enterprises Yazhou Zhoukan Best Business Performance Award 2011 -

Hong Kong Region (The Hong Kong and China Gas Company Limited)

16. CAPITAL Outstanding Enterprise 2011 CAPITAL Outstanding Hong Kong Branding Enterprise

(Miramar Hotel and Investment Company, Limited)

17. 2010/11 One Factory-One Year-One Environmental Project (1-1-1) Programme

Federation of Hong Kong Industries Hang Seng-Pearl River Delta Environmental

Award - Green Participant (The Hongkong & Yaumati Ferry Company Limited)

6.

10.

4.

5.

11.

17.

12.

During the year, Henderson Land again garnered many awards and acknowledgements for the quality of its projects and services, reflecting its continued commercial success and its contributions in important areas such as environmental awareness and sustainability. In the Hong Kong Green Awards 2011, Henderson Land Group companies as a whole won more than 30 awards and certificates, becoming the largest winner of the year. As further recognition of the Group’s comprehensive approach to sustainability, many Group projects are achieving the highest ratings under the globally recognized LEED and BEAM schemes. For example, during the year, Centro achieved a Gold LEED and Platinum BEAM rating, while One International Finance Centre, Two International Finance Centre, Manulife Financial Centre, and Henderson Metropolitan all achieved Platinum BEAM ratings, the highest possible under the scheme’s stringent requirements.

Building Environmental Assessment Method (BEAM) (Left)

Leadership in Energy and Environmental Design (LEED) (Right)

Hong Kong Green Awards 2011

Henderson Land Development Company LimitedAnnual Report 2011 3

1.

7.8.9.

2.

3.

13.14.16. 15.

HendersonLandDevelopmentCompanyLimitedAnnualReport20114

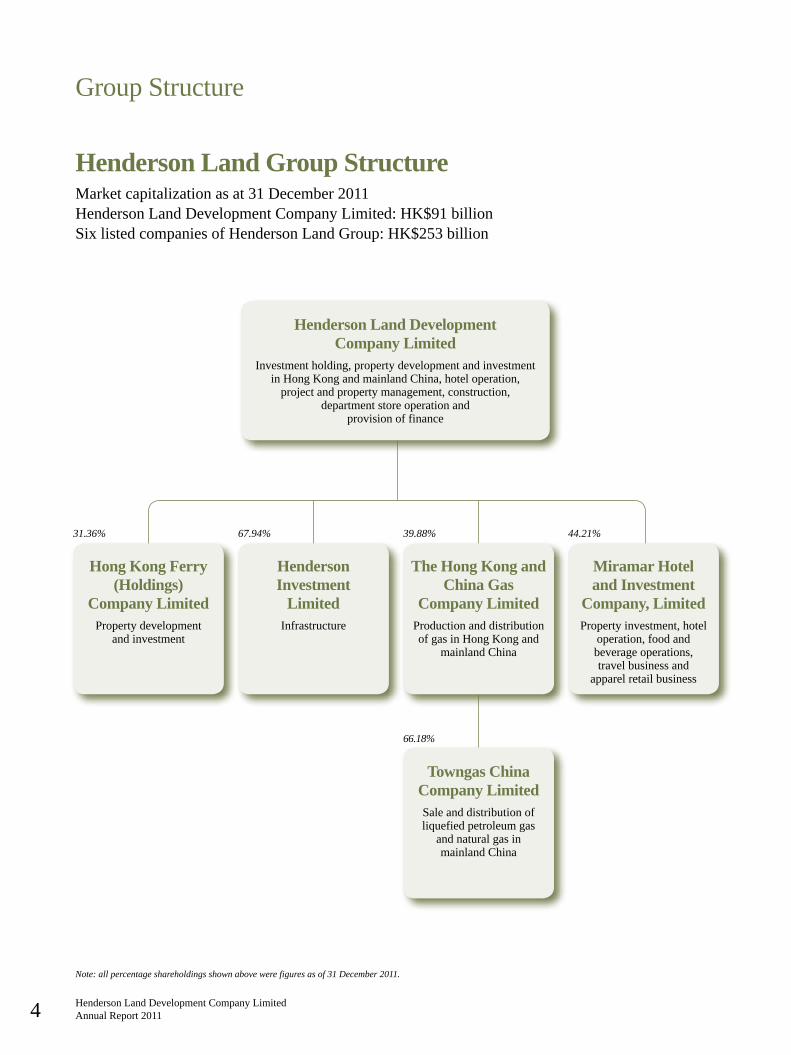

Group Structure

Note: all percentage shareholdings shown above were figures as of 31 December 2011.

Henderson Land Group StructureMarketcapitalizationasat31December2011HendersonLandDevelopmentCompanyLimited:HK$91billionSixlistedcompaniesofHendersonLandGroup:HK$253billion

31.36% 67.94% 39.88% 44.21%

66.18%

Henderson Land Development Company Limited

Investmentholding,propertydevelopmentandinvestmentinHongKongandmainlandChina,hoteloperation,projectandpropertymanagement,construction,

departmentstoreoperationand provisionoffinance

Hong Kong Ferry (Holdings)

Company LimitedPropertydevelopment

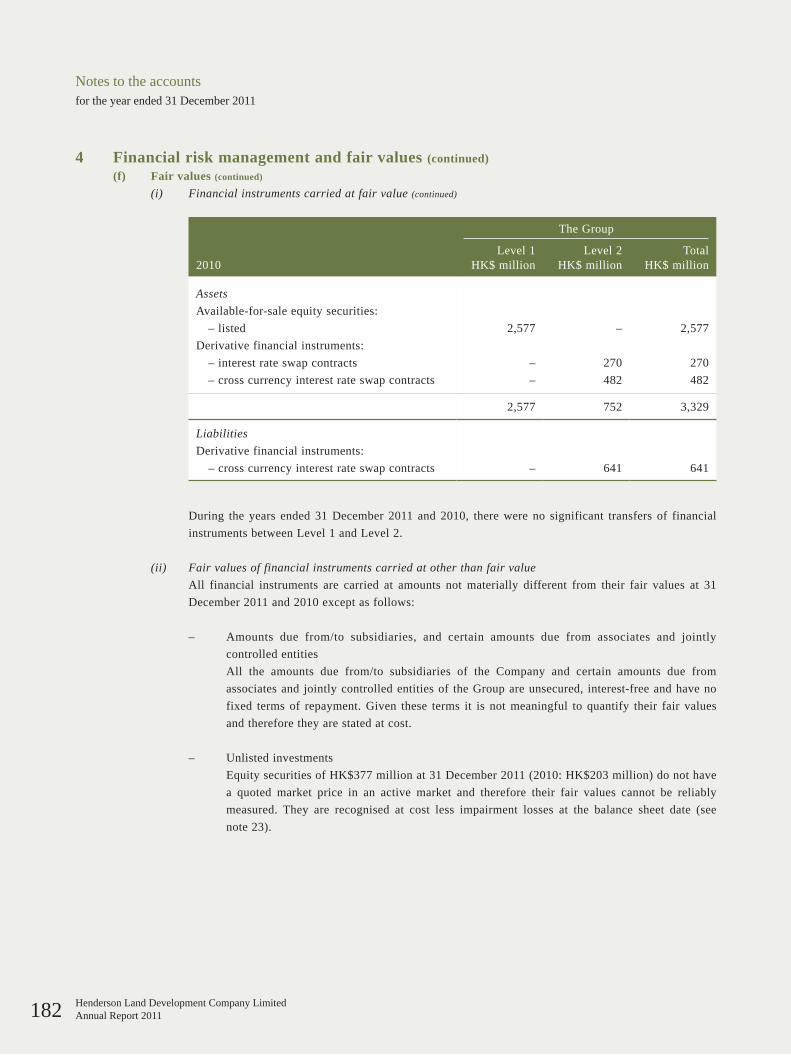

andinvestment

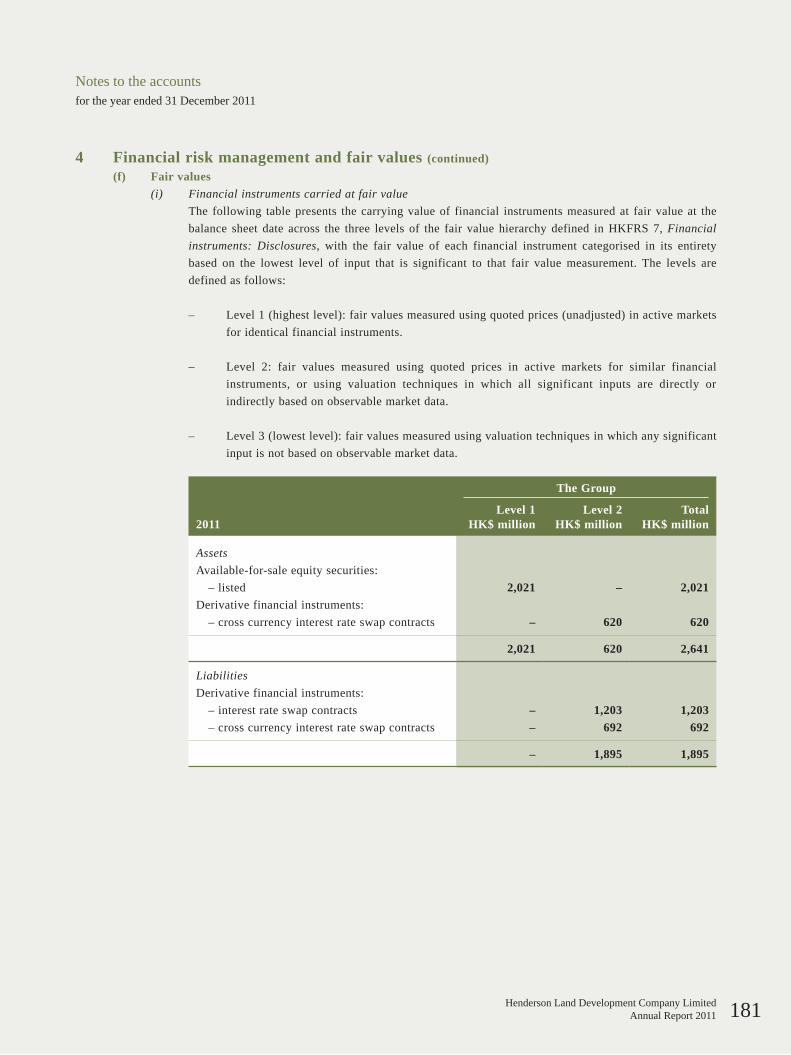

Henderson Investment

LimitedInfrastructure

The Hong Kong and China Gas

Company LimitedProduction and distribution of gas in Hong Kong and

mainlandChina

Miramar Hotel and Investment

Company, LimitedPropertyinvestment,hotel

operation,foodand beverageoperations, travelbusinessand

apparelretailbusiness

Towngas China Company LimitedSaleanddistributionofliquefiedpetroleumgas

andnaturalgasin mainlandChina

HendersonLandDevelopmentCompanyLimitedAnnualReport2011 5

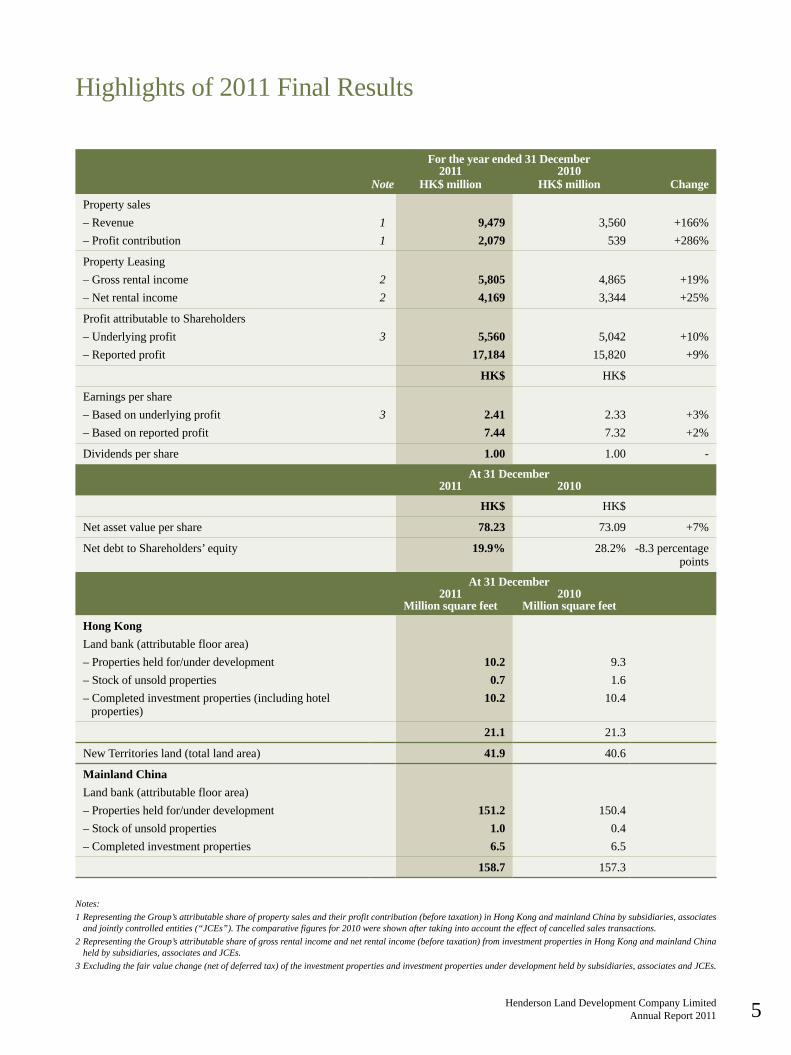

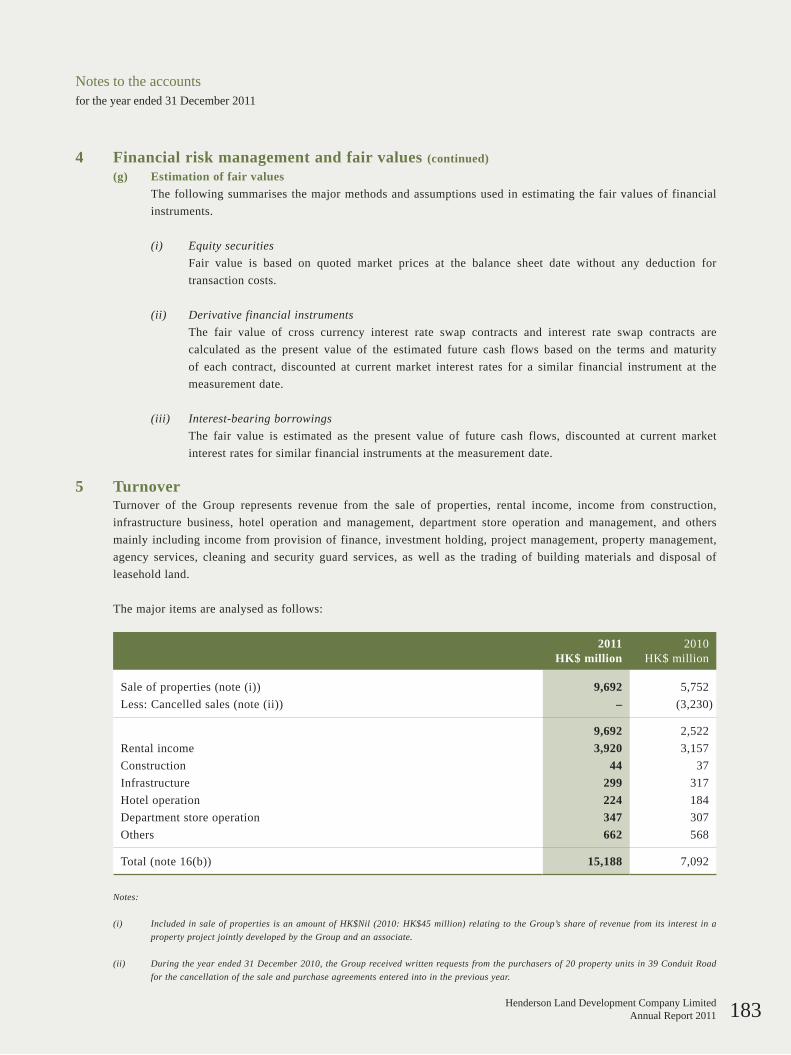

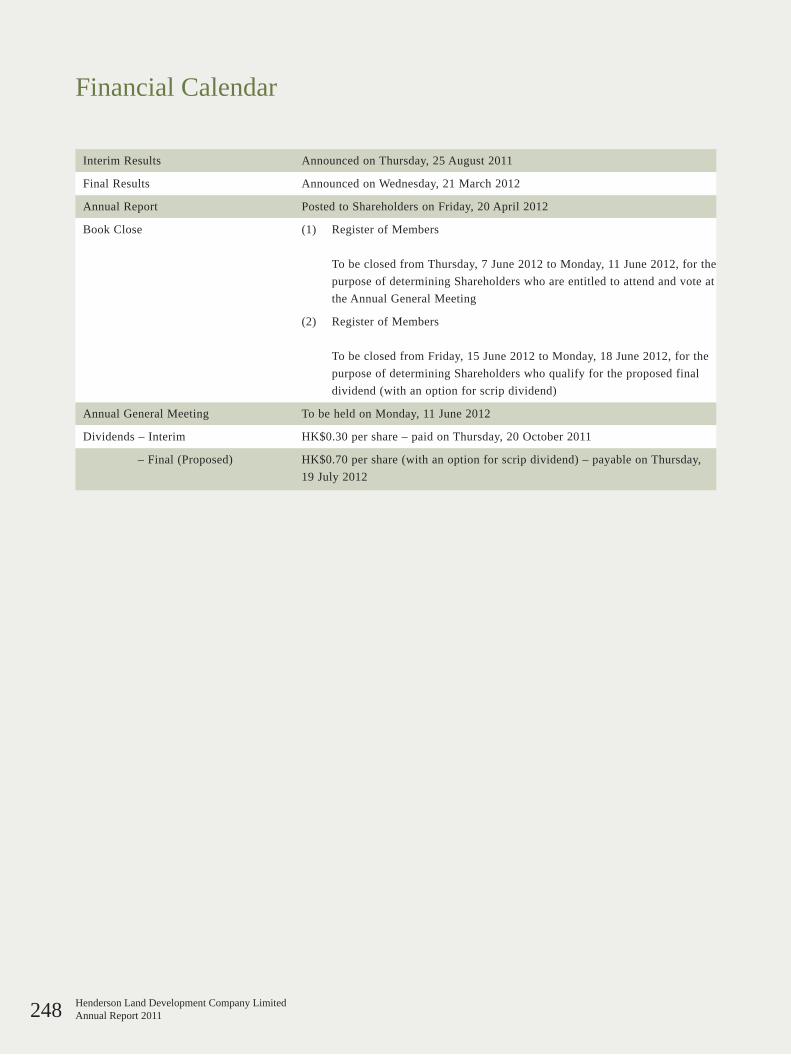

Highlightsof2011FinalResults

For the year ended 31 December

Note2011

HK$ million2010

HK$ million Change

Propertysales–Revenue 1 9,479 3,560 +166%– Profit contribution 1 2,079 539 +286%

Property Leasing–Grossrentalincome 2 5,805 4,865 +19%–Netrentalincome 2 4,169 3,344 +25%

ProfitattributabletoShareholders–Underlyingprofit 3 5,560 5,042 +10%–Reportedprofit 17,184 15,820 +9%

HK$ HK$

Earningspershare–Basedonunderlyingprofit 3 2.41 2.33 +3%– Based on reported profit 7.44 7.32 +2%

Dividendspershare 1.00 1.00 -

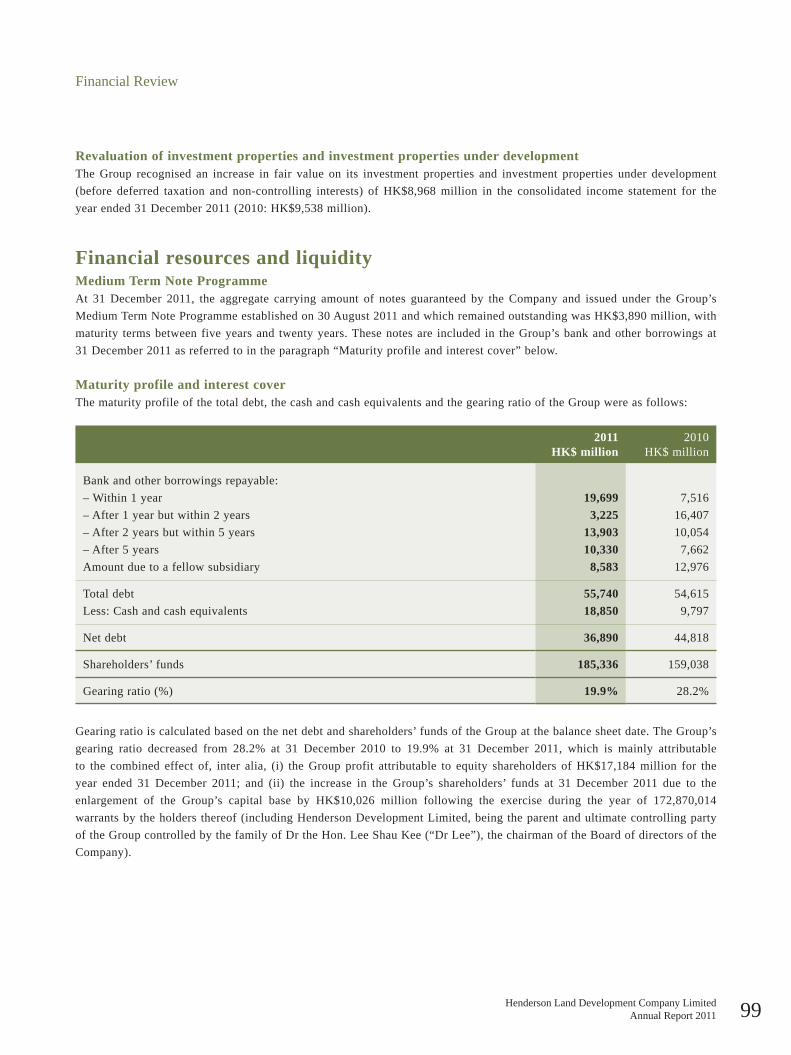

At 31 December 2011 2010

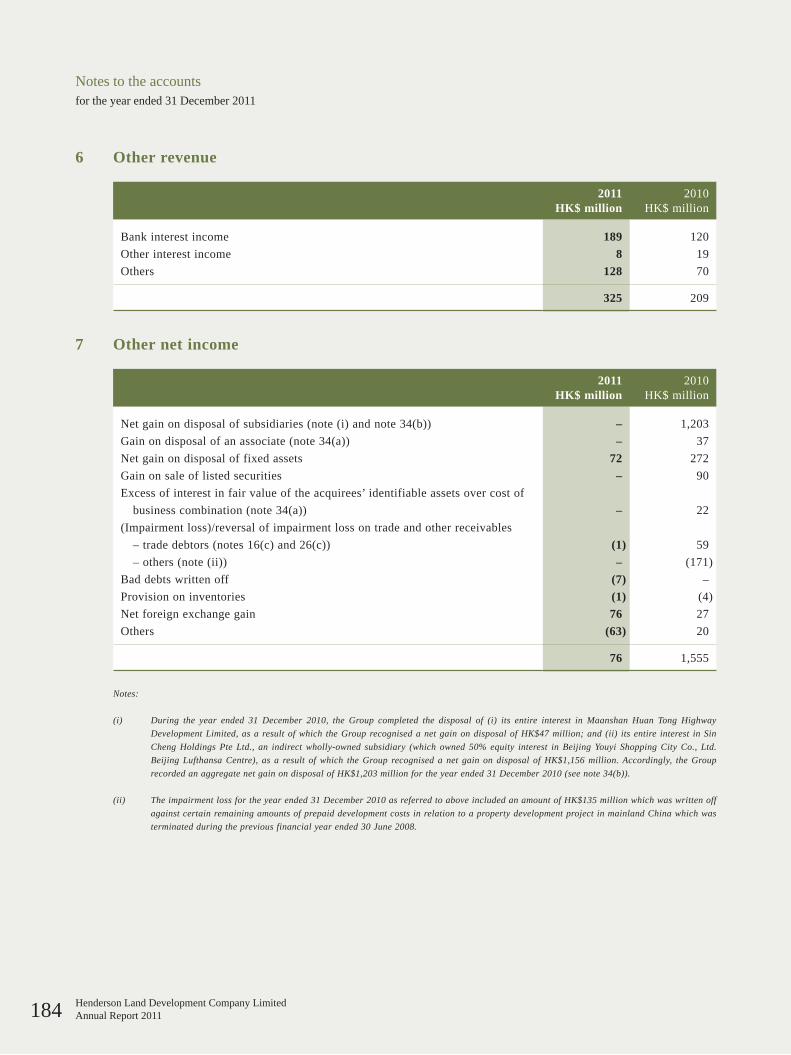

HK$ HK$

Netassetvaluepershare 78.23 73.09 +7%

NetdebttoShareholders’equity 19.9% 28.2% -8.3percentagepoints

At 31 December 2011 2010

Million square feet Million square feet

Hong KongLandbank(attributablefloorarea)–Propertiesheldfor/underdevelopment 10.2 9.3–Stockofunsoldproperties 0.7 1.6–Completedinvestmentproperties(includinghotel

properties)10.2 10.4

21.1 21.3

NewTerritoriesland(totallandarea) 41.9 40.6

Mainland ChinaLandbank(attributablefloorarea)–Propertiesheldfor/underdevelopment 151.2 150.4–Stockofunsoldproperties 1.0 0.4–Completedinvestmentproperties 6.5 6.5

158.7 157.3

Notes:1 Representing the Group’s attributable share of property sales and their profit contribution (before taxation) in Hong Kong and mainland China by subsidiaries, associates

and jointly controlled entities (“JCEs”). The comparative figures for 2010 were shown after taking into account the effect of cancelled sales transactions.2 Representing the Group’s attributable share of gross rental income and net rental income (before taxation) from investment properties in Hong Kong and mainland China

held by subsidiaries, associates and JCEs.3 Excluding the fair value change (net of deferred tax) of the investment properties and investment properties under development held by subsidiaries, associates and JCEs.

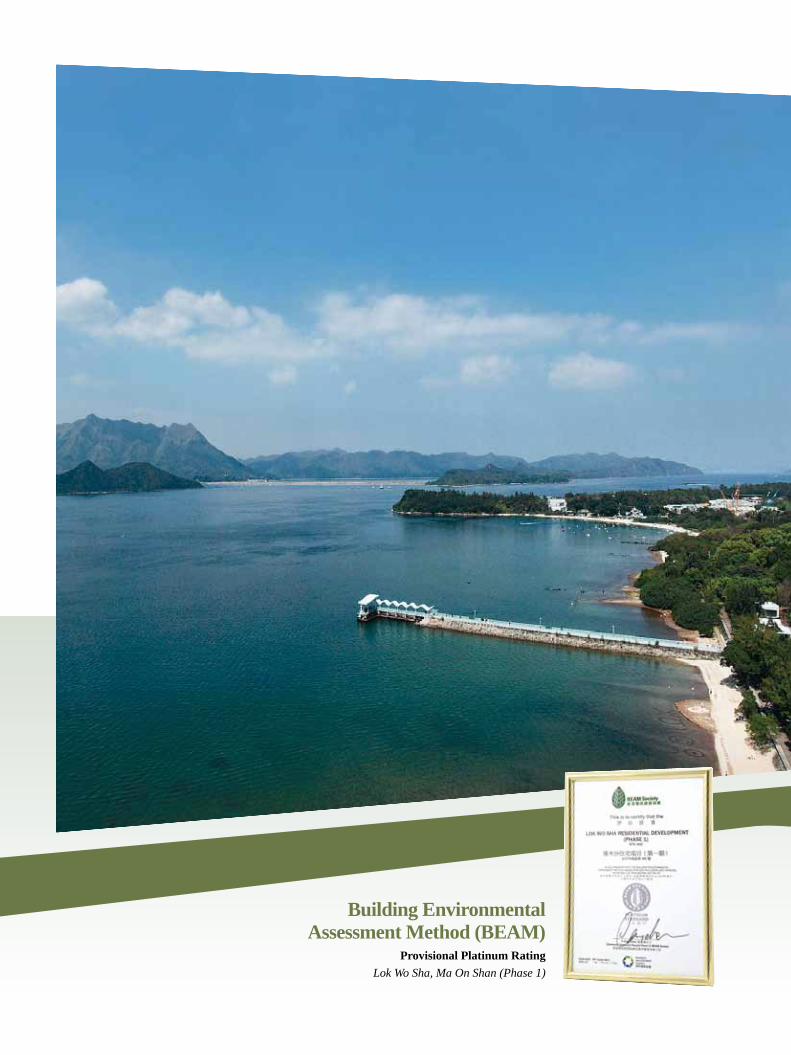

Building Environmental Assessment Method (BEAM)

Provisional Platinum RatingLok Wo Sha, Ma On Shan (Phase 1)

Hong Kong

CHINA

BUILDING FOR THE

FUTUREThe Group’s developments are frequently ahead of their time in both concept and design, embracing world-class standards whilst carefully anticipating the needs and concerns of society in years to come. Spearheaded by the world-renowned master architect Lord Richard Rogers, the Lok Wo Sha project typifies Henderson Land’s conscientious development approach, drawing on world-class design and thoroughly accommodating sustainability and environmental considerations. This project transformed agricultural land into residential use while maintaining the scenic natural beauty of the location.

Dr The Honourable Lee Shau Kee, GBMChairman and Managing Director

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport201110

Dear Shareholders

OnbehalfofyourBoard, Iampleased topresentmyreporton theoperationsof theGroupforthefinancialyearended31December2011.

Profit and Net Assets Attributable to Shareholders

TheGroup’sunderlyingprofitattributableto equity shareholders (before the fairvaluechangeofinvestmentpropertiesandinvestmentpropertiesunderdevelopment)for the year ended 31 December2011 amounted to HK$5,560 million,representing an increase of HK$518millionor10%overHK$5,042millionfortheyearended31December2010.Basedon the underlying profit, the earnings persharewereHK$2.41(HK$2.33fortheyearended31December2010).

Includingthefairvaluechange(netofnon-controllinginterestsanddeferredtaxation)of investment properties and investmentproperties under development, the Groupprofit attributable to equity shareholdersfor the year ended 31 December 2011was HK$17,184 million. Compared withthe Group’s profit attributable to equityshareholders of HK$15,820 million forthe year ended 31 December 2010, thisrepresented an increase of HK$1,364million or 9%. Earnings per share wereHK$7.44(HK$7.32fortheyearended31December2010).

At 31 December 2011, the net assetvalue attributable to equity shareholdersamounted to HK$185,336 million (orHK$78.23 per share), 17% higher thanthe amount of HK$159,038 million (orHK$73.09 per share) at 31 December2010. Net debt (including the amount ofHK$8,583millionduetoawhollyowned

subsidiary of Henderson DevelopmentLimited which is controlled by theprivatefamilytrustsofDrLeeShauKee)amounted to HK$36,890 million (2010:HK$44,818million)withthegearingratioat19.9%(2010:28.2%).

Dividends

Your Board recommends the paymentof afinal dividendofHK$0.70per shareto Shareholders whose names appear ontheRegisterofMembersoftheCompanyon Monday, 18 June 2012, and suchfinal dividend will not be subject to anywithholding tax inHongKong. IncludingtheinterimdividendofHK$0.30persharealreadypaid,thetotaldividendfortheyearended 31December 2011will amount toHK$1.00 per share (2010: HK$1.00 pershare).

The proposed final dividend will bepayableincash,withanoptiontoreceivenewand fully paid shares in lieuof cashunder the scrip dividend scheme (“ScripDividendScheme”).Thenewshareswill,on issue, not be entitled to the proposedfinaldividend,butwillrankparipassuinallotherrespectswiththeexistingshares.Thecircular containing details of the ScripDividendSchemeandtherelevantelectionformwillbesenttoShareholders.

TheScripDividendSchemeisconditionaluponthepassingoftheresolutionrelatingto the payment of final dividend at theforthcomingannualgeneralmeetingoftheCompanyandtheListingCommitteeofTheStock Exchange of Hong Kong Limited

granting the listing of and permission todeal in thenewshares tobe issuedundertheScripDividendScheme.

Final dividend will be distributed, andthe share certificates issued under theScrip Dividend Scheme will be sent toShareholdersonThursday,19July2012.

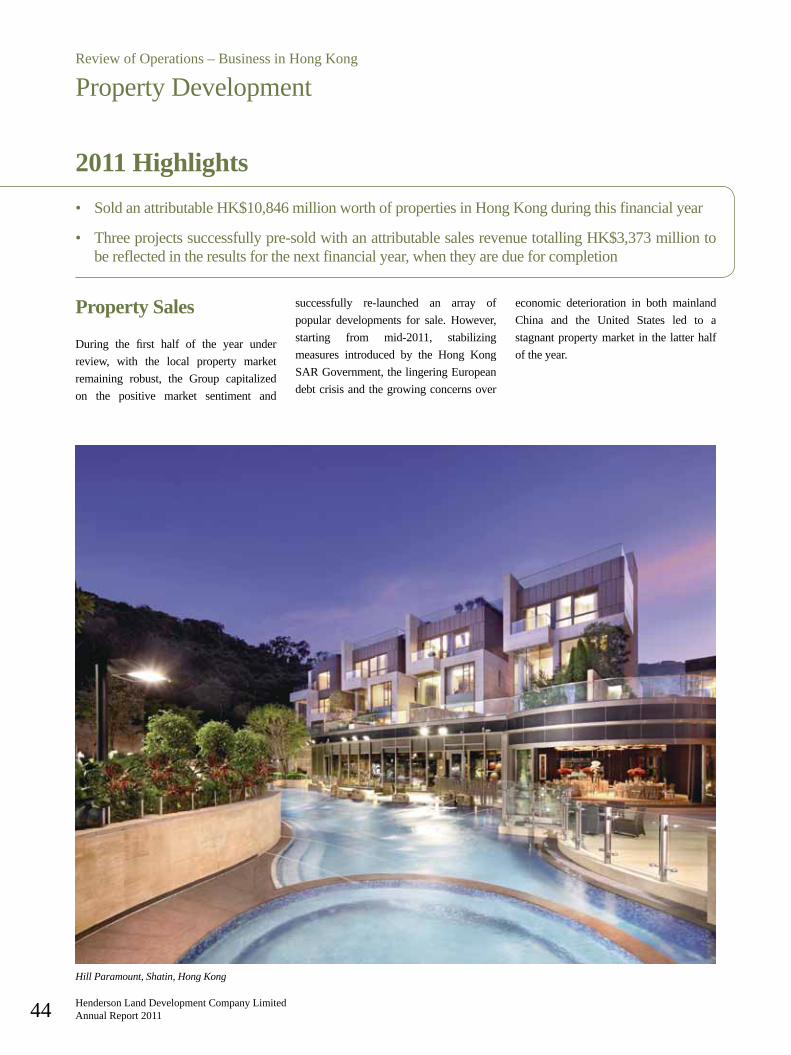

Business Review - Hong Kong

Property SalesDuring the first half of the year underreview, with the local property marketremaining robust, the Group capitalizedon the positive market sentiment andsuccessfully re-launched an array ofpopular developments for sale. However,starting from mid-2011, stabilizingmeasures introduced by the Hong KongSARGovernment,thelingeringEuropeandebtcrisisandthegrowingconcernsovereconomic deterioration in both mainlandChina and the United States led to astagnantpropertymarket in thelatterhalfoftheyear.

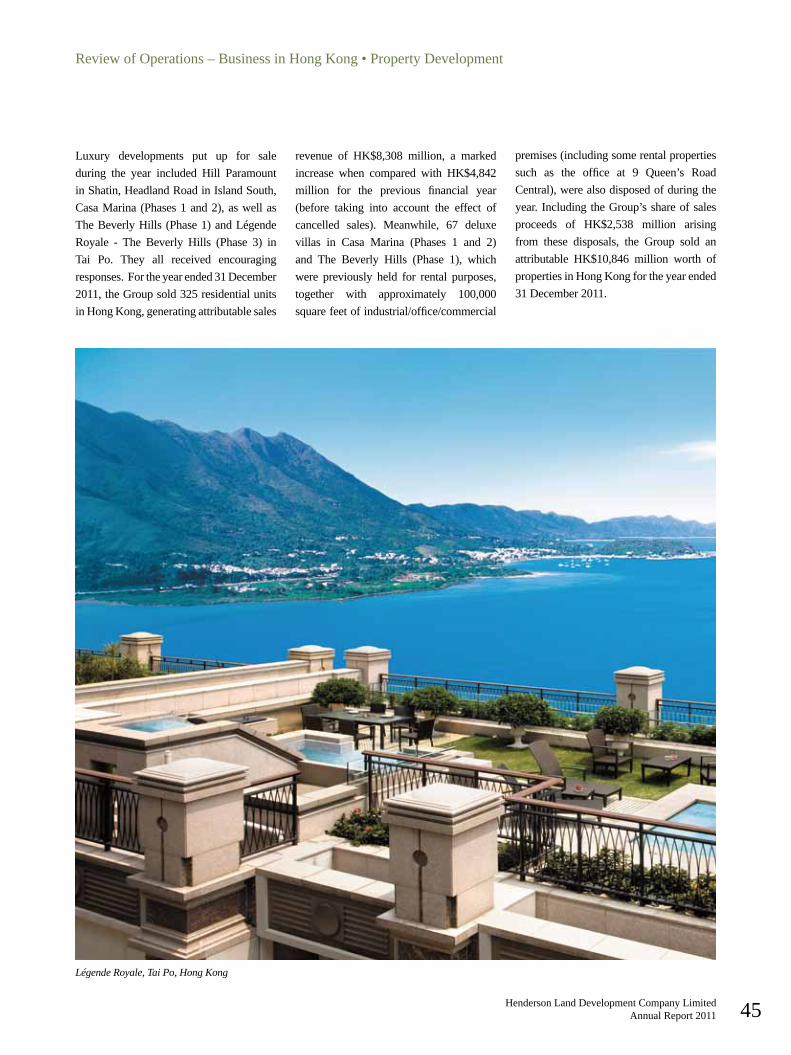

Luxury developments put up for saleduring the year included Hill ParamountinShatin,HeadlandRoadinIslandSouth,CasaMarina(Phases1and2),aswellasTheBeverlyHills(Phase1)andLégendeRoyale - The Beverly Hills (Phase 3) inTai Po. They all received encouragingresponses.Fortheyearended31December2011,theGroupsold325residentialunitsinHongKong,generatingattributablesalesrevenue of HK$8,308 million, a marked

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport2011 11

increase when compared with HK$4,842million for the previous financial year(before taking into account the effect of cancelled sales). Meanwhile, 67 deluxevillas in Casa Marina (Phases 1 and 2)and The Beverly Hills (Phase 1), whichwere previously held for rental purposes,together with approximately 100,000squarefeetofindustrial/office/commercial

The Gloucester and Mira Moon, Wanchai, Hong Kong (artist’s impression)

premises(includingsomerentalpropertiessuch as the office at 9 Queen’s RoadCentral),werealsodisposedofduringtheyear. IncludingtheGroup’sshareofsalesproceeds of HK$2,538 million arisingfrom these disposals, the Group sold anattributable HK$10,846 million worth ofproperties in Hong Kong for the year ended 31December2011.

Furthermore, The Gloucester, an114,000-square-foot signature residentialproject situated on Hong Kong waterfront with full sea views, was launched forpre-sale inApril 2011 with over 90% ofits total 177 residential units snapped upby the end of the year. E-Trade Plaza, a170,000-square-footGradeAoffice towerat IslandEast, also achieved encouragingresultswithabout30%ofitssaleableareasuccessfully sold within a few monthssince its pre-sale in the fourth quarter of2011.AZURA, theGroup’s joint venturedevelopmentatMid-LevelsofHongKongIsland,wentonsaleinNovember2010andcumulatively,98ofitstotal126residentialunits had been pre-sold by the end of2011. Their attributable sales revenuetotallingHK$3,373million,aswellasthecorresponding profit contribution, will bereflectedintheresultsforthenextfinancialyear,whentheyaredueforcompletion.

LaVerte inFanlinghassoldwell since itwasreleasedforsaleinFebruary2012.

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport201112

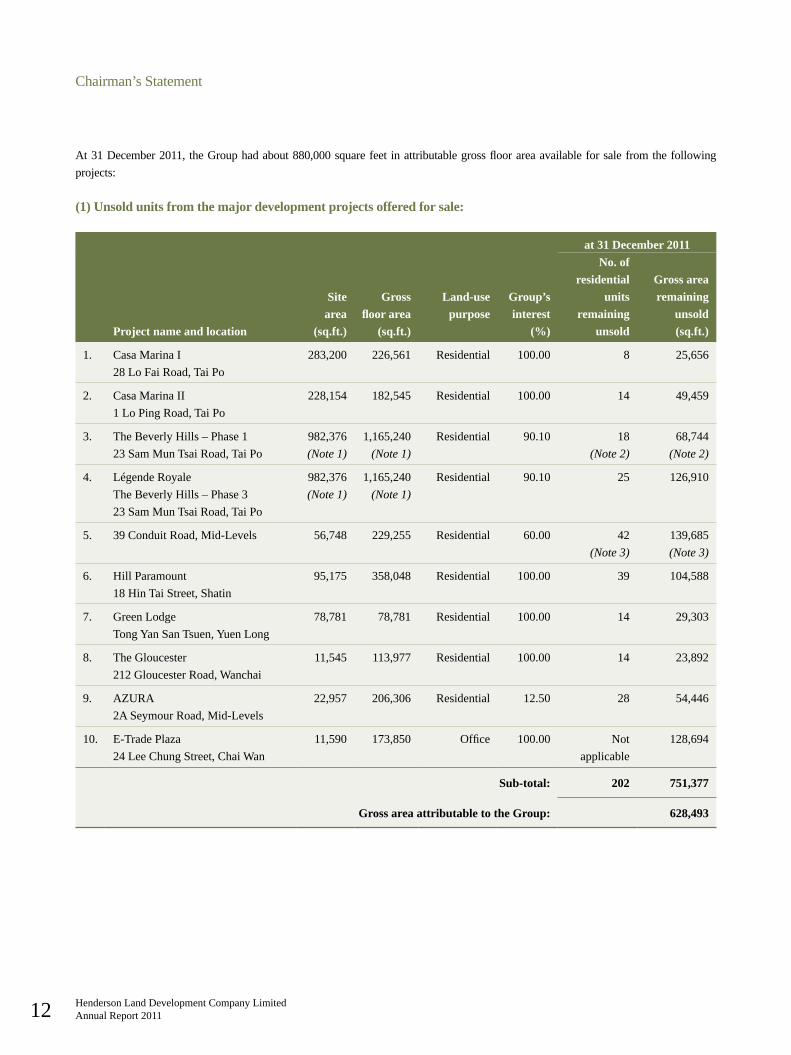

At31December2011, theGrouphadabout880,000squarefeet inattributablegrossfloorareaavailableforsalefromthefollowingprojects:

(1) Unsold units from the major development projects offered for sale:

at 31 December 2011

Project name and location

Sitearea

(sq.ft.)

Gross floor area

(sq.ft.)

Land-usepurpose

Group’s interest

(%)

No. of residential

units remaining

unsold

Gross arearemaining

unsold (sq.ft.)

1. Casa Marina I28LoFaiRoad,TaiPo

283,200 226,561 Residential 100.00 8 25,656

2. Casa Marina II1LoPingRoad,TaiPo

228,154 182,545 Residential 100.00 14 49,459

3. TheBeverlyHills–Phase123SamMunTsaiRoad,TaiPo

982,376(Note 1)

1,165,240(Note 1)

Residential 90.10 18(Note 2)

68,744(Note 2)

4. LégendeRoyaleTheBeverlyHills–Phase323SamMunTsaiRoad,TaiPo

982,376(Note 1)

1,165,240(Note 1)

Residential 90.10 25 126,910

5. 39ConduitRoad,Mid-Levels 56,748 229,255 Residential 60.00 42(Note 3)

139,685(Note 3)

6. HillParamount18HinTaiStreet,Shatin

95,175 358,048 Residential 100.00 39 104,588

7. Green Lodge TongYanSanTsuen,YuenLong

78,781 78,781 Residential 100.00 14 29,303

8. TheGloucester212GloucesterRoad,Wanchai

11,545 113,977 Residential 100.00 14 23,892

9. AZURA2ASeymourRoad,Mid-Levels

22,957 206,306 Residential 12.50 28 54,446

10. E-TradePlaza24LeeChungStreet,ChaiWan

11,590 173,850 Office 100.00 Not applicable

128,694

Sub-total: 202 751,377

Gross area attributable to the Group: 628,493

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport2011 13

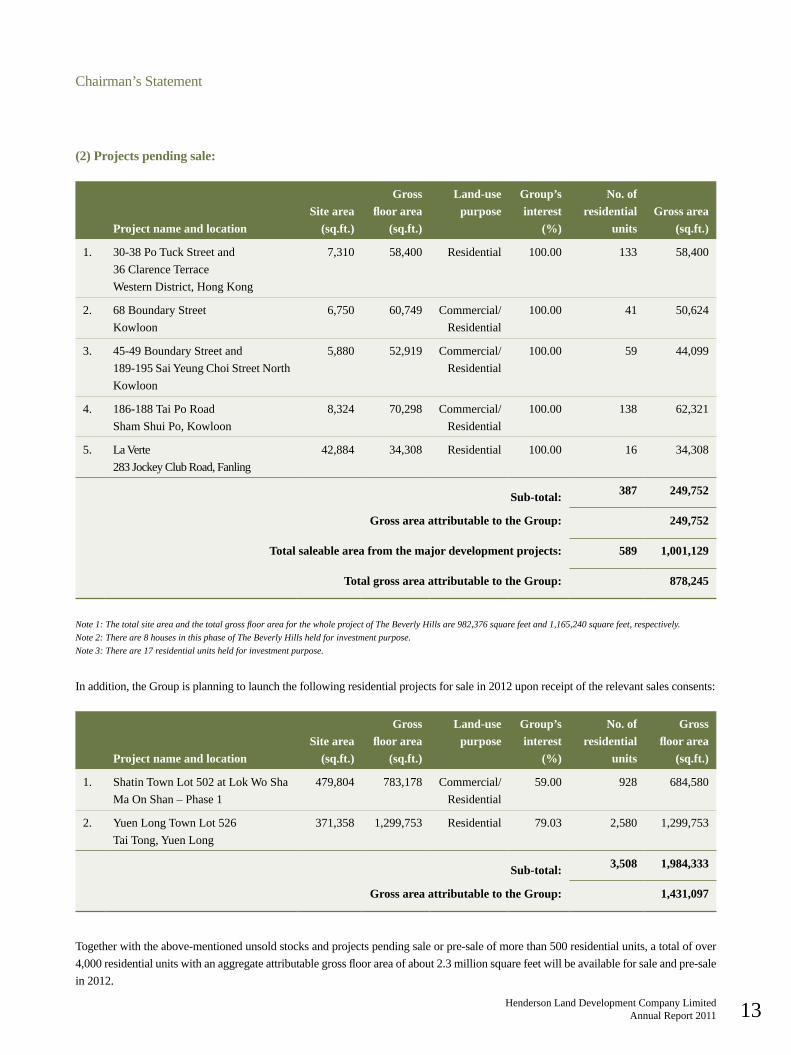

(2) Projects pending sale:

Project name and locationSite area

(sq.ft.)

Gross floor area

(sq.ft.)

Land-use purpose

Group’s interest

(%)

No. ofresidential

unitsGross area

(sq.ft.)

1. 30-38PoTuckStreetand36ClarenceTerraceWesternDistrict,HongKong

7,310 58,400 Residential 100.00 133 58,400

2. 68 Boundary StreetKowloon

6,750 60,749 Commercial/Residential

100.00 41 50,624

3. 45-49BoundaryStreetand189-195SaiYeungChoiStreetNorthKowloon

5,880 52,919 Commercial/Residential

100.00 59 44,099

4. 186-188TaiPoRoadShamShuiPo,Kowloon

8,324 70,298 Commercial/Residential

100.00 138 62,321

5. La Verte283JockeyClubRoad,Fanling

42,884 34,308 Residential 100.00 16 34,308

Sub-total: 387 249,752

Gross area attributable to the Group: 249,752

Total saleable area from the major development projects: 589 1,001,129

Total gross area attributable to the Group: 878,245

Note 1: The total site area and the total gross floor area for the whole project of The Beverly Hills are 982,376 square feet and 1,165,240 square feet, respectively.Note 2: There are 8 houses in this phase of The Beverly Hills held for investment purpose. Note 3: There are 17 residential units held for investment purpose.

Inaddition,theGroupisplanningtolaunchthefollowingresidentialprojectsforsalein2012uponreceiptoftherelevantsalesconsents:

Project name and locationSite area

(sq.ft.)

Gross floor area

(sq.ft.)

Land-use purpose

Group’s interest

(%)

No. ofresidential

units

Gross floor area

(sq.ft.)

1. ShatinTownLot502atLokWoShaMaOnShan–Phase1

479,804 783,178 Commercial/Residential

59.00 928 684,580

2. YuenLongTownLot526TaiTong,YuenLong

371,358 1,299,753 Residential 79.03 2,580 1,299,753

Sub-total: 3,508 1,984,333

Gross area attributable to the Group: 1,431,097

Togetherwiththeabove-mentionedunsoldstocksandprojectspendingsaleorpre-saleofmorethan500residentialunits,atotalofover4,000residentialunitswithanaggregateattributablegrossfloorareaofabout2.3millionsquarefeetwillbeavailableforsaleandpre-salein2012.

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport201114

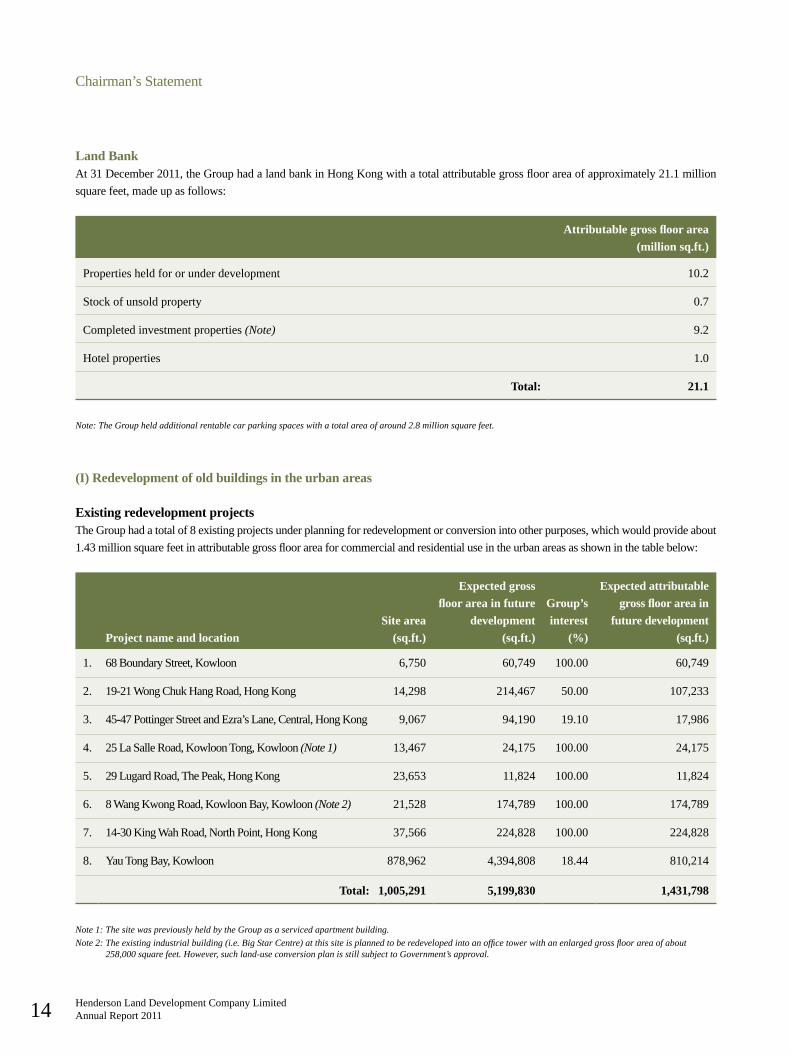

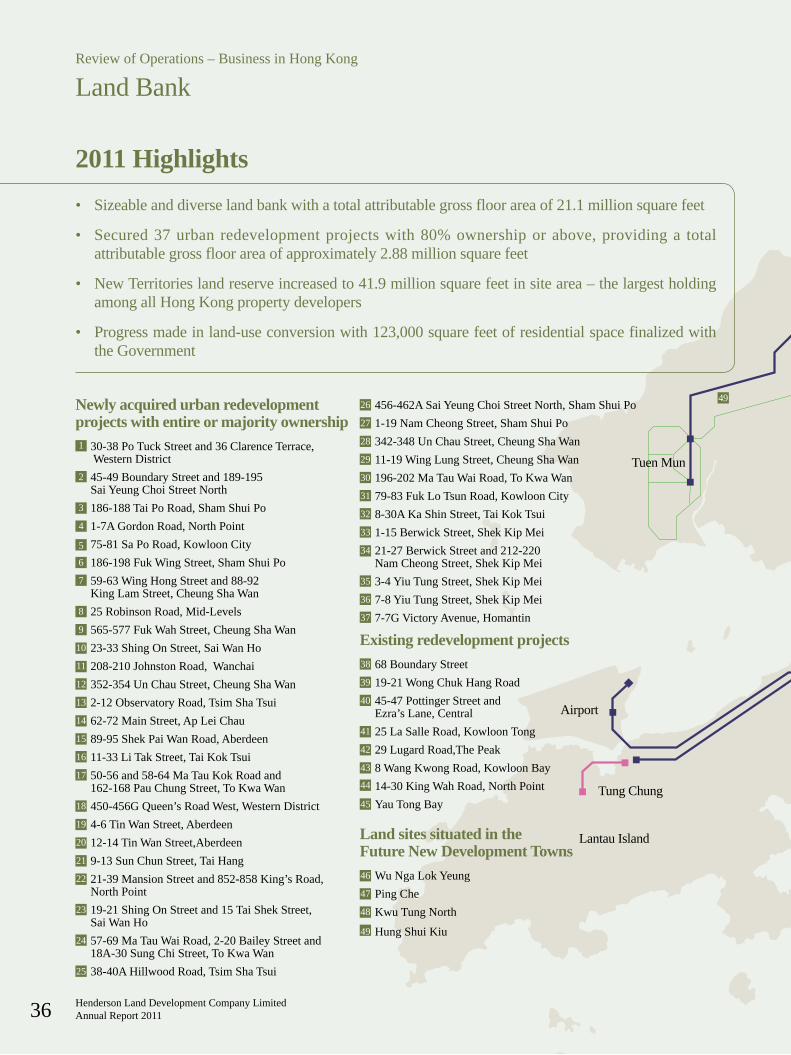

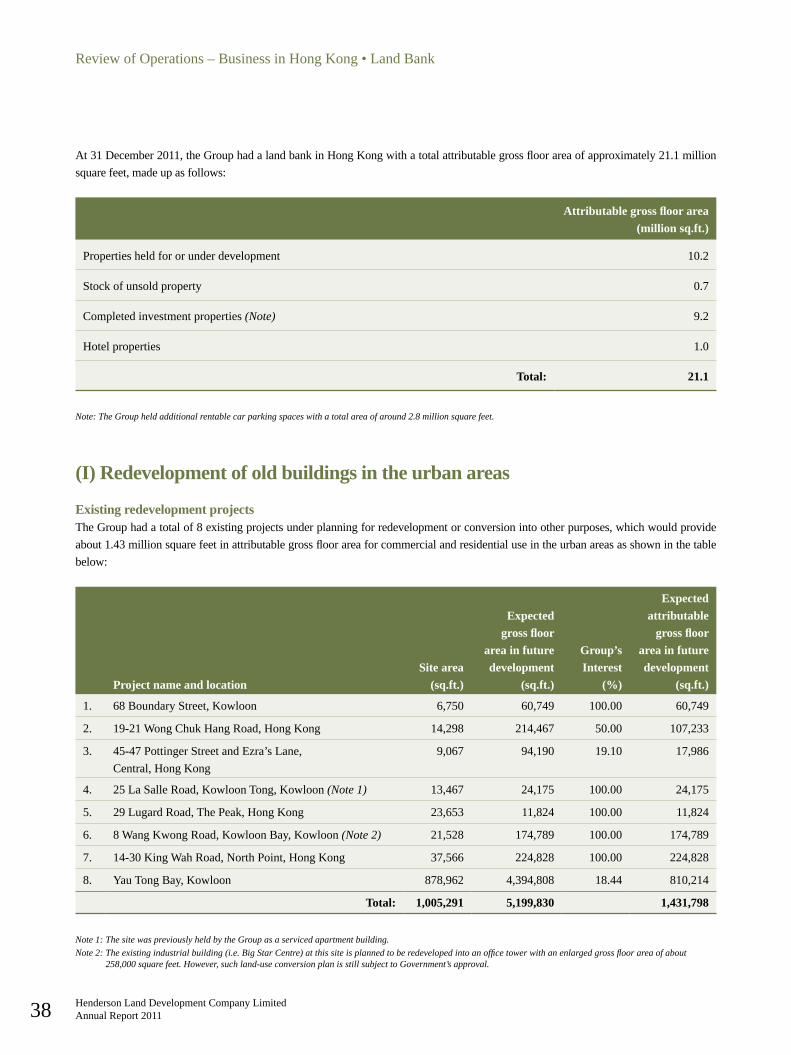

Land Bank At31December2011,theGrouphadalandbankinHongKongwithatotalattributablegrossfloorareaofapproximately21.1millionsquarefeet,madeupasfollows:

Attributable gross floor area(million sq.ft.)

Propertiesheldfororunderdevelopment 10.2

Stockofunsoldproperty 0.7

Completedinvestmentproperties(Note) 9.2

Hotelproperties 1.0

Total: 21.1

Note: The Group held additional rentable car parking spaces with a total area of around 2.8 million square feet.

(I) Redevelopment of old buildings in the urban areas

Existing redevelopment projectsTheGrouphadatotalof8existingprojectsunderplanningforredevelopmentorconversionintootherpurposes,whichwouldprovideabout1.43millionsquarefeetinattributablegrossfloorareaforcommercialandresidentialuseintheurbanareasasshowninthetablebelow:

Project name and locationSite area

(sq.ft.)

Expected gross floor area in future

development(sq.ft.)

Group’sinterest

(%)

Expected attributable gross floor area in

future development(sq.ft.)

1. 68BoundaryStreet,Kowloon 6,750 60,749 100.00 60,749

2. 19-21WongChukHangRoad,HongKong 14,298 214,467 50.00 107,233

3. 45-47PottingerStreetandEzra’sLane,Central,HongKong 9,067 94,190 19.10 17,986

4. 25LaSalleRoad,KowloonTong,Kowloon(Note 1) 13,467 24,175 100.00 24,175

5. 29LugardRoad,ThePeak,HongKong 23,653 11,824 100.00 11,824

6. 8WangKwongRoad,KowloonBay,Kowloon(Note 2) 21,528 174,789 100.00 174,789

7. 14-30KingWahRoad,NorthPoint,HongKong 37,566 224,828 100.00 224,828

8. YauTongBay,Kowloon 878,962 4,394,808 18.44 810,214

Total: 1,005,291 5,199,830 1,431,798

Note 1: The site was previously held by the Group as a serviced apartment building. Note 2: The existing industrial building (i.e. Big Star Centre) at this site is planned to be redeveloped into an office tower with an enlarged gross floor area of about

258,000 square feet. However, such land-use conversion plan is still subject to Government’s approval.

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport2011 15

Project name and location

Site area

(sq.ft.)

Expectedattributable

gross floor areain future development

(sq.ft.)

Expected year of sales launch

(Note 1)

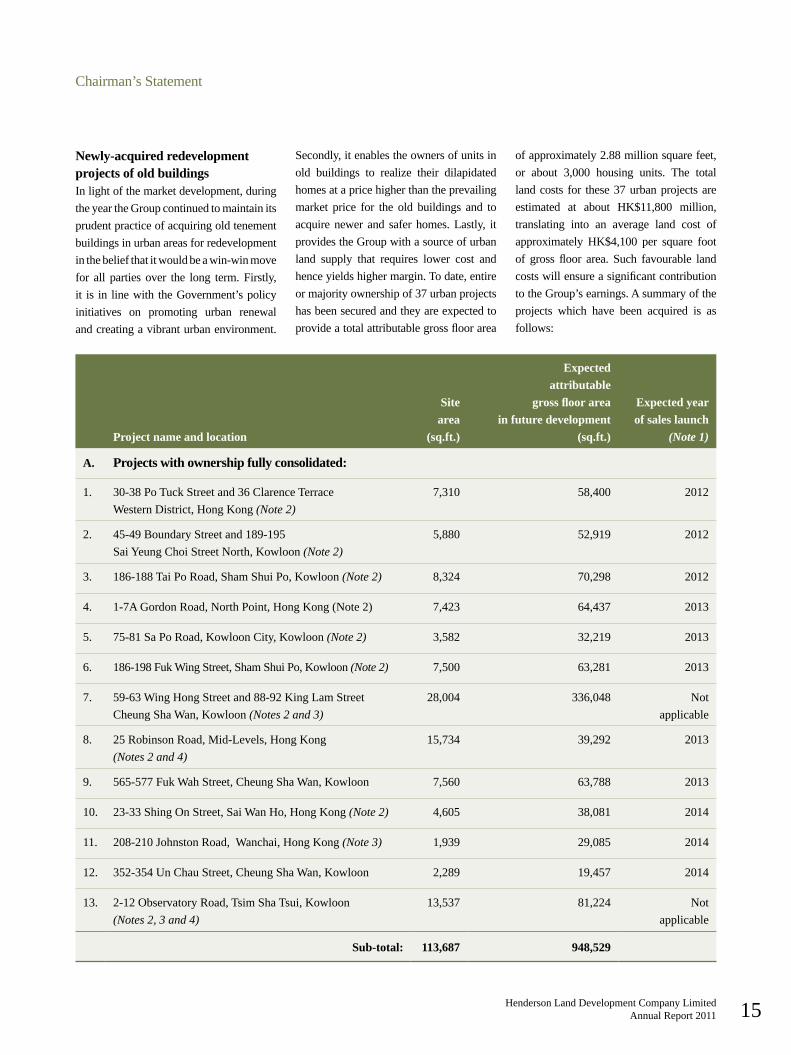

A. Projects with ownership fully consolidated:

1. 30-38PoTuckStreetand36ClarenceTerraceWesternDistrict,HongKong(Note 2)

7,310 58,400 2012

2. 45-49BoundaryStreetand189-195 SaiYeungChoiStreetNorth,Kowloon(Note 2)

5,880 52,919 2012

3. 186-188TaiPoRoad,ShamShuiPo,Kowloon(Note 2) 8,324 70,298 2012

4. 1-7AGordonRoad,NorthPoint,HongKong(Note2) 7,423 64,437 2013

5. 75-81SaPoRoad,KowloonCity,Kowloon(Note 2) 3,582 32,219 2013

6. 186-198FukWingStreet,ShamShuiPo,Kowloon(Note 2) 7,500 63,281 2013

7. 59-63WingHongStreetand88-92KingLamStreetCheungShaWan,Kowloon(Notes 2 and 3)

28,004 336,048 Notapplicable

8. 25RobinsonRoad,Mid-Levels,HongKong(Notes 2 and 4)

15,734 39,292 2013

9. 565-577FukWahStreet,CheungShaWan,Kowloon 7,560 63,788 2013

10. 23-33ShingOnStreet,SaiWanHo,HongKong(Note 2) 4,605 38,081 2014

11. 208-210JohnstonRoad,Wanchai,HongKong(Note 3) 1,939 29,085 2014

12. 352-354UnChauStreet,CheungShaWan,Kowloon 2,289 19,457 2014

13. 2-12ObservatoryRoad,TsimShaTsui,Kowloon(Notes 2, 3 and 4)

13,537 81,224 Notapplicable

Sub-total: 113,687 948,529

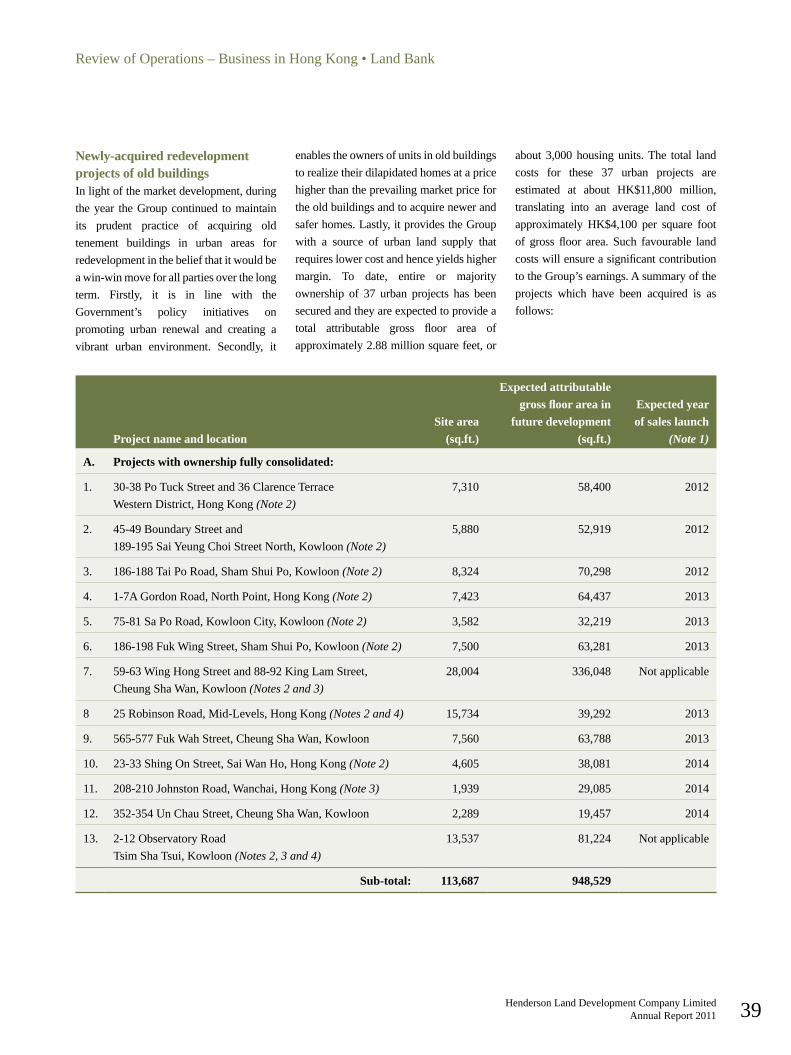

Newly-acquired redevelopment projects of old buildingsInlightofthemarketdevelopment,duringtheyeartheGroupcontinuedtomaintainitsprudentpracticeofacquiringoldtenementbuildingsinurbanareasforredevelopmentinthebeliefthatitwouldbeawin-winmovefor all parties over the long term.Firstly,it is in linewith theGovernment’spolicyinitiatives on promoting urban renewalandcreatingavibranturbanenvironment.

Secondly,itenablestheownersofunitsinold buildings to realize their dilapidatedhomesatapricehigherthantheprevailingmarket price for the old buildings and toacquire newer and safer homes.Lastly, itprovidestheGroupwithasourceofurbanland supply that requires lower cost andhenceyieldshighermargin.Todate,entireormajorityownershipof37urbanprojectshasbeensecuredandtheyareexpectedtoprovideatotalattributablegrossfloorarea

ofapproximately2.88millionsquarefeet,or about 3,000 housing units. The totallandcosts for these37urbanprojectsareestimated at about HK$11,800 million,translating into an average land cost ofapproximately HK$4,100 per square footof gross floor area. Such favourable landcostswillensureasignificantcontributiontotheGroup’searnings.Asummaryoftheprojects which have been acquired is asfollows:

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport201116

Project name and locationSite area

(sq.ft.)

Expectedattributable

gross floor areain future development

(sq.ft.)

Expected year of sales launch

(Note 1)

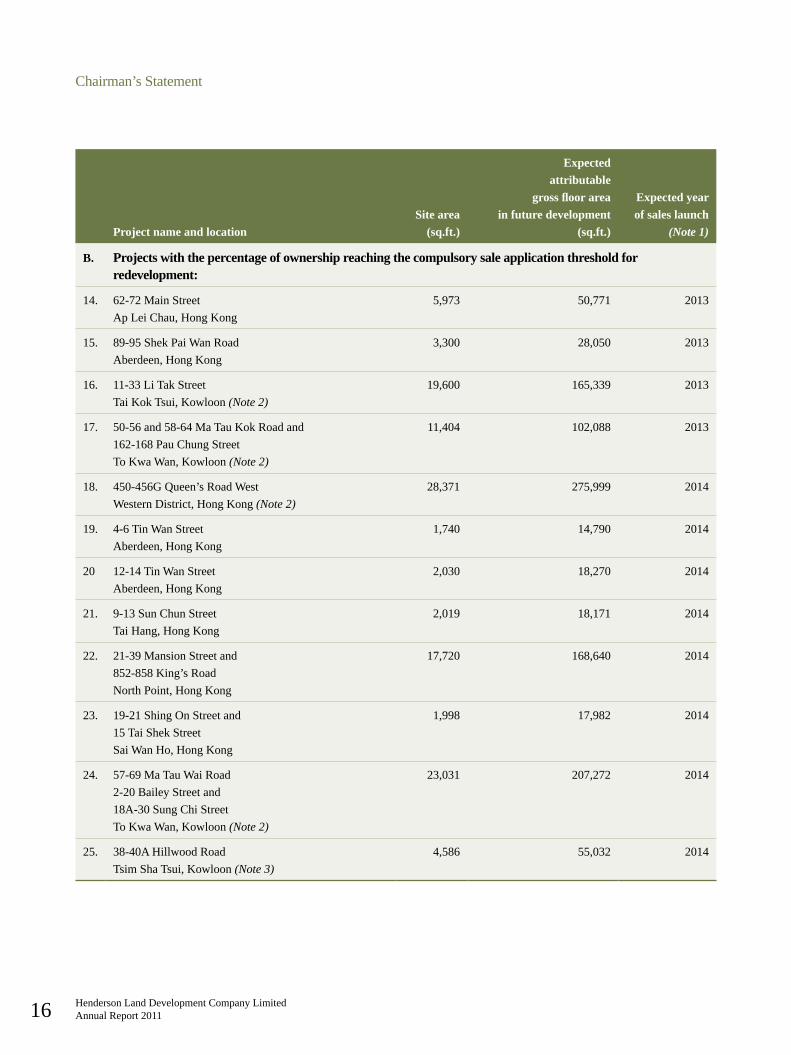

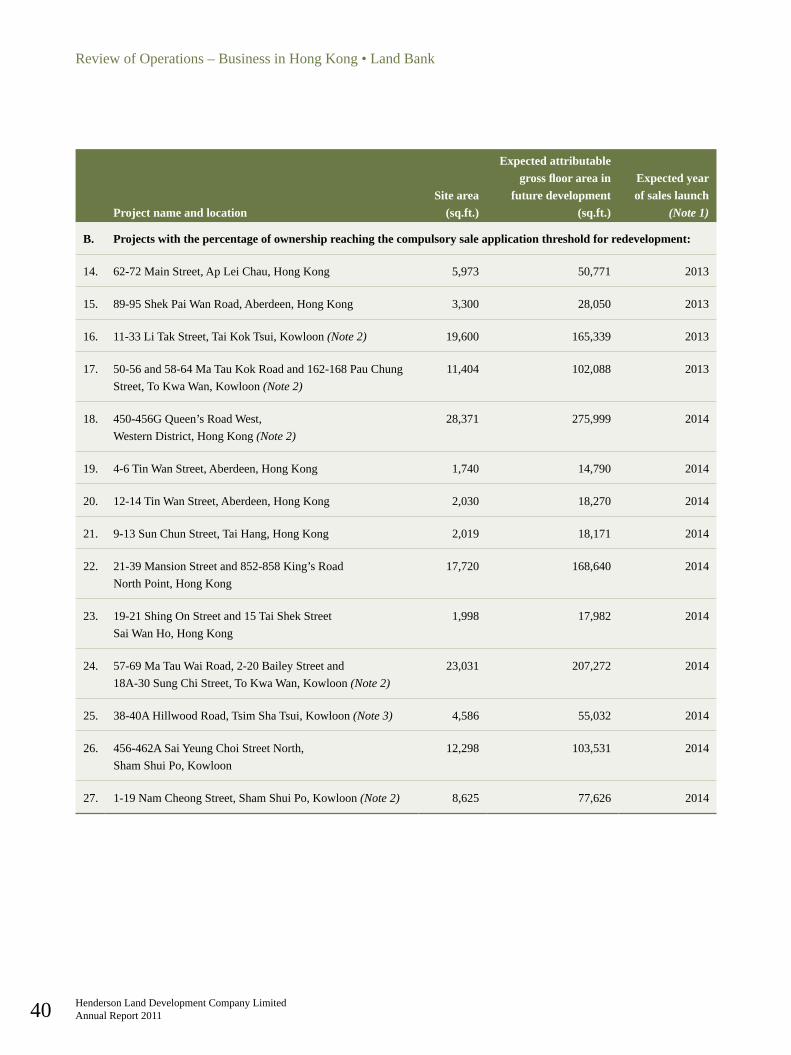

B. Projects with the percentage of ownership reaching the compulsory sale application threshold for redevelopment:

14. 62-72MainStreetApLeiChau,HongKong

5,973 50,771 2013

15. 89-95ShekPaiWanRoadAberdeen,HongKong

3,300 28,050 2013

16. 11-33LiTakStreetTaiKokTsui,Kowloon(Note 2)

19,600 165,339 2013

17. 50-56and58-64MaTauKokRoadand162-168PauChungStreetToKwaWan,Kowloon(Note 2)

11,404 102,088 2013

18. 450-456GQueen’sRoadWestWesternDistrict,HongKong(Note 2)

28,371 275,999 2014

19. 4-6TinWanStreetAberdeen,HongKong

1,740 14,790 2014

20 12-14TinWanStreetAberdeen,HongKong

2,030 18,270 2014

21. 9-13SunChunStreetTaiHang,HongKong

2,019 18,171 2014

22. 21-39MansionStreetand852-858King’sRoadNorthPoint,HongKong

17,720 168,640 2014

23. 19-21ShingOnStreetand15TaiShekStreetSaiWanHo,HongKong

1,998 17,982 2014

24. 57-69MaTauWaiRoad2-20BaileyStreetand18A-30SungChiStreetToKwaWan,Kowloon(Note 2)

23,031 207,272 2014

25. 38-40AHillwoodRoadTsimShaTsui,Kowloon(Note 3)

4,586 55,032 2014

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport2011 17

Project name and locationSite area

(sq.ft.)

Expectedattributable

gross floor areain future development

(sq.ft.)

Expected year of sales launch

(Note 1)

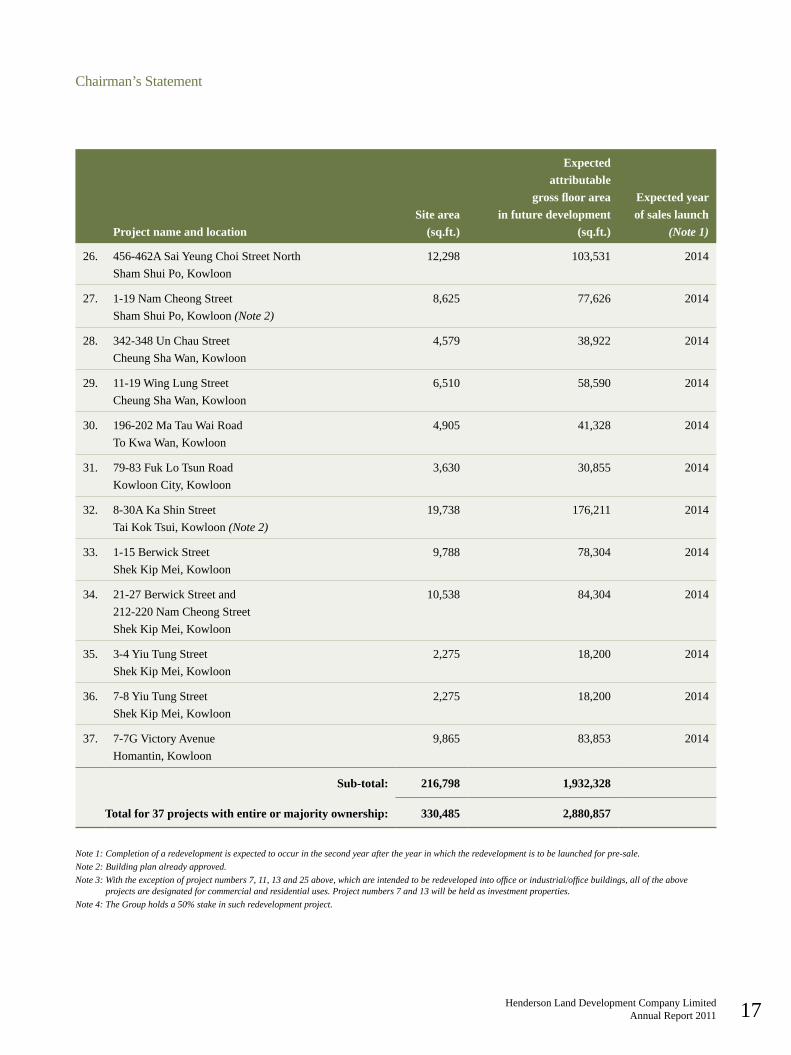

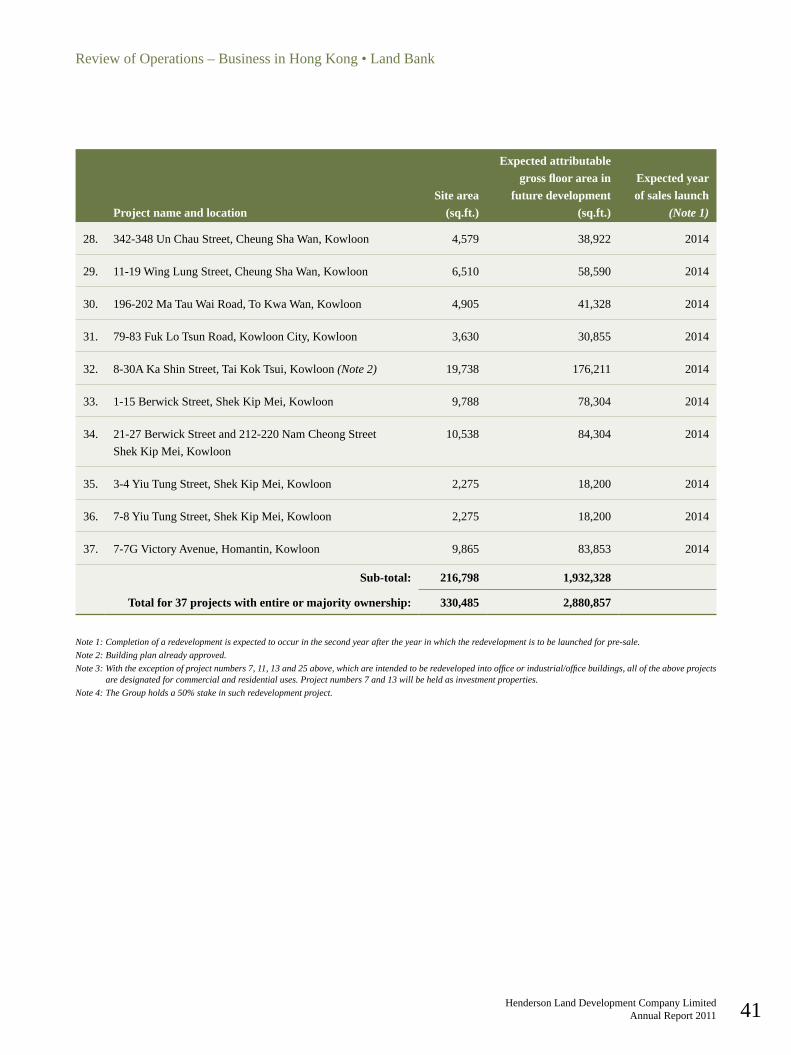

26. 456-462ASaiYeungChoiStreetNorthShamShuiPo,Kowloon

12,298 103,531 2014

27. 1-19NamCheongStreetShamShuiPo,Kowloon(Note 2)

8,625 77,626 2014

28. 342-348UnChauStreetCheungShaWan,Kowloon

4,579 38,922 2014

29. 11-19WingLungStreetCheungShaWan,Kowloon

6,510 58,590 2014

30. 196-202MaTauWaiRoadToKwaWan,Kowloon

4,905 41,328 2014

31. 79-83FukLoTsunRoadKowloonCity,Kowloon

3,630 30,855 2014

32. 8-30AKaShinStreetTaiKokTsui,Kowloon(Note 2)

19,738 176,211 2014

33. 1-15BerwickStreetShekKipMei,Kowloon

9,788 78,304 2014

34. 21-27BerwickStreetand212-220NamCheongStreetShekKipMei,Kowloon

10,538 84,304 2014

35. 3-4YiuTungStreetShekKipMei,Kowloon

2,275 18,200 2014

36. 7-8YiuTungStreetShekKipMei,Kowloon

2,275 18,200 2014

37. 7-7GVictoryAvenueHomantin,Kowloon

9,865 83,853 2014

Sub-total: 216,798 1,932,328

Total for 37 projects with entire or majority ownership: 330,485 2,880,857

Note 1: Completion of a redevelopment is expected to occur in the second year after the year in which the redevelopment is to be launched for pre-sale.Note 2: Building plan already approved.Note 3: With the exception of project numbers 7, 11, 13 and 25 above, which are intended to be redeveloped into office or industrial/office buildings, all of the above

projects are designated for commercial and residential uses. Project numbers 7 and 13 will be held as investment properties.Note 4: The Group holds a 50% stake in such redevelopment project.

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport201118

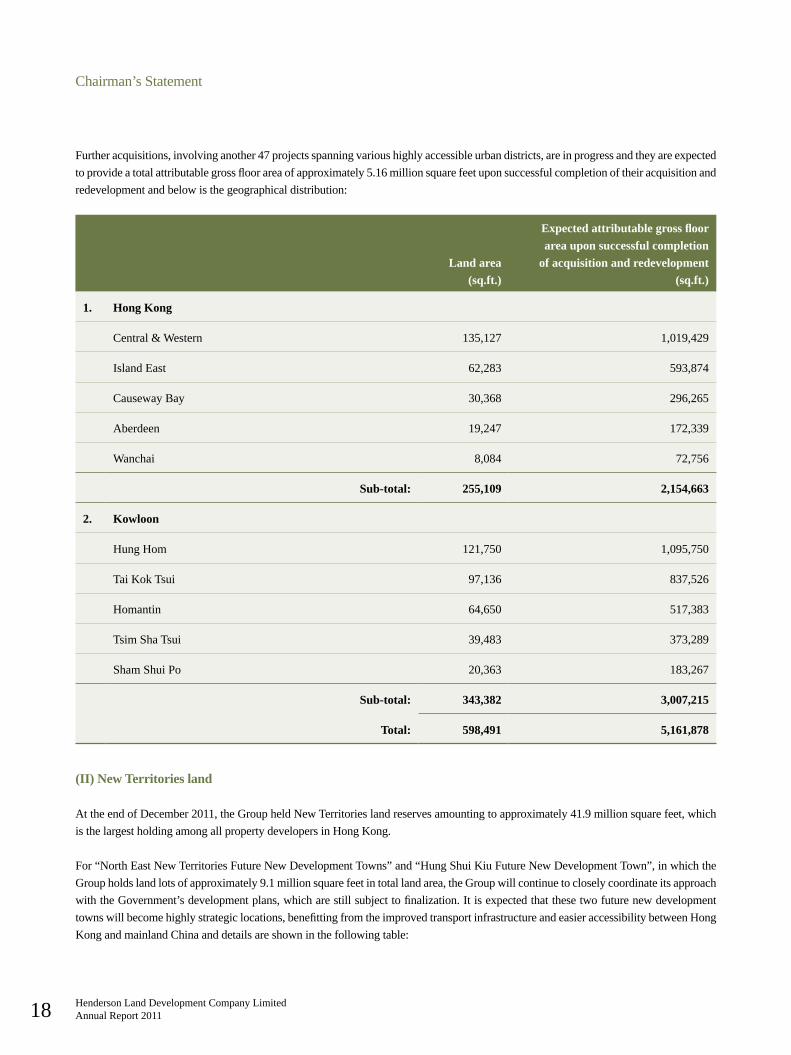

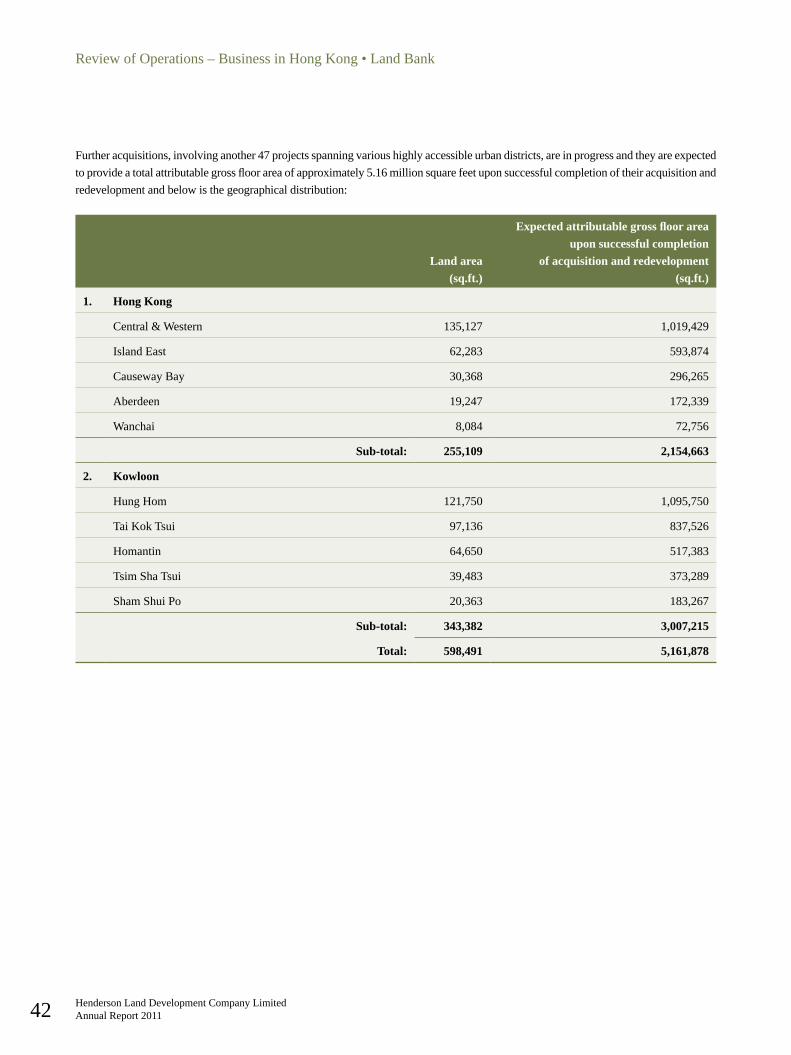

Furtheracquisitions,involvinganother47projectsspanningvarioushighlyaccessibleurbandistricts,areinprogressandtheyareexpectedtoprovideatotalattributablegrossfloorareaofapproximately5.16millionsquarefeetuponsuccessfulcompletionoftheiracquisitionandredevelopmentandbelowisthegeographicaldistribution:

Land area(sq.ft.)

Expected attributable gross floor area upon successful completion

of acquisition and redevelopment (sq.ft.)

1. Hong Kong

Central&Western 135,127 1,019,429

IslandEast 62,283 593,874

Causeway Bay 30,368 296,265

Aberdeen 19,247 172,339

Wanchai 8,084 72,756

Sub-total: 255,109 2,154,663

2. Kowloon

HungHom 121,750 1,095,750

Tai Kok Tsui 97,136 837,526

Homantin 64,650 517,383

TsimShaTsui 39,483 373,289

ShamShuiPo 20,363 183,267

Sub-total: 343,382 3,007,215

Total: 598,491 5,161,878

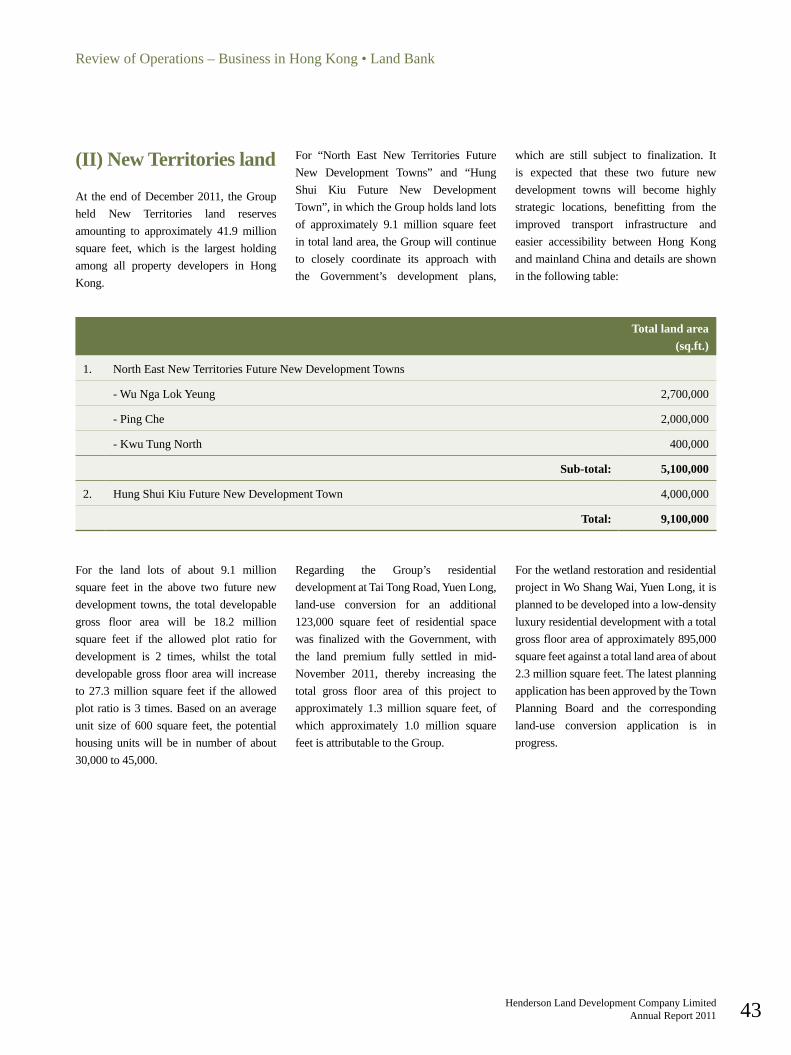

(II) New Territories land

AttheendofDecember2011,theGroupheldNewTerritorieslandreservesamountingtoapproximately41.9millionsquarefeet,whichisthelargestholdingamongallpropertydevelopersinHongKong. For“NorthEastNewTerritoriesFutureNewDevelopmentTowns”and“HungShuiKiuFutureNewDevelopmentTown”,inwhichtheGroupholdslandlotsofapproximately9.1millionsquarefeetintotallandarea,theGroupwillcontinuetocloselycoordinateitsapproachwiththeGovernment’sdevelopmentplans,whicharestillsubjecttofinalization.Itisexpectedthatthesetwofuturenewdevelopmenttownswillbecomehighlystrategiclocations,benefittingfromtheimprovedtransportinfrastructureandeasieraccessibilitybetweenHongKongandmainlandChinaanddetailsareshowninthefollowingtable:

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport2011 19

Total land area(sq.ft.)

1. NorthEastNewTerritoriesFutureNewDevelopmentTowns

-WuNgaLokYeung 2,700,000

-PingChe 2,000,000

-KwuTungNorth 400,000

Sub-total: 5,100,000

2. HungShuiKiuFutureNewDevelopmentTown 4,000,000

Total: 9,100,000

For the land lots of about 9.1 millionsquare feet in the above two future newdevelopment towns, the total developablegross floor area will be 18.2 millionsquare feet if the allowed plot ratio fordevelopment is 2 times, whilst the totaldevelopablegrossfloorareawill increaseto27.3million square feet if the allowedplotratiois3times.Basedonanaverageunit size of 600 square feet, the potentialhousingunitswill be in numberof about30,000to45,000.

Regarding the Group’s residentialdevelopmentatTaiTongRoad,YuenLong,land-use conversion for an additional123,000 square feet of residential spacewas finalized with the Government, withthe land premium fully settled in mid-November 2011, thereby increasing thetotal gross floor area of this project toapproximately 1.3million square feet, ofwhich approximately 1.0 million squarefeetisattributabletotheGroup.

ForthewetlandrestorationandresidentialprojectinWoShangWai,YuenLong,itisplannedtobedevelopedintoalow-densityluxuryresidentialdevelopmentwithatotalgrossfloorareaofapproximately895,000squarefeetagainstatotallandareaofabout

2.3millionsquarefeet.ThelatestplanningapplicationhasbeenapprovedbytheTownPlanning Board and the correspondingland-use conversion application is inprogress.

Investment PropertiesAt 31 December 2011, the Group helda total attributable gross floor area ofapproximately 9.2 million square feet incompleted investment properties inHongKong, comprising 4.5million square feetofcommercialor retailspace,3.4millionsquare feet of office space, 0.9 millionsquare feet of industrial/office space and0.4million square feet of residential andapartment space. This leasing portfoliois geographically diverse, with 25% inHong Kong Island, 34% in Kowloonand the remaining41%in thenew towns(withmost of the latter being large-scaleshoppingmalls). Leasing performance was impressiveduring the year with gross rental incomesetting a new record. The Group’sattributablegrossrentalincomeNote in Hong Kong for the year ended 31 December2011 increased by 11% to HK$4,889million,whilstpre-taxnetrentalincomeNote was HK$3,585 million, representing a

growthof15%overthepreviousyear.At31December2011,theleasingratefortheGroup’scorerentalpropertiesroseto97%.(Note:thisfigureincludesthatderivedfromthe

investment properties owned by the Group’s

subsidiaries (after deducting non-controlling

interests), associates and jointly controlled

entities)

Given continued growth in localconsumption, as well as the ever-increasing number of mainland touristspurchasing international brands, HongKong’s retail sales grew briskly in 2011.In response to market changes and totap new opportunities, the Group stagedinnovative marketing activities, includingorganizingshoppingtoursformainlandersandan increasedadoptionofmulti-mediapromotional channels, to draw moreshoppers to its shoppingmalls and boosttenants’business.Thesemarketingeffortscoupled with the advantageous locationsnear MTR stations make these shoppingmalls the preferred choice for manydiscerning retailers. For instance, Inditex,aglobalfashiongroup,hascommittedtoatotalgrossfloorareaof62,000squarefeetatMetroCityPhaseIIinTseungKwanOforits threewell-known internationalbrands,namely Zara which has opened already,

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport201120

BershkaandPull&Bear,whichareduetoopenconsecutivelyin2012,whilstH&MHennes&MauritzLimited,anotherglobalfashiongroup,hasalsocommittedtoatotalgrossfloorareaofover53,000squarefeetatthismallforitswell-knowninternationalbrand,H&Mwhichisduetoopeninmid-2012.ThewholeSkylinePlaza, a4-levelshoppingmall inTsuenWanwith a totalgross floor area of over 150,000 squarefeet, was leased to a famous departmentstore, which will open for business andprovideone-stopshoppingconveniencein2012.Consequently,most of theGroup’sshoppingmalls, ranging from ifcmall inCentraltoregionalshoppingcentresinnewtowns, recordednearly fulloccupancybytheendofthefinancialyear.

Onthebackofpersistentdemandgrowth,driven by business expansion and newcorporate set-ups particularly in the firsthalfoftheyear,coupledwithlimitednewoffice supply, the Group’s premier officedevelopmentsinthecoreareas,suchastheifc inCentral,AIATower inNorthPointaswellasINGTowerandGoldenCentrein SheungWan, have all performed wellwith increased rents for both renewalsand new lettings. In the up-and-comingcommercial hub of Kowloon East, theGroup’s approximately 2,000,000-square-foot portfolio of premium office andindustrial premises benefitted from thetrend of office decentralization with theoverall leasing rate surging from 87% at31December2010to98%at31December2011.ManulifeFinancialCentreinKwunTong,whichsetanewbenchmarkforgreenoffice buildings in decentralized areasbyachieving the top“platinum” rating inthe Hong Kong Building EnvironmentalAssessment Method (HK-BEAM) inFebruary2011,was98%letbytheendofthefinancialyear.

ifc complex, Central, Hong Kong

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport2011 21

TheGroup’sdeluxeservicedsuitehotelatFour Seasons Place continued to achievehighoccupancyandincreasedrents,whilstluxuryresidencessuchasEvaCourtand39ConduitRoadatMid-Levelsalsorecordedsatisfactoryleasingperformance.

The Group continuously improvesaccessibilityandfacilitiesatitsinvestmentproperties so as to better serve thecommunityandenhancetheirrentalvalues.Metro City Phase II in Tseung Kwan O, which was ranked First by the HongKongFederation of theBlind,Centre forSocial PolicyStudies ofTheHongKongPolytechnic University and few othercharitable organizations for the disabledin Barrier-FreeAssessmentVisit 2011, isundergoing a revamp and the first phaseof renovationworkswillbecompleted inthefirstquarterof2012.Thesecondphaseof renovation commenced in December2011andwillbecompletedbytheendof2014. For theTrend Plaza inTuenMun,renovationtotheexternalwallofitsNorthWingwillalsobecompletedinmid-2012following the recent completion of afacelift at itsSouthWing.Thefirstphaseof refurbishment at Sunshine City PlazainMaOnShanisprogressingwell,whilsttheplanningofrenovationworksforCityLandmarkIinTsuenWanandAIATowerinNorthPointiscurrentlyinthepipeline.ForAIATowerinNorthPoint,acquisitionof its remaining 5.44% interest wascompleted in September 2011, allowingtheGrouptobenefitinfullfromitsfuturemajorrevamp.

Hotel and Retailing OperationsHong Kong’s hospitality industry posteda remarkable growth in 2011with visitorarrivals reaching a record high of around42million.TheFourSeasonsHotel,whichwas widely recognized as the marketleaderintown,continuedtowinnumerousprestigiousaccoladessuchasForbesFive-

Mira Moon, Wanchai, Hong Kong (artist’s impression)

StarAwardforHotelandtop3-starhonoursinthe2011MichelinGuideforitssignatureCapriceandLungKingHeenrestaurants.Asaresult,itenjoyedafurtherincreaseinoccupancyagainstahigheraverage roomrateduringtheyear.Meanwhile,theGroupalso owns and manages the 362-roomNewtonHotelHongKong, the317-roomNewtonInnNorthPointandthe598-room

Newton Place Hotel. Benefitting fromthe ever-increasing number of mainlandtourists, who accounted for over 60% oftheir total customers, the Group’s threeNewtonhotelshaveallachievedadouble-digit increase in average room rateswitha higher occupancy of over 80%. TheGroupisdevelopinganewboutiquehotel,Mira Moon, at388 JaffeRoad,Wanchai

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport201122

andupon its scheduled completion in thesecondquarterof2012,itwillbeoperatedbyTheMiraHongKongand91luxurioussuiteswill be added to theGroup’s hotelportfolio.Fortheyearended31December2011, the profit contributionNote from theGroup’s hotel operations increased by108%toHK$325million.(Note:thisfigureincludesthatderivedfromthehotelsownedby

theGroup’s subsidiaries, associates and jointly

controlledentities)

Established in 1989 as a complementarybusiness to the Group’s shoppingfacilities, Citistore’s retailing operationhas developed into a network of fivedepartment store outlets and two “id:c”specialty stores in Hong Kong. Givenimprovement in both local consumptionand visitor spending, Citistore recordeda satisfactory growth of 20% in pre-taxprofit against a13% increase in turnover.Meanwhile, the Group continued to holdinterests(7.41%at31December2011)inIntimeDepartmentStore(Group)CompanyLimited (stock code: 1833), which is arenowneddepartmentstorechainoperatingand managing 27 department stores andshopping centres across major cities inmainlandChina.

Construction and Property ManagementTheGroup cares for the environment andsupports sustainable development for thebenefitoffuturegenerations.Aspartofthispledge, inter-departmental communicationand stakeholder engagement are alwaysencouraged so as to ensure that localcontext, innovative architecture andsustainabilityfeaturesareperfectlyblendedintoalloftheGroup’snewdevelopmentsinbothHongKongandmainlandChina.Intheconstruction process, energy-efficient andeco-friendly features recommended by theLeadership in Energy and EnvironmentalDesign(LEED)andBuildingEnvironmentalAssessment Method (BEAM) Plus have

been persistently integrated. For instance,pre-fabricatedbuildingcomponentsarenowcommonly used so as to raise efficiencyby accelerating development progress forbetter quality control, whilst minimizingconstruction waste and disruption to the neighbourhoods. During the year, theGroup’s projects emerged as the firstbatchof developments inHongKong toachieve a China Green Building Label(GBL), which calls for reduced energyconsumptionatsiteworks, re-useof localnatural resources and the recycling ofconstructionwasteforbetterenvironmentalmanagement.

The Group’s attention to every detailthroughout the different stages of construction has also been extended toits developments in mainland China.In addition to its tight grip over all keyaspects of development such as selectionof main contractors and subcontractors,materialsourcingandtenderawarding,theConstruction Department also maintainsan ongoing dialogue with contractorsand conducts on-site inspections so as toensure that all the mainland projects arecompleted on schedule, within budgetand in line with the Group’s stringentenvironmental and quality requirements.In July 2011, accreditation as the “MainContractor of Housing Construction (Level III)” was received from BeijingMunicipal Commission of Housing andUrban-Rural Development, enabling theGroup’sConstructionDepartment to takea more active role in mainland propertydevelopmentinfuture.

The Group’s member propertymanagement companies, Hang YickProperties Management Limited (“HangYick”),WellBornRealEstateManagementLimited (“Well Born”) and GoodwillManagementLimited,collectivelymanagearound 76,000 apartments and industrial/commercialunits,7.9millionsquarefeetof

shoppingmallsandofficespaceand18,000carparkingunitsinHongKong.

HangYickandWellBornalsoprovidetheirqualitypropertyhandoverandmanagementservices to the Group’s propertydevelopmentsinmainlandChina.Servingatotalofabout5,000mainlandapartments,theyhavegainedwiderecognitionfortheirexcellent services. Hengbao Huating andHengli Wanpan Huayuan, for instance,were both accredited as a “CommunityShowcase in Guangdong Province” and“CommunityShowcaseinGuangzhou”.

The Group’s Construction and PropertyManagementTeamswereonthefrontlinethroughout the year to fulfil the Group’spledge of providing green efforts andcare to the community. Consequently,the Construction Department earnednumerous accolades during the yearincluding “Considerate Contractors SiteAward” from the Development Bureauof the Hong Kong SAR Government,as well as “Construction EnvironmentalAward – Merit” and “Proactive SafetyContractorAward” fromTheHongKongConstruction Association, whilst theProperty Management Teams also wonnearly 700 performance-related accoladesin addition to widespread recognition for theiradvocacyofcareandloveinthisYearof Care. Their unflagging efforts will beelaboratedinthe“SustainabilityandCSR”sectionoftheAnnualReport.

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport2011 23

Business Review - Mainland China

Inviewof theworseningglobaleconomy,the Central Government continually fine-tuned its austerity measures in 2011 tocool the mainland property market. Bothadministrative and economic initiatives,including restrictions on quantity of homepurchase, amount of mortgage, unit priceand unit size, were adopted in curbinghousingdemand.Suchmeasuresgaverisetoasharpdeclineintransactionvolume.Inthewakeofthetightenedcredit,manymainlanddevelopers traded price for volume, thusdepressingthehomepricesfurther.

Housing was still in great demand inmainland China. In those second andthird-tier cities in which the Grouphas residential development projects,with many infrastructural projects andtransport facilities such as highways,high-speed rails, community amenities

and greenery projects gradually beingcompleted, the environment has muchimproved.Besides,theGroup’sprojectsinChinaboastdistinctivedesignplans, full-range facilities, superb building qualityand proficient property management,targetingend-usersofmediumtohigh-endresidences.Suchprojectsarehighlysoughtafterandearnedacclaiminthemarket.

As a result of the austerity measures,the majority of home buyers wereend-users, who were much concernedabout the building quality and detailsof a development. Therefore, the Groupstepped up the promotion of its qualitybrand-name and refined its marketingcampaigns, whilst making appropriateadjustments to its sales-force. Turning topropertymanagement, theGroup always,wherelocalregulationsallow,providesitsown propertymanagement services to itsmainlanddevelopments.Forthoseprojectswhich require property managementservices to be outsourced, the Group’s

propertymanagementteamstillrendersitsclosesupervision.

TheGrouphasstrengtheneditssupervisionandmanagementoveritsmainlandprojectsin the midst of the market downturn. Toimproveitscompetitiveness,theGrouphasbeen streamlining its manpower structureandslashingsuperfluousspendingtocontrolcosts while also standardizing buildingdesigntoshortendevelopmenttime.

The Group’s leasing team in mainlandChinahasbecomeexperiencedatsolicitingandinteractingwithtenants.Severalglobalbrands were successfully encouraged tobecome core tenants and are expected toemerge as the Group’s strategic partnersin future.With the new leasing team onboard, themainlandshoppingarcadesarenowunderinnovativetransformation,withemphasis on positioning, environmentalintelligence, technologicalquality,aswellas meticulous management and attentiveservices.

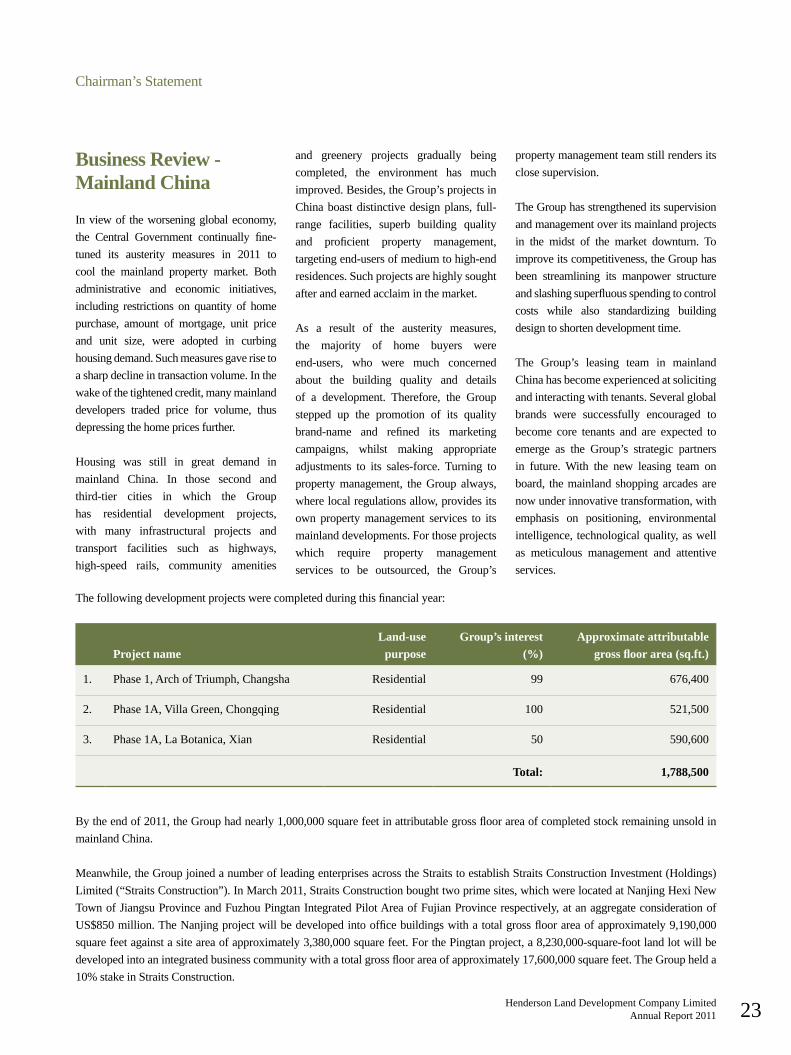

Thefollowingdevelopmentprojectswerecompletedduringthisfinancialyear:

Project nameLand-use

purposeGroup’s interest

(%)Approximate attributable

gross floor area (sq.ft.)

1. Phase1,ArchofTriumph,Changsha Residential 99 676,400

2. Phase1A,VillaGreen,Chongqing Residential 100 521,500

3. Phase1A,LaBotanica,Xian Residential 50 590,600

Total: 1,788,500

Bytheendof2011,theGrouphadnearly1,000,000squarefeetinattributablegrossfloorareaofcompletedstockremainingunsoldinmainlandChina.

Meanwhile,theGroupjoinedanumberofleadingenterprisesacrosstheStraitstoestablishStraitsConstructionInvestment(Holdings)Limited(“StraitsConstruction”).InMarch2011,StraitsConstructionboughttwoprimesites,whichwerelocatedatNanjingHexiNewTownofJiangsuProvinceandFuzhouPingtanIntegratedPilotAreaofFujianProvincerespectively,atanaggregateconsiderationofUS$850million.TheNanjingprojectwillbedevelopedintoofficebuildingswithatotalgrossfloorareaofapproximately9,190,000squarefeetagainstasiteareaofapproximately3,380,000squarefeet.ForthePingtanproject,a8,230,000-square-footlandlotwillbedevelopedintoanintegratedbusinesscommunitywithatotalgrossfloorareaofapproximately17,600,000squarefeet.TheGrouphelda10%stakeinStraitsConstruction.

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport201124

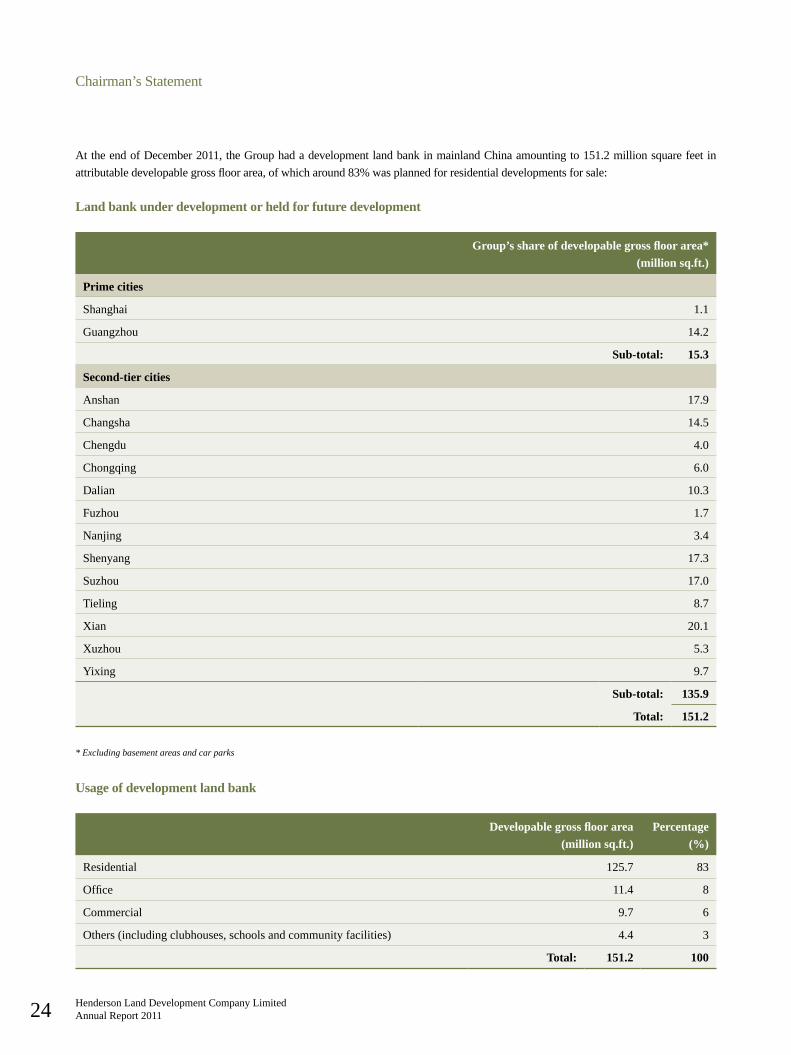

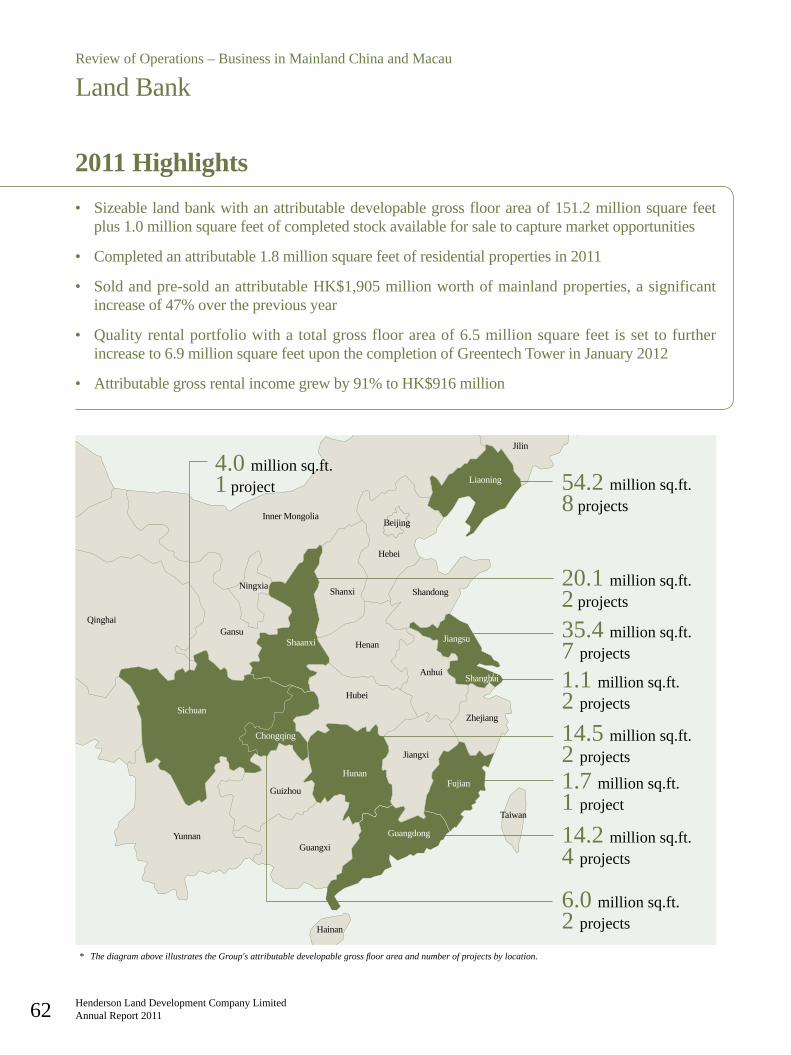

AttheendofDecember2011,theGrouphadadevelopmentlandbankinmainlandChinaamountingto151.2millionsquarefeetinattributabledevelopablegrossfloorarea,ofwhicharound83%wasplannedforresidentialdevelopmentsforsale:

Land bank under development or held for future development

Group’s share of developable gross floor area*(million sq.ft.)

Prime cities

Shanghai 1.1

Guangzhou 14.2

Sub-total: 15.3

Second-tier cities

Anshan 17.9

Changsha 14.5

Chengdu 4.0

Chongqing 6.0

Dalian 10.3

Fuzhou 1.7

Nanjing 3.4

Shenyang 17.3

Suzhou 17.0

Tieling 8.7

Xian 20.1

Xuzhou 5.3

Yixing 9.7

Sub-total: 135.9

Total: 151.2

* Excluding basement areas and car parks

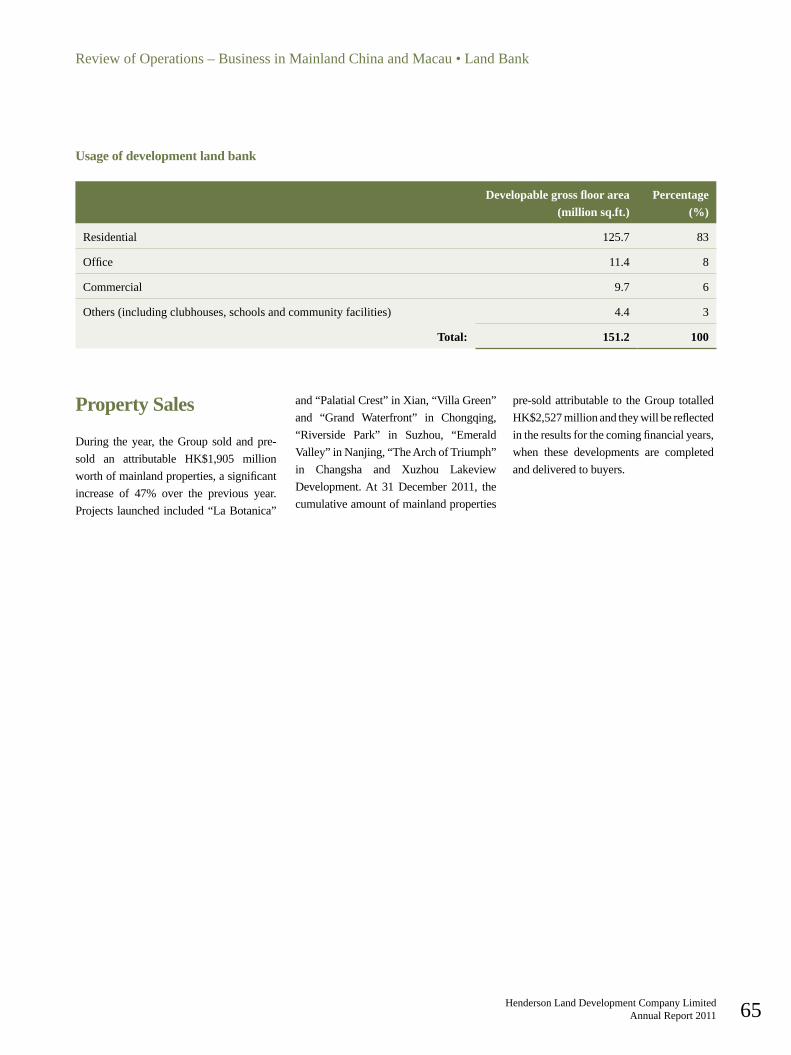

Usage of development land bank

Developable gross floor area (million sq.ft.)

Percentage(%)

Residential 125.7 83

Office 11.4 8

Commercial 9.7 6

Others(includingclubhouses,schoolsandcommunityfacilities) 4.4 3

Total: 151.2 100

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport2011 25

Property SalesDuring the year, theGroup sold andpre-sold an attributable HK$1,905 millionworthofmainlandproperties,asignificantincrease of 47% over the previous year.Projects launchedincluded“LaBotanica”and“PalatialCrest”inXian,“VillaGreen”and “Grand Waterfront” in Chongqing,“Riverside Park” in Suzhou, “EmeraldValley”inNanjing,“TheArchofTriumph”in Changsha and Xuzhou LakeviewDevelopment.At 31December 2011, thecumulativeamountofmainlandpropertiespre-soldattributable to theGroup totalledHK$2,527millionandtheywillbereflectedintheresultsforthecomingfinancialyears,when these developments are completedanddeliveredtobuyers.

Investment PropertiesAs at the year end date, the Group had6.5 million square feet of completedinvestment properties inmainlandChina:mainly offices and shoppingmalls in theprime locations in Beijing, Shanghai andGuangzhou.Duringtheyearunderreview,the Group’s attributable gross rentalincomeandnetrentalincomeincreasedby91% toHK$916millionandby149% toHK$584million,respectively.

In Beijing, World Financial Centrerecordeda170%growthinrentalincometo HK$330 million with a leasing rateexceeding90%at31December2011.Beingtheonlypropertyinthiscapitalcitytohaveachieved the highest possible “Platinum”rating fromboth theUnitedStatesGreenBuildingCouncil’sLEEDandHK-BEAM,many famous financial institutions andmultinational corporations were attractedas its new office tenants. They includedRabobank, CITIC Prudential InsuranceCompany, British Petroleum and ShellChina, whilstMichelin-starred Cantoneserestaurant “Cuisine Cuisine” from HongKong has also established a presence onthe commercial podium. Meanwhile, for

the shoppingmall atBeijingHendersonCentre,leasingperformancewasequallyencouraging after the opening of a large-scale gourmet hall and an upscalesupermarketinitsbasementfloors.

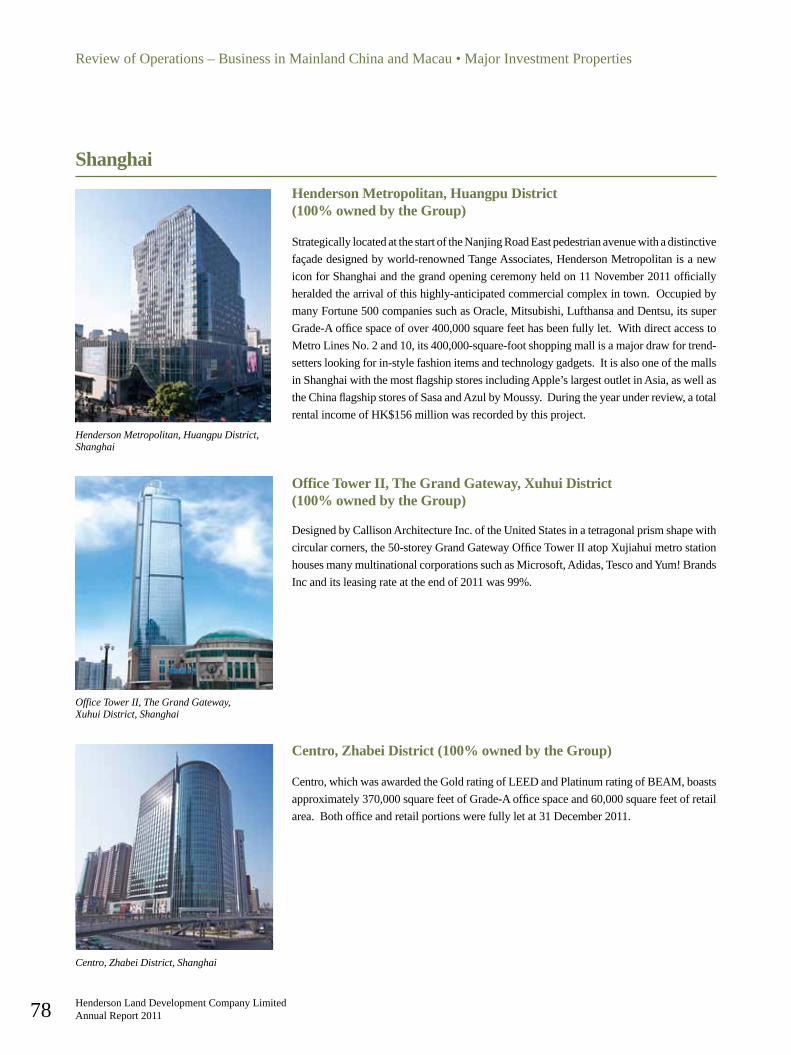

In Shanghai, the grand opening ofHendersonMetropolitanon11November2011 underscored this city’s growingimportance to the Group. Occupiedby many Fortune 500 companies suchas Oracle, Mitsubishi, Lufthansa andDentsu,itssuperGrade-Aofficespaceofover 400,000 square feet has been fullylet,whilstits400,000squarefeetofretailspace was also highly sought-after bymanybrandedretailersasitisconvenientlylocated at the start of theNanjingRoadEastpedestrianavenuewithdirectaccessto subway station from the buildingbasement. The most prominent storesincluded Apple’s largest flagship outletinAsia,aswellasChinaflagshipstoresofSasaandAzulbyMoussy.Duringtheyear under review, a total rental incomeofHK$156millionwasrecordedbythis

project.Meanwhile,GrandGatewayOfficeTowerIIatopXujiahuisubwaystationalsohouses many multinational corporationssuch as Microsoft, Adidas, Tesco andYum!BrandsIncanditsleasingrateattheendof2011was99%.Centro,whichwasawardedaGoldLEEDratingandPlatinumBEAMrating,wasfullyletat31December2011,whilstthepre-leasingresponseforitsneighbouring Greentech Tower was alsoenthusiastic, with many world-renownedcompanies looking to lease sizeable areain this environmentally friendly andtechnologically advanced development.Greentech Tower was completed on 13January 2012, expanding the Group’smainland rental portfolio to 6.9 millionsquare feet. In their vicinity, Skycity inthesameZhabeiDistrictalsoachievedfulloccupancyfor its4-levelshoppingarcadeat31December2011.

InGuangzhou,HengBao Plaza recordeda23%growth inrental incomewithover95%leasingratebytheendof2011.

Grand Opening of Henderson Metropolitan, Shanghai

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport201126

wrotetotheAuthoritiesrequestingfortheconfirmation, the JointVenture Companyhas been chasing after the relevantgovernmentofficialsonseveraloccasions,but no reply had been received from theAuthoritiesforoversixmonths.TheJointVenture Company therefore decided totake one further step and on 9 February2012filedwithLegislativeAffairsOffice,the People’s Government of ZhejiangProvinceanadministrativereconsiderationapplication. The application was to seekanordertoobligetheAuthoritiestocarryout their statutory duties to officiallyconfirmthatthetollfeecollectionrightoftheQianjiangThirdBridge should be foraperiodof30years.WhilstHILwasstillwaiting for the result of the application,the JointVentureCompany on 20March2012 received a letter dated 18 March2012 from 杭州市城巿“四自”工程道路綜合收費管理處 (Hangzhou City“Sizi” Engineering & Highway GeneralToll Fee Administration Office) (the“Hangzhou Toll Office”), which is therelevantgovernmentbodyinHangzhoutorecord the trafficflowandmakepaymentof toll fee of theQianjiangThird Bridgepursuant to the terms of an agreementdated 5 February 2004 (the “CollectionAgreement”) entered into between theJointVentureCompanyandtheHangzhouToll Office. In the letter, the HangzhouTollOfficestatedthat,becausetheGeneralOffice of the People’s Government ofZhejiang Province in 2003 provisionallyfixedtheperiodofentitlementtotollfeeinrespectofQianjiangThirdBridgetoendon19March2012,theywould,commencingfrom 20 March 2012, provisionallysuspend payment of toll fee to the JointVentureCompanyinrespectofQianjiangThird Bridge. The Hangzhou Toll Officealsostatedintheletterthattheywould,inaccordancewiththetermsoftheCollectionAgreement, continue to record the trafficflowofQianjiangThirdBridgeandworkwiththeJointVentureCompany.TheJoint

Joint-Venture Development in MacauInApril 2005, theGroup entered into anagreementtojointlydevelopalarge-scalewaterfront development with a site areaofapproximately1.45millionsquare feetinTaipa,Macau.Theproject issubject toapplication for land-use conversion withthetotalgrossfloorareatobefinalized.

Henderson Investment Limited (“HIL”)For the year ended 31 December 2011,HIL’s turnover amounted to HK$299million,representingadecreaseofHK$18million, or 6%, compared to HK$317million for the previous year ended 31December2010.Suchdecreaseinturnoveris mainly attributable to the period-on-period decrease of approximately 25% intheaveragemonthlytrafficvolumeofthetollbridgeinHangzhou,whichwasHIL’score asset, during the period from1 July2011to31December2011.Thiswasdueto(i)accidentaldamagetooneofthelinkbridgesofthetollbridgeon15July2011which resulted in the four lane two-waytraffic being temporarily reduced to twolanes of two-way traffic in the affectedareaofthetollbridgeuntilthetollbridgewasfullyopento traffic,effectivefrom1October2011;and(ii)theimplementationby Hangzhou Municipal Government ofcertain new policies which control thetrafficflowofvehiclesduringcertainpeakhours each day, effective from8October2011.

Profit attributable to equity shareholdersfor the year ended 31 December 2011amountedtoHK$108million,representingadecreaseofHK$55millionor34%fromHK$163 million for the year ended 31December2010.Thedecreaseinprofitwasattributabletothefactthatinthepreviousyear, a totalprofitofHK$39millionwasreceivedfromcertainone-offitemswhichincludedanetgainofHK$26millionfrom

thedisposalofatollhighwayinMaanshan,AnhuiProvince. HIL has a 60% interest in HangzhouHenderson Qianjiang Third BridgeCompany Limited (“the Joint VentureCompany”) which has been granted theoperating right of the above-mentionedQianjiangThirdBridgeforaperiodof30yearsfrom20March1997(commencementdateofbridgeoperation).ThisprojectwasapprovedbyHangzhouForeignEconomicRelationsandTradeCommission(杭州市對外經濟貿易委員會) in 1997 and wasfurtherapprovedbyNationalDevelopmentand Reform Commission (formerlyknownasStateDevelopment&PlanningCommittee)(發展和改革委員會(前稱為國家發展計劃委員會)) in 1999. TheGeneralOfficeofthePeople’sGovernmentof Zhejiang Province notified ZhejiangProvinceDepartment ofCommunicationsandother relevantgovernmentauthoritiesin2003toprovisionallyfixtheperiodforentitlementtotollfeeinrespectof39tollroads and highways in the province. InthecaseofQianjiangThirdBridge,whichwas also included in the list, the periodwasprovisionallyfixedat15years (from20March 1997 to 19March 2012). TheJointVentureCompany immediately tookaction for clarification and had obtainedfrom the Hangzhou Municipal Bureauof Communications awritten pledge thatthe operation period for 30 years wouldremain unchanged and theywere also ofthe view that the operating right and thetoll fee collection right should be for asameperiod.Forthesakeofreassurance,the Joint Venture Company wrote to thePeople’sGovernmentofZhejiangProvinceand Zhejiang Province Departmentof Communications (collectively the“Authorities”)inJune2011requestingfortheir confirmation that both the operatingright and the toll fee collection right lastforasameperiodof30years.SinceJune2011 when the Joint Venture Company

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport2011 27

VentureCompany has been instructed byHILtowritetotheHangzhouTollOfficetostatethattheactiontakenbytheHangzhouToll Office has no legal or contractualbasis and is unacceptable and to ask theHangzhouTollOffice to clarify the basisoftheiractionandtocontinuetoperformtheir obligations under the CollectionAgreement,failingwhichtheJointVentureCompanywouldhavenoalternativebuttotakelegalactionstoprotectitsinterest.

HIL has obtained legal opinion from anindependentPRClawfirmandhasreceivedfirmadvicethatthetollfeecollectionrightenjoyed by the Joint Venture Companyshouldbeforthesameperiodof30yearsas the operating right enjoyed by the Joint Venture Company. Based on suchadvice, amortization and calculation ofthe recoverable amount of the intangibleoperating right in the preparation of the consolidatedaccountsofHILfortheyearended31December2011areonthebasisthat both the operating right and the tollfeecollectionrightoftheBridgelastforaperiod of 30 years expiring on 19March2027. There is, however, uncertainty asto the response of the Authorities and whether they would ultimately confirmthat the toll fee collection right of theQianjiang Third Bridge should be for aperiod of 30 years. HIL will continue tonegotiatewiththeAuthoritiesandtakeallnecessary actions to protect its interest.If theAuthoritiesconfirmthat the toll feecollection right of the Qianjiang ThirdBridge should last for a period differentfrom the period of the operating rightand/or the Authorities negotiate otherarrangementswithHIL(suchasbuyingoutHIL’s interest in Qianjiang Third Bridgeor paying compensation to HIL), all ofwhicharestilluncertain,HILwouldhavetoreconsidertheremainingusefullifeand/ortherecoverableamountoftheintangibleoperatingright.

Currently, the operating assets of HILcompriseitsinterestintheQianjiangThirdBridge.IfHILceasestohaveaneconomicinterest in the Qianjiang Third Bridge,thedirectorsofHILwould, ifappropriateopportunity arises, identify suitableinvestments forHIL. In theevent thatnosuitable investments are identified andacquiredbyHIL, its assetswould consistsubstantially of cash. As a result, TheStock Exchange of Hong Kong Limitedmay consider that HIL does not have asufficient level of operations or sufficientassets to warrant the continued listing ofHIL’ssharesandmaysuspenddealingsinorcancelthelistingoftheshares.

Associated Companies

The Hong Kong and China Gas Company Limited (“Hong Kong and China Gas”) Profit after taxation attributable toshareholders of this group for the yearamounted to HK$6,149.6 million, anincreaseofHK$564.8millioncomparedto2010mainly due to growth in profit ofmainlandbusinesses.Duringtheyearunderreview, this group invested HK$4,725.1million in production facilities, pipelines,plantsandotherfixedandintangibleassets.

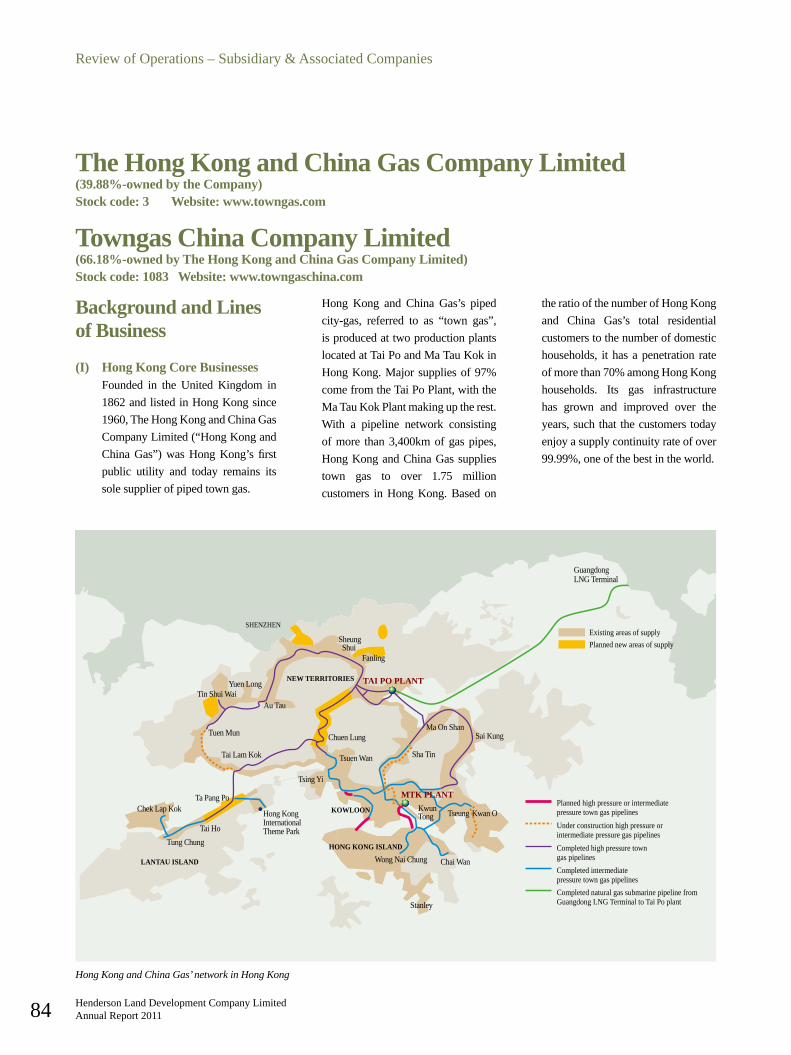

Gas business in Hong KongThe total volume of gas sales in HongKong for the year 2011 rose by 2.1%,whilst appliance sales also increased byabout 8% compared to 2010. As at theendof2011,thenumberofcustomerswas1,750,553,anincreaseof26,237comparedto2010.Layingofa15kmpipelinetobringnatural gas from Tai Po toMa Tau Kokgas production plant, to partially replacenaphtha as feedstock for the production of town gas, is expected to be substantiallycompletedwithin2012.Constructionofa9kmpipelineinthewesternNewTerritories

to strengthen supply reliability is also inprogress.Intandemwiththegovernment’sdevelopmentofWestKowloon,SouthEastKowloon and a cruise terminal, networkplanning,designandconstructionintheselocationsareunderway.ConstructionofanewsubmarinepipelinefromMaTauKokto North Point will commence in 2012.Meanwhile,newgasmainshavebeenlaidtoLeiYueMun.

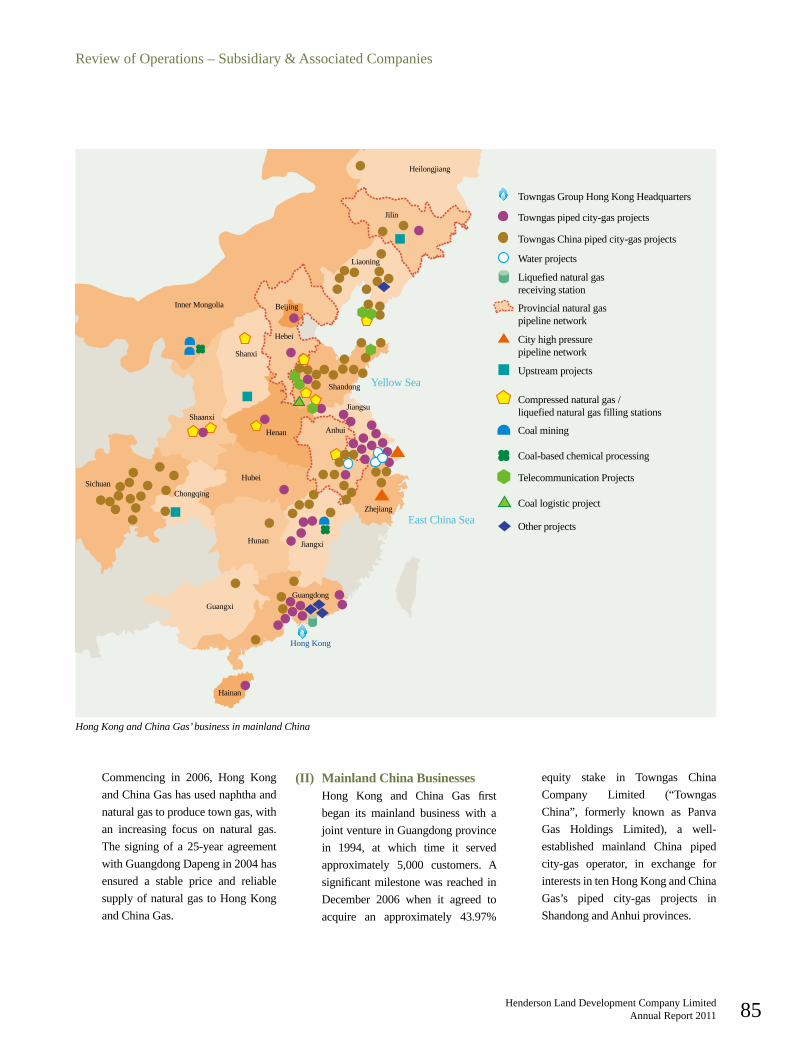

Utility businesses in Mainland ChinaAt theendofDecember2011, thisgrouphad an approximately 66.18% interestin Towngas China Company Limited(“Towngas China”; stock code: 1083),whoseprofitaftertaxationattributabletoitsshareholdersamountedtoHK$709millionin 2011, an increase of approximately62.6% over 2010. In 2011, TowngasChina acquired five new projects locatedinXiushui county andWuning IndustrialPark,bothinJiujiang,Jiangxiprovince;inMiluo,thisgroup’sfirstinHunanprovince;in Bowang New District, Maanshan,Anhuiprovince;andinBeipiao,Liaoningprovince.

Thisgroup’scity-gasbusinessesprogressedwell in 2011, with two new projectssuccessfully established in Chaozhou,GuangdongprovinceandJingxiancounty,Hengshui, Hebei province. Inclusive offivenewprojectsestablishedbyTowngasChinain2011,thisgrouphad100city-gasprojects in mainland cities spread across19 provinces/municipalities/autonomousregionsasattheendof2011.Duringtheyearunderreview,thenumberofgascustomerson the mainland reached approximately13.2millionandtotalvolumeofgassalesalsoexceededtenbillionforthefirsttime,attaining10,300millioncubicmetres.Thisgroupisnowthelargestcity-gasenterpriseonthemainland.

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport201128

Thisgroup’smidstreamnaturalgasprojectsincludehigh-pressurenaturalgaspipelinejoint ventures in Anhui province, Hebeiprovince, Hangzhou, Zhejiang provinceand Jilin province; the GuangdongLiquefiedNaturalGasReceivingTerminalproject; and a natural gas valve stationprojectinSuzhouIndustrialPark,Suzhou,Jiangsuprovince.

Duringthethirdquarterof2011,thisgroupadded a second integrated wastewater treatment project, for a special industry,to its existing integrated water supplyand wastewater joint venture in SuzhouIndustrialPark,Suzhou,Jiangsuprovince.Together with water supply projects inWujiang, Jiangsu province and inWuhu,Anhui province, this group has so farinvestedinandoperatesfourwaterprojects.

Emerging environmentally-friendly energy businessesThis group’s development of emergingenvironmentally-friendly energy projects,throughitswholly-ownedsubsidiaryECOEnvironmental Investments Limited andthelatter’ssubsidiaries(togetherknownas“ECO”),isprogressingwell.

ECO’s coalbed methane and non-conventional methane utilisationbusinesseshavebeendevelopedbasedonthetechnologyandoperationalexperiencegained from its landfill gas utilisationproject which has been successfullyoperatinginHongKongforseveralyears.Since 2008, ECO has been developingsimilarcleanandenvironmentally-friendlyenergyprojectsonthemainland.Acoalbedmethane liquefaction facility locatedin Jincheng, Shanxi province was fullycommissioned during the first quarter of2011. The annual production capacity ofthewhole facility is250million standardcubicmetresofliquefiedcoalbedmethane.The facility has now become the largestliquefaction and utilisation project of itskindonthemainland.

ECO’s coal-mine methane liquefactionprojectinYangquanminingdistrict,Shanxiprovince, is progressing as scheduled;construction is expected to commencein 2012 for commissioning in the firstquarter of 2014. Coal-mine gas, whichtypicallycontainsabout40%methane,willbe used to produce liquefiedmethane bydeployingcoal-minegasdeoxidisationand

coalbed methane cryogenic liquefactiontechnologies.Thisprojecthasanestimatedannual production capacity of about 80millionstandardcubicmetres.

ECO started to develop coal resourcesand coal chemical processing businessesin2009.ECOhasconstructedamethanolproductionplant,with an annual capacityof200,000tonnes,inJunger,Erdos,InnerMongolia. The plant is now at the pilotproductionstageandisexpectedtobefullycommissioned in mid-2012. ConstructionofECO’sXiaoyugoucoalmine,which isassociated with the methanol productionplant,isalsocompleteandpilotproductionstarted in early 2012. ECO acquired anoperative open-pit coal mine in InnerMongolia in September 2011 and this isnowstartingtocontributeadditionalprofits.ECO’scokingcoalmineandcokingplantproject in Fengcheng, Jiangxi province,is also on schedule; commissioning isexpectedin2012.Themainproduct,coke,willbeusedforrefiningsteel,anditsby-product, coke oven gas, will provide anadditional gas source for this group’sFengchengcity-gasproject.

ECO’s energy-related logistics andfacilities businesses originated from itsfive dedicated liquefied petroleum gasvehicular filling stations in Hong Kong.ECOstarteditsgasfillingstationbusinessonthemainlandin2008.Sincethen,ECOhas gradually established a network ofcompressedandliquefiednaturalgasfillingstations servicing heavy-duty trucks inShaanxi,Shandong,Liaoning,Henan andAnhuiprovinces.

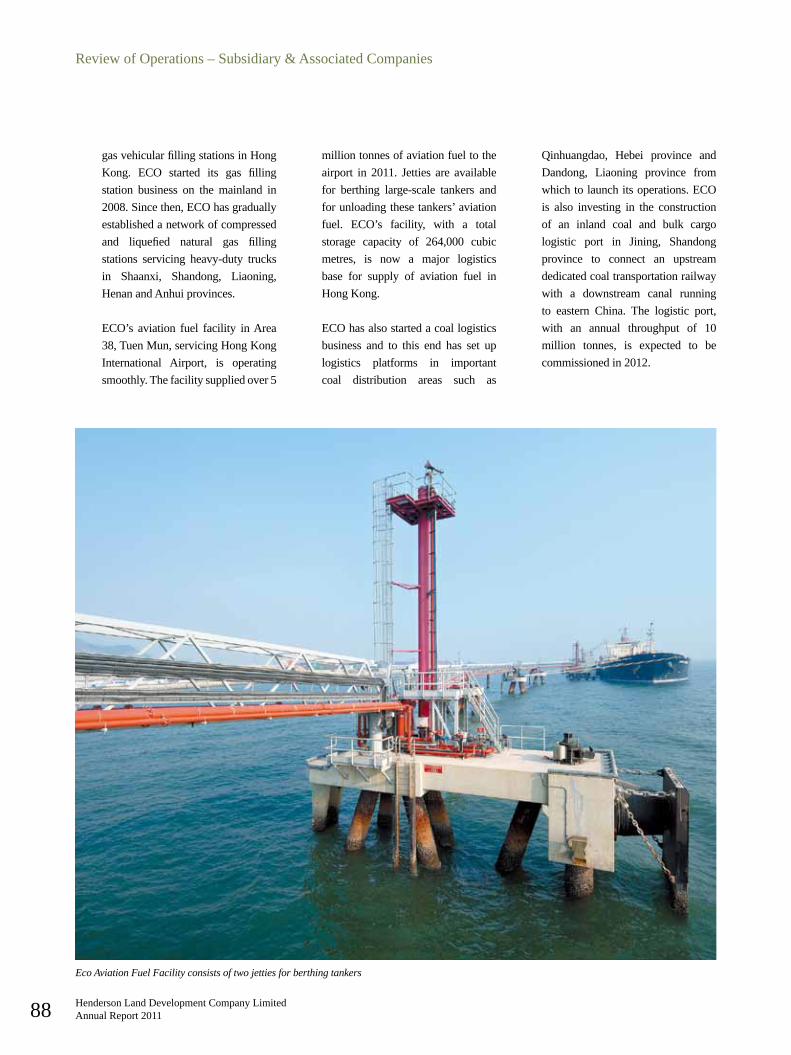

ECO’saviationfuelfacilityinArea38,TuenMun, servicing Hong Kong InternationalAirport,isoperatingsmoothly.Thefacilitysuppliedover5milliontonnesofaviationfuel to the airport in 2011. Jetties areavailable for berthing large-scale tankersand for unloading these tankers’ aviation

ECO Environmental Investments Limited (ECO)’s Aviation Fuel Facility in Tuen Mun

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport2011 29

fuel. ECO’s facility, with a total storagecapacityof264,000cubicmetres,isnowamajorlogisticsbaseforsupplyofaviationfuelinHongKong.

ECO has also started a coal logisticsbusinessandtothisendhassetuplogisticsplatforms in important coal distributionareas such as Qinhuangdao, HebeiprovinceandDandong,Liaoningprovincefromwhichtolaunchitsoperations.ECOisalso investing in theconstructionofaninland coal and bulk cargo logistic portin Jining, Shandong province to connectanupstreamdedicated coal transportationrailwaywithadownstreamcanal runningtoeasternChina.Thelogisticport,withanannualthroughputof10milliontonnes,isexpectedtobecommissionedin2012.

ECO set up a new-energy research anddevelopment centre in 2010 focusingon related application technologies. Thecentre has achieved good progress indeveloping innovative technologies forconvertingmaterialsoflowvalue,suchasnon-edible oil and coal tar oil, into cleanfuelandsubstancesofhighvalue.

Overall,asattheendof2011,inclusiveof the projects of Towngas China, thisgroup had 138 projects on themainland,18more than that in 2010, spread across21 provinces/municipalities/autonomousregions and encompassing upstream,midstream and downstream natural gassectors, water supply and wastewatertreatment sectors, natural gas vehicularfilling stations, environmentally-friendly energy applications, energyresources, logistics businesses andtelecommunications.

Property developmentsAllresidentialunitsoftheGrandWaterfrontpropertydevelopmentprojectlocatedatMaTauKoksouthplantsitehadbeensoldbytheendofDecember2010,whereasthose

ofGrandPromenadehadalsobeensoldbytheendofthefirstquarterof2011.Leasingof the commercial area of the GrandWaterfront property development projectis good.Rental demand for the shoppingmallandofficetowersofIFCcomplex,inwhichanapproximately15.8%interest isheldbythisgroup,continuestoberobust.The occupancy rate of the project’s hotelcomplex, comprising the Four SeasonsHotel and rental serviced apartments,remainshigh.

Financing programmesIn February 2011, this group concludeda HK$3,800 million 5-year syndicatedterm loan and revolving credit facility,mainlyforrefinancingaHK$3,000millioninaugural syndicated facility, taken up in2006, and for its business development.The facility carries an interest margin of0.49%perannumoverHIBOR.

This group issued its first renminbi-denominated notes in Hong Kong inlate March 2011 with a total amount ofRMB1,000 million for a term of fiveyears at a coupon interest rate of 1.4%(the “RMB Notes”). This group is thefirst company among Hang Seng IndexConstituent Stocks in Hong Kong to raise funds through the offshore renminbi debtcapital market. Inclusive of the RMBNotes,thisgrouphasissuedmediumtermnoteswith,uptonow,anaggregateamountequivalent toHK$6,070millionunder itsmediumtermnoteprogramme.

InApril2011,Moody’s InvestorsServiceupgradedbothTowngasChina’sissuerandseniorunsecuredbondratingsfromBaa3toBaa2withastableoutlook.

In 2011, Standard & Poor’s RatingsServices launched the first credit ratingbenchmark developed especially for theregion to assign credit ratings to borrowers active in mainland China, Hong Kong,

and Taiwan (including the fast-growingoffshore renminbi debt market). HongKong and China Gas was assigned the highestratingofcnAAA,whilstTowngasChina was assigned cnA under this Greater Chinalong-termcreditratingscale.

This group predicts an increase of about 25,000 new customers in Hong Kongduring2012andthecombinedresultsofitsemergingenvironmentally-friendlyenergybusinessesandmainlandutilitybusinesseswillovertaketheresultsofitsHongKonggasbusinessin2012,andwillhavefastergrowthmomentumthanitsHongKonggasbusinessthereafter.

Hong Kong Ferry (Holdings) Company Limited (“Hong Kong Ferry”) Thisgroup’sturnoverfortheyearended31December2011amountedtoapproximatelyHK$635 million, representing a decreaseof 30% when compared to the previousyear. This was mainly attributed to thedecreaseinthesalesoftheShiningHeightsandTheSpectacle. Its consolidatedprofitafter taxation amounted to approximatelyHK$565 million, an increase of 17% ascomparedwith theprofitafter taxationofHK$483millionin2010.

This group sold 30 units in TheSpectacle and 7 units in ShiningHeightswhich accounted for a total profit ofapproximately HK$156 million for theyear under review. A profit of HK$37millionwas derived from the disposal ofcertain units of the commercial arcadeofMetroRegalia. Rental and other incomefrom its commercial arcade amountedto approximately HK$50 million. TheoccupancyrateofthecommercialarcadeatShiningHeightswas93%.Thecommercialarcade ofMetroHarbourViewwas fullylet.

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport201130

ThefoundationworksofthedevelopmentprojectatFanlingSheungShuiTownLotNo. 177 (“Fanling project”) have beencompleted. Superstructure works are inprogress.The propertywill be developedintothreeresidentialtowersbuiltonatwo-storey shoppingpodiummallwitha totalgrossfloorareaofapproximately540,000squarefeet.

As regards the project at 204-214 TungChau Street, demolition works havebeen done and superstructure works will commence at the end of the year.The project will be redeveloped into acommercial-cum-residential buildingwitha total gross floor area of approximately54,000squarefeet.

Thisgroupacquiredthesiteatthejunctionof Gillies Avenue South and BulkeleyStreet HungHom Inland LotNo. 555 in2011. Foundation works will commenceuponthecompletionofdemolitionworks.The project will be developed into acommercial-cum-residential buildingwitha total gross floor area of approximately56,000squarefeet.

During the year, the Harbour CruiseOperations achieved a profit of HK$4.7million, representinga15%increaseoverthatoflastyear.FerryOperationsrecordeda profit ofHK$4.7million, a decreaseof36% as comparedwith the profit for lastyear. Due to the provision for bad debtsand the increased operating costs incurred onannualdrydockoftheferries,theFerry,ShipyardandRelatedOperationsrecordedaprofitofonlyHK$5.5million,adecreaseof44%ascomparedwiththesameperiodoflastyear.

During the year under review, this groupachievedaprofitofHK$245millionuponthe disposal of Silvermine Beach Hotel.TheTravelOperationsDivisionregisteredan increaseof29% in itsoperatingprofit

as compared with that for last year.Meanwhile,animpairmentlossofHK$45million was recorded in its available-for-salesecuritiesinvestmentduringtheyear.

ThisgroupexpectstheresidentialunitsoftheFanlingprojecttobesoldinthesecondhalfof thisyear.Thesalesproceedsfromthis project and the remaining units ofShining Heights and The Spectacle areexpectedtobeitsmainsourcesofrevenue.

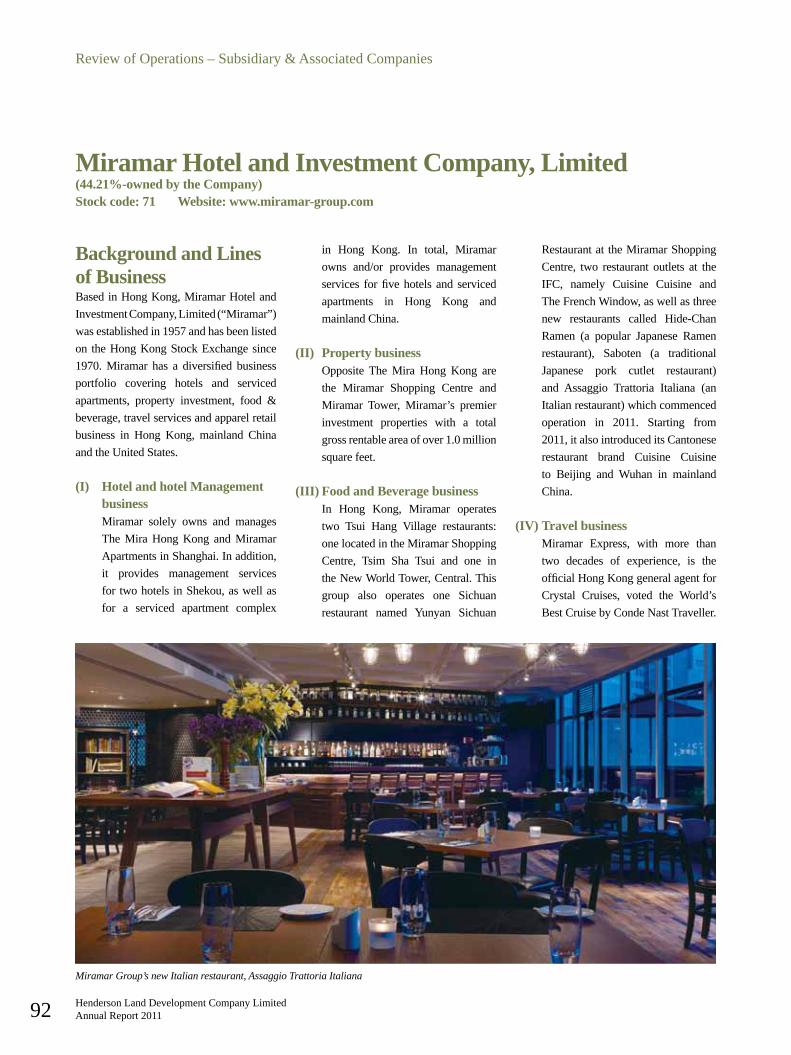

Miramar Hotel and Investment Company, Limited (“Miramar”) Forthefinancialyearended31December2011, Miramar’s turnover amountedto approximately HK$2,496 million,representing an increase of 18% ascomparedwith2010.Profitattributabletoshareholders posted a growth of 69% toapproximately HK$1,325 million (2010:HK$784 million). Excluding the netincreaseinthefairvalueofitsinvestmentproperties,underlyingprofitattributabletoshareholders for 2011was approximatelyHK$411million(2010:HK$378million),representingayear-on-yearincreaseof9%.

Miramar operates five core businesses,namely Hotel and Hotel Managementbusiness, Property Rental business, Foodand Beverage business, Travel businessand the newly-developed Apparel Retailbusiness.

OccupancyrateforTheMiraHongKong(The “Mira”), its flagship hotel, rosefrom 80% in 2010 to 83% in the yearand average room rate posted a growthof 19% from HK$1,470 to HK$1,760.EBITDA (earnings before interest, taxes,depreciation and amortization) of TheMira grew 52% to reach approximatelyHK$206.5million.In2011,itobtainedthehotel management project for a boutiquehotel in Wan Chai. The boutique hotel,which is currently under construction,willbeoperatedunder thebrandnameof

“TheMira”andisexpectedtocommenceoperation in 2013. The boutique hoteloffers a total of approximately 100 guestrooms.

For this year, overall income of PropertyRental Business recorded a growth of15%overthatof2010.Attheendof2011,occupancy rate of Miramar ShoppingCentre was approximately 100% andaverage unit rate also recorded a mildincrease. With the completion of workin the first half of 2011, GradeA officebuildingofMiramarToweralsoachievedapproximately100%occupancyrateattheendof2011withaverageunitrateslightlyincreased as compared to 2010. TherefurbishmentworkintheshoppingcentreatTheMirawas completed in the fourthquarterof2011.

Miramar operates Tsui Hang Villagerestaurants, Sichuan restaurant namedYunyan Sichuan Restaurant, CuisineCuisine and The French Window thatare located at IFC, as well as three newrestaurants, namely Hide-Chan Ramen(a popular Japanese Ramen restaurant),Saboten(atraditionalJapaneseporkcutletrestaurant)andAssaggioTrattoriaItaliana(an Italian restaurant) which commencedoperationduringtheyear.

Miramar introduced its successful brand“Cuisine Cuisine” to themainlandChinamarket. The first Cuisine Cuisine islocated in the Central Business Districtof Chaoyang district, Beijing and wasopenedinSeptember2011.Varnishinganddecoration of the other Cuisine Cuisine in Wuhanwascompletedand isexpected tocommenceoperationinApril2012.Duringtheyear,twoTsuiHangVillagerestaurantswere temporarily closed for renovation.This, together with the write-off of pre-opening expenses of new restaurants,resultedinalossfortheoverallFoodandBeveragebusiness.

Chairman’sStatement

HendersonLandDevelopmentCompanyLimitedAnnualReport2011 31

Turnoverof itsTravelBusiness increased7% to reach HK$1,055 million whilstEBITDAslightlydroppedtoapproximatelyHK$25millionin2011.

Miramar extended its reach to ApparelRetail Business in 2011 and became thedistributor of DKNY Jeans in mainlandChina.Atpresent,itownsandoperatesfiveDKNY Jeans stores in each of Shanghaiand Beijing. In addition, it secured andengaged over 20 franchisees to operateDKNYJeansfranchisedstores.Attheendof2011,therewereover40storesoperatedby Miramar and franchisees. A negativeEBITDAof approximatelyHK$4millionwassustainedduringtheyear.

Corporate Finance

Duringtheyear,theholdingcompanyoftheGroup, namely, Henderson DevelopmentLimitedwhichiscontrolledbytheprivatefamily trustofDrLeeShauKee,madea

capital investment of HK$10,000millioninexercising172,414,000warrantsforthesubscription of 172,414,000 shares in theCompany at a price ofHK$58per share.This has significantly strengthened thecapitalbaseoftheCompany.

Asattheyearenddate,theGroup’sgearingratiowas 19.9%, a significant dropwhencompared with 28.2% for the previousyear. In order to provide additionalfunding resources to the Group to cater foritsgeneralfundingandworkingcapitalrequirements, the Group concluded aHK$10,000million three-year syndicatedterm loan / revolving credit facility on10 January 2011 with a consortium of13 leading international banks and localfinancial institutions. The Group alsosigned up aHK$10,000millionfive-yearsyndicated term loan / revolving creditfacilityon22June2011withaconsortiumof 17 leading international banks andlocalfinancial institutions.Overwhelmingresponses from the banking community

and consecutive successful conclusionsof these two large size syndicated creditfacilities fully demonstrated the strongconfidence and continuing support ofinternationalaswellaslocalbanksfortheGroup.