Embed Size (px)

Citation preview

Vanguard research March 2010

Deficits, the Fed, and rising interest rates: Implications and considerations for bond investors

AuthorsJoseph H. Davis, Ph.D.Roger Aliaga-Díaz, Ph.D.Donald G. Bennyhoff, CFAAndrew J. PattersonYan Zilbering

Executive summary. This paper addresses three related questions:

• Whyarelong-termU.S.interestrates,suchasthe10-yearTreasury yield,below4%,giventheexpectedfuturepathofU.S.government debtlevelsandtheFederalReserve’s“exitstrategy”?Morepointedly,don’tlong-termrateshavetorisedramatically?

• Howmightbondfundsperformintheeventthatratesdoriseover thenextseveralyears?

• Isitnotprudenttore-allocateone’sbondportfoliodefensivelyintoshorter-maturityfundsbeforeratesstartrising?

Webeginbydeconstructingtheyieldona10-yearTreasurybondinto itscomponents,includinginflationexpectations,anticipatedFedpolicy, andtheeffectsofchangesinbondsupply(i.e.,deficits)anddemand. Ourdeconstructionrevealsthattheexpectedupwardpressurefrom thefiscaldeficitonlongbondrateshasbeenoffsetsofarbyincreased bonddemandarisingfromahigherdomesticsavingsrate.

Connect with Vanguard > www.vanguard.com > global.vanguard.com(non-U.S.investors)

2

Ourinterest-ratedeconstructionalsoprovidesabasisforassessingthefutureeconomicscenariothatis“pricedinto”today’sbondvaluations(andhenceintotheforwardyieldcurve).Onthebasisofthisanalysis,wediscusswhyexpectationsforfutureinterest-ratemovementsseemgenerallyplausible.

Thatsaid,historysuggeststhatrateswilllikelyevolvequitedifferentlyfromwhatisexpectedtoday,astheforecastingtrackrecordofthefuturesmarketisnotoriouslypoor.Consequently,wecalculateimpliedfuturereturnsforTreasuryandcorporatebondbenchmarksover1-,5-,and10-yearinvestmenthorizonsbasedonalternativebutplausiblemacroeconomic,fiscal,andFedpolicyscenarios.Wefindthat,mostbroadly,thosescenariosthatproducethehighestrelativereturnsintheshortrun(suchasadouble-diprecessionscenario)wouldbeexpectedtoproducethelowestrelativereturnsoverthelongrun.Conversely,scenariosinwhichratesrisemorethaniscurrentlyexpected(suchasfromafiscalcrisisorarun-upininflation)couldactuallyproducethehighestrelativenominalreturnsovera10-yearperiod.

Theresultsofourscenarios,togetherwiththeperformanceofvariousbondsegmentsoverthepastseveralyears,underscorethebenefitsofabroadlydiversifiedfixedincomeportfolioregardlessofthefuturedirectionofinterestrates.Akeylessonoftheglobalfinancialcrisisisthatimplementingatoonarrowor“surgical”bondallocation(suchasbyshorteningdurationorinvestingsolelyinriskierbondinstruments)involvesimportanttrade-offsthatmayexposeinvestorstounintendedyield-curveorcreditrisks,whilepotentiallydeprivingthemofahigherorlessvolatilefutureincomestream.Thehighuncertaintysurroundingthefuturedirectionofeconomicgrowth,thedeficit,inflation,andinterestrateswouldseemtosupportgreaterfixedincomediversification, notless.

Executive Summary continued

Introduction

RecentcashflowsintobondmutualfundsandETFshavebeenverystrong.AccordingtoMorningstar,throughthefirstthreequartersof2009theseflowswerefairlywelldiversifiedacrossshorter-maturityandlonger-maturitybondfundsinboththetaxableandmunicipalcategories(seeFigure 1,onpage4).Morerecently,aslightlyhigherpercentageofbondcashflowshasgonetoshort-termfunds.Thisisfairlyatypicalforanenvironmentofextremelylowshort-termyields.

Oneofthelikelycatalystsforthistrendhasbeenincreaseddemandfrommoneymarketinvestorsinsearchofhigheryields.WiththeFederalReservemaintainingitsfederalfundsratetargetcloseto0%,

monetarypolicymakershavemadeitextremelydifficultformanysaverstogeneratesufficientincomefromtheirmoneymarketaccounts.Inthissense,saversunfortunatelyremainthe“sacrificiallambs”ofU.S.monetarypolicyastheFederalReserve attempts to stimulate other segments oftheeconomy.

Another probable influence is increasing concern among bond investors that mounting government debtlevelswilleventuallydriveuplonger-term U.S.interestrates,whichatpresentarebelowtheirhistoricalaverages(seeFigure 2,onpage4).Inaddition,thefuturesmarketexpectstheFederalReservetobeginraisingshort-termratesbeforetheendof2010astheU.S.recoverystrengthens.

*This is the formula for forward rates employed on the Bloomberg website:

f = [(FV-1) / (d2-d1)] * 360

where:f = forward rate (simple interest, ACT/360)d1 = number of days from the settlement date to the start date of the forward periodd2 = number of days from the settlement date to the end date of the forward periodFV = future value. The formula is: (1 + [(r2*d2)/360]) / (1 + [(r1*d1)/360])

where:r1 = the spot rate for d1 days (simple interest)r2 = the spot rate for d2 days (simple interest)

3

A note on the chartsThechartsinthispaperarebasedonmarketforwardratesgeneratedbyuseofaformulacommonlycitedintextbooksandothersources.*Forwardratesarenotprojections;rather,theyaremathematicallyderivedfromthecurrentmarketvaluationsforbondsofdifferentmaturities.Forwardratesdonotrepresentanyindividual’sororganization’sviewsaboutfutureinterestrates.Instead,theyarenormallyinterpretedasacollectiveexpectationoftheentirebondmarket.(Asthepaperpointsout,thatcollectiveexpectationisfrequentlywrong.)

Important notes about riskAllinvestmentsaresubjecttorisk.Pastperformanceisnoguaranteeoffutureresults.Investmentsinbondsaresubjecttointerestrate,credit,andinflationrisk.WhileU.S.Treasuryorgovernmentagencysecuritiesprovidesubstantialprotectionagainstcreditrisk,theydonotprotectinvestorsagainstpricechangesduetochanginginterestrates.Foreigninvestinginvolvesadditionalrisksincludingcurrencyfluctuationsandpoliticaluncertainty.Diversificationdoesnotensureaprofitorprotectagainstaloss inadecliningmarket.

An investment in a money market fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although a money market fund seeks to preserve the value of your investment at $1 per share, it is possible to lose money by investing in such a fund.

4

Monthly bond fund and ETF cash flows, January 2009–January 2010

Morningstar monthly municipal, government, and investment-grade fund and ETF cash flows

Figure 1.

Note: Short-term funds and ETFs include the following Morningstar categories: Muni Single State Short, Muni National Short, Short Government, and Short-Term Bond. Intermediate- and long-term funds and ETFs include the following Morningstar categories: Muni California Intermediate/Short, Muni Massachusetts, Muni Minnesota, Muni National Intermediate, Muni New Jersey, Muni New York Intermediate/Short, Muni Ohio, Muni Pennsylvania, Muni Single State Intermediate, Muni New York Long, Muni California Long, Muni National Long, Muni Single State Long, Intermediate Government, Long Government, Intermediate-Term Bond, and Long-Term Bond.

Sources: Morningstar and Vanguard.

Intermediate- and long-termShort-term

Cas

h flo

w ($

Bill

ions

)

0

5000

10000

15000

20000

25000

30000

35000

40000

0

$5B

$10B

$15B

$20B

$25B

$30B

$35B

$40B

81%

19%

69%

31%

67%

33%

75%

25%

66%

34%

56%

44%

60%

40%

60%

40%

61%

39%

55%

45%

56%

44%

41%

59%

54%

46%

Jan.2009

Feb.2009

Mar.2009

April2009

May2009

June2009

July2009

Aug.2009

Sept.2009

Oct.2009

Dec.2009

Nov.2009

Jan.2010

A source of consternation

The current, historical average, and implied future yield on the 10-year Treasury bond

Figure 2.

Note: Calculations are based on data available as of March 29, 2010.

Sources: Bloomberg, Federal Reserve, and Global Financial Data.

2

4

6

8

2

4

6

8%

Yiel

d (%

)

4.9%4.7%

7.3%

4.5%

3.9%

4.4%

5.2%5.6%

Historicalaverages

Forward curve:Bond market expectations

Since1800

Since1900

Since1970

Since2000

Current(3/29/10)

1 yearfrom now

3 yearsfrom now

5 yearsfrom now

Viewingtheseconcernstogether,somebondinvestorsmayhopethatthetotalreturnson shorter-durationfundswillberelativelyinsulatedinthe event that bothshortandlongratesrisebythesameamount(thatis,aparallelupwardshift ininterestrates).

In light of these uncertainties, it’s natural for bond investorstowonderwhethertheyshouldactdefensivelybyreshapingtheirfixedincomeallocationwithanarrowor“surgical”focusonmitigatingrisk.Toprovidebetterperspectiveandgroundsfordiscussion,webeginbyexamininghowthemarketexpectsinterestratestomoveandhowvariousgovernmentbondindexesmightperformifthoseexpectationsweremet.

How might interest rates evolve in the years ahead?

Figure 3showsthebondmarket’sexpectationsforfutureinterestratesalongtheentireyieldcurve.Theseimplicitexpectations—oftenreferredtoastheforwardyieldcurveorsimplyforward rates—canbederivedfromcurrentU.S.Treasurybondprices.Inessence,theforwardcurvecanbeconsideredthesetof“break-even”yieldsthatequalizestheratesofreturnfromTreasurybondsacrosstheentirematurityspectrum.Animportant—andoftenmisunderstood—implicationofFigure3isthatiftheyieldchangesoftheforwardcurvearerealized,thenallTreasurybonds—regardless of their maturity—willearnthesameholding-periodreturn.1

1 For a more detailed and technical discussion of forward rates and yield-curve dynamics, see Ilmanen (1996) and Davis and Aliaga-Díaz (2007).

5

The implied evolution of the U.S. Treasury yield curve—a bear flattening

Spot curve as of February 28, 2010, and selected forward curves

Figure 3.

Source: Bloomberg.

2010

The Fed is expected to flatten the yield curve by (A) raising short-term rates and (B) anchoring long-term inflation expectations.

0

1

2

3

4

5

6

0

1.0

2.0

3.0

4.0

5.0

6.0%

Yiel

d (%

)

1week

2 4 5 6 9 2 3 4 5 7 1510 20131

A

B

2011 2012 2013 2014 2015 2020

Months Years

Giventhedramaticsteepnessoftoday’syieldcurve(asmeasuredbythedifferencebetweenthe10-yearTreasuryyieldandtheyieldonthe3-monthT-bill),thebondmarketexpectstheyieldcurvetoflattensignificantlyintheyearsahead.The“bearflattening”scenarioinFigure3showsthatthemajorityoftheinterestrateadjustmentisexpectedtooccurinshortrates,notlongrates.Asanexample,the2-yearTreasuryyieldisexpectedtorisestronglyoverthenextfiveyearsastheFederalReservenormalizesmonetarypolicy,drivingthe2-yearnotefromitsFebruary2010spotyieldof0.81%to5.28%inFebruary2015.Theyieldona20-yearconstant-maturityTreasurybondisexpectedtoriselessdramatically,fromtheFebruary2010spotyieldof4.43%to5.56%inFebruary2015.

Inshort,theTreasurysecuritymarkethasalready“pricedin”aFedtighteningcyclethatflattenstheyieldcurveinsuchamannerthattheexpectedreturnon,say,ashort-termTreasuryportfoliowouldbeapproximatelythesameasforalonger-durationTreasuryportfolio.

As illustrated in Figure 4, this flattening of the yieldcurvewouldbesimilartowhatoccurredfollowingtheendofthelastlow-rateenvironment(2003–2004).Startingin2004,theFederalReserveraisedshort-termratesinstagesfrom1.00%to5.25%,whiletheyieldonthe10-yearTreasuryhardlychanged.TheFedchiefthen,AlanGreenspan,calledthissituationa“conundrum”becauseitdifferedfromotherFedrate-tighteningcycles,suchasthatof1994,whenlonger-termyieldsrosealmostintandemwiththeriseinthefederalfundsrate.However,others have argued that the conundrum episode waspreciselyhowatighteningcycleshouldoperateunderacrediblecentralbankthateffectivelyanchorslong-terminflationexpectations—theprimarydriveroflongbondyields.

Are the market’s current expectations reasonable?

Anaturalquestion,ofcourse,iswhetherthebondmarket’sexpectationsforfuturelongTreasurybondyieldsarereasonable.InlightoftheconcernsoverU.S.fiscaldeficitsandtheFed’sexitstrategy,manyinvestorsmayfinditperplexingthata10-yearTreasurybondyieldslessthan4%todayandisexpectedtoyieldonlyabout5.5%in2015(recallFigure2).Morepointedly,don’tlong-termrateshave torisemoredramaticallythanthatinresponsetothelargeandgrowingnationaldebt?Inshort,theansweris No, not necessarily.

ItisimportanttorecognizethattherelationshipbetweenU.S.governmentdebtlevelsandlonggovernmentbondyieldsismixedandhasvarieddramaticallyovertime.Figure 5showstheyearlylevelsofdebtandinterestratesintheUnitedStatessincethelate1860s.Asisevidentvisually,theaveragecorrelationbetweenlongbondyieldsandfederal debt levels has been zero.

Infact,wereonetographthecurrentrelationshipbetweendebt-to-GDPratiosandlonggovernmentbondyieldsacross countries,itwouldshowastrikinglysimilarcorrelationofzero.Thereasonfor the general absence of a close association betweendebtandinterestratesisthatthereisonlyaweaklinkbetweendeficitsandinflation,atleastindevelopedmarkets(CataoandTerrones,2003).Theweaknessofthelinkisattributedinparttocross-countrydifferencesincentral-bankcredibility,economicsize,domesticprivatesavingsrates,andperception of futurefiscalprudence.

Japan,forinstance,hasoneofthelowestlong-bondyieldsintheworlddespitehavingthehighestdebt-to-GDPratio.AnexplanationisthatJapan’slong-terminflationexpectationsremaincloseto0%(ifnotoutrightdeflationary),andinvestors(mostlyJapaneseprivatecitizens)havebeenwillingtofundthegovernmentdebt.

6

7

The yield curve tends to flatten when the Fed sufficiently tightens policy

Various constant-maturity Treasury yields since January 1989

Figure 4.

Sources: Federal Reserve and National Bureau of Economic Research.

74% Did not opt out

18% Partial opt-out

8% Full opt-out

1-year excess returns: Europe1-year excess returns: U.S.1-year excess returns: Global

10-year excess returns: Europe10-year excess returns: U.S.10-year excess returns: Global

Parallel shift in 1994 as the Fed begins to raise short-term rates; longer-duration bonds underperform shorter-duration bonds

Bond yields decline in 1995; the Fed’s prior-year tightening is viewed as “too aggressive”

“Conundrum” flattening

Yiel

ds (%

)

0

2

4

6

8

10

12

0

2

4

6

8

10

12%

1989 1990 1991 1992 19951994 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 20101993

0

1

NBER recessions 3-month T-bill 2-year yield 5-year yield 10-year yield

Government debt and government bond yields

U.S. gross debt-to-GDP ratio and U.S. long-term interest rates, 1869–2009

Figure 5.

Sources: Vanguard calculations based on annual data from Global Financial Data, the Federal Reserve Board, the U.S. Census Bureau, and the U.S. Bureau of Labor Statistics.

74% Did not opt out

18% Partial opt-out

8% Full opt-out

1-year excess returns: Europe1-year excess returns: U.S.1-year excess returns: Global

10-year excess returns: Europe10-year excess returns: U.S.10-year excess returns: Global

World War II: Massive war-related debt is funded

largely through higher domestic savings

Late 1970s/early 1980s: Inflation expectations become unanchored

Gross U.S. government debt/GDP ratio (left axis) 10-year U.S. Treasury yield (right axis)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Deb

t/G

DP

rat

io (%

)

0

20

40

60

80

100

120

140%

U.S. Treasury yields (%

)

0

2

4

6

8

10

12

14

16%

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

1869 1879 1889 1899 1909 1919 1929 1939 1949 1959 1969 1979 1989 1999 2009

What explains the current level of yields? Deconstructing the yield curve

To better understand both the current level of long ratesandthemarket’sexpectationfortheserates,wedeconstructtheyieldonaconstant-maturity10-yearTreasurybondintoitsvariouscomponents.These include:

• Long-terminflationexpectations.

• Uncertaintyoverthoseinflationexpectations (i.e.,aninflationriskpremium).

• ExpectedfutureFedpolicy,asexpressedintheinflation-adjustedfederalfundsrate.

• ExpectedrealGDPgrowth.

• Theeffectsofchangesinbondsupply(i.e.,thestructural deficit2).

• Theeffectsofchangesinbonddemand(especiallyfromforeigncentralbanksandU.S.investors).

2 The model focuses on the structural budget deficit as calculated by the Congressional Budget Office. The structural deficit measures the financing needs the government faces using the assumption that the economy is permanently at full employment. While in theory any deficit financing should depress bond prices and increase bond yields, periods of rising deficits usually coincide with periods of economic weakness and loose monetary policy, both of which tend to decrease yields. Thus, the correlation between regular budget deficits and interest rates can be misleading, as it does not factor in the stance of monetary policy.

8

Decomposing the 10-year Treasury yield

Average decomposition in percentage points by decade and in 2009

Figure 6.

Note: The 10-year yield decomposition is based on the coefficients for the variables listed above that were estimated from a multivariate regression on quarterly data, imposing a long-run co-integrated relationship among long-run inflation expectations, the 10-year Treasury yield, and the federal funds rate. For details of a similar methodology used by the Federal Reserve, see Warnock and Warnock (2009). To minimize potential reverse-causality bias in the response of domestic Treasury purchases to changes in interest rates, we have implemented a two-stage least squares (2SLS) estimator that uses the U.S. household savings rate and lags of the other independent variables as instruments.

Sources: Vanguard calculations based on data from the Congressional Budget Office, the Federal Reserve, the Federal Reserve Bank of Philadelphia, the U.S. Bureau of Labor Statistics, and the U.S. Census Bureau.

-2

0

2

4

6

8

10

12

–2

0

2

4

6

8

10

12%

10-y

ear T

reas

ury

yiel

d (%

)

5.3

2.2

1.10.2

2.2

–0.1–0.4

10.6

3.3

0.2

1.9

–0.2 –0.4–0.1

6.6

2.5

0.2 0.4 0.1

1.4

4.5

2.42.9

–0.6

3.3

–1.3

0.2

–0.8

0.50.2

0.51.1

Sum of thecomponents =

Structural fiscal deficit

1980s 1990s 2000s 2009

Foreign Treasury purchases

U.S. household Treasury purchases

Long-run inflation expectations

Real federal funds rate

Inflation risk premium

Expected real GDP growth Average 10-year Treasury yield

Our statistical decomposition is based on a modelfollowingtheworkofvariousFederal Reserveresearchers,includingLaubach(2007)andWarnockandWarnock(2009).Figure 6 presents the decompositionoftheaverageyieldonthe10-yearTreasurybondforthedecadesofthe1980s,the1990s,andthe2000s,aswellasfortheyear2009.

AsignificantfindingshowninFigure6isthattheexpectedupwardpressurefromthefiscaldeficitonlongbondratesin2009hasbeenoffset(atleastthusfar)byincreasedbonddemandarisingfromahigher domestic savings rate.Byourestimates,thisrecentsuppressantoflongbondyieldshasbeenaspowerfulastheso-called“globalsavingsglut”thatFedChairmanBenBernankeandothersbelievehelpedtokeeplongyieldslowthroughoutthepastdecade.AccordingtotheFederalReserve’sFlowofFundsdata,householdsandU.S.mutualfundsownedapproximately20%ofallU.S.Treasurysecuritiesoutstandinginthethirdquarterof2009,versus14%in2007beforethecrisis.

IftheU.S.savingsratestayselevatedintheyearsahead,futurelongbondyieldsmaynotriseasstronglyassomeinvestorsnowfear.ThebehaviorofJapaneseinterestratestodayandofU.S.ratesduringWorldWarIIisareminderofthepowerfulinfluence that a higher domestic savings rate can haveonagovernment’sborrowingcosts.Anothercriticalfactorgoingforwardwillbetheeffectivenessoffuturemonetaryand fiscal policies in maintaining stablelong-terminflationexpectations.AsisclearfromFigure6,inflationexpectationsarethelargestsinglecomponentoflong-terminterestrates.3

Bond market expectations seem reasonable, but they are often wrong

Ourinterestratedecompositionnotonlyshedsmore light on the factors influencing the current leveloflongTreasurybondyieldsbutalsoprovidesa basis for assessing the future economic scenario thatispricedintotoday’sbondvaluations(andhenceintotheforwardyieldcurve).BycombiningthedecompositioninFigure6withthemarket’sexpectationthatthe10-yearTreasuryyieldwillrisetoapproximately5.5%in2015(recallFigure2),itcanbeshownempiricallythattheanticipatedbearflatteningisconsistentwiththefollowingscenariooverthenextfiveyears:

1. TheFederalReserveraisesthefedfundsratetoamore“neutral”levelofapproximately4%by2015.Thisisthecurrentexpectationinthefedfundsfuturesmarket.

2. GDPgrowthexpectationsrisemodestlythough2015asthenascenteconomicrecoverybecomesself-sustaining.

3. Theexpectedrateoflong-termCPIinflationremainsanchoredat2.5%,althoughtheuncertaintysurroundingthatexpectation (i.e.,theinflationriskpremium)risesmodestly overtime.

4. ForeigncentralbankscontinuetopurchaseU.S.Treasuries,buttheirsharedecreasesastheycontinuetodiversifytheirreserveholdings.

5. Domesticinvestorshelptofinancethehighstructural deficit through an elevated savings rate ofapproximately5%,therebyalleviatingsome (butnotall)ofthepressureonlong-termrates.

3 See Vanguard white papers by Davis (2007) and Davis and Cleborne (2009) for additional comments on the importance of—and future risks to—U.S. inflation expectations.

9

10

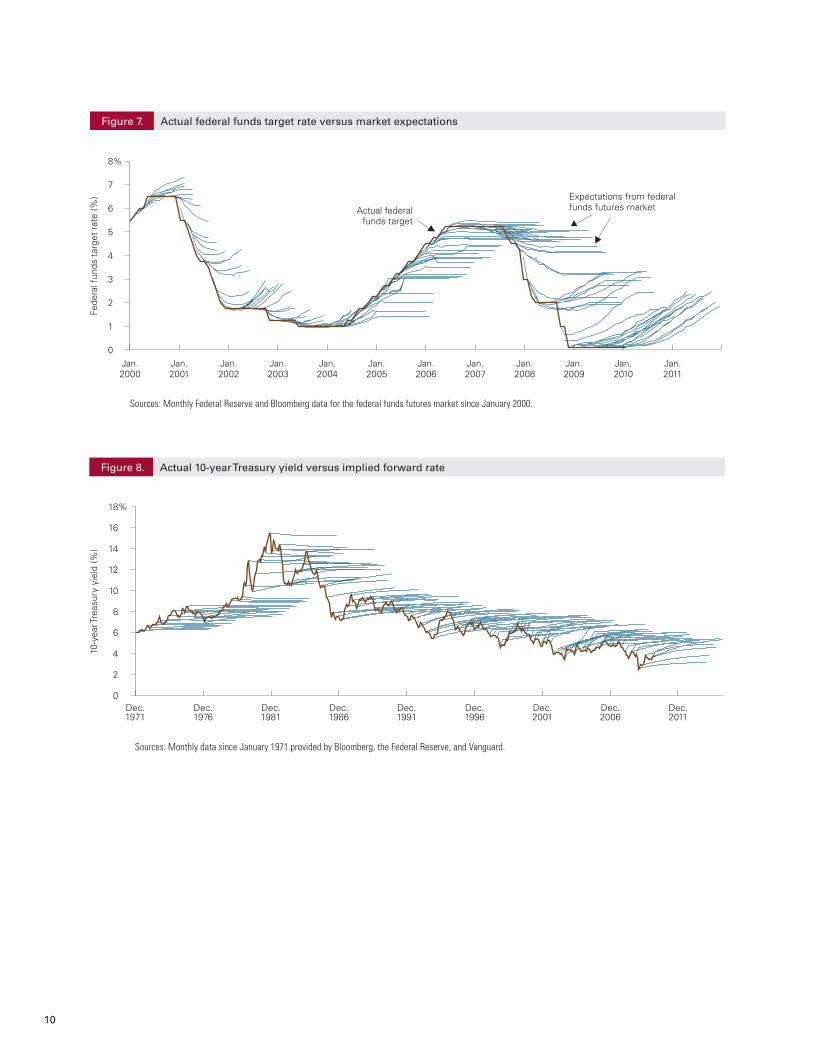

Actual federal funds target rate versus market expectationsFigure 7.

Sources: Monthly Federal Reserve and Bloomberg data for the federal funds futures market since January 2000.

Fede

ral f

unds

tar

get

rate

(%)

0

1

2

3

4

5

6

7

8

0

1

2

3

4

5

6

7

8%

Jan.2000

Jan.2001

Jan.2003

Jan.2004

Jan.2005

Jan.2006

Jan.2007

Jan.2008

Jan.2009

Jan.2010

Jan.2011

Jan.2002

Actual federalfunds target

Expectations from federal funds futures market

Actual 10-year Treasury yield versus implied forward rateFigure 8.

Sources: Monthly data since January 1971 provided by Bloomberg, the Federal Reserve, and Vanguard.

10-y

ear T

reas

ury

yiel

d (%

)

0

2

4

6

8

10

12

14

16

18%

Dec.1971

Dec.1976

Dec.1981

Dec.1986

Dec.1991

Dec.1996

Dec.2001

Dec.2011

Dec.2006

0

2

4

6

8

10

12

14

16

18

Assuch,thebondmarket’sexpectationsforthefutureshapeoftheyieldcurveseemreasonable. Ofcourse,historysuggeststhatrateswilllikelyevolvedifferentlyfromwhatisexpectedtoday.Indeed,weshowthattheTreasuryforwardyieldcurve—aswithotherinterestrateforecasts—hasbeenapoorpredictorofactualfuturerates.4 This hasbeenthecaseforbothshortrates(Figure 7) andlongrates(Figure 8).

Inlightofthisinformation,howshouldbondinvestorsthinkabouttheriskstocurrentmarket rateexpectations?

Implied bond index performance under various future interest rate scenarios

Figure 9,onpage12,presentshypothetical future annualizedtotalreturnsover1-,5-,and10-yearinvestmenthorizonsforfourshort-andintermediate-termindexescommonlyusedasbenchmarksbytaxablebondfunds:

• BarclaysCapitalU.S.1–5YearTreasuryIndex.

• BarclaysCapitalU.S.5–10YearTreasuryIndex.

• BarclaysCapitalU.S.1–5YearCreditIndex.

• BarclaysCapitalU.S.5–10YearCreditIndex.

Recognizingthatthenumberofdistinctfutureyield-curvescenariosisnearlyinfinite,wechosefivepotentialscenariosfrom10,000simulationsgeneratedbytheVanguardCapitalMarketsModel foracalculationofimpliedreturns.Figure9presentstheresults.Forsimplicity,thereturncalculationswerebasedonyieldchangesonlyat12-monthintervals,whilethematuritiesusedtocalculatefutureindexdurationswerechosenbasedontheclosestavailableconstant-maturityTreasuryyield.DetailsofthescenarioassumptionsarelistedwithFigure9.

These simulations have several important implicationsforlong-termbondinvestors.

Mostbroadly,the scenarios that produce the highest short-run returns would be expected to produce the lowest long-run returns.Agoodexampleistheso-calleddouble-dipscenario;forlong-terminvestors,Scenario4wouldlikelybethemosttroubling.Inthisscenario,thepresentlow-rateenvironmentpersistsindefinitelyastheeconomyfallsbackintorecessionandsuffersfromadecade-longmalaisesimilartowhatJapanhasexperiencedforthepasttwodecades.Indeed,itisthisveryoutcomethattheFederalReservehasendeavoredtoavoid.

Conversely,scenariosinwhichratesrisemorein2011thaniscurrentlyexpectedactuallyproducethehighestrelativenominal10-yearreturns.Forinstance,short-termbondindexeshavelowerreturnsinScenario3thaninScenario1becausetheFedraisesratesmorequicklyandaggressivelythanispresentlyexpectedbythemarket.YetinScenario3,long-runinflationexpectationsremainwellanchored,andthusintermediate-termbondindexeshavesimilar10-yearreturnsinbothscenarios.

Indeed, the scenario that is perhaps the most fearedbymanybondinvestors(Scenario5)isalsotheonewiththehighestexpectedreturnovera10-yearhorizon.Naturally,underthis“fiscalcrisis”scenarioallbondindexeswouldbeexpectedtosuffersignificantlynegativereturnsintheshortrunasinterestratesrisesharply.However,overtimethehigherTreasuryandcorporateyieldswouldprovideahigherabsoluteincomestream,asmanyfixedincomeinvestmentseventuallydidinthe1970s andearly1980s.

4 For a more detailed and technical discussion of interest rate predictability, again please see Ilmanen (1996) and Davis and Aliaga-Díaz (2007), as well as the citations therein.

11

12

Implied Treasury and corporate bond returns under alternative scenariosFigure 9.

Barclays Capital Treasury and Credit Index benchmarks

Impliedfutureannualizedreturns

1year 5years 10years (ending (ending (ending 2/2011) 2/2015) 2/2020)

Scenario 1: Treasury forward yield curve is realized

1–5YearTreasuryIndex –0.6% 1.2% 3.1%

5–10YearTreasuryIndex –1.8 1.2 3.2

1–5YearCreditIndex –0.5 1.4 4.0

5–10YearCreditIndex 0.9 2.3 4.0

Scenario 2: Federal Reserve on hold for longer than expected

1–5YearTreasuryIndex 0.7% 1.0% 3.1%

5–10YearTreasuryIndex 2.8 1.6 3.3

1–5YearCreditIndex 3.1 1.0 4.2

5–10YearCreditIndex 6.2 3.6 5.5

Scenario 3: “Preemptive” Federal Reserve is more aggressive than expected

1–5YearTreasuryIndex –1.1% 3.4% 3.7%

5–10YearTreasuryIndex –4.2 1.8 3.2

1–5YearCreditIndex –2.3 3.4 4.0

5–10YearCreditIndex 0.8 3.5 5.4

Scenario 4: Double-dip scenario in 2011; Japan-type economic stagnation thereafter

1–5YearTreasuryIndex 1.4% 2.0% 2.1%

5–10YearTreasuryIndex 11.9 4.0 2.5

1–5YearCreditIndex 0.5 2.4 3.2

5–10YearCreditIndex 8.5 6.4 5.1

Scenario 5: Fiscal and inflation concerns accelerate dramatically; all rates rise

1–5YearTreasuryIndex –1.4% 2.6% 3.9%

5–10YearTreasuryIndex –12.1 0.8 4.5

1–5YearCreditIndex –2.9 3.0 4.7

5–10YearCreditIndex –12.4 1.8 6.5

Sources: Barclays Capital, Bloomberg, Federal Reserve, and Vanguard.

IMPORTANT NOTES: These hypothetical data do not represent the returns on any particular investment. The projections or other information generated by Vanguard Capital Markets Model® simulations regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Results from the model may vary with each use and over time.

Description of investment simulation tool: The Vanguard Capital Markets Model (VCMM) is a proprietary financial simulation tool. Part of the tool is a dynamic module that employs vector autoregressive methods to simulate forward-looking return distributions on a wide array of broad asset classes, including stocks, taxable bonds, and cash. For the VCMM simulations in Figure 9, we used market data available through February 28, 2010, for the Treasury spot yield curves. The VCMM then created projections based on historical relationships of past realizations among the interactions of several macroeconomic and financial variables, including the expectations for future conditions reflected in the U.S. term structure of interest rates. The projections

were applied to the following Barclays Capital U.S. bond indexes: 1–5 Year Treasury Index, 1–5 Year Credit Index, 5–10 Year Treasury Index, and 5–10 Year Credit Index. Importantly, taxes are not factored into the analysis.

Limitations: The projections are based on a statistical analysis of February 2010 yield curves in the context of relationships observed in historical data for both yields and index returns, among other factors. Future returns may behave differently from the historical patterns captured in the distribution of returns generated by the VCMM. It is important to note that our model may be underestimating extreme scenarios that were unobserved in the historical data on which the model is based.

Scenario details: For simplicity, the return calculations were based only on yield changes at 12-month intervals. Specifically, the formula for the implied hypothetical return = Starting Yield - (Starting Duration * (Ending Yield – Starting Yield)), where Duration = ((1– (1+Yield)^(-Maturity))/ (1 – (1+Yield)^(–1))). The index maturities used to calculate future index durations were chosen based on the closest available constant-maturity Treasury yield as follows: the 3-year Treasury constant-maturity yield for the Barclays 1–5 Year Credit Index (3.1 years maturity), and the 7-year Treasury constant-maturity yield for the Barclays 5–10 Year Credit Index (7.7 years maturity).

Details on Scenario 1: The 3-year and 7-year Treasury yields rise at a pace similar to that currently implied by the forward curve. Of course, the simulated interest rate paths in this scenario possess more year-to-year volatility than that implied by the forward curve. As a result, the expected returns of the Barclays 1–5 Year Treasury Index and the Barclays 5–10 Year Treasury Index are similar over the intermediate and long run. Overall, this scenario ranks in the 30%–40% percentile of the VCMM projected average return distribution at a one-year horizon, and ranks near the median 50% percentile of the return distribution on a 10-year investment horizon.

Details on Scenario 2: The 3-year and 7-year Treasury yields rise less than currently implied by the forward curve through 2012 as the Federal Reserve raises short-term rates less than is currently expected. However, Treasury yields rise more quickly over the intermediate term as inflation expectations rise. Over the entire simulation horizon, the averages for the 3-year and 7-year Treasury yields are slightly below the average annual yields reflected in the current forward curve given the delayed monetary-policy response. Overall, this scenario ranks in the 75%–85% percentile of the VCMM projected average return distribution at a one-year horizon, and ranks in the 55%–65% percentile of the return distribution on a 10-year investment horizon.

Details on Scenario 3: The 3-year and 7-year Treasury yields both rise more quickly than they do under the current market forward curve, with the Treasury yield curve almost inverting in 2011 based on the unexpectedly aggressive actions of the Federal Reserve. Over the entire simulation horizon, however, the averages for the 3-year and 7-year Treasury yields are very similar to the average annual yields reflected in the current forward curve. Overall, this scenario ranks in the 15%–25% percentile of the VCMM projected average return distribution at a one-year horizon, and ranks in the 55%–65% percentile of the return distribution on a 10-year investment horizon.

Details on Scenario 4: The 3-year and 7-year Treasury yields both decline in 2011 as the economy falls back into recession. Throughout the simulation horizon, Treasury rates remain below those implied by the current forward curve as both economic growth and inflation expectations remain below current market expectations. For a time, corporate bonds underperform Treasury bonds as credit spreads widen during the double-dip recession. Overall, this scenario ranks in the 70%–80% percentile of the VCMM projected average return distribution at a one-year horizon, and ranks in the 30%–40% percentile of the return distribution on a ten-year investment horizon.

Details on Scenario 5: The 3-year and 7-year Treasury yields both rise more dramatically than they do under the current market forward curve. The 3-year yield rises as high as the 7-year yield by 2015, with the slope of the Treasury yield curve between the 3-year and 7-year Treasury rates inverting for a time as the Federal Reserve attempts to stabilize long-term inflation expectations through more restrictive short-term rates. For a time, corporate bonds under-perform Treasury bonds as credit spreads widen during the crisis. Overall, this scenario ranks in the bottom 10% percentile of the VCMM projected average return distribution at a one-year horizon, and ranks in the 75%–85% percentile of the return distribution on a 10-year investment horizon.

Note: The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Implications for portfolio construction

Akeylessonoftheglobalfinancialcrisisisthatimplementingatoo-narroworsurgicalbondallocation(suchasbyshorteningdurationorinvestingsolely inriskierbondinstruments)involvesimportanttrade-offsthatmayexposebondinvestorstounintendedyield-curveormarketriskswhilepotentiallydeprivingthemofahigherfutureincomestream.Thesetrade-offsareclearlyevidentintherangeofpotentialinterestratescenariosthatwehavedepictedinFigure9.

Thesevaried—butcertainlypossible—ratescenariosattesttothehighdegreeofuncertaintysurroundingthefuturedirectionofeconomicgrowth,thedeficit,

inflation,andinterestrates.Indeed,thedifficulty ofcorrectlyforecastingnotonlywhich(ifany)ofthesescenarioswillunfold,butalsopreciselywhen,isapowerfulreminderthatfocusingoninterestratemovesandshort-termchangesinbondpricescanbecounterproductive.Tous,therangeofpotentialoutcomesinFigure9wouldseemtosupportgreater fixedincomediversificationintheyearsahead, notless.

As illustrated in Figure 10, the performance of varioussegmentsofthebondmarketoverthepastseveralyearsunderscoresthebenefitsofabroadlydiversifiedfixedincomeportfolioregardless of the future direction of interest rates.

13

U.S. taxable bond market returns, 2003–2009

Annual total returns for Barclays Capital benchmarks

Figure 10.

Note: Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Source: Barclays Capital.

Broad-market benchmark: A more broadly diversified portfolio (more securities, exposure to a wide array of risk premiums) that fluctuates less over time

-15

-10

-5

0

5

10

15

20

25

30

–15

–10

–5

0

5

10

15

20

25

30%

2003 2004 2005 2006 2007 2008 2009

Barclays U.S. Aggregate Bond Index

Barclays U.S. 1–5 Year Credit Index

Barclays U.S. Long Credit Index

Barclays U.S. 1–5 Year Treasury Index

Barclays U.S. Long Treasury Index

Overthelongterm,it’sinterestincome—andthereinvestmentofthatincome—thataccountsforthelargestportionoftotalreturnsformanybondfunds.Theimpactofpricefluctuationscanbemorethanoffsetbystayinginvestedandreinvestingincome,evenifthefutureissimilartotherising-rateenvironmentofthelate1970sandearly1980s,asillustratedinFigure11.AccordingtodataprovidedbytheFederalReserve,theyieldonthe10-yearTreasurybondmorethandoubledoverthisperiod,risingfromapproximately6.9%inDecember1976

toashighas15.3%inSeptember1981.Yetthehypothetical$1millioninvestmentmadein1976wouldhavegrowntomorethan$2.0millionbytheendof1983,notnecessarilyadisastrousoutcome given the period’s secular rise in interest rates.Moreover,thehigherlevelofinterestratesintheearly1980ssubsequentlyfellasinflationexpectationsdeclined,settingthestageforevenhigherbondreturnsoverthefollowingdecade.

14

Bond investing in the 1970s and early 1980s

Growth of a $1 million investment in the Barclay’s Capital U.S. Aggregate Bond Index, 1976–1983

Figure 11.

Notes: For this example, we assume that an investor fully funds a $1 million investment in the Barclay’s Capital U.S. Aggregate Bond Index Index on January 1, 1976. We do not account for any expenses or taxes. Interest-on-interest return is calculated as the remainder after subtracting both income and capital returns from the total return.

Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Source: Vanguard calculations based on capital, income, and total return data reported by Barclay's Capital.

Higher interest income more than offsets capital

losses over time

0

500,000

1,000,000

1,500,000

2,000,000

$2,500,000

Dec.1975

Dec.1983

IncomeCapital Interest on interest

Capital losses from arising-rate environment

Dec.1976

Dec.1977

Dec.1979

Dec.1978

Dec.1980

Dec.1981

Dec.1982

References

Catao,Luis,andMarcoE.Terrones,2003.Fiscal Deficits and Inflation.Workingpaper,InternationalMonetaryFund.

Davis,JosephH.,2007.Evolving U.S. inflation dynamics: Explanations and investment implications.Vanguardwhitepaper,ValleyForge,Pa.: TheVanguardGroup.

Davis,JosephH.,2008.Macroeconomic Expectations and the Stock Market: The Importance of a Longer-Term Perspective.ValleyForge,Pa.: TheVanguardGroup.

Davis,JosephH.,andRogerAliaga-Díaz,2007. Real-time forecasting of U.S. bond yields and their excess returns.Workingpaper,SocialScienceResearchNetwork.

Davis,JosephH.,andJonathanCleborne,2009.Recent Policy Actions and the Outlook for U.S. Inflation.ValleyForge,Pa.:TheVanguardGroup.

Engen,EricM.,andR.GlennHubbard,2004. FederalGovernmentDebtandInterestRates. NBER Macroeconomics Annual 2004: 83–138.

Ilmanen,Antti,1996.Market’sRateExpectations andForwardRates.Journal of Fixed Income 6(2,September):8–22.

Laubach,Thomas,2007.New Evidence on the Interest Rate Effects of Budget Deficits and Debt.Workingpaper,U.S.BoardofGovernorsoftheFederalReserveSystem.

Warnock,FrancisE.,andVeronicaCacdacWarnock,2009.InternationalCapitalFlowsandU.S.InterestRates.Journal of International Money and Finance 28:903-919.

15

Vanguard research > Vanguard Center for Retirement Research Vanguard Investment Counseling & Research Vanguard Investment Strategy Group

E-mail > [email protected]

ETF Shares can be bought and sold only through a broker (who will charge a commission) and cannot be redeemed with the issuing fund. The market price of ETF Shares may be more or less than net asset value.

CFA® is a trademark owned by CFA Institute.

P.O.Box2600 ValleyForge,PA19482-2600

© 2010 The Vanguard Group, Inc. All rights reserved.

ICRDIR 032010

Connect with Vanguard® >www.vanguard.com >global.vanguard.com(non-U.S.investors)