Embed Size (px)

Citation preview

DDEEFFEENNCCEE EECCOONNOOMMIICC TTRREENNDDSS IINN TTHHEE AASSIIAA––PPAACCIIFFIICC 22000088

© Commonwealth of Australia 2008 ISSN 1835-386X (Print) ISSN 1835-3878 (Online)

This work is copyright. Apart from any use as permitted under the Copyright Act 1968, no part may be reproduced by any process without prior written permission from the Commonwealth.

Requests and inquiries concerning reproduction and rights should be addressed to:

Commonwealth Copyright Administration, Attorney General’s Department, Robert Garran Offices, National Circuit, Barton ACT 2600

or posted at http://www.ag.gov.au/cca

iii

Table of Contents

Page Preface v South-East Asia — Analysis

Regional Overview 1 Regional Trends 2 Brunei 4 Burma 6 Cambodia 8 Indonesia 10 Laos 12 Malaysia 14 Philippines 16 Singapore 18 Thailand 20 Vietnam 22 East Timor 24

South Pacific — Analysis

Regional Overview 26 Fiji 28 New Zealand 30 Papua New Guinea 32

North Asia — Analysis

Regional Overview 33 Regional Trends 34 China 36 Japan 38 Republic of Korea 40 Taiwan 42 Democratic People’s Republic of Korea 43

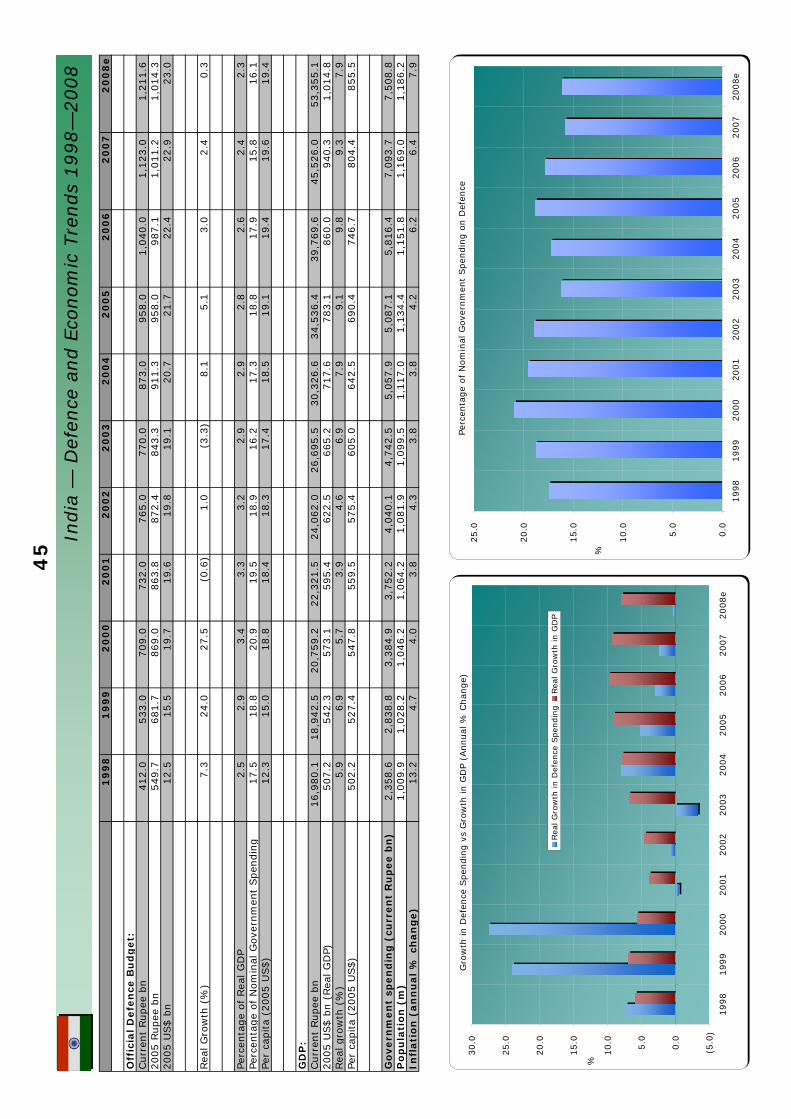

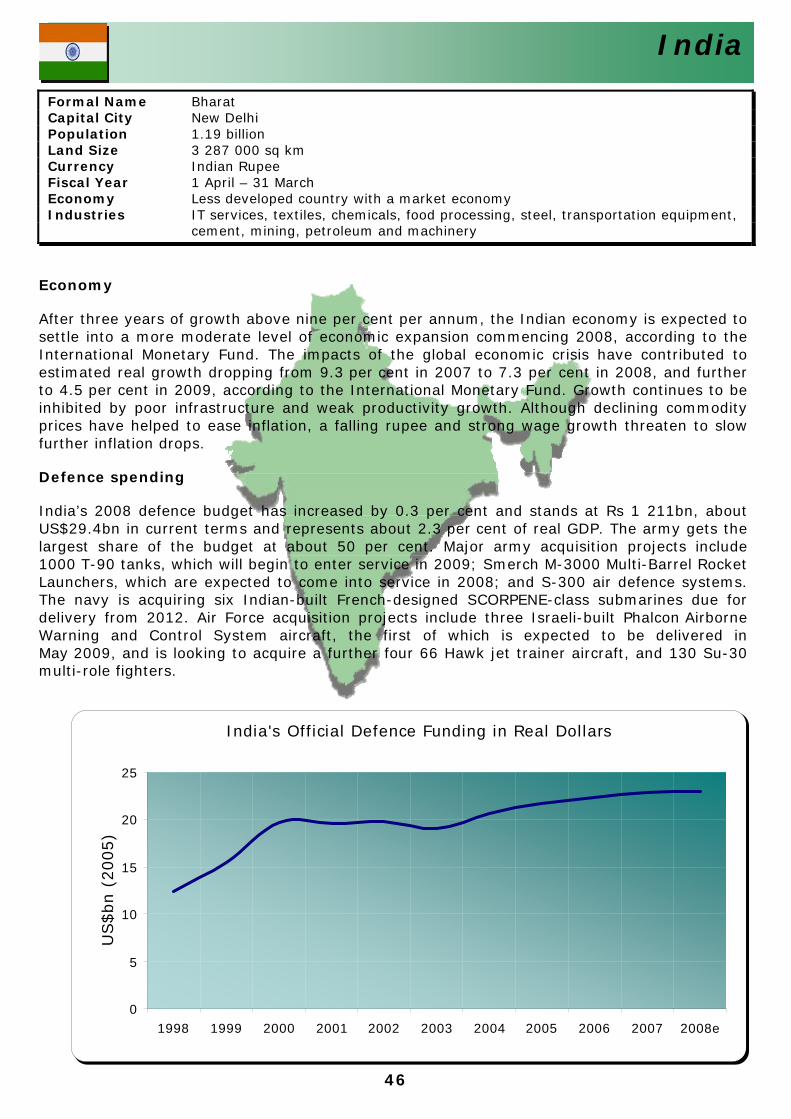

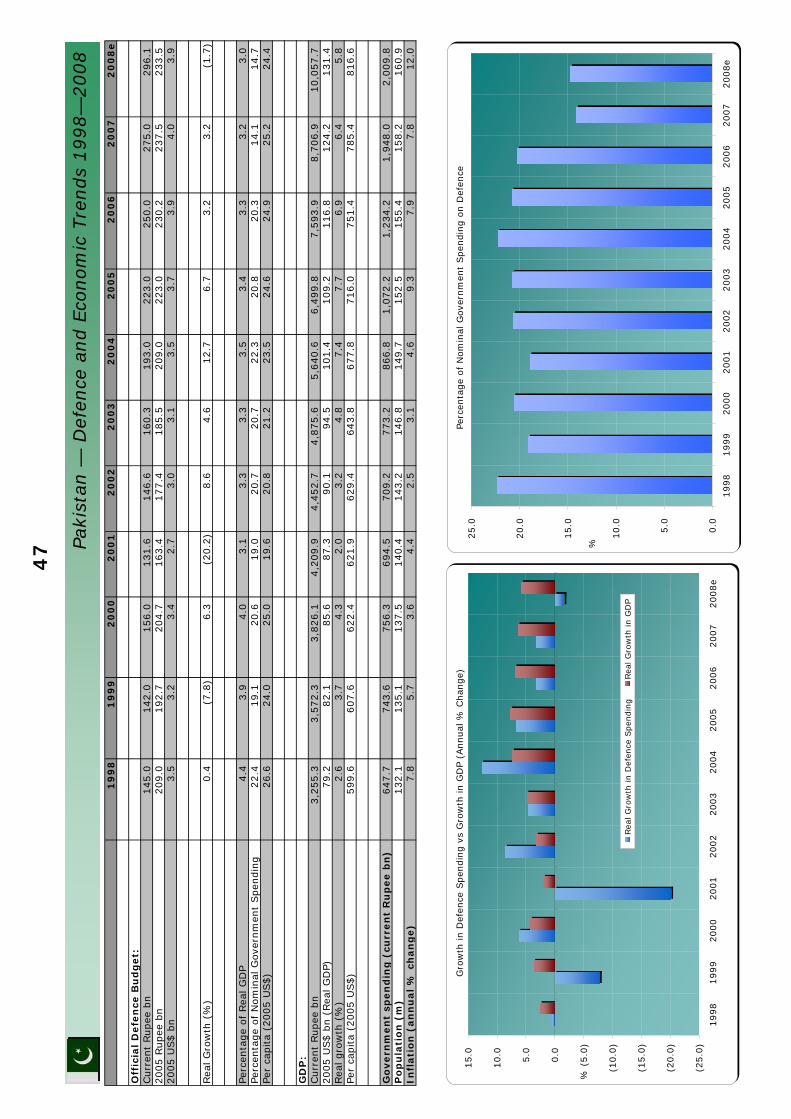

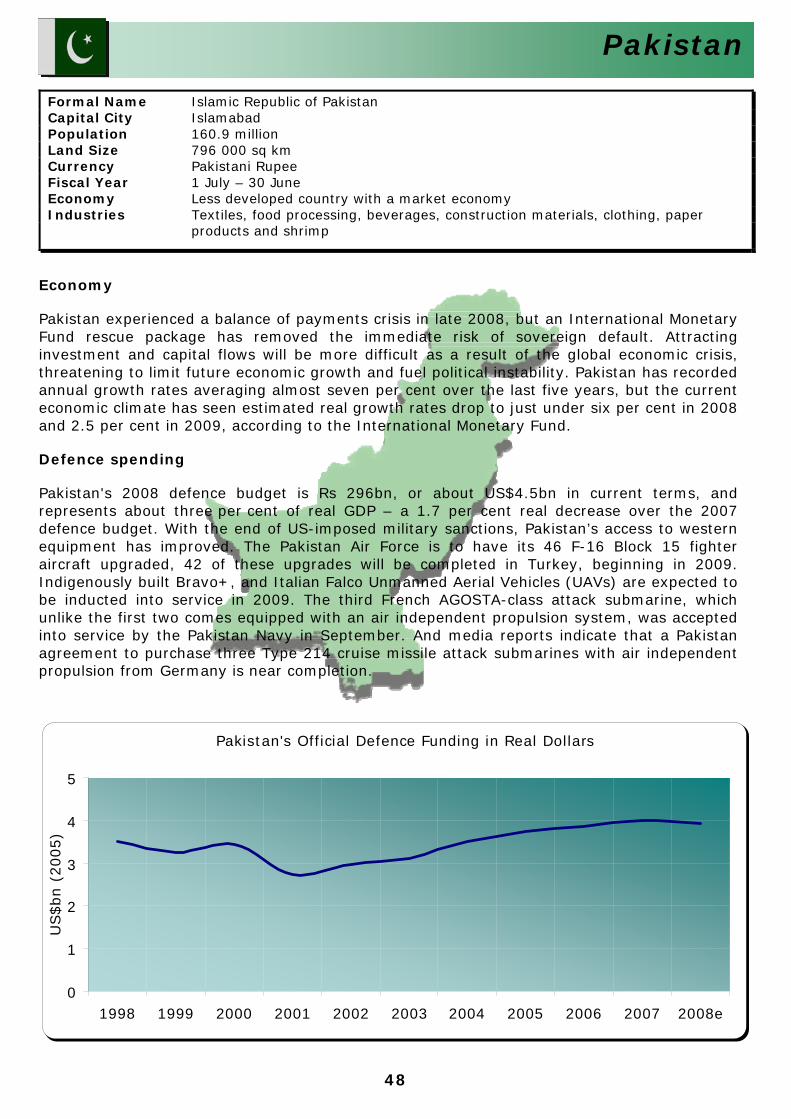

South Asia — Analysis Regional Overview 44 India 46 Pakistan 48

Appendices A: Methodology 54 B: Notes on sources 56

iv

Table of Contents

Tables

Page South-East Asia

Brunei 3 Burma 5 Cambodia 7 Indonesia 9 Laos 11 Malaysia 13 Philippines 15 Singapore 17 Thailand 19 Vietnam 21 East Timor 23

South Pacific

Fiji 27 New Zealand 29 Papua New Guinea 31

North Asia

China 35 Japan 37 Republic of Korea 39 Taiwan 41

South Asia

India 45 Pakistan 47

Australia 50

North America

Canada 52 United States of America 53

v

Preface

Aims The Defence Economic Trends analyses significant trends in defence funding in the Asia-Pacific region. It draws together official defence budgets and national economic data to enable comparisons between countries and over time. Methodology This edition of the Defence Economic Trends in the Asia–Pacific has been updated from the previous methodology introduced in 2000 to compare defence funding trends in the region. Underpinning much of the analysis in this publication are a series of defence spending deflators that are used to convert nominal official defence budgets into constant 2005 terms. While there are some limitations to undertaking expenditure comparisons, our estimates aim to give readers the best available guide to the overall trend for spending on regional armed forces in real terms. For an explanation of the model, and notes on comparing expenditure over time and between countries, please refer to Appendix A. Statistical notes All defence expenditure figures relate to official defence budget estimates unless otherwise stated. Gross domestic product (GDP) and defence budgets are provided both in nominal terms and in constant US dollar terms, to enable comparisons to be made over time and between countries. Online version This publication is available on-line at the Department of Defence’s website: www.defence.gov.au/dio/product.html Feedback We encourage readers to comment on this publication, via the feedback sheet provided, so we can improve next year's edition. If you have any questions in relation to Defence Economic Trends 2008 please contact us direct by phone or fax at:

Defence Intelligence Organisation Telephone: +61 2 6127 5262 Facsimile: +61 2 6127 5086

1

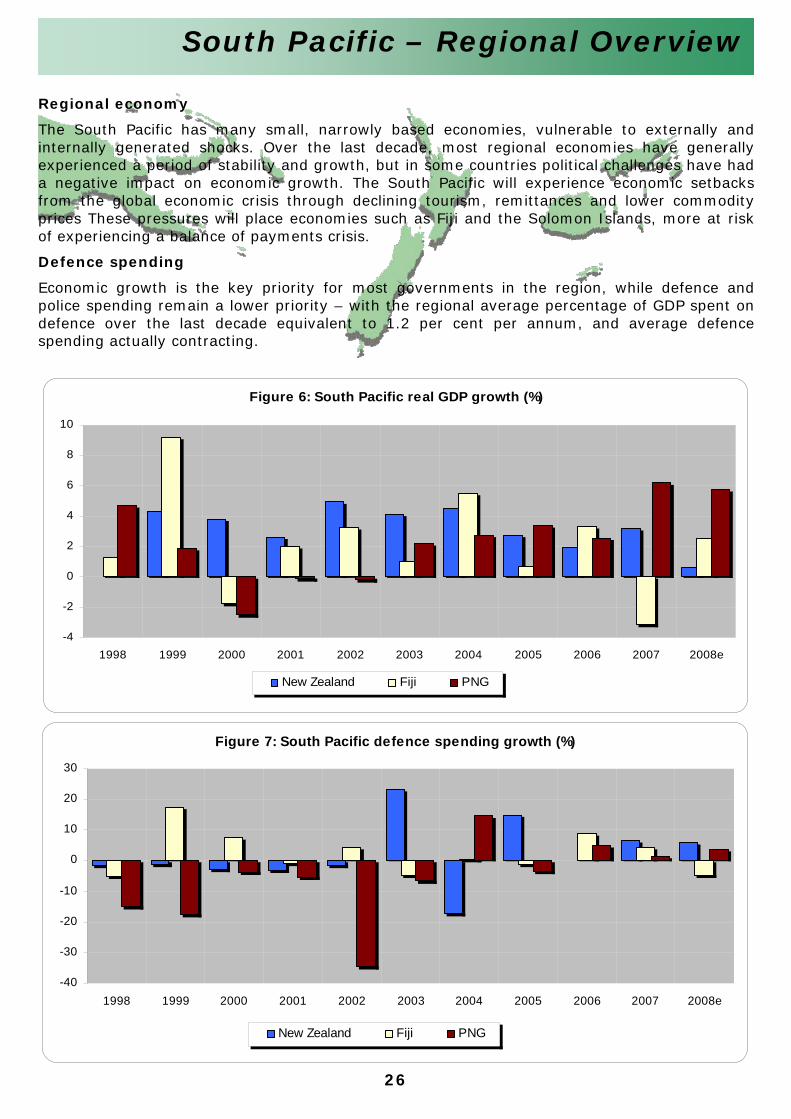

South-East Asia – Regional Overview

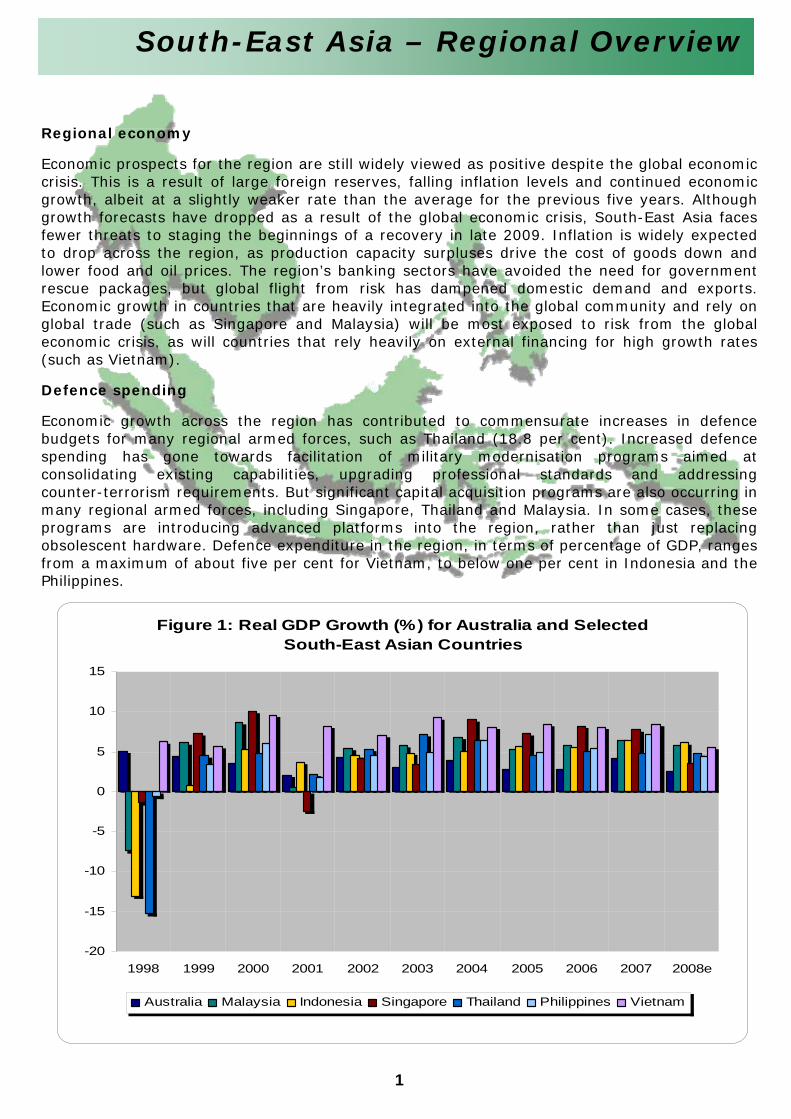

Figure 1: Real GDP Growth (%) for Australia and Selected South-East Asian Countries

-20

-15

-10

-5

0

5

10

15

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

Australia Malaysia Indonesia Singapore Thailand Philippines Vietnam

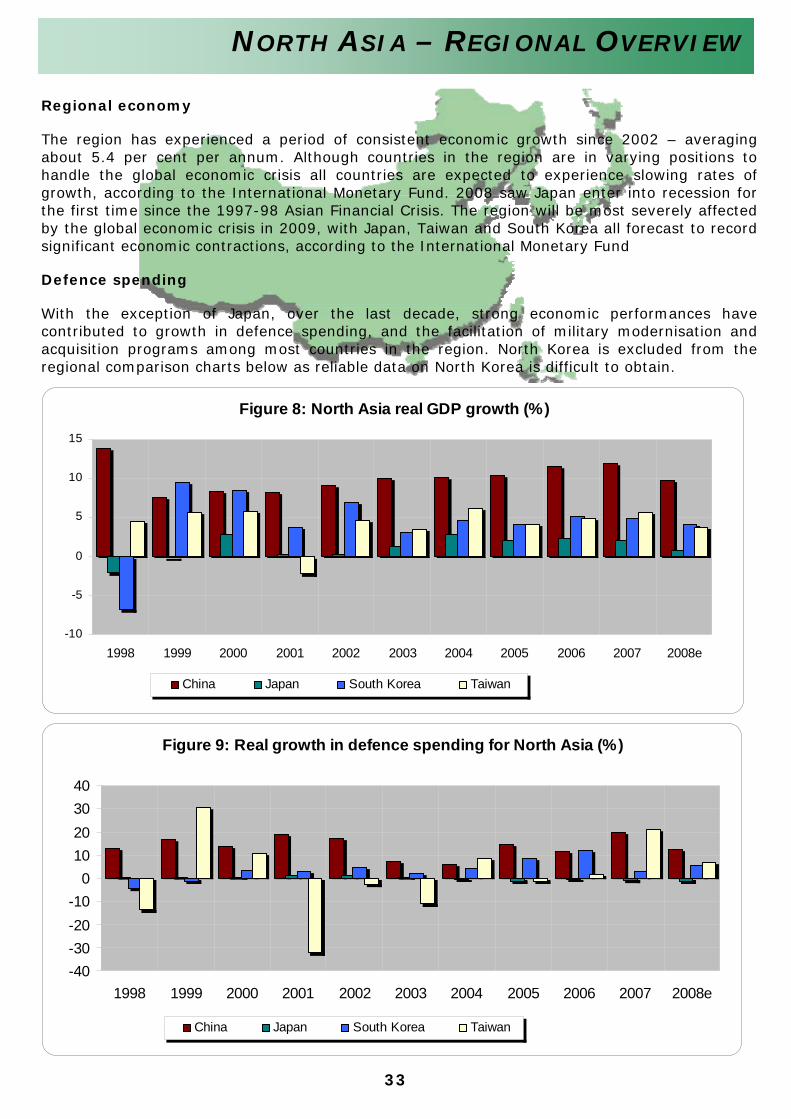

Regional economy

Economic prospects for the region are still widely viewed as positive despite the global economiccrisis. This is a result of large foreign reserves, falling inflation levels and continued economicgrowth, albeit at a slightly weaker rate than the average for the previous five years. Althoughgrowth forecasts have dropped as a result of the global economic crisis, South-East Asia facesfewer threats to staging the beginnings of a recovery in late 2009. Inflation is widely expectedto drop across the region, as production capacity surpluses drive the cost of goods down andlower food and oil prices. The region’s banking sectors have avoided the need for governmentrescue packages, but global flight from risk has dampened domestic demand and exports.Economic growth in countries that are heavily integrated into the global community and rely onglobal trade (such as Singapore and Malaysia) will be most exposed to risk from the globaleconomic crisis, as will countries that rely heavily on external financing for high growth rates(such as Vietnam).

Defence spending

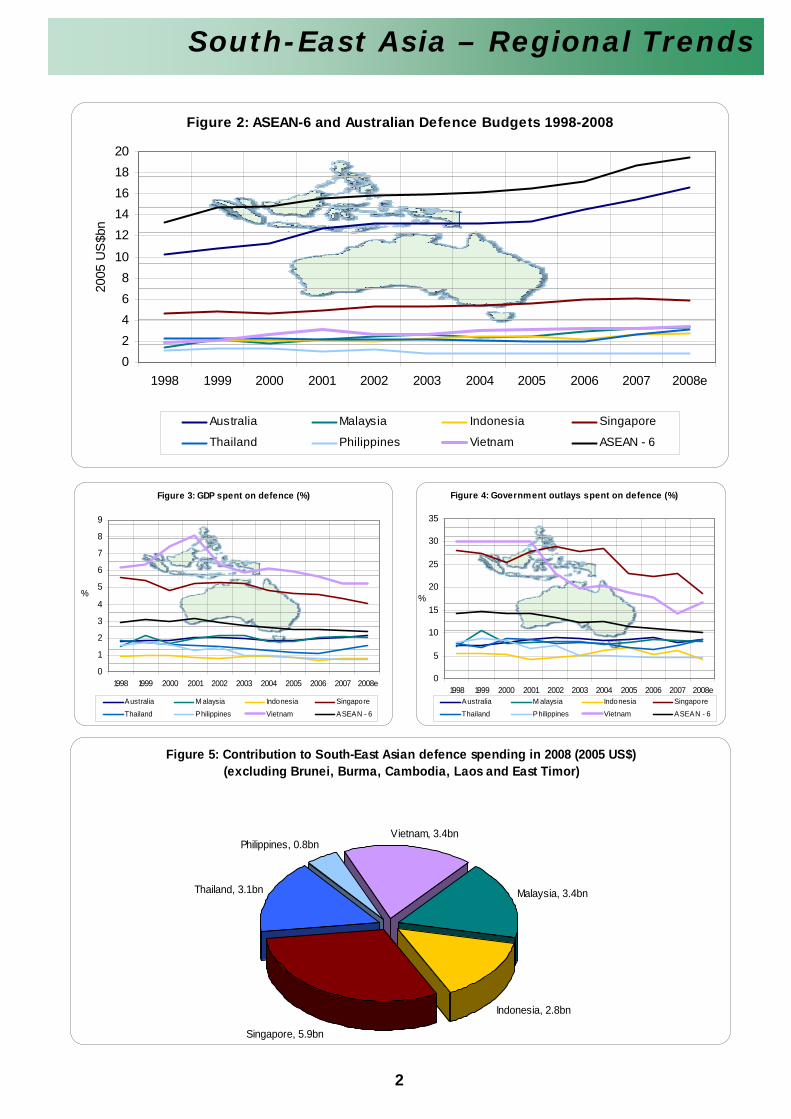

Economic growth across the region has contributed to commensurate increases in defencebudgets for many regional armed forces, such as Thailand (18.8 per cent). Increased defencespending has gone towards facilitation of military modernisation programs aimed atconsolidating existing capabilities, upgrading professional standards and addressingcounter-terrorism requirements. But significant capital acquisition programs are also occurring inmany regional armed forces, including Singapore, Thailand and Malaysia. In some cases, theseprograms are introducing advanced platforms into the region, rather than just replacingobsolescent hardware. Defence expenditure in the region, in terms of percentage of GDP, rangesfrom a maximum of about five per cent for Vietnam, to below one per cent in Indonesia and thePhilippines.

2

South-East Asia – Regional Trends

Figure 2: ASEAN-6 and Australian Defence Budgets 1998-2008

02468

10

1214161820

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

2005

US

$bn

Australia Malaysia Indonesia Singapore

Thailand Philippines Vietnam ASEAN - 6

Figure 5: Contribution to South-East Asian defence spending in 2008 (2005 US$)(excluding Brunei, Burma, Cambodia, Laos and East Timor)

Singapore, 5.9bn

Indonesia, 2.8bn

Malaysia, 3.4bn

Vietnam, 3.4bn

Thailand, 3.1bn

Philippines, 0.8bn

Figure 3: GDP spent on defence (%)

0

1

2

3

4

5

6

7

8

9

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

%

Australia M alaysia Indonesia Singapore

Thailand Philippines Vietnam ASEAN - 6

Figure 4: Government outlays spent on defence (%)

0

5

10

15

20

25

30

35

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

%

Australia M alaysia Indonesia Singapore

Thailand Philippines Vietnam ASEAN - 6

3

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

e

Off

icia

l D

efe

nce

Bu

dg

et:

Curr

ent

B$ b

n0.6

0.6

0.5

0.5

0.5

0.4

0.5

0.5

0.5

0.5

0.5

2005 B

$ b

n0.7

0.8

0.5

0.6

0.5

0.5

0.5

0.5

0.5

0.5

0.4

2005 U

S$ b

n0.4

0.5

0.3

0.3

0.3

0.3

0.3

0.3

0.3

0.3

0.3

Rea

l G

row

th (

%)

16.3

5.0

(30.2

)1.6

(0.5

)(4

.1)

(3.5

)1.0

(4.4

)0.1

(14.1

)

Perc

enta

ge

of

Rea

l G

DP

5.5

5.6

3.8

3.7

3.6

3.3

3.2

3.2

3.0

2.9

2.5

Perc

enta

ge

of

Nom

inal

Gove

rnm

ent

Spen

din

g10.0

10.9

14.6

11.6

11.6

9.4

11.5

10.7

10.1

9.9

9.8

Per

capita

(2005 U

S$)

1,4

35.9

1,4

74.1

1,0

03.5

995.1

966.5

905.6

852.3

833.0

779.3

765.8

644.7

GD

P:

Curr

ent

B$ b

n6.8

7.8

10.3

10.0

10.5

11.4

13.3

15.9

18.2

18.5

24.1

2005 U

S$ b

n (

Rea

l G

DP)

8.1

8.4

8.6

8.8

9.2

9.4

9.5

9.5

10.0

10.0

10.0

Rea

l gro

wth

(%

)(7

.5)

3.1

2.9

2.7

3.9

2.9

0.5

0.4

4.4

0.6

(0.5

)Pe

r ca

pita

(2005 U

S$)

26,1

79.7

26,3

83.3

26,4

68.1

26,5

40.2

26,9

22.0

27,0

68.4

26,5

21.8

25,7

60.4

26,3

25.0

26,0

01.4

25,3

45.8

Go

vern

men

t s p

en

din

g (

curr

en

t B

$ b

n)

5.5

5.5

3.2

4.0

3.9

4.8

4.0

4.8

5.1

5.2

5.3

Po

pu

lati

on

(m

)0.3

0.3

0.3

0.3

0.3

0.3

0.4

0.4

0.4

0.4

0.4

Infl

ati

on

(an

nu

al

% c

han

ge)

(0.4

)(0

.0)

1.2

0.6

(2.3

)0.3

0.9

1.1

0.2

0.3

0.8

Gro

wth

in D

efen

ce S

pen

din

g v

s G

row

th in G

DP

(Annual

% C

han

ge)

(40.0

)

(30.0

)

(20.0

)

(10.0

)

0.0

10.0

20.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Rea

l G

row

th in D

efen

ce S

pen

din

gRea

l G

row

th in G

DP

Perc

enta

ge

of N

om

inal

Gove

rnm

ent

Spen

din

g o

n D

efen

ce

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Bru

nei

Dar

uss

alam

— D

efen

ce a

nd E

conom

ic T

rends

1998—

2008

4

Brunei

EEccoonnoommyy

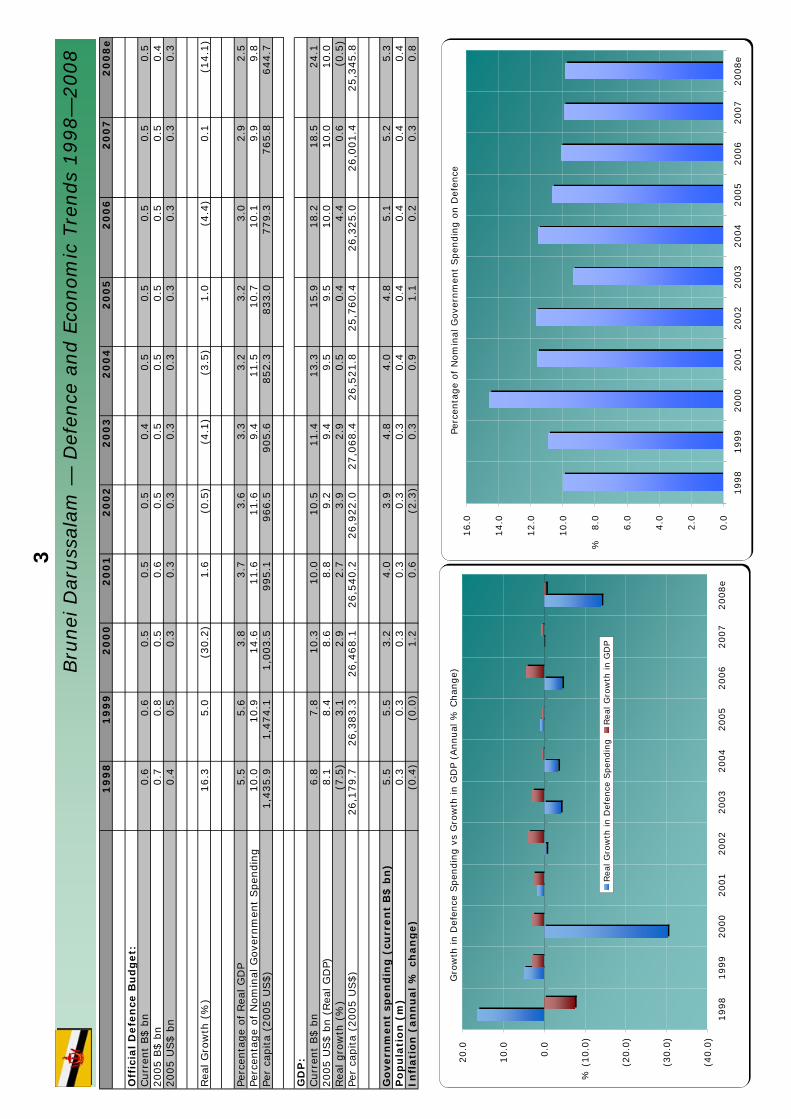

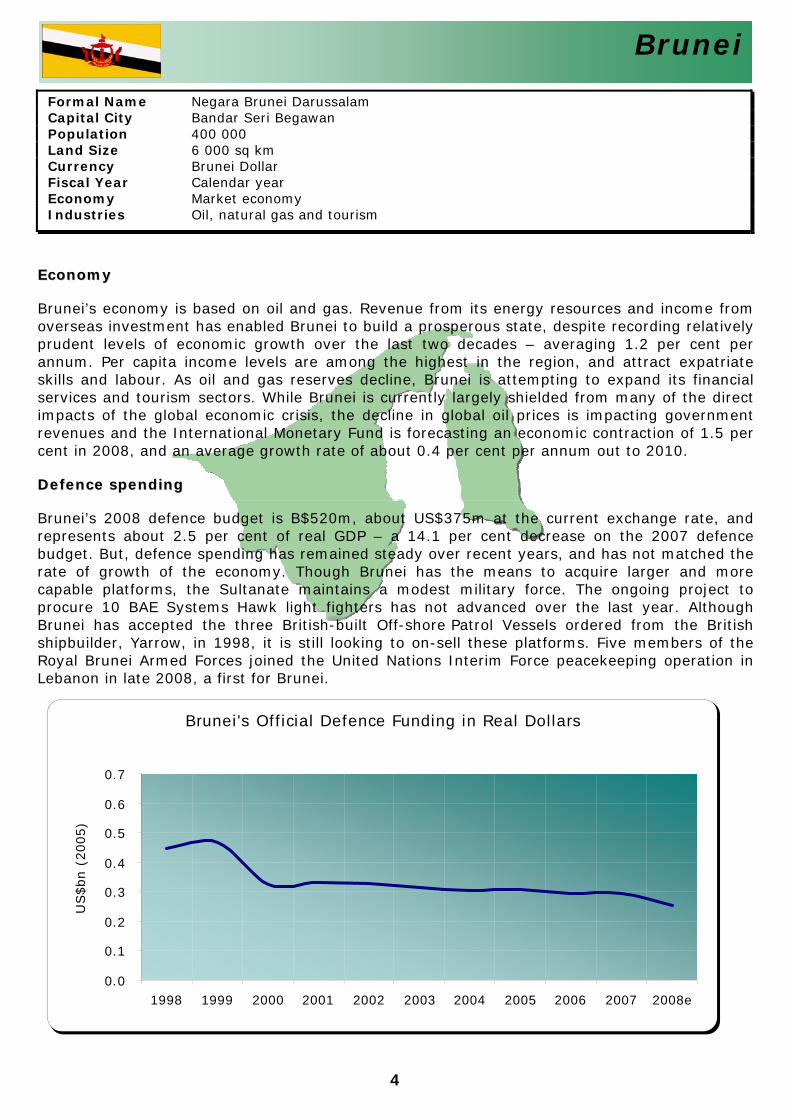

Brunei’s economy is based on oil and gas. Revenue from its energy resources and income from overseas investment has enabled Brunei to build a prosperous state, despite recording relatively prudent levels of economic growth over the last two decades – averaging 1.2 per cent per annum. Per capita income levels are among the highest in the region, and attract expatriate skills and labour. As oil and gas reserves decline, Brunei is attempting to expand its financial services and tourism sectors. While Brunei is currently largely shielded from many of the direct impacts of the global economic crisis, the decline in global oil prices is impacting government revenues and the International Monetary Fund is forecasting an economic contraction of 1.5 per cent in 2008, and an average growth rate of about 0.4 per cent per annum out to 2010.

DDeeffeennccee ssppeennddiinngg

Brunei’s 2008 defence budget is B$520m, about US$375m at the current exchange rate, and represents about 2.5 per cent of real GDP – a 14.1 per cent decrease on the 2007 defence budget. But, defence spending has remained steady over recent years, and has not matched the rate of growth of the economy. Though Brunei has the means to acquire larger and more capable platforms, the Sultanate maintains a modest military force. The ongoing project to procure 10 BAE Systems Hawk light fighters has not advanced over the last year. Although Brunei has accepted the three British-built Off-shore Patrol Vessels ordered from the British shipbuilder, Yarrow, in 1998, it is still looking to on-sell these platforms. Five members of the Royal Brunei Armed Forces joined the United Nations Interim Force peacekeeping operation in Lebanon in late 2008, a first for Brunei.

Brunei's Official Defence Funding in Real Dollars

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

US$bn (

2005)

Formal Name Negara Brunei Darussalam Capital City Bandar Seri Begawan Population 400 000 Land Size 6 000 sq km Currency Brunei Dollar Fiscal Year Calendar year Economy Market economy Industries Oil, natural gas and tourism

5

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

e2

00

8e

Off

icia

l D

efe

nce

Bu

dg

et:

Curr

ent

Kya

ts b

n24.4

31.8

29.8

33.3

37.0

38.0

40.0

40.0

40.0

55.3

74.4

2005 K

yats

bn

80.9

90.2

84.1

72.8

54.0

45.2

45.9

40.0

32.5

33.5

33.5

2005 U

S$ b

n0.0

60.0

70.0

60.0

60.0

40.0

30.0

40.0

30.0

20.0

30.0

3

Rea

l G

row

th (

%)

(11.3

)11.6

(6.7

)(1

3.5

)(2

5.8

)(1

6.3

)1.5

(12.9

)(1

8.8

)3.3

(0.0

)

Perc

enta

ge

of Rea

l G

DP

1.5

1.5

1.3

1.0

0.6

0.5

0.4

0.3

0.2

0.2

0.2

Perc

enta

ge

of N

om

inal

Govt

. Spen

din

g36.5

44.8

36.2

37.6

43.3

39.1

36.2

32.0

29.9

29.3

28.7

Per

capita

(2005 U

S$)

1.3

1.4

1.3

1.1

0.8

0.7

0.7

0.6

0.4

0.4

0.4

GD

P:

Curr

ent

Kya

ts b

n1,6

09.8

2,1

90.3

2,5

52.7

3,5

48.5

5,6

25.3

7,7

16.6

9,0

78.9

12,2

86.8

16,7

15.7

23,6

06.0

32,3

97.0

2005 U

S$ b

n (

Rea

l G

DP)

4.1

4.5

5.2

5.7

6.4

7.3

8.3

9.5

10.7

11.2

11.5

Rea

l gro

wth

(%

)0.7

10.9

13.7

11.3

12.0

13.8

13.6

13.6

12.7

5.5

2.0

Per

capita

(2005 U

S$)

84.9

92.3

102.9

114.6

123.4

137.6

153.2

170.6

188.5

194.9

194.9

Go

vern

men

t sp

en

din

g (

curr

en

t K

yats

bn

)66.9

71.0

82.3

88.7

85.5

97.3

110.5

125.1

133.9

189.1

259.5

Po

pu

lati

on

(m

)48.2

49.1

50.1

50.1

52.2

53.2

54.3

55.4

56.5

57.6

58.8

Infl

ati

on

(an

nu

al

% c

han

ge)

49.1

10.9

(1.7

)34.5

58.1

24.9

3.8

10.7

25.7

33.9

34.5

Gro

wth

in D

efen

ce S

pen

din

g v

s G

row

th in G

DP

(Annual

% C

han

ge)

(30.0

)

(25.0

)

(20.0

)

(15.0

)

(10.0

)

(5.0

)

0.0

5.0

10.0

15.0

20.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007e

2008e

%

Rea

l G

row

th in D

efen

ce S

pen

din

gRea

l G

row

th in G

DP

Perc

enta

ge

of N

om

inal

Gove

rnm

ent

Spen

din

g o

n D

efen

ce

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007e

2008e

%Burm

a —

Def

ence

and E

conom

ic T

rends

1998—

2008

6

Burma

EEccoonnoommyy

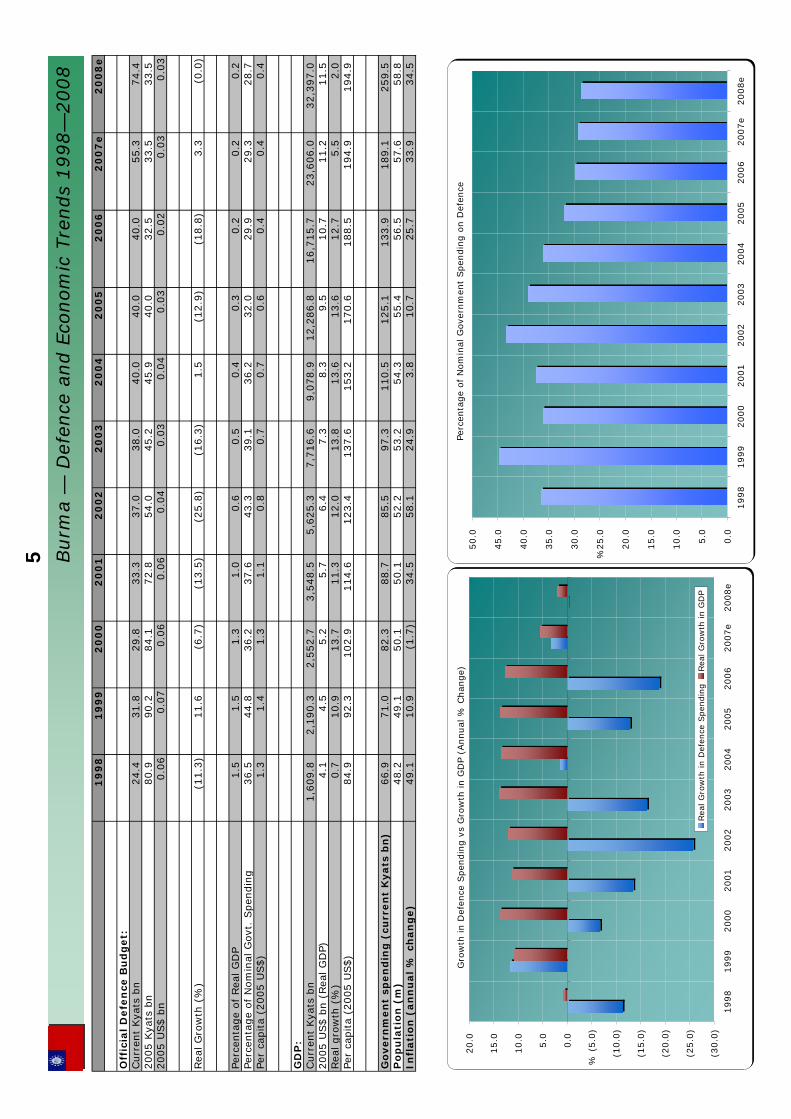

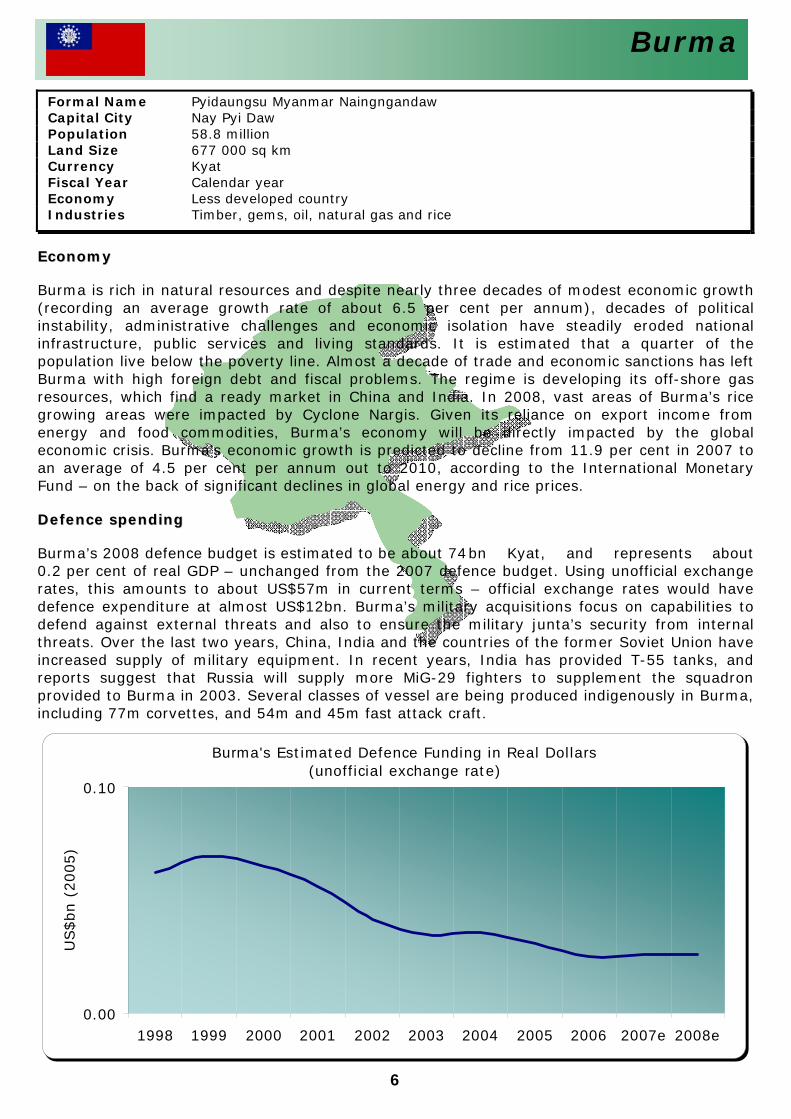

Burma is rich in natural resources and despite nearly three decades of modest economic growth (recording an average growth rate of about 6.5 per cent per annum), decades of political instability, administrative challenges and economic isolation have steadily eroded national infrastructure, public services and living standards. It is estimated that a quarter of the population live below the poverty line. Almost a decade of trade and economic sanctions has left Burma with high foreign debt and fiscal problems. The regime is developing its off-shore gas resources, which find a ready market in China and India. In 2008, vast areas of Burma’s rice growing areas were impacted by Cyclone Nargis. Given its reliance on export income from energy and food commodities, Burma’s economy will be directly impacted by the global economic crisis. Burma’s economic growth is predicted to decline from 11.9 per cent in 2007 to an average of 4.5 per cent per annum out to 2010, according to the International Monetary Fund – on the back of significant declines in global energy and rice prices.

DDeeffeennccee ssppeennddiinngg

Burma’s 2008 defence budget is estimated to be about 74 bn Kyat, and represents about 0.2 per cent of real GDP – unchanged from the 2007 defence budget. Using unofficial exchange rates, this amounts to about US$57m in current terms – official exchange rates would have defence expenditure at almost US$12bn. Burma’s military acquisitions focus on capabilities to defend against external threats and also to ensure the military junta’s security from internal threats. Over the last two years, China, India and the countries of the former Soviet Union have increased supply of military equipment. In recent years, India has provided T-55 tanks, and reports suggest that Russia will supply more MiG-29 fighters to supplement the squadron provided to Burma in 2003. Several classes of vessel are being produced indigenously in Burma, including 77m corvettes, and 54m and 45m fast attack craft.

Burma's Estimated Defence Funding in Real Dollars (unofficial exchange rate)

0.00

0.10

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007e 2008e

US$bn (

2005)

Formal Name Pyidaungsu Myanmar Naingngandaw Capital City Nay Pyi Daw Population 58.8 million Land Size 677 000 sq km Currency Kyat Fiscal Year Calendar year Economy Less developed country Industries Timber, gems, oil, natural gas and rice

7

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

e

Off

icia

l D

efe

nce

Bu

dg

et:

Curr

ent

Rie

ls b

n281.0

330.0

311.2

277.5

265.0

268.0

278.0

456.0

503.0

557.0

692.7

2005 R

iels

bn

328.8

375.3

361.1

317.4

297.2

296.2

294.4

456.0

480.5

501.1

529.2

2005 U

S$ b

n0.0

80.0

90.0

90.0

80.0

70.0

70.0

70.1

10.1

20.1

20.1

3

Rea

l G

row

th (

%)

(11.2

)14.1

(3.8

)(1

2.1

)(6

.4)

(0.3

)(0

.6)

54.9

5.4

4.3

5.6

Perc

enta

ge

of Rea

l G

DP

2.4

2.5

2.2

1.8

1.6

1.4

1.3

1.8

1.7

1.6

1.6

Perc

enta

ge

of N

om

inal

Gove

rnm

ent.

Spen

din

g19.4

22.1

13.2

11.8

10.9

9.7

9.5

13.1

13.3

14.0

15.2

Per

capita

(2005 U

S$)

6.6

7.4

7.0

6.0

5.5

5.4

5.3

8.1

8.3

8.5

8.9

GD

P:

Curr

ent

Rie

ls b

n11,7

18.8

13,3

76.1

14,0

82.6

15,6

33.2

16,7

80.5

18,5

35.2

21,4

38.3

25,7

54.3

29,8

49.1

35,0

39.3

43,2

93.0

2005 U

S$ b

n (

Rea

l G

DP)

3.3

3.7

4.0

4.4

4.6

5.0

5.6

6.3

7.0

7.7

8.2

Rea

l gro

wth

(%

)1.4

12.1

8.8

8.1

6.6

8.5

10.3

13.3

10.8

10.2

7.0

Per

capita

(2005 U

S$)

270.9

296.8

317.6

337.8

354.1

377.9

409.9

455.1

492.2

535.7

563.7

Go

vern

men

t sp

en

din

g (

curr

en

t R

iels

bn

)1,4

45.0

1,4

95.0

2,3

55.0

2,3

44.0

2,4

41.8

2,7

59.0

2,9

37.0

3,4

80.0

3,7

84.0

3,9

77.0

4,5

52.3

Po

pu

lati

on

(m

)12.2

12.5

12.7

12.9

13.1

13.3

13.6

13.8

14.2

14.3

14.6

Infl

ati

on

(an

nu

al %

ch

an

ge)

14.8

4.0

(0.8

)0.2

3.3

1.2

3.8

5.9

4.7

5.9

20.1

Gro

wth

in D

efen

ce S

pen

din

g v

s G

row

th in G

DP

(Annual

% C

han

ge)

(20.0

)

(10.0

)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Rea

l G

row

th in D

efen

ce S

pen

din

gRea

l G

row

th in G

DP

Perc

enta

ge

of N

om

inal

Gove

rnm

ent

Spen

din

g o

n D

efen

ce

0.0

5.0

10.0

15.0

20.0

25.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%Cam

bodia

— D

efen

ce a

nd E

conom

ic T

rends

1998—

2008

8

Cambodia +

Cambodia's Official Defence Funding in Real Dollars

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

US$bn (

2005)

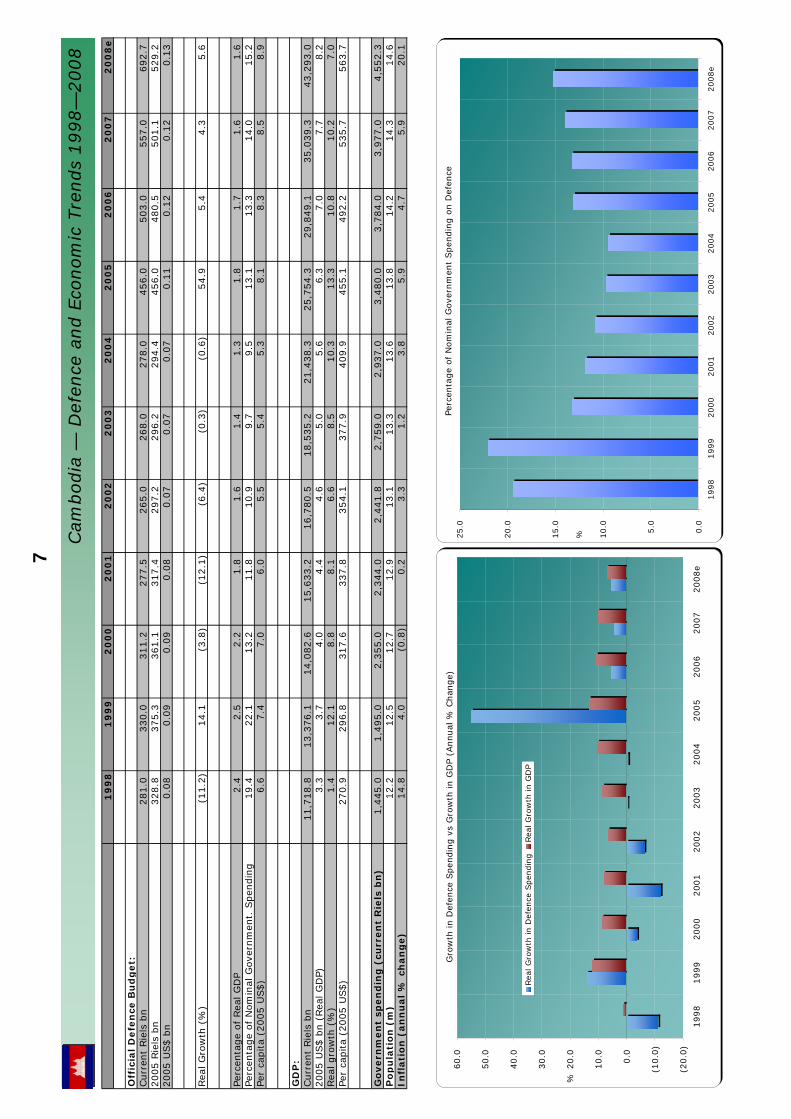

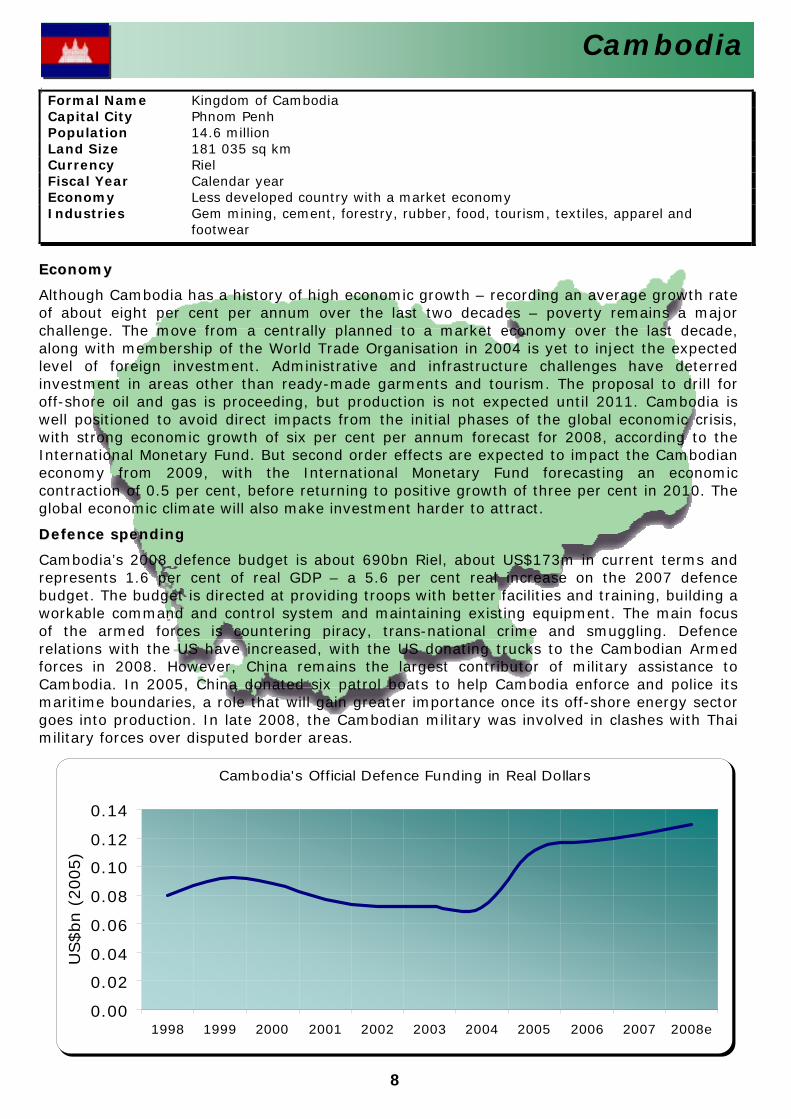

EEccoonnoommyy

Although Cambodia has a history of high economic growth – recording an average growth rate of about eight per cent per annum over the last two decades – poverty remains a major challenge. The move from a centrally planned to a market economy over the last decade, along with membership of the World Trade Organisation in 2004 is yet to inject the expected level of foreign investment. Administrative and infrastructure challenges have deterred investment in areas other than ready-made garments and tourism. The proposal to drill for off-shore oil and gas is proceeding, but production is not expected until 2011. Cambodia is well positioned to avoid direct impacts from the initial phases of the global economic crisis, with strong economic growth of six per cent per annum forecast for 2008, according to the International Monetary Fund. But second order effects are expected to impact the Cambodian economy from 2009, with the International Monetary Fund forecasting an economic contraction of 0.5 per cent, before returning to positive growth of three per cent in 2010. The global economic climate will also make investment harder to attract.

DDeeffeennccee ssppeennddiinngg

Cambodia’s 2008 defence budget is about 690bn Riel, about US$173m in current terms and represents 1.6 per cent of real GDP – a 5.6 per cent real increase on the 2007 defence budget. The budget is directed at providing troops with better facilities and training, building a workable command and control system and maintaining existing equipment. The main focus of the armed forces is countering piracy, trans-national crime and smuggling. Defence relations with the US have increased, with the US donating trucks to the Cambodian Armed forces in 2008. However, China remains the largest contributor of military assistance to Cambodia. In 2005, China donated six patrol boats to help Cambodia enforce and police its maritime boundaries, a role that will gain greater importance once its off-shore energy sector goes into production. In late 2008, the Cambodian military was involved in clashes with Thai military forces over disputed border areas.

Formal Name Kingdom of Cambodia Capital City Phnom Penh Population 14.6 million Land Size 181 035 sq km Currency Riel Fiscal Year Calendar year Economy Less developed country with a market economy Industries Gem mining, cement, forestry, rubber, food, tourism, textiles, apparel and

footwear

9

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

e

Off

icia

l D

efe

nce

Bu

dg

et:

Curr

ent

Rupia

h b

n9,4

00.0

12,1

87.1

13,0

00.0

14,3

00.0

15,4

15.8

18,2

84.0

21,4

10.0

23,9

00.0

23,6

00.0

31,3

00.0

36,4

00.0

2005 R

upia

h b

n18,2

96.6

20,1

09.1

20,2

66.1

19,8

47.5

19,5

36.4

21,8

42.1

23,9

55.7

23,9

00.0

20,8

10.9

25,4

86.0

26,8

65.4

2005 U

S$ b

n1.9

2.1

2.1

2.0

2.0

2.3

2.5

2.5

2.1

2.6

2.8

Rea

l G

row

th (

%)

(17.0

)9.9

0.8

(2.1

)(1

.6)

11.8

9.7

(0.2

)(1

2.9

)22.5

5.4

Perc

enta

ge

of

Rea

l G

DP

0.9

1.0

0.9

0.9

0.8

0.9

0.9

0.9

0.7

0.8

0.8

Perc

enta

ge

of

Nom

inal

Gove

rnm

ent

Spen

din

g5.4

5.6

5.3

4.2

4.6

5.2

6.1

6.7

5.3

6.2

4.3

Per

capita

(2005 U

S$)

9.2

10.0

10.2

9.8

9.6

10.5

11.4

11.2

9.7

11.7

12.2

GD

P:

Curr

ent

Rupia

h b

n1,0

56,1

31.5

1,2

15,2

31.2

1,3

89,7

69.9

1,6

46,3

22.0

1,8

21,8

33.4

2,0

13,6

74.6

2,2

95,8

26.2

2,7

74,2

81.1

3,3

39,4

79.6

3,9

57,4

03.9

4,6

07,5

92.5

2005 U

S$ b

n (

Rea

l G

DP)

213.7

215.4

226.9

235.2

245.8

257.5

270.5

285.9

301.6

320.7

340.2

Rea

l gro

wth

(%

)(1

3.1

)0.8

5.4

3.6

4.5

4.8

5.0

5.7

5.5

6.3

6.1

Per

capita

(2005 U

S$)

1,0

45.6

1,0

38.4

1,1

06.2

1,1

31.1

1,1

66.2

1,2

05.9

1,2

50.0

1,3

04.1

1,3

58.4

1,4

25.6

1,4

93.1

Go

vern

men

t s p

en

din

g (

curr

en

t R

up

iah

bn

)173,9

19.0

215,9

26.0

244,1

33.3

340,3

25.7

332,4

64.5

354,7

75.0

348,3

30.0

358,9

03.0

443,5

09.0

504,7

76.0

854,7

00.0

Po

pu

lati

on

(m

)204.4

207.4

205.1

207.9

210.7

213.6

216.4

219.2

222.1

224.9

227.8

Infl

ati

on

(an

nu

al %

ch

an

ge)

58.0

20.8

3.8

11.5

11.8

6.8

6.1

10.5

13.1

6.2

9.8

Sta

tist

ical N

ote

: In

dones

ia's

fis

cal ye

ar c

han

ged

in 2

000.

As

a re

sult t

he

2000 b

udget

only

cove

rs 9

month

s an

d h

as b

een a

nnual

ised

to p

roduce

the

figure

for

2000.

Gro

wth

in D

efen

ce S

pen

din

g v

s G

row

th in G

DP

(Annual

% C

han

ge)

(20.0

)

(15.0

)

(10.0

)

(5.0

)

0.0

5.0

10.0

15.0

20.0

25.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Rea

l G

row

th in D

efen

ce S

pen

din

gRea

l G

row

th in G

DP

Perc

enta

ge

of N

om

inal

Gove

rnm

ent

Spen

din

g o

n D

efen

ce

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

Indones

ia —

Def

ence

and E

conom

ic T

rends

1998—

2008

10

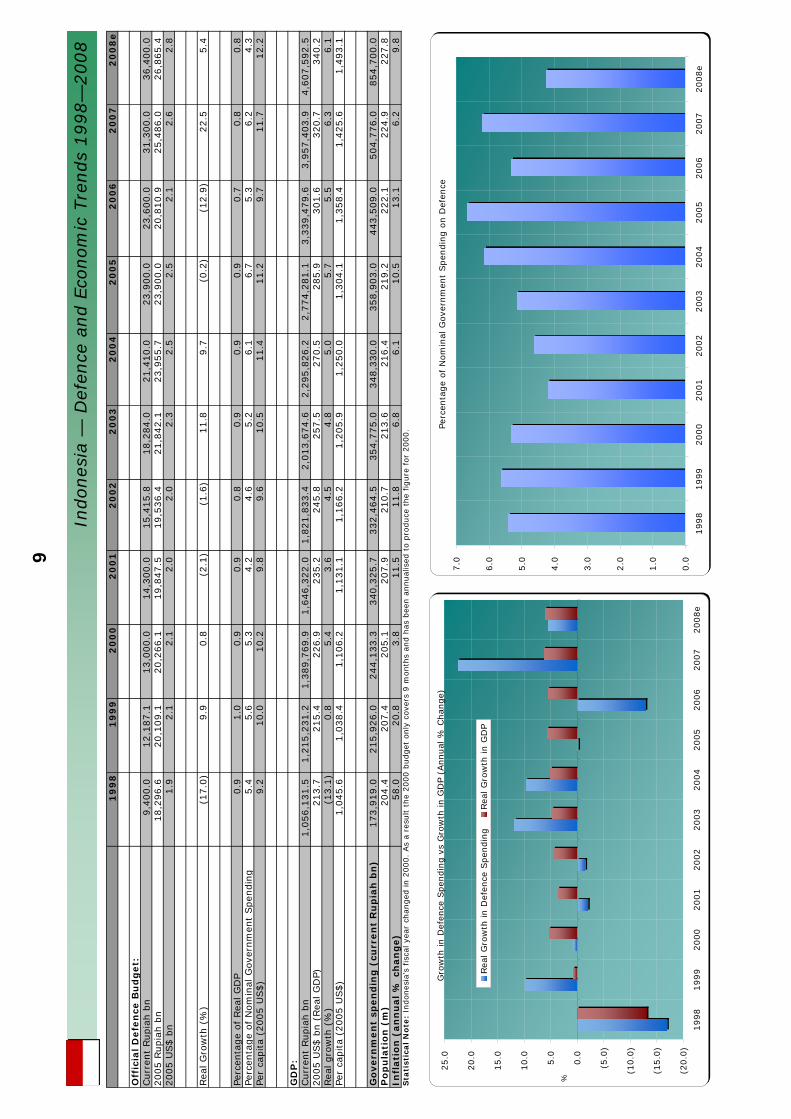

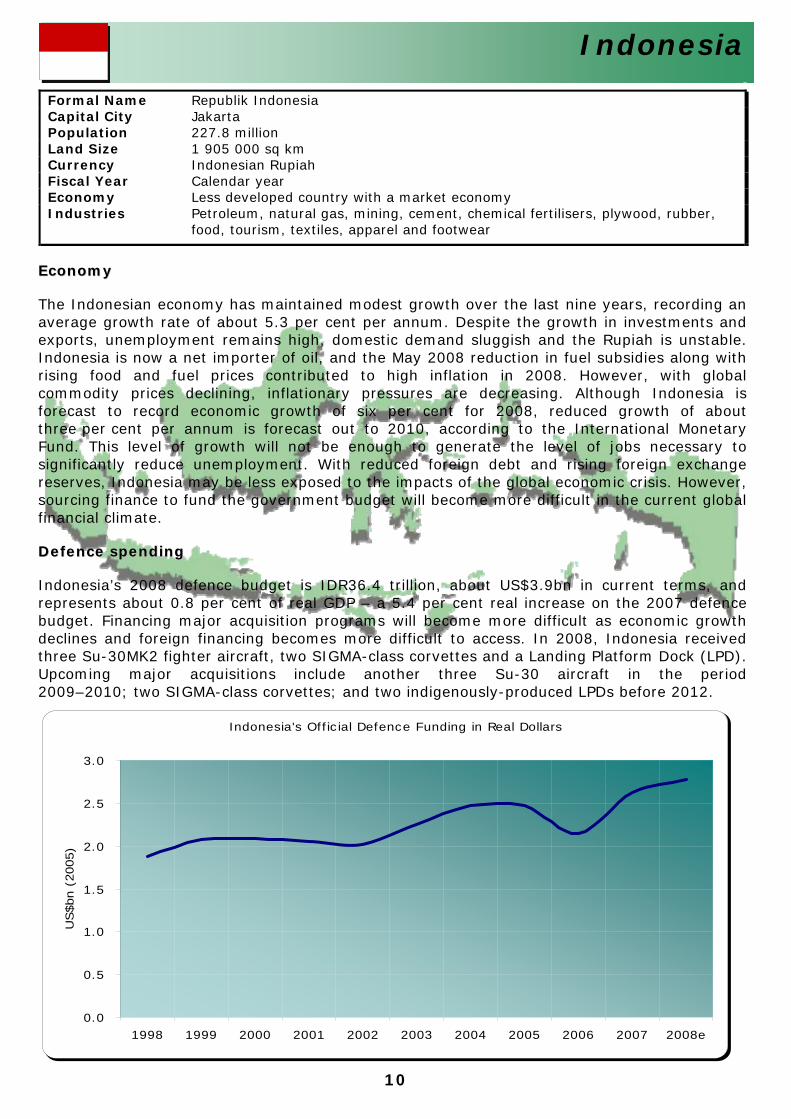

Indonesia

Indonesia's Official Defence Funding in Real Dollars

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

US$bn (

2005)

EEccoonnoommyy

The Indonesian economy has maintained modest growth over the last nine years, recording anaverage growth rate of about 5.3 per cent per annum. Despite the growth in investments and exports, unemployment remains high, domestic demand sluggish and the Rupiah is unstable.Indonesia is now a net importer of oil, and the May 2008 reduction in fuel subsidies along with rising food and fuel prices contributed to high inflation in 2008. However, with global commodity prices declining, inflationary pressures are decreasing. Although Indonesia isforecast to record economic growth of six per cent for 2008, reduced growth of about three per cent per annum is forecast out to 2010, according to the International Monetary Fund. This level of growth will not be enough to generate the level of jobs necessary to significantly reduce unemployment. With reduced foreign debt and rising foreign exchangereserves, Indonesia may be less exposed to the impacts of the global economic crisis. However, sourcing finance to fund the government budget will become more difficult in the current global financial climate.

DDeeffeennccee ssppeennddiinngg

Indonesia’s 2008 defence budget is IDR36.4 trillion, about US$3.9bn in current terms, and represents about 0.8 per cent of real GDP – a 5.4 per cent real increase on the 2007 defence budget. Financing major acquisition programs will become more difficult as economic growthdeclines and foreign financing becomes more difficult to access. In 2008, Indonesia received three Su-30MK2 fighter aircraft, two SIGMA-class corvettes and a Landing Platform Dock (LPD).Upcoming major acquisitions include another three Su-30 aircraft in the period 2009–2010; two SIGMA-class corvettes; and two indigenously-produced LPDs before 2012.

Formal Name Republik Indonesia Capital City Jakarta Population 227.8 million Land Size 1 905 000 sq km Currency Indonesian Rupiah Fiscal Year Calendar year Economy Less developed country with a market economy Industries Petroleum, natural gas, mining, cement, chemical fertilisers, plywood, rubber,

food, tourism, textiles, apparel and footwear

11

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

e

Off

icia

l D

efe

nce

Bu

dg

et:

Curr

ent

Kip

bn

110.0

110.0

107.0

111.8

115.0

115.0

120.6

125.0

135.0

157.1

185.1

2005 K

ip b

n509.6

223.8

175.3

168.1

157.4

136.1

129.2

125.0

126.4

141.5

153.0

2005 U

S$ b

n0.0

50.0

20.0

20.0

20.0

10.0

10.0

10.0

10.0

10.0

10.0

1

Rea

l G

row

th (

%)

(22.9

)(5

6.1

)(2

1.7

)(4

.1)

(6.4

)(1

3.5

)(5

.1)

(3.3

)1.1

11.9

8.1

Perc

enta

ge

of Rea

l G

DP

2.6

1.1

0.8

0.7

0.6

0.5

0.5

0.4

0.4

0.4

0.4

Perc

enta

ge

of N

om

inal

Gove

rnm

ent

Spen

din

gn/a

4.1

3.0

3.1

2.9

3.1

2.4

2.1

1.9

2.0

1.9

Per

capita

(2005 U

S$)

9.5

4.1

3.1

2.9

2.7

2.3

2.1

2.0

2.0

2.2

2.3

GD

P:

Curr

ent

Kip

bn

4,2

40.0

10,3

28.6

13,6

69.5

15,7

01.8

18,4

01.0

22,5

97.1

26,5

49.2

30,4

80.8

35,1

93.1

39,2

85.0

46,2

65.0

2005 U

S$ b

n (

Rea

l G

DP)

1.9

2.0

2.1

2.2

2.4

2.5

2.7

2.9

3.1

3.3

3.6

Rea

l gro

wth

(%

)3.6

7.3

5.8

5.7

5.9

6.1

6.4

7.1

8.1

7.9

7.5

Per

capita

(2005 U

S$)

369.5

387.1

400.2

413.4

427.8

443.5

461.0

484.2

513.2

543.6

573.6

Go

vern

men

t sp

en

din

g (

curr

en

t K

ip b

n)

n/a

2,7

04.9

3,5

31.4

3,6

11.4

4,0

17.0

3,7

21.0

5,1

24.0

6,0

01.0

6,9

68.0

7,9

74.0

9,5

50.0

Po

pu

lati

on

(m

)5.0

5.2

5.3

5.4

5.5

5.7

5.8

5.9

6.0

6.1

6.3

Infl

ati

on

(an

nu

al

% c

han

ge)

90.1

128.4

23.2

9.3

9.2

15.5

10.5

7.2

6.8

4.5

8.4

Gro

wth

in D

efen

ce S

pen

din

g v

s G

row

th in G

DP

(Annual

% C

han

ge)

(60.0

)

(50.0

)

(40.0

)

(30.0

)

(20.0

)

(10.0

)

0.0

10.0

20.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Rea

l G

row

th in D

efen

ce S

pen

din

gRea

l G

row

th in G

DP

Perc

enta

ge

of

Nom

inal

Gove

rnm

ent

Spen

din

g o

n D

efen

ce

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Laos

— D

efen

ce a

nd E

conom

ic T

rends

1998—

2008

12

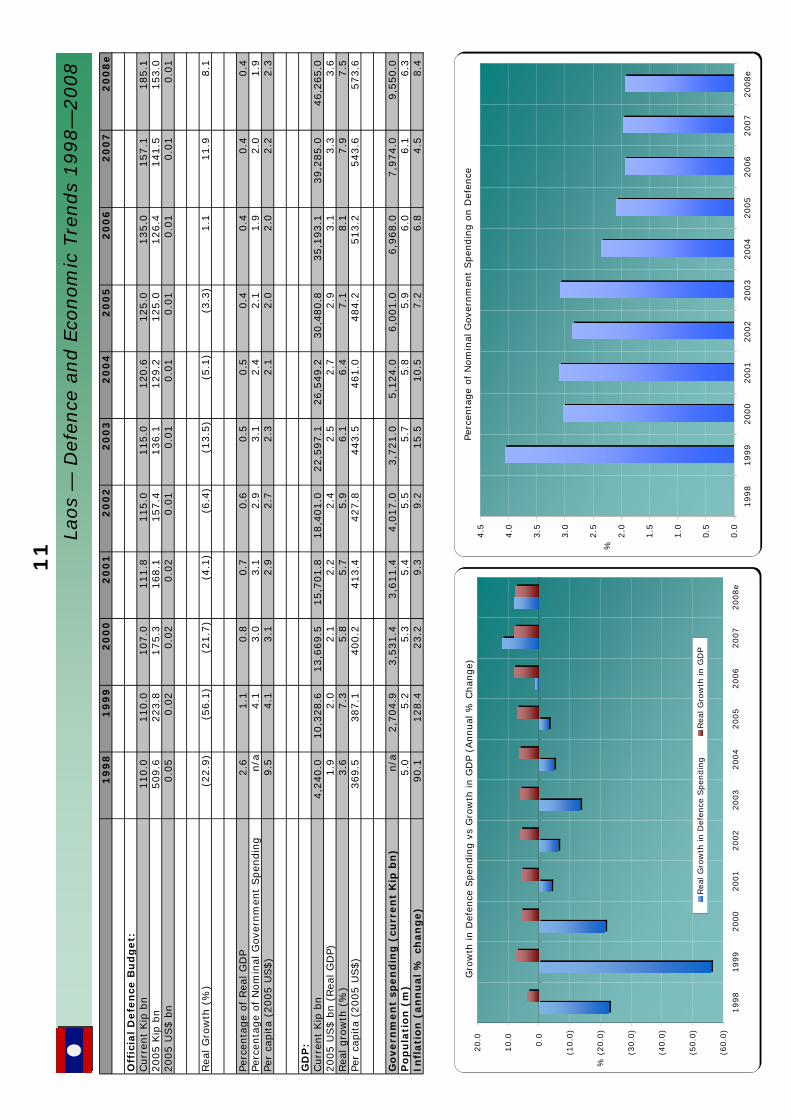

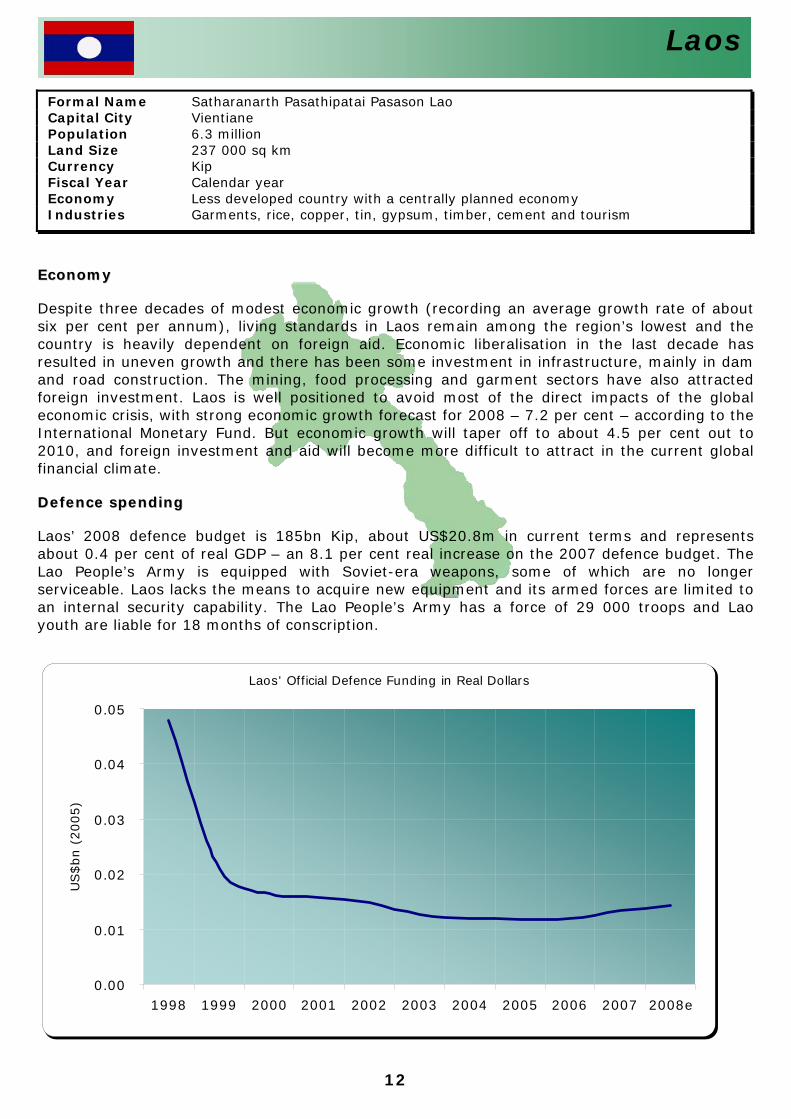

Laos

EEccoonnoommyy

Despite three decades of modest economic growth (recording an average growth rate of about six per cent per annum), living standards in Laos remain among the region’s lowest and the country is heavily dependent on foreign aid. Economic liberalisation in the last decade has resulted in uneven growth and there has been some investment in infrastructure, mainly in dam and road construction. The mining, food processing and garment sectors have also attracted foreign investment. Laos is well positioned to avoid most of the direct impacts of the global economic crisis, with strong economic growth forecast for 2008 – 7.2 per cent – according to the International Monetary Fund. But economic growth will taper off to about 4.5 per cent out to 2010, and foreign investment and aid will become more difficult to attract in the current global financial climate.

DDeeffeennccee ssppeennddiinngg

Laos’ 2008 defence budget is 185bn Kip, about US$20.8m in current terms and represents about 0.4 per cent of real GDP – an 8.1 per cent real increase on the 2007 defence budget. The Lao People’s Army is equipped with Soviet-era weapons, some of which are no longer serviceable. Laos lacks the means to acquire new equipment and its armed forces are limited to an internal security capability. The Lao People’s Army has a force of 29 000 troops and Lao youth are liable for 18 months of conscription.

Laos' Official Defence Funding in Real Dollars

0.00

0.01

0.02

0.03

0.04

0.05

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

US

$bn (

2005)

Formal Name Satharanarth Pasathipatai Pasason Lao Capital City Vientiane Population 6.3 million Land Size 237 000 sq km Currency Kip Fiscal Year Calendar year Economy Less developed country with a centrally planned economy Industries Garments, rice, copper, tin, gypsum, timber, cement and tourism

13

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

e

Off

icia

l D

efe

nce

Bu

dg

et:

Curr

ent

Rin

ggits

bn

4.5

6.9

6.0

7.3

8.3

9.1

8.5

9.4

11.7

13.4

14.5

2005 R

inggits

bn

5.4

8.2

6.9

8.4

9.4

10.0

8.9

9.4

11.2

12.3

12.7

2005 U

S$ b

n1.4

2.2

1.8

2.2

2.5

2.6

2.3

2.5

3.0

3.2

3.4

Rea

l G

row

th (

%)

(16.5

)53.4

(15.8

)20.7

12.1

6.6

(10.9

)5.5

19.1

9.9

3.6

Perc

enta

ge

of

Rea

l G

DP

1.5

2.2

1.7

2.0

2.1

2.2

1.8

1.8

2.0

2.1

2.0

Perc

enta

ge

of

Nom

inal

Gove

rnm

ent

Spen

din

g7.0

10.6

7.7

8.0

8.3

8.3

7.6

8.0

8.6

8.4

8.2

Per

capita

(2005 U

S$)

63.8

95.6

77.8

91.9

100.9

105.6

92.3

95.5

111.9

120.9

123.2

GD

P:

Curr

ent

Rin

ggits

bn

287.5

305.3

356.4

352.6

383.2

418.8

474.0

522.4

573.7

641.9

695.7

2005 U

S$ b

n (

Rea

l G

DP)

94.9

100.7

109.4

110.0

115.9

122.6

131.0

138.0

145.9

155.2

164.1

Rea

l gro

wth

(%

)(7

.4)

6.1

8.7

0.5

5.4

5.8

6.8

5.3

5.8

6.3

5.8

Per

capita

(2005 U

S$)

4,2

77.7

4,4

33.8

4,6

58.1

4,5

81.2

4,7

27.0

4,9

07.4

5,1

42.7

5,3

15.9

5,5

29.0

5,7

81.5

6,0

11.8

Go

vern

men

t sp

en

din

g (

curr

en

t R

ing

git

s b

n)

64.1

65.1

78.0

91.1

100.5

109.8

112.5

117.4

136.7

159.5

176.9

Po

pu

lati

on

(m

)22.2

22.7

23.5

24.0

24.5

25.0

25.5

26.0

26.4

26.8

27.3

Infl

ati

on

Rate

(an

nu

al

% c

han

ge)

5.3

2.7

1.6

1.4

1.8

1.1

1.4

3.0

3.6

2.0

6.0

Stat

istic

al N

ote:

The

200

3 an

d 20

04 fi

gure

s in

clud

e a

fund

ing

supp

lem

ent

Gro

wth

in D

efen

ce S

pen

din

g v

s G

row

th in G

DP

(Annual

% C

han

ge)

(30.0

)

(20.0

)

(10.0

)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Rea

l G

row

th in D

efen

ce S

pen

din

gRea

l G

row

th in G

DP

Perc

enta

ge

of

Nom

inal

Gove

rnm

ent

Spen

din

g o

n D

efen

ce

0.0

2.0

4.0

6.0

8.0

10.0

12.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Mal

aysi

a —

Def

ence

and E

conom

ic T

rends

1998—

2008

14

Malaysia

EEccoonnoommyy

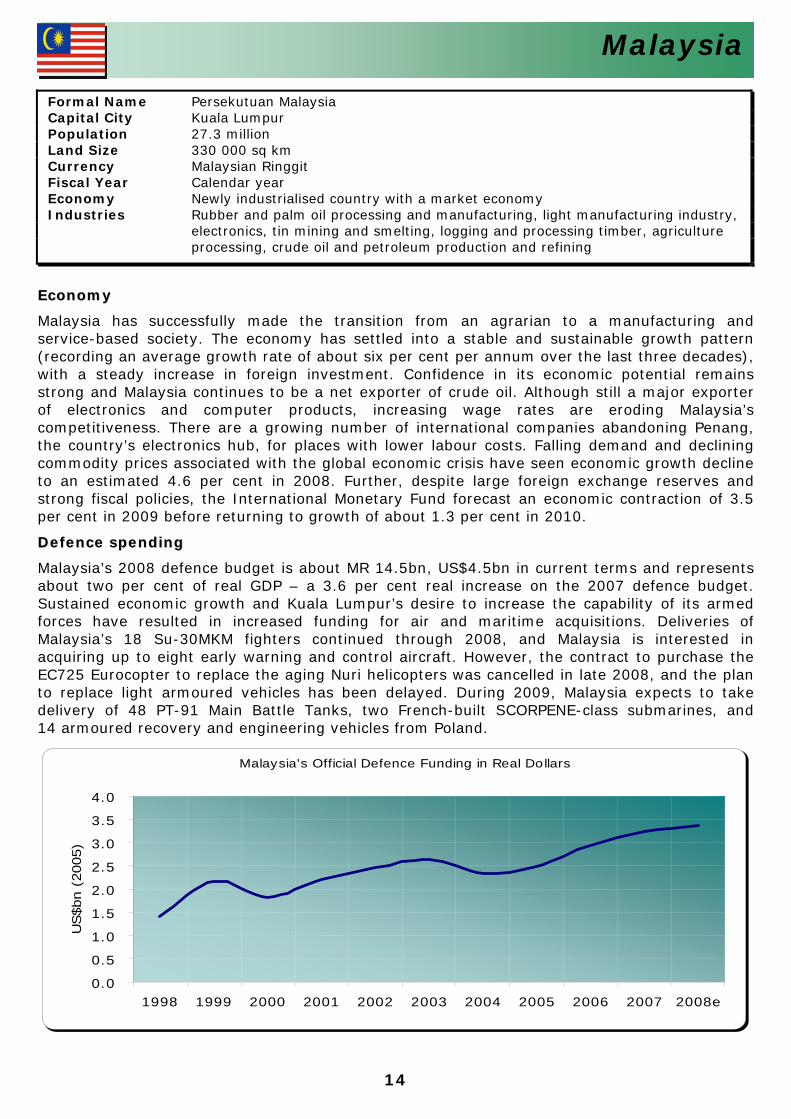

Malaysia has successfully made the transition from an agrarian to a manufacturing and service-based society. The economy has settled into a stable and sustainable growth pattern (recording an average growth rate of about six per cent per annum over the last three decades), with a steady increase in foreign investment. Confidence in its economic potential remains strong and Malaysia continues to be a net exporter of crude oil. Although still a major exporter of electronics and computer products, increasing wage rates are eroding Malaysia’s competitiveness. There are a growing number of international companies abandoning Penang, the country’s electronics hub, for places with lower labour costs. Falling demand and declining commodity prices associated with the global economic crisis have seen economic growth decline to an estimated 4.6 per cent in 2008. Further, despite large foreign exchange reserves and strong fiscal policies, the International Monetary Fund forecast an economic contraction of 3.5 per cent in 2009 before returning to growth of about 1.3 per cent in 2010.

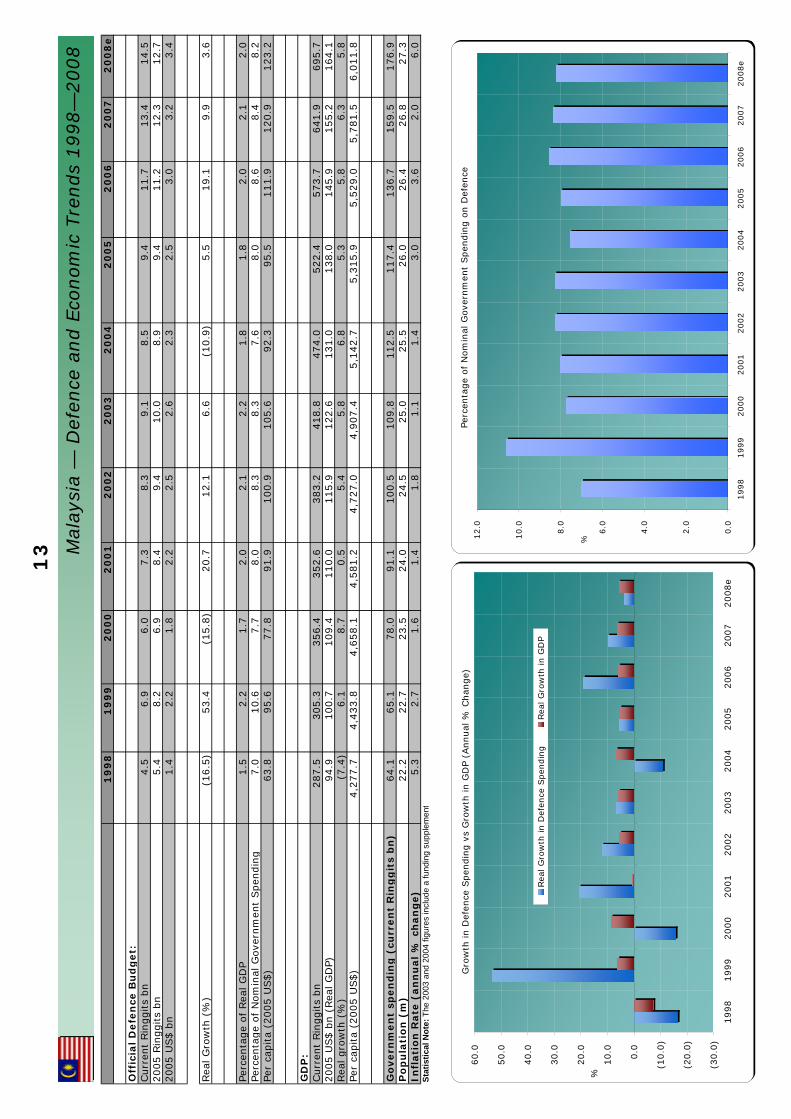

DDeeffeennccee ssppeennddiinngg

Malaysia’s 2008 defence budget is about MR 14.5bn, US$4.5bn in current terms and represents about two per cent of real GDP – a 3.6 per cent real increase on the 2007 defence budget. Sustained economic growth and Kuala Lumpur’s desire to increase the capability of its armed forces have resulted in increased funding for air and maritime acquisitions. Deliveries of Malaysia’s 18 Su-30MKM fighters continued through 2008, and Malaysia is interested in acquiring up to eight early warning and control aircraft. However, the contract to purchase the EC725 Eurocopter to replace the aging Nuri helicopters was cancelled in late 2008, and the plan to replace light armoured vehicles has been delayed. During 2009, Malaysia expects to take delivery of 48 PT-91 Main Battle Tanks, two French-built SCORPENE-class submarines, and 14 armoured recovery and engineering vehicles from Poland.

Malaysia's Official Defence Funding in Real Dollars

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

US$bn (

2005)

Formal Name Persekutuan Malaysia Capital City Kuala Lumpur Population 27.3 million Land Size 330 000 sq km Currency Malaysian Ringgit Fiscal Year Calendar year Economy Newly industrialised country with a market economy Industries Rubber and palm oil processing and manufacturing, light manufacturing industry,

electronics, tin mining and smelting, logging and processing timber, agriculture processing, crude oil and petroleum production and refining

15

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

e

Off

icia

l D

efe

nce

Bu

dg

et:

Curr

ent

Peso

bn

41.0

52.0

54.0

46.8

57.3

42.4

45.2

46.6

49.3

51.5

56.1

2005 P

eso b

n60.9

72.3

71.3

57.5

68.1

48.5

48.7

46.6

46.2

47.0

46.7

2005 U

S$ b

n1.1

1.3

1.3

1.0

1.2

0.9

0.9

0.8

0.8

0.9

0.8

Rea

l G

row

th (

%)

6.8

18.7

(1.3

)(1

9.4

)18.5

(28.8

)0.4

(4.2

)(0

.9)

1.8

(0.7

)

Perc

enta

ge

of

Rea

l G

DP

1.5

1.8

1.6

1.3

1.5

1.0

0.9

0.9

0.8

0.8

0.7

Perc

enta

ge

of

Nom

inal

Gove

rnm

ent

Spen

din

g7.8

8.8

8.3

6.5

7.3

5.0

5.1

4.8

4.7

4.5

4.6

Per

capita

(2005 U

S$)

15.1

17.6

17.0

13.4

15.5

10.8

10.6

9.9

9.6

9.6

9.4

GD

P:

Curr

ent

Peso

bn

2,6

65.1

2,9

76.9

3,3

54.7

3,6

31.5

3,9

63.9

4,3

16.4

4,8

71.6

5,4

44.0

6,0

32.8

6,6

48.3

7,5

63.8

2005 U

S$ b

n (

Rea

l G

DP)

72.4

74.9

79.4

80.8

84.4

88.5

94.2

98.8

104.2

111.7

116.6

Rea

l gro

wth

(%

)(0

.6)

3.4

6.0

1.8

4.4

4.9

6.4

5.0

5.4

7.2

4.4

Per

capita

(2005 U

S$)

990.4

1,0

02.1

1,0

39.6

1,0

36.5

1,0

61.1

1,0

91.7

1,1

26.9

1,1

59.2

1,1

97.7

1,2

60.6

1,2

90.1

Go

vern

men

t sp

en

din

g (

curr

en

t P

eso

bn

)528.0

590.2

649.0

714.5

789.1

839.6

893.8

962.9

1,0

44.4

1,1

49.0

1,2

26.7

Po

pu

lati

on

(m

)73.1

74.7

76.3

77.9

79.5

81.1

83.6

85.3

87.0

88.6

90.4

Infl

ati

on

(an

nu

al

% c

han

ge)

9.7

6.4

4.0

6.8

3.0

3.5

6.0

7.7

6.2

2.8

10.1

Gro

wth

in D

efen

ce S

pen

din

g v

s G

row

th in G

DP

(Annual

% C

han

ge)

(30.0

)

(25.0

)

(20.0

)

(15.0

)

(10.0

)

(5.0

)

0.0

5.0

10.0

15.0

20.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Rea

l G

row

th in D

efen

ce S

pen

din

gRea

l G

row

th in G

DP

Perc

enta

ge

of N

om

inal

Gove

rnm

ent

Spen

din

g o

n D

efen

ce

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Phili

ppin

es —

Def

ence

and E

conom

ic T

rends

1998—

2008

16

Philippines

Philippines' Official Defence Spending in Real Dollars

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

US$bn (2005)

Economy

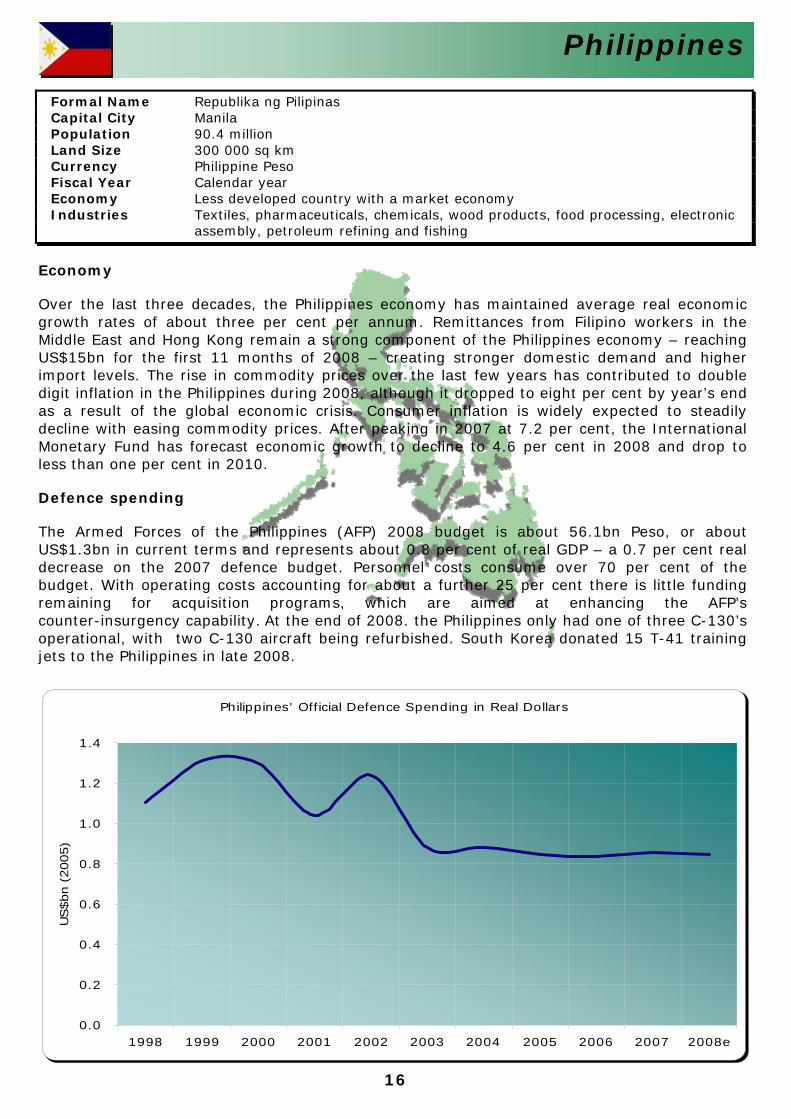

Over the last three decades, the Philippines economy has maintained average real economicgrowth rates of about three per cent per annum. Remittances from Filipino workers in the Middle East and Hong Kong remain a strong component of the Philippines economy – reaching US$15bn for the first 11 months of 2008 – creating stronger domestic demand and higher import levels. The rise in commodity prices over the last few years has contributed to double digit inflation in the Philippines during 2008, although it dropped to eight per cent by year’s endas a result of the global economic crisis. Consumer inflation is widely expected to steadily decline with easing commodity prices. After peaking in 2007 at 7.2 per cent, the International Monetary Fund has forecast economic growth to decline to 4.6 per cent in 2008 and drop to less than one per cent in 2010.

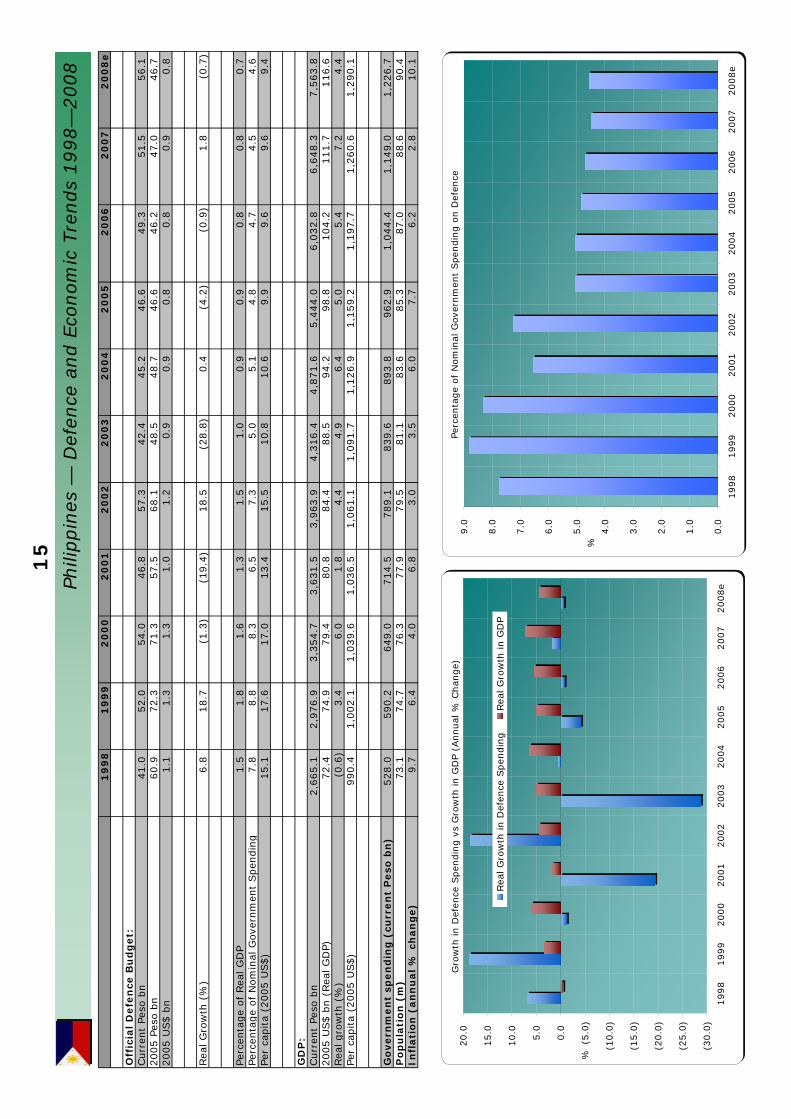

Defence spending

The Armed Forces of the Philippines (AFP) 2008 budget is about 56.1bn Peso, or aboutUS$1.3bn in current terms and represents about 0.8 per cent of real GDP – a 0.7 per cent real decrease on the 2007 defence budget. Personnel costs consume over 70 per cent of thebudget. With operating costs accounting for about a further 25 per cent there is little fundingremaining for acquisition programs, which are aimed at enhancing the AFP’scounter-insurgency capability. At the end of 2008. the Philippines only had one of three C-130’s operational, with two C-130 aircraft being refurbished. South Korea donated 15 T-41 training jets to the Philippines in late 2008.

Formal Name Republika ng Pilipinas Capital City Manila Population 90.4 million Land Size 300 000 sq km Currency Philippine Peso Fiscal Year Calendar year Economy Less developed country with a market economy Industries Textiles, pharmaceuticals, chemicals, wood products, food processing, electronic

assembly, petroleum refining and fishing

17

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

e

Off

icia

l D

efe

nce

Bu

dg

et:

Curr

ent

S$ b

n7.2

7.3

7.4

7.8

8.2

8.3

8.7

9.3

10.1

10.6

10.8

2005 S

$ b

n7.7

8.0

7.8

8.3

8.8

8.9

8.9

9.3

9.9

10.1

9.8

2005 U

S$ b

n4.6

4.8

4.7

5.0

5.3

5.3

5.4

5.6

5.9

6.1

5.9

Rea

l G

row

th (

%)

16.1

3.6

(2.6

)6.3

6.4

1.0

0.4

3.7

6.7

2.7

(2.9

)

Perc

enta

ge

of

Rea

l G

DP

5.6

5.4

4.8

5.2

5.3

5.2

4.8

4.6

4.6

4.4

4.1

Perc

enta

ge

of

Nom

inal

Gove

rnm

ent

Spen

din

g28.1

27.3

25.6

27.9

29.0

27.9

28.5

23.1

22.5

23.0

18.8

Per

capita

(2005 U

S$)

1,1

81.5

1,2

15.0

1,1

63.5

1,2

02.6

1,2

67.6

1,2

97.7

1,2

86.2

1,3

02.8

1,3

47.5

1,3

27.8

1,2

66.9

GD

P:

Curr

ent

S$ b

n137.9

140.0

159.8

153.4

158.0

162.3

184.5

199.4

217.0

243.2

263.3

2005 U

S$ b

n (

Rea

l G

DP)

82.5

88.5

97.4

95.0

99.0

102.4

111.6

119.8

129.6

139.6

144.6

Rea

l gro

wth

(%

)(1

.4)

7.2

10.1

(2.4

)4.2

3.5

9.0

7.3

8.2

7.7

3.6

Per

capita

(2005 U

S$)

21,0

41.2

22,3

91.2

24,2

32.8

22,9

95.8

23,7

26.2

24,8

91.7

26,7

91.6

28,0

79.7

29,4

42.0

30,4

14.5

30,9

81.1

Go

vern

men

t sp

en

din

g (

curr

en

t S

$ b

n)

25.6

26.7

29.0

28.1

28.4

29.9

30.4

40.1

44.7

46.1

57.6

Po

pu

lati

on

(m

)3.9

4.0

4.0

4.1

4.2

4.1

4.2

4.3

4.4

4.6

4.7

Infl

ati

on

(an

nu

al

% c

han

ge)

(0.3

)0.0

1.3

1.0

(0.4

)0.5

1.7

0.5

1.0

2.1

6.5

Gro

wth

in D

efen

ce S

pen

din

g v

s G

row

th in G

DP

(Annual

% C

han

ge)

(5.0

)

0.0

5.0

10.0

15.0

20.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Rea

l G

row

th in D

efen

ce S

pen

din

gRea

l G

row

th in G

DP

Perc

enta

ge

of N

om

inal

Gove

rnm

ent

Spen

din

g o

n D

efen

ce

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Sin

gap

ore

— D

efen

ce a

nd E

conom

ic T

rends

1998—

2008

18

Singapore

Singapore's Official Defence Funding in Real Dollars

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

US$bn (

2005)

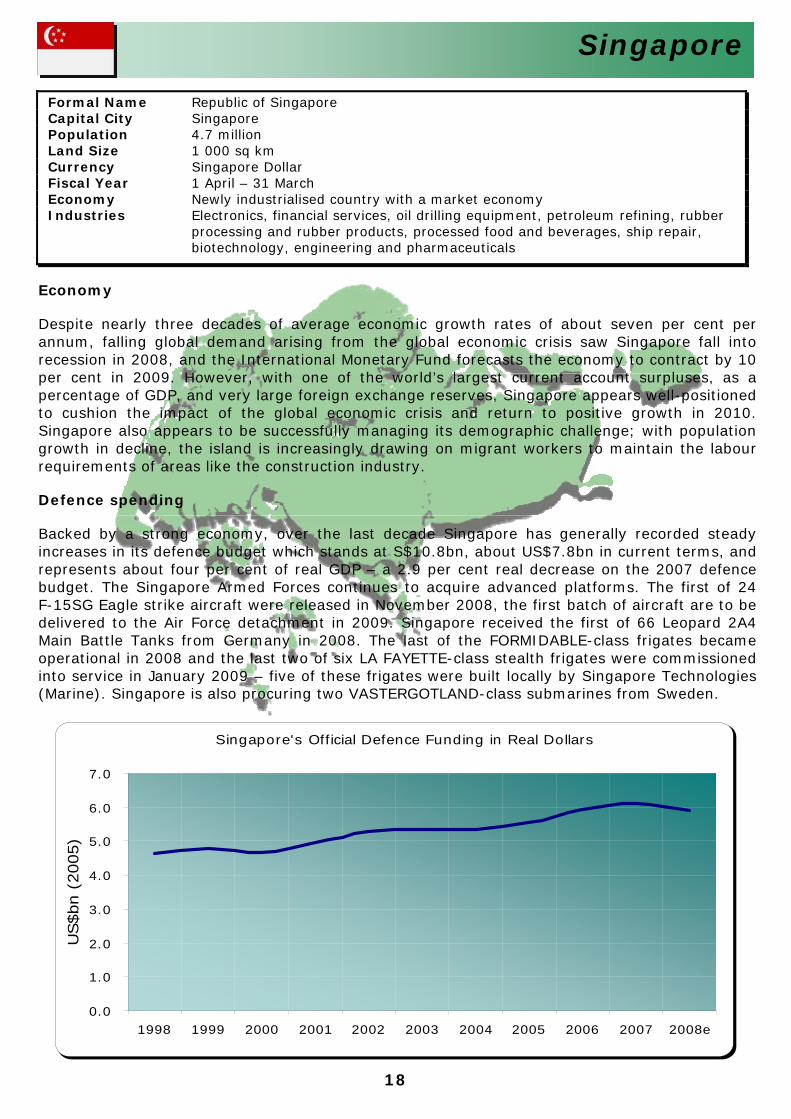

Economy

Despite nearly three decades of average economic growth rates of about seven per cent perannum, falling global demand arising from the global economic crisis saw Singapore fall into recession in 2008, and the International Monetary Fund forecasts the economy to contract by 10per cent in 2009. However, with one of the world’s largest current account surpluses, as apercentage of GDP, and very large foreign exchange reserves, Singapore appears well-positioned to cushion the impact of the global economic crisis and return to positive growth in 2010. Singapore also appears to be successfully managing its demographic challenge; with populationgrowth in decline, the island is increasingly drawing on migrant workers to maintain the labour requirements of areas like the construction industry.

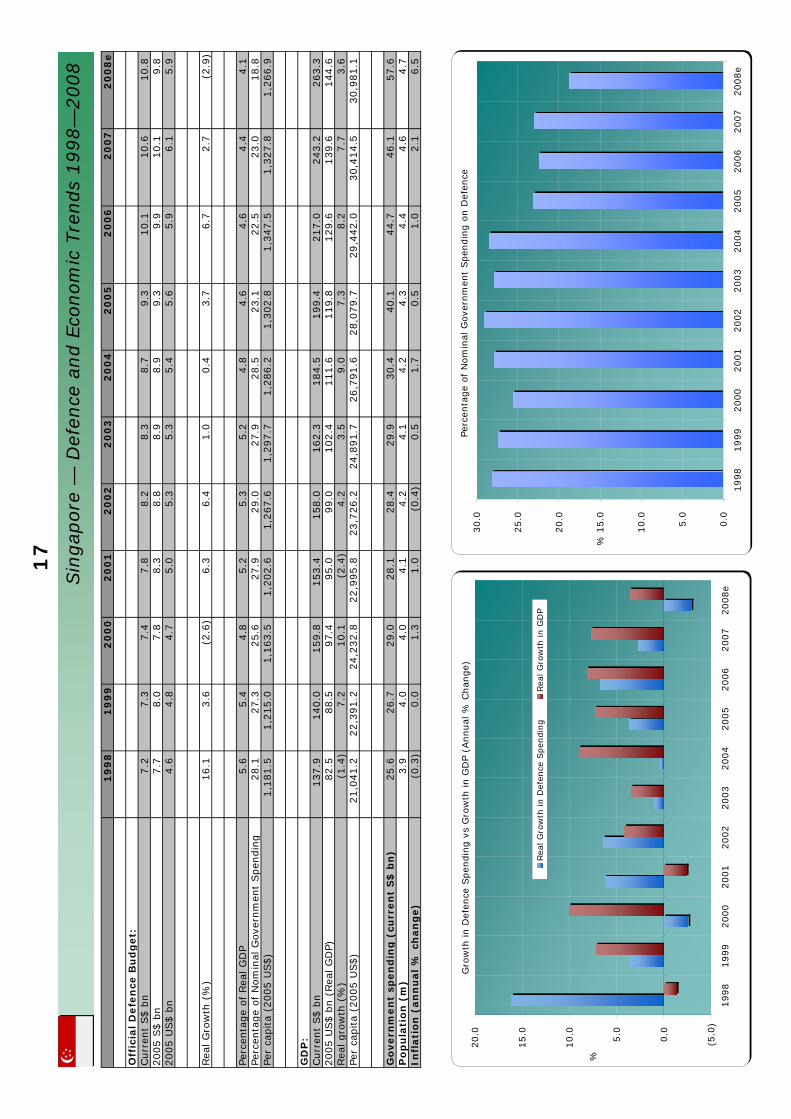

Defence spending

Backed by a strong economy, over the last decade Singapore has generally recorded steady increases in its defence budget which stands at S$10.8bn, about US$7.8bn in current terms, and represents about four per cent of real GDP – a 2.9 per cent real decrease on the 2007 defence budget. The Singapore Armed Forces continues to acquire advanced platforms. The first of 24F-15SG Eagle strike aircraft were released in November 2008, the first batch of aircraft are to be delivered to the Air Force detachment in 2009. Singapore received the first of 66 Leopard 2A4 Main Battle Tanks from Germany in 2008. The last of the FORMIDABLE-class frigates became operational in 2008 and the last two of six LA FAYETTE-class stealth frigates were commissioned into service in January 2009 – five of these frigates were built locally by Singapore Technologies(Marine). Singapore is also procuring two VASTERGOTLAND-class submarines from Sweden.

Formal Name Republic of Singapore Capital City Singapore Population 4.7 million Land Size 1 000 sq km Currency Singapore Dollar Fiscal Year 1 April – 31 March Economy Newly industrialised country with a market economy Industries Electronics, financial services, oil drilling equipment, petroleum refining, rubber

processing and rubber products, processed food and beverages, ship repair, biotechnology, engineering and pharmaceuticals

19

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

e

Off

icia

l D

efe

nce

Bu

dg

et:

Curr

ent

Bah

t bn

81.0

77.4

77.3

77.2

78.5

79.9

78.5

81.2

86.0

115.0

143.5

2005 B

aht

bn

93.2

91.8

89.7

87.8

88.4

88.0

83.1

81.2

81.5

105.9

125.8

2005 U

S$ b

n2.3

2.3

2.2

2.2

2.2

2.2

2.1

2.0

2.0

2.6

3.1

Rea

l G

row

th (

%)

(19.7

)(1

.6)

(2.2

)(2

.1)

0.7

(0.4

)(5

.6)

(2.3

)0.4

29.9

18.8

Perc

enta

ge

of

Rea

l G

DP

1.8

1.7

1.6

1.6

1.5

1.4

1.2

1.1

1.1

1.4

1.5

Perc

enta

ge

of

Nom

inal

Gove

rnm

ent

Spen

din

g7.7

6.7

8.7

8.5

7.7

8.0

7.6

6.8

6.3

7.3

8.6

Per

capita

(2005 U

S$)

37.9

36.9

35.8

34.7

34.6

34.2

31.8

31.0

31.0

40.0

47.1

GD

P:

Curr

ent

Bah

t bn

4,6

26.4

4,6

37.1

4,9

22.7

5,1

33.5

5,4

50.6

5,9

17.4

6,4

89.5

7,0

95.6

7,8

30.3

8,4

69.1

9,1

76.3

2005 U

S$ b

n (

Rea

l G

DP)

125.8

131.4

137.7

140.7

148.1

158.7

168.8

176.4

185.4

194.2

203.4

Rea

l gro

wth

(%

)(1

5.3

)4.4

4.7

2.2

5.3

7.1

6.3

4.5

5.1

4.8

4.7

Per

capita

(2005 U

S$)

2,0

57.1

2,1

27.4

2,2

06.3

2,2

34.9

2,3

34.3

2,4

79.6

2,5

93.4

2,7

09.6

2,8

40.5

2,9

54.7

3,0

63.9

Go

vern

men

t sp

en

din

g (

curr

en

t B

ah

t b

n)

1,0

51.7

1,1

60.2

884.4

910.0

1,0

23.0

999.9

1,0

28.0

1,2

00.0

1,3

60.0

1,5

66.2

1,6

60.0

Po

pu

lati

on

(m

)61.2

61.8

62.4

62.9

63.5

64.0

65.1

65.1

65.3

65.7

66.4

Infl

ati

on

(an

nu

al

% c

han

ge)

8.1

0.3

1.6

1.7

0.6

1.8

2.8

4.5

4.6

2.2

5.7

Gro

wth

in D

efen

ce S

pen

din

g v

s G

row

th in G

DP

(Annual

% C

han

ge)

(20.0

)

(15.0

)

(10.0

)

(5.0

)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Rea

l G

row

th in D

efen

ce S

pen

din

gRea

l G

row

th in G

DP

Perc

enta

ge

of N

om

inal

Gove

rnm

ent

Spen

din

g o

n D

efen

ce

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Thai

land —

Def

ence

and E

conom

ic T

rends

1998—

2008

20

Thailand

Thailand's Official Defence Funding in Real Dollars

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

US$bn

(2005)

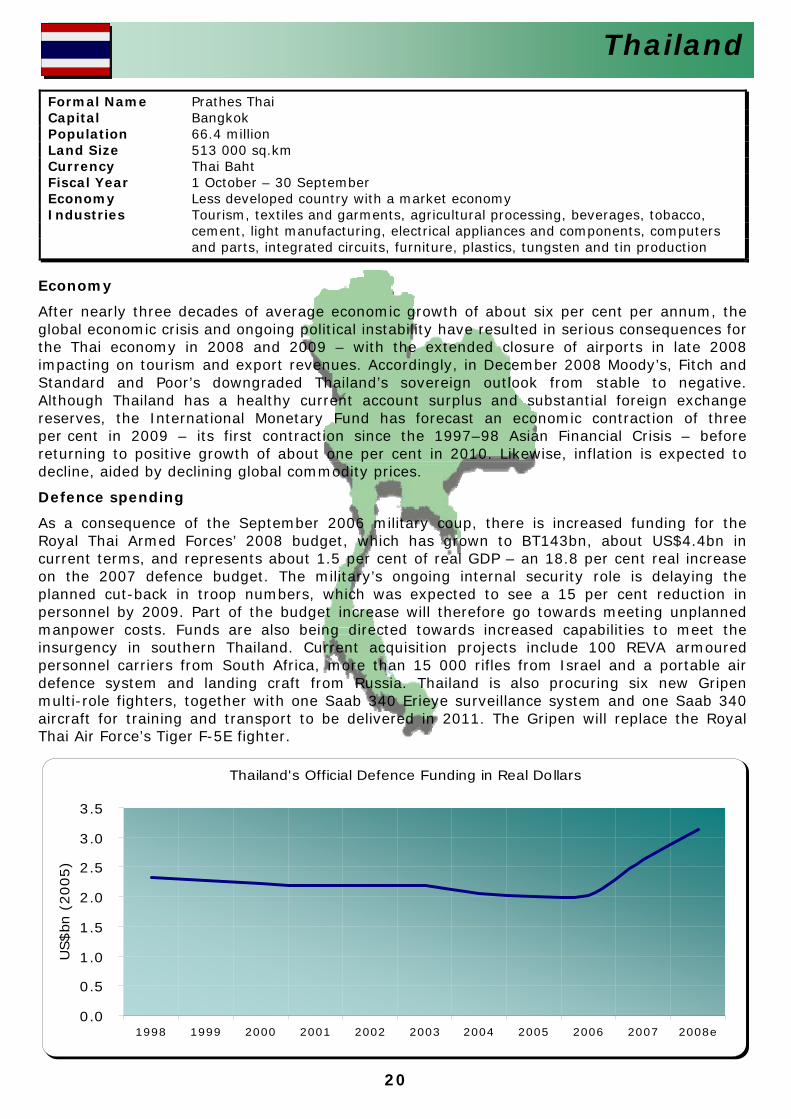

Economy

After nearly three decades of average economic growth of about six per cent per annum, theglobal economic crisis and ongoing political instability have resulted in serious consequences forthe Thai economy in 2008 and 2009 – with the extended closure of airports in late 2008impacting on tourism and export revenues. Accordingly, in December 2008 Moody’s, Fitch and Standard and Poor’s downgraded Thailand’s sovereign outlook from stable to negative.Although Thailand has a healthy current account surplus and substantial foreign exchangereserves, the International Monetary Fund has forecast an economic contraction of three per cent in 2009 – its first contraction since the 1997–98 Asian Financial Crisis – before returning to positive growth of about one per cent in 2010. Likewise, inflation is expected to decline, aided by declining global commodity prices.

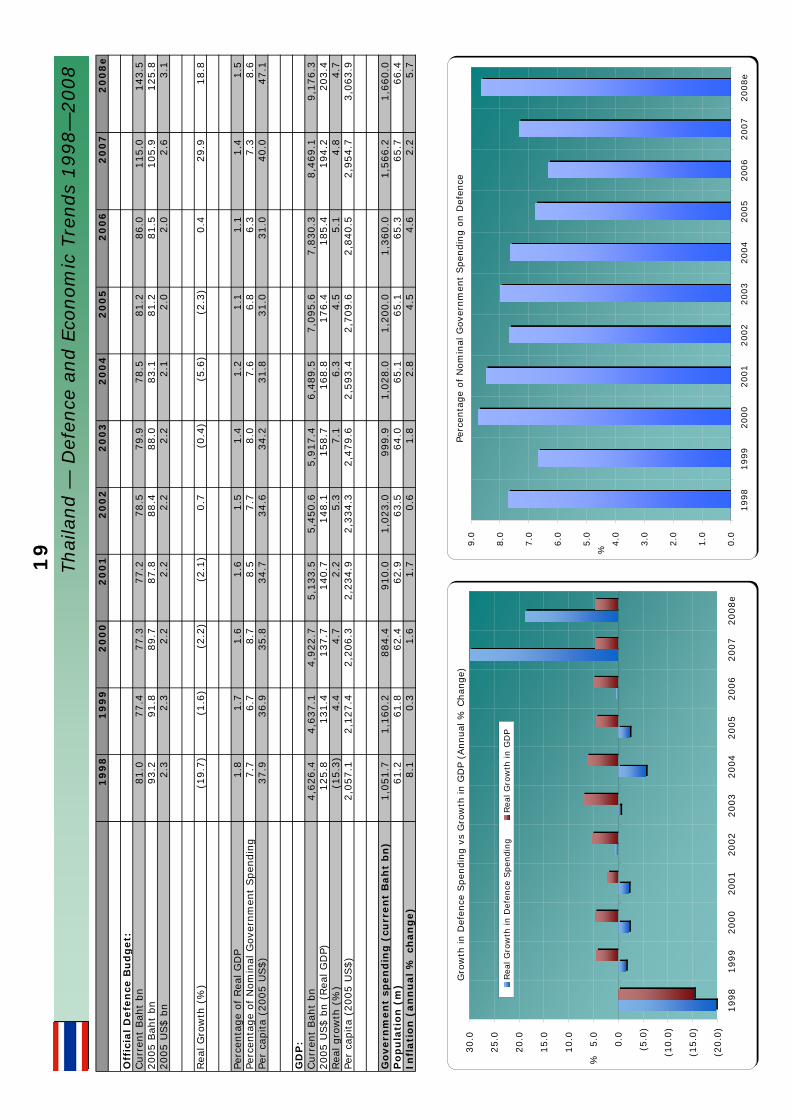

Defence spending

As a consequence of the September 2006 military coup, there is increased funding for the Royal Thai Armed Forces’ 2008 budget, which has grown to BT143bn, about US$4.4bn in current terms, and represents about 1.5 per cent of real GDP – an 18.8 per cent real increase on the 2007 defence budget. The military’s ongoing internal security role is delaying the planned cut-back in troop numbers, which was expected to see a 15 per cent reduction inpersonnel by 2009. Part of the budget increase will therefore go towards meeting unplannedmanpower costs. Funds are also being directed towards increased capabilities to meet the insurgency in southern Thailand. Current acquisition projects include 100 REVA armoured personnel carriers from South Africa, more than 15 000 rifles from Israel and a portable air defence system and landing craft from Russia. Thailand is also procuring six new Gripen multi-role fighters, together with one Saab 340 Erieye surveillance system and one Saab 340aircraft for training and transport to be delivered in 2011. The Gripen will replace the Royal Thai Air Force’s Tiger F-5E fighter.

Formal Name Prathes Thai Capital Bangkok Population 66.4 million Land Size 513 000 sq.km Currency Thai Baht Fiscal Year 1 October – 30 September Economy Less developed country with a market economy Industries Tourism, textiles and garments, agricultural processing, beverages, tobacco,

cement, light manufacturing, electrical appliances and components, computers and parts, integrated circuits, furniture, plastics, tungsten and tin production

21

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

e

Defe

nce

Bu

dg

et

Est

imate

:Curr

ent

Dông b

n22,4

50.0

25,4

45.1

32,6

88.3

38,9

31.9

34,0

19.0

35,8

80.0

43,7

63.0

50,0

00.0

55,0

00.0

60,0

00.0

77,2

98.7

2005 D

ông b

n30,4

58.9

32,9

17.4

41,9

60.6

49,6

07.2

41,7

00.2

41,9

15.6

47,3

60.1

50,0

00.0

51,2

18.6

51,6

05.9

54,0

00.6

2005 U

S$ b

n1.9

2.1

2.6

3.1

2.6

2.6

3.0

3.2

3.2

3.3

3.4

Rea

l G

row

th (

%)

(20.3

)8.1

27.5

18.2

(15.9

)0.5

13.0

5.6

2.4

0.8

4.6

Perc

enta

ge

of

Rea

l G

DP

6.2

6.4

7.4

8.1

6.4

5.8

6.1

6.0

5.6

5.2

5.2

Perc

enta

ge

of

Nom

inal

Gove

rnm

ent

Spen

din

g30.0

30.0

30.0

30.0

23.0

19.8

20.4

19.0

17.9

14.2

16.8

Per

capita

(2005 U

S$)

25.5

27.1

34.1

39.8

33.0

32.7

36.4

37.9

38.3

38.0

39.2

GD

P:

Curr

ent

Dông b

n361,0

16.0

399,9

42.0

441,6

46.0

481,2

95.0

535,4

89.3

613,4

42.9

715,3

07.0

839,2

11.3

974,2

66.2

1,1

44,0

14.7

1,4

86,5

14.3

2005 U

S$ b

n (

Rea

l G

DP)

30.9

32.6

35.7

38.7

41.4

45.2

48.8

52.9

57.2

62.0

65.5

Rea

l gro

wth

(%

)6.3

5.6

9.6

8.2

7.0

9.2

8.0

8.4

8.1

8.5

5.5

Per

capita

(2005 U

S$)

409.3

425.9

460.5

491.4

519.1

558.6

595.0

635.9

677.8

724.9

754.5

Go

vern

men

t sp

en

din

g (

curr

en

t D

ôn

g b

n)

74,7

61.0

84,8

17.0

108,9

61.0

129,7

73.0

148,2

08.0

181,1

83.0

214,1

76.0

262,6

97.0

308,0

58.0

422,9

90.0

459,4

78.0

Po

pu

lati

on

(m

)75.5

76.6

77.6

78.7

79.7

80.9

82.0

83.2

84.4

85.6

86.8

Infl

ati

on

(an

nu

al

% c

han

ge)

7.9

4.1

(1.6

)(0

.4)

4.0

3.2

7.7

8.3

7.5

8.3

24.0

.

Gro

wth

in D

efen

ce S

pen

din

g v

s G

row

th in G

DP

(Annual

% C

han

ge)

(30.0

)

(20.0

)

(10.0

)

0.0

10.0

20.0

30.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Rea

l G

row

th in D

efen

ce S

pen

din

gRea

l G

row

th in G

DP

Perc

enta

ge

of N

om

inal

Gove

rnm

ent

Spen

din

g o

n D

efen

ce

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008e

%

Vie

tnam

— D

efen

ce a

nd E

conom

ic T

rends

1998—

2008

22

Vietnam

Vietnam's Official Defence Funding in Real Dollars

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008e

US$bn

(2005)

Economy

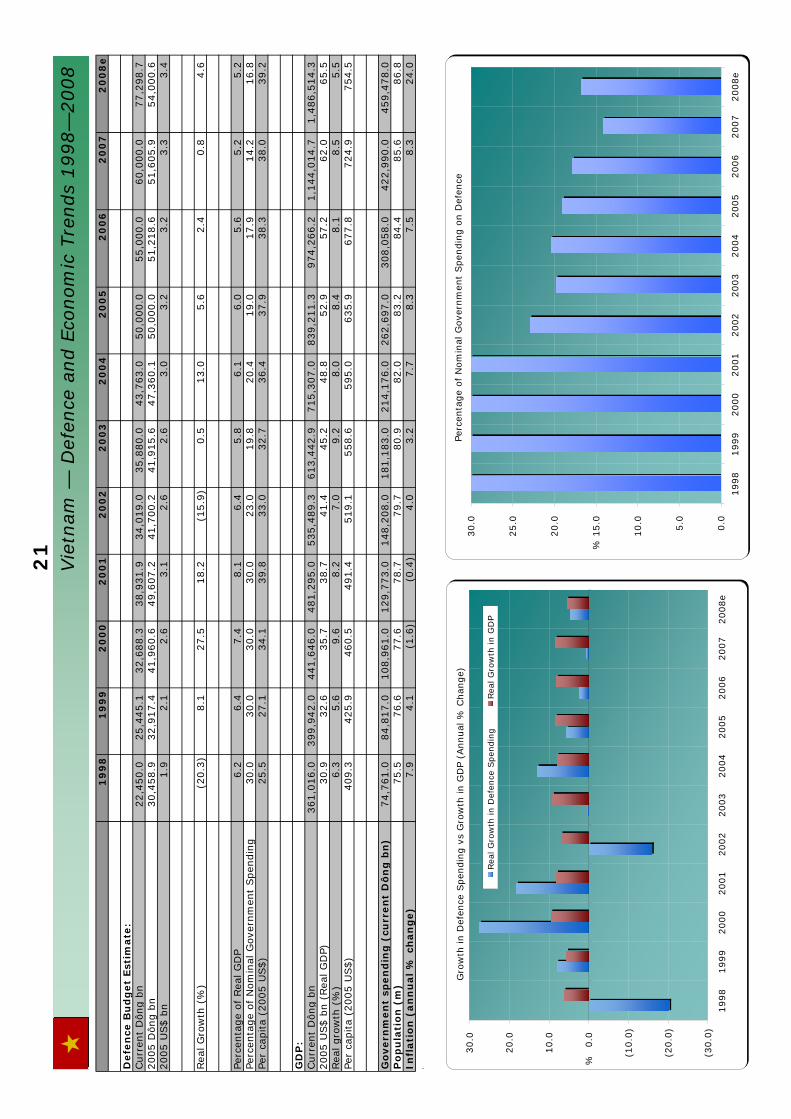

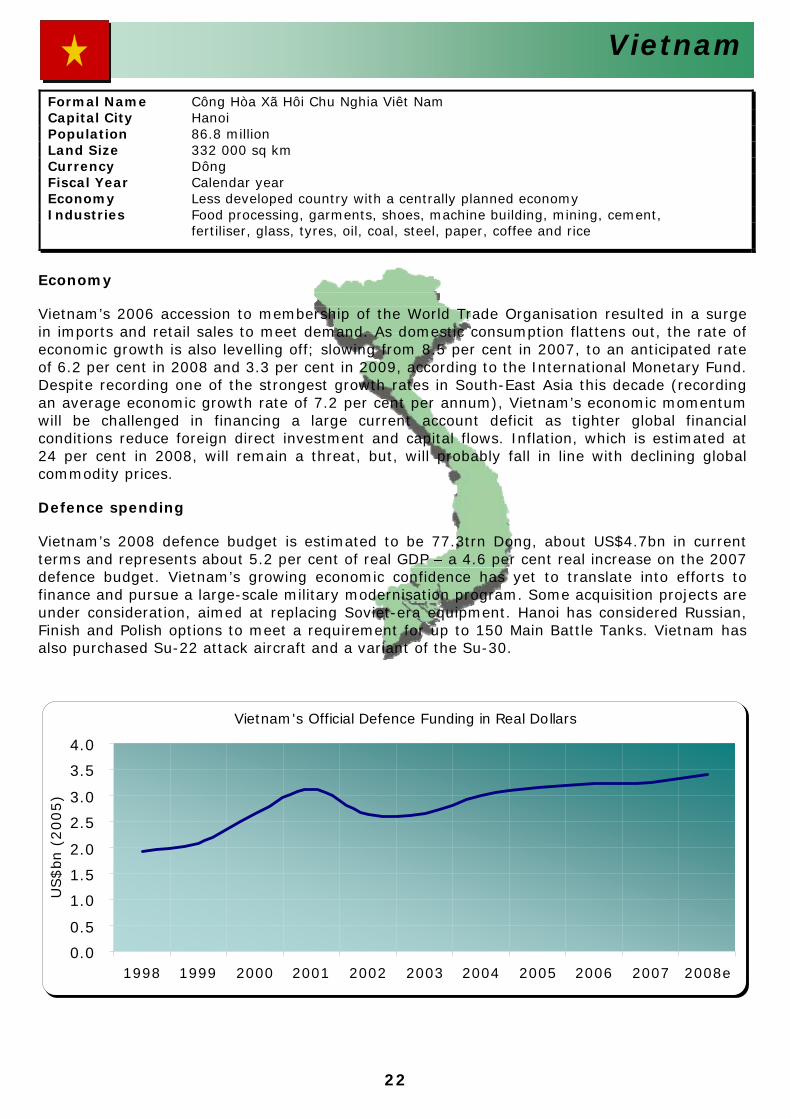

Vietnam’s 2006 accession to membership of the World Trade Organisation resulted in a surgein imports and retail sales to meet demand. As domestic consumption flattens out, the rate of economic growth is also levelling off; slowing from 8.5 per cent in 2007, to an anticipated rate of 6.2 per cent in 2008 and 3.3 per cent in 2009, according to the International Monetary Fund. Despite recording one of the strongest growth rates in South-East Asia this decade (recording an average economic growth rate of 7.2 per cent per annum), Vietnam’s economic momentum will be challenged in financing a large current account deficit as tighter global financialconditions reduce foreign direct investment and capital flows. Inflation, which is estimated at 24 per cent in 2008, will remain a threat, but, will probably fall in line with declining global commodity prices.

Defence spending

Vietnam’s 2008 defence budget is estimated to be 77.3trn Dong, about US$4.7bn in current terms and represents about 5.2 per cent of real GDP – a 4.6 per cent real increase on the 2007 defence budget. Vietnam’s growing economic confidence has yet to translate into efforts tofinance and pursue a large-scale military modernisation program. Some acquisition projects are under consideration, aimed at replacing Soviet-era equipment. Hanoi has considered Russian, Finish and Polish options to meet a requirement for up to 150 Main Battle Tanks. Vietnam has also purchased Su-22 attack aircraft and a variant of the Su-30.

Formal Name Công Hòa Xã Hôi Chu Nghia Viêt Nam Capital City Hanoi Population 86.8 million Land Size 332 000 sq km Currency Dông Fiscal Year Calendar year Economy Less developed country with a centrally planned economy Industries Food processing, garments, shoes, machine building, mining, cement,

fertiliser, glass, tyres, oil, coal, steel, paper, coffee and rice

23

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

e

Off

icia

l D

efe

nce

Bu

dg

et:

Curr

ent

US$ m

n/a

n/a

n/a

n/a

n/a

6.1

6.0

9.8

24.4

18.4

23.7

2005 U

S$ m

n/a

n/a

n/a

n/a

n/a

6.2

6.1

9.8

23.4

16.3

20.1

Rea

l G

row

th (

%)

n/a

n/a

n/a

n/a

n/a

n/a

(2.5

)61.2

138.9

(30.1

)23.2

Perc

enta

ge

of

Rea

l G

DP

n/a

n/a

n/a

n/a

n/a

1.8

1.8

2.8

6.9

4.0

4.8

Perc

enta

ge

of

Nom

inal

Gove

rnm

ent

Spen

din

gn/a

n/a

n/a

n/a

n/a

7.6

7.2

7.4

8.4

7.9

3.0

Per

capita

(2005 U

S$)

n/a

n/a

n/a

n/a

n/a

6,7

27.0

6,3

40.0

9,9

08.8

23,0

14.9

15,6

76.8

18,8

79.2

GD

P:

Curr

ent

US$m

n/a

274.0

316.0

368.0

343.0

336.0

339.0

350.0

353.0

459.0

489.0

2005 U

S$m

(Rea

l G

DP)

n/a

293.6

333.9

389.4

363.1

341.2

342.4

350.0

337.8

405.4

414.6

Rea

l gro

wth

(%

)n/a

n/a

13.7

16.6

(6.8

)(6

.0)

0.4

2.2

(3.5

)20.0

2.3

Per

capita

(2005 U

S$)

n/a

372.6

405.7

454.9

407.5

368.8

357.8

354.6

332.8

389.5

389.3

Go

vern

men

t sp

en

din

g (

curr

en

t U

S$

bn

)n/a

n/a

n/a

n/a

n/a

0.1

0.1

0.1

0.3

0.2

0.8

Po

pu

lati

on

(m

)n/a

0.8

0.8

0.9

0.9

0.9

1.0

1.0

1.0

1.0

1.1

Infl

ati

on

(an

nu

al

% c

han

ge)

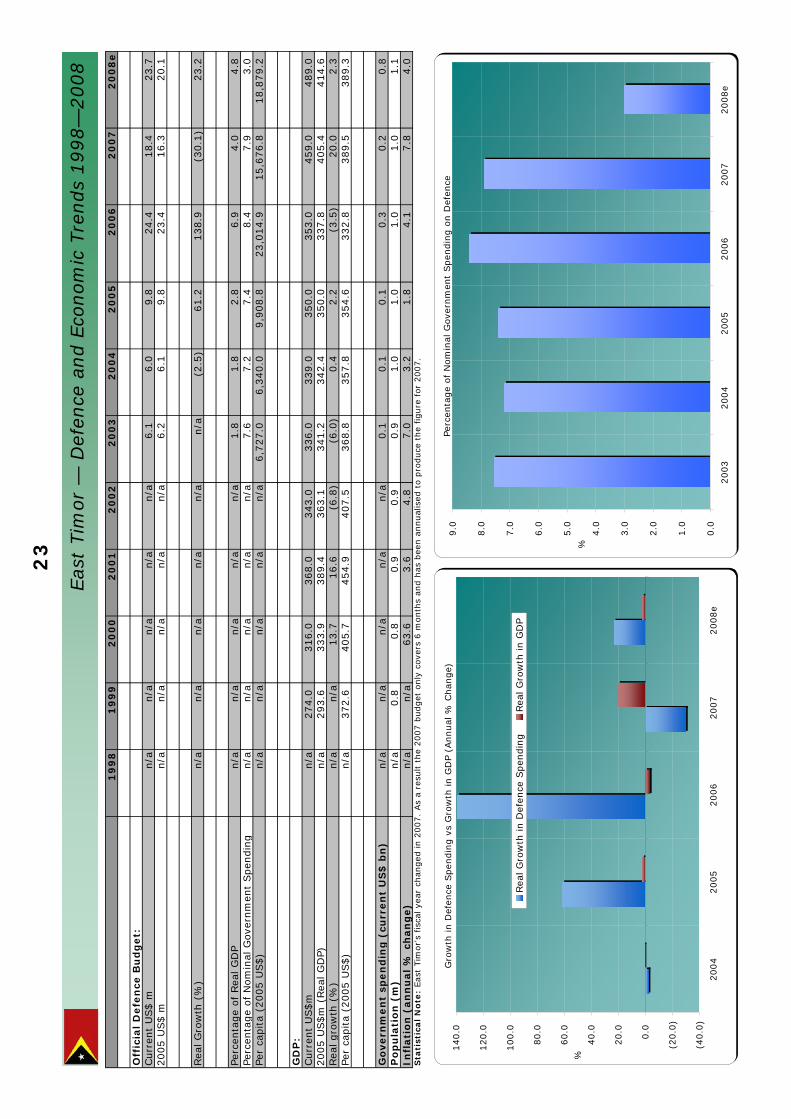

n/a

n/a

63.6

3.6

4.8

7.0

3.2

1.8

4.1

7.8

4.0

Sta

tist

ical

No

te:

Eas

t Tim

or's

fisc

al y

ear

chan

ged

in 2

007.

As

a re

sult t

he

2007 b

udget

only

cove

rs 6

month

s an

d h

as b

een a

nnual

ised

to p