Embed Size (px)

Citation preview

182

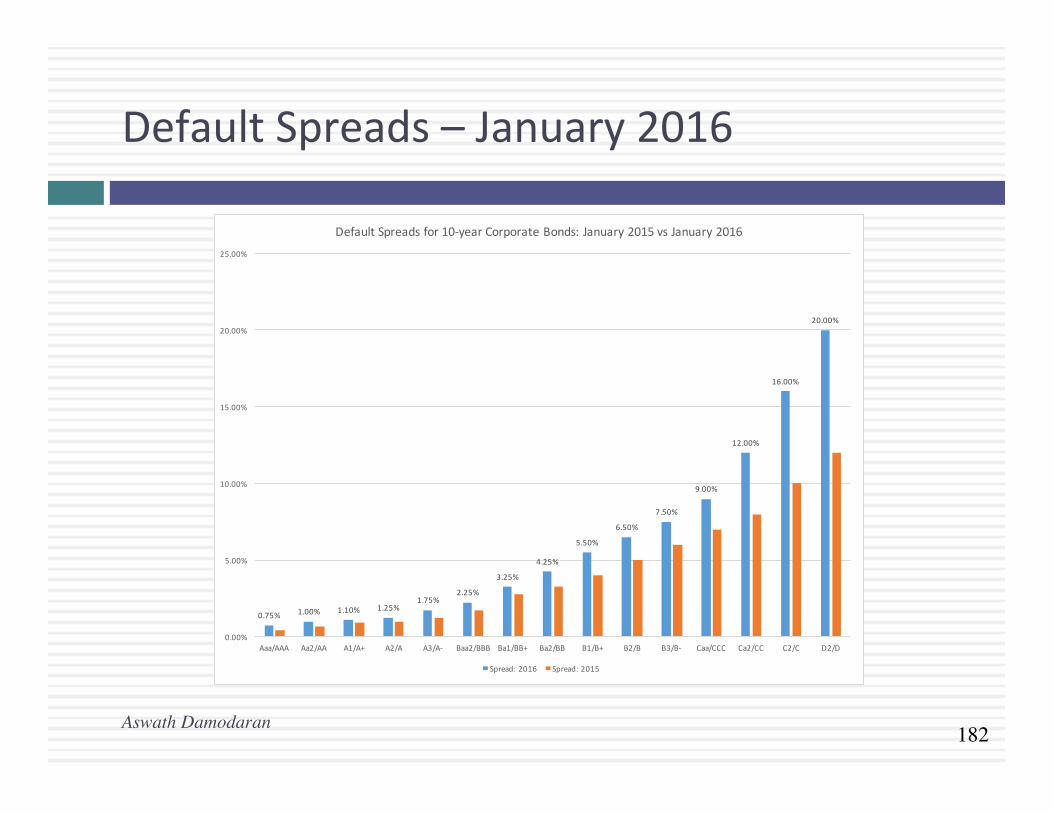

DefaultSpreads–January2016

Aswath Damodaran

0.75% 1.00% 1.10% 1.25%1.75%

2.25%

3.25%

4.25%

5.50%

6.50%

7.50%

9.00%

12.00%

16.00%

20.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Aaa/AAA Aa2/AA A1/A+ A2/A A3/A- Baa2/BBB Ba1/BB+ Ba2/BB B1/B+ B2/B B3/B- Caa/CCC Ca2/CC C2/C D2/D

DefaultSpreadsfor10-yearCorporateBonds:January2015vsJanuary2016

Spread:2016 Spread:2015

183

Applica9onTest:Es9ma9ngaCostofDebt

AswathDamodaran

183

¨ Baseduponyourfirm’scurrentearningsbeforeinterestandtaxes,itsinterestexpenses,es9mate¤ Aninterestcoveragera9oforyourfirm¤ Asynthe9cra9ngforyourfirm(usethetablesfrompriorpages)

¤ Apre-taxcostofdebtforyourfirm¤ AnaKer-taxcostofdebtforyourfirm

184

CostsofHybrids

AswathDamodaran

184

¨ Preferredstocksharessomeofthecharacteris9csofdebt-thepreferreddividendispre-specifiedatthe9meoftheissueandispaidoutbeforecommondividend--andsomeofthecharacteris9csofequity-thepaymentsofpreferreddividendarenottaxdeduc9ble.Ifpreferredstockisviewedasperpetual,thecostofpreferredstockcanbewriSenasfollows:¤ kps=PreferredDividendpershare/MarketPriceperpreferredshare

¨ Conver9bledebtispartdebt(thebondpart)andpartequity(theconversionop9on).Itisbesttobreakitupintoitscomponentpartsandeliminateitfromthemixaltogether.

185

WeightsforCostofCapitalCalcula9on

AswathDamodaran

185

¨ Theweightsusedinthecostofcapitalcomputa9onshouldbemarketvalues.

¨ Therearethreespeciousargumentsusedagainstmarketvalue¤ Bookvalueismorereliablethanmarketvaluebecauseitisnotas

vola9le:Whileitistruethatbookvaluedoesnotchangeasmuchasmarketvalue,thisismoreareflec9onofweaknessthanstrength

¤ Usingbookvalueratherthanmarketvalueisamoreconserva9veapproachtoes9ma9ngdebtra9os:Formostcompanies,usingbookvalueswillyieldalowercostofcapitalthanusingmarketvalueweights.

¤ Sinceaccoun9ngreturnsarecomputedbaseduponbookvalue,consistencyrequirestheuseofbookvalueincompu9ngcostofcapital:Whileitmayseemconsistenttousebookvaluesforbothaccoun9ngreturnandcostofcapitalcalcula9ons,itdoesnotmakeeconomicsense.

186

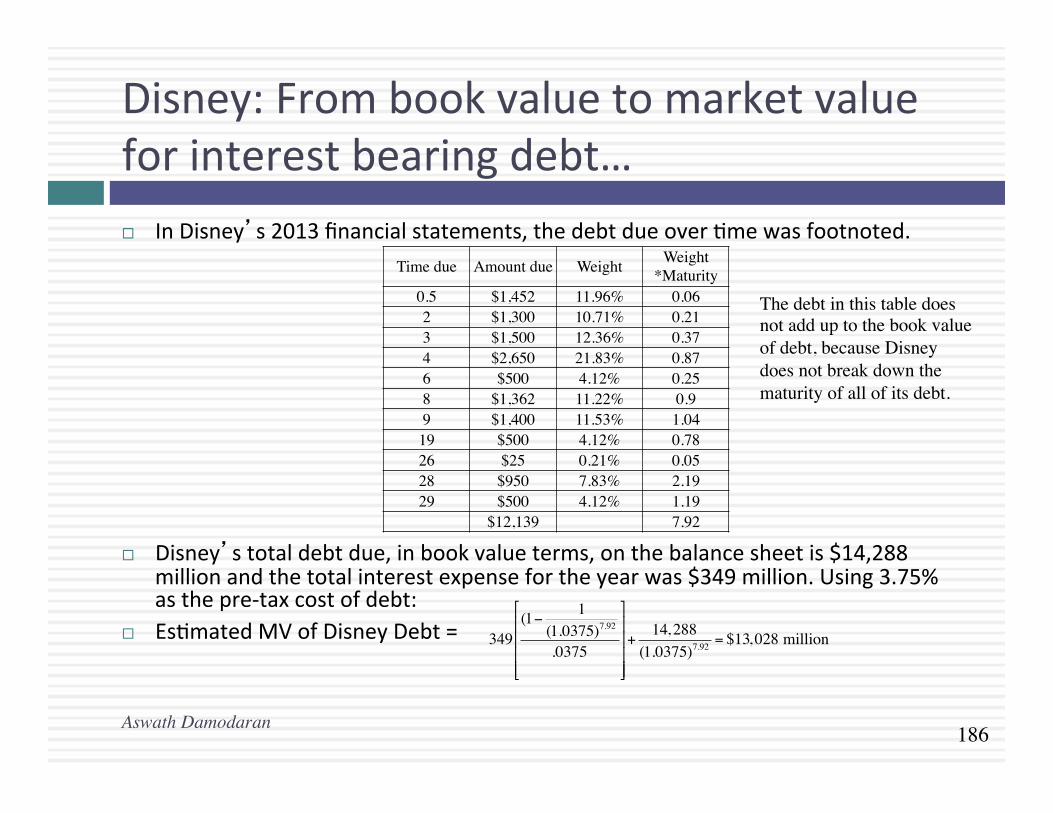

Disney:Frombookvaluetomarketvalueforinterestbearingdebt…¨ InDisney’s2013financialstatements,thedebtdueover9mewasfootnoted.

¨ Disney’stotaldebtdue,inbookvalueterms,onthebalancesheetis$14,288millionandthetotalinterestexpensefortheyearwas$349million.Using3.75%asthepre-taxcostofdebt:

¨ Es9matedMVofDisneyDebt=

Aswath Damodaran

Time due Amount due Weight Weight *Maturity

0.5 $1,452 11.96% 0.062 $1,300 10.71% 0.213 $1,500 12.36% 0.374 $2,650 21.83% 0.876 $500 4.12% 0.258 $1,362 11.22% 0.99 $1,400 11.53% 1.0419 $500 4.12% 0.7826 $25 0.21% 0.0528 $950 7.83% 2.1929 $500 4.12% 1.19 $12,139 7.92

349(1− 1

(1.0375)7.92

.0375

"

#

$$$$

%

&

''''

+14, 288

(1.0375)7.92 = $13, 028 million

The debt in this table does not add up to the book value of debt, because Disney does not break down the maturity of all of its debt.

187

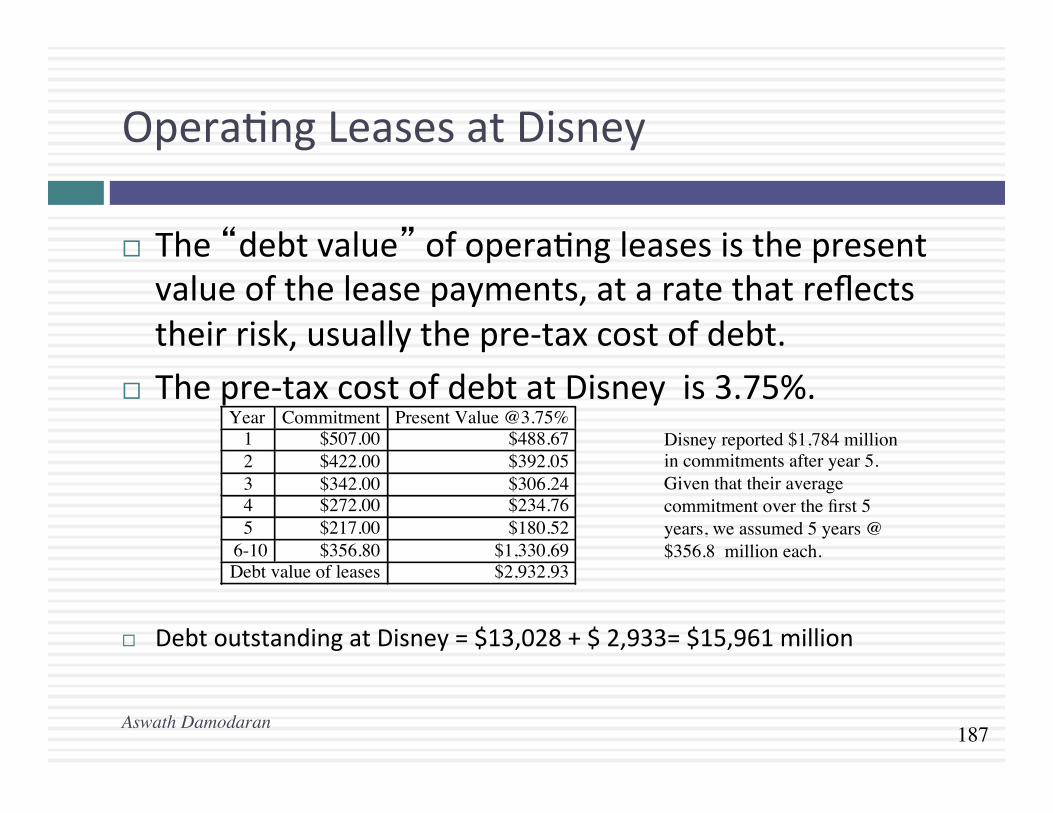

Opera9ngLeasesatDisney

¨ The“debtvalue”ofopera9ngleasesisthepresentvalueoftheleasepayments,ataratethatreflectstheirrisk,usuallythepre-taxcostofdebt.

¨ Thepre-taxcostofdebtatDisneyis3.75%.

¨ DebtoutstandingatDisney=$13,028+$2,933=$15,961million

Disney reported $1,784 million in commitments after year 5. Given that their average commitment over the first 5 years, we assumed 5 years @ $356.8 million each.

Aswath Damodaran

Year Commitment Present Value @3.75% 1 $507.00 $488.67 2 $422.00 $392.05 3 $342.00 $306.24 4 $272.00 $234.76 5 $217.00 $180.52

6-10 $356.80 $1,330.69 Debt value of leases $2,932.93

188

Applica9onTest:Es9ma9ngMarketValue

AswathDamodaran

188

¨ Es9matethe¤ MarketvalueofequityatyourfirmandBookValueofequity

¤ Marketvalueofdebtandbookvalueofdebt(Ifyoucannotfindtheaveragematurityofyourdebt,use3years):Remembertocapitalizethevalueofopera9ngleasesandaddthemontoboththebookvalueandthemarketvalueofdebt.

¨ Es9matethe¤ Weightsforequityanddebtbaseduponmarketvalue¤ Weightsforequityanddebtbaseduponbookvalue

189

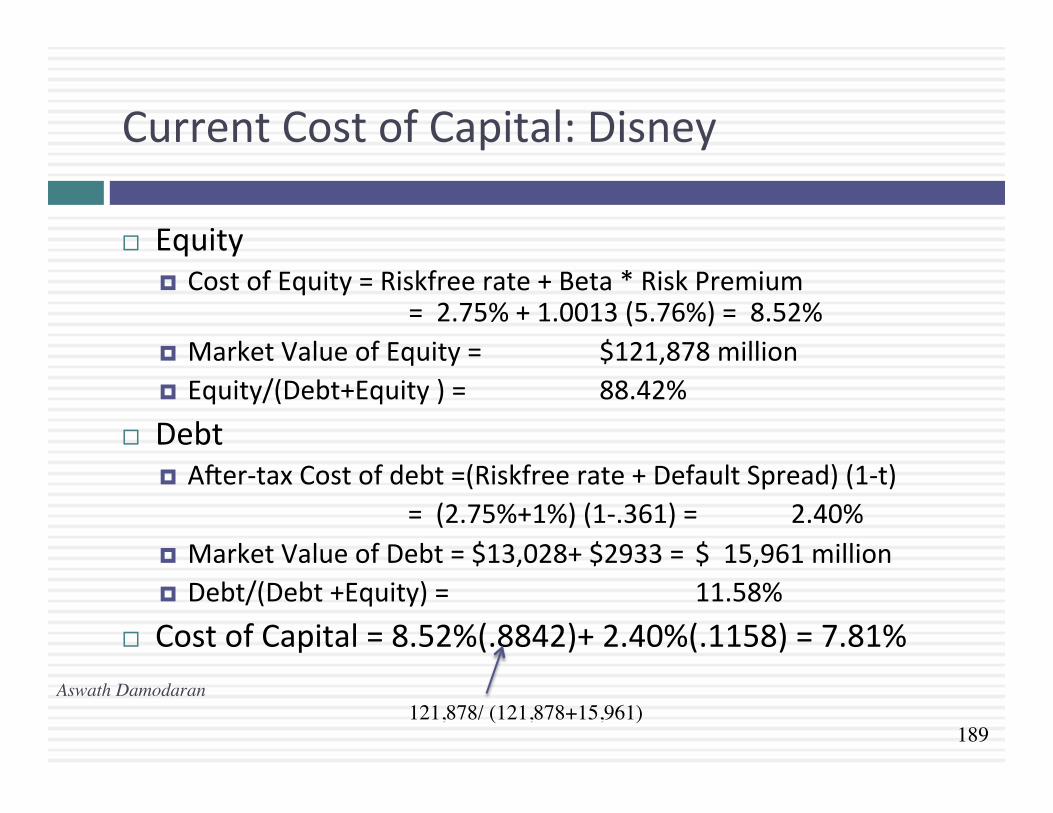

CurrentCostofCapital:Disney

¨ Equity¤ CostofEquity=Riskfreerate+Beta*RiskPremium

=2.75%+1.0013(5.76%)=8.52%¤ MarketValueofEquity= $121,878million¤ Equity/(Debt+Equity)= 88.42%

¨ Debt¤ AKer-taxCostofdebt=(Riskfreerate+DefaultSpread)(1-t)

=(2.75%+1%)(1-.361)= 2.40%¤ MarketValueofDebt=$13,028+$2933= $15,961million¤ Debt/(Debt+Equity)= 11.58%

¨ CostofCapital=8.52%(.8842)+2.40%(.1158)=7.81%

121,878/ (121,878+15,961)Aswath Damodaran

190

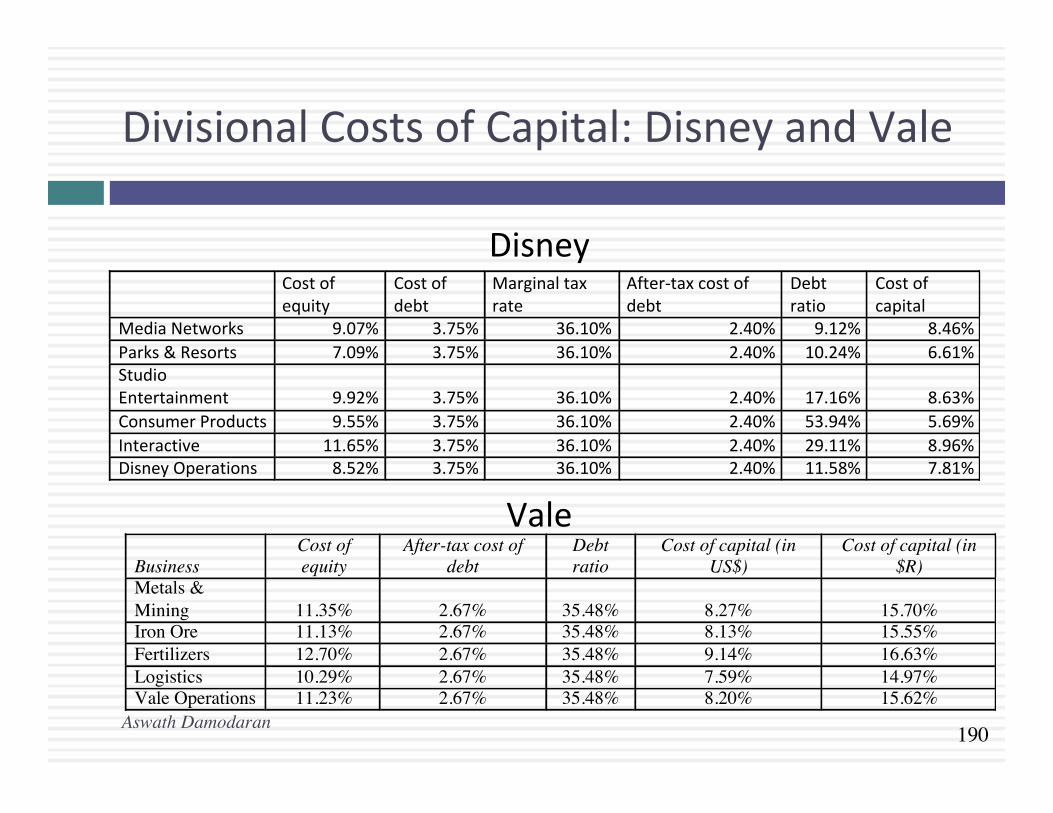

DivisionalCostsofCapital:DisneyandVale

Disney

Vale

Aswath Damodaran

!!Cost!of!equity!

Cost!of!debt!

Marginal!tax!rate!

After6tax!cost!of!debt!

Debt!ratio!

Cost!of!capital!

Media!Networks! 9.07%! 3.75%! 36.10%! 2.40%! 9.12%! 8.46%!Parks!&!Resorts! 7.09%! 3.75%! 36.10%! 2.40%! 10.24%! 6.61%!Studio!Entertainment! 9.92%! 3.75%! 36.10%! 2.40%! 17.16%! 8.63%!Consumer!Products! 9.55%! 3.75%! 36.10%! 2.40%! 53.94%! 5.69%!Interactive! 11.65%! 3.75%! 36.10%! 2.40%! 29.11%! 8.96%!Disney!Operations! 8.52%! 3.75%! 36.10%! 2.40%! 11.58%! 7.81%!

Business Cost of equity

After-tax cost of debt

Debt ratio

Cost of capital (in US$)

Cost of capital (in $R)

Metals & Mining 11.35% 2.67% 35.48% 8.27% 15.70% Iron Ore 11.13% 2.67% 35.48% 8.13% 15.55% Fertilizers 12.70% 2.67% 35.48% 9.14% 16.63% Logistics 10.29% 2.67% 35.48% 7.59% 14.97% Vale Operations 11.23% 2.67% 35.48% 8.20% 15.62%

191

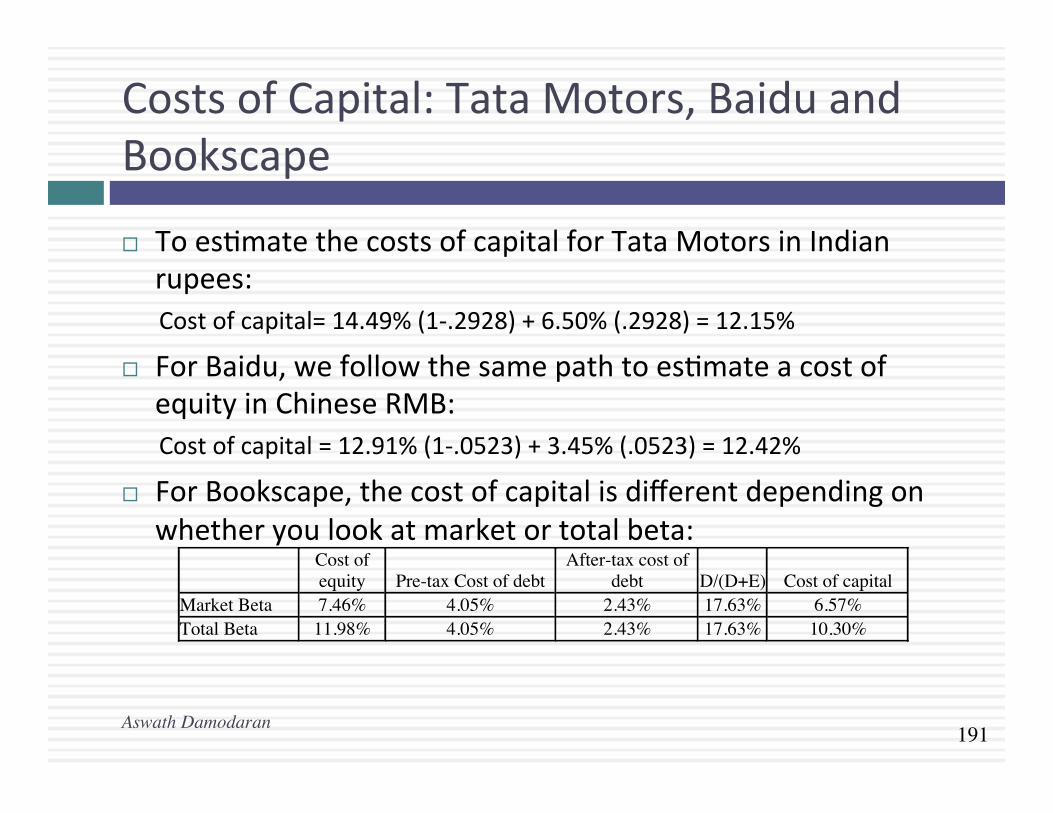

CostsofCapital:TataMotors,BaiduandBookscape

¨ Toes9matethecostsofcapitalforTataMotorsinIndianrupees:Costofcapital=14.49%(1-.2928)+6.50%(.2928)=12.15%

¨ ForBaidu,wefollowthesamepathtoes9mateacostofequityinChineseRMB:Costofcapital=12.91%(1-.0523)+3.45%(.0523)=12.42%

¨ ForBookscape,thecostofcapitalisdifferentdependingonwhetheryoulookatmarketortotalbeta:

Aswath Damodaran

Cost of equity Pre-tax Cost of debt

After-tax cost of debt D/(D+E) Cost of capital

Market Beta 7.46% 4.05% 2.43% 17.63% 6.57% Total Beta 11.98% 4.05% 2.43% 17.63% 10.30%

192

Applica9onTest:Es9ma9ngCostofCapital

AswathDamodaran

192

¨ UsingtheboSom-upunleveredbetathatyoucomputedforyourfirm,andthevaluesofdebtandequityyouhavees9matedforyourfirm,es9mateaboSom-upleveredbetaandcostofequityforyourfirm.

¨ Baseduponthecostsofequityanddebtthatyouhavees9mated,andtheweightsforeach,es9matethecostofcapitalforyourfirm.

¨ Howdifferentwouldyourcostofcapitalhavebeen,ifyouusedbookvalueweights?

193

ChoosingaHurdleRate

AswathDamodaran

193

¨ Eitherthecostofequityorthecostofcapitalcanbeusedasahurdlerate,dependinguponwhetherthereturnsmeasuredaretoequityinvestorsortoallclaimholdersonthefirm(capital)

¨ Ifreturnsaremeasuredtoequityinvestors,theappropriatehurdlerateisthecostofequity.

¨ Ifreturnsaremeasuredtocapital(orthefirm),theappropriatehurdlerateisthecostofcapital.

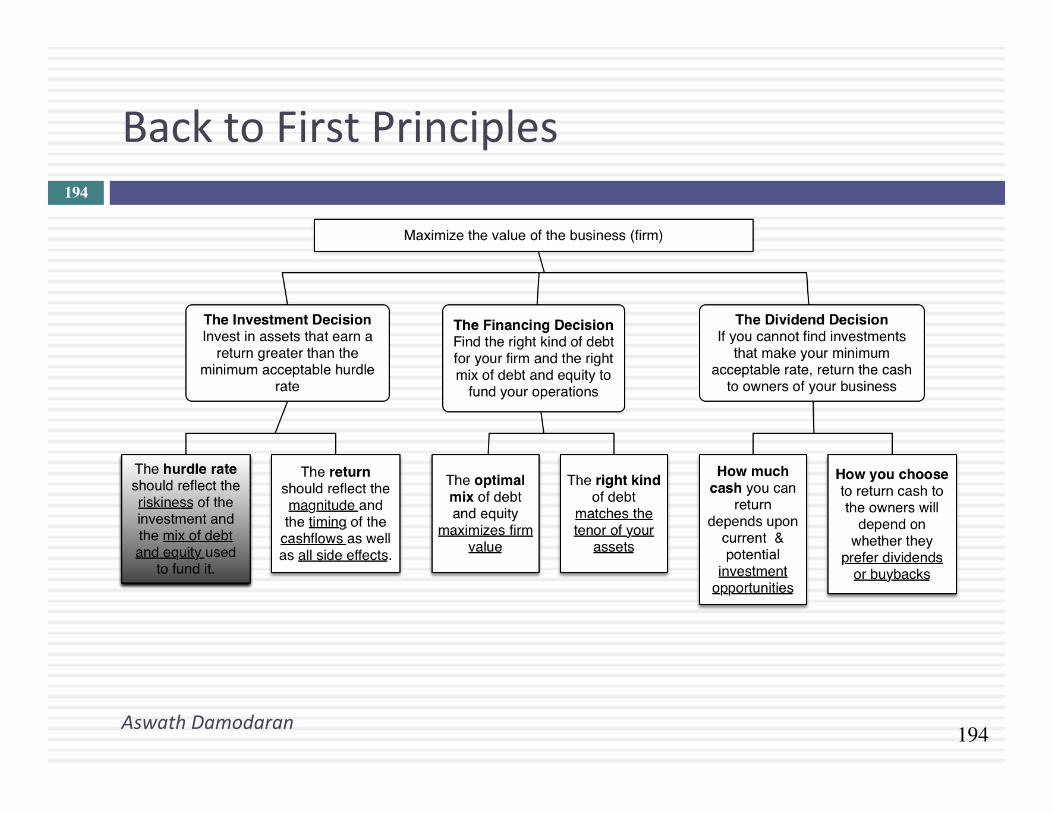

194

BacktoFirstPrinciples

AswathDamodaran

194

MEASURINGINVESTMENTRETURNSI:THEMECHANICSOFINVESTMENTANALYSIS“Showmethemoney”

fromJerryMaguire

AswathDamodaran 195

196

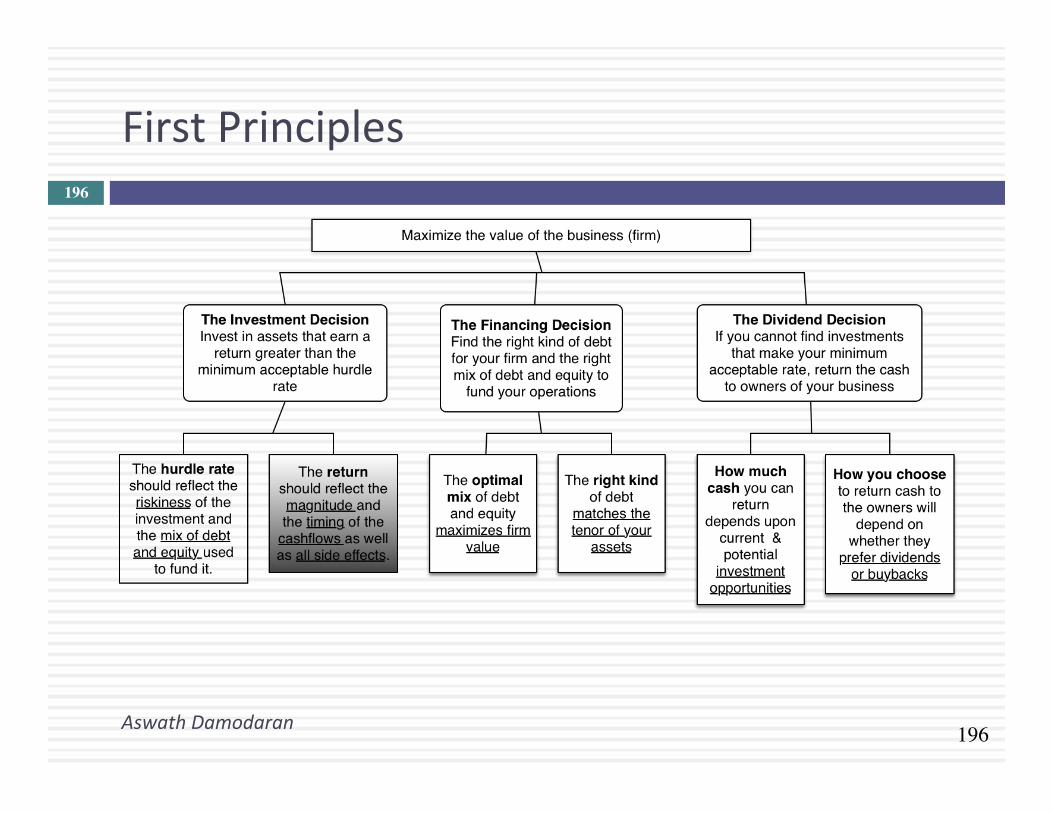

FirstPrinciples

AswathDamodaran

196

197

Measuresofreturn:earningsversuscashflows

AswathDamodaran

197

¨ PrinciplesGoverningAccoun9ngEarningsMeasurement¤ AccrualAccoun9ng:Showrevenueswhenproductsandservicesare

soldorprovided,notwhentheyarepaidfor.Showexpensesassociatedwiththeserevenuesratherthancashexpenses.

¤ Opera9ngversusCapitalExpenditures:Onlyexpensesassociatedwithcrea9ngrevenuesinthecurrentperiodshouldbetreatedasopera9ngexpenses.ExpensesthatcreatebenefitsoverseveralperiodsarewriSenoffovermul9pleperiods(asdeprecia9onoramor9za9on)

¨ Togetfromaccoun9ngearningstocashflows:¤ youhavetoaddbacknon-cashexpenses(likedeprecia9on)¤ youhavetosubtractoutcashouplowswhicharenotexpensed(such

ascapitalexpenditures)¤ youhavetomakeaccrualrevenuesandexpensesintocashrevenues

andexpenses(byconsideringchangesinworkingcapital).

198

MeasuringReturnsRight:TheBasicPrinciples

AswathDamodaran

198

¨ Usecashflowsratherthanearnings.Youcannotspendearnings.

¨ Use“incremental”cashflowsrela9ngtotheinvestmentdecision,i.e.,cashflowsthatoccurasaconsequenceofthedecision,ratherthantotalcashflows.

¨ Use“9meweighted”returns,i.e.,valuecashflowsthatoccurearliermorethancashflowsthatoccurlater.TheReturnMantra:“Time-weighted,IncrementalCash

FlowReturn”

199

Seqngthetable:Whatisaninvestment/project?

AswathDamodaran

199

¨ Aninvestment/projectcanrangethespectrumfrombigtosmall,moneymakingtocostsaving:¤ Majorstrategicdecisionstoenternewareasofbusinessornewmarkets.

¤ Acquisi9onsofotherfirmsareprojectsaswell,notwithstandingaSemptstocreateseparatesetsofrulesforthem.

¤ Decisionsonnewventureswithinexis9ngbusinessesormarkets.

¤ Decisionsthatmaychangethewayexis9ngventuresandprojectsarerun.

¤ Decisionsonhowbesttodeliveraservicethatisnecessaryforthebusinesstorunsmoothly.

¨ Putinbroaderterms,everychoicemadebyafirmcanbeframedasaninvestment.

200

Herearefourexamples…

AswathDamodaran

200

¨ RioDisney:WewillconsiderwhetherDisneyshouldinvestinitsfirstthemeparksinSouthAmerica.Theseparks,whilesimilartothosethatDisneyhasinotherpartsoftheworld,willrequireustoconsidertheeffectsofcountryriskandcurrencyissuesinprojectanalysis.

¨ NewironoremineforVale:ThisisanironoreminethatValeisconsideringinWesternLabrador,Canada.

¨ AnOnlineStoreforBookscape:Bookscapeisevalua9ngwhetheritshouldcreateanonlinestoretosellbooks.Whileitisanextensionoftheirbasisbusiness,itwillrequiredifferentinvestments(andpoten9allyexposethemtodifferenttypesofrisk).

¨ Acquisi9onofHarmanbyTataMotors:Across-borderbidbyTataforHarmanInterna9onal,apubliclytradedUSfirmthatmanufactureshigh-endaudioequipment,withtheintentofupgradingtheaudioupgradesonTataMotors’automobiles.Thisinvestmentwillallowustoexaminecurrencyandriskissuesinsuchatransac9on.

201

EarningsversusCashFlows:ADisneyThemePark

AswathDamodaran

201

¨ ThethemeparkstobebuiltnearRio,modeledonEuroDisneyinParisandDisneyWorldinOrlando.

¨ Thecomplexwillincludea“MagicKingdom”tobeconstructed,beginningimmediately,andbecomingopera9onalatthebeginningofthesecondyear,andasecondthemeparkmodeledonEpcotCenteratOrlandotobeconstructedinthesecondandthirdyearandbecomingopera9onalatthebeginningofthefourthyear.

¨ Theearningsandcashflowsarees9matedinnominalU.S.Dollars.

202

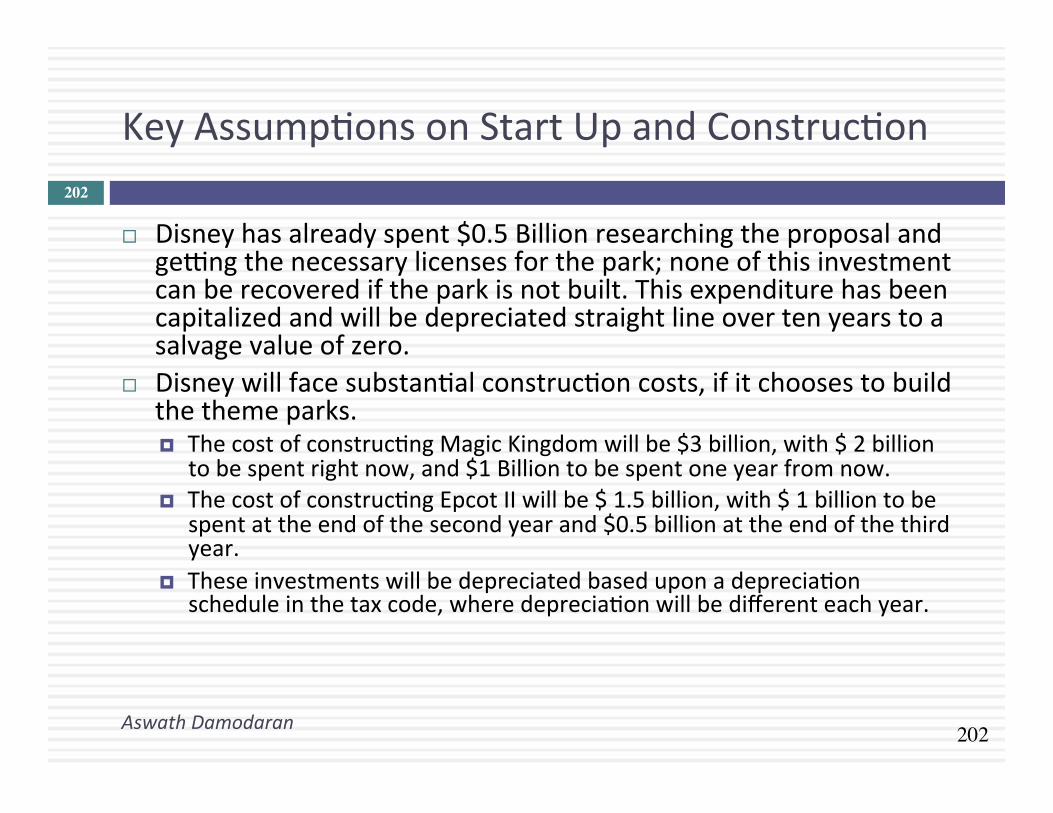

KeyAssump9onsonStartUpandConstruc9on

AswathDamodaran

202

¨ Disneyhasalreadyspent$0.5Billionresearchingtheproposalandgeqngthenecessarylicensesforthepark;noneofthisinvestmentcanberecoverediftheparkisnotbuilt.Thisexpenditurehasbeencapitalizedandwillbedepreciatedstraightlineovertenyearstoasalvagevalueofzero.

¨ Disneywillfacesubstan9alconstruc9oncosts,ifitchoosestobuildthethemeparks.¤ Thecostofconstruc9ngMagicKingdomwillbe$3billion,with$2billion

tobespentrightnow,and$1Billiontobespentoneyearfromnow.¤ Thecostofconstruc9ngEpcotIIwillbe$1.5billion,with$1billiontobe

spentattheendofthesecondyearand$0.5billionattheendofthethirdyear.

¤ Theseinvestmentswillbedepreciatedbaseduponadeprecia9onscheduleinthetaxcode,wheredeprecia9onwillbedifferenteachyear.

203

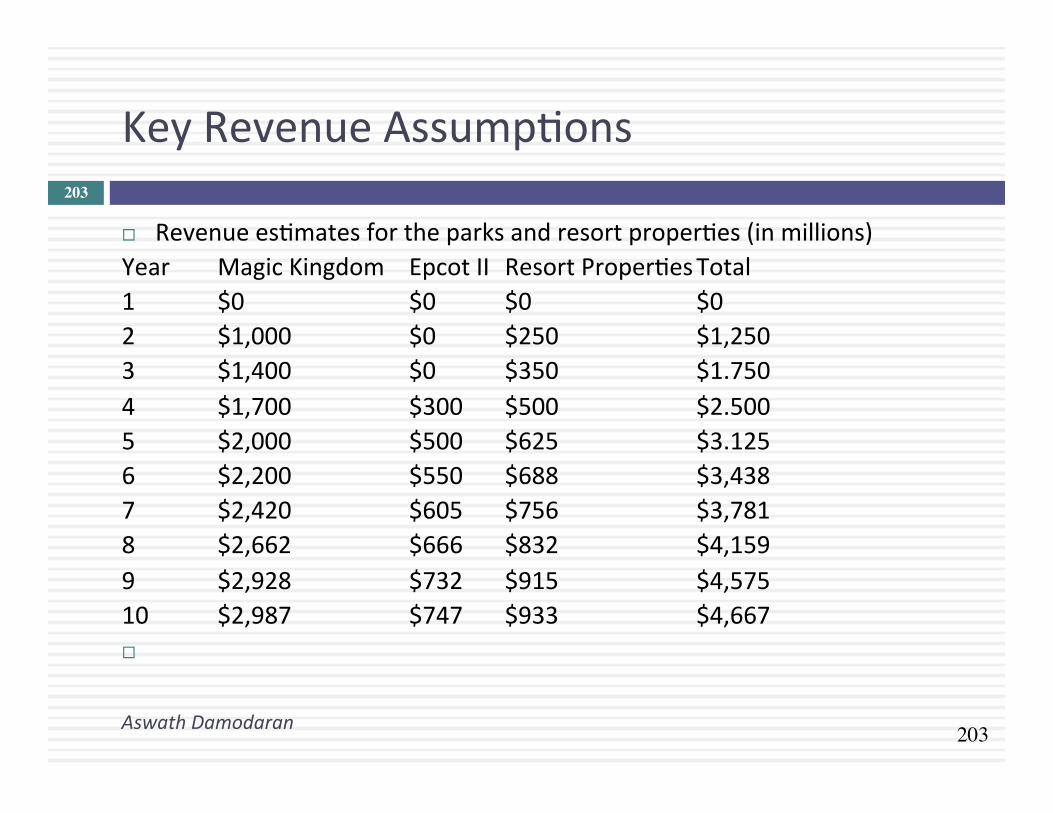

KeyRevenueAssump9ons

AswathDamodaran

203

¨ Revenuees9matesfortheparksandresortproper9es(inmillions)Year MagicKingdom EpcotII ResortProper9esTotal1 $0 $0 $0 $02 $1,000 $0 $250 $1,2503 $1,400 $0 $350 $1.7504 $1,700 $300 $500 $2.5005 $2,000 $500 $625 $3.1256 $2,200 $550 $688 $3,4387 $2,420 $605 $756 $3,7818 $2,662 $666 $832 $4,1599 $2,928 $732 $915 $4,57510 $2,987 $747 $933 $4,667¨

204

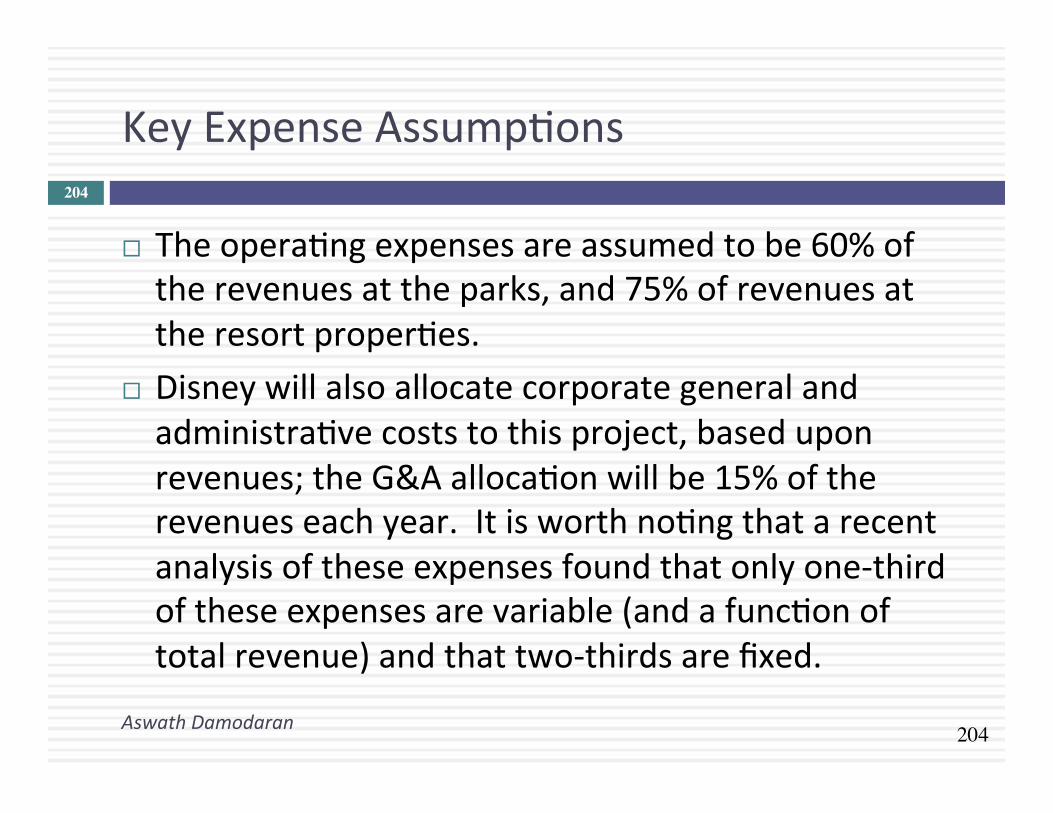

KeyExpenseAssump9ons

AswathDamodaran

204

¨ Theopera9ngexpensesareassumedtobe60%oftherevenuesattheparks,and75%ofrevenuesattheresortproper9es.

¨ Disneywillalsoallocatecorporategeneralandadministra9vecoststothisproject,baseduponrevenues;theG&Aalloca9onwillbe15%oftherevenueseachyear.Itisworthno9ngthatarecentanalysisoftheseexpensesfoundthatonlyone-thirdoftheseexpensesarevariable(andafunc9onoftotalrevenue)andthattwo-thirdsarefixed.

205

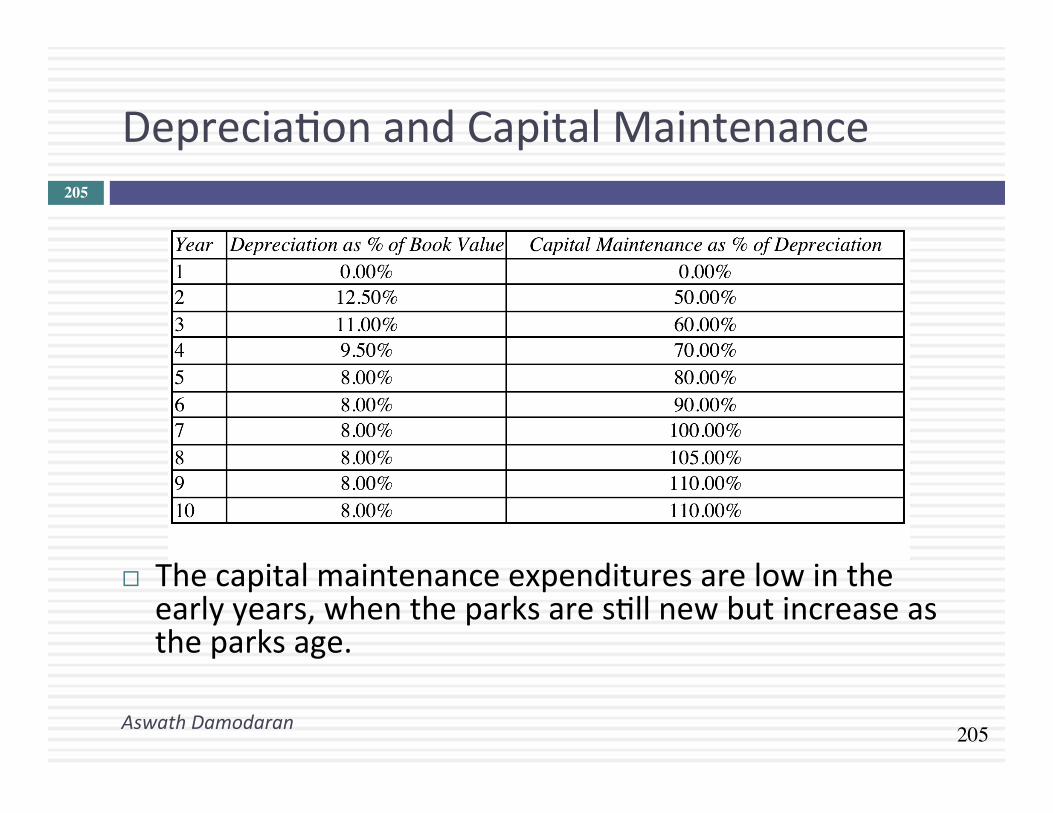

Deprecia9onandCapitalMaintenance

AswathDamodaran

205

¨ Thecapitalmaintenanceexpendituresarelowintheearlyyears,whentheparksares9llnewbutincreaseastheparksage.