Embed Size (px)

Citation preview

Default Aversion: Strategies and Outcomes

TACCBO Conference PresentationJune 23, 2016

Dr. Harold WhitisDistrict Director of Student Financial Aid

What is a Default?

Under section 435(l) of the Higher Education Act of 1965, as amended (HEA), a borrower who is 270 or more days past due in repaying a Federal Family Education Loan (FFEL) Program loan or a William D. Ford Federal Direct Loan (Direct Loan) Program loan is considered to be in default.

What is a Cohort Default Rate?

The school’s cohort default rate is the percentage of a school’s borrowers who enter repayment during that fiscal year and default within the cohort default period.

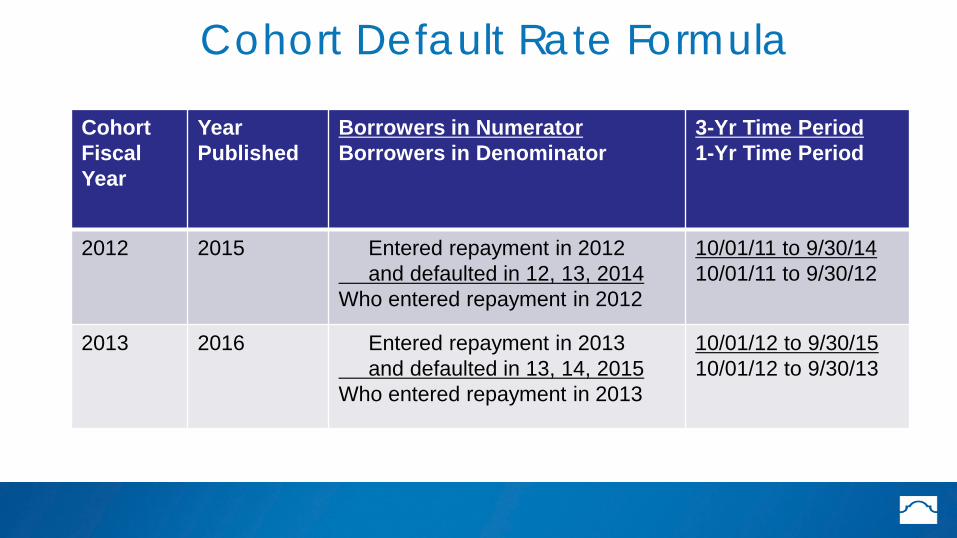

Cohort Default Rate Formula

Cohort Fiscal Year

Year Published

Borrowers in NumeratorBorrowers in Denominator

3-Yr Time Period1-Yr Time Period

2012 2015 Entered repayment in 2012 and defaulted in 12, 13, 2014

Who entered repayment in 2012

10/01/11 to 9/30/1410/01/11 to 9/30/12

2013 2016 Entered repayment in 2013 and defaulted in 13, 14, 2015

Who entered repayment in 2013

10/01/12 to 9/30/1510/01/12 to 9/30/13

Importance of a Low CDRNeed to produce financial responsible

graduates. If your rate goes above 30 % you run the risk

of losing all Title IV financial assistance.Gainful employment programs are

becoming at risk as the Earning/Debt ratios are published.

First Step in Default Aversion

Most important before they borrow:Have a robust Entrance and Exit counseling

strategy. Educate before students borrow and all

through their career Examine your awarding strategies Split disbursements into two per term

First Step in Default AversionAfter they leave school:Have an in house operation to perform due

diligence on students in repayment to help prevent them from going into default.

Hire a third party vendor to perform the due diligence.

Limitations of Both and Recommendation In house: Staff turnover, training, knowledge

of regulations, diversions of efforts. Third party: Cost

To me having a third party vendor handle your due diligence is more than worth the cost.

Tools to Prevent Default

⋅ Flexible payment plans to meet the students needs ⋅ Deferments

– In School– Military Service– Public Service

⋅ Forbearance– Temporary cessation of payments during hardship

⋅ Forgiveness – Total and permanent disability

Standard Repayment Plan

Standard Repayment Plan ⋅ Time borrower has to repay: Up to 10

years. (10- to 30-year repayment period for Direct Consolidation Loans)

⋅ Payments remain constant throughout the repayment period.

Graduated Repayment PlanGraduated Repayment Plan ⋅ Time borrower has to repay: Up to 10

years. (10- to 30-year repayment period for Direct Consolidation Loans)

⋅ Payments start low and gradually increase every two years over life of loan.

Extended Repayment PlanExtended Repayment Plan ⋅ Time borrower has to repay: Up to 25 years. ⋅ Payments will be an amount that ensures

the loan will be paid in full in 25 years. Borrower can choose to make either fixed or graduated payments.

⋅ Borrower must have more than $30,000 in Federal Direct Loans to qualify.

Income Driven Repayment Plans⋅ Income-Driven Repayment Plans (Income-Based

Repayment Plan, Pay as You Earn Repayment Plan, and Income-Contingent Repayment Plan)

⋅ Time borrower has to repay: Up to 20 or 25 years depending on the repayment plan.

⋅ Monthly payment amount tied to borrower’s income and adjusted annually.

⋅ Any outstanding balance remaining at end of loan repayment period will be forgiven.

3 Unexpected Stats (ASA)Stat 1 Students were asked: How much debt should students take

on to pursue higher education? Response: More than one third of students think they should

only borrow what can be paid off in five years at their expected starting salary.

Fact: On average, it takes 19.7 years to pay off undergraduate loans.

(http://www.asa.org/for-partners/schools/content-pages/3-unexpected-stats-)

3 Unexpected Stats (ASA)Stat 2 Administrators were asked: How much debt should students

take on to pursue higher education? Response: Students should only borrow what they can pay off

in 10 years. Fact: Given today’s average starting salary of $48,127, loan

calculators say students should borrow a maximum of $28,256. loans. Today’s average debt at graduation is $35,000.

(http://www.asa.org/for-partners/schools/content-pages/3-unexpected-stats-)

3 Unexpected Stats (ASA)Stat 3 Almost a quarter of students and school administrators are

unsure how much debt students should take on. This strongly suggests that greater financial education is

required. Students need to understand the impact of these long-term obligations before taking them on.

(http://www.asa.org/for-partners/schools/content-pages/3-unexpected-stats-)

NFCC Key FindingsCredit Reports and Credit Scores In 2014, most adults have not reviewed their credit

score (60%) or their credit report (65%) within the past 12 months.

More than half (54%) reviewed neither. Among those who did not order their credit

report(s), more than one in four (27%) say they didn’t know of any reason why they should.

https://www.nfcc.org/NewsRoom/FinancialLiteracy/files2013/NFCC_2014FinancialLiteracySurvey_datasheet_and_key_findings_031314%20FINAL.pdf

National Financial Capability Study

In Texas, 19% of individuals reported that over the past year, their household spent more than their income, while 30% of individuals reported having medical bills that are past due.

Source: FINRA Investor Education Foundation, National Financial Capability Study (2015). Making Ends Meet. http://www.usfinancialcapability.org/results.php?region=TX

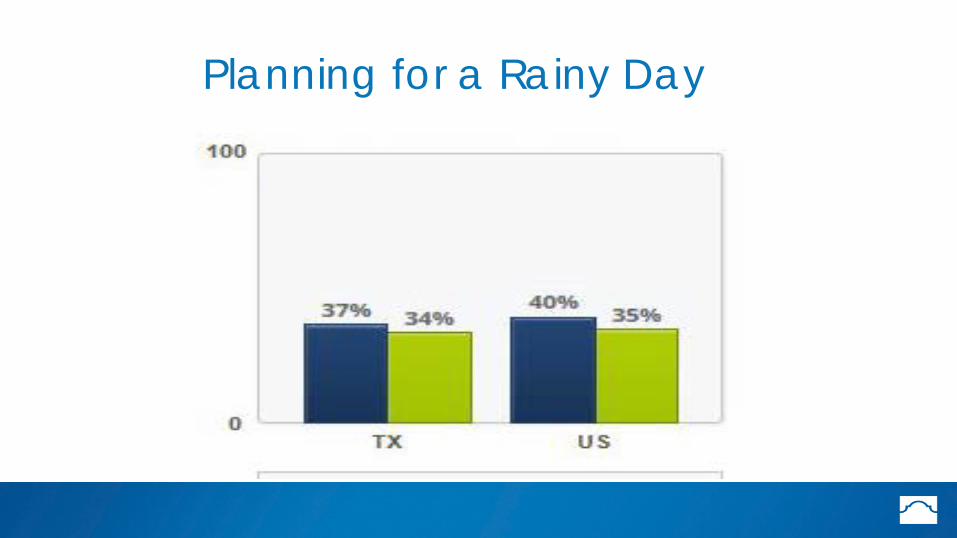

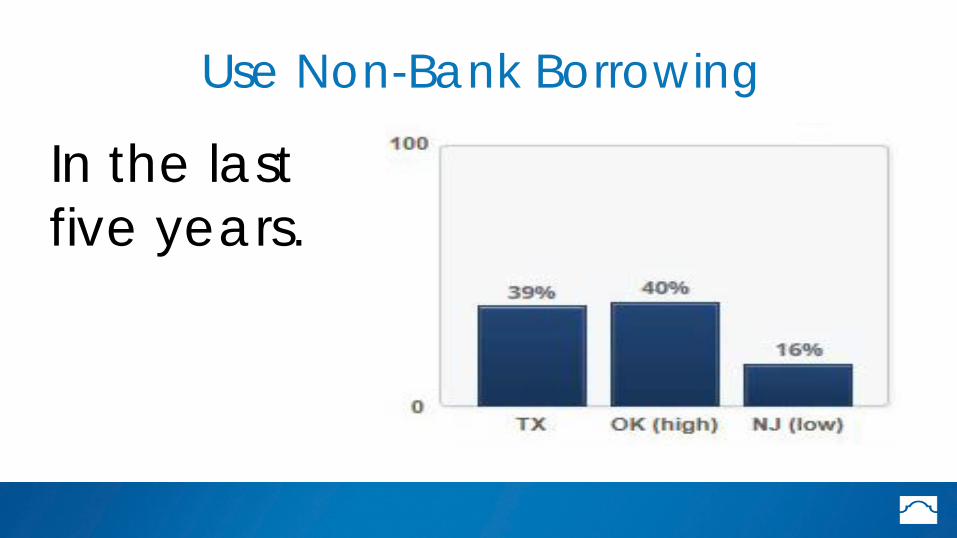

Planning for a Rainy Day

In the last five years.

Use Non-Bank Borrowing

Second Step in Default Aversion

Financial Literacy

Where Did Alamo Colleges Start?

In 2011 we contracted with a third party provider for Default Aversion Services

St. Philip’s College had already been receiving assistance from USA Funds.

We created a District Default Aversion Committee

We focused an Associate Director position specifically on Financial Literacy.

We Learned

⋅ The Association of Community Colleges Trustees released a report called “Protecting Colleges and Students: Community College Strategies to Prevent Default (McKibben, et.al., 2014)

⋅ St. Philip’s College and several other national colleges participated in the study.

⋅ A result of the study was the development of a “Default Aversion Plan”.

ACCT Study Strategies Direct Student InterventionClassroom ParticipationOutreach to StudentsStaged Curriculum

Analyze Borrowers and Defaulters Track a cohort through collegePartner with Institutional Research

Stress Benefits of Full-time Enrollment

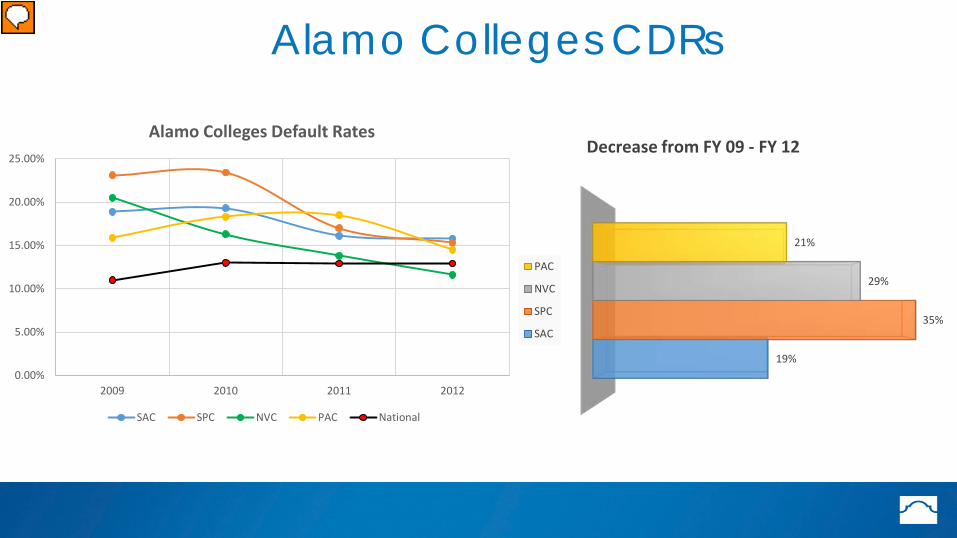

Alamo Colleges CDRs

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

2009 2010 2011 2012

Alamo Colleges Default Rates

SAC SPC NVC PAC National

19%

35%

29%

21%

Decrease from FY 09 - FY 12

PAC

NVC

SPC

SAC

We Continued to Learn In January of 2015, the Vice Chancellor for

Student Success arranged for interested parties to view a webinar presented by Syracuse University entitled “Increasing Student Engagement in Financial Literacy Programming”.

In collaboration between the Student Financial Aid Office, Student Success and the Student Leadership Institute, the Student Driven Financial Literacy Program was launched in the fall of 2015.

Student Driven Financial Literacy Program

Title: Managing My Money (MMM)

Slogan: Managing My Money Makes Sen$e!

Mission: To increase all Alamo College student’s financial awareness and empower our diverse communities for financial success

Managing My Money ProgressWe felt it was important to have the student focusWe hired one Work Study student at each

campus to serve as a resource for students with Financial Literacy Questions.We don’t expect them to be experts but to guide

students to the resources we have identified and to our website.

Identifying a Vehicle

Free, Sponsored by the National Endowment for Financial Education (NEFE).OnlineCommercial FreeBranded to Alamo CollegesMultiple Departments Can Use at Once

How We Want to Use CashCourse

Intrusive Financial Literacy Education through cooperation with the SDEV instructorsCreating a Financial Literacy Certificate for

students who complete a specific curriculum Educate students to guide peers to the

information

Managing My Money ProgressWe have become active in the Texas

Association of College Financial Education ProfessionalsWe have begun holding multiple presentations

on campus by enlisting community professionalsWe received a $1,500 grant from the National

Endowment for Financial Education

Achieving the Dream Grant

In December of 2015, we applied for a Student Empowerment Grant through Achieving the Dream and were one of five colleges awarded a $25,000 grant, funded in part by One-Main Financial.

Our plan is to implement all of the ACCT strategies that were outlined in their report with participation from all the campuses.

There is No Silver Bullet!

Default Aversion is a Collaborative Effort