Embed Size (px)

Citation preview

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 1/71

A

Summer Training Project Report

On

“A STUDY OF POSITIONING STRATEGIES ADOPTED BY MUTUAL FUNDS

COMPANIES IN INDIA. ”

KARVY STOCK BROCKING LTD.

A dissertation submitted in partial fulfillment of the requirment for the degree of Masters of Business Administration course of Kurukshetra Univerrsity

Under guidance of Submitted by:Mrs.Poonam Mahendru Sandeep kumar yadav

S/O Sh.Lalan yadav

Roll no:246Univ.Regd.No. 07-MY-716

Univ.Roll.No

Batch:2010-2012

CH.DEVI LAL INSTITUTE OF MGT STUDIES.BHAGWANGARH,BURIA

ROAD,JAGADHRI,DISTT.YAMUNA NAGAR

1

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 2/71

CERTIFICATE

This is to certify that this Research Project entitled, “A STUDY OF

POSITIONING STRATEGIES ADOPTED BY MUTUAL FUND

COMPANIES IN INDIA” submitted in partial fulfillment of the requirement

for the degree of Master of Business Administration (MBA), at CH. DEVI

LAL INSTITUTE OF MANAGEMENT STUDIES JAGADHARI, affiliated to

Kurukshetra University kurukshetra is bona fide research work carried out

by SANDEEP KUMAR YADAV under my supervision, and no part of this

project report has been submitted for any other degree. The assistance

and help received during the course of the project has been fully

acknowledged.

Project Guide

Mrs.Poonam Mahendru

2

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 3/71

ABSTRACT

A Mutual Fund is a trust that pools the savings of a number of investor

who share common financial goal. The money thus collected is then invested i

capital market instruments such as shares, debentures and other securities. Th

income earned through these investments and the capital appreciation realized

shared by its unit holders in proportion to the number of units owned by them

There are three major asset classes where money can be put in, namely EQUITIE

FIXED INCOME AND MONEY MARKET INSTRUMENTS. In order to decide how much of th

money goes into which investment class first few important factors.

Distribution and comparison of mutual funds: The objective of the project is

to generate new business by attracting new investors and maintaining the

existing investors/clients and to recommend on the type of investment

depending upon the various objectives of investment and resources

available as on parameters of risk, return and liquidity,In order to generate

new business for the company the methodology being followed is tele

calling, cold calling and direct marketing. For generating new leads I am

doing tele calling on the data provided by the company guide. For

generating new business I have already visited PUDA, NABARD, UDYOG

3

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 4/71

BHAVAN, IOC, SIDBI and GAIL. In order to compare the various mutual

funds I have selected some of the mutual funds as due to time constraint it is

not possible to cover every mutual fund. Mutual funds can be compared on

the basis of mutual fund family and category. The basis of the comparison

is ALPHA, BETA, PE RATIO etc. Mutual funds are also compared withMutual funds are also compared with

other products like banks deposits,ULIP and post office saving schemesother products like banks deposits,ULIP and post office saving schemes

ACKNOWLEDGEMENT

“No project is ever a work of only one person and this one is no exception”

I take this opportunity to thank all those people who have helped me during this project.

At the outset I would like to express my gratitude to Mr.Jaswinder singh , Branch Manager,

Karvy stock brocking ltd.. Yamuna nagar without whom this project could not have been possible. His practical observation on the subject has helped us app thank Mrs. Poonam

Mahendru,,HOD of ch.devi lal institute of mgt studies who has assisted me in successful

completion of this project.

4

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 5/71

TABLE OF CONTENTS

Title Page No

Acknowledgement. 4

Objective Of The Study

Positioning strategies 6

Industry Profile 7

Over View of Karvy 8

History of Karvy 9

Mission of karvy 10

Quality policy 11

Service of karvy 12

Introduction of mutual fund 13-14

History of mutual fund 15-16

Structure of India mutual fund industry 17

Company profile 18-20

Basics of mutual fund 21-26

Types of mutual fund 27-30Benefits of mutual funds 31-34

Risk associated with mutual fund 35-37

Importance financing planning 38-47

Investment avnues 48-51

Comparative analysis 52-53

Purchasing selling mutual fund 54-57

Selection of mutual fund 58-60

Performance of mutual fund 61-66

Recommendations & Conclusion 67-68

Bibliography 69-70

5

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 6/71

OBJECTIVE OF THE STUDY

The Objective of the study was to get an understanding of the mutual funds. The Scope

of the study involves

To Study Mutual Funds and their types and structure.

Measuring the impact of the mutual fund on Indian market.

Analyzing the performance of mutual fund industry.

Comparing mutual funds with various others investment products.

POSITIONING STRATGIES

➢ Product Attributes: What are the specific product attributes?

➢ Benefits: What are the benefits to the customers?

➢ Usage Occasions: When / how can the product be used?

➢ Users: Identify a class of users.

➢ Against a competitor: Positioned directly against a competitor.

➢ Away from a competitor: Positioned away from competitor.

➢ Product Classes: Compared to different classes of products.

6

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 7/71

INDUSTRY PROFILE

OVERVIEW OF KARVYOVERVIEW OF KARVY

7

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 8/71

KARVYKARVY, is a premier integrated financial services provider, and ranked among the top five in th, is a premier integrated financial services provider, and ranked among the top five in th

country in all its business segments, services over 16 million individual investors in various capacitiecountry in all its business segments, services over 16 million individual investors in various capacitie

and provides investor services to over 300 corporates. KARVY covers the entire spectrum of financiand provides investor services to over 300 corporates. KARVY covers the entire spectrum of financi

services such as Stock broking, Depository Participants, Distribution of financial products - mutuservices such as Stock broking, Depository Participants, Distribution of financial products - mutu

funds, bonds, fixed deposit, equities, Insurance Broking, Commodities Broking, Personal Finanfunds, bonds, fixed deposit, equities, Insurance Broking, Commodities Broking, Personal Finan

Advisory Services, Merchant Banking & Corporate Finance, placement of equity, IPOs, among otheAdvisory Services, Merchant Banking & Corporate Finance, placement of equity, IPOs, among other

Karvy has a professional management team and ranks among the best in technology, operations anKarvy has a professional management team and ranks among the best in technology, operations an

research of various industrial segments.research of various industrial segments.

8

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 9/71

History of History of KARVYKARVY

The birth of Karvy was on a modest scale in 1981. ItThe birth of Karvy was on a modest scale in 1981. It with the vision anwith the vision an

enterprise of a small group of practicing Chartered Accountants who founded thenterprise of a small group of practicing Chartered Accountants who founded th

flagship company …Karvy Consultants Limited and the KARVY word derived froflagship company …Karvy Consultants Limited and the KARVY word derived from

the first letter of the name of each five founders. We started with consulting anthe first letter of the name of each five founders. We started with consulting an

financial accounting automation, and carved inroads into the field of registry anfinancial accounting automation, and carved inroads into the field of registry an

share accounting by 1985. Since then, we have utilized our experience anshare accounting by 1985. Since then, we have utilized our experience an

superlative expertise to go from strength to strength…to better our services, superlative expertise to go from strength to strength…to better our services, t

provide new ones, to innovate, diversify and in the process, evolved Karvy aprovide new ones, to innovate, diversify and in the process, evolved Karvy a

one of India’s premier integrated financial service enterprise.one of India’s premier integrated financial service enterprise.

Thus over the last 20 years Karvy has traveled the success route, toward

building a reputation as an integrated financial services provider, offering a wid

spectrum of services. And we have made this journey by taking the route o

quality service, path breaking innovations in service, versatility in service an

beganbegan finally…totality in service.

They are highly qualified manpower, cutting-edge technology, comprehensiv

infrastructure and total customer-focus has secured for the position of a

emerging financial services giant enjoying the confidence and support of a

enviable clientele across diverse fields in the financial world

9

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 10/71

Mission of KARVYMission of KARVY

RespectRespect

Each and every individual is an essential building block of our organization.Each and every individual is an essential building block of our organization.

They are the kiln that hones individuals to perfection. Be they our employees, shareholders They are the kiln that hones individuals to perfection. Be they our employees, shareholders

investors. They do so by upholding their dignity & pride, inculcating trust and achieving a sensitiinvestors. They do so by upholding their dignity & pride, inculcating trust and achieving a sensiti

balance of their professional and personal lives. balance of their professional and personal lives.

Teamwork Teamwork

None of us is more important than all of usNone of us is more important than all of us . .

Each team member is the face of Karvy. Together They offer diverse services with speed, accuraEach team member is the face of Karvy. Together They offer diverse services with speed, accurac

and quality to deliver only one product: excellence. Transparency, co-operation, invaluable individuand quality to deliver only one product: excellence. Transparency, co-operation, invaluable individu

contributions for a collective goal, and respecting individual uniqueness within a corporate whole, contributions for a collective goal, and respecting individual uniqueness within a corporate whole,

how They deliver again and again.how They deliver again and again.

Responsible CitizenshipResponsible Citizenship

A social balance sheet is as rewarding as a business one.A social balance sheet is as rewarding as a business one.

As a responsible corporate citizen, our duty is to foster a better environment in theAs a responsible corporate citizen, our duty is to foster a better environment in the society whesociety whe

they live and work. Abiding by its norms, and behaving responsibly towards ththey live and work. Abiding by its norms, and behaving responsibly towards th

environment, are some of growing initiatives towards realizing it.environment, are some of growing initiatives towards realizing it.

10

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 11/71

Quality policyQuality policy

To achieve and retain leadership, Karvy shall aim for complete customer satisfaction by combining To achieve and retain leadership, Karvy shall aim for complete customer satisfaction by combining i

human & technological resources, to provide superior quality financial services. In the process, Karvhuman & technological resources, to provide superior quality financial services. In the process, Karv

will strive to exceed customer’s satisfactionwill strive to exceed customer’s satisfaction

Quality objectivesQuality objectives

As per the quality policy, Karvy will:As per the quality policy, Karvy will:

Establish a partner relationship with its investor service agents and vendors that will help inEstablish a partner relationship with its investor service agents and vendors that will help in

keeping up its commitment to the customers.keeping up its commitment to the customers.

Provide high quality of work life for all its employees and equip them with adequateProvide high quality of work life for all its employees and equip them with adequate

knowledge & skills so as to respond to customers needs.knowledge & skills so as to respond to customers needs.

Continue to uphold the value of honesty & integrity and strive to establish unparalleledContinue to uphold the value of honesty & integrity and strive to establish unparalleled

standards in business ethics.standards in business ethics.

Strive to be a reliable source of value added financial products and services and constantlyStrive to be a reliable source of value added financial products and services and constantly

guide the individual and institutions in making a judious choice of it.guide the individual and institutions in making a judious choice of it.

Strive to keep all stake-holders (share holders, client, investor, employee, supplier &Strive to keep all stake-holders (share holders, client, investor, employee, supplier &

regulatory authority) proud & satisfiedregulatory authority) proud & satisfied

11

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 12/71

SERVICES BY KARVY

Commodities trading (NCDEX & MCX)

Personal finance advisory services

Corporate finance & merchant banking

Depository participant services (NSDL & CDSL)

Financial products distribution (investments/loan products)

Mutual fund services

Stock broking (NSE & BSE, F&O)

E-Tds, tan/pan card/ mapin

Insurance (life & general)

Registrar & transfer agents

12

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 13/71

MUTUAL FUNDS

Saving for future is basic instinct of the human being. It started with hiding the money

and assets in pots, underground, roofs and any other safe place for retrieval at the time of need.Today an individual wants to invest surplus assets for safety and growth in a large number

sources such as fixed income instruments of post offices, banks provident funds, real estates,

equity shares, bonds, derivatives and other assets. However the individual does not possess the

knowledge, skills, inclination and time to keep track of events, understand their implications

and act speedily to save or appreciate his investments. A mutual fund is seen as an answer to

all these difficulties. It is an ideal investment vehicle for a common man in complex and

modern financial scenario.

MEANING OF MUTUAL FUNDS

A Mutual Fund is a trust that pools the savings of a number of investors who share a common

financial goal. The money thus collected is invested by the fund manager in different securities

depending upon the objective of the scheme. These could range from shares to debentures and

to money market instruments. The income earned through these investments and the capital

appreciation realized by the scheme are shared by its unit holders in proportion to the number

of units owned by them (pro rata). Thus a Mutual Fund is the most suitable investment for the

common man as it offers an opportunity to invest in a diversified, professionally managed

portfolio at a relatively low cost. Anybody with a surplus of as little as a few thousand rupees

can invest in Mutual Funds. Each Mutual Fund scheme has a defined investment objective and

strategy.

13

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 14/71

On launching of a scheme of the fund a draft offer document is prepared specifying theinvestment objectives, the risk associated, the costs involved in the process and the broad rules

for entry into and exit from the scheme and other areas of operation. In most of the countries,

these regulators approve these schemes of the fund. In case of India, the regulator is SEBI

(Securities exchange Board of India). The SEBI looks at track records of the sponsor and its

financial strength before granting approval for commencing operations to the fund.

The sponsor then hires an Asset Management Company (AMC) to invest the funds according

to the investment objective of the fund. It also hires another entity to be the custodian of the

assets of the fund and third one to handle registry work for the unit holders of the fund. In the

Indian context, the sponsor promotes the Asset Management Company, in which it has to hold

a majority stake which can go up to 100%. In the case of Principal PNB Asset Management

Company its sponsor Principal Financial Services Inc. has 65% stake in it while rest of stake

lies with PNB and Vijay Bank.

14

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 15/71

HISTORY OF MUTUAL FUNDS IN INDIA

The mutual fund industry in India started in 1963 with the formation of Unit Trust of

India, at the initiative of the Government of India and Reserve Bank the. The history of

mutual funds in India can be broadly divided into four distinct phases.

First Phase – 1964-87

Unit Trust of India (UTI) was established on 1963 by an Act of Parliament. It was set

up by the Reserve Bank of India and functioned under the Regulatory and

administrative control of the Reserve Bank of India. In 1978 UTI was de-linked from

the RBI and the Industrial Development Bank of India (IDBI) took over the regulatoryand administrative control in place of RBI. The first scheme launched by UTI was Unit

Scheme 1964. At the end of 1988 UTI had Rs.6, 700 crores of assets under

management.

Second Phase – 1987-1993

(Entry of Public Sector Funds) 1987 marked the entry of non- UTI, public sector mutual funds set up by public sector banks and Life Insurance Corporation of India

(LIC) and General Insurance Corporation of India (GIC). SBI Mutual Fund was the first

non- UTI Mutual Fund established in June 1987 followed by Canbank Mutual Fund

(Dec 87), Punjab National Bank Mutual Fund (Aug 89), Indian Bank Mutual Fund

(Nov 89), Bank of India (Jun 90), Bank of Baroda Mutual Fund (Oct 92). LIC

established its mutual fund in June 1989 while GIC had set up its mutual fund in

December 1990. At the end of 1993, the mutual fund industry had assets under

management of Rs.47, 004 crores.

Third Phase – 1993-2003 (Entry of Private Sector Funds)

15

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 16/71

With the entry of private sector funds in 1993, a new era started in the Indian mutual

fund industry, giving the Indian investors a wider choice of fund families. Also, 1993

was the year in which the first Mutual Fund Regulations came into being, under which

all mutual funds, except UTI were to be registered and governed. The erstwhile Kothari

Pioneer (now merged with Franklin Templeton) was the first private sector mutual fund

registered in July 1993. The 1993 SEBI (Mutual Fund) Regulations were substituted by

a more comprehensive and revised Mutual Fund Regulations in 1996. The industry now

functions under the SEBI (Mutual Fund) Regulations 1996. The number of mutual fund

houses went on increasing, with many foreign mutual funds setting up funds in India

and also the industry has witnessed several mergers and acquisitions. As at the end of

January 2003, there were 33 mutual funds with total assets of Rs. 1,21,805 crores. The

Unit Trust of India with Rs.44, 541 crores of assets under management was way ahead

of other mutual funds.

Fourth Phase – since February 2003 In February 2003

Following the repeal of the Unit Trust of India Act 1963 UTI was bifurcated into two

separate entities. One is the Specified Undertaking of the Unit Trust of India with assets

under management of Rs.29, 835 crores as at the end of January 2003, representing broadly, the assets of US 64 scheme, assured return and certain other schemes. The

Specified Undertaking of Unit Trust of India, functioning under an administrator and

under the rules framed by Government of India and does not come under the purview of

the Mutual Fund Regulations. The second is the UTI Mutual Fund Ltd, sponsored by

SBI, PNB, BOB and LIC. It is registered with SEBI and functions under the Mutual

Fund Regulations. With the bifurcation of the erstwhile UTI which had in March 2000

more than Rs.76,000 crores of assets under management and with the setting up of a

UTI Mutual Fund, conforming to the SEBI Mutual Fund Regulations, and with recent

mergers taking place among different private sector funds, the mutual fund industry has

16

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 17/71

Structure of the Indian mutual fund industry

The Indian mutual fund industry is dominated by the Unit Trust of India which has a

total corpus of Rs700bn collected from more than 20 million investors. The Unit

Scheme 1964 (US 64), which is a balanced fund, is the biggest scheme with a corpus of

about Rs200bn. The second largest category of mutual funds are Canbank Asset

Management and SBI Funds Management and Jeevan Bima Sahayog AMC. The

aggregate corpus of funds managed by this category of AMCs is about Rs150bn. In

private sector the largest are Prudential ICICI AMC and Birla Sun Life AMC. The

aggregate corpus of assets managed by this category of AMCs is in excess of Rs.

250bn.

Future Scenario

The asset base, it is expected, will continue to grow at an annual rate of about 30 to 35

% over the next few years as investors shift their assets from banks and other traditional

avenues with low interest rates. Some of the older public and private sector players will

either close shop or be taken over. The market will witness a flurry of new players

entering the arena. There will be a large number of offers from various asset

management companies in the time to come. Some big names like Fidelity, Principal,

Old Mutual etc. are looking at Indian market seriously. One important reason for it is

that most major players already have presence here and hence these big names would

hardly like to get left behind.

The mutual fund industry is awaiting the introduction of derivatives in India as this

would enable it to hedge its risk and this in turn would be reflected in it'sNet Asset

Value (NAV). SEBI is working out the norms for enabling the existing mutual fundschemes to trade in derivatives.

17

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 18/71

COMPANY

PROFILE

18

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 19/71

Karvy stock brocking ltd.

Karvy stock brocking ltd.. (FSL) is a wholly owned subsidiary of Karvy Financial

Services Ltd. (FFSL), a Company promoted by the late Dr. Parvinder Singh, Ex-CMD

of Ranbaxy Laboratories Ltd.

The primary focus of FSL is to cater to services in Capital Market Operations to

Institutional Investors. The Company is a member of the National Stock Exchange

(NSE) and OTCEI. The growing list of financial institutions with whom FSL is

empanelled, as approved Broker is a reflection of the high levels of services maintained

by the Company.

As on date the Company is empanelled with UTI, IDBI, IFCI, SBI, BOI-MF, Punjab National Bank, PNB-MF, Oriental Insurance, GIC, UTI-Offshore, ICICI Canbank MF,

Punjab & Sind Bank, Pioneer ITI, SUN F&C, IDBI Principal, Prudential ICICI, ING

Baring and J M Mutual Fund.

History of Karvy stock brocking ltd.

Karvy Securities Limited, a Ranbaxy Promoter Group Company, was founded by late

Dr. Parvinder Singh (CMD Ranbaxy Laboratories Limited), with the vision of

providing integrated financial care driven by the relationship of trust & confidence. To

realize its vision the Karvy group provides various financial services which include

broking (stocks & commodities), depository participant services, portfolio management

services, advisory on mutual fund investments and many more. Working on the

philosophy of being “Financial Care Partner”, Karvy unlike other traditional broking

firms not only executes the trades for the clients but also provides them critical and

timely investment advice. The growing list of financial institutions with which Karvy is

empanelled as an approved broker is a reflection of the high levels of service standard

maintained by the company. Karvy is a truly professional financial service provider

managed by a team of highly skilled professionals who have proven track record in

19

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 20/71

their respective domains. Karvy has the widest reach through its Regional, Zonal and

Branch Offices spread across the length & breadth of the country.

Now a days Karvy is driven by ethical and dynamic process for wealth creation.

Based on this, the company started its endeavor in the financial market.

Karvy Enterprises Limited (A Ranbaxy Promoter Group Company) through Karvy

Securities Limited, Karvy Finevest Limited, Karvy Commodities Limited and Karvy

Insurance Advisory Services Limited provides integrated financial solutions to its

corporate, retail and wealth management clients. Today, we provide various financial

services which include Investment Banking, Corporate Finance, Portfolio Management

Services, Equity & Commodity Broking, Insurance and Mutual Funds. Plus, there’s a

lot more to come your way.

Karvy is proud of being a truly professional financial service provider managed by a

highly skilled team, who have proven track record in their respective domains. Karvy

operations are managed by more than 1500 highly skilled professionals who subscribe

to Karvy philosophy and are spread across its country wide branches. . Today, we have

a growing network of 150 branches and more than 300 business partners spread across

180 cities in India and a fully operational international office at London. However, our

target is to have 350 branches and 1000 business partners in 300 cities of India and

more than 7 International offices by the end of 2006.

Unlike a traditional broking firm, Karvy group works on the philosophy of partnering

for wealth creation. We not only execute trades for our clients but also provide them

critical and timely investment advice. The growing list of financial institutions with

which Karvy is empanelled as an approved broker is a reflection of the high level

service standard maintained by the company

20

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 21/71

Basics

Of Mutual Funds

21

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 22/71

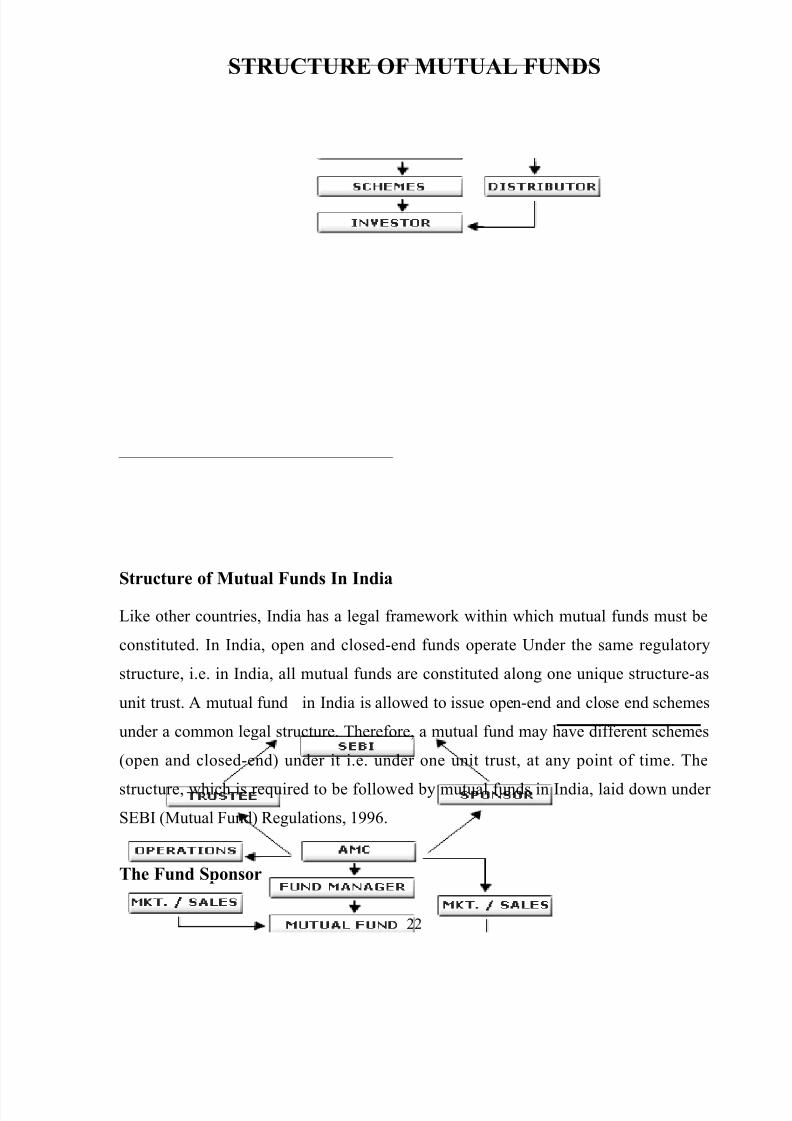

STRUCTURE OF MUTUAL FUNDS

Structure of Mutual Funds In India

Like other countries, India has a legal framework within which mutual funds must be

constituted. In India, open and closed-end funds operate Under the same regulatory

structure, i.e. in India, all mutual funds are constituted along one unique structure-as

unit trust. A mutual fund in India is allowed to issue open-end and close end schemes

under a common legal structure. Therefore, a mutual fund may have different schemes

(open and closed-end) under it i.e. under one unit trust, at any point of time. The

structure, which is required to be followed by mutual funds in India, laid down under

SEBI (Mutual Fund) Regulations, 1996.

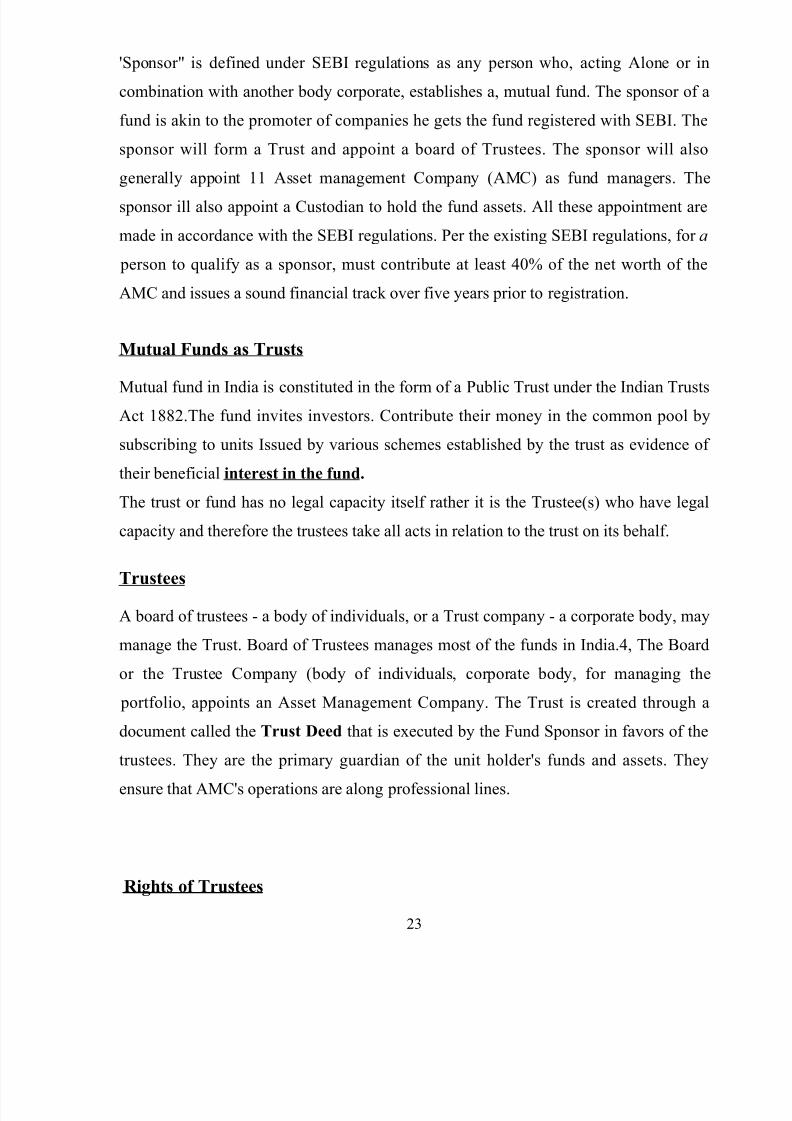

The Fund Sponsor

22

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 23/71

'Sponsor" is defined under SEBI regulations as any person who, acting Alone or in

combination with another body corporate, establishes a, mutual fund. The sponsor of a

fund is akin to the promoter of companies he gets the fund registered with SEBI. The

sponsor will form a Trust and appoint a board of Trustees. The sponsor will also

generally appoint 11 Asset management Company (AMC) as fund managers. The

sponsor ill also appoint a Custodian to hold the fund assets. All these appointment are

made in accordance with the SEBI regulations. Per the existing SEBI regulations, for a

person to qualify as a sponsor, must contribute at least 40% of the net worth of the

AMC and issues a sound financial track over five years prior to registration.

Mutual Funds as Trusts

Mutual fund in India is constituted in the form of a Public Trust under the Indian TrustsAct 1882.The fund invites investors. Contribute their money in the common pool by

subscribing to units Issued by various schemes established by the trust as evidence of

their beneficial interest in the fund.

The trust or fund has no legal capacity itself rather it is the Trustee(s) who have legal

capacity and therefore the trustees take all acts in relation to the trust on its behalf.

Trustees

A board of trustees - a body of individuals, or a Trust company - a corporate body, may

manage the Trust. Board of Trustees manages most of the funds in India.4, The Board

or the Trustee Company (body of individuals, corporate body, for managing the

portfolio, appoints an Asset Management Company. The Trust is created through a

document called the Trust Deed that is executed by the Fund Sponsor in favors of the

trustees. They are the primary guardian of the unit holder's funds and assets. They

ensure that AMC's operations are along professional lines.

Rights of Trustees

23

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 24/71

Appoint the AMC with the prior approval of SEBI.

Approve each of the schemes floated by the AMC.

Have the right to request any necessary information from the AMC concerning

the operations of various schemes managed by the AMC as often as required, to

ensure that the AMC is in compliance with the Trust Deed and regulation.

It my take remedial action if they believe that the conduct of the funds business

is not in accordance with Sebi regulations.

Direction of the trustees. The AMC is required to be approved and registered

with SEBI as an AMC; The Trustees are empowered to terminate the

appointment of the AMC and may appoint new AMC with the prior approval of

the Board and holders. The AMC floats and then manages the different

investment schemes.

The AMC of a mutual Fund must have a net worth of at least 1O Crores at all

the times. The AMC cannot act as a trustee any other mutual fund. The AMC

must report to the trustees with respect to its activities.

Obligations of the AMC and its Directors

They must ensure that:

Investment of funds is in accordance with SEBI Regulations and the Trust Deed.

Take responsibility for the act of its employees and others whose services it has

procured

They are answerable to the trustees and must submit quarterly reports to them

on AMC activities and compliance with SEBI Regulations

If the AMC uses the services of a sponsor, associate or employee, it must take

appropriate disclosure to unit holders, including the amount of brokerage or

commission paid.

24

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 25/71

Do not undertake any other activity conflicting with managing the fund.

Will float schemes only after obtaining disclosure to the investors in areas such

as calculation of NAV and repurchase price. Certain specific events, the

trustees have the right to dismiss the AMC with the approval of SEBI in

accordance with the regulations.

Right to ensure that, based on their quarterly review of the AMC's net worth, any

shortfall is made up.

Obligations of Trustees

Must enter into an investment management agreement with the AMC in

accordance with the Fourth Schedule of SEBI (MF)Regulations, 1996.

Must ensure that the funds transactions are in accordance with the Trust Deed.

Are responsible for ensuring that the AMC has proper systems and procedures in

place and has appointed key personnel including Fund Managers and a

Compliance Officer besides other constituents such as the auditors and

registrar.

Must ensure due diligence on the part of the AMC for empanelment of brokers

Must ensure that the AMC is managing schemes independent of

other activities and that the interest of unit holders of one scheme

are not compromised with those of other schemes

Must furnish to SEBI on a half-yearly basis, a report on the funds activities and a

certificate stating that the AMC has been managing the schemes independently

of other activities

Asset Management Company

The role of an Asset Management Company (AMC) is to act as the investment manager

of the trust under the Board supervision.

25

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 26/71

Transfer Agents

Transfer agents are responsible for issuing and redeeming units of the mutual fund and

provide other related services such as preparation of transfer documents updating

investors' records. A fund may choose to out this activity in-house or by an outside

transfer agent.

Distributors

AMC’s usually appoint Distributors or Brokers, who sell units on behalf bf the fund.

Some funds require that all transactions to be routed through such brokers.

In India, besides brokers, independent individuals are appointed as agents for the

purpose of selling the fund scheme to the investors. While individual constitute the

largest segment in the category of mutual fund distributors, other distributors include banks, NBFCs and corporate.

Bankers

A fund's activities involve dealing with the money on a continuous basis primarily with

respect to buying and selling units, paying for investment made, receiving the proceeds

on sale of investment and discharging its obligations towards operating expenses. A

funds banker therefore play a crucial role with respect to its financial dealings by

holding its bank account and providing it with remittance services

Custodian and Depository

The custodian is appointed by the Board of Trustees for safekeeping of securities in

terms of physical delivery and eventual safe keeping or participating in the clearing

system through approved depository companies on behalf of the mutual

fund and must fulfill its responsibilities in accordance with its agreement with

the mutual fund. The Indian markets are moving away from having physical certificates

26

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 27/71

for securities, to ownership of these securities in dematerialized form with a

depository. Thus, a fund's physical securities will continue to be held by a custodian.

TYPES OF MUTUAL FUNDS

Mutual Funds Schemes may be classified on the basis of its structure and its investment

objectives.

By Structure

Open-ended Funds

An open-end fund is one that is available for subscription all through the year. These do

not have a fixed maturity. Investors can conveniently buy and sell units at Net AssetValue ("NAV") related prices. The key feature of open-end schemes is liquidity.

27

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 28/71

Closed-ended Fund

A close-end fund has a stipulated maturity period which generally ranging from 3 to 15

years. The fund is open for subscription only during an A closed-end fund has a

stipulated maturity period which generally specified period. Investors can invest in the

scheme at the time of the initial public issue and thereafter they can buy or sell the units

of the scheme on the stock exchanges where they are listed. In order to provide an exit

route to the investors, some close-ended funds give an option of selling back the units

to the Mutual Fund through periodic repurchase at NAV related prices. SEBI

Regulations stipulate that at least one of the two exit routes is provided to the investor.

Interval Funds

Interval funds combine the features of open-ended and close-ended schemes. They are

open for sale or redemption during pre-determined intervals at NAV related prices.

By Investment

Growth Funds

The aim of growth funds is to provide capital appreciation over the medium to long-

term. Such schemes normally invest a majority of their corpus in equities. It has been

proven that returns from stocks, have outperformed most other kind of investments held

over the long term.

Growth schemes are ideal for investors having a long-term outlook seeking growth over

a period of time.

Income Funds

28

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 29/71

The aim of income funds is to provide regular and steady income to investors. Such

schemes generally invest in fixed income securities such as bonds, corporate debentures

and Government securities. Income Funds.

Balanced Funds

The aim of balanced funds is to provide both growth and regular income. Such schemes

periodically distribute a part of their earning and invest both in equities and fixed

income securities in the proportion indicated in their offer documents. In a rising stock

market, the NAV of these schemes may not normally keep pace, or fall equally when

the market falls. These are ideal for investors looking for a combination of income and

moderate growth.

Money Market Funds

The aim of money market funds is to provide easy liquidity, preservation of capital and

moderate income. These schemes generally invest in safer short-term instruments such

as treasury bills, certificates of deposit, commercial paper and inter-bank call money.

Returns on these schemes may fluctuate depending upon the interest rates prevailing in

the market. These are ideal for Corporate and individual investors as a means to park

their surplus funds for short periods.

Load Funds

A Load Fund is one that charges a commission for entry or exit. That is, each time you

buy or sell units in the fund, a commission will be payable. Typically entry and exit

loads range from 1% to 2.25%. It could be worth paying the load, if the fund has a good

performance history.

No-Load Funds

29

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 30/71

A No-Load Fund is one that does not charge a commission for entry or exit. That is, no

commission is payable on purchase or sale of units in the fund. The advantage of a no

load fund is that the entire corpus is put to work.

Other Schemes

Tax Saving Schemes

These schemes offer tax rebates to the investors under specific provisions of the Indian

Income Tax laws as the Government offers tax incentives for investment in specified

avenues. Investments made in Equity Linked Savings Schemes (ELSS) and

Pension Schemes are allowed as deduction u/s 80 of the Income Tax Act, 1961.

The Act also provides opportunities to investors to Save capital gains u/s 54EA and

54EB by investing in Mutual Funds, provided the capital asset has been sold prior to

April 1, 2000 and the amount is invested before September 30, 2000.

Special Schemes

Industry Specific Schemes

Industry Specific Schemes invest only in the industries specified in the offer document.

The investment of these funds is limited to specific industries like InfoTech, FMCG,

and Pharmaceuticals etc.

Index Schemes

Index Funds attempt to replicate the performance of a

particular index such as the BSE Sensex or the NSE 50

Sectoral Schemes

Sectoral Funds are those, which invest exclusively in a specified industry or a group of

industries or various segments such as 'A' Group

30

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 31/71

.BENEFITS OF MUTUAL FUNDS

Various benefits of mutual funds are:

1. Professional Management

Mutual Funds provide the services of experienced and skilled professionals, backed by

a dedicated investment research team that analyses the performance and prospects of

companies and selects suitable investments to achieve the objectives of the scheme.

2. Diversification

Mutual Funds invest in a number of companies across a broad cross-section of

industries and sectors. This diversification reduces the risk because seldom do all stocks

decline at the same time and in the same proportion. You achieve this diversification

through a Mutual Fund with far less money than you can do on your own.

31

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 32/71

3. Affordability

A mutual fund invests in a portfolio of assets, i.e. bonds, shares, etc. depending upon

the investment objective of the scheme. An investor can buy in to a portfolio of

equities, which would otherwise be extremely expensive. Each unit holder thus gets an

exposure to such portfolios with an investment as modest as Rs.500/-. This amount

today would get you less than quarter of an Infosys share! Thus it would be affordable

for an investor to build a portfolio of investments through a mutual fund rather than

investing directly in the stock market.

4. Variety

Mutual funds offer a tremendous variety of schemes. This variety is beneficial in two

ways: first, it offers different types of schemes to investors with different needs and risk

appetites; secondly, it offers an opportunity to an investor to invest sums across a

variety of schemes, both debt and equity. For example, an investor can invest his

money in a Growth Fund (equity scheme) and Income Fund (debt scheme) depending

on his risk appetite and thus create a balanced portfolio easily or simply just buy a

Balanced Scheme.

5. Tax Benefits

Any income distributed after March 31, 2002 will be subject to tax in the assessment of

all Unit holders. However, as a measure of concession to Unit holders of open-ended

equity-oriented funds, income distributions for the year ending March 31, 2003, will be

taxed at a concessional rate of 10

In case of Individuals and Hindu Undivided Families a deduction upto Rs.

1000000,from the Total Income will be admissible in respect of income from

investments specified in Section 80c, including income from Units of the Mutual Fund.

Units of the schemes are not subject to Wealth-Tax and Gift-Tax.

32

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 33/71

6. Regulations

Securities Exchange Board of India (“SEBI”), the mutual funds regulator has clearly

defined rules, which govern mutual funds. These rules relate to the formation,

administration and management of mutual funds and also prescribe disclosure and

accounting requirements. Such a high level of regulation seeks to protect the interest of

investors.

7. Convenient Administration

Investing in a Mutual Fund reduces paperwork and helps you avoid many problems

such as bad deliveries, delayed payments and follow up with brokers and companies.

Mutual Funds save your time and make investing easy and convenient.

8. Return Potential

Over a medium to long-term, Mutual Funds have the potential to provide a higher

return as they invest in a diversified basket of selected securities.

9. Low Costs

Investing in the capital markets because the benefits of scale in brokerage, Mutual

Funds are a relatively less expensive way to invest compared to directly custodial and

other fees translate into" lower costs for investors.

10.Liquidity

In open-end schemes, the investor gets the money back promptly at net asset value

related prices from the Mutual Fund. In closed-ends schemes, the units can be sold on astock exchange at the prevailing market price or the investor can avail of the facility of

direct repurchase at NAV related prices by the Mutual Fund.

33

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 34/71

11.Transparency

You get regular information on the value of your investment in addition to

disclosure on the specific investments made by your scheme, the proportion invested in

each class of assets and the fund manager's investment strategy and outlook.

12.Flexibility

Through features such as regular investment plans, regular withdrawal plans and

dividend reinvestment plans, you can systematically invest or withdraw funds

according to your needs and convenience.

13.Well Regulated

All Mutual Funds are registered with SEBI and they function within the provisions of

strict regulations designed to protect the interests of investors. The operations of Mutual

Funds are regularly

34

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 35/71

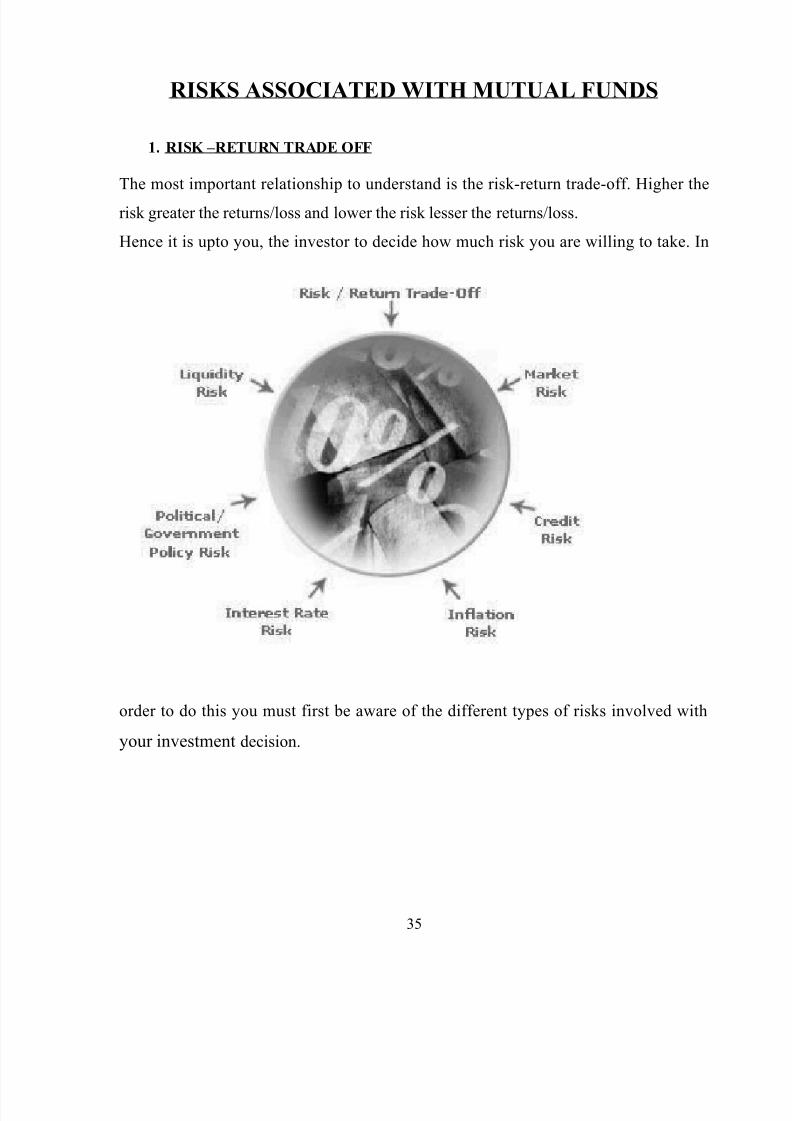

RISKS ASSOCIATED WITH MUTUAL FUNDS

1. RISK –RETURN TRADE OFF

The most important relationship to understand is the risk-return trade-off. Higher the

risk greater the returns/loss and lower the risk lesser the returns/loss.

Hence it is upto you, the investor to decide how much risk you are willing to take. In

order to do this you must first be aware of the different types of risks involved with

your investment decision.

35

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 36/71

MARKET RISK

Sometimes prices and yields of all securities rise and fall. Broad outside influences

affecting the market in general lead to this. This is true, may it be big corporations or

smaller mid-sized companies. This is known as Market Risk. A Systematic Investment

Plan (“SIP”) that works on the concept of Rupee Cost Averaging (“RCA”) might help

mitigate this risk.

2. CREDIT RISK

The debt servicing ability (may it be interest payments or repayment of principal) of a

company through its cashflows determines the Credit Risk faced by you. This credit

risk is measured by independent rating agencies like CRISIL who rate companies and

their paper. A ‘AAA’ rating is considered the safest whereas a ‘D’ rating is considered

poor credit quality. A well-diversified portfolio might help mitigate this risk.

3. INFLATION RISK

Things you hear people talk about:

“Rs. 100 today is worth more than Rs. 100 tomorrow.”

“Remember the time when a bus ride costed 50 paise?”

“Mehangai Ka Jamana Hai.”

The root cause, Inflation. Inflation is the loss of purchasing power over time. A lot of

times people make conservative investment decisions to protect their capital but end up

with a sum of money that can buy less than what the principal could at the time of the

investment. This happens when inflation grows faster than the return on your

investment. A well-diversified portfolio with some investment in equities might help

mitigate this risk.

4. INTEREST RATE RISK

36

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 37/71

In a free market economy interest rates are difficult if not impossible to predict.

Changes in interest rates affect the prices of bonds as well as equities. If interest rates

rise the prices of bonds fall and vice versa. Equity might be negatively affected as well

in a rising interest rate environment. A well-diversified portfolio might help mitigate

this risk.

5. POLITICAL RISK

Changes in government policy and political decision can change the investment

environment. They can create a favorable environment for investment or vice versa.

6. LIQUIDITY RISK

Liquidity risk arises when it becomes difficult to sell the securities that one has

purchased. Liquidity Risk can be partly mitigated by diversification, staggering of

maturities as well as internal risk controls that lean towards purchase of liquid

securities. You have been reading about diversification above, but what is it?

Diversification the nuclear weapon in your arsenal for your fight against Risk. It simplymeans that you must spread your investment across different securities (stocks, bonds,

money market instruments, real estate, fixed deposits etc.) and different sectors (auto,

textile, information technology etc.). This kind of a diversification may add to the

stability of your returns, for example during one period of time equities might under

perform but bonds and money market instruments might do well enough to offset the

effect of a slump in the equity markets. Similarly the information technology sector

might be faring poorly but the auto and textile sectors might do well and may protect

you principal investment as well as help you meet your return objectives.

37

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 38/71

IMPORTANCE

Of

FINANCIAL

PLANNING

38

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 39/71

IMPORTANCE OF FINANCIAL PLANNING

OUR GOALS

The first and most important step in your life as an investor is to define your goals at

the onset of your investing activity. This will map the road ahead for you in terms of time, amount, type of asset and risk. At this point of time you must also decide how

much you are willing to save. When you look at defining your goals think carefully and

try to include all your requirements, here are a few things that might help you:

Retirement – In how many years?

How much money will you need?

How long will you need it for?

Daughter’s/Son’s wedding – When and how much?

Daughter’s/Son’s education – When and how much?

Purchase of big ticket items e.g. House, Car etc. –

Again, when and how much?

A simple way to get an overall perspective is to draw a time line starting from today

with the amount you have saved up till now labeled at time zero. Going forward you

can label your major outflows as and when they occur till retirement and then the

steady outflows for your retirement income. Please remember your worst enemy

“Inflation” and factor this into your targets. Remember that in an inflationary

environment an apple will

cost more tomorrow than today. For example:

Let us say that you have Rs. 5,00,000 saved up today. In addition to this you figure that

in year 10 you will need Rs. 5,00,000 for your daughter’s wedding. Also you decide

with your wife that you will retire in thirty years time and will need Rs. 6,00,000 per

year for 15 years after that. You also decide that you want to play it safe and want to

invest only in debt products. Taking an annual rate of return of 7.00% you will have to

save Rs. 38,042 per year for thirty year and you will be able to withdraw Rs. 4,61,958

39

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 40/71

(5,00,000 – 38,042) for your daughter’s wedding in year 10. Another scenario with

9.00% is available as well. Now let us assume that you and your wife require Rs.

20,00,000 per annum for 15 years after retirement and want to spend Rs. 15,00,000 on

your daughter’s wedding. Knowing this you decide to take the additional risk of

investing your money in equities that historically do tend to provide double-digit

returns in the long run. Assuming an annual rate of return on 13.00% per annum you

would have to save Rs. 36,328 per year for thirty years to achieve your goals. An

example with a 15.00% return is provided as well.

Investors usually diversify their investment between debt and equities and earn returns

that are commensurate with their asset allocations

MEETING YOUR GOALS

40

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 41/71

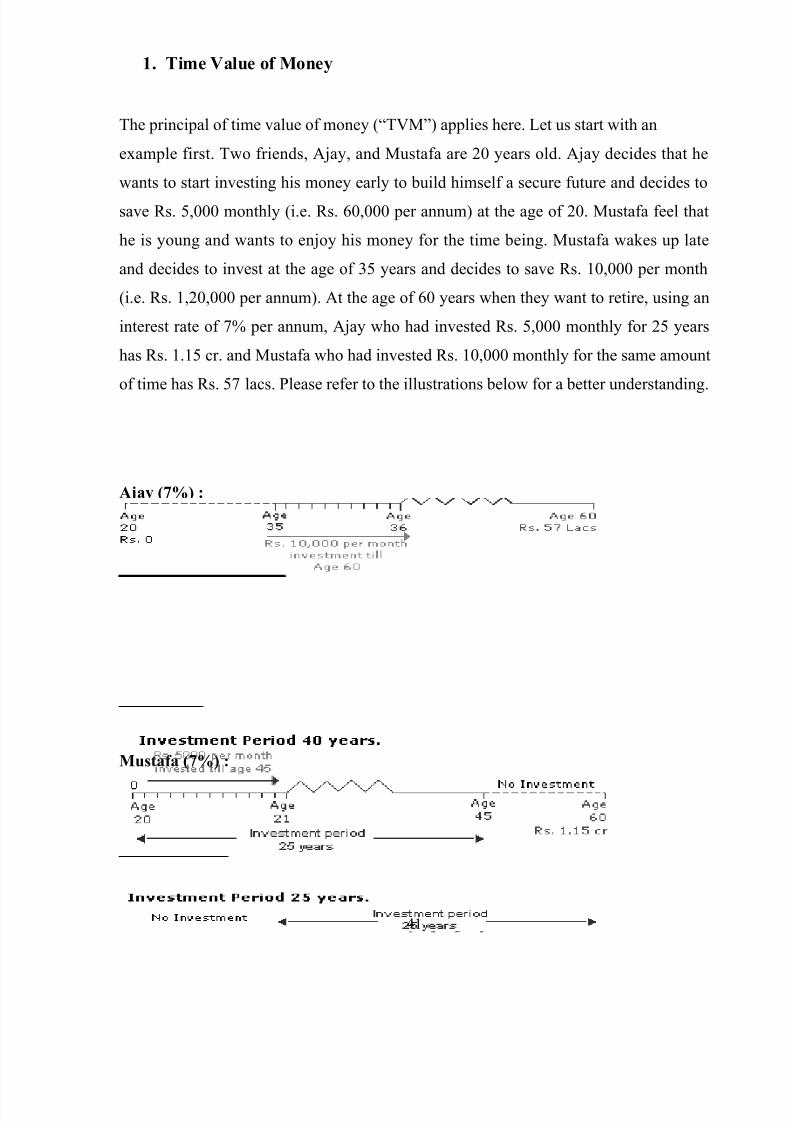

1. Time Value of Money

The principal of time value of money (“TVM”) applies here. Let us start with an

example first. Two friends, Ajay, and Mustafa are 20 years old. Ajay decides that he

wants to start investing his money early to build himself a secure future and decides to

save Rs. 5,000 monthly (i.e. Rs. 60,000 per annum) at the age of 20. Mustafa feel that

he is young and wants to enjoy his money for the time being. Mustafa wakes up late

and decides to invest at the age of 35 years and decides to save Rs. 10,000 per month

(i.e. Rs. 1,20,000 per annum). At the age of 60 years when they want to retire, using an

interest rate of 7% per annum, Ajay who had invested Rs. 5,000 monthly for 25 years

has Rs. 1.15 cr. and Mustafa who had invested Rs. 10,000 monthly for the same amount

of time has Rs. 57 lacs. Please refer to the illustrations below for a better understanding.

Ajay (7%) :

Mustafa (7%) :

41

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 42/71

2. DIVERSIFICATION

The nuclear weapon in your arsenal for your fight against Risk. It simply means that

you must spread your investment across different securities (stocks, bonds, money

market instruments, real estate, fixed deposits etc.) and different sectors (auto, textile,

information technology etc.). This kind of a diversification may add to the stability of

your returns, for example during one period of time equities might under perform but

bonds and money market instruments might do well enough to offset the effect of a

slump in the equity markets. Similarly the information technology sector might be

faring poorly but the auto and textile sectors might do well and may protect you

principal investment as well as help you meet your return objectives.

3. INFLATION

Things you hear people talk about:

“Rs. 100 today is worth more than Rs. 100 tomorrow.”

“Remember the time when a bus ride costed 50 paise?”

“Mehangai Ka Jamana Hai.”

The root cause, Inflation. Inflation is the loss of purchasing power over time. A lot of

times people make conservative investment decisions to protect their capital but end up

with a sum of money that can buy less than what the principal could at the time of the

investment. This happens when inflation grows faster than the return on your

investment. A well-diversified portfolio with some investment in equities might help

mitigate this risk.

4. DAY TRADING

More often than not we find investors buying stocks in companies suggest by their

friends, while not knowing what the company does or how it is performing. The aim -

to make a quick buck. The result – they may probably lose their money. We believe in

buying value, it is imperative that you either do your homework or hire a professional

42

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 43/71

financial advisor to do it for you. Buying and holding undervalued securities is the

probably the best way to beat the market.

5. LIQUIDITY

This depends on your cash requirements. If you feel that you might need the funds that

your are investing say sometime in the near future you might consider investing in

liquid assets or plan your cashflows accordingly. Higher liquidity translates into lower

returns and consequently lower risk.

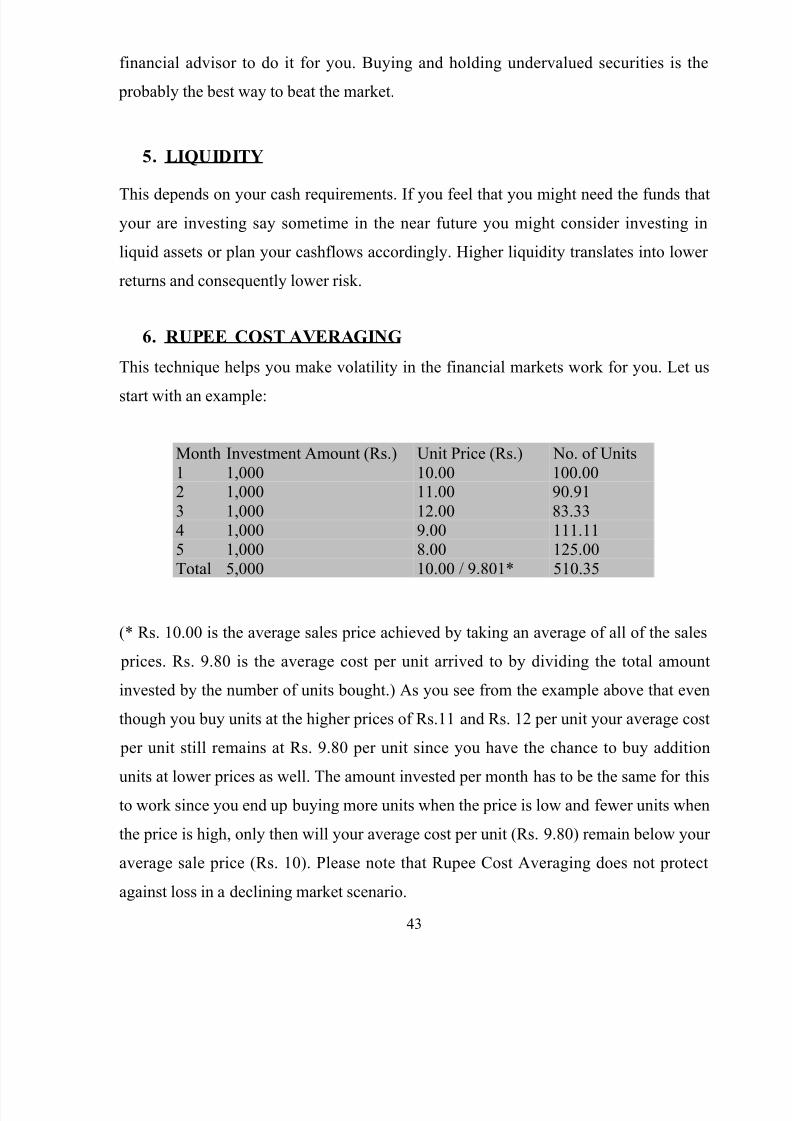

6. RUPEE COST AVERAGING

This technique helps you make volatility in the financial markets work for you. Let us

start with an example:

Month Investment Amount (Rs.) Unit Price (Rs.) No. of Units

1 1,000 10.00 100.002 1,000 11.00 90.91

3 1,000 12.00 83.33

4 1,000 9.00 111.11

5 1,000 8.00 125.00

Total 5,000 10.00 / 9.801* 510.35

(* Rs. 10.00 is the average sales price achieved by taking an average of all of the sales

prices. Rs. 9.80 is the average cost per unit arrived to by dividing the total amount

invested by the number of units bought.) As you see from the example above that even

though you buy units at the higher prices of Rs.11 and Rs. 12 per unit your average cost

per unit still remains at Rs. 9.80 per unit since you have the chance to buy addition

units at lower prices as well. The amount invested per month has to be the same for this

to work since you end up buying more units when the price is low and fewer units when

the price is high, only then will your average cost per unit (Rs. 9.80) remain below your

average sale price (Rs. 10). Please note that Rupee Cost Averaging does not protect

against loss in a declining market scenario.

43

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 44/71

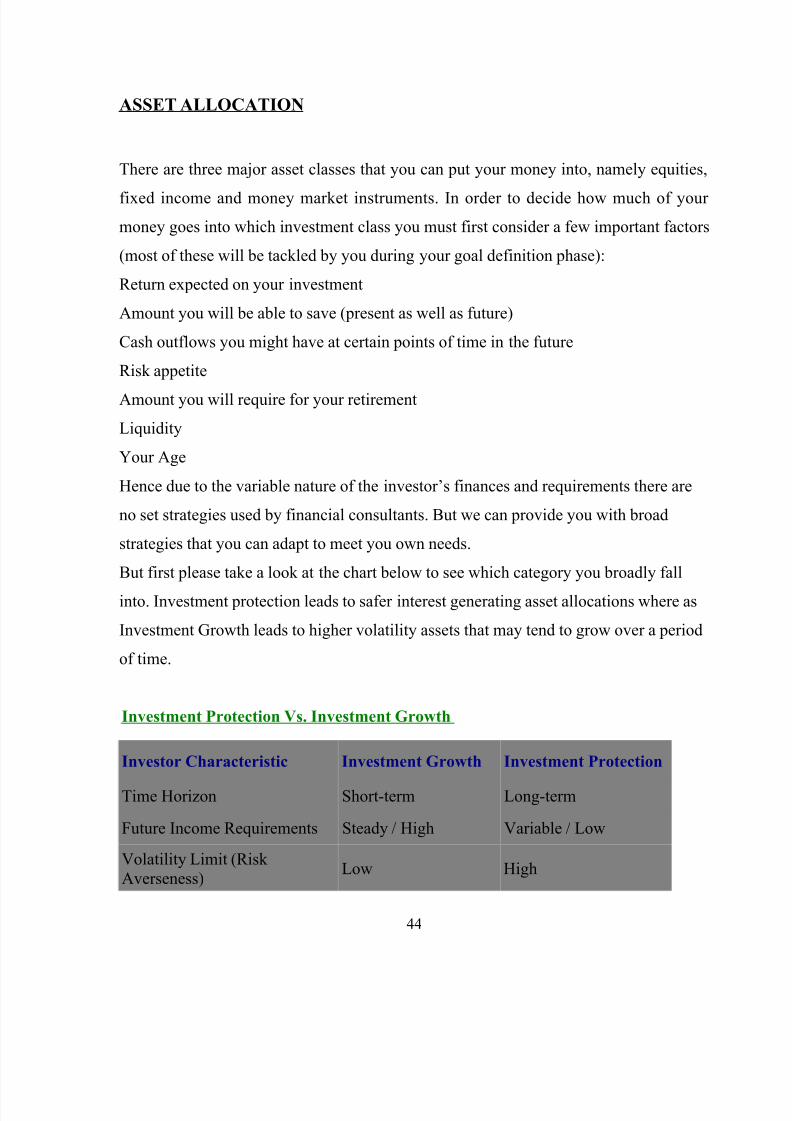

ASSET ALLOCATION

There are three major asset classes that you can put your money into, namely equities,

fixed income and money market instruments. In order to decide how much of your

money goes into which investment class you must first consider a few important factors

(most of these will be tackled by you during your goal definition phase):

Return expected on your investment

Amount you will be able to save (present as well as future)

Cash outflows you might have at certain points of time in the future

Risk appetite

Amount you will require for your retirement

Liquidity

Your Age

Hence due to the variable nature of the investor’s finances and requirements there are

no set strategies used by financial consultants. But we can provide you with broad

strategies that you can adapt to meet you own needs.

But first please take a look at the chart below to see which category you broadly fall

into. Investment protection leads to safer interest generating asset allocations where as

Investment Growth leads to higher volatility assets that may tend to grow over a period

of time.

Investment Protection Vs. Investment Growth

Investor Characteristic Investment Growth Investment Protection

Time Horizon Short-term Long-term

Future Income Requirements Steady / High Variable / Low

Volatility Limit (Risk

Averseness)Low High

44

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 45/71

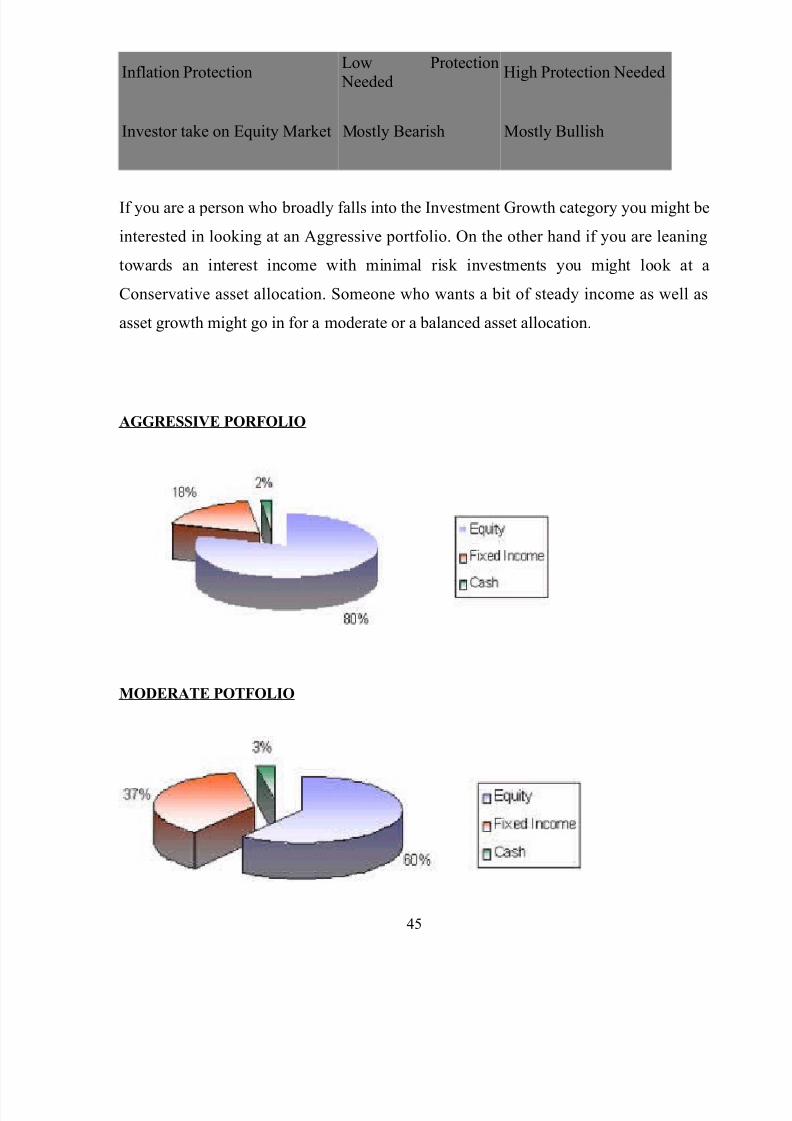

Inflation ProtectionLow Protection Needed

High Protection Needed

Investor take on Equity Market Mostly Bearish Mostly Bullish

If you are a person who broadly falls into the Investment Growth category you might be

interested in looking at an Aggressive portfolio. On the other hand if you are leaning

towards an interest income with minimal risk investments you might look at a

Conservative asset allocation. Someone who wants a bit of steady income as well as

asset growth might go in for a moderate or a balanced asset allocation.

AGGRESSIVE PORFOLIO

MODERATE POTFOLIO

45

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 46/71

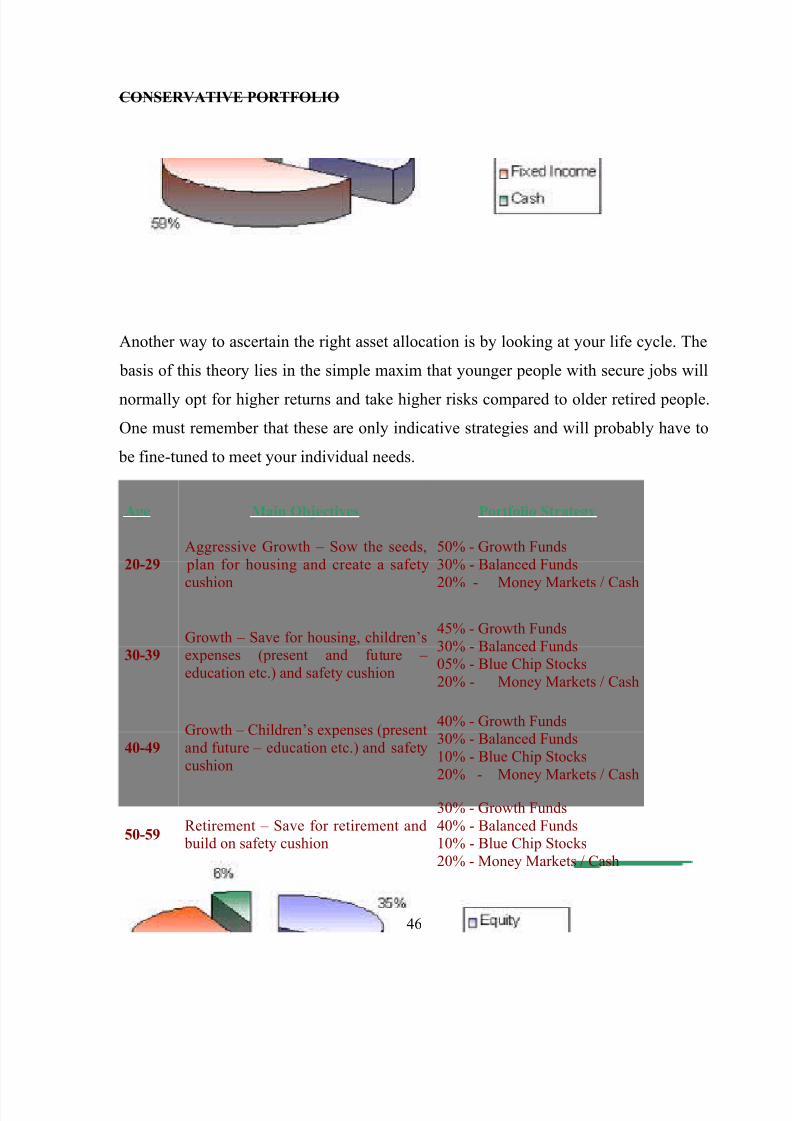

CONSERVATIVE PORTFOLIO

Another way to ascertain the right asset allocation is by looking at your life cycle. The

basis of this theory lies in the simple maxim that younger people with secure jobs will

normally opt for higher returns and take higher risks compared to older retired people.

One must remember that these are only indicative strategies and will probably have to

be fine-tuned to meet your individual needs.

Age Main Objectives Portfolio Strategy

20-29

Aggressive Growth – Sow the seeds,

plan for housing and create a safety

cushion

50% - Growth Funds

30% - Balanced Funds

20% - Money Markets / Cash

30-39

Growth – Save for housing, children’sexpenses (present and future –

education etc.) and safety cushion

45% - Growth Funds

30% - Balanced Funds05% - Blue Chip Stocks

20% - Money Markets / Cash

40-49

Growth – Children’s expenses (present

and future – education etc.) and safety

cushion

40% - Growth Funds30% - Balanced Funds

10% - Blue Chip Stocks

20% - Money Markets / Cash

50-59Retirement – Save for retirement and build on safety cushion

30% - Growth Funds

40% - Balanced Funds10% - Blue Chip Stocks

20% - Money Markets / Cash

46

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 47/71

60-69Safety – Preserve investments/ savings

and opt for minimal growth

10% - Balanced Funds

15% - Income Funds

10% - Blue Chip Stocks20% - Dividend Stocks

30% - Certificates of Deposits

(Shorter-term)15% - Money Markets / Cash

70 + Safety – Preserve investments/ savings

30% - Income Funds25% - Dividend Stocks

35% - Certificates of Deposits(Shorter-term)

10% - Money Markets / Cash

47

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 48/71

Investmen

tAvenues

INVESTMENT AVENUES

48

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 49/71

Apart from illiquid avenues like real estate, jewellery there are four major investment

avenues available to you, namely:

Debt Instruments

Equity

Money Market Instruments

Mutual Funds

• Debt Instruments

Traditionally debt instruments are known for generating a predetermined income for a

given period of time, other than in cases of default. Hence they are also known as fixed

income instruments. Some examples include:

NBFC Deposits

Company Deposits

Bonds

Debentures

Bank Deposits (FDs and savings accounts)

Government Small Savings Schemes (E.g. PPF)

The introduction of Floating Rate securities moves away from the concept of receivinga fixed rate of interest but suggests a variable rate of interest based on an underlying

factor such as London Interbank Offer Rate (“LIBOR”) or Mumbai Interbank Offer

Rate (“MIBOR”). An example of such a security is a Floating Rate Bond whose interest

rate is MIBOR plus 50 basis points, where MIBOR is variable.

A preference share is a hybrid instrument, which can be categorized as a fixed income

instrument since the investors receive a fixed dividend before the regular equity holdersreceive their dividend.

• Equity

49

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 50/71

Is a share in the ownership of a company’s assets and earnings. Companies usually

issue equity when they require addition capital to fund their existing business or

expand. At this point of time the company sells part of the ownership of the company to

the public. Listed equities are generally highly liquid since they are traded in the stock

exchange.

An investor makes money from equity through dividends paid out by the company

(from its profits) on a periodic basis as well as capital appreciation as reflected in the

stock price, which fluctuates in the market. Hence an investors returns are directly

related to the performance of the company’s business. Equities do not offer any assured

returns, but

historically promise the highest return in the long run, as depicted by the graph below.

Investment Returns (CAGR 1980 – 1998)

• Money Market Instruments

50

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 51/71

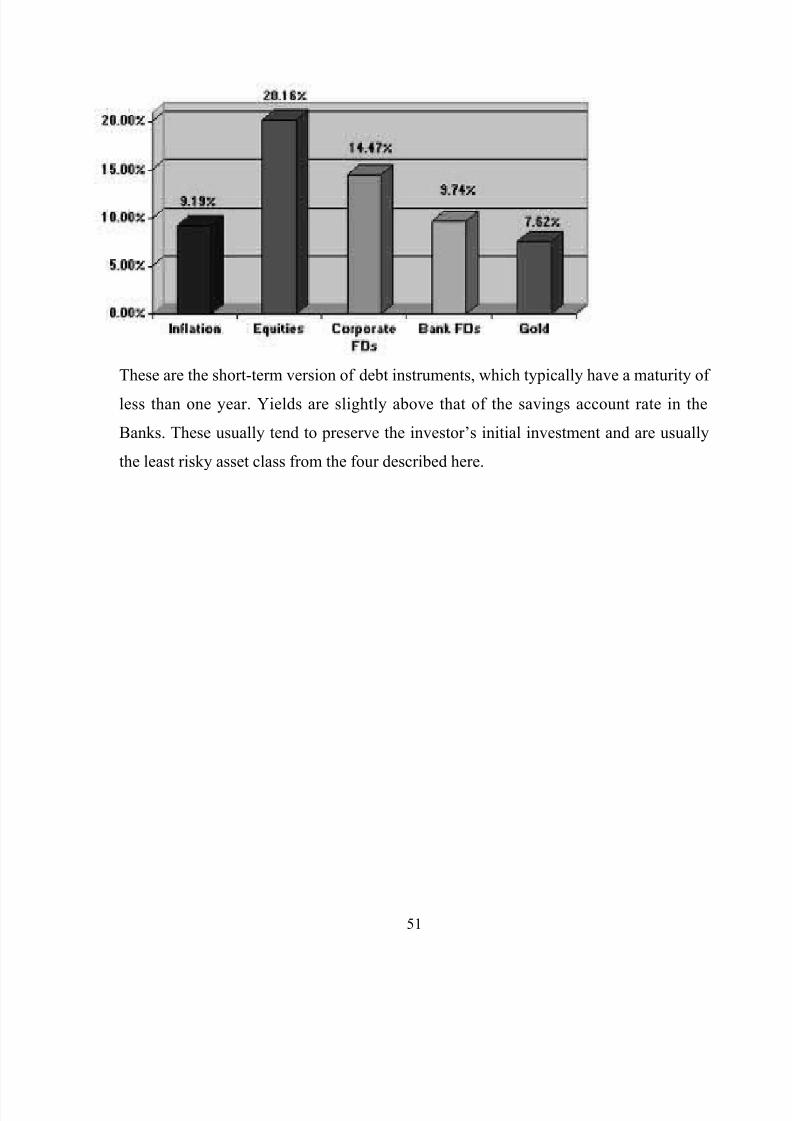

These are the short-term version of debt instruments, which typically have a maturity of

less than one year. Yields are slightly above that of the savings account rate in the

Banks. These usually tend to preserve the investor’s initial investment and are usually

the least risky asset class from the four described here.

51

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 52/71

Comparativ

e Analysis

52

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 53/71

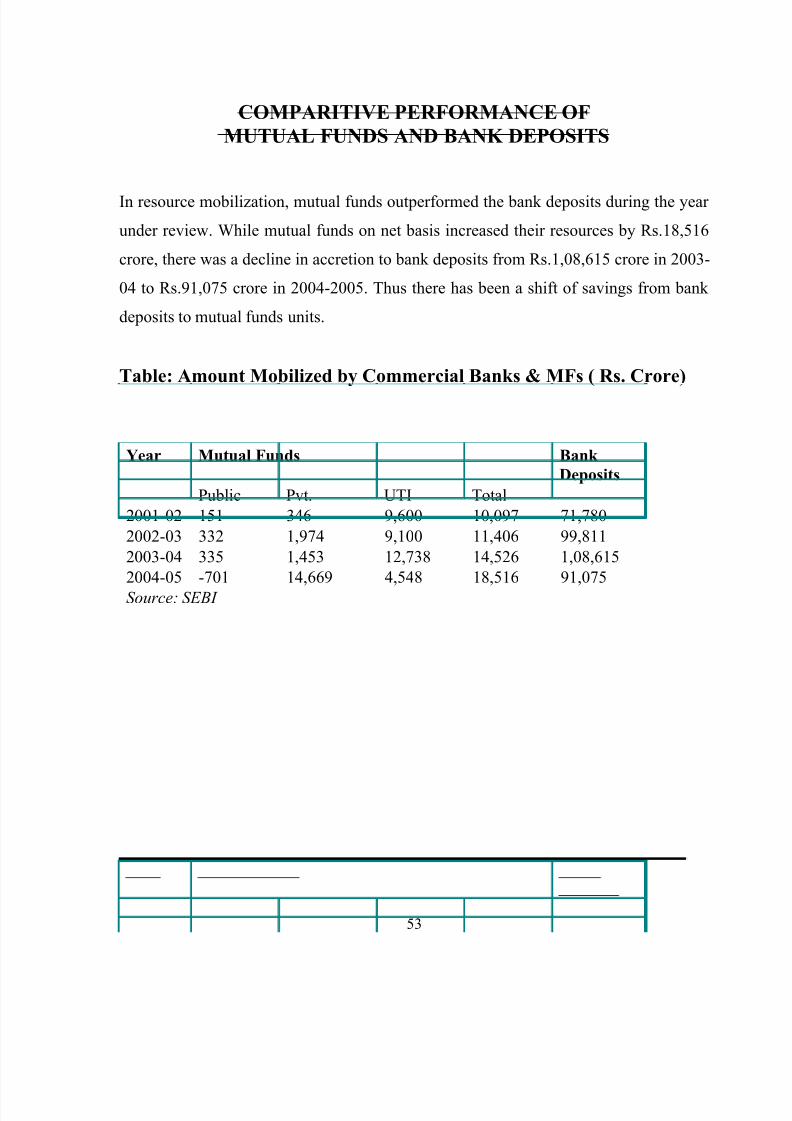

COMPARITIVE PERFORMANCE OF

MUTUAL FUNDS AND BANK DEPOSITS

In resource mobilization, mutual funds outperformed the bank deposits during the year

under review. While mutual funds on net basis increased their resources by Rs.18,516

crore, there was a decline in accretion to bank deposits from Rs.1,08,615 crore in 2003-

04 to Rs.91,075 crore in 2004-2005. Thus there has been a shift of savings from bank

deposits to mutual funds units.

Table: Amount Mobilized by Commercial Banks & MFs ( Rs. Crore)

Year Mutual Funds Bank

Deposits

Public Pvt. UTI Total

2001-02 151 346 9,600 10,097 71,780

2002-03 332 1,974 9,100 11,406 99,811

2003-04 335 1,453 12,738 14,526 1,08,615

2004-05 -701 14,669 4,548 18,516 91,075

Source: SEBI

53

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 54/71

Purchasing/SellingOf

Mutual Funds

54

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 55/71

Purchasing / Selling Mutual Funds

Purchasing mutual funds

Purchasing during IPO

Like companies, even mutual funds offer initial public offering. It is when they launch

the scheme for the first time. You can buy units at par (usually Rs.10) on this occasion.[

Purchasing existing mutual fund units

You can buy units of an open-ended scheme any time at the NAV-related price. Most

mutual funds charge an entry load of up to 2-2.5%. This is the additional amount you

have to shell out to buy the units. You can buy the scheme directly from the mutual

fund or through its distributor.

Selling mutual funds

You can sell or redeem units very easily. As per Sebi guidelines, a mutual fund unit

holder has the right to receive redemption or repurchase proceeds within 10 days of the

redemption or repurchase request.

When should you sell your mutual fund investment is a crucial question. Ideally, you

should sell when you have met your target profit. The other reason is that you need the

money or your profile has changed due to some changes in your life situation. Other

than this, you should sell the units if you find that the fund has been taken over by

another mutual fund house, whose investment philosophy, reputation, etc. you are not

comfortable with. Any major changes in the objective of the fund or a sharp rise in

55

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 56/71

expenses could also be valid reasons to redeem units. Following a favorite fund

manager is also a usual practice. However, it need not be always rewarding.

Speedy investment, redemption and income receipts

Thanks to the Electronic Clearing Services (ECS), a mutual fund investor now has the

option of automatic credit of dividends and redemptions into his bank account. This

saves a lot of paperwork, for both the investor and the fund.

Income from Mutual Funds

Mutual funds distribute their income as dividend. An investor has the option of

receiving the dividend or opting for reinvestment of the dividend. Another choice

before him is the growth or cumulative option. In this case, there is no dividend

declared. The appreciation in the corpus is reflected in growth in the value of the NAV.

The only difference between the dividend reinvestment option and the growth option is

that in case of the former, the investor gets more units depending on the dividend

declared and the NAV of the scheme on date of declaration of the dividend while incase of the latter, there is no change in the number of units but the NAV value increases

with increase in market value of the scheme’s investments.

Deciding between the dividend reinvestment option and the growth option is mainly on

account of tax*.

In the case of equity mutual funds, if the investor holds on to his investment for more

than a year, capital gain earned on sale of the units is termed as long-term capital gain,

which is completely tax-free. Also, dividends declared by equity mutual funds are

completely tax-free. Hence, deciding between dividend and growth in this case makes

56

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 57/71

no difference. However, if the equity mutual fund is held for less than one year, capital

gains on sale of the units are termed as short-term capital gains and are taxable at the

rate of 10%. In this case, it makes more sense to opt for dividend, which is tax-free.

In the case of debt mutual funds

If the investor holds on to his investment for more than a year, capital gain earned on

sale of the units is termed as long-term capital gain, which is taxable at 10% without

indexation or 20% with indexation. Dividends declared by debt mutual funds attract a

dividend distribution tax of 13.07% in case of individual investors and 20.91% in case

of corporate investors. In this case, if the investor needs liquidity, he can opt for the

dividend payout option. However, if he is looking at capital appreciation, it makessense to opt for the growth option

57

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 58/71

SelectionOf

MutualFund

58

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 59/71

SELECTING A MUTUAL FUND

Your objective

The first point to note before investing in a fund is to find out whether your objective

matches that of the scheme. It is necessary, as any conflict would directly affect your

prospective returns. For example, a scheme that invests heavily in mid-cap stocks is not

suited for a conservative equity investor. He should be better off in a scheme, which

invests mainly in blue chips. Similarly, you should pick schemes that meet your

specific needs. Examples: pension plans, children’s plans, sector-specific schemes, etc.

Your risk capacity and capability

This dictates the choice of schemes. Those with no risk tolerance should go for debt

schemes, as they are relatively safer. Aggressive investors can go for equity

investments. Investors that are even more aggressive can try schemes that invest in

specific industries or sectors.

Fund Manager’s and scheme’s track record

Since you are giving your hard-earned money to someone to manage it, it is imperative

that he manages it well. It is also essential that the fund house you choose has an

acceptable track record. It also should be professional and maintain high transparency

in operations. Look at the performance of the scheme against relevant market

59

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 60/71

benchmarks and its competitors. Look at the performance over a longer period, as it

will reveal how the scheme has fared in different market conditions.

Cost factor

Though the AMC fee is regulated, you should look at the expense ratio of the fund

before investing. This is because the money is deducted from your investments. A

higher entry load or exit load also will eat into your returns. A higher expense ratio can

be justified only by superlative returns. It is very crucial in a debt fund, as it will devour

a few percentages from your modest returns

60

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 61/71

Performance

of Mutual

Funds61

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 62/71

PERFORMANCE AND GROWTH OF MUTUAL FUND INDUSTRY

GROWTH IN ASSETS UNDER MANAGEMENT

62

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 63/71

RESOURCES MOBILIZED BY MUTUAL FUNDS

The mutual funds during 1998-99 suffered a serious set back by reporting a sharp

decline in net resource mobilization. There was a net outflow of Rs.950 crore during the

entire year. The concern for this situation got reflected in the incentives offered to

mutual funds scheme in the Union Budget for 1999-2000.

The performance has been extremely good during 2003-2004 as the gross amount

mobilised by them increased to Rs. 61,241.23 from Rs. 22,710.73 crore during 2003-04

showing an increase of around 170 per cent in 2004-05. The Government exempted the

income of unit holders received from UTI or from mutual fund. The Government

further exempted income distributed under the US-64 scheme and other open-ended

equity oriented schemes of UTI and mutual funds from the 10 per cent flat rate of tax.

These fiscal incentives have favourably impacted the resource mobilisation by the

mutual funds industry. However, redemption had been very heavy which form nearly

more than 100 per cent in 2002-03 and 69 per cent during the current financial year.

As regards the net resource mobilisation, there has been a massive inflow of

Rs.18,969.88 crore during the current financial year under review as against a net

outflow of Rs.949.67 crore during the entire financial year of 2003-04.

Details of funds mobilised, repurchase/redemption amount and the net inflow/outflowof funds for the financial year 2004-05 are given in Annexure 1.

As regards sector-wise performance, there was a net inflow of Rs.15,426.77 crore in

case of private sector mutual funds (net inflow of Rs.1,452.70 crore during 2002-04)

followed by UTI with a net inflow of Rs.4,548.32 crore (net outflow of Rs.2,737.53

crore during 2003-04). On the contrary there was a net outflow of Rs.744.92 crore in

case of public sector mutual funds (net inflow of Rs.335.16 crore during 2003-04) due

to massive redemption / repurchase of close ended schemes. Thus it is found that

probably organizational and ownership structure have been influencing the performance

of mutual funds.

63

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 64/71

It is observed that in case of private and public sector mutual funds, the entire net

inflow of fund has been from open-ended schemes and there was net outflow in respect

of close-ended schemes. However, incase of UTI, 77.28 per cent of net inflow has been

from the close-ended schemes.

TRACKING PERFORMANCE OF MUTUAL FUNDS SCHEMES

Objective parameters

You can assess the performance of your mutual fund investment by computing

appreciation in the NAV of the scheme over different periods of time on a stand-alone

basis (one month, three months, six months, one year, three years, since inception),

against relevant benchmarks and against average returns offered by mutual funds in the

same category. For example, if you have invested in a diversified equity fund, you can

benchmark your return against the BSE Sensex, as it is representative of the whole

market. If your fund has outperformed the Sensex, you can be sure that the fund

manager has done a good job. However, if he is lagging the benchmark, you shouldclosely watch the fund (its investment strategy, portfolio, etc.) and quit it if there is no

improvement in its performance.

Subjective parameters

The performance alone does not make a fund house a winner. Equally important is the

service standards and transparency in actions. It is also essential that the fund should

offer speedy solutions to grievances of investors. The reputation of the fund house

among its investors and public at large indicates how well the fund scores on this front.

Information sources

64

8/2/2019 deepak Soni

http://slidepdf.com/reader/full/deepak-soni 65/71

Every financial daily offers daily NAVs of all mutual fund schemes. Magazines also

come out with annual survey of mutual funds. There are even magazines dedicated

entirely towards mutual fund industry. Internet is also a great place for information.

There are dedicated sites as well as financial sites, which offer information on mutual