Embed Size (px)

Citation preview

DEEP CYCLICAL INVESTING: GETTING IT RIGHT MARCH 2016

FOR PROFESSIONAL CLIENTS ONLY

Cyclical investing is often likened to a rollercoaster ride. It’s an over used, but sometimes fitting analogy: a series of dramatic highs and lows, both exhilarating and nerve shredding. In reality though, cyclical investing need not warrant such an adrenalin-fuelled reputation. Indeed, for investors that are disciplined enough to ignore the perennial noise of markets, deeply cyclical businesses can present attractive ‘contrarian’ opportunities, as the market often has difficulties valuing these properly beyond the short term.

Matthew FranklinInvestment Analyst

www.martincurrie.com/active

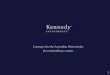

Stages of the cycle

Although it’s difficult to know with any ‘real-time’ precision where one is in the cycle, it is helpful to divide it into different phases, with the amplitudes characterised alternately by pessimism and optimism. In the later stages of an up-cycle, markets tend to price in the elevated levels of earnings by reducing the price to earnings (p/e) ratio. This is the ‘de-rating’ phase, a tricky period as investors can get wrong-footed by seemingly attractive valuations, but with earnings having little upside potential. The autos sector currently is a good example of this.

The converse of this is the ‘re-rating’ phase. As soon as investors get even the slightest hint that the bottom may have been reached, shares tend to get re-valued very swiftly. To catch these potentially explosive up-moves, an investor has to react very fast and this, unsurprisingly, isn’t easy. The critical period, therefore, is the time directly preceding this. Importantly, we aim to complete research on a company well in advance of a purchase decision being made, so that we have sufficient conviction in the final ‘reactive’ stage when investors are moving en masse. Leaving the analysis until the first ‘green shoots’ arrive, more often than not, means you will be too late.

active VIEWPOINT: ALL CYCLICALS ARE NOT CREATED EQUAL

Many investors will have some notion of the stylised version of the business cycle, with its regular and symmetrical peaks and troughs. Needless to say, reality is somewhat messier, and anyone doubting this can examine the track record of macroeconomic forecasters for proof. Turning points are notoriously difficult to identify, as we have an innate tendency to extrapolate from the immediate past. However, long-term investors do not necessarily have to get the timing exactly right to make good returns. As the saying goes, better to be roughly right than precisely wrong.

Hunting down ‘cyclical compounders’

As the label suggests, cyclical companies’ earnings and cash flows fluctuate along with general economic conditions. Industries related to commodities and those producing heavy industrial equipment, fall into this category. Open any financial paper these days, and odds are that there will be at least one piece about energy and materials companies facing hard times. But cyclical companies are by no means created equal, and, as always, the challenge for investors is to separate the wheat from the chaff. I look for what I call a ‘cyclical compounder’, which is a business whose earnings will move with the cycle, but where the structural trend is positive and driven principally by organic growth and the incremental return on investment.

Peaks and troughs – knowing where you are

Navigating Japanese cyclicality – Christopher Taylor, Portfolio Manager Japan

In many markets, it can be fruitful to seek cyclical stocks with a secular growth trend in their main business and to buy when the cycle is low; although it may not be possible to call the bottom with any precision, on average the growth element will produce decent risk-adjusted returns. In Japan, however, traditional cyclical sectors such as steel and bulk chemicals face significant secular headwinds. Their customers in the auto and electronics industries have often moved – or are moving – production offshore. And attempting to set up new bases, in China for example, is difficult or impossible for basic industries due to strong competition from low-cost local players, as well as many other barriers to entry. This is in contrast to many Japanese parts-and-services suppliers that have successfully followed their customers abroad. Japanese basic industries also face significant and growing import competition from new Asian players in their home market.

Where value can be found is in companies that have successfully diversified and moved up the value chain, for example from bulk chemicals to fine chemicals; or from commodity plastics to specialised films used in smartphones. Of course, stock prices can be dragged down from time to time by concerns over legacy deep cyclical businesses, but we believe that in many cases this provides a buying opportunity. Here we tend to look for companies that exercise tight cost control in and have lean assets, but are prepared to invest in new areas where they have a defendable technological or manufacturing edge and can steadily build value over time.

On the other hand, in our long/short funds, we also look for short opportunities relating to businesses in decline, unsuccessful diversification strategies and weak balance sheets, when cyclical upswings drive up share prices. Industry consolidation can create opportunities on both the long and the short side of the portfolio, as political and other considerations not related to the fundamental value of companies often lead to mergers and acquisitions at valuations which are either materially too low or too high.

Earn

ings

per

sha

re (E

PS)

Time

EPSTrendline

De-ratingstage

Panicstage Re-rating

stage

Preparationstage

Seeing the wood for the trees

It goes without saying that there is no fool-proof way of valuing deeply cyclical businesses, nor any other company for that matter, but there are some helpful rules of thumb.

Short-term multiples can be highly misleading, so it is important to try to assess where the trend lies. One shorthand way is to look at normalised, mid-cycle earnings per share and to multiply this by a reasonable mid-cycle multiple, based on organic growth potential, returns and strength of the company’s competitive ‘moat’. That said, a multi-faceted approach, including discounted cash flow (DCF) and balance sheet analysis is ultimately needed to build a truly holistic picture.

Focusing excessively on consensus can be very dangerous, with sell-side analysts tending to be behind the cycle, while the buy-side is out in front. Nonetheless, it is important to try to gauge where market expectations are. Buying when there may still be risk of a 10–20% move to the downside can sometimes make sense if sufficient confidence can be established that there is real long-term value. But caution is required. Indeed, impulsive investors risk catching the proverbial ‘falling knife’ at this point. And steering clear of

PAGE 3

lower-quality (highly leveraged) businesses is important in this regard, as some of these may never make it out of a trough.

The difficulty of getting the timing right is an inherent drawback of cyclical investing. Even seasoned stock pickers can rush in too early, and staying the course can test the nerves of the most stoic of investors. Nor is history necessarily a reliable guide. Take a well-established name like Caterpillar, which has just had three consecutive negative years for the first time since the Second World War – and now 2016 looks like it will be the fourth. What is more, finding concrete signposts is not an easy task. Although it’s certainly possible to identify a company that looks very attractive on a medium-term basis, there is rarely enough (tangible) evidence to corroborate prognostications of a rebound.

…a multi-faceted approach, including discounted cash flow (DCF) and balance sheet

analysis is ultimately needed to build a truly holistic picture.

The information provided should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any of the securities discussed here were, or will prove to be, profitable.

I keep a close eye on margins, as the absence of upside potential often means that there is a risk of compression, even if the market or management refer to it as a mere ‘plateau’. Pricing is also vitally important, and this tends to be affected more during prolonged (rather than short and sharp) downturns. More positively, one should not forget the phenomenon of de-stocking, which can have a very powerful impact and create opportunities for businesses when it causes demand to fall well below underlying activity.

Focusing on the structural trend

In short, while cyclical businesses inevitably come with more risk, they shouldn’t be lumped together indiscriminately. By focusing on quality and structural trends I believe it is possible to find businesses where the risk-reward profile is very compelling. And for me, the key is to buy these companies during the bleaker stage of the cycle, when they have fallen out of favour, and to avoid them when investors’ spirits are high. In some ways this is the archetypal contrarian approach to investing, and although great care is unquestionably needed, we believe deep cyclical opportunities can be found even during the most tumultuous of times.

Important lessons

There are numerous factors to take into consideration when looking at deeply cyclical companies. Critically, when examining a business I try to imagine a worst-case scenario 12 months down the line, factoring in how much negative operational leverage there is and how much protection we can expect from aftermarket activity. It is also important to try to determine if there is any structural deterioration in a company’s fundamentals. The cycle can often mask underlying changes, which can catch investors out when the times get tough. Importantly, rosy forecasts of the replacement cycle should be avoided as this always takes longer than expected to come through. Connected to this is the danger of assuming structural growth in businesses that are heavily exposed to capital expenditure, when such spending can clearly oscillate wildly with the cycle.

Cyclicals down under – Michael Slack, Portfolio Manager Australia

The Australian cyclical landscape is dominated by resources and associated service industries. The resources sector is characterised by high capital intensity and growth ambitions which manifests in individual commodities being turned from deficit markets to surplus markets over relatively short periods of time. The ensuing commodity price cycles can wreak havoc with earnings in the sector, thereby putting pressure on the ability of resources companies to sustain capital investment and returns to shareholders. This ebb and flow impacts the fortunes of related industries – for example, mining services, construction and equipment suppliers – with activity and pricing power tightly intertwined with the investment cycle of the ‘extractors’.

When looking for investment opportunities in these segments, we look for an anchor against which to judge relative value at any point in the cycle. We analyse commodity markets to identify where prices sit relative to incentive prices (the price required to justify investment in new capacity) and marginal cost (the position where prices intersect the cost curve, usually the 90th percentile, for the particular commodity). The interplay between marginal cost and incentive prices drives our normalised price assumption which, in turn, drives normalised company returns and our valuations.

Of course, we like to invest in these companies when their share prices are at the widest discount to our intrinsic, risk-adjusted valuations. However, picking the bottom of the share price cycle is often difficult as commodity prices and market expectations of future prices may continue to fall. To gain greater conviction, we look for the rate of change of these price falls and expectations to slow, and the absolute prices to reach a point on the cost curve where the balance of risk of future price movements is to the upside.

active VIEWPOINT: ALL CYCLICALS ARE NOT CREATED EQUAL

By focusing on quality and structural trends I believe it is possible to find businesses

where the risk-reward profile is very compelling. And for me, the key is to buy these

companies during the bleaker stage of the cycle, when they have fallen out of favour,

and to avoid them when investors’ spirits are high.

Important information

This information is issued and approved by Martin Currie Investment Management Limited (‘MCIM’). It does not constitute investment advice. The document may not be distributed to third parties and is intended only for the recipient. The document does not form the basis of, nor should it be relied upon in connection with, any subsequent contract or agreement. It does not constitute and may not be used for the purpose of an offer or invitation to subscribe for or otherwise acquire shares in any of the products mentioned.

The information contained has been complied with considerable care to ensure its accuracy. However, no representation or warranty, express or implied, is made to its accuracy or completeness. The opinions contained in this document are those of the named manager. They may not necessarily represent the views of other Martin Currie managers, strategies or funds.

Investors should also be aware of the following risk factors which may be applicable to the strategies shown in this document.

Investing in foreign markets introduces a risk where adverse movements in currency exchange rates could result in a decrease in the value of your investment.

For Investors in the USA, the information contained within this [presentation] is for Institutional Investors only who meet the definition of Accredited Investor as defined in Rule 501 of the United States Securities Act of 1933, as amended (‘The 1933 Act’) and the definition of Qualified Purchasers as defined in section 2 (a) (51) (A) of the United States Investment Company Act of 1940, as amended (‘the 1940 Act’). It is not for intended for use by members of the general public.

Any distribution of this material in Australia is by Martin Currie Australia Limited (‘MCA’). Martin Currie Australia is a division of Legg Mason Asset Management Australia Limited (ABN 76 004 835 849). Legg Mason Asset Management Australia Limited holds an Australian Financial Services Licence (AFSL No. AFSL 240827) issued pursuant to the Corporations Act 2001.

Martin Currie Investment Management Limited, registered in Scotland (no SC066107) Martin Currie Inc, incorporated in New York and having a UK branch registered in Scotland (no SF000300), Saltire Court, 20 Castle Terrace, Edinburgh EH1 2ES

Tel: (44) 131 229 5252 Fax: (44) 131 222 2532 www.martincurrie.com

Both companies are authorised and regulated by the Financial Conduct Authority. Martin Currie Inc, 1350 Avenue of the Americas, Suite 3010, New York, NY 10019 is also registered with the Securities Exchange Commission. Please note that calls to the above numbers may be recorded.

active VIEWPOINT is just one part of our range of investment materials. To access further perspectives on our strategies and key investment themes, visit our active library: www.martincurrie.com/active-library/

Get in touch

For further information visit our website www.martincurrie.com

Alternatively please call:

Edinburgh (headquarters)44 (0) 131 229 5252

London 44 (0) 20 7065 5970

Asia and Australia(61) 3 9017 8640

Media44 (0) 131 479 5892

New York(1) 212 258 1900

Global consultants 44 (0) 20 7065 5967

PAGE 5