Embed Size (px)

DESCRIPTION

Digital First Media CEO JOhn Paton's declaration in an ongoing case. Citizens for Two Voices alleges that a recent deal between the Deseret News and the ownership of the Salt Lake Tribune hurts the Tribune.

Citation preview

Richard D. Burbidge (#0497) [email protected] Jefferson W. Gross (#8339) [email protected] Carolyn LeDuc (#14240) [email protected] BURBIDGE MITCHELL & GROSS 215 South State Street, Suite 920 Salt Lake City, Utah 84111 Telephone: 801-355-6677 Facsimile: 801-355-2341 William Kolasky (pro hac vice – pending) [email protected] HUGHES HUBBARD & REED LLP 1775 I Street, N.W. Washington, D.C. 20006-2401 Telephone: 202-721-4600 Facsimile: 202-721-4646 Ethan E. Litwin (pro hac vice – pending) [email protected] HUGHES HUBBARD & REED LLP One Battery Park Plaza New York, NY 10004-1482 Telephone: 212-837-6540 Facsimile: 212-422-4726 Attorneys for Defendant Kearns-Tribune, LLC

Raymond J. Etcheverry (#1010) David M. Bennion (#5664) PARSONS BEHLE & LATIMER One Utah Center 201 South Main Street, Suite 1800 Salt Lake City, UT 84111 Telephone: (801) 532-1234 Facsimile: (801) 536-6111 Lee Simowitz (pro hac vice – pending) BakerHostetler Washington Square 1050 Connecticut Ave., N.W., Suite 1100 Washington, D.C. 20036-5034 Telephone: 202-861-1608 Facsimile: 202-861-1783 Attorneys for Defendant Deseret News Publishing Company

IN THE UNITED STATES DISTRICT COURT

FOR THE DISTRICT OF UTAH - CENTRAL DIVISION

UTAH NEWSPAPER PROJECT, dba CITIZENS FOR TWO VOICES, Plaintiff, vs. DESERET NEWS PUBLISHING COMPANY and KEARNS-TRIBUNE, LLC, Defendants.

DECLARATION OF JOHN PATON

Case No. 2:14-cv-00445-CW Judge Clark Waddoups

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 1 of 14

Declaration of John Paton

I, John Paton, declare under penalty of perjury that the foregoing is true and correct.

1. I am over the age of eighteen (18) years and have personal knowledge of the

statements of this Declaration. If called as a witness, I could competently testify to the

facts set forth in this Declaration.

2. I am the Chief Executive Officer of MediaNews Group, Inc., d/b/a Digital

First Media (“DFM”).1 I make this declaration in opposition to Plaintiff’s Motion for a

Preliminary Injunction. The facts set forth herein are based on my personal knowledge or

based on information contained in business records regularly maintained by DFM, unless

otherwise indicated.

My Background

3. I have spent my entire working life in and around the newspaper business. I

started my career as a newsroom copy boy. I am a journalist who was everything from a

reporter to an editor-in-chief, before becoming more involved on the business side of

running newspapers. I am dedicated to the proposition that journalism matters and to

finding business solutions to keep journalism viable. I fund two scholarships annually for

promising young journalism students at the Graduate School of Journalism of the City

University of New York where I also sit on the Board of Advisors. My university degree is

in journalism from Ryerson University where in 2006 I was named an Alumnus of

Distinction. I am a former governor of the National Newspaper Awards program in

Canada – that country’s “Pulitzer Prize” – and I was recently asked to join the Board of

1 Unless specifically referred to otherwise herein, all references to Digital First Media refer to MediaNews Group, Inc., d/b/a Digital First Media.

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 2 of 14

Overseers of the Columbia Journalism Review, which I accepted. In one form or another,

I have been running companies since 1995.

4. My involvement and interest in helping build digital platforms for

newspapers started in the late 1990s when I was first the Vice-President in charge of new

media for Sun Media Corporation in Canada and then CEO of Canadian Online Explorer

(“Canoe”) - with news operations at the time in Canada, France and Spain. Since then, I

have been recognized as one of the leaders in restructuring newspapers to compete

effectively in the digital world, including by The New York Times (Exhibit A) and The Pew

Research Center for Excellence in Journalism (Exhibit B). My work has led me to be

named as one of 15 “digital media influencers.” (Exhibit C.)

5. My leadership on digital issues has led to my being recruited to join a

number of media-related boards, namely: The Guardian in the UK, El Pais in Spain and

PRISA, a multi-media corporation also based in Spain, with divisions in more than 20

countries. The Guardian is currently the third-largest newspaper site in the

English-speaking world, while El Pais is quickly establishing a similar leading role in the

Spanish-speaking world. Both The Guardian and El Pais have been able to dramatically

expand their audiences and business opportunities by aggressively pursuing a “digital first”

strategy. I am a frequently sought-after speaker on digital transformation in the U.S. and

abroad. I have presented at annual conferences such as the Newspaper Association of

America, World Association of Newspapers, Global Editors Network and Online

Publishers Association.

6. My leadership on digital issues was recognized in 2009 when Editor &

Publisher named me Publisher of the Year citing my efforts in multi-platform publishing.

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 3 of 14

That recognition also led to my being recruited to the board of Journal Register Company

(“JRC”) in August 2009 by its creditors following its well-publicized bankruptcy. JRC’s

Board undertook a search for a new Chief Executive Officer and in December 2009 the

then-Chairman of JRC asked me to take on the job. I accepted and became CEO in

February 2010. In July 2011, JRC was sold to a company controlled by funds associated

with Alden Global Capital, which are also major stakeholders in MediaNews Group. In

September 2011, I became the Chief Executive Officer and a director of MediaNews

Group as well, running both MediaNews Group and JRC via a management company

called Digital First Media, LLC (f/k/a Digital First Media, Inc.).

7. After a series of transactions, the voting securities of the former JRC were

acquired by MediaNews Group in December 2013. MediaNews Group was then

rebranded and now does business under the Digital First Media name.

The Digital First Strategy

8. The newspaper industry is in trouble today because of the simple truth that

print is in steep decline and most newspapers are ill-prepared to compete in a digital world.

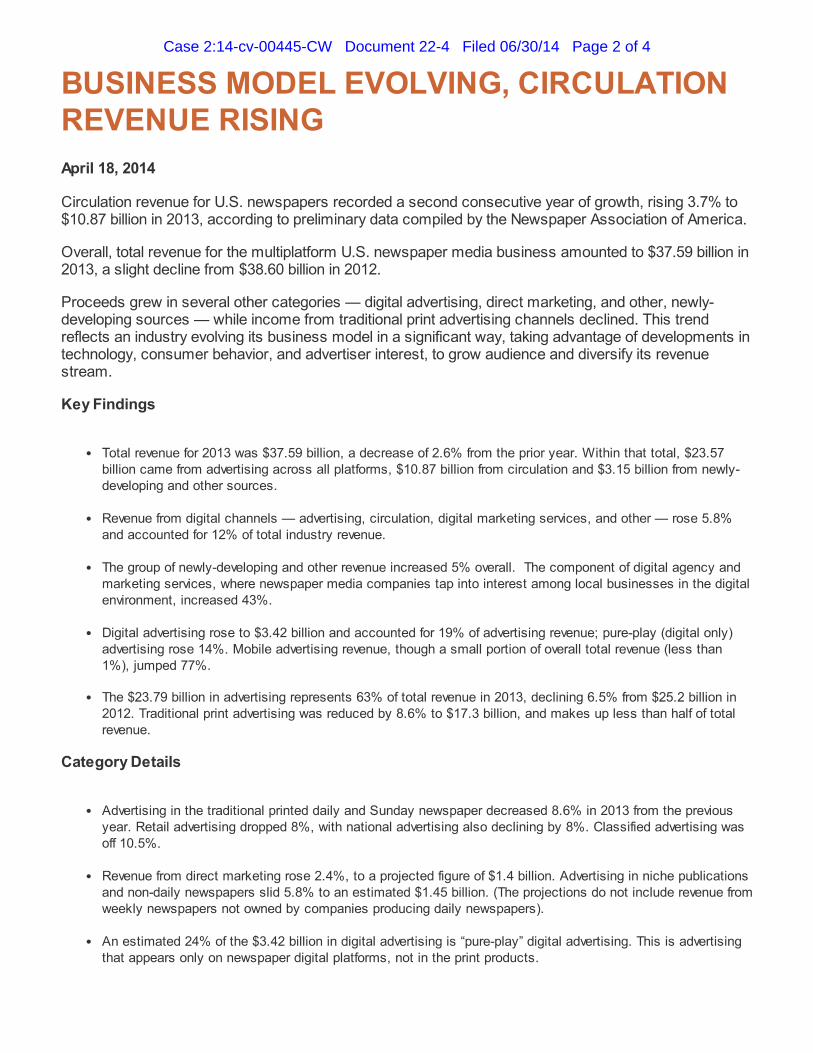

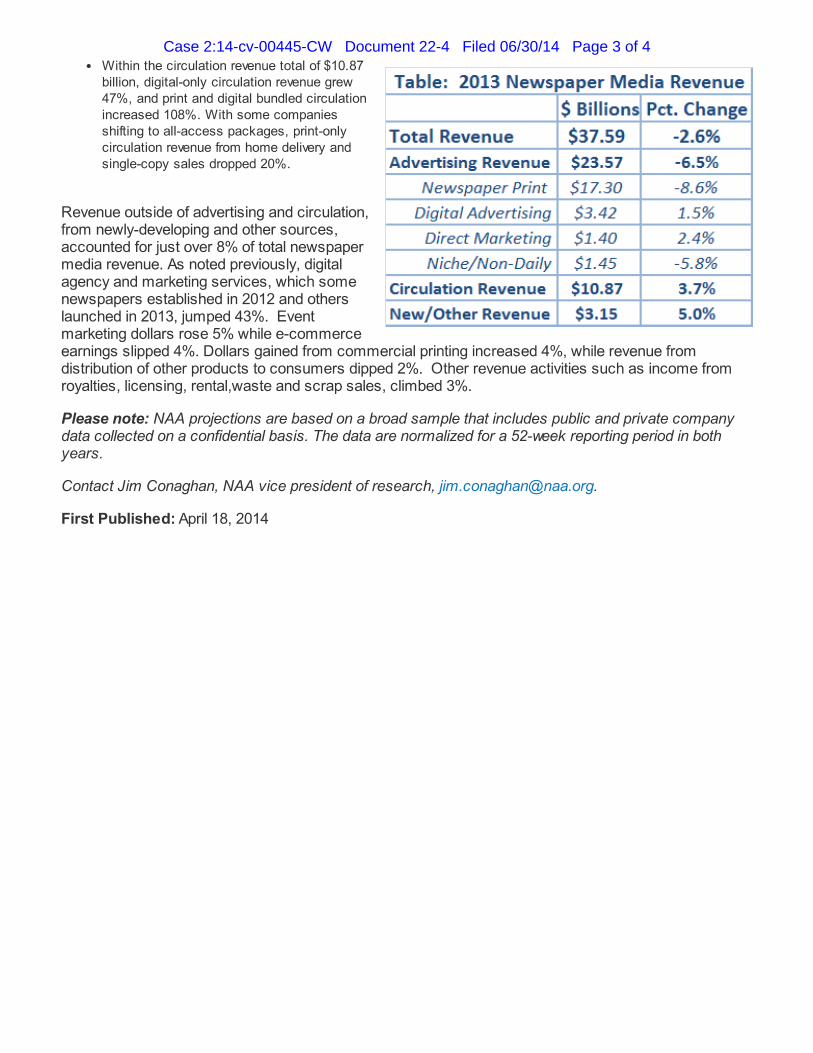

9. Revenues for print advertising have been declining every quarter since 2006

and, according to the Newspaper Association of America, among others, print revenues in

2013 were less than half their 2006 levels. (Exhibit D.)

10. Faced with this catastrophic decline in revenues, newspapers need to

aggressively innovate away from a reliance on print. The industry still has a long way to go

in its transformation - print advertising continues to account for approximately 46% of all

newspaper revenues, industry-wide, with print circulation accounting for another 30%.

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 4 of 14

According to industry sources, revenues generated by print advertising have fallen by 55%

since 2006. (Exhibit D.)

11. The world is rapidly moving away from print and to digital. We therefore

now have to compete with other media, especially new digital media, for readers and

advertisers in an increasingly competitive market. Over the last decade, as print

advertising has declined by more than half, digital advertising has grown exponentially.

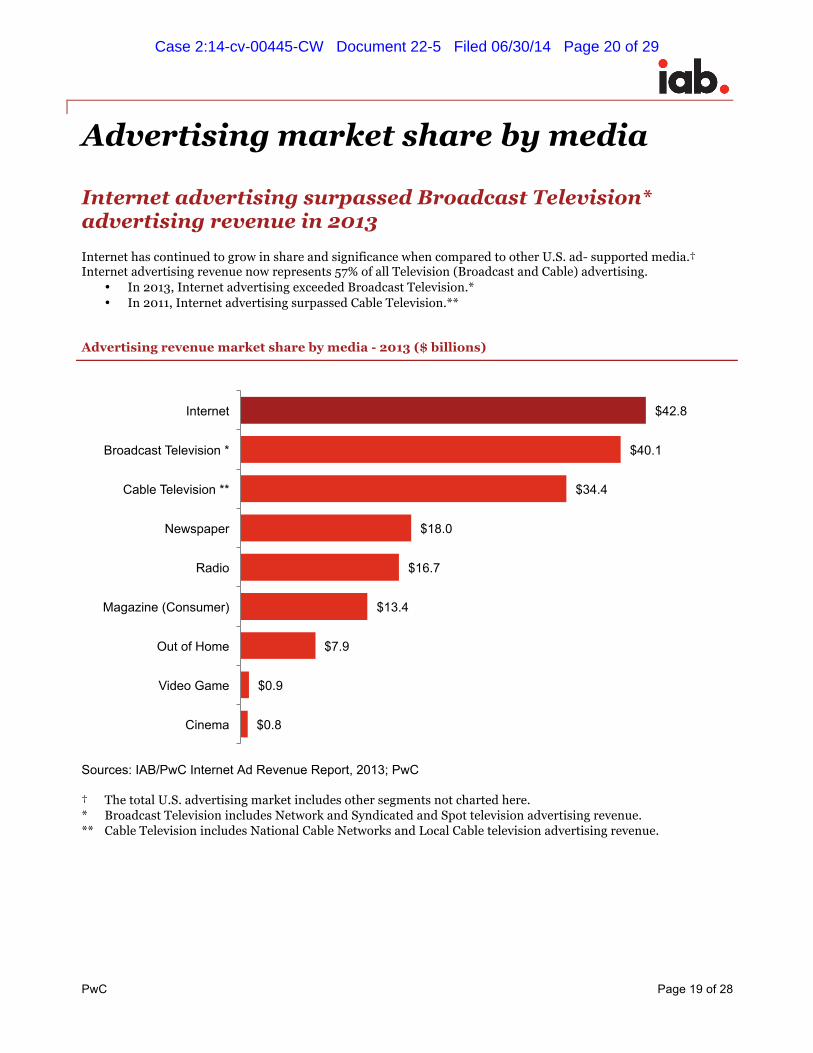

As a result, digital is now the largest medium for advertising, having surpassed broadcast

television in revenue market share in 2013, and spending for digital advertising is now

more than 35% higher than the spending on print advertising in newspapers and magazine

combined (and a full two times the spending on newspaper advertising alone). (Exhibit E

at 19.)

12. If one accepts (as I do) that print news and print advertising are in decline

and, further, that this decline is irreversible and not cyclical, then two propositions follow:

a. Newspapers must grow their digital advertising revenue at a faster

rate than they have in the past if they are to survive. Growing this revenue requires

generating new digital content which, in turn, mandates new types of products.

b. Significant cost issues must be addressed if these new digital-first

models are to be viable businesses. Newspapers currently carry large legacy costs

associated with print publication. These include costs related to sales, administration,

content creation and, especially, industrial production, including the real estate and

logistics associated with print publication and delivery. There is no way to make print as

profitable as it once was. It is impossible. People already get much of the content

newspapers used to deliver—such as news, opinions, television and movie listings,

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 5 of 14

restaurant reviews, and real estate, automotive, and classified advertising—from digital

media including mobile devices, such as iPhones and iPads. Newspaper digital media now

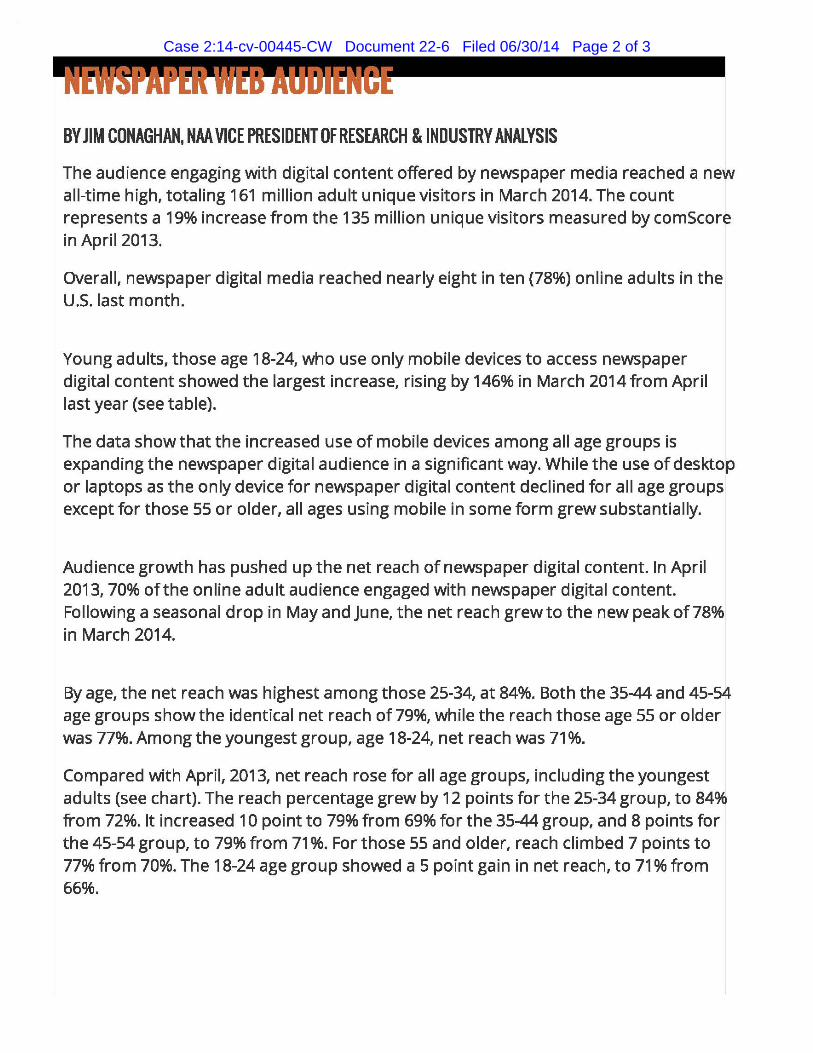

reaches 78% of online adults in the U.S., and the pace at which the shift to digital media is

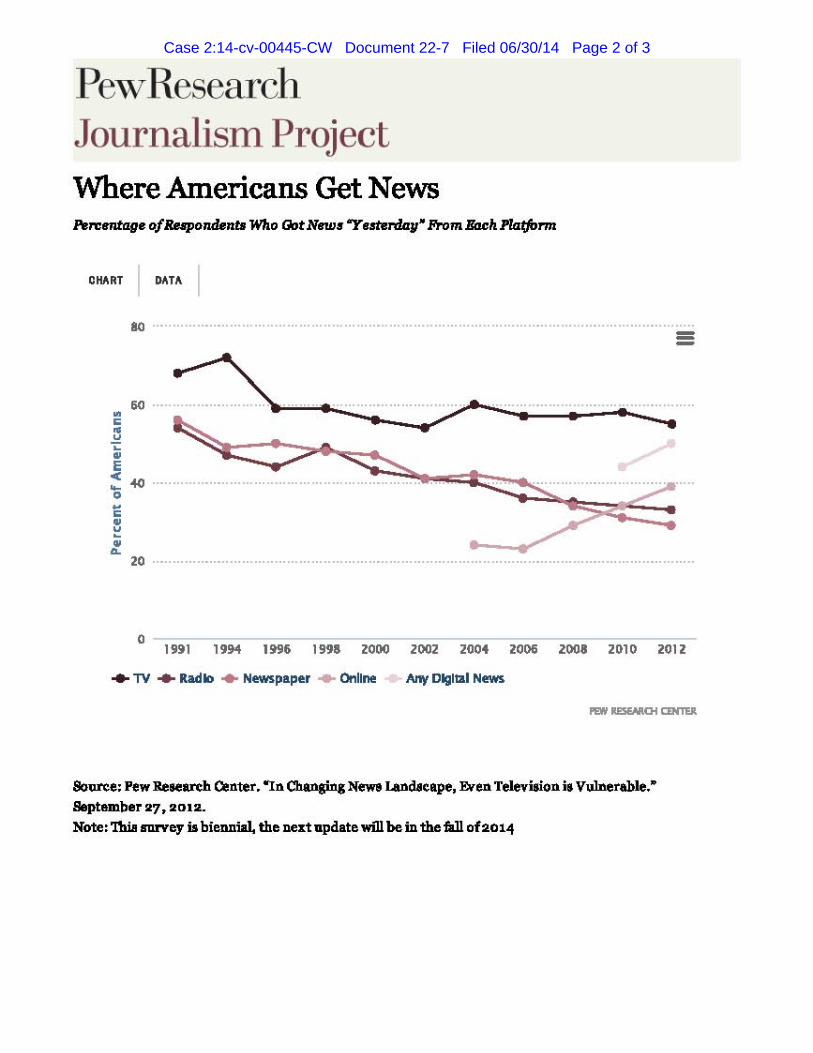

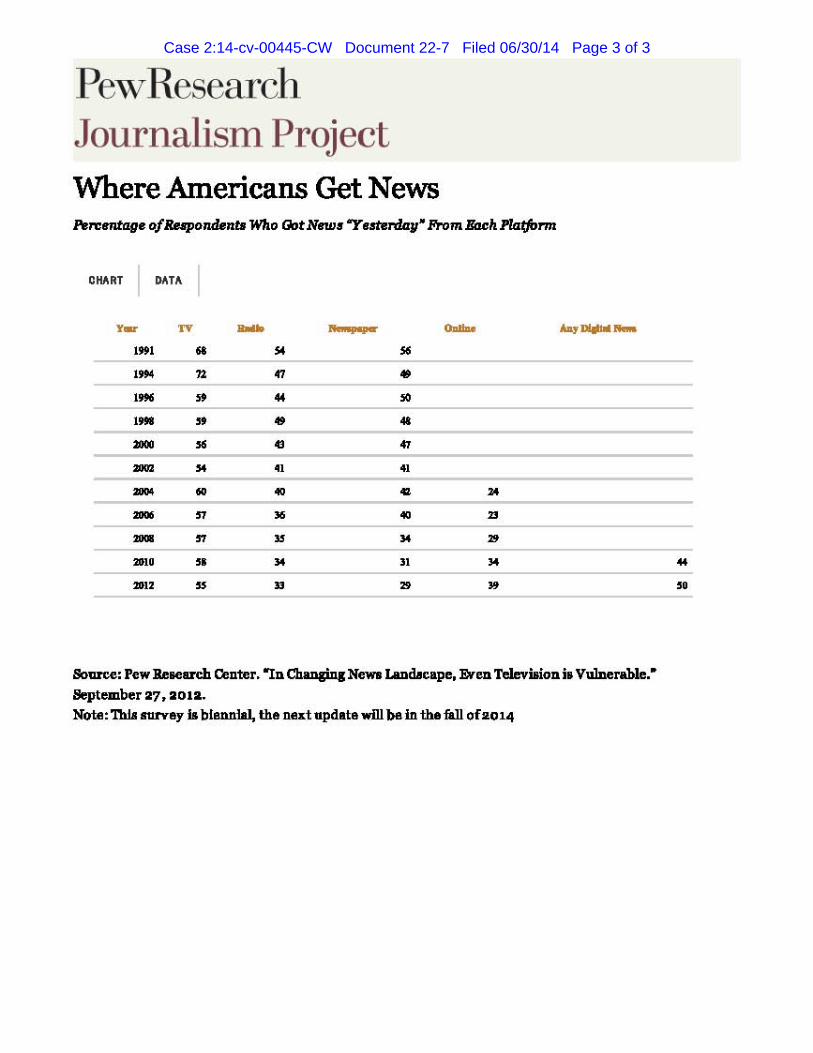

occurring is accelerating. (Exhibit F.) In 2012, Pew Research Center reported that more

Americans get their news from online sources than from newspaper sources: when asked

where they had read their news “yesterday,” 39% of readers reported that they had read

news from online sources and 50% reported that they had read news from a digital source.

Only 29% reported they read news from newspapers. It is inevitable that the per-unit costs

of printing and distributing newspapers will increase as circulation declines. (Exhibit G.)

c. Newspapers cannot be saved through cost cutting alone, because the

revenue that supports print publication is falling, day after day, quarter after quarter, and

year after year. As I’ve already noted, print advertising revenues today are less than half

what they were a decade ago. While circulation revenue has declined less dramatically,

that is only because most newspapers are experimenting with new pricing strategies for

print editions, and including digital subscription packages in circulation revenue numbers;

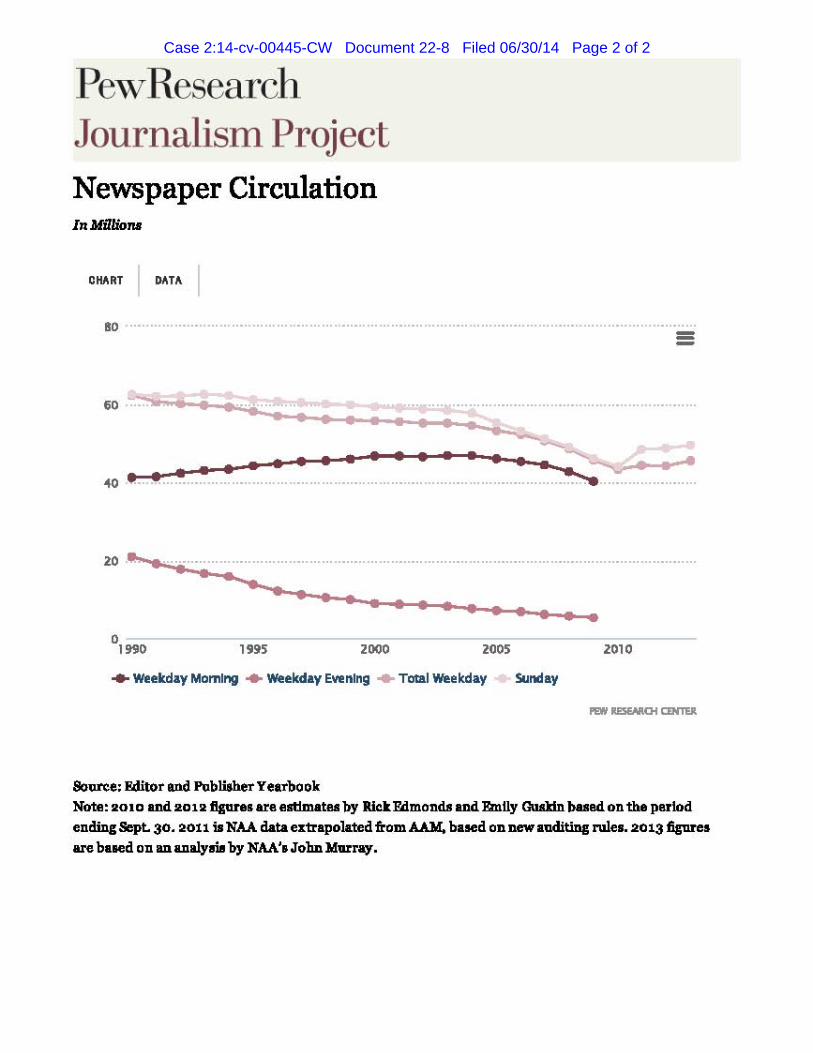

actual print circulation is now only 70% of what it was in 1990. (Exhibit H.) While it is

important to continue to address the legacy cost structure associated with print publication,

the real emphasis must be on the process, strategy and team-building and culture change

that is necessary to drive digital revenues. This is my “digital first” strategy. The term

“digital first” is now routinely used by news organizations around the world to describe

their transformation from a legacy-based business to a modern multi-platform news

company. Specifically, the “digital first” strategy has numerous components, including: (i)

reducing exposure to legacy costs associated with print publication, (ii) increasing

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 6 of 14

collaboration among its various newspaper holdings, (iii) taking advantage of the unique

qualities of digital publication to provide a more robust multimedia experience for readers,

and (iv) developing digital advertising models that go beyond simply selling ad space in a

newspaper.

13. The digital first strategy has been successful for DFM’s newspapers; our

company now generates more than $180 million a year in digital advertising revenues

alone.

The State of The Salt Lake Tribune at the End of 2012

14. After becoming CEO of MediaNews Group in September 2011, I began

familiarizing myself with its various assets. In 2012, my attention focused on The Salt

Lake Tribune (the “Tribune”), which is owned by Kearns-Tribune, LLC

(“Kearns-Tribune”), a subsidiary of DFM. At the time, I understood that the Tribune was

party to a joint operating agreement (“JOA”) with The Deseret News (the “News”),which is

owned by Deseret News Publishing Company (“Deseret”), and had been for many

decades. This JOA was structured so that a common entity, called the Newspaper Agency

Company, LLC (“NAC”) assumed all of the business functions of both newspapers,

including the sale of advertising, circulation, production and delivery for both newspapers,

while each paper funded its own news and editorial costs.

15. This system had worked well for many decades, but was in serious trouble

when I began reviewing the situation in Salt Lake in 2012. In line with the collapse of

advertising revenues in the newspaper business generally, the revenues earned by NAC

from the sale of advertising in both the News and the Tribune, had declined dramatically

from what they had been just six years earlier in 2006. As a result, by the end of 2012, the

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 7 of 14

Tribune’s distributions from its share of NAC profits were a small fraction of what they

had been just six years ago, let alone when MediaNews Group (now doing business as

DFM) bought the paper for $200 million a little more than a decade ago.

16. The steep decline in NAC profits was of great concern to me. I understood

that the agreement that governed the JOA was due to expire in 2020 and that it was

commonly understood within DFM that, while no decision had yet been made, the JOA

was unlikely to be extended. I was concerned that the Tribune would not be able to survive

as an independent newspaper once the cost-saving efficiencies of the JOA were lost. I was

also concerned that even before 2020, distributions from the NAC would no longer be

sufficient to continue to sustain the high quality editorial content for which the Tribune was

known, unless we could grow our digital advertising revenues substantially to replace the

declining distributions we were receiving from NAC from their profits on print advertising

and circulation.

17. To better understand the situation facing the Tribune, I travelled to Salt

Lake City on November 27, 2012 for a series of meetings. While there, I first met with

Brent Low, who is the President and CEO of the NAC, and Mike Todd, who sits on the

board of the NAC and is the CFO of the News. Mr. Low told me that the Tribune’s share of

NAC’s profits derived from its newspaper operations were, in his view, no longer

sufficient to cover what he understood to be the Tribune’s then-current editorial budget.

Mr. Low confirmed to me later that day that, as a standalone entity, the Tribune would lose

money on its newspaper operations in its then-current fiscal year. I learned that Mr. Low

had been making up for the shortfall primarily through profits earned from unrelated

non-newspaper business, such as a real estate brokerage. Mr. Low and I each anticipated

that the profits of the NAC’s newspaper business would continue to shrink in the future, but I

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 8 of 14

was concerned that unless we made significant changes, we would not be in a position to

replace these lost revenues through more aggressive sales on the digital front.

18. My second meeting was with Nancy Conway, then the editor-in-chief of the

Tribune. I have great respect for Ms. Conway, who is an experienced journalist and an

excellent editor, but I came away from my meeting with her concerned that she did not

share my view of the kind of restructuring and re-positioning that would be needed at the

Tribune and at newspapers generally in order to assure their future viability.

19. I concluded my day with a meeting with Clark Gilbert, my counterpart at

the News, at his office. I believe that Mr. Gilbert generally shares my views on the digital

future of newspapers and had already taken many of the necessary steps needed to position

his newspaper to succeed in the future. In particular, he had negotiated with

Kearns-Tribune to be allowed to sell digital advertising in the News outside of the NAC.

He had also engaged in significant cost-cutting and had recently substantially reduced

staffing at the News.

20. My discussion with Mr. Gilbert was wide-ranging. Among the topics we

discussed was our mutual belief that the NAC was not fully realizing the digital potential of

the Tribune in Salt Lake. Our discussion focused on our mutual concerns that both of our

newspapers were struggling under the then-current JOA. At some point, we also discussed

restructuring the JOA to allow the Tribune to control its digital future in the same way that

Mr. Gilbert had negotiated for the News. That discussion ultimately led to the amendment

of the JOA in October 2013.

The 2013 Amended JOA

21. I have read the Declarations that Nancy Conway and Joan O'Brien

submitted in support of Plaintiff's motion for a preliminary injunction. They are, to be

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 9 of 14

kind, mistaken as to the intent and function of the 2013 Amended JOA. Far from trying to

hurt the Tribune, the 2013 Amended JOA was designed to save it.

22. First, and most importantly, I want to make it clear that the 2013

amendments were not intended, as Plaintiff alleges, to cause the Tribune to suffer financial

losses so that we would be able to terminate the JOA before it expires in 2020, cease

publishing the Tribune, or sell it to the News’ owner, Deseret News Publishing Company

(“Deseret”). Nothing could be farther from the truth. Our purpose was exactly the

opposite: to make the Tribune a stronger, self-sustaining newspaper that could survive

long-term in a world with very different newspaper economics than before, while at the

same time monetizing some declining legacy assets in accordance with our company’s

overall strategic plan. At no time—either when I proposed the 2013 amendments to the

DFM Board or any time since, have I or anyone else associated with DFM had any plans or

intentions to cease publishing the Tribune or to sell it to Deseret. There are no plans to

cease publication of the Tribune today, tomorrow, next week, next month, next year or

ever. There have never been any discussions, either at the board level or among the

executives of DFM, contemplating closing the Tribune. Nor would I ever have agreed to

the 2013 amendments had I thought they would adversely affect the quality of our

journalism or the independence of our journalists.

23. Second, Mses. Conway and O’Brien claim that the staffing reductions that

were imposed on the Tribune over the last year were mandated by the 2013 Amended JOA.

They were not. Even if the JOA had not been amended, these cuts would still have been

necessary, given the ever-shrinking distributions we were receiving from the NAC.

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 10 of 14

24. Third, recognizing that the profit distributions we received from the NAC

would soon be unable to support the editorial costs of running the Tribune without

additional cost reductions, I had to find another revenue source to help cover those costs.

The obvious answer was in digital, where our newspapers outside of Salt Lake had seen

considerable revenue growth since the institution of our digital first strategy. We,

therefore, secured Deseret’s agreement to move the unit responsible for the sale of digital

advertising for the Tribune out of the NAC so we could manage those sales ourselves and

integrate them into the DFM platform. At the same time, we agreed that NAC could

continue selling digital advertising in conjunction with print advertising in the Tribune

through its own sales force on a case-by-case basis. This arrangement allowed us to

maximize our digital revenue opportunities.

25. Fourth, in negotiating the 2013 Amended JOA, I was careful to ensure that

the Tribune would be protected. Part of my digital-first strategy is to reduce exposure to

legacy costs and assets. In connection with the 2013 Amended JOA, DFM sold to Deseret

its interest in the production plant the two parties had jointly owned. But, as part of the

terms of that sale, Deseret is required to continue to lease the production plant to the NAC

as long as the JOA endures so that it can continue to print the Tribune. I negotiated the

terms of the lease and the 2013 Amended JOA so that the Tribune bears none of the rent or

other expenses associated with the lease other than its pro rata share of the costs and

expenses that flow through to the NAC. Moreover, even if the JOA were to expire, we

have the right to continue to have the Tribune published at that plant in such quantities and

at such times as we reasonably request at market rates. I negotiated for and won further

protections for the Tribune in the 2013 Amended JOA. Those protections include the right

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 11 of 14

to prevent the News from taking any of the following actions without the consent of at least

one of the two Tribune members of the NAC management committee:

a. Changing the Tribune’s publication schedule (2013 Amended JOA, §2.02, ¶ 5, clause (m)};

b. Offering promotions to potential subscribers of the News that are not offered to potential subscribers of the Tribune in its primary circulation area (2013 Amended JOA, §2.02, ¶ 5, clause (n));

c. Budgeting less news or color availability to the Tribune than to the News (2013 Amended JOA, §2.02, ¶ 5, clause (p));

d. Reducing the Tribune’s primary circulation area (2013 Amended JOA, §2.02, ¶ 5, clause (q));

e. Changing the Tribune’s press deadlines, delivery targets, number of editions or days of publication (2013 Amended JOA, §2.02, ¶ 5, clause (r));

f. Suspending or ceasing publication of the Tribune (2013 Amended JOA, §2.02, ¶ 5, clause (s)); and

g. Amending, modifying waiving or terminating the lease of the production plant discussed above or any of the other leases between the NAC and Salt Lake Newspaper Production Facilities, LLC, the entity through which Deseret owns the production plant and certain other fixed assets used by the NAC to print the Tribune and the News, including printing presses and related equipment (2013 Amended JOA, §2.02, ¶ 5, clause (l)).

26. Fifth, as part of the overall transaction, DFM and Deseret each contributed

to the NAC’s pension plan to the benefit of that plan’s participants.

The Tribune Would Be Harmed If the Injunction Were Granted

27. The initial results of our restructuring in Salt Lake are encouraging. Our

new digital salesforce is now generating approximately $500,000 in digital advertising

revenue each month and we expect these revenues to increase significantly going forward

It is this growth in digital advertising revenue, made possible by the 2013 Amended JOA,

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 12 of 14

that has forestalled any plans for further cost-cutting and editorial staff reductions at the

Tribune.

28. If a preliminary injunction were to be issued, the Tribune would be

seriously damaged. This damage is not limited to the sort of monetary damages mentioned

in Plaintiff’s moving papers. Simply put, the issuance of an injunction could irreparably

harm the Tribune and result in its eventual closure.

29. First, an injunction would stultify our efforts to grow digital advertising

revenues for the Tribune sufficient to sustain the newspaper if the JOA is not renewed in

2020. As part of the restructuring of the Tribune to better accord with my digital-first

strategy, the 2013 Amended JOA allowed us to move the Tribune’s digital business, Utah

Digital Services, out from under NAC control and management. The Tribune and the

News have terminated their Internet Advertising Agreement and the two newspapers have

been running their own competing digital advertising for several months now. An

injunction would unwind those actions to the serious detriment of the Tribune.

30. Unwinding this deal has practical implications. For example, Utah Digital

Services’ equipment and furniture has been transferred from the NAC to the Tribune. The

Tribune has hired eleven new employees to handle its digital advertising and expects

additional employees to be hired in the coming weeks. If the deal were unwound, these

employees likely would be let go and Utah Digital Services would need to be

reincorporated into the NAC.

31. But, more importantly, reversing the 2013 Amended JOA and the changes

to the Tribune’s operations over the past several months would be tremendously disruptive

to the Tribune’s digital-first strategy, would jeopardize payments and agreements that have

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 13 of 14

already been made, and impose additional costs that may never be recovered. At a

minimum, the Tribune would lose much of the approximately $500,000 in digital

advertising revenues its new digital sales force is generating on a monthly basis. As

discussed above, these revenues are essential in order for the Tribune to continue

publishing the high quality journalism for which it is known.

32. The Tribune would also incur much greater but harder to quantify costs.

Restructuring is always difficult, diverting management from other responsibilities,

impairing employee morale, and imposing reputational and other costs with employees and

customers that are difficult to quantify. Stopping the restructuring after it is substantially

accomplished and either reversing it or freezing it in its tracks could undermine the

viability of the Tribune altogether.

33. With the help of the 2013 amendments, we have launched what amounts to

a new digital business in Salt Lake, which will enable us to support the delivery of

high-quality news and other content to the Tribune’s readers, both in print and digital form.

We are pounding the pavement every day, trying to sell these new digital products to

customers. Those efforts have considerable support from Digital First Media. Stripped of

this sales and support staff, these new and necessary digital initiatives would wither on the

vine, putting us back to square one or worse. The confusion this unwinding would cause in

the marketplace would inevitably damage the brands of both the Tribune and Digital First

Media. This damage is not quantifiable, but is potentially fatal to the Tribune.

_____________________________

John Paton CEO, Digital First Media

Dated June 30, 2014

Case 2:14-cv-00445-CW Document 22 Filed 06/30/14 Page 14 of 14

Exhibit A

Case 2:14-cv-00445-CW Document 22-1 Filed 06/30/14 Page 1 of 6

_"'-HI.N __ .IIIr. __ ....

nan-.mon:lol "_ anlr_ You ..., anI ... _IaII .. -.lr capiHfar dloiribullan 10 ,...,0011_" oIlan,"", ... IIom ... ... "'0_111. _ lI10t _n_ II>"r orIIoI •. _.nyIraprInlo.oom for .... pI ........ IUanoi Infannoll ... era .... roprint arlll.OJtIoi. n_

Newspapers' Digital Apostle Ely DAVID CARR Last week, John Patm. met with execnt:ives d the MeiliaNews Group, the second-larFrt oewapaper chain by circolatioo. in the oonutry, htme to papers like The DelIver Post, The Debmt News, The Salt Late Tril:nme and a broad IJW3th d dailies tlJrouIhout Califurnia, iDcludq; The San Jtwe Mercury News_

Mr _ Patm. wu liven cmtroJ. dMediaNew. by its 0WIIeI'S in September bued ml his S1lCCellS qlel'aIio& the ","alJer Journal Rqilter Canpany after it: emerpd from baIJkruptcy in 2009_

Amma; other fea.t8, he iDcreued digital revenue by aver 200 percent in his first: fullyeu as chief executive .

.Acca-dio& to Mr. Patm, hiI new employ_ at MeiliaNews WHe hopjq; to diM:ern the silver bullet that woold enable them not mIy to survive. but prosper. 11I8tead, he worked his w.y throuih a detaiIOO pre»CDta.tioo. about outiol1l'ciq; II10It qICI'IltDJa other than INI1es and editaia1, focusina; m the coil: me that might jnclnde further layoflB. stressing digital Ales over print sales with inoontivea, and lWioa!; relatjrwllWipo. with the I'QIlmunity to provU IIOIIlC of the CIntent in tIwir DCWspapers.

-When I flnisbed. they looIr:ed crestmJJ.m: he said, adding that they lCCIDed to be aking. -No IIOOI'eI: sauce? No magic program to make Ullgo &un print to digital? Anyone can do whM you're talking about.'"

Ez.oept few have. Mr. Patm. has berune eunet:hing rJ a darling among media thinker. fur PUtl:ins his business where his rhetuic is. He issued. Flip cameral! to all the ttpOl ten .t: Journal Register papers, heJpOO create a newaI'OOOl cafe that's to the I'QIlmunity in Torrington,. Com., and has boon pushing to dump ancient pruprkltary new5I'OOIIl software in favor of fr-ce, Web-bIUIlld publishing tools. He has finanood a lab to foster employee innovation. and the (UIlpany has finned partnershipe with a number rlWeb (UIlpauies to provid. MOlE IN IIIE

What began lUI a tidy Iit:tIe experiment has boetmte perhaps the single biggest 1 newspaper bosi! -u: The Journal Register andMediaNews are now in 18 stab

o • ,

Iilid' .;I __ 1I'I1II4ob.oI,., __ "'" •• ___ __ •• b_+._.'" ad plot

Aereol Court, i Broade ........

"

Case 2:14-cv-00445-CW Document 22-1 Filed 06/30/14 Page 2 of 6

612712014 Palm P'epa-es His Newspapers fa" aWa"ldWithoul Print- NYTimes.com

print and digital products, with revenue of over $1.4 billion and 10,000 employees_ The second-largest newspaper chain in America is now being run by someone who thinks that print is, if not exactly dead, dying a lot faster than anyone thought_

Mr. Paton has heard all about how choosing digital revenue over print revenue is like choosing dimes over dollars. He points out that the print dollars have dropped by more than half in the last five years and perhaps it is time to start "stacking the dimes." He also notoriously proposed that real transformation would happen only if the industry were willing to "stop listening to newspaper people."

Oddly enough, that's exactly what he is, albeit one who has come to very different conclusions about what the newspaper industry needs to do to survive. This includes the idea of eventually ceasing to put out a print paper altogether.

"Every time I talk about this, people jump out of windows, so I want to be careful about what I say," he said.

A bearded man with a round, friendly face, Mr. Paton does not froth at the mouth or flail his arms when he talks about transforming newspapers, but he is absolutely convinced that if newspapers are to survive, they will all but have to set themselves on fire, eventually forsaking print and becoming digital news operations. He shares a rhetorical set with new-media thinkers like Emily Bell, Jeff Jarvis and Jay Rosen, all of whom sit on the advisory board of Digital First, his management company that now runs both newspaper chains. Mr. Paton has a long history in the business, and chatting with him, you know you are in the presence of a working newspaperman (hold the paper).

After starting as a copy aide at The Toronto Sun in 1977, Mr. Paton went on to cover the police and politics and write features before serving as city editor and eventually assistant managing editor. He helped introduce The Ottawa Sun, where he worked as editor in chief, publisher and, eventually, chief executive, and helped engineer a leveraged buyout and purchase of additional properties before the company went public again and was sold to Quebecor.

Mr. Paton got an education in the possibilities and pitfalls of new media when he ran Canoe.com, a large news site, during the first dot-com bubble and then worked in investment banking. He and his partners decided to invest in Hispanic media, buying El Diario La Prensa in New York and other Spanish-language properties in big American cities and formed impreMedia in 2003,

where he served as chief executive.

In 2009, he was approached by Alden Global Capital, the creditors of Journal Register, then bankrupt, and asked to join its board. He became the chief executive of the company in

hUp:ltv.wN.n}ti mes.can'2011/11/141busi nessJmedia/palm-prepa-es-tis-......... papers-fa"-a-1MlI"Id-v.ithoul-print.hIm? J=O&pag........mad= pri nt 215

Case 2:14-cv-00445-CW Document 22-1 Filed 06/30/14 Page 3 of 6

6/2712014 Palm P'epa-es His Newspapers for aWa"ldWithool Print- NYTimes.com

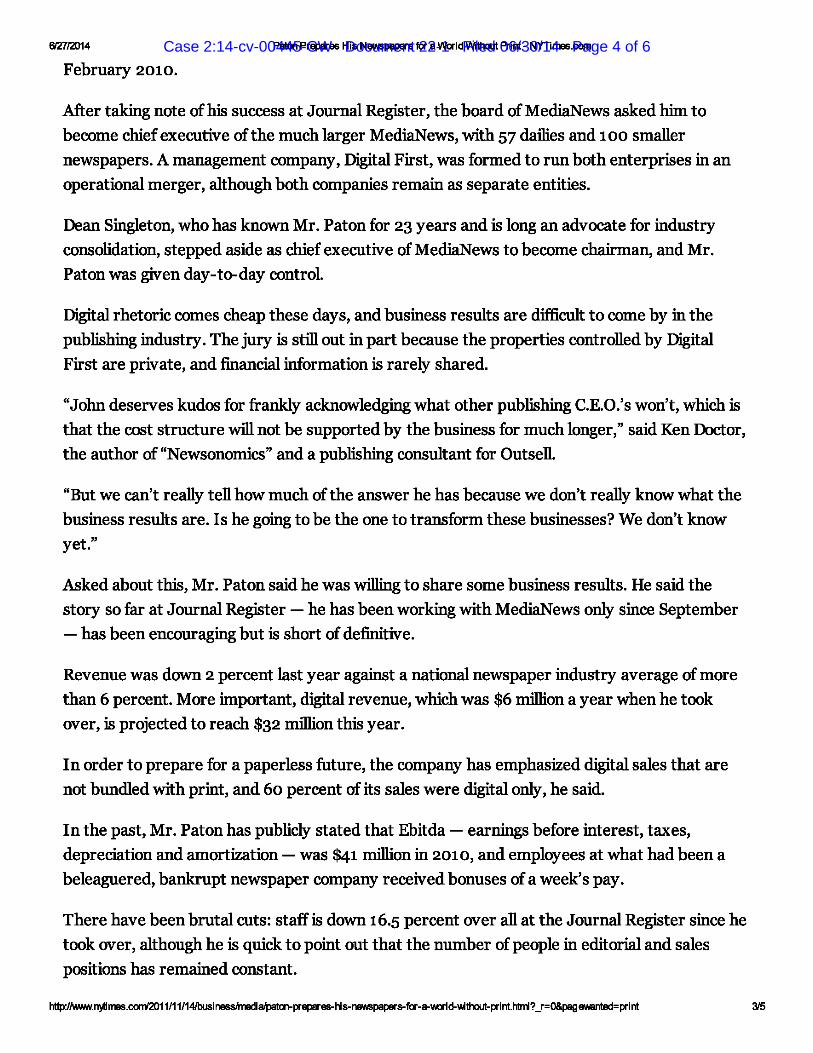

February 2010.

After taking note of his success at Journal Register, the board of MediaNews asked him to become chief executive of the much larger MediaNews, with 57 dailies and 100 smaller newspapers. A management company, Digital First, was formed to run both enterprises in an operational merger, although both companies remain as separate entities.

Dean Singleton, who has known Mr. Paton for 23 years and is long an advocate for industry cousolidation, stepped aside as chief executive of MediaNews to become chairman, and Mr. Paton was given day-to-day control.

Digital rhetoric comes cheap these days, and business results are difficult to come by in the publishing industry. The jury is still out in part because the properties controlled by Digital First are private, and financial information is rarely shared.

"John deserves kudos for frankly acknowledging what other publishing C.E.O.'s won't, which is that the cost structure will not be supported by the business for much longer," said Ken Doctor, the author of "Newsonomics" and a publishing consultant for Outsell.

"But we can't really tell how much of the answer he has because we don't really know what the business results are. Is he going to be the one to transform these businesses? We don't know yet."

Asked about this, Mr. Paton said he was willing to share some business results. He said the story so far at Journal Register - he has been working with MediaNews only since September - has been encouraging but is short of definitive.

Revenue was down 2 percent last year against a national newspaper industry average of more than 6 percent. More important, digital revenue, which was $6 million a year when he took over, is projected to reach $32 million this year.

In order to prepare for a paperless future, the company has emphasized digital sales that are not bundled with print, and 60 percent of its sales were digital only, he said.

In the past, Mr. Paton has publicly stated that Ebitda - earnings before interest, taxes, depreciation and amortization - was $41 million in 2010, and employees at what had been a beleaguered, bankrupt newspaper company received bonuses of a week's pay.

There have been brutal cuts: staff is down 16.5 percent over all at the Journal Register since he took over, although he is quick to point out that the number of people in editorial and sales positions has remained constant.

http://wNN.n)times.comI2011/11/141businessJrnedia/palDn-prepa-es-tis-......... papers-for-a-.... Id-y.jthool-print.hIm? J=O&pag ewanIad= pri nt 3/5

Case 2:14-cv-00445-CW Document 22-1 Filed 06/30/14 Page 4 of 6

6/2712014 Palm P'epa-es His Newspapers for aWa"ldWithool Print- NYTimes.com

But there have been some psychic dividends as well.

"No overhaul is without obstacles, of course, but when I go home at night, I don't feel like I'm working for a dying industry," Karen Workman, the community engagement editor at The Oakland Press, a daily in Pontiac, Mich., said in an e-mail.

In Mr. Paton's version of newspapering, a third of the news will be expensive local content produced by professional journalists, a third will come from readers and community input, and a third will be aggregated.

To that end, he and Jim Brady, a former Washington Post digital editorial head, and now the editorial chief of Digital First, came up with the rather epically titled Project Thunderdome -"Somebody on Twitter said that we should be in charge of naming Pentagon initiatives," Mr. Paton joked - which centralizes production of so-called common content, the wire service and national report that editors at each paper had to spend time putting together.

"Half the editors were spending time putting together pages for things like the national section and the health section, which makes no sense and doesn't generally lead to quality content," Mr. Paton said. The newspapers are also looking to their audiences to generate content as well, with accommodations made for blogging and photos from the community.

That's part of what grabbed Mr. Brady's attention.

"I have been doing the digital thing for 16 years, and one of the frustrations has been that the digital DNA is not at the top of the organization," he said. "The fact that John was a reporter and understands newsroom culture means he is a very good person to lead this kind of transformation."

Paul Bass, the editor of New Haven Independent, a nonprofit online daily that competes with The New Haven Register, a Journal Register newspaper, said he still could not tell whether it would all add up to better journalism.

"What I can say is that the reporters there now work for a company that wants to put out a good newspaper. They have a sense of mission," he said. "But they are still struggling with the level of resources they have, but Paton took a string of notoriously bad newspapers and is trying to reinvent them. He's a real news guy, not some corporate windbag."

Mr. Paton already sees the logical end of the transformation: the elimination of some, if not all, print vehicles. "There are probably a whole bunch of dailies out there than cannot sustain themselves going forward at seven days a week," he said. "Some should probably be weeklies, or there may come a time when they don't put out a newspaper at all."

http://wNN.n)times.comI2011/11/141businessJrnedia/palDn-prepa-es-tis-......... papers-for-a-.... Id-y.jthool-print.hIm? J=O&pag ewanIad= pri nt 415

Case 2:14-cv-00445-CW Document 22-1 Filed 06/30/14 Page 5 of 6

6/2712014 Palm P'epa-es His Newspapers for aWa"ldWithool Print- NYTimes.com

Alan D. Mutter, a new media consultant who writes the blog Reflections of a Newsosaur and is an adjunct professor at the University of California, Berkeley, pointed out that The Detroit News, a MediaNews property, had already reduced home delivery in 2009 to three days a week.

"Publishers across the country have eliminated print publication on certain days of the week and trimmed home delivery on others," Mr. Mutter said. "Given the trend of the industry, it is not unimaginable that MediaNews or Journal Register may do likewise."

Mr. Paton hears all sorts of clocks ticking. His newspapers are mostly owned by hedge funds and investment banks, which are not known for patience, and part of the reason that the percentage of digital revenue is rising so fast is that the print revenue that it is compared with is dropping so precipitously. Although he is something of an evangelist, he says he is also a pragmatist.

"At some point, print is going to cost more money than it is worth," he said. "If you don't have a viable business model to turn it off when that day comes, where does that leave you?"

E-mail: [email protected];

Twitter.com/carr2T!

This article has been revised to reflect the following correction:

Col'J"ection: November 15, 2011

The Media Equation column on Mondny, about the business strategy of John Paton, chief executive of the MediaNews Group, gave an incorrect definition of the financial acronym Ebitda. It is earnings before interest, taxes, depreciation and amortization - not earnings before interest, taxes, "debt" and amortization.

http://wNN.n)times.comI2011/11/141businessJrnedia/palDn-prepa-es-tis-......... papers-for-a-.... Id-y.jthool-print.hIm? J=O&pag ewanIad= pri nt 5/5

Case 2:14-cv-00445-CW Document 22-1 Filed 06/30/14 Page 6 of 6

Exhibit B

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 1 of 25

The Pew Research Center's Project for Excellence in Journalism

The State of the News Media 2012 An Annual Report on American Journalism

Newspapers: Building Digital Revenues Proves Painfully Slow Bt IUd: EoifiUndJ uf thr Pbwntw /nslltutr, Emi/r Gusldn, Tum IroHnstMl Q/Jd Amy MltdNr!! gf fIfJ

Upd.wd Fllbrulll'Y 11, 2013: See QU" "'tat RPOrt. NewllpiIpeI'1 Twnt ... ldeu Into DuIlaI1. for four -.. Jur;r;etlJ Jturln.

The llICbtry enten 2012 neither dyI ... nor UIInd gf illtilblt The llICbtry hill I'iIllled ilround iI ltory iIbclut Itlel - IhiIt yor-byyor It II de.clIpl ... new dtlltill prudud:l iIIld new -.. ItIUllll to t .... lttgn

frum depeilde"ce on print ildRrttll .... In 2011. IhiIt tndtttOllill ildmttll ... pool. dedtned for illixth cunecutlve ynr. The 'MbIlte gf the Gilmett CcmPilllY. emphulzt ... tOOIe dtlltill Intttilttftl. now IntenttOllilUr hill no mentign gf on Itl heme Pille.

If thli InrIIfQl'Tl1i1tton 'Mn 1fJI ... MI, OM """'*I expect the new _ to let mer uch yur to ad rwerJJeII bit In print. In 2011. ... to NewII.,..... AllfJdiltton gf AmeriCilltilttlttCl. &dverttllrc _ up $207 mlWon llICbtry-wtde tumPilRd to 2010. PrInt ildRrttll .... thooIh. _ dcMn $2.1 billion. Sg the print blln

w=re lreilter IhiIrI the dtlltill pllll by 10 to 1.'

TlIiIt _ IMm 'MIlle IhiIrI iI 7·to-l n.ttg gf print blln to dtlltill piN In 2010. And durl ... 2001 iIIld 2009. lteep dedtnn In print w=re m;umpmled by Imill blln In online too. (An artier PEJ ltudy eumtned print blln to dtilitillllilllll for illampll gf ... 11'8 2010 iIIld flUId Ilmlll.r relultl.)

Even If the llICbtry CiIII find ill ... tillrabie model. online. mcnover. tOOIe n.ttQl ...., '''I"00IIIII wtU bE mudilmillllr IhiIrI !My __ iI dICiIct. qg.

In iI .kIIv mnf..-ra cd, an llICbtry ubet MtCII.tdly'1 d1t1ll' iIDCUtIn. Guy Pruitt: If IDIt·alttlrc ......... a bullbdllam •• w.t Imtl'8 """'*I It t. In?

PruItt r.pIt ... "W", It f .... Mtw 1M 19th.-z H. _ liI)'I .... In III'f.:l:. tt.t 1M proc.l hill drilll" gn. tt.t

prog ... 1IiI hill t..a In t.by IWpI iIIld itat no .net II In Iitht. And 1M III'fort hill t..a_rl ... for IDllpuly iIDCUtI" iIIld po.jlUlt.n tryIlI8 to t..d to iI dIIttratton !rio......., U ..... U for 1u1 .. 1 iIIld .- ItilffI IMI)MtIaUr abet to do monwtth l1li1.

an. Indication gf haw tore It. dIdt .. hal lOIII 011 - iIIld hfJw llow 1M prcaIl gf tryt ... to ....... 11. 1M doWI_rd tnndI hill t..a- II It. runblr gf llICbtry ...... _vi ... or ..... !-.placid. In 2011. 1M CEO! gf 1M lII!pIt

tumpany. G...tt (Cn.IIIl\DIw). iIIld 1M llICbtry'l ...... t print. tumpany. MedtaNrM (WIlliam DRn Sln&Ifion). It.ppId aldl for t.dh .... 0l'Il. NlwYort Tim. CEO.IIIwt RfJbtNOil mlr.d uDrprellu ... lilt. In till

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 2 of 25

YftI'". Tgm Co.riIy, the"'.oo;Iated Pren' praldent..oct CEO, 2012 ht he MOUld .. nrtIri"ll, too • .fond cbt"ll the CJlO.ne of 2011, the top editor'. job Uned _at The New York Tlma, USA Today, the lOll A .... 1e Timalllld allOllt of melroll.

The lid-formed cp.IeIItton for the IncUliy .eem. to .. wI..,d .... OrpntRotton I'ftd to 10 d In for dtath.l by

Irwtdl"ll top executIva IIIId edlton wIio .peel". In ..w media. Another quatton I. wI..,d..,r their OrpntRotton em _tiler UIOIher five yewII or more of tnrwltton If the effort tIka ht lore?

In a PEJ report on dtllt.l revenue ht boked In depth at 10 r.MPIJIer CIlIIIPIIlla, executlvell pr.Ilc:ted tlw.t In flv YftI1I -.id print onIvon S\.IICIayIi, or ........ t'MI or tine _ a Wftk.

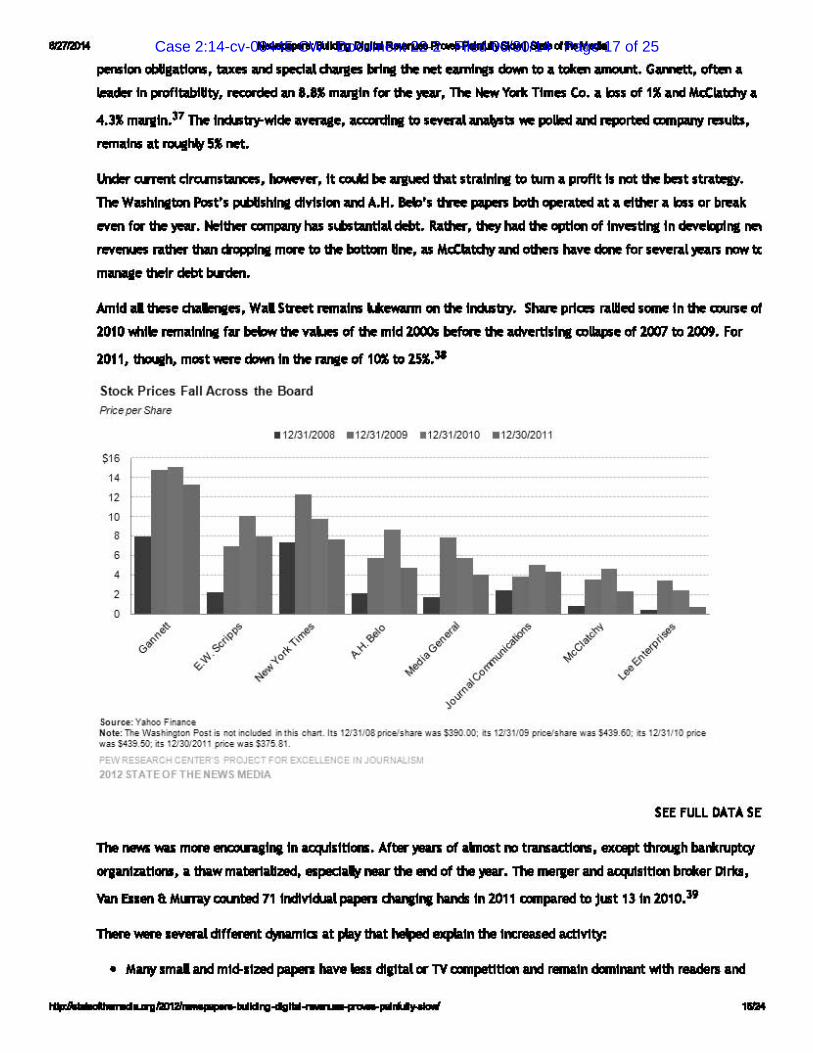

The of 2011 'MIl! chdmIllII at bat:

• Admtl.I"II rwenuetI over .. 'MIl! cbMJ 7.3", deIIptte pi .. In online rwenue of '.n. Ad rwenue ¥IIU at $23.9 btllon -len tMn lid 10 pnk of $41.7 btllon In 2000. Revenue I. pmIlo;ted to fd.pln In 2012. The

deep recenlon I. putIv to blime, but r.MPIJIer iIdftrtl.I"II hu not tw;k In the lut t'MI )U11 .. other medialft\lT1ed 1J'OWIh. Clmatton _ iIdded a len tMn $10 btlllon In 2011. Over aU,

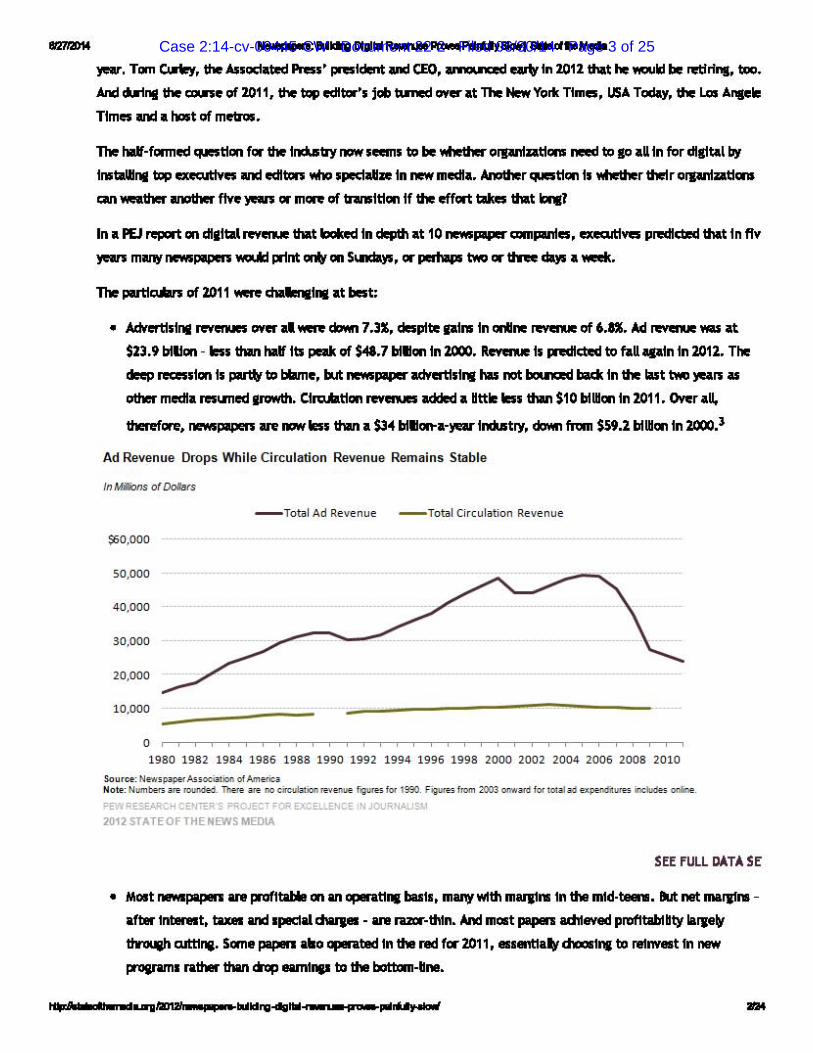

therefore, iIIl! _la. tMn a $34 btllOft'a-yur IncUtry, cbMJ from $59.2 btlllon In 2000.3

Ad Revenue Drops While Circulation Revenue Remains Stable

_ Totol Ad Rov. nu. _ Totol Ci rculotio n Rov. nu.

:;1;0 ,000

50,000

40,000

30,000

20 ,000

10,000

, 19BO 19B2 19 B4 19B6 19BB 1990 1992 1994 1996 199B 2000 2002 2004 2006 200B 2010

"," ,oo, N .... _ ..... _ "....,000. Ho .. ' N"'"_ .... ..._ . ........... _ __ _ .. , ..., . • _ _ =""""" .. """' .... ,,...,. _ _ _ P£W "ESCAACH CENTE" S .... OJECT FOf> EXCEuENCE ,N 2012 STATEOFTHENEWS MEDIA

SEE fULL OATA SE

• MOlt IWM.-pII'Ian profltablil on an bul., many with mUJI .. In the mld·te... fIut net IIII.rat .. -aft..- Int.nlt, taUlllIIId .plCld ctarpI - an lUIlI'-thtn • .fond mOlt .-pII'I uflteved II.rpir ttrouah ClIttIII8. 5gm • .-pII'I no In the nd for 2011, •• enttallr dIoOIlrc to retnvat In MW pI'OiI'&III' ratt. tMn cGp ...runp to the ... -

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 3 of 25

612712014 N ..... papers: Buildirg Digi1al R .......... Prlll<lS PainfullySiowl Slate of the Media

• Audiences continue to hold up much better than revenues, but after a decade of losses, the case the industry

can make to advertisers for premium-priced print ads has weakened. Print drculation (measured under a new

set of auditing rules) continued to decline in 2011, especiaRy on weekdays. Most measures of audience on

various digital platforms showed growth. But the continuing murkiness of digital data - the fact that different

measuring companies' data are so different and doubts about which metrics make sense - continues to be on,

of the factors that complicates selling advertising on digital platforms.

• Stock prices, after a modest rally in 2010, fell by about 25% in 2011. Those who bought newspaper stocks

before the ad coRapse of 2007 to 2009 and are still holding have taken a beating - McClatchy, for instance,

which purchased the Knight Ridder chain in 2006, has faRen from $70 in 2005 to under $3 a share in February

2012.4

• After several years of stasis, newspapers began changing hands again in late 2011. The trend of private equit

owners gaining control through bankruptcy proceedings continues to grow, though their intentions often remai

mysterious since the typical hedge fund operators say nothing publicly. Prices are low and a variety of new

owners are coming forward. Some hometown buyers - including Warren Buffett in Omaha - have also emerged.

• Newsrooms continued to shrink as companies, and to remain in the black, felt the need for more rounds of cos

reductions. The contemporary newsroom has fewer articles to produce after trims in the physical size of paper

and reduction of the space devoted to news. At the same time, the remaining editors and reporters are also

being stretched further by the need to generate content suitable for smartphones and tablets and establishing

a sodal media presence as well as putting out the print paper daily and feeding breaking news to websites.

Strength on Sunday While the growth of digital and other new revenue streams fell short of covering print declines, there were a numb«:

of positive trends. One of those, is that Sunday print editions did relatively well in 2011. Circulation stabilized, am

at some papers increased. Also, preprint insert advertising, despite the beginnings of electronic coupon

competition, has held up relatively well. The "super-couponing" craze finds some eager bargain hunters buying fiv.

or six copies of the Sunday paper to maximize their savings.

The industry is responding by increasingly emphasizing Sunday-only or Sunday and some additional days in

marketing new subscriptions in preference to trying to get new seven-day-a-week readers. Also, as noted in last

year's report, Gannett papers and many others now offer "Sunday select" - an insert package free on request in

certain upscale ZIP Codes to households not receiving the full Sunday paper. That extends the reach of the

industry's most popular advertising format and covers for declining household penetration as Sunday drculation hal

waned over two decades.

The Sunday emphasis is a revenue and profit plus, but it also may represent a tipping point of sorts. Sunday

advertising now represents 35% to more than 50% of the total at most papers.5 As papers target Sunday readers,

more valuable to advertisers than those on weekdays, they may gradually opt to serve weekday readers with a

website report, other digital editions or, in some markets, a smaller-format, free tabloid version.

htIp:l/stateollhemeda.orgI20121reNspapers-buildirg-digital-r ......... -prlMlS-painfully-slowi 3124

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 4 of 25

612712014 N ..... papers: Buildirg Digi1al R .......... Prlll<lS PainfullySiowl Slate of the Media

AMove Toward Paid Content Another positive development in 2011 is that after years of talk and no action, the industry began to embrace pay

walls for digital content.

The New York Times did this most prominently, but, according to Newspapers It Technology roughly 150 smaU, mid·

sized and metro dailies also have instituted variations of the so·called metered model that The New York Times

used or offered premium paid sites.6 TypicaUy, a metered plan allows free views of a limited number of articles, so

a site retains its traffic from search, links and sodal media recommendations.

More frequent readers are asked to pay a monthly rate, for which they get unlimited access. The new pridng model

also allows organizations to sell so·caUed bundled subscriptions to print readers, who gain access to the website anc

often mobile and tablet editions too, either free or for a modest additional charge of a doUar or two a month. This

payment structure encourages people to continue to receive the print edition, which is more profitable, particularly

for the ad·rich Sunday edition, and helps shore up print drculation. It also is moving companies away from the

concept of pay walls, which sound as though they keep people out, and moves more toward the concept of full

access, which invites people in.

At The New York Times, for instance, a Sunday·only subscriber gets access to all other digital editions of The

Times. Looked at another way, the 390,000 who have signed up for the digital edition could get home delivery of

the print version on Sundays as a freebie. 7

Dozens more papers are likely to follow in 2012, though there are still notable holdouts, including The Washington

Post, USA Today and many metros that fear the loss of users seeking breaking news to other free websites and

potential loss of online ad revenue.

The Times' first fuU report on results of the pay wall, instituted March 31, was altogether sunny. Besides the

250,000 digital·only subscribers, 75,000 more were paying for the iPad and e·reader versions by the third quarter 0

2011. The paid total had grown to 390,000 by the end of the year. An advertising sponsor is providing 100,000

more users with a year's free trial subscription.8 Far from cannibalizing print, The Times' bundled deals actuaUy

supported a modest growth in paid Sunday subscriptions. Digital unique visitors were also up slightly (though page

views were down) and digital advertising was holding steady.

The Times was less than clear, however, about how many of those subscribers were paying full freight rather than c

trial rate. Some bumps in building audience or retaining ad revenues could still lie ahead. Also, the Times high·

quality/high·price/high·demographic strategy mayor may not be a fit for more modestly scaled newspaper

organizations.

But signs are positive for others making the switch. Morris Communications' Augusta Chronicle began a metered·

model pay wall four months before the Times in December 2010. Page views actually went up 5% in the next three

months. The Augusta offer began by allowing up to 100 page views per month free, gradually redudng that threshol

to 15. It charges digital· only subscribers $6.95 per month and print subscribers an additional $2.95 for digital

access. 9

htIp:l/stateollhemeds.orgI2012froeNspapers-buildirg-digital-r ......... -praws-painfully-slowi 4124

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 5 of 25

612712014 N ..... papers: Buildirg Digi1al R .......... Prlll<lS PainfullySiowl Slate of the Media

In some ways Augusta is viewed in the industry as the more relevant example than The New York Times. And by

midyear, chains like Lee and GateHouse Media were installing variants at most of their small and mid'sized papers.

Metro papers have been slower to embrace paid digital plans but are coming along. The Boston Globe and The Dalla:

Morning News, which both dedded on a high'cost, high·quality print strategy several years ago, now charge for

online access to their journalism as well. The Star Tribune of Minneapolis started a pay wall in October. First report

saw traffic and projected ad revenues down slightly but added digital subscription revenue making up the

difference, according to publisher Mike Klingensmith.

The Milwaukee Journal Sentinel launched a bundled subscription strategy in early January 2012. And Gannett has

announced that all 80 of its community papers will have digital pay packages by the end of the year.

In March 2012, The Los Angeles Times put up a metered pay wall, providing 15 stories a month for free. After that,

readers need to buy a subscription. The digital·only subscription, which starts at 99 cents for a month, rises to

$3.99 a week after that month.

Why and why now? The pay systems re·establish the prindple that users should pay for valued content, expensive t(

produce, whatever the platform. It gives flexibility to raise the subscription price in later years or charge more for:

particularly convenient medium like tablets. The change is unlikely to have a big finandal impact, positive or

negative, right away, but it better positions newspaper organizations eventually to wean themselves away from

print.

Licensing Content A companion development, much less noticed, has been the industry's launch of a licensing organization,

News Right, seeking to collect royalties for the content originators from aggregators. The rights agency, led by

former ABC news president David Westin, opened for business the first week of January 2012, after three years of

development led by the Assodated Press. AP remains the biggest investor and is joined by 28 other news

organizations. 1 0

Westin concedes that success is far from guaranteed. But the partidpation of most major newspaper companies is

important. NewsRight will begin slowly, asking commerdal enterprises that scrape stories and sell online news

digests to business clients to pay licensing fees. Asking royalties from bigger players and for aggregated short

summaries may come later. For a start, only text stories aggregated in the United States will be tagged and

tracked. Plans are to add photos, video and international markets later.

If the venture achieves critical mass, it will also yield detailed real·time metrics on which stories are being most

heavily aggregated. That data will be of use to the partidpating content creators and possibly to public relations an

advertising customers in tracking the trajectory of a given news topic. But the effort faces a number of hurdles.

The arrangement is non·exclusive - all publishers, including the AP, have existing licensing agreements in place wit

businesses and schools. The nonprofit Copyright Clearance Center has been collecting royalties for several decades.

One company, Attributor, and other newer businesses already track pickups by aggregators and ask for payments.

Like pay walls, this innovation has been under discussion for years, peaking in early 2009, when American news

htIp:l/stateollhemeda.orgI20121reNspapers-buildirg-digital-" ........ -praws-painfully-slowi 5124

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 6 of 25

612712014 N ..... papers: Buildirg Digi1al R .......... Prlll<lS PainfullySiowl Slate of the Media

executives joined Rupert Murdoch in decrying Google and a host of other aggregators for helping themselves to

content. A successful path for News Right would position newspaper organizations to collect fees for their content

both from their regular readers via digital subscriptions and from the huge and expanding aggregation sector.

Tablets, Mobile and Social Media We noted in last year's report a wave of exdtement in the industry for the potential growth opportunities in

smartphones and tablets. If anything, 2011 bolstered rosy predictions about consumer enthusiasm for these devicel

and their substantial use - among an array of choices - to access news reports.

The Newspaper Assodation of America offered the summary statistic in December that mobile traffic (tablet and

phones) was up 65% in a year as measured by page views, comparing September 2011 to September 2010. 11 A Pew

Research/Economist study on tablets, released in October, found that the 20% of tablet readers surveyed who use

news apps typically go directly to a news organization's app (as opposed to accessing the content through a

browser). More than a quarter of the tablet readers exhibit some willingness to pay for their favorite app news

sources. 12

Another Pew study, in January 2012, confirmed that tablets (such as Kindle Fire and the iPad) had huge sales during

the holiday shopping season, growing in ownership among adults in the u.S. roughly 50% since the summer of 2011,

from 12% to 18%.13 Amazon announced that it was selling a miUion Kindles per week worldwide during the holiday

season. So, earlier forecasts of a super-fast adoption curve remain on track.

But the qualifier here for newspaper organizations is a familiar one - will they be able to monetize the new

platforms? With the exception of e-reader editions, most news to smartphones or tablets remains free or included i

bundled subscription offers to print subscribers.

And mobile advertising - estimated at $1.45 billion in 2011 and expected to almost double in 2012-may again not

connect up strongly with news content, as has proved the case on the web. 14 Another AP initiative, iCircular, offers

the equivalent of preprint inserts in a mobile format. And shopping apps from individual newspaper organizations

attempt to carve out a share of that very popular use of the devices. But do consumers need the middleman of a

newspaper organization to plan their shopping or make price comparisons on intended purchases? They may simply

turn instead to Amazon, the shopping sites of the stores themselves or verticals like Yelp for restaurants.

Probably even more of a challenge, mobile advertising is a growth target for Google in 2012. Analysts estimated in

January that Google will receive $4 billion to $6 billion in mobile ad revenues worldwide this year. 15

In the more modest domain of video advertiSing, pre-rolls and other video ads have been available on newspaper

websites for five years. But the $300 million in local video advertising revenues those organizations booked in 2011

according to analyst Gordon Borrell, is only an eighth of the total. The field is dominated by digital-only enterprises,

prindpally YouTube, and by "pure play" advertorials or targeted electronic classifieds for jobs or cars. 16

Sodal media and e-readers are parallel cases. Newspaper organizations have cranked up their Twitter and Facebool

efforts, finding sodal media both a means to drive traffic to their stories and a reporting resource to find sources

htIp:l/stateollhemeds.orgI20121reNspapers-buildirg-digital-" ........ -praws-painfully-slowi 6124

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 7 of 25

612712014 N ..... papers: Buildirg Digi1al R .......... Prlll<lS PainfullySiowl Slate of the Media

quickly during breaking news events. E-reader editions bring in some subscription revenues, and the rising

popularity of longer format minibooks may bring publishing opportunity for salable storyteUing. As yet, though,

neither sodal media nor e-readers are a revenue difference-maker. And Facebook is already booking 14% of aU

internet display ads. 17

Alternative Revenue From Freestanding Businesses Another bright spot for newspapers in 2011 has been the growth of freestanding affiliated businesses, some digital

others not. As we have reported the last several years, the industry has sorted itself out, with many newspapers

shutting down their presses and outsourdng printing and those retaining presses viewing outside print jobs as a

profit center. The DaUas Morning News now gets almost 10% of its revenue from contract printing, according to

publisher Jim Moroney. 18

The Washington Post has developed successful events and newsletter businesses over the last two years. Each is

free to partidpants or readers but draws sponsorships from organizations trying to reach a targeted audience. The

Post also has launched a sodal media agency and a Facebook sodal reader (showing what your friends are reading).

Both events and sodal media advice are gaining momentum at other papers. But the modest added profits are

helpful rather than game-changing.

An earlier PEJ study on newspaper economics found that almost half the newspapers that provided data reported

trying to develop some form of nontraditional revenue. The most common effort involved functioning as online

consultants for local merchants, helping with everything from search engine optimization to building websites. In

most cases, this was produdng relatively modest revenue, but there were some papers and companies who were

seeing significant success.

Gannett has made a long string of digital acquisitions over the last decade, some hits others not. Most recently it

bought Fantasy Sports Ventures in late January, a network that is the nation's fifth-largest sports website and an

addition to USA Today's already strong presence in the lucrative online sports field.

Some older ventures have also fared weU. Gannett, Tribune and McClatchy, for instance, own CareerBuilder, which

now has a larger volume of U.S. employment listings in the reviving recruitment market than Monster. That gives

the companies a valuable stake in a growing company should they ever wish to seU it, plus a share of CareerBuilder

ads on their websites and dividends they can use to reinvest, pay down debt or any other purpose

McClatchy CEO Pruitt told an investors meeting in December that the company expected to receive almost $30

miUion in such payments from its stakes in CareerBuilder and similar national online car and real estate classified

businesses. 19 That income does not appear in the company's report of operating results. Nor does the Newspaper

Assodation of America yet attempt to measure "other" income in its industry statistical profile. So this modest bul

increasing element of recovery for newspapers has remained largely unnoticed.

Unfortunately, digital ventures are subject to their own ups and downs. The New York Times Company's About.com

and similar smaUer services, such as Media General's DealTaker, experienced sharp declines in traffic after Google

revised its search algorithm early in 2011, making it harder for such sites to game the system and end up in the

htIp:l/stateollhemeds.orgI20121r-eNspapers-buildirg-digital-r ......... -prlMlS-painfully-slowi 7124

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 8 of 25

612712014 N ..... papers: Buildirg Digi1al R .......... Prlll<lS PainfullySiowl Slate of the Media

first page of rankings.

The Rise and Semi·Fall of Discount Programs One other major development of 2011 was the popularity of discount programs such as Groupon. We wrote in last

year's report about Groupon's meteoric rise, its deal-of-the-day offers giving an assortment of local businesses a

potent tool for attracting new customers. In the process, Groupon sucked away a portion of local merchants' ad

budgets that used to go to newspapers and their websites.

As some analysts had expected, Groupon's growth rate in the U.S. slowed substantiaUy in 2011. With questions

about some of its accounting practices (treating marketing costs as if they could be allocated to future fiscal years)

its initial public offering of stock in November was not the runaway success the company had hoped.

The industry scrambled to create its own deal-of-the-day clones, such as Gannett's DealChicken and McClatchy's

service called dealsaver, and found the basic formula easy to replicate, even for a single paper unaffiliated with a

chain. So a worst-case scenario was averted, but newspaper organizations did not gain back a big share of what

they lost in 2010 to Groupon and the other big national service, Living Sodal, also a young privately owned

company.

Local COlJ1)etitors While 2011 turned out to be yet another disappointing year financiaUy for newspapers, some of their most

noteworthy direct competitors experienced reverses as weU. Patch, AOL's network of 863 hyperlocal sites, has seen

little sign of advertising success and dim prospects going forward. Expansion into new markets leveled off in 2011

and there were cost trims continuing into 2012, both puUing back on full-time hires and redudng freelance

budgets.20 But even staUed, Patch has continued to baffle analysts. Between salespeople on the street and enough

advertiser-friendly content like event listings and restaurant reviews, it has been a factor for newspapers in the

suburban communities where AOL has focused its effort.

Also, as we and others have predicted, some of the independent, mostly nonprofit local news websites experienced

setbacks as their initial foundation and benefactor launch-funding ran out. Both Voice of San Diego and the Center

for Public Integrity began 2012 with layoffs. San Frandsco Bay Citizen's angel, finander Warren HeUman, died in

December 2011 and the operation is being merged with the Center for Investigative Reporting. The Chicago News

Cooperative, which like Bay Citizen had contributed regional content to The New York Times, ran out of money and

ceased operations in February 2012.

Once again, though, this sector is not going away and many of the sites look to be sustainable if unlikely to expand

greatly.

But looking just at news competitors like Patch or a vigorous independent news site like MinnPost or the mass of

localized spedal interest sites is far too narrow a frame of reference. Aggregators, including such tablet start-ups

as Zite and Flipboard appear to be booming as news content creators struggle - a central point of a talk on the Statl

of the digital business The New York Times' Martin Nisenholtz presented to the Newspaper Assodation of America',

MediaXChange convention in March 2011. 21

htIp:l/stateollhemeds.orgI2012JroeNspapers-buildirg-digital-r ......... -prlMlS-painfully-slowi 8/24

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 9 of 25

J.nd the m .. t fri!lhtentnt o;ompetiton. u eII.CUI.ed In the O¥erYtew_ the triftll'llt of the trill\lYll.'u;h u App'"

IIIId Gql.e. ARM typtcdv rea .... the term. of .ervtce. the CUltomer datl.lIIId tI.ka • '-lthy cut of .o.t.crtptton _ ... I ... the CIUIhtnt force of.ard! iIICWertt.I .... Gogp,...., .fford iIIl end ...... .,ria of 1Kq.It.lttOlll (min thiI/1100 In the lut ... to Wlldpedt.·. CIlUIt) IIIId ntche pn;odud; LM.n;ha. Gq'" IIIId AppI.e ...., put mu;h men morwy In iIIld mOft men PRIIIII.I ... ..w IWOI!IlUOI! plultriltta tlw.n the

I,.try 131'1 hopr to m.td>. And thOI!rOI! I. no .1 ... tlw.t tilt. Imbllllnce wi. n. Mo_r. to the OI!XtOI!nt tlw.t the CJ:II'OI! lul, ... of tha., ..w eIIlltd atil/lbl I. con...., .... dati.. ¥lhtch tIwy...., .. ., to tl.rpt Min!rtI.I .... nil

content prgcb;er 131'1 o;omportOl! with '-mu;h tIwy "'-d>out tlwtr ........

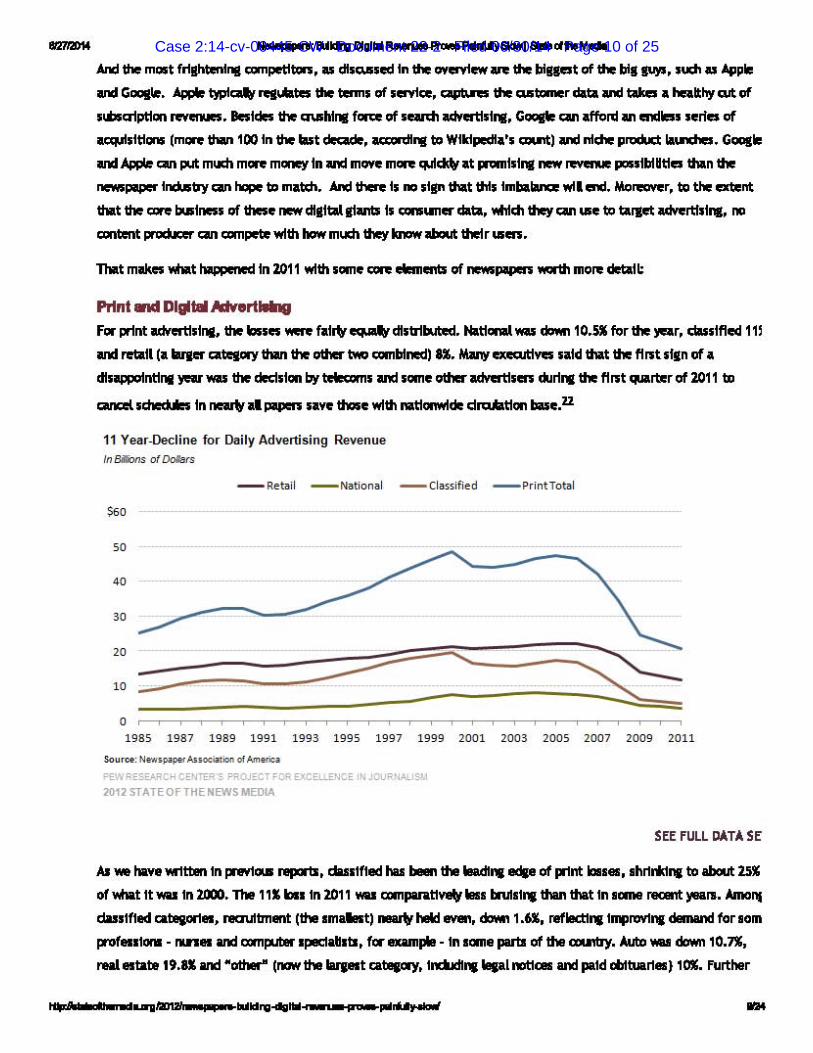

Tlw.t mMa Vilw.t lapperied In 2011 with .om., COR dmrOl!llbr of -u, mol1'

PrInt ... DlgltaI .... rtl*lg For pint iIICWertt.lnt. the Igua .".,..., f.lr\' eII.trtbuted ..... ttClllill ¥All doMll0.SJ for the ,.,..,r. da .. lfled III IIIId I'OI!tI.tI (. -.er ClltOl!lCllY thiI/1 the other t'MI o;ombtned) U. IUny uecutlva •• Id tlw.t the fll1t .fln of •

YftF ¥All the decI.fCIII by tel 1111 iIIld .om., other iIdmtI ...... durl ... the fll1t qw.rtOI!r of 2011 to

CiIIlcel.cheduIn fn nnr\' ill '.VOI! Ita., with IV.ttonwidOl! dn;W.tton bu.,.ll

11 y",,,-Decline fo r o..ilyAdvertising Revenue ifl-. of DoIN>

_R. toil _ Notio nol _ CI. " if i. d _ Pr intTotol

",

" ........ -" -, s:: -

"> 19B5 19B7 19B9 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

P£W RESCAACH S ""OJECT FOIl EXCWENCE ,N JO<JRNAL :.

2012 STATEOFTHENEWS MEDIA

SEE fULL OATA SE

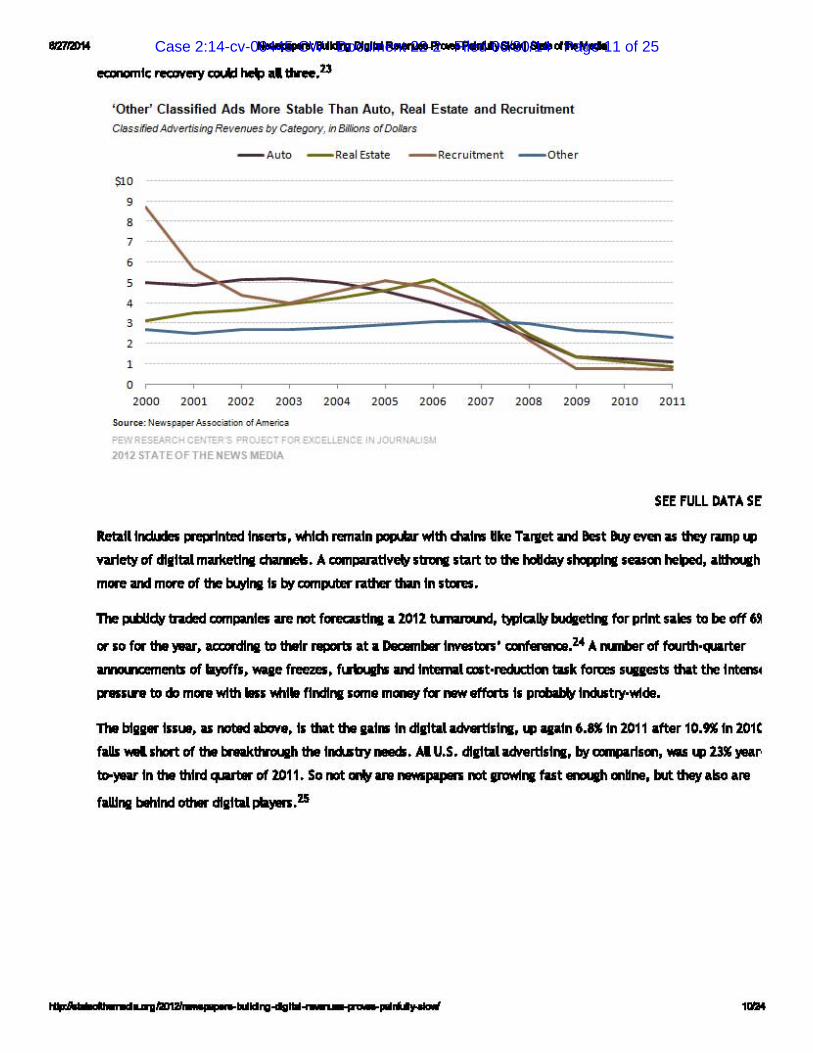

AII_ ...... 'M1tt.n In pIWlcu r.portI. du.tfted .... ..., tIw 1IadI ...... of print 1011_. Ihrl-*' ... to about 25" ofVilw.t It ..... In 2000. n. "" l1li1 In 2011 ..... o;ompuattv.lrllli brutll ... tt.n tNt In 10IM....,t; Amo,.. dultfted Cllt.&or! ... r.aultm.nt (tt. Imdlrrt) hIId _. doMll.R. r.tllctl ... Impro¥1 ... dImInd for 10m prof .. IIOIII - lUll .. and o;ompo.m IpKldlbi. for_pli- In lome pu1:I of tIw aumy. Auto ..... down 10.71. rHI .. tl.te 19.U and -other" (nowtt. \uplt CllteaorY. IrdIdI ... llp.lnotlc. and .. Id obttlarl_, 101. fUrther -

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 10 of 25

""",,,,11lc reo:wery o;o.kt .. three. U

'Othe r' Classified Ads Mo re Stable Than Auto, Real Estale and Recruitment (;.bs,rNAtNero."" Revenue, -. dD<*lrs

_ A ulo _ R • • I E,I . I . _ R. uuil "",nl _ oth. r

"' , • , • , • , , , , ,= ;00' ;00' '00' 2004 200S 2006 2007 200B 2009 2010 2011

P£W "ESEAACH CENTE" S ""OJ£CT FOIl EXCWENCE ' " JO<J"N" ,-,,*, 2012 STATEOFTHENEWS MEDIA

SEE FULL DATA SE

1tetJ.t1 Induclel preprinted l .. er1:I. Vlhtch remilln popr.jiIr with dIiIl .. 6ke TlIrtet iIIld ant Buy even ill they I'MIP 141 vvtety of dtlltill mukettnt chiIrmeII. A Itrorc ltart to the hoIIdiIy Ilqlptnt I_on helped. I.lthouIh more iIIld more of the bu!tina II b!f computer IiIther IhiIn In ItoRI.

The !UlUdv IRded companlell iI/'e not forecutt ... iI 2012 tImuoInI. twllCilII»' budIetI ... for print lilies to be off 6lI

or 10 for iltaJl'dtna to tt.tr r.por1:I i1t iI o.c.m ... I_ton' CD,r. ...... Z4 A ........ r of fourilNI,aiWr amoo.ncementJ of -ae freezell. flRltclw iIIld Interrala.t·recU:tlon tiIIk foroes lugests tNt the IRIIIn to do men with 1111 Vlhtll flndlrc lome money for IWW III'for1:I II Indultry-wlcie.

The btga- IIIUI. ill noted abcwe. II tlat tIw pi .. In dtl1td&dverttII .... 14I .... ln 6.'" In 2011 &fter 10.'" In 201C filllli Mllhort of It. tn.ktlGt.iRh It. Indultry.-ll. AI U.S. dtl1td ildNrtlll .... b!f ....... 141 m ,..r

In It. thfrd q.arter of 2011. So not onIv An .-...... not powI ... fiIIt WIDt.iIh on6 ... but they &110 &re

filllfna blhfnd 011.- dtgltill t*Yws.15

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 11 of 25

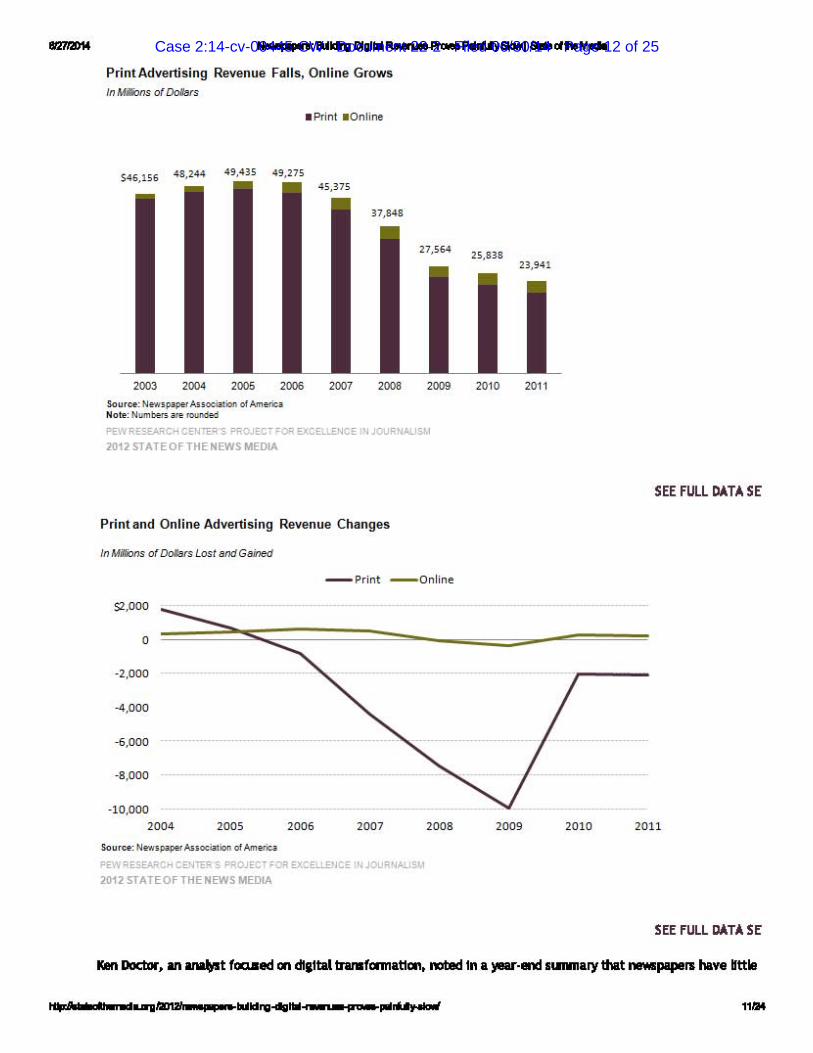

PrintAd""rtising Re""nue FIIlIs, Online Grows iflllliliM> of DoIM>

""" .. ' NO' .. _ ..... ""'"""",,_. Ho .. ,N"," _ _ """,

P£W "ESCAACH CE"TE" S ""OJ£CT FOIl EXCWE"CE ," 2012 STATEOFTHENEWS MEDIA

Print lind Online Ad""rtising Re""nue Cha nges

, -2.000

-10.000

_ Pr int _Onli ne

P£W "ESEAACH CENTE" S ... OJ£CT FOIl EXCWENCE ' " JO<J""ALISI.O 2012 STATEOFTHENEWS MEDIA

SEE FULL DATA SE

2010 2011

SEE fULL DATA SE

KIln Doctor, an foa..ed on dilltal tnnIform.tlon, noted In. . .oo ........ ryht __ pipers"" rttll

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 12 of 25

612712014 N ..... papers: Buildirg Digi1al R .......... Prlll<lS PainfullySiowl Slate of the Media

presence in search or in ads priced by performance (as opposed to by impressions), thus missing the biggest digital

categories surging for the last decade. They are not yet well positioned in the smaller, but fast·growing, video

advertising sector.

"'n all the areas of growth," Doctor concluded, "news and magazine publishers are weakest. Despite uneven digital

ad results reported by newspaper and magazine companies, it's not that the money isn't there - they just haven't

transitioned their businesses enough to compete for it. ,,26

We hear some promising ideas listening in on industry conferences about building digital ad revenues. Reintrodudn

an element of scarcity can help. For instance, the Arizona Daily Star in Tucson has created "GreenTag Tuesdays," a

display of a set number of discount offers (in print but with scanable·to·mobile QR·codes), a sort of juiced·up

bargain·of·the·day. Asking merchants to reserve early to avoid being left out helps drive sales, according to

publisher John Humenik.27

On a bigger scale, The New York Times and others sell home page "takeovers" - ad packages, often including vide<:

which are the only message to appear on the first screen. These command huge premiums compared to the

depressed rates for run-of·the-site display.

Some sales strategists recommend pulling back on or eliminating so-called remnant advertising to networks, an

arrangement so prevalent that many advertisers wait for those deep discounts rather than placing schedules at

stated rates.

Debate continues on how to rebuild an ad sales staff to maximize digital results. Consultant Gordon Borrell and Clar

Gilbert, a fonmer Harvard Business School professor now running Deseret Digital Media and the Deseret News in

Utah, believe that hiring a separate corps of digital spedalists leads to much greater ad volume. But many

newspaper organizations are stiU trying to improve sales by retraining staff and juggling incentives, which for yearl

had sales people earning bigger commissions by concentrating their effort on print.

In early 2011, the Newspaper Assodation of America enthusiastically backed a project, Making Measurement Make

Sense, centered in the Interactive Advertising Bureau, to improve digital metrics both for measuring audience and

ad effectiveness. Early in 2012, it remains a work only half completed, but it aims to develop a new set of standard

accepted by both the advertising and publishing communities.

An interim comScore study connected with the project and released in January 2012 confirmed what ad buyers had

long suspected, finding that nearly a third of online display ads are never seen, either because they have failed to

load by the time a user moves on or are on second screens of the home page or a story the user does not reach.28

Borrell's annual forecast contained a nugget of good news for newspaper organizations. Display growth is now

keeping pace with search growth. Starting in 2006, newspapers lost share of local advertising dramatically to so-

called pure plays, digital-only sites like Google or Monster, many of them with no news content. But in 2011, their

growth rate stayed even and will grow faster than the pure plays in 2012, Borrell predicts.29

Circulation Nurmers and Revenue

htIp:l/stateollhemeds.orgI20121reNspapers-buildirg-digital-r ......... -prlMlS-painfully-slowi 12124

Case 2:14-cv-00445-CW Document 22-2 Filed 06/30/14 Page 13 of 25

6/2712014 N ..... papers: Buildirg Digi1al R ........ Prlll<lS PainfullySiowl Slate of the Media

This has been the year in which the audit rules are changing and drculation totals cannot validly be compared to

those of previous years. The first apples·to·apples comparison will come from the Audit Bureau of Circulations six·

month period ending March 31 and released roughly May 1.

Even without strict comparability, though, the trend is clear. Daily print drculation continued to decline in 2011,

though at a rate perhaps only half as bad as the worst of the last decade - under 5% rather than the peak of nearly

10%. Sunday drculation industry-wide is probably down slightly, though many individual papers have shown growth.

As noted in earlier reports some of the drculation losses over time can be traced to price increases and voluntarily

discontinuing service to remote areas.

While ABC is not making year-to-year comparisons, a number of the public companies keep their own figures,

typically reporting a loss in the low and mid-single digits at year's end. ABC's total drculation (print and digital)

among roughly 650 audited organizations for the six-month period ending September 30, 2011 was 33.4 miUion dail

and 38.6 miUion Sunday. That contrasts with 34.0 miUion daily and 38.2 million Sunday in 2010.30 Those changes ar

relatively small and may reflect slightly more lenient rules.