Embed Size (px)

Citation preview

Pakistan Market Strategy 2016

Debunking the myth of the cheap KSE

2

TABLE OF CONTENTS

SLIDE OVERVIEW 3

STRATEGY 7

SECTOR-WISE ANALYSIS AND RECOMMENDATION 20

BANKS 27

E&P 32

CEMENTS 35

STEEL 37

AUTOS 38

OMC 39

FERTILIZER 42

POWER 43

3

OVERVIEW

4

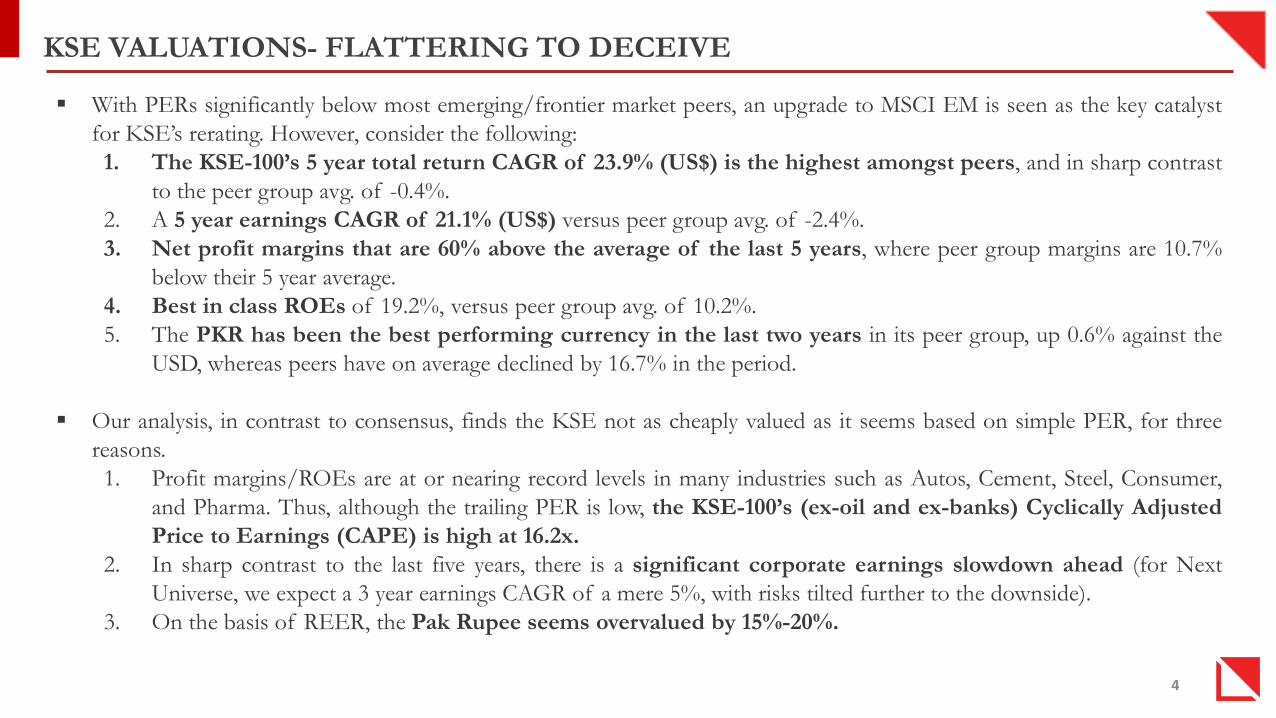

KSE VALUATIONS- FLATTERING TO DECEIVE

With PERs significantly below most emerging/frontier market peers, an upgrade to MSCI EM is seen as the key catalyst

for KSE’s rerating. However, consider the following:

1. The KSE-100’s 5 year total return CAGR of 23.9% (US$) is the highest amongst peers, and in sharp contrast

to the peer group avg. of -0.4%.

2. A 5 year earnings CAGR of 21.1% (US$) versus peer group avg. of -2.4%.

3. Net profit margins that are 60% above the average of the last 5 years, where peer group margins are 10.7%

below their 5 year average.

4. Best in class ROEs of 19.2%, versus peer group avg. of 10.2%.

5. The PKR has been the best performing currency in the last two years in its peer group, up 0.6% against the

USD, whereas peers have on average declined by 16.7% in the period.

Our analysis, in contrast to consensus, finds the KSE not as cheaply valued as it seems based on simple PER, for three

reasons.

1. Profit margins/ROEs are at or nearing record levels in many industries such as Autos, Cement, Steel, Consumer,

and Pharma. Thus, although the trailing PER is low, the KSE-100’s (ex-oil and ex-banks) Cyclically Adjusted

Price to Earnings (CAPE) is high at 16.2x.

2. In sharp contrast to the last five years, there is a significant corporate earnings slowdown ahead (for Next

Universe, we expect a 3 year earnings CAGR of a mere 5%, with risks tilted further to the downside).

3. On the basis of REER, the Pak Rupee seems overvalued by 15%-20%.

5

CAN SUCH HIGH PROFIT MARGINS SUSTAIN?

“Profit margins are probably the most mean-reverting series in finance.” Jeremy Grantham- GMO

Over the last 5 years, margins in Pakistan have been aided by a lack of local and international competition, due to a weak

economic outlook. As a result, incumbents have benefited from the lack of competition. However, this is now likely to change

as Pakistan’s economic outlook is improving considerably, and both local and foreign investment will be more forthcoming.

Competitive pressures are likely to rise across industries.

The PKR’s strength has considerably helped profitability in sectors such as Pharma and Autos. Sooner or later, policy-

makers will need to reduce the extent of overvaluation of the PKR.

Import duty has also been a key driver for margin sustainability in certain manufacturing sectors. However, with China now having

significant surplus capacity in key industries, such as Steel, Cement, and Fertilizer, it is only a matter of time before

Pakistani manufacturers feel the heat in terms of pricing power.

China has now got a stated “Go Abroad” strategy for its manufacturing firms. With Chinese investment already initiated in the

power sector, it is possible that Chinese Steel, Cement and Auto manufacturers directly set-up plants in Pakistan. There is

precedent of this in Africa and Central Asia.

CPEC, the development of the Western Chinese province of Xinjiang, and removal of Iranian sanctions will also be a key

factor in keeping profit margins of Pakistani companies in check. Previously, as China’s western province was not developed,

and Iran was closed for trade, Pak manufacturing sector was relatively insulated from import pressures. These will be felt more

keenly, going forward, in our view.

6

RECOMMENDATION- BUY VALUE RATHER THAN CHASE THE TREND

In this context, we find no gaping under-valuation for the KSE as a whole, and advise a strict bottom-up approach to identify

value.

We recommend a high conviction Overweight stance on the Pak Banking sector, which we believe will see significant foreign

interest in case of an MSCI upgrade. It is also an ideal play on Pakistan’s improving economic prospects, with valuations at very

attractive levels. In the back-drop of improving economic growth, Pak banks are likely to catch up in the next 3-5 years to emerging

market peers in terms of pvt. sector credit growth.

Conglomerates like ENGRO and LUCK will also be key beneficiaries of a potential upgrade to MSCI EM, being foreign

investor favorites, and likely included in the MSCI Pak.

Selected plays in E&Ps (OGDC), OMCs (PSO), Fertilizers (EFERT) and Power (PKGP and LPL) offer significant value as well.

These stocks all hold up well in the case of oil remaining “lower for longer.”

However, in sectors like Autos and Cements, the extent of current high margins will likely limit rerating upside. Whilst these

sectors may look very attractive on trailing PER, on CAPE basis they seem more fairly valued. CHCC remains our top pick in the

Cement sector.

• Sectors such as Consumer and Pharma already seem “priced to perfection”, with margins above historical averages, and very

high PE multiples.

7

STRATEGY

8

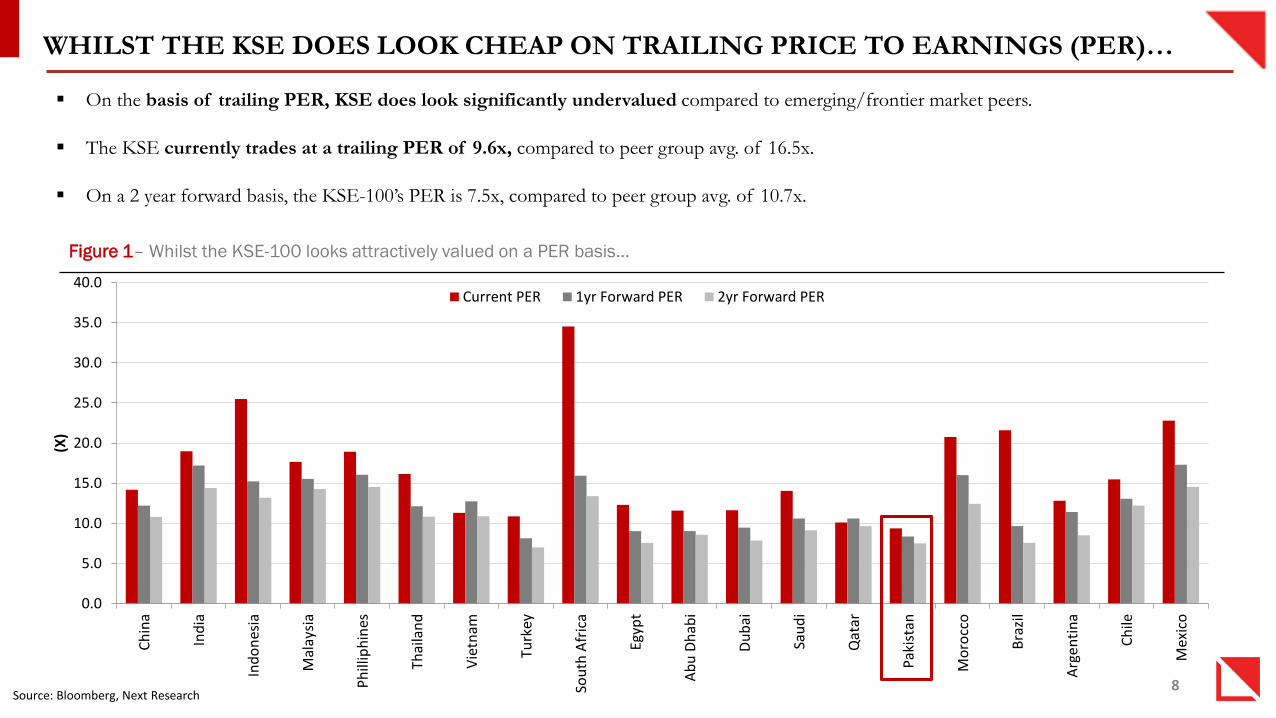

WHILST THE KSE DOES LOOK CHEAP ON TRAILING PRICE TO EARNINGS (PER)…

Source: Bloomberg, Next Research

Figure 1– Whilst the KSE-100 looks attractively valued on a PER basis…

On the basis of trailing PER, KSE does look significantly undervalued compared to emerging/frontier market peers.

The KSE currently trades at a trailing PER of 9.6x, compared to peer group avg. of 16.5x.

On a 2 year forward basis, the KSE-100’s PER is 7.5x, compared to peer group avg. of 10.7x.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Ch

ina

Ind

ia

Ind

on

esia

Mal

aysi

a

Ph

illip

hin

es

Thai

lan

d

Vie

tnam

Turk

ey

Sou

th A

fric

a

Egyp

t

Ab

u D

hab

i

Du

bai

Sau

di

Qat

ar

Pak

ista

n

Mo

rocc

o

Bra

zil

Arg

enti

na

Ch

ile

Mex

ico

(X)

Current PER 1yr Forward PER 2yr Forward PER

9

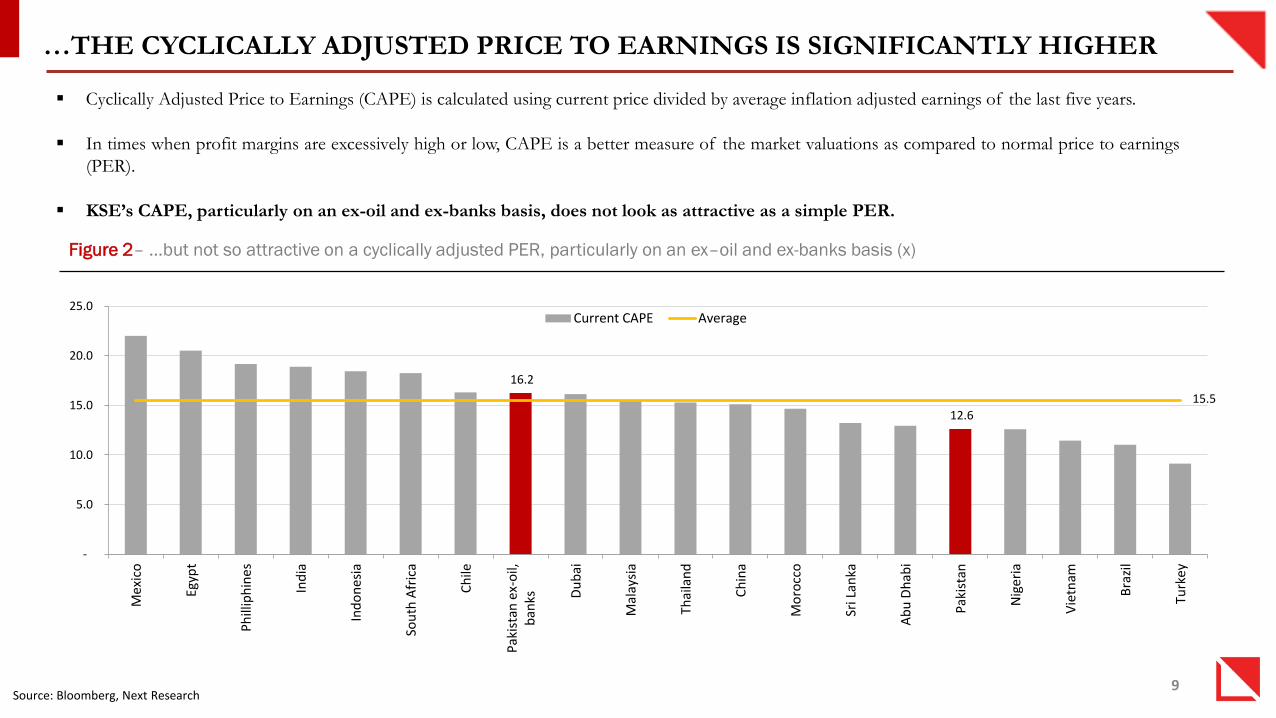

…THE CYCLICALLY ADJUSTED PRICE TO EARNINGS IS SIGNIFICANTLY HIGHER

Source: Bloomberg, Next Research

Figure 2– …but not so attractive on a cyclically adjusted PER, particularly on an ex–oil and ex-banks basis (x)

Cyclically Adjusted Price to Earnings (CAPE) is calculated using current price divided by average inflation adjusted earnings of the last five years.

In times when profit margins are excessively high or low, CAPE is a better measure of the market valuations as compared to normal price to earnings

(PER).

KSE’s CAPE, particularly on an ex-oil and ex-banks basis, does not look as attractive as a simple PER.

16.2

12.6

15.5

-

5.0

10.0

15.0

20.0

25.0

Mex

ico

Egyp

t

Ph

illip

hin

es

Ind

ia

Ind

on

esia

Sou

th A

fric

a

Ch

ile

Pak

ista

n e

x-o

il,b

anks D

ub

ai

Mal

aysi

a

Thai

lan

d

Ch

ina

Mo

rocc

o

Sri L

anka

Ab

u D

hab

i

Pak

ista

n

Nig

eria

Vie

tnam

Bra

zil

Turk

ey

Current CAPE Average

10

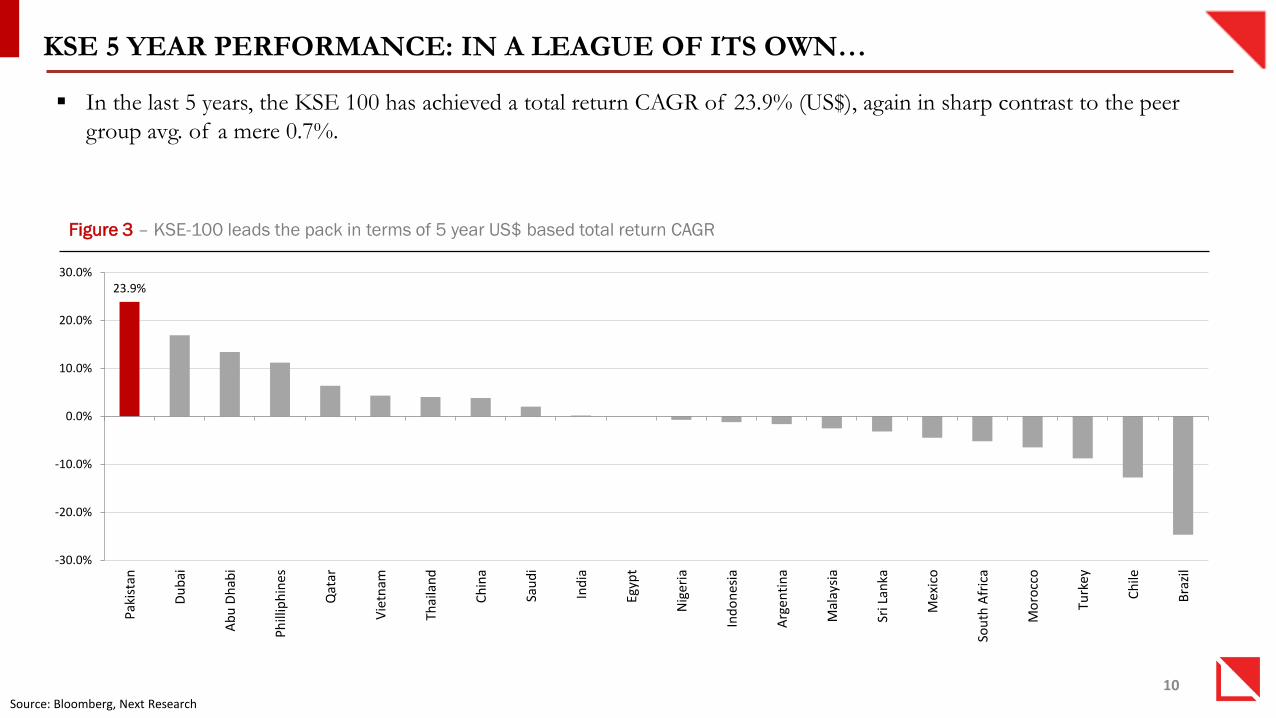

KSE 5 YEAR PERFORMANCE: IN A LEAGUE OF ITS OWN…

Source: Bloomberg, Next Research

In the last 5 years, the KSE 100 has achieved a total return CAGR of 23.9% (US$), again in sharp contrast to the peer

group avg. of a mere 0.7%.

Figure 3 – KSE-100 leads the pack in terms of 5 year US$ based total return CAGR

23.9%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

Pak

ista

n

Du

bai

Ab

u D

hab

i

Ph

illip

hin

es

Qat

ar

Vie

tnam

Thai

lan

d

Ch

ina

Sau

di

Ind

ia

Egyp

t

Nig

eria

Ind

on

esia

Arg

enti

na

Mal

aysi

a

Sri L

anka

Mex

ico

Sou

th A

fric

a

Mo

rocc

o

Turk

ey

Ch

ile

Bra

zil

11

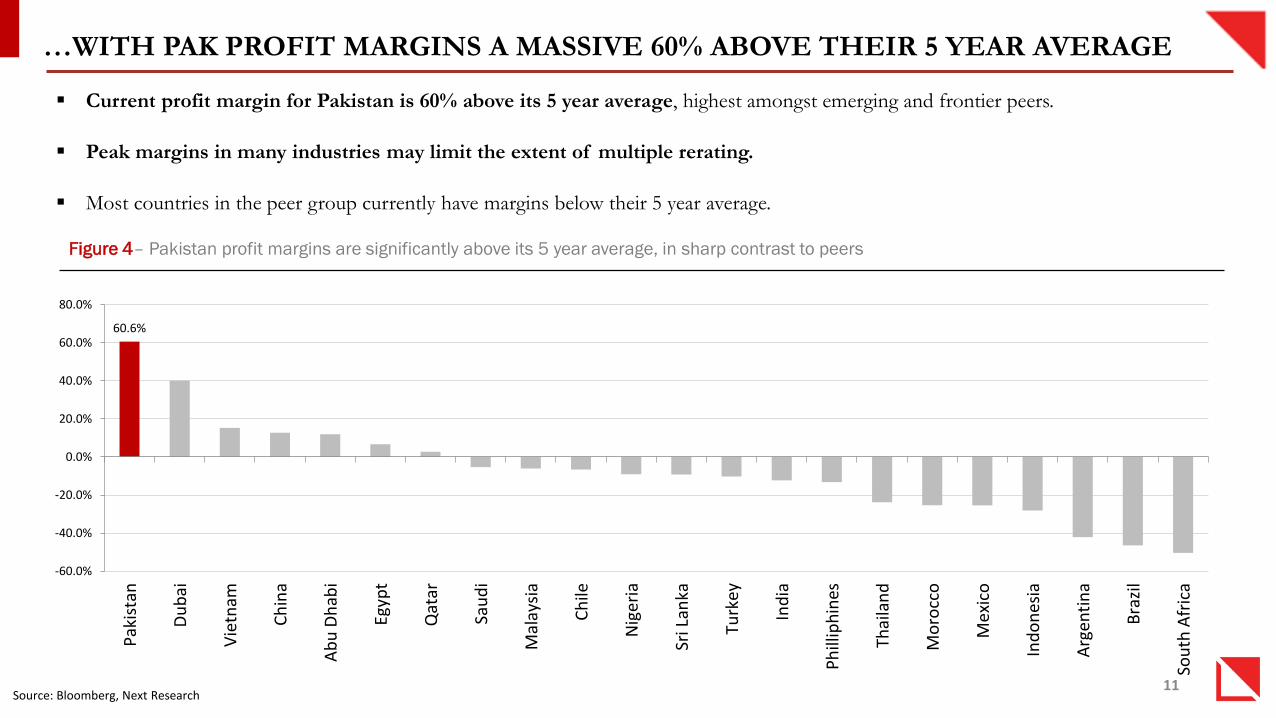

…WITH PAK PROFIT MARGINS A MASSIVE 60% ABOVE THEIR 5 YEAR AVERAGE

Source: Bloomberg, Next Research

Figure 4– Pakistan profit margins are significantly above its 5 year average, in sharp contrast to peers

Current profit margin for Pakistan is 60% above its 5 year average, highest amongst emerging and frontier peers.

Peak margins in many industries may limit the extent of multiple rerating.

Most countries in the peer group currently have margins below their 5 year average.

60.6%

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

Pak

ista

n

Du

bai

Vie

tnam

Ch

ina

Ab

u D

hab

i

Egyp

t

Qat

ar

Sau

di

Mal

aysi

a

Ch

ile

Nig

eria

Sri L

anka

Turk

ey

Ind

ia

Ph

illip

hin

es

Thai

lan

d

Mo

rocc

o

Mex

ico

Ind

on

esia

Arg

enti

na

Bra

zil

Sou

th A

fric

a

12

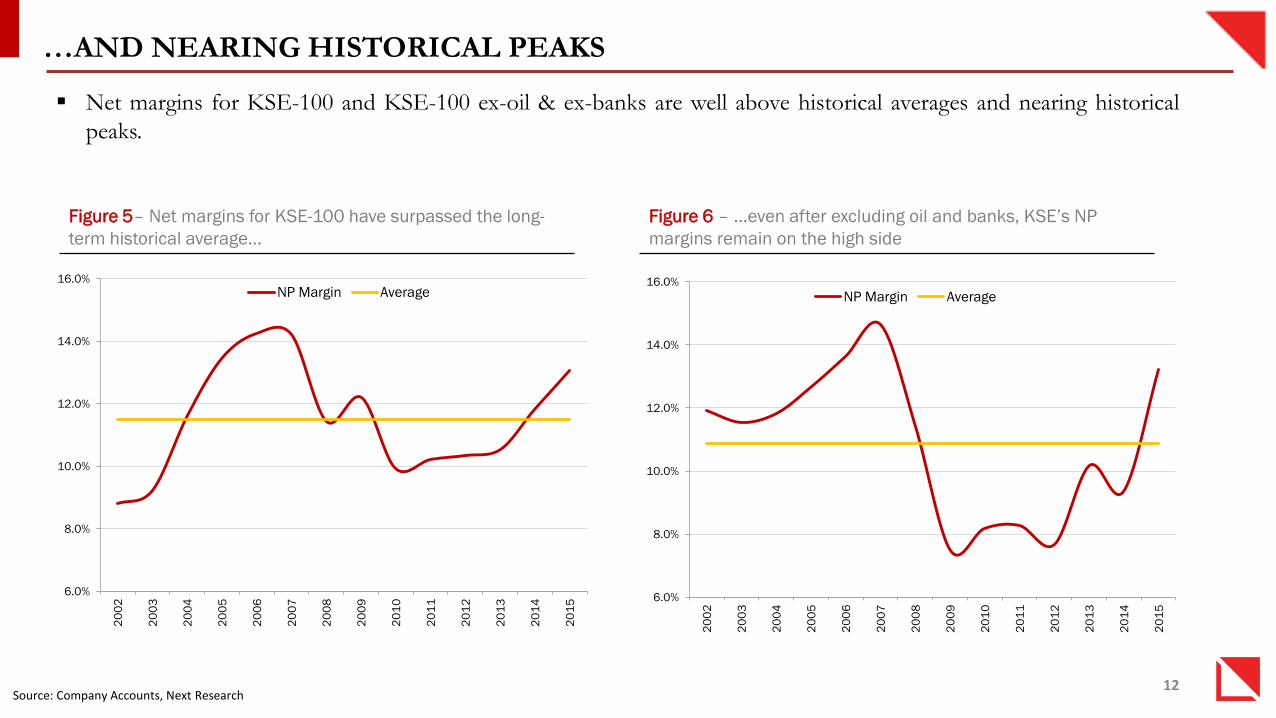

…AND NEARING HISTORICAL PEAKS

Source: Company Accounts, Next Research

Figure 5– Net margins for KSE-100 have surpassed the long-

term historical average…

Net margins for KSE-100 and KSE-100 ex-oil & ex-banks are well above historical averages and nearing historical

peaks.

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

NP Margin Average

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

NP Margin Average

Figure 6 – …even after excluding oil and banks, KSE’s NP

margins remain on the high side

13

PAK ROE HIGHEST AMONGST EMERGING & FRONTIER PEERS…

Source: Bloomberg, Company Accounts, Next Research

Figure 7– Pakistan ROEs are best in class

KSE-100’s ROE at 19.2% is the highest amongst emerging and frontier market peer group, helped by a combination

of lower commodity prices, lack of internal competition, import duty protection, and a strong exchange rate.

As competition rises both locally and internationally, sustaining ROEs at these elevated levels will be difficult.

19.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Pa

kis

tan

Vie

tna

m

Qa

tar

Ch

ina

Ph

illip

hin

es

Tu

rke

y

Nig

eri

a

Ind

ia

Ab

u D

ha

bi

Sri

La

nk

a

Sa

ud

i

Ma

lays

ia

Mo

rocco

Ind

on

esia

Du

ba

i

Me

xico

Ch

ile

Th

aila

nd

Arg

en

tin

a

Egyp

t

So

uth

Afr

ica

Bra

zil

Current 5 yr avg.

14

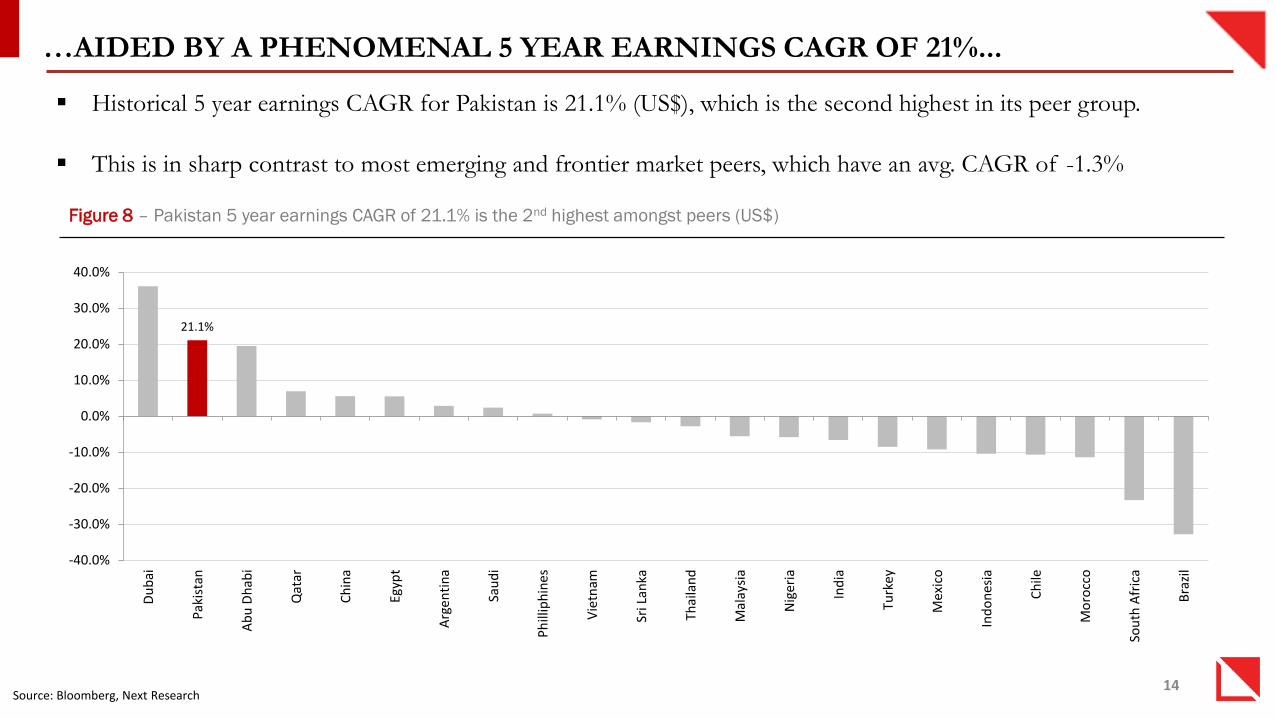

…AIDED BY A PHENOMENAL 5 YEAR EARNINGS CAGR OF 21%...

Source: Bloomberg, Next Research

Figure 8 – Pakistan 5 year earnings CAGR of 21.1% is the 2nd highest amongst peers (US$)

Historical 5 year earnings CAGR for Pakistan is 21.1% (US$), which is the second highest in its peer group.

This is in sharp contrast to most emerging and frontier market peers, which have an avg. CAGR of -1.3%

21.1%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

Du

bai

Pak

ista

n

Ab

u D

hab

i

Qat

ar

Ch

ina

Egyp

t

Arg

enti

na

Sau

di

Ph

illip

hin

es

Vie

tnam

Sri L

anka

Thai

lan

d

Mal

aysi

a

Nig

eria

Ind

ia

Turk

ey

Mex

ico

Ind

on

esia

Ch

ile

Mo

rocc

o

Sou

th A

fric

a

Bra

zil

15

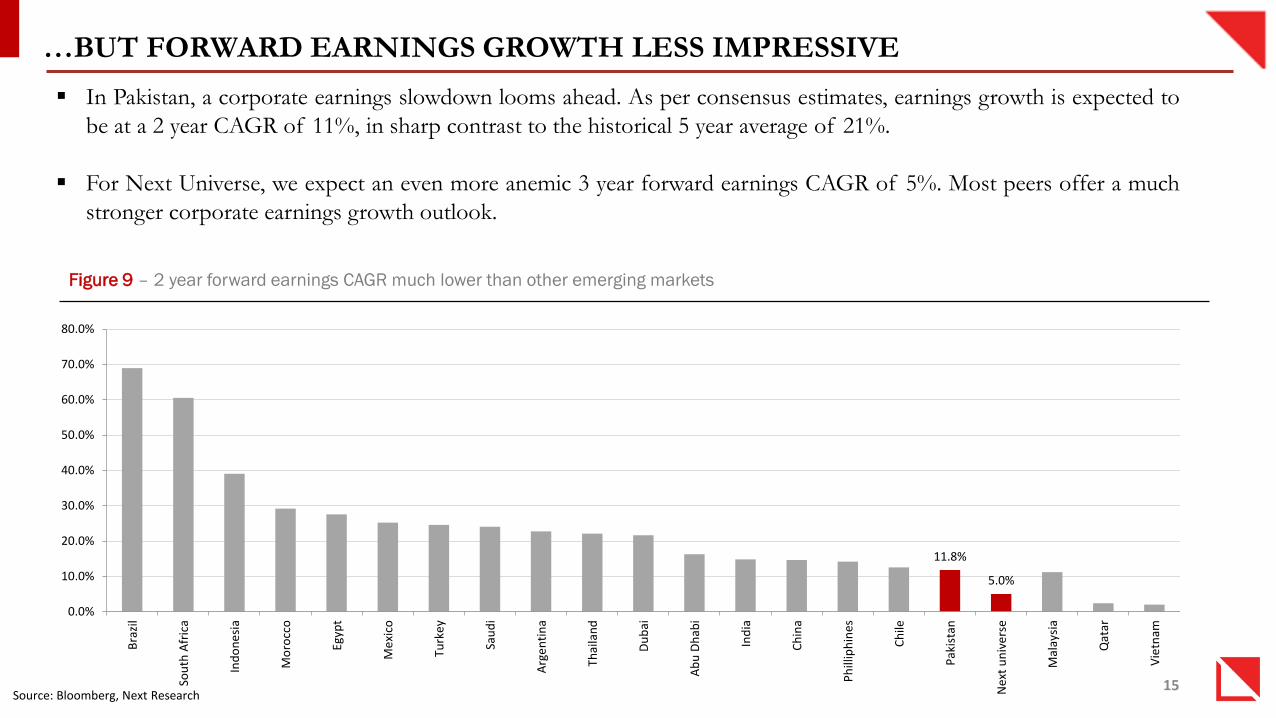

…BUT FORWARD EARNINGS GROWTH LESS IMPRESSIVE

Source: Bloomberg, Next Research

In Pakistan, a corporate earnings slowdown looms ahead. As per consensus estimates, earnings growth is expected to

be at a 2 year CAGR of 11%, in sharp contrast to the historical 5 year average of 21%.

For Next Universe, we expect an even more anemic 3 year forward earnings CAGR of 5%. Most peers offer a much

stronger corporate earnings growth outlook.

Figure 9 – 2 year forward earnings CAGR much lower than other emerging markets

11.8%

5.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Bra

zil

Sou

th A

fric

a

Ind

on

esi

a

Mo

rocc

o

Egyp

t

Me

xico

Turk

ey

Sau

di

Arg

en

tin

a

Thai

lan

d

Du

bai

Ab

u D

hab

i

Ind

ia

Ch

ina

Ph

illip

hin

es

Ch

ile

Pak

ista

n

Nex

t u

niv

ers

e

Mal

aysi

a

Qat

ar

Vie

tnam

16

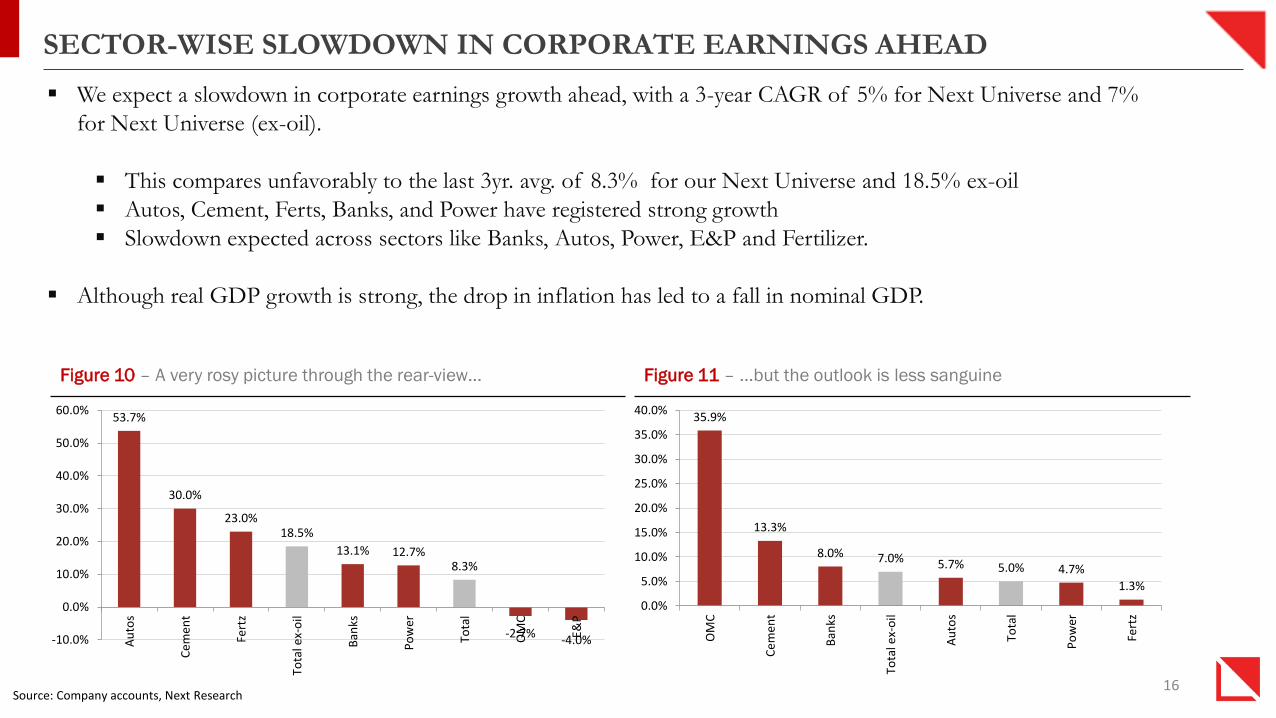

SECTOR-WISE SLOWDOWN IN CORPORATE EARNINGS AHEAD

We expect a slowdown in corporate earnings growth ahead, with a 3-year CAGR of 5% for Next Universe and 7%

for Next Universe (ex-oil).

This compares unfavorably to the last 3yr. avg. of 8.3% for our Next Universe and 18.5% ex-oil

Autos, Cement, Ferts, Banks, and Power have registered strong growth

Slowdown expected across sectors like Banks, Autos, Power, E&P and Fertilizer.

Although real GDP growth is strong, the drop in inflation has led to a fall in nominal GDP.

53.7%

30.0%

23.0%18.5%

13.1% 12.7%8.3%

-2.7%-4.0%-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Au

tos

Ce

me

nt

Fert

z

Tota

l ex-

oil

Ban

ks

Po

wer

Tota

l

OM

C

E&P

35.9%

13.3%

8.0% 7.0% 5.7% 5.0% 4.7%

1.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

OM

C

Ce

me

nt

Ban

ks

Tota

l ex-

oil

Au

tos

Tota

l

Po

wer

Fert

z

Figure 11 – …but the outlook is less sanguineFigure 10 – A very rosy picture through the rear-view…

Source: Company accounts, Next Research

17

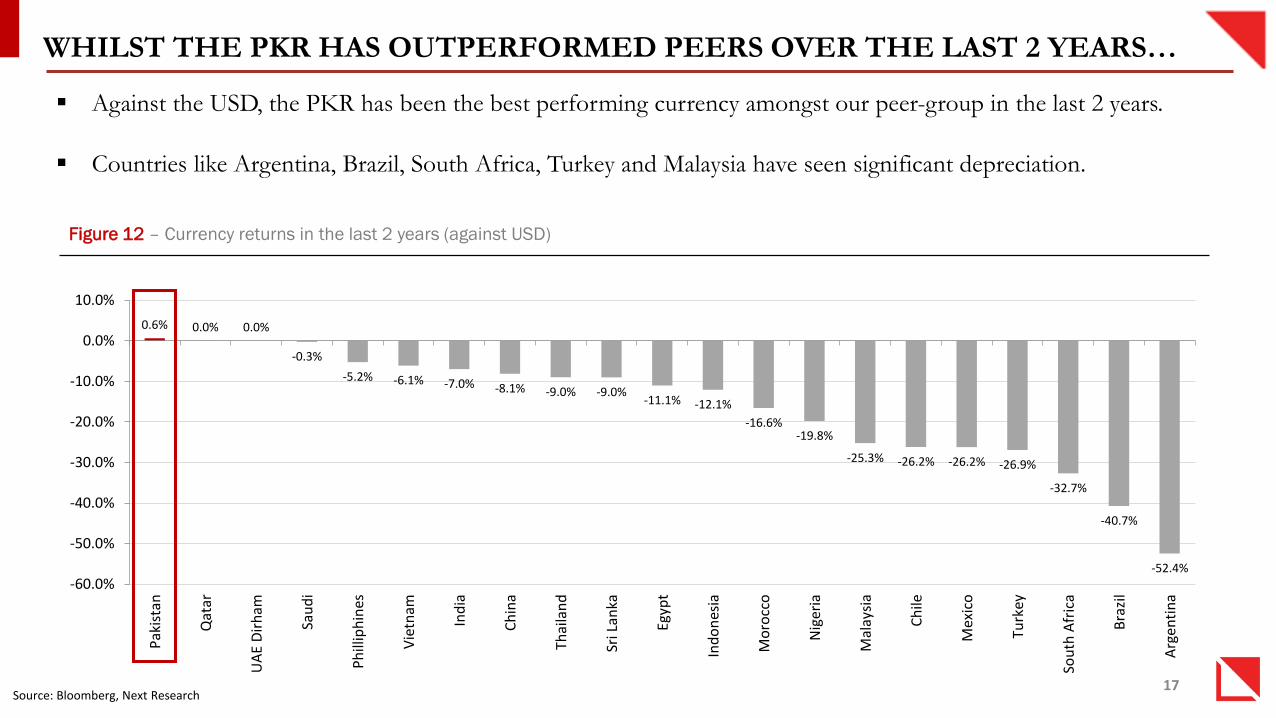

WHILST THE PKR HAS OUTPERFORMED PEERS OVER THE LAST 2 YEARS…

Source: Bloomberg, Next Research

Against the USD, the PKR has been the best performing currency amongst our peer-group in the last 2 years.

Countries like Argentina, Brazil, South Africa, Turkey and Malaysia have seen significant depreciation.

Figure 12 – Currency returns in the last 2 years (against USD)

0.6% 0.0% 0.0%

-0.3%

-5.2% -6.1% -7.0% -8.1% -9.0% -9.0%-11.1% -12.1%

-16.6%-19.8%

-25.3% -26.2% -26.2% -26.9%

-32.7%

-40.7%

-52.4%

-60.0%

-50.0%

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

Pak

ista

n

Qat

ar

UA

E D

irh

am

Sau

di

Ph

illip

hin

es

Vie

tnam

Ind

ia

Ch

ina

Thai

lan

d

Sri L

anka

Egyp

t

Ind

on

esia

Mo

rocc

o

Nig

eria

Mal

aysi

a

Ch

ile

Mex

ico

Turk

ey

Sou

th A

fric

a

Bra

zil

Arg

enti

na

18

…IT NOW LOOKS STEEPLY OVERVALUED ON A REER BASIS

Source: Bloomberg, SBP, Next Research

The PKR is now amongst the most overvalued currencies in the world, on the basis of its Real Effective Exchange Rate

(REER).

REER measures a currency versus its trading partners; a level of 100 is neutral, and above 100 indicates overvaluation. The

PKR is currently at a level of 121.2.

In contrast, many emerging market currencies look decidedly undervalued after their recent sharp depreciation.

Figure 13 – PKR is overvalued by 21%, which can dampen market return in US$

21.0

(40.0)

(30.0)

(20.0)

(10.0)

-

10.0

20.0

30.0

40.0

Ch

ina

Sa

ud

i

Pa

kis

tan

Ph

illip

hin

es

UA

E

Ind

ia

Th

aila

nd

Arg

en

tin

a

Ind

on

esia

Me

xico

Ch

ile

Ma

lays

ia

Tu

rke

y

So

uth

Afr

ica

Bra

zil

Ove

rva

luta

tio

n/(U

nd

erv

alu

ati

on

)

19

10-15% DEVALUATION NEEDED TO REVIVE EXPORTS

Source: SBP, Next Research

The PKR’s REER is in uncharted territory, seen in a historical context.

Average REER in the last 13 years has been 101.4.

During the 2004-2007 period of relative FX stability, REER was consistently below the neutral level of 100.

Without a 10-15% depreciation in PKR versus trading partners, exports cannot be revived.

Figure 14 – PKR REER extremely overvalued, even seen in a historical context

80

85

90

95

100

105

110

115

120

125

Jun

e'0

2

Jun

e'0

3

Jun

e'0

4

Jun

e'0

5

Jun

e'0

6

Jun

e'0

7

Jun

e'0

8

Jun

e'0

9

Jun

e'1

0

Jun

e'1

1

Jun

e'1

2

Jun

e'1

3

Jun

e'1

4

Jun

e'1

5

No

v'1

5

20

SECTOR-WISE ANALYSIS & RECOMMENDATIONS

21

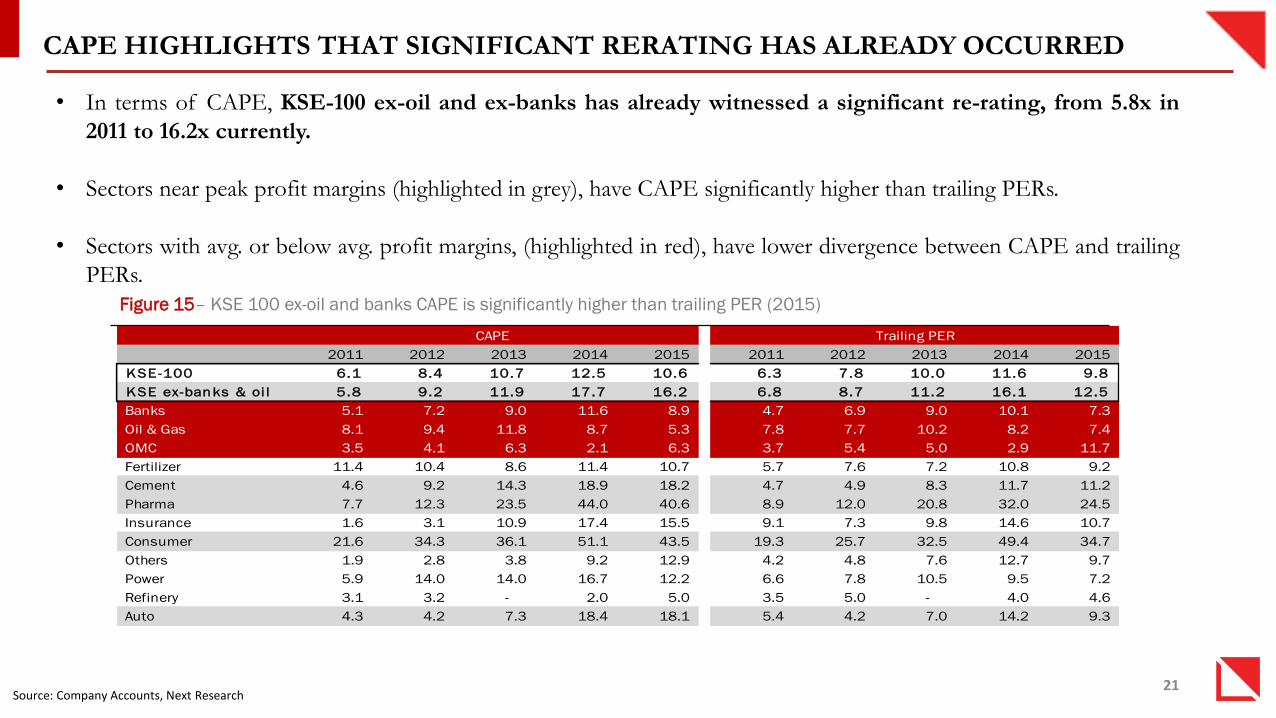

CAPE HIGHLIGHTS THAT SIGNIFICANT RERATING HAS ALREADY OCCURRED

Source: Company Accounts, Next Research

Figure 15– KSE 100 ex-oil and banks CAPE is significantly higher than trailing PER (2015)

• In terms of CAPE, KSE-100 ex-oil and ex-banks has already witnessed a significant re-rating, from 5.8x in

2011 to 16.2x currently.

• Sectors near peak profit margins (highlighted in grey), have CAPE significantly higher than trailing PERs.

• Sectors with avg. or below avg. profit margins, (highlighted in red), have lower divergence between CAPE and trailing

PERs.

2011 2012 2013 2014 2015 2011 2012 2013 2014 2015

KSE-100 6.1 8.4 10.7 12.5 10.6 6.3 7.8 10.0 11.6 9.8

KSE ex-banks & oi l 5.8 9.2 11.9 17.7 16.2 6.8 8.7 11.2 16.1 12.5

Banks 5.1 7.2 9.0 11.6 8.9 4.7 6.9 9.0 10.1 7.3

Oil & Gas 8.1 9.4 11.8 8.7 5.3 7.8 7.7 10.2 8.2 7.4

OMC 3.5 4.1 6.3 2.1 6.3 3.7 5.4 5.0 2.9 11.7

Fertilizer 11.4 10.4 8.6 11.4 10.7 5.7 7.6 7.2 10.8 9.2

Cement 4.6 9.2 14.3 18.9 18.2 4.7 4.9 8.3 11.7 11.2

Pharma 7.7 12.3 23.5 44.0 40.6 8.9 12.0 20.8 32.0 24.5

Insurance 1.6 3.1 10.9 17.4 15.5 9.1 7.3 9.8 14.6 10.7

Consumer 21.6 34.3 36.1 51.1 43.5 19.3 25.7 32.5 49.4 34.7

Others 1.9 2.8 3.8 9.2 12.9 4.2 4.8 7.6 12.7 9.7

Power 5.9 14.0 14.0 16.7 12.2 6.6 7.8 10.5 9.5 7.2

Refinery 3.1 3.2 - 2.0 5.0 3.5 5.0 - 4.0 4.6

Auto 4.3 4.2 7.3 18.4 18.1 5.4 4.2 7.0 14.2 9.3

CAPE Trailing PER

22

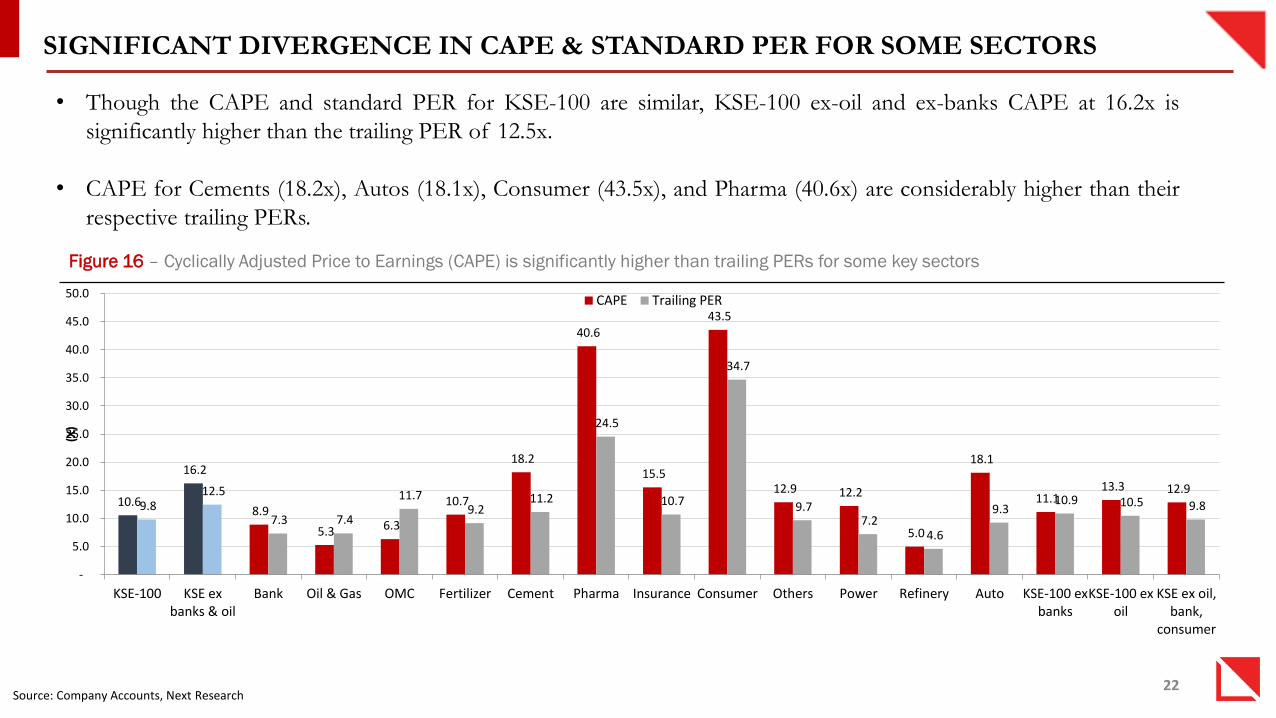

SIGNIFICANT DIVERGENCE IN CAPE & STANDARD PER FOR SOME SECTORS

Source: Company Accounts, Next Research

Figure 16 – Cyclically Adjusted Price to Earnings (CAPE) is significantly higher than trailing PERs for some key sectors

• Though the CAPE and standard PER for KSE-100 are similar, KSE-100 ex-oil and ex-banks CAPE at 16.2x is

significantly higher than the trailing PER of 12.5x.

• CAPE for Cements (18.2x), Autos (18.1x), Consumer (43.5x), and Pharma (40.6x) are considerably higher than their

respective trailing PERs.

10.6

16.2

8.9

5.3 6.3

10.7

18.2

40.6

15.5

43.5

12.9 12.2

5.0

18.1

11.1 13.3 12.9

9.8 12.5

7.3 7.4

11.7 9.2

11.2

24.5

10.7

34.7

9.7 7.2

4.6

9.3 10.9 10.5 9.8

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

KSE-100 KSE exbanks & oil

Bank Oil & Gas OMC Fertilizer Cement Pharma Insurance Consumer Others Power Refinery Auto KSE-100 exbanks

KSE-100 exoil

KSE ex oil,bank,

consumer

(X)

CAPE Trailing PER

23

PEAK MARGINS RESULT IN HIGH CAPE FOR AUTOS & CEMENTS …

Source: Company Accounts, Next Research

Figure 17 – Auto margins at their highest level…

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

NP Margin Average

Figure 18 – …leading to a wide gap between CAPE & PER

Figure 19 – Cement margins also nearing historic highs … Figure 20 – …with CAPE valuations reflecting the trend

18.1

9.3

-

5.0

10.0

15.0

20.0

25.0

2011 2012 2013 2014 2015

(X)

CAPE Trailing PER

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

NP Margin Average

18.2

11.2

-

5.0

10.0

15.0

20.0

25.0

2011 2012 2013 2014 2015(X

)

CAPE Trailing PER

24

…AND FOR CONSUMER & PHARMA AS WELL

Source: Company Accounts, Next Research

Figure 21 – Consumer margins above historical avg... Figure 22– …with CAPE at 43x points to rich valuations

Figure 23– Pharmaceuticals margins on the up as well… Figure 24– …with CAPE at a hefty 40x.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

NP Margin Average

0.0%

5.0%

10.0%

15.0%

20.0%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

NP Margin Average

43.5

34.7

20.0

30.0

40.0

50.0

60.0

2011 2012 2013 2014 2015

(X)

CAPE Trailing PER

40.6

24.5

-

10.0

20.0

30.0

40.0

50.0

2011 2012 2013 2014 2015(X

)

CAPE Trailing PER

25

HOWEVER, BANKS & E&P WITH AVG. MARGINS OFFER BETTER VALUE…

Source: Company Accounts, Next Research

Figure 25– Banks’ margins near historical avg… Figure 26– …with CAPE also in a reasonable range…

Figure 27– …and a similar trend in E&Ps… Figure 28– …with CAPE currently below trailing PER

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

NP Margin Average

8.9

7.3

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2011 2012 2013 2014 2015

(X)

CAPE Trailing PER

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

NP Margin Average

5.3

7.4

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2011 2012 2013 2014 2015

(X)

CAPE Trailing PER

26

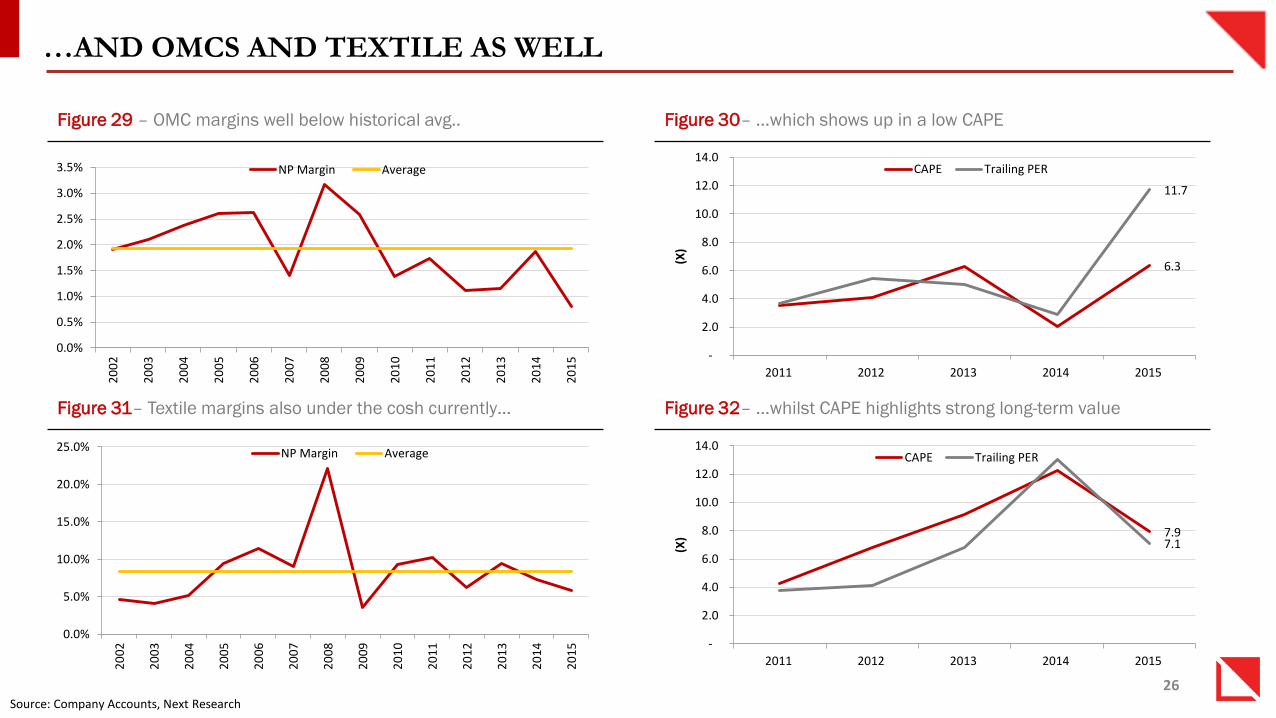

…AND OMCS AND TEXTILE AS WELL

Source: Company Accounts, Next Research

Figure 29 – OMC margins well below historical avg.. Figure 30– …which shows up in a low CAPE

Figure 31– Textile margins also under the cosh currently… Figure 32– …whilst CAPE highlights strong long-term value

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

NP Margin Average

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

NP Margin Average

6.3

11.7

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2011 2012 2013 2014 2015

(X)

CAPE Trailing PER

7.9 7.1

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2011 2012 2013 2014 2015

(X)

CAPE Trailing PER

27

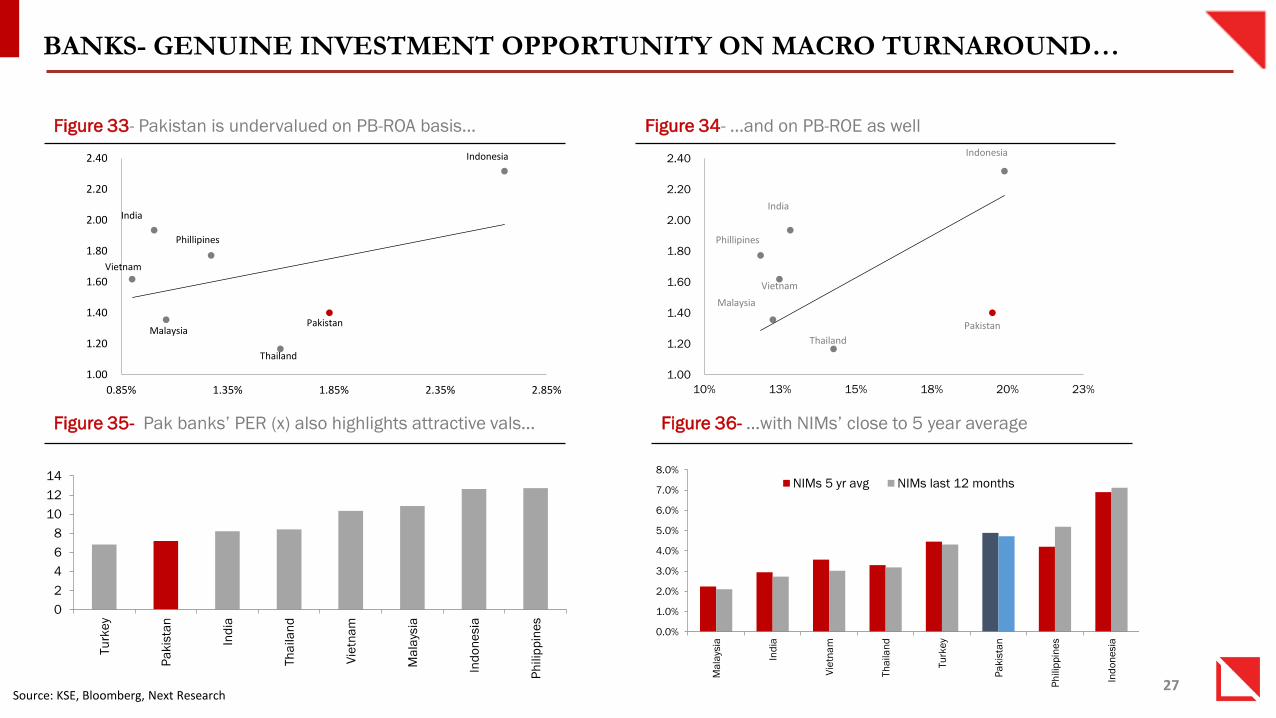

BANKS- GENUINE INVESTMENT OPPORTUNITY ON MACRO TURNAROUND…

Source: KSE, Bloomberg, Next Research

Figure 33- Pakistan is undervalued on PB-ROA basis… Figure 34- …and on PB-ROE as well

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

0.85% 1.35% 1.85% 2.35% 2.85%

Indonesia

Malaysia

Vietnam

Phillipines

India

Thailand

Pakistan

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

10% 13% 15% 18% 20% 23%

Pakistan

India

Indonesia

Malaysia

Phillipines

Thailand

Vietnam

0

2

4

6

8

10

12

14

Tu

rke

y

Pa

kis

tan

Ind

ia

Th

aila

nd

Vie

tna

m

Ma

lays

ia

Ind

on

esia

Ph

ilip

pin

es

Figure 35- Pak banks’ PER (x) also highlights attractive vals… Figure 36- …with NIMs’ close to 5 year average

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Ma

lays

ia

Ind

ia

Vie

tna

m

Th

aila

nd

Tu

rke

y

Pa

kis

tan

Ph

ilip

pin

es

Ind

on

esia

NIMs 5 yr avg NIMs last 12 months

28

VALUATIONS ATTRACTIVE IN A HISTORICAL CONTEXT

• Next banking universe trades at the 25th percentile of its 5 year P/B range, with UBL, MCB, ABL and BAHL trading

near their 5 year lows.

• On a PER basis, UBL, MCB, and ABL look attractively valued. On avg, Pak banks currently trade at 43rd percentile of

its 5 year PE average.

Source: KSE, Bloomberg, Next Research

Figure 38- Pakistan Banks trade at 43 percentile in PERFigure 37- Pak Banks trade at 25 percentile P/B of its 5yr range

25%

15%

57%

0%

8%

29%

18%

44%

0%

20%

40%

60%

80%

100%

Industry UBL PA HBL PA MCB PA ABL PA BAFL PA BAHL PA HMB PA

43%

26%

60%

8%

26%

52% 55%

13%

0%

20%

40%

60%

80%

100%

Industry UBL PA HBL PA MCB PA ABL PA BAFL PA BAHL PA HMB PA

29

PAK ECONOMIC TURNAROUND NOT YET PRICED INTO BANKING STOCKS

Source: KSE, Bloomberg, Next Research

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Pakistan

Philippines Indonesia

Turkey

India

Vietnam

Malaysia

Thailand

Figure 40- …has resulted in Pakistan missing the train of private sector credit

growth (as % of GDP)

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

Pa

kis

tan

Th

aila

nd

Tu

rke

y

Ma

lays

ia

Ind

on

esia

Ph

ilip

pin

es

Ind

ia

5yr Real GDP CAGR

Pakistan’s sluggish real GDP growth avg. of 3.2% in the last 5 years explains the disappointing growth in private sector credit

during the period of 2008-2014.

During the last decade, Pakistan’s pvt. sector credit as a % of GDP has declined to 15.4% from 28% in 2004, whereas peers like

Turkey, Philippines, Indonesia and India have witnessed steep increases.

Turkey in particular, has seen astonishing growth, which was below Pakistan at 17% in 2004, and currently stands at 74%.

With Pakistan’s GDP growth trajectory now on the up, Pakistan is well positioned to catch up significantly to peers in the years

ahead.

Figure 39- Historically sluggish 5year real GDP CAGR of 3.2%,

the lowest in our APAC sample…

30

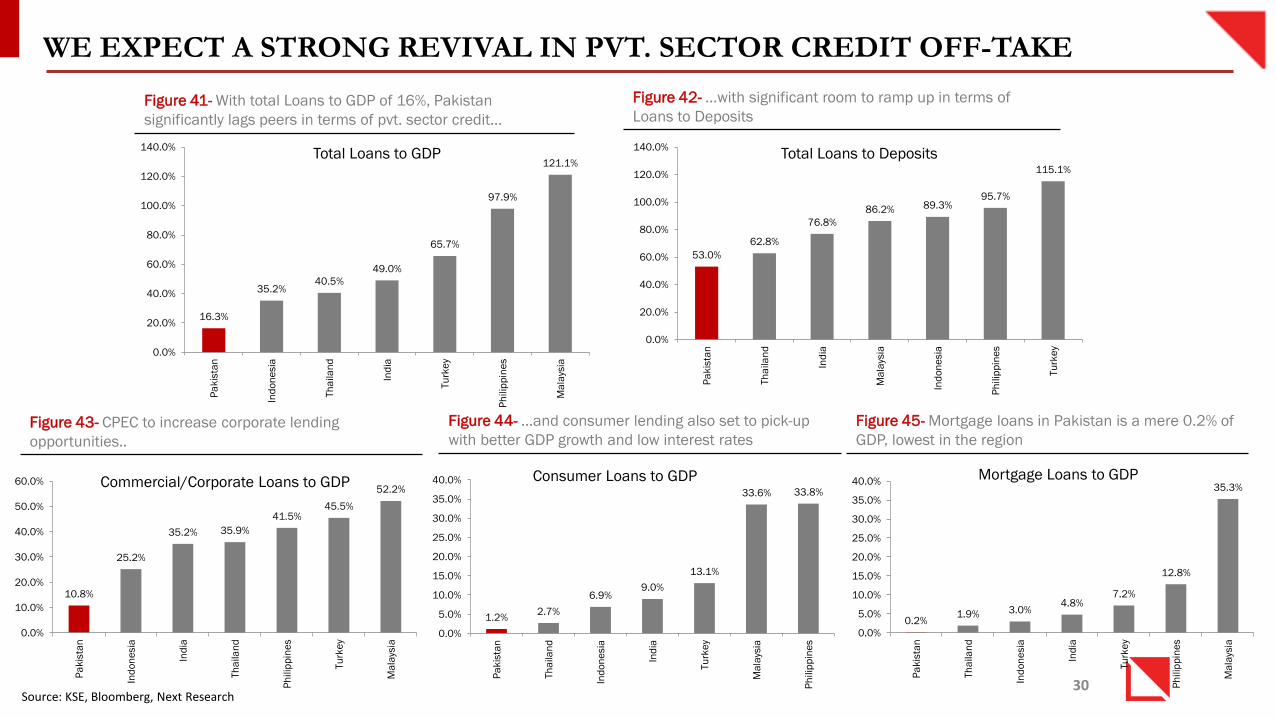

WE EXPECT A STRONG REVIVAL IN PVT. SECTOR CREDIT OFF-TAKE

Source: KSE, Bloomberg, Next Research

16.3%

35.2%40.5%

49.0%

65.7%

97.9%

121.1%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

Pa

kis

tan

Ind

on

esia

Th

aila

nd

Ind

ia

Tu

rke

y

Ph

ilip

pin

es

Ma

lays

ia

53.0%

62.8%

76.8%

86.2% 89.3%95.7%

115.1%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

Pa

kis

tan

Th

aila

nd

Ind

ia

Ma

lays

ia

Ind

on

esia

Ph

ilip

pin

es

Tu

rke

y

Figure 41- With total Loans to GDP of 16%, Pakistan

significantly lags peers in terms of pvt. sector credit…

Figure 42- …with significant room to ramp up in terms of

Loans to Deposits

1.2%2.7%

6.9%9.0%

13.1%

33.6% 33.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Pa

kis

tan

Th

aila

nd

Ind

on

esia

Ind

ia

Tu

rke

y

Ma

lays

ia

Ph

ilip

pin

es

0.2%1.9% 3.0%

4.8%7.2%

12.8%

35.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Pa

kis

tan

Th

aila

nd

Ind

on

esia

Ind

ia

Tu

rke

y

Ph

ilip

pin

es

Ma

lays

ia

10.8%

25.2%

35.2% 35.9%

41.5%45.5%

52.2%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Pa

kis

tan

Ind

on

esia

Ind

ia

Th

aila

nd

Ph

ilip

pin

es

Tu

rke

y

Ma

lays

ia

Figure 43- CPEC to increase corporate lending

opportunities..

Figure 44- …and consumer lending also set to pick-up

with better GDP growth and low interest rates

Figure 45- Mortgage loans in Pakistan is a mere 0.2% of

GDP, lowest in the region

Total Loans to GDP Total Loans to Deposits

Mortgage Loans to GDPConsumer Loans to GDPCommercial/Corporate Loans to GDP

31

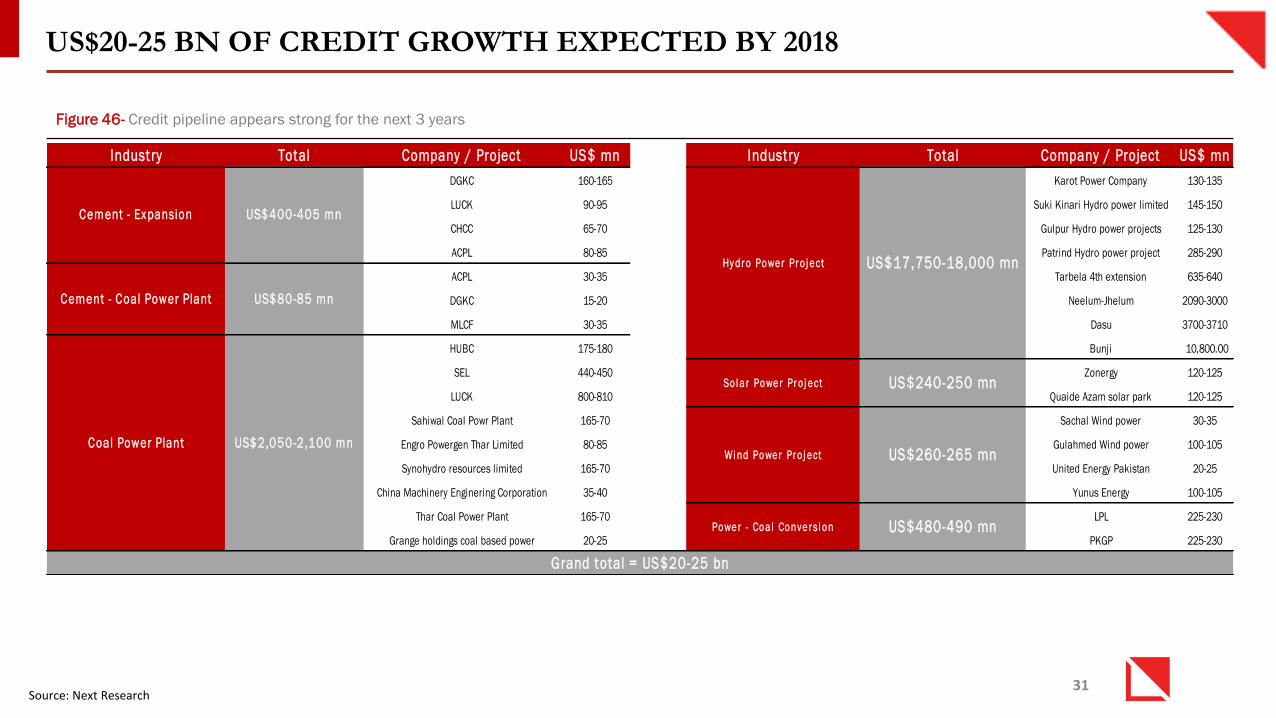

US$20-25 BN OF CREDIT GROWTH EXPECTED BY 2018

Source: Next Research

Industry Total Company / Project US$ mn Industry Total Company / Project US$ mn

DGKC 160-165 Karot Power Company 130-135

LUCK 90-95 Suki Kinari Hydro power limited 145-150

CHCC 65-70 Gulpur Hydro power projects 125-130

ACPL 80-85 Patrind Hydro power project 285-290

ACPL 30-35 Tarbela 4th extension 635-640

DGKC 15-20 Neelum-Jhelum 2090-3000

MLCF 30-35 Dasu 3700-3710

HUBC 175-180 Bunji 10,800.00

SEL 440-450 Zonergy 120-125

LUCK 800-810 Quaide Azam solar park 120-125

Sahiwal Coal Powr Plant 165-70 Sachal Wind power 30-35

Engro Powergen Thar Limited 80-85 Gulahmed Wind power 100-105

Synohydro resources limited 165-70 United Energy Pakistan 20-25

China Machinery Enginering Corporation 35-40 Yunus Energy 100-105

Thar Coal Power Plant 165-70 LPL 225-230

Grange holdings coal based power 20-25 PKGP 225-230

Grand total = US$20-25 bn

Power - Coal Conversi on US$480-490 mn

Cement - Expansion US$400-405 mn

Sol ar Power Pro j ect US$240-250 mn

Wi nd Power Pro j ect US$260-265 mn

Cement - Coal Power Plant US$80-85 mn

Coal Power Plant US$2,050-2,100 mn

US$17,750-18,000 mnHy dro Power Pro j ect

Figure 46- Credit pipeline appears strong for the next 3 years

32

E&P – OGDC RESILIENT IN A LOW CRUDE PRICE ENVIRONMENT

• Pak E&Ps will likely draw attention in 2016 as the valuation

discount appears favorable. Where we eye strong domestic activity,

we flag that the sector may not attract much foreign interest; thus,

lowering the rerating potential.

• We assert that OGDC’s investment case is largely intact owing to

larger chunk of capped pricing for gas fields, and attractive

valuation.

• Although PPL offers a decent upside, uncertainty on the extension

of Sui Mining Lease compels us to remain cautious in the stock.

Source: PPIS, Next Research

FY17E EPS (PKR) PE (x) TP (PKR/sh)

US$/BBL PPL POL OGDC PPL POL OGDC PPL POL OGDC

60 19.1 37.1 23.2 6.0x 6.8x 4.7x 230 380 178

50 16.3 31.9 21.4 7.1x 7.9x 5.1x 211 343 168

40 13.4 26.6 19.2 8.6x 9.5x 5.7x 190 305 157

30 10.2 20.6 16.8 11.3x 12.2x 6.5x 168 263 145

20 6.2 13.6 13.7 18.6x 18.5x 8.0x 140 216 129

Figure 47: OGDC earnings more resilient in a low crude price

6.3% 4.3%

63.6%

0.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

Regional avg PPL POL OGDC

Figure 48: OGDC looks attractive on forward PER… Figure 49: …and on P/B as well, trading at a 5 year low

39.7%

52.3%

32.4%

5.2%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

Regional avg PPL POL OGDC

33

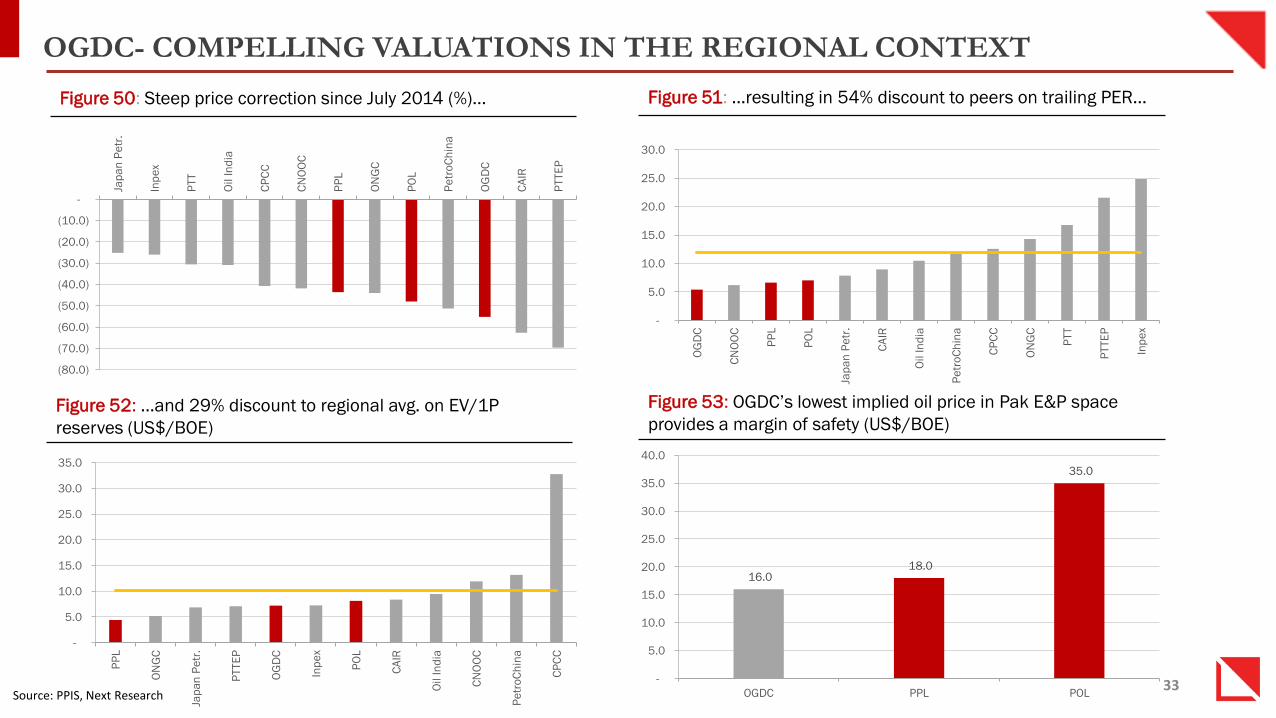

OGDC- COMPELLING VALUATIONS IN THE REGIONAL CONTEXT

Source: PPIS, Next Research

Figure 50: Steep price correction since July 2014 (%)… Figure 51: …resulting in 54% discount to peers on trailing PER…

Figure 52: …and 29% discount to regional avg. on EV/1P

reserves (US$/BOE)

Figure 53: OGDC’s lowest implied oil price in Pak E&P space

provides a margin of safety (US$/BOE)

(80.0)

(70.0)

(60.0)

(50.0)

(40.0)

(30.0)

(20.0)

(10.0)

-

Jap

an

Pe

tr.

Inp

ex

PTT

Oil In

dia

CP

CC

CN

OO

C

PP

L

ON

GC

PO

L

Pe

tro

Ch

ina

OG

DC

CA

IR

PTTE

P

-

5.0

10.0

15.0

20.0

25.0

30.0

OG

DC

CN

OO

C

PP

L

PO

L

Jap

an

Pe

tr.

CA

IR

Oil In

dia

Pe

tro

Ch

ina

CP

CC

ON

GC

PTT

PTTE

P

Inp

ex

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

PP

L

ON

GC

Jap

an

Pe

tr.

PTTE

P

OG

DC

Inp

ex

PO

L

CA

IR

Oil In

dia

CN

OO

C

Pe

tro

Ch

ina

CP

CC

16.0 18.0

35.0

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

OGDC PPL POL

34

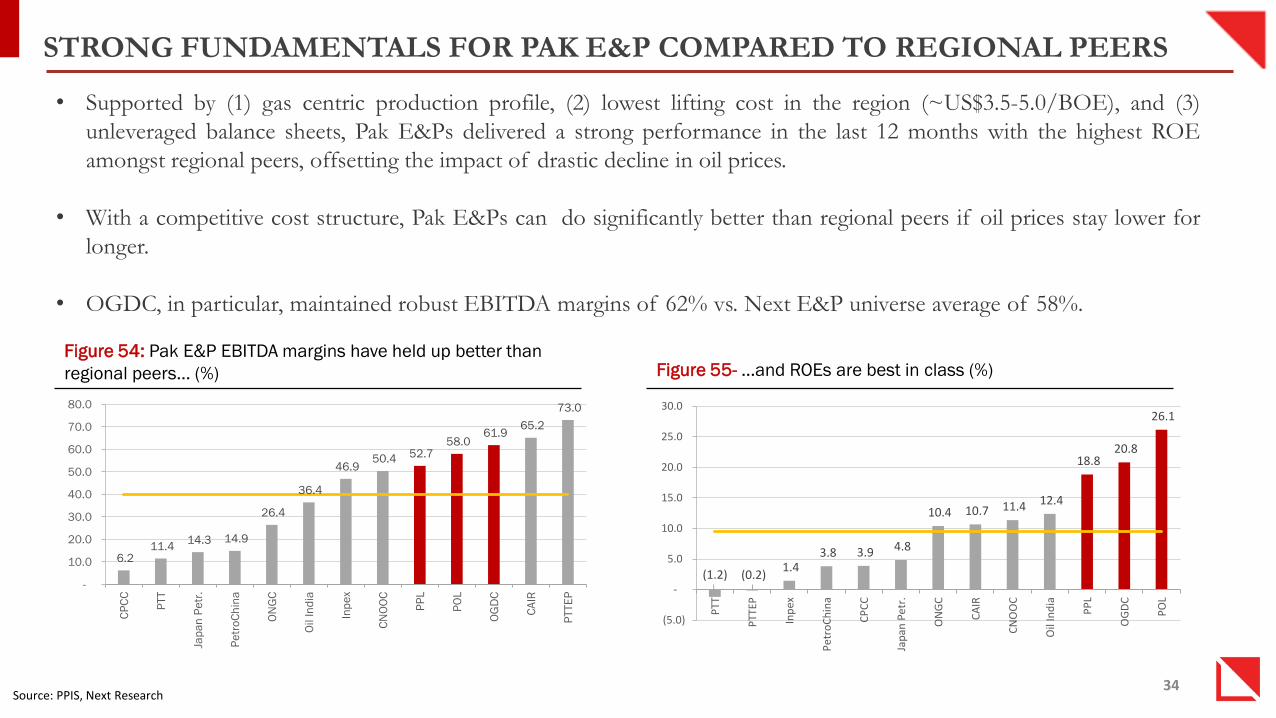

STRONG FUNDAMENTALS FOR PAK E&P COMPARED TO REGIONAL PEERS

Source: PPIS, Next Research

• Supported by (1) gas centric production profile, (2) lowest lifting cost in the region (~US$3.5-5.0/BOE), and (3)

unleveraged balance sheets, Pak E&Ps delivered a strong performance in the last 12 months with the highest ROE

amongst regional peers, offsetting the impact of drastic decline in oil prices.

• With a competitive cost structure, Pak E&Ps can do significantly better than regional peers if oil prices stay lower for

longer.

• OGDC, in particular, maintained robust EBITDA margins of 62% vs. Next E&P universe average of 58%.

(1.2) (0.2)1.4

3.8 3.9 4.8

10.4 10.7 11.4 12.4

18.8 20.8

26.1

(5.0)

-

5.0

10.0

15.0

20.0

25.0

30.0

PTT

PTT

EP

Inp

ex

Pet

roC

hin

a

CP

CC

Jap

an P

etr

.

ON

GC

CA

IR

CN

OO

C

Oil

Ind

ia

PP

L

OG

DC

PO

L

Figure 54: Pak E&P EBITDA margins have held up better than

regional peers… (%) Figure 55- …and ROEs are best in class (%)

6.2 11.4

14.3 14.9

26.4

36.4

46.9 50.4 52.7

58.0 61.9

65.2

73.0

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

CP

CC

PTT

Jap

an

Pe

tr.

Pe

tro

Ch

ina

ON

GC

Oil In

dia

Inp

ex

CN

OO

C

PP

L

PO

L

OG

DC

CA

IR

PTTE

P

35

CEMENTS – A CASE OF TWO VALUATIONS

Source: Bloomberg, Next Research

86

130 138 142 147

187

215

-

50

100

150

200

250

China Pakistan Malaysia Indonesia India Thailand Phillipines

0x

5x

10x

15x

20x

25x

30x

Pakistan China Thailand Phillipines Indonesia Malaysia India

2016E P/E 5 year avg. P/E

Figure 56- Pakistan appears cheap on forward P/E basis… Figure 57- …but similar to regional peers on EV/ton basis (US$)

• Pakistan is the cheapest amongst our peer group on PER basis. However, on an EV/ton basis, which is a more relevant

metric for cross regional comparison, Pakistan is largely similar to the peer group average, suggesting limited room for

rerating.

• Our top pick in the sector is Cherat Cement, which is best suited to capture volume growth and market share as its

capacity is expected to more than double by Dec-16. .

• Lucky Cement also remains an attractive proposition due to superior capital allocation relative to peers & potential

inclusion in MSCI Pak. Given the preference of foreign investors for Lucky Cement, an upgrade to MSCI EM would be

a significant boast for LUCK’s stock price.

36

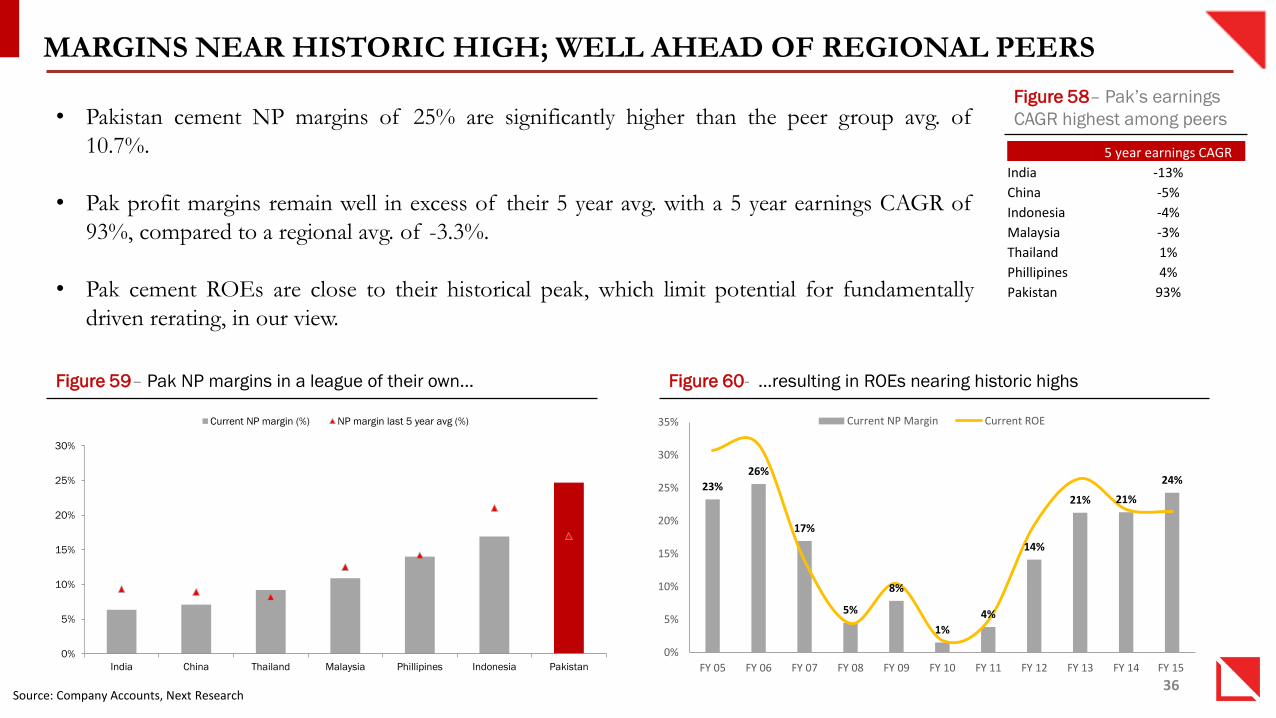

MARGINS NEAR HISTORIC HIGH; WELL AHEAD OF REGIONAL PEERS

• Pakistan cement NP margins of 25% are significantly higher than the peer group avg. of

10.7%.

• Pak profit margins remain well in excess of their 5 year avg. with a 5 year earnings CAGR of

93%, compared to a regional avg. of -3.3%.

• Pak cement ROEs are close to their historical peak, which limit potential for fundamentally

driven rerating, in our view.

Source: Company Accounts, Next Research

Figure 59– Pak NP margins in a league of their own… Figure 60- …resulting in ROEs nearing historic highs

Figure 58– Pak’s earnings

CAGR highest among peers

5 year earnings CAGR

India -13%

China -5%

Indonesia -4%

Malaysia -3%

Thailand 1%

Phillipines 4%

Pakistan 93%

0%

5%

10%

15%

20%

25%

30%

India China Thailand Malaysia Phillipines Indonesia Pakistan

Current NP margin (%) NP margin last 5 year avg (%)

23%

26%

17%

5%

8%

1%

4%

14%

21% 21%

24%

0%

5%

10%

15%

20%

25%

30%

35%

FY 05 FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13 FY 14 FY 15

Current NP Margin Current ROE

37

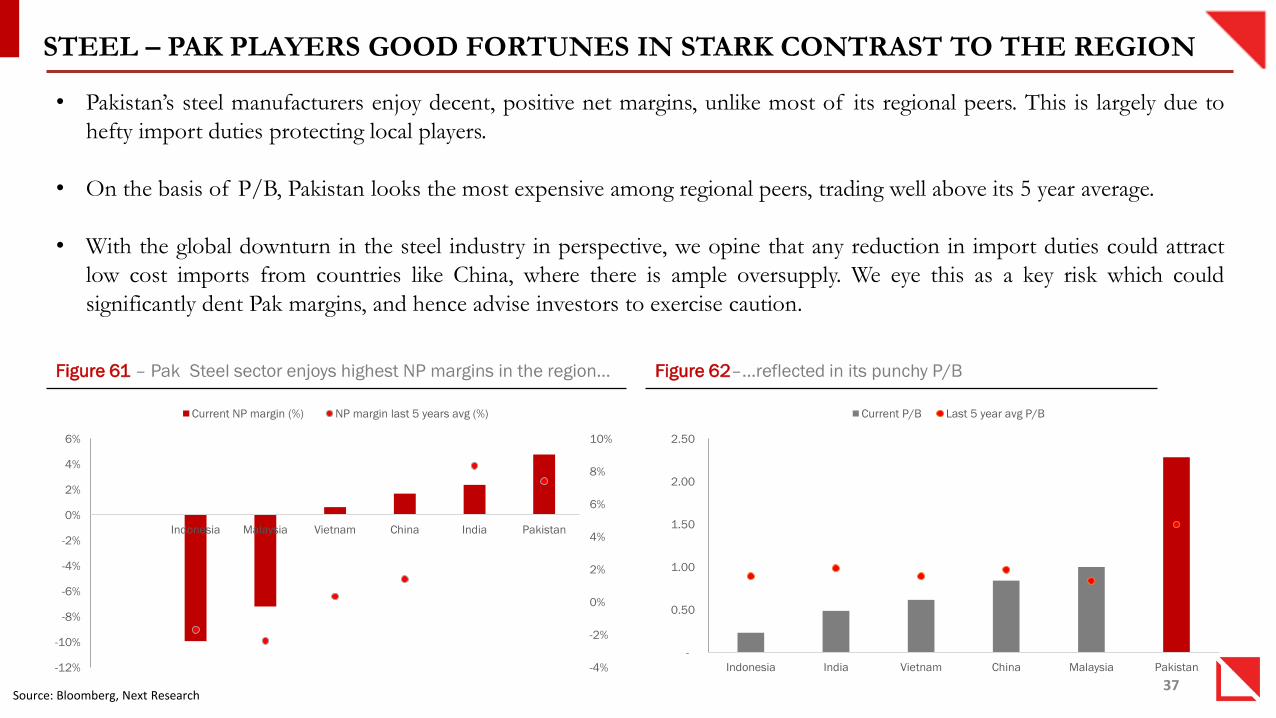

STEEL – PAK PLAYERS GOOD FORTUNES IN STARK CONTRAST TO THE REGION

Source: Bloomberg, Next Research

Figure 62–…reflected in its punchy P/B

• Pakistan’s steel manufacturers enjoy decent, positive net margins, unlike most of its regional peers. This is largely due to

hefty import duties protecting local players.

• On the basis of P/B, Pakistan looks the most expensive among regional peers, trading well above its 5 year average.

• With the global downturn in the steel industry in perspective, we opine that any reduction in import duties could attract

low cost imports from countries like China, where there is ample oversupply. We eye this as a key risk which could

significantly dent Pak margins, and hence advise investors to exercise caution.

-

0.50

1.00

1.50

2.00

2.50

Indonesia India Vietnam China Malaysia Pakistan

Current P/B Last 5 year avg P/B

-4%

-2%

0%

2%

4%

6%

8%

10%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Indonesia Malaysia Vietnam China India Pakistan

Current NP margin (%) NP margin last 5 years avg (%)

Figure 61 – Pak Steel sector enjoys highest NP margins in the region…

38

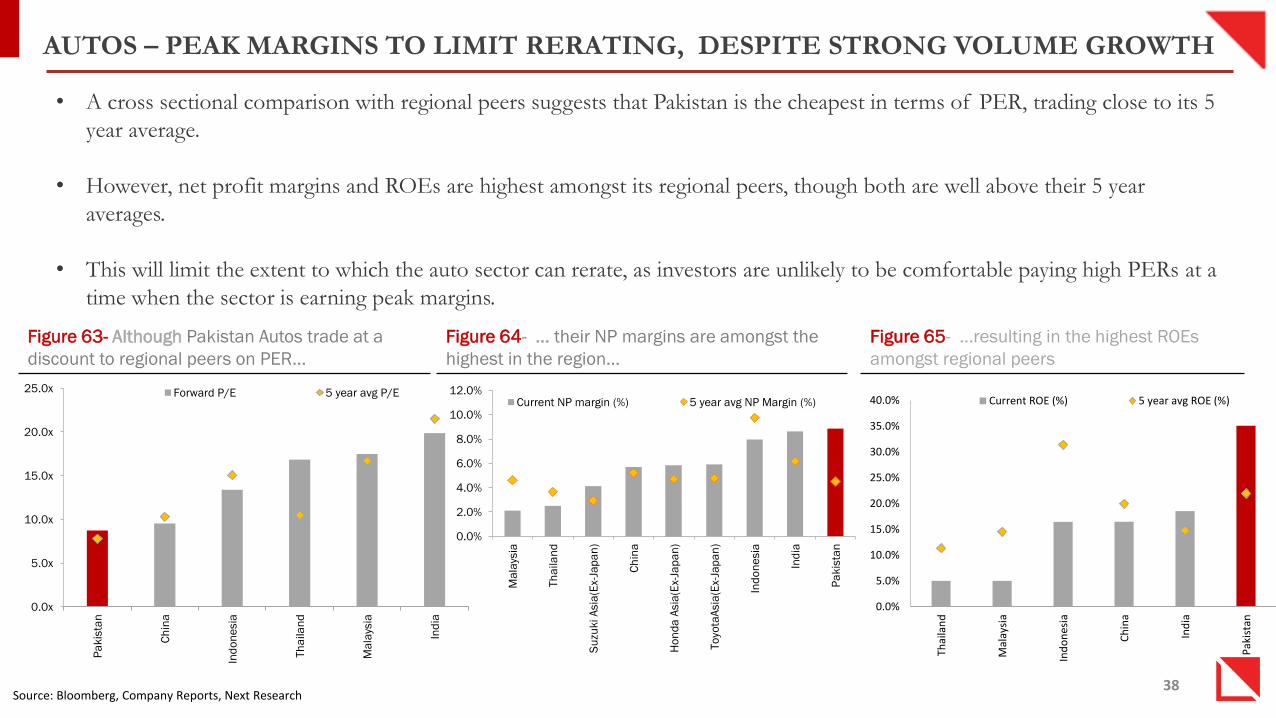

AUTOS – PEAK MARGINS TO LIMIT RERATING, DESPITE STRONG VOLUME GROWTH

Source: Bloomberg, Company Reports, Next Research

0.0x

5.0x

10.0x

15.0x

20.0x

25.0x

Pa

kis

tan

Ch

ina

Ind

on

esia

Th

aila

nd

Ma

lays

ia

Ind

ia

Forward P/E 5 year avg P/E

Figure 63- Although Pakistan Autos trade at a

discount to regional peers on PER…

• A cross sectional comparison with regional peers suggests that Pakistan is the cheapest in terms of PER, trading close to its 5

year average.

• However, net profit margins and ROEs are highest amongst its regional peers, though both are well above their 5 year

averages.

• This will limit the extent to which the auto sector can rerate, as investors are unlikely to be comfortable paying high PERs at a

time when the sector is earning peak margins.

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Ma

lays

ia

Th

aila

nd

Su

zuki A

sia

(Ex-

Jap

an

)

Ch

ina

Ho

nd

a A

sia

(Ex-

Jap

an

)

To

yota

Asia

(Ex-

Jap

an

)

Ind

on

esia

Ind

ia

Pa

kis

tan

Current NP margin (%) 5 year avg NP Margin (%)

Figure 64- … their NP margins are amongst the

highest in the region…

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Thai

lan

d

Mal

aysi

a

Ind

on

esia

Ch

ina

Ind

ia

Pak

ista

n

Current ROE (%) 5 year avg ROE (%)

Figure 65- …resulting in the highest ROEs

amongst regional peers

39

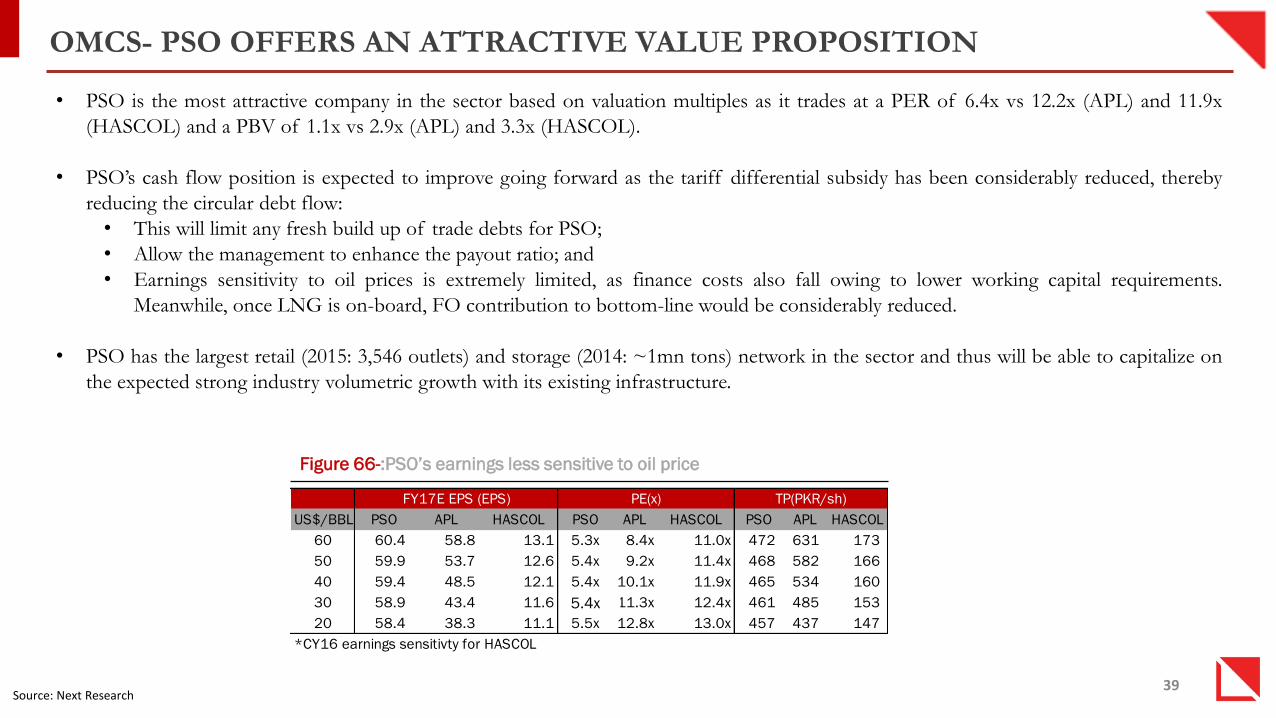

• PSO is the most attractive company in the sector based on valuation multiples as it trades at a PER of 6.4x vs 12.2x (APL) and 11.9x

(HASCOL) and a PBV of 1.1x vs 2.9x (APL) and 3.3x (HASCOL).

• PSO’s cash flow position is expected to improve going forward as the tariff differential subsidy has been considerably reduced, thereby

reducing the circular debt flow:

• This will limit any fresh build up of trade debts for PSO;

• Allow the management to enhance the payout ratio; and

• Earnings sensitivity to oil prices is extremely limited, as finance costs also fall owing to lower working capital requirements.

Meanwhile, once LNG is on-board, FO contribution to bottom-line would be considerably reduced.

• PSO has the largest retail (2015: 3,546 outlets) and storage (2014: ~1mn tons) network in the sector and thus will be able to capitalize on

the expected strong industry volumetric growth with its existing infrastructure.

OMCS- PSO OFFERS AN ATTRACTIVE VALUE PROPOSITION

US$/BBL PSO APL HASCOL PSO APL HASCOL PSO APL HASCOL

60 60.4 58.8 13.1 5.3x 8.4x 11.0x 472 631 173

50 59.9 53.7 12.6 5.4x 9.2x 11.4x 468 582 166

40 59.4 48.5 12.1 5.4x 10.1x 11.9x 465 534 160

30 58.9 43.4 11.6 5.6x 11.3x 12.4x 461 485 153

20 58.4 38.3 11.1 5.5x 12.8x 13.0x 457 437 147

*CY16 earnings sensitivty for HASCOL

FY17E EPS (EPS) PE(x) TP(PKR/sh)

Figure 66-:PSO’s earnings less sensitive to oil price

Source: Next Research

5.4x

40

CIRCULAR DEBT TO ABATE; PSO’S LIQUIDITY TO IMPROVE

Source: IMF, Next Research

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2012 2013 2014 2015 2016E 2017E

Actual Cost of Generation Determined tariff- NEPRA Notified tariff- GoP

Circular debt

TDS

PKR/kwh 2012 2013 2014 2015 2016E 2017E

Actual Cost 14.0 17.2 16.7 16.2 13.6 13.5

Determined tariff- NEPRA 11.9 14.3 14.3 13.9 12.0 13.0

Notified tariff- GoP 8.7 8.7 11.5 12.4 12.0 13.0

Circular Debt 2.1 2.9 2.4 2.3 1.6 0.5

TDS 3.2 5.6 2.8 1.5 - -

Total (per KwH) 5.3 8.5 5.2 3.8 1.6 0.5

Total (PKR mn) 530 850 520 380 160 50

• The difference between actual cost and the tariff determined by NEPRA adds up to the circular debt as shown in Figure below,

whereas tariff differential subsidy (TDS) is the difference between determined tariff by NEPRA and notified tariff by GoP, the

amount of TDS is paid by government to DISCOs.

• TDS in 2012 was PKR3.2/kWh which decreased to PKR1.5/kWh in 2015.

• As per IMF estimates and one of the conditions of Extended Fund Facility, GoP will have to withdraw TDS and keep the

notified tariff in line with determined tariff by NEPRA.

•

• We believe that once TDS amount is reduced in FY16, the government can also bring down the circular debt stock.

Figure 67 :-Circular debt concerns to reduce as TDS falls

41

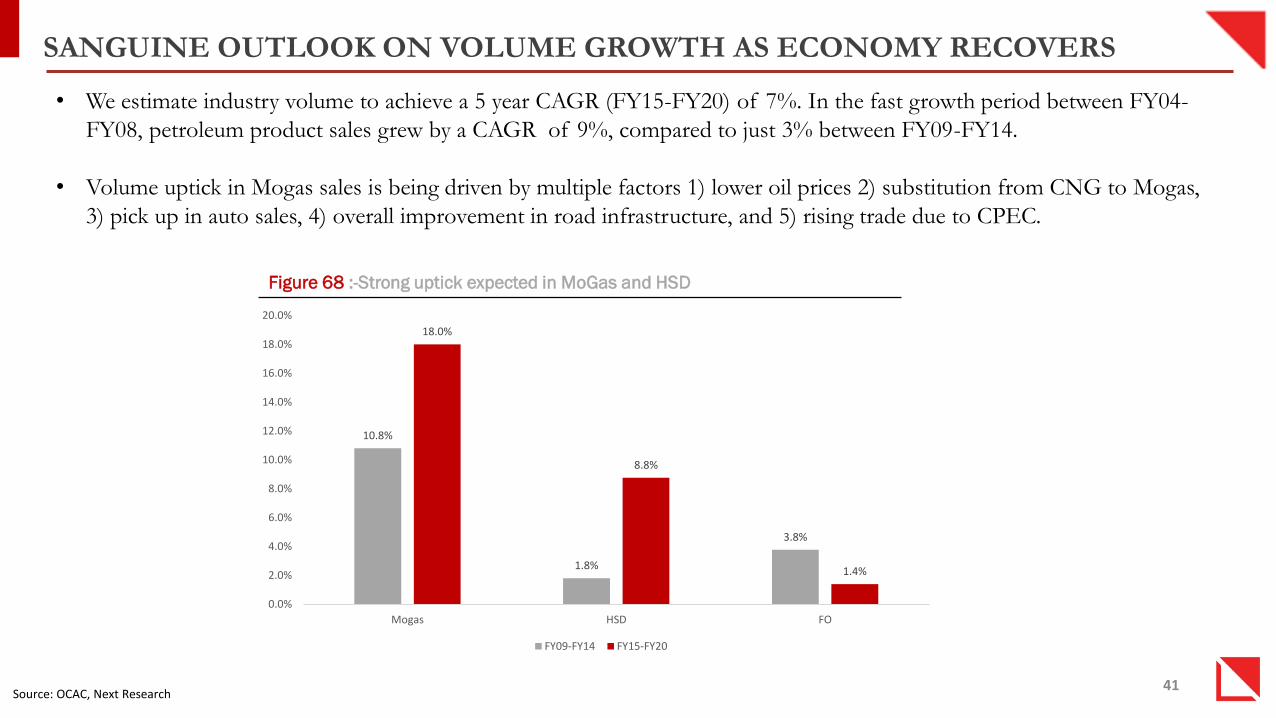

SANGUINE OUTLOOK ON VOLUME GROWTH AS ECONOMY RECOVERS

• We estimate industry volume to achieve a 5 year CAGR (FY15-FY20) of 7%. In the fast growth period between FY04-

FY08, petroleum product sales grew by a CAGR of 9%, compared to just 3% between FY09-FY14.

• Volume uptick in Mogas sales is being driven by multiple factors 1) lower oil prices 2) substitution from CNG to Mogas,

3) pick up in auto sales, 4) overall improvement in road infrastructure, and 5) rising trade due to CPEC.

Source: OCAC, Next Research

10.8%

1.8%

3.8%

18.0%

8.8%

1.4%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

Mogas HSD FO

FY09-FY14 FY15-FY20

Figure 68 :-Strong uptick expected in MoGas and HSD

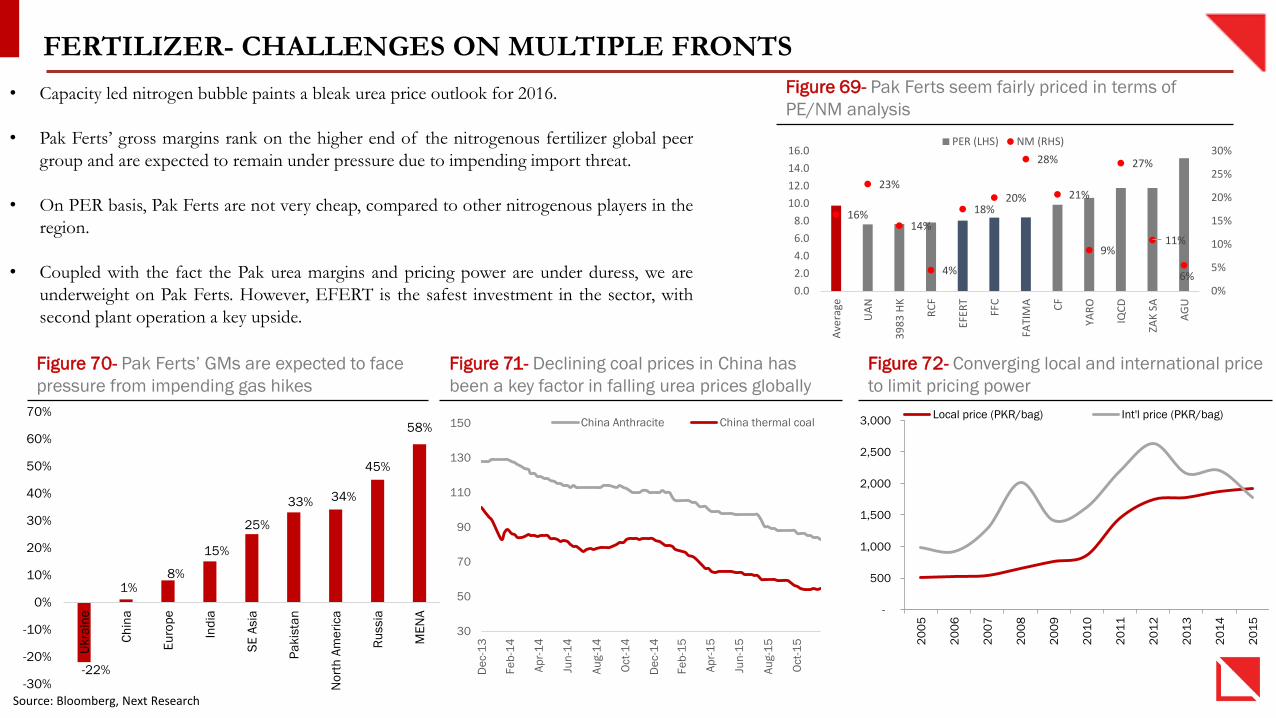

FERTILIZER- CHALLENGES ON MULTIPLE FRONTS

-22%

1%8%

15%

25%

33% 34%

45%

58%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

Ukra

ine

Ch

ina

Eu

rop

e

Ind

ia

SE

Asia

Pa

kis

tan

No

rth

Am

eri

ca

Ru

ssia

ME

NA

• Capacity led nitrogen bubble paints a bleak urea price outlook for 2016.

• Pak Ferts’ gross margins rank on the higher end of the nitrogenous fertilizer global peer

group and are expected to remain under pressure due to impending import threat.

• On PER basis, Pak Ferts are not very cheap, compared to other nitrogenous players in the

region.

• Coupled with the fact the Pak urea margins and pricing power are under duress, we are

underweight on Pak Ferts. However, EFERT is the safest investment in the sector, with

second plant operation a key upside.

Figure 70- Pak Ferts’ GMs are expected to face

pressure from impending gas hikes

Figure 71- Declining coal prices in China has

been a key factor in falling urea prices globally

Figure 72- Converging local and international price

to limit pricing power

-

500

1,000

1,500

2,000

2,500

3,000

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Local price (PKR/bag) Int'l price (PKR/bag)

30

50

70

90

110

130

150

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Jun

-14

Au

g-1

4

Oct-

14

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Jun

-15

Au

g-1

5

Oct-

15

China Anthracite China thermal coal

16%

23%

14%

4%

18%20%

28%

21%

9%

27%

11%

6%0%

5%

10%

15%

20%

25%

30%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Ave

rage

UA

N

39

83

HK

RC

F

EFER

T

FFC

FATI

MA CF

YAR

O

IQC

D

ZAK

SA

AG

U

PER (LHS) NM (RHS)

Figure 69- Pak Ferts seem fairly priced in terms of

PE/NM analysis

Source: Bloomberg, Next Research

43

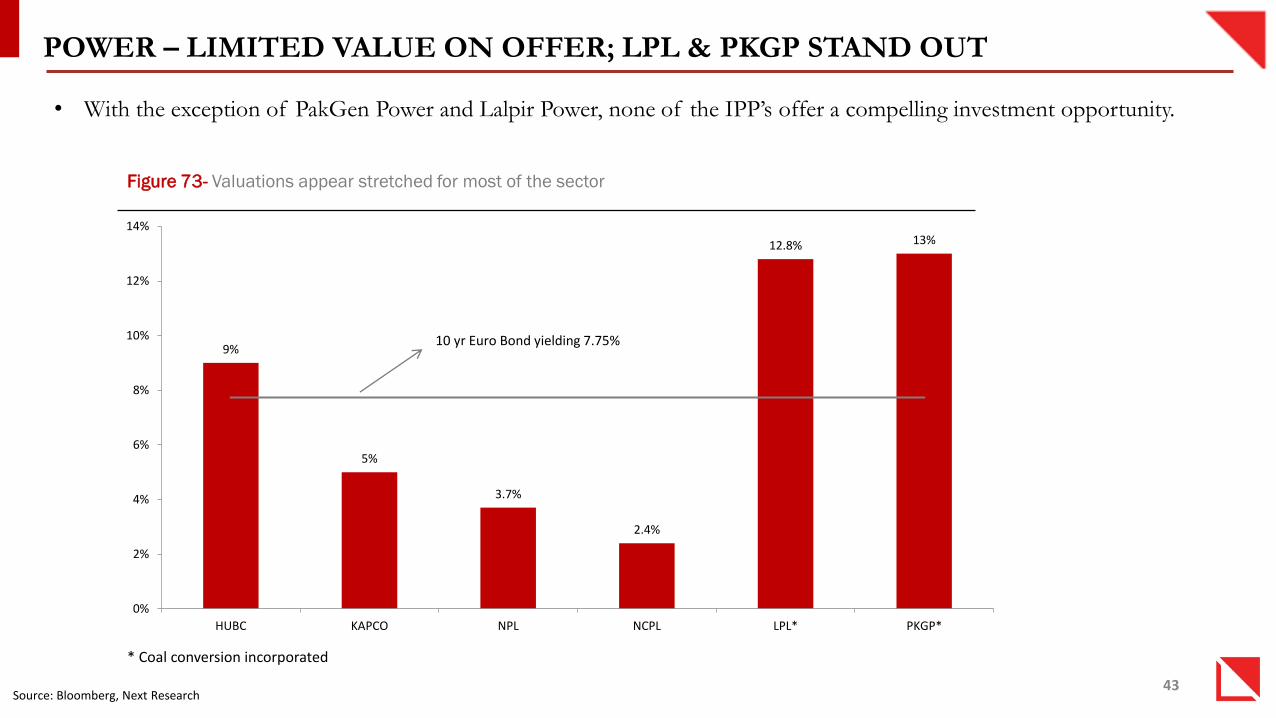

POWER – LIMITED VALUE ON OFFER; LPL & PKGP STAND OUT

Source: Bloomberg, Next Research

* Coal conversion incorporated

• With the exception of PakGen Power and Lalpir Power, none of the IPP’s offer a compelling investment opportunity.

9%

5%

3.7%

2.4%

12.8% 13%

0%

2%

4%

6%

8%

10%

12%

14%

HUBC KAPCO NPL NCPL LPL* PKGP*

10 yr Euro Bond yielding 7.75%

Figure 73- Valuations appear stretched for most of the sector

NEXT CAPITAL RESEARCH AND SALES TEAM

44

Research Team Sectors Contact Email

Farrukh Karim Khan, CFA Strategy +92-21-35295650 [email protected]

Ameet Doulat Fertilizer & Banks +92-21-35169519 [email protected]

Muhammad Ali Cement & Power +92-21-35169515 [email protected]

Sonia Agarwal E&Ps +92-111-639-825 Ext 109 [email protected]

Naseer uddin Khalid Fertilizer, Power & Steel +92-111-639-825 Ext 109 [email protected]

Nayhan Mohajir Automobile & OMC +92-21-35169518 [email protected]

Sohaib Subzwari Consumer & Textile +92-111-639-825 Ext 109 [email protected]

Owais Shahid Manager Database +92-21-35169516 [email protected]

Sales Team Contact Email

Karachi

Shoib Memon +92-21-35292640-41 [email protected]

Saad Iqbal +92-21-35292642 [email protected]

Syed Faheem Raza +92-21-35292644 [email protected]

Muhammad Shakeel +92-21-35293637 [email protected]

Saad Rafi +92-21-35169512 [email protected]

Abdul Basit +92-21-35169517 [email protected]

KSE Office

Muhammad Zubair Ellahi +92-21-32468865-66 [email protected]

Lahore

Zulqarnain Khan +92-321-4252200 [email protected]

Muhammad Yaqoob +92-301-4604045 [email protected]

Asim Aslam +92-322-4306868 [email protected]

Email: [email protected]

DISCLAIMER (1/2)

45

Analyst Certification: All of the views expressed in this report accurately reflect the personal views of the responsible analyst(s) about any and all of the subject securities or

issuers. No part of the compensation of the responsible analyst(s) named herein is, or will be, directly or indirectly, related to the specific recommendations or views expressed

by the responsible analyst(s) in this report.

Disclaimer

This information and opinion contained in this report have been complied by our research department from sources believed by it to be reliable and in good faith, but no

representation or warranty, express or implied, is made as to their accuracy, completeness or correctness. All opinions and estimates contained in the document constitute the

department’s judgment as of the date of this document and are subject to change without notice and are provided in good faith but without legal responsibility.

This report is not, and should not be construed as, an offer to sell or a solicitation of an offer to buy any securities. Next Capital Limited (the company) or persons connected

with it may from time to time have an investment banking or other relationship, including but not limited to, the participation or investment in commercial banking

transactions (including loans) with some or all of the issuers mentioned therein, either for their own account or the ac- count of their customers. Persons connected with the

company may provide or have provided corporate finance and other services to the issuer of the securities mentioned herein, including the issuance of options on securities

mentioned herein or any related investment and may make a purchase and/or sale, or offer to make a purchase and/or sale of the securities or any related investment from

time to time in the open market or otherwise, in each case either as principal or agent.

This report may contain forward looking statements which are often but not always identified by the use of words such as “anticipate”, “believe”, “estimate”, “intend”, “plan”,

“expect”, “forecast”, “predict” and “project” and statements that an event or result “may”, “will”, “can”, “should”, “could” or “might” occur or be achieved and other

similar expressions. Such forward looking statements are based on assumptions made and information currently available to us and are subject to certain risks and uncertainties

that could cause the actual results to differ materially from those expressed in any forward looking statements. Readers are cautioned not to place undue relevance on these

forward looking statements. NCEL expressly disclaims any obligation to update or revise any such forward looking statements to reflect new information, events or

circumstances after the date of this publication or to reflect the occurrence of unanticipated events.

Exchange rate fluctuations may affect the return to investors. Neither the company or any of its affiliates, nor any other person, accepts any liability whatsoever for any direct

or consequential loss arising from any use of this report or the information contained therein.

Next Capital Limited, its respective affiliate companies, associates, directors and/or employees may have investments in securities or derivatives of securities of companies

mentioned in this report, and may make investment decisions that are inconsistent with the views expressed in this report.

DISCLAIMER (2/2)

46

Rating System

Next Capital Limited employs a three tier rating system depending upon sector’s proposed weight in the portfolio as compared to sectors weight in KSE-100 index, as follows:

Ratings are updated regularly based on the latest developments in the economy/sector/company, changes in stock prices, and changes in analyst’s assumptions.

Next Capital Limited employs a three tier rating system, depending upon expected total return (R) of the stock, as follows:

Where;

•R = Expected Dividend Yield + Expected Capital Gain

•‘R’ is before tax

•Investment horizon is between six months to twelve months

Ratings are updated regularly based on the latest developments in the economy/sector/company, changes in stock prices, and changes in analyst’s assumptions.

Valuation Methodology

The Research Analyst(s) has used DDM methodology to arrive at Target Price for Power Companies, Justified P/B methodology to arrive at Target Price for Banks and DCF

methodology to arrive at Target Price for all other sectors.

Key Risks

Currency devaluation. Commodity price fluctuation. Interest rate fluctuations. Increase in gas prices. Delay in projects (new/expansions/efficiency)

Unfavorable outcome on GIDC imposition on fertilizer plants having fixed price contracts

Slower than expected private sector credit growth.

Deteriorating receivable position (Circular debt). Unfavorable law & order situation. Heavy dependence on few fields.

Decline in cement prices, greater than expected increase in coal prices, delay in expected projects (expansion, efficiency projects)

Increase in scrap prices, increase in oil prices, reduction in import duty leading to cheaper imports, greater than expected increase in electricity tariff.

WAPDA’s inability to pay dues, oil price reversal to take away efficiency gains for inefficient IPP’s (LPL and PKGP).

GoP’s inability to implement IMF polices of arrears reduction plan in the power sector. Decline in auto sales

New auto policy. Increase in imported cars

Rating Sector’s proposed weight in the portfolio

Over Weight > Weight in KSE 100 index

Market Weight = Weight in KSE 100 Index

Under Weight < Weight in KSE 100 Index

Rating Expected Total Return

Buy R ≥ 15%

Neutral 0% ≥ R < 15%

Sell R < 0%