Embed Size (px)

DESCRIPTION

The March issue of Debtfree DIGI Magazine. SA's free debt counselling and debt review industry magazine. We look at all the recent workshops and conferences, discuss new court cases and cover not only the latest news but talk about PDA fees.

Citation preview

South Africa’s debt counselling magazine

March 2016www.debtfreedigi.co.za

What you can expect from Hyphen PDA:

• IncreasedDebtCounsellorProfitability

• Flawless Systems

•MeaningfulReporting

•Contented Consumers!

Malcom Povey, Head: Operations PDA082 445 5604

ChrisvanderStraaten,Head: PDA082 557 0437

www.hyphenpda.co.za

www.hyphenpda.co.za

Don’t expect to hear an endless amount of“spin”aroundwhythingsfailed!.

Specialist Attorneys dealing with Debt Review matters

Magistrates Court and High Court Matters

TEL 021 913 2514 FAX 0866070940 EMAIL [email protected] ADDRESS 7 Chenin Blanc Street, Oude Westhof POSTAL ADDRESS PO Box 3407, tygervalley, 7536

It always seems impossible until it is done” - Nelson Mandela

“

C O N T E N T S

NEWS

NEDBANK V NORRIS NCR WORKSHOP

SERVICE DIRECTORY

HAVE YOUR PDA FEES CHANGED?

FNB WORKSHOP

March sees a spate of public holidays and long weekends. A brief respite from the pressures that weigh down both those religious and secular. Of course, all the public holidays are either a boon or curse depending on whether you earn on those days or not. For those who have to pay staff regardless, it is hardly a boon but rather a burden. For those who do not earn on days they do not work, it is a frustrating time of year which sees bank balances further decimated. For the rest, it gives a moment of quiet in the storm to collect ones thoughts and plan ahead.

As the last days of summer slip between our fingers, it seems that clever consumers are clambering for debt help through debt review. The chickens (of Dec and Jan spending) are home to roost and for many February was a harsh month calling for action which was finally taken in March. Application numbers are high. The interest rate hikes and food price increases at the shops are hitting all of us hard. Predictions are that further rate hikes and more pressure on the Rand lies ahead so, brace yourself.

March has been the month of industry workshops by both the Regulator and credit providers. This issue we look into the recent series of NCR workshops rolling out across the country for Debt Counsellors and Credit Providers and see how the very well supported

meeting held in Cape Town suddenly turned sour.

We look into all the local news about the industry and consider how this will impact on consumers and debt counselling firms. New court cases have also captured the attention of the industry recently. These matters may shape the way ahead or may simply be another matter referenced in upcoming appeals cases. Either way we have a look at what has been coming out of the courts in this issue.

Debt Review can also be a real respite from debt pressures that are weighing in on you. If you are feeling crushed and unsure about how to deal with debt then head down to your local Debt Counsellor. Get a fresh perspective, professional advice on your situation and take the first steps towards being debt free.

EDITOR’S NOTE

Switch to easy

Agent: Petro de Beere-maill: [email protected]: 083 6139 826

www.dcpartner.co.za

• Individual, dedicated business bank account per Debt Counsellor

• National Representation - regular office visits by skilled, trained agents

• 24 hour access to system, including distributions data - from any PC, cell phone or tablet with internet access

• Dedicated account managers for EACH Debt Counsellor

TEL: 021 872 1968 11 MARKET STREET, PAARL

www.steyncoetzee.co.za

PROFESSIONAL DEBT COUNSELLING ATTORNEYS

INDUSTRY CONSUMER

NEWS FLASHREPO RATE CLIMBSIn March, Reserve Bank Governor Lesetja Kganyago announced that due to pressures on the economy (including a higher than hoped for inflation rate) and weakening national currency the Reserve Bank had decided to push up the rate to 7%. This follows on the heels of similar hikes over the last few months in reaction to the world and local economy and is not expected to be the last increase this year.

LEWIS GET GO AHEADLast year, Lewis Stores announced their intention to purchase Beares and Ellerines (for something of a bargain from their struggling parent company). It has taken until this month for all the red tape by the regulatory and competition authorities to give the green light for the transaction to go ahead. Though Lewis themselves have been going through tough times with share prices being low and pressure from new legislation and investigations by the NCR making life interesting, they are still looking ahead to diversify and expand into a higher income client bracket. 3/4 of the 57 new stores acquired carry the Beares brand (the rest are Ellerines stores). It is hoped that with the acquisition of many Beares Stores , Lewis will be able to gain traction among higher income earners, who will be able to comply with more ease with recent changes to affordability assessments as per new legislation. Consumers

applying for credit are now required to provide not only bank slips but also proof of recent income (eg. 3 months pay slips). Lewis recently reported little growth (1.1%) over the end of 2015 and this was attributed, in part, to challenges facing the lower to middle income earners who comprise most of their current clientele.

LEAVING DEBT REVIEW NCR GUIDELINEWhen a person approaches a Debt Counsellor they begin a statutory process governed by the National Credit Act (NCA). When a person asks a Debt Counsellor to look over their situation this needs to be indicated on the National Credit Regulator’s (NCR) data base. They, in turn notify the credit bureaus. Then the Debt Counsellor asks the consumer and all their credit providers for more information (the Debt Counsellor sends out a form called a Form 17.1). Once they have looked over that info they know if the person needs to simply adjust their monthly spending habits or whether they need legal protection though the NCA and debt review. At this point the Debt Counsellor will send out a form called a Form 17.2 which says either the consumer needs help or not. If the consumer needs help the Debt Counsellor will make a few proposals to the credit providers and gather their responses for inclusion in a court document. The matter

For daily debt counselling news in 3 minutes or less visit www.debtfreedigi.co.za

then goes to court for a debt restructuring court order. This stays in force for as long as the consumer pays according to the arrangement. Later the Consumer’s situation may change drastically and they may be able to leave debt review sooner than planned or they may pay according to the plan and come to the end of the arrangement with all their debt settled. The NCR issued a guideline on how to treat the process when someone wants to leave debt review. Not too long ago the National Credit Act was amended to allow for consumers who had paid up all their smaller debt to leave the process sooner. Thus the process changed somewhat and the NCR issued a new guideline or non binding opinion. The guideline highlights that the process is a serious one and should not be undertaken lightly and without commitment to the process. The NCR wish to help create uniformity across the industry with how the withdrawal process should be conducted. DOWNLOAD THE GUIDELINEhttp://debtfreedigi .co.za/wp-content/uploads/2016/03/Withdrawal-from-debt-review-NCR-guidelines-Feb-2015.pdf

NCR ISSUE MASSIVE R1 MILLION FINEAccording to the National Credit Act if a person or company want to issue credit to consumers they have to register with the National Credit Regulator. The idea behind the legislation is to stop the prevalence of loan sharks in communities across South Africa. These loan sharks have a terrible reputation for taking advantage of those they loan funds to. The NCA also requires that after registration the credit provider pay an annual fee so that the

NCR can keep an eye on who is currently in business. The NCR have reminded registrants that they do not have to remind them of the annual renewal of their registration fee (though they do via email normally). If the annual renewal fee is not paid then the registrant is technically not allowed to trade. Recently the National Credit Regulator took action against an unregistered (un-renewed) credit provider Akudle Kutshiyele who operate in Nelspruit in Mpumalanga. The firm had let their registration lapse without renewing but had continued to offer new credit to consumers. The matter was referred to the National Consumer Tribunal who handed down a R1 million fine. The fine covered not only offering new credit while not renewed but also granting credit to consumers without checking if they could afford it. They also on many occasions did not inform consumers in advance in a quotation or “pre agreement” document of what the total cost of the credit will be. This means that they were offering “reckless credit”. Akudle also took consumers bank cards and ID books from consumers borrowing funds in an effort to enforce payment of their loans. This is illegal and if a credit provider (big or small) ever ask you for them you should report the matter to the NCR as soon as possible or simply refuse.

‘GARNISHEE’ CASE GOES TO CONSTITUTIONAL COURTThe all important Constitutional Court case regarding Emoluments Attachment Orders – EAOs (often called Garnishee Orders) was heard on the 3rd of March 2016. The case began a long while back in Stellenbosch in Cape Town and has to do with a specific number of EAOs against several farm workers

NEWS CONTINUED

Credit ProteCtion – debt review

ONE Insurance Underwriting Managers (PTY) LTD Reg No. 1996/008987/07 Authorised Financial Services Provider FSP8783 VAT No. 4370160501

A Member of A member of the Group

Underwritten by:

SuReApplied to go under debt review? Restructuring your monthly expenses?why not insure all your accounts on the one Credit Protection?

we will contribute towards your accounts in the event of the following:

• death – we settle the account• temporary disability – we pay the Debt Review payment for 6 months• Permanent disability – we settle the account• Critical illness – we settle the account• retrenchment – we pay the Debt Review payment for up to 9 months

At a rate of R 2.95 per R1000, our rates are among the best and our benefit structure is the best in the market.

ContACt one oR youR debt Counsellor! 0861 266 562 www.one.za.com

sam Haasbroek: 082 550 [email protected]

marijke wessels:082 729 [email protected]

terms & Conditions aPPly

Credit ProteCtion – debt review

ONE Insurance Underwriting Managers (PTY) LTD Reg No. 1996/008987/07 Authorised Financial Services Provider FSP8783 VAT No. 4370160501

A Member of A member of the Group

Underwritten by:

SuReApplied to go under debt review? Restructuring your monthly expenses?why not insure all your accounts on the one Credit Protection?

we will contribute towards your accounts in the event of the following:

• death – we settle the account• temporary disability – we pay the Debt Review payment for 6 months• Permanent disability – we settle the account• Critical illness – we settle the account• retrenchment – we pay the Debt Review payment for up to 9 months

At a rate of R 2.95 per R1000, our rates are among the best and our benefit structure is the best in the market.

ContACt one oR youR debt Counsellor! 0861 266 562 www.one.za.com

sam Haasbroek: 082 550 [email protected]

marijke wessels:082 729 [email protected]

terms & Conditions aPPly

Credit ProteCtion – debt review

ONE Insurance Underwriting Managers (PTY) LTD Reg No. 1996/008987/07 Authorised Financial Services Provider FSP8783 VAT No. 4370160501

A Member of A member of the Group

Underwritten by:

SuReApplied to go under debt review? Restructuring your monthly expenses?why not insure all your accounts on the one Credit Protection?

we will contribute towards your accounts in the event of the following:

• death – we settle the account• temporary disability – we pay the Debt Review payment for 6 months• Permanent disability – we settle the account• Critical illness – we settle the account• retrenchment – we pay the Debt Review payment for up to 9 months

At a rate of R 2.95 per R1000, our rates are among the best and our benefit structure is the best in the market.

ContACt one oR youR debt Counsellor! 0861 266 562 www.one.za.com

sam Haasbroek: 082 550 [email protected]

marijke wessels:082 729 [email protected]

terms & Conditions aPPly

which Cape Town’s courts felt were not valid for a variety of reasons. The court case raised big (constitutional) issues in regard to the use and abuse of the EAO system. The Con Court case touches on a number of important and far reaching common practices in regard to EAOs - most of which are very bad and unfair to consumers. Often times the way things have been done in the past prevented consumers from having their day in court to protect themselves from abuse. Some even claim that credit provider’s collection agents regularly engage in ‘forum shopping’ at far away courts in order to get their EAOs rubber stamped and prevent consumers from every changing these deductions. An EAO currently has to be changed at the court it was granted in. If that court is far from the consumer’s home town this makes it expensive and extremely difficult

to get the EAO changed or thrown out. At High Court things went the consumers way and as a result many EAOs in the Western Cape have not been enforced since that ruling. If things once again go the consumers way it would have a massive impact on how many legal collections firms and credit providers go about recovering funds from consumers across the entire country.

NEWS CONTINUED

MELIORLEAF WON’T LOAD YOUR PREMIUMS

OR REPUDIATE A LEGITIMATE CLAIM

Specialist insurance for people in debt review. Ask your debt counsellor.

CALL US NOW 0861 635 467www.meliorleaf.co.za

For daily debt counselling news in 3 minutes or less visit www.debtfreedigi.co.za

With changes to the National Credit Act made last year by the National Credit Amendment Act one aspect that was set to change was the fees charged by the Payment Distribution Agencies (PDAs).

HAVE YOUR PDA FEES CHANGED?

These are firms which distribute funds on behalf of consumers to their various credit providers in accordance with the payment plan set out by the Debt Counsellor. Consumers have the right to distribute their own funds but most would struggle to do so in the right amount, to the right account, at the right time, with the right reference each month as the plan shifts and changes. Use of a PDA reduces confusion and increases accuracy of payment amounts. It also allows for good record keeping should disputes arise.

When the changes were first announced the PDAs (who have previously operated under a service level agreement with the NCR and were not required to be ‘registered’) were concerned partially about the reduction of income as a result of the changes. Their main concern mainly focused on the timelines for payments which were published with the amendments as it leaves them exposed to returns and disputes and the loss of revenue as a result. In many cases they would have to pay funds over before they had even received them (cleared), never mind if the consumer later went and reversed them. In such a case they would have paid for the consumers debt out of their own pocket. Since they deal with hundreds of thousands of consumers the threat to their viability is clear. The various PDAs have been meeting repeatedly since last year with the NCR, DTI and Parliamentary committees in an effort to get the fee structure and timelines adjusted. In the meantime, the PDAs have indicated that once registered they will stick to the required fee amounts. All the previously NCR service level agreement recognised PDAs have submitted all needed documents and made the needed payments etc. They now await their certification and the outcome of their conversations with the various bodies.

NEW FEE STRUCTURE MARCH 2016Here is a look at the new fee structure for payments as set out with the amendments to the Act. If consumers check their statements from the PDAs they will soon see these new amounts (should they not change in the next week or two) shown.

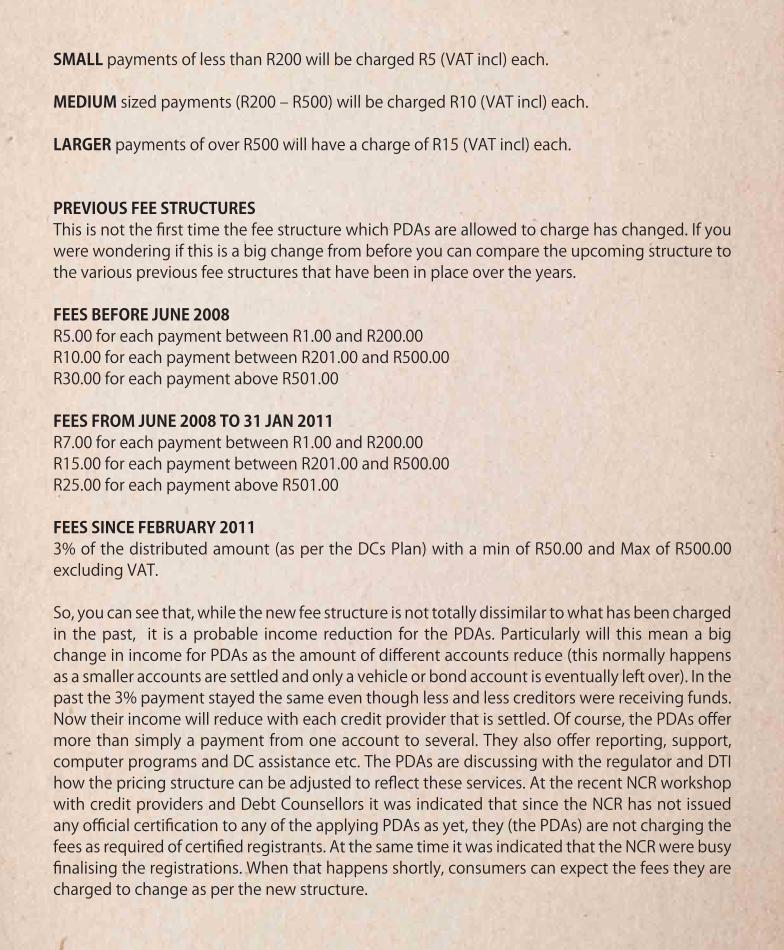

SMALL payments of less than R200 will be charged R5 (VAT incl) each.

MEDIUM sized payments (R200 – R500) will be charged R10 (VAT incl) each.

LARGER payments of over R500 will have a charge of R15 (VAT incl) each.

PREVIOUS FEE STRUCTURESThis is not the first time the fee structure which PDAs are allowed to charge has changed. If you were wondering if this is a big change from before you can compare the upcoming structure to the various previous fee structures that have been in place over the years.

FEES BEFORE JUNE 2008R5.00 for each payment between R1.00 and R200.00R10.00 for each payment between R201.00 and R500.00R30.00 for each payment above R501.00

FEES FROM JUNE 2008 TO 31 JAN 2011R7.00 for each payment between R1.00 and R200.00R15.00 for each payment between R201.00 and R500.00R25.00 for each payment above R501.00

FEES SINCE FEBRUARY 20113% of the distributed amount (as per the DCs Plan) with a min of R50.00 and Max of R500.00 excluding VAT.

So, you can see that, while the new fee structure is not totally dissimilar to what has been charged in the past, it is a probable income reduction for the PDAs. Particularly will this mean a big change in income for PDAs as the amount of different accounts reduce (this normally happens as a smaller accounts are settled and only a vehicle or bond account is eventually left over). In the past the 3% payment stayed the same even though less and less creditors were receiving funds. Now their income will reduce with each credit provider that is settled. Of course, the PDAs offer more than simply a payment from one account to several. They also offer reporting, support, computer programs and DC assistance etc. The PDAs are discussing with the regulator and DTI how the pricing structure can be adjusted to reflect these services. At the recent NCR workshop with credit providers and Debt Counsellors it was indicated that since the NCR has not issued any official certification to any of the applying PDAs as yet, they (the PDAs) are not charging the fees as required of certified registrants. At the same time it was indicated that the NCR were busy finalising the registrations. When that happens shortly, consumers can expect the fees they are charged to change as per the new structure.

All professionals have professional indemnity if the unforeseen happens. Do you as a professional Debt Counselor have

professional indemnity as stipulated by the ethical code?

contact us today for more information 086 111 2882

TELEPHONE 0861 112 882 FACSIMILE 086 605 9751 MOBILE 082 449 6856 EMAIL [email protected]

www.in2insurance.co.za

(AND MAGISTRATE DUMANI N.O.)

NEDBANK V

NORRIS

A recent court case out of the Eastern Cape has caught the attention of the Debt Counselling Community. In the case Nedbank asked the court to review a debt restructuring order which had happened without them attending and where the interest rate was changed without their consent. The PE High Court overturned the debt restructuring court order and issued 2 interesting declaratory judgments.SOME BACKGROUNDIn 2011 Mr Norris took an unsecured personal loan in the amount of R120 000 with Nedbank. Nedbank checked that he could afford the loan and issued it to him. The total repayment amount would be a whopping R220 000 over the 60 months of the loan. Monthly Mr Norris was to repay R3674.49 at 17.5% interest. Not to be forgotten was the Credit Life insurance of R529.80 on the amount each month (+- R 31 000 over the 60 months).

Within two years Mr Norris had a change of circumstances and due to increased pressure to service all debt approached a Debt Counsellor in PE. (Sonja Volschenk of Madiba Bay Debt counsellors 041 379 2621 [email protected])

At this point Mr Norris still owed R105 612. 15 on this particular loan (figure probably taken from the Nedbank CoB) and don’t forget those monthly insurance costs.

Whereas Nedbank wanted R 3674.49 monthly for their loan now the Debt Counsellor determined that Mr Norris had only R1600 to pay all his debt each month (incl amounts to among others ABSA , Wonga, Ellerines, Edgars, Bridge loans, African bank).

Proposals were sent to all creditors (which were all for very low amounts over a very long time). The proposals were then turned into a court application and the matter was set down for a short while later in Jan 2014.

Nedbank put on record and submitted their intention to oppose the application as they were not happy with the proposals. Due to a somewhat irregular chain of events the court matter was not held the day it was originally planned (when Nedbank did show up) but several days later when Nedbank were not present (note: they had asked to be informed of the new set down date but never heard back from the consumers attorneys).

As a result Magistrate Dumani N.O. granted an order and the court order reduced Nedbank’s interest to zero (instead of letting run to induplum)At R289.15 a month x 260 (the DC had planned for a cascading increase in the repayment amount over time as smaller debts were settled)

Nedbank were obviously not happy that they had not got to oppose and that the interest amount had been changed without their consent and wanted to rescind the court order. They then later applied to the court and rather than hear the whole matter the court changed interest rate back to the original 17.5 %. Nedbank were still not happy and the repayment amount of R289.15 was thus too little to cover interest (and don’t forget the credit life insurance of R529.80)

Many banks prefer to recover funds over 60 months (for unsecured credit). It is a target they like to achieve. If the consumers circumstances did nto change at all (which they likely would over time) the reality is that even if Nedbank got every cent from the consumer each month (R1600 x 60) this amount would simply be too little as well if the interest rate and credit life payments were not adjusted). Thus the need for the debt review.

In November 2015 Nedbank’s case was heard by the High Court in Port Elizabeth. We will refer to the case as : Nedbank V Norris (& Magistrate Dumani N.O.) The judgement was handed down in March 2016 and has since been much discussed.

After summarising the original loan agreement, the application for debt review and the granted court order the judgement focused on Jurisdictional matters for a while before looking into the matter.

The PE High Court pointed to deficiencies in not only the fact that Nedbank never got their day in court but that the original debt restructuring court application did not have a lot of evidence in it that Mr Norris was actually over indebted (he obviously was but you have to show it not just say it)

The High Court (not considering any cascading payment increases over time) pointed out that the proposed repayment plan of R289.15 x 260 doesn’t add up to total figure owed at zero interest (never mind the interest). Obviously, cascading payments change that but this is hard to show without the full cascading repayment schedule.

The High Court then focused on the fact that the Magistrate had reduced interest from 17.5 % to 0% without the creditor agreeing to this/ proposing this. This is not in line with the powers set out in the National Credit Act regarding debt restructuring.

Next discussed was the irregular manner in which the interest rate was just changed back to

17.5% and how this hadn’t take into consideration the effect on the other creditors.

As a result of these facts the High Court ordered that the 2014 debt restructuring court order be set aside. And that the Jan 2015 court order changing interest back to 17.5 % be set aside.

Next 2 declaratory orders were made:

DECLARATORY ORDER #1:It was ordered that a Magistrates Court must not change a contractually “agreed” interest rate.

Obviously this needs to be taken in context since the recent Declaratory Order (made prior to this case in March 2015) Van der Hoven Attorneys v The National Credit Regulator and 4 others states that where parties do agree to a reduction it (the interest rate) can be included in the court order. This would be due to changes to the “agreed” amended agreement between the parties.

Nedbank have issued a statement to the same effect that the law is very clear that, where the parties have reached an agreement with regards to the re-arrangement of a debt , that any court hearing the matter has the authority to grant such an order.

DECLARATORY ORDER #2:It was ordered that a rearrangement proposal in terms of NCA S86(7)(c) which pays (monthly) less than interest rate increase amount (monthly) doesn’t match the purpose of the NCA and would be “ultra vires” and a Magistrates Court has no jurisdiction to grant such an order.

This makes sense when enough funds are available to match the interest portion. In this case clearly at first no such available funds.

QUESTIONS TO CONSIDER:Such an order could effectively remove debt review as a legal right from those who have too little in total to cover full un-adjusted interest portions toward their credit agreements even if over indebted.

Admittedly there is less short term benefit to the credit provider if the consumers debt continues to grow over time (with the safety net of Sect 103(5) in duplum which insures that a credit provider gets the full legal limit of recovery from a defaulting consumer).

If all credit providers decided to refuse to change interest rates (which would be their right) most debt restructuring proposals would probably fall into such a case (where someone, somewhere among the creditors is getting less than the interest amounts as the debt grows to the legally built in Sect 103(5) in duplum limit).

However this declaratory order makes no allowance for increased payments over time though low at first. Eg a consumer who is receiving a salary increase, at a time shortly after the order would be made, which would drastically increase the monthly repayment amounts.

OTHER OPTIONS A COURT WOULD HAVE IN SUCH A CASE:Though it can unilaterally change interest rates without consent a court can order that certain payment obligations are set aside for a brief time (eg if consumer loses job and is looking for new work). The focus of the NCA is not on monthly meeting of the obligation but “eventual” satisfaction of the debt. So, where consumers don’t have enough to cover the interest portion these debts could have their payments stopped for a while to allow other debts to be settled. The challenge would then be to decide who gets their money first in a fair manner. Not a great alternative really.

So, it seems that with this second declaratory order there is potential conflict since the NCA lays importance on “eventual” satisfaction of the debt and not monthly satisfaction of interest amounts. Thus the NCA has built in protections for consumers and creditors such as NCA Section 103(5).

There is little doubt that Nedbank V Norris (& Magistrate Dumani N.O.) will be referenced in future cases so Debt Counsellors and Attorneys should become familiar with it.

Fortunately Nedbank and Mr Norris have already come to an agreement about his debt. The debt restructuring court order has been set aside, but a payment plan is in place. PS. If Mr Norris were to switch credit life products to companies such as ONE|SURE his monthly credit life cover on that debt would only be R317.70.

South Africa’s leading Debt Counsellors

Having a Debt Counsellor assess your financial health to see if you qualify for debt review is a positive first step towards paying back your credit providers and becoming debt free. But some people are still apprehensive about debt review and that’s why NDA have compiled an insightful, to-the-point Q & A to clear up any doubts.

DEBT REVIEWQ & A WITH NDA!

1. I’m worried about debt review fees. Won’t I just rack up more debt? Debt review fees are regulated by the National Credit Regulator (NCR) to stop unscrupulous Debt Counsellors from charging consumers excessive rates and tariffs for debt review services. NDA is an official NCR-registered debt counselling firm. We always ensure our clients can afford their living expenses, monthly instalments and our fees comfortably, without struggling.

2. Can I take out more credit while I’m under debt review?Not until you have settled all of your debts and received a clearance certificate. Which is really a good thing if you think about it! Debt review is an official, proven way of rehabilitating consumers into the credit market, which means you’ll be able to apply for credit upon completion.

3. Does debt review take forever and a day to complete, as the rumours suggest? Debt review does involve extending your repayment term. But, it also means that your credit providers will reduce your monthly instalments and interest rates now. This will allow you to keep up with your payments and maintain a normal standard of living, instead of barely scraping by each month.

4. Will my house and car be protected while I’m under debt review? As soon as we notify your credit providers that you are under debt review, they won’t be able to take legal action against you. Meaning, your home, car and other valuable assets will be protected. We hope this clears things up for anyone who is still unsure about entering debt review. I’m sure you will agree the pros of debt review really do outweigh the cons!

To find out if you qualify for debt review with National Debt Advisors, get in touch at: http://nationaldebtadvisors.co.za/contact-us/

The debt review industry is one which incorporates business, the distribution of funds and helping over indebted people across the county. It is my goal to help as many people along the way as possible. My main function is to provide a service to Debt Counsellors, train them on our programs and help them wherever needed. Due to effective and consistent training provided to Debt Counsellors from DC Partner and myself I believe our DCs are able to provide a better service to their clients. DC Partner is a PDA ( Payment Distribution Agency) and this also one of the reasons I entered this industry as it involves the distribution of small to tremendously large amounts of money which are paid from the consumer to the creditors. DC Partner has been distributing funds for over 9 years now. They come highly recommended. I have always wanted to work for a big corporate company such as DC Partner.î

My name is Storm Horstead. I am twenty one years of age, studying a Bachelor of Commerce in Marketing and Management.

I am passionate about business and finance. I have recently been employed full time as an agent based in Kwa-Zulu Natal. I could not have wished for a better start to my business career as I have been blessed with the opportunity to work alongside extremely experienced and talented staff at DC Partner.

Storm Horstead

www.dcpartner.co.za

DEBT COUNSELLING CAN MAKE A POSITIVE

ECONOMIC IMPACT

IN A NUTSHELL

Minister Pravin Gordhan’s 2016 budget speech earlier this year reiterated the following statement several times “We are resilient, we are committed, we are resourceful”. He chose to repeat this statement no less than five times during his budget address. An address whose message was primarily hopeful. Times are tough, but South Africans are resilient, and if we are committed as a nation we can find creative and resourceful ways to improve our economic future.

Characterising these tough times is the fragile business confidence in the region, the concern and theory that our debt will soon be given junk status, and the impact of the current severe drought. Our weak forecast of economic growth at only 0,9% further exacerbates this sentiment. Investopedia describes ‘economic growth as an increase in the capacity of an economy to produce goods and services.’ Economic growth is a measure of a country’s productivity, and its ability to increase revenue. If revenue is under pressure and costs are increasing then the only way to avoid the debt trap in the short-term is to curb costs.

South Africa as a country much like its citizens spends more than it earns. To make up the shortfall, South Africa needs to borrow R139 billion, which is equivalent to 3.4% of the Gross Domestic Profit (GDP). Similarly, based on the latest statistics from the National Credit Regulator (NCR) close to 50% of South Africans are over-indebted, which means they spend more than they earn.Minster Pravin Gordhan did not offer much regarding consumer relief. Although the lower to middle-income groups will gain a personal income tax relief of R5.5 billion, this is a marginal amount on an individual basis. Here are two examples, an individual earning a modest salary of R8,000 per month will gain an annual relief of R243. An individual earning R25,000 per will gain an annual relief of R1,206. These marginal gains will be eroded by the rising costs of living, driven by increases in the fuel price, electricity, interest rates and the decline in the exchange rate. Inflation is expected to be in the region of 6.8%. The general fuel levy will be raised by 30c/litre to R2.85/l for petrol and R2.70/l for diesel. Most goods are transported by road which means that this will impact food prices and other goods. The National Energy Regulator (Nersa) recently announced that electricity prices will be increasing by 9.4% from April 2016. Before consumers reach for that glass of wine or beer to drown their sorrows, sin tax is going up as well, meaning that the prices on alcoholic beverages and tobacco products are also increasing between 6% to 8%.

IN A NUTSHELL is brought you by the DCM Business Partnership Programme™, designed to support debt counsellors and consumers during the debt review process, in collaboration with the National Payment Distribution Agency (NPDA). For help, contact the NPDA on 0861 628 628.

The NPDA was recognised as the industry winner for PAYMENT DISTRIBUTION and Care Premier as the industry winner for DEBT COUNSELLING SOFTWARE at the Debt Review Awards 2015.

If you have suggestions for topics that you would like covered in future, please email [email protected]

For consumers to keep their heads above water, they will need to reassess their budgets and kerb expenses where possible. Budgeting and budget monitoring become crucial in tough economic times.

Consumers who battle to meet their debt obligations and are at risk of losing their homes and cars need to consider debt counselling as an option. The latest Credit Bureau statistics for the quarter ending Sep 2015 indicate that of the over 23 million credit active consumers, 9.91 million have impaired credit records. An impaired record means that a consumer is more than three months in arrears on payments.

At this time in our economy, it is necessary that all South Africans take responsible and resourceful steps to improve their financial situation. Overindebtedness adds to the costs of borrowing money for all borrowers in the economy. If borrowers were to borrow and repay responsibly, it would free up more capital for investment.

Debt Counsellors have a very important role to play in helping overindebted consumers budget responsibly, educating them on the benefits of debt counselling and encouraging their commitment to the debt review process.

Consumers that are already under debt review should have an annual review with their debt counsellor to reassess their budgets in light of the expected increase in the cost of living.

As South Africans, we are resilient, we are committed, we are resourceful. But we all need to work together to achieve financial freedom.

If you’re a Debt Counsellor, consider sharing this article with your clients.

NCR WORKSHOPThe National Credit Regulator recently began a series of workshops for Debt Counsellors (and Credit Providers) across the country. The workshop is an opportunity for registrants to network and be briefed by the NCR on their plans and recent industry trends. Debtfree reports on the Recent Workshop held in Cape Town.

Ms. Tshepa Molefi acted as Chairperson for the day and in the morning introduced Ms. Kedilatile Legodi (who is Manager of the NCR’s Debt Counselling Department) to welcome everyone and set out the agenda for the day. Ms Legodi said in her opening remarks that she hoped the workshop would inspire, excite and challenge those attending.

The first speaker for the day was ms Mmbatho Senyarelo of the NCR Investigations and Enforcement Department. She discussed some recent NCR labelled “raids” on large debt counselling firms in Cape Town. Since these so called raids nothing has happened and members of the audience were no doubt curious to find out what was happening and why there had been raids as opposed to the normal monitoring visits. Ms Senyarelo said that raids do not necessarily mean there were violations by the Debt Counsellors. She stated that in some cases no contraventions were found. She went on to say that referral of contraventions to the National Consumer Tribunal was also not automatic. Even if matters were referred to the NCT the NCR would still engage with these firms to resolve matters. She did however state that some of the firms (plural) who had been raided have been referred to the NCT. This has not previously been public knowledge.

After vaguely fielding questions about why the NCR were lax on taking action against debt mediators (debt review outside of the NCA) and ADRAs who offered debt review-like services, outside of what they were allowed to do, she mentioned that a recent raid in Limpopo had resulted in the DC being referred to the NCT.

Ms Georgina Kgadima next spoke on behalf of the NCR monitoring office. Ms Kgadima spoke on the topic of Debt Counsellors cancelling appointments last minute and how the NCR have a problem with the promotion of debt review over the phone or via a call centre set up. This was one of the first times that the NCR have somewhat defined what they are concerned about when it comes to consumers dealing with call centres. The NCR even has a billboard campaign costing thousands and the reasons have never been clear as to why they disapprove. It seems that some of the concern is over consumers being contacted (not contacting a DC themselves) and told about debt review. In some cases, consumers have been signed up for debt review without making a proper commitment to the process. Later such consumers ,who go looking for further credit, find they cannot get it as they are now registered with the NCR. They then contact the NCR, creating more work for the NCR in trying to sort the matter out.

POPI IGNORED?An interesting question was raised in regard to POPI violation when the NCR arrives at a Debt Counsellors Office and asks to see consumers private and confidential information without consent from the consumer. Ms Kgadima indicated that waiting for permission from such consumers would make it hard for the NCR to monitor timeously and thus “it would not work” for them. No real resolution was reached about if this represented a POPI violation or not.

Magistrate Mannie Van Reenen (of the Bellville Magistrates Court) presented regarding the 2009 Declaratory Order and more recent court matters including FNB v Barnardt (where the DC was ordered to pay costs) and Nedbank v Norris & Magistrate Dumani (where the High Court said the Magistrate should never have unilaterally changed interest rates without consent). He discussed how he likes applications to look and stated;” I am not a difficult Magistrate”.

After a presentation by Ms Lizelle Squirra ( NCR Registrations & Compliance) regarding affordability assessments Ms Celancia Froneman of the new African Bank (formerly known as African Bank) discussed the recent organisational changes at African Bank. Recently the Bank has split into Residual Debt Services and the all new African Bank. African Bank will collect on behalf of Residual Debt Services so little will change from a consumer perspective. She did however explain the changes that may be needed for court documentation in regard to registration numbers and phrasing that may be needed to clarify who was who. She also had the opportunity to review the new look African Bank CoBs which will help clarify which debt is with whom.

Lunch was a busy affair with lots of opportunities to mingle and engage with various displaying

service providers and registrants. The various PDAs were in attendance as well as several banks and ONE|SURE.

After lunch it was down to the serious business as Mr Graham Bellairs and Ms Yusria Cornelius presented on behalf of the Cape Law Society. The topic of the hour is something called “fee sharing” between Debt Counsellors and Attorneys. They discussed several ways in which some firms are using funds from one consumer to help cover the legal fee costs of another consumer or where the Debt Counsellor does not use the funds exclusively for legal work or where the legal firm may reimburse the Debt Counsellor in some way. Their message was clear: fee sharing is illegal.

Ms Cornelius mentioned that some attorneys have not been able to get work from Debt Counselling firms because they refuse to share fees in some way. The NCR and the Law Society have met and will issue a joint statement on the topic shortly.

Ms Cornelius mentioned that Debt Counsellors can do legal work and prepare documentation etc (they are the applicant) but they simply must not charge for the work (unless it is legal work for the NCT where the NCR has said that Debt Counsellors can charge a “legal fee”).

Where the presentation had been going strong (if somewhat stern) things next turned sour as Ms Cornelius made seemingly condescending comments about longstanding Debt Counsellor Mr John Steyn’s contribution in helping establish the now commonly used debt review court application documentation. These were not well received and the meeting almost came to a halt among the raised voices, hushed boos and heckling. Ms Kedilitile Legodi apologised on behalf of the Cape Law Society and managed to get things back under control, though some people began to leave at that point.

Ms Senyarelo next took the podium again to discuss the NCRs complaints process. The NCR are trying to resolve complaints within 14 days and she discussed the steps the NCR use in this process. Interestingly as per the NCA the NCR are not required (or supposed) to resolve matters only consider and the refer them to the relevant body to do so.

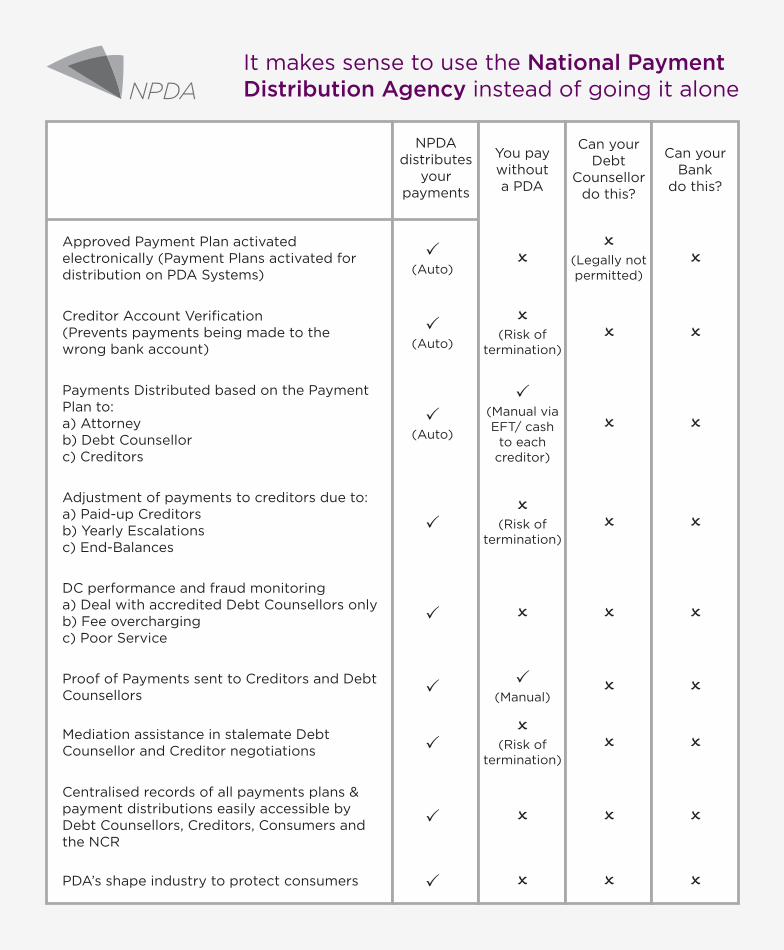

PDAs have been a hot topic with the recent deadline for the PDAs to register with the NCR happening at this time. Ms Legodi discussed how out of all consumers the NCR think are under debt review only half make use of a PDA. On average consumers making use of a PDA make payments around R4500 monthly and each month the PDAs pay over R569 Million to credit providers. It came out during the day that only registered PDAs have to charge according to the new fee structure and that none of the PDAs registrations had been finalised (Debt Counsellors often wait between 6 to 9 months for their registrations to come through) yet. Thus none of the current PDAs had changed their fee structure yet.

Mr. Peter Michaels made a spirited presentation toward the close of the day and broached the topic of recent industry updates in the wake of the amendments to the NCA last year. He also touched on all the sub committees being formed by the NCR organised Credit Industry Forum (CIF). Some of the upcoming projects include: Section 103(5), Clarity on Withdrawal Guidelines, End Balance Disputes, the NCR Debt Help System, PBLs, Reckless Lending Process (when complaints/allegations are made to the NCR). He also touched on the recent court judgements regarding debt review. In one case a DC was forced to pay fees partially because they followed the NCR’s guideline on fees and caused the consumers vehicle to go into default (among other issues). He lightly glossed over that as he focussed on how there had been no plan (within the 60 days of review) to sell the consumers second house. He also touched on the Nedbank v Norris & Mag. Dumani case. The NCR feel that where the credit provider and consumer agree to lower the interest rates not doing so would prejudice the consumer.

The NCR trying to figure out why consumers are wanting to/ are changing Debt Counsellors so much. It is causing havoc with their NCR Debt Help system and making lots of work for them. It also was said that Debt Counsellor training material has been updated in line with amendments to the NCA. Very exciting was a comment that the NCR will soon be releasing a very pro debt review brochure.

Ms Legodi closed out the day by discouraging credit providers from reckless credit granting and saying the NCR want to see consumers maximising the use of debt review to address debt.

THE GOOD, THE BAD AND THE UGLY

GOODThe venue and large number of attendees was great. Ms Legodi said that there will be a review of Debt Counselling fees (no indication of when and by who).

BADThe NCR indicated that as per rumour they wish to take their non binding guidelines and try squeeze them into the Debt Counsellor conditions of registration (thus making them binding). This will no doubt lead to lots of applications to the NCT contesting this.

UGLYThe Cape Law Society presentation started out strong but ended ugly.

It can happen that when dealing with a consumer’s debt situation Debt Counsellors and Credit Providers take opposite views on the same account. This can occasionally lead to some conflict. This is why relationship building is so vital in maintaining a professional industry. Workshops held by credit providers make it possible for them to meet and engage with Debt Counsellors and reduce difference in understanding of their processes. This can in turn reduce possible causes for conflict.

Recently, FNB held such a conference with Debt Counsellors in Gauteng. Topics ranged from Annual Reviews (where DCs check on a consumers situation) to FNB’s outreach programs. When it comes to annual reviews credit providers often hope that consumers will have received increases that outstrip the increased cost of living. This is sadly seldom the case but FNB feel it is an important step for both themselves and Debt Counsellors to try in order to try help consumers shorten their time under debt review, if possible.

NEW PROJECTSFNB are busy sending notices long in advance of any possible 86(10) Termination letters. This pre-termination project helps reduce unnecessary extra work for all parties by identifying where wires may be getting crossed. It was stressed that DCs should please send as much documentation to support any replies as possible to speed things along.

FNB are also trying to clean up their files on certain clients and may contact DCs in regard to missing documentation. They ask that DCs help them and not get upset even if they have sent these documents before. They hope that they will get good co-operation with this project.

Another very exciting project is FNB sending out balances to DCs for FNB products. This is still in the pilot phase but could help reduce end balance differences and speed up issuing of clearance certificates greatly.

Attending Debt Counsellors benefited, as always, from the well run workshop and look forward to engaging with FNB with now increased understanding of recent trends at FNB. FNB plan to hold similar workshops across the country over time in an ongoing commitment to engaging with Debt Counsellors.

FNB WORKSHOPGAUTENG

DEBT COUNSELLING COMMUNITY SUPPORT

DEBT COUNSELLING COMMUNITY SUPPORT

With the help of our generous sponsors DCCS was able to assist vulnerable debt review families from across SA to get their kids back to school with all the needed stationery and school

goodies. We want to thank both our sponsors and those DCs in the community who helped identify these families.

If you would like to get involved and help keep hard working, regularly paying, responsible debt review families in the debt review process please feel free to contact us on

www.DCCSupport.co.za

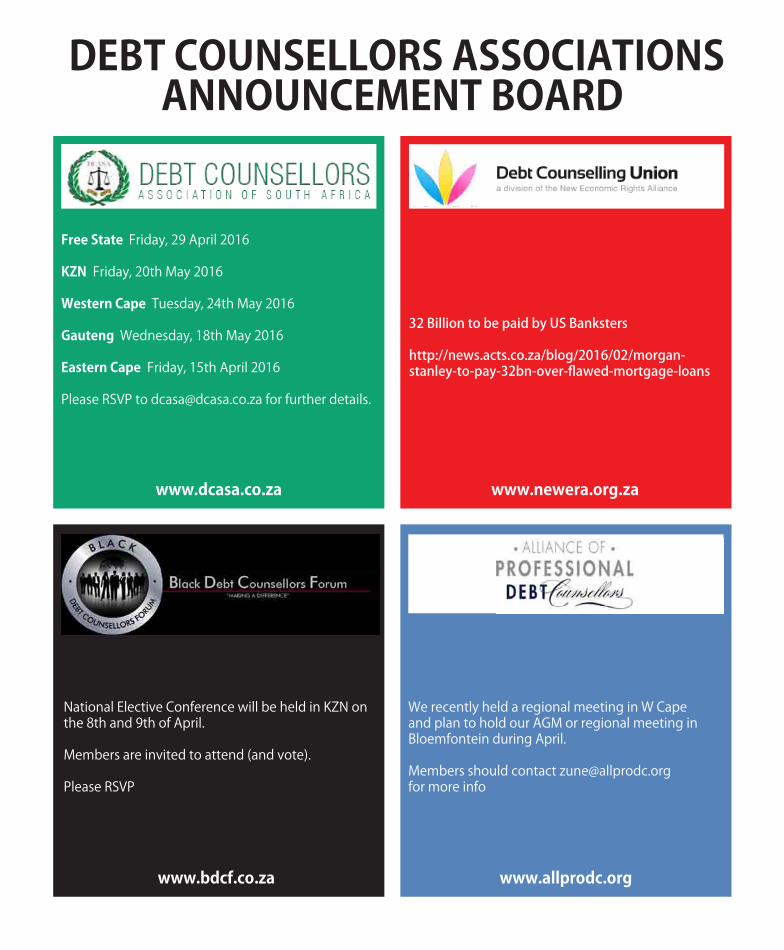

Free State Friday, 29 April 2016

KZN Friday, 20th May 2016

Western Cape Tuesday, 24th May 2016

Gauteng Wednesday, 18th May 2016

Eastern Cape Friday, 15th April 2016

Please RSVP to [email protected] for further details.

DEBT COUNSELLORS ASSOCIATIONS ANNOUNCEMENT BOARD

32 Billion to be paid by US Banksters

http://news.acts.co.za/blog/2016/02/morgan-stanley-to-pay-32bn-over-flawed-mortgage-loans

www.newera.org.za

www.bdcf.co.za

We recently held a regional meeting in W Cape and plan to hold our AGM or regional meeting in Bloemfontein during April.

Members should contact [email protected] for more info

www.allprodc.org

National Elective Conference will be held in KZN on the 8th and 9th of April.

Members are invited to attend (and vote).

Please RSVP

www.dcasa.co.za

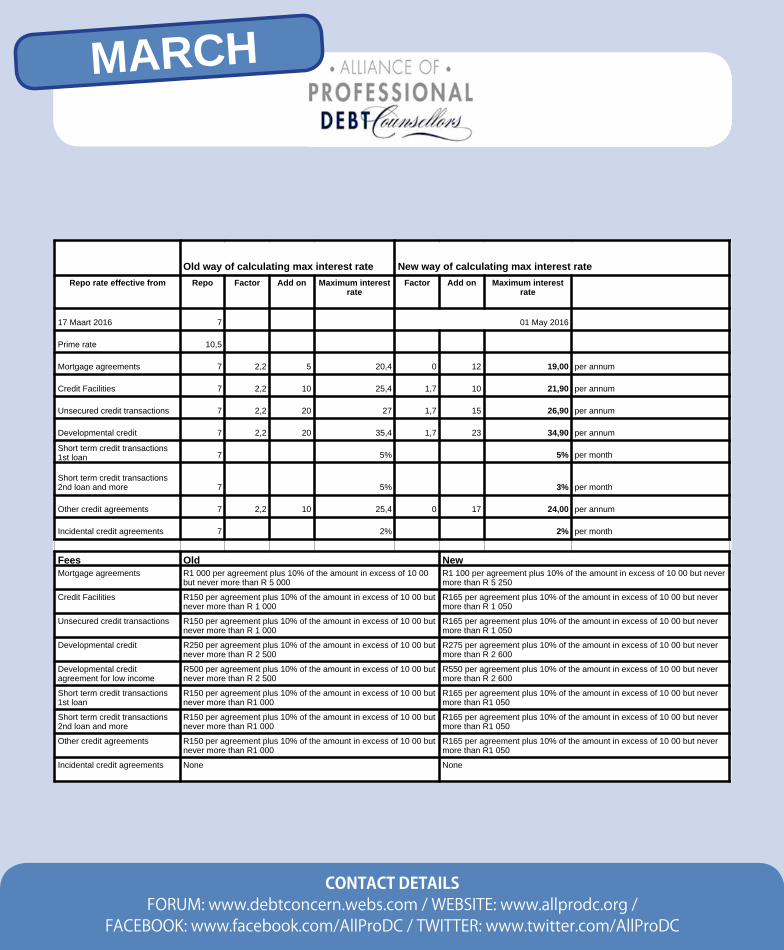

MARCH

CONTACT DETAILSFORUM: www.debtconcern.webs.com / WEBSITE: www.allprodc.org /

FACEBOOK: www.facebook.com/AllProDC / TWITTER: www.twitter.com/AllProDC

Old way of calculating max interest rate New way of calculating max interest rateRepo rate effective from Repo Factor Add on Maximum interest

rateFactor Add on Maximum interest

rate

17 Maart 2016 7 01 May 2016

Prime rate 10,5

Mortgage agreements 7 2,2 5 20,4 0 12 19,00 per annum

Credit Facilities 7 2,2 10 25,4 1,7 10 21,90 per annum

Unsecured credit transactions 7 2,2 20 27 1,7 15 26,90 per annum

Developmental credit 7 2,2 20 35,4 1,7 23 34,90 per annum

Short term credit transactions 1st loan 7 5% 5% per month

Short term credit transactions 2nd loan and more 7 5% 3% per month

Other credit agreements 7 2,2 10 25,4 0 17 24,00 per annum

Incidental credit agreements 7 2% 2% per month

Fees Old NewMortgage agreements R1 000 per agreement plus 10% of the amount in excess of 10 00

but never more than R 5 000R1 100 per agreement plus 10% of the amount in excess of 10 00 but never more than R 5 250

Credit Facilities R150 per agreement plus 10% of the amount in excess of 10 00 but never more than R 1 000

R165 per agreement plus 10% of the amount in excess of 10 00 but never more than R 1 050

Unsecured credit transactions R150 per agreement plus 10% of the amount in excess of 10 00 but never more than R 1 000

R165 per agreement plus 10% of the amount in excess of 10 00 but never more than R 1 050

Developmental credit R250 per agreement plus 10% of the amount in excess of 10 00 but never more than R 2 500

R275 per agreement plus 10% of the amount in excess of 10 00 but never more than R 2 600

Developmental credit agreement for low income housing

R500 per agreement plus 10% of the amount in excess of 10 00 but never more than R 2 500

R550 per agreement plus 10% of the amount in excess of 10 00 but never more than R 2 600

Short term credit transactions 1st loan

R150 per agreement plus 10% of the amount in excess of 10 00 but never more than R1 000

R165 per agreement plus 10% of the amount in excess of 10 00 but never more than R1 050

Short term credit transactions 2nd loan and more

R150 per agreement plus 10% of the amount in excess of 10 00 but never more than R1 000

R165 per agreement plus 10% of the amount in excess of 10 00 but never more than R1 050

Other credit agreements R150 per agreement plus 10% of the amount in excess of 10 00 but never more than R1 000

R165 per agreement plus 10% of the amount in excess of 10 00 but never more than R1 050

Incidental credit agreements None None

SERVICE DIRECTORYDEBT COUNSELLORS

SUPPORT SERVICES

FINANCIAL PLANNINGFINANCIAL

TRAINING

CLICK THE CATEGORY

SERVICE DIRECTORY

FINANCIAL PLANNING

CLICK THE CATEGORY

LEGAL

CREDIT BUREAUSPAYMENT

DISTRIBUTION AGENCIES

CREDIT PROVIDER CONTACT DETAILS & ESCALATION PROCESS

DO YOU WANT TO LIST YOUR COMPANY?

GAUTENG KWAZULU-NATAL

FREE STATE

DEBT COUNSELLORS

LIMPOPO NORTH WEST EASTERN CAPE

MPUMALANGA NORTHERN CAPE WESTERN CAPE

Armani Debt CounsellingTake the First Step

to Financial Freedom Tania Dekker

Tel: 011 849 3654 / 7659www.armanigroup.co.za

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

Dynamix Debt Counselling TLCAlida Christie NCRDC2324

Office 1, 34 Beefwoodstreet, Vanderbijlpark, 1911

Tel: 079 520 4369Tel: 016 100 8020

National Debt AdvisorsFighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

GAUTENG

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

Dynamix Debt Counselling TLCAlida Christie NCRDC2324

Office 1, 34 Beefwoodstreet, Vanderbijlpark, 1911

Tel: 079 520 4369Tel: 016 100 8020

Specialist Debt Management CentreBeverley Ludick, NCRDC948

PretoriaTel: 012 377-3557

Email: [email protected]: [email protected]

www.obligco.co.za Tel: 0861 123 644Email: [email protected]

NCRDC197Tel: 011 660 9970Fax: 086 540 5017

KRUGERSDORPe-mail: [email protected]

www.nvdmdc.co.za

All Debt SolutionsFast tracking your financial freedomTel: 0861 255 3328 / 021-557 9981

Email: [email protected]://www.facebook.com/

alldebtsolutions

Creators In Financial Wellbeing

NCRDC677You Are Not Alone

We’ll handle your creditors so you don’t have to!

1 Dingler Street, Rynfield, Benoni0861 10 11 00

KWAZULU-NATAL

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

National Debt AdvisorsFighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Tel: 0861 123 644Email: [email protected]

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

FREE STATE

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

National Debt AdvisorsFighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Tel: 0861 123 644Email: [email protected]

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

LIMPOPO

SMS Salary Management ServicesAnnerien de Jager

Registered Debt Counsellor NCRDC0075

015 307 [email protected]

National Debt AdvisorsFighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Tel: 0861 123 644Email: [email protected]

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

MPUMALANGA

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

National Debt AdvisorsFighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Tel: 0861 123 644Email: [email protected]

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

NORTH WEST

National Debt AdvisorsFighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Tel: 0861 123 644Email: [email protected]

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

NORTHERN CAPE

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

National Debt AdvisorsFighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Tel: 0861 123 644Email: [email protected]

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

EASTERN CAPE

Debt Counselling Group SAAffordable Assistance with offices across

the EASTERN CAPE.Casper Francois le Grange

NCRDC 1560 / CALL: 086 100 1047Offices:

East London: Shop 7, New Colonnade Building, Devereux Av, Vincent

Port Elizabeth: Room 302, Pier 14, 444 Goven Mbeki Av, North End

Queenstown: Office 107, Nedbank Building, 89 Cathcart Road

King Williams Town: Office 4, 49 Eales Street

E-mail: [email protected]

www.facebook.com/dcg.southafrica

National Debt AdvisorsFighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Tel: 0861 123 644Email: [email protected]

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

DON’T WORK WITH AN OUT DATED VERSION OF THE ACT

We are happy to announce that the Amended National Credit Act bookletis now available via our shop.

Get the latest version for only R250.00

ORDER NOWhttp://debtfreedigi.co.za/product/pocket-sized-national-credit-act-booklet/

UPDATED2015

debt therapyintegrity guaranteed

WEBSITE | www.debt-therapy.co.za

SCARED OF ANSWERING YOUR CALLS?

Take back control of your life in 1 easy step!

debt therapy is registered with NCR | NCRDC49

Take the first step to financial freedom by visiting our :

|FREE CALL 0800 20 47 28

Drasticallyreduceyourmonthlydebt repayments

Let US help 0861111863Regain control of your finances

www.debt-therapy.co.za

WESTERN CAPE

CONSOLIDEBTHeidie Knorr NCRDC209

Paarl, Worcester, Wellington, Ceres, Piketberg, Clanwilliam, VredendalTel: 021 863 2754 / 082 380 4401

Encouraging Freedom, Creating WealthEtienne Pieterse (NCRDC 2210)

Tel. (021) [email protected]

www.financialfreedomsolutions.co.za

National Debt AdvisorsFighting For Consumer Justice

Tel: 021 007 1688 www.nationaldebtadvisors.co.za

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

ISISEKO DEBT HELPGet Your Life back on track

TEL: 087 230 0223FAX: 086 551 1649

EMAIL: [email protected]: www.isiseko.co.za

DEBT REVIEW AND SUPPORT CENTRE

Annienne Nel NCRDC2452Kairo’s House, 22 Fairfield Southstreet, Parow, 7550

Office: 021 930 5791Cell: 082 641 2328Fax: 086 563 3264

e-mail: [email protected]

All Debt SolutionsFast tracking your financial freedomTel: 0861 255 3328 / 021-557 9981

Email: [email protected]://www.facebook.com/

alldebtsolutions

NCRDC1142 No 2 Golden Isle Building

281 Durban Road, Oakdale,Bellville, 7535

Tel: 086 111 3749Email: [email protected]

www.zerodebt.co.za

Debt BudgetOne Monthly Payment For All Your Debt

Bruce Leslie BorezNCRDC1643

52 Church Street, “NBS Building”,Wynberg

Tel: 021 824 8885www.debtbudget.co.za

Credit MattersSouth Africa’s Leading

Debt Counsellors14th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 086 111 6197Fax: 021 425 6292

CONSUMER

& Solution CentreNCRDC2452

don’t be a twit

http://twitter.com/Debtfree_DIGI

SUPPORT SERVICES

lana Van Herwaarde,DC Operation Centre (PTY)

Tel: 0867227405 Email: [email protected]

DEBT086 126 6562

[email protected] www.one.za.com

Detect ID Theft or possible ID Fraud

Akani SolutionsInformation Data Solutions

Credit Report App

ID Protector

Access Your Credit Bureau Report Instantly on Your Phone

DCs help your clients use it during application & to protect their ID

Subscribers notified by SMS when number is activated

FINANCIAL PLANNING

TRAININGCOMING SOON

COMING SOON

LEGAL

Liddles & Associates“It always seems impossible until it

is done” N. Mandela(T) 021 930 5790(F) 0866070940

RM Brown and Associates 16th Floor, The Pinnacle

Cnr Strand & Burg StCape Town

Tel: 021 202 1111, f: 021 425 0875 Email: [email protected]

Steyn Coetzee Attorneys / Prokureurs

Adri de Bruyn11 Market Street / Markstraat 11,

Paarl, 7646Tel: 021 872 1968Fax: 021 872 2678

CREDIT BUREAUSCOMING SOON

Kim ArmfieldAttorney & Family Law Mediator Address: Unit 1B, FinansHuis, 7

Voortrekker Road, BellvilleTel: 021 949 1758 / 021 945 2526

Office cell: 084 8588 [email protected]

Your Debt Counselling Attorneys

Johannesburg | Cape Town

Andre Van Zyl021 494 4862

www.bassonvanzyl.com

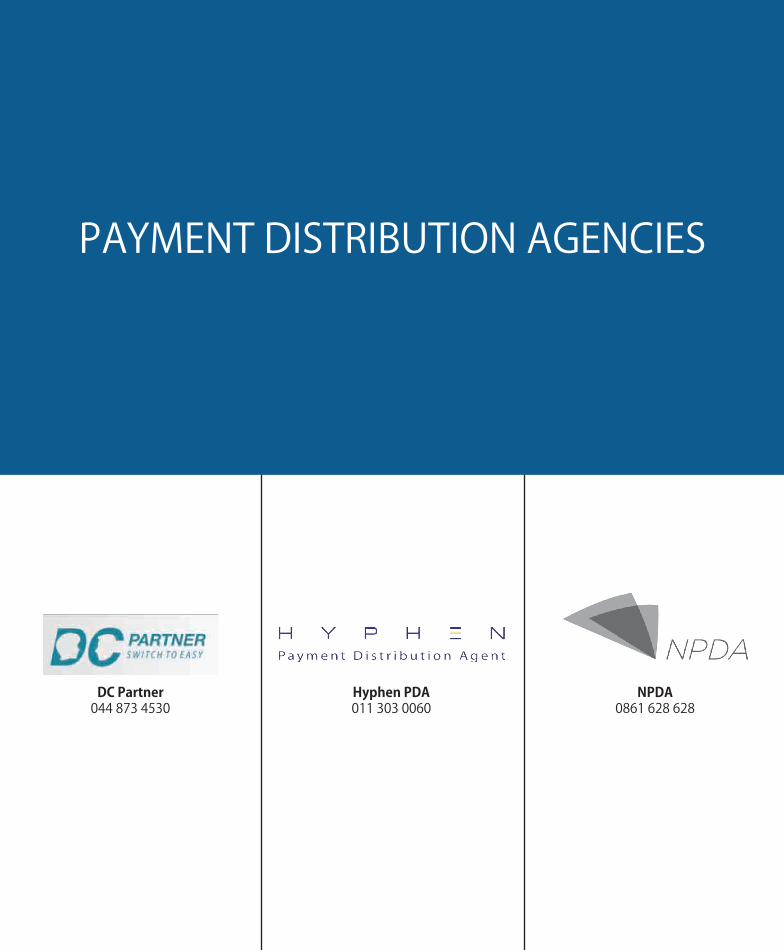

PAYMENT DISTRIBUTION AGENCIES

DC Partner044 873 4530

Hyphen PDA011 303 0060

NPDA0861 628 628

NPDA0861 628 628

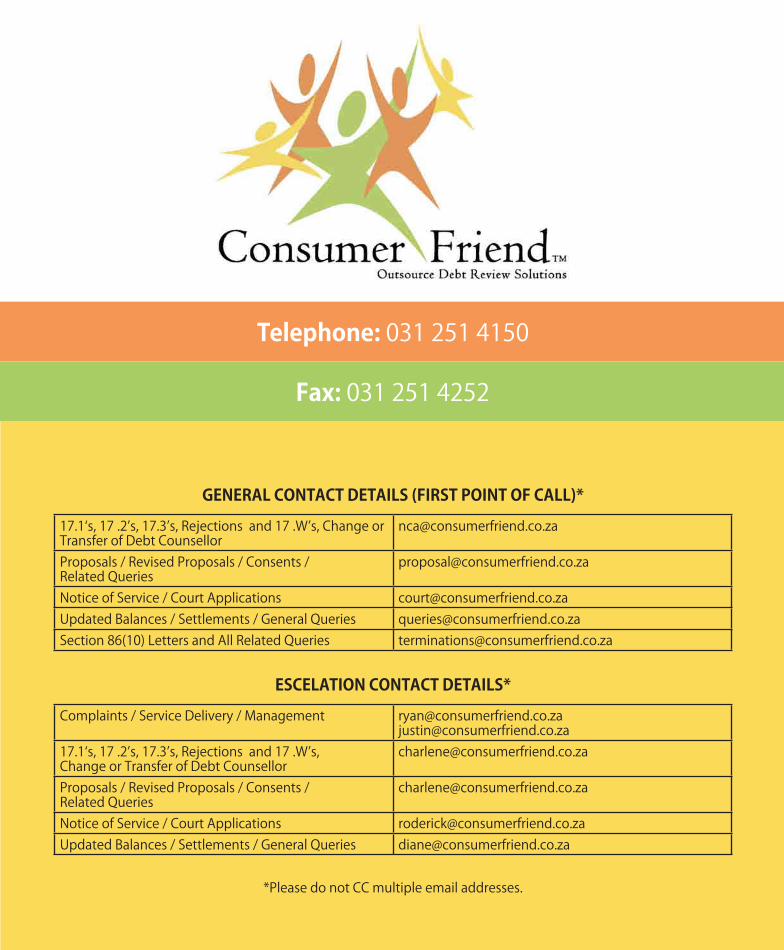

Telephone: 031 251 4150

GENERAL CONTACT DETAILS (FIRST POINT OF CALL)*

17.1‘s, 17 .2’s, 17.3’s, Rejections and 17 .W’s, Change or Transfer of Debt Counsellor

Proposals / Revised Proposals / Consents / Related Queries

Notice of Service / Court Applications [email protected] Balances / Settlements / General Queries [email protected] 86(10) Letters and All Related Queries [email protected]

ESCELATION CONTACT DETAILS*

Complaints / Service Delivery / Management [email protected]@consumerfriend.co.za

17.1‘s, 17 .2’s, 17.3’s, Rejections and 17 .W’s, Change or Transfer of Debt Counsellor

Proposals / Revised Proposals / Consents / Related Queries

Notice of Service / Court Applications [email protected] Balances / Settlements / General Queries [email protected]

*Please do not CC multiple email addresses.

Fax: 031 251 4252

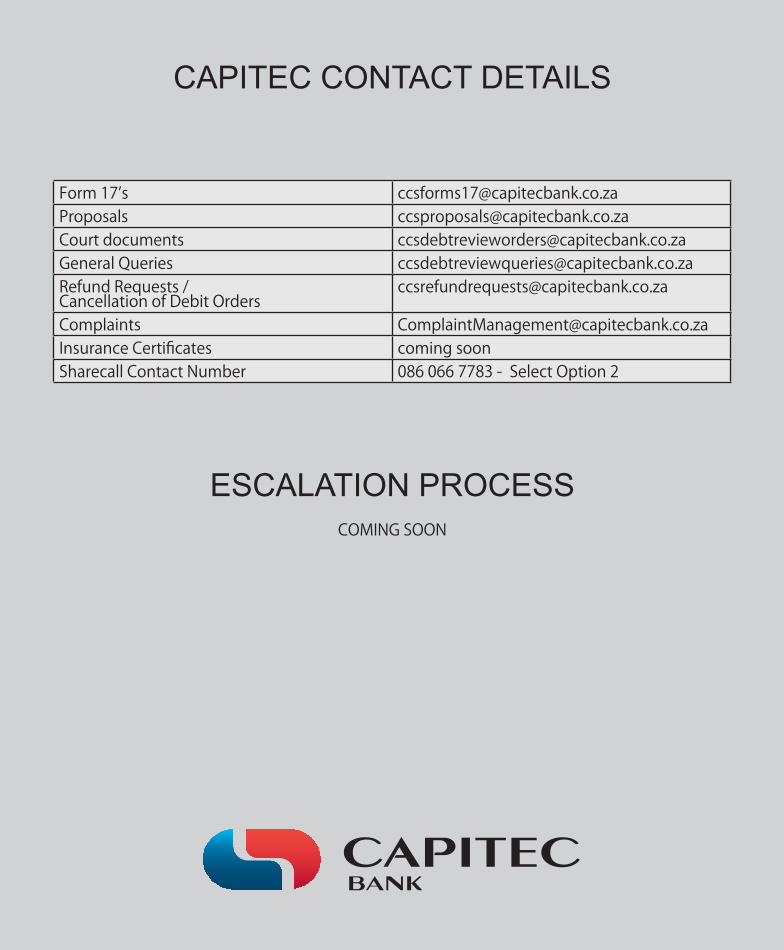

CAPITEC CONTACT DETAILS

Form 17’s [email protected] [email protected] documents [email protected] Queries [email protected] Requests / Cancellation of Debit Orders

Complaints [email protected] Certificates coming soonSharecall Contact Number 086 066 7783 - Select Option 2

ESCALATION PROCESSCOMING SOON

Debt Review DepartmentEmail Address Turnaround Time

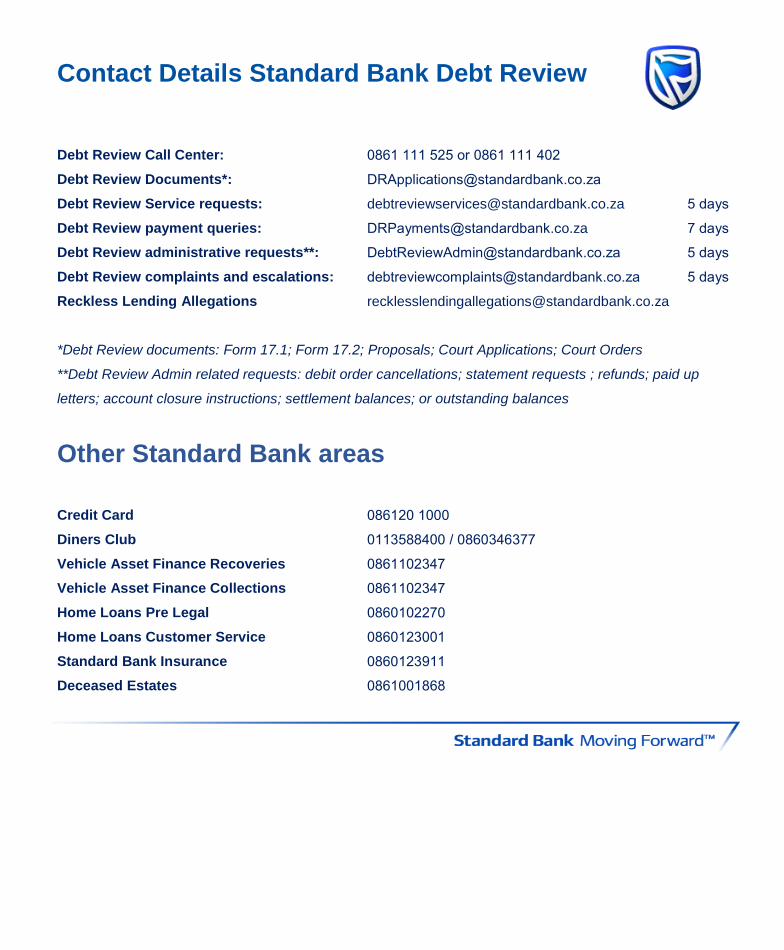

Contact Details Standard Bank Debt Review

Debt Review Call Center: 0861 111 525 or 0861 111 402

Debt Review Documents*: [email protected]

Debt Review Service requests: [email protected] 5 days

Debt Review payment queries: [email protected] 7 days

Debt Review administrative requests**: [email protected] 5 days

Debt Review complaints and escalations: [email protected] 5 days

Reckless Lending Allegations [email protected]

*Debt Review documents: Form 17.1; Form 17.2; Proposals; Court Applications; Court Orders

**Debt Review Admin related requests: debit order cancellations; statement requests ; refunds; paid up

letters; account closure instructions; settlement balances; or outstanding balances

Other Standard Bank areas

Credit Card 086120 1000

Diners Club 0113588400 / 0860346377

Vehicle Asset Finance Recoveries 0861102347

Vehicle Asset Finance Collections 0861102347

Home Loans Pre Legal 0860102270

Home Loans Customer Service 0860123001

Standard Bank Insurance 0860123911

Deceased Estates 0861001868

ABSA TASK SPECIFIC DEBT REVIEW ENTRY POINTS

ABSA TASK SPECIFIC DEBT REVIEW ENTRY POINTS

Form 17.1 [email protected]

Debit Order Cancellations [email protected]

Proposals [email protected]

Exits from Debt Review [email protected]

All Court Documents [email protected]

DC Switches [email protected]

Termination Queries [email protected]

Queries [email protected]

Escalated Queries [email protected]

Call Centre 0861 222 272

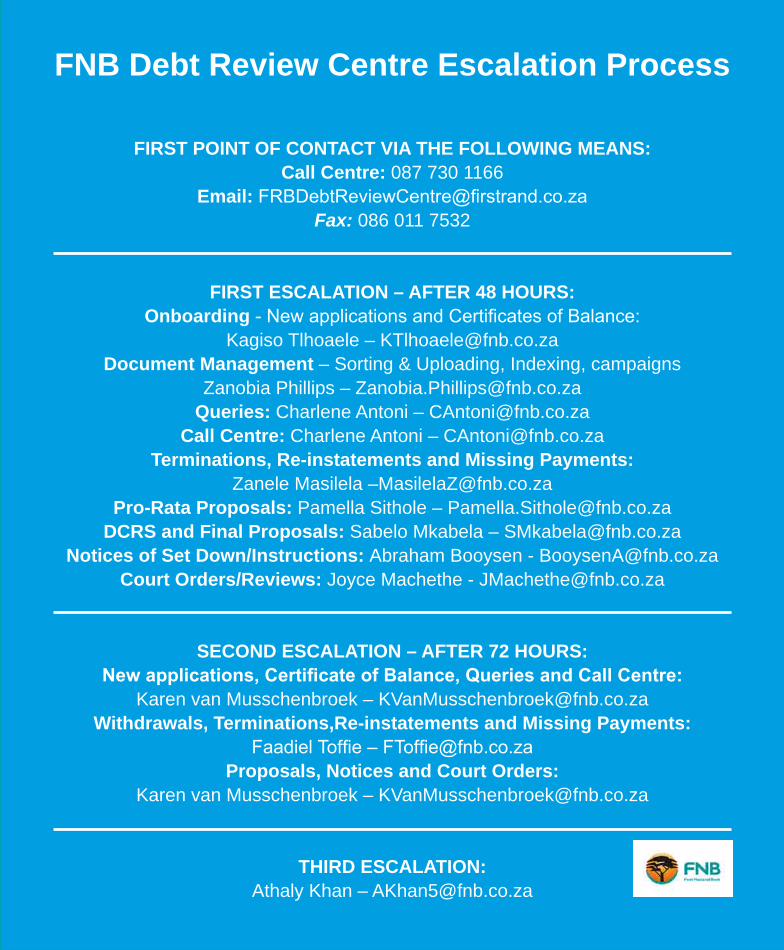

FIRST POINT OF CONTACT VIA THE FOLLOWING MEANS:Call Centre: 087 730 1166

Email: [email protected] Fax: 086 011 7532

FIRST ESCALATION – AFTER 48 HOURS:Onboarding - New applications and Certificates of Balance:

Kagiso Tlhoaele – [email protected] Management – Sorting & Uploading, Indexing, campaigns

Zanobia Phillips – [email protected]: Charlene Antoni – [email protected]

Call Centre: Charlene Antoni – [email protected], Re-instatements and Missing Payments:

Zanele Masilela –[email protected] Proposals: Pamella Sithole – [email protected]

DCRS and Final Proposals: Sabelo Mkabela – [email protected] of Set Down/Instructions: Abraham Booysen - [email protected]

Court Orders/Reviews: Joyce Machethe - [email protected]

SECOND ESCALATION – AFTER 72 HOURS:New applications, Certificate of Balance, Queries and Call Centre:

Karen van Musschenbroek – [email protected], Terminations,Re-instatements and Missing Payments:

Faadiel Toffie – [email protected], Notices and Court Orders:

Karen van Musschenbroek – [email protected]

THIRD ESCALATION:Athaly Khan – [email protected]

FNB Debt Review Centre Escalation Process

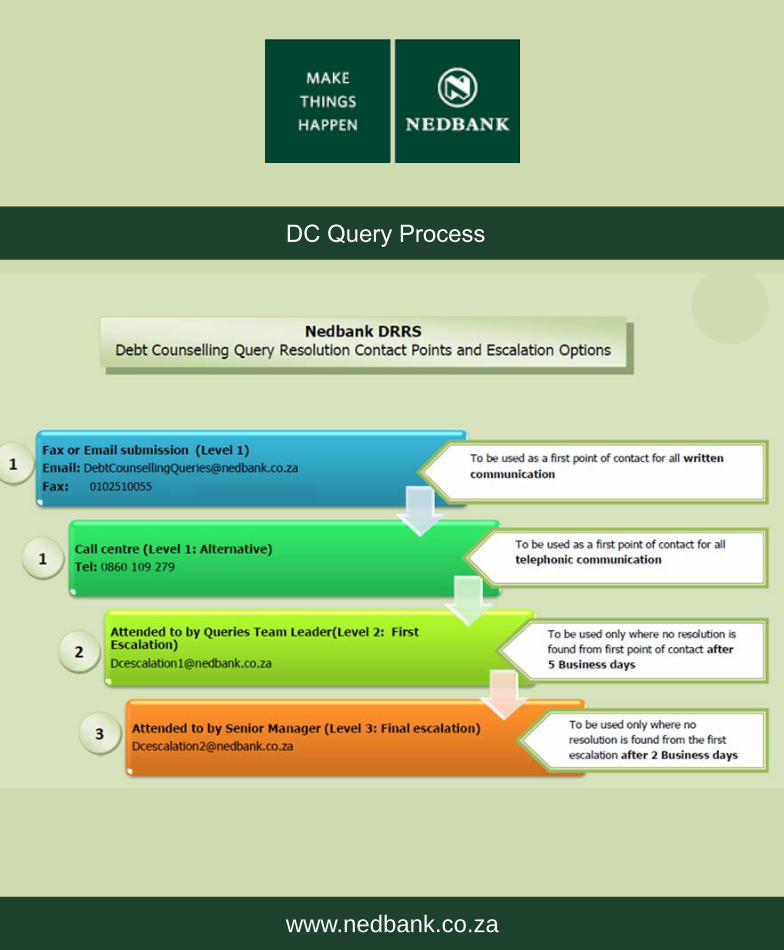

DC Query Process

www.nedbank.co.za

DC Query Process