Embed Size (px)

Citation preview

Debt Road Show Presentation

29 May 2014

- Howard Millar CFO & Deputy Chief Executive

- Neil Sorahan Finance Director

- John O’Flynn Treasury Manager

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

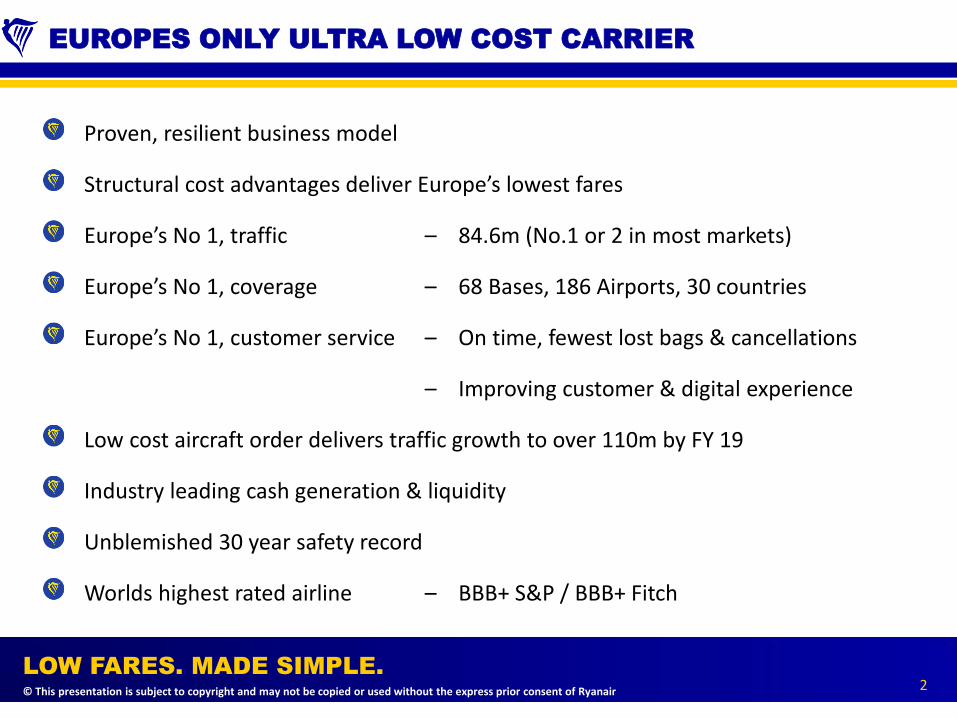

EUROPES ONLY ULTRA LOW COST CARRIER

2

Proven, resilient business model

Structural cost advantages deliver Europe’s lowest fares

Europe’s No 1, traffic – 84.6m (No.1 or 2 in most markets)

Europe’s No 1, coverage – 68 Bases, 186 Airports, 30 countries

Europe’s No 1, customer service – On time, fewest lost bags & cancellations

– Improving customer & digital experience

Low cost aircraft order delivers traffic growth to over 110m by FY 19

Industry leading cash generation & liquidity

Unblemished 30 year safety record

Worlds highest rated airline – BBB+ S&P / BBB+ Fitch

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

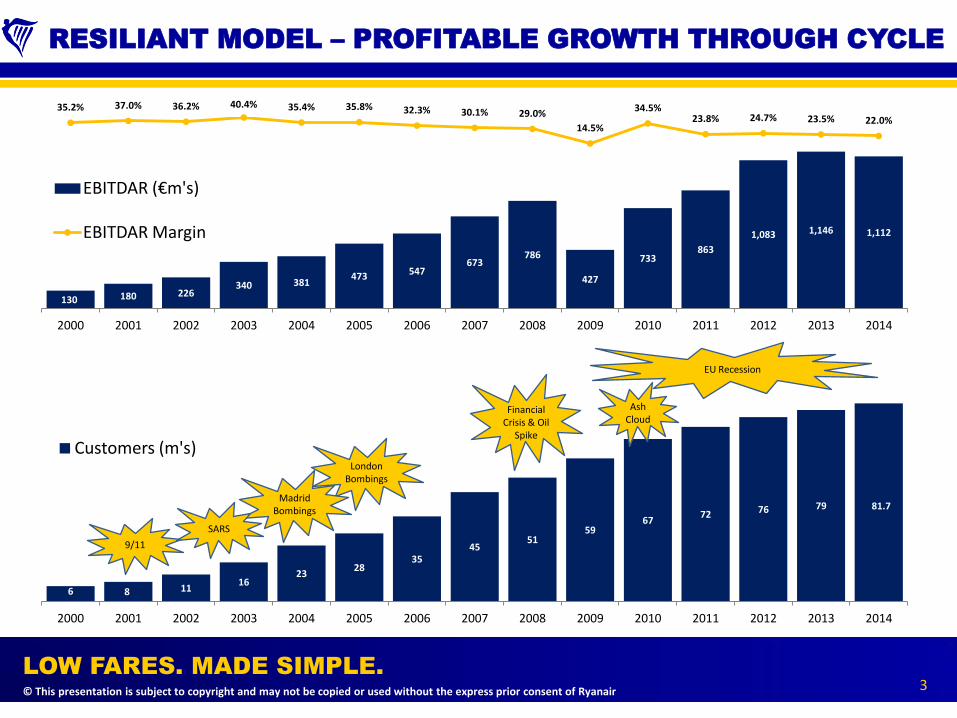

RESILIANT MODEL – PROFITABLE GROWTH THROUGH CYCLE

3

130 180 226 340 381

473 547 673

786

427

733 863

1,083 1,146 1,112

35.2% 37.0% 36.2% 40.4% 35.4% 35.8% 32.3% 30.1% 29.0%

14.5%

34.5% 23.8% 24.7% 23.5% 22.0%

-150.0%

-130.0%

-110.0%

-90.0%

-70.0%

-50.0%

-30.0%

-10.0%

10.0%

30.0%

0

200

400

600

800

1000

1200

1400

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

EBITDAR (€m's)

EBITDAR Margin

6 8 11 16

23 28

35 45

51 59

67 72 76 79

-

10

20

30

40

50

60

70

80

90

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Customers (m's)

EU Recession

London Bombings

Madrid Bombings 81.7

9/11

SARS

Financial Crisis & Oil

Spike

Ash Cloud

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

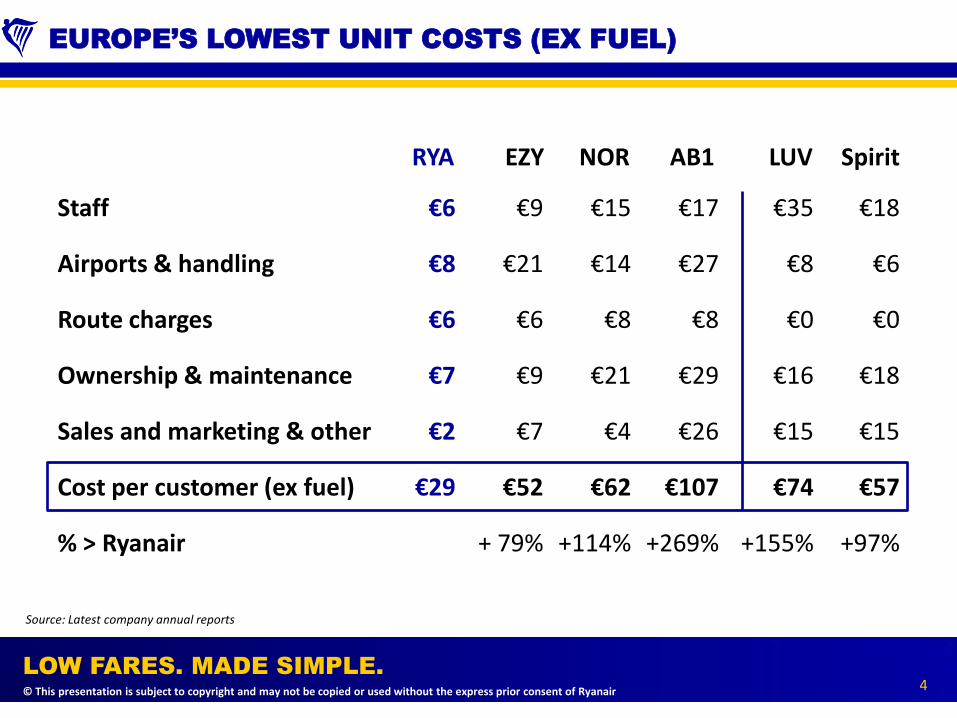

EUROPE’S LOWEST UNIT COSTS (EX FUEL)

4

Source: Latest company annual reports

RYA EZY NOR

Staff

Airports & handling

Route charges

Ownership & maintenance

Sales and marketing & other

Cost per customer (ex fuel)

% > Ryanair

€6

€8

€6

€7

€2

€29

€9

€21

€6

€9

€7

€52

+ 79%

€15

€14

€8

€21

€4

€62

+114%

€35

€8

€0

€16

€15

€74

+155%

LUV Spirit

€18

€6

€0

€18

€15

€57

+97%

€17

€27

€8

€29

€26

€107

+269%

AB1

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

EUROPE’S LOWEST FARES

5

LOW Ryanair

MEDIUM Norwegian

easyJet

Aer Lingus (s/h)

Air Berlin

HIGH Alitalia

Lufthansa

IAG

AF-KLM

+ 80%

+ 83%

+ 102%

+ 163%

+ 222%

+ 411%

+ 426%

+ 552%

% > Ryanair Avg. Fare

€46

€83

€84

€93

€121

€148

€235

€242

€300 Source: Latest company annual reports.

(-4%)

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

EUROPE’S NO.1 – TRAFFIC

6

52 54

61 62

81.7 84.6

89.0

96.0

104.0

112.0

50

60

70

80

90

100

110

Customers (m’s)

FY 2014

FY 2016 FY 2015 FY 2018 FY 2017 FY 2019

Ryanair Growth Projections Source: Latest traffic stats from company websites (inter European short haul only) for 12 mths to Mar14 .

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

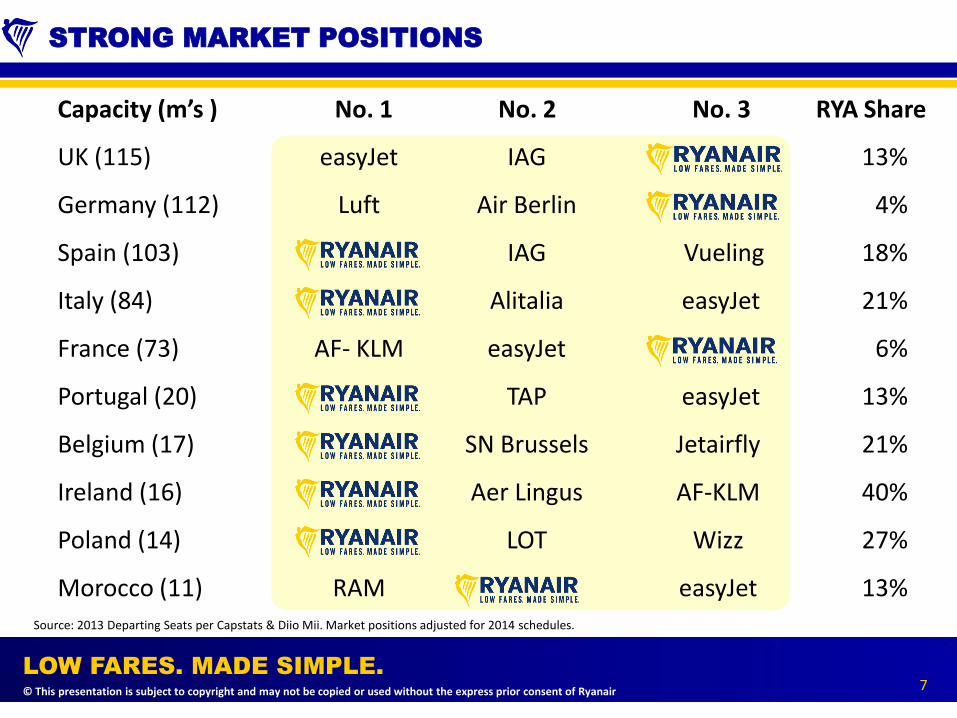

STRONG MARKET POSITIONS

7

UK (115)

Germany (112)

Spain (103)

Italy (84)

France (73)

Portugal (20)

Belgium (17)

Ireland (16)

Poland (14)

Morocco (11)

13%

4%

18%

21%

6%

13%

21%

40%

27%

13%

RYA Share

Source: 2013 Departing Seats per Capstats & Diio Mii. Market positions adjusted for 2014 schedules.

Capacity (m’s ) No. 1 No. 2

Vueling

easyJet

easyJet

Jetairfly

AF-KLM

Wizz

easyJet

No. 3

IAG

Air Berlin

IAG

Alitalia

easyJet

TAP

SN Brussels

Aer Lingus

LOT

easyJet

Luft

AF- KLM

RAM

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

8

EUROPE’S NO.1 – COVERAGE

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

CUSTOMER EXPERIENCE IMPROVING

9

RECAPTCHA scrapped for individuals – Oct 13

24hr grace period to correct minor booking errors – Nov 13

Quiet flights (early AM, late PM) – Nov 13

2nd free small carry on bag – Dec 13

Boarding card reissue & bag fees cut – Dec 13

New Groups & Corporate Travel Department – Jan 14

Allocated seating – Feb 14

Improving experience supported by T.V. advertising

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

DIGITAL EXPERIENCE IMPROVING

10

Simpler website (17 to 5 clicks) – Nov 13

“My Ryanair”, customer registration – Dec 13

New website including “Fare Finder” feature, great response – Mar 14

GDS partnership (Galileo/Worldspan platform) for business agents – April 14

New mobile app for smart phones & tablets – June 14

New family and business products in pipeline

Program of continuous IT & digital improvement underway

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

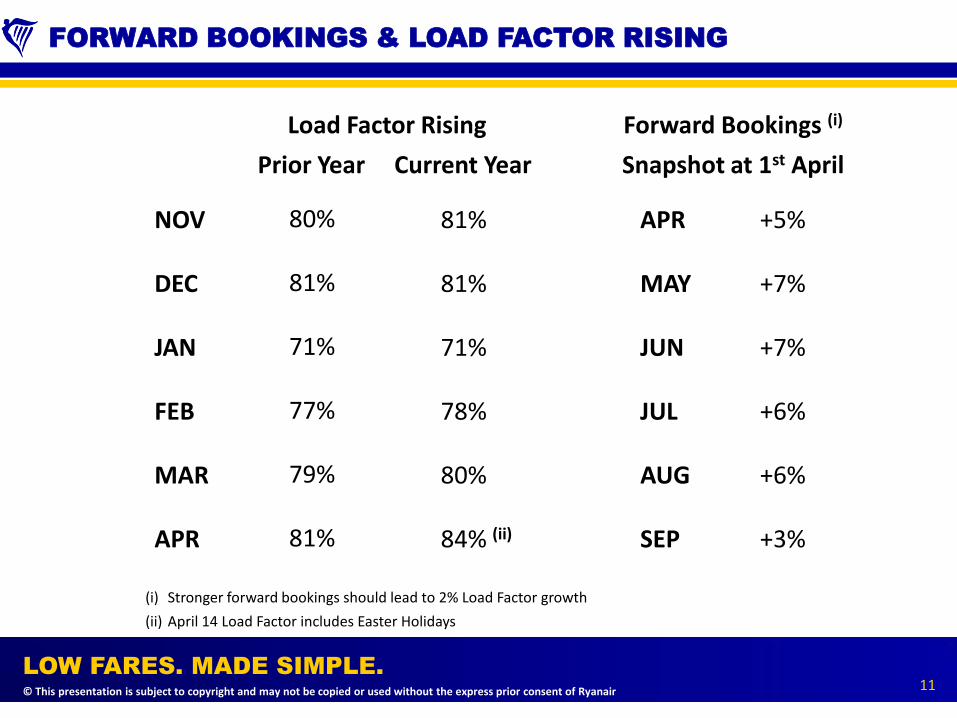

FORWARD BOOKINGS & LOAD FACTOR RISING

11

NOV

DEC

JAN

FEB

MAR

APR

Load Factor Rising

Prior Year Current Year

80%

81%

71%

77%

79%

81%

81%

81%

71%

78%

80%

84% (ii)

Snapshot at 1st April

APR

MAY

JUN

JUL

AUG

SEP

+5%

+7%

+7%

+6%

+6%

+3%

(ii) April 14 Load Factor includes Easter Holidays

(i) Stronger forward bookings should lead to 2% Load Factor growth

Forward Bookings (i)

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

LOW COST 180 AIRCRAFT ORDER

12

All Boeing 737-800NG aircraft

Maintains cost leadership and fleet commonality

USD pricing “not dissimilar” to previous 2005 order. EUR/USD rate better.

Provides passenger growth to c. 110m by FY19

Maintains young fleet – average age 5 years

EU flags restructuring - creates airport demand for Ryanair growth

25% of growth allocated to low cost London Stansted

Deals at Warsaw, Dublin, Lisbon, Brussels, Rome, Athens & Cologne

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

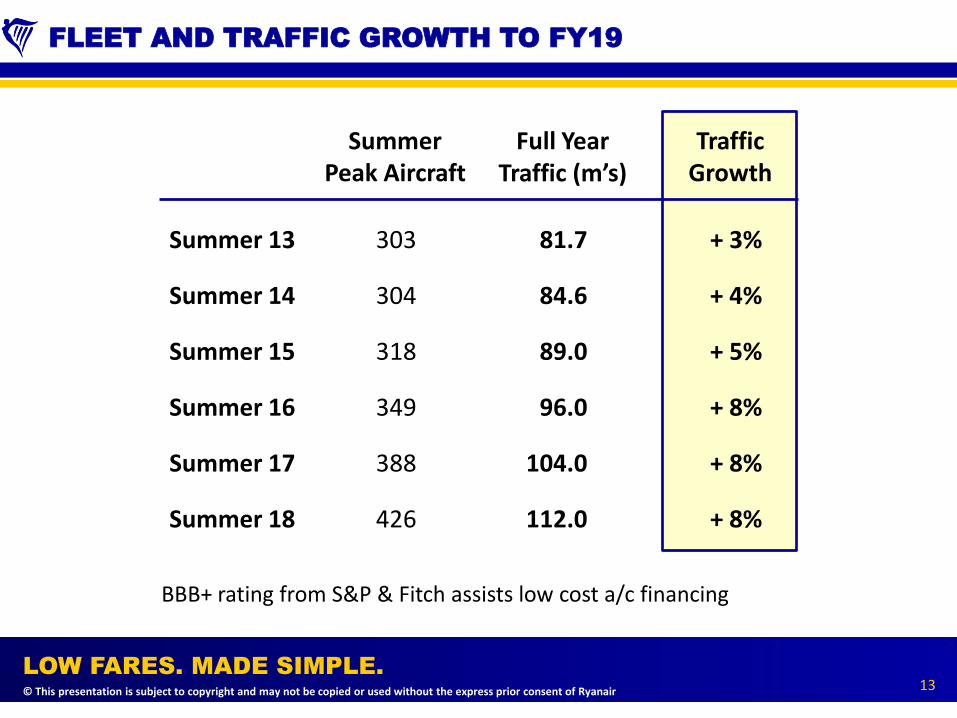

FLEET AND TRAFFIC GROWTH TO FY19

13

81.7

84.6

89.0

96.0

104.0

112.0

Summer 13

Summer 14

Summer 15

Summer 16

Summer 17

Summer 18

303

304

318

349

388

426

+ 3%

+ 4%

+ 5%

+ 8%

+ 8%

+ 8%

Summer Peak Aircraft

Full Year Traffic (m’s)

Traffic Growth

BBB+ rating from S&P & Fitch assists low cost a/c financing

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

FULL YEAR RESULTS

14

Traffic

Load Factor

Average Fare (includes bag)

Revenue Per Passenger

Revenue

Profit after Tax

79.3m

82%

€48

€62

€4,884m

€569m

Mar 13

Mar 14

81.7m

83%

€46

€62

€5,037m

€523m

+3%

+1%

-4%

0%

+3%

-8%

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

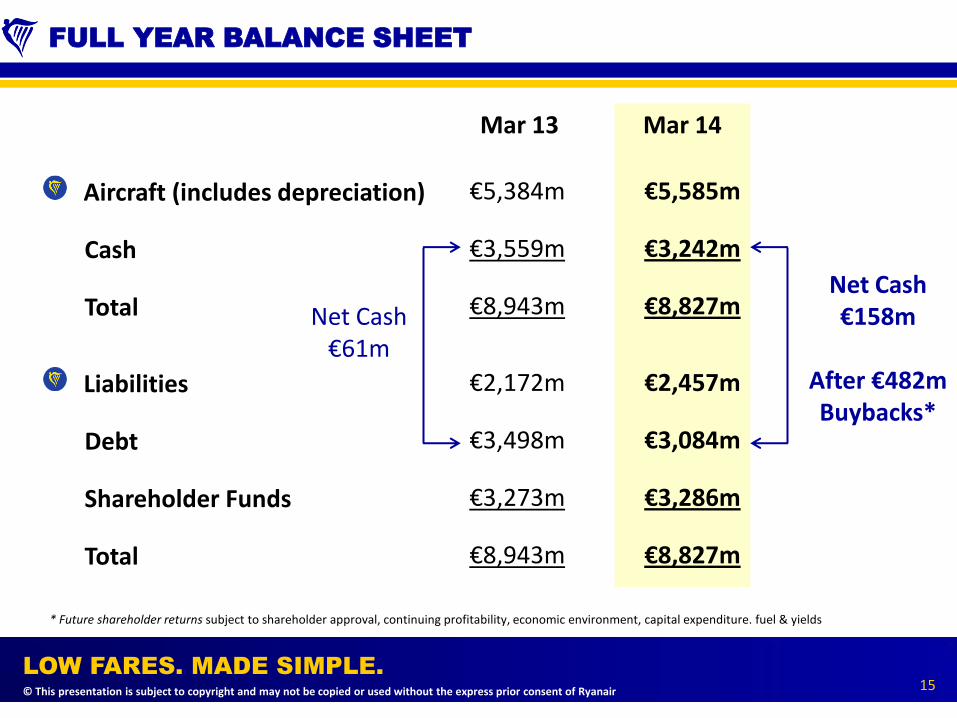

FULL YEAR BALANCE SHEET

15

Aircraft (includes depreciation)

Cash

Total

Liabilities

Debt

Shareholder Funds

Total

€5,384m

€3,559m

€8,943m

€2,172m

€3,498m

€3,273m

€8,943m

Mar 13

€5,585m

€3,242m

€8,827m

€2,457m

€3,084m

€3,286m

€8,827m

Mar 14

Net Cash €61m

Net Cash €158m

After €482m Buybacks*

* Future shareholder returns subject to shareholder approval, continuing profitability, economic environment, capital expenditure. fuel & yields

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

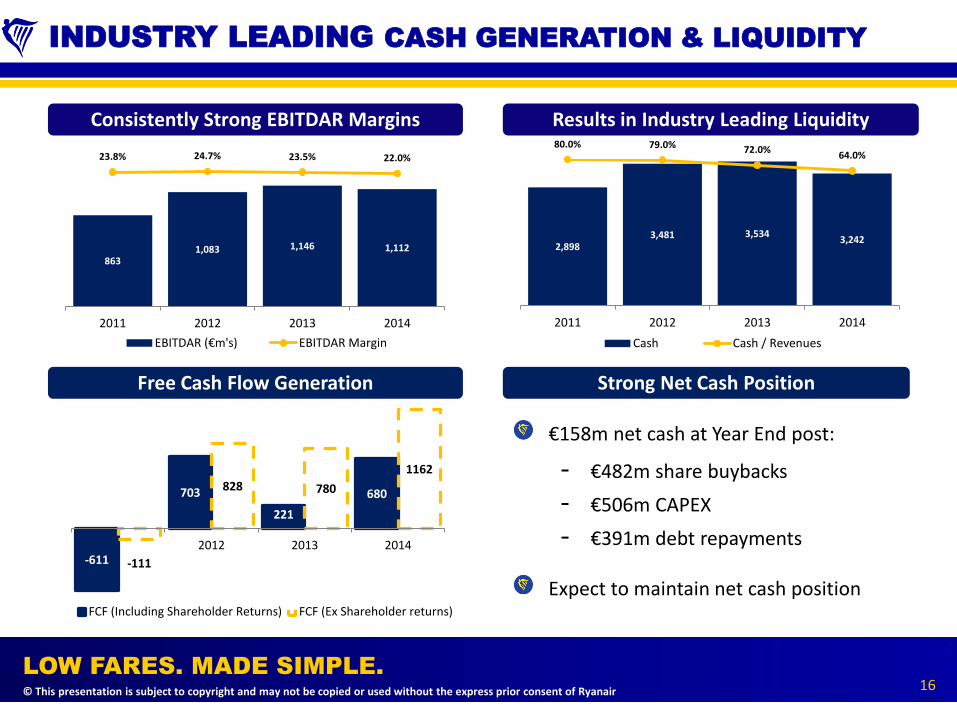

INDUSTRY LEADING CASH GENERATION & LIQUIDITY

16

Free Cash Flow Generation

Results in Industry Leading Liquidity Consistently Strong EBITDAR Margins

863 1,083 1,146 1,112

23.8% 24.7% 23.5% 22.0%

-150.0% -130.0% -110.0% -90.0% -70.0% -50.0% -30.0% -10.0% 10.0% 30.0%

0

200

400

600

800

1000

1200

1400

2011 2012 2013 2014

EBITDAR (€m's) EBITDAR Margin

2,898 3,481 3,534

3,242

80.0% 79.0% 72.0% 64.0%

-150.0%

-100.0%

-50.0%

0.0%

50.0%

-400

100

600

1100

1600

2100

2600

3100

3600

2011 2012 2013 2014

Cash Cash / Revenues

€158m net cash at Year End post:

- €482m share buybacks

- €506m CAPEX

- €391m debt repayments

Expect to maintain net cash position

Strong Net Cash Position

-611

703

221

680

-111

828 780

1162

2012 2013 2014

FCF (Including Shareholder Returns) FCF (Ex Shareholder returns)

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

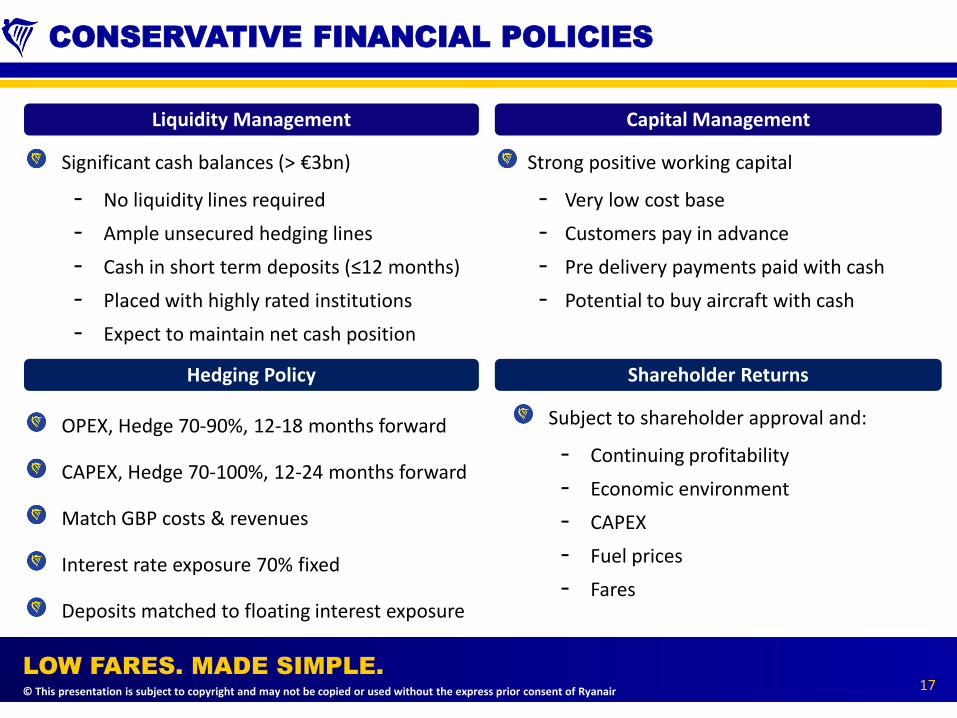

CONSERVATIVE FINANCIAL POLICIES

17

Hedging Policy

Capital Management Liquidity Management

Shareholder Returns

Subject to shareholder approval and:

- Continuing profitability

- Economic environment

- CAPEX

- Fuel prices

- Fares

Strong positive working capital

- Very low cost base

- Customers pay in advance

- Pre delivery payments paid with cash

- Potential to buy aircraft with cash

Significant cash balances (> €3bn)

- No liquidity lines required

- Ample unsecured hedging lines

- Cash in short term deposits (≤12 months)

- Placed with highly rated institutions

- Expect to maintain net cash position

OPEX, Hedge 70-90%, 12-18 months forward

CAPEX, Hedge 70-100%, 12-24 months forward

Match GBP costs & revenues

Interest rate exposure 70% fixed

Deposits matched to floating interest exposure

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

WORLDS HIGHEST RATED AIRLINE

18

BBB+ corporate rating from S&P & Fitch

– Worlds highest rated airline

– Stable outlooks

– “a-” anchor (S&P), notched due to possible CAPEX & shareholder returns

– Industry leading liquidity, cost base & cash generation

– BBB+ note rating expected

Ratings provide direct access to competitive capital markets funding

Scalable source of Euro unsecured debt + EETC financing

Supplements existing financing options, Ex-Im available as low cost backstop

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

DEBUT ISSUANCE – TERMS AND CONDITIONS

19

Issuer Ryanair Limited

Guarantor Ryanair Holdings PLC

Issuer Ratings BBB+/BBB+

Expected Note Rating BBB+/BBB+

Status Senior, unsecured

Currency EUR

Tenor 7 years

Size Benchmark

Use of Proceeds GCP

Denomination €100K + €1k

Governing Law English

Listing Dublin

Covenants Change of Control, Negative Pledge, Cross Default

Documentation Ryanair Limited EUR3bn EMTN Programme

Global Co-ordinator Citi

Bookrunners BNP Paribas, Citi, Deutsche Bank

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

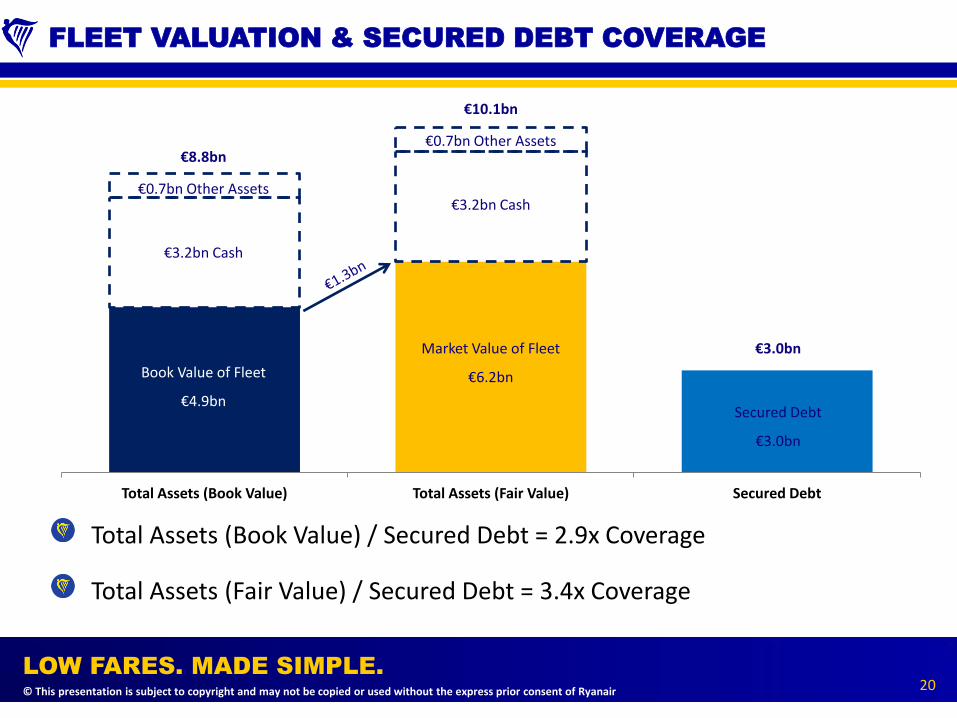

Total Assets (Book Value) Total Assets (Fair Value) Secured Debt

FLEET VALUATION & SECURED DEBT COVERAGE

20

Total Assets (Book Value) / Secured Debt = 2.9x Coverage

Total Assets (Fair Value) / Secured Debt = 3.4x Coverage

€0.7bn Other Assets

€3.2bn Cash

Market Value of Fleet

€6.2bn

Secured Debt

€3.0bn

Book Value of Fleet

€4.9bn

€0.7bn Other Assets

€3.2bn Cash

€8.8bn

€10.1bn

€3.0bn

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

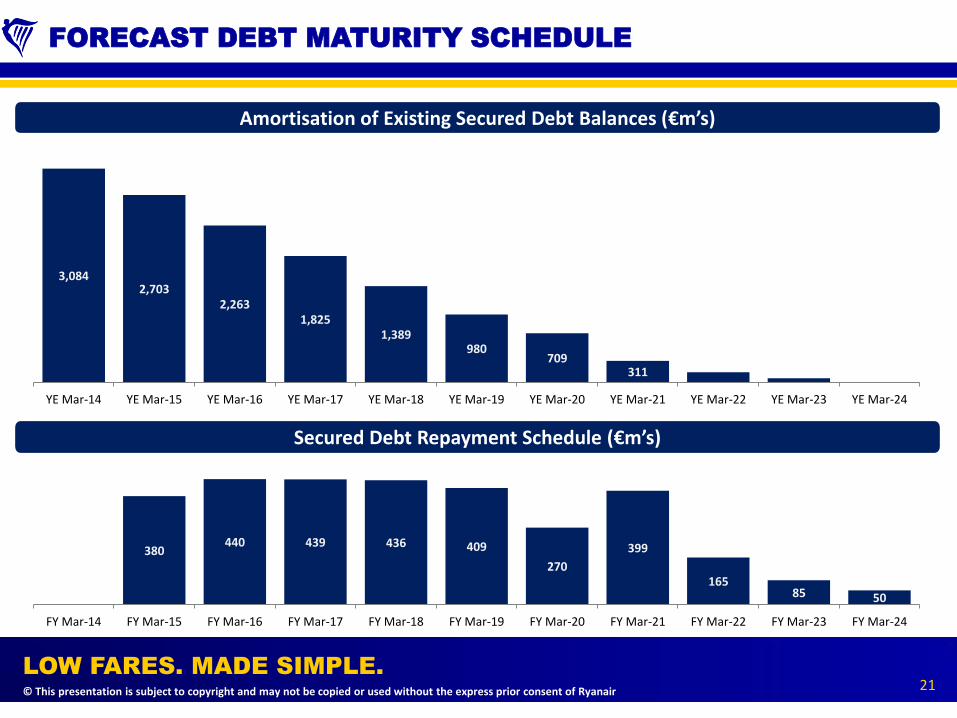

FORECAST DEBT MATURITY SCHEDULE

21

Secured Debt Repayment Schedule (€m’s)

Amortisation of Existing Secured Debt Balances (€m’s)

3,084 2,703

2,263 1,825

1,389 980

709 311

YE Mar-14 YE Mar-15 YE Mar-16 YE Mar-17 YE Mar-18 YE Mar-19 YE Mar-20 YE Mar-21 YE Mar-22 YE Mar-23 YE Mar-24

380 440 439 436 409

270

399

165 85 50

FY Mar-14 FY Mar-15 FY Mar-16 FY Mar-17 FY Mar-18 FY Mar-19 FY Mar-20 FY Mar-21 FY Mar-22 FY Mar-23 FY Mar-24

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

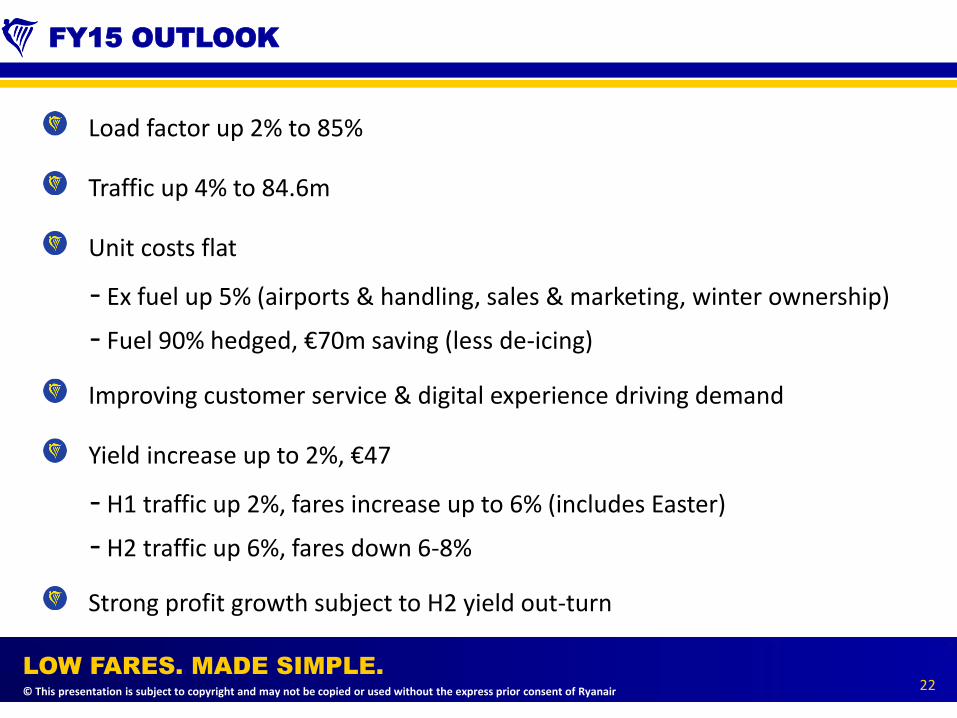

FY15 OUTLOOK

22

Load factor up 2% to 85%

Traffic up 4% to 84.6m

Unit costs flat

- Ex fuel up 5% (airports & handling, sales & marketing, winter ownership)

- Fuel 90% hedged, €70m saving (less de-icing)

Improving customer service & digital experience driving demand

Yield increase up to 2%, €47

- H1 traffic up 2%, fares increase up to 6% (includes Easter)

- H2 traffic up 6%, fares down 6-8%

Strong profit growth subject to H2 yield out-turn

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

SUMMARY

23

Proven, resilient business model – unique structural cost advantages

Lowest costs and fares in Europe

Industry leading liquidity and cash generation

No 1 or 2 share in major EU markets

Fwd bookings & load factors ahead of 2013

Worlds highest rated airline

– Provides access to low cost capital markets to fund 180 new aircraft

“Always getting better” delivers for customers, people & stakeholders

Appendices

19 May 2014

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

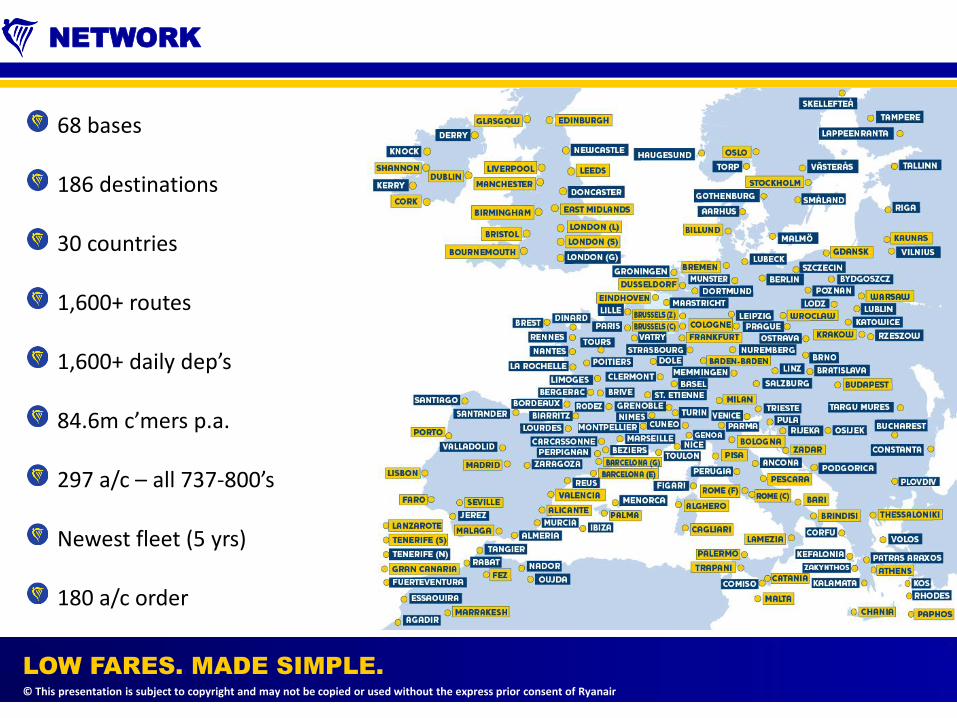

NETWORK

68 bases

186 destinations

30 countries

1,600+ routes

1,600+ daily dep’s

84.6m c’mers p.a.

297 a/c – all 737-800’s

Newest fleet (5 yrs)

180 a/c order

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

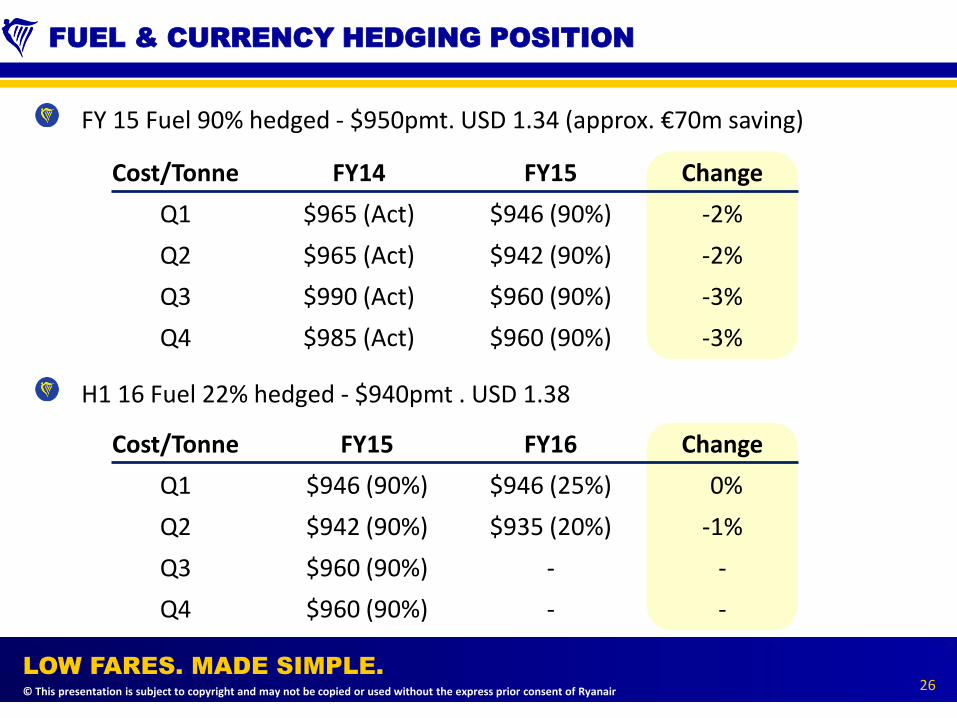

FUEL & CURRENCY HEDGING POSITION

26

FY 15 Fuel 90% hedged - $950pmt. USD 1.34 (approx. €70m saving)

H1 16 Fuel 22% hedged - $940pmt . USD 1.38

Cost/Tonne

Q1

Q2

Q3

Q4

FY14

$965 (Act)

$965 (Act)

$990 (Act)

$985 (Act)

FY15

$946 (90%)

$942 (90%)

$960 (90%)

$960 (90%)

Change

-2%

-2%

-3%

-3%

Cost/Tonne

Q1

Q2

Q3

Q4

FY16

$946 (25%)

$935 (20%)

-

-

Change

0%

-1%

-

-

FY15

$946 (90%)

$942 (90%)

$960 (90%)

$960 (90%)

© This presentation is subject to copyright and may not be copied or used without the express prior consent of Ryanair

LOW FARES. MADE SIMPLE.

DISCLAIMER

THIS PRESENTATION IS NOT AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL SECURITIES. IT IS SOLELY FOR USE AT AN INVESTOR PRESENTATION AND IS PROVIDED AS INFORMATION ONLY. THIS PRESENTATION DOES NOT CONTAIN ALL OF THE INFORMATION THAT IS MATERIAL TO AN INVESTOR. BY ATTENDING THE PRESENTATION OR BY READING THE PRESENTATION SLIDES YOU AGREE TO BE BOUND AS FOLLOWS:

This presentation is strictly confidential to the recipient, is being distributed to a limited range of invited persons solely for their own information, may not be distributed to the press or any other person, and may not be reproduced or published, in whole or in part, in any form. Failure to comply with this restriction may constitute a violation of applicable securities laws.

This document is not a prospectus for any securities. Investors should only subscribe for any securities on the basis of information in a relevant prospectus and term sheet, and not on the basis of any information provided herein.

This presentation has been prepared by Ryanair Limited (the “Company”) and may be amended and supplemented and may not be relied upon for the purposes of entering into any transaction. The information contained herein has been obtained from sources believed to be reliable. Although the Company has taken all reasonable care to ensure that the information herein is accurate and correct, no representation, warranty or undertaking, express or implied, is given by or on behalf of the Company or any of its directors, officers, employees, shareholders, affiliates, agents, advisers, other representatives (collectively, "Representatives") or any other person as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or the opinions contained herein or any other material discussed at the presentation. Neither the Company nor any Representatives nor any other person shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this presentation or any other material discussed at the presentation or their contents or otherwise arising in connection with the presentation. The views reflected herein are solely those of the Company and are subject to change without notice. All estimates, projections, valuations and statistical analyses are provided to assist the recipient in the evaluation of the matters described herein and may be based on subjective assessments and assumptions and may use one among alternative methodologies that produce different results, and to the extent that they are based on historical information, they should not be relied upon as an accurate prediction of future performance. Certain analysis is presented herein and is intended solely for purposes of indicating a range of outcomes that may result from changes in market parameters. It is not intended to suggest that any outcome is more likely than another, and it does not include all possible outcomes or the range of possible outcomes, one of which may be that the investment value declines to zero.

This presentation may include forward-looking statements that reflect the Company’s intentions, beliefs or current expectations. Forward-looking statements involve all matters that are not historical by using the words “may”, “will”, “would”, “should”, “expect”, “intend”, “estimate”, “anticipate”, “target”, “believe” and similar expressions or their negatives. Such statements are made on the basis of assumptions and expectations that the Company currently believes are reasonable, but could prove to be wrong. Any forward-looking statements made by or on behalf of the Company speak only as at the date of this presentation. Save as required by any applicable laws or regulations, the Company undertakes no obligation publicly to release the results of any revisions to any forward-looking statements in this document that may occur due to any change in its expectations or to reflect events or circumstances after the date of this document.

No action has been taken or will be taken that would permit a public offering of any securities in any jurisdiction in which action for that purpose is required. No offers, sales, resales or delivery of any securities or distribution of any offering material relating to any such securities may be made in or from any jurisdiction except in circumstances which will result in compliance with any applicable laws and regulations.

This presentation is for the recipient’s use only. This presentation is not for distribution to retail clients. In particular , neither this presentation nor any copy hereof may be sent or taken or distributed in the United States or to any U.S. person (as such term is defined in Regulation S under the U.S. Securities Act 1933, as amended (the “Securities Act”)), except pursuant to an exemption from the registration requirements of the Securities Act. This presentation, if handed out at a physical investor meeting or presentation, should be returned promptly at the end of such meeting or presentation. If this presentation has been received in error it must be returned immediately to the Company. Accordingly, this presentation is being provided only to persons that are (i)“qualified institutional buyers” within the meaning of Rule 144A under the Securities Act or (ii) not “U.S. persons” within the meaning of Regulation S under the Securities Act. By accepting the delivery of this presentation, the recipient warrants and acknowledges that it falls within the category of persons under clause (i) or (ii). No representation can be made as to the availability of the exemption provided by Rule 144 for re-sales of any securities offered by or guaranteed by the Company. No securities offered by or guaranteed by the Company have been recommended by, or approved by, the United States Securities and Exchange Commission or any other United States federal or state securities commission or regulatory authority, nor has any such commission or regulatory authority passed upon the accuracy or adequacy of this presentation.

This presentation is being communicated only to (i) persons who have professional experience in matters relating to investments falling within Article 19(5) of The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”), or (ii) high net worth entities, and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order (all such persons together being referred to as “relevant persons”). This presentation is communicated only to relevant persons and must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this presentation relates is available only to relevant persons and will be engaged in only with relevant persons. By attending the presentation to which this document relates or by accepting this document you will be taken to have represented, warranted and undertaken that (i) you are a relevant person (as defined above); (ii) you have read and agree to comply with the contents of this notice; and (iii) you will treat and safeguard as strictly private and confidential all such information and take all reasonable steps to preserve such confidentiality.

This presentation does not constitute an offer or an agreement, or a solicitation of an offer or an agreement, to enter into any transaction (including for the provision of any services). No assurance is given that any such transaction can or will be arranged or agreed. Before entering into any transaction, you should consider the suitability of the transaction to your particular circumstances and independently review (with your professional advisers as necessary) the specific financial risks as well as the legal, regulatory, credit, tax and accounting consequences. This document does not disclose all the risks and other significant issues related to an investment in any securities/transaction. Prior to transacting, potential investors should ensure that they fully understand the terms of any securities/transaction and any applicable risks.