-

8/3/2019 Debt Report

1/5

DEBT

CAPITAL MARKETSFINANCIAL TIMES SPECIAL REPORT | Friday November

19 2010

www.ft.com/debt capital markets 2010 | twitter.com/ftre

-

8/3/2019 Debt Report

2/5

2 FINANCIAL TIMES FRIDAY NOVEMBER 19 2010 FINANCIAL TIMES FRIDAY

NOVEMBER 19 2010

Contributors

Jennifer HughesSenior MarketsCorrespondent

Richard MilneCapital Markets Editor

David OakleyCapital MarketsCorrespondent

Anousha SakouiCapital Markets Reporter

Lindsay WhippTokyo Correspondent

Nicole BullockCapital Markets Reporter

Michael MacKenzieUS MarketsCorrespondent

Patrick StilesCommissioning Editor

Steven Bird

Designer

Andy MearsPicture Editor

For advertising, contact:Ceri Williams on:tel: +44 (0)20 7873

6321fax: +44 (0)20 7873 4296e mail:[email protected]

All editorial content in thissupplement is producedby the

FT.

In This Issue

Investors ready to accept more riskRETURNS Richard Milne

considers what theoptions are for those who want more yield ina low

interest rate environment Page 3

Mergers and acquisitions limber upDEALMAKING A return to

corporate activitycreates the risk of releveraging forbondholders,

writes Anousha Sakoui Page 4

Samurai bonds make a comebackJAPAN Issuance of yen denominated

paperby foreign institutions has returned to itsformer volume,

despite the absence of USinvestment banks from the market Page

6

Banks explore innovative structuresCONTINGENT CAPITAL Regulators

are seekingnew ways of protecting taxpayers frombail outs in the

case of institutions failing,

reports Jennifer Hughes Page 7

Greece transforms government debtSOVEREIGN CREDIT

Investors approachto risk hasundergone asignificant shiftsince

Athensrevealed inSeptember2009 thatits financeswere in evenworse

shape thanreported, writesDavid Oakley Page 7

Debt Capital Markets Debt Cap

Sectorbracedforvolatility

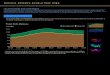

Risk taking rises, as thesearch for yield goes on

This pa s t ye a r fo rinvestors in capitalm a rk et s c a n b

esummed up in one

phrase: the search for yield.With the perceived risk-

free rates offered by US, UKo r G e rma n g o vernmentbonds at

or close to recordlows, investors wantingdecent returns have had

togo elsewhere to find yield.

That in turn has sent theinterest rates for emergingmarkets and

the lowest-rated companies lower andlower.

Yield is becoming a veryscarce commodity, saysJohan Jooste, a

strategist atMerrill Lynch Wealth Man-agement. Gary Jenkins,he ad o

f fixe d inco me a tEvolution Securities, adds: Eithe r w e a re g

o ing t o

have to get used to lowerreturns or people are goingto have to

take more risk.

So far, it looks like mostinvestors are plumping forthe latter

option and head-ing into the riskier parts ofthe debt markets.

Total returns for the risk-iest companies, those ratedCCC by

rating agencies,have totalled 16 per centthis year, compared with

just 7 pe r ce nt fo r t hesafest AAA-rated compa-nies, according

to Citi.

The big question is howda nge rous t his hunt fo ryield is. For

some investors,t he w e a k s t a t e o f mo stwestern economies

justifies

a focus on credit. AbdullahSheikh, director of researchat

JPMorgans strategicinvestment advisory group,says: Asset classes

thatmay well outperform duringperiods of anaemic growthand

moderately low infla-tion seem to be, while notobvious, those in

the fixed-income universe.

Anot he r a rgume nt infa vo ur o f t he s e a rch fo ryield is

that while absoluteinterest rates paid by high-

yield companies or emerg-ing markets are low, thes prea ds t he

diffe rencebetween the yields and therisk-free rate of US

Treasur-ies are in line with histori-cal averages.

T he pro blem fo r ma ny

asset managers is that thereturn targets they use toattract

investors are stillmostly absolute rather thanrelative ones. Thus,

manyfunds still have 6-8 per centtargets, although that nowimplie s

a much hig he rreturn relative to govern-ment debt.

Mr Sheikh says the prob-lem of too high return tar-gets is front

and centre inpeoples minds. Potentially,we are in a new

paradigmwhere the passive 8 per centnumber is too high.

T he he ad o f o ne o f t heworlds largest insurers,and by

extension one of thebiggest investors, says theresult is panic, as

investorstry to ignore the implica-tions of their targets.

This person says: Assetmanagers are panicking,absolutely

panicking. Themargin for error is gone.Before, you could make afew

errors and still earn 8per cent. Now, if you make

an error you are below thebenchmark, and the bench-mark today is

zero.

That is where the biggestworries come from. Inves-tors are now

chasing lowera n d l o we r y i el d s. T h eEMBI+ emerging

marketindex reached 2.31 percent-age points over US Treasur-ies in

early November, com-pa re d w ith 9 pe rce nt ag epoints 18 months

ago.

It is far from certain thatall investors are comforta-ble with

what they are buy-ing. A leading emerging-markets banker says: It

isunsustainable. They arebuying things that they tellyo u t he y do

nt like . W eca nt hit re cords e verymonth for yields or

flows.

Rod Davidson, head offixed income at AllianceTrust Asset

Management, issteering clear of high-yield.He says: We think at

themoment that the additionalyield isnt sufficient for

theadditional volatility you

take on.Still, the alternatives for

inves t ors a re s lim in aworld of uncertainty. MrSheikh

highlights the per-sistent reluctance of manyinvestors to buy

equities.With a double-dip recessiona t t he mo me nt lo o king

relatively unlikely, bond-holders are taking comfortfrom low levels

of companydefaults.

Some, however, are start-ing to think about what to

ho ld w he n t he hunt fo ryield comes to an end.

Ha ns Lo renz en, creditstrategist at Citi, says: Thereach for

yield in 2011 maybe inevitable, but, at theselofty levels, think

twiceabout what you choose to

hold on to its a long waydown.

Or, as Mr Jooste says, beaware of who is holding therisk in this

search-for-yieldenvironment: It is verymuch an issuers market,not

an investors one.

Returns

Richard Milne

considers investorsoptions in a

low interest rateenvironment

but t his co uld a lso be atrend for coming year.

Mr Marks adds: This is

not only an ongoing moveby companies away fromrelying on bank

financing,but also a sustained interestfrom inves t ors w ho a

remindful of pressures onpublic finances in severalEuropean

jurisdictions.

That said, the ultra-lowinterest rate environmenthas produced

record lowcorporate borrowing costsfor the largest companies.

Recently Walmart, the USsupermarket group, issued$750m t hree

-yea r bo ndswith a coupon of 0.75 percent and five-year notes

at1.5 per cent. Colgate-Palmo-live soon beat that; its five-year

notes offered an inter-est rate of 1.375 per cent.

Low-coupon notes thoseoffering less than 5 per cent are now

making up morethan half of issuance. In thethird quarter, before

theFederal Reserve announcedits new $600bn bond-buyingprogramme,

low-couponbonds made up 57 per cent

of those issued the highestpe rce nt ag e o n a re cordg o ing

ba ck t o 1970, s a idThomson Reuters.

Low coupons among themore established householdnames have led to

a returnto one of the bond marketsfa vourit e t he me s : t

hesearch for yield.

Emerging markets andhigh-yield bonds saw recordissuance in the

third quar-ter. For the year to date,issuance in the two

sectorsstood at $514bn and $221bnrespectively also a

record,according to Thomson Reu-ters.

At its more extreme, theyield search has encouragedissuers to

offer ultra-long-dated bonds, including a$350m 100-year, or

cen-tury deal from Rabobank,the Dutch mutual and, inthe biggest

century, $1bnfrom the Mexican govern-ment.

Pension funds and otherswith long-dated liabilities

have gobbled up the deals,which the cynics have nick-na med t he

s ome body-elses-problem bond.

Low yields have not beenenough to resuscitate thesecuritisation

market, how-e ver. W hile is s ua nce o f ultra-safe covered

bondshas reached record levels,t he re g ula r ma rket ha semerged

from its frozen cri-sis state only very slowly,leaving the market

as some-thing bank treasurers can

tap occasionally for fund-ing, but not one they canyet rely

on.

For bank treasuries ingeneral, it has been a trickyyear and the

outlook is notmuch cle a rer. A virtua lfreeze in the European

mar-ket for senior unsecureddebt the bread-and-butterof a banks

borrowing plans in May and June was anuncomfortable reminderthat

conditions are still far

from their pre-crisis norms.Ba nk e xecut ive s ha ve

also been wrestling withregulators plans to reformthe role of

debt, notablyhybrid bonds.

Policymakers have madeit clear bondholders will beexpected to

share in thepain in an effort to ease theburden on the taxpayer

andto encourage investors tobetter price the risks theytake.

But how best to do this?

Ideas include contingentcapital, improved subordi-nated bonds

that convert toequity when a pre-definedt rigg e r is bre ache d, o

rbail-in, the notion that allbondholders, including sen-ior

noteholders, could beforced into losses by regula-

tors if a bank needed to berecapitalised.

Recently, Swiss regula-tors backed contingent capi-tal, commonly

known asCo cos , ca lling o n Cre ditSuisse and UBS to raise

bil-lions in contingent capitalto provide a buffer. Other

regulators are waiting forguidance from the Baselco mmit t ee o

f ba nking supervisors, which is study-ing the issue.

Whichever way it goes and the two solutions arenot mutually

exclusive bankers are expecting as lew o f hybrids in s o meform

next year.

Banks are becoming avery positive credit storyrig ht no w if yo

u t hink

a bout it , s a id S a nde e pAgarwal, head of Europeanfinancial

institutions debtcapital markets at CreditSuisse.

He adds: All the regula-tory focus on equity andcapital means

anyone in thedebt structure should feelsafer. They dont, becauseof

recent history; but thats just what it is history, notw it hs t

anding t he ris ksposed by sovereign issuescurrently in the

market.

Banks arebecoming a very

positive credit storyright now if youthink about it

Capital buffer: Swiss regulators have called on UBS to raise

billions in Cocos Bloomberg

Continued from Page 1

Either we are goingto have to get usedto lower returns orpeople

are goingto have to takemore risk

Slim pickings: alternatives fo

FRONT PAGE ILLUSTRATION Ian Dodds

-

8/3/2019 Debt Report

3/5

4 FINANCIAL TIMES FRIDAYNOVEMBER 19 2010 FINANCIAL TIMES FRIDAY

NOVEMBER 19 2010

Debt Capital Markets Debt Cap

Fed seeks wealth effect with bout of QE2For some time, buyers of

USg o vernment bo nds ha vedebated whether low yieldsare

symptomatic of a nascentbubble. Now, with the Fed-e ral R e se rve

buying mo reTreasuries, key benchmarkyields have hit record lowsa n

d a r e s et f o r f u r t he rdeclines.

Under t he Fe ds s e co ndround of quantitative easing,dubbed

QE2, the central bankwill buy $600bn of Treasury

de bt until t he e nd o f ne xtJune. That buying will comeon top

of some $300bn in addi-tional Treasury purchasesfrom the Fed, as it

reinveststhe proceeds from maturingmortgage bonds back

intogovernment bonds.

The underlying rationale ofthe Feds policy action is tolower

Treasury yields, forceba nks t o le nd mo ney a ndpush investors

out of govern-ment debt into riskier securi-

ties. A further rally in equi-t ie s a nd o t he r ris k a s s e

tst ra ns la te s int o a w ea lthe ffe ct o n co nsume rs a

ndcompanies. This, in turn, itis hoped, will boost confidencea nd s

t imula te e co no micactivity.

T he Fe d w a nt s t o pushcash into risky assets such asstocks

which, it is hoped, willfacilitate a virtuous cycle ofspending,

investment, and hir-ing, says Eric Green, chief

US ra te s s t rat e gis t a t T DSecurities.

All told, the bond marketexpects the Fed will be buyingsome

$110bn of Treasurieseach month, an amount thatwill offset monthly

sales ofnew debt by the US Treasury.T he Fe d w ill t a rg et 86 pe

rce nt o f it s impe nding pur-chases in the 2.5-year to 10-year

sector of the market.

That supply and demande quat io n s hould re s ult in

lower yields out to the 10-yearsector of the market, as this

iswhere the Fed is targeting thebulk of its buying.

Not surprisingly, yields ontwo-, three-, five-, and seven-ye ar

T rea s ury no te s ha verecently fallen to record lowssince the

Fed announced QE2.Analysts at Deutsche Bankbelieve yields for the

five-year currently at 1.45 per cent a n d l e ss c a n c o mp r es

stowards 0.50 per cent.

However, against the back-drop of having the Fed as abig buyer

of Treasuries andsupporting the market, thereare risks.

The Feds buying puts afloor under the market, butits not a

guarantee, saysRick Klingman, managingdirector at BNP Paribas.

I f w e g e t a s t ri n g o f s t rong er da ta , t he re is

achance that the Fed decides toease back on buying bondsand you

will see 10-year ratesrise pretty quickly, he says.

After signs of solid private-sector hiring in the

Octoberunemployment report at thestart of November, the yieldo n t

he be nchmark 10-ye a rno te s its a t 2.85 pe r ce nt.Since the

start of QE2, thebenchmark yield has not been

able to break its October lowof 2.33 per cent.

Many in the bond marketexpect that as QE2 unfolds,the benchmark

yield will falltowards 2 per cent and eclipseit s mo dern lo w o f

2.04 pe rcent, set in December 2008at the height of the

financialcrisis.

With the Fed buying more10-ye a r pa pe r t ha n t he USTreasury

will sell through toJune, De uts che Ba nk, fo rexample, targets 2

per cent on10-year yields by early 2011.

But t he s ucce s s o f Q E2depends on boosting growthand

inflation, a combination

that will also push long-termyields much higher.

The real message is thatthe Fed will do what it takesto ensure a

robust recoverya nd it do es nt mind if t hisleads to a dose of

inflation,s a ys Da vid S hairp, g loba lstrategist at JPMorgan

AssetManagement.

Evidence of rising inflationwill weigh more on

long-termTreasuries and other long-term bonds, as their

fixedreturns are at the greatestris k o f be ing e rode d o ve

rtime by a climate of risingprices.

All of this suggests that

US

The central bank isflirting with inflationas it tries to ensure

arobust recovery, saysMichael MacKenzie

The Feds buyingputs a floor underthe market but it isnot a

guarantee

Rick Klingman,Managing director

at BNP Paribas

Scene set for newera of M&A and leveraged buy outs

The recovery in creditmarkets over the pastyear has set the

scenefor the return of M&A

and leveraged buy-outs.Their volumes are already

rising, but the return of deal-making has raised the risk

forbondholders of the releverag-ing of borrowers.

When it emerged in July thatthe two controlling sharehold-ers in

Abertis, along with pri-vate equity group CVC, wereworking on a

leveraged buy-outof the Spanish infrastructuregroup, it reminded

the marketonce again of the risks to bond-holders.

The companys bonds fell invalue in reaction to the news.Its 2016

bonds had been tradingsteadily at 102.16 just beforethe deal was

announced, butdropped to 89.50 on the news a price below par,

indicatinginvestors fear they will not berepaid in full when the

bondsmature.

Investors were spooked and

s o me w e re pro mpt ed t o re -examine the covenants on

theirdebt the protection they haveagainst suddenly finding them-s e

lve s le nding t o a ris kie rentity.

Giles Hutson, head of EMEACorporates, Debt Capital Mar-kets at

Bank of America Mer-rill Lync, says: The use of pro-ceeds from the

financings weare executing is moving slowlyfrom a pay-down of debt

into ageneral corporate purposes,capex, or dividend recap, type

transaction. The shift is notextreme, but it is happeningand has

implications for bond-holders in 2011.

T he va lue o f M &A de a lsworldwide reached $1.75bn

dur-ing the first nine months of2010, a 21 per cent increase ont he

s a me pe rio d la st ye ar,according to data from Thom-

son Reuters.A potentially greater risk for

bo ndho lde rs is t he ris ing number of leveraged

buy-outs,which has rebounded from a25-year low last year.

There was 12.5bn ($19.9bn)of private equity deals in theUK in

the year to September,up fro m 4.7bn in t he s a meperiod last

year, according toresearch from the Centre forManagement Buy-out

Researchat Nottingham University.

Buy-outs are typically nega-tive for bondholders of a target

co mpa ny be caus e priva t eequity firms more often use

high le vels o f de bt t o fundacquisitions.

However, bondholders do notnecessarily have reason toworry. Mr

Hutson thinks corpo-rate balance sheets are in verygood shape,

particularly amonglarge caps.

He says: Im not concernedfor bondholders overall, be-cause the

lack of bond supplyand the liquidity on corporateba lance s hee t s

is unpre ce-d e nt ed a n d w i ll s u pp o rtspreads. On

single-name basis,

there are potential examples ofreleveraging and that may

putpressure on ratings.

Valentijn van Nieuwenhui- jzen, head of strategy in

INGInvestment ManagementsStrategy & Tactical Asset Allo-cation

Group, says the pick-upin dealmaking could be a posi-tive sign for

credit investors.

We are seeing a releverag-ing in corporate credit, withmore

M&A but the amountsinvolved indicate this is justthe early

stages, says Mr vanNieuwenhuijzen.

He adds: If it increases thenit will also demonstrate anincrease

in corporate confi-dence, which is positive forcredit. Moreover, he

says, sofar 60 per cent of M&A dealsare being financed out of

cash.

At some point, improvedconfidence combined with anincrease in

equity financingcould be a sweet spot for bond-holders, says Mr Van

Nieu-wenhuijzen. But there willprobably be some releveragingand

capex that may be a riskfor bondholders in 2012.

Hakan Wohlin, co-head ofEuropean debt capital marketsat Deutsche

Bank, believes thatnext year more companies willus e bo nd ma rke t

s t o fundacquisitions.

Corporates will use cashand new debt to pay for acqui-sitions,

rather than shares.

Debt financing is currentlycheap, and a lot of companiesha ve ca

s h o n t heir ba lancesheet that they need to put towork, says Mr

Wohlin.

In recent months, companiessuch as IBM, Johnson & John-s o n

a n d C o ca - Co l a h a vesecured some of the loweste ver co s ts

o f bo nd ma rke tfunding.

However, Mr Wohlin doesnot believe companies will putat risk

their long-term creditratings to do deals, and does

not expect a pick-up in M&At o le a d t o a big increa s e

inleverage.

He says: Some companiesratings may be under short-term pressure

as a result of an

acquisition, but they will bedisciplined and wont tradeaway good

ratings to do a deal.

T he y w ill ke ep w ithin along-term rating perimeter, hesays.

Companies wont give

ratings up and they dont haveto.

Mr Wohlin believes compa-nies may look to alternativefinancing

ro ut e s s uch a shybrids for funding. Many are

considering these, he says.In recent months there has

been a revival in the sale ofcorporate hybrid bonds. Theseca n

co unt a s e quit y fro m acredit perspective, and have

been used by companies sucha s S co tt is h a nd S o uthe rnEne

rg y, w hich in O ct obe rraised 1.2bn with a hybridbond issue to

help shore up itscredit rating.

Dealmaking

Activity raises the riskfor bondholders ofreleveraging,

writesAnousha Sakoui

Corporates will usecash and new debt topay for

acquisitions,rather than shares;debt financing iscurrently

cheap

Alternative financing routes: Scottish and Southern Energy

raised 1.2bn in October with a hybrid bond issue to help shore up

its credit rating PA

-

8/3/2019 Debt Report

4/5

6 FINANCIAL TIMES FRIDAY NOVEMBER 19 2010 FINANCIAL TIMES FRIDAY

NOVEMBER 19 2010

Debt Capital Markets Debt Cap

Banks explore innovative stru

Sovereign credit Greeces woes have transformed the government

bond world, making it more difficult tWhat a difference a year

makes. Theeurozone government bond market has seena transformation

in the past 12 months asall the rules have been turned on their

head,writes David Oakley.

The market, once safe and predictable,has seen swings in price

and volatility moreakin to an emerging market basket caseeconomy,

as mounting public debt levelshave created unprecedented risks

forinvestors.

Critically, it may even have created a newclass of investor one

that straddles thedeveloped world economies of the eurozoneand

those traditionally more risky in theemerging markets.

Bill Northfield, head of sovereign,supranational and agency

origination atDeutsche Bank, says: Investors approachto risk has,

rightly, shifted in the past two years, and that has impacted

spreads acrossall asset classes.

This has meant bankers and investorshave had to carry out more

research intothe weaker eurozone economies, such asGreece, Ireland

and Portugal, on theperiphery of the single currency.

In essence, the bonds of these countriesare being treated more

like those ofcorporates or emerging markets in the so

called credit markets. This is because the riskof default, which

was considered unthinkablefor an advanced eurozone economy last

year,is now a real danger for anyone holdingbonds of the peripheral

governments.

However, in spite of the greater risks, MrNorthfield says there

is still good investorappetite for peripheral eurozone

countriesdebt. What has become harder has beenpricing it, he

says.

As the eurozone periphery is beingconsidered almost like a new

asset class initself, separate from the bigger

industrialisedeconomies and the emerging markets, it hasbecome more

difficult to determine whatyields investors should receive.

Should they receive yields similar toadvanced economy bonds or

those more likeemerging markets or corporate bonds, whichare

higher?

For those who like the safety of bigindustrialised world

products, which are onlyinfluenced by inflation and growth, they

aretoo unpredictable.

But even investors in corporates andemerging markets are not

sure that theseperipheral bonds should be priced at thesame levels

as their markets.

For some of these investors, peripheralbonds are considered

riskier than those in

the corporate and emerging market world.In short, the travails

of Greece, which first

sparked the problems in the periphery, havetransformed the

sovereign bond world andmade it harder to categorise.

It was in September last year, whenAthens revealed that its

public finances weremuch worse than the markets had been ledto

believe, that the transformation processbegan.

Over the ensuing months, Greek economicdata deteriorated to the

pointthat many investors refused tobuy the debt of Athens,forcing

thegovernment to turn

to the internationalcommunity forfinancial supportin May.

Contagion fromGreece hasalso spread tothe rest ofthe

periphery,with fears thatIreland and Portugal couldbecome as

vulnerable asAthens.

There are even worries

among some oSpain or Italy,which both havare vulnerable,in

Madrid and tRome.

Steven Majoresearch at HSaware of the ptoo.

The problemthat they are stbecause of themeasures that

debt.In contr

emerginmuch strong

offeringIreland, P

Evermome

sense tin the p

deciscons

If ndebt wdange

extremely unce

B

ert Bruggink, chieffinancial officer of

Rabobank, countsthe week his team

met investors to discuss anew form of contingent cap-ital as one

of the hardest inhis working life.

In early March, two teamsfrom the Dutch mutual metmore than 100

investors inless than a week a whirl-wind roadshow by anydebt

issuers standards.

This deal was really dif-ferent,he says. Bond dealsare all

exciting, but inves-tors usually know about theproduct. On this, we

had toexplain about the productand investors really had todo their

own maths, too.

The roadshow resulted ina 1.25bn ($1.7bn) bond thatpays a

regular couponunless the bank breaches apre-agreed capital ratio,

atwhich point investors per-manently forfeit 75 per centof their

investment.

Eight months on, andRabobank is still one ofonly two examples of

a new

breed of so-called contin-gent capital, a structurebeing

carefully consideredby regulators around theworld as part of their

effortsto buttress the financialsystem and protect taxpay-ers from

future bail-outs.

As in the Rabobank deal,contingent capital deals, orCocos, act

like bonds in good

times, but theoretically pro-vide a struggling bank witha

capital cushion in timesof stress. In the case of alisted bank such

as LloydsBanking Group, the onlyother to have issued Cocos,the

shares convert intocommon equity.

Cocos supporters hopethey will replace old-stylehybrid bonds,

which weredesigned with the sameintention, but failed to helpbanks

bolster their capitalbefore they were forced toturn to

taxpayers.

The bonds received aboost when the Swiss regu-lator recommended

its sys-

temically important banks,Credit Suisse and UBS,issue billions

worth as partof its efforts to buttress itsbanking system.

New bond structures arenot, however, the only idea.Others have

advanced thenotion of a so-called bail-

in, whereby regulatorswould force losses on allbonds including

seniordebt, previously considereduntouchable before tax-payers were

forced to bail abank out.

The Association for Fin-ancial Markets in Europe,an industry

body, has sup-ported bail-ins and has cal-

culated the cost if it hadbeen applied to LehmanBrothers, the US

bankwhose failure helped dragthe financial system to thebrink of

collapse in 2008.

It calculates that $25bn ofshareholders equity wouldhave been

wiped out and

replaced with $25bn fromconverting all outstandingpreferred

shares and subor-dinated debt.

Senior debtholders couldhave retained nearly 90 percent of their

investment compared with 20 per centof face value they can nowget

in the market for theirclaims of the banks estate.

The conversion woulhave given the bank a corcapital ratio of 20

per cent at least double many bankcurrent levels which,

withliquidity from a centrabank, would in theory havallowed it to

open its dooron the Monday for business

But not everyone is convinced that the turmoil surrounding a

struggling bancould be resolved so simplyWould that bank be able

togo to the market for funding the next day? I thinnot, says one

debt banker

Bail-ins run into practicaproblems, too, not least thneed for

each country t

Contingent capital

Regulators wantnew tools to shieldtaxpayers frombail outs,

saysJennifer Hughes

Whats in it for bondholders? Investors have expressed

reservations about Cocos and bail in Get

In for the verylong term

In 1910, Portugal became arepublic, S Duncan Blackand Alonzo G

Deckerstarted a hardware storeand Henry Ford sold morethan 10,000

Model Ts.

Such historical factoidsare fun trivia, but the stay-ing power

of countries andcompanies has become thetopic of debate in the

creditmarkets with the return ofcentury bonds and

otherultra-long-term borrowing.

Low-interest rates andstrong investor demand foryield have

prompted asmattering of debt salesthat do not come due for100

years. Century bondsare not unprecedented, butthey are not

common.

A niche market exists,with companies and inves-tors perennially

weighingthe pros and cons of suchlong-term bets.

There will be sporadicissuance of institutionalcentury bonds,

says Jonny

Fine, head of GoldmanSachs US investment-gradesyndicate desk.

There is asmall number of borrowerswho can issue into thismarket

and a reasonablysmall number of investorswho are willing to

buy.

When Norfolk Southernreopened the century bondmarket in August

afterabout five years withoutsuch issuance, some marketparticipants

wonderedwhether transport will stillinvolve rails and rollingstock

100 years from now(Norfolk added on to anexisting century bond

from2005) and if investorsshould accept just 5.95 percent for the

wager.

But the operator of about21,000 route miles in 22states and the

District ofColumbia sold more thantwice the amount of bondsit

announced.

In the ensuing months, itwas followed into the cen-tury market

by Rabobank

of the Netherlands and theMexican government, thelatter with a

$1bn deal at6.1 per cent.

For borrowers, centurybonds are not necessarilycheap, even if

absoluterates are low. Mexico paid apremium of about 85 basispoints

to its 30-year debt,says Jacob Gearhart, headof emerging markets

syndi-cate for the Americas atDeutsche Bank, which co-managed the

deal.

You have to take a viewon rates to justify that pre-mium, he

said. But in thegrand scheme of things, itis not too irrational

forMexico to think that lock-ing in circa 6 per cent for100 years

is good for thecountry and its borrowingstrategy.

Bragging rights also pro-vide some of the incentivefor issuers

periodically totest the appetite for theselong-term loans.

Sandeep Agarwal, head offinancial institutions debtcapital

markets withinEurope at Credit Suisse,says that century bondsalso

have a signallingeffect.

Those able to sell them,do it, he says. Not onlybecause it is

necessary tomatch the asset base, butbecause it demonstrates tothe

market that the busi-ness is so strong it canissue at the very long

end.

For investors, centurybonds can represent a wayto boost returns

in a cli-mate of low rates.

But some have questionedthe logic of lending for sucha long

time, particularlywhen interest rates are solow.

A rise in rates at somepoint during the next cen-tury will mean

a drop in theprice of these bonds. Thecentury bond market also

isnot without its rogues gal-lery, highlighting the diffi-culty of

predicting thefuture of a business even 10years out.

Among the past issuerswere Chrysler and Ambac,the bond insurer,

whichboth seemed solid whenthey sold the bonds in thelate 1990s,

but have sincegone bankrupt.

Nonetheless, there havebeen eager buyers of cen-tury bonds. The

very long-term income stream is agood match for investorswith very

long-term liabili-ties, such as insurance com-

panies and pension funds.But retail investors look-

ing for alternatives tolow-yielding money-marketfunds and bank

accountsalso have been drawn bylong-term issues from well-known

borrowers.

Goldman Sachs tailored arecent sale of 50-year bondsto

individuals rather thaninstitutions by pricing it in$25 increments,

raising$1.3bn for interest of just6.125 per cent.

Century bonds

There are pros andcons to taking a100 year view, saysNicole

Bullock

Samurais make a comeback

Japans so-called samuraibond market has facedtough times since

Lehman

Brothers collapsed in Sep-tember 2008, not onlyspooking

investors butremoving one of the stapleissuers from the market:

USinvestment banks.

However, this year themarket for yen-denomi-nated debt issued by

foreigninstitutions has made astrong comeback, with issu-ance

volumes nearly match-ing those before the col-lapse of Lehman.

The twist is that issuancevolumes have returneddespite the

absence of USinvestment banks.

Instead, that hole is beingfilled by more issuancefrom highly

rated Europeaninstitutions, and govern-ment debt of south-eastAsia

and Latin Americathat is almost fully guaran-teed by the Japan Bank

ofInternational Cooperation(JBIC).

Dealogic data show thatin the year to date, samuraiissuance has

reached

$20.6bn, a 56 per cent jumpfrom the same period in2009. In 2008,

the marketreached $21.8bn, but closedfor about three months

inSeptember after Lehmansdemise.

While it is far from 1996srecord full year of $34.2bn,the

figures suggest thatsupply is returning, withthis year showing the

third-highest volume.

Deals have also comefrom Australian banks,which are regular

issuers,and Korean institutionsand companies. Barclaysissued the

biggest samuraisince the Lehman shock,selling Y143bn ($1.74bn)

inSeptember.

There are quite activedeal flows [now] withoutsectors that were

a signifi-cant part of the market justtwo years ago, says onesenior

Nomura debt capitalmarkets official.

Investors have beenchoosier over what they

will buy from Europe giventhe worries about the Greekdebt

crisis.

Bankers say that senti-ment has been improvingsince the second

quarter,when eurozone anxietieswere at their most intense.However,

investors aremonitoring the situationclosely still given the

recentworries about Ireland andPortugal.

Demand for samuraibonds is extremely strong.

Institutional investors, whobuy the debt, are conserva-tive, and

tend to purchaseonly bonds of companiesand institutions with

thehighest credit ratings.

Domestic institutionalinvestors, particularlybanks, are

suffering fromweak loan demand and thushave excess deposits

toinvest.

Already filled to the brimwith Japanese governmentbonds (JGBs)

that havebenchmark 10-year yields ofbarely 1 per cent, they

arelooking elsewhere as well.

The domestic corporatebond market is small relativeto the size

of the economy,and spreads over JGBs havebecome extremely

narrow.This has made samuraibonds even more attractive,

as in general investors willdemand additional spreadrelative to

comparabledomestic institutions.

A l though s am ur aispreads are also narrowing,the gap remains

widebetween a samurai and adomestic credit, notesKenji Setogawa,

debt syndi-cate manager at BarclaysCapital Japan.

Were seeing lots of newinvestors, Mr Setogawasays. [There are

more]

regional banks in the mar-ket these days because theyare

suffering low yields onJGBs and narrow spreads[for domestic

corporatebonds].

The move by JBIC thisyear fully to establish aprogramme

partially toguarantee samurai bondsof developing economieson an

ongoing basis hashelped augment much-needed issuance.

Normally, governments ofcountries such as the Phil-

ippines, Indonesia and evenMexico, which has aninvestment-grade

credit rat-ing, would find it difficultto tap the samurai

market,because of the conservativenature of investors.

However, with a partialguarantee that is about 95per cent by

JBIC, investorsare more confident toinvest, getting a widerspread

than they wouldwith more highly ratedissuers. The guarantee

reduces the funding costsfor the issuer as well.

With investor demandstill strong, Barclays isworking on deals

with com-panies of lower credit rat-ings, which should

helpdiversify the market.

One such deal came formHyundai Capital of Korea,which sold Y30bn

of samu-rai bonds on November 12.The company is rated BBB+by

Standard & Poors, onenotch higher than Mexicossovereign

rating.

This shows investors aregetting more comfortablewith BBB names

and [mov-ing] down the credit curve,says Barclays Mr Seto-gawa,

joint lead manager ofthe deal.

Bankers expect moredemand to come from the

highly rated financial insti-tutions. The Nomura offi-cial says:

Because of theamount of financing we sawwith government guaran-tees

during the financialcrisis, there will be contin-ued pressure for

refinanc-ing over the next two orthree years. So its quiteimportant

for institutionsto continue diversifying andextend their duration

fromvery short-term funds tolonger-term funds.

Japan

Volumes have comeback even withoutUS issuers, writesLindsay

Whipp

In demand: the market for yen denominated debt is extremely

strong Dreamstime

Were seeing lotsof new investors.There are moreregional

banks

Some havequestioned thelogic of lending forsuch a long time

-

8/3/2019 Debt Report

5/5

8 FINANCIALTIMESFRIDAYNOVEMBER 19 2010