Embed Size (px)

Citation preview

Debt policy under constraints:Philip II, the Cortes, and

Genoese bankers1

By CARLOS ÁLVAREZ-NOGAL and CHRISTOPHE CHAMLEY*

Under Philip II, Castile was the first country with a large nation-wide domesticpublic debt. A new view of that fiscal system is presented that is potentially relevantfor other fiscal systems in Europe before 1800.The credibility of the debt, mostly inperpetual redeemable annuities, was enhanced by decentralized funding throughtaxes administered by cities making up the Realm in the Cortes.The accumulation ofshort-term debt depended on refinancing through long-term debt. Financial crises inthe short-term debt occurred when the service of the long-term debt reached therevenues of its servicing taxes. They were not caused by liquidity crises and wereresolved after protracted negotiations in the Cortes by tax increases and interest ratereductions.

K ing Philip II, as head of the first modern super-power, managed a budget ona scale that had not been seen since the height of the Roman Empire.2 No

state before had faced such extraordinary fluctuations and imbalances, both inrevenue and expenditure. Large military expenses were required by the politics ofEurope and the revolution in military technology. The variability in both revenueand expenses, coupled with a large foreign component, was met by large publicborrowings up to modern levels, a historical innovation that, in later centuries,would be followed by the Netherlands, France, and England. Like eighteenth-century England, Castile (about 80 per cent of modern-day Spain) established itsmilitary supremacy through its superior ability to mobilize large resources throughborrowing.

The debt-to-GDP ratio exceeded 50 per cent, according to some estimates, andthe ratio between interest service and tax revenues at the end of the century wasabout 50 per cent, as it would be in England or France two centuries later.3 Theseimpressive numbers were achieved without a central administration to collect tax

* Author affiliations: Carlos Álvarez-Nogal, Universidad Carlos III de Madrid; Christophe Chamley, BostonUniversity and PSE.

1 We would like to thank Jean-Laurent Rosenthal, Gilles Postel-Vinay, Pierre-Cyrille Hautcoeur, LeandroPrados de la Escosura, and the referees for their comments and suggestions. Financial support was received fromthe HI-POD Project, European Commission’s Seventh Research Framework Programme and Ministry ofEconomy and Competitiveness (Spain) HAR2012-39034-C03-02.

2 At 6 million ducats (the average around 1560), with a ducat at 35 grams of silver, it amounted to 210 tonsof silver per year with a population of about 5 million, while the Roman Empire’s budget was between 500 and1,000 tons for a population of 50 million; Hopkins, ‘Rome’.The size of the monetized government revenues andexpenditures, per capita, had been small throughout the middle ages in western Europe; Bean, ‘War’.

3 Álvarez-Nogal and Prados de la Escosura, ‘Decline of Spain’, pp. 352–4.

bs_bs_banner

Economic History Review (2013)

© Economic History Society 2013. Published by John Wiley & Sons Ltd, 9600 Garsington Road, Oxford OX4 2DQ, UK and 350 MainStreet, Malden, MA 02148, USA.

revenues and without a centralized capital market that could facilitate the man-agement of the public debt.4

Under Philip II, four ‘defaults’ are alleged to have occurred, and these financialcrises have attracted considerable attention. We propose an interpretation of thefinancial crises under Philip II that is totally new.These crises were not caused bya ‘sudden stop’ from foreign bankers, by a problem of liquidity, or by the inabilityof the Crown to raise sufficient revenues. Since the crises that took place con-cerned loans with Genoese bankers, all previous studies have focused on relationsbetween the Crown and the bankers.We show that the cause of each of the criseslay elsewhere, in the protracted negotiations about higher taxes that took place inthe Cortes between the Crown and the cities of Castile.

In a decentralized system with no central administration, the cities managed thetaxes that serviced the most secure component of the domestic debt, and thesetaxes effectively put a ceiling on the domestic debt. Any significant accumulationof loans with foreign bankers had to be converted eventually into domestic debt.When the service of that debt reached the implicit ceiling imposed by the domestictaxes, protracted negotiations had to take place between the Crown and the cities.These negotiations triggered a suspension of payments by the Crown on the loanswith foreign bankers.

In our argument, the alleged defaults were part of a system that had efficientproperties in the institutional context. Our argument focuses on the economics,but it also sheds some light on the political state of Castile, and on the develop-ment of states and their finances in early modern Europe, especially for compositemonarchies of the kind exemplified by Castile.5

The public debt had been created and developed gradually by Italian cities sincethe twelfth century.6 Within a city-state, a credible public debt could be issuedbecause debt holders had some control over the collection of taxes that wouldservice that debt.The Italian system was extended in the Netherlands under PhilipII’s father, Charles V: the state’s debt was issued through the cities that were partof a central political regime.7 In this way, bondholders kept control of the revenuesthat would service the debt. In Castile, that system was introduced by Charles Vand developed further under Philip II. The dominant part of the debt was thedomestic debt, called juros, and the main part of the juros was administered bycities that controlled taxes. Hence, the lack of a central administration whichwould control and enforce tax revenues did not diminish but reinforced thecapability of the Crown to borrow because it restricted its ability to divert taxrevenues away from servicing the debt.

The domestic debt provided collateral, either implicit or explicit, for the short-term debt, the asientos, which could be converted into long-term juros. Followingthe routine established in the previous century,8 the Crown converted any signifi-cant accumulation of short-term debt into long-term domestic debt. Each citycontributed a fixed lump-sum amount per year that was established, by majority

4 In England, both the tax administration and capital markets developed only after the Glorious Revolution;Brewer, Sinews; Dickson, Financial revolution.

5 This issue has been the subject of a number of important recent studies that cannot be summarized here.Weprovide references on specific issues.

6 Pezzolo, ‘Government debts’.7 Tracy, Financial revolution; Gelderblom and Jonker, ‘Public finance’.8 Andrés Díaz, El último decenio.

2 CARLOS ÁLVAREZ-NOGAL AND CHRISTOPHE CHAMLEY

© Economic History Society 2013 Economic History Review (2013)

vote, at the meeting of 18 cities in the Cortes. Hence, the total contributionestablished a de facto ceiling on the service of the public debt.When the domesticdebt grew and the ceiling was reached, the short-term debt could no longer beconverted into long-term debt and a crisis took place.This structure explains boththe existence of a large, credible domestic debt and the repeated crises.

Each of the three financial crises under Philip II (in 1557–60, 1575–7, and1596–7) formally started when the Crown declared a suspension of payments onshort-term loan contracts, the asientos.9 However, each crisis occurred when theservice of the long-term debt reached the previously agreed-upon ceiling of the citytax payments.10 The crises had no adverse effect on the long-term debt interestrate, which declined during the century.

Previous works on the financial crises in sixteenth-century Castile fall into oneof two categories. The first category, favoured especially by economists, viewsCastile as a modern state with central control over expenditures and revenues anda budget policy that could be evaluated by aggregates according to InternationalMonetary Fund criteria.11 Some economists even interpret the so-called ‘defaults’of the late sixteenth century as proper solvency crises that resulted from anincompatibility of revenue-raising capacity and expenditure.12 More recently,Drelichman andVoth, following earlier work byThompson and others, have shownthat solvency was never the issue, from the point of view of a centralized govern-ment, but that instead these crises were liquidity crises followed by renegotiationsand a conversion of short-term loans into long-term bonds.13

We agree that solvency was not the issue, but we do not think that the crisesunder Philip II were short-term liquidity crises.14 In a standard liquidity crisis,lenders refuse to provide additional short-term lending or loan roll-overs.However, each of the crises was not triggered by such a constraint but instead bya suspension of payments declared by Philip II.The most important crisis, in 1575,could have been avoided easily if Philip II had asked for a moderate increase of taxrevenues from the cities instead of embarking on a power play to triple theserevenues.

The second category of historical research on Spain follows Elliott in empha-sizing the ‘composite’ nature of the state in which territories preserved most oftheir political-administrative structure and historic freedoms.15 We support thisview and argue that relations between the Crown and the cities were directlyrelated to the dealings between the Crown and the Genoese bankers who provided

9 The two crises of 1557 and 1560 are actually two parts of the same crisis.10 The process is reminiscent of the deadlock that almost took place in the summer of 2011 in the US between

the legislative and the executive branch of the government.11 Lovett, ‘Castilian bankruptcy’; Conklin, ‘Theory of sovereign debt’; Drelichman and Voth, ‘Sustainable

debts’.12 Reinhart and Rogoff, This time is different.13 Drelichman and Voth, ‘Sustainable debts’; Thompson, ‘Castile’.14 For example, the statement that ‘a compromise [between Philip II and the Cortes] emerged in 1575, too late

to prevent a default on short-term debt’ (Drelichman and Voth, ‘Sustainable debts’, p. 816) is contrary tohistorical evidence of the protracted negotiations that we discuss in our detailed account of the 1575 crisis insection V.

15 Elliott, ‘Europe’; Grafe, Distant tyranny; Artola, La Hacienda; Gelabert, La bolsa del rey; Sanz Ayán, ‘Pro-cedimientos’; Tracy, Emperor CharlesV; Irigoin and Grafe, ‘Bargaining for absolutism’.

DEBT POLICY UNDER CONSTRAINTS 3

© Economic History Society 2013 Economic History Review (2013)

short-term loans.16 In order to understand the financial crises it is important tostudy both relationships at the same time.

In this article, we also provide a new description of the actual nature of thefinancial crises under Philip II. Traditionally, the literature has labelled thembankruptcies.17 Such a Procrustean classification neglects the historical features offinancial instruments in Castile and confuses interest reduction with debt reduc-tion. Most of the domestic debt was in perpetual annuities redeemable at par (jurosal quitar): the Crown could repay the principal at any time. This feature had beenintroduced in the fifteenth century and, by the end of that century, the Crown wasroutinely using the redeemability of the annuities to lower their interest rate as themarket rate decreased gradually over the century. Each interest reduction was notforced and included the provision that the debt holder could choose instead thecash payment of the face value of the principal.

Although interest reductions were indeed conducted during the crisis resolu-tions of 1575–7 and 1596–7, they were not defaults, as is often alleged. Wecertainly do not deny that some of the debt was reduced, but we think that thequoted amounts (for example, those given by Drelichman and Voth) are over-stated.18 More work is needed on this issue, however.

The article is organized along the following lines. The backbone of the system,the long-term domestic juros, is presented in section I. The funding of the juros isanalysed in Section II. Section III is devoted to the short-term debt, the asientos.Section IV discusses principles of fiscal and debt policy under the constraint of aquantum cost of adjusting taxes. A mathematical formulation of the fiscal problemis beyond the scope of this article and could not do full justice, at this stage, to thecomplexity of the interactions between the Crown, the cities, and the Genoesebankers. In the context of a quantum cost of adjustment, some accumulation ofshort-term debt can be efficient despite its higher cost, and it is entirely convertedinto long-term debt when there is a tax adjustment. Indeed this actually occurredunder Philip II. In sectionV, each of the three crises is analysed in light of our mainargument.

I

The core of the fiscal system of Castile was its long-term debt. In order tounderstand its funding mechanism and the interest reductions on the debt, it isnecessary to examine the financial instruments of this long-term debt, called juros.They had been introduced in the twelfth century as pension rewards for servicesduring the Reconquista.19 Their marketability increased gradually over the centu-ries. Given the stage of development and the institutions in the sixteenth century,there was no central market with price quotations as, centuries later, there would

16 Historians have either specialized in the relations between the Crown and the Cortes (for example, ForteaPérez, Monarquía y Cortes), or in the relations between the Crown and the bankers (Carlos Morales, Felipe II, andthe cited literature).

17 Reinhart and Rogoff, This time is different.18 A central point made by Drelichman andVoth is that Genoese bankers did rather well on their loans, ex post,

in spite of the debt reductions. Our argument about interest reduction reinforces their conclusion.19 See Barthe Porcel, Los juros; Toboso Sánchez, La deuda pública; Pérez-Prendes and Torres López, Los juros.

4 CARLOS ÁLVAREZ-NOGAL AND CHRISTOPHE CHAMLEY

© Economic History Society 2013 Economic History Review (2013)

be in the Netherlands and England. More importantly, in the political structure ofCastile, there could not be such a market.The juros were serviced at the city levelto ensure their credibility.Thus, for a juro issued in Seville, the coupons had to becollected in Seville and not in Madrid.The same office would service the juros andcollect the local sales tax revenues on which the service of juros had first claim.Juros were also ranked by local order of seniority according to their date ofissuance. No default took place on juros in the sixteenth century, but there couldbe local delays of payment. Juros were traded and not attached to a particularholder (transactions had to be registered).They were not homogeneous like the 3or 4 per cent annuity found in eighteenth-century England, but they could betraded throughout the entire realm.20

Juros were either perpetual and redeemable annuities (juros al quitar), or lifeannuities (juros de por vida), which were also redeemable.21 Juros al quitar had a facevalue, the principal, which could be paid back by the government at any time.Theredeemable feature enabled the government to reduce the debt in times of surplusand to refinance when the interest rate decreased. Such interest reductions hadtaken place in the fifteenth century, from 10 to 7 per cent and from 8 to 6 per cent.At the same time, the Crown sold new juros at rates of 7 and 6 per cent.22

Redeemable annuities with a fixed income complied with the usury laws of thechurch that essentially aimed at preventing a state of servitude of the debtor. Inlater centuries (for example, in France in the seventeenth century and England inthe eighteenth century), refinancing at a lower interest rate was achieved by areduction of the coupon while keeping the face value of the loan unchanged.23 InCastile, following the tradition established in the previous century, the interestreduction kept the annual income constant and demanded from the lender anaugmentation of the capital of the loan, known as the crecimiento. A juro wasdefined by the capital amount needed to generate 1,000 maravedis (mrs). Forexample, ‘14,000 al millar’ means an interest of 7.14 per cent. In a crecimiento, theholder of the juro was given the choice between either receiving its face value incash, or paying the difference with the new face value. In a reduction from 7.14 to5 per cent, the holder of a juro that was ‘increased’ to 20,000 had to make apayment of 6,000 in order to keep the juro. In such cases, the new face value wouldbe registered.24

The crecimiento may also have provided a commitment device against a forceddebt reduction, since a forced increase of a bond’s capital value is perhaps moredifficult to implement than a decrease of a bond’s coupon.25 No juro had its annualincome reduced during the reign of Philip II. Crecimientos are a central issue in theinterpretation of the resolution of the crises of 1575–7 and 1596–7.

20 The Netherlands did not have a central bond market at that time either. Issuances were at the local level asin Castile; van Bochove, ‘Intermediaries’.

21 The fraction of juros al quitar was 76% in 1559, 82% in 1575, and about 90% at the end of the century;Artola, La Hacienda, p. 88.

22 Andrés Díaz, El último decenio.23 Chamley, ‘Interest reductions’.24 The market value of old juros (that carry a high dividend ratio) depended on the long-term rate and on the

expectation about future crecimientos, in addition to local conditions.25 In a similar sense, tontines were more vulnerable than life annuities and were indeed reduced to life annuities

by Joseph Marie Terray, Controller-General of Finances during the reign of Louis XV in France, in his debtreduction of 1770.

DEBT POLICY UNDER CONSTRAINTS 5

© Economic History Society 2013 Economic History Review (2013)

II

The funding of the domestic debt should, above all, have a stable basis. Thestandard method of increasing credibility, since the creation of the public debt inthe Italian cities during the middle ages, has been an alignment between the debtholders and the people who control and enforce the taxes that service the debt.26

What was good for a city-state could also be used by a state that included cities.The Italian system was generalized in the sixteenth century to states that includedcities.27 In Castile, the system of ‘borrowing through cities’ had an ideal setting:most of the Castilian realm was represented by 18 cities and their surroundingregions, and negotiations between the Crown and the realm were centralized in theCortes.

The main tax in Castile was the alcabalas, a sales tax collected by tax farmingbefore 1536, with a nominal rate of 10 per cent (de facto a legal maximum).28 Theactual rate was much lower, possibly around 2 per cent.29 The Cortes of 1536established the system of the encabezamiento general by which each city was com-mitted to an annual lump-sum payment that was fixed for the following six years.These amounts were adopted in the Cortes by majority voting. Each readjustmentof the encabezamientos would require protracted negotiations. After 1536, theencabezamiento provided the most stable basis for servicing the juros.

The lack of a central administration to collect the alcabalas directly preventedthe central government from diverting revenues away from servicing the debt. Itthus enhanced the borrowing capability of the government. The delegation of taxrevenues and the debt service was a commitment device that enabled the Crownto increase the domestic debt to a level that was unprecedented in the sixteenthcentury.

Juros were administered by cities, but they were legal contracts between holdersand the Crown, rather than contracts between holders and cities. Hence, theycould be traded throughout the entire realm with registered sales and transfers.30

Because of the delegation of revenue collection, there was no centralized market(as in eighteenth-century England) and it should not be surprising that the couponrates for apparently similar juros were not identical.

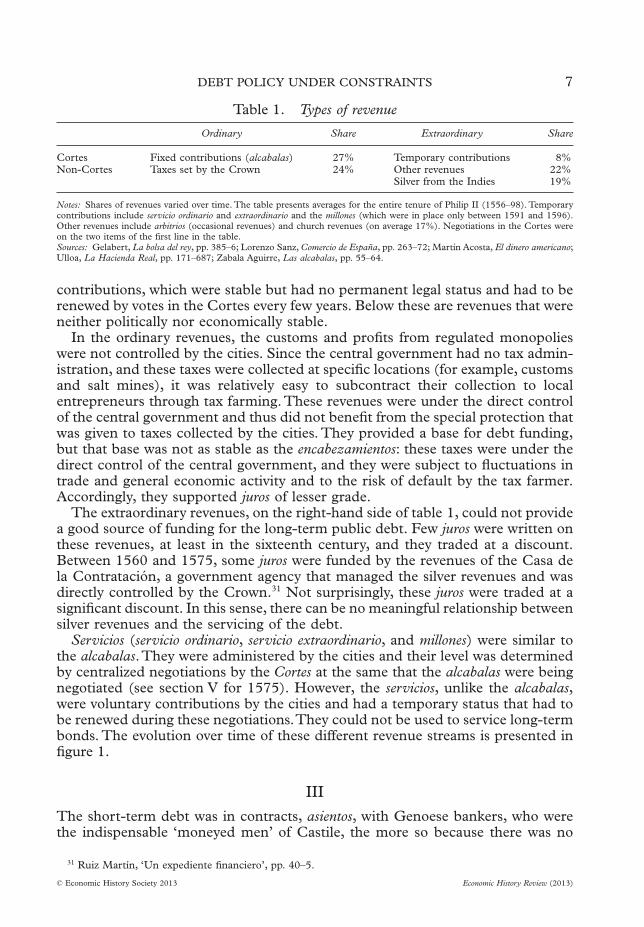

The alcalabas and the associated servicios (see below) represented the moststable basis for the funding of the debt, but they were only part of the Crown’srevenues. An overview of these revenues is presented in table 1 according to theircapacity for debt servicing.The table is in four parts, each defined by its reliabilityfor servicing the public debt. On the left-hand side are the ordinary revenues,which provided a stable source of funding. At the top is the fixed contribution ofcities, which was determined in the Cortes, and provided the most reliable base.Below are the taxes that were administered directly by the Crown (for example,import duties and monopolies), which were less reliable. On the right-hand sideare the extraordinary revenues, which were of two types. At the top are the city

26 Pezzolo, ‘Government debts’.27 For the Low Countries under Carlos V, see Tracy, Financial revolution, esp. pp. 71–108. In 1522, Francis I

issued the Rentes sur l’Hôtel de Ville de Paris; Vührer, Histoire.28 Zabala Aguirre, Las alcabalas, p. 57.29 Artola, La Hacienda, p. 50.30 Archivo Histórico Nacional, Madrid (hereafter AHN), Consejos Juros, leg. 1733, fo. 7; AGS, Contaduría de

Mercedes, leg. 227.

6 CARLOS ÁLVAREZ-NOGAL AND CHRISTOPHE CHAMLEY

© Economic History Society 2013 Economic History Review (2013)

contributions, which were stable but had no permanent legal status and had to berenewed by votes in the Cortes every few years. Below these are revenues that wereneither politically nor economically stable.

In the ordinary revenues, the customs and profits from regulated monopolieswere not controlled by the cities. Since the central government had no tax admin-istration, and these taxes were collected at specific locations (for example, customsand salt mines), it was relatively easy to subcontract their collection to localentrepreneurs through tax farming. These revenues were under the direct controlof the central government and thus did not benefit from the special protection thatwas given to taxes collected by the cities. They provided a base for debt funding,but that base was not as stable as the encabezamientos: these taxes were under thedirect control of the central government, and they were subject to fluctuations intrade and general economic activity and to the risk of default by the tax farmer.Accordingly, they supported juros of lesser grade.

The extraordinary revenues, on the right-hand side of table 1, could not providea good source of funding for the long-term public debt. Few juros were written onthese revenues, at least in the sixteenth century, and they traded at a discount.Between 1560 and 1575, some juros were funded by the revenues of the Casa dela Contratación, a government agency that managed the silver revenues and wasdirectly controlled by the Crown.31 Not surprisingly, these juros were traded at asignificant discount. In this sense, there can be no meaningful relationship betweensilver revenues and the servicing of the debt.

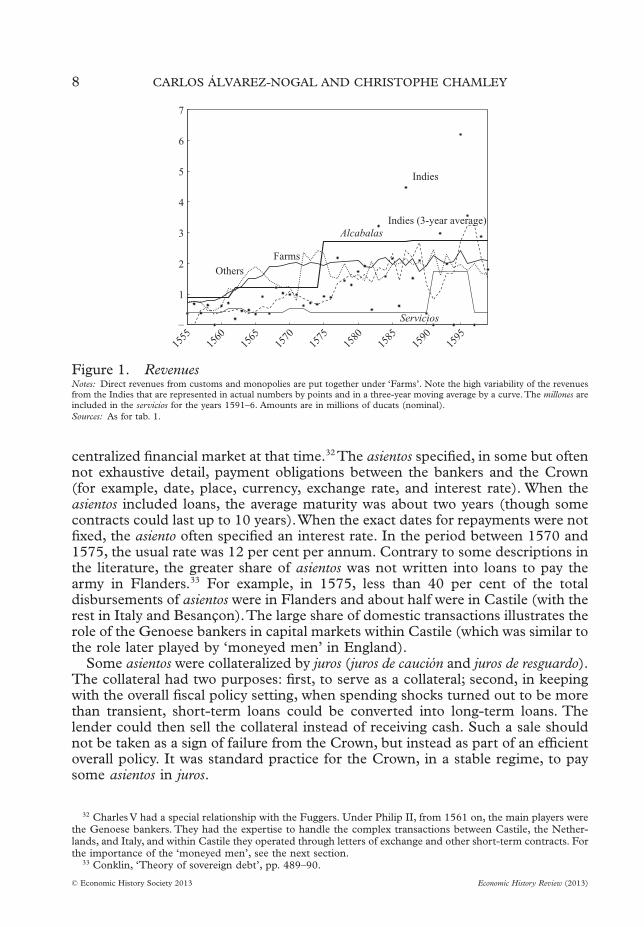

Servicios (servicio ordinario, servicio extraordinario, and millones) were similar tothe alcabalas.They were administered by the cities and their level was determinedby centralized negotiations by the Cortes at the same that the alcabalas were beingnegotiated (see section V for 1575). However, the servicios, unlike the alcabalas,were voluntary contributions by the cities and had a temporary status that had tobe renewed during these negotiations.They could not be used to service long-termbonds. The evolution over time of these different revenue streams is presented infigure 1.

III

The short-term debt was in contracts, asientos, with Genoese bankers, who werethe indispensable ‘moneyed men’ of Castile, the more so because there was no

31 Ruiz Martín, ‘Un expediente financiero’, pp. 40–5.

Table 1. Types of revenue

Ordinary Share Extraordinary Share

Cortes Fixed contributions (alcabalas) 27% Temporary contributions 8%Non-Cortes Taxes set by the Crown 24% Other revenues 22%

Silver from the Indies 19%

Notes: Shares of revenues varied over time. The table presents averages for the entire tenure of Philip II (1556–98). Temporarycontributions include servicio ordinario and extraordinario and the millones (which were in place only between 1591 and 1596).Other revenues include arbitrios (occasional revenues) and church revenues (on average 17%). Negotiations in the Cortes wereon the two items of the first line in the table.Sources: Gelabert, La bolsa del rey, pp. 385–6; Lorenzo Sanz, Comercio de España, pp. 263–72; Martín Acosta, El dinero americano;Ulloa, La Hacienda Real, pp. 171–687; Zabala Aguirre, Las alcabalas, pp. 55–64.

DEBT POLICY UNDER CONSTRAINTS 7

© Economic History Society 2013 Economic History Review (2013)

centralized financial market at that time.32 The asientos specified, in some but oftennot exhaustive detail, payment obligations between the bankers and the Crown(for example, date, place, currency, exchange rate, and interest rate). When theasientos included loans, the average maturity was about two years (though somecontracts could last up to 10 years).When the exact dates for repayments were notfixed, the asiento often specified an interest rate. In the period between 1570 and1575, the usual rate was 12 per cent per annum. Contrary to some descriptions inthe literature, the greater share of asientos was not written into loans to pay thearmy in Flanders.33 For example, in 1575, less than 40 per cent of the totaldisbursements of asientos were in Flanders and about half were in Castile (with therest in Italy and Besançon).The large share of domestic transactions illustrates therole of the Genoese bankers in capital markets within Castile (which was similar tothe role later played by ‘moneyed men’ in England).

Some asientos were collateralized by juros (juros de caución and juros de resguardo).The collateral had two purposes: first, to serve as a collateral; second, in keepingwith the overall fiscal policy setting, when spending shocks turned out to be morethan transient, short-term loans could be converted into long-term loans. Thelender could then sell the collateral instead of receiving cash. Such a sale shouldnot be taken as a sign of failure from the Crown, but instead as part of an efficientoverall policy. It was standard practice for the Crown, in a stable regime, to paysome asientos in juros.

32 Charles V had a special relationship with the Fuggers. Under Philip II, from 1561 on, the main players werethe Genoese bankers. They had the expertise to handle the complex transactions between Castile, the Nether-lands, and Italy, and within Castile they operated through letters of exchange and other short-term contracts. Forthe importance of the ‘moneyed men’, see the next section.

33 Conklin, ‘Theory of sovereign debt’, pp. 489–90.

–

1

2

3

4

5

6

7

1555

1560

1565

1570

1575

1580

1585

1590

1595

Alcabalas

Farms

Servicios

Others

Indies

Indies (3-year average)

Figure 1. RevenuesNotes: Direct revenues from customs and monopolies are put together under ‘Farms’. Note the high variability of the revenuesfrom the Indies that are represented in actual numbers by points and in a three-year moving average by a curve.The millones areincluded in the servicios for the years 1591–6. Amounts are in millions of ducats (nominal).Sources: As for tab. 1.

8 CARLOS ÁLVAREZ-NOGAL AND CHRISTOPHE CHAMLEY

© Economic History Society 2013 Economic History Review (2013)

Under Charles V, the juros as collateral could be sold only if the Crown did notmeet the terms of the asiento (juros de caución). Starting in 1561, following aninitiative by the banker Juan Curiel de la Torre, some collaterals, called juros deresguardo, could be sold by the banker provided that he returned a similar juro laterif the Crown met the payment schedule of the asiento.34 In this case, the service ofthe juro that had been sold would be deducted from the liability of the Crown.Thesystem of the juros de resguardo enabled bankers to refinance asientos at a lowinterest rate. That system increased the banker’s profitability. However, in thecontext of the fragmented juros market, the system introduced some confusion inthe definition of the net debt of the Crown. It is therefore not surprising that thecrisis of 1575 was, among other things, an ‘information event’ in which the Crownattempted to recalculate the liability it had accumulated since 1560, as actualizedat the average rate of asientos (12 per cent).35

IV

Expenditure in Castile was driven by wars and was highly variable. The standardmodern theory of public finance assumes a central government that minimizes taxdistortions through tax smoothing. Any surprise in expenditure should be met witha frictionless adjustment of taxes to meet the intertemporal resource constraint. Atextbook illustration is presented by parliamentary England in the eighteenthcentury (although it departed from that model during the NapoleonicWars).36 TheEnglish method of debt financing became operational only after a long transition,between 1690 and 1740, that has been called a ‘financial revolution’.37 Dickson hasemphasized that, even after the completion of that transition, the English govern-ment could not issue large quantities of liabilities, both long- and short-term,without the close collaboration of institutions such as the Bank of England and theSouth Sea Company, and of skilled financiers.38

In Castile, as with all the governments at the time, the Crown had exclusiveauthority over expenditure. Cities, however, controlled the best taxes for servicingthe debt and their contribution (encabezamiento) was set through collective bar-gaining in the Cortes. The Cortes could not meet independently like a modernParliament. Instead, they had to be called by the Crown. No increase in theencabezamiento could be carried out without a meeting of the Cortes and theagreement of the cities. Negotiations with the cities would be protracted becauseof divergent political interests between the cities and the Crown and because ofimperfect information between the Crown and the cities, between the Genoese

34 Ruiz Martín, ‘Las finanzas españolas’. During a brief period up to 1563, some asientos had as collateral jurospor acomodar that were similar to juros de resguardo; Carlos Morales, Felipe II, pp. 93–4.

35 In the modern theory of the debt contract (Townsend, ‘Optimal contracts’), the creditor can get informationon the debtor at some cost. The debt contract with a fixed interest rate is efficient because the creditor needs toget this information only in the case of default. Such an event can be called an ‘information event’. In the caseof Philip II, the debtor also had imperfect information on the creditors as they traded in collaterals. Hence, therewas some efficiency in acquiring information about creditors only in the ‘information event’ of a suspension ofpayments.There is no formal analysis of this situation of double asymmetric information in debt contracts in theliterature and it is beyond the scope of the present article.

36 Barro, ‘Government spending’.37 Dickson, Financial revolution.38 However, the interests that were represented by these institutions and people restricted the capability of the

government to conduct efficient reductions of the interest rate on the public debt; Chamley, ‘Interest reductions’.

DEBT POLICY UNDER CONSTRAINTS 9

© Economic History Society 2013 Economic History Review (2013)

bankers and the Crown/cities, and between the cities themselves. The problem ofasymmetric information between the Crown and the realm was well known in allfeudal countries where the sovereign faced a constraint of ‘evident necessity’ andhad to justify taxation (in men or money) for wars. A contribution to the solutionof the information problem was found in the twelfth century in the Cortes ofAragon,39 and in the thirteenth century in England.40

The Cortes did not have the power completely to oppose a tax increase, but theycould impose a cost on the Crown by reducing the amount of the tax increase, ordelay its implementation for a few years, as in the crisis of 1573–7. Revenues fromthe encabezamiento and other ordinary taxes provided a ceiling on the service of thejuros that were of the highest grade. As long as the ceiling was not reached, theCrown could issue more juros. In that regime, the Crown used the short-termunfunded asientos, which had a rate about twice the rate of the funded juros (about12 per cent against 6 per cent), in order to absorb transitory shocks and fundtransfers abroad. However, there was no significant accumulation of short-termdebt.

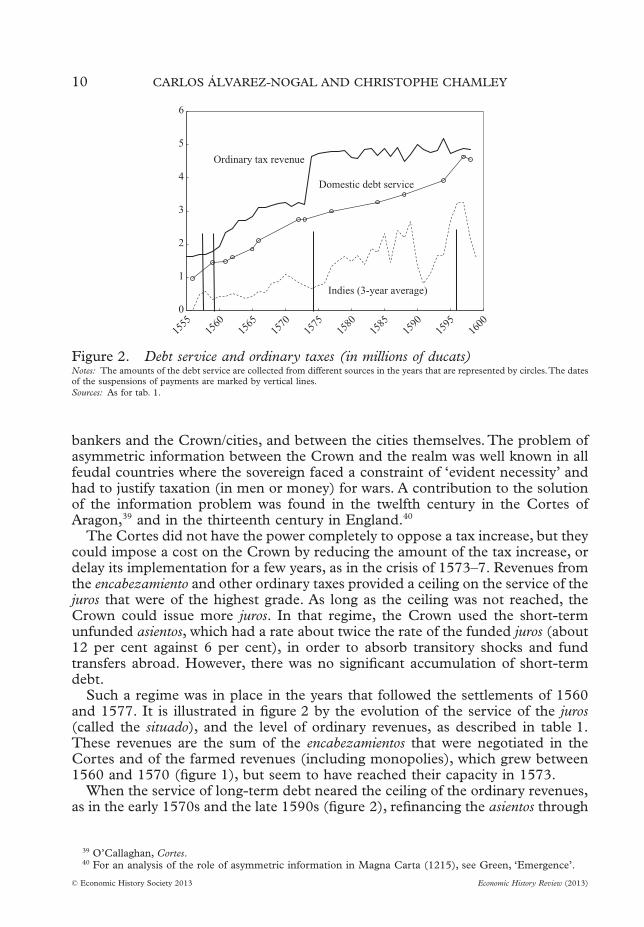

Such a regime was in place in the years that followed the settlements of 1560and 1577. It is illustrated in figure 2 by the evolution of the service of the juros(called the situado), and the level of ordinary revenues, as described in table 1.These revenues are the sum of the encabezamientos that were negotiated in theCortes and of the farmed revenues (including monopolies), which grew between1560 and 1570 (figure 1), but seem to have reached their capacity in 1573.

When the service of long-term debt neared the ceiling of the ordinary revenues,as in the early 1570s and the late 1590s (figure 2), refinancing the asientos through

39 O’Callaghan, Cortes.40 For an analysis of the role of asymmetric information in Magna Carta (1215), see Green, ‘Emergence’.

0

1

2

3

4

5

6

1555

1560

1565

1570

1575

1580

1585

1590

1595

1600

Domestic debt service

Ordinary tax revenue

Indies (3-year average)

Figure 2. Debt service and ordinary taxes (in millions of ducats)Notes: The amounts of the debt service are collected from different sources in the years that are represented by circles.The datesof the suspensions of payments are marked by vertical lines.Sources: As for tab. 1.

10 CARLOS ÁLVAREZ-NOGAL AND CHRISTOPHE CHAMLEY

© Economic History Society 2013 Economic History Review (2013)

juros became more difficult and the Crown initiated negotiations with the cities.41

During this phase, asientos accumulated. Before the suspensions of payments in1557, 1575, and 1596, the amounts of outstanding asientos, gross of the collaterals,were 7.5, 15, and 7 million ducats, respectively. Each of these crises is representedby a vertical line. The first two, in 1557 and 1560, are actually two steps of thesame crisis. At the end of each crisis, all the outstanding asientos were convertedinto juros.

Each crisis formally began with a suspension of payments on the short-termdebt to the foreign bankers. (In 1575, this came as a surprise to the bankers.) Ina situation of asymmetric information, a suspension of payments may be anadditional argument for the Crown to convince the cities of the ‘evident necessity’of more funds. In 1575, the suspension of payments also provided an opportunityto review dealings in the collaterals of the asientos.

A crisis after a suspension of payments lasted until the Crown settled first withthe cities, and then with the bankers in a final document called the Medio General.(There was no Medio General in the resolution of the 1560 crisis.)The bankers mayhave taken a debt reduction, but the empirical evidence about the exact amount ofdebt reduction is not clear at this point. The cities accepted higher taxes in thesettlements of 1560 and 1577. In 1598, taxes were not increased but the interestrate was reduced on some juros. However, that settlement should be viewed as aprelude to the next negotiations of 1607, after the death of Philip II, as thetemporary settlement of 1558 preceded that of 1560. A key feature of eachsettlement was the conversion of all the asientos, net of any debt reduction, intolong-term juros.That feature has been neglected in the literature but reinforces ourinterpretation of the debt policy of the kingdom of Castile. We now analyse thethree crises in more detail.

V

The events of 1557–60 must be considered as one single, long financial crisis. Atthe beginning of his reign in 1556, Philip II inherited from his father, Charles V, adebt of 7.5 million ducats in asientos.42 He ordered a review of the accounts andbegan negotiations with some bankers to refinance asientos into juros. However, theservice of the debt was reaching the total amount of ordinary revenues, leaving noroom for more juros (figure 2). On 17 April 1557, Philip II declared his firstsuspension of payments.

The decree was not intended to repudiate the asientos, even partially. It declareda conversion of some asientos into juros at 5 per cent—the bankers could sell theseon the market.43 That conversion did not apply to the Fuggers who were, at the

41 Because of the decentralization of the juros, their service in some towns may be up to the revenue constraintbefore the aggregate service reaches the aggregate ordinary revenues (fig. 3).

42 Carlos Morales, Felipe II, p. 38. See also a report from March 1557 (AGS, Estado, leg. 121, fo. 61) that isreferenced by Toboso Sánchez, La deuda pública, p. 115. The computation of the short-term debt is alwaysapproximate. Asientos were not traded in a market and the indebtedness on a particular contract at a particularpoint of time depends on assumptions about the interest rates and the exchange rates. There is no such thing as‘the interest rate’, in today’s economies and a fortiori, in the fragmented capital market of Castile.

43 Ruiz Martín, ‘Un expediente financiero’, p. 11, reports that for the year 1552, 47% of the juros wereredeemable. In that type, 47.6% paid a rate of 7.14%, 5.2% a rate of 5.5% and 30% a rate of 5%.The remaining16% paid other rates.

DEBT POLICY UNDER CONSTRAINTS 11

© Economic History Society 2013 Economic History Review (2013)

time, some of the main creditors, and it did not address the main problem, whichwas the ceiling on ordinary revenues. The second part of the policy was thepromulgation on 30 April 1558, by the regent in Castile, the princess Doña Juana,of a new tax on wool exports. New customs were also created between Portugaland Castile on 30 January 1559.44

Genoese bankers had accepted the juros at 5 per cent in order to settle thenegotiations. However, juros at 7.14 per cent were obviously selling faster than jurosat 5 per cent. The bankers therefore proposed to undertake the conversion intojuros at a rate between 7.14 and 10 per cent in the following years, while theygranted new asientos. That policy, which was probably viewed as a stopgap, wasinitiated by Nicolao de Grimaldo in May 1558 and followed by all other bankersbetween 1558 and 1560.

When Philip II returned from Flanders to Castile for the first time as king on 8September 1559, he intended to put the finances of the Crown in order. Hesummoned the Cortes in Toledo and ordered a general review of the budget. Thestock of juros was 21.7 million ducats, with an interest service of 1.5 million.45

The debt in asientos was 4.5 million, as the 1557 decree had refinanced onlysome of the short-term debt.46 Negotiations would last for the entire year. On14 November 1560, the king declared his second suspension of payment onthe asientos.

The conversion from asientos to juros was made possible because the 1559–60Cortes agreed to increase the alcabalas by 37 per cent, effective from 1562. Allasientos were then converted into juros. In the current state of knowledge, it isdoubtful that the first suspension of payments of Philip II generated any default onthe asientos. There was no Medio General after the suspensions of payments of1557–60. After the settlements, which were made separately between individualbankers and the Crown, the signing of new asientos resumed rapidly.47 From 1562onwards, juros de resguardo would be issued on the new alcabalas.

The crisis of 1573–7 was a pivotal moment for the finances of Philip II. As inother crises, the interaction between the Crown and the cities should take centrestage, and that power game began well before the suspension of payments in1575.48

Following the Dutch revolt in the late 1560s, military expenditures increasedrapidly during the early 1570s, both in Flanders and on the sea (the Battle ofLepanto occurred in 1571). As revenues from the Indies had decreased during thisperiod (see figure 1), the deficit increased. The encabezamiento had been fixed, innominal terms, in 1562. During the 1560s, the Crown increased the ordinaryrevenues through higher rates on existing taxes and through the introduction of

44 Ulloa, La Hacienda Real, p. 253.45 Pulido Bueno, La Corte, p. 76.46 Neri, Uomini d’affari, p. 83.47 Some asientos were written with non-tradable collaterals (juros de caución) at 7.14% (14,000 al millar). At the

same time, for one million ducats of the pre-1560 debt that had been paid in juros at 5% in the 1560 decree, therate was increased to 7.14%. The episode illustrates that the amount of debt reduction was raised in laternegotiations with the bankers. One cannot take the terms of a Medio General for an accurate estimation of theactual debt reduction.The gradual conversion of juros on the Casa de la Contratación into juros of higher grade wasimplemented through contract clauses in new asientos; Ulloa, La Hacienda Real, p. 763.

48 For the historical descriptions, see reference works: Fortea Pérez, Monarquía y Cortes, pp. 42–88; idem,‘¿Impuestos o servicios?’.

12 CARLOS ÁLVAREZ-NOGAL AND CHRISTOPHE CHAMLEY

© Economic History Society 2013 Economic History Review (2013)

new taxes and new regulated monopolies.49 Figure 2 illustrates the rise of theserevenues.Their growth stopped in the early 1570s for two reasons. First, there werelimited opportunities for an increase in the tax base, or in the existing rates.Second, most of these revenues were related to trade, which suffered after thebeginning of the Dutch revolt. In any case, these ordinary revenues were farmedout and could not support juros at the lowest rate, of the same type as those thatwere funded by the encabezamientos.

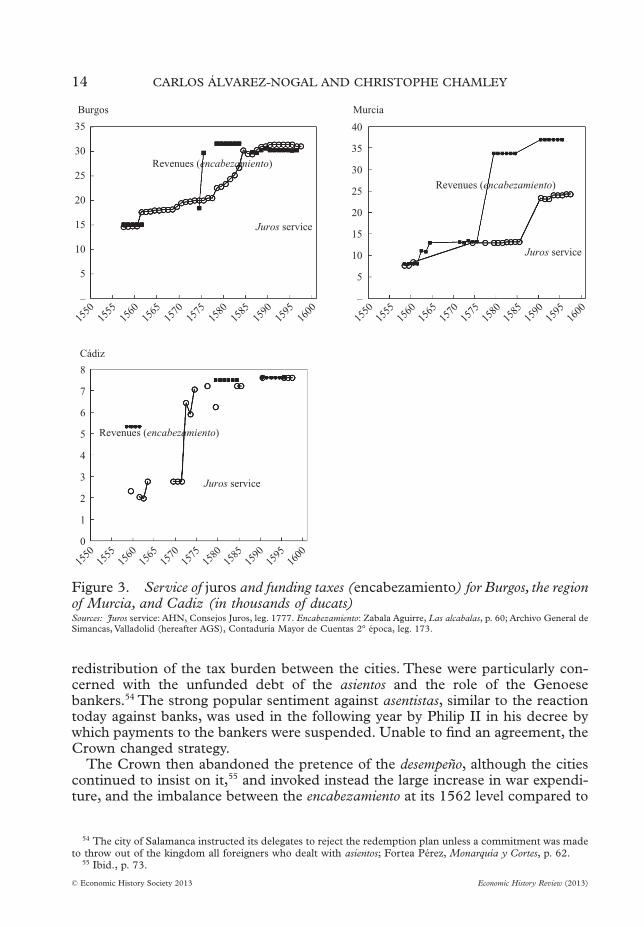

It was obvious that the service of the debt was absorbing most of the Crown’sordinary revenues (figure 2). As juros were issued against revenues from cities, thelocal constraints on these revenues became effective in some cities; for example, inBurgos and Murcia (figure 3).

The situation called for an increase in tax revenues for the funding of the publicdebt, and therefore it was necessary for the Cortes to meet. The crisis developedin two phases. First, from 1573 to 1575, the Crown made a number of attempts toobtain more revenues from the cities.When that process failed, the Crown prom-ulgated through a decree, in September 1575, a stop on the short-term debtpayments, and conducted negotiations on two fronts with the cities and thebankers.That second phase lasted until the final settlement, first with the cities atthe end of November 1577, and immediately afterwards with the bankers in theMedio General.50

The crisis began in April 1573, when Philip II summoned the Cortes and, as inprevious negotiations in 1559, proposed a 30-year plan to get rid of the public debt(desempeño):51 higher taxes would generate a surplus for 20 years and, for the last10 years, the burden would be reduced to finish off the remaining debt. Initially,the cities accepted the general idea of the plan, but they continued to negotiatethrough the Cortes. No stable agreement could be achieved without the formalapproval of all the cities.

While negotiations dragged on, Philip II tried a second plan in December 1573:a new flour tax would be created that would be applicable without exemption. Inthis way, the increased tax burden would be evenly distributed throughout theSpanish realm. The flour tax, even at a low rate, would have provided a hugeextension of the tax base.52 The cities strongly opposed the tax and insisted insteadon a commitment to a permanent reduction of taxation in the future, and to a stopon the sales of offices.53 The Cortes were suspended at the end of 1573 to enablethe delegates to return to their cities for consultation. Heated discussions delayedthe resumption of the Cortes until June 1574.

Each delegate came back with special ad hoc demands. As a further complica-tion, taxation of the clergy required a papal decree. During the summer of 1574,other issues were discussed, such as the formal transfer of the juros in quotas to thecities, which would then be free to choose how to service or redeem them, or the

49 In 1559, the customs tax base was extended. The import tax rate from the Americas was raised in 1566.Additional taxes on wool exports were introduced in 1558 and 1566. After 1564, a regulated monopoly wasintroduced to increase the revenues from the salt tax up to 0.2 million ducats (1/6 of the alcabalas). In 1563,another monopoly was introduced on the production of mercury.

50 Lovett, ‘Castilian bankruptcy’, p. 910; idem, ‘General Settlement’, p. 19.51 Fortea Pérez, Monarquía y Cortes, p. 45.52 The tax could have yielded between three and four million ducats; ibid., pp. 418–20.53 Furthermore, they were sceptical regarding the Crown’s commitment to a budget surplus—a claim no more

credible in the sixteenth century than it would be in the twenty-first.

DEBT POLICY UNDER CONSTRAINTS 13

© Economic History Society 2013 Economic History Review (2013)

redistribution of the tax burden between the cities. These were particularly con-cerned with the unfunded debt of the asientos and the role of the Genoesebankers.54 The strong popular sentiment against asentistas, similar to the reactiontoday against banks, was used in the following year by Philip II in his decree bywhich payments to the bankers were suspended. Unable to find an agreement, theCrown changed strategy.

The Crown then abandoned the pretence of the desempeño, although the citiescontinued to insist on it,55 and invoked instead the large increase in war expendi-ture, and the imbalance between the encabezamiento at its 1562 level compared to

54 The city of Salamanca instructed its delegates to reject the redemption plan unless a commitment was madeto throw out of the kingdom all foreigners who dealt with asientos; Fortea Pérez, Monarquía y Cortes, p. 62.

55 Ibid., p. 73.

35

Burgos

Cádiz

Murcia

30

25Revenues (encabezamiento)

Revenues (encabezamiento)

Juros service

Juros service

20

15

10

5

–

35

40

30

25

20

15

10

5

–

6

7

8

5

4

3

2

1

0

1560

1555

1550

1565

1570

1575

1580

1585

1590

1595

1600

1560

1555

1550

1565

1570

1575

1580

1585

1590

1595

1600

1560

1555

1550

1565

1570

1575

1580

1585

1590

1595

1600

Revenues (encabezamiento)

Juros service

Figure 3. Service of juros and funding taxes (encabezamiento) for Burgos, the regionof Murcia, and Cadiz (in thousands of ducats)Sources: Juros service: AHN, Consejos Juros, leg. 1777. Encabezamiento: Zabala Aguirre, Las alcabalas, p. 60; Archivo General deSimancas, Valladolid (hereafter AGS), Contaduría Mayor de Cuentas 2° época, leg. 173.

14 CARLOS ÁLVAREZ-NOGAL AND CHRISTOPHE CHAMLEY

© Economic History Society 2013 Economic History Review (2013)

the increase in other tax revenues. During these protracted negotiations, the gapbetween the ordinary revenues and the interest service of the juros continued toclose.

On 20 September 1574, Philip II tripled the encabezamiento general from 1.2 to3.7 million.56 The policy was extraordinary in its timing and amount. All previouslevels of the encabezamientos in 1536, 1547, 1552, and 1562 had been determinedduring meetings of the Cortes. Without the cities’ agreement the tax could nothave been expected to be stable. Legally, it was just another extraordinary levy.Despite Philip II’s efforts to employ a special task force of ‘administrators, tax-farmers and public inspectors’,57 it is doubtful that the decree of 1574 was actuallyimplemented.58 Why Philip II insisted on such a large increase is not clear.Obviously, a smaller increase would have provided sufficient room for greater debtservice—as was the case for another 10 years after the final settlement of 1577.Since the encabezamiento had not changed since 1562 with a fall in real value of12 per cent, and since the cities eventually accepted, in 1577, a doubling of theencabezamiento, it is clear that if the issue had been a liquidity crisis the Crowncould have obtained agreement on a modest tax increase. However, the Crown haddecided from 1573 onwards to obtain a large increase of revenues and it wasengaged in a power play with the cities.

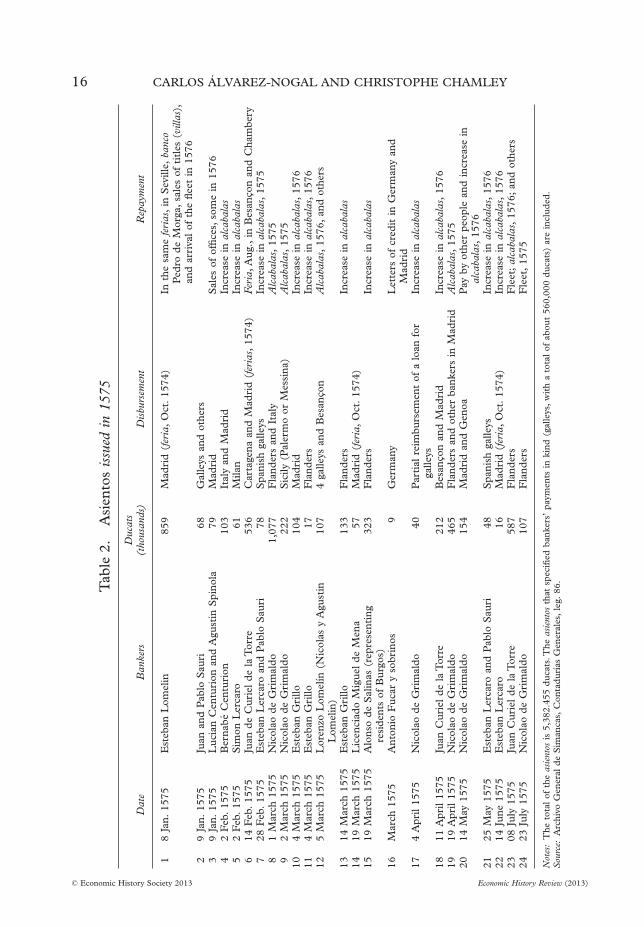

Philip II signed a decree that put a stop to payments to the Genoese bankers on1 September 1575, following the arrival of the fleet on 11 August 1575.59 During1574, new asientos had been issued to an amount of 6.219 million ducats, close tothe record level of 1572 (6.248 million ducats).That total included 2.658 millionducats to be paid in Flanders, about 3 million ducats in Castile, and the rest inItaly.60 A complete list of all the asientos signed between January and the suspen-sion of payments is presented in table 2.

During the eight months before the suspension in September 1575, Genoesebankers signed new asientos for 4.8 million ducats, the highest amount within sucha short interval. Between March and July, Nicolao de Grimaldo made the mostimportant loans, by far, for a total amount of 1.9 million ducats. The first one(1.3 million ducats) was provided for disbursements during 1575 and repaymentsby the king during the same year in three tranches after each four-month period(37.5 per cent for each of the first two). The short maturity of that loan showsthat Grimaldo was prudent. All bankers must have been cognizant of the financialsituation of the Crown. As moneyed men, they had close ties with the governmentin Castile. Some may even have participated in financial committees of the gov-ernment.The cities would resist an increase in the alcabalas, but the bankers wereconfident that there was a base for higher taxes and many of the asientos during thespring of 1575 were written on the promise of higher alcabalas from 1575 onwards.The situation is easy to picture in the context of the current lending crisis in

56 It was expected that a large part of the increase would come from an extension of the tax base to includebread, wine, fruit, and agricultural products that had so far been exempted de facto, and would now be taxed atabout 4 %; ibid., p. 71.

57 Jago, ‘Philip II’, p. 31; Hernández Esteve, Establecimiento de la partida doble, pp. 164–5.58 Thompson, ‘Castile’, p. 169, claims that revenues could even have decreased, in reaction to the tax jump.59 Revenues from the Indies in 1575 were 0.9 million ducats, about a 50% increase on the average of the

previous three years.60 AGS, Contadurías Generales, leg. 86.

DEBT POLICY UNDER CONSTRAINTS 15

© Economic History Society 2013 Economic History Review (2013)

Tab

le2.

Asi

ento

sis

sued

in15

75

Dat

eB

anke

rsD

ucat

s(t

hous

ands

)D

isbu

rsem

ent

Rep

aym

ent

18

Jan.

1575

Est

eban

Lom

elin

859

Mad

rid

(fer

ia,

Oct

.15

74)

Inth

esa

me

feri

as,

inS

evill

e,ba

nco

Ped

rode

Mor

ga,

sale

sof

titl

es(v

illas

),an

dar

riva

lof

the

fleet

in15

762

9Ja

n.15

75Ju

anan

dP

ablo

Sau

ri68

Gal

leys

and

othe

rs3

9Ja

n.15

75L

ucia

nC

entu

rion

and

Agu

stin

Spi

nola

79M

adri

dS

ales

ofof

fices

,so

me

in15

764

2F

eb.

1575

Ber

nabé

Cen

turi

on10

3It

aly

and

Mad

rid

Incr

ease

inal

caba

las

52

Feb

.15

75S

imon

Ler

caro

61M

ilan

Incr

ease

inal

caba

las

614

Feb

.15

75Ju

ande

Cur

iel

dela

Tor

re53

6C

arta

gena

and

Mad

rid

(fer

ias,

1574

)Fe

ria,

Aug

.,in

Bes

anço

nan

dC

ham

bery

728

Feb

.15

75E

steb

anL

erca

roan

dP

ablo

Sau

ri78

Spa

nish

galle

ysIn

crea

sein

alca

bala

s,15

758

1M

arch

1575

Nic

olao

deG

rim

aldo

1,07

7F

land

ers

and

Ital

yA

lcab

alas

,15

759

2M

arch

1575

Nic

olao

deG

rim

aldo

222

Sic

ily(P

aler

mo

orM

essi

na)

Alc

abal

as,

1575

104

Mar

ch15

75E

steb

anG

rillo

104

Mad

rid

Incr

ease

inal

caba

las,

1576

114

Mar

ch15

75E

steb

anG

rillo

17F

land

ers

Incr

ease

inal

caba

las,

1576

125

Mar

ch15

75L

oren

zoL

omel

ín(N

icol

asy

Agu

stin

Lom

elin

)10

74

galle

ysan

dB

esan

çon

Alc

abal

as,

1576

,an

dot

hers

1314

Mar

ch15

75E

steb

anG

rillo

133

Fla

nder

sIn

crea

sein

alca

bala

s14

19M

arch

1575

Lic

enci

ado

Mig

uel

deM

ena

57M

adri

d(f

eria

,O

ct.

1574

)15

19M

arch

1575

Alo

nso

deS

alin

as(r

epre

sent

ing

resi

dent

sof

Bur

gos)

323

Fla

nder

sIn

crea

sein

alca

bala

s

16M

arch

1575

Ant

onio

Fuc

ary

sobr

inos

9G

erm

any

Let

ters

ofcr

edit

inG

erm

any

and

Mad

rid

174

Apr

il15

75N

icol

aode

Gri

mal

do40

Par

tial

reim

burs

emen

tof

alo

anfo

rga

lleys

Incr

ease

inal

caba

las

1811

Apr

il15

75Ju

anC

urie

lde

laT

orre

212

Bes

anço

nan

dM

adri

dIn

crea

sein

alca

bala

s,15

7619

19A

pril

1575

Nic

olao

deG

rim

aldo

465

Fla

nder

san

dot

her

bank

ers

inM

adri

dA

lcab

alas

,15

7520

14M

ay15

75N

icol

aode

Gri

mal

do15

4M

adri

dan

dG

enoa

Pay

byot

her

peop

lean

din

crea

sein

alca

bala

s,15

7621

25M

ay15

75E

steb

anL

erca

roan

dP

ablo

Sau

ri48

Spa

nish

galle

ysIn

crea

sein

alca

bala

s,15

7622

14Ju

ne15

75E

steb

anL

erca

ro16

Mad

rid

(fer

ia,

Oct

.15

74)

Incr

ease

inal

caba

las,

1576

2308

July

1575

Juan

Cur

iel

dela

Tor

re58

7F

land

ers

Fle

et;

alca

bala

s,15

76;

and

othe

rs24

23Ju

ly15

75N

icol

aode

Gri

mal

do10

7F

land

ers

Fle

et,

1575

Not

es:

The

tota

lof

the

asie

ntos

is5,

382.

455

duca

ts.T

heas

ient

osth

atsp

ecifi

edba

nker

s’pa

ymen

tsin

kind

(gal

leys

,w

ith

ato

tal

ofab

out

560,

000

duca

ts)

are

incl

uded

.S

ourc

e:A

rchi

voG

ener

alde

Sim

anca

s,C

onta

durí

asG

ener

ales

,le

g.86

.

16 CARLOS ÁLVAREZ-NOGAL AND CHRISTOPHE CHAMLEY

© Economic History Society 2013 Economic History Review (2013)

Greece. The bankers knew that the situation was risky, but they would not havemade these record loans in the spring of 1575 if they had anticipated the suspen-sion in September.

After Philip II had given a clear signal in the decree both of his need for morerevenues and of his toughness towards the resented asentistas, he again called theCortes to begin negotiations in November.61 The business of the Cortes was toreadjust three types of taxes, the encabezamiento of the alcabalas, the ordinaryservice, and the extraordinary service. The usual sequence was to agree on theservicio ordinario and the servicio extraordinario first, and then to bargain on themain item, the encabezamiento.This time, however, the Cortes, in order to increasetheir bargaining power, reversed the order and requested first a renegotiation ofthe 1574 decree (which had tripled the encabezamiento), before voting on the twoservices.

Negotiations were very slow. Why did Philip II reject his impatient aides’ facileadvice to use force? We think that he had at least two motives. First, he knew thathe had to play a political game with the cities that represented the realm, and thatthe game was likely to be repeated. Second, Philip II was rational and he probablyanticipated the eventual consequences of the suspension of payments for the creditmarket and the trading activities of the cities. We discuss this issue briefly below.

It took almost a year, until August 1576, to agree to move the servicio ordinarioup the agenda, before the encabezamiento. Then the negotiations dragged onfor more than another year, until 29 October 1577. In previous adjustmentsof the encabezamiento, increases had been roughly proportional across cities.For the contract of 1577, however, the shares of some cities jumped up: Sevillefrom 10.2 per cent in 1557 to 17.5 per cent in 1577, and Toledo from 5.8 to7.6 per cent, while Granada’s share dropped from 9.2 to 5 per cent.62 After theagreement on the encabezamiento, voting on the servicio extraordinario was accel-erated and a final agreement was reached in the following month.

For the Crown and also for the Genoese bankers, the suspension of paymentsdid not mean a default to the bankers. Before the end of the year, the Crown setthe principle that all the debt would be paid at 12 per cent. The question was,which debt? Recent literature has emphasized the role of bankruptcy as theoutcome of an efficient loan contract that saves the cost of information that mustbe acquired by the lender.63 In 1575, one could argue that the need for moreinformation was on the side of the borrower, Philip II. A simple theoretical modelthat captures the complexity of the network of asientos and their related side-contracts is beyond the scope of this article. Because of these intertwined side-contracts, especially on the collaterals, there was a dire need for a review of all thecontracts. That review had to be comprehensive because of the connectionsbetween loans and collaterals in juros, and in order to achieve an orderly conversionof all short-term asientos into long-term juros.

Because the bankers substituted some of the asiento’s collaterals (juros deresguardo) with juros of lower grade, the liabilities of the different parties weredifficult to assess.This justified the Crown’s creation of a commission to review allasientos that had been signed since 14 November 1560: 296 contracts with 66

61 Fortea Pérez, Monarquía y Cortes, p. 248.62 Zabala Aguirre, Las alcabalas, pp. 55–98, and esp. tab. 9, p. 64.63 Townsend, ‘Optimal contracts’.

DEBT POLICY UNDER CONSTRAINTS 17

© Economic History Society 2013 Economic History Review (2013)

people (35 with Nicolao de Grimaldo, 34 with Lucian Centurion, 32 with LorenzoSpinola, and so on). The balance of each active asiento was computed by bring-ing past payments up to the current date with the standard interest rate of12 per cent.64

The Crown and the bankers agreed on the amount of 15.2 million ducats in theearly spring of 1577, as stated in the final settlement. The larger part of the debtwas not in unpaid arrears, but in repayments that were contractually scheduled forthe future.We have examined all the asientos that were initiated between 1570 and1575 (and some before 1570), and extracted those that specify contracts after1575.The total amount of the payments scheduled after 1575 exceeded 12 millionducats. Given the average maturity of these remaining liabilities, an approximateestimate of the present value of the scheduled repayments is about 10 millionducats. Arrears would then represent about 5 million ducats.65

The terms of the final settlement between the Crown and the bankers had beenset in March 1577, but the signing of the settlement had to wait, with no significantchange, for another nine months until the end of the negotiations in the Cortes.The long delay between the agreement with the bankers in March 1577 and thesignature in December after the closing of the Cortes is additional evidence thatthe difficult negotiations between the Crown and the cities was the major cause ofthe suspension of payments. Immediately after the agreement in the Cortes, theMedio General was signed between the Crown and the bankers on 5 December1577.

A powerful incentive for the cities to settle was the adverse impact of the crisison the domestic credit market and trade.We have seen that a large fraction of theasientos was internal to Castile. Like the moneyed men of eighteenth-centuryEngland, the Rothschilds in the Napoleonic era, or modern bankers today, themain role of Genoese bankers was to underwrite loans, and not to lend on theirown funds. It is very likely that the funds for the asientos that were disbursed inCastile came from Castile.

The suspension of payments on the asientos also put a stop to the main fairs atMedina del Campo. They eventually resumed, in 1578, but they had lost theirpre-eminence in the network of commercial fairs and never regained it.

In the settlement, the debt of 15.2 million ducats was divided into two parts:10.4 and 4.8 million ducats, respectively.66 The first part, 10.4 million ducats,corresponded to juros: 8 million ducats were paid by juros de resguardo that hadbeen written at 7.14 per cent and were reduced to 5 per cent. The remaining2.4 million ducats corresponded to juros written on the Casa de la Contrataciónand were accounted for at their market value, 55 per cent of the face value. Thesecond part of the debt, 4.8 million ducats, was subdivided into two parts.Two-thirds were paid by juros on salt at the rate of 3.3 per cent (30,000 al millar).For the remaining third, the holders of asientos were compensated by the monetaryequivalent of property rights on individuals (vasallos) and of the granting of legalpowers (jurisdicciones) on some church territories that had been allowed by a bull

64 Carlos Morales, Felipe II, p. 164.65 The existence of arrears is also confirmed by the terms of some asientos signed before 1575 that included

clauses for the payments of arrears.66 We use rounded numbers. The Medio General specified exact numbers that can be found in the literature;

Carlos Morales, Felipe II, p. 178. Here, the exact amount is 15,184,464 ducats.

18 CARLOS ÁLVAREZ-NOGAL AND CHRISTOPHE CHAMLEY

© Economic History Society 2013 Economic History Review (2013)

of Gregory XIII on 6 April 1574. The values of these effects were computed withdiscount rates at 6.5 and 2.35 per cent (16,000 and 42,500 al millar) dependingwhere they were situated in Castile.

We emphasized in the introduction that some details of the settlement with thebankers are critical for its interpretation and for the evaluation of any debtreduction. As shown in the description of the juros, the reduction of the interestrate from 7 to 5 per cent could not be a default, contrary to previous literaturecited above.We also noted previously that the reference to a unique interest rate onjuros would be ahistorical because of the fragmented credit market.The reductionof the interest on old juros through the crecimiento necessarily implied the coexist-ence of juros with different interest rates that had different expectations of redemp-tion and were arbitraged by the market.The actual interest rate on juros dependedon the marketability of new juros. Ruiz Martin has provided some evidence of jurosat 5 per cent that traded during the period of 1570 to 1575 for 17,000 al millar,which is equivalent to a rate of 5.88 per cent.67 In the archives of Simancas, thereare numerous documents that show sales of juros at 5 per cent, or even lower (seebelow), throughout the 1570s.68

After the signing of the Medio General, the Crown issued a number of orders tospecify the details of the payments. Under some special provisions, bankers couldbe in charge of applying the crecimiento to some juros and recovering the proceed-ings from reimbursements for asientos.

With regard to the second part of the debt (4.8 million ducats), the terms of theMedio General do not enable us to have a precise evaluation of the terms of thesettlement. The rate of the juros written on the salt tax was equal to 3.33 per cent(30,000 al millar).There is some indication that the ‘market rate’ of such juros wasless than 5 per cent, but this issue is yet to be researched. If we apply the samediscount to the other third of the debt of 4.8 million ducats, the upper bound forthe reduction of the 1575 short-term debt is equal to 1.6 million, that is, 11 percent of the total.69

In 1588, the disaster of the Great Armada was apparent to all, without asym-metric information on the revenue needs of the Crown (as mentioned in the recordof the 1589 Cortes). Although the debt service was far below the ordinary revenues(figure 2), the cities quickly granted a special tax. Patriotism trumped tax smooth-ing. It was levied like the alcabalas under the encabezamiento, but the cities insistedon the specific purpose of the tax, which was given a different name, the servicio demillones, and the payment was limited to a term of six years.

When the millones ended in 1596, as scheduled, the service of the long-termdebt, which had gradually increased since the previous settlement, had reached thelevel of the funding revenues (figure 2). The Crown first attempted to renew themillones, under a different name (the cuentos).70 After no majority agreement couldbe reached in the Cortes, the government abandoned the project, leaving itsimplementation to the next king, Philip III.

67 Ruiz Martín, ‘Las finanzas españolas’.68 For more details, see the working paper and data at http://people.bu.edu/chamley/papers/documents/

juros1572.pdf.69 Some decrees after 1577 compensated bankers for losses that they had incurred in the settlement of 1577.70 Fortea Pérez, Monarquía y Cortes, p. 155.

DEBT POLICY UNDER CONSTRAINTS 19

© Economic History Society 2013 Economic History Review (2013)

As in the previous crisis of 1575, the crisis of 1596 was not caused by a liquidityproblem but by the refusal of the cities to raise taxes.This imposed a ceiling on thedomestic debt.71 If the ratio between the service of the long-term debt and thefunding revenues had been the same as in the early 1590s, no crisis would haveoccurred.

The decree was published on 29 November 1596, again to the surprise of theasentistas and to the satisfaction of the cities.72The total debt recognized by the kingwas 7 million ducats.73 Unlike 1575, the suspension of payments to the Genoesebankers was not used as a device to increase ordinary revenues. Economic activityhad stopped growing since the 1580s, which explains the fact that the ordinaryrevenues were stationary (figure 1). The Crown and the Cortes probably felt thathigher domestic taxation would be difficult to enforce. On the other hand, interestrates on juros had decreased since the previous financial crisis. The conversion ofasientos into juros was achieved by a combination of interest reduction and issuanceof juros on some available ordinary revenues that were less stable.74 We havedescribed previously how interest reductions through crecimientos were not defaults.

VI

The fiscal system of Philip II was much more ingenious than previous literaturesuggests.We have shown how it was adapted to the constraints of its time and thatits evaluation according to the standards of twenty-first-century economies canlead to serious misinterpretation.The main achievement of Philip II’s governmentwas to mobilize large financial resources by transforming the apparent weakness ofthe kingdom’s fragmented political and economic institutions into a strength.Thisallowed the king to build the domestic public debt to something akin to that ofmodern magnitude.

Philip II’s suspensions of payments were not caused by liquidity problems butwere part of the overall efficiency of the system.Thompson, who is an exception inthe literature, was the first to express that point of view.75 To apply the expression‘serial defaulter’ to Philip II is thus an error of interpretation. Furthermore,evidence about the actual dealings between the government (Tesoro General) andthe Genoese bankers seems to indicate that a significant part of alleged reductionswere transactions at prices not far from market values. An exact computation of theactual debt reduction would require the examination of documents in the yearsafter the crisis resolutions and is thus beyond the scope of the present paper.

Many aspects of the finances of Castile under Philip II, large and small, are yetto be examined. The archives in Simancas contain a large amount of informationthat will be useful for this task. In future work, the fiscal system of Philip II should

71 The shortfall of the millones (1.33 million ducats) was compensated for by the high silver revenues, 6.2million and 3.5 million ducats in 1595 and 1596, compared to an average of 1.225 million for 1591–4 (fig. 1).

72 Ulloa, La Hacienda Real, p. 820.73 Sanz Ayán, ‘Procedimientos’, p. 30, gives a figure of 7 million ducats, while Ulloa, La Hacienda Real, p. 823,

gives a figure of 7,831,251 ducats.74 See above, n. 67.75 ‘This very periodicity [of the fiscal crises] suggests that rather than the manifestation of “crisis” these

“bankruptcies” were an integral part of the financial system of the Monarchy. The term “bankruptcy” can bemisleading’; Thompson, ‘Castile’, p. 160.

20 CARLOS ÁLVAREZ-NOGAL AND CHRISTOPHE CHAMLEY

© Economic History Society 2013 Economic History Review (2013)

also be integrated with the history of political institutions and studies by historianswho highlight the high degree of autonomy of the cities in the kingdom of Castile.

Date submitted 17 January 2012Revised version submitted 16 November 2012Accepted 21 November 2012

DOI: 10.1111/1468-0289.12010

Footnote referencesÁlvarez-Nogal, C. and Prados de la Escosura, L., ‘The decline of Spain, 1500–1850: conjectural estimates’,

European Review of Economic History, 11 (2007), pp. 319–66.Andrés Díaz, R. d., El último decenio del reinado de Isabel I a través de la tesorería de Alonso de Morales (1495-1504)

(Valladolid, 2003).Artola, M., La Hacienda del Antiguo Régimen (Madrid, 1982).Barro, R. J., ‘Government spending, interest rates, prices, and budget deficits in the United Kingdom,

1701–1918’, Journal of Monetary Economics, 20 (1987), pp. 221–47.Barthe Porcel, J., Los juros (desde el juro de heredat hasta la desparición de los cargos de justicia, siglos XIII al XX),

Anales Universidad (Murcia, 1949).Bean, R., ‘War and the birth of the nation state’, Journal of Economic History, 33 (1973), pp. 203–21.van Bochove, C., ‘Intermediaries and the secondary market for public debt in the Dutch Republic’, Utrecht Univ.

working paper (2012).Brewer, J., The sinews of power (Cambridge, 1988).Carlos Morales, C. J. d., Felipe II: el imperio en bancarrota. La Hacienda Real de Castilla y los negocios financieros del

rey Prudente (Madrid, 2008).Chamley, C., ‘Interest reductions in the politico-financial nexus of 18th century England’, Journal of Economic

History, 71 (2011), pp. 555–89.Conklin, J., ‘The theory of sovereign debt and Spain under Philip II’, Journal of Political Economy, 106 (1998),

pp. 483–514.Dickson, P. G. M., The financial revolution in England: a study in the development of public credit 1688–1756 (1967).Drelichman, M. and Voth, H.-J., ‘The sustainable debts of Philip II: a reconstruction of Spain’s fiscal position,

1566–1596’, Journal of Economic History, 70 (2010), pp. 814–43.Elliott, J. H., ‘A Europe of composite monarchies’, Past and Present, 137 (1992), pp. 48–71.Fortea Pérez, J. I., Monarquía y Cortes en la Corona de Castill:. las ciudades ante la política fiscal de Felipe II

(Salamanca, 1990).Fortea Pérez, J. I., ‘¿Impuestos o servicios?: Las Cortes de Castilla y la política fiscal de Felipe II (1573–1598)’,

in J. I. Fortea Pérez, ed., Las Cortes de Castilla y León bajo los Austrias: una interpretación (Valladolid, 2008),pp. 161–89.

Gelabert, J. E., La bolsa del rey: rey, reino y fisco en Castilla (1598–1648) (Barcelona, 1997).Gelderblom, O. and Jonker, J., ‘Public finance and economic growth: the case of Holland in the seventeenth

century’, Journal of Economic History, 71 (2011), pp. 1–39.Grafe, R., Distant tyranny: markets, power, and backwardness in Spain, 1650–1800 (Princeton, N.J., 2012).Green, E. J., ‘On the emergence of parliamentary government: the role of private information’, Quarterly Review,

17 (1993), pp. 2–16.Hernández Esteve, E., Establecimiento de la partida doble en las cuentas centrales de la Real Hacienda de Castilla

(1952), vol. I (Madrid, 1986).Hopkins, K., ‘Rome, taxes, rents and trade’, in W. Scheidel and S. von Reden, eds., The ancient economy (1995),

pp. 190–230.Irigoin, A. and Grafe, R., ‘Bargaining for absolutism: a Spanish path to nation-state and empire building’,

Hispanic American Historical Review, 88 (2008), pp. 173–209.Jago, C., ‘Philip II and the Cortes of Castile: the case of the Cortes of 1576’, Past and Present, 109 (1985),

pp. 24–43.Lorenzo Sanz, E., Comercio de España con América en la época de Felipe II (Valladolid, 1979).Lovett, A., ‘The Castilian bankruptcy of 1575’, Historical Journal, 23 (1980), pp. 899–911.Lovett, A., ‘The General Settlement of 1577: an aspect of Spanish finance in the early modern period’, Historical

Journal, 25 (1982), pp. 1–22.Martín Acosta, M. E., El dinero americano y la política del Imperio (Madrid, 1992).Neri, E., Uomini d’affari e di governo tra Genova e Madrid (secoli XVI e XVII) (Milán, 1989).O’Callaghan, J. F., The Cortes of Castile-León, 1188–1350 (Philadelphia, Pa., 1989).Pérez-Prendes, J. and Torres López, M., Los juros: aportación documental para una historia de la deuda pública en

España (Madrid, 1963).

DEBT POLICY UNDER CONSTRAINTS 21

© Economic History Society 2013 Economic History Review (2013)

Pezzolo, L., ‘Government debts and credit markets in Renaissance Italy’, in F. Piola Caselli, ed., Government debtsand financial markets in Europe (2008), pp. 17–33.

Pulido Bueno, I., La Corte, las Cortes y los mercaderes: política imperial y desempeño de la Hacienda Real en la Españade los Austrias (Huelva, 2002).

Reinhart, C. M. and Rogoff, K., This time is different: eight centuries of financial folly (2009).Ruiz Martín, F., ‘Un expediente financiero entre 1560 y 1575: La Hacienda de Felipe II y la Casa de la

Contratación de Sevilla’, Moneda y Crédito, 92 (1965), pp. 3–58.Ruiz Martín, F., ‘Las finanzas españolas durante el reinado de Felipe II’, Cuadernos de Historia.Anexos de la Revista

‘Hispania 2 Extra’, 2 (1968), pp. 109–73.Sanz Ayán, C., ‘Procedimientos de la Monarquía ante la suspensión de pagos de 1596’, in C. Sanz Ayán, ed.,

Estado, monarquía y finanzas: estudios de historia financiera en tiempos de los Austrias (Madrid, 2004), pp. 21–37.Thompson, I. A. A., ‘Castile: polity, fiscality, and fiscal crisis’, in P.T. Hoffman and K. Norberg, eds., Fiscal crisis,

liberty, and representative government, 1450–1789 (Stanford, Calif., 1994), pp. 140–81.Toboso Sánchez, P., La deuda pública castellana durante el Antiguo Régimen (Juros) y su liquidación en el siglo XIX

(Madrid, 1987).Townsend, R. M., ‘Optimal contracts and competitive markets with costly state verification’, Journal of Economic

Theory, 21 (1979), pp. 265–93.Tracy, J. D., A financial revolution in the Habsburg Netherlands: renten and renteniers in the County of Holland,

1515–1565 (Berkeley, Calif., 1985).Tracy, J. D., Emperor Charles V, impresario of war: campaign strategy, international finance, and domestic politics

(Cambridge, 2002).Ulloa, M., La Hacienda Real de Castilla en el reinado de Felipe II (Madrid, 1977).Vührer, A., Histoire de la dette publique en France (Paris, 1886).Zabala Aguirre, P., Las alcabalas y la Hacienda Real en Castilla. Siglo XVI (Santander, 2000).