Embed Size (px)

Citation preview

DEBT AND TRADE: MAKING LINKAGES FOR THE PROMOTION OF DEVELOPMENT

DE

BT

AN

D T

RA

DE

: MA

KIN

G LIN

KA

GE

S F

OR

TH

E P

RO

MO

TIO

N O

F D

EV

ELO

PM

EN

T

1225 Otis Street, NEWashington, DC 20017

United States 202.635.2757 | PHONE

202.832.9494 | FAX

www.coc.org

DEBT AND TRADE:

MAKING LINKAGES FOR THE

PROMOTION OF DEVELOPMENT

REPORT FROM A POLICY ROUNDTABLE

GENEVA, SWITZERLAND

Edited by Aldo Caliari

THE SOUTH CENTRE

In August 1995, the South Centre became a permanent intergovernmental organization of developing countries. In pursuing its objectives of promoting South solidarity, South-South cooperation, and

coordinated participation by developing countries in international forums, the South Centre prepares, publishes and distributes information, strategic analyses and recommendations on international economic, social and political matters of concern to the South. For

detailed information about the South Centre see its website www.southcentre.org.

The South Centre enjoys support from the governments of its member countries and of other countries of the South, and is in regular working contact with the Group of 77 and the Non-Aligned Movement. Its

studies and publications benefit from technical and intellectual capacities existing within South governments and institutions and among individuals of the South. Through working group sessions and

consultations involving experts from different parts of the South, and also from the North, common challenges faced by the South are studied and experience and knowledge are shared.

THE CENTER OF CONCERN

Rooted in Catholic social tradition, the Center of Concern works collaboratively to create a world where economic and social systems guarantee basic rights, uphold human dignity, promote sustainable livelihoods and renew Earth. (www.coc.org)

ACKNOWLEDGMENTS

This publication and the event that it documents were made possible thanks to generous support provided by (in alphabetical order) the Agence Française de Développement (AFD), the Ford Foundation, the

Forum for Environment and Development (Norway), Oxfam Novib, the United Nations Conference on Trade and Development, the United Nations Foundation and the Swedish Ministry of Foreign Affairs.

The contents of this publication or the views and perspectives expressed do not necessarily reflect the official opinions or policy positions of the United Nations Conference for Trade and Development or its member

States, South Centre or its member States, the Center of Concern, the Agence Française de Développement (AFD), the Ford Foundation, the Forum for Environment and Development (Norway), Oxfam Novib, the United Nations Foundation and the Swedish Ministry of Foreign Affairs.

Reproduction of all or part of this publication for educational or other non-commercial purposes is authorized without prior written permission from the copyright holder provided that the source is fully

acknowledged and any alterations to its integrity are indicated. Reproductions of this publication for resale or other commercial purposes is prohibited without prior consent of the copyright holder.

Center of Concern, 1225 Otis St., NE, Washington DC, 20017, USA

© Center of Concern, 2009

DEBT AND TRADE:

MAKING LINKAGES FOR THE

PROMOTION OF DEVELOPMENT

TABLE OF CONTENTS

DEBT AND TRADE: MAKING LINKAGES FOR THE

PROMOTION OF DEVELOPMENT—AN INTRODUCTION Aldo Caliari and Vicente Paolo Yu........................................................... i

OPENING ADDRESS: LINKING DEBT, TRADE AND

FINANCE ISSUES

Yash Tandon .............................................................................................. xi

I. THE POLITICAL DIMENSIONS OF LINKING

DEBT AND TRADE .................................................................... 1

I.1 TIME FOR CHANGE IN GLOBAL TRADE AND FINANCIAL

GOVERNANCE.

Barry Herman.......................................................................... 1

II. THE TECHNICAL DIMENSIONS OF LINKING

DEBT AND TRADE ................................................................... 18

II.1. THE DEBT TRADE CAUSALITY IN BALANCE OF PAYMENTS

ACCOUNTING.

Jan Kregel ........................................................................... 18

II.2. CONCEPTUALIZING SOVEREIGN DEBT

Matthias Rau. ...................................................................... 24

III. THE POTENTIAL AND LIMITATIONS OF MARKET

ACCESS TRADE TRENDS AND WHAT THEY MEAN

IN TERMS OF INCOME GAINS FOR DEVELOPING

COUNTRIES................................................................................ 29

III.1. TRADE TRENDS AND WHAT THEY MEAN FOR

INCOME TRENDS OF DEVELOPING COUNTRIES Mr. Jörg Mayer ................................................................. 29

III.2. EXPORT-LED GROWTH BASED ON MANUFACTURES

Mr. Arslan Razmi .............................................................. 37

III.3. TEXTILES AND PREFERENCE EROSION:

THE CASE OF MAURITIUS

Mr. Umesh Sookmani ........................................................42

III.4. Mr. Matthew Odedokun ....................................................48

IV. ISSUES IN THE EXPORT GROWTH-DEBT

REPAYMENT LINK ...................................................................53

IV.1. Ms. Lida Nunez ...................................................................53

IV.2. Mr. Richard Kozul-Wright .................................................60

V. FOREIGN DIRECT INVESTMENT RULES AND THEIR

EFFECTS ON DEBT ...................................................................67

V.1. Professor Andreas Antoniou ..............................................67

V.2. Mr. Alfredo Calcagno ..........................................................70

V.3. Ms. Christina Weller............................................................80

VI. DOMESTIC MONETARY POLICY AND DEBT ...................87

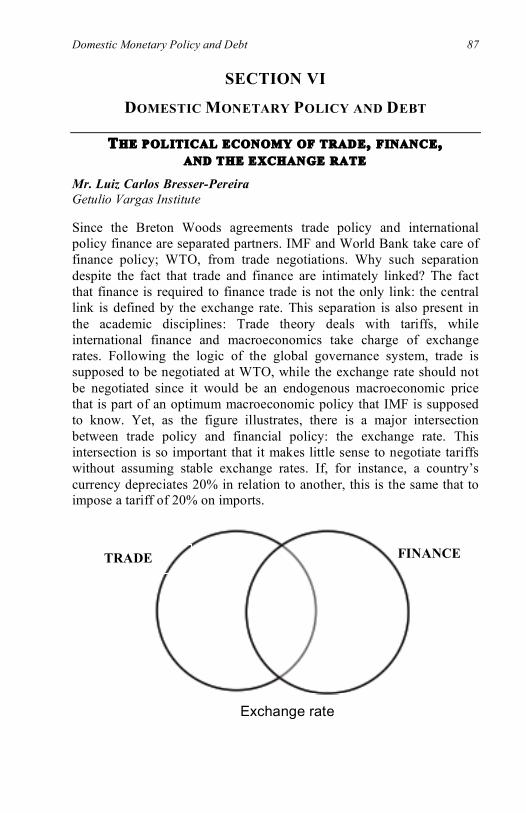

VI.1. THE POLITICAL ECONOMY OF TRADE,

FINANCE AND THE EXCHANGE RATE

Mr. Luiz Carlos Bresser-Pereira ................................................87

VI.2. Mr. Heiner Flassbeck. ........................................................92

VI.3. Mr. Richard Kozul-Wright .................................................95

VII. DEFINING DEBT SUSTAINABILITY.....................................98

VII.1. Mr. Damian Ondo Mane ..................................................98

VII.2. Ms. Machiko Nissanke ....................................................101

VII.3. Mr. Matthew Odedokun ..................................................106

VIII. FACTORING TRADE PERFORMANCE INTO DEBT

SUSTAINABILITY ASSESSMENTS .....................................111

VIII.1. Mr. Manuel Montes .......................................................111

VIII.2. Ms. Cecile Valadier .......................................................115

Overview i

DEBT AND TRADE: MAKING LINKAGES FOR THE PROMOTION OF

DEVELOPMENT—AN INTRODUCTION

Aldo Caliari, Center of Concern and Vicente Paolo Yu, South Centre

This volume gathers the presentations delivered at the second in a series of policy roundtables

1 that had the objective of promoting an integrated

approach to policy-making on trade and finance. The premise of this and

the previous roundtable is that a holistic approach to policy –making in trade and finance can bring substantial improvements in ensuring systemic coherence and providing better development outcomes than an approach that would take such areas in isolation.

The roundtable “Debt and Trade: Making linkages for the Promotion of

Development” also jumped off from that same premise. This time, however, it singled out debt as a specific area of finance. The objective was to create a space to explore the potential implications that an

integrated approach that bridges trade and debt may have for policy-makers focusing on, or specializing separately in, each of those areas. We would like to express our deep appreciation to the participants at the

Seminar on Debt and Trade Linkages that was held in Geneva on 13-14 September 2007.

2

The next piece after this introductory section is a transcript of the inspirational opening speech delivered by Mr. Yash Tandon, the Executive Director of the South Centre (from January 2005 to February

2009), which sets the stage for the discussions that followed. Mr. Tandon lays out the way that the structural interdependence between debt and trade has operated as a constraint to development in developing

countries. The real debate, he argues, about debt and trade policy coherence is over space in which developing countries can freely pursue

1 The first in the series was called “Trade and Finance Linkages for Promoting Development”

which took place in 19-20 October 2006 in Geneva and was cosponsored by Center of Concern, South Centre and German Marshall Fund of the US. The proceedings were gathered in a book that is available from both South Centre and Center of Concern, and can be downloaded at http://www.southcentre.org/.

2Details on this second seminar are available at

http://southcentrenet.blogspot.com/2007/09/south-centre-organizes-seminar-on-debt.html.

their own development policies and priorities. The central questions are on the roles that both debt and trade can play in the economic reform

process, to what extent deeper integration into the current global economic framework is or is not desirable for developing countries, and the alternatives they have in strategically selecting their terms of engagement or disengagement.

Section I, with a focus on the political dimensions of linking debt and

trade, comprises only one presentation, by Mr. Barry Herman, of the New School in New York. Mr. Herman observes that the specialized economic institutions have strong mandates in their own fields, but that

there is no effective mechanism to bring about inter-institutional coherence. The Group of 7 has acted as the one forum where Heads of State meet and can make their respective trade, finance and development

ministers work together in institutions they share, but this is an exclusive forum. He traces the efforts to generate integrated discussions on trade and finance in a more inclusive forum back to UNCTAD in 1964. But such process gradually lost momentum. It is in this context of

failing mechanisms for coherence that he places the unique set of circumstances characterizing the lead up to the Monterrey Conference on Financing for Development in 2002. He states that the UN offers still

the best opportunity for a confidence-building process on global economic reform. As it was the case before the Monterrey Summit, this process requires extensive cross-fertilization between UN delegates and their finance and trade ministry colleagues.

In Section II, the focus is on the technical dimensions of linking debt

and trade. The presentation by Mr. Jan Kregel, of the Levy Institute, provides the right starting point by looking at “The debt-trade causality in balance of payments accounting.” Examining the experience of the

19th

century he argues that trade was seen as an engine of growth not because of a perceived efficiency of open versus closed trade but a result of foreign capital and labor inflows to the developing areas. These

flows created exactly the production and the exports processes that were necessary to allow the repayment of financial obligations. In contrast, the paradigm prevailing since the GATT system emphasizes separation of trade in goods from financial factors. It focuses on trade as a way to

create efficiency gains via opening closed markets, thus separated from the accompanying financial processes that were key to the 19

th century

concept of trade as an engine of growth. Trade is perceived as the cause,

not the consequence of financial flows, and gives rise to a theory on the adjustment of the balance of payments that relies on income adjustment.

Overview iii

But the impact of capital flows on trade cannot be simply wished away. So, as globalization and capital mobility progress, the relationship

becomes even clearer, and can be seen in how it is the investment decisions of large multinational companies that decide which parts of the production chain take place in different countries, and the trade patterns across them.

The intervention by Mr. Matthias Rau, from UNCTAD, takes on the

conceptualization of sovereign debt. His input is important for the characterization of the trade –debt relationship. It is usually understood that the need to generate foreign exchange for payment of external debt

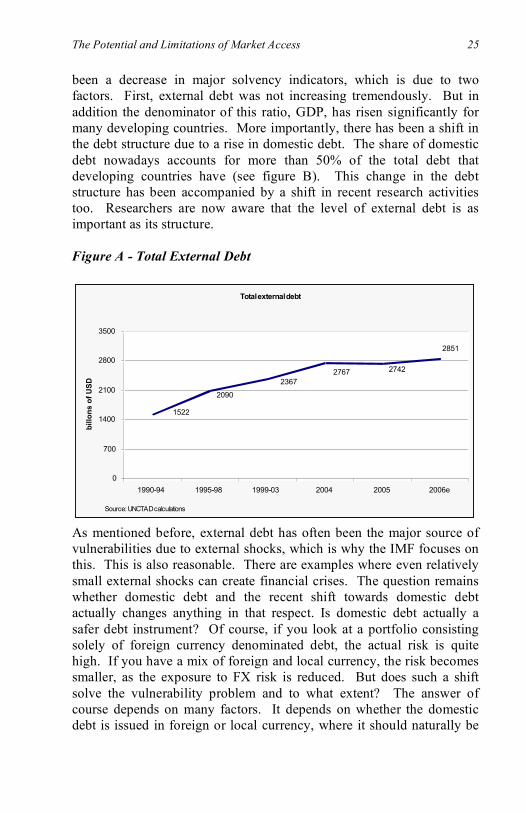

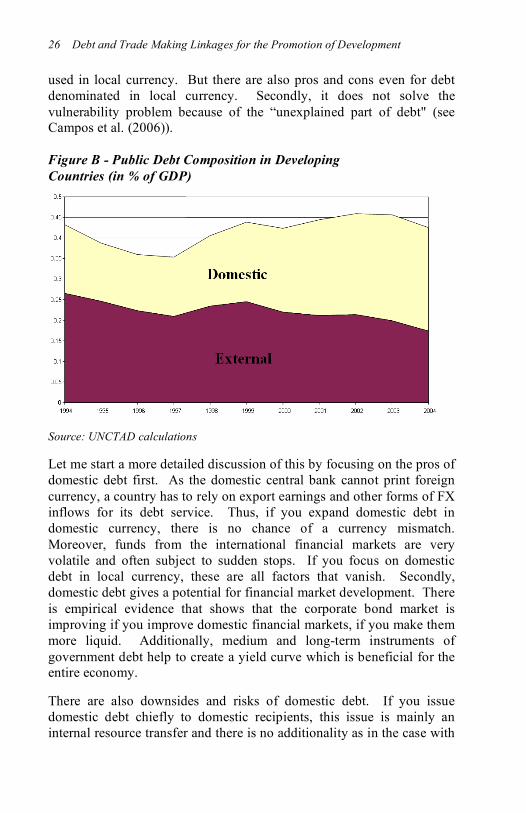

is an important motivator for the generation of export income. But Mr. Rau explains that the share of domestic debt in developing countries has been growing and amounts to more than 50 percent of their total debt.

While this may represent a reduction of vulnerability to external shocks, there are also risks inherent to the greater reliance on domestic debt. At the time of this presentation, the period had been one of improved solvency indicators but the shift to domestic debt was also opening up

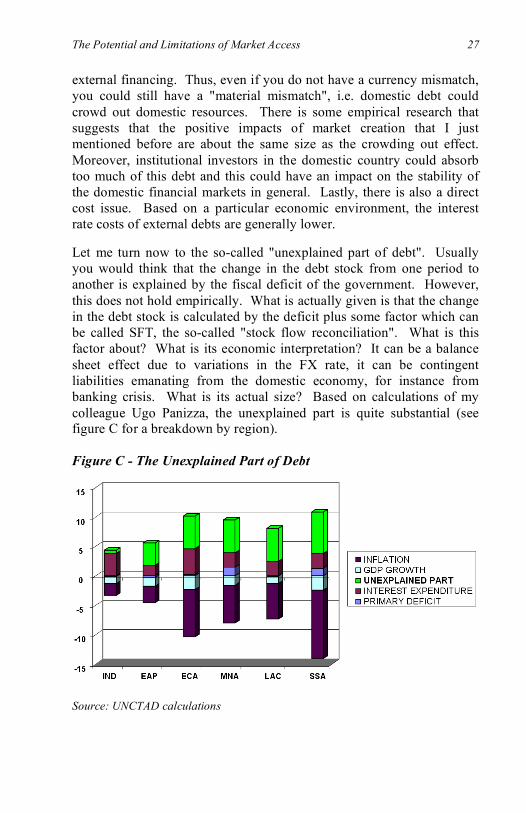

new risks in what he calls “the unexplained part of debt,” whose materialization he foresees could take place under less benign conditions.

Section III starts to address more concrete impacts of an integrated approach to debt and trade by looking at “The Potential and Limitations

of Market Access.” Indeed, a central idea behind the reform programs adopted by a large number of countries since the 1980s was that an export-oriented model would allow them to earn the foreign exchange to

attend growing external debt payments. Even today, there is a widespread perception that enlarged market access for developing country export products is the most direct trade response to solve the

debt problem in a sustainable way. Interventions were asked to address to what extent was there a relevant link between market access and a solution to the debt problem.

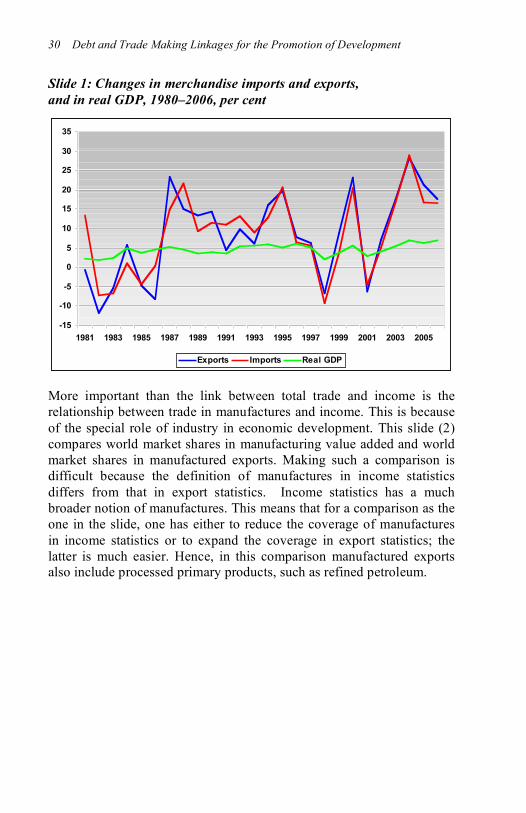

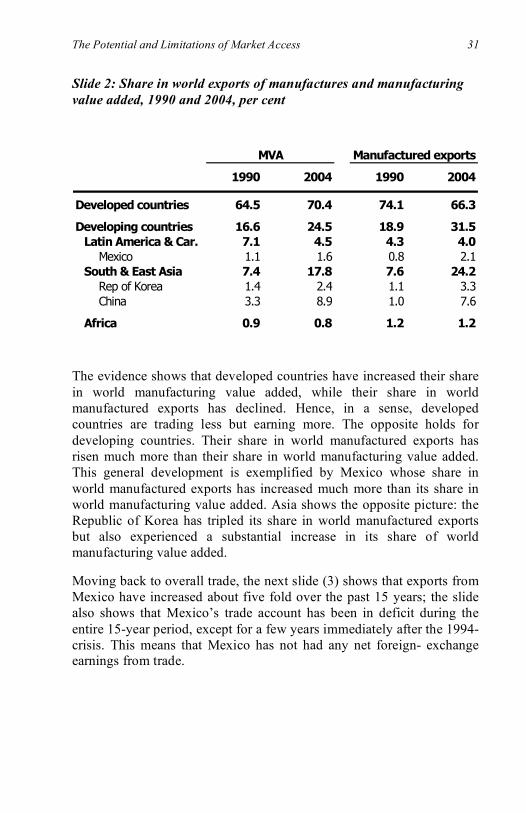

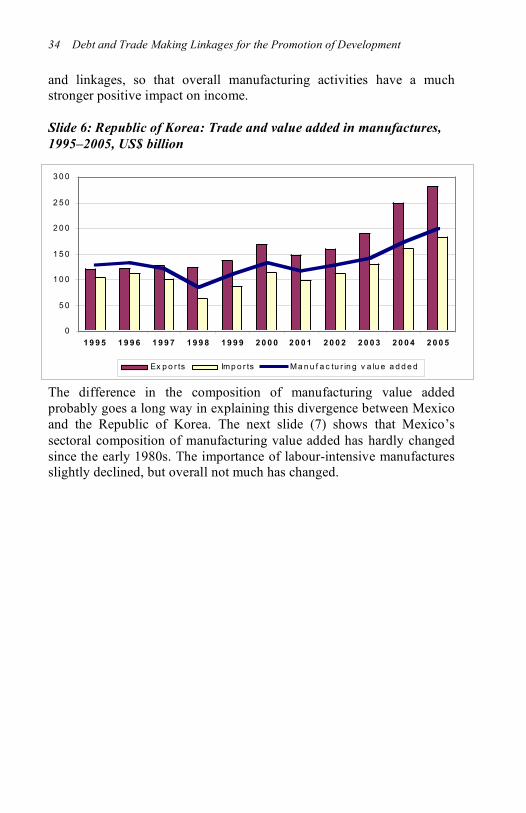

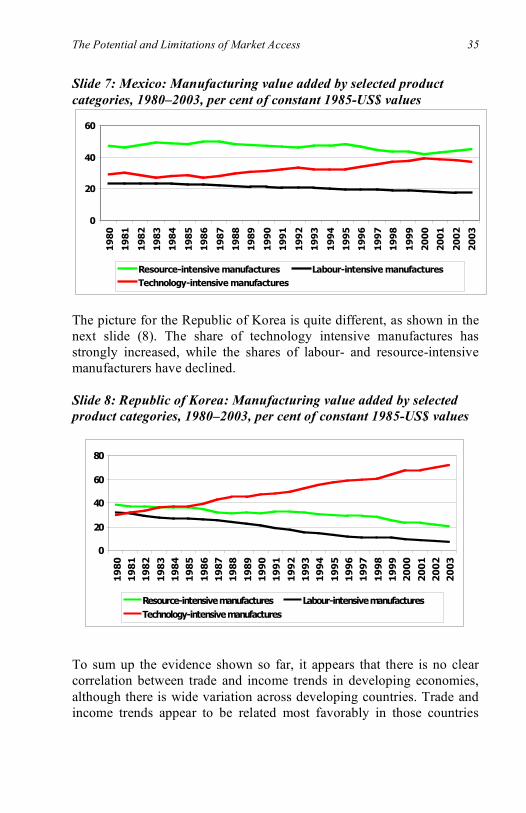

Mr. Joerg Mayer, from UNCTAD, shows that the relationship between trade growth and income growth is not a straightforward one. In fact,

while developing countries have increased their share in world manufacturing trade, their share in world manufacturing value added had declined. While this is true in the aggregate, it appears that trade and

income are most favorably related in countries that succeeded in upgrading their manufacturing activities toward more technology-intensive products. From this he draws important conclusions for trade

integration strategies. In order to improve income generation and, thus, debt servicing capacity, integration should rather be part of a wider

outward oriented industrialization strategy. While deep integration might simply boost exports of goods with high import content, strategic integration might make trade growth less pronounced, but generating a

denser domestic production network, thus favoring domestic income generation.

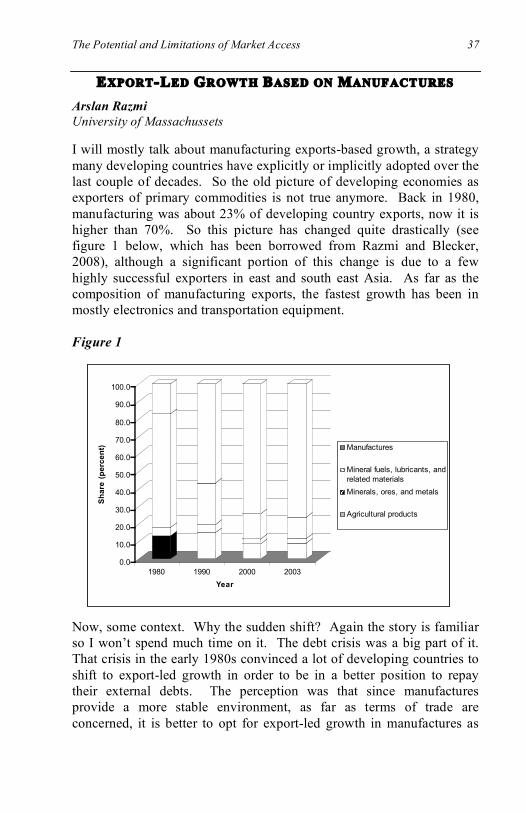

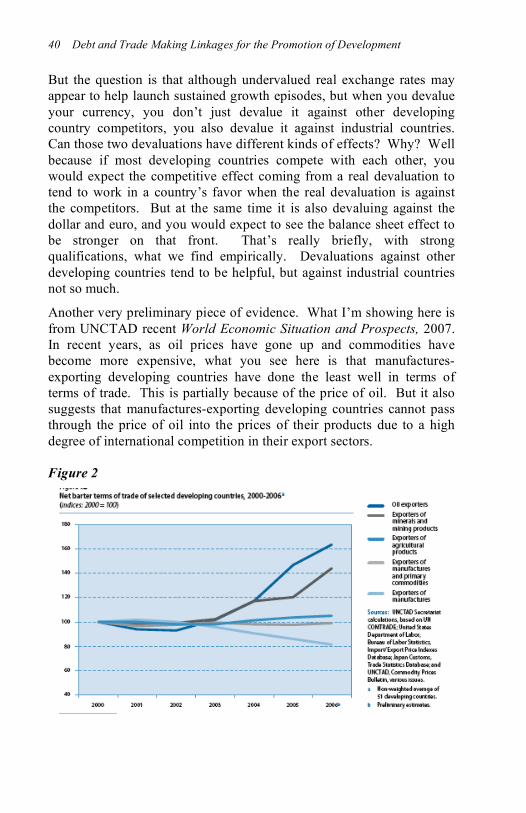

Prof. Arslan Razmi of the University of Massachusetts then assesses the case of developing countries that went for an export-led growth strategy based on manufactures, as opposed to commodities, as a way to improve

terms of trade. In his view, confirmed by looking at a sample of developing country exporters, the fact that many countries pursue similar export markets in similar products puts them in competition with

each other. The fallacy of composition, typically associated with commodities, becomes true for manufacturing exports, too. It creates incentives to lower costs and the short-term ways to do that are lower wages and /or an undervalued exchange rate. Moreover, it ensures that if

gains are made, they come at the expense of other developing countries. An important insight also emerges from his presentation regarding strategies of exchange rate undervaluation. While their export

consequences would usually affect more strongly other developing countries that compete in the same product, the currency composition of the external debt would lead to balance sheet effects that worsen the position relative to developed countries.

Mr. Umesh Sookmani, from the Mission of Mauritius at the UN and the

WTO in Geneva, offers a good complement to the previous intervention by presenting the experience of Mauritius. This is one of the countries that have made better use of trade preferences, transforming from a

monocrop agricultural economy in the 1970s through a gradual diversification into manufacturing, tourism, etc. But now that preferences are coming to an end it faces a number of challenges, that

may be aggravated with the liberalization being promoted in negotiations on non-agricultural market access. He details the negative effects on employment, Foreign Direct Investment and export revenue, as well as the possibility that deep cuts in industrial tariffs in traditional

markets of export may represent further erosion of its margins. At the end he presents an illustration of the measures that Mauritius is putting in place but also a clear sense that these measures cannot go very far

without support from the international community’s policies on aid, debt and trade.

Overview v

In the presentation that follows, Mr. Matthew Odedokun addresses the problem of commodity price instability and how it affects debt. In low

income countries generally the export structure is heavily focused on a few –sometimes one or two—commodities. The dynamics this creates is that during commodity boom years the excess revenue leads to

excessive borrowing –supported by less prudence by both lenders and borrowers. During the bust years, loans are taken to defend past commitments and complete projects started in good times, while debt service tends to be renegotiated into less favorable ones, due to

increased risk. He suggests an emphasis on three sets of measures: the prevention of exports price instability, the mitigation of its consequences, and policies and incentives to change management of the boom-bust cycle.

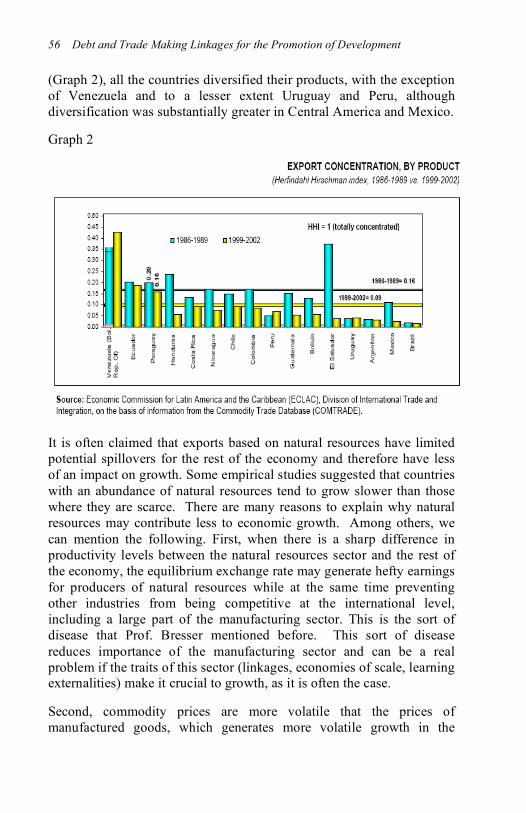

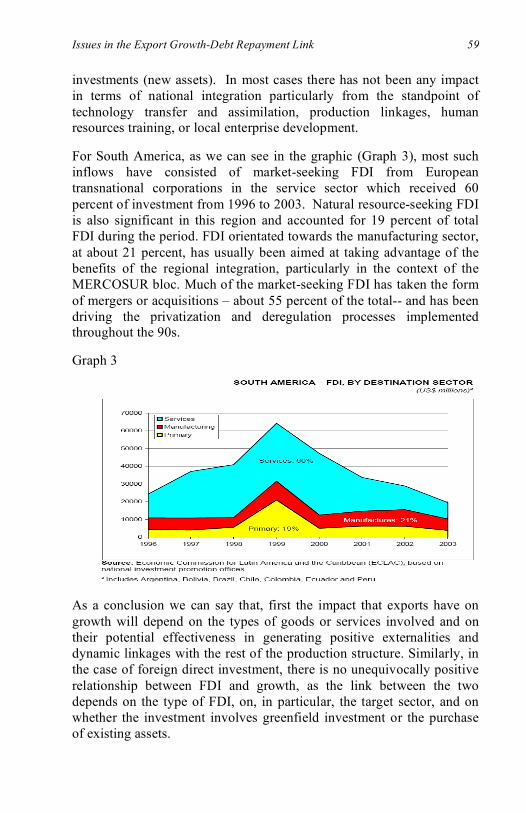

Section IV undertakes an exploration of selected “Issues in the export growth-debt repayment link.” The first presentation under this section, by Ms. Lida Nu!ez, from Corporación de Investigación y Acción Social y Económica (Colombia), addresses experience relevant to the export

growth-debt repayment link in Latin America. In this experience, increases in exports have failed to boost GPD growth significantly, with marginal improvements on the debt situation. The heavy focus on

natural resources that is a feature of the export basket may be a factor but some South American countries, especially in the MERCOSUR area, have diversified their exports. She identifies the difficulty in

adding value and knowledge to exports as the main limitation to the growth-boosting potential of exports. On the other hand, the export base bears the promise of a platform for strategies that boost domestic value

added and the intensification and extension of learning processes and innovation. The experience on FDI reinforce the notion that for it to lead to growth, it is crucial to avoid that it goes into enclaves, mere purchase of existing assets that may be associated to it and/or massive capital outflows in the form of royalties and dividends.

Mr. Richard Kozul-Wright, in the following presentation, argues that the debt crisis was also a crisis of inward-orientation, leading to a sort of win-win logic that focused on removing distortions and state intervention as a way to foster a virtuous growth cycle. But an

alternative view of the link between trade and development is on the rise again, one where a key aspect of trade policy is how to translate increased export revenue into investment in new lines of economic

activity. This thinking is validated by the finding that it is diversification, not specialization, that favors growth processes. He

points to the essential role of policy to drive manufacturing and changes of structure— “getting structure right”, as opposed to “getting incentives right.”

Foreshadowed in the previous section is the focus of Section V: FDI

rules and their relation to debt. One of the warnings of Mr. Kozul Wright at the end of his presentation is to not confuse linking investment to exports with attracting foreign investment. Indeed,

common advice to developing countries tends to equate the attraction of FDI with improvements in the balance of payment constraints, and the plugging of debt gaps. The presentations in this section offer three

perspectives in discerning the relationship between the role of FDI and debt. Professor Andreas Antoniou’s presentation, in a first take at this relationship. While it is argued that FDI stimulates growth and enhances

the competitiveness of the economy, thus diminishing the risk of default, there are also detrimental effects that FDI may have on the risk of default.

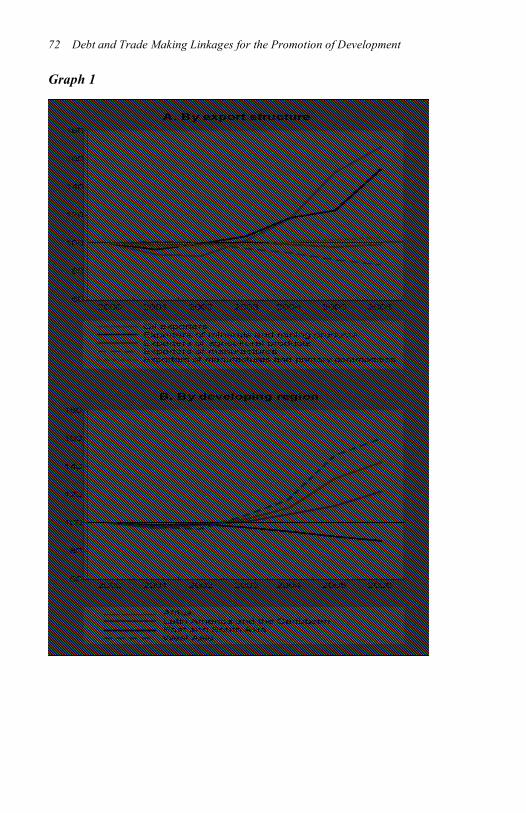

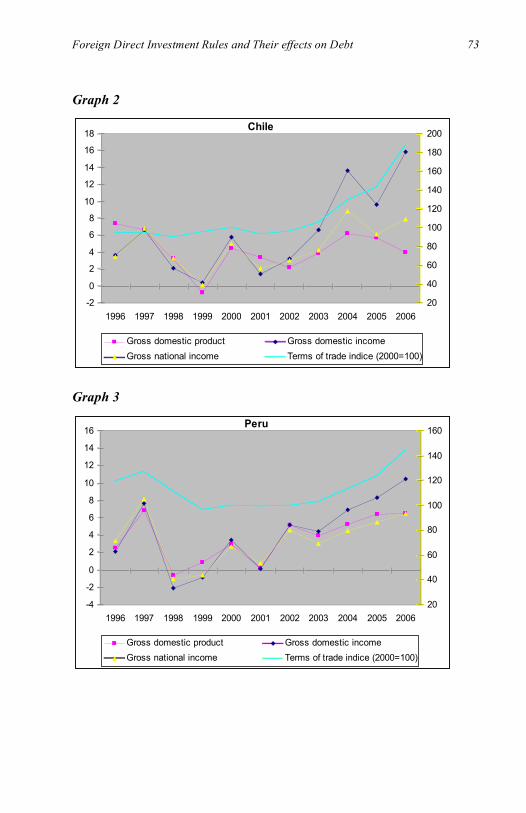

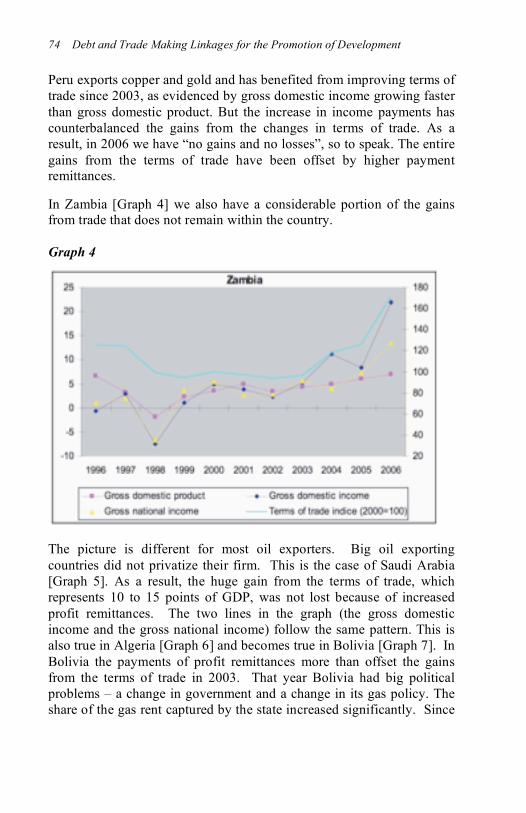

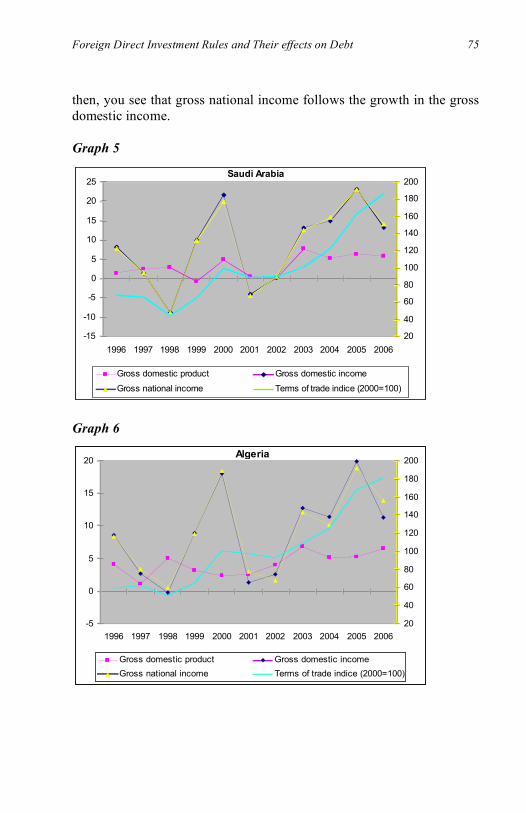

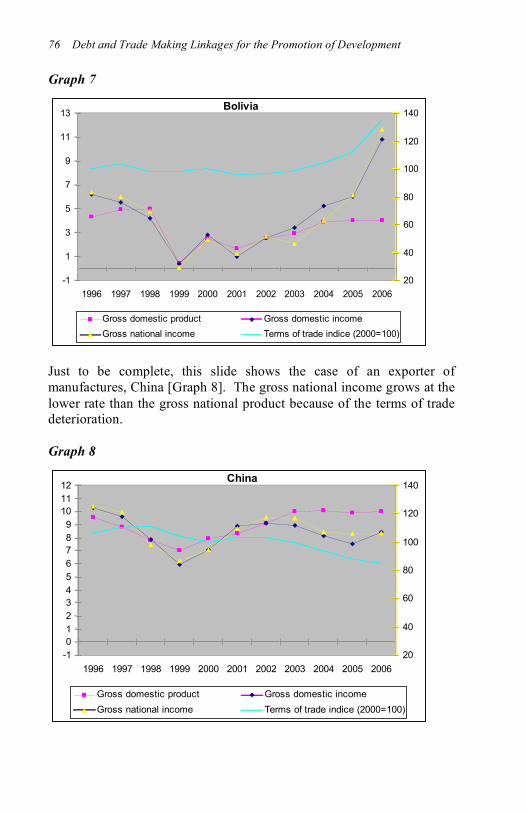

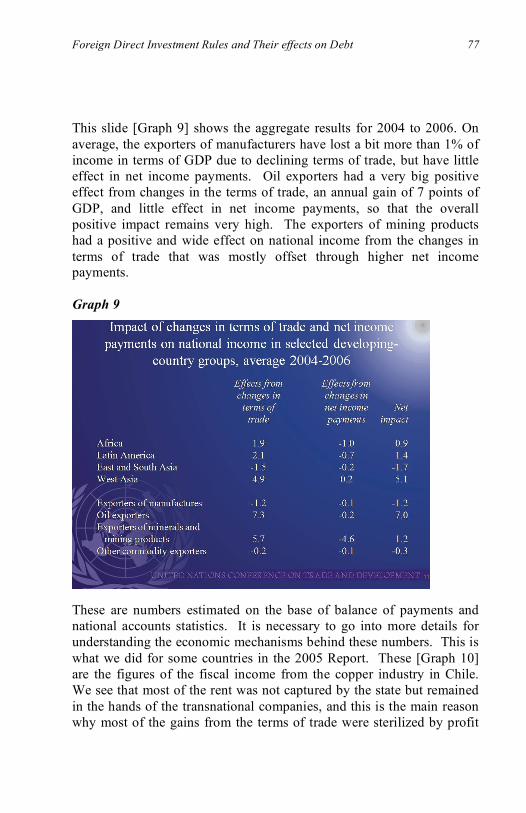

A second take at the relationship is in the intervention by Alfredo Calcagno, of UNCTAD. Drawing on a rich sample of country case

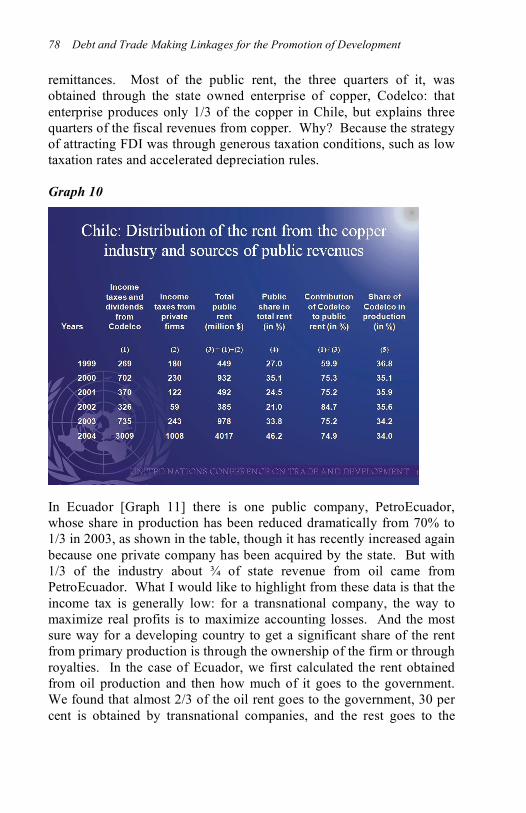

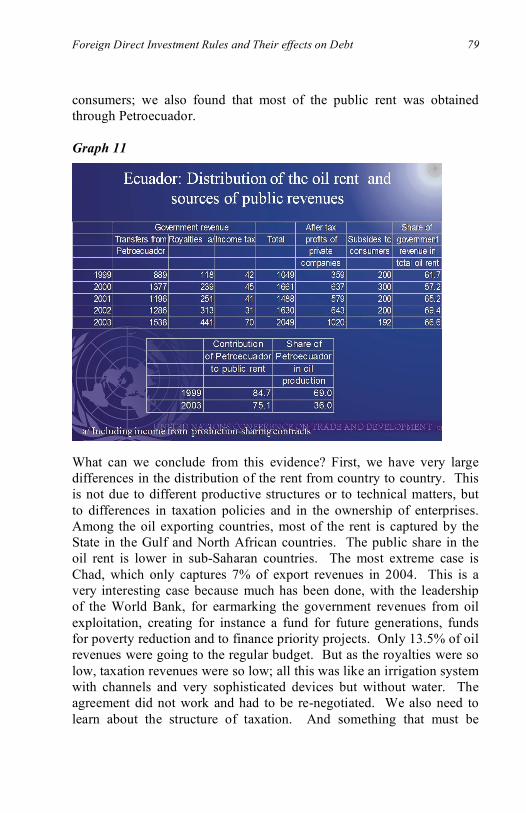

studies, he shows that the distribution of the rent of natural resources makes a big difference to whether the higher prices from these resources accrue to the local economy. The structure of foreign investment in the sector can determine that net income payments offset the improvements in terms of trade, erasing the potentially beneficial effects of trade.

Yet a third approach is contained in a presentation by Ms. Christina Weller, of Christian Aid. While she reinforces some of the points of the previous presenters, her intervention raises important points regarding

the interaction of the FDI regime with the capacity of governments to appropriately tax economic activity and stop capital flight. Given that public revenue is the crucial denominator in talking about debt risk and debt servicing capacity, the importance of this approach to FDI cannot

be overstated and bears clear implications for the regulation of FDI, some of which she mentions in her recommendations.

The following Section VI looks at debt and trade and how their link is modulated through monetary policy. Professor Bresser Pereira, from Getulio Vargas Institute and former Minister of Finance of Brazil, holds

that the exchange rate is a strategic macroeconomic price and that developing countries are better off managing it than letting it freely float. Otherwise, the tendency is towards an appreciation, due to Dutch

Overview vii

disease, growth cum foreign savings policy, or what he calls “exchange rate populism.” In this condition, contrary to conventional wisdom, the

equilibrium exchange rate will not be one that equilibrates intertemporally the current account, with negative consequences for the competitiveness or profitability of tradable industries.

In his presentation, Mr. Heiner Flassbeck, from UNCTAD, continues the thread of analysis on managed exchange rates but puts it in the

context of more structural regulatory gaps in international financial markets. Carrying money from low to high interest rate countries actually exacerbates the difficulties with a freely floating exchange rate

and is the main reason why exchange rates left to float will fluctuate farther, rather than closer, from equilibrium. On the other hand, not all countries can keep an undervalued currency. As long as large surpluses

of some countries need to be matched by large deficits in others, this is not a lasting solution and that is why UNCTAD advocates an international agreement on exchange rates that rationalizes the discussion on what equilibrium exchange rates are.

The section finishes with an intervention by Mr. Richard Kozul Wright

where he connects the earlier discussions on FDI and its impact on trade patterns with the one on domestic monetary policy. He speaks about the “financialization” of investment, meaning that finance is dominant not only in the short term, but also in the long term capital flows that were

considered a more beneficial form of FDI. He hypothesizes that, in such scenario, the view prevalent in the early post-war period, which treated FDI just as another capital flow, might make more sense as a framework

for analysis. Monetary policy of developing countries is likely to be a much bigger issue under this approach to FDI.

While the previous sections looked at the linkage between debt and trade more with an eye on trade or investment policy, Section VII moves to discuss the linkage with an eye on the debt sustainability and debt management policies.

Mr. Damian Ondo Mane, former Executive Director for one of the African Countries constituencies in the IMF, examines a number of issues that compromise debt sustainability in African low income countries. His view is that there are examples where trade has been used

to reduce poverty and wealth inequality, but that is far from being the case in Africa. Administrative capacity, economic infrastructure, the level of labor market skills available, as well as limitations in the

markets of export interest (tariff escalation, technical and scientific standards that cannot be fulfilled, etc.) are among the obstacles to

overcome. Debt sustainability and avoiding a new debt crisis are crucial to ensure investment reaches low income countries.

In next presentation Ms. Machiko Nissanke, Professor at School of Oriental and African Studies in London, observes that the donor and creditor community has identified policy failure to be the root of the

debt problem of low income countries. Thus, in aid and in debt sustainability assessments there is a heavy role attached to Performance-Based Allocation systems. But there is a direct connection between the

continued deterioration of the debt of low-income countries and their export dependence on commodities. Consequently, a focus on vulnerability to external shocks in guiding aid allocation and debt

sustainability processes would yield better results, as it more accurately would capture the reality of the target countries. She proposes state-contingent aid and debt contracts that operate as a sort of ex ante debt relief mechanism: a contingent credit line would be activated should an exogenous shock materialize.

In a presentation delivered under this section, Mr. Matthew Odedokun from the Commonwealth Secretariat addresses different concepts of debt sustainability and some of their intricacies. They are debt sustainability as a sustainable return on projects financed by such debt,

debt sustainability as debt repayment capacity and the human development concept. He advocates this latter could be adapted to incorporate not just spending to meet MDGs, but also spending to invest on trade that generates new public finance resources.

The final section, “Factoring trade performance into debt sustainability assessments” offers a complement and follow up to the previous one. Mr. Manuel Montes, from the UN Financing for Development Office, makes the point that before trying to infuse trade considerations in the

indicator it is important to understand to whom the indicator is intended to be of use. Debt sustainability indicators are currently of use to the lenders, they protect them. But borrowers arguably have an interest, too,

on shaping them. Trade is needed to service the debt so, to the extent that trade shocks are excluded from consideration in assessing debt sustainability, the risk is shifted to the borrower. He notes that the

current debt sustainability exercise incorporates stress testing, but does not distinguish between endogenous and exogenous shocks.

Overview ix

In the final presentation Ms. Cecile Valadier, from Ecole Normale Superieure of Paris, closely follows other presentations in holding that

the high concentration of exports in low income countries constitutes a vulnerability that plays a large role in determining debt distress events. As a response to this issue she introduces a lending instrument that can

decrease the likelihood of debt crises and costly restructuring processes. This is a concessional loan with a fixed grace period and a floating one. If a shock occurs, the borrower can make use of the floating grace period, thus smoothing debt service. In spite of a number of operational

challenges, there is promise that a mainstreaming of this mechanism could help practically factor trade performance of borrowers in debt sustainability.

Trade, debt and the global financial and economic crisis

While the policy roundtable took place in the cusp of an unprecedented boom of world trade, as this volume was being compiled and edited a

crisis that begun in the subprime mortgage market of the US in 2007 became a financial and economic crisis of global proportions.

As a result what was, in the aggregate, an improving debt situation for developing countries has taken again a turn for the worse. Global trade is expected to contract in a 10 per cent in 2009, the greatest contraction

since the Great Depression. Many developing countries have seen their situation of trade surplus rapidly turn into a deficit. This creates an environment where developing countries, much more highly dependent

on exports for their income, will see their access to foreign exchange diminished, and pressure on their public debt profiles intensified.

In the face of this crisis the agenda proposed throughout the contributions in this volume is far from having lost currency. On the contrary, their attentive reading will reveal that the crisis is not an

anomaly in what was an otherwise harmonious growth of trade, but rather the patterns and characteristics of the trade boom sowed the seeds of the vulnerability that countries are experiencing in these difficult times.

As the crisis exposes the fault lines throughout the current model that

links international trading and public debt, nationally and internationally, the material in this book represents a useful roadmap to the issues that need to be addressed. Indeed, only crisis recovery

measures that dare to reshape the paradigm linking trade and debt on the

basis of the lessons learned can lead to a more resilient and development-oriented global economy.

Introduction xi

OPENING ADDRESS:

LINKING DEBT, TRADE AND FINANCE ISSUES

Yash Tandon

Executive Director, South Centre

This meeting is the second meeting in a series that was organized to address the issue of the interface between trade and finance, which is

very critical. In the first meeting, that we had last year, the discussion was on trade and finance linkages to promote development. In this particular meeting we hope to address the issue of trade and debt, and

see the complex links between these two factors. We know that for those of us who come from the South, development has been a challenging objective, especially those of us who come from the smaller countries in the South – from Africa and the Caribbean – and therefore it’s very

important for us to be able to address critical dimensions of development in international trade.

The link between trade components and debt levels is highly

interdependent and complex. Debt can be, and often is, in many countries, a major constraint on development, and international trade. Poor trade performance, added to by declining terms of trade or

monetary crises, can bring about a downward trend in the development scenario. The problem of the large debt overhang in developing countries is a result of the confluence between the particular

circumstances of trade, within the international economic system, and the structure of that very system. That makes it very difficult to develop. We have structural constraints and circumstantial constraints to development.

There are a number of factors that can intensify these problems for

developing countries, and the ways in which each sector behaves, or is acted upon, by the global trading system, simply accentuates the debt crisis. The main factor is the continued reliance of many developing

countries on primary commodities, and low value-added goods. We have discovered over the years that on the account of the hasty trade liberalization on the part of many of those countries, one of the effects of that has been de-industrialization and in some countries, even de-

agriculturization. We have moved away from productive enterprises, through floating our human resources outside our countries.

xii Debt and Trade Making Linkages for the Promotion of Development

The unpredictable and volatile nature of finance also increases our vulnerability in the international system. Unable to rely on sure

incomes, the shift to higher value-added goods production is nearly impossible for many developing countries. The second factor is the continued application of poorly planned policy reform advice, especially

that type given by the Bretton Woods institutions and other governments. That policy advice factor is a major issue that we need to examine.

We must also deal with international trade and financial institution-sanctioned protectionism and discrimination against developing goods,

and limited amounts of support in breaking free from the debt trap. There are two dimensions here that we need to look into. We need to look both into the investment regime, and the trade regime. We haven’t

had the quality of investments in our countries that can add value to production in many of the countries in the South – by no means all countries in the South, but many countries in the South.

The global trading system as a whole and international trade, WTO, and IFIs, play of course a major role in the continuation of this trade debt

problem. There are trade commodity price stability, tariff and non-tariff barriers, and financial problems, financing and exchange rates – these create a system of destruction in which many poor countries are embedded. And to get out of this kind of structure is challenging to us.

The international trade groups designed and hosted by the WTO reflect

major inequalities between members and within the larger world trading system. Lop-sided free trade constitutes the main problem that continues to be inadequately approached. Conditionalities continue to be attached

to loans and debt relief mechanisms that are poorly designed and mismanaged by the Bretton Woods institutions. The accompanying policy advice tends to have as its aim the repayment of the debt, rather than addressing the root cause of the problem, mainly the low level of development of developing countries.

In recent years, as a result of debt relief to some poor countries in the South, especially in Africa and Latin America, for once, they made the possibility for us to exercise more policy space, more policy options, and one of the challenges that we must address, is how best we can

utilize this policy space that we now have, in order for us to design our own policies, independent of the Bretton Woods institutions. So the

Introduction xiii

question of trade and debt is something that we will examine closely within the next few days.

The global trade and debt policies must enable developing countries to maintain and even expand their policy space to allow for greater flexibility. The key question for global economic institutions, such as

the Bretton Woods institutions and the WTO therefore is whether they are in the present form capable of supporting this need for greater development policy space and flexibility for developing countries. Are

there actions that could be taken within their institutional constraints that could promote policy space? Are they, and other global institutions such as UNCTAD, capable of stabilizing the markets of concern to

developing countries, especially fabric commodities and low value-added manufacturers, to better assure them more reliable incomes in the short to medium-term, while promoting a system in producing and

trading higher value-added goods? These are questions we need to address.

Hence, the real debate central to debt and trade policy coherence and global economic policy-making is over space for development policies and priorities. The central question should be about the kinds of

economic development policies that will be taken, their sequencing, the roles that both debt and trade can play in the economic reform process, the extent to which deeper integration into the current global economic

framework is or is not desirable for developing countries, and the alternatives that developing countries have in strategically selecting their terms of engagement or disengagement with such a global economic framework. We need to keep our mind open, even to the

possibility of limited and selected disengagement from the global system, for some of our countries, in order for them to be able to organize their own production systems and their own regional

integration, so that, with a position of strength and increased economic power, they can renegotiate their entry into the global system on better terms than the present. So we must be open-minded about all possible options.

It is my and the South Centre’s hope that through this seminar, we may

able to move a step forward in discerning the answers to these questions. Of course we are facing a rapidly changing world, economically, politically, and climatically, and changing conditions require innovative

responses, fresh perspectives, and flexible solutions. We do have the possibility of exploiting the new political geographic configuration that

xiv Debt and Trade Making Linkages for the Promotion of Development

has now shifted – some of the energies of economic development, from the North to countries of the South like China, Brazil, and South Africa

– and we must see if these new possibilities open up options for the smaller countries in the South to be able to engage or realign themselves differently from what they have been into in the last thirty or forty years.

So we need flexible solutions, we need open minds, we need alternatives, we need to look into details in the relationship between

debt and finance. I hope that the deliberations of this meeting will perhaps inform current debate and I hope they’ll also inform the debate on financial development that takes place in October in New York. I

hope that with the membership of this meeting – as I can see many of you come from very experienced backgrounds from your countries, engaged in not only academic discourse, but also policy making – I hope

this is a source of rich interaction among you, and that we are able to address some of the challenging questions that face us as we go into the next decade. On behalf of the South Centre, and our co-sponsors, I’d like to welcome you and to wish you a good discussion. Thank you.

The Political Dimensions of Linking Debt and Trade 1

SECTION I

THE POLITICAL DIMENSIONS OF LINKING DEBT AND TRADE

TIME FOR CHANGE IN GLOBAL TRADE AND

FINANCIAL GOVERNANCE

Barry Herman

Graduate Program in International Affairs, The New School, New York

One of the advantages of retiring from a long career in the UN Secretariat and rejoining academia is that you can step back from daily responsibilities. You can ask yourself, “After almost 30 years, what

sense does it all make?” I have begun to think about that and I will say some things to you today based on such reflections.

I’ve been asked to address global political dimensions of the linkages between the international trade and external debt of developing countries. I am basically going to make three points, and then draw a

conclusion. First, international trade and external finance — and thus trade and debt — are so intimately linked that it is amazing we even need to think about linkages. Probably the reason has to do with my

second point, which is that international policy makers have largely separated decision making on international trade and financial policy into distinct, specialized forums. There should be no surprise if the

decisions they reach are not always consistent with broad international policy goals. Third, while there is one international forum at which coherent policy decisions can be made on trade and financial policy, most countries have been excluded from participating in it. The

decisions that are made in that forum presumably accord at least with the policy goals of the countries that participate in making them. My conclusion is that the world is not better for this structure. The current

challenges in the major international trade and financial institutions only underline the problem. Policy makers in the North and South would do well to ask themselves how to reach better international decisions on

trade and financial policy. The intergovernmental conference at the end of 2008 in Doha, Qatar to review the Monterrey Consensus on Financing for Development provides an opportunity to kick off a collective effort to design a more balanced and effective structure.

3

3 In a post-script, I will point to a proposal (not my own) on how to start looking, post-Doha.

2 Debt and Trade Making Linkages for the Promotion of Development

Trade and Finance Are Inextricably Intertwined

First point, perhaps not necessary to state explicitly, but for

completeness here it is: international trade requires international finance and vice versa. Trade is not on a cash basis; trade takes time and so it needs to be financed. Also, from the start, ships carrying international

trade also carried the mail, including not only commercial and personal mail but also securities. Shipping — and electronic communication today — is an internationally provided service and thus itself part of international trade. So, international trade and finance have always been intimately linked.

Trade has even provided opportunities for creating financial securities that are then traded on domestic financial markets. A prominent example is the “banker’s acceptance” in which an importer takes a loan

from a bank in his country which accepts to pay a foreign exporter’s bill for goods shipped. The importer repays the bank after selling the imported goods. The bank can hold the acceptance until repayment by the importer on maturity of the loan, or sell it on the local financial

market at a discount. The buyer of such a security receives the face value of the security when it matures and thus gets his money back plus interest; he has bought a short-term bank-issued security and could not

care less that it finances international trade. When did this market start? It was already known in 12

th century Europe.

You can also say, at least at the level of a country as a whole, that international finance does nothing more than change the time path of a nation’s international trade. Twenty years ago I was working for a UN

commission concerned about African debt,4 when a member of the

commission, Robert Hormats of Goldman Sachs, made the simple and in the context startling observation that external debt is simply

postponed trade. What he meant is that when financial flows are accommodating, the total value of imports into a country can exceed exports and the balance of trade in goods and services will then be

negative. The deficit would be financed by financial inflows; there is a “net transfer” of financial resources to the country. For the most part, these inflows are not grants; they are loans. Add them up and you have the country’s foreign debt.

5 The makers of loans expect that at a later

4 See Financing Africa’s Recovery (Report and Recommendations of the Advisory Group on Financial Flows to Africa, Sir Douglas Wass, Chairman), United Nations, New York, 1988.

5 To be precise, the “net transfer” comprises all financial flows in and out of a country,

including interest and profit payments, direct and equity portfolio investment, and grants and

The Political Dimensions of Linking Debt and Trade 3

point they will be repaid, which means at the country level that at some point the trade balance has to be reversed. You then have a balance of

trade surplus and thus a net financial transfer abroad; exports will be greater than imports. The policy question is only a matter of when it is appropriate for the shift to take place. That is the nature of the intimate

linkage of international finance and trade at the macroeconomic level. Economists have been talking about these issues for the longest time.

Furthermore, the International Monetary Fund (IMF) today examines the linkages of international trade and finance of member countries as part of its standard, annual “Article IV consultations.” It considers the

prospective sustainability of each country’s external debt by looking at the future path of the ratio of external debt to export revenues under “baseline” and alternative scenarios.

6 If the exercise shows that the ratio

“explodes” at some future point or under some potential economic shock that is tested, such as a significant devaluation of the exchange rate, the debt is deemed excessive and policy adjustments are recommended. For low-income countries, the Fund goes a step further,

in cooperation with the World Bank, and assesses the current external-debt-to-export ratio against a set of benchmarks meant to flag when the debt is too high, at which point official creditors are asked to switch

support of the country from loans to grants (whether or which creditors do so is a separate story).

In carrying out their debt sustainability analyses, IMF and the Bank cannot help but notice the linkages of trade and debt. They may see that developed country import restraints on developing country exports

impede their achieving debt sustainability, but they are impotent to do anything about it. They must also accept the volatility of international commodity markets as a given. Policies that might address these issues

are classified as trade policies and are thus beyond the mandate of the two institutions.

7

loans made to and by residents of the country or its government (see United Nations, World

Economic Situation and Prospects, issued annually, which regularly tracks the net financial transfers of groups of developing countries). For most developing countries, especially at an

early stage of their development, the net transfer primarily comprises foreign lending to the country.

6 It similarly analyzes the dynamics of total government debt relative to gross domestic product under multiple scenarios.

7 This notwithstanding, IMF and World Bank are widely accused of asymmetrically pushing developing countries to unilaterally remove their trade barriers as part of the conditionality for

financial support (see “The IMF’s Approach to International Trade Policy Issues: Preliminary

4 Debt and Trade Making Linkages for the Promotion of Development

The Power Politics of Debt and Trade

The relationship of a developing country to its foreign government and

multilateral official creditors is obviously a political one, by definition. But this is only one aspect of the politics of international debt. From early in the 19

th century until Second World War, much of the

international financial flows that were not directly financing trade were monies lent to the governments of developing countries, usually in the form of foreign private purchases of sovereign bonds or of corporate bonds linked to major government supported infrastructure projects,

such as building railroads. When some of the borrowing governments found they could not repay, bondholders formed national committees to try to recoup their investments and often complained to their own

governments. That being the age of imperialism, the governments sometimes — albeit infrequently — took military action in support of the defaulted creditors. The most famous examples were the bombing

of the port of Veracruz, Mexico by Great Britain, France and Spain in 1861 (followed by the French invasion in 1863), and the joint blockade of the ports of Venezuela by Germany, Britain and Italy in 1902-3 to capture customs house revenues to pay off the debt.

Outright interventions to collect sovereign debts not only were extreme

ways to settle financial disputes, but they also provided excuses for expanding imperial influence over developing countries and territories, as in Tunisia (1869-70) and Egypt (1876), as well as in Latin America.

Thus, when intergovernmental peace conferences were convoked in Europe to seek ways to settle international disputes short of war, one focus of attention was sovereign debt crises. The result in this case was

the “Convention Respecting the Limitation of the Employment of Force for the Recovery of Contract Debts” signed at The Hague in 1907. It sought to substitute international arbitration for invasion of defaulting debtor countries.

While the United States supported this treaty, it had also earlier taken a

unilateral policy stance. The new policy, announced by President Theodore Roosevelt in 1904, took the form of a corollary to the “Monroe Doctrine,” which the United States had proclaimed in 1823 and which said that any European attempt to recapture the newly

independent countries in Latin America would be regarded as a hostile act by the United States (not that the US was in a position to do much

Draft Issues Paper for an Evaluation by the Independent Evaluation Office (IEO),” IMF, March 18, 2008).

The Political Dimensions of Linking Debt and Trade 5

about it at that time). Roosevelt’s corollary was that European governments should also not invade to collect debts from defaulting

Latin American governments. This did not necessarily mean debt relief, however, but that the United States would help collect the debts for the European creditors (as well as its own). The US would itself invade if

deemed necessary, as it did in the Dominican Republic in 1904. In other cases, the US worked with local governments having distressed debt who understood Roosevelt’s threat and who with US intermediation reached settlements with their foreign bondholders, as in Colombia and

Venezuela in 1905, Costa Rica in 1911, Nicaragua in 1912 and Guatemala in 1913.

8 The policy stood until 1933, when the other

President Roosevelt, Franklin Delano Roosevelt, replaced it with the “Good Neighbor Policy.”

In each of the cases noted, economic adjustment policies had to be adopted by the debtor countries so they could generate enough resources for foreign debt servicing. In the period since the end of Second World War, this has been done in a more subtle way through adjustment

programs arranged with multilateral institutions. In other words, if one judges that the current international system for sovereign debt workouts is excessively creditor friendly, I think you can see that it has deep historical roots.

The Executive Committee of the World Economy

Just as the emerging United States and the major European powers

reached an accommodation on handling Latin American external debt problems in the early 20

th century, essentially the same governments,

joined by Japan, took a leadership role in developing international

policies on developing country debt in the second half of the century. Indeed, to the degree that there is coherence in any area of international trade and financial policies today, it is due to the same self-appointed club of governments that set the policy on sovereign debt workouts. I

am referring, of course, to the Group of 7 (G7), which has met annually at summit level since 1976.

9 The Group was formed in the aftermath of

8 See Kris James Mitchener and James Weidenmer, “Empire, Public Goods and the Roosevelt

Corollary,” Journal of Economic History, vol. 65, No. 3 (September, 2005), pp. 658-692. Another good source on this period is Christian Suter and Hanspeter Stamm, “Coping with

Global Debt Crises: Debt Settlements, 1820-1986,” Comparative Studies in Society and History, vol. 34, No. 4 (October, 1992), pp. 645-678.

9 Members are Canada, France, Germany, Italy, Japan, United Kingdom and United States, as well as the European Commission, which represents the members of the European Union on trade policy matters.

6 Debt and Trade Making Linkages for the Promotion of Development

the collapse of the “Bretton Woods system” of international monetary relations that had been established after the Second World War.

Although there has always been a “variable geometry” of important countries that come together on specific issues, the G7 became the

standing forum of the major developed countries for global economic policy reform and coherence. It formulated “the” general policy strategy for the world economy, which has been to move toward full

trade and financial liberalization, on the argument that this would foster global economic stability, growth and development. Implementation of the policy strategy has been uneven, however, as the group has pressed

harder for action in some areas and less in others, and as it has pressed some countries more consistently to liberalize than others. The G7 has always been, after all, a political body. That is, on the one hand, the

general strategy is meant to apply across the board. On the other hand, the more independent the country, the less its policy makers were willing to apply the strategy whole cloth (consider the successful resistance to liberalizing short-term capital flows in China or India). In

addition, the stronger politically the sector within a G7 country, the more completely the country would itself ignore the liberalization prescription (agricultural protectionism in the G7 owing to effectively organized farmers being an especially telling case in point).

When the G7 does reach a consensus on a policy matter in the trade and

financial realm, it is then generally adopted and implemented by one or more of the relevant global trade and financial institutions, which the club has been able to control, at least until recently. The World Trade

Organization (WTO) — successor in 1995 to the General Agreement on Tariffs and Trade (GATT) — serves as the main forum for global trade policy negotiations and oversight of national trade policy commitments,

although certain commercial policy issues, such as cooperation on cross-border aspects of tax policy and setting limits to competition between officially supported export credit agencies (as on interest rates), have

been assigned to the more limited membership Organization for Economic Cooperation and Development. The G7 charged the IMF, in essence, to align the economic policies of the rest of the world (excluding the Soviet bloc while it existed) with the G7 strategy, sharing

the “structural adjustment” part of this job with the World Bank and the regional development banks.

While adhering fairly constantly to its general policy orientation, the G7 has been somewhat more flexible in its membership. Thus, after the

Cold War ended it began post-summit meetings with the Russian

The Political Dimensions of Linking Debt and Trade 7

Federation and in 1997 invited Russia into the club itself, creating the “G8.” By the same token, the Heads of State of the G8 have also invited

groups of developing country leaders to meet with them from time to time on the fringes of their summits. Finally, in 2007 the G8 formulated a more permanent outreach project in the “Heiligendamm Process.” In

this, under Germany’s leadership, they sought to bring the governments of Brazil, China, India, Mexico and South Africa closer to their fold as the “O5,” at least for a two-year trial period of discussions on a menu of economic policy matters of mutual concern.

10

How the Specialized Institutions Interact

Whether or not the G8 invitation to the O5 bears fruit, no major reform has yet taken place in the structure or governance of the specialized

institutions that implement the international economic policy decisions of the “executive committee.” The first thing to observe is that each of the specialized economic institutions, especially WTO, IMF and the

World Bank, has a strong mandate in its own field and that there is no effective mechanism to bring about inter-institution coherence other than the fact that the G7 heads of state can make their respective trade,

finance and development ministers work together in the institutions they share in governing.

11

On paper, the international trade and financial institutions are meant to cooperate with each other. Indeed, IMF’s charter states that its purpose includes facilitating “the expansion and balanced growth of international

trade.”12

In fact, the ministerial oversight committees of the Bretton Woods institutions — the International Monetary and Financial

10 The issues, as stated in the joint communiqué of Germany and the 5

leaders at the Heiligendamm Summit (June 2007), were: “promoting cross

border investment to our mutual benefit; promoting research and

innovation; development, particularly Africa; and sharing knowledge for

improving energy efficiency.” It may be noted that the G20, described

below, only deals with financial issues and that proposals to raise it to heads

of state level have not borne fruit.

11 To be fair, the G7 is less in control in the WTO than in the Fund and Bank. Under the GATT, once a deal was brokered between the US, Europe and Japan, it was fairly certain to be adopted globally. This can no longer be assured in the larger WTO.

12 See Articles of Agreement of the International Monetary Fund, adopted at the United Nations Monetary and Financial Conference, Bretton Woods, New Hampshire, July 22, 1944, Article I.

8 Debt and Trade Making Linkages for the Promotion of Development

Committee (24 finance ministers and central bank governors) and the Development Committee (24 finance and development cooperation

ministers) — do not hesitate to discuss aspects of trade policy as they impinge on their respective mandates. But these committees are not empowered to reach decisions on trade policy.

13 In addition, the WTO’s

founding documents include an explicit declaration to cooperate with the IMF and the World Bank to achieve “greater coherence in global economic policymaking,” while mutually respecting the mandates and autonomy of each institution.

14 In practice, this has meant merely that

senior managers of the Fund and Bank are given observer status at the ministerial meetings of the WTO (consisting of trade ministers of the full membership), and similarly management of WTO may attend the

Bank/Fund ministerial meetings.15

This does not add up to a mechanism to reach coherence among international trade and financial policies.

UNCTAD and the UN General Assembly

Once upon a time, however, there was a broad international effort to forge a coherent set of international economic policies that would be consistent with promoting the development of the developing countries.

The effort began with the United Nations Conference on Trade and Development (UNCTAD) in 1964. You will find that integrated discussions of trade and finance took place at that conference and that the follow up mechanism that was instituted after the conference sought

to continue such discussions to the point of negotiation on specific trade and financial policies. A permanent structure was created of specialized standing commissions under an overarching body, the Trade and

Development Board (TDB). Every four years, UNCTAD would meet as a major international conference, assess the work so far, and give new discussion and negotiation mandates for the next four years, which the TDB would oversee.

Although certain policy measures were successfully negotiated already

13 Formally, the committees are advisory in their own institutions, as the executive boards and boards of governors have decision-making power; nevertheless, the policy advice of the committees is routinely implemented by the IMF and the World Bank.

14 See “Declaration on the Contribution of the World Trade Organization to Achieving Greater

Coherence in Global Economic Policymaking,” which forms part of the “legal texts” concluding the Uruguay Round, adopted in Marrakesh, April 15, 1994.

15 This notwithstanding, cooperation on technical assistance and staff consultation on specialized topics have been more intense.

The Political Dimensions of Linking Debt and Trade 9

in the 1960s, such as the Generalized System of [Tariff] Preferences (1968), UNCTAD reached its high point as a negotiating forum on a

range of trade and financial issues in the 1970s. While it was not empowered to strengthen the overall policy coherence with development in IMF, the World Bank or the GATT, donor governments made

commitments in UNCTAD on aid and debt policies (including retroactively adjusting the terms of outstanding aid loans to match the easier terms of more recent loans, and agreeing on a nascent set of principles for renegotiating sovereign debt). The Integrated Program for

Commodities produced detailed agreements to smooth out price fluctuations on specific international markets, including through the use of buffer stocks (which IMF agreed to support through a new window

for loans to make buffer stock purchases). Agreements were also reached on international shipping.

16

Although I am sure the specific negotiations were never easy, I imagine they benefited from a political commitment reached in the UN General Assembly in 1974, which called for the establishment of a New

International Economic Order (NIEO). It was not an accident that the special Assembly meeting that issued the call took place soon after the first sharp increase in petroleum prices managed by the Organization of

the Petroleum Exporting Countries (OPEC). This was followed in 1975 by another special session of the General Assembly on economic issues that did not break any new ground, although separately, the IMF

adopted special lending programs for oil-importing developing countries in distress.

There was a view that the 1975 General Assembly session failed to produce more than a non-committal text because too many countries had to be brought together to reach consensus. Thus, a smaller group of

countries from the North and South was convoked as the Conference on International Economic Cooperation in Paris in 1976. The implicit deal that was targeted was more stable oil markets in exchange for enhanced

trade and financial cooperation for development. But there was no breakthrough in Paris either and at the end of the decade the discussions returned to the United Nations.

This is where I entered the scene as a junior staff member of the UN Secretariat in New York. It was a time of major change in the

16 See UNCTAD, Beyond Conventional Wisdom in Development Policy: An Intellectual History of UNCTAD, 1964-2004, United Nations, 2004.

10 Debt and Trade Making Linkages for the Promotion of Development

Secretariat. UNCTAD had decided to consolidate its staff in Geneva and reduced its New York office to representational duties in the

General Assembly. Some of the economists who remained behind in New York joined the Department of Economic and Social Affairs, which was also reorganizing. Most important in our context is that

France sent Jean Ripert to be the new Under-Secretary-General in charge of that department. As he told a small team of DESA and ex-UNCTAD staff that would assist him, he came with a mandate from France to try to make a success of the resumed North-South Dialogue at

the UN. He had a limited and, he knew, temporary opportunity. He felt, however, that there was enough good will for one more attempt to forge a comprehensive deal for development.

It failed and I witnessed the moment it happened. The General

Assembly had convoked itself in 1979 as a Committee of the Whole (COW) to continue the Paris discussions. Some governments sent senior officials to lead their negotiations, underlining the importance of the opportunity. And yet, the discussions got stuck on words. There was no political will to negotiate on substance.

The COW had broken into working groups on the different chapters of the proposed declaration. I was assigned to assist in the one dealing with financial cooperation. Like the other groups, it met in one of what were then smoke-filled rooms in the basement of the UN building in

New York. But instead of negotiating on actual policies, the country representatives were hung up on whether they should spell the New International Economic Order with upper or lower-case letters, and

whether it should be “a” new international order or “the” new order. Lower-level diplomats carried out the negotiations, but senior officials might come in from time to time to listen to how they were going.

Richard Cooper, who was US Under-Secretary of State for Economic Affairs in the administration of Jimmy Carter, came to listen to this conversation and after a few moments said in a stage whisper that this

was [expletive deleted] and he got up and left.17

That was the end of it. He was right. There would be no breakthrough here either.

Things only got worse for the North-South Dialogue in the 1980s. The United States joined the United Kingdom as a market fundamentalist regime in 1981, while rolling back inflation became the first priority of

economic policy in all the G7 countries, whatever the cost and whoever

17 I asked him about it many years later and he only denied the expletive.

The Political Dimensions of Linking Debt and Trade 11

would bear it. In the widespread recession that followed, oil and other commodity prices plummeted, after having peaked at the end of the

inflationary 1970s. The ensuing debt crisis hobbled many major (and minor) developing countries. Latin America would later refer to the 1980s as the “lost decade,” and Africa would see per capita output fall

in the 1980s and then again in the 1990s. One may conclude that the North no longer felt it needed to cut a deal with the South. Indeed, UNCTAD lost its role as a negotiating forum and today its quadrennial conferences — I hesitate to say this but I think it is true — merely set

the research and technical assistance agenda of the organization until the next conference.

The Monterrey Opening

There is an aspect of the story above that is not much commented upon. The UN is a foreign ministry forum, just as IMF is a finance ministry/central bank forum and WTO is for trade ministries. Whenever

the UN found itself a locus for substantive North-South economic policy agreements, it seems it was always for foreign policy reasons. Initially, development policy followed naturally from the UN’s role in

decolonization. But decolonization was largely over by the 1970s so something else must have brought foreign policy makers to call for an NIEO at the UN.

Indeed, the North was then absorbing the fact that power over a central commodity had been grabbed by certain countries of the South. A

number of major commodity prices had long been controlled, often in collaboration between producers and consumers, such as the supportive role the US tin stockpile played in helping to manage the international

tin price. OPEC, on the other hand, was purely a supplier organization, even if some of its members were close allies of the major powers.

18 It

has even been said — but I have no way to know if it is true — that Henry Kissinger, US Secretary of State in the administrations of Richard

Nixon and Gerald Ford, conceived the 1974 General Assembly special session on the NIEO as a way to talk the developing world into exhaustion, doing nothing while seeming to do something. In fact, that

is too cynical, as some policy advances were made after 1974, including

18 The discovery that OPEC could effectively increase oil prices sent a shock wave through the US administration and Congress at the time. Some “hawks” clamored for military intervention

to “defend” oil production and transportation lines. They were civilians, of course, while the military authorities cautioned that they were unprepared for a desert war (private conversations, US Army War College, Carlisle Barracks, Pennsylvania, 1974).

12 Debt and Trade Making Linkages for the Promotion of Development

in UNCTAD as mentioned earlier.

In any event, by the 1980s, OPEC showed itself to be less formidable than feared, and all the joint international commodity arrangements with economic provisions eventually broke down. The attention of foreign

ministries at the UN was increasingly limited to the political side of the house; economic discussions were a side-show and some governments sent less and less skilled diplomats to cover the discussions that did take

place. The action on economic policy matters was elsewhere. Indeed, when WTO was created, the trade negotiators very explicitly decided not to become a specialized agency of the United Nations.

Nevertheless, the North-South Dialogue never fully disappeared from the UN. In 1980 there was an effort to get a “global round” of

negotiations going; it never happened. In 1990 there was another effort. In 1997 the newly appointed Deputy Permanent Representative of Venezuela, Ambassador Oscar de Rojas, decided to try again. This time

it led to the 2002 International Conference on Financing for Development (FfD), which adopted the Monterrey Consensus.

The process that led to the summit meeting at Monterrey was unique. It is the only major UN conference that originated as a developing country proposal. It began as a Latin American initiative, was adopted by the

developing country governments at the UN represented by the Group of 77, but then it also drew support from the United States, joined by Japan and the Republic of Korea, and finally the Europeans. It found a

champion in the World Bank, which seconded staff to assist the UN Secretariat in preparing for the conference and was supported as well by the IMF and the management of WTO.

This is not the place to discuss in any detail how the process of preparing Monterrey overcame the hesitancy of most governments to

look to the UN as a potentially serious forum on international economic matters.

19 I would instead just note that several factors made the UN an

attractive political forum on economic policy and Monterrey an

opportune occasion. First, the credibility of the IMF and World Bank had been increasingly challenged as the 1990s wore on, not only in

19 For that, and a discussion of backsliding after 2002, see Barry Herman, “The Politics of Inclusion in the Monterrey Process,” in Jessica Green and W. Bradnee Chambers, eds., The

Politics of Participation in Sustainable Development Governance (United Nations University Press, 2006); also available as DESA Working Paper No. 23, United Nations (ST/ESA/2006/DWP/23), April 2006.

The Political Dimensions of Linking Debt and Trade 13

developing countries that had been through “structural adjustment,” but also in the legislatures of some donor countries, especially the US.

Second, the UN had successfully given voice to the European social agenda through the global UN conferences on environment, gender and social affairs more broadly. Indeed, it appears that World Bank

management appreciated that the anti-poverty focus of its new President, James Wolfensohn, could benefit from embracing the UN. Third, the onset of the Asian financial crisis in 1997, followed by the meltdown of Russia while IMF held its hand in 1998, brought the

reappearance of “financial architecture reform” to the world policy agenda after two decades without major institutional change. This time, the developing countries were demanding a bigger voice in international

policy reform and it was hard to argue against their view; nevertheless, the G7 response maintained its centrality by selectively inviting certain finance ministers and central bank governors to meet with them in a new

Group of 20 (G20).20

Fourth, the “9/11” bombing of the World Trade Center in New York shook the confidence of the developed world in its own physical security, raising the attractiveness of pending possibilities to reach out in an expression of solidarity with the developing world.

I do not want to suggest Monterrey was a North-South love-in.

Relations were always delicate among governments and with the specialized multilateral institutions, in particular with WTO. The degree of delicacy as regards WTO is perhaps worth noting as an extreme

example (with the other institutions it was rather just under the surface). Allow me one anecdote to give you a sense of this.

In 2001, the Chairman of the Trade and Development Committee of WTO, Ambassador Nathan Irumba (Uganda), while in New York, invited the Bureau of the FfD Preparatory Committee to come to the

WTO in Geneva and have an informal inter-governmental and inter-institutional meeting to help advance FfD preparations. The Bureau had already met with the Executive Boards of the IMF and the World Bank.

20 The G20 first met in 1999, after the G7 tried meetings with different configurations of

middle-sized economies (G22, G33). Besides the G7, the members include Argentina, Australia, Brazil, China, India, Indonesia, Republic of Korea, Mexico, Russian Federation, Saudi Arabia, South Africa, and Turkey. The finance minister of the rotating Presidency of the

Council of the European Union and the head of the European Central Bank attend as well. “To ensure global economic forums and institutions work together,” the heads of IMF and the World Bank and the chairs of the two Bretton Woods ministerial committees also attend (See

www.g20.org). The latter notwithstanding, the G20 have sufficient weight and influence to assure that any policy consensus they might reach is also adopted by those ministerial committees.

14 Debt and Trade Making Linkages for the Promotion of Development

It only made sense that it also meet with the WTO. A WTO colleague privately described the Trade and Development Committee as less a

negotiating forum than a “church meeting,” but the Bureau saw it as an opportunity and went anyway. The first meeting at WTO was with the Director-General, Michael Moore, accompanied by Ambassador Stuart

Harbinson (Hong Kong, China), the Chair of the General Council, which is the committee of the whole that oversees WTO activities between ministerial meetings. Senior WTO management also participated. The discussions were very friendly but also frank. After

that, it was all downhill. The inter-governmental meeting began with WTO staff giving briefings on the current state of negotiations in the different WTO committees, which lasted for about an hour. The

Chairman then said thank you and adjourned the meeting. The Chair of the UN committee, Ambassador Jørgen Bøjer (Denmark), rose to complain that the UN delegation had come all the way from New York

to have a meeting and now they were not having a meeting. The WTO Chair said, in effect, “That’s right. We are not ready to talk to you.” And no interchange on substantive matters took place.

Conclusion: Use the UN Opportunity to Start a New Reform

Process

It is now seven years later. WTO negotiations are stuck. The organization continues to go through the motions of negotiations even

though the negotiating authority of one major party, the United States, has expired and will not be renewed before 2009 when a new US president is in office. The IMF has run out of “paying customers,” in

that when Turkey repays its last outstanding loan, there will be very few (and small) non-concessional loans still outstanding. This may only be temporary, but several countries have repaid their loans before they

were due and all former customers are seeking a large enough cushion of foreign exchange reserves to prevent having to return to IMF for help under its traditional conditionality. The World Bank is still recovering

from the presidency of Paul Wolfowitz and the distrust he sowed in borrowing countries. Meanwhile, the US financial crisis that began in the summer of 2007 has caused bank failures in Europe as well as in the US, and is raising questions once again of the need for international

financial architecture reform. This time, developing countries are not yet victims and are concerned to stop the crisis from spreading to them. They also want to protect their overseas financial assets invested in the

developed world. Taking all these factors together, perhaps it is again time for a political meeting on international economic reform at the UN.

The Political Dimensions of Linking Debt and Trade 15

The G7 or G8 will not be able to solve what it seems fair to call a crisis of international economic cooperation. It will not do for the G8 to

unilaterally decide who should speak for the rest of the world in discussions with them on global economic policy. Indeed, nobody elected the G8 to carry out global economic policy leadership. And

even if the 7 original countries were the dominant economic powers in the 1970s, they do not have quite the same exclusive centrality today, and it is even less clear that they will be the right club 10 years from now. Moreover, while there is a certain logic in a two-stage structure