Embed Size (px)

Citation preview

Dealing with disruption 16th Annual Global CEO Survey Key findings in the forest, paper & packaging industry

www.pwc.com/ceosurvey

February 2013

PwC

Welcome Far-reaching changes are taking place, and they’re taking place faster than ever. In this new era of ‘stable instability’, risks that once seemed improbable and even remote have become the norm and for CEOs across the world, ‘expect the unexpected’ has become the mantra. The only solution is to build organisations that can thrive amidst disorder: organisations that are agile and adaptable, able to cope with disruption, and emerge stronger than before.

We polled 1,330 CEOs in 68 countries, and talked face-to-face with another 33 CEOs, in our 16th Annual Global CEO Survey, to find out how they’re creating resilient organisations that can flourish under stress. Dealing with disruption shows that CEOs are:

• focusing on a few carefully selected initiatives to stimulate organic growth, • exploring new ways to attract and keep customers and • balancing efficiency with agility.

And to succeed in these three goals, CEOs are recognising the role that trust plays, and that they’ll have to work hard to repair the bridges between business and society.

This report is a summary of our key findings in the forest, paper & packaging sector, based on interviews with 38 CEOs in 15 countries.

To see the full results of the 16th Annual Global Survey, please visit www.pwc.com/ceosurvey.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 2

PwC

Contents

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 3

Page

Introduction 4

The disruptive decade 6

What worries CEOs 9

What CEOs are doing • Targeting pockets of opportunity 14

• Concentrating on the customer 18

• Improving operational effectiveness 21

It’s a question of trust 25

PwC

Introduction

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 4

PwC

Introduction Profound changes are happening in the forest, paper & packaging industry. CEOs are dealing with significant shifts in demand patterns, increasing scarcity of supply, and overcapacity in some regions and grades. Our sector results for this year’s 16th Annual Global CEO Survey reflect these concerns. Forest, paper & packaging CEOs say they are:

• Dealing with overcapacity through cost reduction

• Exiting unprofitable businesses

• Addressing natural resource issues

With the economic situation uncertain and so many changes happening, it’s no wonder that forest, paper & packaging CEOs are less confident of growth over the next 12 months than are their peers in other sectors.

But there’s hope for the future too. We see signs of significant changes happening in sector business models, with a strong emphasis on R&D and deals. Forest, paper & packaging CEOs tell us they are focusing on developing the strong leaders they’ll need to drive change and continuing the sector’s emphasis on environmental responsibility.

The result? Looking out over three years, far more forest, paper & packaging CEOs are optimistic about their company’s prospects for revenue growth.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 5

PwC

The disruptive decade

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 6

only 21% of forest, paper & packaging CEOs are very confident they can raise the revenues their companies generate over the next 12 months

PwC

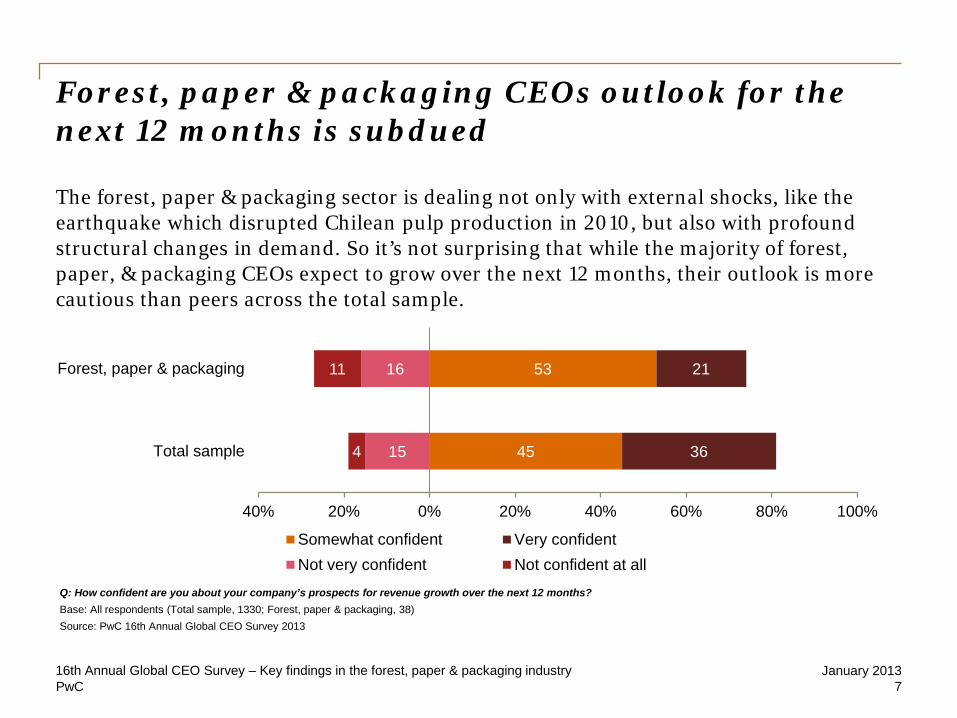

Forest, paper & packaging CEOs outlook for the next 12 months is subdued

The forest, paper & packaging sector is dealing not only with external shocks, like the earthquake which disrupted Chilean pulp production in 2010, but also with profound structural changes in demand. So it’s not surprising that while the majority of forest, paper, & packaging CEOs expect to grow over the next 12 months, their outlook is more cautious than peers across the total sample.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 7

45

53

36

21

15

16

4

11

40% 20% 0% 20% 40% 60% 80% 100%

Total sample

Forest, paper & packaging

Somewhat confident Very confidentNot very confident Not confident at all

Q: How confident are you about your company’s prospects for revenue growth over the next 12 months? Base: All respondents (Total sample, 1330; Forest, paper & packaging, 38) Source: PwC 16th Annual Global CEO Survey 2013

PwC

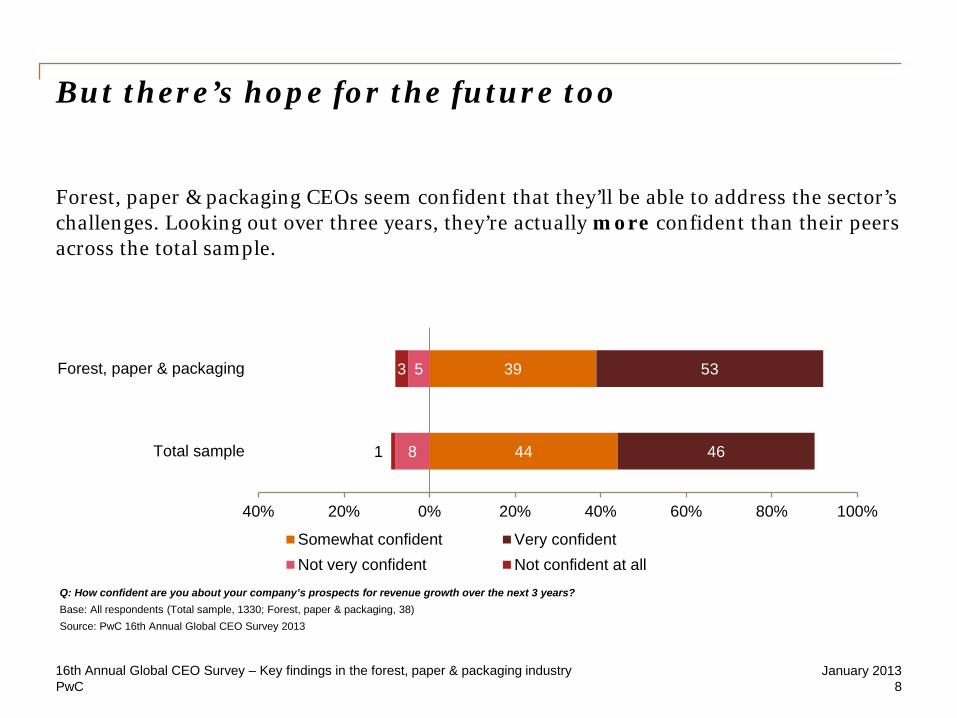

But there’s hope for the future too

Forest, paper & packaging CEOs seem confident that they’ll be able to address the sector’s challenges. Looking out over three years, they’re actually more confident than their peers across the total sample.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 8

44

39

46

53

8

5

1

3

40% 20% 0% 20% 40% 60% 80% 100%

Total sample

Forest, paper & packaging

Somewhat confident Very confidentNot very confident Not confident at all

Q: How confident are you about your company’s prospects for revenue growth over the next 3 years? Base: All respondents (Total sample, 1330; Forest, paper & packaging, 38) Source: PwC 16th Annual Global CEO Survey 2013

PwC

What worries CEOs?

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 9

PwC

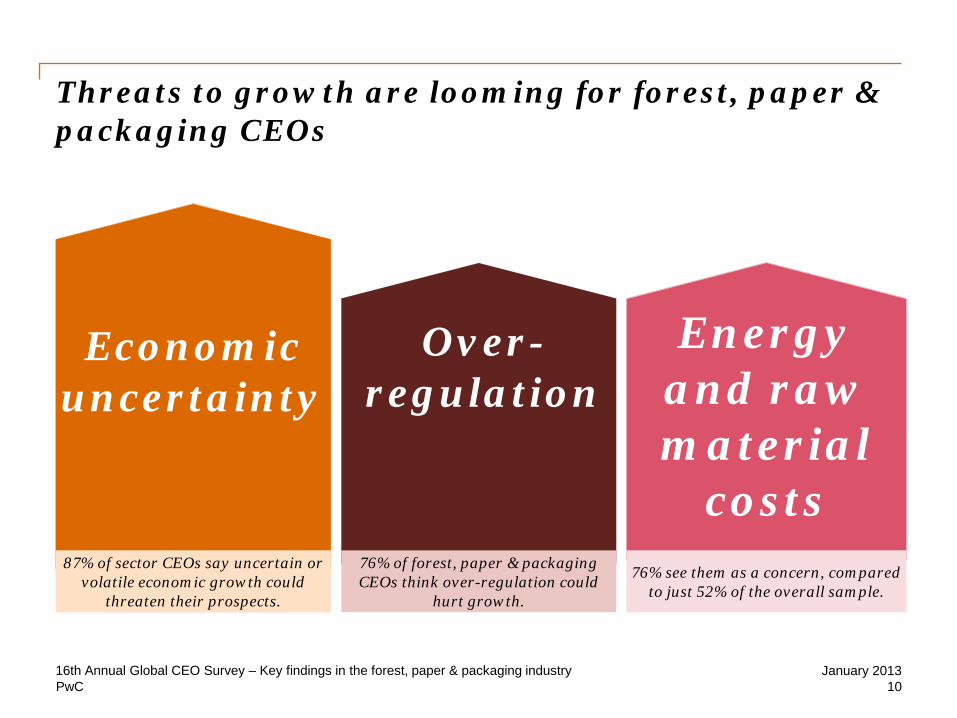

Threats to growth are looming for forest, paper & packaging CEOs

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 10

87% of sector CEOs say uncertain or volatile economic growth could

threaten their prospects.

76% of forest, paper & packaging CEOs think over-regulation could

hurt growth.

76% see them as a concern, compared

to just 52% of the overall sample.

Economic uncertainty

Over-regulation

Energy and raw material

costs

PwC

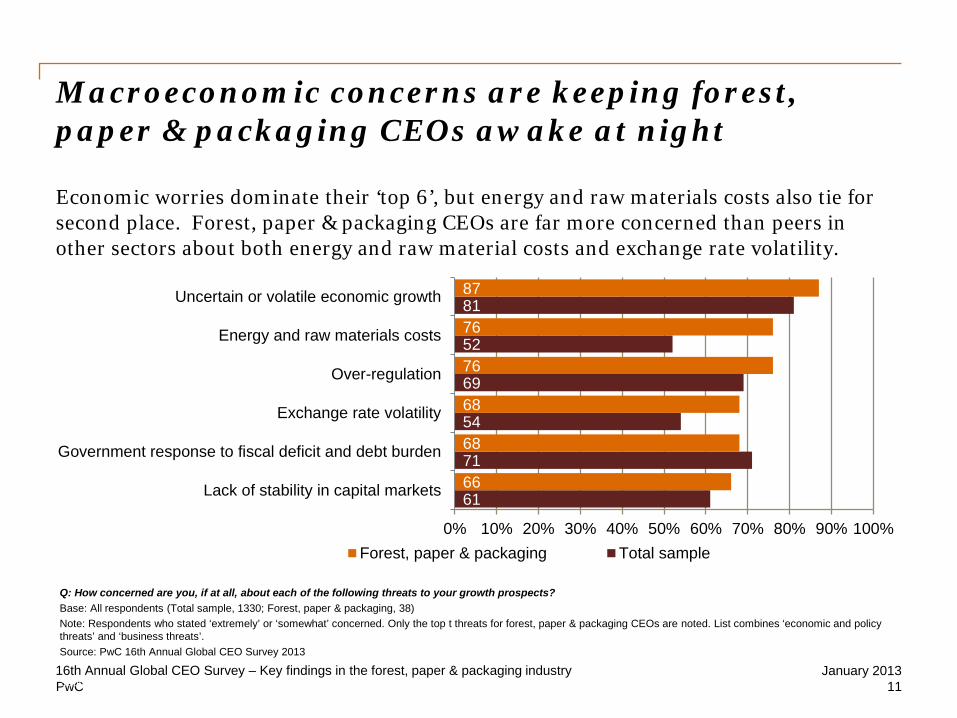

Macroeconomic concerns are keeping forest, paper & packaging CEOs awake at night

Economic worries dominate their ‘top 6’, but energy and raw materials costs also tie for second place. Forest, paper & packaging CEOs are far more concerned than peers in other sectors about both energy and raw material costs and exchange rate volatility.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 11

61

71

54

69

52

81

66

68

68

76

76

87

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Lack of stability in capital markets

Government response to fiscal deficit and debt burden

Exchange rate volatility

Over-regulation

Energy and raw materials costs

Uncertain or volatile economic growth

Forest, paper & packaging Total sample

Q: How concerned are you, if at all, about each of the following threats to your growth prospects? Base: All respondents (Total sample, 1330; Forest, paper & packaging, 38) Note: Respondents who stated ‘extremely’ or ‘somewhat’ concerned. Only the top t threats for forest, paper & packaging CEOs are noted. List combines ‘economic and policy threats’ and ‘business threats’. Source: PwC 16th Annual Global CEO Survey 2013 Source: PwC 16th Annual Global CEO Survey 2013

PwC

Facing natural resource threats

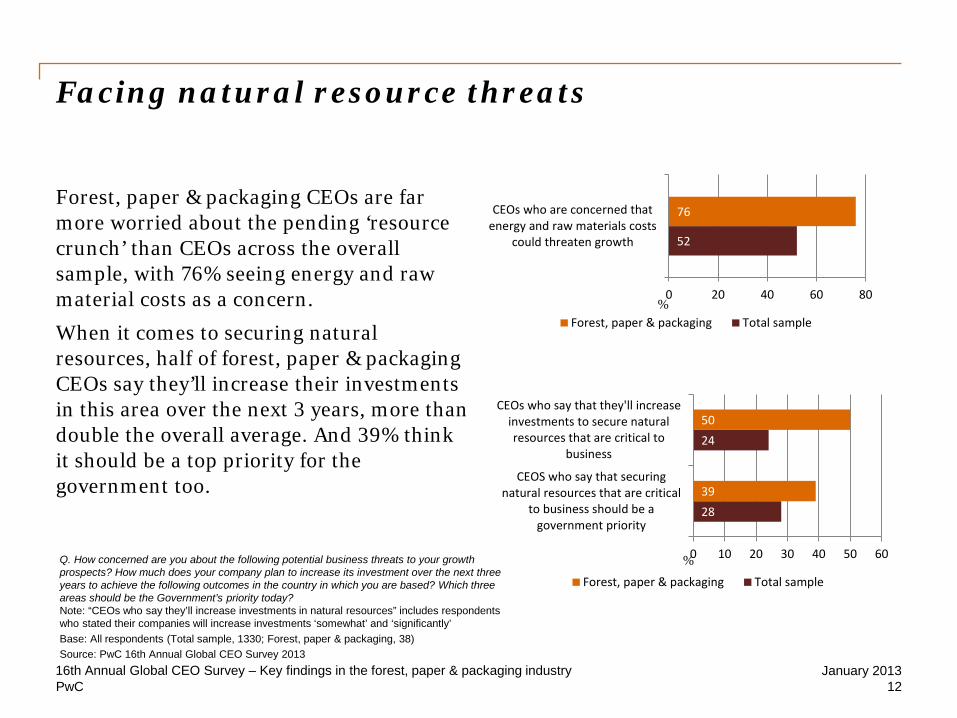

Forest, paper & packaging CEOs are far more worried about the pending ‘resource crunch’ than CEOs across the overall sample, with 76% seeing energy and raw material costs as a concern.

When it comes to securing natural resources, half of forest, paper & packaging CEOs say they’ll increase their investments in this area over the next 3 years, more than double the overall average. And 39% think it should be a top priority for the government too.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 12

52

76

0 20 40 60 80

CEOs who are concerned thatenergy and raw materials costs

could threaten growth

Forest, paper & packaging Total sample

28

24

39

50

0 10 20 30 40 50 60

CEOS who say that securingnatural resources that are critical

to business should be agovernment priority

CEOs who say that they'll increaseinvestments to secure naturalresources that are critical to

business

Forest, paper & packaging Total sample

Q. How concerned are you about the following potential business threats to your growth prospects? How much does your company plan to increase its investment over the next three years to achieve the following outcomes in the country in which you are based? Which three areas should be the Government’s priority today? Note: “CEOs who say they’ll increase investments in natural resources” includes respondents who stated their companies will increase investments ‘somewhat’ and ‘significantly’ Base: All respondents (Total sample, 1330; Forest, paper & packaging, 38) Source: PwC 16th Annual Global CEO Survey 2013

%

%

PwC

So what are CEOs doing?

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 13

• Targeting pockets of opportunity • Concentrating on the customer • Improving operational effectiveness

PwC

Targeting pockets of opportunity

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 14

50% of forest, paper & packaging CEOs entered into a new strategic alliance or joint venture in the past 12 months

PwC

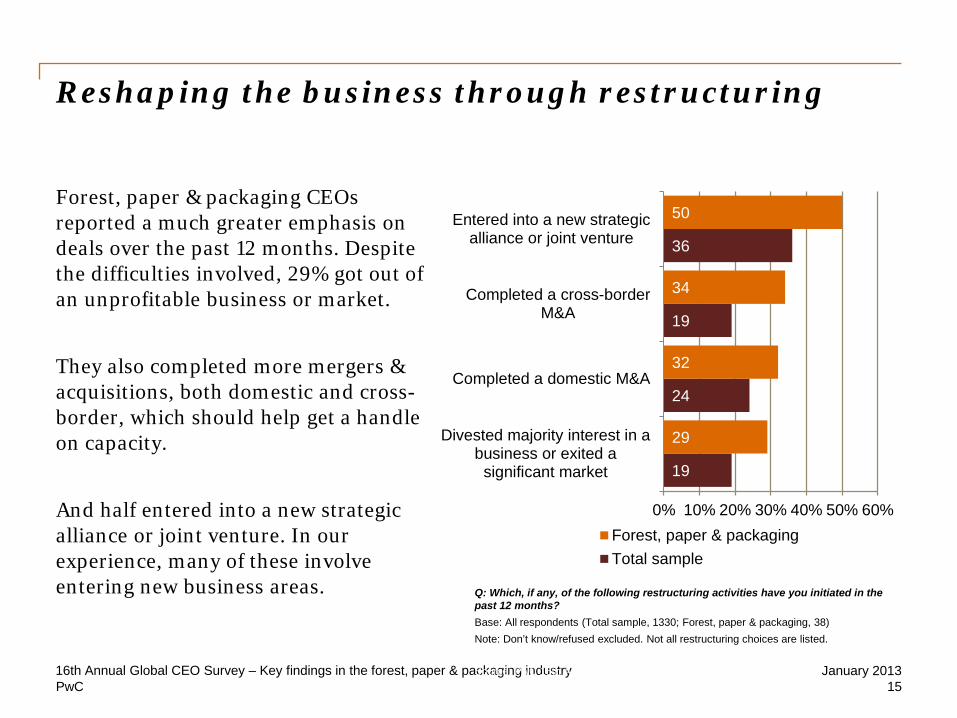

Reshaping the business through restructuring

Forest, paper & packaging CEOs reported a much greater emphasis on deals over the past 12 months. Despite the difficulties involved, 29% got out of an unprofitable business or market.

They also completed more mergers & acquisitions, both domestic and cross-border, which should help get a handle on capacity.

And half entered into a new strategic alliance or joint venture. In our experience, many of these involve entering new business areas.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 15

19

24

19

36

29

32

34

50

0% 10% 20% 30% 40% 50% 60%

Divested majority interest in abusiness or exited a

significant market

Completed a domestic M&A

Completed a cross-borderM&A

Entered into a new strategicalliance or joint venture

Forest, paper & packagingTotal sample

Q: Which, if any, of the following restructuring activities have you initiated in the past 12 months? Base: All respondents (Total sample, 1330; Forest, paper & packaging, 38) Note: Don’t know/refused excluded. Not all restructuring choices are listed. Source: PwC 16th Annual Global CEO Survey 2013

PwC

and continuing to do deals next year, too

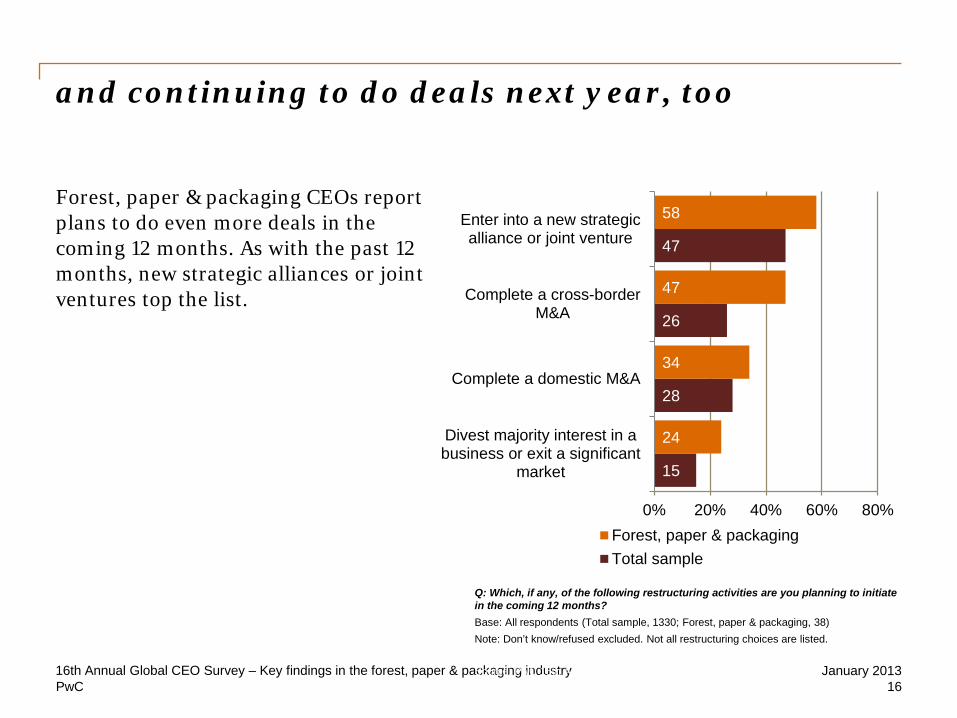

Forest, paper & packaging CEOs report plans to do even more deals in the coming 12 months. As with the past 12 months, new strategic alliances or joint ventures top the list.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 16

15

28

26

47

24

34

47

58

0% 20% 40% 60% 80%

Divest majority interest in abusiness or exit a significant

market

Complete a domestic M&A

Complete a cross-borderM&A

Enter into a new strategicalliance or joint venture

Forest, paper & packagingTotal sample

Q: Which, if any, of the following restructuring activities are you planning to initiate in the coming 12 months? Base: All respondents (Total sample, 1330; Forest, paper & packaging, 38) Note: Don’t know/refused excluded. Not all restructuring choices are listed. Source: PwC 16th Annual Global CEO Survey 2013

PwC

R&D and innovation becoming a top priority

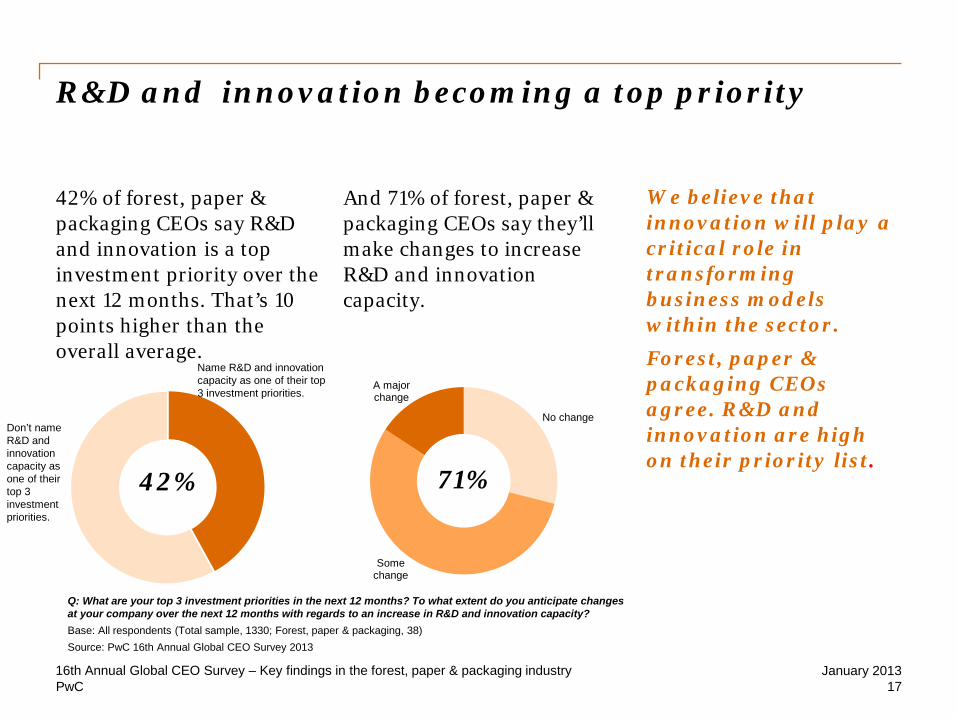

42% of forest, paper & packaging CEOs say R&D and innovation is a top investment priority over the next 12 months. That’s 10 points higher than the overall average.

And 71% of forest, paper & packaging CEOs say they’ll make changes to increase R&D and innovation capacity.

We believe that innovation will play a critical role in transforming business models within the sector. Forest, paper & packaging CEOs agree. R&D and innovation are high on their priority list.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 17

42%

No change

Some change

A major change

71%

Q: What are your top 3 investment priorities in the next 12 months? To what extent do you anticipate changes at your company over the next 12 months with regards to an increase in R&D and innovation capacity? Base: All respondents (Total sample, 1330; Forest, paper & packaging, 38) Source: PwC 16th Annual Global CEO Survey 2013

Name R&D and innovation capacity as one of their top 3 investment priorities.

Don’t name R&D and innovation capacity as one of their top 3 investment priorities.

PwC

Concentrating on the customer

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 18

100% of forest, paper & packaging CEOs say that customers have a ‘significant’ influence on their strategy.

PwC

Customers are shaping strategy

This placeholder text (20pt Georgia regular) is intended to show the correct position and size of the real text used in this location. To ensure that you have the correct size, colour and location of the text, it is recommended that you select. Overtype this placeholder text.

In our sector -specific CEO Perspectives reports in 2008 and 2010, we heard a strong message that CEOs viewed top-notch customer service as a truly differentiating factor. That’s validated by this year’s cross-industry results. Forest, paper & packaging is the only sector where every single CEO said customers were a significant influence on their business strategy.

And most forest, paper & packaging CEOs said they’ll increase their efforts to strengthen engagement with customers too.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 19

Are increasing efforts to strengthen customer engagement

87%

PwC

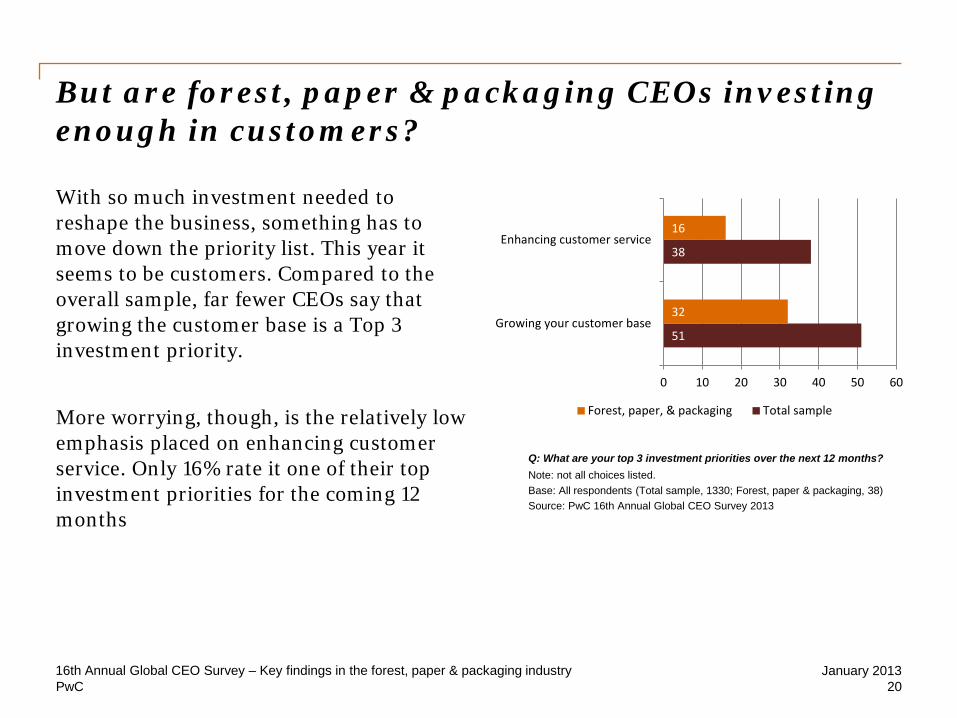

But are forest, paper & packaging CEOs investing enough in customers?

With so much investment needed to reshape the business, something has to move down the priority list. This year it seems to be customers. Compared to the overall sample, far fewer CEOs say that growing the customer base is a Top 3 investment priority.

More worrying, though, is the relatively low emphasis placed on enhancing customer service. Only 16% rate it one of their top investment priorities for the coming 12 months

51

38

32

16

0 10 20 30 40 50 60

Growing your customer base

Enhancing customer service

Forest, paper, & packaging Total sample

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 20

Q: What are your top 3 investment priorities over the next 12 months? Note: not all choices listed. Base: All respondents (Total sample, 1330; Forest, paper & packaging, 38) Source: PwC 16th Annual Global CEO Survey 2013

PwC

Improving operational effectiveness

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 21

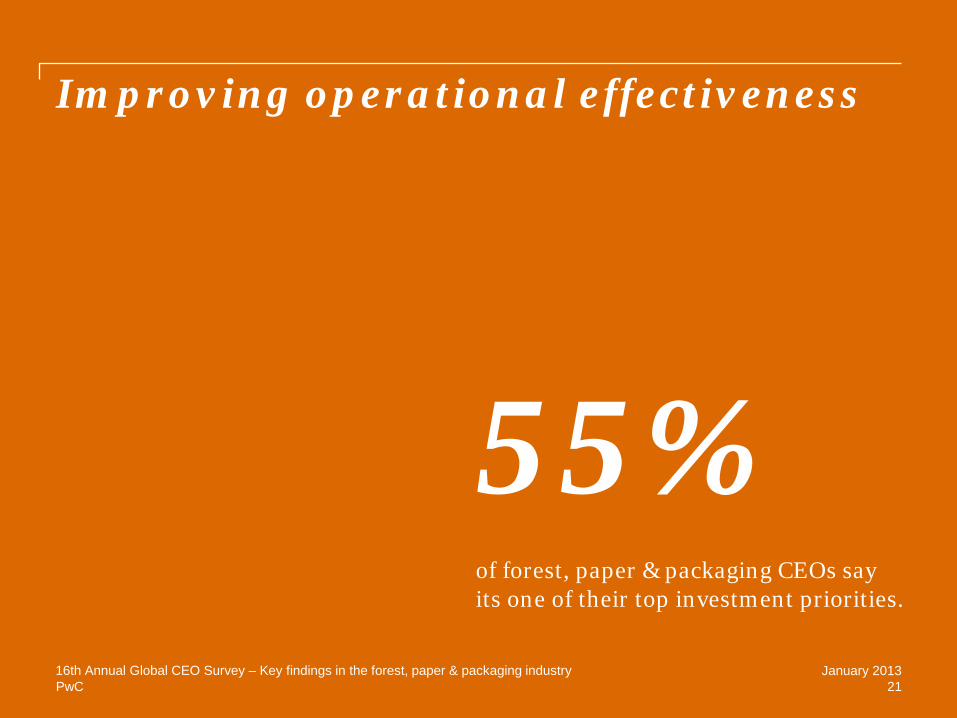

55% of forest, paper & packaging CEOs say its one of their top investment priorities.

PwC

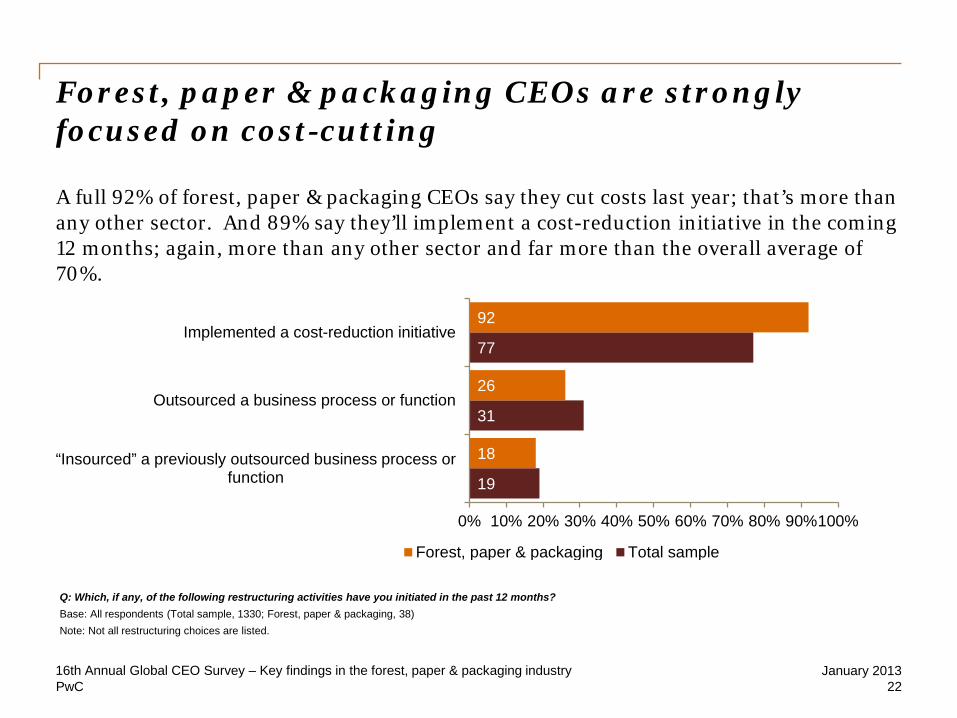

Forest, paper & packaging CEOs are strongly focused on cost-cutting

A full 92% of forest, paper & packaging CEOs say they cut costs last year; that’s more than any other sector. And 89% say they’ll implement a cost-reduction initiative in the coming 12 months; again, more than any other sector and far more than the overall average of 70%.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 22

19

31

77

18

26

92

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%100%

“Insourced” a previously outsourced business process or function

Outsourced a business process or function

Implemented a cost-reduction initiative

Forest, paper & packaging Total sample

Q: Which, if any, of the following restructuring activities have you initiated in the past 12 months? Base: All respondents (Total sample, 1330; Forest, paper & packaging, 38) Note: Not all restructuring choices are listed.

PwC

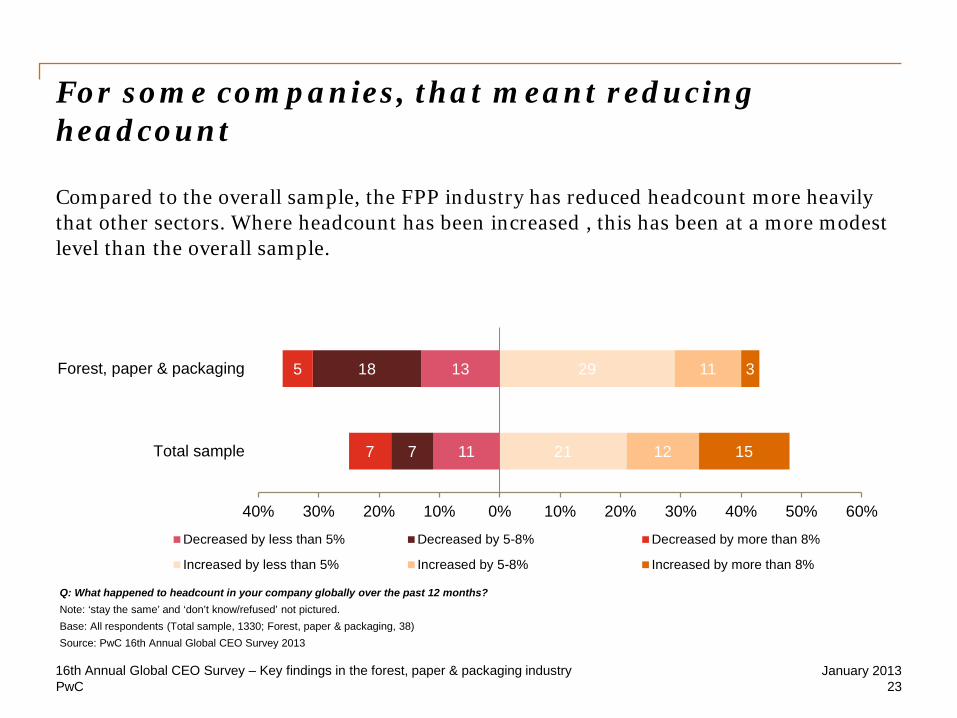

For some companies, that meant reducing headcount

Compared to the overall sample, the FPP industry has reduced headcount more heavily that other sectors. Where headcount has been increased , this has been at a more modest level than the overall sample.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 23

11

13

7

18

7

5

21

29

12

11

15

3

40% 30% 20% 10% 0% 10% 20% 30% 40% 50% 60%

Total sample

Forest, paper & packaging

Decreased by less than 5% Decreased by 5-8% Decreased by more than 8%

Increased by less than 5% Increased by 5-8% Increased by more than 8%

Q: What happened to headcount in your company globally over the past 12 months? Note: ‘stay the same’ and ‘don’t know/refused’ not pictured. Base: All respondents (Total sample, 1330; Forest, paper & packaging, 38) Source: PwC 16th Annual Global CEO Survey 2013

PwC

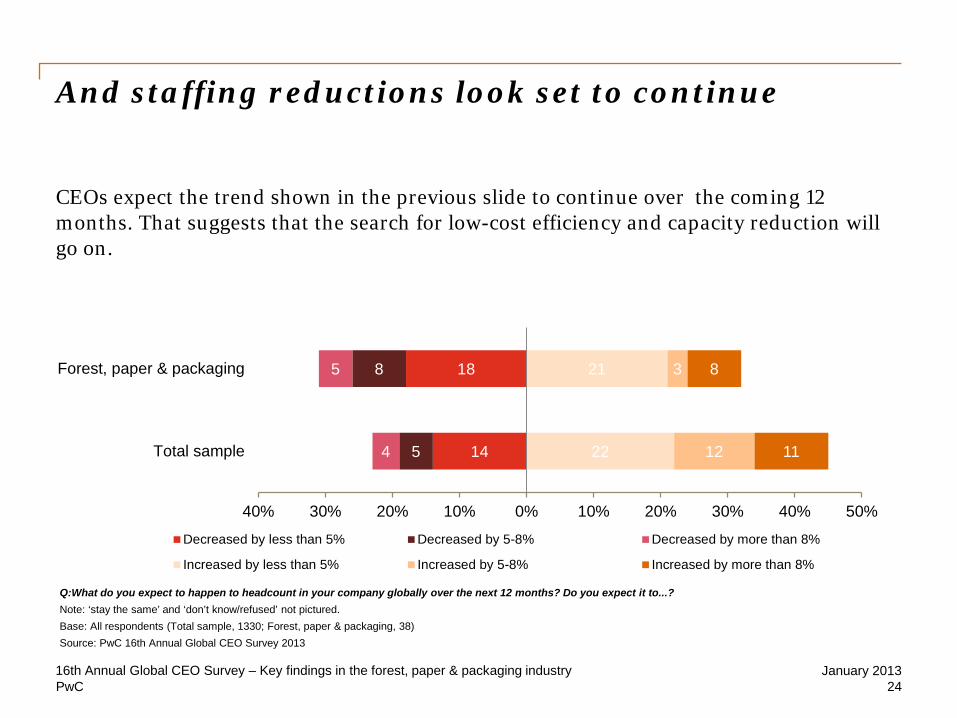

And staffing reductions look set to continue

CEOs expect the trend shown in the previous slide to continue over the coming 12 months. That suggests that the search for low-cost efficiency and capacity reduction will go on.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 24

14

18

5

8

4

5

22

21

12

3

11

8

40% 30% 20% 10% 0% 10% 20% 30% 40% 50%

Total sample

Forest, paper & packaging

Decreased by less than 5% Decreased by 5-8% Decreased by more than 8%

Increased by less than 5% Increased by 5-8% Increased by more than 8%

Q:What do you expect to happen to headcount in your company globally over the next 12 months? Do you expect it to...? Note: ‘stay the same’ and ‘don’t know/refused’ not pictured. Base: All respondents (Total sample, 1330; Forest, paper & packaging, 38) Source: PwC 16th Annual Global CEO Survey 2013

PwC

It’s a question of trust

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 25

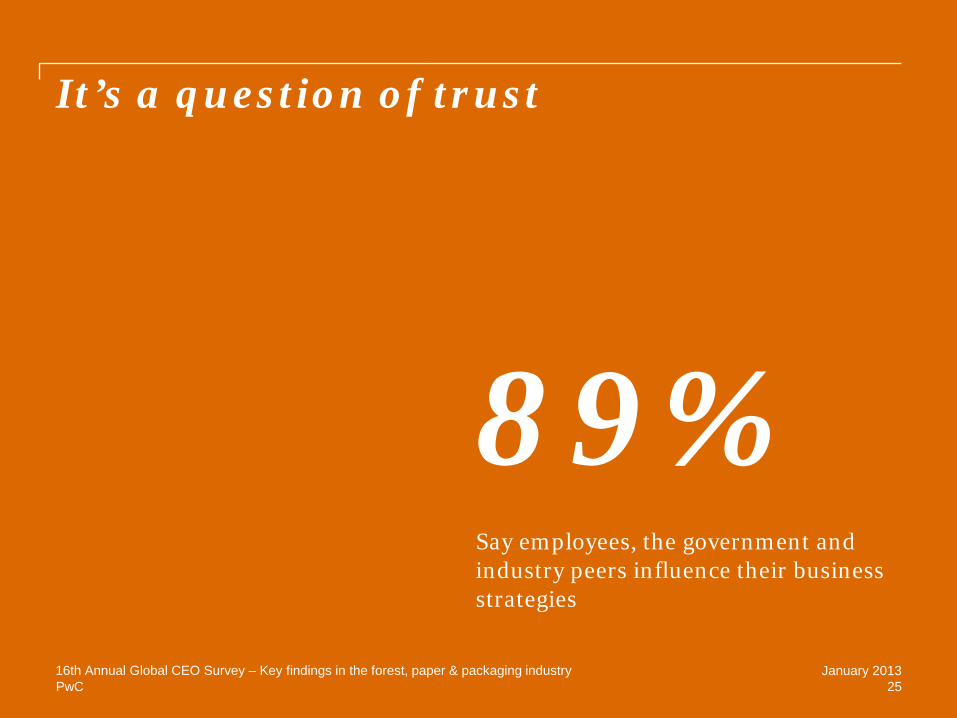

89% Say employees, the government and industry peers influence their business strategies

PwC

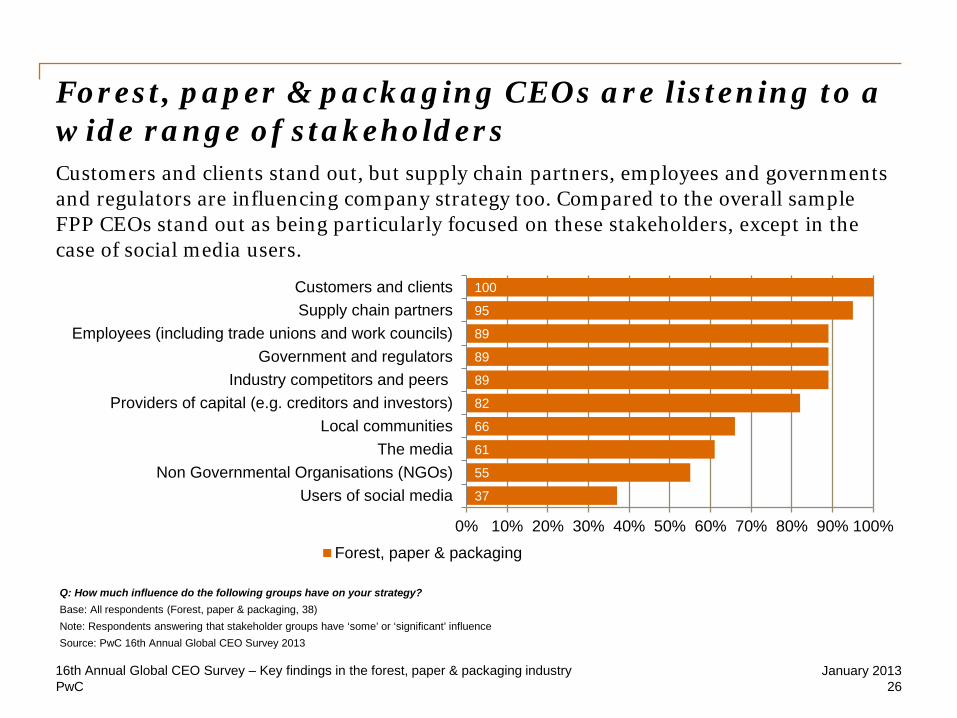

Forest, paper & packaging CEOs are listening to a wide range of stakeholders Customers and clients stand out, but supply chain partners, employees and governments and regulators are influencing company strategy too. Compared to the overall sample FPP CEOs stand out as being particularly focused on these stakeholders, except in the case of social media users.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 26

37

55

61

66

82

89

89

89

95

100

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Users of social mediaNon Governmental Organisations (NGOs)

The mediaLocal communities

Providers of capital (e.g. creditors and investors)Industry competitors and peers

Government and regulatorsEmployees (including trade unions and work councils)

Supply chain partnersCustomers and clients

Forest, paper & packaging

Q: How much influence do the following groups have on your strategy? Base: All respondents (Forest, paper & packaging, 38) Note: Respondents answering that stakeholder groups have ‘some’ or ‘significant’ influence Source: PwC 16th Annual Global CEO Survey 2013 concerned.

PwC

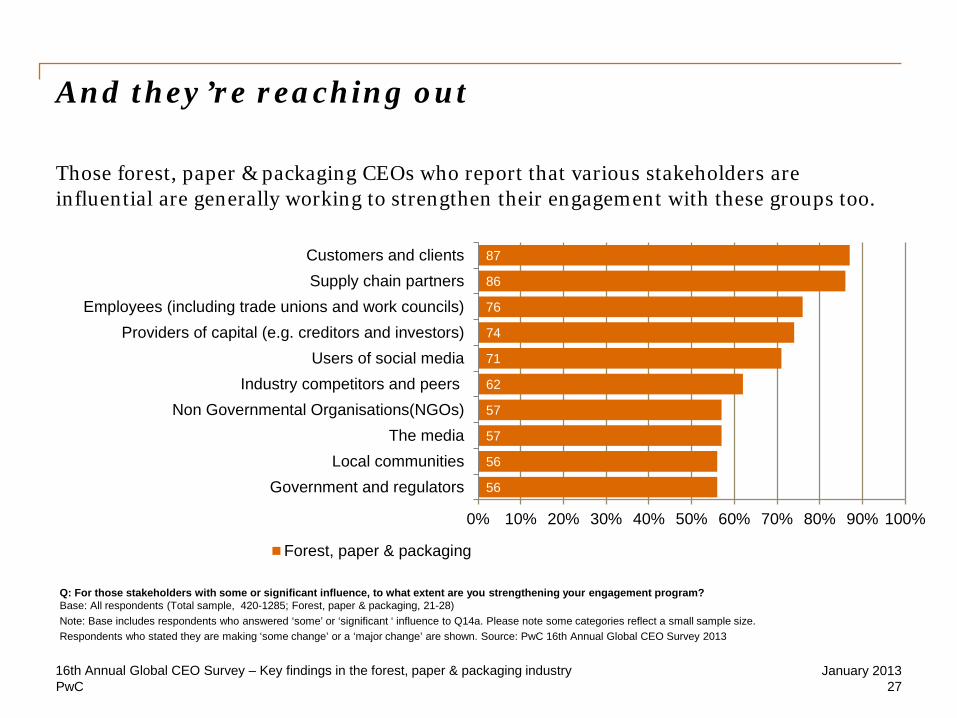

And they’re reaching out Those forest, paper & packaging CEOs who report that various stakeholders are influential are generally working to strengthen their engagement with these groups too.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 27

56

56

57

57

62

71

74

76

86

87

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Government and regulatorsLocal communities

The mediaNon Governmental Organisations(NGOs)

Industry competitors and peersUsers of social media

Providers of capital (e.g. creditors and investors)Employees (including trade unions and work councils)

Supply chain partnersCustomers and clients

Forest, paper & packaging

Q: For those stakeholders with some or significant influence, to what extent are you strengthening your engagement program? Base: All respondents (Total sample, 420-1285; Forest, paper & packaging, 21-28) Note: Base includes respondents who answered ‘some’ or ‘significant ‘ influence to Q14a. Please note some categories reflect a small sample size.’ Respondents who stated they are making ‘some change’ or a ‘major change’ are shown. Source: PwC 16th Annual Global CEO Survey 2013

PwC

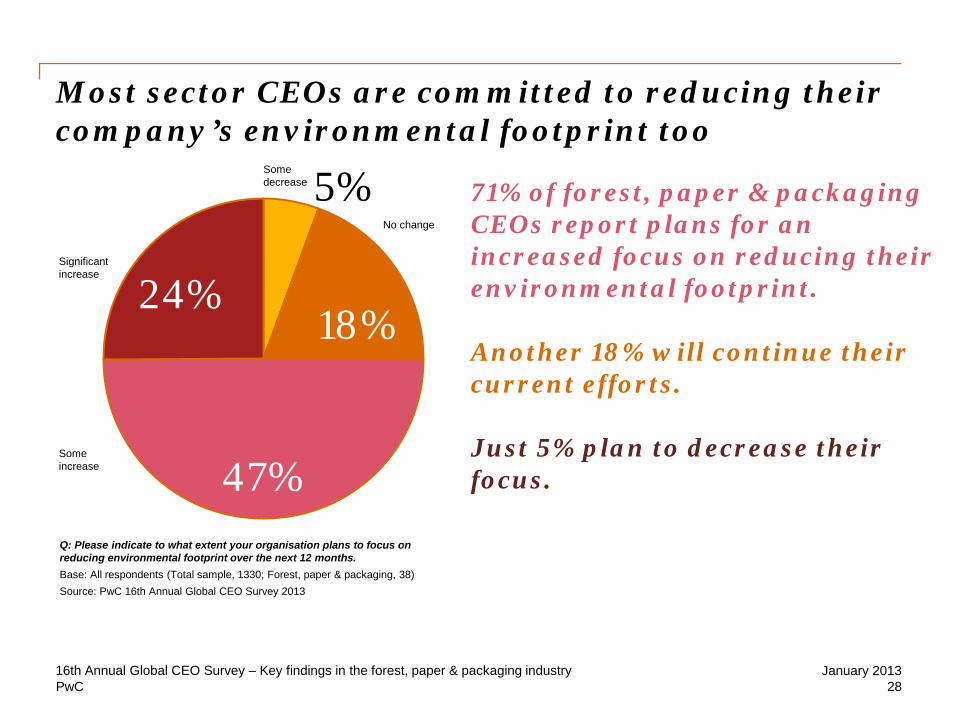

Most sector CEOs are committed to reducing their company’s environmental footprint too

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 28

71% of forest, paper & packaging CEOs report plans for an increased focus on reducing their environmental footprint. Another 18% will continue their current efforts. Just 5% plan to decrease their focus.

5%

18%

47%

24%

Some increase

No change

Some decrease

Q: Please indicate to what extent your organisation plans to focus on reducing environmental footprint over the next 12 months. Base: All respondents (Total sample, 1330; Forest, paper & packaging, 38) Source: PwC 16th Annual Global CEO Survey 2013

Significant increase

PwC

For more information, please contact:

Or visit www.pwc.com/ceosurvey

To continue the discussion on the outlook for the global forest, paper & packaging industry, don't miss PwC's 26th Annual Global Forest Industry Conference. Click here to find out more or register for our conference.

January 2013 16th Annual Global CEO Survey – Key findings in the forest, paper & packaging industry 29

Bruce McIntyre Canadian Leader, Forest, Paper & Packaging Practice

Ian Murdoch European Leader, Forest, Paper & Packaging Practice

Max Blocker United States Leader, Forest, Paper & Packaging Practice

Andrew McPherson Australian Leader, Forest, Paper & Packaging Practice

T: +1 604-806-7595 [email protected]

T: +43 1 501 88 1420 [email protected]

T: +1 (678) 419-4180

[email protected] T: +61 (2) 8266 3275 [email protected]

Download the main report, access the results and explore the CEO interviews from our 16th Annual Global CEO Survey online at www.pwc.com/ceosurvey.

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PwC does do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2013 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.

121211-130640-EA-OS