Embed Size (px)

Citation preview

7/31/2019 DEADLY CLEAR---WHY DOES'N'T THE JUDGE SEE? MINISTERIAL...REALLY??

http://slidepdf.com/reader/full/deadly-clear-why-doesnt-the-judge-see-ministerialreally 1/11

POSTED JULY 1 2012 BY DEADLY CLEAR

The new word in the securities fraud cover-up banter is “ministerial”

– and so very far from the truth. On April 2, 2007, New Century Financial Corporation and its related entities

filed voluntary petitions for relief under Chapter 11 of the UnitedStates Bankruptcy Code in the United States Bankruptcy Court, District of Delaware and is currently heard and administered by the Honorable Kevin J.Carey.With the filing of bankruptcy, New Century took down a list of affiliate / entities including New Century Mortgage Corporation, Home123Corporation, New Century Mortgage Ventures, Midwest Home Mortgage,among a host of others. New Century was one of the largest subprimelenders in the boom times. It grew from only $357 million in loanoriginations in 1996 to over $56 billion in 2005. New Century Financial

Corporation listed liabilities of more than $100 million. On May 25, 2007,they filed their form 8-K, a day after stating that they “…probably overstated2005 earnings.” Ya think?On March 26, 2008, an unsealed report by bankruptcy courtexaminer Michael J. Missal outlined a number of “significant improper and

imprudent practices related to its loan originations, operations,accounting and financial reporting processes,” and accusedauditor KPMG with helping the company conceal the problems during 2005and 2006. The full report is strangely missing, but you may click here for apartial report.

7/31/2019 DEADLY CLEAR---WHY DOES'N'T THE JUDGE SEE? MINISTERIAL...REALLY??

http://slidepdf.com/reader/full/deadly-clear-why-doesnt-the-judge-see-ministerialreally 2/11

On December 7, 2009, Federal regulators suedthree former officers of New Century Financial Corp., accusing them of misleading the company’s investors about the company’s prospects, aspervasive bad acts in the mortgage industry began to become widely known.On July 31, 2010, the Los Angeles Times reported that settlements had beenreached between the SEC, plaintiffs representing a class of investors, anddirectors and officers of New Century. The SEC settlement, which involved

an action brought by the SEC against three officers of New Century, barred

those three officers from serving as directors of publiccompanies for five years, and levied fines and profit-disgorgement onthe 3 officers. The corporate officers involved in the SEC matter were PattiM. Dodge, Brad Morrice and David N. Kenneally.Here we are five years later and New Century bad acts are still proliferating

the country. Thousands (if not millions) of loans that were allegedly sold(years ago) by New Century before its bankruptcy are surfacing in staterecordation offices… several years after the debtor’s (New Century)bankruptcy was filed alleging to assign mortgages directly from New

Century Mortgage to trusts that have been closed for several years.Homeowners have been unknowingly foreclosed upon with what astute andintellectual judges and U.S. Senators have deemed to be fraudulentdocuments. The chain of title in these cases is of course a mess.

7/31/2019 DEADLY CLEAR---WHY DOES'N'T THE JUDGE SEE? MINISTERIAL...REALLY??

http://slidepdf.com/reader/full/deadly-clear-why-doesnt-the-judge-see-ministerialreally 3/11

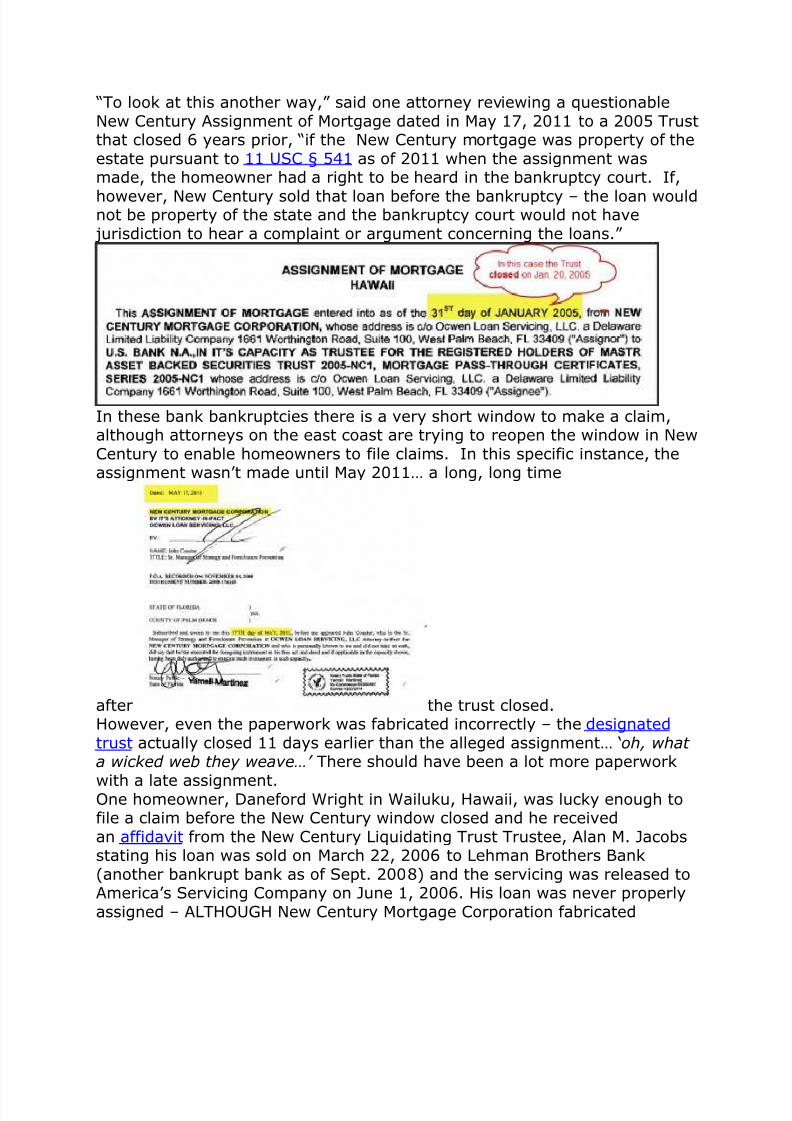

“To look at this another way,” said one attorney reviewing a questionableNew Century Assignment of Mortgage dated in May 17, 2011 to a 2005 Trustthat closed 6 years prior, “if the New Century mortgage was property of theestate pursuant to 11 USC § 541 as of 2011 when the assignment wasmade, the homeowner had a right to be heard in the bankruptcy court. If,

however, New Century sold that loan before the bankruptcy – the loan wouldnot be property of the state and the bankruptcy court would not have jurisdiction to hear a complaint or argument concerning the loans.”

In these bank bankruptcies there is a very short window to make a claim,although attorneys on the east coast are trying to reopen the window in NewCentury to enable homeowners to file claims. In this specific instance, theassignment wasn’t made until May 2011… a long, long time

after the trust closed.However, even the paperwork was fabricated incorrectly – the designatedtrust actually closed 11 days earlier than the alleged assignment… ‘oh, what a wicked web they weave…’ There should have been a lot more paperwork

with a late assignment.One homeowner, Daneford Wright in Wailuku, Hawaii, was lucky enough tofile a claim before the New Century window closed and he receivedan affidavit from the New Century Liquidating Trust Trustee, Alan M. Jacobsstating his loan was sold on March 22, 2006 to Lehman Brothers Bank(another bankrupt bank as of Sept. 2008) and the servicing was released toAmerica’s Servicing Company on June 1, 2006. His loan was never properlyassigned – ALTHOUGH New Century Mortgage Corporation fabricated

7/31/2019 DEADLY CLEAR---WHY DOES'N'T THE JUDGE SEE? MINISTERIAL...REALLY??

http://slidepdf.com/reader/full/deadly-clear-why-doesnt-the-judge-see-ministerialreally 4/11

an assignment of mortgage to US Bank National as Trustee for SASCO 2006-NC1.It is seriously not clear how much the judiciary understands about thisshadow banking and bank fraud, but it is obvious with everyday they get alittle bit clearer picture of the enormous amount of damage it has caused.

Early in the New Century bankruptcy a group of banks motioned JudgeCarey in June 2008 to allow them to clean-up what appeared to be aministerial process relating the debtor’s interest in the mortgage loans.The group of banks, of course were the normal cartel players Credit SuisseFirst Boston, Deutsche Bank, Wells Fargo, Fidelity Nat’l, Ocwen, Saxon, Bankof America…etc.

The banks told Judge Carey: ”As part of their business, theDebtors would typically sell the newly-originated mortgage loans to wholeloan purchasers or assign them to securitization trusts. Frequently when theloans were originated, the mortgages were recorded in the name of theDebtor that originated the loan and thereafter an assignment of themortgage would have been recorded in the name of the assignee. However,in instances where a mortgage loan was repurchased by the Debtors due to,for example, an early payment default by a borrower or a breach of arepresentation or warranty by the Debtor in connection with the sale of the

loan to a third party, the mortgage may remain in the Debtor’s name until itis resold” [see paragraph 7 of the motion].Now, if that were true - why would assignments to trusts from thedebtor, years AFTER the trust had closed, be necessary? Let’s go back to the November 16, 2010 Congressional Oversight Panel’s(COP) report titled “Examining the Consequences of Mortgage

Irregularities for Financial Stability and Foreclosure Mitigation” stated as well as the PSA and New York trust law.

Senator Ted Kaufman warned that the COPinvestigation found evidence that he stated as the worse case scenario,

7/31/2019 DEADLY CLEAR---WHY DOES'N'T THE JUDGE SEE? MINISTERIAL...REALLY??

http://slidepdf.com/reader/full/deadly-clear-why-doesnt-the-judge-see-ministerialreally 5/11

“considerably grimmer” where “robo-signers served to conceal the factthe banks cannot prove that they own the mortgage loans that theyclaim to own.” “[I]n order to convey good title into the trust and provide the trust with bothgood title to the collateral and the income from the mortgages, each transfer

in this process required particular steps. Most PSAs [pooling and servicingagreements] are governed by New York law and create trusts governed byNew York law. New York trust law requires strict compliance with the trustdocuments; any transaction by the trust that is in contravention of the trustdocuments is void, meaning that the transfer cannot actually take place as amatter of law. Therefore, if the transfer for the notes and mortgages

did not comply with the PSA, the transfer would be void, and theassets would not have been transferred to the trust. Moreover, inmany cases the assets could not now be transferred to the trust. PSAsgenerally require that the loans transferred to the trust not be in default,which would prevent the transfer of any non-performing loans to the trustnow. Furthermore, PSAs frequently have timeliness requirementsregarding the transfer in order to ensure that the trusts qualify for

favored tax treatment.” The COP report was concluded AFTER the banks had snowed the New

Century Mortgage bankruptcy court – butnevertheless, late assignments would be void, and the assets would nothave been transferred to the trust. Once the report was published it isaxiomatic that the U.S. Senate expected the courts to ‘do the rightthing.’

Furthermore, as in the Daneford Wright case – the loan had been sold in2006. It was no longer property of the debtor’s estate and therefore outsideof the bankruptcy court’s jurisdiction pursuant to §541, so no matter whatthe banks “thought” they could sneak by the Judge – it appears it wouldn’tbe applicable to Assignments of Mortgage.In every Assignment of Mortgage case, the trust PSA dictates that theassignments, transfers and sale to the trust must be made by the

7/31/2019 DEADLY CLEAR---WHY DOES'N'T THE JUDGE SEE? MINISTERIAL...REALLY??

http://slidepdf.com/reader/full/deadly-clear-why-doesnt-the-judge-see-ministerialreally 6/11

Depositor… not the originator (New Century). Some attorneys think thatbecause these bogus assignments were made in the name of New Centurythat it may well open the door for homeowners to petition the bankruptcycourt for relief and, of course there may well be more than an appearance of fraud…’cause why were these mortgage documents not assigned to

the trusts before the trusts closed?

And that sixty-four thousand dollarquestion, it appears, may well open up the gateway to the great casino of shadow banking and possible off-shore money laundering schemes.It’s not hard to understand how judges can be snowed in these cases.The banks in New Century made questionable statements in their motion toJudge Carey like, ”[I]n addition, with respect to the mortgage loans being

serviced by New Century Mortgage Corporation (“NCMC”), the mortgageswould frequently be listed in the name of NCMC or an affiliate, even though

the owner of the economic interest in the loan would be the securitization

trust or whole loan buyer. In those instances, NCMC would only hold barelegal title to these mortgages” [see paragraph 8 of the motion]. Oh pleeeze! In mortgage lien states, like Hawaii for example, it “is to bedeemed a mortgage and shall create a lien only as security for the obligationand shall not be deemed to pass title” [HRS §506-1]. But aside fromthat, servicers are merely debt collectors and if they hold interest in themortgages – it would have to be a piece of the securities… and then are wetalking about a non-negotiable instrument? And at that point, if there is afinancial back-end deal – doesn’t it belongs to the creditors (of which thehomeowners should have a right to become one of) and aren’t we are backto “property of the estate” and the homeowner’s day in the New Century

bankruptcy court?In any event, it isn’t the servicing rights that are being fraudulently assigned “late” to these trusts. It is the mortgage and the note.Recently, an attorney asked the New Century bankruptcy Trustee (throughthe Trustee’s attorneys) to identify a short list of 5 of his clients and providethe name of the entity that New Century sold the homeowner’s loan to. TheNew Century Liquidating Trust Trustee’s

7/31/2019 DEADLY CLEAR---WHY DOES'N'T THE JUDGE SEE? MINISTERIAL...REALLY??

http://slidepdf.com/reader/full/deadly-clear-why-doesnt-the-judge-see-ministerialreally 7/11

attorneys replied back with a date thatthe servicing rights of these loans were sold.Of course that wasn’t the question that was asked – but what reason wouldthe Trustee have to evade the issue of who the loans were actually soldto? Servicers do not sell, transfer or assign loans to the trusts pursuant tothe trust controlling documents (PSA). So, do these guys assume that

everybody is an idiot until it’s proven otherwise or are they just trying tohide the facts from the Judge and the investors?In the initial motion [discussed earlier] the banks were cognizant of the factthat there would be millions of cases coming into the bankruptcy courtbecause of the failure to properly assign the mortgages, not to mention theinvestors’ lawsuits and adversary proceedings. The banks so nicely couchedit for the Judge and asked him to “blanket order” that there was no need topursue relief from stay – that they could clean up this little ministerial messwithout bothering the court. They just didn’t tell him that, as it appears,they intended to commit fraud – as they fabricated documents and made

late assignments on behalf of the debtor under the guise of a ministerialoversight:

“Additionally, so as to reduce theadministrative burden on the Court and substantial administrativeexpense to the Estates’, the Debtors request that the Court (i) order anyparty seeking to foreclose upon a mortgage lien recorded against realproperty in which a Debtor is listed as the holder of the mortgage not to filea motion for relief from stay relating thereto nor to serve any documents

7/31/2019 DEADLY CLEAR---WHY DOES'N'T THE JUDGE SEE? MINISTERIAL...REALLY??

http://slidepdf.com/reader/full/deadly-clear-why-doesnt-the-judge-see-ministerialreally 8/11

related thereto upon the Debtors, the Committee, the LiquidatingTrustee/Plan Administrator or their respective counsel and (ii) authorize suchprofessionals to dispose of and discard all such foreclosure pleadings servedupon them prior to or following entry of the order granting this Motion” [seeparagraph 12 of the motion]. Of course we’re doing this for you, judge….

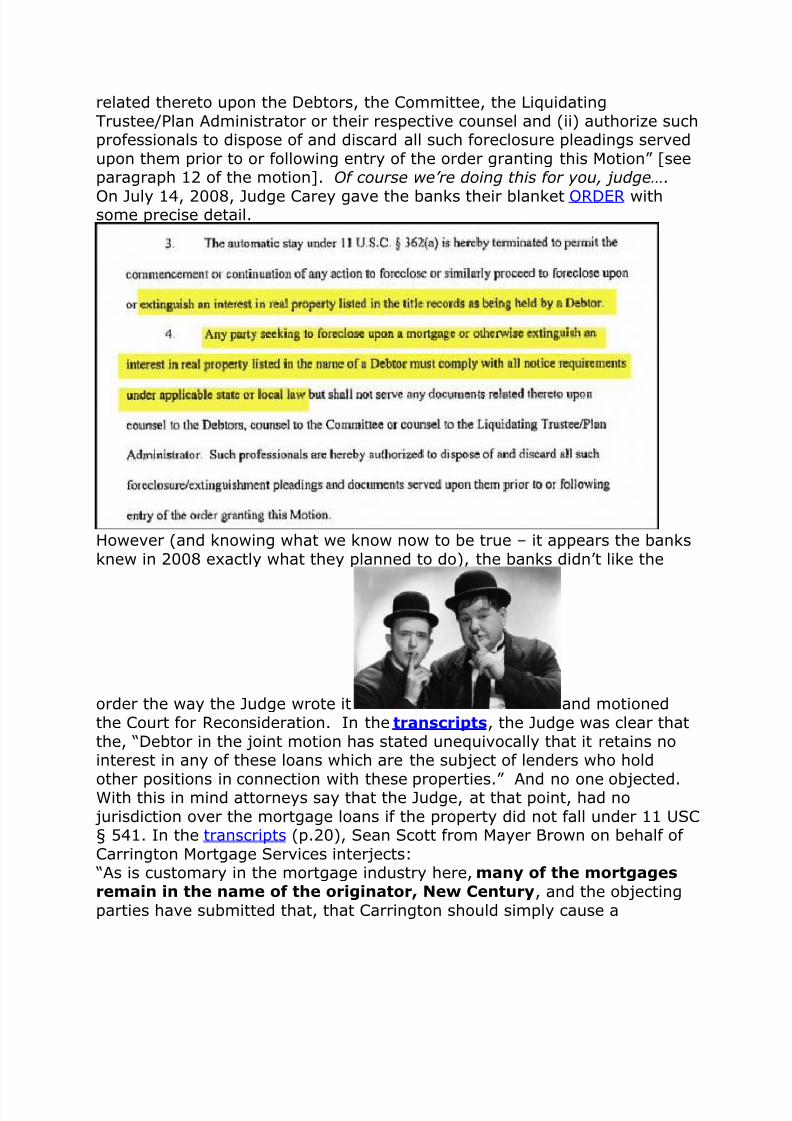

On July 14, 2008, Judge Carey gave the banks their blanket ORDER withsome precise detail.

However (and knowing what we know now to be true – it appears the banksknew in 2008 exactly what they planned to do), the banks didn’t like the

order the way the Judge wrote it and motionedthe Court for Reconsideration. In the transcripts, the Judge was clear thatthe, “Debtor in the joint motion has stated unequivocally that it retains nointerest in any of these loans which are the subject of lenders who hold

other positions in connection with these properties.” And no one objected.With this in mind attorneys say that the Judge, at that point, had no jurisdiction over the mortgage loans if the property did not fall under 11 USC§ 541. In the transcripts (p.20), Sean Scott from Mayer Brown on behalf of Carrington Mortgage Services interjects: “As is customary in the mortgage industry here, many of the mortgages

remain in the name of the originator, New Century, and the objectingparties have submitted that, that Carrington should simply cause a

7/31/2019 DEADLY CLEAR---WHY DOES'N'T THE JUDGE SEE? MINISTERIAL...REALLY??

http://slidepdf.com/reader/full/deadly-clear-why-doesnt-the-judge-see-ministerialreally 9/11

recordation of the assignments of those mortgages. That wouldimpose significant costs not on Carrington Mortgage Services, because it issimply the servicer here, but in fact our reading of the documents is thatthe cost of that recordation would fall back upon the estate, and thenin particular on New Century Capital Corporation, which is the

responsible party in the applicable pooling and servicing agreements.”

Hogwash. It appears Mr. Scott wasbanking on the fact that the Judge would not be familiar with the Poolingand Servicing Agreements – or maybe Mr. Scott wasn’t thoroughlyversed. But the truth is in the documents.Section 2.01 Conveyance in nearly all trusts defines responsibility of the “players,” for example, it clarifies that the “Trustee shall promptly (withinsixty Business Days following the later of the Closing Date and the date of

receipt by the Trustee or the Custodian of the recording information for aMortgage, but in no event later than ninety days following the ClosingDate) enforce the obligations of NC Capital pursuant to the terms of the Mortgage Loan Purchase Agreement to submit or cause to be

submitted for recording, at no expense to the Trust Fund…” So… it appears maybe the Trustee did not do its job?? Why didn’t theTrustee “enforce” the obligations of NC Capital at the appropriate time whenit first wrote the loans?Don’t you think the investors would want to know that the assets were notlegally transferred into the trust pursuant to the PSA? How about the IRS?

And what about the American public? We’re picking up a horrendously largetax tab for the bailout of the banks – don’t we deserve to know of the REMICs have failed and who actually owes all that tax money thatwas supposed to be sheltered? The borrowers certainly want to know wherethe collateral is and who they owe – if they owe anything at all. But let’s getback to the investors. This “blanket order” idea appeared to be a greatstrategy and “not have to alert the investors to the fact that the loans neverwere properly assigned…”

7/31/2019 DEADLY CLEAR---WHY DOES'N'T THE JUDGE SEE? MINISTERIAL...REALLY??

http://slidepdf.com/reader/full/deadly-clear-why-doesnt-the-judge-see-ministerialreally 10/11

It’s just difficult to believe that a judge would sweep such a big issue under

the rug if he knew. The investors have

a right to know – and it’s probably actionable from their prospective. Theborrowers have a right to challenge a faulty assignment (see Deutsche Bank v. Williams); and as far as saving the estate money – doesn’t the bankruptcy judge have super powers under 11 USC § 105?Nobody brought up the fact that the securitized trust Trustees wereresponsible and apparently remiss because the Trustees, under thePSA SECTION 2.02. Acceptance of REMIC I by Trustee, are supposed to “acknowledge receipt” of the loan documents and that everything is in orderpursuant to Section 2.01 [Source: MASTR Asset Backed Securities Trust2005-NC1]. Well, that apparently didn’t happen either. The Judge couldhave ordered the Trustees liable for the recordation costs or any of the

parties that were responsible for the documents including the servicers andthe custodians… and if the investors knew that there were no loans assignedto the trusts – well, now that’s a whole other issue…and the Judge’s ownpension plan might likely be affected.Judge Carey signed another Order on September 3, 2008 that left out muchof the original detail, however he penned a couple very important points tothis “servicing rights” related order:

7/31/2019 DEADLY CLEAR---WHY DOES'N'T THE JUDGE SEE? MINISTERIAL...REALLY??

http://slidepdf.com/reader/full/deadly-clear-why-doesnt-the-judge-see-ministerialreally 11/11

The fact is there were loans, likely millions of loans, that were neverassigned to the trusts… And certainly, Mr. Scott’s client Carrington Mortgagedoes not want to alert the investors to the fact that assignments were notmade and it’s likely nobody wants to start discussing “why” theseassignments were not made on time or what New Century and other banks

may have been doing with these mortgages in the meantime because thatmight mean deeper discussions into shadow banking.Or maybe the investors (at least their agents) knew that the assignmentswere not going to be made because these loans were bad to begin with sowhy assign them when they’d likely default in a couple of years anyway – just a waste of paperwork, time and expense…??? And if that’s the case –their goes their lawsuits … flush – swish!

It’s unlikely in 2008 that Honorable Kevin J. Careyhad figured out the depth of the fraud or the securitization and shadow

banking scheme. Was he lied to?? Well, that’s for the a judge or jury todecide, but one thing is for sure – if the loans were sold – it would be best tocome clean and determine exactly who purchased the loans and what theydid with them and why… because they were never assigned to the trusts ontime.As Senator Ted Kaufman warned and COP (who did a thorough andcomplete investigation - listen up!) has clearly indicated: “if the transferfor the notes and mortgages did not comply with the PSA, the

transfer would be void, and the assets would not have beentransferred to the trust. ...

FOR MORE DEADLY CLEAR GO HERE:

http://deadlyclear.wordpress.com/