Embed Size (px)

Citation preview

Deacons Financial Services Client Seminar 2014General SFC Licensing and Compliance UpdateJane McBride, Partner & Head of Financial Services Licensing, Compliance and Regulatory 1:00 pm – 2:00 pm, Monday, 10 November 2014

These materials are for general guidance only and should not be relied upon as, or treated as a substitute for, specific advice. Deacons accepts no responsibility for any loss which may arise from reliance on any of the information contained in these materials. If you would like advice on any of the issues raised, please contact us.

Disclaimer

© Deacons 2014 1

Today’s topics

1. New SFC approach to compliance?

2. Professional Investor Regime

3. Disclosure in SFC Applications

4. On-going SFC Notifications

5. SFC Annual Report

6. Enforcement by SFC

© Deacons 2014 2

1. New SFC approach to compliance?

SFC Supervisory briefing session (September 2014)• Corporate culture

Top down / Senior management approach – General Principle 9 of the Code of Conduct

No surprises culture – communication with the SFC• Inspections

Electronic trading controls, AML and supervision• Enforcement

Top down approach Equal liability on both the firm and individuals Sanctions rather than solutions

© Deacons 2014 3

1. New SFC approach to compliance?

“Supervision of intermediaries: key initiatives and focus in 2014” by James Shipton (Executive Director of Intermediaries)

Culture• “Importantly, what is clear is that regulators around the world are now

emphasising that culture is an important subject for regulators to focus on when supervising firms.”

• “When we speak of conduct, behaviour and processes at firms we have to take a step back and remember that all these things originate from decisions of individuals within firms and from decision-making processes by those firms.”

• “General Principles 1 and 2 requires licensees, both individual and corporate, to ‘act honestly, fairly and in the best interests of its clients and the integrity of the market’.”

© Deacons 2014 4

1. New SFC approach to compliance?

Regulatory Inspections

• “This drives home the need for a more ‘judgment-based’ and ‘forward-looking’ approach to supervision. To do this, we will examine the ‘root causes’ of decision-making, conduct and behaviour at firms – that is, looking beyond the mere existence of a compliance or control framework to see if it has a supporting culture. It also means that the SFC are adopting, as our own strategy, an outcomes-oriented and inquisitive approach.”

© Deacons 2014 5

1. New SFC approach to compliance?

Regulatory Inspections• “This judgment-based and outcomes-oriented supervisory approach also

means that we will be looking at the ‘sum of the parts’ and ‘joining the dots’when we supervise firms. In other words we will not look narrowly at particular instances or incidents, whether in Hong Kong or abroad. Instead we will look to see what such incidents say about a firm's control environment and culture and how it reflects on its decisions and decision-making processes.”

• “This means, going forward, we will be taking an interest in: (i) how incentives and disincentives impact decisions and conduct within

firms; (ii) the leadership and decision-making structures of firms; and (iii) the corporate values and professionalism of firms – in other words –

their organisational culture.”

© Deacons 2014 6

1. New SFC approach to compliance?

Senior management responsibility• “This means that the entire management structure has to take real

responsibility for regulatory matters and avoid overly delegating responsibility to compliance or other control functions.”

• “In my experience it is the senior vice presidents and junior managing directors who are responsible for teams that are the crucial conduits in this regard. So it is important that these people in authority have the right professionalism, values and supporting culture.”

© Deacons 2014 7

2. Professional Investor Regime -Product Disclosure and Conduct Regulations Overview

Two pillars

• Product disclosure

• Conduct Regulation (including Suitability Obligations)

Conduct regulation is relevant to all intermediaries to all regulated services they provide regardless of whether the offering documents are exempted from SFC authorization

© Deacons 2014 8

2. Professional Investor Regime -Product Disclosure

The first pillar

Companies (Winding Up and Miscellaneous Provisions) Ordinance (CO) - shares & debentures (prospectus regime)CO and SFO

not subject to authorised product regulatory standards

Private placement to PIs under either prospectus (CO) or as offer of investment (SFO)

SFO, SFC Handbook - funds & structured products (offer of investment regime)

Regulatory standardsPublic

SourceOffering documentOffering

© Deacons 2014 9

2. Professional Investor Regime -Conduct Regulation (Suitability Obligations)

The second pillar – key conduct requirements

• General Principle (GP)1 – Honesty and fairness

• GP 2 – Diligence

• GP 5 – Information for clients

e.g. disclosure before point of sale in terms of sales related information

e.g. disclosure after sale in terms of reporting statements under the Contract Notes Rules

• Know your Client (KYC) process

• Suitability Obligations – 5.2© Deacons 2014 10

2. Professional Investor Regime –Category A PI

Category A PI

• Regulated financial institution (e.g. bank, licensed corporation, investment service provider)

• Regulated insurance company

• Recognized exchange company

• Fund

• Mandatory Provident Fund

• Occupational Retirement Scheme

• Government (e.g. HKSAR Government)

© Deacons 2014 11

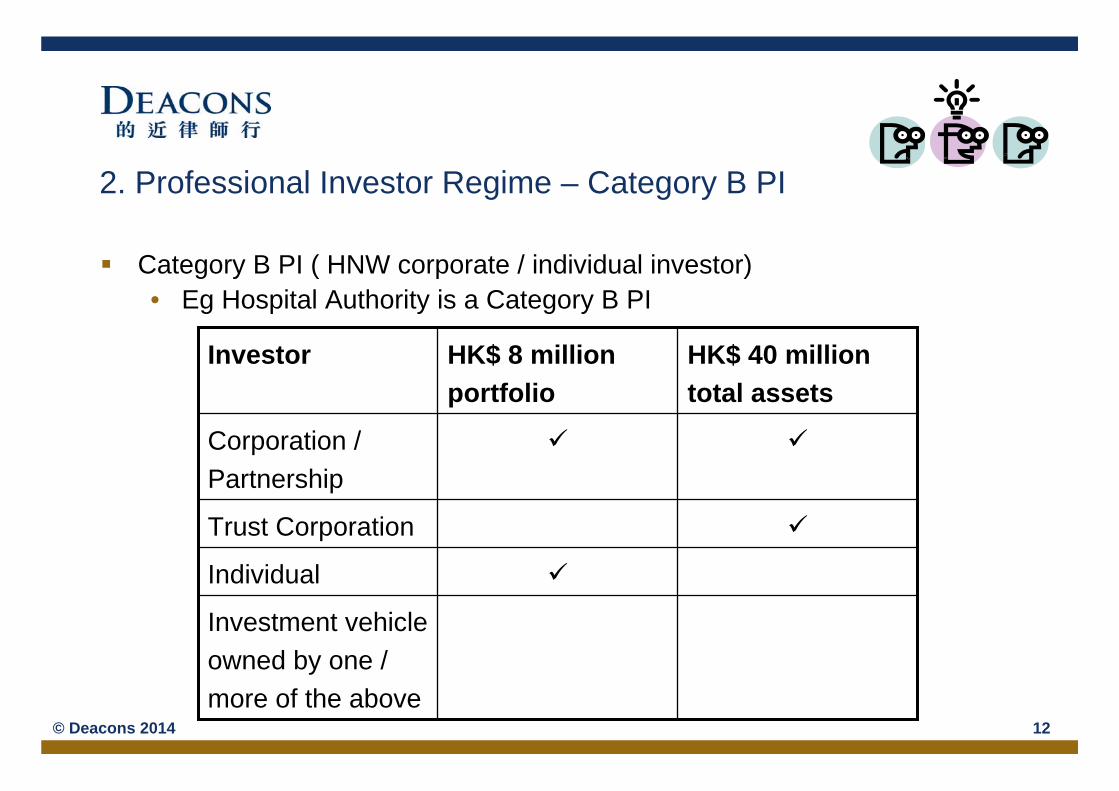

2. Professional Investor Regime – Category B PI

Category B PI ( HNW corporate / individual investor)• Eg Hospital Authority is a Category B PI

Investment vehicle owned by one / more of the above

Individual

Trust Corporation

Corporation / Partnership

HK$ 40 million total assets

HK$ 8 million portfolio

Investor

© Deacons 2014 12

2. Professional Investor Regime – Conduct Regulation Establishment of PI “status”

• Both Categories A and B PI status need to (i) be verified and (ii) keep evidence on file (one of the deficiencies in the thematic inspection report)

“Treatment”

• Category A PIs – automatic waiver – no knowledge / experience assessment or (ii) consent / declaration required

• Category B PIs – optional to go through the two-tier waiver process

• Go through the process?

Option 1 - No comply with all investor protection provisions

Option 2 - Yes waive most of the investor protection provisions

• See steps in next slide© Deacons 2014 13

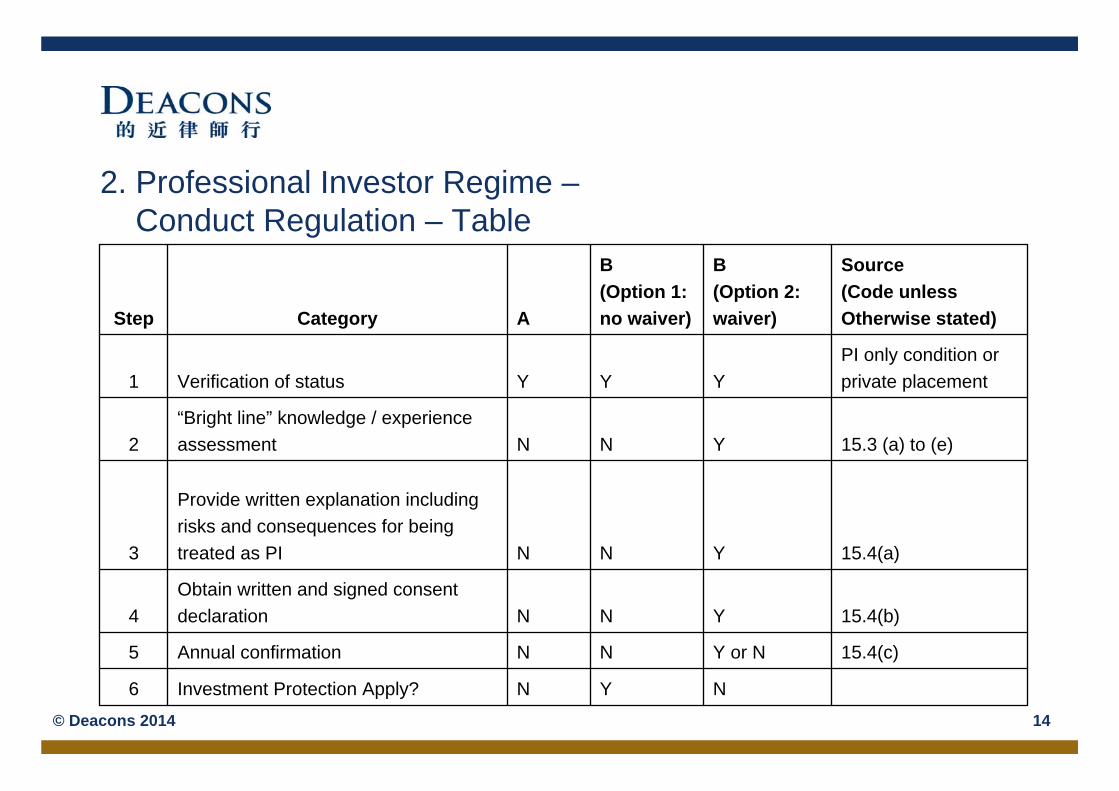

2. Professional Investor Regime –Conduct Regulation – Table

15.4(c)Y or NNNAnnual confirmation5

NYNInvestment Protection Apply?6

15.4(b)YNNObtain written and signed consent declaration4

15.4(a)YNN

Provide written explanation including risks and consequences for being treated as PI3

15.3 (a) to (e)YNN“Bright line” knowledge / experience assessment2

PI only condition orprivate placementYYYVerification of status1

Source(Code unlessOtherwise stated)

B (Option 2: waiver)

B (Option 1: no waiver)ACategoryStep

© Deacons 2014 14

2. Professional Investor Regime -Investor Protection Provisions which can be waived

Code of Conduct (Code) requirements• Know your client circumstances - 5.1(a)• Investor characterization of derivative knowledge – 5.1A• Suitability obligation – 5.2 • For discretionary accounts, obtaining written authority before effecting

transactions for clients and annual confirmation – 5.4• Confirm promptly with client transaction features after effecting each

transaction for client – 8.2• Inform client about the licensed corporation – 8.1• Disclosure certain benefits including sales related information – 8.3A• Written client agreement – 6

© Deacons 2014 15

2. Professional Investor Regime -Investor Protection Provisions which cannot be waived

KYC• Verify the true identity of client - 5.1(a)

• Derivative products - assure oneself client understand risks and has sufficient net worth to assume the risks and bear the potential loss -5.3

Information for client• Financial information of the licensed corporation if requested by client - 8.4

• Corporate actions in relation to client assets, only applicable if hold client assets - 8.5

© Deacons 2014 16

2. Professional Investor Regime -PI Consultation Conclusions

Conclusions (finally) published on 25 September 2014

• Conclusions on amendments to the PI regime

• Further Consultation on the client agreement requirements

paragraph 15 of the Code of Conduct will be replaced in full

paragraphs 5.1A and 8.3A of the Code of Conduct will be amended.

Effective on 25 March 2016

© Deacons 2014 17

2. Professional Investor Regime -PI Consultation Conclusions

Purpose – better protect PIs who are:• Corporate;• Individuals; and• Investment vehicles wholly owned by individuals / family trusts

(Family Offices) Individual Professional Investors

Comply with 15.3B (i.e. full explanation of consequences, signing declaration on consent and carry out confirmation annually) for semi exemptions (15.5 – information for clients), exempting the need to:

i. inform clients re info of the licensed personii. confirm essential features of transactioniii. document on Nasdaq-Amex Pilot Program

Other investor protection provisions including suitability obligations will need to be fully complied with

© Deacons 2014 18

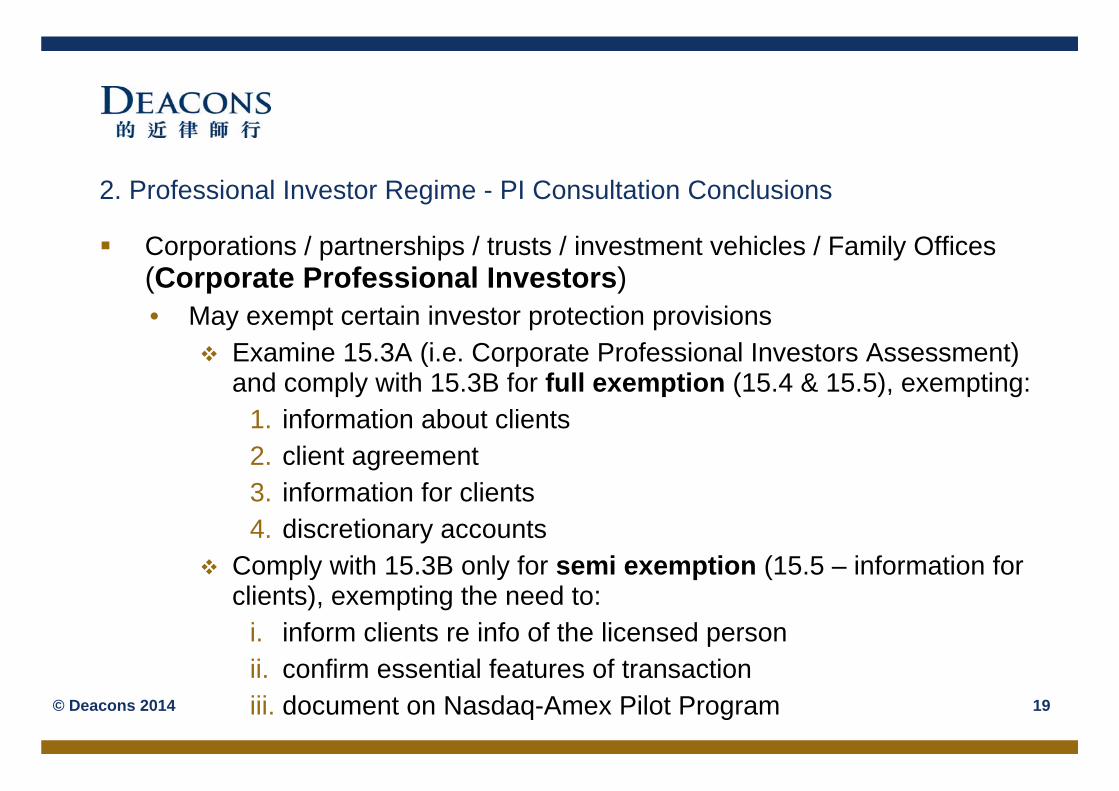

2. Professional Investor Regime - PI Consultation Conclusions

Corporations / partnerships / trusts / investment vehicles / Family Offices (Corporate Professional Investors)• May exempt certain investor protection provisions

Examine 15.3A (i.e. Corporate Professional Investors Assessment)and comply with 15.3B for full exemption (15.4 & 15.5), exempting:

1. information about clients2. client agreement3. information for clients 4. discretionary accounts

Comply with 15.3B only for semi exemption (15.5 – information for clients), exempting the need to:

i. inform clients re info of the licensed personii. confirm essential features of transactioniii. document on Nasdaq-Amex Pilot Program© Deacons 2014 19

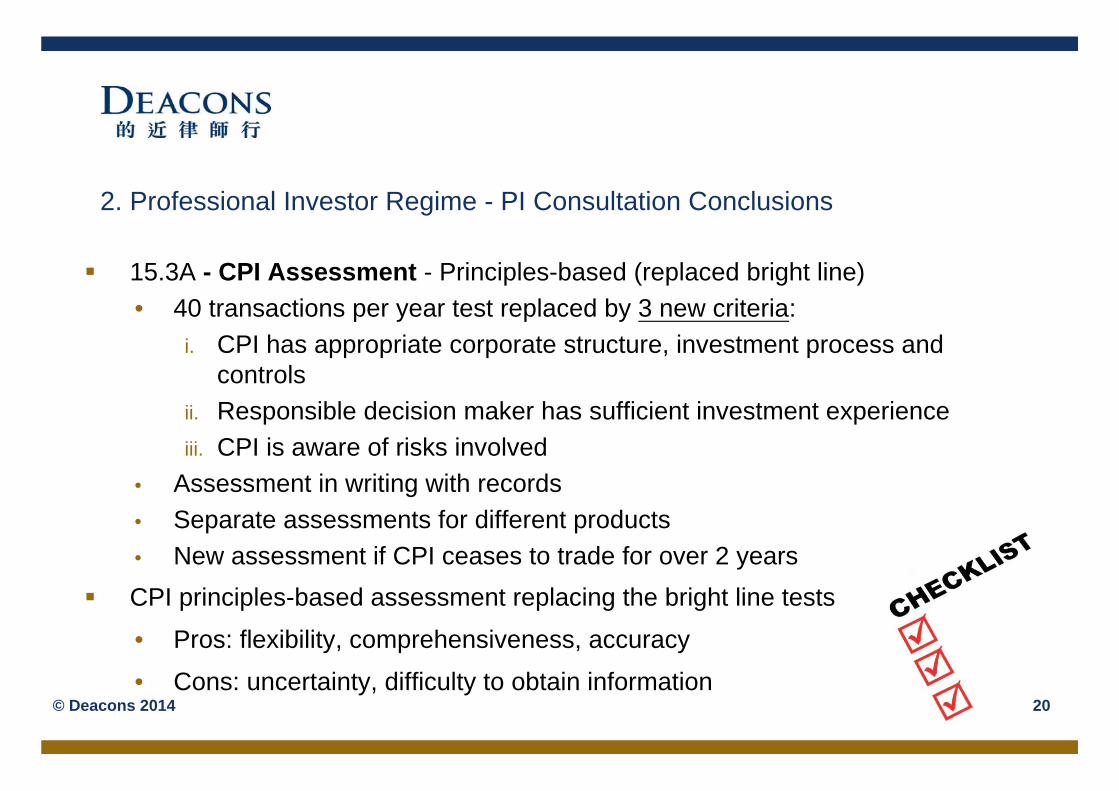

2. Professional Investor Regime - PI Consultation Conclusions

15.3A - CPI Assessment - Principles-based (replaced bright line) • 40 transactions per year test replaced by 3 new criteria:

i. CPI has appropriate corporate structure, investment process and controls

ii. Responsible decision maker has sufficient investment experienceiii. CPI is aware of risks involved

• Assessment in writing with records• Separate assessments for different products• New assessment if CPI ceases to trade for over 2 years

CPI principles-based assessment replacing the bright line tests

• Pros: flexibility, comprehensiveness, accuracy

• Cons: uncertainty, difficulty to obtain information© Deacons 2014 20

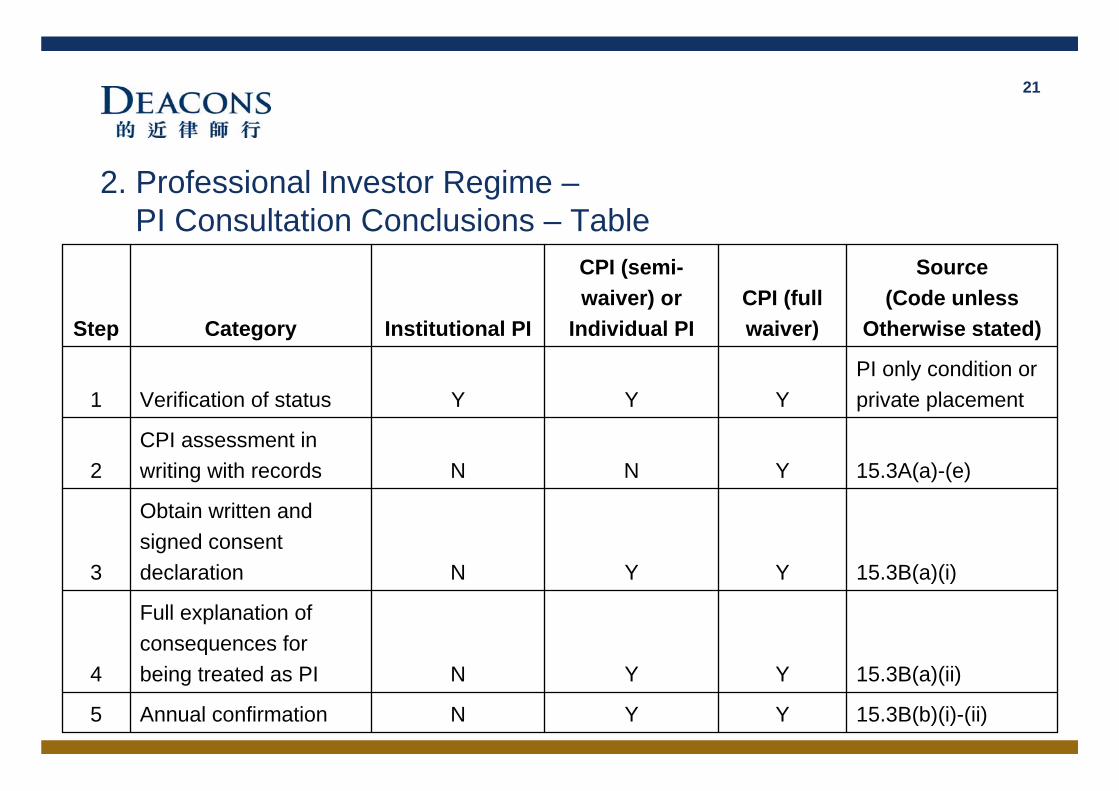

2. Professional Investor Regime –PI Consultation Conclusions – Table

Source(Code unless

Otherwise stated)CPI (full waiver)

CPI (semi-waiver) or

Individual PIInstitutional PICategoryStep

15.3B(a)(i)YYN

Obtain written and signed consent declaration3

15.3B(b)(i)-(ii)YYNAnnual confirmation5

15.3B(a)(ii)YYN

Full explanation of consequences for being treated as PI4

15.3A(a)-(e)YNNCPI assessment in writing with records2

PI only condition orprivate placementYYYVerification of status1

21

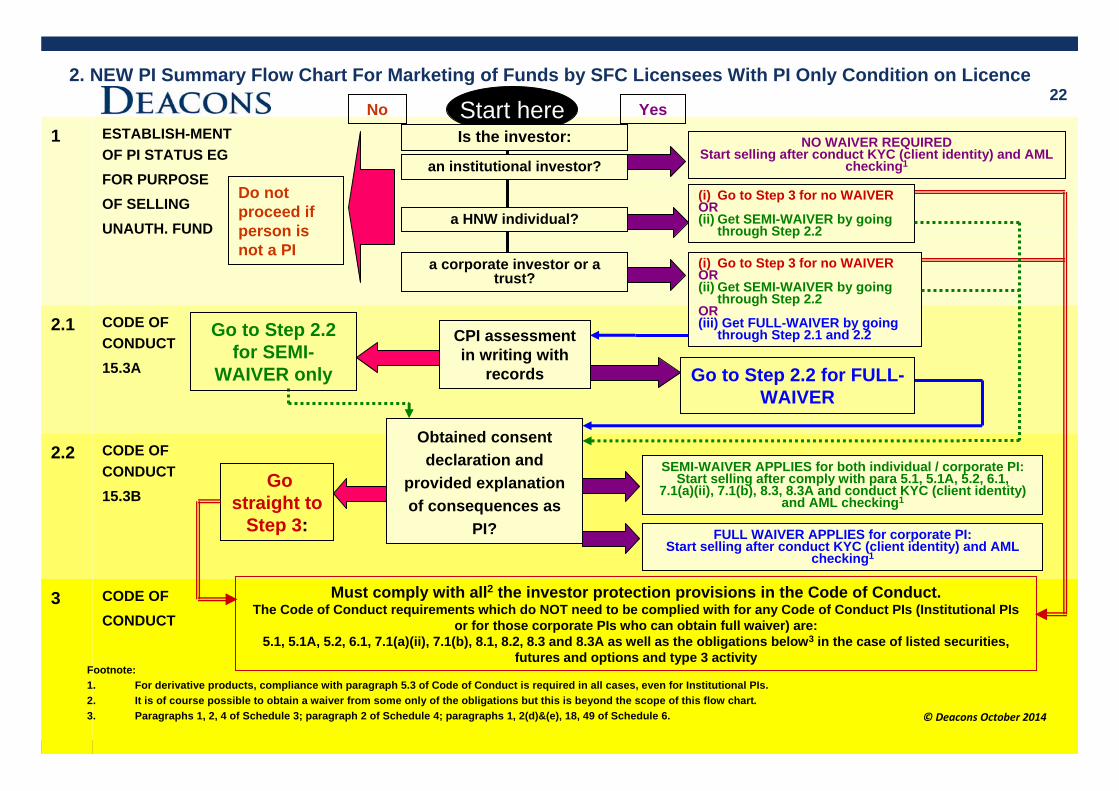

2. NEW PI Summary Flow Chart For Marketing of Funds by SFC Licensees With PI Only Condition on Licence

CODE OF CONDUCT 15.3B

2.2

CODE OF CONDUCT

3

CODE OF CONDUCT 15.3A

2.1

ESTABLISH-MENT OF PI STATUS EGFOR PURPOSE OF SELLINGUNAUTH. FUND

1Start here

Go straight to

Step 3:

NO WAIVER REQUIREDStart selling after conduct KYC (client identity) and AML

checking1

FULL WAIVER APPLIES for corporate PI:Start selling after conduct KYC (client identity) and AML

checking1

Must comply with all2 the investor protection provisions in the Code of Conduct.The Code of Conduct requirements which do NOT need to be complied with for any Code of Conduct PIs (Institutional PIs

or for those corporate PIs who can obtain full waiver) are: 5.1, 5.1A, 5.2, 6.1, 7.1(a)(ii), 7.1(b), 8.1, 8.2, 8.3 and 8.3A as well as the obligations below3 in the case of listed securities,

futures and options and type 3 activity

Obtained consent declaration and

provided explanation of consequences as

PI?

CPI assessment in writing with

records

an institutional investor?

a corporate investor or a trust?

a HNW individual?

No Yes

Footnote:1. For derivative products, compliance with paragraph 5.3 of Code of Conduct is required in all cases, even for Institutional PIs.2. It is of course possible to obtain a waiver from some only of the obligations but this is beyond the scope of this flow chart.3. Paragraphs 1, 2, 4 of Schedule 3; paragraph 2 of Schedule 4; paragraphs 1, 2(d)&(e), 18, 49 of Schedule 6.

Do not proceed if person is not a PI

Go to Step 2.2 for SEMI-

WAIVER only

©Deacons October 2014

Is the investor:

(i) Go to Step 3 for no WAIVEROR (ii) Get SEMI-WAIVER by going

through Step 2.2

SEMI-WAIVER APPLIES for both individual / corporate PI:Start selling after comply with para 5.1, 5.1A, 5.2, 6.1,

7.1(a)(ii), 7.1(b), 8.3, 8.3A and conduct KYC (client identity) and AML checking1

(i) Go to Step 3 for no WAIVEROR (ii) Get SEMI-WAIVER by going

through Step 2.2OR(iii) Get FULL-WAIVER by going

through Step 2.1 and 2.2

Go to Step 2.2 for FULL-WAIVER

22

2. Professional Investor Regime -PI Consultation Conclusions – Client Agreements

Client agreement requirements in 2013 consultation• Suitability requirements should be included in the client agreements as contractual terms

• Client agreements should not contain terms which are inconsistent with the Code

• Client agreements should clearly set out in clear terms the actual services to be provided to client

Revised paragraph 6 in 2014 consultation• The SFC is now proposing that a new clause on suitability and non-derogation be inserted in

client agreements: “If we [the intermediary] solicit the sale of or recommend any financial product to you [the client], the

financial product must be reasonably suitable for you having regard to your financial situation, investment experience and investment objectives. No other provision of this agreement or any other document we may ask you to sign and no statement we may ask you to make derogates from this clause.”

• SFC is now seeking comments on the new clause on or before 24 December 2014.

© Deacons 2014 23

2. Professional Investor Regime -PI Consultation Conclusions

Institutional Professional Investors• continue to be automatically entitled to all current automatic Code exemptions

© Deacons 2014 24

2. Professional Investor Regime -PI Consultation Conclusions

No changes to PI Rules or prescribed monetary threshold so no effect on private placements or PI only condition compliance – can still sell private funds to anyone who is PI without getting their consent

© Deacons 2014 25

2. Professional Investor Regime -PI Consultation Conclusions

© Deacons 2014 26

STILL TO COME

• ….. yet further guidance on Suitability

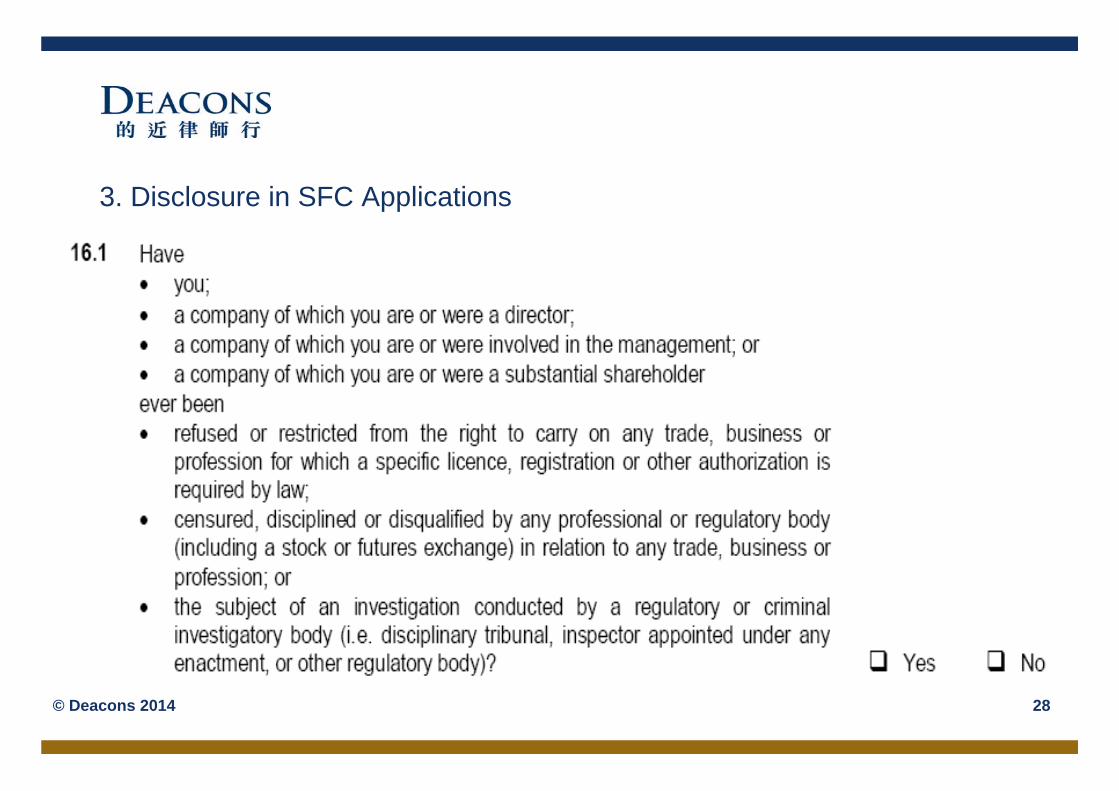

3. Disclosure in SFC Applications Disclosure in SFC applications

• Who needs to make disclosures

Licence applicants (company and individuals) Directors of licence applicant company (executive and NEDs) Substantial shareholders Directors of substantial shareholder (and substantial shareholders of

any corporate directors or equivalent e.g. GPs)• What kind of information needs to be provided?

Basic (e.g. Date of Birth, Contact Details, Academic and Professional Qualifications, Employment History)

vs

Sensitive (e.g. Disciplinary Actions and Investigations, Financial Status, Character, Mental Health)

How broad? © Deacons 2014 27

3. Disclosure in SFC Applications

© Deacons 2014 28

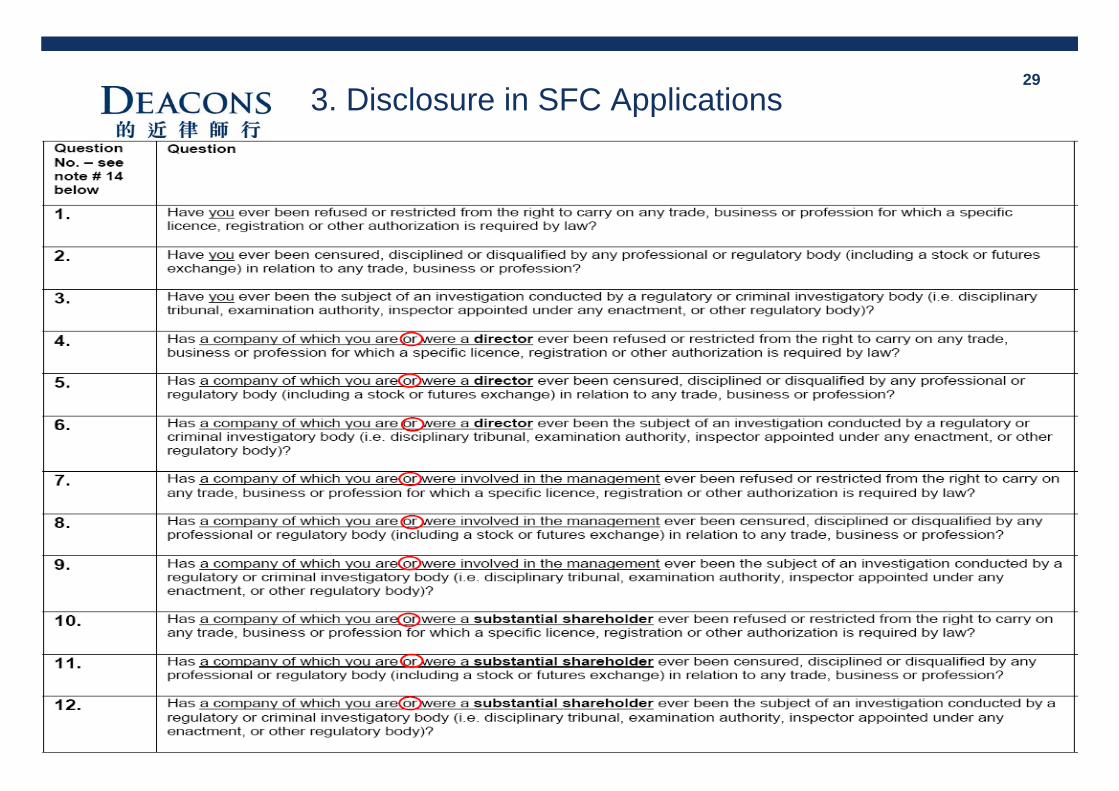

3. Disclosure in SFC Applications29

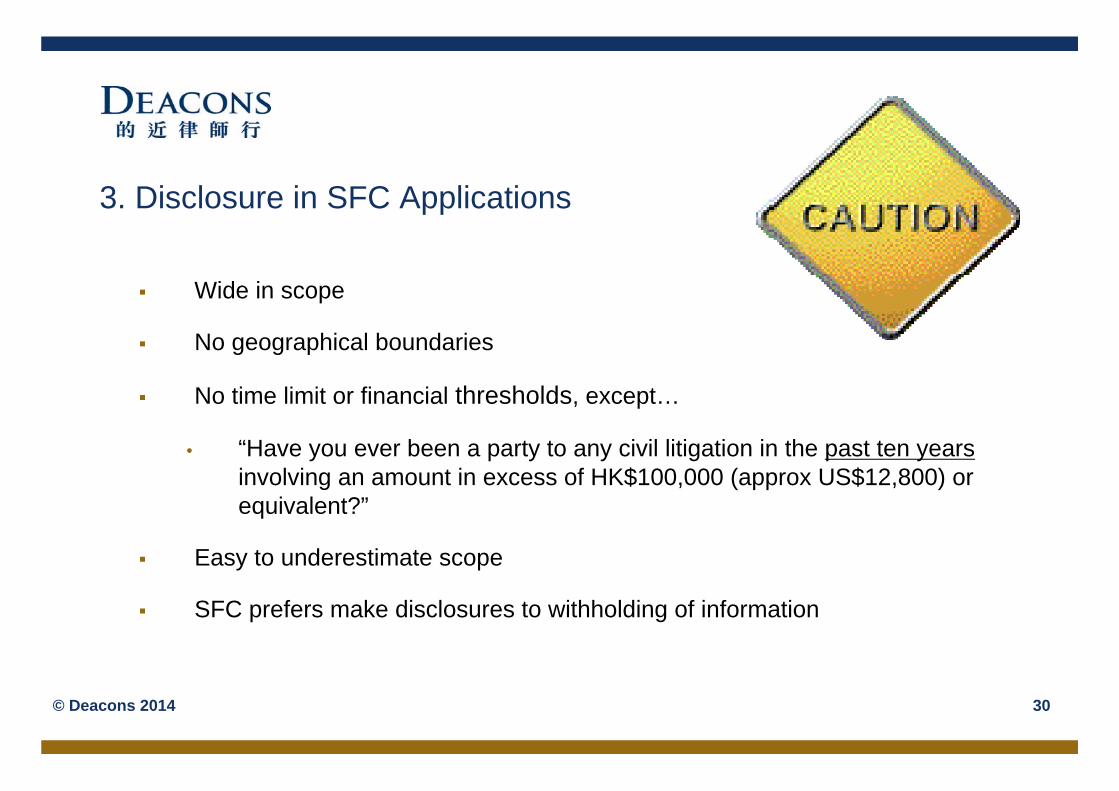

3. Disclosure in SFC Applications

Wide in scope

No geographical boundaries

No time limit or financial thresholds, except…

• “Have you ever been a party to any civil litigation in the past ten yearsinvolving an amount in excess of HK$100,000 (approx US$12,800) or equivalent?”

Easy to underestimate scope

SFC prefers make disclosures to withholding of information

© Deacons 2014 30

4. SFC prior approval required:

Changes to regulated activities Change in substantial shareholders and ROs Change in record keeping premise Publication of marketing materials Change of financial year Licensing of corporations or individuals Accreditation of individuals Variation of type or regulated activity Modifications or waivers

Note: This list is not exhaustive.

© Deacons 2014 31

4. On-going SFC Notifications

Who needs to notify SFC of changes / new incidents?

Usually post notification only is sufficient

Notification deadline - within 7 business days after the change / after the new incident

Prior approval

• new substantial shareholder

• new record keeping address

© Deacons 2014 32

4. On-going SFC Notifications

Trivial

• change in residential address of a licensed individual • change in complaints officer / emergency contact person of licensed

company • change in bank accounts of licensed company

Controversial / Sensitive / Hard

• conviction of / charge with criminal offence • subject to disciplinary action or investigation by regulatory body • judicial proceedings• change in overseas licence / registration status for the licensed individual /

company

© Deacons 2014 33

4. On-going SFC Notifications

5 Common Late Notification Items / Breaches

1. Licensed individual has new passport / residential address 2. Licensed individual has become / resigned as director of another

company (e.g. portfolio company)3. Individual has been appointed to or resigned from board of

company (e.g. portfolio company)4. Shareholding structure of licensed company has changed 5. Substantial shareholder has been subject to disciplinary action or

investigation

••

© Deacons 2014 34

4. On-going SFC Notifications –Penalties

A person who, without reasonable excuse, breaches the notification requirements commits an offence and is liable on conviction to a fine

Also there are criminal penalties for proceeding in certain cases without SFC prior approval

© Deacons 2014 35

5. SFC Annual Report

Highlights of the SFC’s Licensing, Supervision, Enforcement and Investment Products operations :• Over 2,500 Hong Kong and overseas investors compensated in three

enforcement cases

• 296 risk-based inspections of licensed corporations concluded

• Around 2,500 SFC-authorised collective investment schemes on offer to the public

© Deacons 2014 36

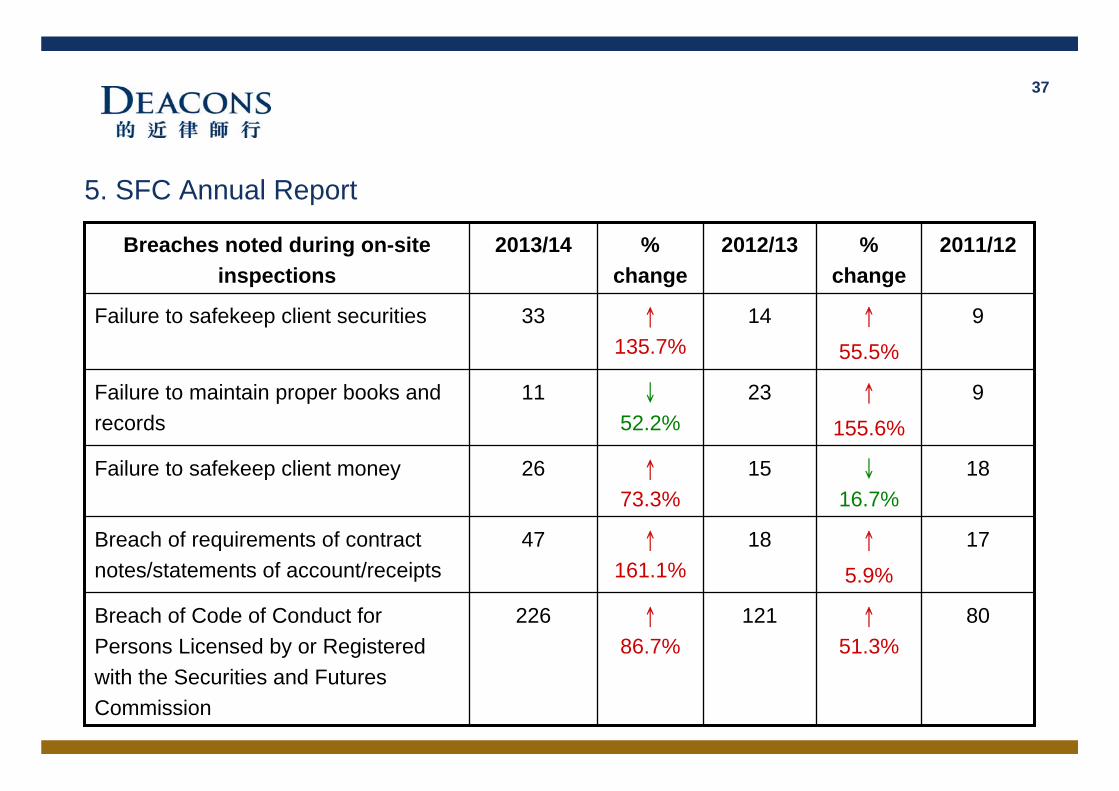

5. SFC Annual Report

80↑

51.3%121↑

86.7%226Breach of Code of Conduct for

Persons Licensed by or Registered with the Securities and Futures Commission

17↑

5.9%

18↑

161.1%47Breach of requirements of contract

notes/statements of account/receipts

18↓

16.7%15↑

73.3%26Failure to safekeep client money

9↑

155.6%

23↓

52.2%11Failure to maintain proper books and

records

9 ↑

55.5%

14 ↑

135.7%33 Failure to safekeep client securities

2011/12 % change

2012/13% change

2013/14Breaches noted during on-site inspections

37

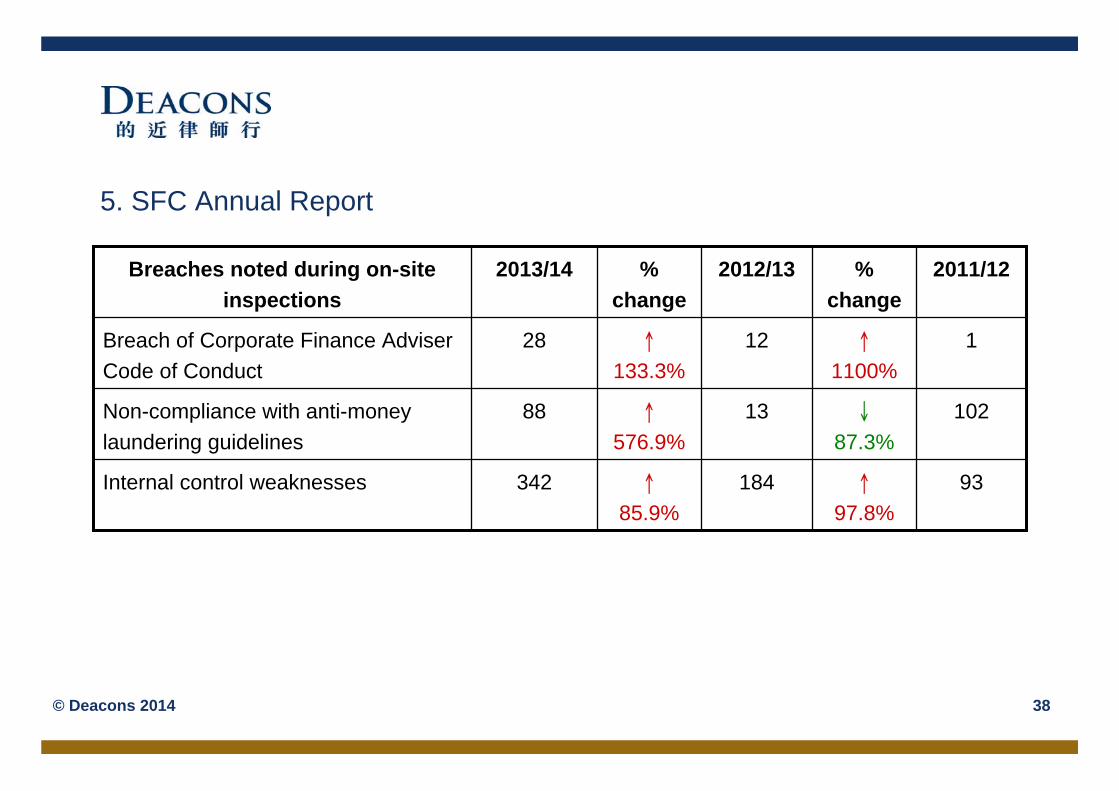

5. SFC Annual Report

93↑

97.8%184↑

85.9%342Internal control weaknesses

102↓

87.3%13↑

576.9%88Non-compliance with anti-money

laundering guidelines

1↑

1100%12↑

133.3%28Breach of Corporate Finance Adviser

Code of Conduct

2011/12 % change

2012/13% change

2013/14Breaches noted during on-site inspections

© Deacons 2014 38

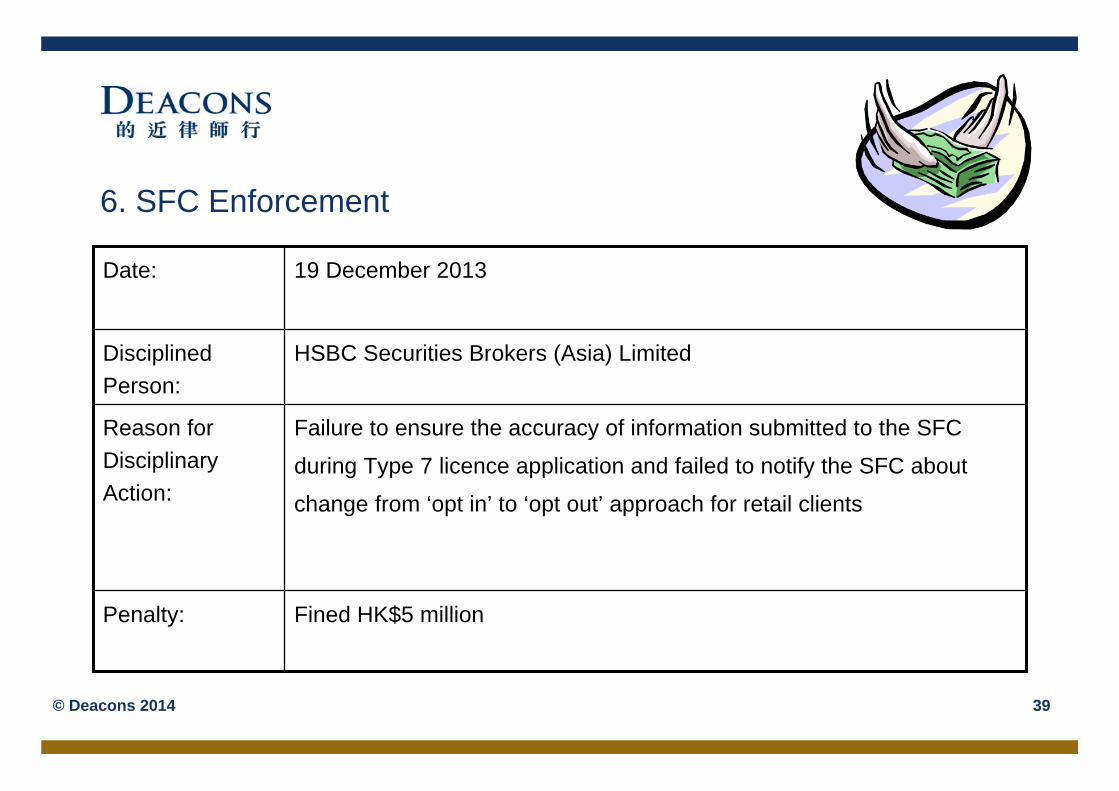

6. SFC Enforcement

Failure to ensure the accuracy of information submitted to the SFC

during Type 7 licence application and failed to notify the SFC about

change from ‘opt in’ to ‘opt out’ approach for retail clients

Reason for Disciplinary Action:

Fined HK$5 millionPenalty:

HSBC Securities Brokers (Asia) LimitedDisciplined Person:

19 December 2013Date:

© Deacons 2014 39

6. SFC Enforcement

Eastern Magistrates’ Court convicted both parties on three counts of

providing advisory services on corporate finance without an SFC

licence

Reason for Disciplinary Action:

Fine of HK$1.5 million and director given 6 month jail sentence suspended for 18 months

Penalty:

C.L. Management Services Limited and its directorDisciplined Person:

19 May 2014Date:

© Deacons 2014 40