Embed Size (px)

Citation preview

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 1/65

Page 1KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 2/65

Page 2KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

COMPANY PROFILE

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 3/65

Page 3KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

COMPANY PROFILE

DBFS Securities ltd is a associate of, Doha Bank, Qatar, One of India¶s Leading & fastest

growing private sector financial services companies, With interests in Asset Management and

Mutual Funds, and other activities in financial services.

DBFS Securities ltd offers a single window platform for the financial transactions. Offering an

investment avenue for a wide range of asset classes like Equity, Equity & Commodity

Derivatives, Mutual Funds, IPO Undertaking, Offshore Investments, Their endeavor is to change

the way India transacts in financial markets and avails financial services. One of their key

features is that the most cost-effective, convenient and secure way to transact in a wide range of

financial products and services. DBFS Securities ltd is targeting the low level of retail

penetration in Indian retail financial market. Retail participation in equities in India is amongst

the lowest in the world, with less than 3 percent of household sector financial savings invested in

equity/equity-related assets.

The company has formally commenced operations in April 1992, as one of the first corporate

brokerages in India, The Doha Brokerage & Financial Services Ltd (formerly Select Securities

Ltd), is the flagship company of the DBFS group. Doha Brokerage & Financial Services Ltd is

focused on creating utmost value for its customers, consistently by drawing on our collective

expertise, resources and global exposure.

To serve our customers better, the company has gone beyond the traditional brokerage business,

and offers a wide range of services, which include total wealth management and investment

solutions. With a pan Indian presence, which comprises over 260 branches across major cities, as

well as in Dubai and Doha in the Middle East, DBFS is always closer to its customers.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 4/65

Page 4KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

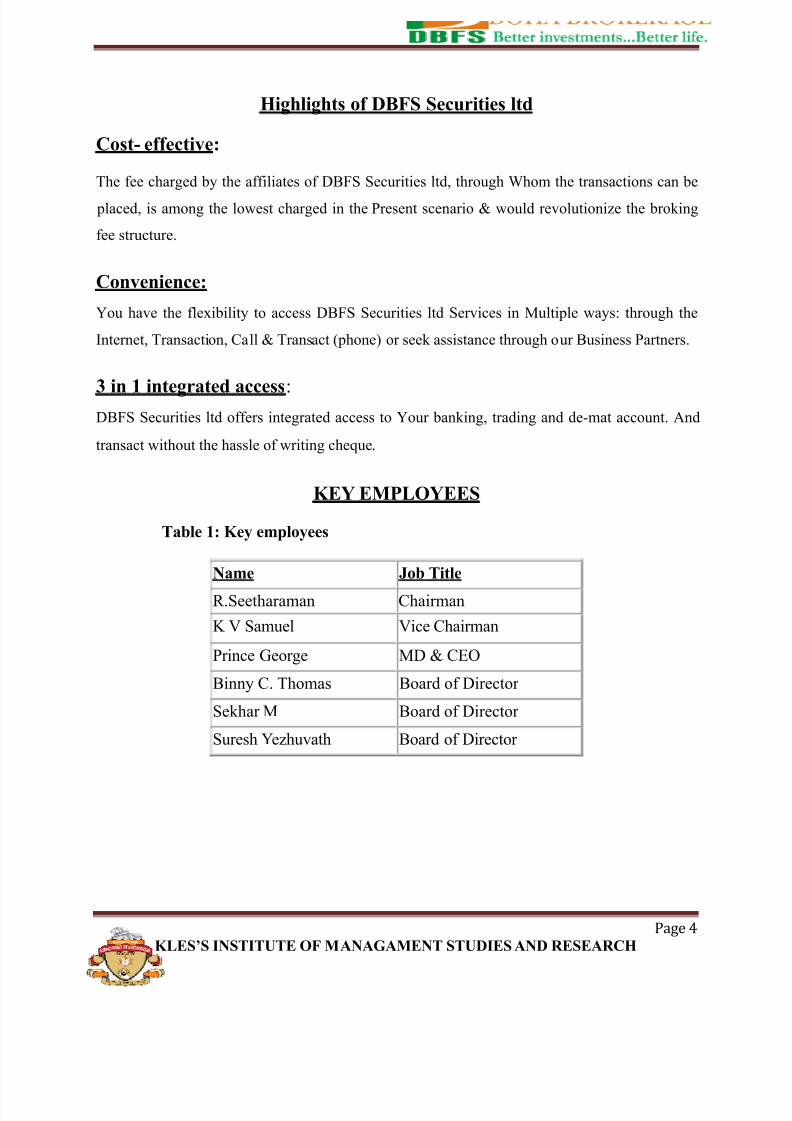

Highlights of DBFS Securities ltd

Cost- effective:

The fee charged by the affiliates of DBFS Securities ltd, through Whom the transactions can be

placed, is among the lowest charged in the Present scenario & would revolutionize the broking

fee structure.

Convenience:

You have the flexibility to access DBFS Securities ltd Services in Multiple ways: through the

Internet, Transaction, Call & Transact (phone) or seek assistance through our Business Partners.

3 in 1 integrated access:DBFS Securities ltd offers integrated access to Your banking, trading and de-mat account. And

transact without the hassle of writing cheque.

KEY EMPLOYEES

Table 1: Key employees

Name Job Title

R.Seetharaman Chairman

K V Samuel Vice Chairman

Prince George MD & CEO

Binny C. Thomas Board of Director

Sekhar M Board of Director

Suresh Yezhuvath Board of Director

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 5/65

Page 5KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

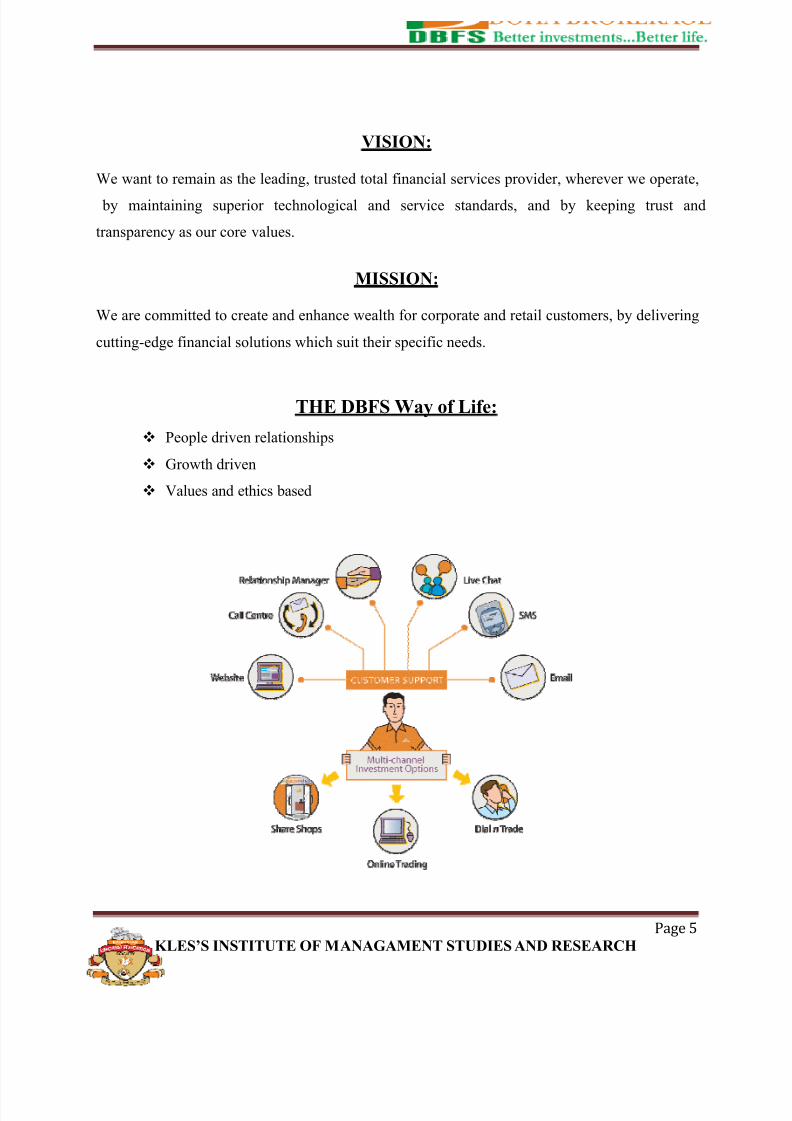

VISION:

We want to remain as the leading, trusted total financial services provider, wherever we operate,

by maintaining superior technological and service standards, and by keeping trust and

transparency as our core values.

MISSION:

We are committed to create and enhance wealth for corporate and retail customers, by delivering

cutting-edge financial solutions which suit their specific needs.

THE DBFS Way of Life:

People driven relationships

Growth driven

Values and ethics based

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 6/65

Page 6KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

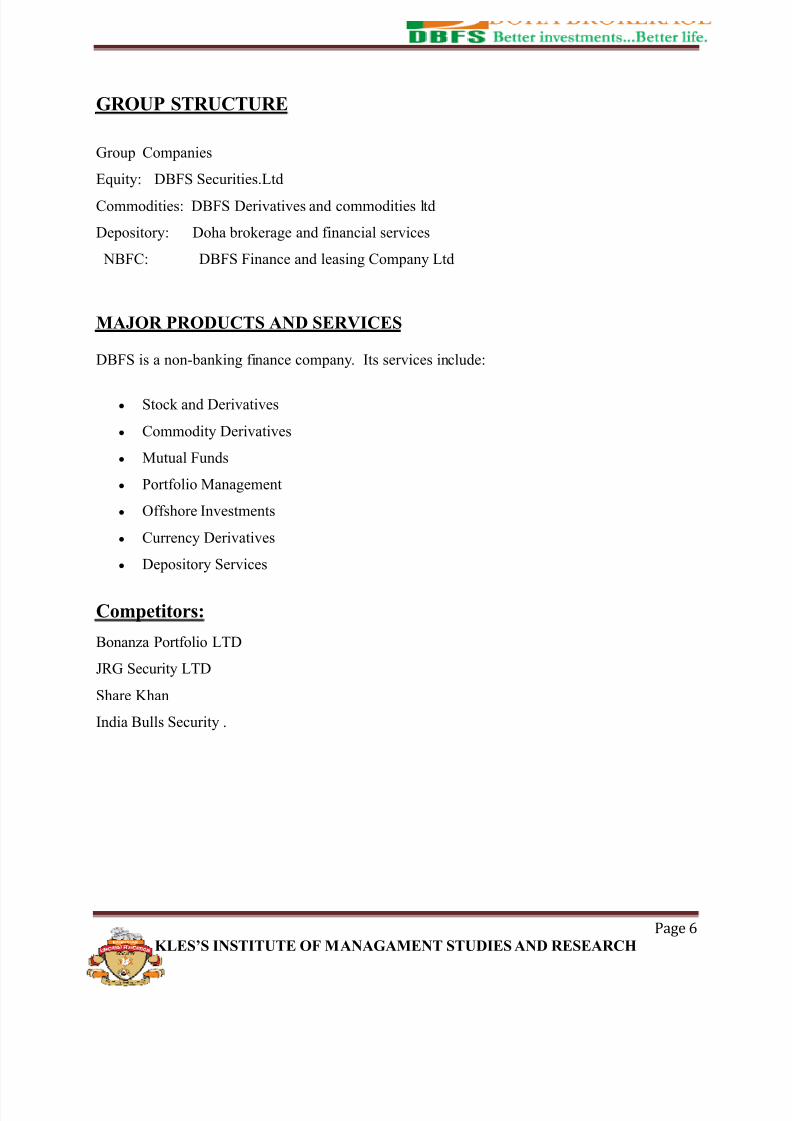

GROUP STRUCTURE

Group Companies

Equity: DBFS Securities.Ltd

Commodities: DBFS Derivatives and commodities ltd

Depository: Doha brokerage and financial services

NBFC: DBFS Finance and leasing Company Ltd

MAJOR PRODUCTS AND SERVICES

DBFS is a non-banking finance company. Its services include:

y Stock and Derivatives

y Commodity Derivatives

y Mutual Funds

y Portfolio Management

y Offshore Investments

y Currency Derivatives

y Depository Services

Competitors:

Bonanza Portfolio LTD

JRG Security LTD

Share Khan

India Bulls Security .

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 7/65

Page 7KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Requirements to open De-mat Account at DBFS Securities.

De-mat account

Meaning :

Demat means dematerilisation of securities in dematerilisation process physical form of

securities will be converted in to electronic form and this account just we require to store the

shares we bought.

We can open a demat account with registered Depository participant.

The typical steps involved in opening a demat account are as follows.

1. Filling an account opening form by physically or electronically.

2. Signing an agreement with Depository Participant.

3. Submitting documents supporting the proof of your identity and address which has to be

attested copies of the account details given by the bank , pan card , and 2 recent

photographs ,and account opening charges.

Doha brokerage and Financial Services have been providing demats in three ways¶ viz.

1. Zero account opening.

2. Rs1000 account opening.

3. Rs3000 account opening.

4. Rs5000 account opening.

Zero account opening.

We can open demat account without any charges at DBFS securities Ltd. for this zero account

opening the company will be charging Rs500 as annual maintenance charges.

Rs.1000 account opening .

We can open demat account with charge of Rs1000 as account opening charge at

DBFS securities Ltd. for this account opening the company will be providing free annualmaintenance services for first three years.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 8/65

Page 8KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Rs.3000 account opening.

We can open demat acconut with charge of Rs3000 as account openimng charge at

DBFS securities Ltd. for this account opening the copmany will be providing free

services for first three years which are listed below.

1. Three year annual maintainance free

2. Three year service charges free.

3. Three year demat charges free.

4. Three year depository Participant charges free.

Rs 5000 account opening.

We can open demat account with charge of Rs3000 as account opening charge at

DBFS securities Ltd. for this account opening the company will be providing free

Services for first three years which are listed below.

1. Life time annual maintenance free

2. Life time service charges free.

3. Life time demat charges free.

4. Life time depository Participant charges free.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 9/65

Page 9KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

BASICS OF STOCK MARKET

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 10/65

Page 10KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

BASICS OF STOCK MARKET:

The stock market is one of the most important sources for companies to raise money. This allows

businesses to be publicly traded, or raise additional capital for expansion by selling shares of

ownership of the company in a public market. The liquidity that an exchange provides affords

investors the ability to quickly and easily sell securities. This is an attractive feature of investing

in stocks, compared to other less liquid investments such as real estate. History has shown that

the price of shares and other assets is an important part of the dynamics of economic activity, and

can influence or be an indicator of social mood.

An economy where the stock market is on the rise is considered to be an up coming economy. In

fact, the stock market is often considered the primary indicator of a country's economic strength

and development. Rising share prices, for instance, tend to be associated with increased business

investment and vice versa. Share prices also affect the wealth of households and their

consumption. Therefore, central banks tend to keep an eye on the control and behavior of the

stock market and, in general, on the smooth operation of financial system functions. Financial

stability is the raison of central banks. Exchanges also act as the clearinghouse for each

transaction, meaning that they collect and deliver the shares, and guarantee payment to the seller

of a security. This eliminates the risk to an individual buyer or seller that the counterparty could

default on the transaction.

The smooth functioning of all these activities facilitates economic growth in that lower

costs and enterprise risks promote the production of goods and services as well as employment.

In this way the financial system contributes to increased prosperity. The financial system in most

western countries has undergone a remarkable transformation. One feature of this development is

disintermediation. A portion of the funds involved in saving and financing flows directly to the

financial markets instead of being routed via banks' traditional lending and deposit operations.

The general public's heightened interest in investing in the stock market, either directly or

through mutual funds, has been an important component of this process.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 11/65

Page 11KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Statistics show that in recent decades shares have made up an increasingly large proportion of

households' financial assets in many countries. In the 1970s, in Sweden, deposit accounts and

other very liquid assets with little risk made up almost 60 per cent of households' financial

wealth, compared to less than 20 per cent in the 2000s. The major part of this adjustment in

financial portfolios has gone directly to shares but a good deal now takes the form of various

kinds of institutional investment for groups of individuals, e.g., pension funds, mutual funds,

hedge funds, insurance investment of premiums, etc. The trend towards forms of saving with a

higher risk has been accentuated by new rules for most funds and insurance, permitting a higher

proportion of shares to bonds. Similar tendencies are to be found in other industrialized

countries.

In all developed economic systems, such as the European Union, the United States, Japan andother developed nations, the trend has been the same: saving has moved away from traditional

(government insured) bank deposits to more risky securities of one sort or another.

Riskier long-term saving requires that an individual possess the ability to manage the associated

increased risks. Stock prices fluctuate widely, in marked contrast to the stability of (government

insured) bank deposits or bonds. This is something that could affect not only the individual

investor or household, but also the economy on a large scale. The following deals with some of

the risks of the financial sector in general and the stock market in particular. This is certainly

more important now that so many newcomers have entered the stock market, or have acquired

other 'risky' investments (such as 'investment' property, i.e., real estate and collectables).

This is a quote from the preface to a published biography about the long-term value-oriented

stock investor Warren Buffett. Buffett began his career with $100, and $105,000 from seven

limited partners consisting of Buffett's family and friends. Over the years he has built himself a

multi-billion-dollar fortune. The quote illustrates some of what has been happening in the stock

market during the end of the 20th century and the beginning of the 21st century.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 12/65

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 13/65

Page 13KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Speculator:

Speculator is a person who trades with a higher-than-average risk, in return for a higher-than-

average profit potential. Speculators take large risks, especially with respect to anticipating

future price movements, or gambling, in the hopes of making quick, large gains.

Going long:

It means holding the security for an extended period of time. Depending on the type of security, a

long-term asset can be held for as little as one year or more

Going short

Selling the existing security immediately to protect the profit made or to minimizing the loss.

Squaring off´:

Its an intraday trading in the trader first sells the shares and then reverse the process (buying

/selling) within the closing of the market on the same day and pays off difference amount if he

has lost or gains profit. So by doing so at the end of the day he owns shares in his account.

Derivatives markets:

Derivatives markets provides instruments for handling of financial risks.Derivatives markets

broadly can be classified into two categories, those that are traded on the exchange and the those

traded one to one or µover the counter¶. They are hence known as.

y Exchange Traded Derivatives .y OTC Derivatives (Over The Counter ).

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 14/65

Page 14KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

OTC Equity Derivatives

y Traditionally equity derivatives have a long history in India in the OTC market.

y Options of various kinds (called Teji and Mandi and Fatak) in un-organized markets were

traded as early as 1900 in Mumbai y The SCRA however banned all kind of options in 1956.

Bombay Stock Exchange

LOGO

The Bombay Stock Exchange (BSE) is located in Dalal Street, Mumbai. Established in

1875, BSE is the oldest stock exchange in Asia. There are around 3,500 companies in the

country which are listed and have a significant trading volume. As of July 2005, the

market capitalization of the BSE is about Rs. 20 trillion (US $466 billion). The BSE

`Sensex' is a widely used market index for the BSE. As of 2005, it is among the 5 biggest

stock exchanges in the world in terms of number of transactions.

Along with the NSE, the companies listed on the BSE have a combined market cap of

$125.5Billion.

An informal group of 22 stockbrokers had been trading under a banyan tree opposite the

Town Hall of Bombay from mid-1850s. This banyan tree still stands in Horniman Circle

Park, Mumbai. This informal group of stockbrokers organized themselves as The Native

Share and Stockbrokers Association which, in 1875, was formally organized as the

Bombay Stock Exchange (BSE). BSE is the oldest stock exchange in Asia, the second

being the Tokyo Stock Exchange, established in 1878. Premchand Roychand was a

leading stockbroker of that time, and he assisted in setting out traditions, conventions,

and procedures for the trading of stocks at Bombay Stock Exchange and they are still

being followed.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 15/65

Page 15KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

y Dalal Street

James M. Maclean inaugurated the Brokers Hall in January 1899. After the First World

War, BSE was shifted to an old building, near the Bombay Town Hall and in 1928, the

plot on which the BSE building now stands, on Dalal Street, was acquired, and a buildingwas constructed in 1930.The Bombay Stock Exchange followed the familiar outcry

system for stock trading, which was replaced, in the year 1995, with screen-based e-

Trading. BSE is presently housed in a 28-storied Jeejeebhoy Towers, where the older

structure once stood: the present building derives its name from Sir Phiroze Jamshedjee

Jeejeebhoy, the chairman of the Bombay Stock Exchange from 1966, until his death in

1980.

y BSE Sensex

The BSE Sensex is a value-weighted index composed of top 30 companies, with the base

April 1979 = 100. The set of companies in the index is essentially fixed. These

companies account for around one-fifth of the market capitalization of the BSE.

BSE - other Indices

Apart from BSE Sensex, which is the most popular stock index in India, BSE uses other

stock Indices as well:

y BSE 100

y BSE 500

y BSEPSU

BSEMIDCAP

BSESMLCAP

BSEBANKEX.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 16/65

Page 16KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Hours of operation

y Beginning of the Day Session....8:00 - 9:00

y Login Session....9:00 - 9:30

y Trading Session....9:55 - 15:30

y Position Transfer Session....15:30 - 15:50

y Closing Session....15:50 - 16:05

y Option Exercise Session....16:05 - 16:35

y Margin Session....16:35 - 16:50

y Query Session....16:50 - 17:35

y End of Day Session....17:35

The hours of operation for the BSE quoted above are stated in terms of the local time in

Mumbai, India (also known as Bombay). This translates into a standard time zone

UTC/GMT +5:30.

BSE categories

Bombay Stock Exchange or the BSE is the largest stock exchange in India in terms of

highest number of companies listed with the stock exchange. If you consider the market

capitalization of the companies listed with BSE even then the stock exchange is the

largest in the country. There are thousands of companies listed at the stock exchange and

they are divided into different categories depending on various factors including market

capitalization, parameters set by the Securities and Exchange Board of India or the SEBI,

number of years of listing at the exchange, equity capital of the company, liquidity of the

company and so many other factors.

Market capitalization of the company is a determining factor for dividing the stocks indifferent groups. Market capitalization of a company is calculated by multiplying the

number of outstanding stocks of the company at the market with the current price of the

stock at the market. Along with that the bonds at the debt market of the company are also

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 17/65

Page 17KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

taken into consideration. Depending on the market capitalization stocks are divided

mainly into three categories ± the large cap stocks, mid cap stocks and the small cap

stocks. Generally the biggest companies with a market capital of more than $10 billion

are considered to be large cap stocks. The range for determining the mid cap stocks is

between $ 2 billion to $ 10 billion. Companies that have a market capitalization of the

less than $ 2 billion are grouped under the small cap stocks.

Securities and Exchange Board of India is the governing body for all the stock exchanges

in India and they frame the rules and regulations for the stock exchanges. Starting right

from the listing of the companies, issuing of securities, trading of stocks at the stock

market, everything is controlled by the Securities and Exchange Board of India or SEBI.

Based on the guideline and parameters of trading by the SEBI authorities, the stockslisted at the BSE are divided. That means there are different trading guidelines and rules

for each of the categories of stocks listed at the Bombay Stock Exchange.

Other factors like the number of years of listing of the company are considered for

determining the authenticity of the company and the business potential of the company.

The equity capital of the company and the asset of the companies are also considered for

examining the financial potential of the company. When a company applies for listing at

the Bombay Stock Exchange they have to fulfill all the set conditions and then the BSE

authority carries out a due diligence to examine the company. After that depending on the

parameters of the categorization the company is listed at the appropriate group. Often

times listed stocks are rearranged by the BSE. That is the group or the category of the

stocks is changed on the basis of the parameters that are set for determining the category

of the stock. Here we are presenting the existing groups or categories in which the BSE

stocks are divided.

Primarily there are five groups in which the listed stocks are divided and they are

A, B, T, Z, and F. The µA¶ group comprises stocks that have fairly good growth rate.

These companies offer dividend to the investors and have good capital appreciation over

the time. The stocks that are listed with µA¶ category have the facility to carry forward to

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 18/65

Page 18KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

the next settlement cycle. This is an advantage from the margin and derivative trading

point of view. The category µB¶ is basically a subset of all the listed stocks and the stocks

listed in this category have greater market capitalization that the rest of the stocks. The

trading of the stocks that are listed in the µT¶ category needs to be settled on the very

trading day and the deals can not be carried forward. This is done by BSE to restrict any

unwanted movement in these scripts. The stocks in the µZ¶ group are marked for not

complying with the rules and regulations of the stock exchange and these stocks are often

suspended from trading. The µF¶ group is reserved for the stocks listed at the debt market.

National Stock Exchange (NSE)

LOGO

With the liberalization of the Indian economy, it was found inevitable to lift the Indian

stock market trading system on par with the international standards. On the basis of the

recommendations of high powered Pherwani Committee, the National Stock Exchange was

incorporated in 1992 by Industrial Development Bank of India, Industrial Credit and Investment

Corporation of India, Industrial Finance Corporation of India, all Insurance Corporations,

selected commercial banks and others.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 19/65

Page 19KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Trading at NSE can be classified under two broad categories:

(a) Wholesale debt market and

(b) Capital market.

Wholesale debt market operations are similar to money market operations - institutions

and corporate bodies enter into high value transactions in financial instruments such as

government securities, treasury bills, public sector unit bonds, commercial paper, certificate of

deposit, etc.

There are two kinds of players in NSE:

(a) trading members and

(b) participants.

Recognized members of NSE are called trading members who trade on behalf of

themselves and their clients. Participants include trading members and large players like banks

who take direct settlement responsibility.

Trading at NSE takes place through a fully automated screen-based trading mechanism

which adopts the principle of an order-driven market. Trading members can stay at their offices

and execute the trading, since they are linked through a communication network. The prices at

which the buyer and seller are willing to transact will appear on the screen. When the prices

match the transaction will be completed and a confirmation slip will be printed at the office of

the trading member.

NSE has several advantages over the traditional trading exchanges. They are as follows:

y NSE brings an integrated stock market trading network across the nation.

y Investors can trade at the same price from anywhere in the country since inter-market

operations are streamlined coupled with the countrywide access to the securities.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 20/65

Page 20KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

y Delays in communication, late payments and the malpractice¶s prevailing in the

traditional trading mechanism can be done away with greater operational efficiency and

informational transparency in the stock market operations, with the support of total

computerized network.

Unless stock markets provide professionalised service, small investors and foreign investors

will not be interested in capital market operations. And capital market being one of the major

sources of long-term finance for industrial projects, India cannot afford to damage the capital

market path. In this regard NSE gains vital importance in the Indian capital market system.

NSE categories

NSE or the National Stock Exchange is one of the largest stock exchanges in India. In fact it is

the biggest in terms of daily trading and turn over. It is being speculated that the National Stock

Exchange will surpass the Bombay Stock Exchange in terms of market capitalization within

2010. There are thousands of companies that are listed with the NSE and they are divided into

different categories primarily depending on market capitalization.

Market capitalization is the primary factor for categorically dividing the listed stocks at the stock

exchanges all over the world. Basically market capitalization is calculated by multiplying the

present market price of the stock with the number of outstanding stocks in the market. While

calculating the market capitalization of a company the bonds of that company at the debt market

is considered as well. The market capitalization of a company is an indication of the financial

position of the company. It also gives an idea of the fact that how big is the company.

Primarily the stocks that are listed in the National Stock Exchange are divided into three

different categories on the basis of the market capitalization large cap, mid cap and the small

cap. There are certain criteria that are decided by the NSE authorities to determine which stockswill fall in the large cap segment and which one will come under the small cap category.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 21/65

Page 21KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Large Cap Stocks ± These are stocks that represent the biggest and most reputed companies

among all the listed companies in the stock exchange. Generally the companies that have a

market capitalization of more than $ 10 billion are considered to have a large market

capitalization. The stocks of these companies are categorized as the large cap stocks. At NSE as

well companies with the large market capital is labeled as the large cap stocks. The large cap

companies are mostly the companies that are in business for years and making significant growth

in terms of profit and asset accumulation. This is primarily the reason that the large cap stocks

are considered for including in the Nifty that is the prime index of the National Stock Exchange.

Mid Cap Stocks ± The mid size businesses with moderate market capitalization are considered

to be mid cap companies. Generally those companies that have a market capital between $ 2

billion and $ 10 billion is considered to be mid cap companies. The stocks of these companiesare categorized as the mid cap stocks. The mid cap stocks have great investment proposition as

they have all the sign of rising in the market and give you good return on your investment.

Small Cap Stocks ± Then there are of course the small cap companies that have small capital.

Generally companies with a market capital between $ 200 million and $ 2 billion are said to be

small cap companies and stocks of these companies are considered in the small cal segment.

Mostly the small cap companies are relatively new companies that have got listed at the stock

market. Investing in the small cap stocks are have more risk as these companies take too long to

rise in the market. As these companies are relative new and you hardly have any resources to

guess the potential of the company it is not wise to invest in these companies for long term. But

you can invest in these companies and do some margin trading if you have definite and

trustworthy tips.

Apart from these prominent stock categories in National Stock Exchange there are of

course other categories like the Micro cap and the penny stocks. While the micro cap

segment has companies with less than $ 300 million market capital, the penny stocks are

low priced stocks. Besides the division that is made on the basis of the market

capitalization, the stocks at the National Stock Exchange are also categorized on the basis

of the sectors of the companies.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 22/65

Page 22KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Securities and Exchange Board of India

It was formed officially by the Government of India in 1992 with SEBI Act 1992 being passed

by the Indian Parliament. SEBI is headquartered in the business district of Bandra-Kurla

complex in Mumbai, and has Northern, Eastern, Southern and Western regional offices in New

Delhi, Kolkata, Chennai and Ahmadabad.

Controller of Capital Issues was the regulatory authority before SEBI came into existence it

derived authority from the Capital Issues (Control) Act, 1947.

Initially SEBI was a non statutory body without any statutory power. However in 1995, the SEBI

was given additional statutory power by the Government of India through an amendment to the

securities and Exchange Board of India Act 1992. In April, 1998 the SEBI was constituted as the

regulator of capital market in India under a resolution of the Government of India.

Functions and responsibilities

SEBI has to be responsive to the needs of three groups, which constitute the market:

y the issuers of securities

y the investors

y the market intermediaries.

SEBI has three functions rolled into one body: quasi-legislative, quasi-judicial and quasi-

executive. It drafts regulations in its legislative capacity, it conducts investigation and

enforcement action in its executive function and it passes rulings and orders in its judicial

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 23/65

Page 23KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

capacity. Though this makes it very powerful, there is an appeals process to createaccountability.

There is a Securities Appellate Tribunal which is a three-member tribunal and is presently

headed by a former Chief Justice of a High court - Mr. Justice NK Sodhi. A second appeal lies

directly to the Supreme Court.

SEBI has enjoyed success as a regulator by pushing systemic reforms aggressively and

successively (e.g. the quick movement towards making the markets electronic and paperless

rolling settlement on T+2 basis). SEBI has been active in setting up the regulations as required

under law.

SEBI has also been instrumental in taking quick and effective steps in light of the global

meltdown and the Satyam fiasco it had increased the extent and quantity of disclosures to be

made by Indian corporate promoters. More recently, in light of the global meltdown, it

liberalised the takeover code to facilitate investments by removing regulatory structures. In one

such move, SEBI has increased the application limit for retail investors to Rs 2 lakh, from Rs 1

lakh at present

SEBI has been obligated to protect the interests of the investors in securities andto promote

and development of, and to regulate the securities market by such measures,as it thinks fit.

(a) Regulating the business in stock exchanges and any other securities markets.

(b) Registering and regulating the working of stock brokers, sub-brokers, share transfer

agents, bankers to an issue, trustees of trust deeds, registrars to an issue,

merchant bankers, underwriters, portfolio managers, investment advisers and such

otherintermediaries who may be associated with securities markets in any manner.

c) Registering and regulating the working of the depositories, participants, custodians of

securities, foreign institutional investors, credit rating agencies and such

otherintermediaries as SEBI may, by notification, specify in this behalf.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 24/65

Page 24KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

d) Registering and regulating the working of venture capital funds and

collective investment schemes including mutual funds.

e) Promoting and regulating self-regulatory organizations.

f) Prohibiting fraudulent and unfair trade practices relating to securities markets.

g) Promoting investors' education and training of intermediaries of securities markets.

h) Prohibiting insider trading in securities.

i) Regulating substantial acquisition of shares and take-over of companies.

j) Calling for information from, undertaking inspection, conducting inquiries and audits of

the stock exchanges, mutual funds, other persons associated with the securities

market, intermediaries and self-regulatory organizations in the securities market.

k) Calling for information and record from any bank or any other authority or board or l) Corporation established or constituted by or under any Central, State or Provincial Actin

respect of any transaction in securities which is under investigation or inquiry bythe

Board.

m) Performing such functions and exercising according to Securities Contracts

(Regulation) Act, 1956, as may be delegated to it by the Central Government.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 25/65

Page 25KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Powers

For the discharge of its functions efficiently, SEBI has been invested with the necessary powers which

are:

1. To approve byílaws of stock exchanges.

2. To require the stock exchange to amend their byílaws.

3. Inspect the books of accounts and call for periodical returns from recognized stock

exchanges.

4. Inspect the books of accounts of financial intermediaries.

5. Compel certain companies to list their shares in one or more stock exchanges.

6. Levy fees and other charges on the intermediaries for performing its functions.

7. Grant licence to any person for the purpose of dealing in certain areas.

8. Delegate powers exercisable by it.

9. Prosecute and judge directly the violation of certain provisions of the companies Act.

SEBI Committees

1. Technical Advisory Committee.

2. Committee for review of structure of market infrastructure institutions.

3. Members of the Advisory Committee for the SEBI Investor Protection and Education

Fund.

4. Takeover Regulations Advisory Committee.

5. Primary Market Advisory Committee (PMAC).

6. Secondary Market Advisory Committee (SMAC).

7. Mutual Fund Advisory Committee.

8. Corporate Bonds & Securitization Advisory Committee.

9. Takeover Panel.

10. SEBI Committee on Disclosures and Accounting Standards (SCODA).

11. High Powered Advisory Committee on consent orders and compounding of offences.

12. Derivatives Market Review Committee.

13. Committee on Infrastructure Funds.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 26/65

Page 26KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

INDIAN INVESTMENT SCENARIO

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 27/65

Page 27KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Investment scenario in India :

Investment is the employment of funds on assets with the aim of earning income or capital

appreciation. Investment has two attributes namely time and risk.

Present consumption is sacrificed to get a return in the future. The sacrifice that has to be

borne is certain but the return in the future may be uncertain. This attribute of investment

indicates the risk factor. The risk is undertaken with a view to reap some return from the

investment. For a layman, investment means monetary commitment. A person¶s commitment to

buy a flat or house for his personal use may be an investment from his point of view. This cannot

be considered as an actual investment as it involves sacrifice but does not yield any financial

return. To the economist, investment is the net addition made to the nation¶s capital stock that

consists of goods and services that are used in the production process. A net addition to the stock means an increase in the buildings, equipments or inventories. These capital stocks are used to

produce other goods and services.

Financial investment is the allocation of money to assets that are expected to yield some

gain over a period of time. It is an exchange of financial claims such as stock and bonds for

money. They are expected to yield returns and experience capital growth over the years.The

financial and economic meanings are related to each other because the savings of the individual

flow into the capital market as financial investments, to be economic investment. Even though

they are related to each other, we are concerned only about the financial investment made on

securities.

Investment Objectives:

The main investment objectives are increasing the rate of return and reducing the risk. Other

objectives like safety, liquidity and hedge against inflation can be considered as subsidiary

objectives.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 28/65

Page 28KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

1) Return:

Investors always expect a good rate of return from their investments. Rate of return could

be defined as the total income the investor receives during the holding period stated ass a

percentage of the purchasing price at the beginning of the holding period.

Rate of return is stated semi-annually or annually to help comparison among the different

investment alternatives. If it is a stock, the investor gets the dividend as well as the capital

appreciation as returns. Market return of the stock indicates the price appreciation for the

particular stock.

2) Risk:

Risk of holding securities is related with the probability of actual return becoming less than

the expected return. The word risk is synonymous with the phrase variability of return.

Investments¶ risk is just as important as measuring its expected rate of return because minimizing

risk and maximizing the rate of return are interrelated objectives in the investment management.

An investment whose rate of return varies widely from period to period is risky than whose

return that does not change much. Every investor likes to reduce the risk of his investment by

proper combination of different securities.

3) Liquidity:

Marketability of the investment provides liquidity to the investment. The liquidity depends

upon the marketing and trading facility. If a portion of the investment could be converted into

cash without much loss of time, it would help the investor meet the emergencies. Stocks are

liquid only if they command good market by providing adequate return through dividends and

capital appreciation.

4) Hedge against inflation:

Since there is inflation in almost all the economy, the rate of return should ensure a cover

against the inflation. The return rate should be higher than the rate of inflation else the investor

will have loss in real terms.Growth stocks would appreciate in their values overtime and provide

a protection against inflation. The return thus earned should assure the safety of the principal

amount, regular flow of income and be a hedge against inflation.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 29/65

Page 29KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

5) Safety:

The selected investment avenue should be under the legal and regulatory frame work. If it

is not under the legal frame work, it is difficult to represent the grievances, if any. Approval of

the law itself adds a flavour of safety. Even though approved by law, the safety of the principal

differs from one mode of investment to another. Investments done with the government assure

more safety than with the private party.

From the safety point of view investments can be ranked as follows: bank deposits,

government bonds, UTI units, non-convertible debentures, convertible debentures, equity shares,

and deposits with the non-banking financial companies.

The Investment Process:

There are five main steps in investment management:

Setting investment objectives.

Establishing investment policy.

Selecting the portfolio strategy.

Selecting the assets.

Measuring and evaluating performance

1. Setting Investment Objectives:

The first main step in the investment management process is setting investment objectives.

For institutions such as pension funds and life insurance companies, these objectives may be a

cash flow specification to satisfy a liability due at some future date or a series of liabilities due at

different future dates. A guaranteed investment contract (GIC) sold by a life insurance company

is an example of the former; the projected benefit payout to beneficiaries of a pension plan and

an annuity policy sold by a life insurance company are examples of multiple liabilities.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 30/65

Page 30KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

For institutions such as banks and thrifts, the objective may be to lock-in a minimum interest

rate spread over the cost of their funds. For others, such as mutual funds and some trust accounts,

the investment objective may be to maximize return.

2. Establishing Investment Policy:

The second main step is establishing policy guidelines to satisfy the objectives. Setting

policy begins with asset allocation among the major asset classes-the products of the capital

market. The major asset classes include equities, fixed income securities, real estate, and foreign

securities. Client and regulatory constraints must be considered in establishing an investment

policy. For example, state regulators of insurance companies (life insurance companies and

property and casualty insurance companies) may restrict the amount of funds allocated to certain

major asset classes. Even the amount allocated within a major asset class may be restricted based

on the characteristics of the particular asset. So too must tax and financial reporting implications

be considered in adopting investment policies.

For example, life insurance companies have certain tax advantages that make investing in

tax-exempt municipal securities generally unappealing. Since pension funds are exempt from

taxes, they too would not usually be interested in tax-exempt municipal securities. Property and

casualty insurance companies will vary their ownership of tax-exempt municipal securities

depending on projected profits from underwriting operations. Commercial banks at one time

were major buyers of municipal securities; however, the 1986 tax act made investing in

municipal bonds somewhat less attractive to commercial banks.

Financial reporting requirements, in particular Statement of Financial Accounting Board

Nos. 87 and 88 and the Omnibus Budget Reconciliation Act of 1987 (a legislative initiative

which reinforces the FASB 87 interpretation of liabilities), affect the way in which pension funds

establish investment policies. Unfortunately, sometimes financial reporting considerations force

institutions to establish investment policies that may not be in the best interest of the institution

in the long run.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 31/65

Page 31KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

3. Selecting a Portfolio Strategy:

Selecting a portfolio strategy that is consistent with the objectives and policy guidelines

of the client or institution is the third step in the investment management process. Portfolio

strategies can be classified as either active strategies or passive strategies. Essential to all activestrategies are expectations about the factors that are expected to influence the performance of an

asset class. For example, with active equity strategies this may include forecasts of futures

earnings, dividends or price-earnings ratios. With active fixed income

Portfolios this may involve forecasts of future interest rates, future interest rate volatility

or future yield spreads. Active portfolio strategies involving foreign securities will require

forecasts of future exchange rates.

Passive strategies involve minimal expectation input. The most popular type of passive

strategy is indexing. The objective in indexing is to replicate the performance of a predetermined

index. While indexing has been employed extensively in the management of equity portfolios,

the use of indexing for managing fixed income portfolios is a relatively new practice.

Between these extremes of active and passive strategies have sprung strategies that have

elements of both. For example, the core of a portfolio may be indexed with the balance managed

actively. Or a portfolio may be primarily indexed but employ low risk strategies to enhance the

indexed return. This strategy is commonly referred to as ³enhanced indexing´ or ³indexing plus.´

In the fixed income area, several strategies classified as structured portfolio strategies

have been commonly used. A structured portfolio strategy is one in which a portfolio is designed

so as to achieve the performance of some predetermined benchmark. These strategies are

frequently used in funding liabilities.

When the predetermined benchmark is to have sufficient funds to satisfy a single liability

regardless of the course of future interest rates, a strategy known as immunization is used. When

the predetermined benchmark is multiple future liabilities that must be funded regardless of how

interest rates change, the strategy that can be used is immunization or cash flow matching.

Even within the immunization and cash flow matching strategies, low risk active

management strategies can be employed. One immunization strategy, contingent immunization,

allows the portfolio manager to actively manage a portfolio until Certain parameters are realized.

If those parameters are realized, the portfolio is then immunized.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 32/65

Page 32KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Indexing can be considered a structured portfolio strategy where the benchmark is to achieve the

performance of some predetermined index. Portfolio insurance strategies, where the objective is

to ensure that the value of the portfolio does not fall below a predetermined amount is also

viewed as a structured portfolio strategy.

4. Selecting Assets:

Once a portfolio is selected, the next main step is the selection of the specific assets to be

included in the portfolio. It is in this phase that financial theory tells us the investment manager

attempts to construct an optimal or efficient portfolio. An optimal or efficient portfolio is one that

provides the greatest expected return for a given level of risk, or equivalently, the lowest risk for

a given expected return.

5. Measuring and Evaluating Performance:

The measurement and evaluation of investment performance is the last step in the

investment management process. (Actually, it is improper to say that it is the last step since

investment management is an ongoing process.) This step involves measuring the performance

and then evaluating that performance relative to some realistic benchmark.

While the performance of a portfolio manager when compared to some benchmark may

demonstrate superior performance, this does not necessarily mean that the portfolio satisfied its

investment objective.

For example, suppose that a life insurance company establishes as its objective

maximization of Portfolio returns and allocates 75% of the fund to stocks and the balance to

bonds.

Suppose further that the portfolio manager responsible for the equity portfolio of this

pension fund earns a return over a one year horizon that is 4% higher than the Standard & Poor¶s

500 stock index (a benchmark used to evaluate equity performance). Assuming that the risk of

the portfolio was similar to that of the S&P 500, it would appear that the portfolio manager

performed well. However, suppose in spite of this performance the life insurance company

cannot meet its liabilities. The failure was in establishing the investment objectives and setting

policy, not with the manager responsible for managing the portfolio.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 33/65

Page 33KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Investment Avenues:

1. Life Insurance:Life insurance is a contract for payment of a sum of money to the person assured (or to

the person entitled to receive the same) on the happenings of event insured against. Usually the

contract provides for the payment of an amount on the date of maturity or at specified dates at

periodic intervals or if unfortunate death occurs. Among other things, the contracts also provide

for the payment of premium periodically to the corporation by the policy holders. Life insurance

eliminates risk.

There are many variants of a life insurance policy:

1. Whole Life Assurance Plans: These are low-cost insurance plans where the sum assured is

payable on the death of the insured

2. E ndowment Assurance Plans: Under these plans, the sum assured is pay-able on the

maturity of the policy or in case of death of the insured individual before maturity of the

policy.

3. T erm Assurance Plans: Under these plans, the sum assured is payable only on the death of

the insured individual before expiry of the policy.

4. Pension Plans: These plans provide for either immediate or deferred pension for life. The

pension payments are made till the death of the annuitant (person who has a pension plan)

unless the policy has provision of guaranteed period.

Life Insurance Corporation (LIC) is a government company. Till the year 2000, the LIC

was the sole provider of life insurance policies to the Indian public. However, the Insurance

Regulatory & Development Authority (IRDA) has now issued licenses to private companies to

conduct the business of life insurance. Some of the major private players in the sector are:

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 34/65

Page 34KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

y Bajaj Allianz Life Insurance Corporation

y Birla SunLife Insurance Co. Ltd.

y HDFC Standard Life Insurance Co. Ltd.

y ICICI Prudential Life Insurance Co. Ltd.

y ING Vysya Life Insurance Co. Pvt. Ltd.

y MAX New York Life Insurance Co. Ltd.

y MetLife India Insurance Co. Pvt. Ltd.

y Kotak Mahindra Old Mutual Life Insurance Co. Ltd.

y SBI Life Insurance Co. Ltd.

y TATA AIG Life Insurance Co. Ltd.

y AMP Sanmar Assurance Co. Ltd.

y AVIVA Life Insurance Co. Pvt. Ltd.

y Sahara India Life Insurance Co. Ltd.

y Shriram Life Insurance Co. Ltd.

The major advantages of life insurance are given below:

Protection:

Saving through life insurance guarantees full protection against risk of death of the saver. The

full assured sum is paid, whereas in other schemes only the amount saved is paid.

Easy payments:

For the salaried people the salary savings¶ schemes are introduced. Further, there is an easy

installment facility method of payment through monthly, quarterly, half yearly or yearly mode.

Liquidity:

Loans can be raised on the security of the policy.

Tax relief :

Tax relief in Income Tax and Wealth Tax is available for amounts paid by way of premium for life insurance subject to the tax rates in force.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 35/65

Page 35KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

2. Mutual Funds:

Investment companies or investment trusts obtain funds from large number of investors

through sale of units. The funds collected from the investors are placed under professional

management for the benefit of the investors. The mutual funds are broadly classified into open-

ended scheme and close-ended scheme.

Open-ended scheme:

The open-ended scheme offers its units on a continuous basis and accepts funds from

investors continuously. Repurchase is carried out on a continuing basis thus, helping the

investors to withdraw their money at any time. In other words, there is an uninterrupted entry

and exit into the funds. The open-end scheme has no maturity period and they are not listed in

the stock exchanges. Investor can deal directly with the mutual fund for investment as well as

redemption. The open-ended fund provides liquidity to the investors since the repurchase

facility is available. Repurchase price is fixed on the basis of net asset value of the unit. In 1998

the open-ended schemes have crossed 80 in number.

Closed-ended funds:

The close-ended funds have a fixed maturity period. The first time investments are madewhen the close end scheme is kept open for a limited period. Once closed, the units are listed on

a stock exchange. Investors can buy and sell their units only through stock exchanges. The

demand and supply factors influence the prices of the units. The investor¶s expectation also

affects unit prices. The market price may not be the same as the net asset value.

Sometimes mutual funds with the features of close-ended and open-ended schemes have been

launched, known as interval funds. They can be listed in the stock exchange or may be available

for repurchase during specific periods at net asset value or relative prices.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 36/65

Page 36KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Interval Funds

Interval funds combine the features of open-ended and close-ended schemes. They are

open for sale or redemption during pre-determined intervals at NAV related prices.

Let us now classify Mutual Fund Schemes on the Basis of its Investment Objective:

Growth Funds

The aim of growth funds is to provide capital appreciation over the medium to long-term.

Such schemes normally invest a majority of their corpus in equities. It has been proven that

returns from stocks, have outperformed most other kind of investments held over the long term.

Growth schemes are ideal for investors having a long-term outlook seeking growth over a period

of time.

Income Funds

The aim of income funds is to provide regular and steady income to investors. Such

schemes generally invest in fixed income securities such as bonds, corporate debentures and

Government securities. Income Funds are ideal for capital stability and regular income.

Balanced Funds

The aim of balanced funds is to provide both growth and regular income. Such schemes

periodically distribute a part of their earning and invest both in equities and fixed income

securities in the proportion indicated in their offer documents. In a rising stock market, the NAV

of these schemes may not normally keep pace, or fall equally when the market falls. These are

ideal for investors looking for a combination of income and moderate growth.

TAX IMPLICATIONS

While dividend paid on closed-ended mutual funds is fully tax exempt, on redemption or

sale of units in the secondary market, your realization will attract short-term capital gains tax of

10 per cent. However, you can save tax by investing in Equity-Linked Savings Scheme (ELSS)

under Section 88 of the Income Tax Act, 1961, according to which 20 per cent of the amount

invested in ELSS which have a lock-in period of 3 years-can be deducted from your tax liability

subject to a maximum investment of Rs.10,000 per year. Also available under Section 88 are two

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 37/65

Page 37KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

pension plans: Unit Trust of India¶s Retirement Benefit Unit Plan (RBP) and Kothari Pioneer¶s

Pension Plan.

3. Equity Shares:

Equity shares are commonly referred to common stock or ordinary shares. Even though the

words shares and stocks are interchangeably used, there is difference between them. Share

capital of a company is divided into a no. of small units of equal value called shares. The term

stock is the aggregate of a member¶s fully paid up shares of equal value merged into one fund. It

is a set of shares put together in a bundle. The ³stock´ is expressed in terms of money and not as

many shares. Stock can be divided into fractions of any amount and such fractions may be

transferred like shares.

Equity shares have the following rights according to section 85(2) of the companies act 1956.

1. Right to vote at the general body meetings of the company.

2. Right to control the management of the company.

3. Right to share in the profits in the firm of dividends and bonus shares.

4. Right to claim on the residual after repayment of all the claims in the case of winding of

the company.

5. Right of pre-emption in the matter of issue of new capital.6. Right to apply to court if there is any discrepancy in the rights set aside.

7. Right to receive a copy of the statutory report, copies of annual accounts along with

audited report.

8. Right to apply the central government to call an annual when a company fails to call such

a meeting.

9. Right to apply the Company Law Board for calling an extraordinary general meeting.

In a limited company the equity shareholders are liable to pay the company¶s debit only

to the extent of their share in the paid up capital.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 38/65

Page 38KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

The equity shares have certain advantages. The main advantages are

Capital Appreciation

Limited liability

Free tradability

Tax advantages (in certain cases) and

Hedge against inflation.

TAX IMPLICATIONS ON EQUITY SHARES

While dividend is not taxable at the hands of the investor, capital gains are. When you sell

your shares at a profit, it attracts a capital gains tax. Gains realized within one year of purchase

of shares come under the short-term capital gains tax, and are included in gross taxable income.

If the duration is more than one year, it is termed as long-term capital gains tax. The rate is 10

percent for short-term capital gains and nil for long-term capital gains (long-term capital gains is

exempted totally).

4. Bonds:

Bond is a long term debt instrument that promises to pay a fixed annual sum as interest

for specified period of time.

The basic features of the bond are given below.

1) Bonds have face value. The face value is called par value. The bonds may be issued at par

value or at discount.

2) The interest rate is fixed sometimes it may be variable at as in the case of floating rate

bond. Interest is paid semi-annually or annually. The interest rate is known as coupon

rate. The interest rate is specified in the certificate.

3) The maturity date of the bond is usually specified at the issue time except in the case of

perpetual bonds.

4) The redemption value is also stated in the bonds. The redemption value may at par value

or at premium.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 39/65

Page 39KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

5) Bonds are traded in the stock market. When they are traded the market value may be at

par or at premium or at discount. The market value and redemption value need not be the

same.

The different bonds are:

Secured bonds and unsecured bonds

Perpetual bonds and redeemable bonds

Fixed interest rate bonds and floating interest bonds

Zero coupon bonds

Deep discount bonds

Capital indexed bonds

Debentures:

According to Companies Act 1956 ³debenture includes debenture stock, bonds and any

other securities of company, whether constituting a charge on the assets of the company or not´.

Debentures are generally issued by the private sector companies as a long-term promissory note

fro raising loan capital. The company promises to pay interest and principal as stipulated. Bond

is an alternative form of debenture in India. Public sector companies and financial institutions

issue bonds. Some of the characteristic features of debentures are from it is given in the form of certificate of indebtedness by the company specifying the date of redemption and interest rate.

Interest:

The rate of interest is fixed at the time of issue itself which is known as contractual or

coupon rate of interest. Interest is paid as a percentage of the par.

Redemption

As earlier the redemption date would be specified in the issue itself. The maturity

period may range from 5 years to 10 years in India. They may be redeemed in installments.

Redemption is done through a creation of sinking fund by the company. A trustee In charge

of the fund buys the debentures either from the market or owners. Creation of the sinking

fund eliminates the risk of facing financial difficulty at the time of redemption because

redemption requires huge sum.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 40/65

Page 40KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Buy back provisions help the company to redeem the debentures at a special price before the

maturity date. Usually the special price is higher than the par value of the debenture.

Indenture

It is a trust deed between the company issuing debenture and the debenture trustee who

represents the debenture holders. The trustee takes the responsibility of protecting the interest

of the debenture holders and ensures that the company fulfills the contractual obligations.

Financial institutions, banks, insurance companies or firm attorneies act s trustees to the

investors.

In the indenture the terms of the agreement, description of debentures, rights if the debenture

holders, rights of the issuing company and the responsibilities of the company are specified

clearly. Debentures are classified on the basis of the security and convertibility as

1) Secured or unsecured

2) Fully convertible debenture

3) Partly convertible debenture

4) Non-convertible debenture

TAX IMPLICATIONS ON BONDS

There are specific tax saving bonds in the market that offer various concessions and tax- breaks. Tax-free bonds offer tax relief under Section 88 of the Income Tax Act, 1961. Interest

income from bonds, up to a limit of Rs.12,000, is exempt under section 80L of the Income tax

Act, plus Rs.3,000 exclusively for interest from government securities. However, if you sell

bonds in the secondary market, any capital appreciation is subject to the Capital Gains Tax.

Tax-Saving Bonds

Some bonds have a special provision that allows the investor to save on tax. These are termedas Tax-Saving Bonds, and are widely used by individual investors as a tax-saving tool. Examples

of such bonds are:

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 41/65

Page 41KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

a. Infrastructure Bonds under Section 88 of the Income Tax Act, 1961

b. Capital Gains Bonds under Section 54EC of the Income Tax Act, 1961

c. RBI Savings Bonds (erstwhile, RBI Relief Bonds)

T ax Saving Infrastructure Bonds

Infrastructure bonds are available through issues of ICICI Bank and IDBI, brought out in the

name of ICICI Safety Bonds and IDBI Flexi bonds. These provide tax-saving benefits under

Section 88 of the Income Tax Act, 1961, up to an investment of Rs.1, 00,000, subject to the

bonds being held for a minimum period of three years from the date of allotment.

Tax Saving Capital Gains Bonds

Investments in bonds issued by the Rural Electrification Corporation (REC) are at present

eligible for capital gains tax savings. Gains made out of a capital transfer need to be invested in

the above bonds within six months of sale of capital assets in order for the proceeds of such sale

to be exempt from capital gains tax.

RBI Savings Bonds

RBI Savings Bonds are an instrument that are issued by the RBI, and currently has two

options ± one carrying an 8 percent rate of interest per annum, which is taxable and the other one

carries a 6.5 percent (tax-free) interest per annum. The interest is compounded half-yearly and

there is no maximum limit for investment in these bonds. The maturity period of the 8 percent

(taxable) bond is six years and that of the 6.5 percent (tax-free) bond is five years

5. Real Estate:

The real estate market offers a high return to the investors. The word real estate means

land and buildings. There is a normal notion that the price of the real estate has increased by

more than 12 percent over the past ten years. The population growth and the exodus of people

towards the urban cities have made the prices to increase manifold. Recently, the recession in the

economy has affected the real estate. Prices marked a substantial fall in 1998 from the 1997

prices.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 42/65

Page 42KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

Reasons for investing in real estate are given below:

y High capital appreciation compared to gold or silver particularly in the urban area.

y Availability of loans for the construction of houses. The 1999-2000 budget provides

huge incentives to the middle class to avail of housing loans. Scheduled banks now

have to disburse 3 percent of their incremental deposits in housing finance.

y Tax rebate is given to the interest paid on the housing loans.

Further Rs.75, 000 tax rebate on a loan up to Rs.5 lakhs which is availed of after April

1999.

If an investor invests in a house for about Rs.6-7lakh, he provides a seed capital of about Rs.1-2

lakh. The Rs.5 lakh loan, which draws an interest rate of 15 percent, will work out to be less than

9.6 percent because of the Rs.75, 000 exempted from tax annually. In assessing the wealth tax,

the value of the residential home is estimated at its historical cost and not on its present market

value.

The possession of a house gives an investor a psychologically secure feeling and a standing

among his friends and relatives.

Apart from making investment in the residential houses, the people in the higher income

bracket invest their money in time share plans of the holiday resorts and land situated near the

city limit with the anticipation of a capital appreciation. Farm houses and plantations also fall inthe line. In spite of the fast capital appreciation investors generally do not invest in the real estate

apart in the real estate apart from owning one or two houses. The reasons are:

y Requirement of huge capital: To purchase a land or house in the urban area, the

investor needs money in lakhs whereas he can buy equity, gold or other form of

investment by investing thousands of rupees.

y Malpractices: often-gullible investors become cheated in the purchase of land.

The properties already sold are resold to the investors. The investor has to lose the

hard-earned money.

y Restriction of the purchase: The land ceiling Act restricts the purchase of

agriculture land beyond a limit.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 43/65

Page 43KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

y Lack of liquidity: If the investor wants to sell the property, he cannot immediately

realize the money. The waiting period may be months or years.

The points to be taken care of while purchasing the real estate are:

y The plots should be approved by the local authority because on the un approved

layout construction of a house is not permitted.

y Possibility of capital appreciation. It depends upon the locality and facilities of the

site.

y Originality of title deeds. The site should be free from encumbrance. Encumbrance

certificate for a minimum period of latest 15 years should be got from the registrars¶

office.

y Plinth area should be verified.

Earliest records of securities trading in India are available from the end of eighteenth

century. Before 1850 there was business conducted in Mumbai in the share of bank and the

securities of east India Company, which were consider as securities for buying, selling and

exchange. The share of commercial bank, mercantile bank and bank of Bombay were some of the prominent shares traded. The business was conducted under a sprawling banyan tree in front

of the town hall, which is known as horniman Circle Park. In 1850, the companies act was

passed and that heralded the commencement of joint stock companies in India.

It was the American civil war that helped Indians to established broking business. The

leading broker, Shri Premchand Roichand designed and developed a procedure to be followed

while dealing in shares. In 1874 the dalal street became the prominent place for meeting of the

brokers to conduct business. The broker organized an association on 9th July 1875 known as

native share and stock broker association to protect the character, status of the native brokers.

That was the foundation of the stock exchange, Mumbai.

The exchange was established with 318 members. The stock exchange, Mumbai did not

have to look back as it started raiding high ladder of growth. The stock exchange is a market

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 44/65

Page 44KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

place, like any other centralize market where buyers and sellers can transact business in

securities at given point of a time in a convenient and competitive manner at the fairest possible

prizes.

In Jan 1899, Mr. James M Mac Len, MP inaugurated the brokers hall. After the first

world war the stock exchange was housed properly at an old building near the Town hall in1928,

the present premises where acquired surrounded by Dalal street, Mumbai samachar marg and

hamam street. A new building a present location was constructed and was occupied on 1st

Dec

1930.In 1950 the regulation of business in securities and stock exchange became an exclusively

central Government sub following adaptation of constitution of India. In 1956, the security

contract act was passed by the parliament of India. to regulate the securities market, SEBI was

initial established on Oct 12 1988 as an interim board under control of ministry of finance,

Government of India. In 1992, SEBI act was passed through which the SEBI came into

existence.

Hence SEBI acquired statutory status on 30th Jan 1992 by passing an ordinance, which

was subsequently converted into an act passed by the parliament on April 4th 1992. The main

objective of SEBI is to protect the interest of investor, regulate and promote the capital market by

creating an environment, which would facilitate mobilization of resources through efficient

allocation and to generate confidents among the investor.

As such SEBI is responsible for regulating stock exchanges and other intermediaries who may

be associated with capital market and the process of the public companies rising capital by

issuing instrument that will be traded on capital market. SEBI has been empowered by the

central government to develop and regulate capital markets in India and there by protect the

interest of investors. In 1992, OTCI (Over the counter exchange of India) came in to existent

where equities of small companies are listed.

In 1994, NSE(national stock exchange) came into existent which brought an and

to the open but cry system of trading securities which was in vogue for 150 years, and

introduced screen based trading system.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 45/65

Page 45KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

BSE (Bombay stock exchange) online trading system was launched on March 14th 1995. Online

trading can be done who are authorized by the stock exchange.

In screen based trading, investor place there buy and sale orders with brokers whose enter

the orders in the automated trading system. When buy and sale order matches, a trade is

generated and trade details are given to respective brokers. After a trade has taken place, the

buyer as to pay money and seller has to deliver the securities.

On the stock exchange hundred & thousands of trades take place every day.

Buyers and sellers are spread over a large geographical area. Due to these problems completing a

trade by paying cash to the seller & securities to buyer immediately on execution of trades on an

individually basis is virtually impossible. So the exchange allows trading to take place for a

specified period which is called trading cycle.

A unique settlement number identifies each trading cycle. Once the trading period is

over, buyer broker pays money and seller broker delivers securities to the CC/CH on a

predefined day. This process is called as pay in, after pay in securities are given to the buyer

brokers and money is given to seller brokers by the CC/CH, this process is called as pay out.

This process of pay in & payout is called settlement.

Initially the trading cycle was of one fortnight, which was reduced to one week. The

transactions entered during this period, of a fortnight or one week, were used to be settled either

by payment for purchase or by delivery of shares certificates sold on notified days one fortnight

or one week of expiry of the trading. The settlement schedules are made known to the members

of the exchange in advance.

The weekly settlement period was reduced by daily settlement popularly known as rolling

settlement, in which each day is separate trading day. With effect from December 2001, t+%

rolling settlement cycle was introduced for all equities where T is the trading day and pay in &

pay out for the settlement was done on the 5th business day after the trade day.

8/4/2019 DBFS Project

http://slidepdf.com/reader/full/dbfs-project 46/65

Page 46KLES¶S INSTITUTE OF MANAGAMENT STUDIES AND RESEARCH

6. GOLD

Of all the choice of investments available, can this yellow metal take pride of the place as a

financial investment alternative option? Opinion on the subject of gold is divided, on several

issues ± are the yields from an investment in gold positive? Are its uses productive? Is the strain