Embed Size (px)

Citation preview

David T. DootSecretary

April 3, 2015

VIA ELECTRONIC MAIL

TO: MEMBERS AND ALTERNATES OF THE NEPOOL PARTICIPANTS COMMITTEE

RE: Supplemental Notice of April 10, 2015 NEPOOL Participants Committee Meeting

Pursuant to Section 6.6 of the Second Restated New England Power Pool Agreement,supplemental notice is hereby given that a meeting of the NEPOOL Participants Committee willbe held on Friday, April 10, 2015, at 10:00 a.m. at The Seaport Boston Hotel, 1 SeaportLane, Boston, MA. The Participants Committee meeting will be held in Seaport Ballroom (inthe Seaport Hotel) for the purposes set forth on the attached agenda and posted with the meetingmaterials at http://nepool.com/NPC_2015.php. For your information, this meeting is recorded,as are all the NEPOOL Participants Committee meetings.

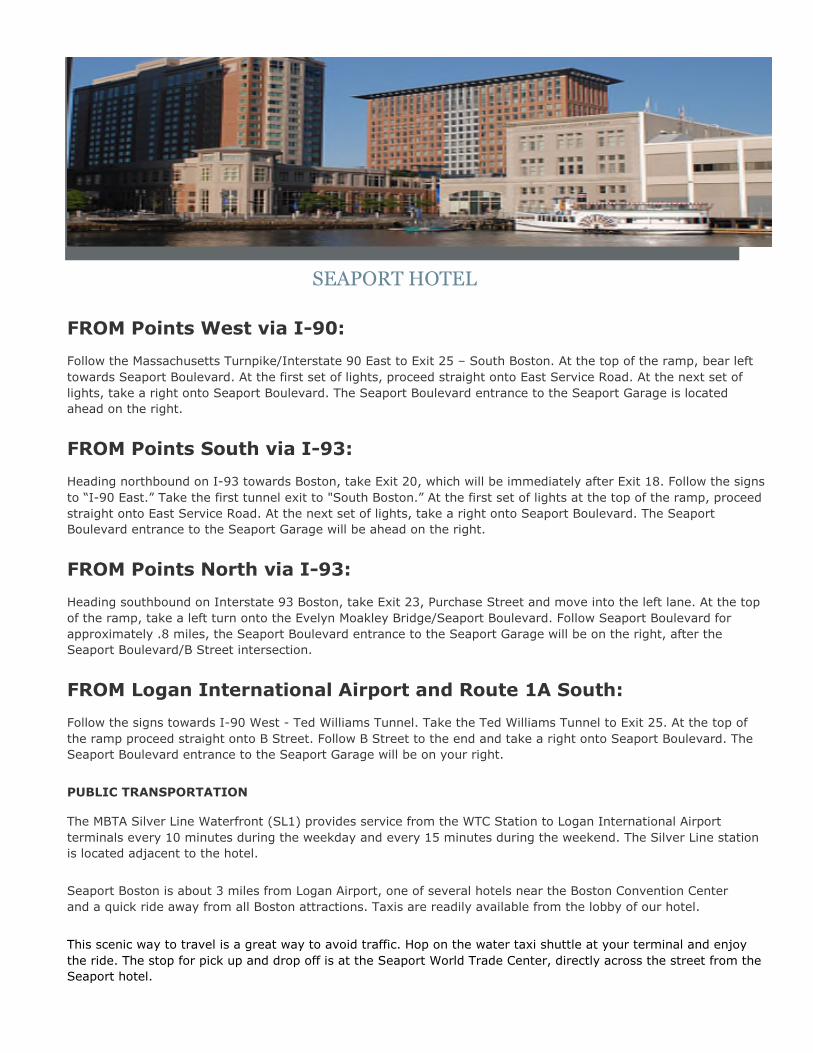

Directions to the Seaport Hotel are included with this notice. We hope you have all madeovernight reservations as needed, since rooms are scarce and at a premium. If you still need areservation, please contact the Seaport directly (617-385-4000) to see if they have any roomsavailable outside of the NEPOOL block. Cindy Jacobs, NEPOOL Administrator,([email protected]/860-275-0246) will also try to assist if you are not successful withSeaport.

Looking ahead, please mark your calendars for the 14th Annual NEPOOL ParticipantsCommittee Summer Meeting, which will be held at The Stoweflake Resort & ConferenceCenter, Stowe, VT, on June 23-25, 2015 (http://www.stoweflake.com/). As in the past, there willbe a welcome reception with the ISO Board and New England Regulators on Monday, June 22for those who are able to arrive early. Detailed information regarding the ParticipantsCommittee Summer Meeting will be provided in future notices, including information regarding the reservations block, once the block is open.

Respectfully yours,

/s/David T. Doot, Secretary

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING

FINAL AGENDA

1. To approve the preliminary minutes of the Participants Committee meeting held onMarch 6, 2015. The draft minutes of the March 6 meeting marked to show changes fromthe draft circulated with the initial notice are included with this supplemental notice andposted with the meeting materials.

2. To adopt and approve all actions recommended by the Technical Committees set forth onthe Consent Agenda included with this supplemental notice.

3. To receive an ISO Chief Executive Officer Report.

4. To receive an ISO Chief Operating Officer Report. Please note that the COO report thismonth will also include discussion of the 2014/15 Winter Program experiences.

5. To consider, and take action, as appropriate, on revisions to the ISO Financial AssurancePolicy related to Foreign Entities’ ability to use BlackRock accounts as a collateral andconforming revisions to the ISO Billing Policy, as recommended by the Budget &Finance Subcommittee. Background materials and a draft resolution are included withthis supplemental notice and posted with the meeting materials.

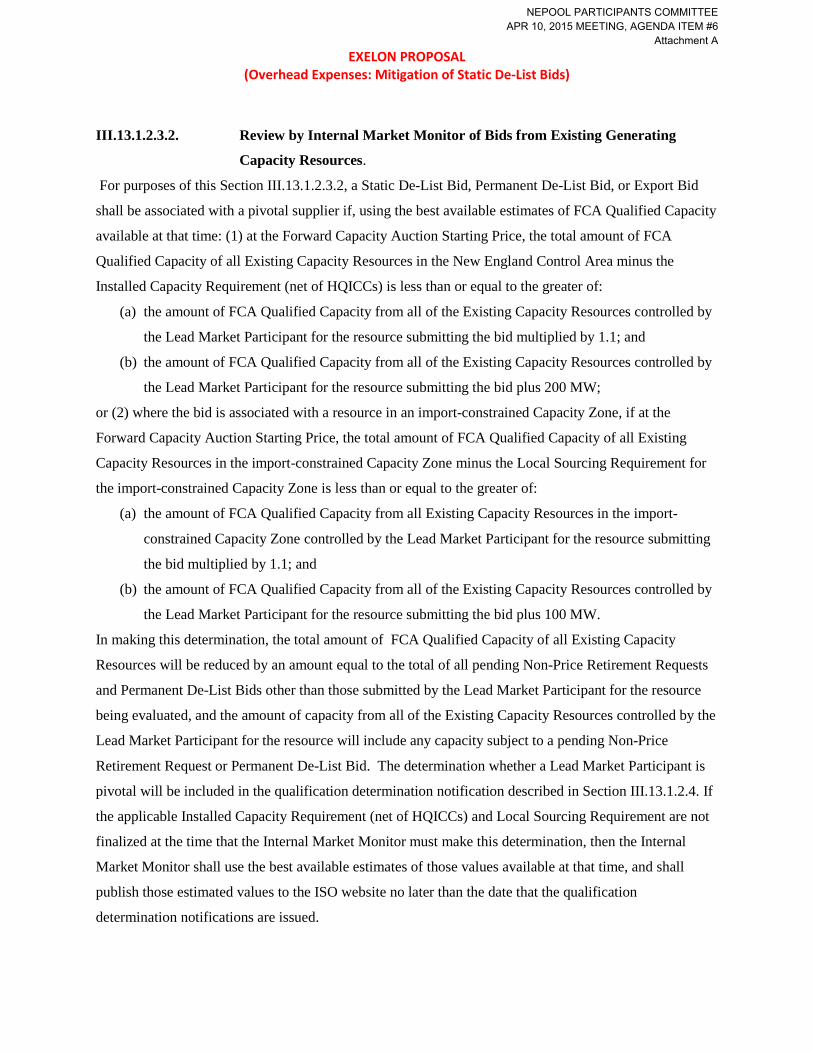

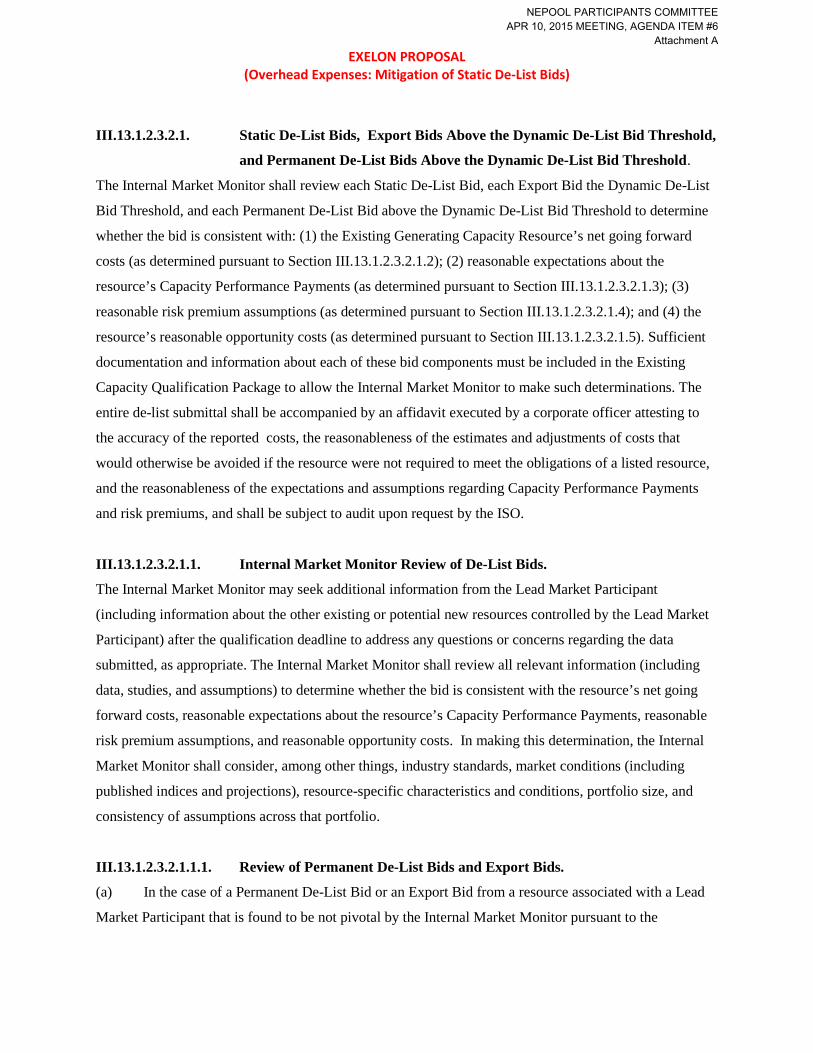

6. To consider, and take action as appropriate, on revisions to Market Rule 1 to allowoverhead/centralized costs to be included, up to a specified default rate, in Static De-ListBids submitted in the FCM, as proposed by Exelon Generation Company, LLC.Background materials and a draft resolution are included with this supplemental noticeand posted with the meeting materials.

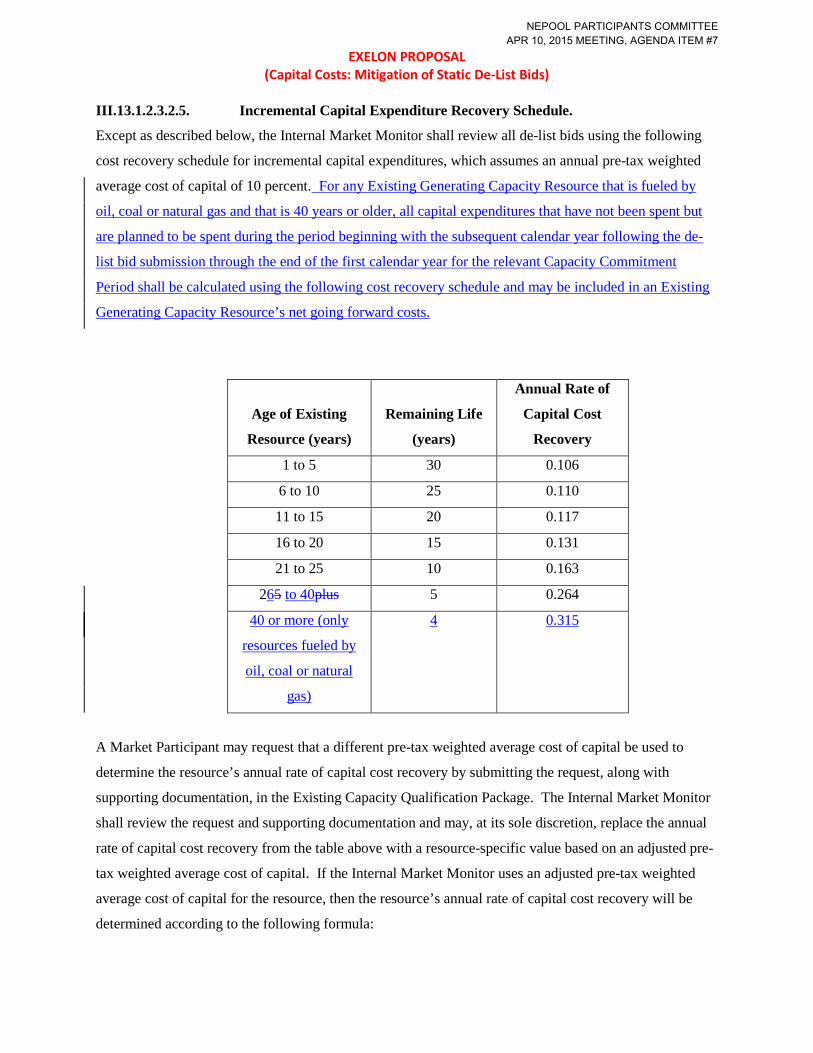

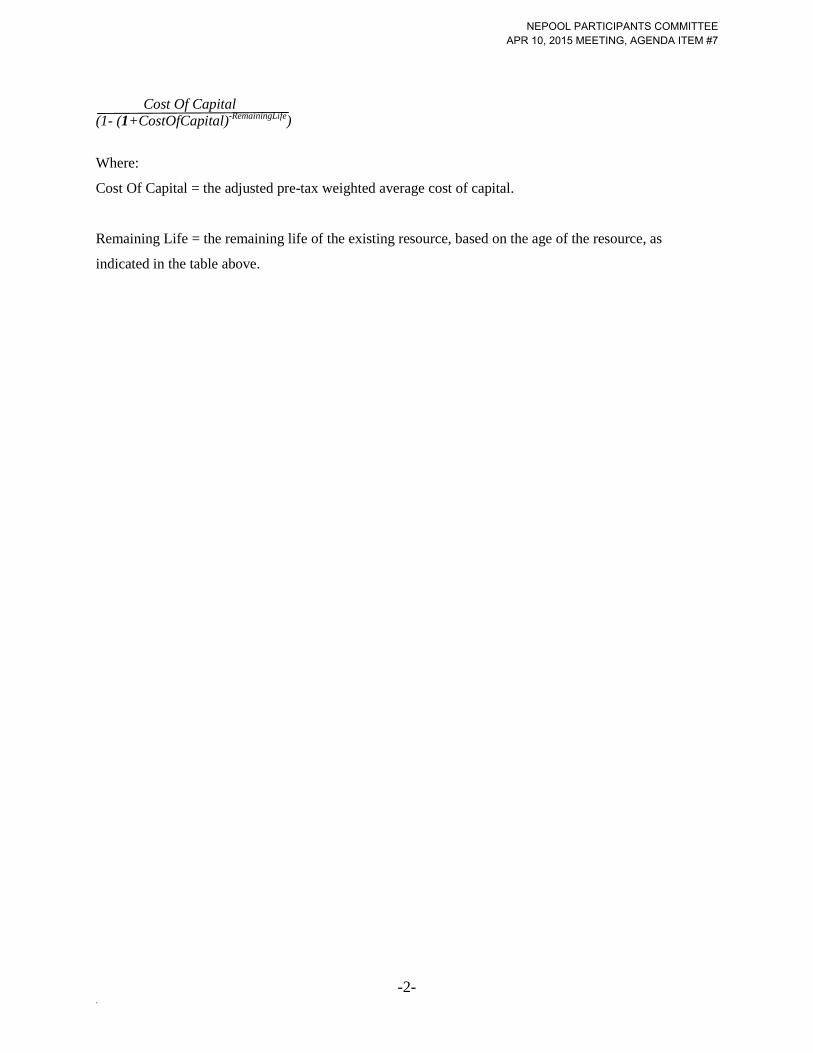

7. To consider, and take action as appropriate, on revisions to Market Rule 1 to allow thefull inclusion of capital costs in FCM de-list bids, as proposed by Exelon GenerationCompany, LLC. Background materials and a draft resolution are included with thissupplemental notice and posted with the meeting materials.

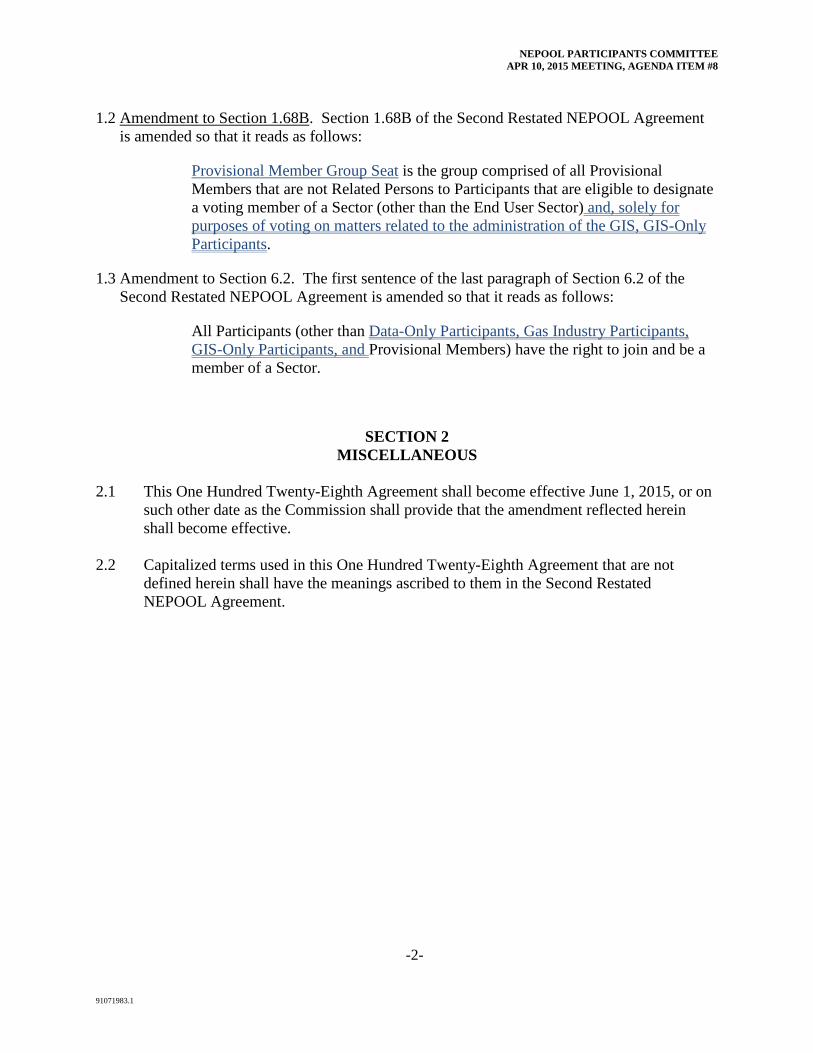

8. To consider and take action, as appropriate, on proposed amendments to the NEPOOLAgreement to create a GIS-Only Participant status, as recommended by the MembershipSubcommittee. Background materials and a draft resolution to approve the amendmentsfor balloting are included with this supplemental notice and posted with the meetingmaterials.

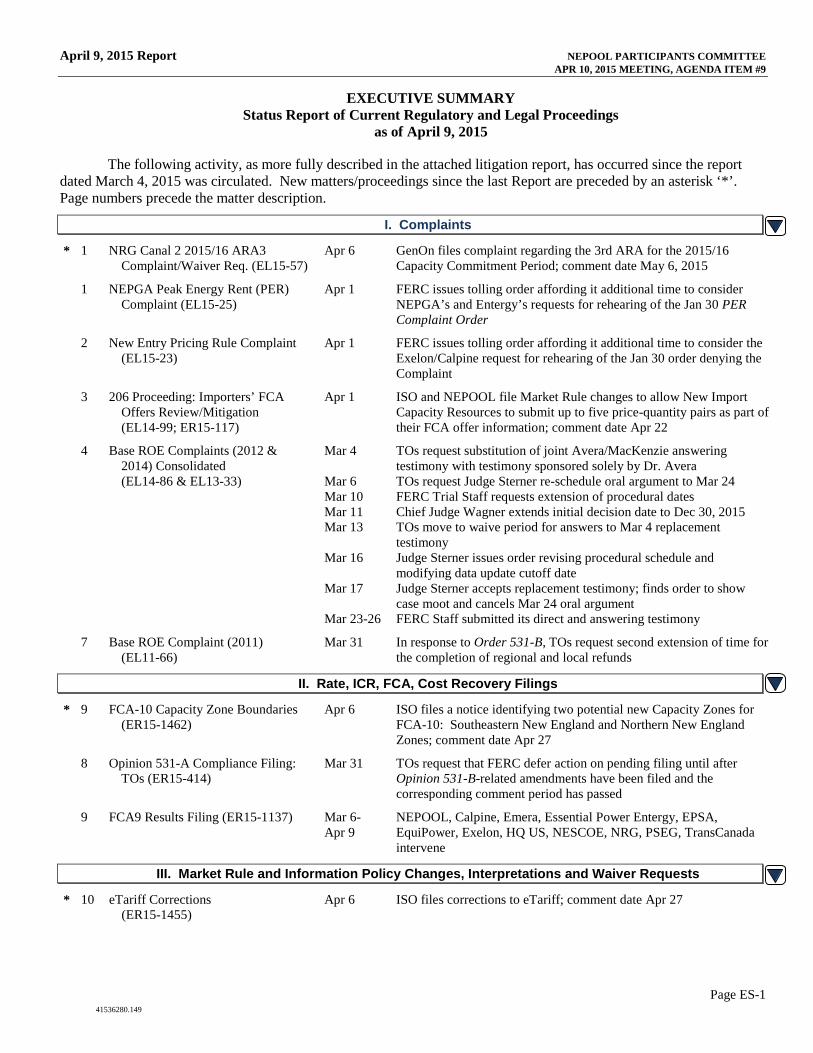

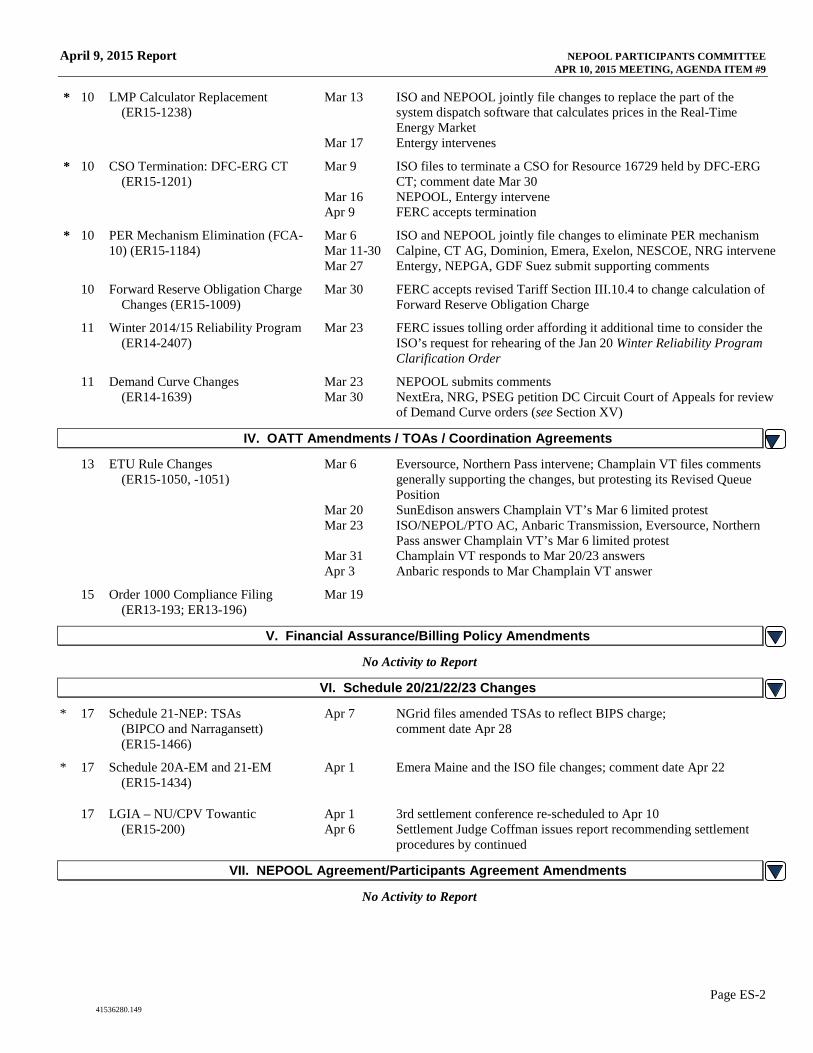

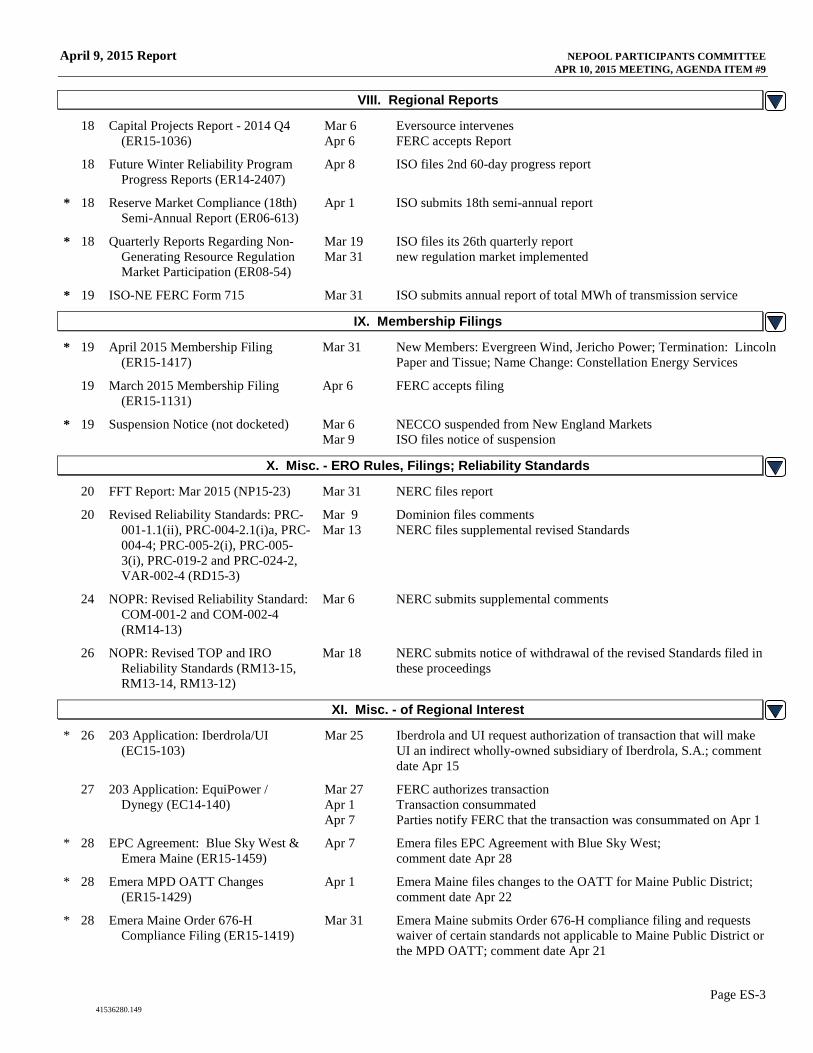

9. To receive a report on current matters relating to regional wholesale power andtransmission arrangements that are pending before the regulators and the courts. Thelitigation report will be circulated in advance of the meeting.

10. To receive reports from committees and subcommittees.

11. To transact such other business as may properly come before the meeting.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3415

PRELIMINARY

A meeting of the NEPOOL Participants Committee was held beginning at 10:00 a.m. on

Friday, March 6, 2015 at The Colonnade Hotel, Boston, Massachusetts, pursuant to notice duly

given. A quorum determined in accordance with the Second Restated NEPOOL Agreement was

present and acting throughout the meeting. Attachment 1 identifies the members, alternates and

temporary alternates attending the meeting.

Mr. Joel Gordon, Chairman, presided and Mr. David Doot, Secretary, recorded. Mr.

Gordon welcomed the members, alternates and guests who were present.

ACKNOWLEDGMENT IN MEMORIAM -- ALLISON SMITH

Mr. Gordon began the meeting acknowledging Ms. Allison Smith, most recently of

NESCOE, who was recently killed in a car accident. He quoted the following passage from

Maya Angelou: “I've learned that people will forget what you said, people will forget what you

did, but people will never forget how you made them feel.” He recalled Allison’s magical ability,

in every interaction, on any issue, to leave her colleagues with a smile and a warm feeling. Mr.

Gordon requested that, in Allison’s memory, the minutes reflect Allison’s presence at the March

6 Participants Committee meeting.

Mr. Doot then read the following resolution of appreciation honoring Allison’s

contributions:

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3416

APPRECIATION IN MEMORIAMOF ALLISON SMITH

WHEREAS, we pause to express our gratitude for the pleasure and opportunityto work with Ms. Allison Smith, who shared with us her passion for life, for friends,for the industry and for the environment;

WHEREAS, Allison always contributed to NEPOOL discussions withhumility, grace, great thought, self-confidence, a sincere effort to understand the diverseinterests of the region, and ever-increasing demonstration of her growth in thatunderstanding, a genuine respect for those around the table, and a refreshing sense ofhumor; and

WHEREAS, Allison leaves with us her legacy of caring, for which she will alwaysbe remembered and we will always be grateful.

NOW, THEREFORE, the Participants Committee of the New England PowerPool, on behalf of the NEPOOL Participants, hereby expresses sincere gratitude toAllison for her years of participation in NEPOOL and for her warm, enthusiastic andvisible efforts to make our region a more welcoming, happier and better place. She willbe missed.

The motion of appreciation was duly made, seconded and by acclimation unanimously

approved by the Committee. Mr. Doot stated that originals of the resolution would be sent to

Allison’s parents and her spouse following the meeting.

APPROVAL OF MINUTES OF FEBRUARY 6, 2015

Mr. Gordon referred the Committee to the preliminary minutes of the February 6, 2015

meeting that were circulated and posted in advance of the meeting. Following motion duly made

and seconded, the preliminary minutes of the February 6, 2015 meeting were unanimously

approved without change.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3417

CONSENT AGENDA

Mr. Gordon referred the Committee to the Consent Agenda circulated in advance of the

meeting. A motion was duly made and seconded to approve the Consent Agenda, with Item No.

3 (support for revisions to Market Rule 1 to eliminate the Peak Energy Rent (PER) mechanism

for the June 1, 2019 – May 31, 2020 Capacity Commitment Period (CCP-10) and beyond)

removed for discussion later in the meeting. That motion was unanimously approved without

comment.

REPORT OF THE ISO CHIEF EXECUTIVE OFFICER

Mr. Gordon van Welie, ISO Chief Executive Officer, referred the Committee to the

summary of the February 5 and February 19, 2015 ISO Board and Board Committee meetings,

which had been circulated and posted in advance of the meeting. There were no questions or

comments on that report.

Mr. van Welie then reported that the ISO planned to release in April a document

exploring options for addressing demand response (DR) depending on the outcome of the

Supreme Court action on the Order 745 appeals. He stressed that the document would not be a

contingency plan but, rather, a document to identify the different possibilities for discussions

with the ISO Board and NEPOOL Markets Committee. Following those discussions, the ISO

was seeking to have contingency plans in place prior to final Supreme Court action. In response

to a question, Mr. van Welie confirmed that the ISO was exploring the implications to both the

energy and capacity markets given the possibility for either a narrow or broader interpretation by

the Courts and the FERC on the DR issues.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3418

REPORT OF THE ISO CHIEF OPERATING OFFICER

Dr. Vamsi Chadalavada, ISO Chief Operating Officer, reviewed highlights from the

March COO report, which had been circulated and posted in advance of the meeting. Focusing

on report highlights, which he noted reflected experiences through February 25 (except Real-

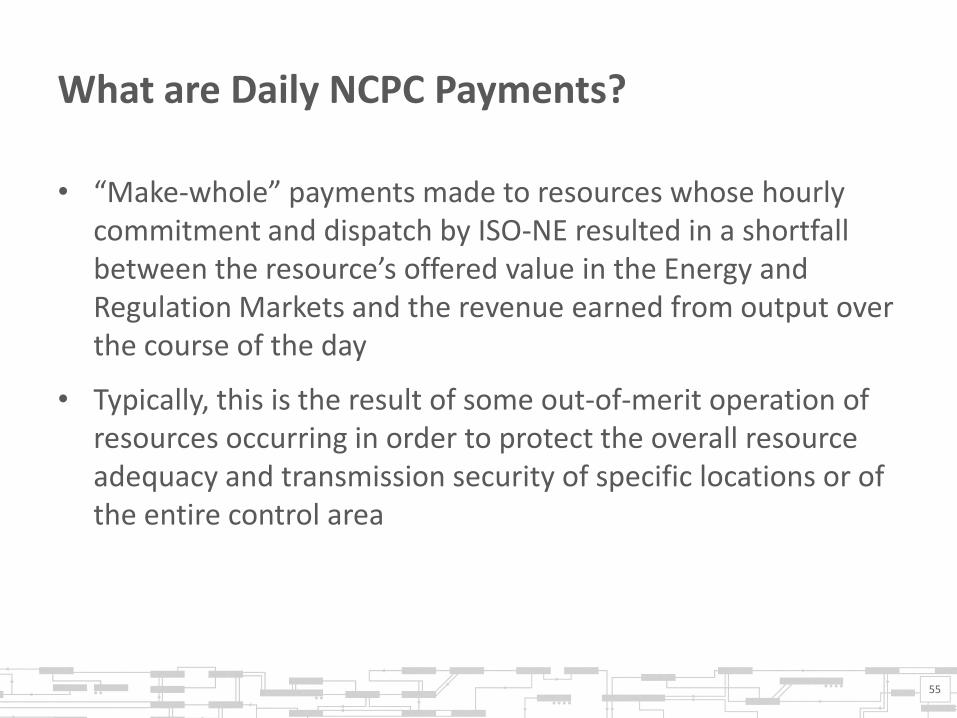

Time Net Commitment Period Compensation (NCPC), which was only through February 23), he

stated that in February: (i) Energy Market value was $1.2 billion, up $339,000 from the prior

month, but down $492,000 from February 2014; (ii) natural gas prices were 74% higher than

January 2015 average values; (iii) Real-Time Hub locational marginal prices (LMPs) on average

were 89% higher than January 2015 LMPs; (iv) average daily (peak hour) Day-Ahead cleared

physical Energy, as a percentage of forecasted load, was 99.2% in February 2015, down from

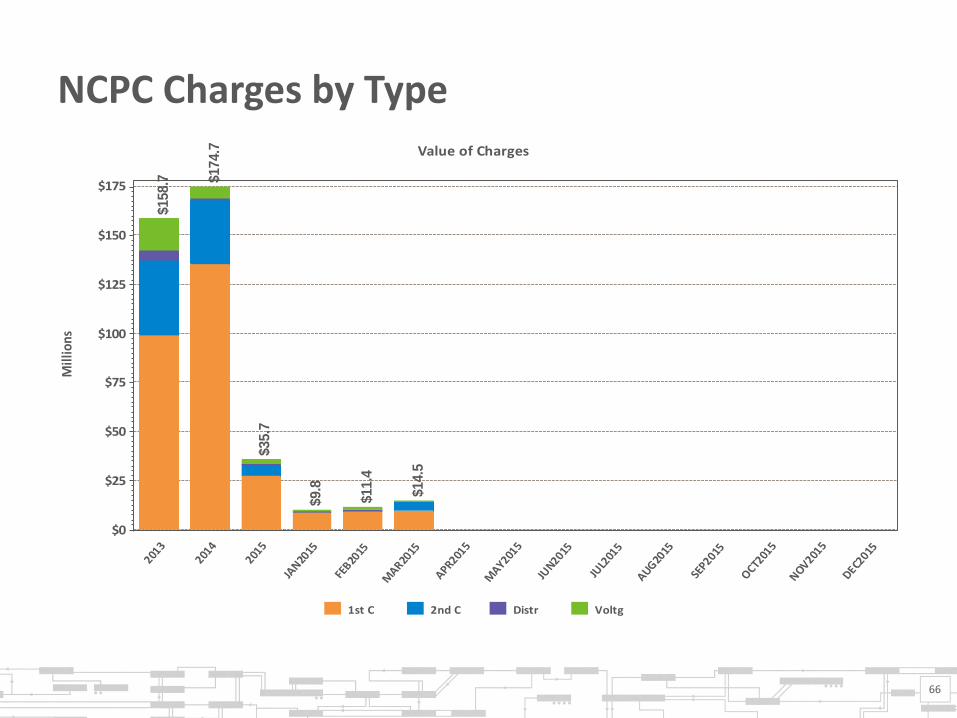

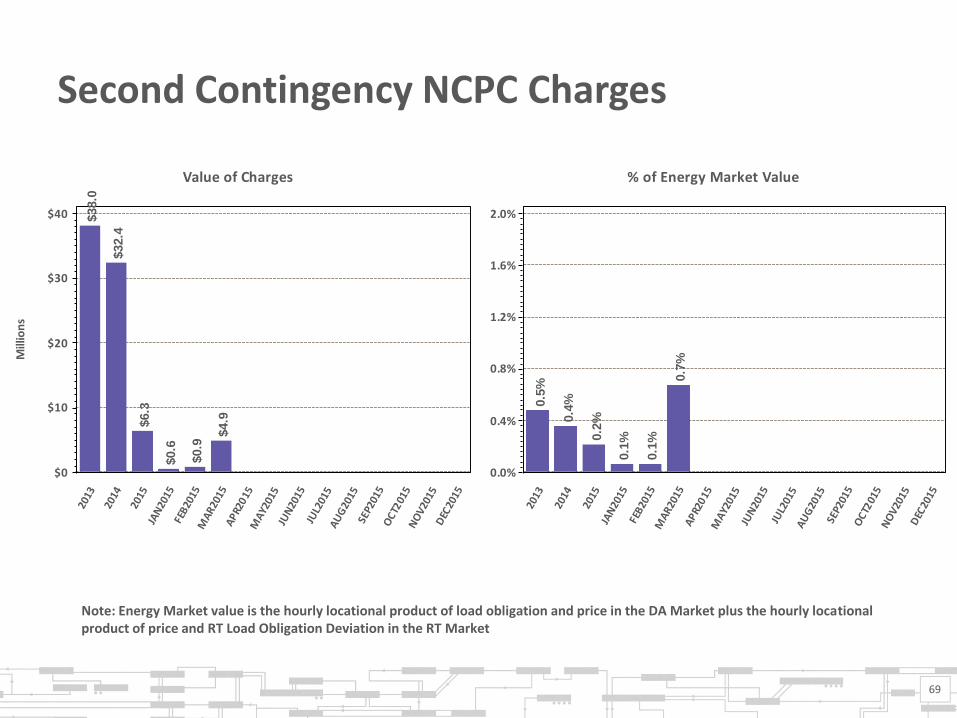

99.8% in January 2015; (v) daily NCPC through February 23 totaled $8.9 million, up $946,000

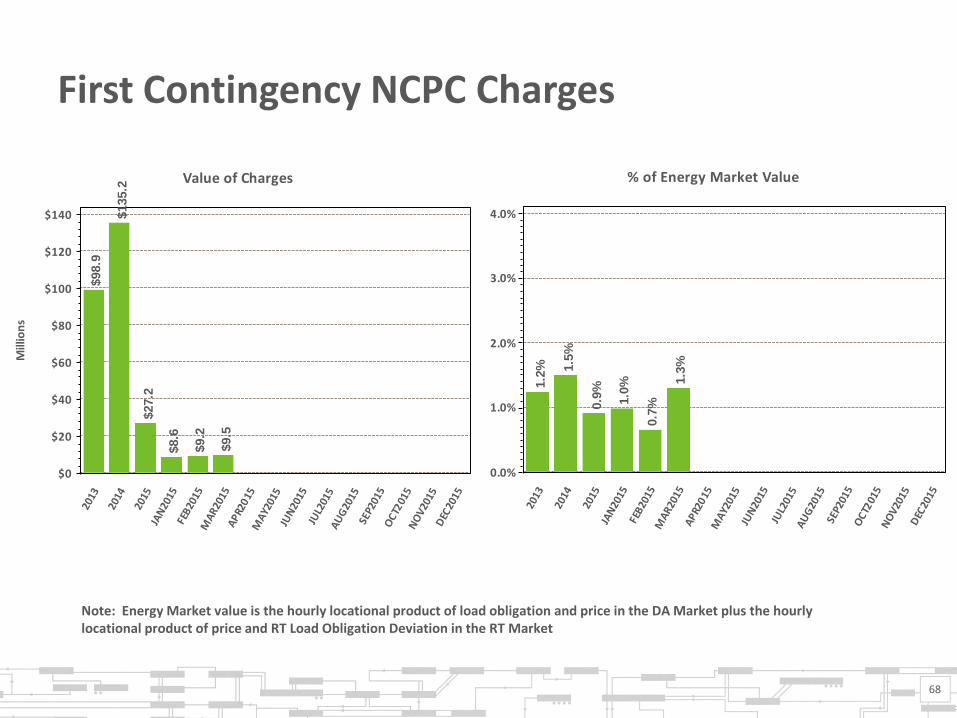

from January; (vi) first contingency payments totaled $7 million, up $300,000 from January’s;

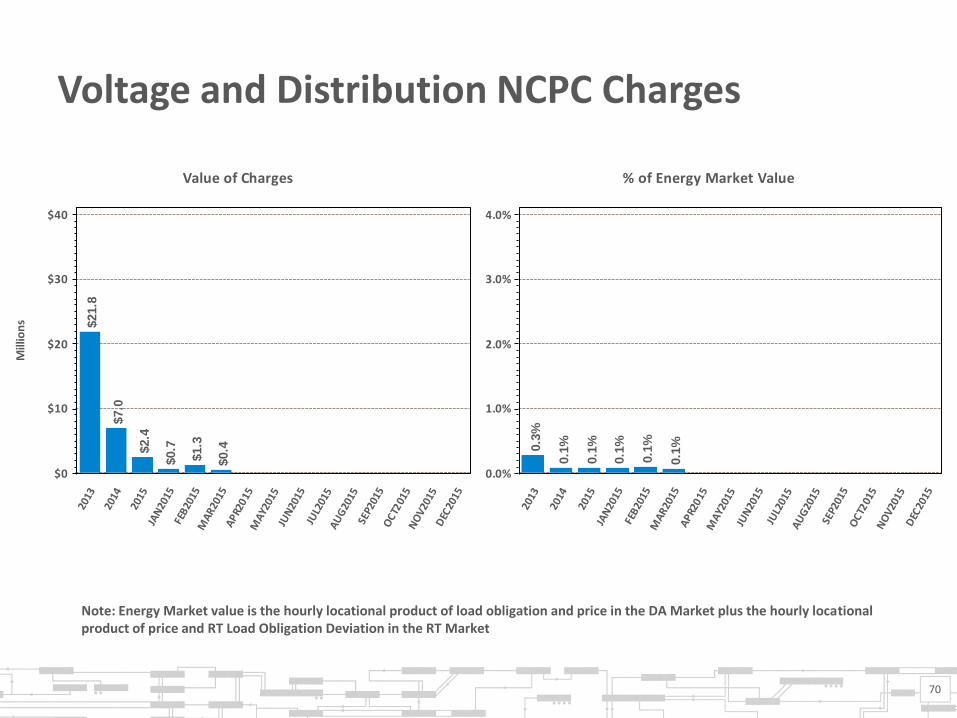

(vii) second contingency payments totaled $865,000, up from $559,000 in January; (viii) voltage

support payments totaled $928,000, up $241,000 from January; and (ix) distribution payments

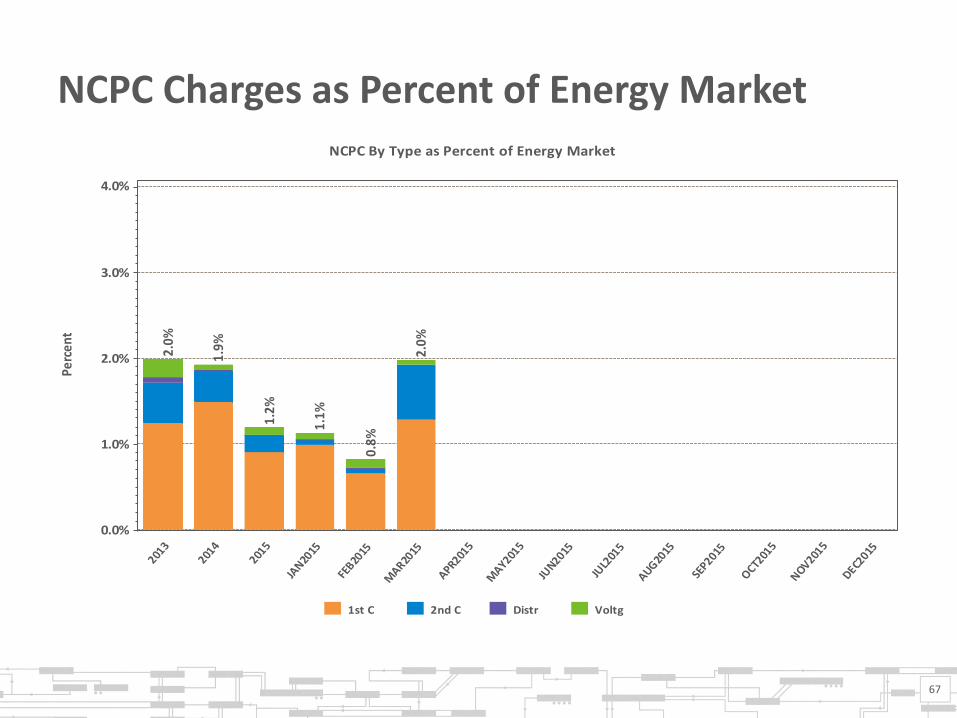

totaled $21,000; and (x) NCPC payments were 0.7% of the total Energy Market value.

Dr. Chadalavada reviewed the amount of Day-Ahead cleared physical energy, which had

recently been between 99.5 - 99.8%, was fairly remarkable, and had resulted in an almost

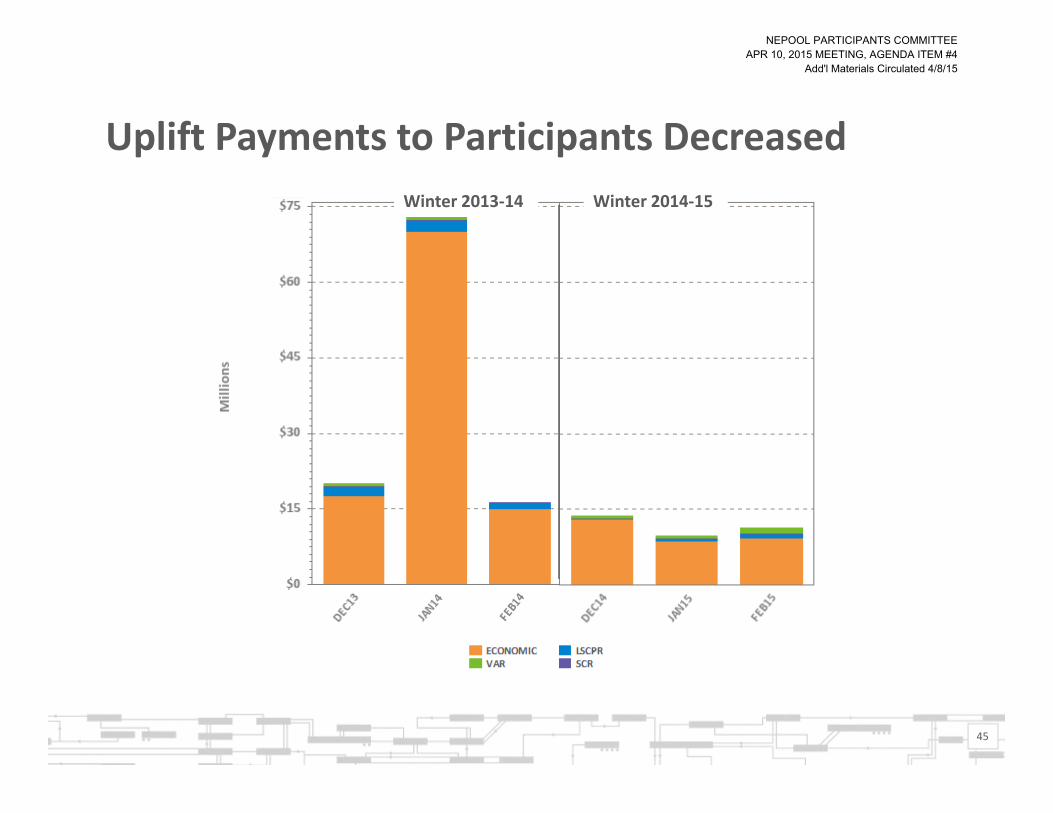

complete elimination of supplemental commitments. He reported for 2014/15 Winter about $32

million of uplift, down sharply from the almost $110 million for Winter 2013/14, which he

attributed to a more balanced optimization of grid operations, price formation improvements, and

improved Control Room judgments. He added that similar evaluations would be prepared for the

spring, summer and fall periods, with some variations expected in the spring and fall due to

maintenance outages. He noted that, in general, System performance during the peaks was good.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3419

Turning to NCPC, Dr. Chadalavada said that the calculation of, and compensation for,

NCPC had been substantially changed with the implementation of hourly offers. The ISO still

needed to analyze the impact of the NCPC design and its contribution to commitment costs. By

way of example, he stated the NCPC design changes explained a portion of the $7 million first

contingency payments in the prior month. He noted that the ISO would report on the

observations, causes and contributions towards the uplift amount at the May or June Participants

or Markets Committee meetings. He stated that almost all second contingency uplift costs were

for NEMA in early February; uplift for voltage were largely in Western Massachusetts; and

NCPC was 0.7% of total Energy Market value.

Dr. Chadalavada reported that the Show-of-Interest (SOI) window for new resource

participation in the tenth Forward Capacity Auction (FCA-10) had closed on March 3, with a

total of 17,000 MW of new resources being proposed, including new generation, new DR and

imports. He compared this interest to the approximately 12,000 MW of new resources that

expressed interest in FCA9. He referred stakeholders to the interconnection queue, which at

least from the generation standpoint, provided additional information.

In response to clarifying questions, Dr. Chadalavada explained the favorably low

Supplemental Commitments by explaining how first contingency uplift was created and other

features of the recently implemented Market Rules. Dr. Chadalavada confirmed that, were there

a sub-hourly settlement (a project included in the 2015 Work Plan), some of the remaining uplift

would also go awayhave been eliminated. Overall, Dr. Chadalavada noted that the region had

experienced a dramatic reduction in uplift costs, with aggregate annual levels dropping over the

past five to ten years from $250-$350 million to $100 million.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3420

With respect to resources in the FCAs, Dr. Chadalavada confirmed that 16.25 MW of

renewable technology resources (RTR) had cleared in FCA9 (against the 200 MW aggregate

exemption). He also noted the breakdown in the report of DR resources that cleared from FCA1

to FCA9.

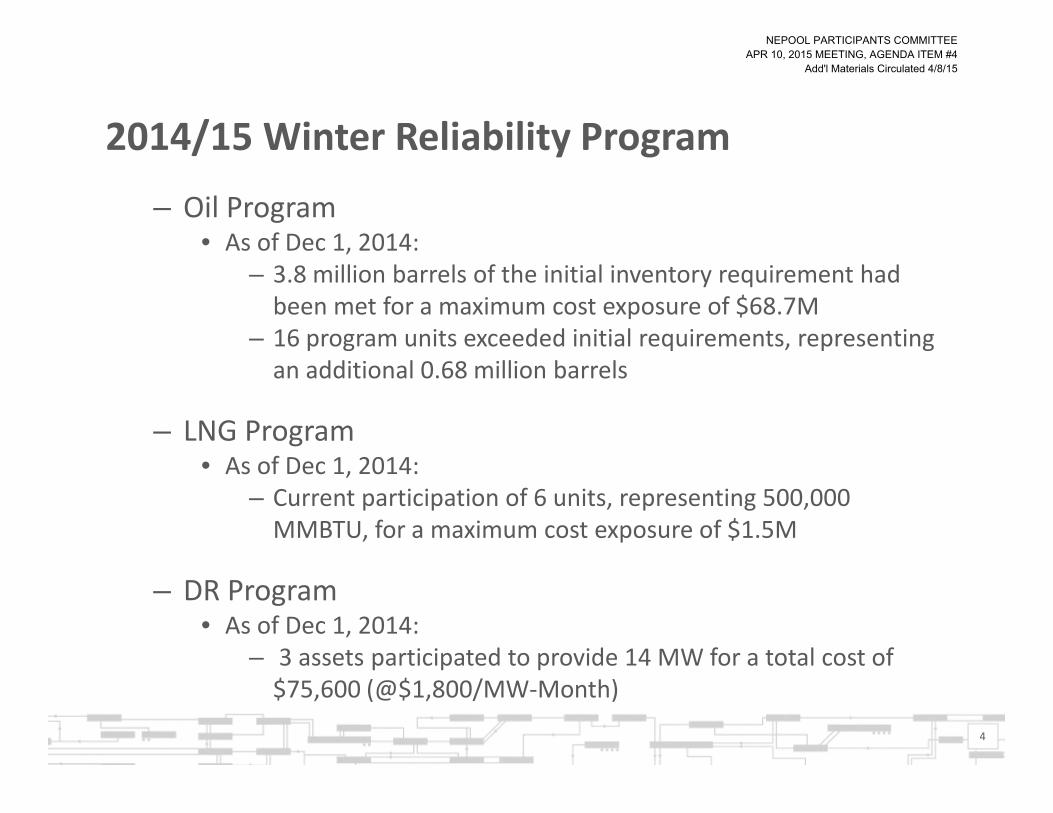

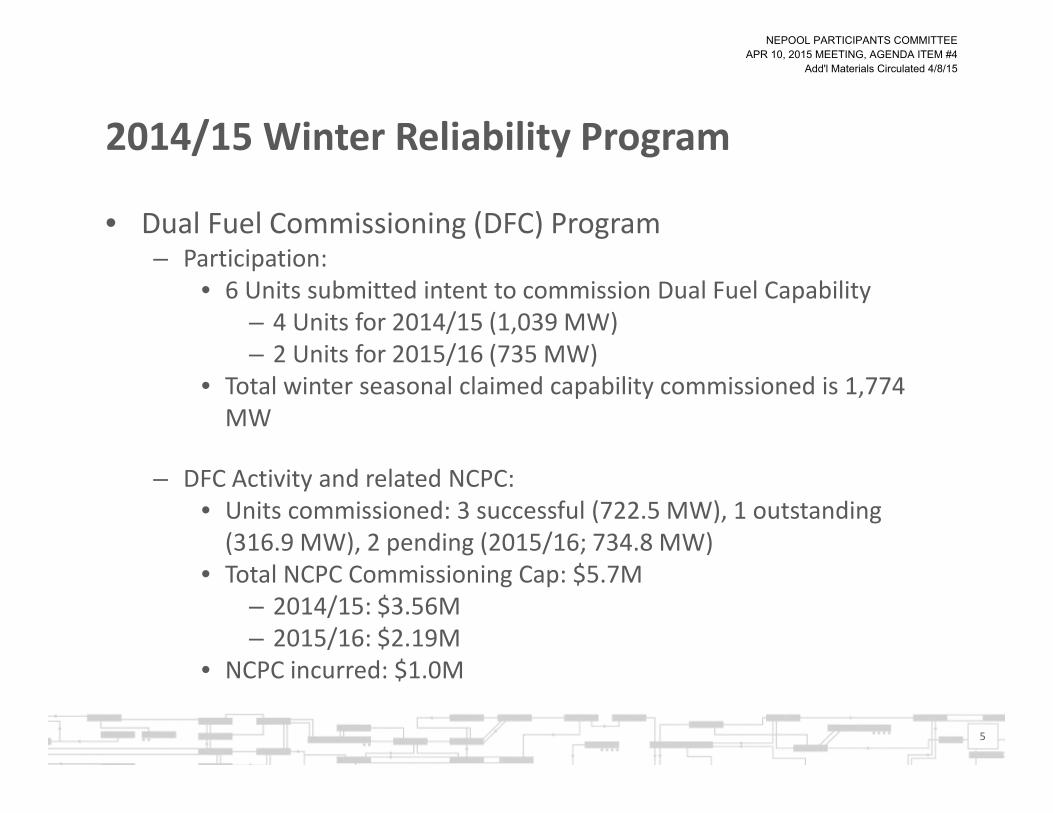

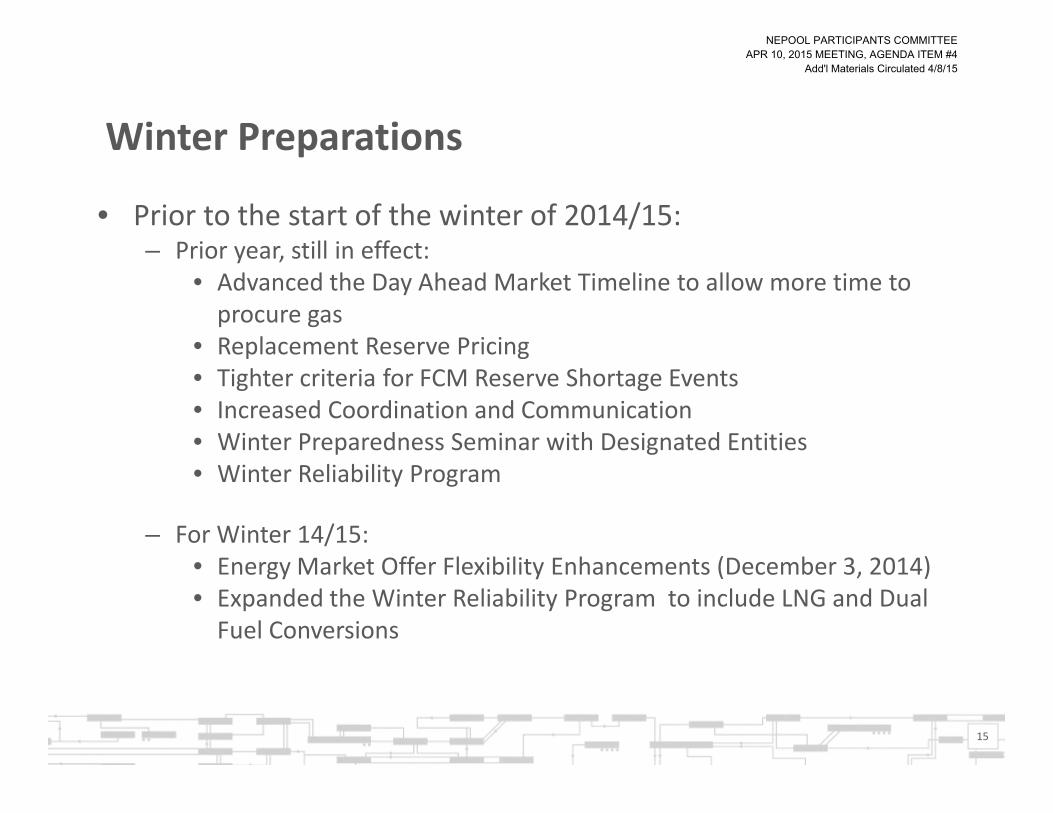

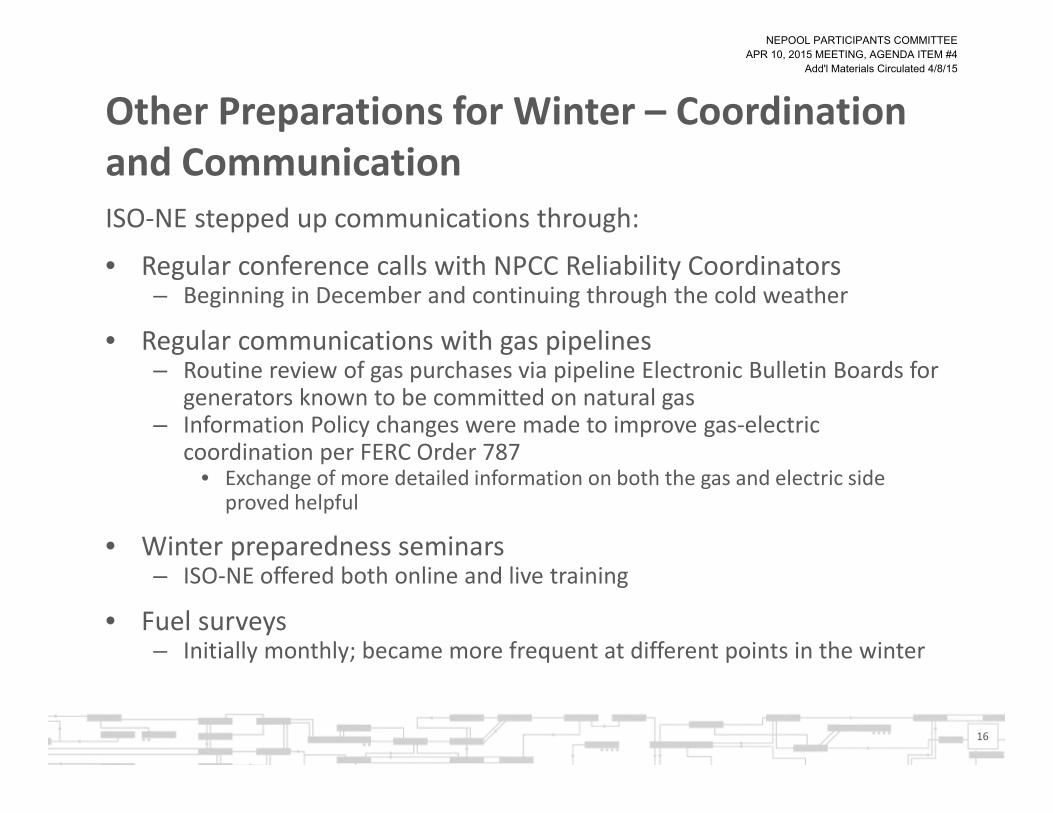

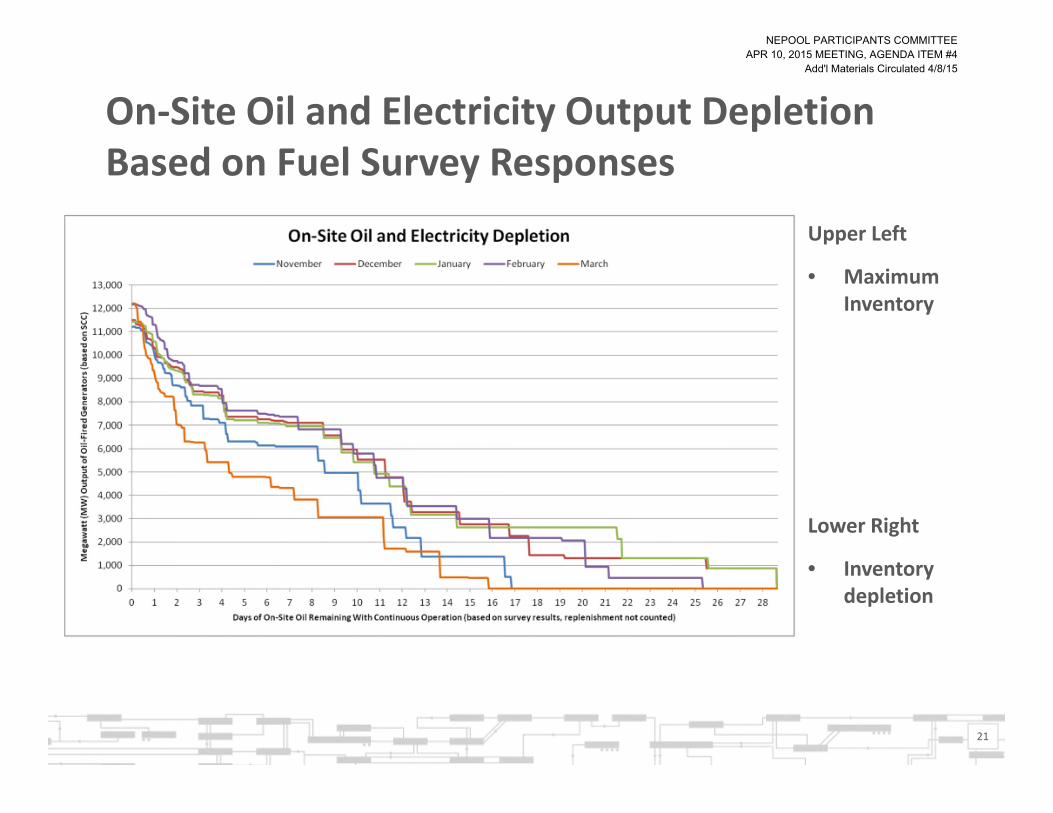

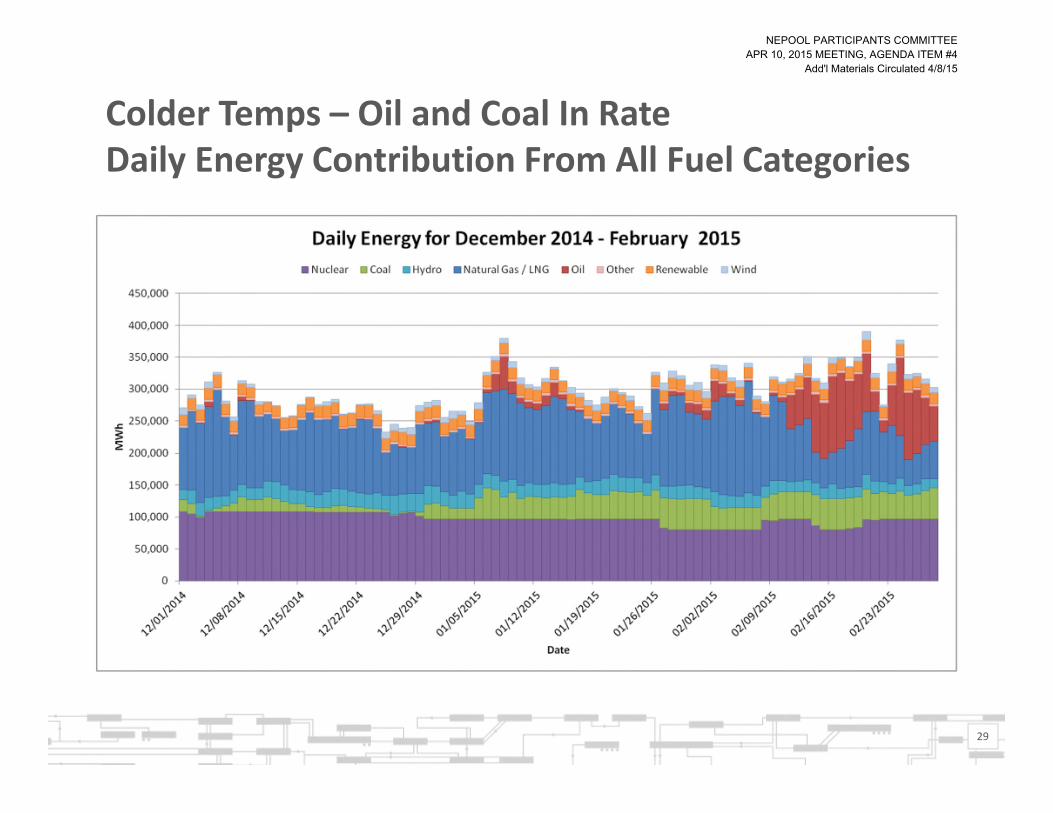

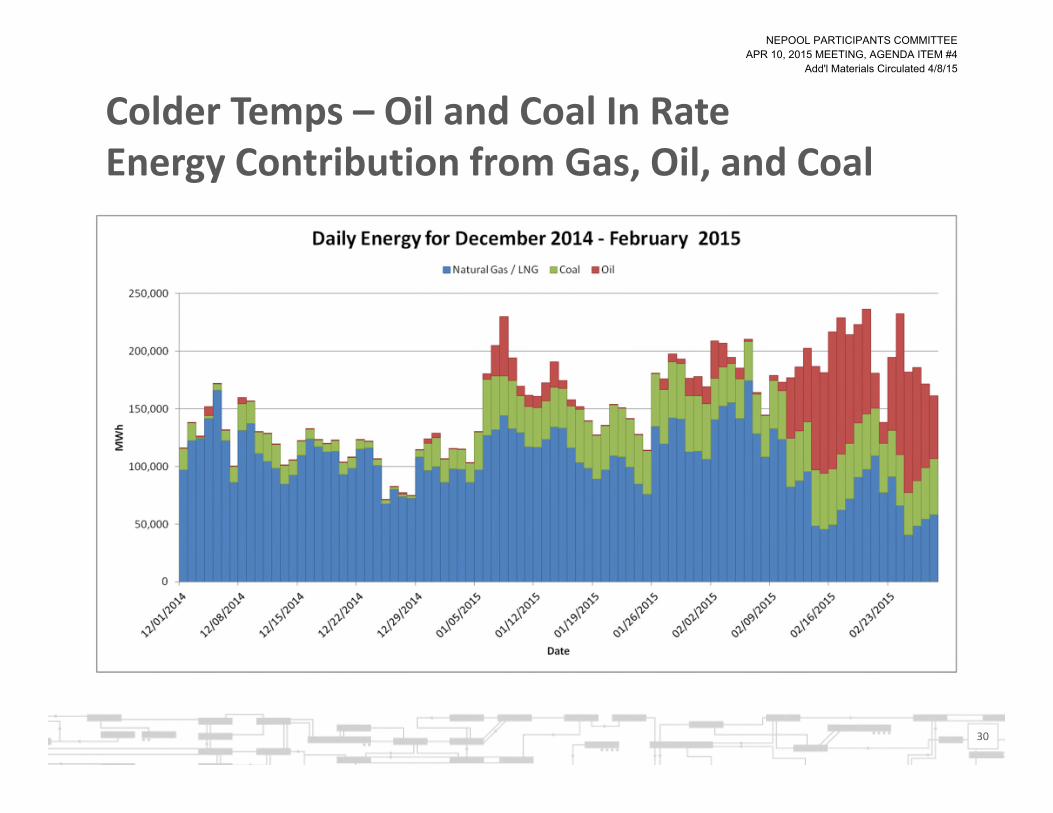

Turning next to the 2014/15 Winter Reliability Program, Dr. Chadalavada updated the

Committee on the Dual-Fuel Commissioning Program, reporting that, as of February 3, three of

four units had successfully commissioned their Dual-Fuel capability during Winter 2014/15.

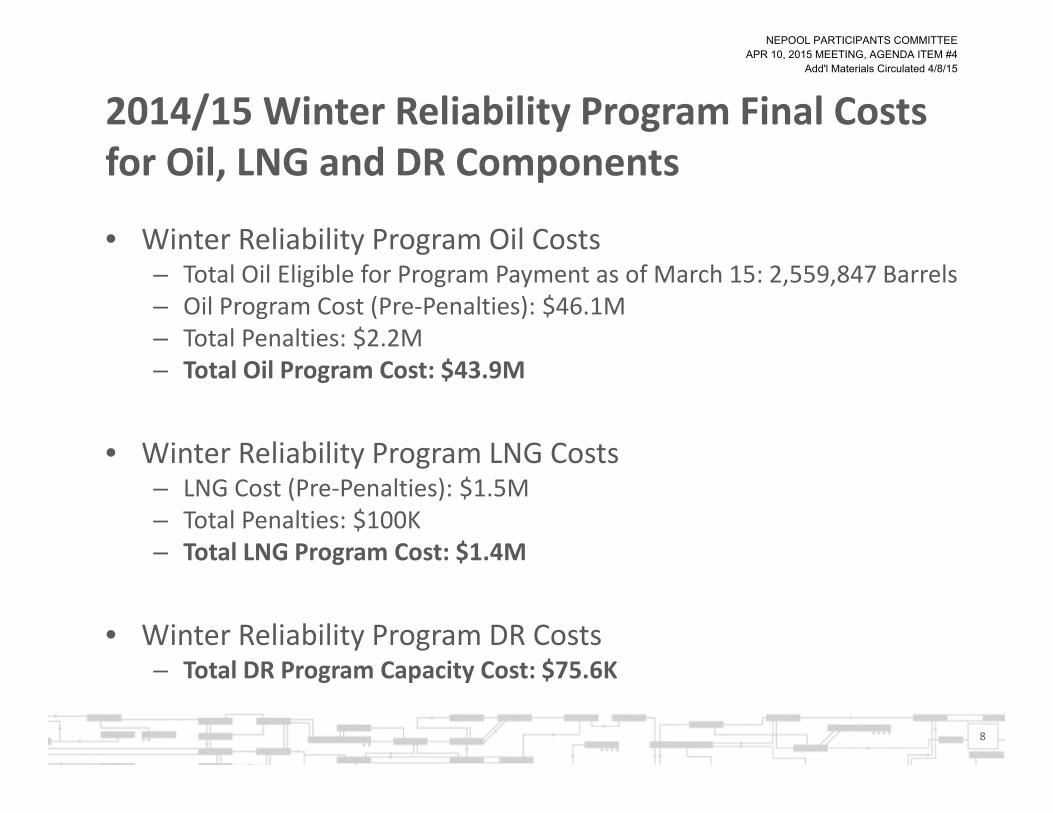

NCPC totaling $1 million had been incurred from November 1 through February 23, leaving

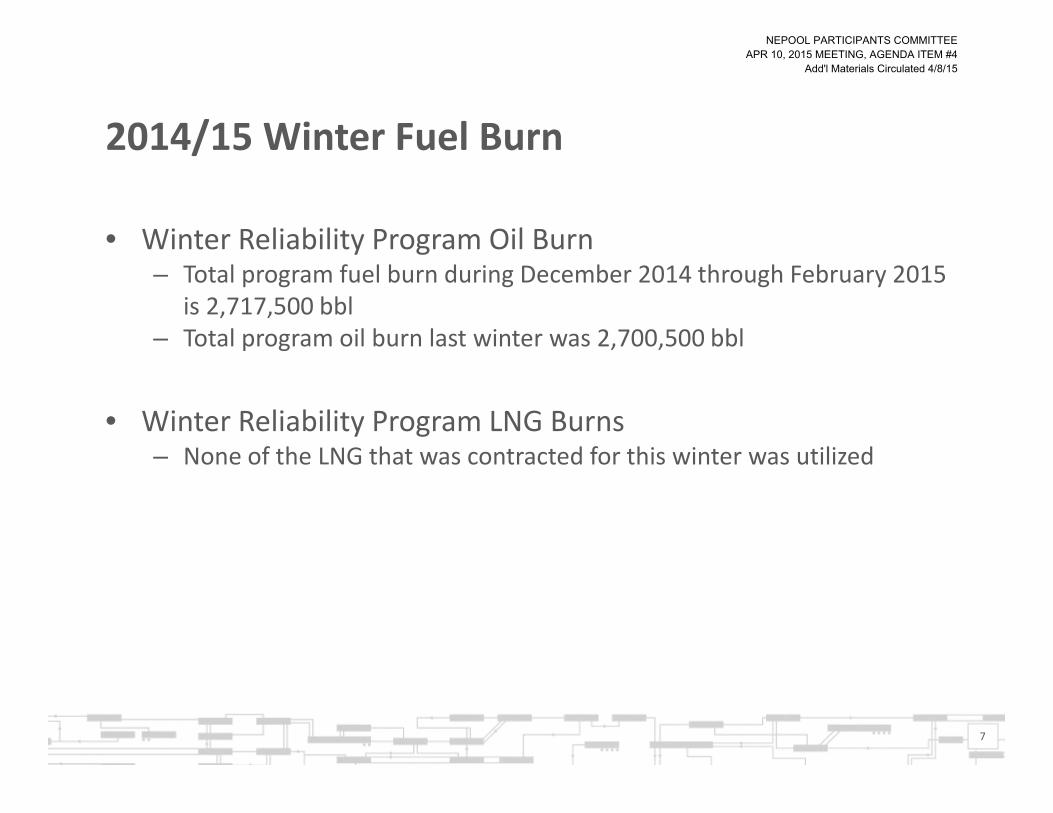

$1.2 million remaining under the 2014/15 Commissioning Cap. He reported the total Program

fuel burn for December 2014 through February 2015 was 2.72 million barrels, roughly the same

amount burned during the same period in 2013/14, but which would have been much higher but

for the unavailability of two large oil generating units that were out-of-service during key

portions of February. Dr. Chadalavada indicated that, except for a few commitments in the

beginning of February for second contingency in NEMA, none of the 2.72 million barrels of oil

were burned out-of-merit. Final information regarding oil replenishments was not yet available

but would be provided in April and sooner if possible.

Operationally, he reported that, notwithstanding the cold temperatures, February was

uneventful, in part because gas units had access to LNG, there was high availability of nuclear,

coal, and oil-fired base load units, imports from Quebec, few contingencies, few forced outages,

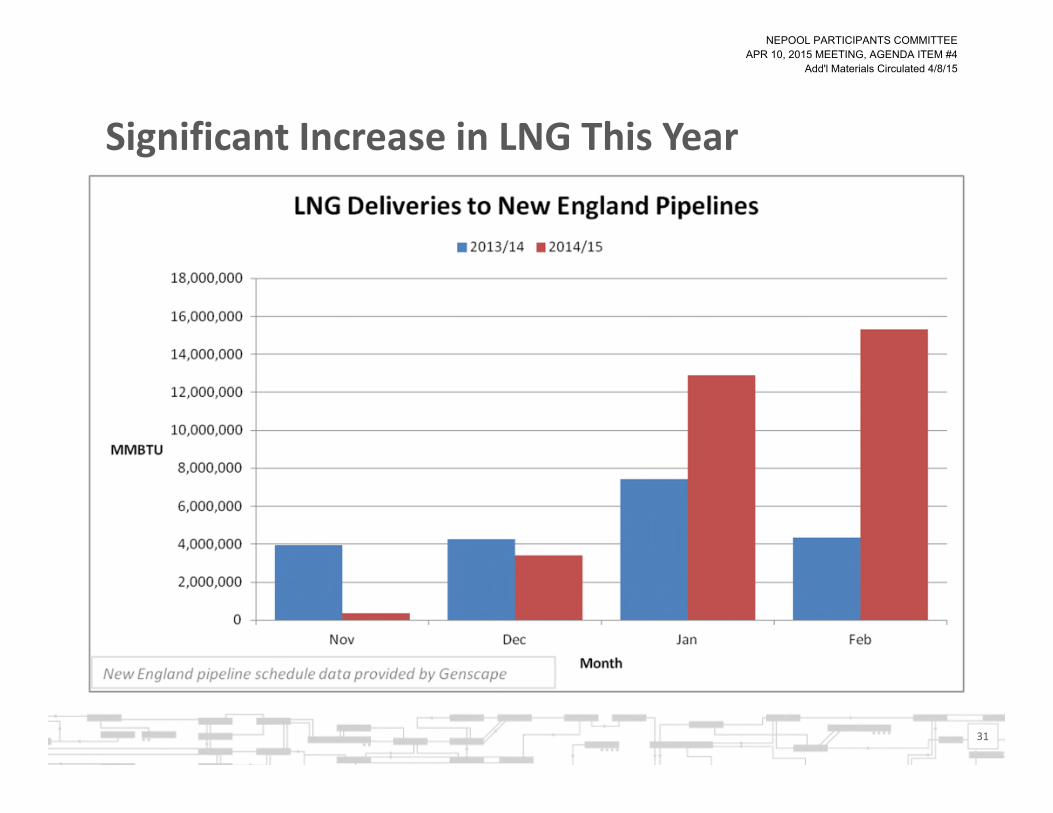

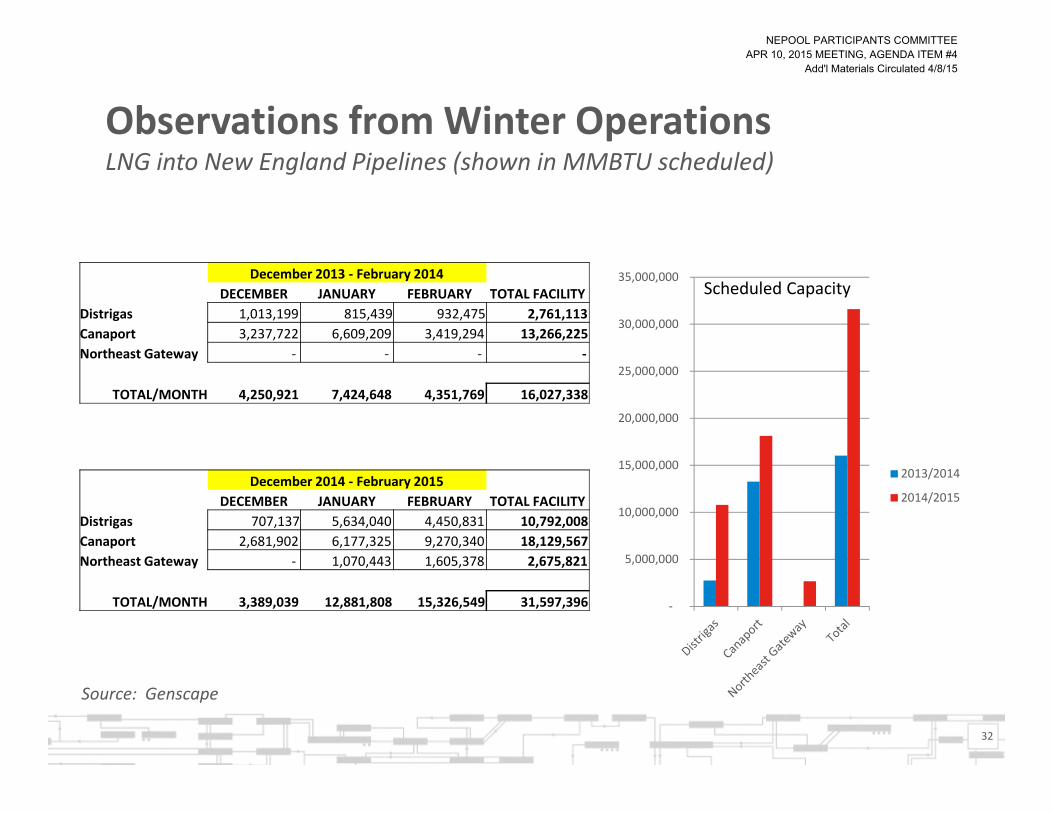

and very nominal load forecast variations. He reported that LNG injections were substantially

lower in February, and three of the four dual-fuel units were running low on oil, but two were

switched to gas as gas prices moderated. He expected the switch from oil to gas to continue

through March.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3421

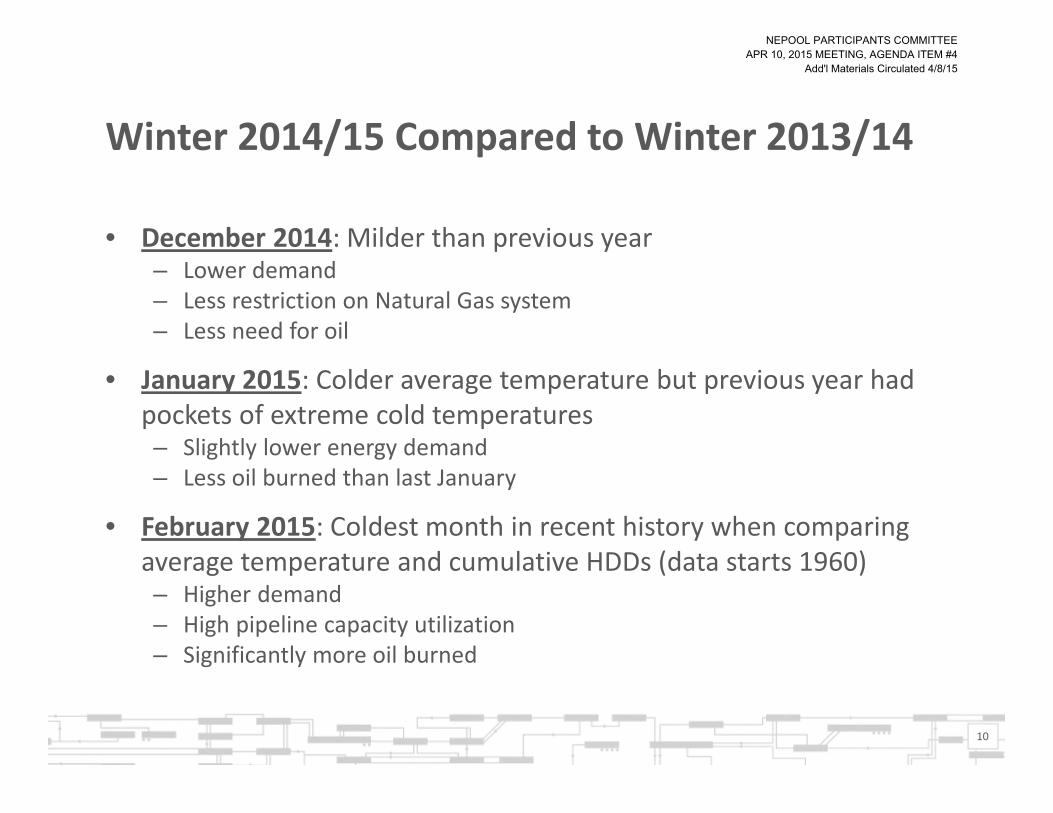

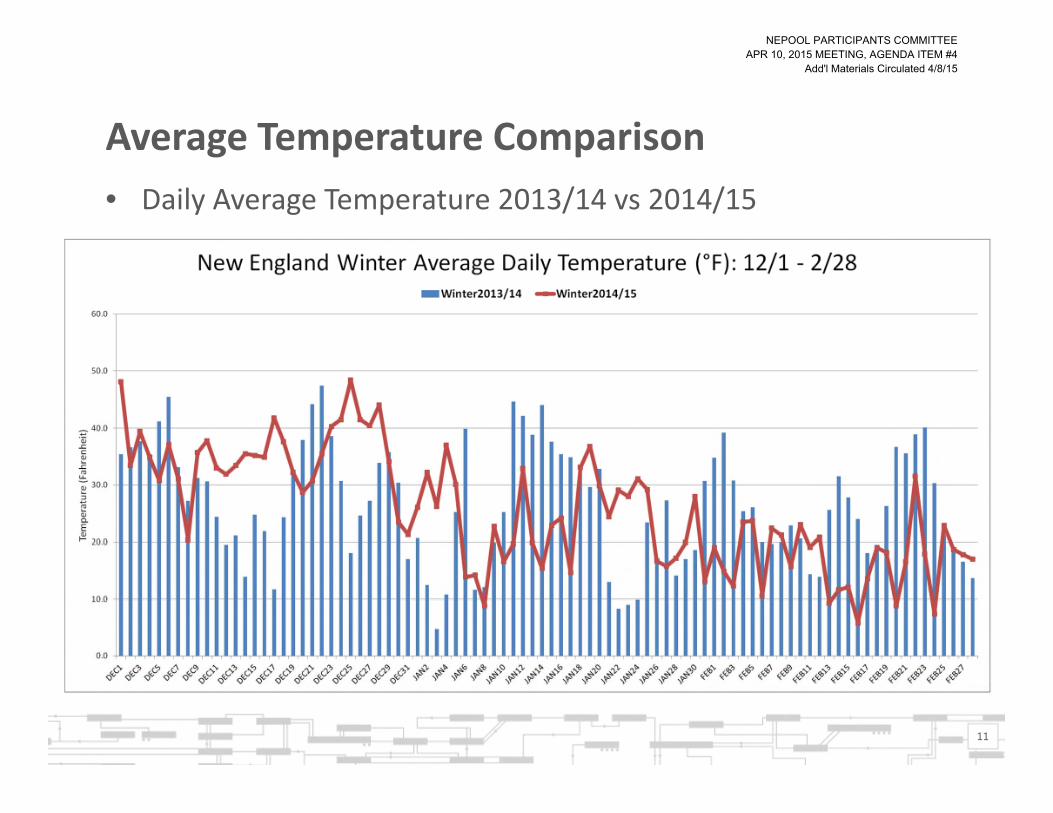

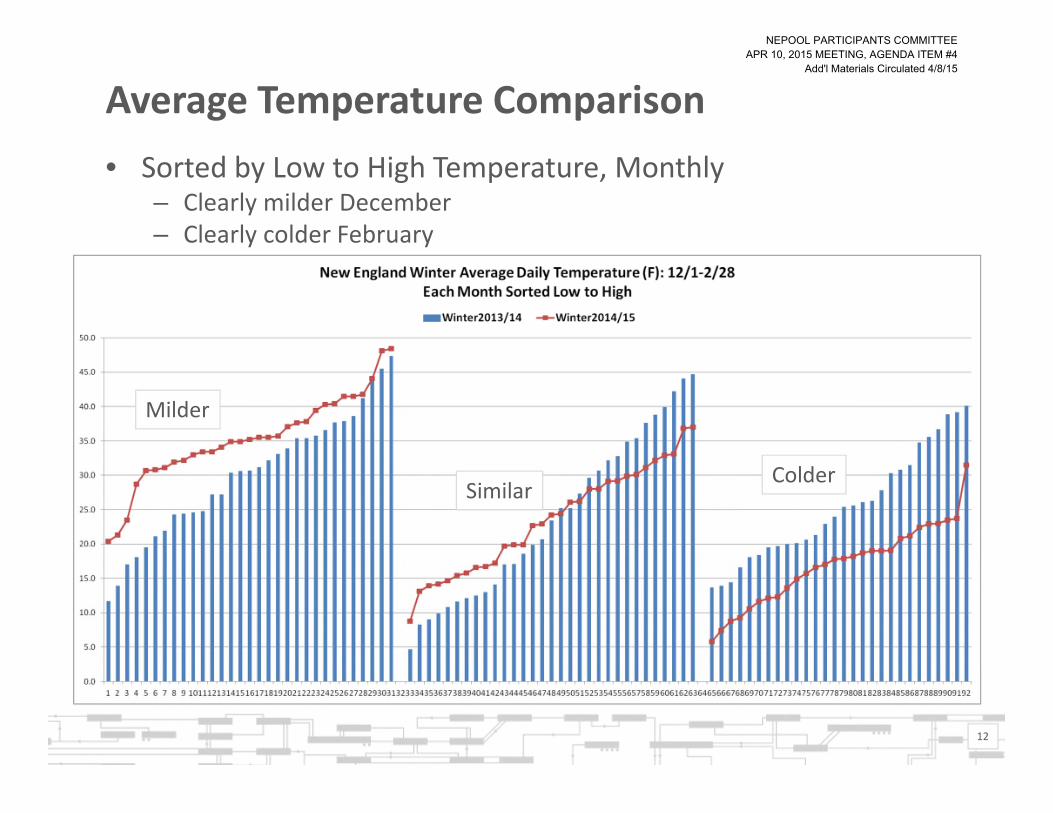

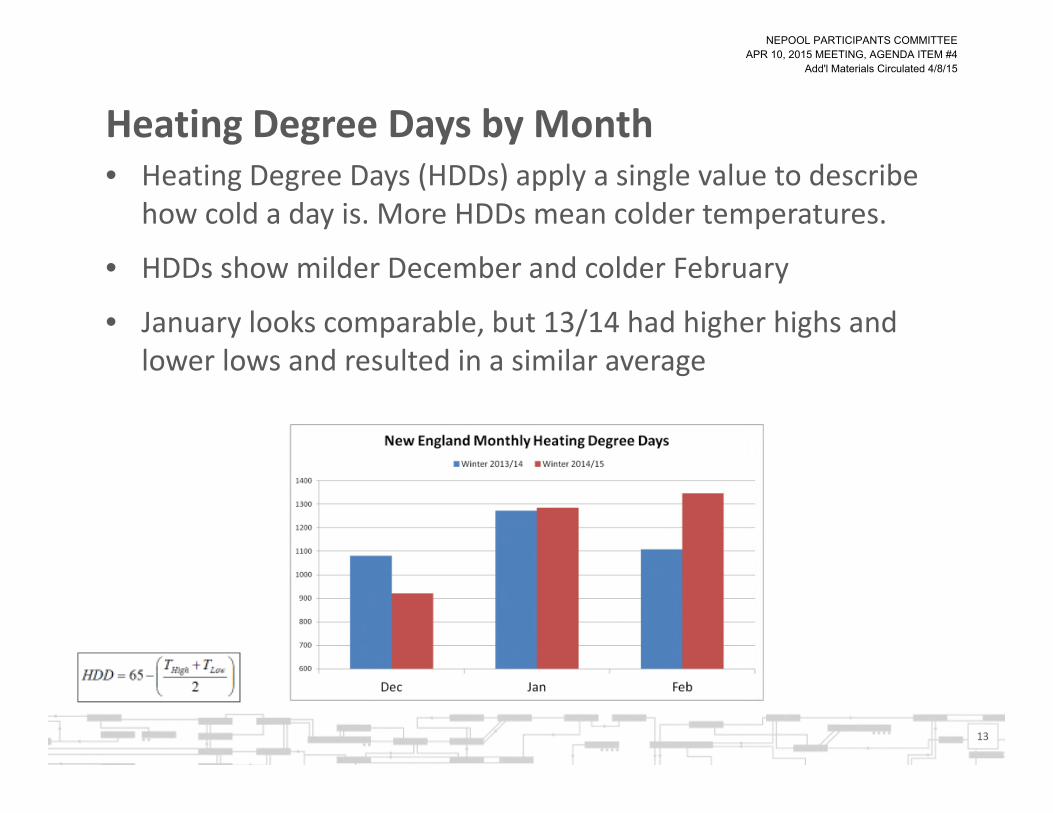

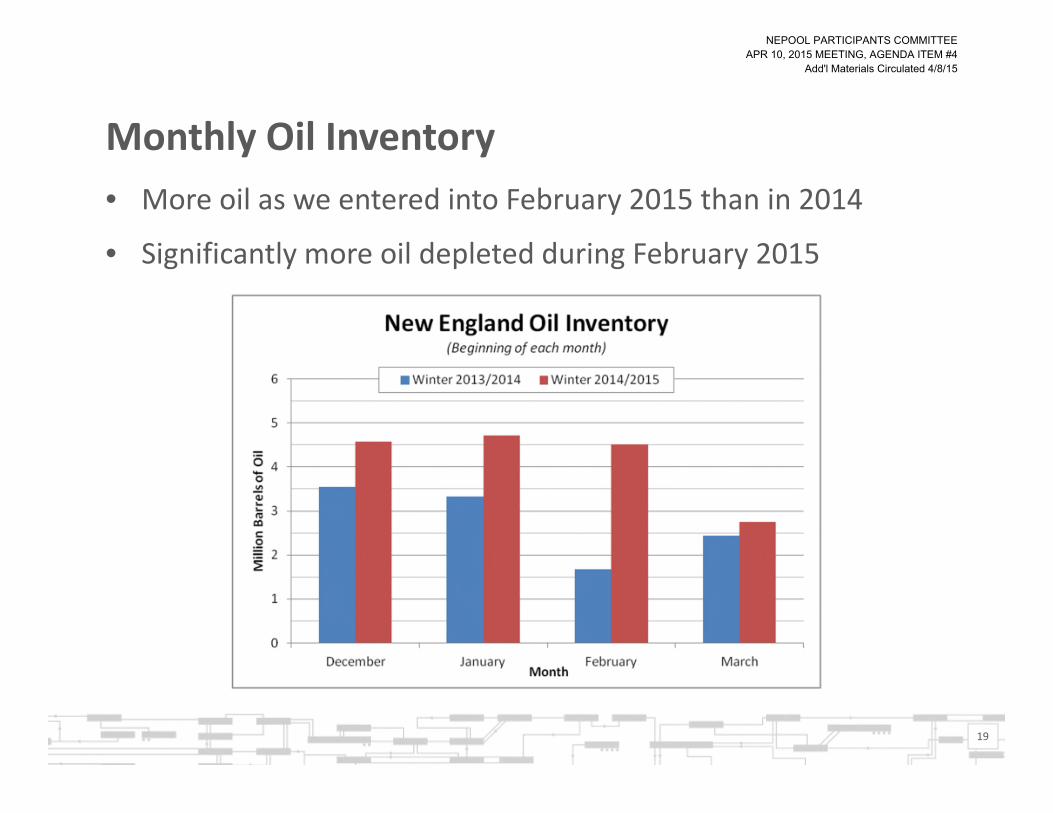

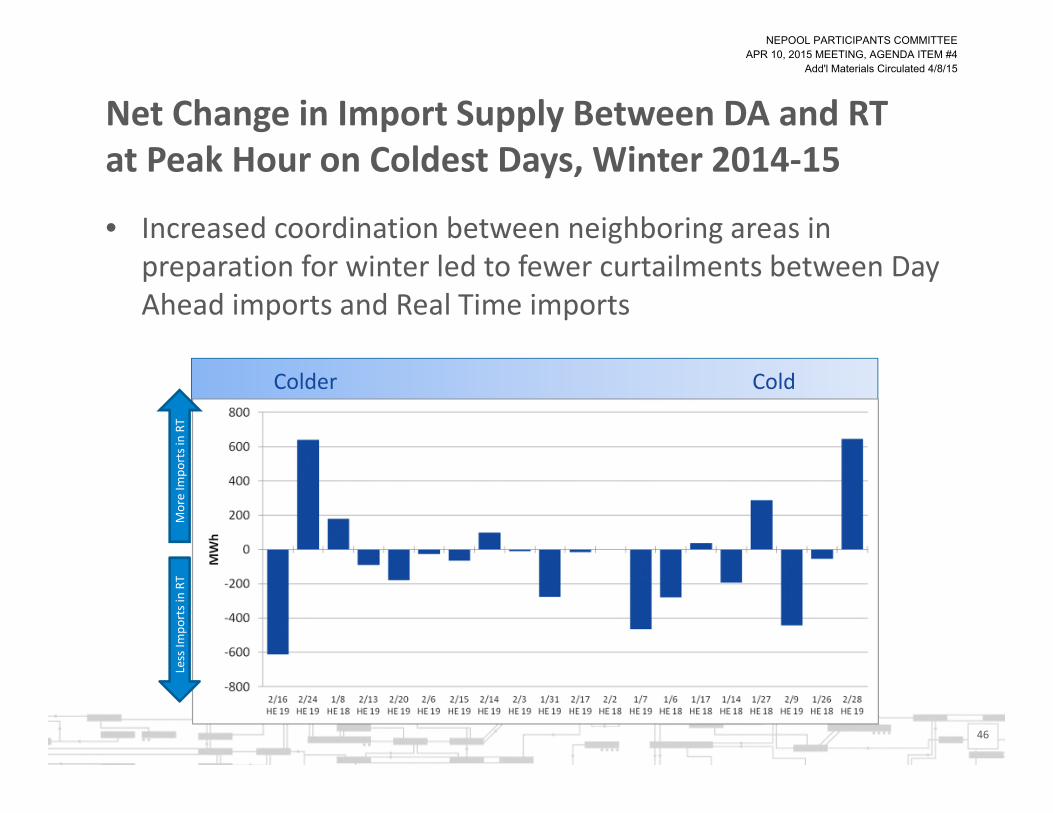

Dr. Chadalavada concluded that the timing of the Winter 2014/15’s colder temperatures,

and the incentives to increase oil inventory, had worked in the region’s favor. He showed with

charts that the coldest temperatures during Winter 2014/15 were in February. Had the cold

period occurred in January rather than in February, there would have been higher loads (1,000 to

1,5000 MW higher), roughly 1 million additional barrels of oil would have been burned, and it

would have been more challenging to maintain System reliability. Mr. van Welie cautioned that

reliability concerns for future Winter periods continue through Winter 2017, particularly given

the impending loss of significant amounts of non-gas-fired generation such as Brayton Point.

Dr. Chadalavada committed to provide more detailed information at future meetings

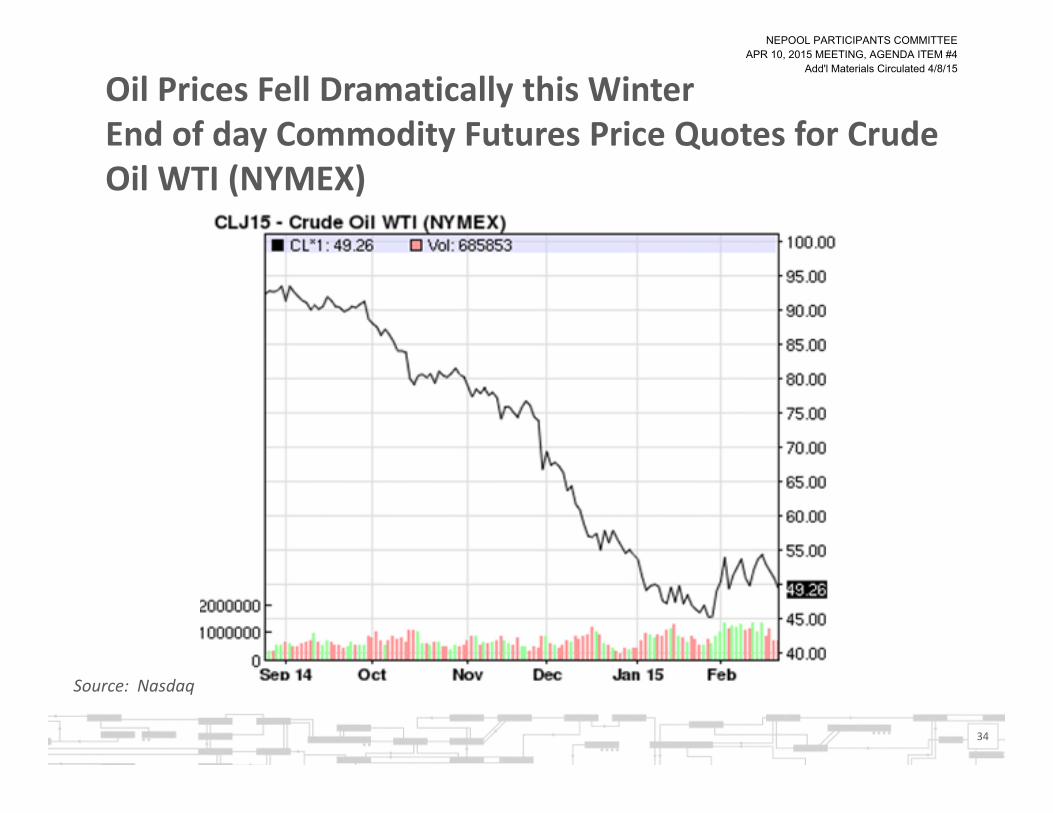

regarding total oil burned. He confirmed that the lower oil price during Winter 2014/15 had also

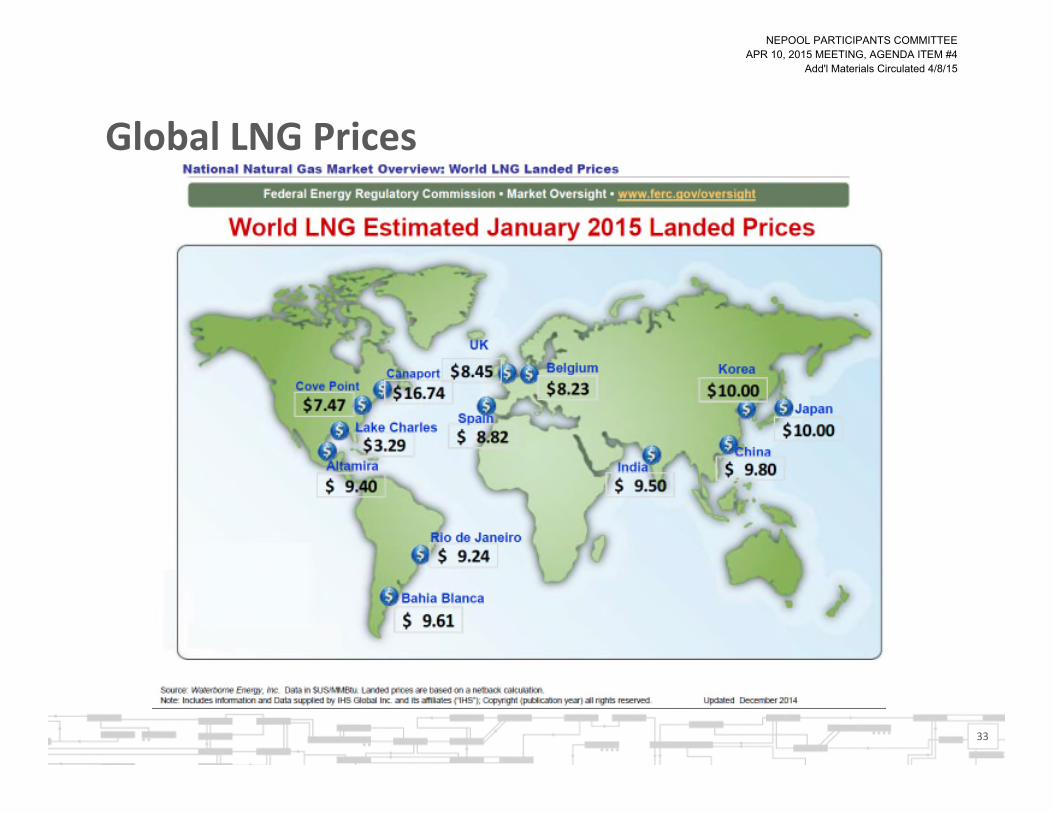

benefitted New England. He explained that, with the world LNG market indexed to the price of

crude oil, lower oil prices had reduced LNG shipments world-wide, but not to New England

which, for the second winter in a row, had the most expensive LNG prices. Dr. Chadalavada

explained that the ISO saw increased LNG during Winter 2014/15, although the reason still

needed to be ascertained. It was clear, however, that the dip in oil prices and the amount of LNG

available to the New England System had disciplined Energy Market clearing prices.

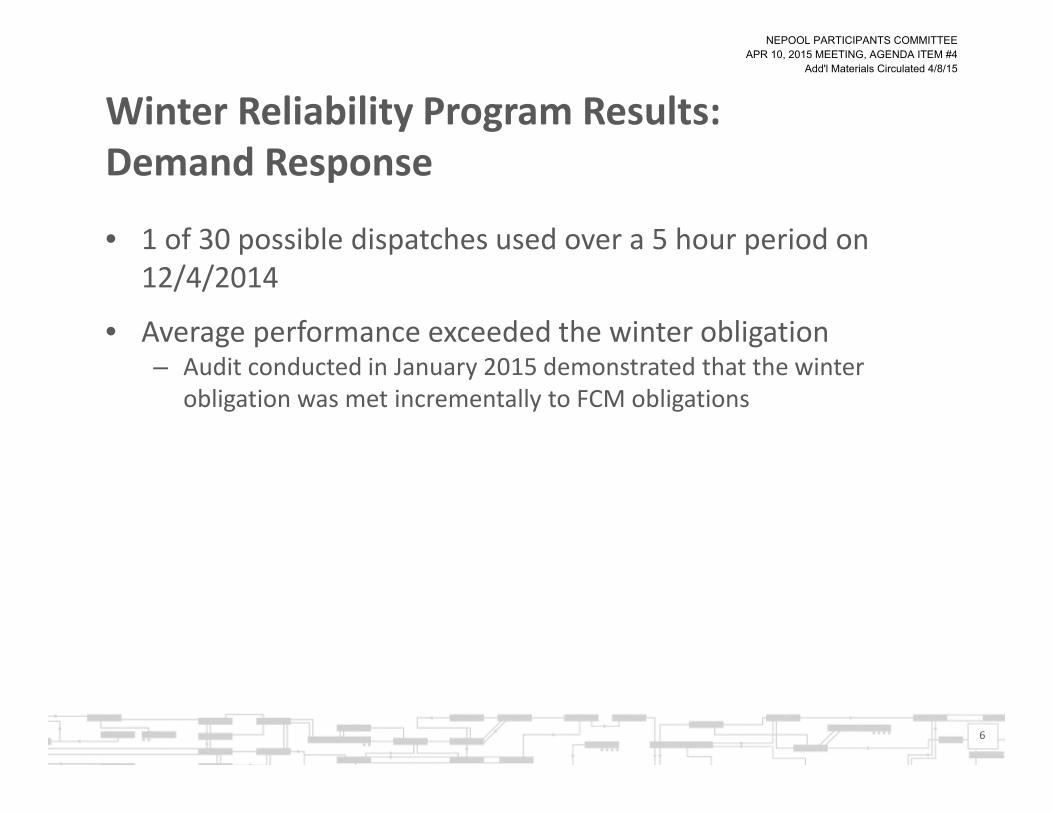

A NESCOE representative asked why none of the LNG was burned in the program. Dr.

Chadalavada postulated that higher strike prices had likely inhibited broader use of LNG inLNG

call option contracts under the Winter 2014/15 Program. With respect to LNG replenishment

data, the ISO committed to do its best to make that data available as soon as possible likely had

strike prices above the prevailing LNG market prices during this period and therefore went

unstruck.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3422

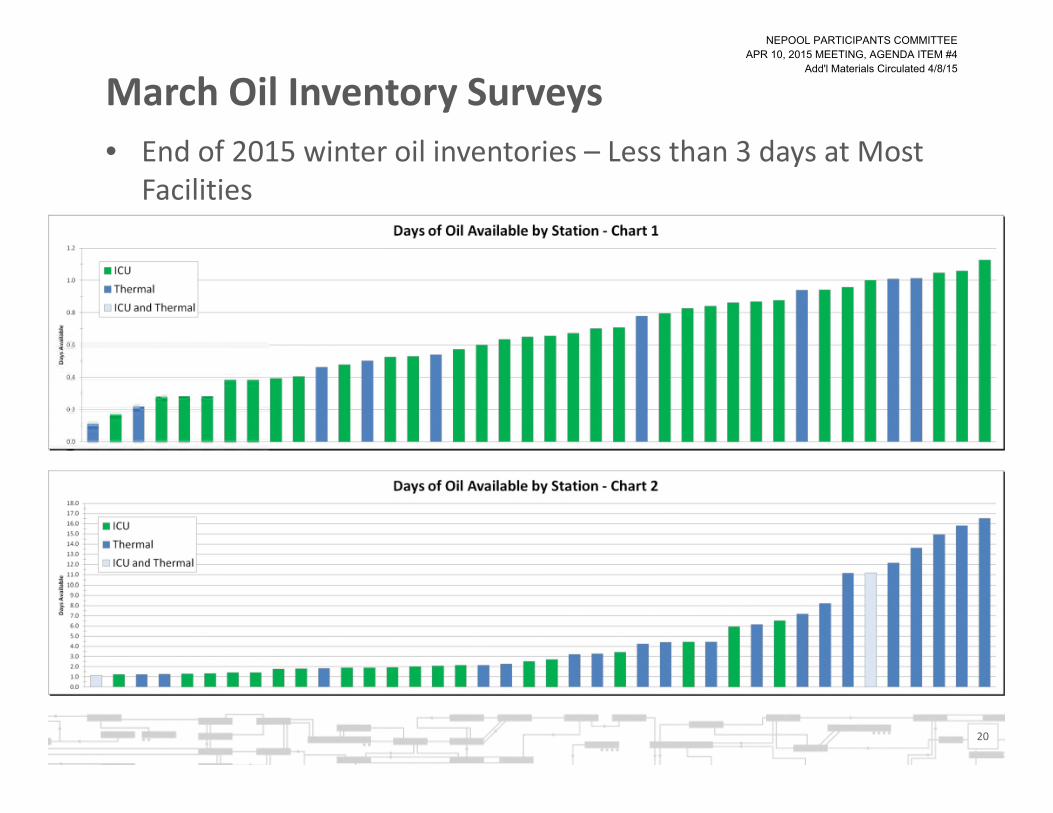

Dr. Chadalavada indicated that a comprehensive summary of Winter 2014/15 operations,

including several additional exhibits, would be presented to NEPOOL as soon as possible

following the conclusion of the winter.

2015 WORK PLAN

Mr. Gordon referred the Committee to the revised 2015 Work Plan that was circulated

and posted in advance of the meeting, reminding members that it had been introduced at the

February teleconference meeting. He said the presentation at this meeting was forto support a

more in-depth discussion of the Plan.

Dr. Chadalavada then reviewed the Work Plan noting that it had been revised to update

the timelines for the Third Party FTR clearing project, to be implemented in 2016 for the 2017

annual FTR auction, and the “Do Not Exceed” (DNE) wind dispatch project, targeted for

implementation in April 2016. He explained in that reviewed that the cyber security-related

projects required substantial operational efforts and a capital investment. He expected the work

load associated with this project to increase faster than any other project, with plans in 2015 to

implement a 24x7 security operations center to address cyber threats. He reported that this

project would result in an incremental headcount addition in 2015, which had not been reflected

in the 2015 budget, but would be trued up in the 2016 budget.

In the area of market design, Dr. Chadalavada stated the focus would be on energy price

formation and continued FCM reforms, including fast start pricing, ramp constraint pricing, and

full co-optimization of energy and reserves in the Day-Ahead Energy Market. Turning to the full

integration of Demand Resources, as touched on earlier in the meeting by Mr. van Welie, he

noted the ISO’s plan to discuss development of contingency plans to address potential impacts of

Supreme Court action on the EPSA v. FERC matter. He pointed out that the full integration of

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3423

price responsive demand (PRD), previously scheduled for June 1, 2017, would be delayed at

least one year, to June 1, 2018, to minimize capital investment to implement PRD before

knowing how it might be impacted by EPSA v. FERC.

Dr. Chadalavada also noted uncertainty surrounding the level of efforts to be required on

Order 1000 compliance. He noted the potential for incremental costs, both in 2015 and 2016,.

He said that scheduling around probabilistic planning would be discussed at the April Planning

Advisory Committee (PAC) meeting.

Dr. Chadalavada agreed with members’ requests to time the development and release of

the Work Plan to coincide more closely with budget development and review. Although he

indicated that many activities were in a “steady state,” the following three areas in the 2015

Work Plan could potentially lead to spikes in needed personnel resources or expenditures: (1)

cyber security; (2) NERC/NPCC compliance and standards; and (3) Order 1000 compliance and

implementation. Similarly, Mr. van Welie reported that the IMM had requested a slightly higher

headcount, which would be funded as a contingency in 2015 from the management and Board

contingency funds. The additional resources, once hired, would be included in 2016’s baseline

headcount.

Addressing the implementation schedule for third party clearing of FTRs, Dr.

Chadalavada explained that the projected delay resulted from personnel constraints related

primarily to implementation of Coordinated Transaction Scheduling and Generation Control

Application in the 4th quarter. He acknowledged Participants’ sensitivity to the additional delay,

but indicated that the ISO would continue to work on this project in 2015 (albeit at a slower pace

than previously projected) and that the project would be a high priority project in 2016.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3424

In planning for combined discussions of the Work Plan and budgets, Mr. Gordon

reminded the Committee of the timing of the 2016 budget process, with the first ISO

presentations to be made in June at the NECPUC Symposium and Participants Committee

Summer Meeting, in August at the Budget & Finance Subcommittee, and then again at the

Participants Committee in September and/or October for final consideration, prior to its filing

with the FERC.

ISO INTERNAL MARKET MONITOR (IMM) QUARTERLY MARKETS REPORT

Mr. Jeffrey McDonald, the ISO IMM, referred the Committee to the IMM 2014 Fourth

Quarter (Q4 2014) Quarterly Markets report circulated in advance of the meeting. He

highlighted that Energy Market prices in Q4 2014 were consistent with those expected of a

competitive market and were generally concentrated and structurally competitive.

Summarizing with more details, he reported that:

• Lower natural gas prices in Q4 2014 led to lower Day-Ahead and Real-Time EnergyMarket prices when compared to Q4 2013.

• NCPC payments totaled $27.8 million in Q4 2014, a 6% drop compared to the sameperiod in 2013.

• Real-Time Reserve payments totaled $8 million in Q4 2014, which was a 60% decreasefrom Q4 2013.

• Regulation payments totaled $5.8 million in Q4 2014, a 10% decrease from Q4 2013.

Mr. McDonald then reviewed a chart reflecting NCPC payments, highlighting which

payments were higher and lower from prior periods. He summarized that NCPC payments

increased 143% in Q4 2014 compared to Q3 2014, attributing that increase to, among other

things, the implementation of hourly offers and negative LMPs, and subject to further study,

hourly settlement for NCPC.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3425

For the next quarterly report, Mr. McDonald committed to provide a more holistic look at

what was driving NCPC as well as pricing by addressing gas availability during Winter 2014/15,

the effectiveness of hourly offers, and the settlement change that permits negative pricing. He

reported a substantial increase in Second Contingency Payments from $2.84 million in Q4 2013

to $8.7 million in Q4 2014. He explained that Second Contingency Payments for Q4 2014 were

primarily driven by NEMA/Boston, with commitment decisions needed to meet reserve

requirements impacted by the loss of Salem Harbor for Q4 and most of Q3.

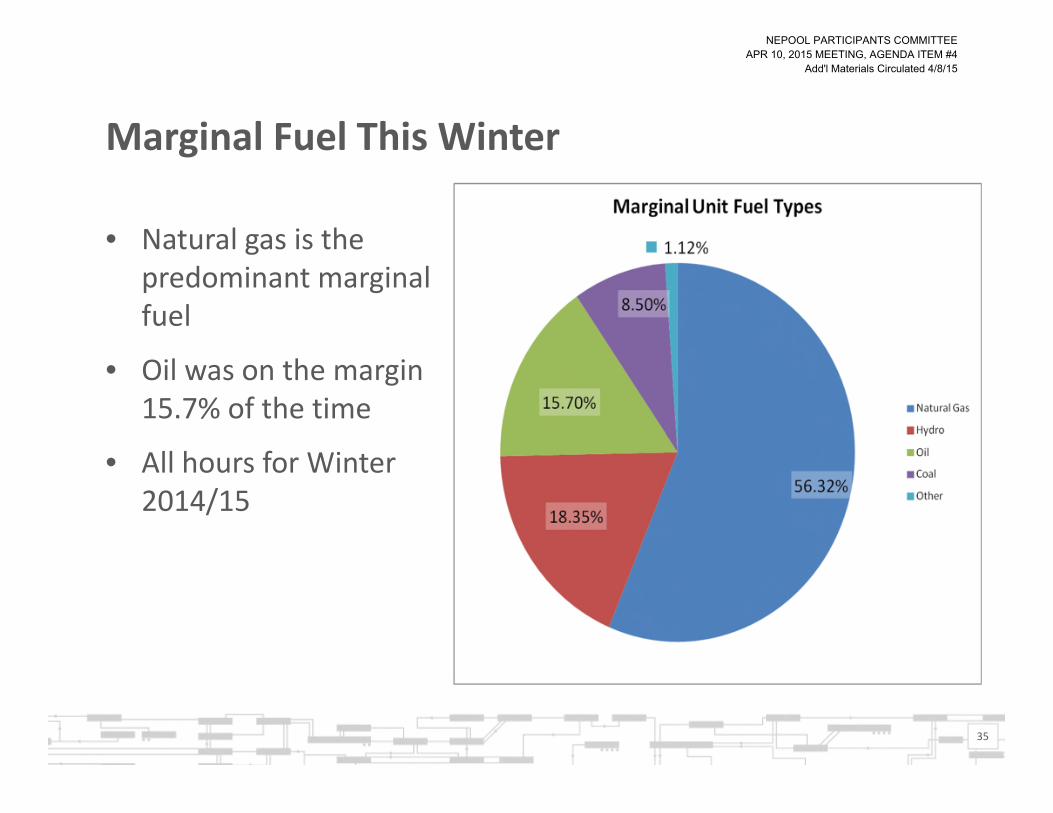

Mr. McDonald reviewed a slide illustrating the marginal units by fuel type for Q4 and

provided a breakdown of the percentages including: natural gas - 74.9%; oil - 0.6%, diesel -

0.9%, pumped storage - 11.6%, other hydro, wood, refuse - 4.9%; and coal - 7.4%. In response

to a question, Mr. McDonald committed to report back at a subsequent meeting as to whether the

pump storage percentage included only generation pump storage or if it also included the

pumping side when setting the price.

Mr. McDonald then updated the Committee on the Energy Market Offer Flexibility

(EMOF) changes that were implemented on December 3, 2014. He reviewed that the changes

allow Market Participants to vary Energy Market Offers by hour and to change Offers in Real-

Time during the Operating Day. He stated the offers that are more reflective of actual fuel prices

improve Energy Market price signals and permit a better match between those prices and the cost

of procuring fuel in Real-Time. He reported the IMM would continue to monitor how the EMOF

changes were working and would include an update in the Q1 2015 Quarterly Markets Report.

In response to a request that the next quarterly report include an analysis of negative bids, Mr.

McDonald indicated that he was not certain that there would be sufficient time to include that

detailed analysis in the Q1 2015 report, but would ensure its inclusion in the Q2 report.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3426

Mr. Gordon asked whether the ISO had considered whether there would be benefits to

changing the timing of these periodic reports, such that they might be more aligned with physical

market operations (winter, summer, shoulder periods), rather than by calendar quarters. Mr.

McDonald noted the FERC requirement that the ISO produce quarterly markets reports, but

agreed to consider whether a modified schedule for Committee presentations might be beneficial

and/or more efficient.

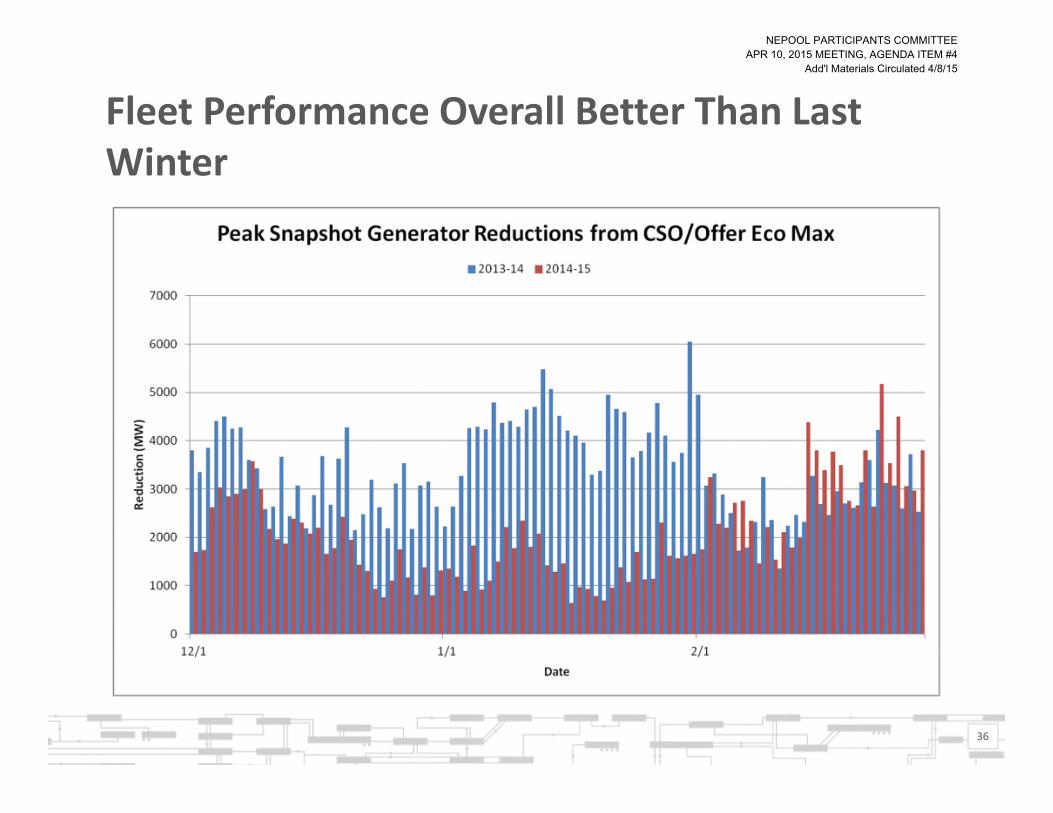

Mr. McDonald concluded his presentation by reporting on an OP4 event that occurred on

December 4, 2014 and referred the Committee to charts reflecting an operational summary of

that event. He reported a loss of nearly 2,000 MW from Hydro-Quebec as two large

transmission lines went out, which caused the ISO to implement Action 1 of OP4 to allow for

depletion of Thirty-Minute Operating Reserves. He reviewed that no demand responseDR was

dispatched during the event, and sufficient reserves were available after the evening peak

occurred, at which point OP4 was cancelled.

A member asked for an update with respect to a pending request for an evaluation of the

Forward Reserve Market clearing during summer 2014. Mr. McDonald responded that the

analysis had not been completed and released for two reasons. First, the ISO’s lead analyst had

left for another job opportunity before the analysis was finalized. Second, the IMM believed that

the benefits of a public report had been overtaken by ISO efforts to evaluate revamping the

procurement of ancillary services/reserves, in response to a recommendation by the External

Market Monitor move towards a Day-Ahead and Real-Time, rather than forward, procurement.

The member urged the IMM to reconsider releasing the analysis, particularly given the length of

time that would be required to fully consider such changes.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3427

ELIMINATION OF PER MECHANISM FOR CCP-10

Ms. Allison DiGrande, Markets Committee Chair, referred the Committee to the

materials circulated and posted in advance of the meeting regarding revisions to Market Rule 1

to eliminate the FCM PER mechanism beginning with the Capacity Commitment Period

associated with the tenth Forward Capacity Auction that is scheduled to commence on June 1,

2019 (CCP-10). She reported that the Markets Committee recommended Participants Committee

support for these changes at its February 10-11, 2015 meeting.

The following motion was duly made, seconded:

RESOLVED, that the Participants Committee supports revisions toMarket Rule 1 to eliminate the Peak Energy Rent mechanism forthe June 1, 2019 – May 31, 2020 Capacity Commitment Period(CCP-10) and beyond, as circulated to this Committee anddiscussed at this meeting, with such further non-substantivechanges as the Chair and Vice-Chair of the Markets Committeemay approve.

Mr. Gordon reported that this matter was initially included as Item #3 on the March 6

Consent Agenda, but was removed for discussion at the request of the Maine Office of the Public

Advocate (MOPA) and the New Hampshire Office of Consumer Advocate (NHOCA). The

MOPA and NHOCA representative explained that the item had been removed from the Consent

Agenda so that there would be an opportunity to hear and discuss the IMM’s plans to continue

monitoring of Real-Time offers, both during the three-year period in which PER will remain in

effect as well as once the PER mechanism is no longer in effect.

In response, Mr. McDonald explained that there were a number of market power

mitigation measures to address economic or physical withholding that PER was specifically

designed to address that would be unaffected by whether PER is, or is not, in place. He

explained that the existing PER provisions still required careful monitoring of bidding activities

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3428

in any event to protect against physical withholding. Looking ahead, he indicated that the

penalties or take backs from capacity market revenues to be implemented with the

implementation of the pay-for-performance rules would provide a reasonable, if not an exact,

substitute for the PER mechanism. In addition, Mr. McDonald opined that the ISO was already

in a better position to use availability/outage and portfolio profitability data to conduct the

necessary daily and weekly monitoring, and noted efforts underway to further bolster the IMM’s

monitoring capabilities, including improving the speed and automation of data access.

The National Grid representative stated his company would oppose the elimination of the

PER mechanism, explaining that, with the strike price set intentionally at a level well above what

could be considered a competitive energy price, it was unnecessary to allow resources to be paid

and retain revenues at that extreme price, would otherwise be an overpayment in the combined

Energy and Capacity Markets, and would not impact the true cost of new entry. For the same

reasons expressed by the National Grid representative, the MMWEC representative stated he

would oppose the changes. Providing the opposite view, a member of the Generation Sector

indicated his support for the changes, which he viewed as eliminating a penalty for those selling

into the Day-Ahead Energy Market during a PER hour.

The Committee then considered and approved the motion with oppositions noted by: CT

OCC, Harvard, National Grid, and each of members of the Publicly Owned Entity Sector with

representatives in attendance.

INTERMITTENT RESOURCE REAL-TIME DNE DISPATCH RULES

Ms. DiGrande referred the Committee to the materials circulated and posted in advance

of the meeting regarding revisions to Market Rule 1, Appendix F to Market Rule 1 and Tariff

Section I.2.2 to implement Real-Time Do Not Exceed (DNE) dispatch rules for intermittent

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3429

resources (DNE Dispatch Rules). She reported that the Markets Committee recommended the

changes with a 74.54% Vote in favor at its February 10-11, 2015 meeting. She noted that the

DNE Dispatch Rules were not on the Consent Agenda in light of discussion that continued

following the Markets Committee recommendation that suggested a high probability that either

the ISO would propose substantive changes to the Markets Committee-recommended DNE

Dispatch Rules or one or more Participant motions to amend those recommended changes would

be forthcoming.

The following motion was duly made and seconded:

RESOLVED, that the Participants Committee supports revisions toMarket Rule 1, Appendix F to Market Rule 1 and Tariff Section I.2.2 toimplement Real-Time Do Not Exceed dispatch rules for intermittentresources, as circulated to this Committee and discussed at thismeeting, with such non-substantive changes as may be approved bythe Chair and Vice-Chair of the Markets Committee.

Members commented on the revisions. The Brookfield representative expressed

appreciation to the ISO for meeting with his company to discuss some of the operational

challenges that hydro facilities would face under the rules. He stated that the ISO had agreed to

consider the development of new parameters that might support better representation of the

physical characteristics of hydro facilities. He stated Brookfield would abstain on the motion

because the parameters and the full design were not yet fully identified or captured in the Market

Rules. He also urged the ISO to consider implementing, as soon as practicable, dispatch

characteristics for other resources that could elect to be non-dispatchable.

Others noted their concerns and echoed appreciation for the ISO’s efforts on the changes.

A Generation Sector representative, noting a general preference for inclusion of details in the

Tariff itself, was satisfied that, in this case, the details would be developed in a new appendix to

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3430

Operating Procedure No. 14 (OP-14), and was pleased that details of the requirements would be

known and clarified in advance of implementation. Explaining their abstentions, the Eversource

representative noted a desire to see the OP-14 changes developed and to have a more complete

understanding of the associated costs and obligations prior to taking a final position, while a

representative of the Publicly Owned Entity Sector noted that the Sector’s members had not yet

gotten comfortable with the implications for hydro resources (though acknowledging the

advantages to wind resources) or with the implications for other categories of resources,

particularly those that may not be participating directly in the markets (e.g. demand responseDR

resources).

After further discussion, the Committee then considered and unanimously approved the

motion with abstentions noted by: Brookfield, CSC, Dominion, Eversource, LIPA, National

Grid, UI, and the Publicly Owned Entity Sector.

SRECTRADE, INC. MEMBERSHIPAPPLICATION

Mr. Patrick Gerity, NEPOOL Counsel, referred the Committee to the materials circulated

and posted in advance of the meeting regarding the application for membership in NEPOOL by

SRECTrade, Inc. (SRECTrade). He explained that SRECTrade, an Entity in the business of

brokering and trading in solar renewable energy credits (SRECs) and active participant in the

NEPOOL Generation Information System (GIS), did not qualify for membership in any Sector of

NEPOOL without changes being made to the NEPOOL arrangements. He summarized ongoing

efforts by the Membership Subcommittee to identify changes to the membership provisions to

address that issue, including the elements of a proposal to establish a “GIS-Only Participant”

status. Mr. Gerity reported that the details of that proposal were scheduled to be finalized at the

March 16 meeting of the Membership Subcommittee, encouraged all those interested to

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3431

participate, and indicated that, if finalized at the March Subcommittee meeting, the proposal

would be presented for Participants Committee consideration at its April 10 meeting.

Members then asked clarifying questions and provided input on the elements of the GIS-

Only Participant proposal. In response to a members’ questions, Mr. Gerity clarified that a GIS-

Only Participant would be a treated like any other Participant for all purposes, other than with

respect to making a motion and voting, where they would be a voting member for, and could

make motions only with respect to, GIS matters. When voting on GIS matters, GIS-Only

Participants would vote as members of the Provisional Member Group Seat.

Addressing a request by SRECTrade to participate in the Pool while the arrangements

governing its membership were finalized, Mr. Gerity reported that SRECTrade had requested,

and the Subcommittee had not opposed, that SRECTrade be admitted as a Provisional Member

for a limited, interim period of time. Mr. Gerity clarified that, in order to address concerns that

the interim period of time be both long enough to ensure time for the long-term arrangements to

be finalized and become effective, but not be of unlimited duration (thereby incenting

completion of the arrangements), an additional sunset condition to SRECTrade’s membership

had been recommended that would have SRECTrade’s membership as a Provisional Member

expire upon the earlier to occur of (i) the effectiveness of changes to the NEPOOL Agreement to

address SRECTrade’s participation in the Pool or (ii) January 1, 2016 (at most, nine months).

The following motion was then duly made, seconded, and unanimously approved:

RESOLVED, that the Participants Committee approves the membership ofSRECTrade, Inc. (SRECTrade) in the New England Power Pool, subjectto the following conditions: (1) that NEPOOL Counsel and the ISO findthe application by SRECTrade complete; and (2) that SRECTrade accept(a) the Standard Membership Conditions, Waivers and Reminders and (b)the following additional condition: SRECTrade’s status as a ProvisionalMember will expire upon the earlier to occur of (x) the effectiveness of

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3432

changes to the NEPOOL Agreement to address SRECTrade’s Sectoreligibility or alternative participation in the Pool or (y) January 1, 2016.

LITIGATION REPORT

Mr. Gerity then referred the Committee to the March 4 Litigation Report that had been

circulated and posted in advance of the meeting. He highlighted recent activity in the complaint

proceedings, including a number of requests for rehearing of orders issued on January 30 and an

order denying rehearing of FERC Opinions 531 and 531-A.

COMMITTEE REPORTS

The Vice-Chairs of each of the Technical Committees reported on the schedule for

Committee meetings in March (see NEPOOL calendar). Mr. Dell Orto reported that the next

Budget & Finance Subcommittee meeting was scheduled for March 26 and would include, in

addition to routine matters, a discussion of GIS cost allocation practices. He encouraged those

with an interest in those practices to participate in that meeting. Ms. Abigail Krich, Vice-Chair

of the Variable Resources Working Group (VRWG), reported that the VRWG was scheduled to

meet on March 30 at the Publick House in Sturbridge, with discussion to include potential OP-14

changes to support DNE dispatch rules for intermittent hydro resources (as noted earlier in the

meeting) and Day-Ahead Energy Market Offers from, and NCPC calculations for, variable

resources. Mr. Jose Rotger reported that, following some re-scheduling, the Planning Advisory

Committee was scheduled to meet on March 24.

OTHER BUSINESS

Mr. Doot reported that the next Participants Committee meeting was scheduled for April

10, 2015, at the Seaport Hotel, with the discounted room block open for reservations already full

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015

3433

and asked that anyone still needing a reservation to contact Ms. Cynthia Jacobs, NEPOOL

Administrator, for her assistance. Looking ahead, he encouraged people to mark their calendars

for the Summer Meeting, scheduled to be held at the Stoweflake Resort & Conference Center in

Stowe, Vermont, on June 23-25 with a welcome reception on June 22. He indicated that the

room block for the summer meeting had not yet opened as of yet and to stay tuned for that

information in future notices of upcoming meetings.

Highlighting additional meetings on the March calendar, Mr. Doot noted that the

Consumer Liaison Group was scheduled to meet at Stoweflake on March 13 and that the FERC

had scheduled a March 11 Eastern region technical conference on the implications of compliance

approaches to the Environmental Protection Agency’s proposed Clean Power Plan at the same

time as the second day of the previously announced March Markets Committee meeting. He

encouraged those impacted to focus on arranging coverage for both.

There being no further business, the meeting adjourned at 12:05 p.m.

Respectfully submitted,

______________________David T. Doot, Secretary

NEPOOL PARTICIPANTS COMMITTEE MEETINGAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015ATTACHMENT 1

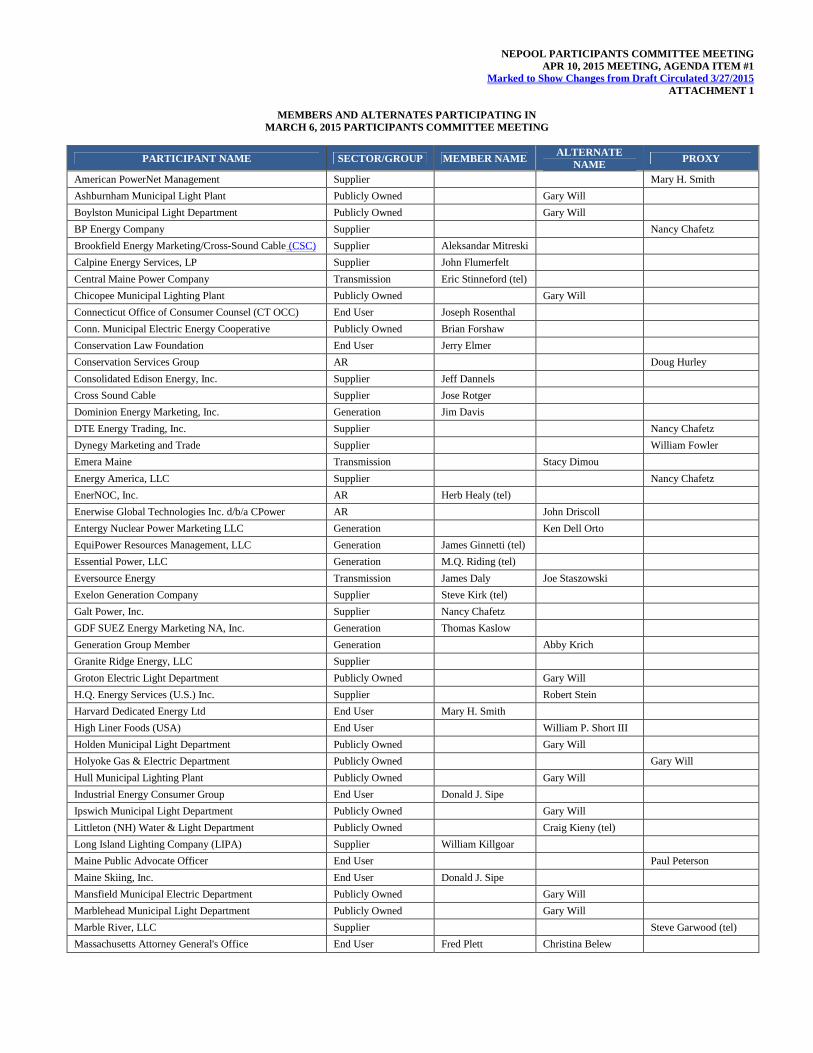

MEMBERS AND ALTERNATES PARTICIPATING INMARCH 6, 2015 PARTICIPANTS COMMITTEE MEETING

PARTICIPANT NAME SECTOR/GROUP MEMBER NAMEALTERNATE

NAMEPROXY

American PowerNet Management Supplier Mary H. Smith

Ashburnham Municipal Light Plant Publicly Owned Gary Will

Boylston Municipal Light Department Publicly Owned Gary Will

BP Energy Company Supplier Nancy Chafetz

Brookfield Energy Marketing/Cross-Sound Cable (CSC) Supplier Aleksandar Mitreski

Calpine Energy Services, LP Supplier John Flumerfelt

Central Maine Power Company Transmission Eric Stinneford (tel)

Chicopee Municipal Lighting Plant Publicly Owned Gary Will

Connecticut Office of Consumer Counsel (CT OCC) End User Joseph Rosenthal

Conn. Municipal Electric Energy Cooperative Publicly Owned Brian Forshaw

Conservation Law Foundation End User Jerry Elmer

Conservation Services Group AR Doug Hurley

Consolidated Edison Energy, Inc. Supplier Jeff Dannels

Cross Sound Cable Supplier Jose Rotger

Dominion Energy Marketing, Inc. Generation Jim Davis

DTE Energy Trading, Inc. Supplier Nancy Chafetz

Dynegy Marketing and Trade Supplier William Fowler

Emera Maine Transmission Stacy Dimou

Energy America, LLC Supplier Nancy Chafetz

EnerNOC, Inc. AR Herb Healy (tel)

Enerwise Global Technologies Inc. d/b/a CPower AR John Driscoll

Entergy Nuclear Power Marketing LLC Generation Ken Dell Orto

EquiPower Resources Management, LLC Generation James Ginnetti (tel)

Essential Power, LLC Generation M.Q. Riding (tel)

Eversource Energy Transmission James Daly Joe Staszowski

Exelon Generation Company Supplier Steve Kirk (tel)

Galt Power, Inc. Supplier Nancy Chafetz

GDF SUEZ Energy Marketing NA, Inc. Generation Thomas Kaslow

Generation Group Member Generation Abby Krich

Granite Ridge Energy, LLC Supplier

Groton Electric Light Department Publicly Owned Gary Will

H.Q. Energy Services (U.S.) Inc. Supplier Robert Stein

Harvard Dedicated Energy Ltd End User Mary H. Smith

High Liner Foods (USA) End User William P. Short III

Holden Municipal Light Department Publicly Owned Gary Will

Holyoke Gas & Electric Department Publicly Owned Gary Will

Hull Municipal Lighting Plant Publicly Owned Gary Will

Industrial Energy Consumer Group End User Donald J. Sipe

Ipswich Municipal Light Department Publicly Owned Gary Will

Littleton (NH) Water & Light Department Publicly Owned Craig Kieny (tel)

Long Island Lighting Company (LIPA) Supplier William Killgoar

Maine Public Advocate Officer End User Paul Peterson

Maine Skiing, Inc. End User Donald J. Sipe

Mansfield Municipal Electric Department Publicly Owned Gary Will

Marblehead Municipal Light Department Publicly Owned Gary Will

Marble River, LLC Supplier Steve Garwood (tel)

Massachusetts Attorney General's Office End User Fred Plett Christina Belew

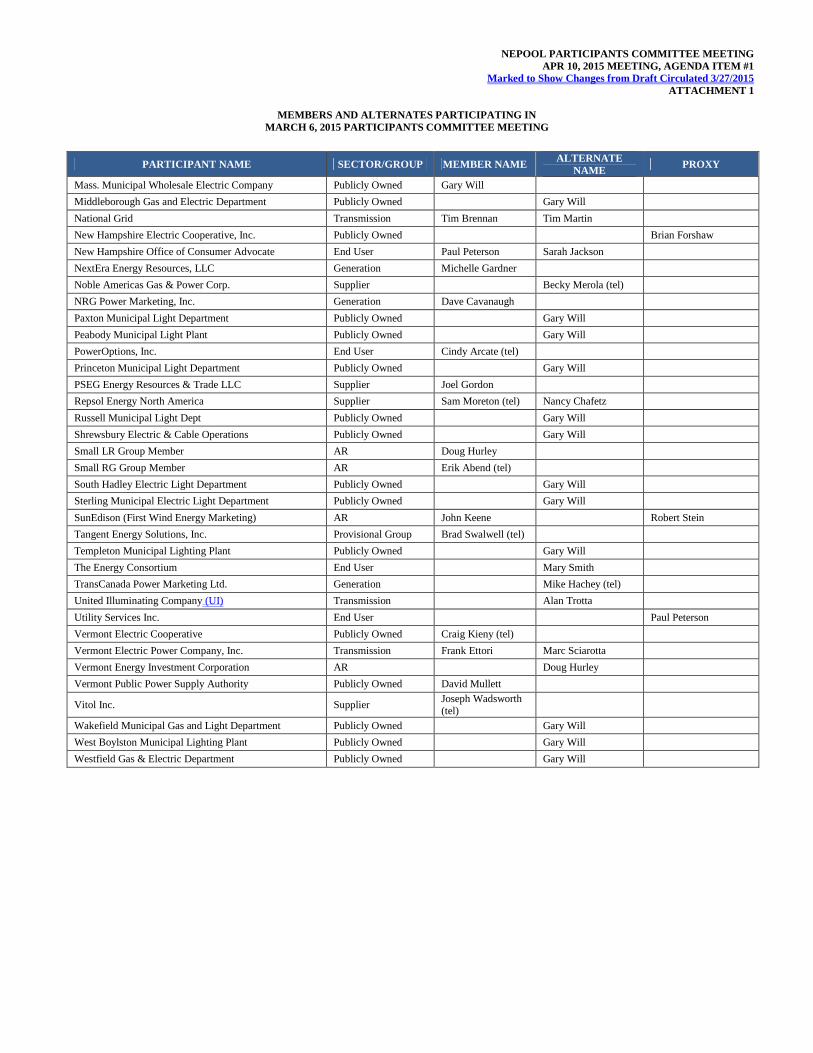

NEPOOL PARTICIPANTS COMMITTEE MEETINGAPR 10, 2015 MEETING, AGENDA ITEM #1

Marked to Show Changes from Draft Circulated 3/27/2015ATTACHMENT 1

MEMBERS AND ALTERNATES PARTICIPATING INMARCH 6, 2015 PARTICIPANTS COMMITTEE MEETING

PARTICIPANT NAME SECTOR/GROUP MEMBER NAMEALTERNATE

NAMEPROXY

Mass. Municipal Wholesale Electric Company Publicly Owned Gary Will

Middleborough Gas and Electric Department Publicly Owned Gary Will

National Grid Transmission Tim Brennan Tim Martin

New Hampshire Electric Cooperative, Inc. Publicly Owned Brian Forshaw

New Hampshire Office of Consumer Advocate End User Paul Peterson Sarah Jackson

NextEra Energy Resources, LLC Generation Michelle Gardner

Noble Americas Gas & Power Corp. Supplier Becky Merola (tel)

NRG Power Marketing, Inc. Generation Dave Cavanaugh

Paxton Municipal Light Department Publicly Owned Gary Will

Peabody Municipal Light Plant Publicly Owned Gary Will

PowerOptions, Inc. End User Cindy Arcate (tel)

Princeton Municipal Light Department Publicly Owned Gary Will

PSEG Energy Resources & Trade LLC Supplier Joel Gordon

Repsol Energy North America Supplier Sam Moreton (tel) Nancy Chafetz

Russell Municipal Light Dept Publicly Owned Gary Will

Shrewsbury Electric & Cable Operations Publicly Owned Gary Will

Small LR Group Member AR Doug Hurley

Small RG Group Member AR Erik Abend (tel)

South Hadley Electric Light Department Publicly Owned Gary Will

Sterling Municipal Electric Light Department Publicly Owned Gary Will

SunEdison (First Wind Energy Marketing) AR John Keene Robert Stein

Tangent Energy Solutions, Inc. Provisional Group Brad Swalwell (tel)

Templeton Municipal Lighting Plant Publicly Owned Gary Will

The Energy Consortium End User Mary Smith

TransCanada Power Marketing Ltd. Generation Mike Hachey (tel)

United Illuminating Company (UI) Transmission Alan Trotta

Utility Services Inc. End User Paul Peterson

Vermont Electric Cooperative Publicly Owned Craig Kieny (tel)

Vermont Electric Power Company, Inc. Transmission Frank Ettori Marc Sciarotta

Vermont Energy Investment Corporation AR Doug Hurley

Vermont Public Power Supply Authority Publicly Owned David Mullett

Vitol Inc. SupplierJoseph Wadsworth(tel)

Wakefield Municipal Gas and Light Department Publicly Owned Gary Will

West Boylston Municipal Lighting Plant Publicly Owned Gary Will

Westfield Gas & Electric Department Publicly Owned Gary Will

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #2

CONSENT AGENDA

From the notice of actions of the March 17, 2015 Reliability Committee1 meeting, dated March 17, 2015,which has been previously circulated:

1. Revisions to OP-23 Appendix G (Testing Date, Unit Listing, and REMVEC/NGRID Table Titlechanges)

Support revisions to Operating Procedure No. 23 Appendix G (Generators Required toPerform Reactive Capability Testing), which modify testing dates, add and removeunits at the request of the Voltage Task Force, and change the title of Table 5 (toREMVEC/NGRID), as recommended by the Reliability Committee at its March 17, 2015meeting, with such further non-substantive changes as the Chair and Vice-Chair of theReliability Committee may approve.

The motion to recommend Participants Committee support was approved unanimously.

1 Reliability Committee Notices of Actions are posted on the ISO website at: http://www.iso-ne.com/committees/reliability/reliability-committee.

Summary of ISO New England Board and Committee Meetings

April 10, 2015 Participants Committee Meeting

Since the last Participants Committee meeting, the Audit and Finance Committee, the Compensation and

Human Resources Committee, the Nominating and Governance Committee, the Markets Committee, and the

Board of Directors each met in Holyoke on March 19.

The Audit and Finance Committee was presented with the 2015 audit plan. The Committee discussed

the major areas of coverage, including cyber security, hourly offers, reliability standards, and local control

center reviews. Next, the Committee received an update on current Internal Audit Department activities

and the risks and outcomes pertaining to Internal Audit’s work. The Committee discussed audit ratings,

their meanings and the best way to convey audit results. The Committee also discussed the performance

and cost effectiveness of the Company’s external auditors. Following this discussion, the Committee

approved the 2015 audit plan. The Committee also approved the appointment of KPMG as auditor of the

Company’s financial statements and to conduct the Service Organization Controls engagement, and

approved Meyers Brothers Kalicka as auditor of the Company’s benefit plans. Next, the Committee met

with representatives from KPMG and reviewed the objectives for the 2015 Service Organization Controls

report. The Committee discussed the scope of the report, including objectives, audit team and

methodology. KPMG and management reviewed the 2014 audited financial statements with the

Committee and discussed disclosure controls. The Committee then held an executive session with KPMG.

Following the executive session, the Committee voted to recommend the adoption of the audited financial

statements by the Board of Directors. Next, the Committee reviewed the Company’s cyber security plan,

including the timeline, funding, and design of the plan. The Committee discussed the significant elements

of the plan and how management intends to prioritize and address the various elements. The Committee

received a status update on financial performance against the 2015 budget, and also conducted its biennial

review of the committee charter to confirm compliance. The Committee agreed that the charter was

accurate and that the Committee is in compliance with its terms. Finally, the Committee discussed the

Company’s rules prohibiting directors and employees from investing in securities of market participants,

and the changes recently made to similar rules by other independent system operators and regional

transmission organizations. The Committee agreed not to pursue changes to the Company’s rules at this

time, and to reconsider the issue in the future.

The Compensation and Human Resources Committee discussed a report benchmarking certain of the

Company’s benefits against other independent system operators and regional transmission organizations as

well as non-profit and for-profit companies.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #3

Add'l Materials Circulated 4/8/15

2

The Nominating and Governance Committee considered the 2015 evaluation process for the Board and

Committees and the use of facilitated evaluations. The Committee also discussed director succession

planning and board succession trends. The Committee reviewed the important factors to consider in

succession planning, including committee membership composition, retirements and timing of vacancies,

and requisite areas of board expertise.

The Markets Committee received reports on market monitoring, mitigation and reliability costs,

including the External Market Monitor’s quarterly report on market performance. The Committee

discussed the amount of load cleared in the day-ahead market, reviewed changes in the payment of Net

Commitment Period Compensation that took place during the month, and also discussed the premium that

New England is paying for gas-fired electricity compared to other areas. The Committee reviewed the

Company’s draft contingency plan options for demand response in light of the Court of Appeals decision

vacating Order 745 and finding that the Federal Energy Regulatory Commission lacked jurisdiction over

demand response in certain circumstances. The Committee noted that the various options will be

discussed with stakeholders in the NEPOOL stakeholder process. Finally, the Committee received an

overview of the Company’s plans to address price formation issues, and discussed stakeholders’ interests

and varying incentives along with the Federal Energy Regulatory Commission’s process for considering

the issues.

The Board of Directors received reports from the standing committees and the Chief Executive Officer.

During the committee reports, the Board approved the 2014 audited financial statements and discussed the

evaluation process for board and committee evaluations. The Board then reviewed various issues

concerning capacity zone formation, show of interest, and zonal pricing related to Forward Capacity

Auction #10.

NEPOOL PARTICIPANTS COMMITTEEAPR 10, 2015 MEETING, AGENDA ITEM #3

Add'l Materials Circulated 4/8/15

A P R I L 1 0 , 2 0 1 5 | B O S T O N , M A

Vamsi Chadalavada E X E C U T I V E V I C E P R E S I D E N T A N D C H I E F O P E R A T I N G O F F I C E R

April 2015

NEPOOL Participants Committee Report

NEPOOL PARTICIPANTS COMMITTEE MEETING 04/10/15 MEETING, AGENDA ITEM #4

2

Table of Contents • Highlights Page 3

• System Operations Page 9

• Market Operations Page 20

• Back-Up Detail Page 37

– Load Response Page 38 – New Generation Page 40 – Forward Capacity Market Page 47 – Reliability Costs - Net Commitment Period

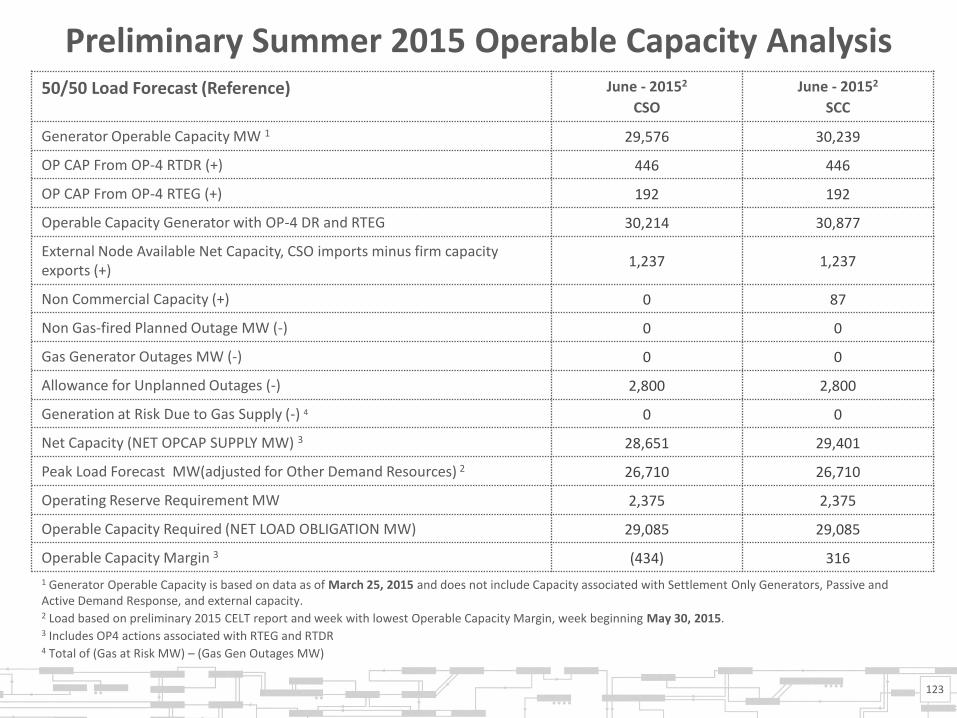

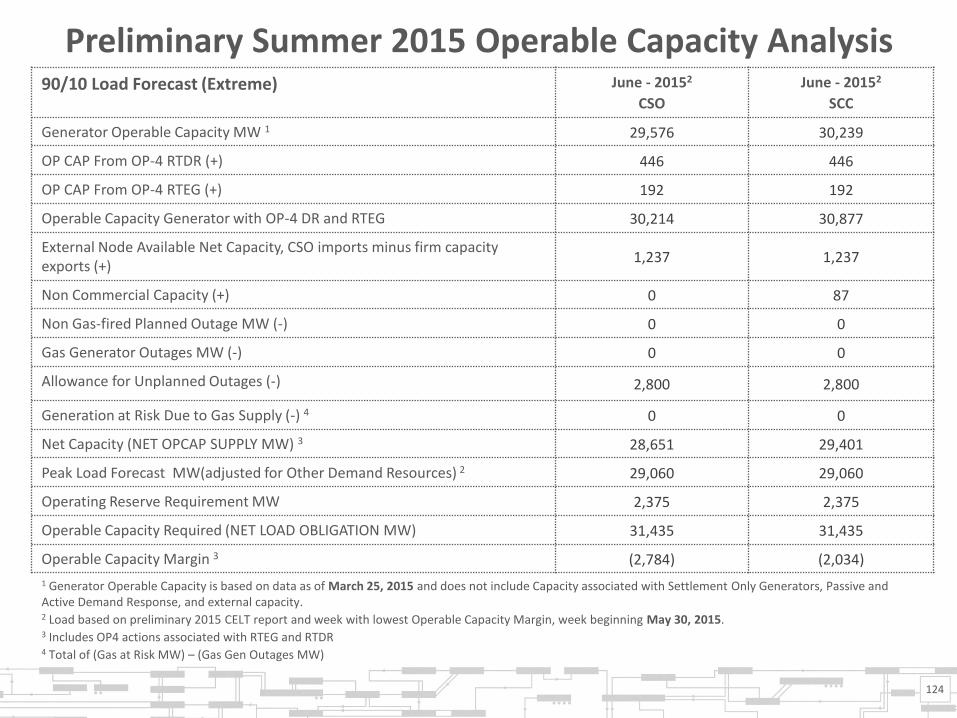

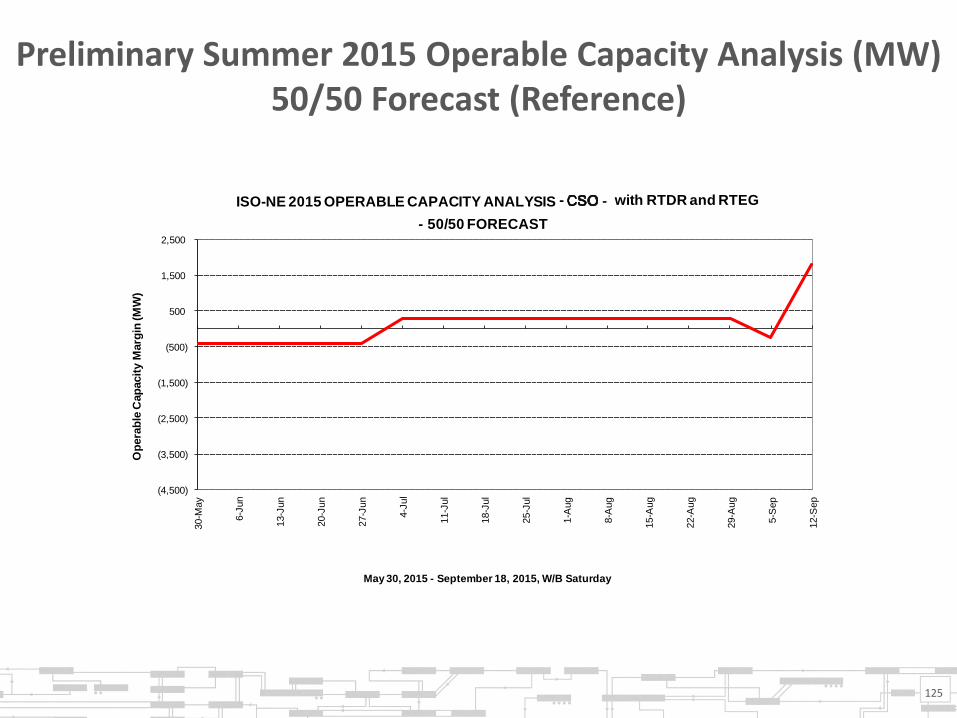

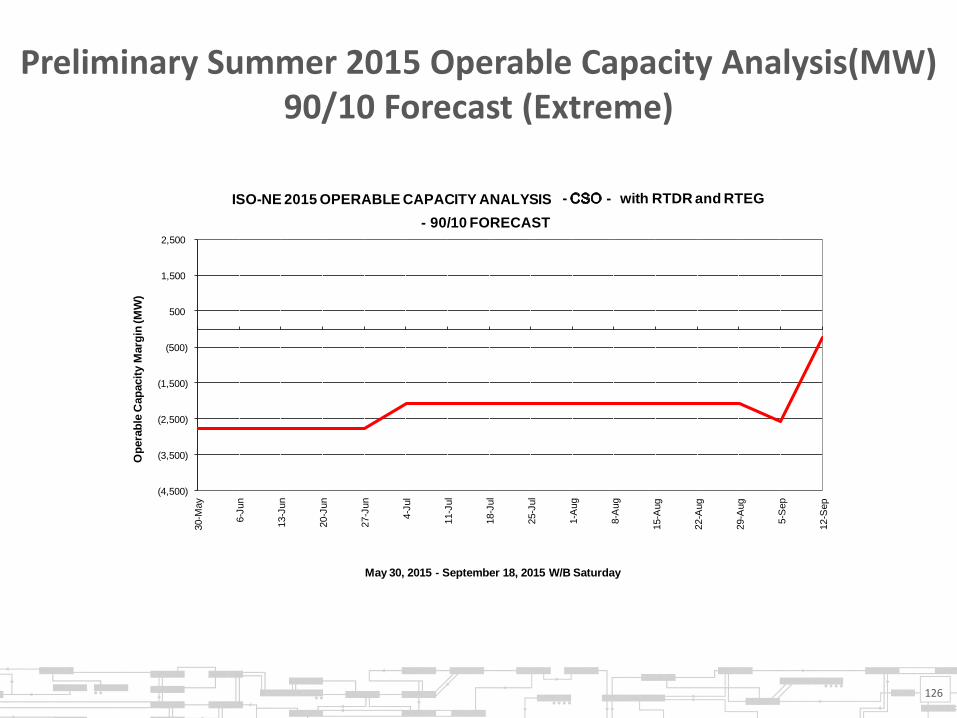

Compensation (NCPC) Operating Costs Page 54 – Regional System Plan (RSP) & Interregional Planning Page 85 – Operable Capacity Analysis – Spring 2015 Page 115 – Operable Capacity Analysis – Preliminary

Summer 2015 Page 122 – Operable Capacity Analysis – Appendix Page 129

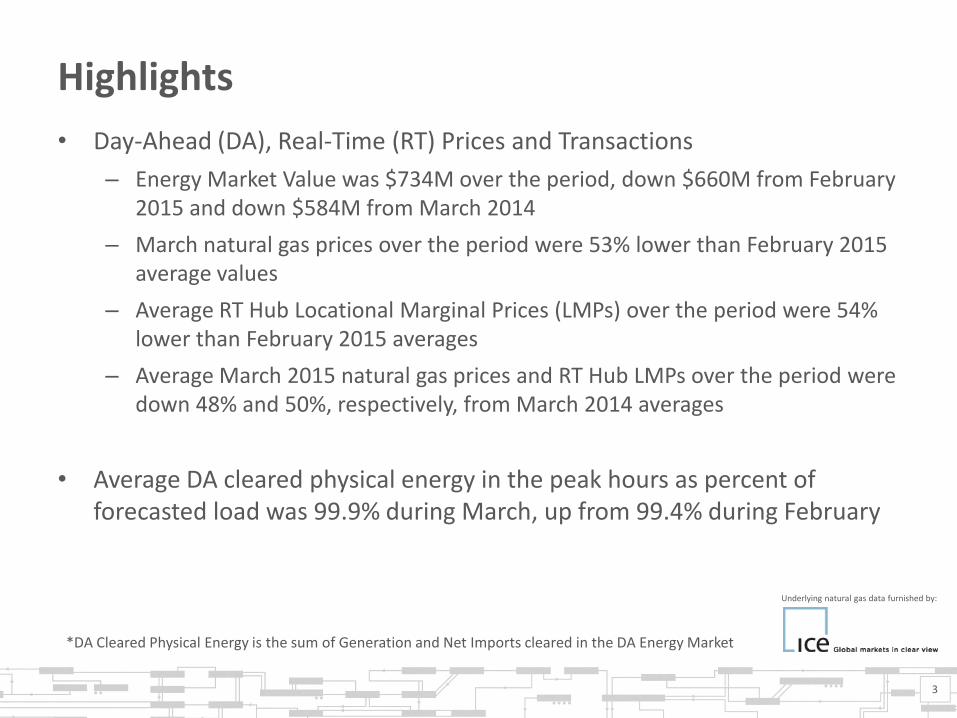

Highlights

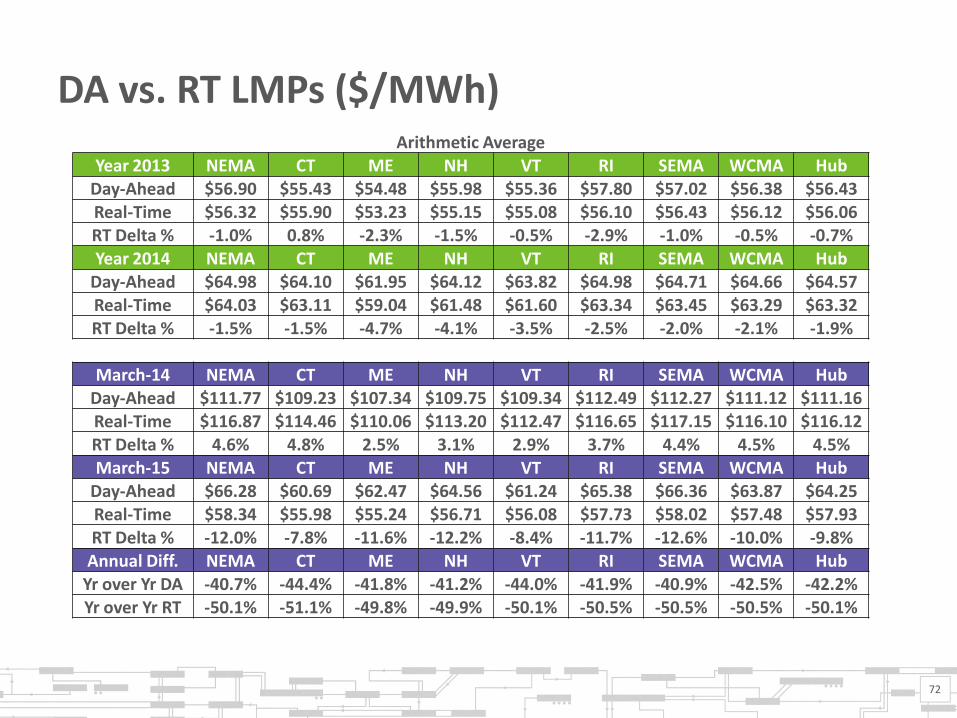

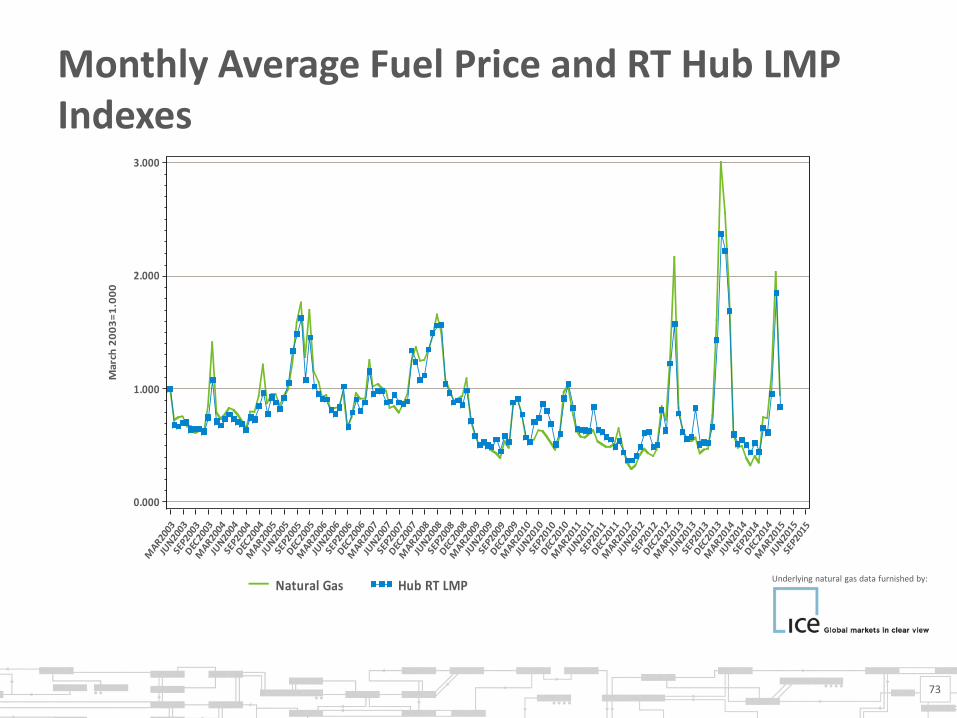

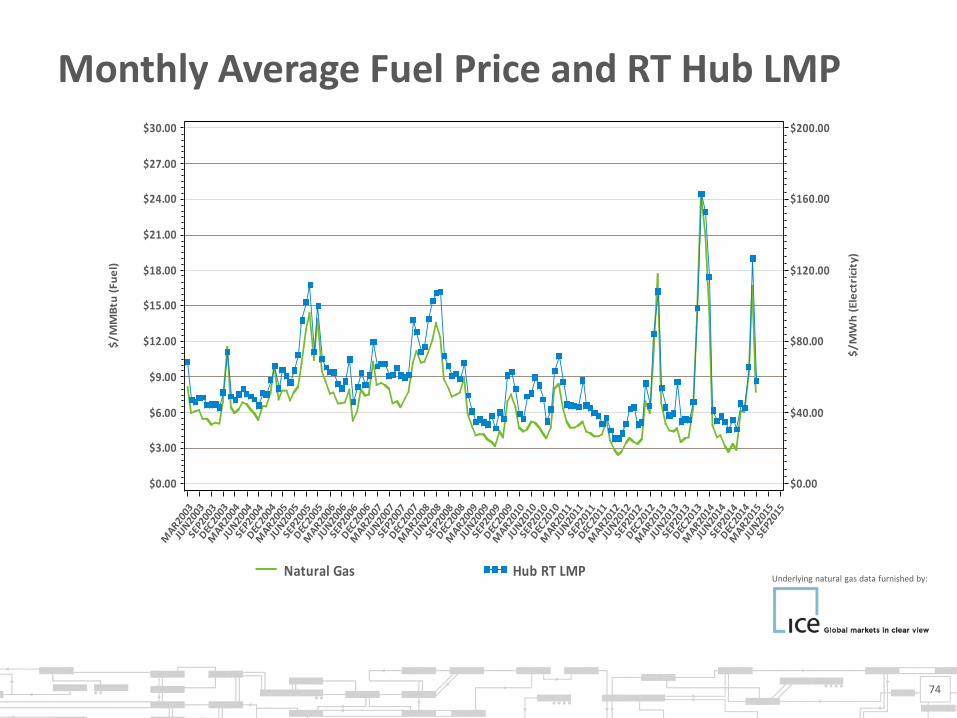

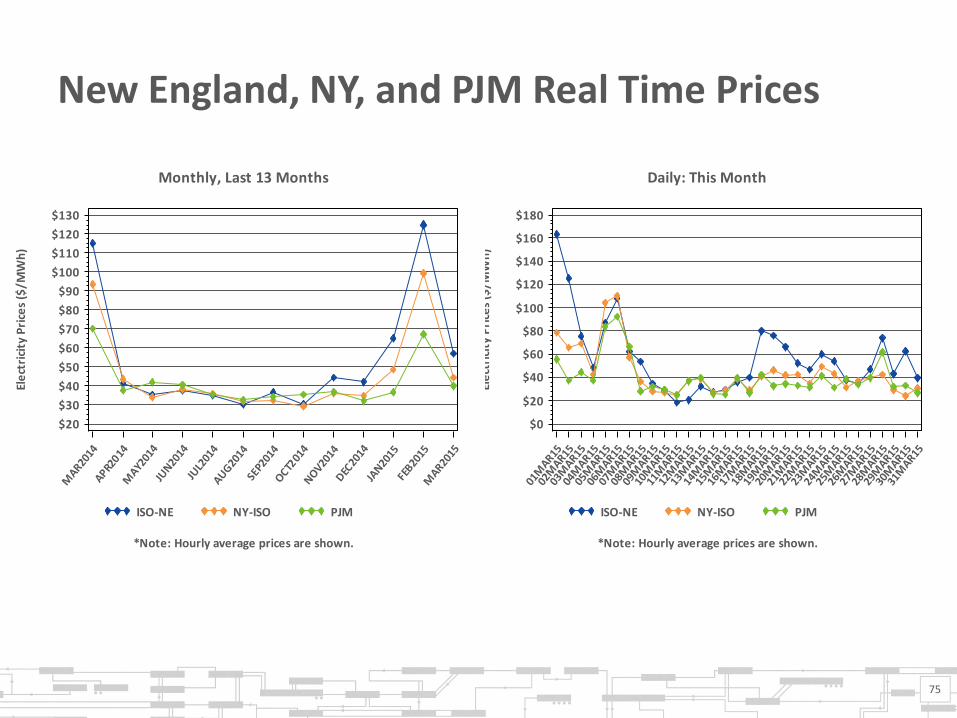

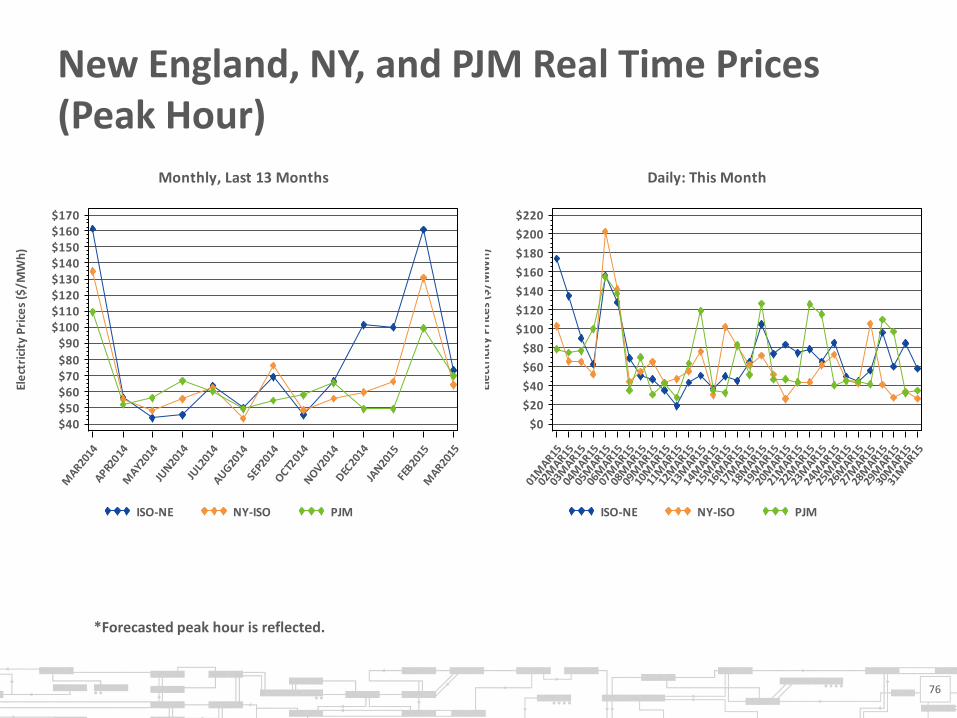

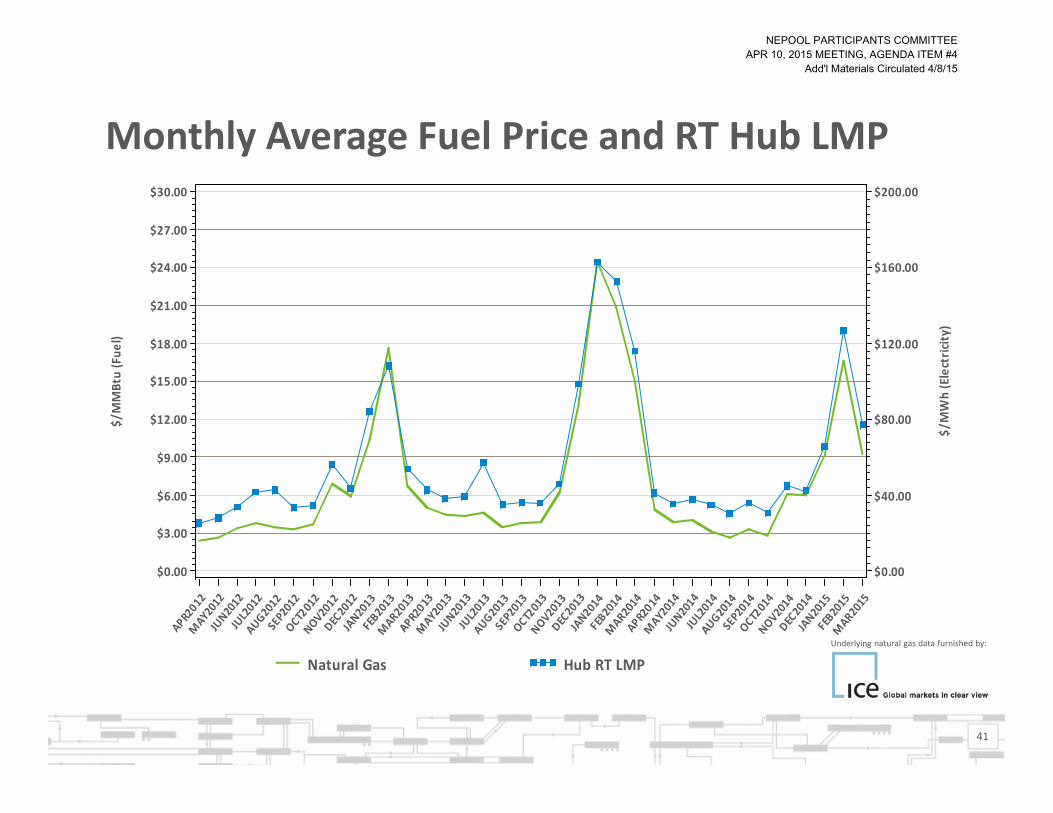

• Day-Ahead (DA), Real-Time (RT) Prices and Transactions

– Energy Market Value was $734M over the period, down $660M from February 2015 and down $584M from March 2014

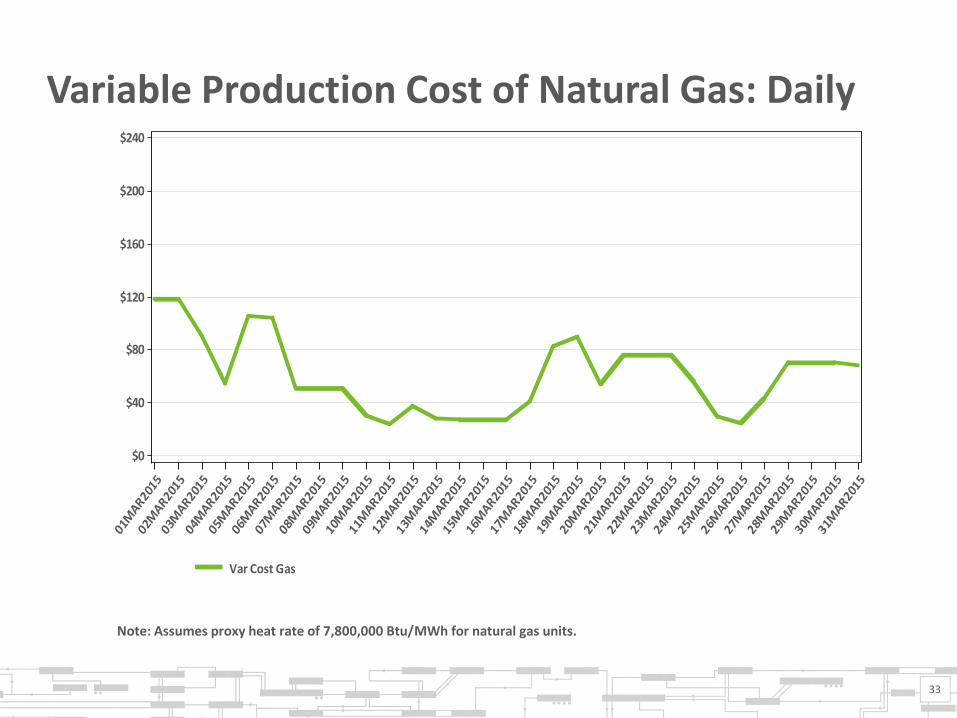

– March natural gas prices over the period were 53% lower than February 2015 average values

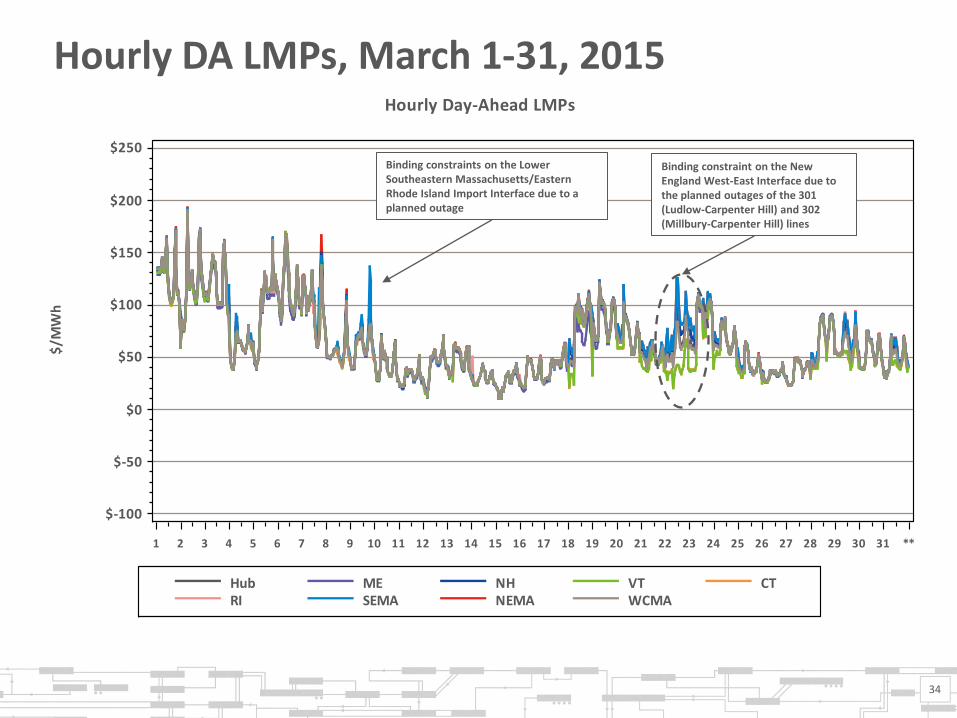

– Average RT Hub Locational Marginal Prices (LMPs) over the period were 54% lower than February 2015 averages

– Average March 2015 natural gas prices and RT Hub LMPs over the period were down 48% and 50%, respectively, from March 2014 averages

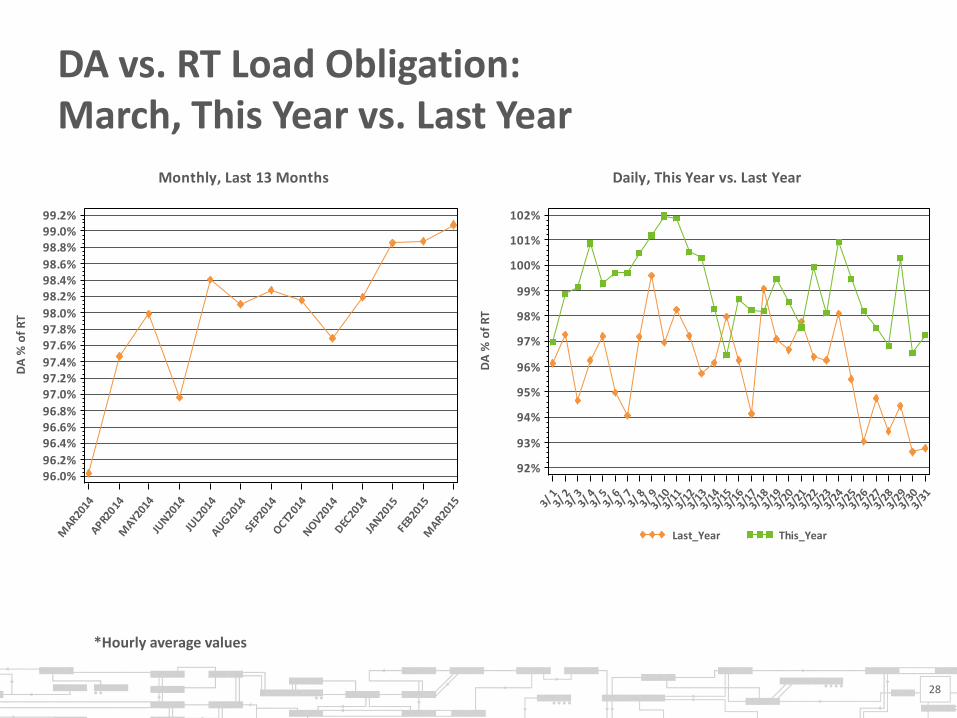

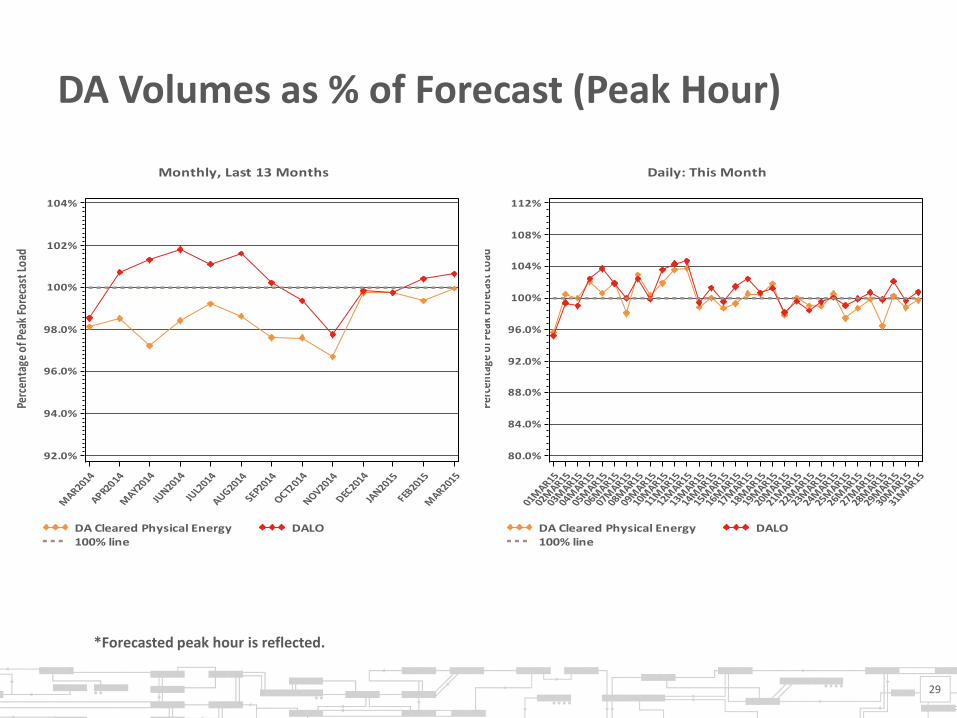

• Average DA cleared physical energy in the peak hours as percent of forecasted load was 99.9% during March, up from 99.4% during February

3

Underlying natural gas data furnished by:

*DA Cleared Physical Energy is the sum of Generation and Net Imports cleared in the DA Energy Market

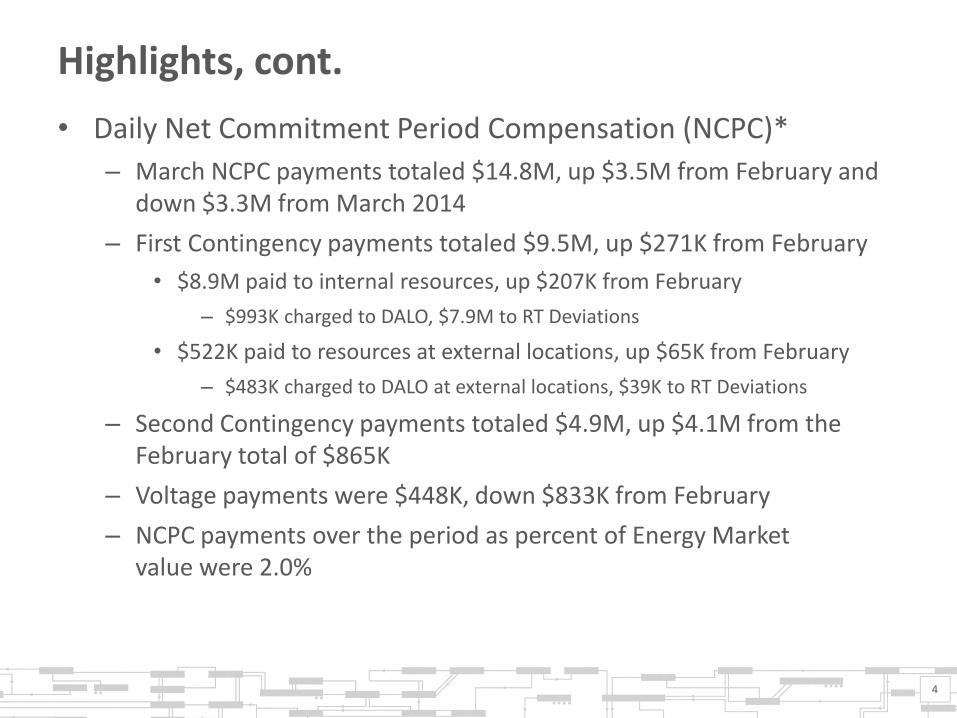

Highlights, cont.

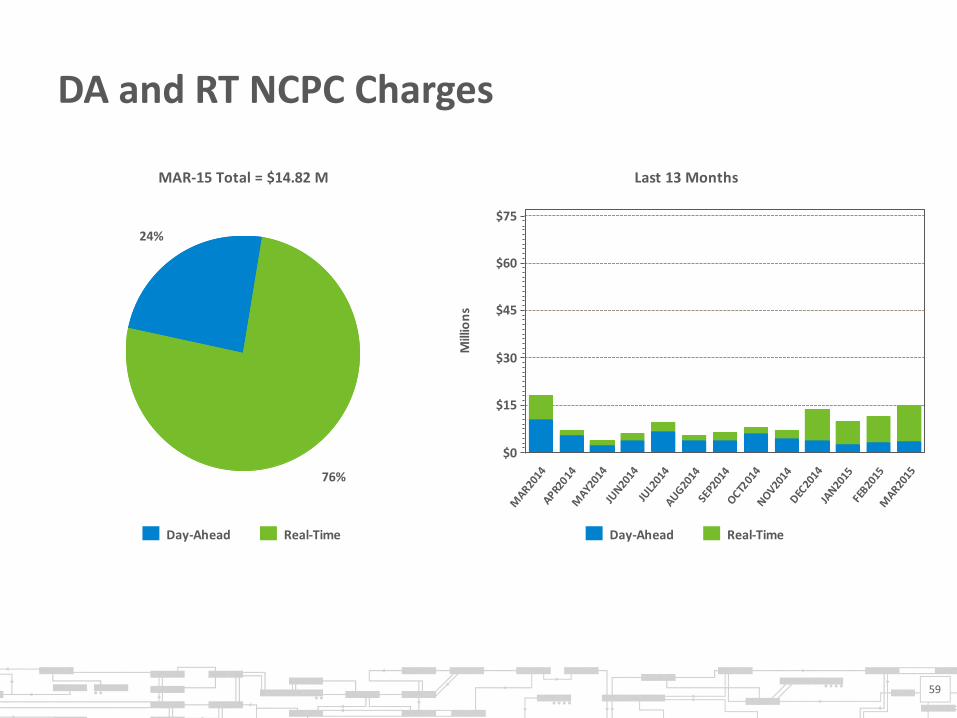

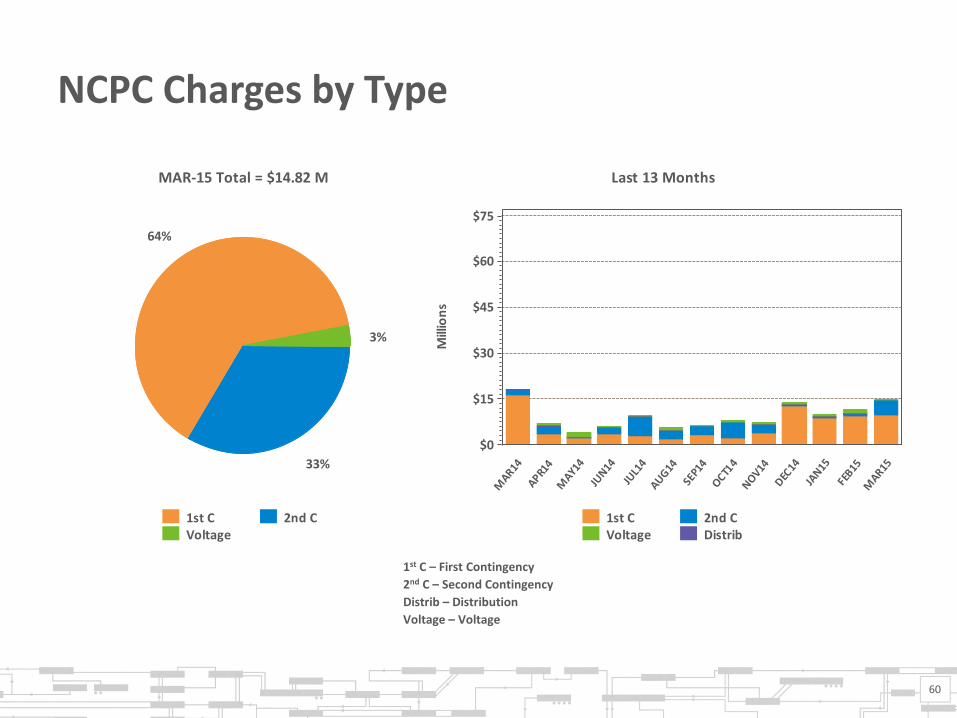

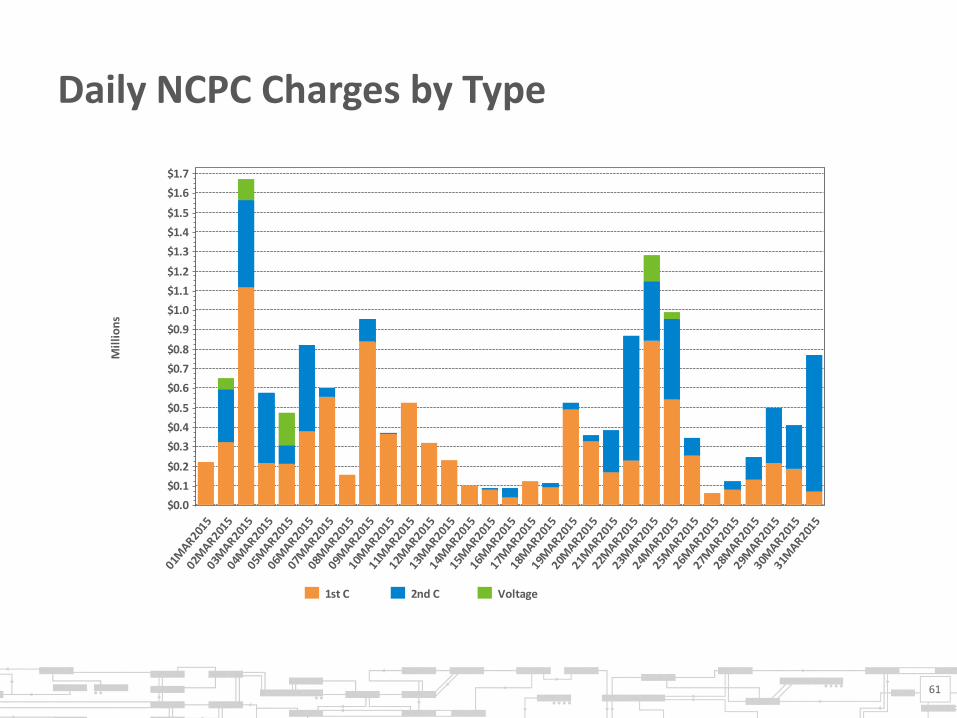

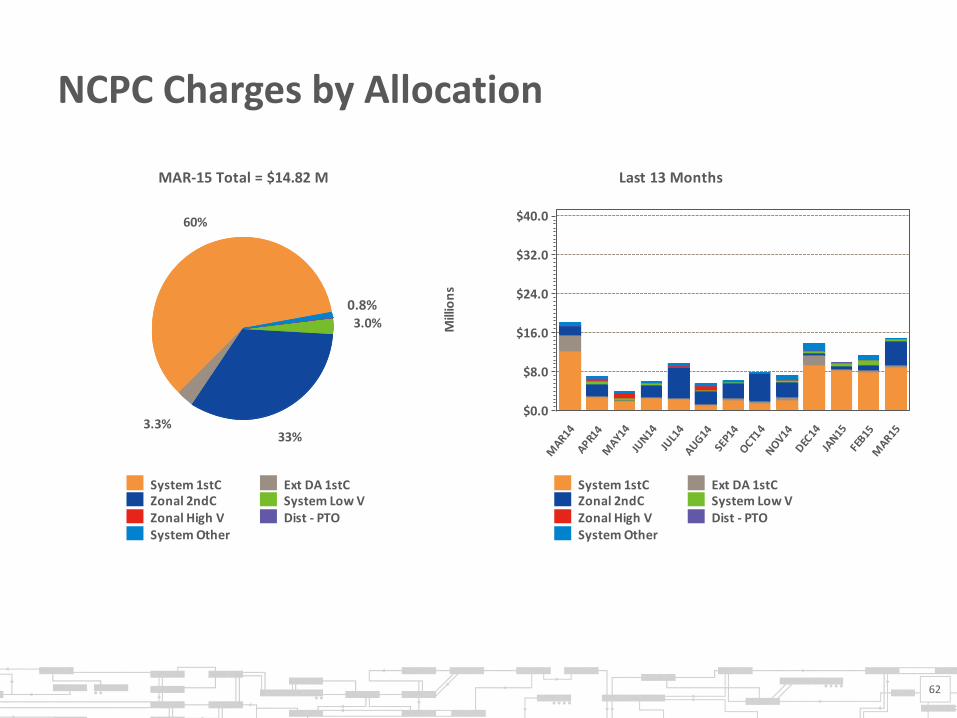

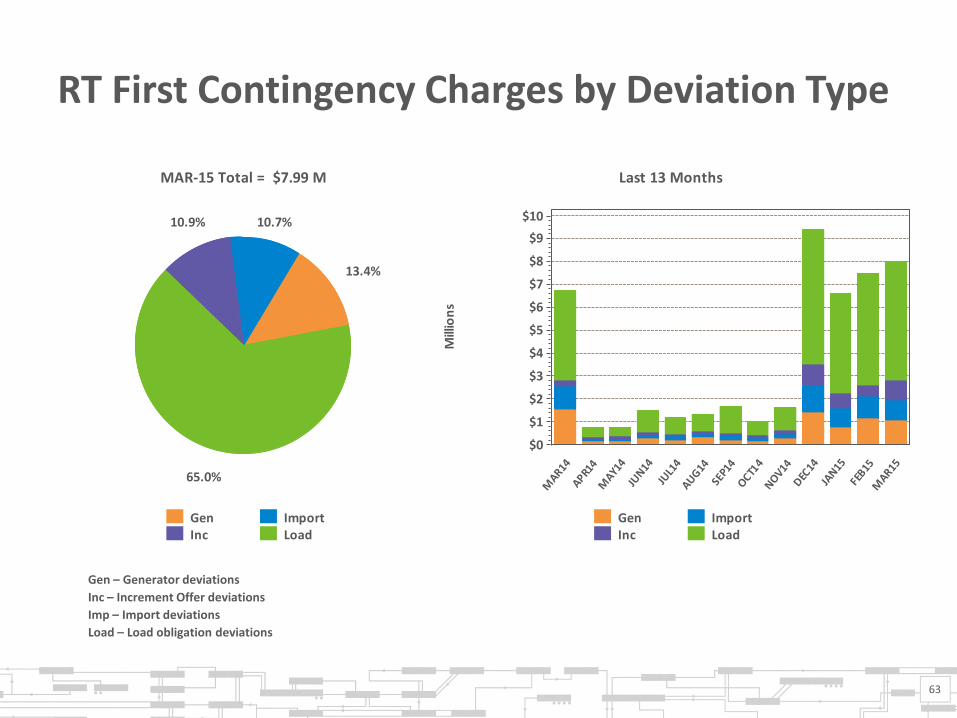

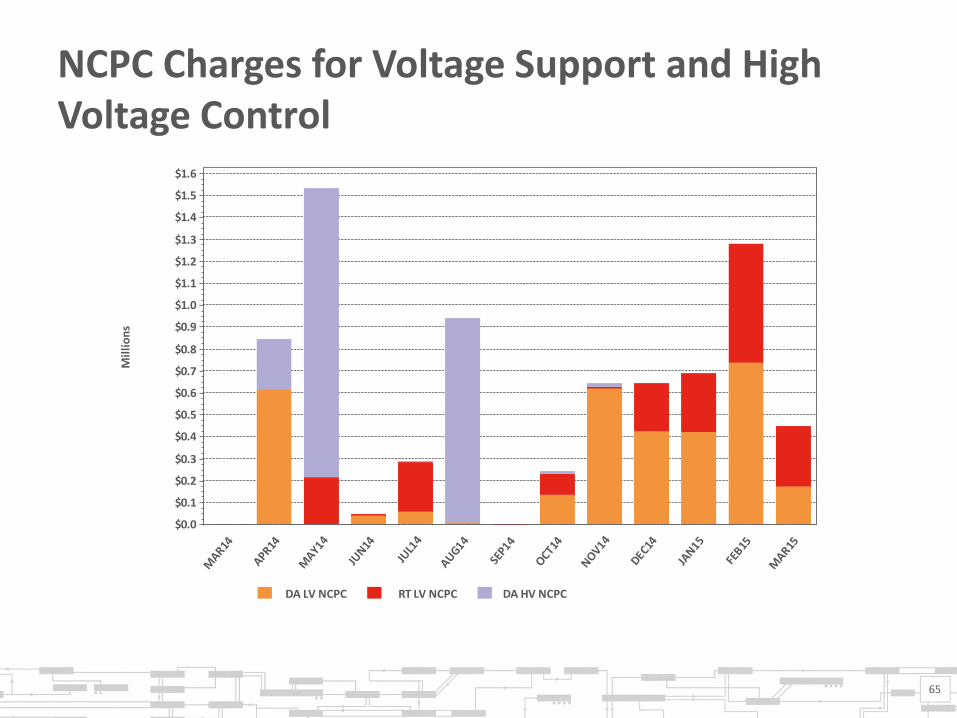

• Daily Net Commitment Period Compensation (NCPC)*

– March NCPC payments totaled $14.8M, up $3.5M from February and down $3.3M from March 2014

– First Contingency payments totaled $9.5M, up $271K from February

• $8.9M paid to internal resources, up $207K from February

– $993K charged to DALO, $7.9M to RT Deviations

• $522K paid to resources at external locations, up $65K from February

– $483K charged to DALO at external locations, $39K to RT Deviations

– Second Contingency payments totaled $4.9M, up $4.1M from the February total of $865K

– Voltage payments were $448K, down $833K from February

– NCPC payments over the period as percent of Energy Market value were 2.0%

4

Highlights, cont.

5

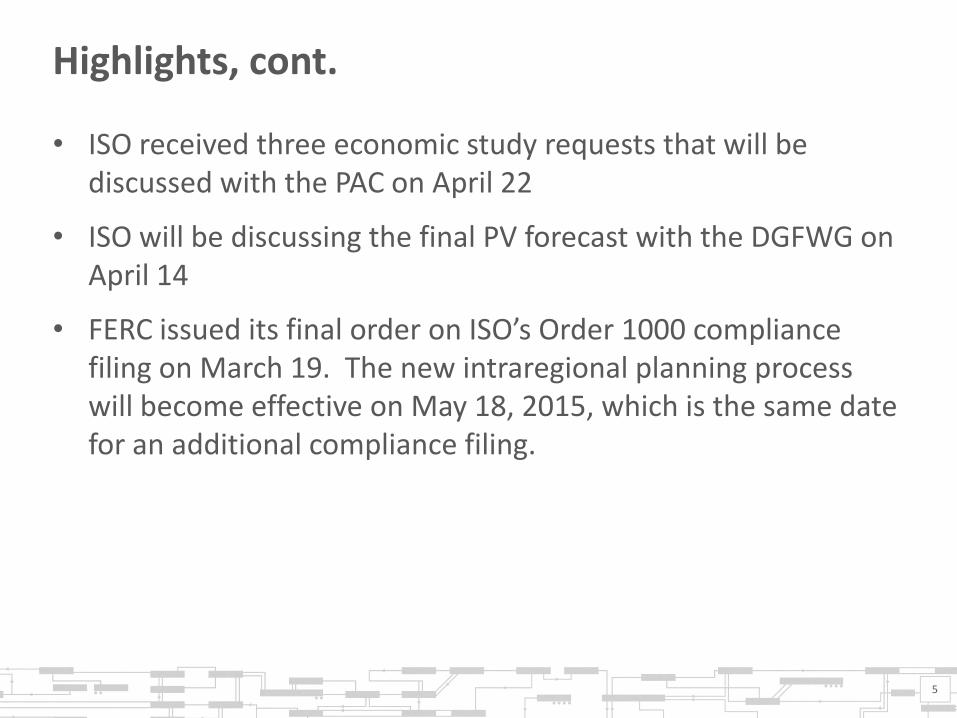

• ISO received three economic study requests that will be discussed with the PAC on April 22

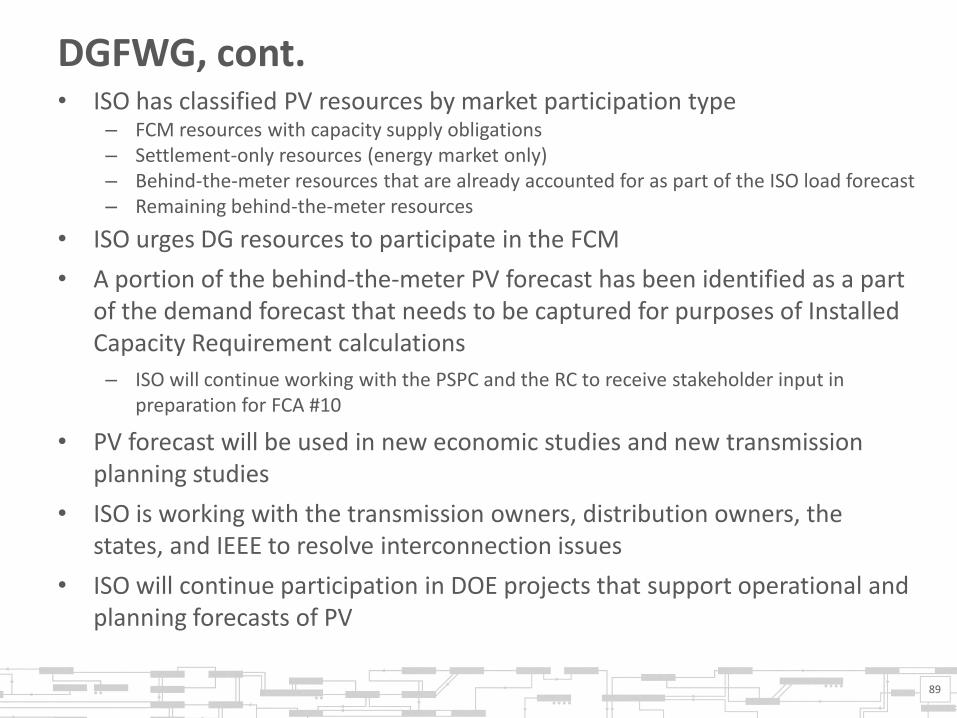

• ISO will be discussing the final PV forecast with the DGFWG on April 14

• FERC issued its final order on ISO’s Order 1000 compliance filing on March 19. The new intraregional planning process will become effective on May 18, 2015, which is the same date for an additional compliance filing.

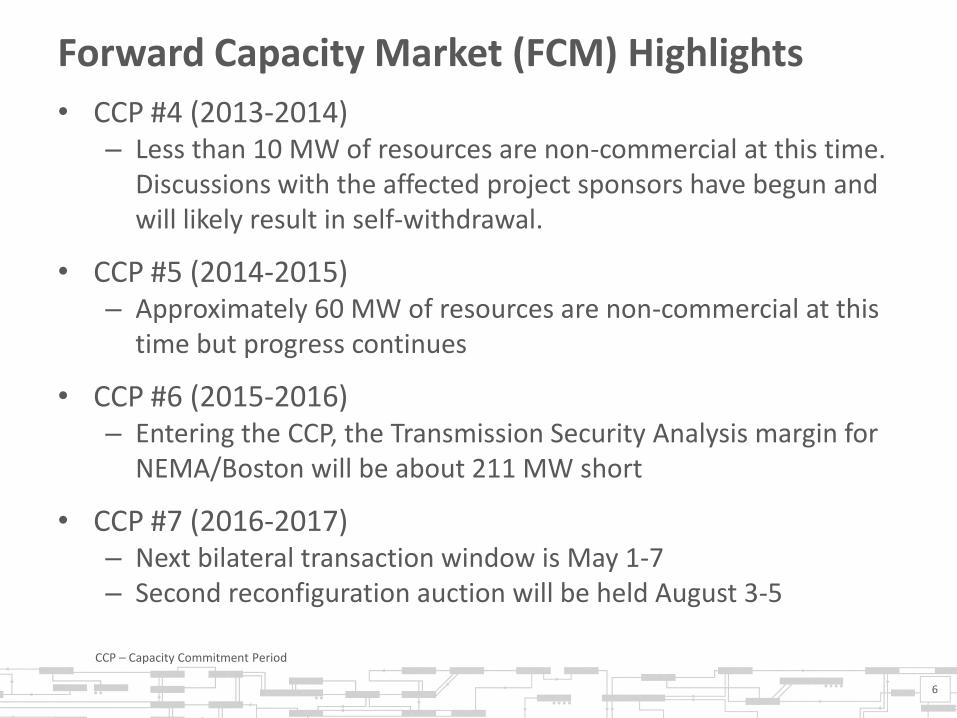

Forward Capacity Market (FCM) Highlights

6

CCP – Capacity Commitment Period

• CCP #4 (2013-2014) – Less than 10 MW of resources are non-commercial at this time.

Discussions with the affected project sponsors have begun and will likely result in self-withdrawal.

• CCP #5 (2014-2015) – Approximately 60 MW of resources are non-commercial at this

time but progress continues

• CCP #6 (2015-2016) – Entering the CCP, the Transmission Security Analysis margin for

NEMA/Boston will be about 211 MW short

• CCP #7 (2016-2017) – Next bilateral transaction window is May 1-7 – Second reconfiguration auction will be held August 3-5

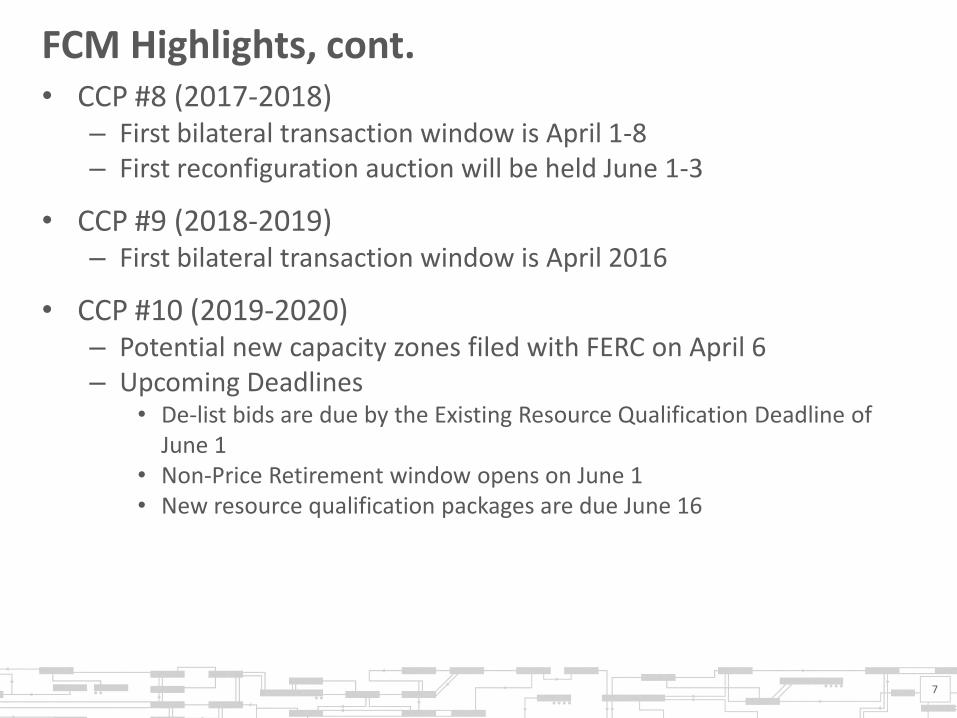

FCM Highlights, cont.

7

• CCP #8 (2017-2018) – First bilateral transaction window is April 1-8 – First reconfiguration auction will be held June 1-3

• CCP #9 (2018-2019) – First bilateral transaction window is April 2016

• CCP #10 (2019-2020) – Potential new capacity zones filed with FERC on April 6 – Upcoming Deadlines

• De-list bids are due by the Existing Resource Qualification Deadline of June 1

• Non-Price Retirement window opens on June 1 • New resource qualification packages are due June 16

Highlights, cont.

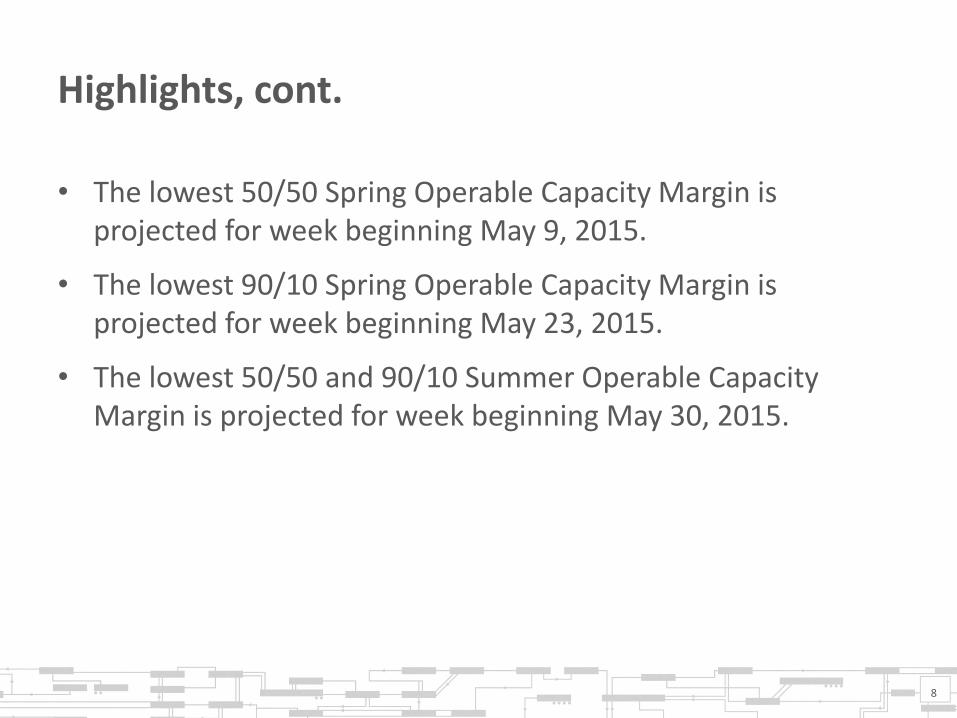

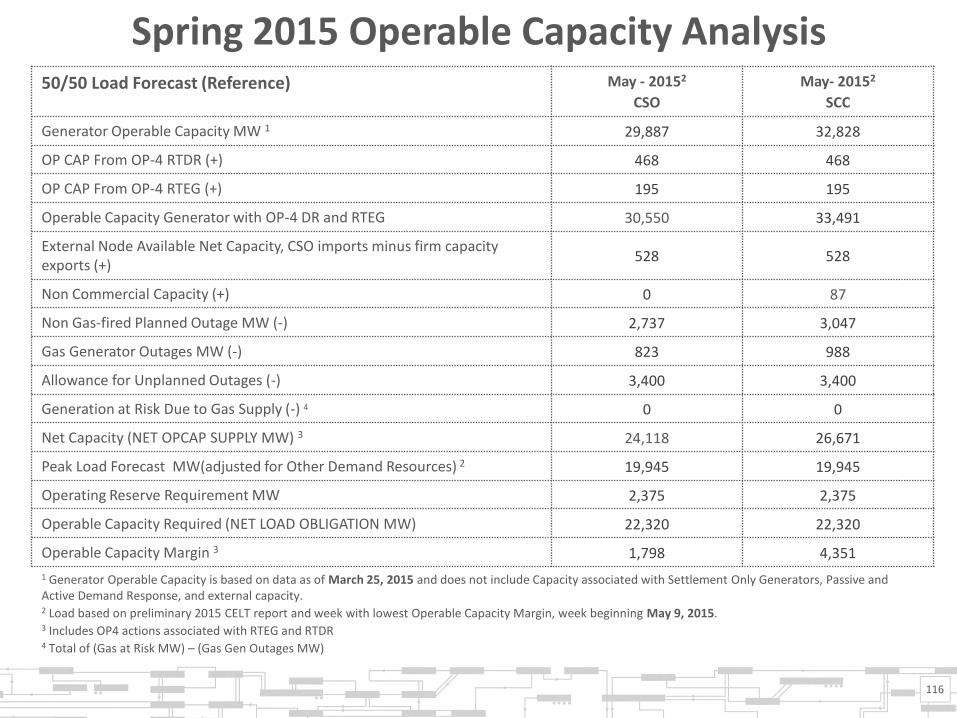

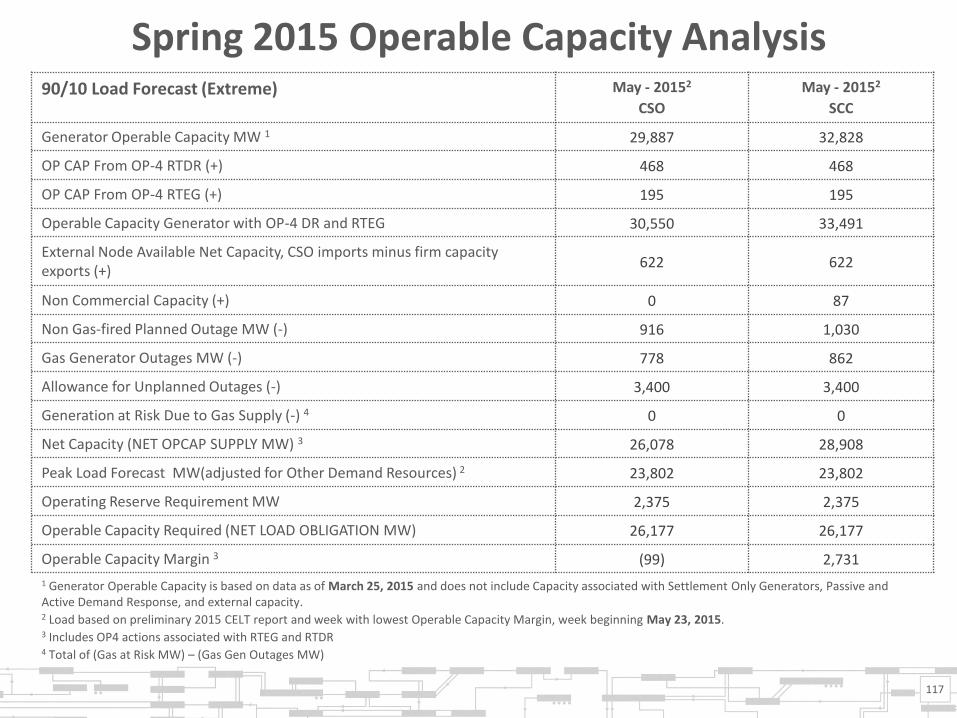

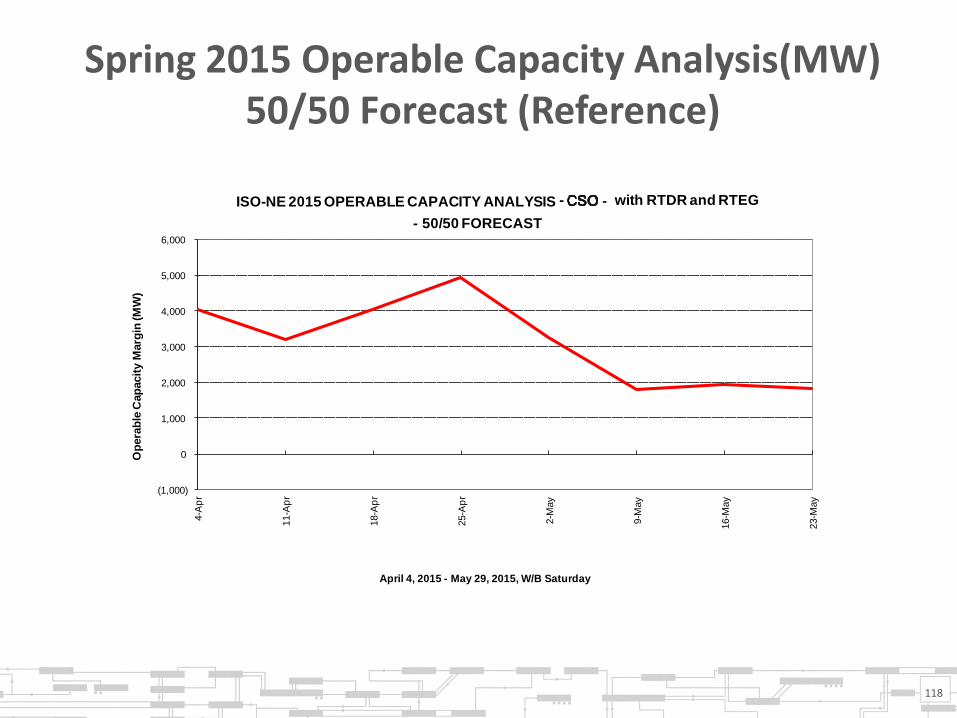

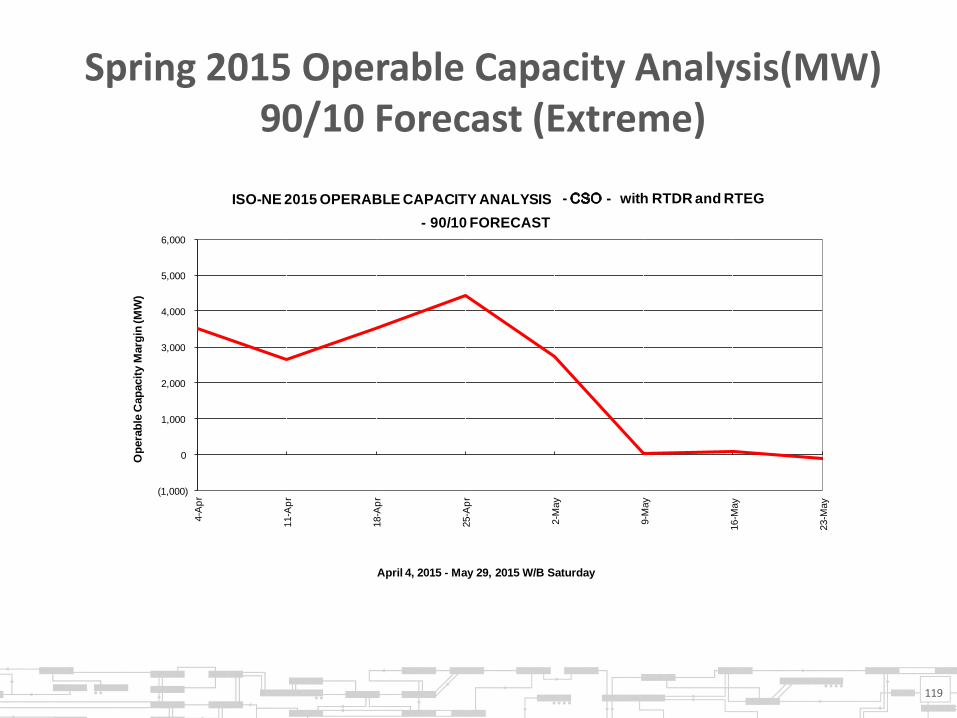

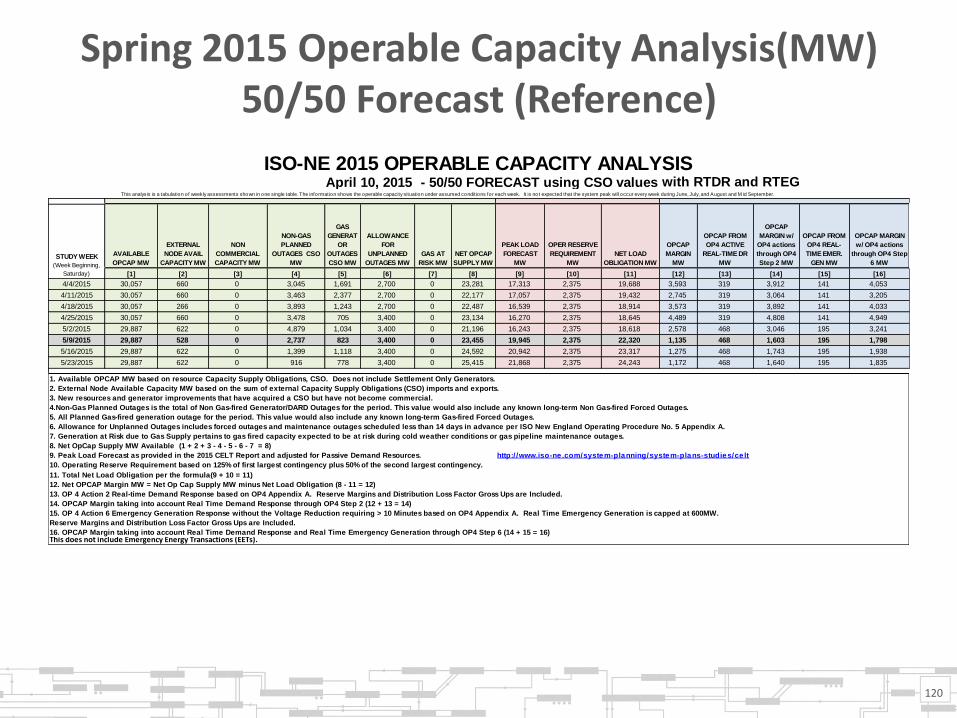

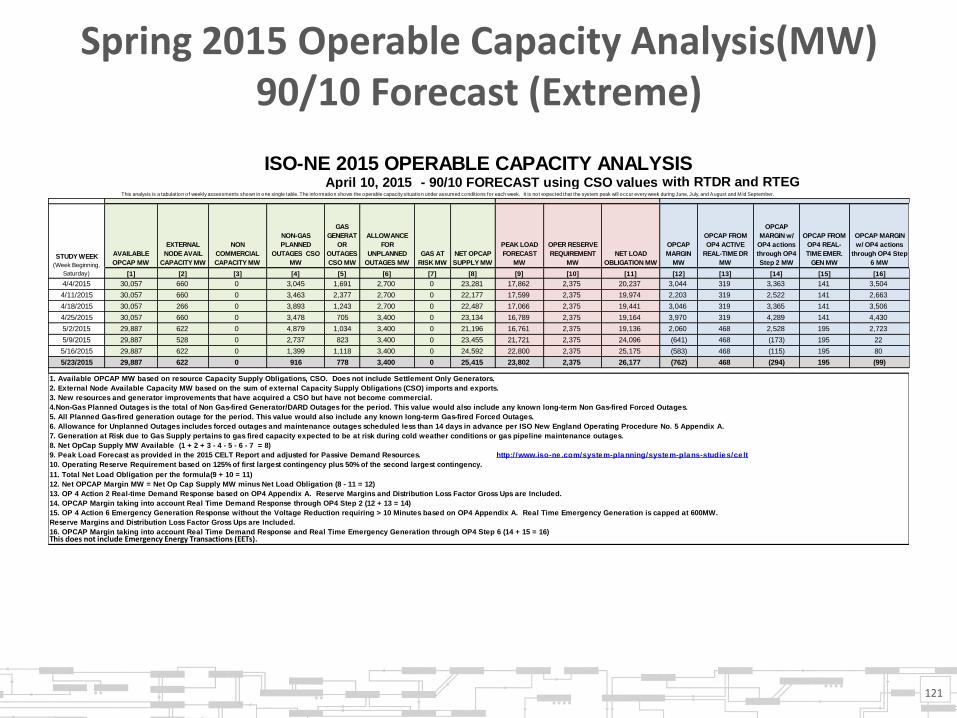

• The lowest 50/50 Spring Operable Capacity Margin is projected for week beginning May 9, 2015.

• The lowest 90/10 Spring Operable Capacity Margin is projected for week beginning May 23, 2015.

• The lowest 50/50 and 90/10 Summer Operable Capacity Margin is projected for week beginning May 30, 2015.

8

SYSTEM OPERATIONS

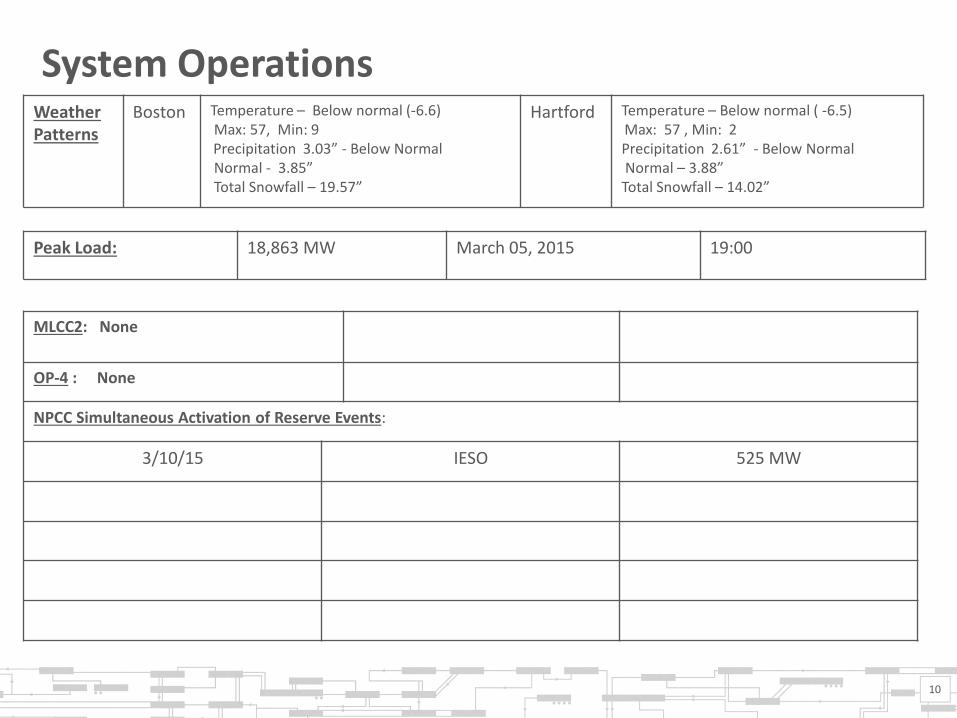

System Operations Weather Patterns

Boston Temperature – Below normal (-6.6) Max: 57, Min: 9 Precipitation 3.03” - Below Normal Normal - 3.85” Total Snowfall – 19.57”

Hartford Temperature – Below normal ( -6.5) Max: 57 , Min: 2

Precipitation 2.61” - Below Normal Normal – 3.88”

Total Snowfall – 14.02”

10

Peak Load: 18,863 MW March 05, 2015 19:00

MLCC2: None

OP-4 : None

NPCC Simultaneous Activation of Reserve Events:

3/10/15 IESO 525 MW

System Operations, cont.

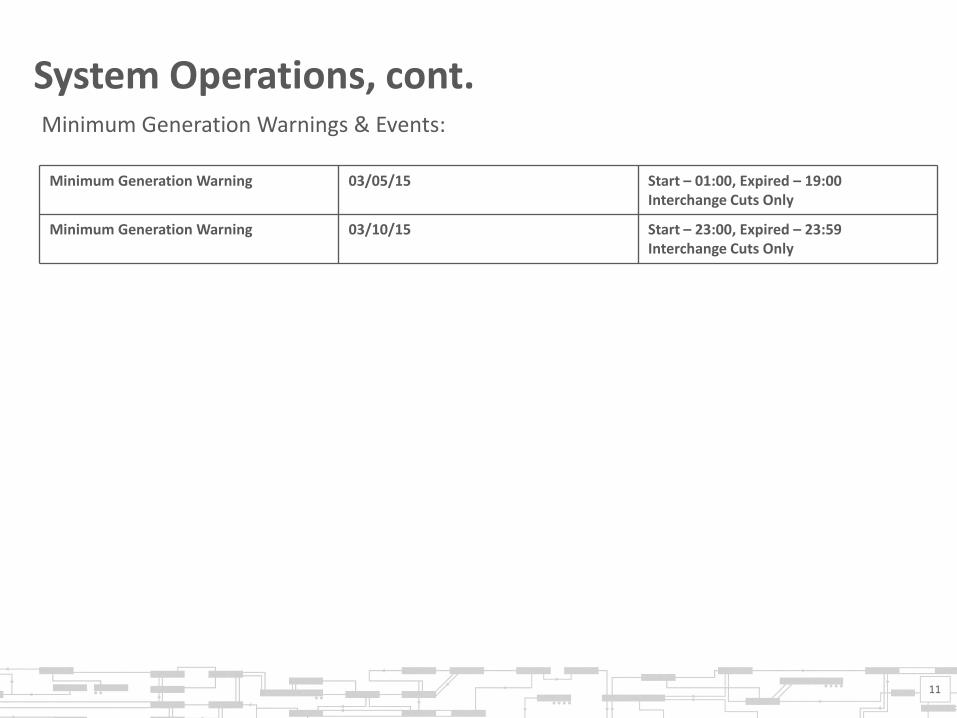

11

Minimum Generation Warnings & Events:

Minimum Generation Warning 03/05/15 Start – 01:00, Expired – 19:00 Interchange Cuts Only

Minimum Generation Warning 03/10/15 Start – 23:00, Expired – 23:59 Interchange Cuts Only

12

0.0

2.0

4.0

6.0

8.0

10.0

J F M A M J J A S O N D Cum. Avg

% E

rro

r

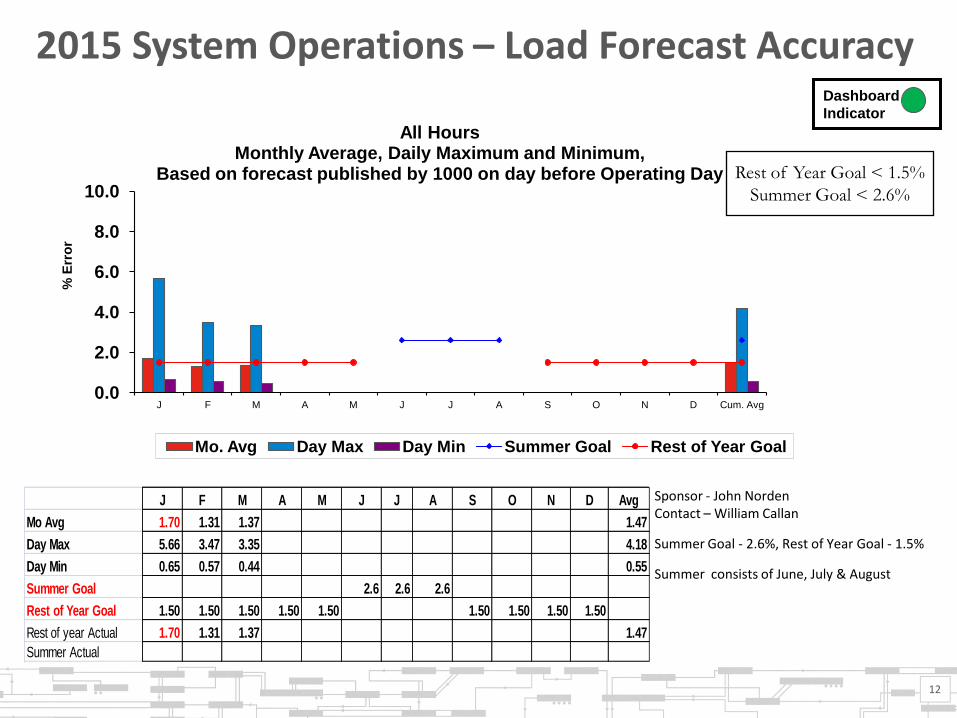

All Hours Monthly Average, Daily Maximum and Minimum,

Based on forecast published by 1000 on day before Operating Day

Mo. Avg Day Max Day Min Summer Goal Rest of Year Goal

2015 System Operations – Load Forecast Accuracy Dashboard

Indicator

J F M A M J J A S O N D Avg

Mo Avg 1.70 1.31 1.37 1.47

Day Max 5.66 3.47 3.35 4.18

Day Min 0.65 0.57 0.44 0.55

Summer Goal 2.6 2.6 2.6

Rest of Year Goal 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50

Rest of year Actual 1.70 1.31 1.37 1.47

Summer Actual

Rest of Year Goal < 1.5%

Summer Goal < 2.6%

Sponsor - John Norden Contact – William Callan

Summer Goal - 2.6%, Rest of Year Goal - 1.5%

Summer consists of June, July & August

13

0.0

2.0

4.0

6.0

8.0

10.0

12.0

J F M A M J J A S O N D Cum. Avg

% E

rro

r

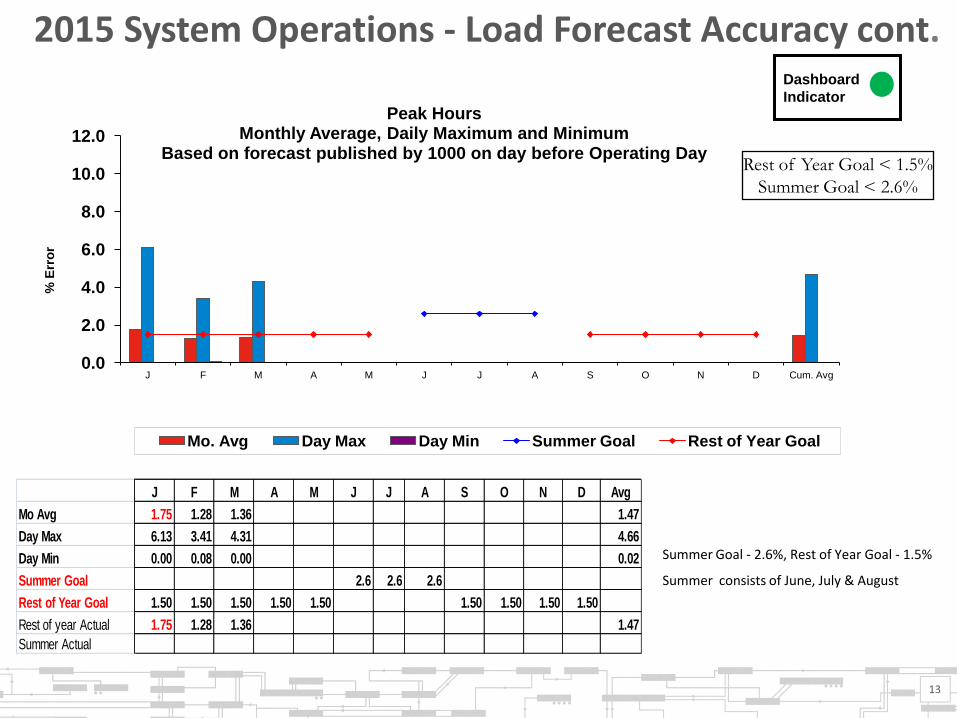

Peak Hours Monthly Average, Daily Maximum and Minimum

Based on forecast published by 1000 on day before Operating Day

Mo. Avg Day Max Day Min Summer Goal Rest of Year Goal

2015 System Operations - Load Forecast Accuracy cont. Dashboard

Indicator

Rest of Year Goal < 1.5%

Summer Goal < 2.6%

Summer Goal - 2.6%, Rest of Year Goal - 1.5%

Summer consists of June, July & August

J F M A M J J A S O N D Avg

Mo Avg 1.75 1.28 1.36 1.47

Day Max 6.13 3.41 4.31 4.66

Day Min 0.00 0.08 0.00 0.02

Summer Goal 2.6 2.6 2.6

Rest of Year Goal 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50 1.50

Rest of year Actual 1.75 1.28 1.36 1.47

Summer Actual

14

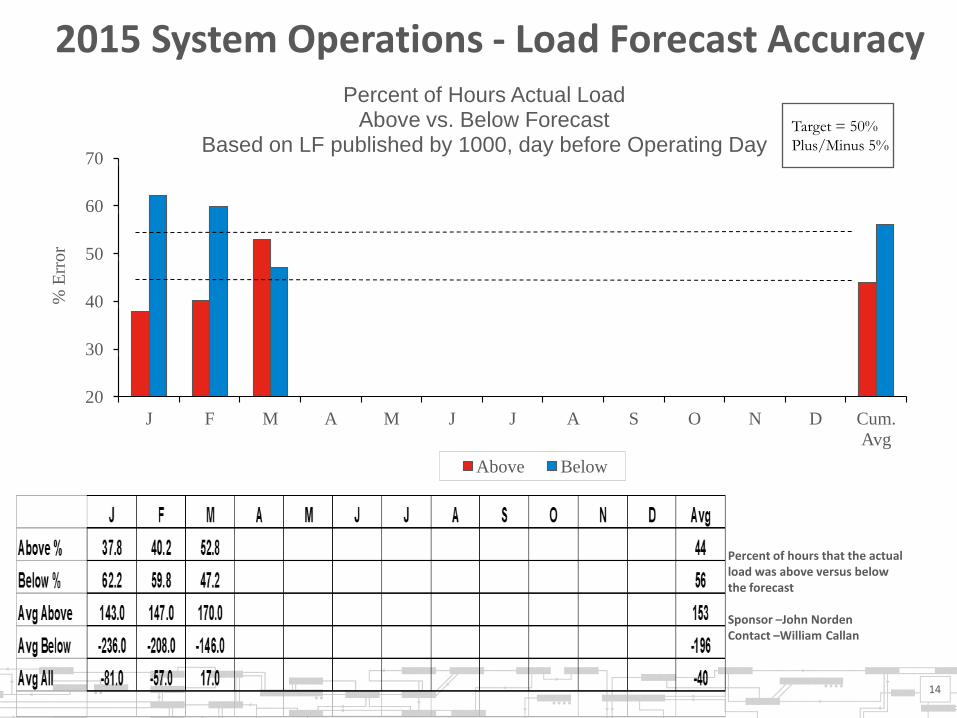

20

30

40

50

60

70

J F M A M J J A S O N D Cum.

Avg

% E

rro

r

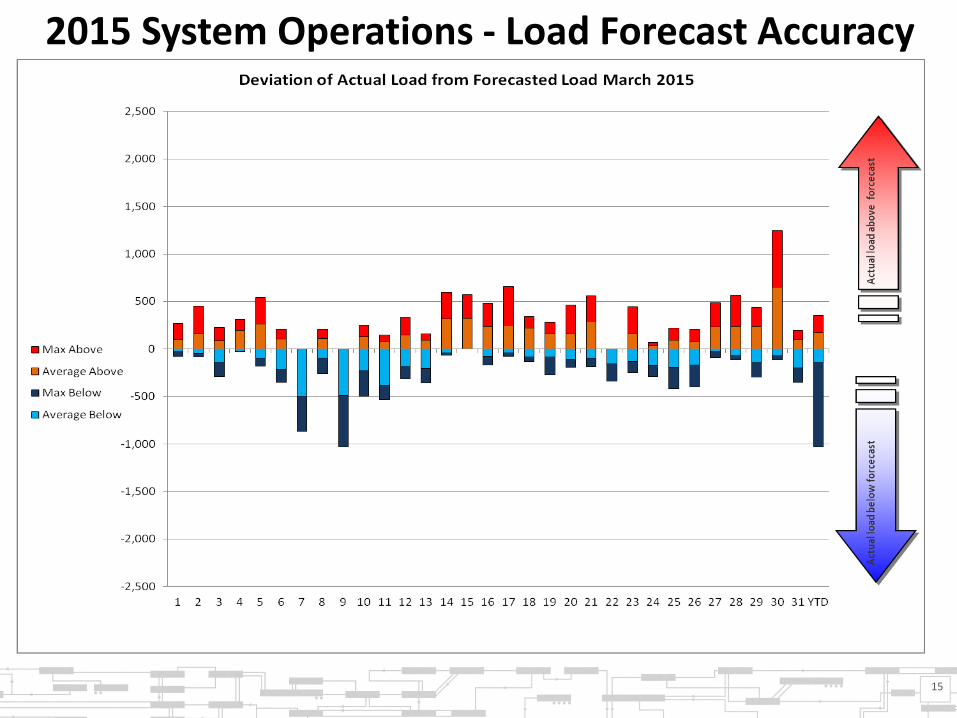

Percent of Hours Actual Load Above vs. Below Forecast

Based on LF published by 1000, day before Operating Day

Above Below

2015 System Operations - Load Forecast Accuracy

Target = 50%

Plus/Minus 5%

Percent of hours that the actual load was above versus below the forecast Sponsor –John Norden Contact –William Callan

15

2015 System Operations - Load Forecast Accuracy

Sponsor –John Norden Contact – William Callan

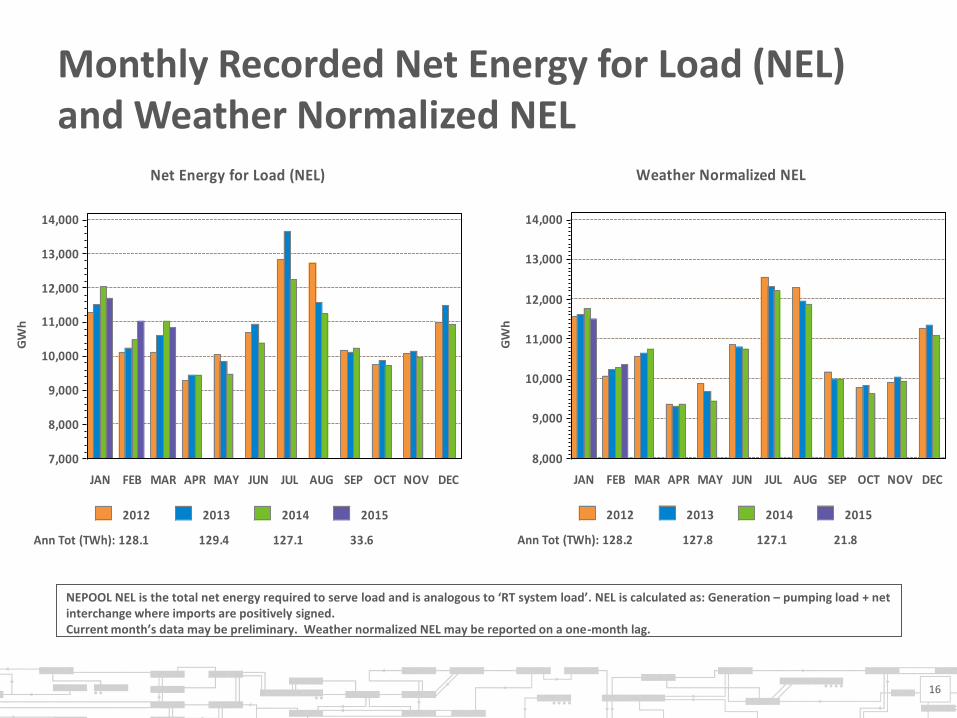

GR:wnnel GR:nel

Ann Tot (TWh): 128.2 127.8 127.1 21.8

Weather Normalized NEL

2012 2013 2014 2015G

Wh

8,000

9,000

10,000

11,000

12,000

13,000

14,000

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Ann Tot (TWh): 128.1 129.4 127.1 33.6

Net Energy for Load (NEL)

2012 2013 2014 2015

GW

h

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Monthly Recorded Net Energy for Load (NEL) and Weather Normalized NEL

16

NEPOOL NEL is the total net energy required to serve load and is analogous to ‘RT system load’. NEL is calculated as: Generation – pumping load + net interchange where imports are positively signed. Current month’s data may be preliminary. Weather normalized NEL may be reported on a one-month lag.

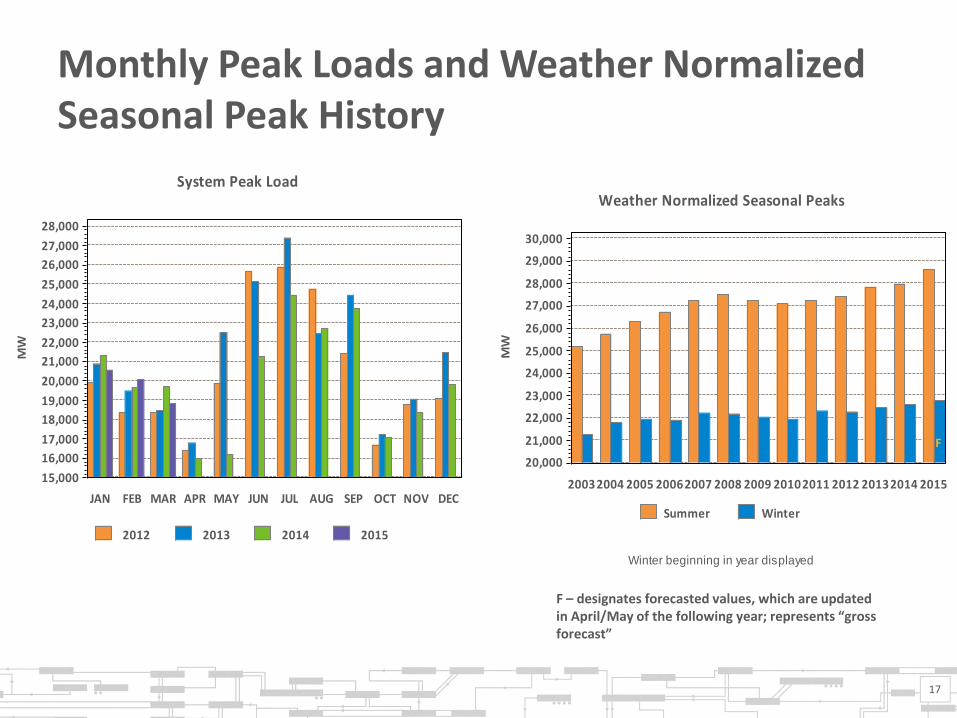

GR:SeasonalPeak GR:PeakEnergy

Weather Normalized Seasonal Peaks

Winter beginning in year displayed

Summer WinterM

W

20,000

21,000

22,000

23,000

24,000

25,000

26,000

27,000

28,000

29,000

30,000

20032004 2005 20062007 2008 2009 20102011 2012 20132014 2015

System Peak Load

2012 2013 2014 2015

MW

15,000

16,000

17,000

18,000

19,000

20,000

21,000

22,000

23,000

24,000

25,000

26,000

27,000

28,000

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Monthly Peak Loads and Weather Normalized Seasonal Peak History

17

F – designates forecasted values, which are updated in April/May of the following year; represents “gross forecast”

F

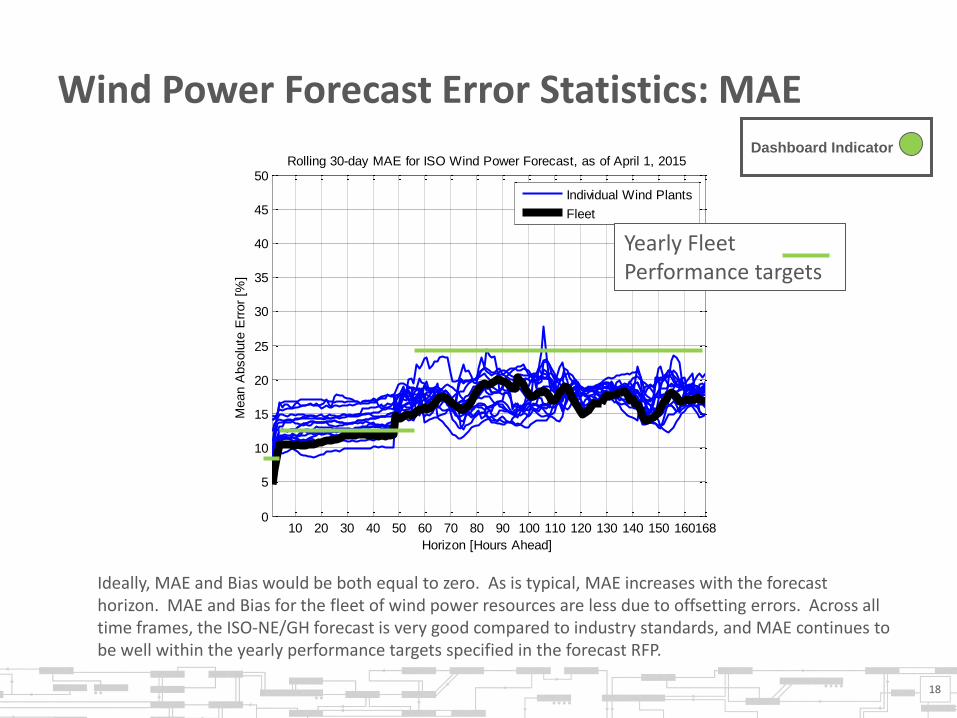

10 20 30 40 50 60 70 80 90 100 110 120 130 140 150 1601680

5

10

15

20

25

30

35

40

45

50

Horizon [Hours Ahead]

Mean A

bsolu

te E

rror

[%]

Rolling 30-day MAE for ISO Wind Power Forecast, as of April 1, 2015

Individual Wind Plants

Fleet

Wind Power Forecast Error Statistics: MAE

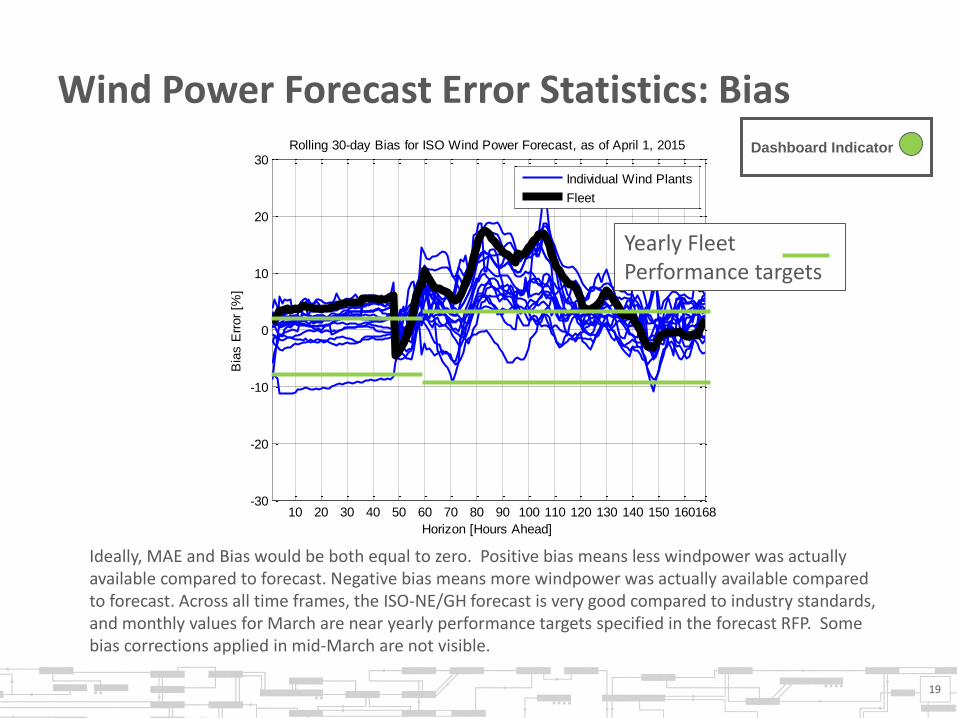

Ideally, MAE and Bias would be both equal to zero. As is typical, MAE increases with the forecast horizon. MAE and Bias for the fleet of wind power resources are less due to offsetting errors. Across all time frames, the ISO-NE/GH forecast is very good compared to industry standards, and MAE continues to be well within the yearly performance targets specified in the forecast RFP.

Dashboard Indicator

Yearly Fleet Performance targets

18

10 20 30 40 50 60 70 80 90 100 110 120 130 140 150 160168-30

-20

-10

0

10

20

30

Horizon [Hours Ahead]

Bia

s E

rror

[%]

Rolling 30-day Bias for ISO Wind Power Forecast, as of April 1, 2015

Individual Wind Plants

Fleet

Wind Power Forecast Error Statistics: Bias Dashboard Indicator

Ideally, MAE and Bias would be both equal to zero. Positive bias means less windpower was actually available compared to forecast. Negative bias means more windpower was actually available compared to forecast. Across all time frames, the ISO-NE/GH forecast is very good compared to industry standards, and monthly values for March are near yearly performance targets specified in the forecast RFP. Some bias corrections applied in mid-March are not visible.

Yearly Fleet Performance targets

19

MARKET OPERATIONS

GR:Hubwgas

Ele

ctri

city

Pri

ces

($/M

Wh

)

$0.00

$50.00

$100.00

$150.00

$200.00

$250.0003/

01/1

503/

03/1

503/

05/1

503/

07/1

503/

09/1

503/

11/1

503/

13/1

503/

15/1

503/

17/1

503/

19/1

503/

21/1

503/

23/1

503/

25/1

503/

27/1

503/

29/1

503/

31/1

5

Fue

l Pri

ce (

$/M

MB

tu)

$0.00

$7.00

$14.00

$21.00

$28.00

$35.00

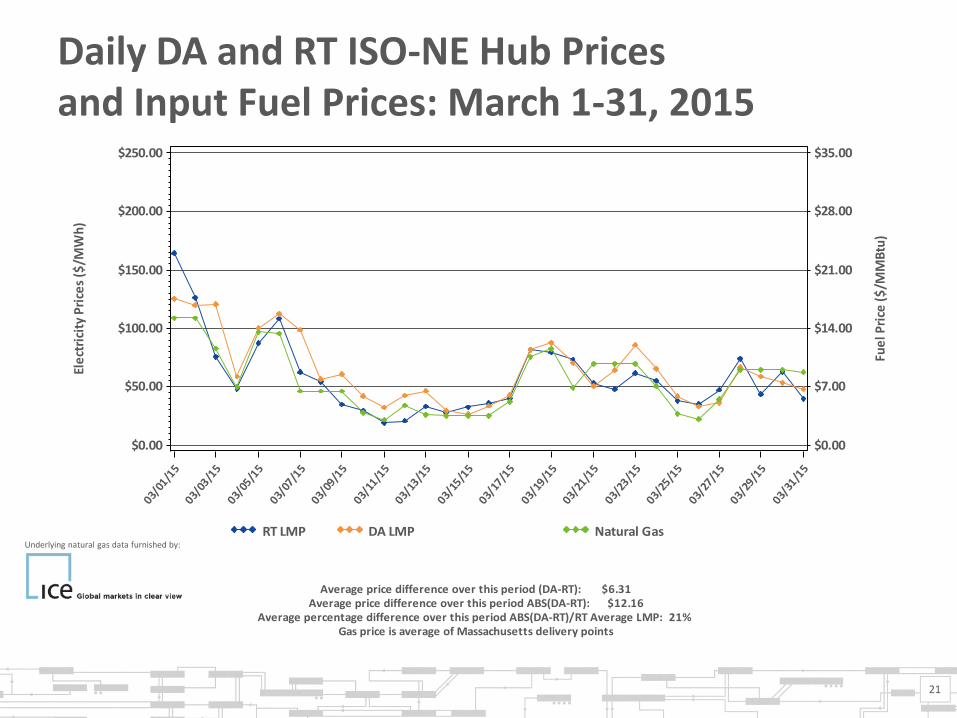

Gas price is average of Massachusetts delivery pointsAverage percentage difference over this period ABS(DA-RT)/RT Average LMP: 21%

Average price difference over this period ABS(DA-RT): $12.16Average price difference over this period (DA-RT): $6.31

RT LMP DA LMP Natural Gas

Daily DA and RT ISO-NE Hub Prices and Input Fuel Prices: March 1-31, 2015

21

Underlying natural gas data furnished by:

GR:DA_Bar

LMP Congestion Marginal Losses

$/M

Wh

$-20

$0

$20

$40

$60

$80

$100

$120

$140

Hub ME NH VT CT RI SEMA WCMA NEMA

( 2.8%) 0.5% ( 4.7%) ( 5.5%) 1.8% 3.3% ( 0.6%) 3.2%

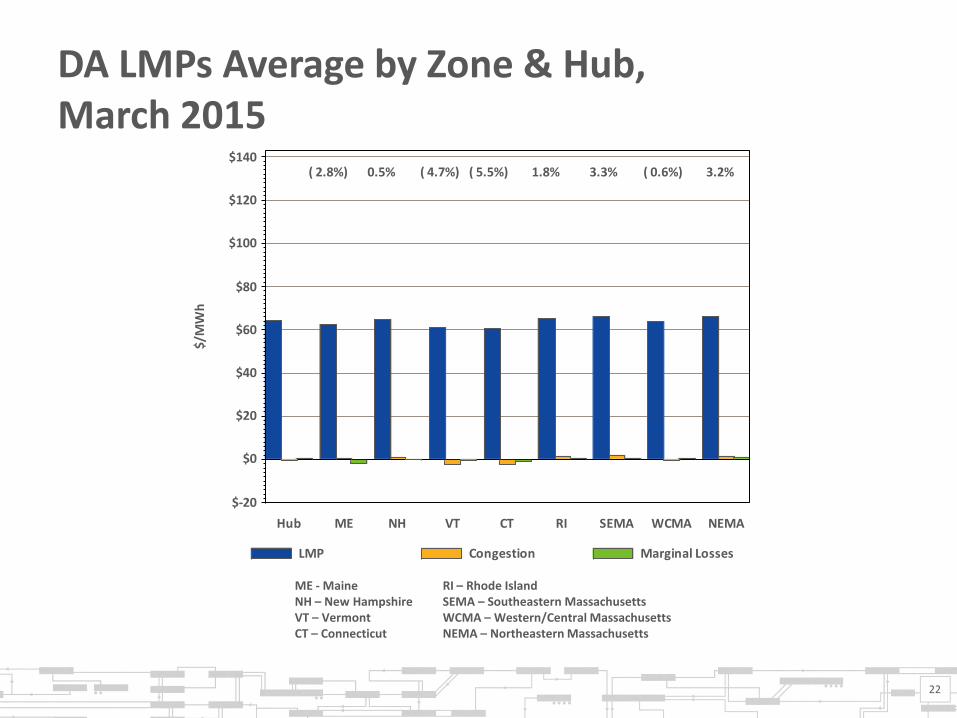

DA LMPs Average by Zone & Hub, March 2015

22

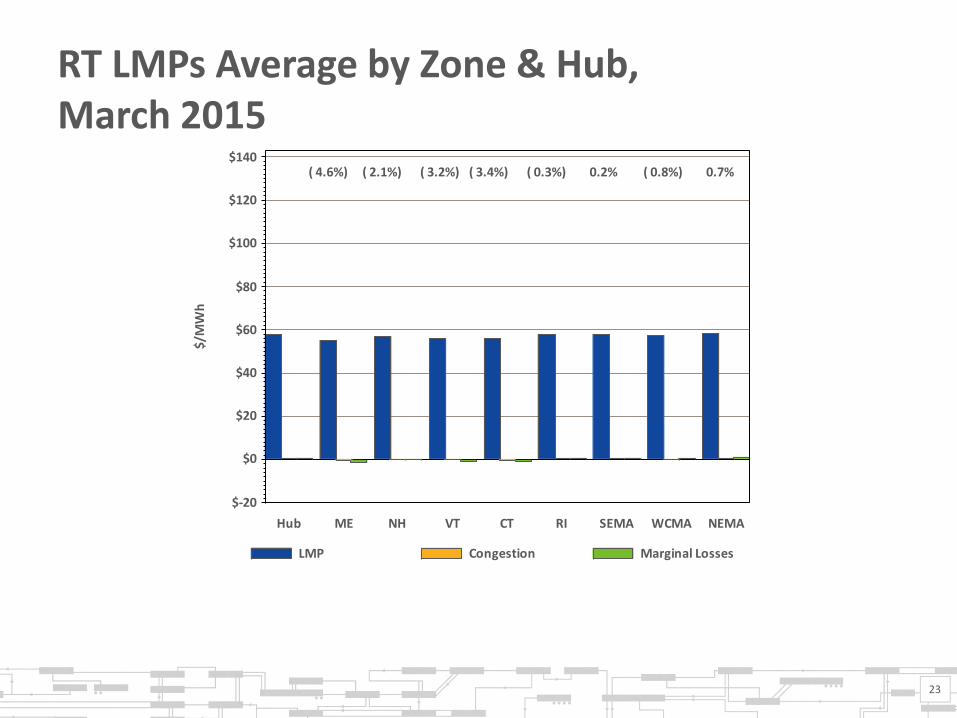

ME - Maine NH – New Hampshire VT – Vermont CT – Connecticut

RI – Rhode Island SEMA – Southeastern Massachusetts WCMA – Western/Central Massachusetts NEMA – Northeastern Massachusetts

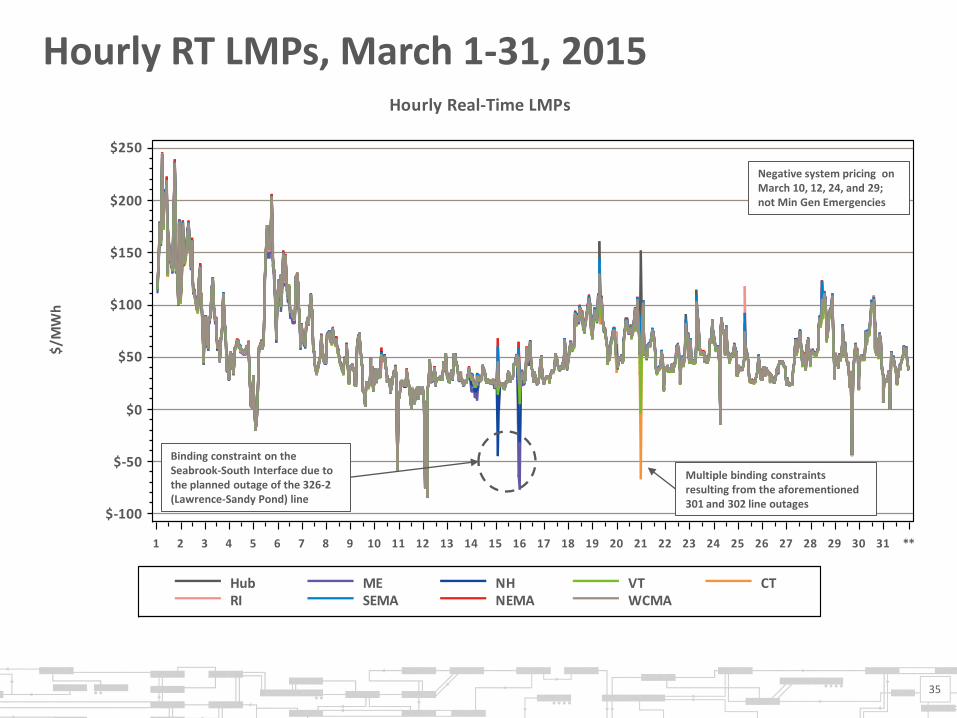

GR:RT_Bar

LMP Congestion Marginal Losses

$/M

Wh

$-20

$0

$20

$40

$60

$80

$100

$120

$140

Hub ME NH VT CT RI SEMA WCMA NEMA

( 4.6%) ( 2.1%) ( 3.2%) ( 3.4%) ( 0.3%) 0.2% ( 0.8%) 0.7%

RT LMPs Average by Zone & Hub, March 2015

23

Definitions

24

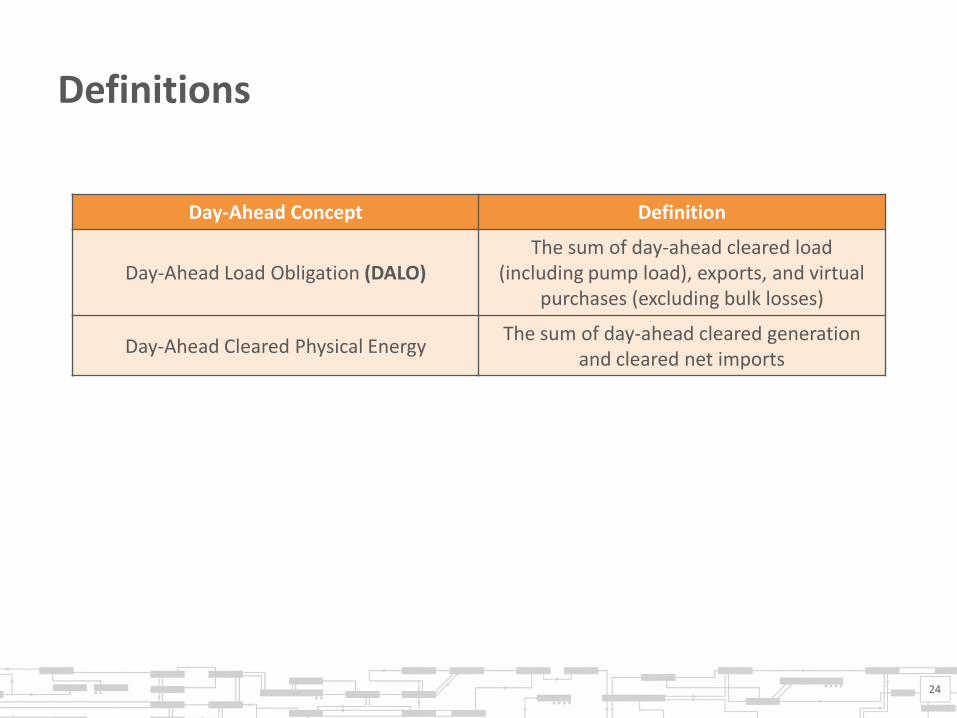

Day-Ahead Concept Definition

Day-Ahead Load Obligation (DALO) The sum of day-ahead cleared load

(including pump load), exports, and virtual purchases (excluding bulk losses)

Day-Ahead Cleared Physical Energy The sum of day-ahead cleared generation

and cleared net imports

GR:Graph36R GR:Graph36L

Fixed Dem PrSens Dem Decs

Losses Exports

Avg

Ho

url

y M

W 0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

22,500

JAN2015 FEB2015 MAR2015

Gen Imports

Incs

Avg

Ho

url

y M

W

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

22,500

JAN2015 FEB2015 MAR2015

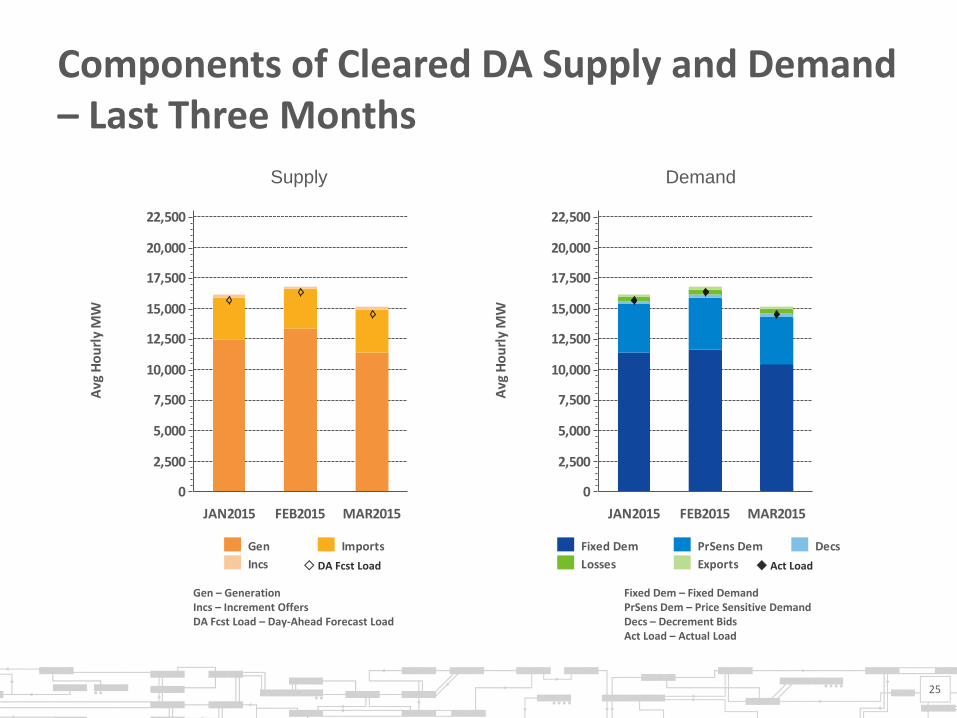

Components of Cleared DA Supply and Demand – Last Three Months

25

DA Fcst Load

Demand

Act Load

Supply

Gen – Generation Incs – Increment Offers DA Fcst Load – Day-Ahead Forecast Load

Fixed Dem – Fixed Demand PrSens Dem – Price Sensitive Demand Decs – Decrement Bids Act Load – Actual Load

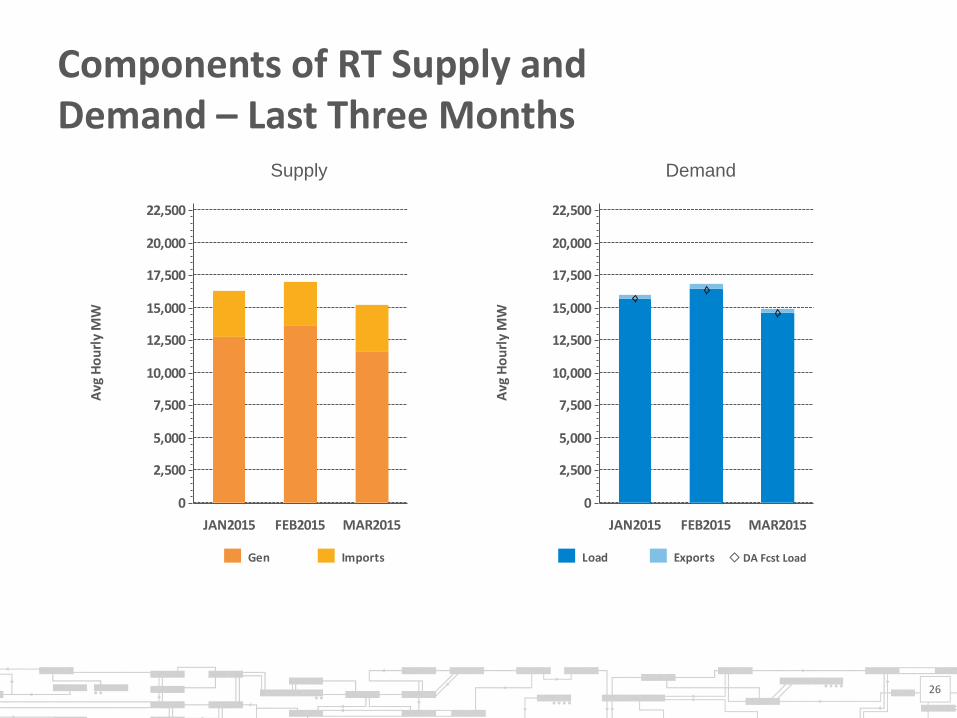

GR:Graph37R GR:Graph37L

Load Exports

Avg

Ho

url

y M

W 0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

22,500

JAN2015 FEB2015 MAR2015

Gen Imports

Avg

Ho

url

y M

W

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

22,500

JAN2015 FEB2015 MAR2015

Components of RT Supply and Demand – Last Three Months

26

Supply

DA Fcst Load

Demand

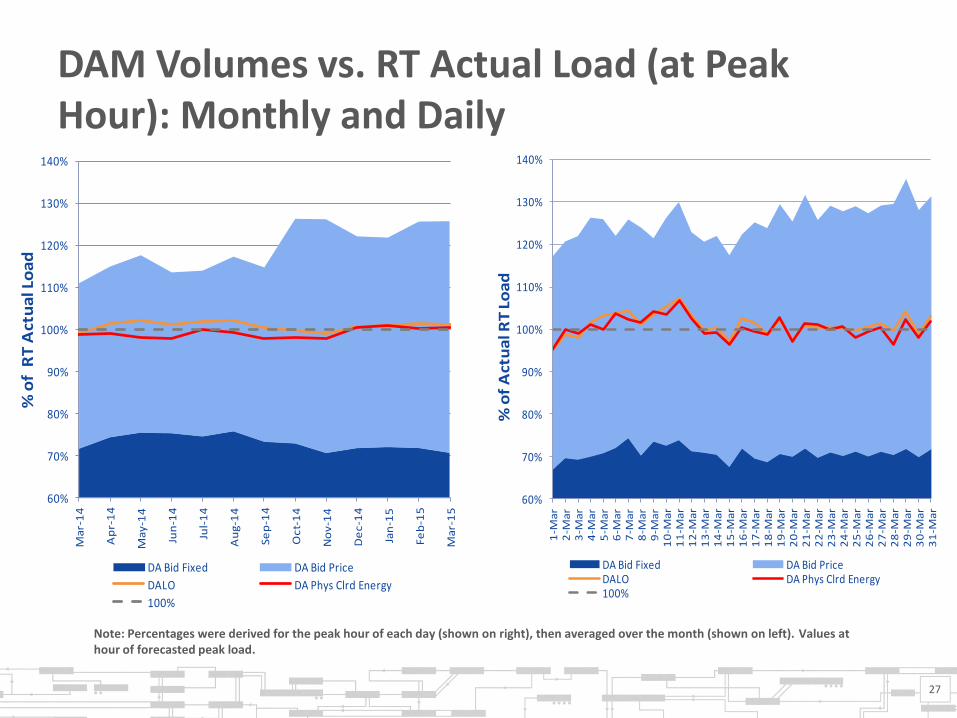

DAM Volumes vs. RT Actual Load (at Peak Hour): Monthly and Daily

27

Note: Percentages were derived for the peak hour of each day (shown on right), then averaged over the month (shown on left). Values at hour of forecasted peak load.

60%

70%

80%

90%

100%

110%

120%

130%

140%

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Jun

-14

Jul-

14

Au

g-1

4

Se

p-1

4

Oc

t-1

4

No

v-1

4

De

c-1

4

Jan

-15

Fe

b-1

5

Ma

r-1

5

% o

f R

T A

ctu

al L

oa

d

DA Bid Fixed DA Bid Price

DALO DA Phys Clrd Energy

100%

60%

70%

80%

90%

100%

110%

120%

130%

140%

1-M

ar

2-M

ar

3-M

ar

4-M

ar

5-M

ar

6-M

ar

7-M

ar

8-M

ar

9-M

ar

10

-Ma

r1

1-M

ar

12

-Ma

r1

3-M

ar

14

-Ma

r1

5-M

ar

16

-Ma

r1

7-M

ar

18

-Ma

r1

9-M

ar

20

-Ma

r2

1-M

ar

22

-Ma

r2

3-M

ar

24

-Ma

r2

5-M

ar

26

-Ma

r2

7-M

ar

28

-Ma

r2

9-M

ar

30

-Ma

r3

1-M

ar

% o

f A

ctu

al R

T L

oa

d

DA Bid Fixed DA Bid PriceDALO DA Phys Clrd Energy100%

GR:Graph26 GR:Graph27

DA

% o

f R

T

96.0% 96.2%

96.4% 96.6% 96.8%

97.0% 97.2% 97.4%

97.6% 97.8% 98.0%

98.2% 98.4% 98.6%

98.8% 99.0% 99.2%

MAR20

14APR2

014M

AY201

4JU

N20

14JU

L201

4AU

G20

14SE

P201

4O

CT201

4N

OV20

14D

EC20

14JA

N20

15FE

B2015

MAR20

15

Monthly, Last 13 Months

DA

% o

f R

T

92%

93%

94%

95%

96%

97%

98%

99%

100%

101%

102%

3/ 1

3/ 2

3/ 3

3/ 4

3/ 5

3/ 6

3/ 7

3/ 8

3/ 9

3/10

3/11

3/12

3/13

3/14

3/15

3/16

3/17

3/18

3/19

3/20

3/21

3/22

3/23

3/24

3/25

3/26

3/27

3/28

3/29

3/30

3/31

Daily, This Year vs. Last Year

Last_Year This_Year

DA vs. RT Load Obligation: March, This Year vs. Last Year

28

*Hourly average values

GR:dapce_dalo_pct_fxlo_fpk_dly_small GR:dapce_dalo_pct_fxlo_fpk_mly_small

Perc

enta

ge o

f Pea

k Fo

reca

st L

oad

80.0%

84.0%

88.0%

92.0%

96.0%

100%

104%

108%

112%

01MAR15

02MAR15

03MAR15

04MAR15

05MAR15

06MAR15

07MAR15

08MAR15

09MAR15

10MAR15

11MAR15

12MAR15

13MAR15

14MAR15

15MAR15

16MAR15

17MAR15

18MAR15

19MAR15

20MAR15

21MAR15

22MAR15

23MAR15

24MAR15

25MAR15

26MAR15

27MAR15

28MAR15

29MAR15

30MAR15

31MAR15

Daily: This Month

DA Cleared Physical Energy DALO100% line

Perc

enta

ge o

f Pea

k Fo

reca

st L

oad

92.0%

94.0%

96.0%

98.0%

100%

102%

104%

MAR2014

APR2014

MAY2014

JUN2014

JUL2

014

AUG2014

SEP2014

OCT2014

NOV2014

DEC2014

JAN2015

FEB2015

MAR2015

Monthly, Last 13 Months

DA Cleared Physical Energy DALO100% line

DA Volumes as % of Forecast (Peak Hour)

29

*Forecasted peak hour is reflected.

GR:dapce_delta_fpk_dly_bar

MW

h

-3,000

-2,500

-2,000

-1,500

-1,000

-500

0

500

1,000

1,500

01MAR20

1502M

AR2015

03MAR20

1504M

AR2015

05MAR20

1506M

AR2015

07MAR20

1508M

AR2015

09MAR20

1510M

AR2015

11MAR20

1512M

AR2015

13MAR20

1514M

AR2015

15MAR20

1516M

AR2015

17MAR20

1518M

AR2015

19MAR20

1520M

AR2015

21MAR20

1522M

AR2015

23MAR20

1524M

AR2015

25MAR20

1526M

AR2015

27MAR20

1528M

AR2015

29MAR20

1530M

AR2015

31MAR20

15

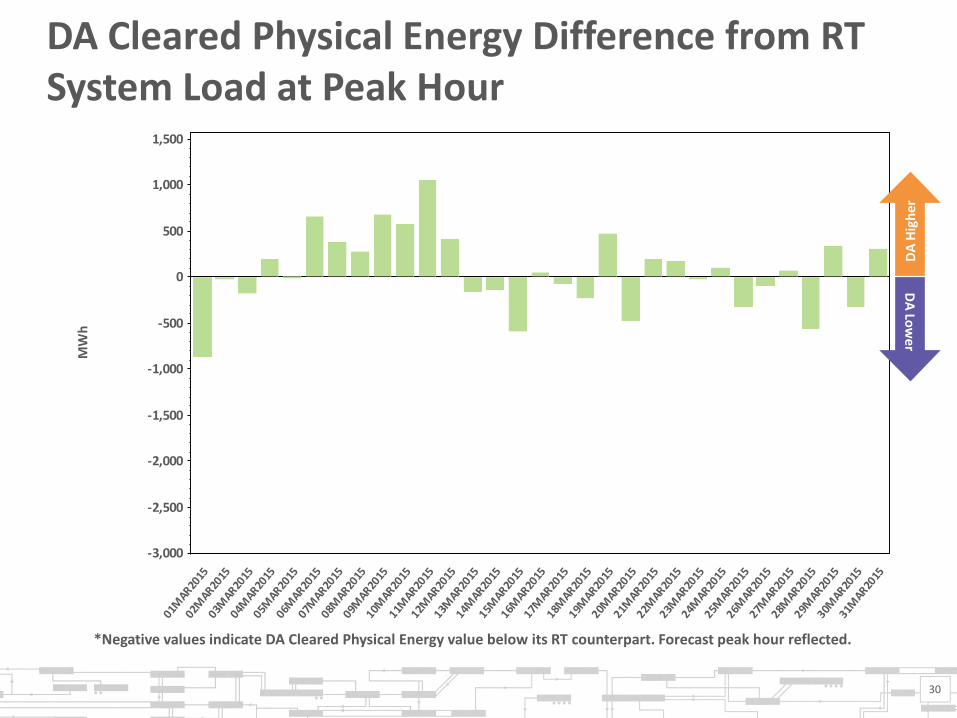

DA Cleared Physical Energy Difference from RT System Load at Peak Hour

30

*Negative values indicate DA Cleared Physical Energy value below its RT counterpart. Forecast peak hour reflected.

DA

Hig

he

r

DA

Low

er

GR:Graph32 GR:Graph33

Ne

t M

Wh

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

01

MA

R1

40

2M

AR

14

03

MA

R1

40

4M

AR

14

05

MA

R1

40

6M

AR

14

07

MA

R1

40

8M

AR

14

09

MA

R1

41

0M

AR

14

11

MA

R1

41

2M

AR

14

13

MA

R1

41

4M

AR

14

15

MA

R1

41

6M

AR

14

17

MA

R1

41

8M

AR

14

19

MA

R1

42

0M

AR

14

21

MA

R1

42

2M

AR

14

23

MA

R1

42

4M

AR

14

25

MA

R1

42

6M

AR

14

27

MA

R1

42

8M

AR

14

29

MA

R1

43

0M

AR

14

31

MA

R1

4

Hourly Average by Day, Last Year

Day-Ahead Real-Time

Ne

t M

Wh

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

01

MA

R1

50

2M

AR

15

03

MA

R1

50

4M

AR

15

05

MA

R1

50

6M

AR

15

07

MA

R1

50

8M

AR

15

09

MA

R1

51

0M

AR

15

11

MA

R1

51

2M

AR

15

13

MA

R1

51

4M

AR

15

15

MA

R1

51

6M

AR

15

17

MA

R1

51

8M

AR

15

19

MA

R1

52

0M

AR

15

21

MA

R1

52

2M

AR

15

23

MA

R1

52

4M

AR

15

25

MA

R1

52

6M

AR

15

27

MA

R1

52

8M

AR

15

29

MA

R1

53

0M

AR

15

31

MA

R1

5

Hourly Average by Day, This Year

Day-Ahead Real-Time

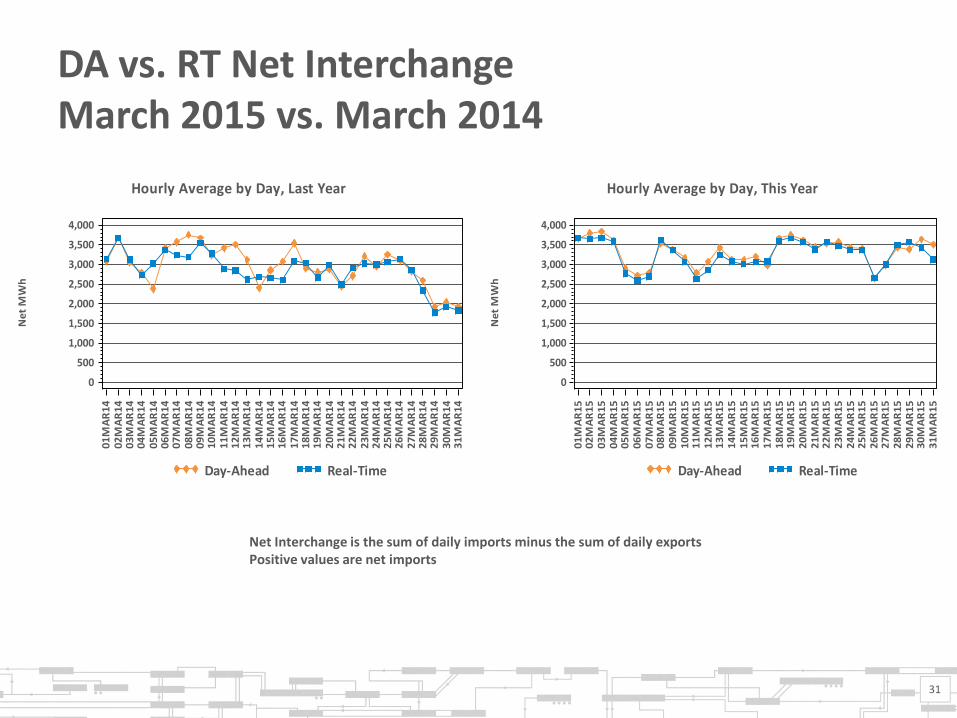

DA vs. RT Net Interchange March 2015 vs. March 2014

31

Net Interchange is the sum of daily imports minus the sum of daily exports Positive values are net imports

GR:Var_Cost_Gas_Mly

$0

$40

$80

$120

$160

$200

MAR20

13APR

2013

MAY2

013

JUN

2013

JUL2

013

AUG20

13SE

P201

3O

CT20

13N

OV20

13DEC

2013

JAN

2014

FEB20

14M

AR2014

APR20