Embed Size (px)

Citation preview

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 1

Keynes the Investor

CFS Lecture

House of Finance, Frankfurt, 6 November 2017

David Chambers

Judge Business School

University of Cambridge

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 2

Keynes: 1883-1946

▪ 1902-05 undergraduate, King’s Cambridge

▪ 1906 India Office

▪ 1909 Fellow, King’s

▪ WW1 UK Treasury

▪ 1919 Economic Consequences of the Peace

▪ 1923 Tract on Monetary Reform

▪ 1925 Economic Consequences of Mr Churchill

▪ 1931 MacMillan Committee

▪ 1936 General Theory

▪ WW2 UK Treasury, Bank of England

▪ 1944 Bretton Woods

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 3

Agenda

▪ Keynes the stock investor

▪ Keynes the currency trader

▪ Keynes the art investor

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 4

Agenda

▪ Keynes the stock investor

▪ Keynes the currency trader

▪ Keynes the art investor

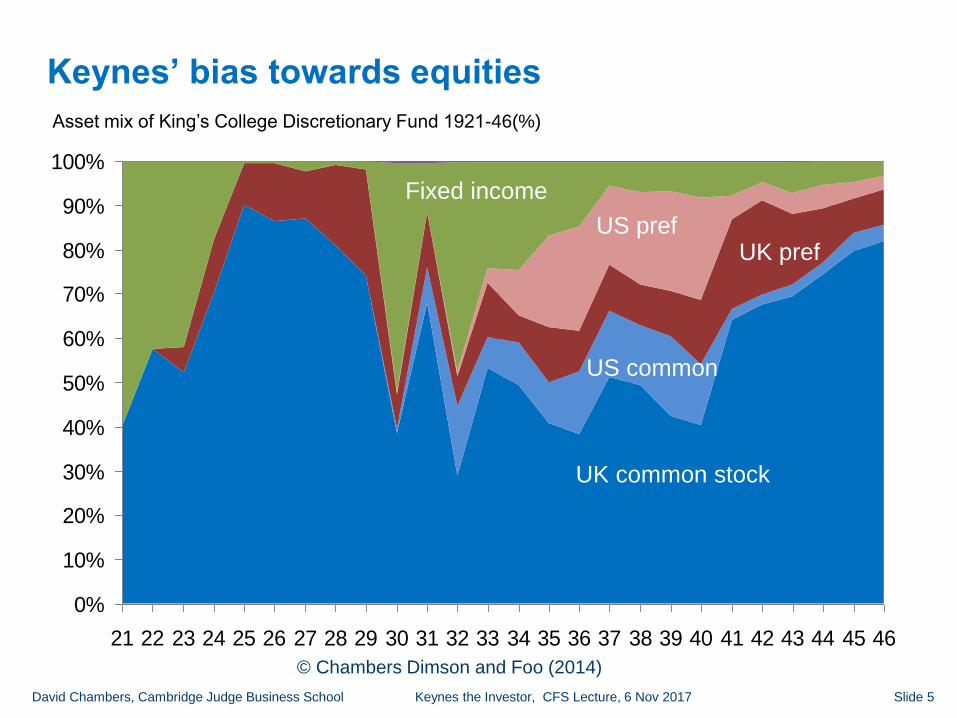

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 5

Asset mix of King’s College Discretionary Fund 1921-46(%)

UK common stock

US common stock

Keynes’ bias towards equities

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46

UK CMN US CMN UK PREF USPREF FIXED_INCOME OTHER

Fixed income

US prefUK pref

US common

UK common stock

© Chambers Dimson and Foo (2014)

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 6

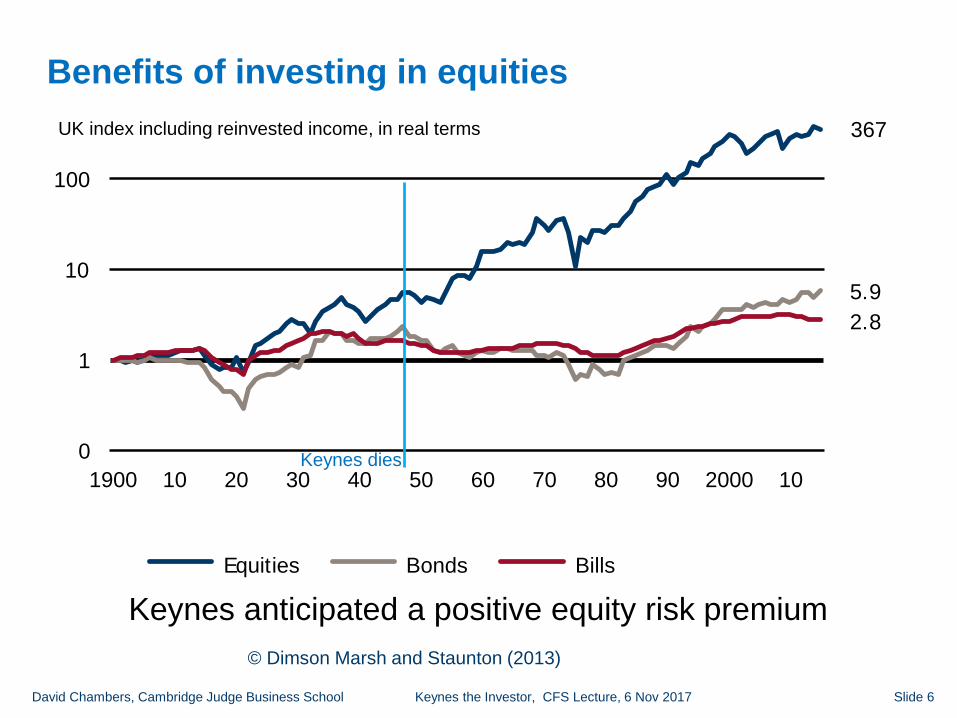

Benefits of investing in equities

367

5.9

2.8

0

1

10

100

1,000

1900 10 20 30 40 50 60 70 80 90 2000 10

Equities Bonds Bills

Keynes anticipated a positive equity risk premium

UK index including reinvested income, in real terms

Keynes dies

© Dimson Marsh and Staunton (2013)

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 7

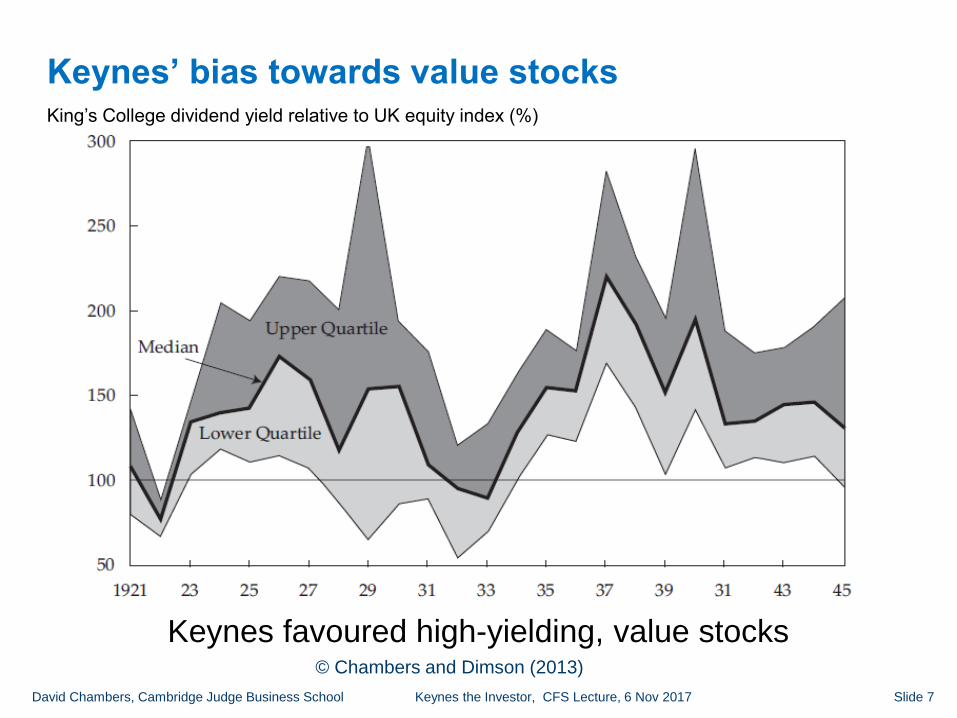

Keynes’ bias towards value stocksKing’s College dividend yield relative to UK equity index (%)

Keynes favoured high-yielding, value stocks© Chambers and Dimson (2013)

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 8

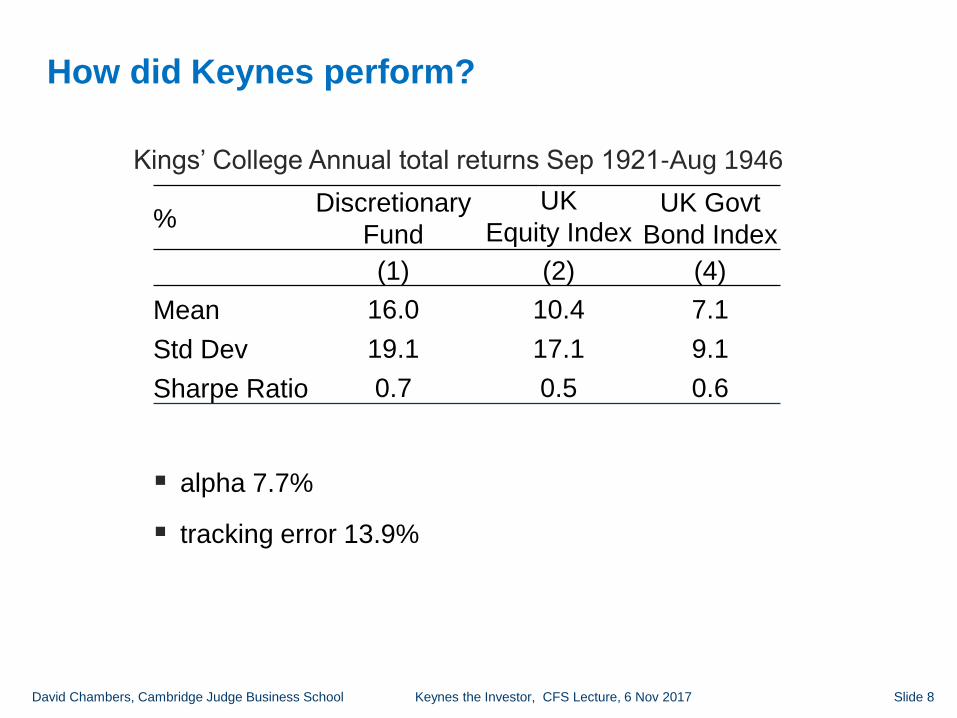

How did Keynes perform?

▪ alpha 7.7%

▪ tracking error 13.9%

%Discretionary

Fund

UK

Equity Index UK Govt

Bond Index

(1) (2) (4)

Mean 16.0 10.4 7.1

Std Dev 19.1 17.1 9.1

Sharpe Ratio 0.7 0.5 0.6

Kings’ College Annual total returns Sep 1921-Aug 1946

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 9

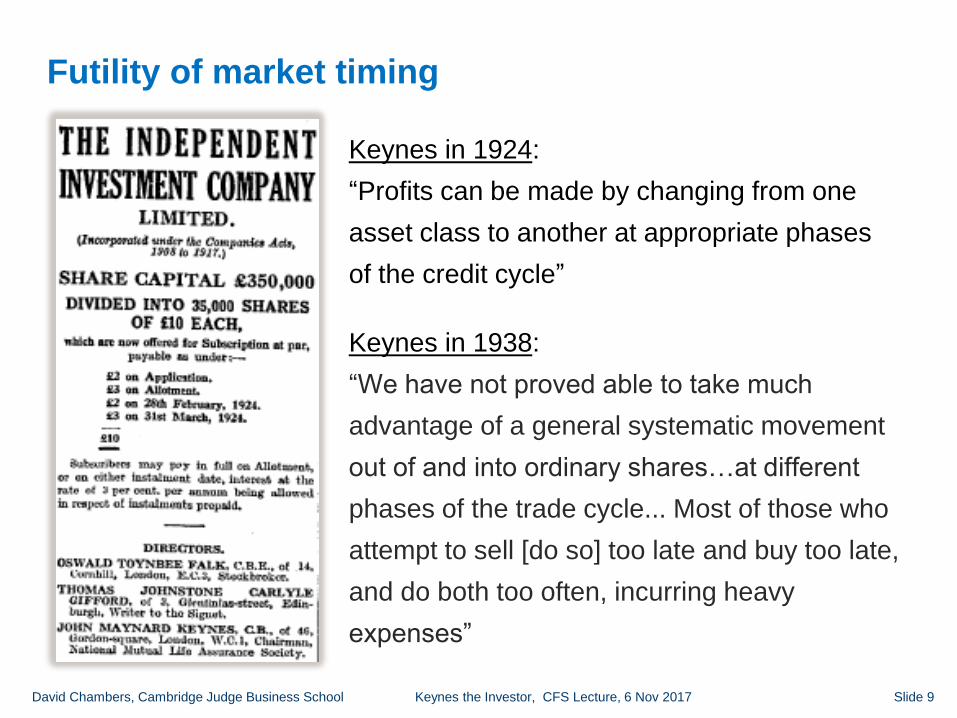

Keynes in 1924:

“Profits can be made by changing from one

asset class to another at appropriate phases

of the credit cycle”

Keynes in 1938:

“We have not proved able to take much

advantage of a general systematic movement

out of and into ordinary shares…at different

phases of the trade cycle... Most of those who

attempt to sell [do so] too late and buy too late,

and do both too often, incurring heavy

expenses”

Futility of market timing

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 10

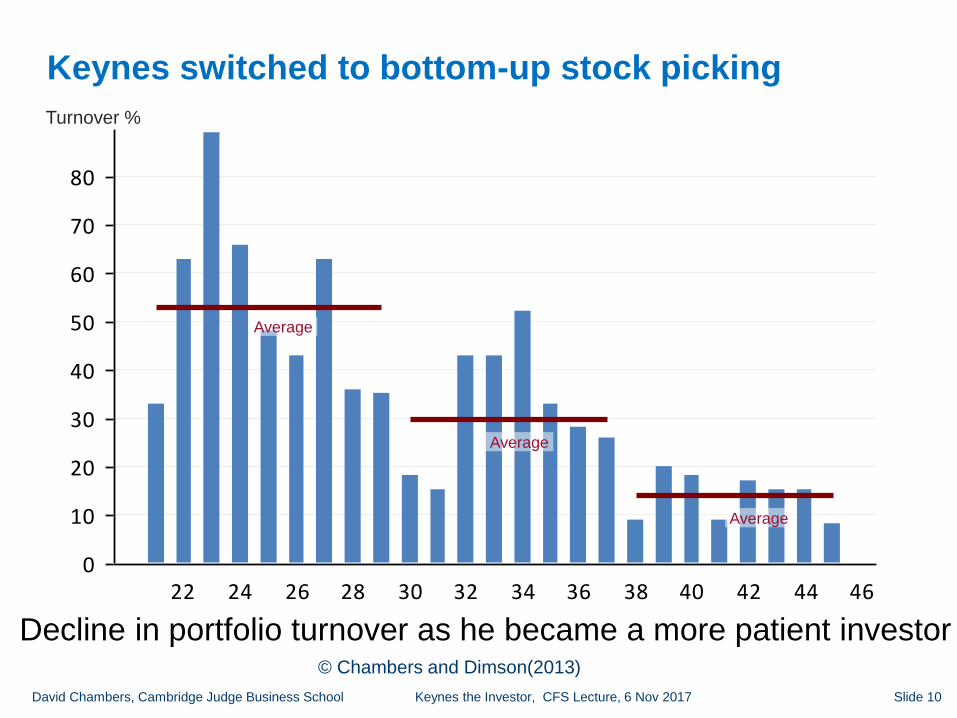

Keynes switched to bottom-up stock picking

0

10

20

30

40

50

60

70

80

22 24 26 28 30 32 34 36 38 40 42 44 46

Turnover %

Average

Average

Average

Decline in portfolio turnover as he became a more patient investor© Chambers and Dimson(2013)

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 11

Some lessons from Keynes on stock investing

▪ Equities earn a risk premium for the long term investor

▪ Market timing is very difficult

▪ Value and Size factors

▪ Challenges of being unconventional and contrarian

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 12

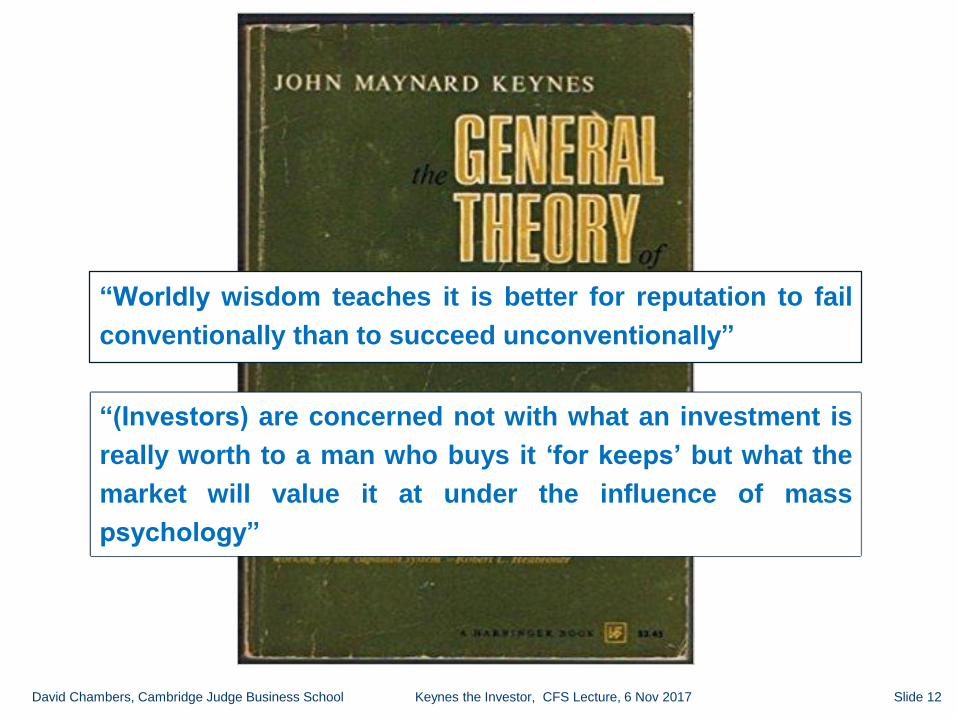

“Worldly wisdom teaches it is better for reputation to fail

conventionally than to succeed unconventionally”

“(Investors) are concerned not with what an investment is

really worth to a man who buys it ‘for keeps’ but what the

market will value it at under the influence of mass

psychology”

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 13

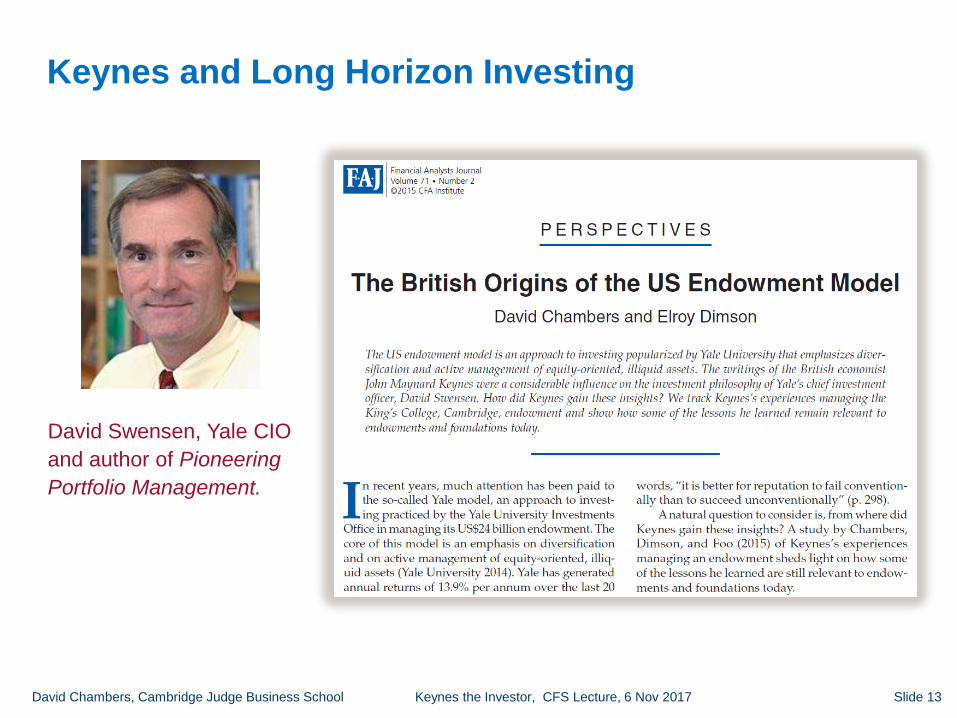

Keynes and Long Horizon Investing

David Swensen, Yale CIO

and author of Pioneering

Portfolio Management.

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 14

Agenda

▪ Keynes the stock investor

▪ Keynes the currency trader

▪ Keynes the art investor

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 15

Keynes’ FX strategy

▪ followed a discretionary fundamentals-based approach

close monitoring of trade, capital flows, inflation, interest rates,

central bank intervention and politics

▪ well-connected but no evidence of private information

“Taking a slightly longer view, I should expect the dollar to

appreciate in terms of sterling rather than otherwise”

16 March 1933

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 16

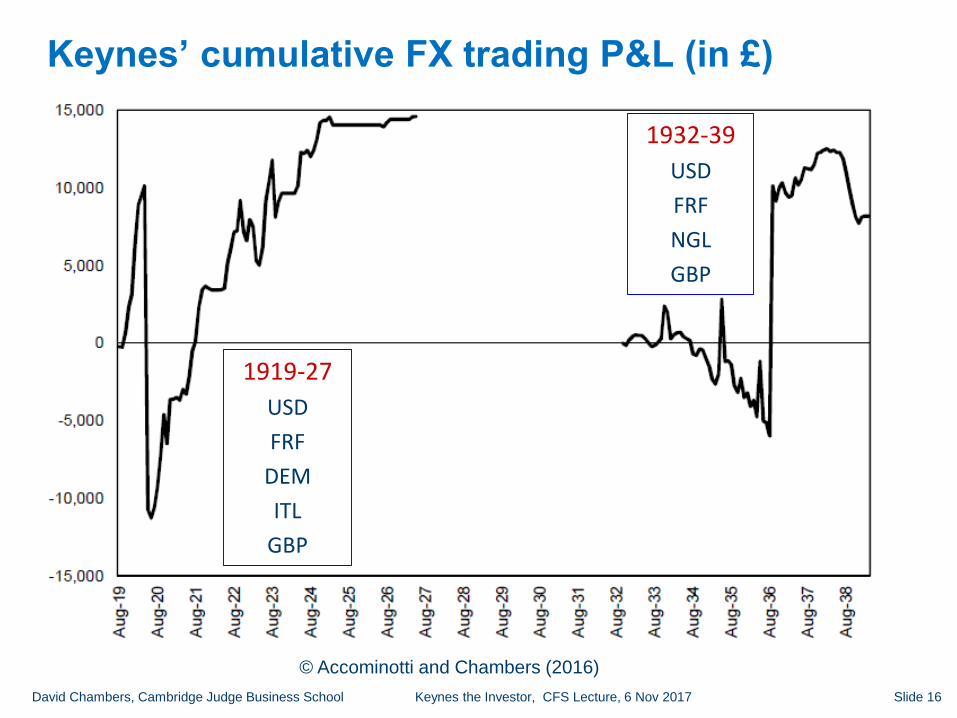

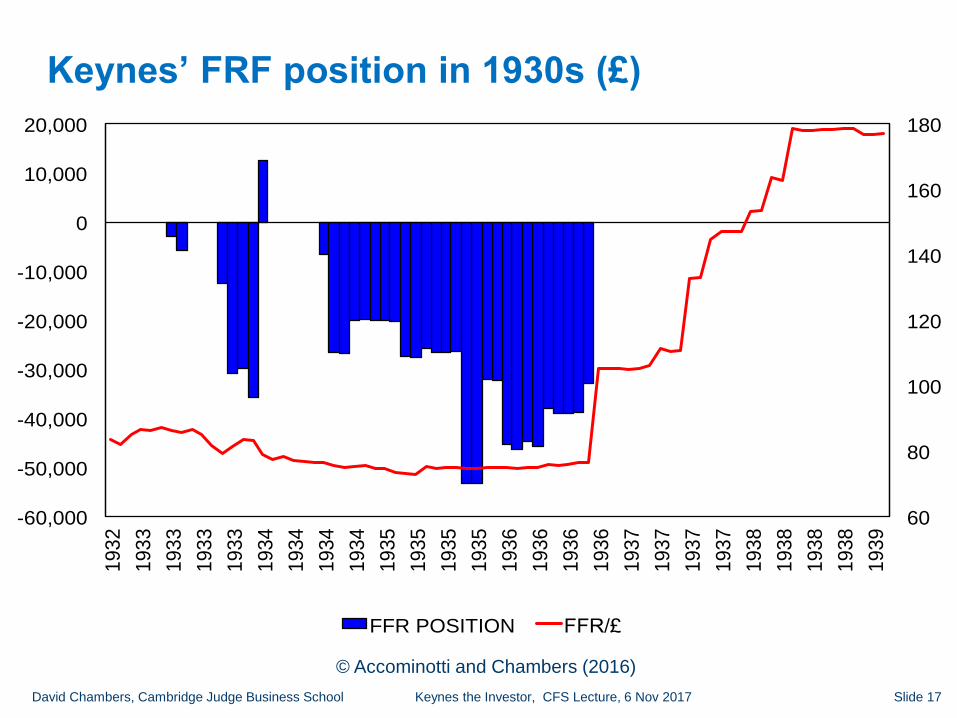

Keynes’ cumulative FX trading P&L (in £)

1919-27

USD

FRF

DEM

ITL

GBP

1932-39

USD

FRF

NGL

GBP

© Accominotti and Chambers (2016)

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 17

60

80

100

120

140

160

180

-60,000

-50,000

-40,000

-30,000

-20,000

-10,000

0

10,000

20,000 1

0/1

93

2

01

/193

3

04

/193

3

07

/193

3

10

/193

3

01

/193

4

04

/193

4

07

/193

4

10

/193

4

01

/193

5

04

/193

5

07

/193

5

10

/193

5

01

/193

6

04

/193

6

07

/193

6

10

/193

6

01

/193

7

04

/193

7

07

/193

7

10

/193

7

01

/193

8

04

/193

8

07

/193

8

10

/193

8

01

/193

9

FFR POSITION FFR/£

Keynes’ FRF position in 1930s (£)

© Accominotti and Chambers (2016)

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 18

Some lessons from Keynes on currency trading

▪ timing currency moves is very challenging

“Nothing is more rash than a forecast with regard to dates on this

matter. The event when it comes will come suddenly. The best thing

is to allow for probability and put little trust in forecasts of the date,

whether soon or late”

(Dec-1934 on prospective FFR and DFL devaluations)

▪ traders experience “limits to arbitrage” due to lack of

conviction or capital or both

“Markets can remain irrational longer than you can remain solvent”

(attributed to Keynes)

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 19

Agenda

▪ Keynes the stock investor

▪ Keynes the currency trader

▪ Keynes the art investor

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 20

Keynes and the Degas Sale 1918

Paul Cezanne Still Life with Apples c1878

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 21

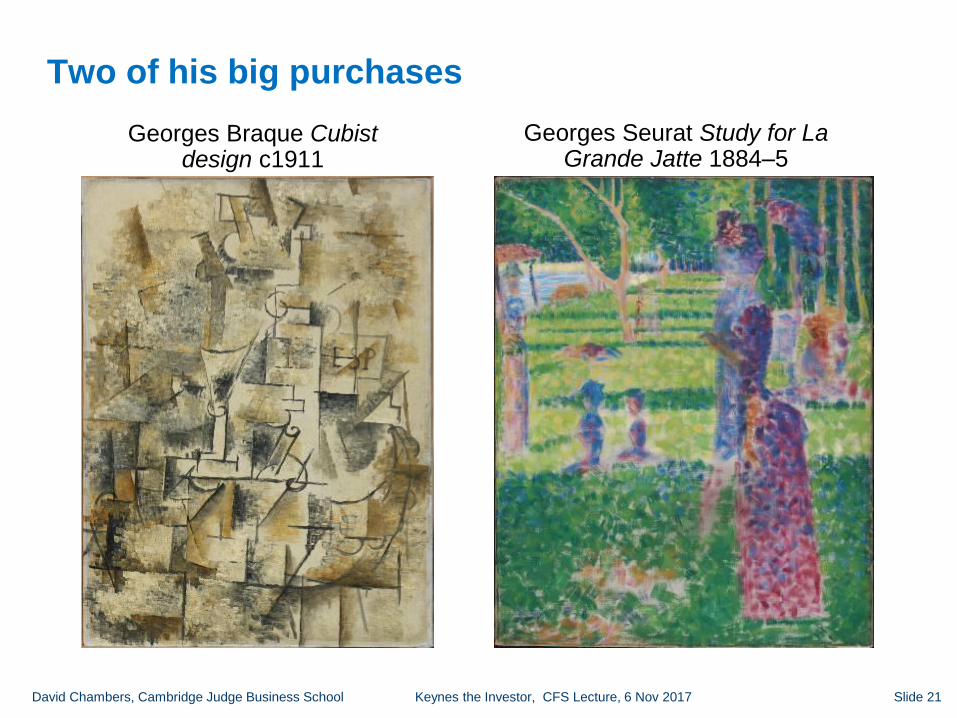

Two of his big purchases

Georges Seurat Study for La Grande Jatte 1884–5

Georges Braque Cubist design c1911

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 22

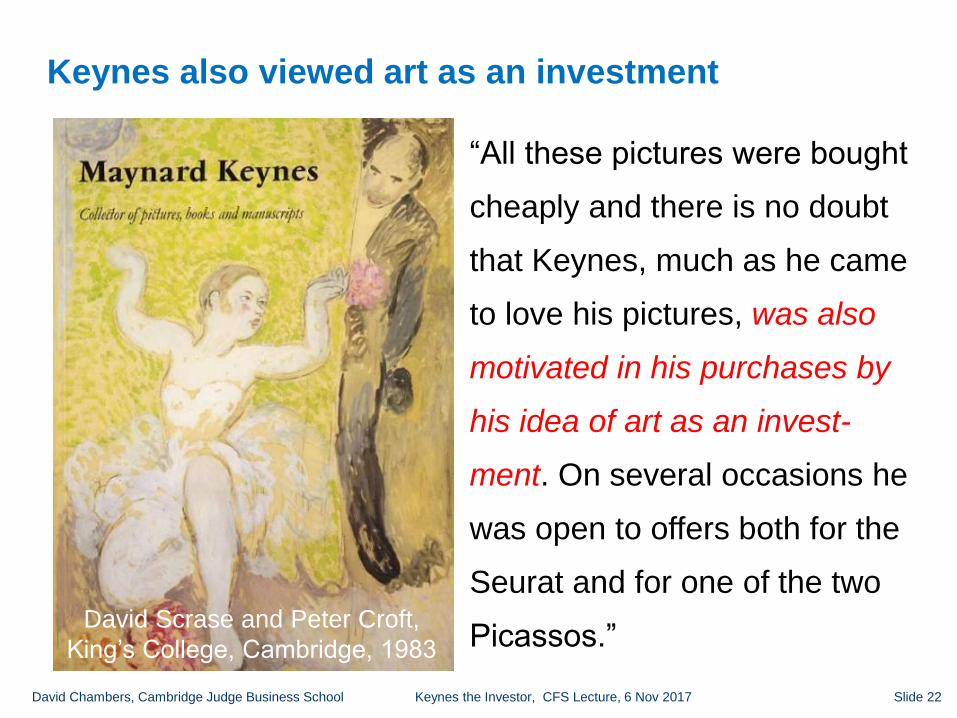

Keynes also viewed art as an investment

“All these pictures were bought

cheaply and there is no doubt

that Keynes, much as he came

to love his pictures, was also

motivated in his purchases by

his idea of art as an invest-

ment. On several occasions he

was open to offers both for the

Seurat and for one of the two

Picassos.”David Scrase and Peter Croft,

King’s College, Cambridge, 1983

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 23

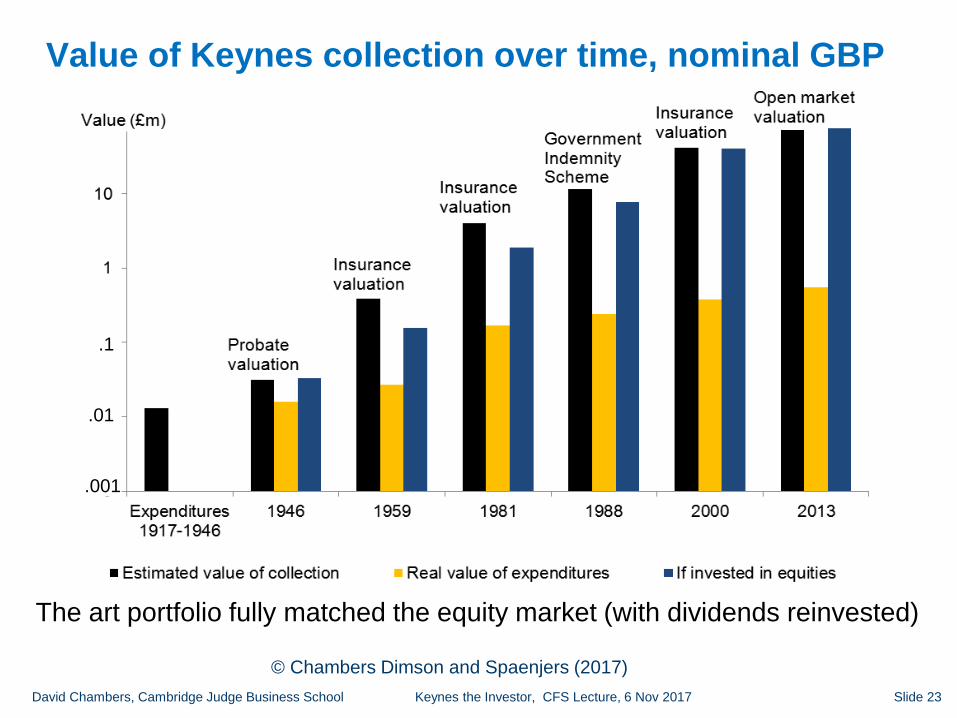

Value of Keynes collection over time, nominal GBP

The art portfolio fully matched the equity market (with dividends reinvested)

.1

.01

.001

© Chambers Dimson and Spaenjers (2017)

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 24

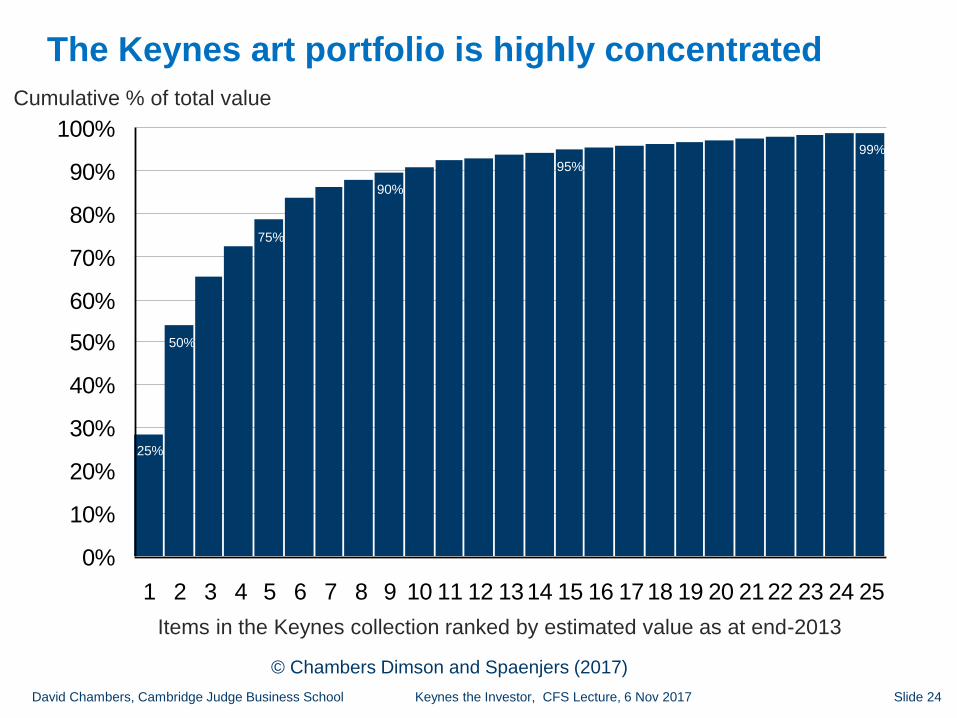

The Keynes art portfolio is highly concentrated

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5 6 7 8 9 10 11 12 1314 15 16 1718 19 20 2122 23 24 25

Items in the Keynes collection ranked by estimated value as at end-2013

Cumulative % of total value

25%

50%

75%

90%

95%

99%

© Chambers Dimson and Spaenjers (2017)

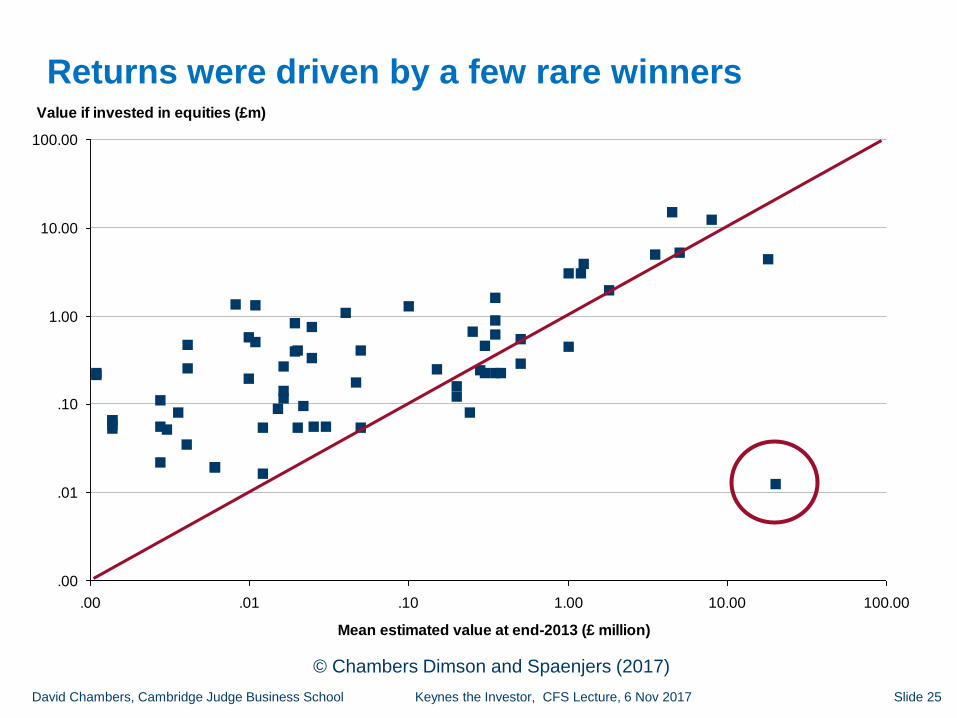

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 25

Value if invested in equities (£m)

.00

.01

.10

1.00

10.00

100.00

.00 .01 .10 1.00 10.00 100.00

Mean estimated value at end-2013 (£ million)

Returns were driven by a few rare winners

© Chambers Dimson and Spaenjers (2017)

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 26

Some lessons from Keynes on art investing

▪ Art portfolios also have a “style tilt”

▪ Portfolio concentration is the norm in art portfolios

▪ Returns are heavily skewed, like private equity

David Chambers, Cambridge Judge Business School Keynes the Investor, CFS Lecture, 6 Nov 2017 Slide 27

Articles on Keynes

▪ Stocks

“Keynes the stock market investor: A Quantitative Analysis” (with Elroy Dimson and Justin

Foo) Journal of Financial and Quantitative Analysis 2015, 50 (4): 843-868.

“Retrospectives: John Maynard Keynes, Investment Innovator” (with Elroy Dimson) Journal

of Economic Perspectives 2013, 27(3): 213–228.

“Keynes and Wall Street” (with Ali Kabiri) Business History Review 2016, 90 (4): 342-386.

▪ Currencies

“If You’re So Smart: The Currency Trading Record of John Maynard Keynes” (with Olivier

Accominotti) Journal of Economic History 2016, 76 (2): 342-386.

▪ Art

“Art as an Asset: Evidence from Keynes the Collector” (with Christophe Spaenjers and

Elroy Dimson) SSRN working paper.

▪ Long-term investing

“Keynes, King’s and Endowment Asset Management” (with Elroy Dimson and Justin Foo) in

Brown J. and Hoxby C. (ed.s) How the Great Recession Affected Higher Education.

National Bureau of Economic Research. Chicago University Press (2014) ch.4 pp.127-150.

“The British Origins of the US Endowment Model” (with Elroy Dimson) Financial Analysts

Journal 2015 vol.71 no.2.