Embed Size (px)

Citation preview

1

DAVE JANNY FEBRUARY TWO 2018 INVESTMENT LETTER

2018 Volume 4

“THE GRAND ILLUSION: PROMISES, FORTUNATE SONS AND THE

GHOST OF TOM JOAD”

In 1995 Bruce Springsteen released “The Ghost of Tom Joad”:

“The highway is alive tonight

Where it's headed everybody knows

I'm sitting down here in the campfire light

With the ghost of old Tom Joad”

In this Letter I’m going to take you back to your school days when classic

literature was part of your reading regimen. One novel you may have read was

John Steinbeck’s “The Grapes of Wrath”. Wikipedia sets the stage:

“Set during the Great Depression, the novel focuses on the Joads, a poor family of

tenant farmers driven from their Oklahoma home by drought, economic hardship,

agricultural industry changes, and bank foreclosures forcing tenant farmers out of

work. Due to their nearly hopeless situation, and in part because they are trapped

in the Dust Bowl, the Joads set out for California. Along with thousands of other

"Okies", they seek jobs, land, dignity, and a future.”

2

Tom Joad is one of the main characters of the novel, the plot weaves in the tough

times and circumstances that he and his family faced while at the same time

shows Tom’s personal growth and development. According to Cliff Notes:

“Tom is kind and often merciful, yet quick to anger and fiercely independent. As a

man of action, he embodies one of the novel's main philosophical strands,

pragmatism.”

A question that is often asked about today’s FED is “what will the legacy of

Bernanke, Yellen and new FED chair Jay Powell be”? My answer to this reminded

me of the “The Ghost of Tom Joad”. Springsteen’s original song was a rather slow

but moving folk song that told the story of Tom Joad. The version I’m thinking of

was the “electrified” “live” version where Tom Morello of the band Rage Against

The Machine joins Springsteen for a powerful emotional collaboration that

features the incredible guitar playing of Morello. I’ve personally witnessed the

“live” performance, but if you’re not familiar with it, I’d urge you to check out the

video on You Tube to fully appreciate what I’m talking about. “Tom Joad” in this

Letter will serve as a symbol of the “working class” man in today’s world of QE

(Quantitative Easing). Before I fill in the details to my answer on FED legacy, let

me further set the stage with some of my other musical references.

In 1969, Credence Clearwater Revival released their song “Fortunate Son”. It was

a protest song against the “privileged”. Writer and lead singer John Fogarty said

of the song, “it speaks more to the unfairness of class”. Hold that thought.

“Promises” is a song by Eric “Slowhand” Clapton, one of the great guitarists of all

time. Clapton’s song reminds me of the usual government and central bank

tactics of giving people something today in the form of “promises” for short term

political gain at the expense of long term potential financial pain. I’ll weave that

idea into my FED legacy theory.

All of this with the backdrop of “The Grand Illusion”; this is now the fourth

straight Letter that utilizes that Styx song as on overlay of the supposed “fix” of

the 2007-2009 “financial crisis”. As the title implies and as the repeated usage

suggests, I’m obviously skeptical of the “fix”; it just doesn’t seem to make sense to

me to be able to “fix” a debt crisis by creating a lot more of it.

3

By the way, speaking of the FED, “welcome to the show” Jay Powell. Powell was

rudely greeted with a quick, sharp and “at moments” scary stock market

correction. Here’s what Powell said in 2012 about QE:

““My concern is that for very modest benefits, we are piling up risks for the future

and that it could be habit-forming. When it is time for us to sell, or even to stop

buying, the response could be quite strong.”

Well here we are at the point where the FED is selling treasury and mortgage

bonds after years of “piling up habit–forming risks”. In other words QT

(Quantitative Tightening) is here; like I said “welcome to the show”. Before we get

into FED legacy and “The Ghost of Tom Joad”, let’s start with some quick market

observations.

MARKET OBSERVATIONS

The almost two year uninterrupted stock market rally ended on 1/26/18, I

previously described it as a euphoric “blow-off” top. According to Thomson the

S&P 500 peak was 2872. The ensuing explosion in what had been dormant market

“volatility” (that I described as the “fire” in my last Letter “THE GRAND ILLUSION:

RING OF FIRE ON THE MOUNTAIN”) led to a correction, that included two rather

terrifying 1000 point plus down days in the Dow Jones Industrial Average, taking

the S&P to an intraday low of 2532 on 2/9/18. We finally got the 10% correction,

a feat that felt like it would never happen again. At the minimum, take it as a first

warning shot. Now that S&P high and low I just documented gives us a wide

trading range to work through before we can determine whether or not the 9

year bull market rally ended. The market has subsequently attempted a V-shaped

rally that has taken us up about 2/3 of the way through the aforementioned

trading range. This week’s intraday sell-offs and reluctance to move more forward

likely gives some credence to the thought of, at the minimum, a retest of the

recent low. In the background the stock market gets a bit jittery on days when

treasuries yields rise and then gets more comfortable on days when rates fall.

Either way, breaking the top or breaking the low, will give us a better handle on

the intermediate term market trend. Breaking the low would probably carry more

weight as we haven’t seen many or even any instances of that in quite a long

4

time. Again, keep in mind, this is all occurring with the backdrop of never-

attempted QT in the face of the largest and longest historic coordinated global

central bank intervention ever embarked upon. Good luck.

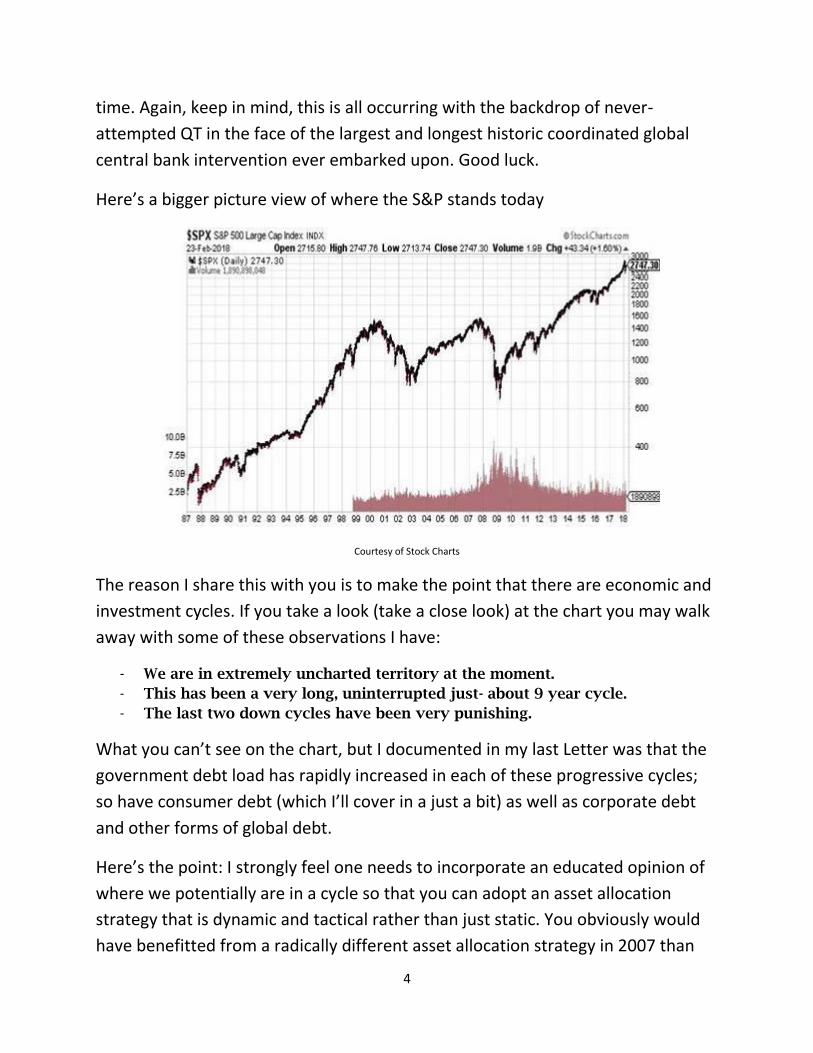

Here’s a bigger picture view of where the S&P stands today

Courtesy of Stock Charts

The reason I share this with you is to make the point that there are economic and

investment cycles. If you take a look (take a close look) at the chart you may walk

away with some of these observations I have:

- We are in extremely uncharted territory at the moment.

- This has been a very long, uninterrupted just- about 9 year cycle.

- The last two down cycles have been very punishing.

What you can’t see on the chart, but I documented in my last Letter was that the

government debt load has rapidly increased in each of these progressive cycles;

so have consumer debt (which I’ll cover in a just a bit) as well as corporate debt

and other forms of global debt.

Here’s the point: I strongly feel one needs to incorporate an educated opinion of

where we potentially are in a cycle so that you can adopt an asset allocation

strategy that is dynamic and tactical rather than just static. You obviously would

have benefitted from a radically different asset allocation strategy in 2007 than

5

would have been beneficial in 2009. I hear many investors call themselves long

term investors, that’s great but take a close look at the above chart and ask

yourself if you want to own as many stocks today as you would have ideally

wanted to own at the bottom in March of 2009. I’m not suggesting owning “no

stock” but I’m certainly advocating owning “less stock”. Unfortunately with the

handicap of human emotion, people want to typically become long term investors

when things look the best, which is actually more closely related to a market

“top” when one needs to be reducing risk. My job as a financial advisor and one

of the main objectives of my Investment Letters is to warn you about those

potential inflection points, where you need to be taking a “different” approach.

An eventual “normal” 20% correction would require a “different” approach, but if

you believe that we potentially could be in “The Grand Illusion”, you really need a

much “different” approach. If we haven’t had a conversation about your personal

situation I urge you to reach out to me at [email protected] or call me directly

at 203 221-6093 to further discuss.

I want to share a great article from Richard Rosso of Real Investment Advice titled

“2 Ways to Walk The Line With Your Money” that does a great job affirming my

above thoughts; I strongly encourage you to read it:

https://www.linkedin.com/feed/update/urn:li:activity:6370007847274582016

“TOM JOAD”, “FORTUNATE SONS” AND THE LEGACY OF THE FED

Let me jump straight to my answer to the question of what will the legacy of

Bernanke, Yellen and Powell be:

- A global asset bubble, the third in the last 20 years

- Debt, debt and more debt.

- Expanding wealth and income inequality that will lead to political change

For this Letter let’s focus on that third point “expanding wealth and income

inequality”. As I mentioned earlier “Tom Joad” will serve as my metaphor for the

“working class”/”middle class” American that is the unfortunate loser in the

global and domestic QE that we’ve seen for the last 9 years. The central bank plan

was simple; flood the system with money and intervene in the markets to lower

6

interest rates as much as possible and force up asset prices so that the wealth

effect creates consumer demand to create economic growth. After a series of QEs

here in the U.S., magnified by even more aggressive intervention in Europe, Japan

and China, boy did asset prices go up. Economic growth? Not so much. Benefits to

“Tom Joad”? Even less.

Before we delve into what happened to “Tom Joad” during this unprecedented

intervention, I want you to understand where I’m coming from. I am a free-

market capitalist. I want to see all people prosper and succeed and I don’t at all

begrudge the upper economic strata of the population for accumulating huge

sums of wealth; so when I point out the widening wealth and income inequality

gap, what I’m really disappointed with is how it has come about. Ladies and

gentlemen, we are not operating in a free-market capitalist system; with the

global elitists at the helm, capitalism has been hijacked by the “state”. The “state”

is off course big and growing government that especially since the financial crisis

has changed the rules to the benefit of the “fortunate sons” and to the detriment

of “Tom Joad”. Ever growing dependence on debt at all levels, an ever increasing

social welfare state, an alarming number of examples of “kicking the can down

the road” rather than making tough but needed political and financial decisions

and finally the implementation of a massive financial experiment by global central

bankers that has completely stacked the deck in favor of the wealthy are the

signposts of a warped capitalism, corrupted and run amok. The actions of central

bankers the last number of years has looked like a fruitless attempt to end

economic cycles, which has prevented a needed cleansing of global debt

structures and created dangerous and unprecedented moral hazard by distorting

financial markets.

Here in the U.S., “Tom Joad” has not readily participated in the FED-induced asset

bubble and either become more dependent on government welfare or been

faced with bleak job prospects with no wage growth and increasingly has been

forced to take on more and more debt to just “keep up” or pay for needed

healthcare and educational costs that have been disproportionately rising and

hurting him. Corporations have been more interested in forms of

“financialization” like stock buybacks at the expense of capital investment. Low

7

rates have forced marginal savers to “reach for yield” and increase the risk

they’ve been forced to take on their investments. Technological advances are

increasingly threatening “Tom Joad’s” job prospects. I’m going to estimate that

roughly 80% of our population is in the “Tom Joad” camp.

Back on 10/23/17, Ray Dalio who runs Bridgewater Capital, the world’s largest

hedge fund, posted a piece to LinkedIn called “Our Biggest Economic, Social and

Political Issue”. Dalio called it “the two economies: the top 40% and the bottom

60%”. Since I’m a lot closer to “Tom Joad” than Dalio, I’ll stick with my 80%

demarcation line rather than his 60%. One of his main points is that in describing

the health of the U.S. economy it is dangerous to use averages. Here’s what he

said:

“To understand what’s going on in “the economy,” it is a serious mistake to look at

average statistics. This is because the wealth and income skews are so great that

average statistics no longer reflect the conditions of the average man. For example,

as shown in the chart below, the wealth of the top one-tenth of 1% of the population

is about equal to that of the bottom 90% of the population, which is the same sort of

wealth gap that existed during the 1935-40 period.”

That’s a staggering statistic. He went on to add these facts:

“There has been no growth in earned income, and income and wealth gaps have

grown and are enormous. Since 1980, median household real incomes have been

about flat, and the average household in the top 40% earns four times more than

the average household in the bottom 60%. While they’ve experienced some growth

recently, real incomes have been flat to down slightly for the average household in

the bottom 60% since 1980 (while they have been up for the top 40%). Those in the

top 40% now have on average 10 times as much wealth as those in the bottom 60%.

That is up from six times as much in 1980.”

“Only about a third of the bottom 60% saves any of its income (in cash or financial

assets). As a result, according to a recent Federal Reserve study, most people in this

group would struggle to raise $400 in an emergency.”

I’ve accumulated additional facts from other sources that I’ll share with you that

clearly illustrate the plight of “Tom Joad”. The Richard Rosso Real Investment

Advice article I utilized above shared these additional facts:

“Crippling student loan debt: Per a study by the Brookings Institute, student loan

borrowers who left school owing at least $50,000 in student loans in 2010 had

8

failed to pay down any of the debt four years later. There are approximately 5

million borrowers affected out of a total of 44 million Americans saddled with

student loan obligations. The most recent overall loan delinquency rate stands at

11.2% and the median monthly student loan payment is $203 per one of my

favorite internet hubs of information – www.studentloanhero.com.

A downright embarrassing personal savings rate, overall: as of December 2017, the

personal U.S. saving rate fell to 2.4%. You need to return to the summer of 2005 to

get close to an equally dismal percentage.”

So “Tom Joad” is saving less and borrowing more and basically doesn’t have

enough money for emergencies. From the 12/30/17 issue of the Stansberry Digest

come some more sobering statistics:

Credit Suisse Chief Global Strategist Jonathan Wilmot published some debt

research that looked at debt-to-income ratios across different segments of the

population. In the late 1980s, the 20% of Americans with the least amount of

income held little debt, measured against their income levels. Today, however, this

segment of the population is the most in debt when measured against income.

The poorest Americans now hold debts in excess of 250% of their incomes, or about

five times more debt than the wealthiest 20%.

This massive change in the character of our household debts came about because

of "innovations" in lending – like subprime auto loans, payday lenders, and, most

important, student loans. Today, total household debt is almost $13 trillion. That's

higher than the previous all-time high of $12.6 trillion, set in the third quarter of

2008 – immediately prior to the last crisis.

And what's most important to understand is that the cost of this debt burden has

been artificially reduced since 2009 by the Fed. These costs – not just the normal

debt service, but also the cost of defaults – are about to soar.

More than 10% of these loans are student loans ($1.5 trillion outstanding). Most

were made to poor people against zero collateral, where there isn't any legal

process to deal with defaults. This is a serious economic problem that will

transform into a serious political problem because we have no economic or legal

way to deal with these debts.

And yet... the issuance of these bad debts continues to soar. Since 2013, the average

balance of all student borrowers has increased by 17% to more than $30,000.

9

“Tom Joad” now disproportionately owes the most debt. Michelle DiMartino

Booth of Money Strong LLC, shares these thoughts from a 1/3/18 interview with

Greg Hunter of USA Watchdog.com:

“We have seen 24 consecutive back-to-back months when credit card spending has

outpaced incomes. That tells you households are struggling to get by. This is not

Yves Saint Laurent handbags and Jimmy Choo shoes. These are families who are

using their credit cards to take care of the necessities, to fill up the gas tank, to buy

groceries and fill up their refrigerator...

We have seen month after month of subprime automobile delinquencies, and we are

starting to see a big tic up in FHA mortgage delinquencies as well.

...We are at almost 10% (delinquencies) of FHA mortgage loans. Underlying this

sugar high that we will see from all of these hurricanes and rebuilding efforts and

wildfires, underneath that, still waters run deep and the economy is not doing well.

We are a consumption driven economy that is weakening underneath.

The sugar high will absolutely wear off in 2018.”

I do believe that our economy is more fragile than “average” statistics would

suggest. “Tom Joad” is obviously hurting. “Tom Joad” has also not participated in

asset wealth creation as Patrick Watson who writes Connecting The Dots for John

Mauldin in a 2/13/18 piece he titled “The Stock Market Isn’t America” shows:

“About half of US households have zero exposure to the stock market: no stocks,

no mutual funds, no 401(k), no IRA, nothing.

According to research by New York University economist Edward Wolff, some 84%

of the stocks owned by Americans belong to the wealthiest 10% of households.

Subtract that 10%, and subtract the 50% who own no stocks, the remaining 40% of

Americans split about 15% of the stock market. For many, their investment is

negligible—maybe a few hundred dollars in an old 401(k). Others have a big part of

their net worth tied up in stocks. Maybe you’re in that group.

But a solid majority of the American population feels no direct impact from stock

market performance.”

Lastly David Effrig of Stansberry Research in his 2/15/18 edition of Income

intelligence further evidenced the problems of “Tom Joad”,

10

“First, wage growth for the middle class has been painfully slow over the long term.

Since 1993, real gross domestic product (GDP) per capita has risen about 40%, but

the median household income has grown only about 15%.

Second, there is an important group of necessities that have not trended lower in

costs. In particular, education, health care, and housing have all increased

drastically.

These aren't costs you can avoid...

•Since 1978, the CPI is up about 280%. But the CPI's measure of college tuition and

fees is up 1,225%.

•In 1970, we spent about $356 per person per year on health care ($1,714 in

inflation-adjusted terms). By 2013, that had risen to $9,255.

•And as far as housing goes, the median rent has risen about 33% since 1980 after

adjusting for inflation.”

“Tom Joad” obviously faces significant headwinds. On the other hand, I’m not

going to document the success of the “fortunate sons” but rather just have you

take another look at the S&P 500 chart I included on page 4 of this Investment

Letter; suffice to say the “fortunate sons” have done well in the QE regime that

global central bankers and the “elitists” have constructed. Eric Peters of One River

Asset Management succinctly sums up the conundrum and includes some political

assessment and consequences as well that may not be good for the “fortunate

sons”:

“So interest rates, just generally speaking, are very low. Debt is extremely high.

And inflation has remained low. So we’re somewhat caught in a dynamic where it’s

extremely difficult for rates to go up very high without raising a significant burden

on economies. The only way to alleviate that burden is to create more inflation.

But I think, as everyone looks at the world as they see it today, they go, well, it’s

going to be difficult for inflation to go up very far. Consequently rates can’t go up

very far, because if they do they’ll, essentially, bankrupt economies. And obviously

they won’t bankrupt the whole economy.

We’ve reached that tipping point within society where income inequality has

become sufficiently large that we’re seeing political shifts, whether it’s here in the

US, in the UK, in Germany – certainly in those three places – where there’s clear

pushback by the mid-skill worker against low wages, low wage growth.

11

As these things happen, as political winds shift, we’re seeing some of the natural

consequences. Which is, let’s call it de-globalization. I don’t think it’s going to be a

radical de-globalization. But it’s pretty clear that we’re seeing policies in these

various countries that, on balance, are going to lead to less globalization. “

“Promises” by way of social safety nets and pension and retirement programs

have been another way for the “elitists” in charge to communicate to “Tom Joad”

that in the long run everything will be okay because his retirement will be taken

care of. These “promises” have been given in exchange for votes that keep the

powers to be in power. There’s only one problem, more and more people are

seeing through the “promises” and realizing that pensions and our own Social

Security and Medicare programs are massively underfunded. Debt continues to

grow unchecked at all government levels throughout the world.

A 2/13/18 Zero Hedge article titled “$1.2 Trillion Asset Manager: Forget Volatility,

The Real Financial Timebomb is Public Pensions” gives some public pension stats

as well as some commentary from David Hunt of PGIM. By the way, I’m still

worried about “volatility” but let’s stick with script:

As we have reported over and over and over (and over, and over), public pensions

are in deep, deep trouble.

In addition critical funding shortfalls (U.S. public pensions had just 71.8% of assets

required to meet obligations as of June 2016), many of the country's largest

pensions have completely unrealistic target rates-of-return of 7% on average

"If you were going to look for what’s the possible real crack in the financial

architecture for the next crisis, rather than looking in the rearview mirror, pension

funds would be on our list,” Hunt said in a Friday interview with Bloomberg,

discussing what municipalities and states will do when local tax revenues decline

and unemployment worsens. "So we're worried about those pension obligations.”

PGIM, owned by New Jersey-based Prudential Financial, advises 147 of the 300

largest pension funds around the world.

Hunt said that corporate retirement funds typically outperform their public

counterparts. To that end, one of the most difficult aspects of managing money for

public plans, says Hunt, is the fact that lawmakers are promising unrealistic goals

to retirees. As such, he has advised public-pension clients to stop seeking the

highest returns, and "start doing what the corporate folks have long been doing,

12

which is to find ways to minimize the deficit and to take risk gradually off the

table.”

Adding to that, here are some comments from John Rubino of Dollar

Collapse.com that encapsulates the issues of “promises’ and the debt bubble

we’ve so incredibly created:

“Thirty or so years ago, state and local politicians and the leaders of their public

employee unions had a shared epiphany: If they offered workers hyper-generous

pensions they could buy labor peace without having to grant eye-popping and

headline-grabbing wage increases. And if they made unrealistically high

assumptions about the returns they could generate on pension plan assets they

could keep required contributions nice and low, thus making both workers and

taxpayers happy. The result: job security for politicians and union leaders and a

false sense of affluence for workers and taxpayers.

This scam worked beautifully for as long as it needed to – which is to say until the

architects of the over-generous benefits and unrealistic assumptions retired rich

and happy.

But now the unworkable math is coming to light and pension funds are responding

with two strategies:

1) Roll the dice by loading up on equities – the most volatile asset class available –

along with “real estate, commodities, hedge funds and private-equity holdings.”

2) Buy the dips. As the above highlighted quote illustrates, stocks have been going

up so steadily for so long that pension fund managers now see “volatility as an

investing opportunity.” When the next downturn hits they’ll throw good money

after bad, magnifying their losses.

Eventually a real bear market will shred the duct tape and chewing gum that’s

holding the public pension machine together. And several trillion dollars of

obligations will migrate from state and local governments to Washington, which is

to say taxpayers in general, at a time when federal debts are already soaring.

This is not a pretty picture. Pensions are still significantly underfunded despite a 9

year bull market in equities. As Rubino points out, what happens when we see the

unfortunate but inevitable down side of the cycle?

FINAL THOUGHTS

In my opening comments, Cliff Notes suggested that “pragmatism” was one of

“Tom Joad’s” main attributes. Much “pragmatism” will be required under the

13

current circumstances. Not only “Tom Joad”, but all of us face many challenges

ahead. Tough decisions will need to be made and political changes will be

required and continued “kicking the can down the road” will not be acceptable.

We can’t keep postponing dealing with issues that need to be addressed today

because of political convenience.

As far as global markets are concerned, there will be unintended consequences. I

don’t know when this very long market and economic cycle ends, but I do know

that there are clear warning signs that we should be heeding by employing risk

reduction strategies. If “Tom Joad” truly represents approximately 80% of the

population as I had suggested, the end may be nearer than you think. Thanks for

your readership, I look forward to any thoughts and comments and I strongly urge

you to reach out to me directly to see if I could be of help.

David Janny

Senior Vice President

Senior Portfolio Manager

Financial Advisor

NMLS# 1279369

Morgan Stanley Wealth Management

500 Post Road East

3rd Floor

Westport, CT 06880

203 221-6093

Visit my website http://fa.morganstanley.com/david.janny/

Connect with me on LinkedIn: https://www.linkedin.com/in/david-janny-ba2734115

The views expressed herein are those of the author and do not necessarily reflect the views of Morgan Stanley Wealth

Management or its affiliates. All opinions are subject to change without notice. Neither the information provided nor any

opinion expressed constitutes a solicitation for the purchase or sale of any security. Past performance is no guarantee of future

results.

Please be advised by clicking on a third party URL or hyperlink, you will leave morganstanley.com. Morgan Stanley Smith Barney

LLC is not implying an affiliation, sponsorship, endorsement with/of the third party or that any monitoring is being done by

Morgan Stanley of any information contained within the web site. Morgan Stanley is not responsible for the information

contained on the third party web site or your use of or inability to use such site. Nor do we guarantee their accuracy and

completeness

Information contained herein has been obtained from sources considered to be reliable, but we do not guarantee their accuracy

or completeness

14

Equity securities may fluctuate in response to news on companies, industries, market conditions and the general economic

environment.

This material does not provide individually tailored investment advice. It has been prepared without regard to the individual

financial circumstances and objectives of persons who receive it. The strategies and/or investments discussed in this material

may not be suitable for all investors. Morgan Stanley Wealth Management recommends that investors independently evaluate

particular investments and strategies, and encourages investors to seek the advice of a Financial Advisor. The appropriateness

of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

Principal value and return of an investment will fluctuate with changes in market conditions.

Investors should carefully consider the investment objectives and risks as well as charges and expenses of exchange traded

funds (ETFs) before investing. To obtain a prospectus, contact your Financial Advisor or visit the fund company’s website. The

prospectus contains this and other important information about the ETFs. Read the prospectus carefully before investing.

International investing may not be suitable for every investor and is subject to additional risks, including currency fluctuations,

political factors, withholding, lack of liquidity, the absence of adequate financial information, and exchange control restrictions

impacting foreign issuers. These risks may be magnified in emerging markets.

Investing in commodities entails significant risks. Commodity prices may be affected by a variety of factors at any time, including

but not limited to, (i) changes in supply and demand relationships, (ii) governmental programs and policies, (iii) national and

international political and economic events, war and terrorist events, (iv) changes in interest and exchange rates, (v) trading

activities in commodities and related contracts, (vi) pestilence, technological change and weather, and (vii) the price volatility of

a commodity. In addition, the commodities markets are subject to temporary distortions or other disruptions due to various

factors, including lack of liquidity, participation of speculators and government intervention.

Bonds are subject to interest rate risk. When interest rates rise, bond prices fall; generally the longer a bond's maturity, the more

sensitive it is to this risk. Bonds may also be subject to call risk, which is the risk that the issuer will redeem the debt at its option,

fully or partially, before the scheduled maturity date. The market value of debt instruments may fluctuate, and proceeds from

sales prior to maturity may be more or less than the amount originally invested or the maturity value due to changes in market

conditions or changes in the credit quality of the issuer. Bonds are subject to the credit risk of the issuer. This is the risk that the

issuer might be unable to make interest and/or principal payments on a timely basis. Bonds are also subject to reinvestment risk,

which is the risk that principal and/or interest payments from a given investment may be reinvested at a lower interest rate.

Interest on municipal bonds is generally exempt from federal income tax; however, some bonds may be subject to the

alternative minimum tax (AMT). Typically, state tax-exemption applies if securities are issued within one’s state of residence

and, if applicable, local tax-exemption applies if securities are issued within one’s city of residence. The tax-exempt status of

municipal securities may be changed by legislative process, which could affect their value and marketability.

Bonds rated below investment grade may have speculative characteristics and present significant risks beyond those of

investment grade securities, including greater credit risk, price volatility, and limited liquidity in the secondary market. Investors

should be careful to consider these risks alongside their individual circumstances, objectives and risk tolerance before investing

in high-yield bonds. High yield bonds should comprise only a limited portion of a balanced portfolio.

Foreign currencies may have significant price movements, even within the same day, and any currency held in an account may

lose value against other currencies. Foreign currency exchanges depend on the relative values of two different currencies and

are therefore subject to the risk of fluctuations caused by a variety of economic and political factors in each of the two relevant

countries, as well as global pressures. These risks include national debt levels, trade deficits and balance of payments, domestic

and foreign interest rates and inflation, global, regional or national political and economic events, monetary policies of

governments and possible government intervention in the currency markets, or other markets.

15

Technical analysis is the study of past price and volume trends of a security in an attempt to predict the security's future price

and volume trends. Its limitations include but are not limited to: the lack of fundamental analysis of a security's financial

condition, lack of analysis of macro economic trend forecasts, the bias of the technician's view and the possibility

that past participants were not entirely rational in their past purchases or sales of the security being analyzed. Investors using

technical analysis should consider these limitations prior to making an investment decision.

Physical precious metals are non-regulated products. Precious metals are speculative investments which may experience short-

term and long-term price volatility. The value of precious metals investments may fluctuate and may appreciate or decline,

depending on market conditions. If sold in a declining market, the price you receive may be less than your original investment.

Unlike bonds and stocks, precious metals do not make interest or dividend payments. Therefore, precious metals may not be

suitable for investors who require current income. Precious metals are commodities that should be safely stored, which may

impose additional costs on the investor. The Securities Investor Protection Corporation (SIPC) provides certain protection for

customers’ cash and securities in the event of a brokerage firm’s bankruptcy, other financial difficulties, or if customers’ assets

are missing. SIPC insurance does not apply to precious metals or other commodities.

Asset allocation does not guarantee a profit or protect against a loss in a declining financial market.

Past performance is no guarantee of future results.

NASDAQ Composite Index is a market-value-weighted index of all NASDAQ domestic and non-U.S. based common stocks listed

on NASDAQ stock market. An investment cannot be made directly in a market index.

S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock

market. An investment cannot be made directly in a market index.

The NYSE Arca Gold BUGS Index, also known as the AMEX Gold BUGS Index, is a modified equal dollar weighted index of

companies involved in major gold mining. The index was designed to give investors significant exposure to near term

movements in gold prices by including companies that do not hedge their gold production beyond 1½ years. The index was

developed with a base value of 200 as of March 15, 1996.

Morgan Stanley Smith Barney LLC. Member SIPC. CRC 2030504 02/2018