Embed Size (px)

DESCRIPTION

In this month’s issue, the editorial letter explores the influx and implications of microgrids on the power sector. The “In-Depth” article examines the history of oil since 1973. Focusing on the relations between the Middle East and Western economies, author Aiman El-Ramly shows how our present oil situation is the direct product of decades of geopolitical turmoil. Numerous short articles provide updates on EEX launching Nordic power futures, CME Group and GFI Group terminating their merger agreement, Deutsche Börse Market Data + Services becoming the exclusive licensor of PEGAS, and much more.

Citation preview

The Seven Ages of Oil:Boom and Bust, War and Peace,

Growth and Decline

By Aiman El-Ramly, C.S.O. ZE PowerGroup [email protected]

Part Two of Tw

o

New products and data sources

Delisting of products and data sources

Potential impact on data

Changes to data attributes, replacement of products

Powered by

FEBRUARY 2015

Summ

ary

February 2015

ContentsEditorial 5The Emerging Power Markets’ New Player – the Microgrid Operator 5

Power 7ICE Futures US Lists PJM, MISO, and SPP Power Futures Contracts 7EEX Launches Nordic Power Futures 8EEX Launches Online Shop for Market Data and New SFTP Server 8Italian Borders Market Coupling Launches 9Platts to Remove Descriptive Fields in North American Power CSV Files 9Platts to Discontinue UK High/Low Power Assessments 10APX and Dutch Energy Regulator Sign MOU on REMIT Implementation 10

Petroleum 11 Platts to Launch Rotterdam FOB Jet Barge Swaps 11Platts to Launch CFR India Petcoke Assessments 11Platts to Launch Weekly Turkey Mid-Sulfur Petcoke Assessment 11Platts Introduces Naptha against M3 Waterborne Gasoline Assessments 12Platts Launches Colonial Pipeline Line Space Assessments 13Argus Introduces New European Gasoil Bunker Assessments 14Argus Adds New Weekly Snapshot Value for German Diesel Barge 14Argus Launches New Petcoke Assessments 14Argus Adds New Ukrainian Diesel and Gasoline Assessments 15Argus Introduces New Paraxylene Sinopec Assessments 16Argus Adds New Gasoil Bunker Codes 16CME to List European and South Korean Trade Month Benzene Futures 17CME to Launch Crude Oil and Refined Futures 17ICE Launches New European Oil Futures 18Platts to Discontinue European and Mediterranean Low Sulfur 1% Bunker Assessments 19Platts to End No. 2 New York Harbor Cargos at London MOC 20Platts Stops Weekly DOP Assessment 20Platts Discontinues US Ketones Assessments 20Argus Stops Publishing European and Mediterranean Fuel Oil Bunker Assessments 21Argus Discontinues US Diesel and Fuel Oil Assessments 21CME Delists Two Brent Crude Oil CFD Futures Contracts 22Platts to Extend Low Sulfur Gasoil Futures Curve 22Platts Edits European Polymer Contract Price Assessment Parameters 22Platts’ Data Source Changes Petroleum Floor Trading Volumes 23

Natural Gas 24Platts Adds Cross-Fuels Data to European Gas Daily 24Argus Adds European Natural Gas Assessments 24Argus Adds New North American and European Natural Gas Codes 24CME Europe Launches Italian Natural Gas Futures 25ICE Futures US Lists Six New Natural Gas Futures 26Deutsche Börse Market Data + Services Becomes Exclusive Licensor of PEGAS 26

2

Summ

ary

Summ

ary

February 2015

Marex Spectron Trades CME Europe TTF and NBP Natural Gas Futures 26Platts to Discontinue Descriptive Fields in North American Natural Gas CSV Files 27Argus to Discontinue Propane Swap Assessments 27Argus Discontinues New York Natural Gas Assessments 28Platts’ Data Source Changes Henry Hub Floor Trading Volumes 28

Coal 29Platts to Publish CME Group Open Interest for Coal 29Platts and Fenwei to Launch CMCI Met Coal Assessment Series 29Platts Publishes Front-Month, Front-Quarter Coal Averages 30Argus Discontinues New York BTU Value Coal Assessment 30Platts to Discontinue Compliance Coal Spread 30

Softs and Metals 31SOFTS 31Platts to Launch Expanded Sugar Futures Assessments 31Platts to Decouple Two T2 German Ethanol Assessments 31CME Launches Short-Dated Crop Soybean Meal and Soybean Oil Options 32CME Europe Lists Fertilizer Cash Settled Futures 33New MGEX Calendar Spread Options Launched on CME Globex 33Marex Spectron Launches Physical Sugar Broking 34DCE Lists New Soybean, Corn, Palm Olein, Fiberboard, Blockboard, and Corn Starch Contracts 34Euronext Extends Milling Wheat Contract to Johannesburg Stock Exchange 35METALS 36Platts to Publish Iron Ore Phosphorus Differential 36Argus Launches Gadolinium Oxide Assessment 36NYMEX Lists Gold Kilo Futures for Hong Kong Deliveries 37ICE to Administer the LBMA Gold Price 38Platts Discontinues Platts Tubular Market Data File 38CME Changes FIX Tags for Metals Futures 39LME Extends Publication of Live Forward Price Curves 39

Finance 40Platts to Launch New USD-INR Forex Assessment 40 CME Introduces Ratio Calendar Spread for Treasury Bond Futures 40CME Globex Lists Second Generation Deliverable Interest Rate Swap Futures 41CME Europe Lists Euro and US Dollar Denominated Deliverable Swap Futures 41ICE Introduces Additional Euribor and Short Sterling Options 43ICE Introduces Flexible Individual Equity Option and Single Stock Futures Contracts 43DGCX Adds New Spread Contracts in Indian Rupee Futures 43Ossiam Launches New Smart Beta ETF on Xetra 44UBS AG Lists New ETF on Xetra 44ICAP Launches the ICAP Bond Correlated Call US Treasury Index 45ICAP e-Commerce Launches Scrapbook Service for the Corporate Bond Market 45TAIFEX Launches Two New EFT Futures 46Source Launches Two New Equity Index ETFs on Xetra 46

3

Summ

ary

Summ

ary

4February 2015

Summ

aryCFTC Issues Order of Registration for Bursa Malaysia Derivatives Berhad 47TickSmith Launches Chi-X Canada Historical Market Data Portal 47Amundi Launches Two New Bond Index ETFs on Xetra 48CME Group and GFI Group Terminate Merger Agreement 48DGCX Suspends Existing Spread Contracts in Indian Rupee Futures 49ICAP Partners with Wind Information Co. to Provide Data to the Chinese Market 49TOCOM Granted Registration as Foreign Board of Trade by CFTC 49Eurex Authorized to Launch Eurex Clearing Asia 50CME Amends Product Titles of Six CME FX Futures and Options 50IBA Introduces New Calculation Methodology for ISDAFIX 51

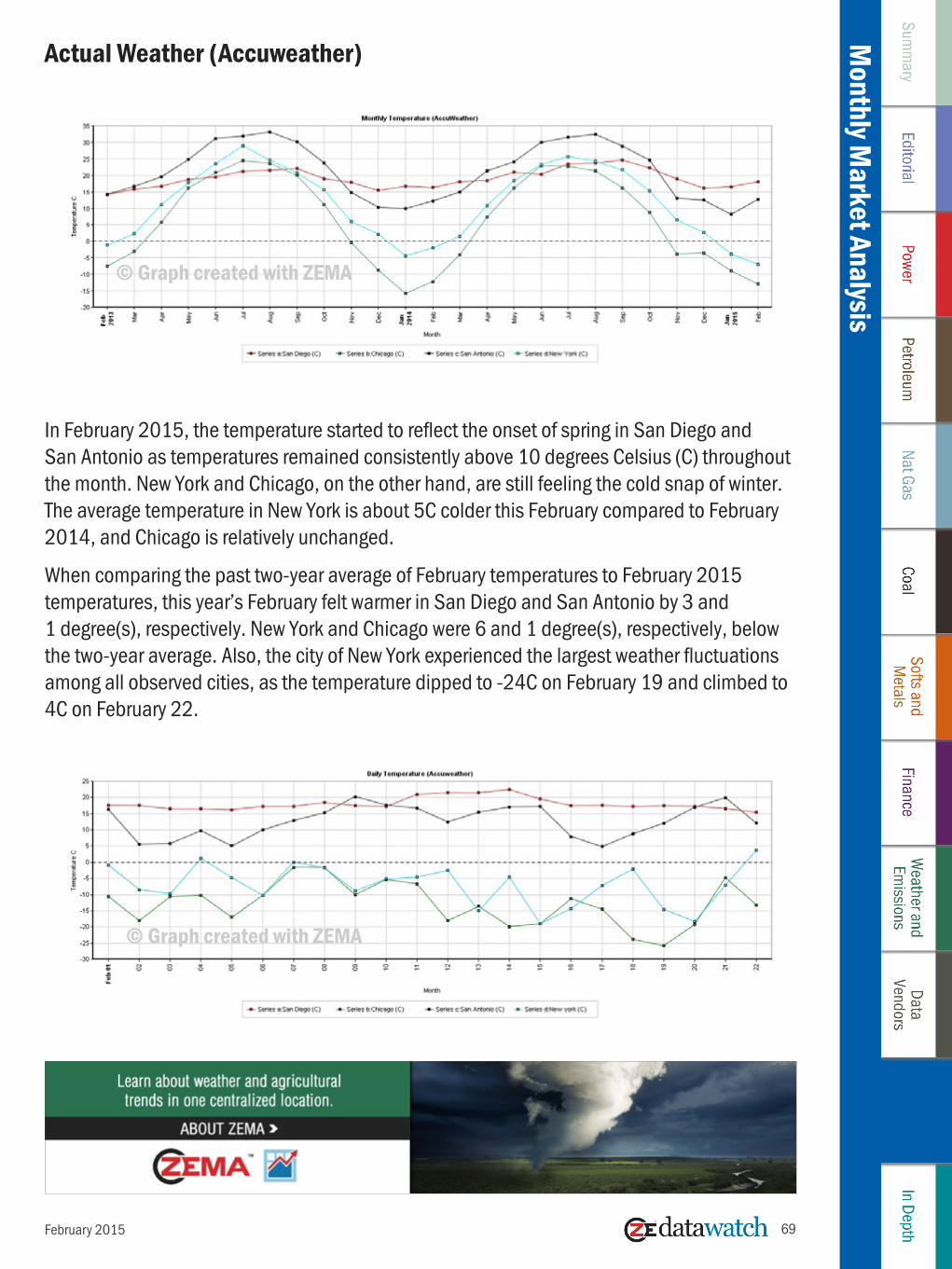

Weather and Emissions 52ICE Futures US Lists Air Pollution Allowance, Solar, and Compliance Futures 52Alternext Lists Oceasoft Sensor Technology Developer 53Platts Discontinues Clean Air Interstate Rule Allowance Assessments 53Argus Discontinues US NOx Codes in Argus Air Daily 54AccuWeather Acquires WeatherBank 54

News from Data Vendors 55ZEMA Adds Oil, Power, Natural Gas, Metals, and Weather Data Sources in February 55ZE Launches ZEMA User Community Platform 56ZE Enhances Corporate Footprint with TIBCO Spotfire 57PEGAS to Enhance Geographical Offer with NBP, ZEE, and PSV Contracts 59PEGAS Introduces Trading for New Common Market Area “TRS” in Southern France on 31 March 60Italian Borders Market Coupling to Launch on February 24, 2015 61Ten Considerations for the European Internal Energy Market 62Platts Forward Curves – Petrochemicals 63OTC Global Holdings Launches EOXLive Markets 64

Monthly Market Analysis 65Crude Oil Brent vs. WTI: Prompt-Month Contract (NYMEX) 65Crude Oil Brent vs. WTI: Forward Curve (NYMEX) 66North American Natural Gas Spot Prices (NYMEX) 67Henry Hub Natural Gas Forward Curve (NYMEX) 68Actual Weather (Accuweather) 69Electricity: Day-Ahead Prices (ICE) 70

In Depth 71Part 2 of 2: The Seven Ages of Oil: Boom and Bust, War and Peace, Growth and Decline 71 The Seven Ages Continued 711973-1994: The Middle East Shrugs its Shackles 731994–2008: Deregulation, Speculation, Manipulation, and Detonation 752008-2015: All Fracked Up 78An Implausible Future 80

Editorial

5February 2015

The concept of microgrids is gaining momentum; their share in the energy space is growing. Microgrid is not a novel concept, as in most remote communities self-containment is the only feasible approach to power supply. For many years, localities without access to major power grids have been served by diesel-fueled power generators hooked up to local distribution systems. Also, it has been almost common for hospitals to have backup, off-grid power supply systems. Nowadays, we are witnessing modernized versions of those microgrids, and this concept expands beyond just providing a backup support for live-critical operations or solving geographical constraints.

Spun off from the smart grid concept, these modern microgrids incorporate similar bells and whistles, such as smart meters, substation automation, energy storage, bidirectional electric vehicle charging, etc. In fact, they are at times being referred to by some analysts as “smart microgrids.” Meanwhile, the concept of scaling down the power supply systems and segregating them from major grids has been gaining larger ground.

Nowadays, independently-run, self-sufficient, and self-reliant grids support the operations of not only hospitals, but also jails, university campuses, and data centers. The microgrid concept is expanding from the level of buildings to municipalities; microgrids are being considered by local authorities to ensure regional sustainability and/or reliability. Thus the East Coast, heavily impacted by weather almost every winter, has been looking for solutions

EditorialThe Emerging Power Markets’ New Player – the Microgrid Operator

By Olga Gorstenko, Editor-In-Chief [email protected]

Editorialthat can ensure power supply to the communities in an “island mode” during times of major grid failures. There are currently several microgrid projects on the table in New York State, ranging from 10 to 200 MW installations.

Those who adopt goals of high penetration of renewable generation and prefer relying on local resources are also lining up for microgrids. Low carbon-based and renewable-based technologies are the main focus of California authorities. On February 3, 2015, the California Energy Commission announced winners of over $20 million that the state allocated to fund microgrid and electric vehicle (EV) charging projects that serve exactly these purposes.

The impact from microgrids on traditional utilities raises reasonable concerns. Obviously, microgrids are taking over the clientele, resulting in utilities losing large demand pockets. Some utilities, like Consolidated Edison in New York, take preventive measures and embark on developing mutually beneficial solutions together with microgrid operators. The most common approach is to view these microgrids as assets to support major grids’ operations. In fact, microgrids can be treated as a special customer class with bidirectional supply. During times of demand spikes, microgrids can become just another source of power supply to the grid.

The next step is creating technological platforms that are capable of monitoring and optimizing microgrid operations. Microsoft and Apple are couple of the first pioneers to provide software platforms and apps. GE and Siemens are working on the hardware side. But this is just a beginning. We have

yet to see what types of new contacts and services are developed between microgrid operators and utilities, as well as ISO/RTOs, and how microgrids will fit into their dispatch stacks. But there are many gaps that microgrid developers have yet to close, from finding sustainable and less expensive batteries to reducing dependence on diesel generators, which are still the most available and reliable generation source. When this happens, we will move one step closer to a new paradigm with a new type of energy markets player, the microgrid operators. In this paradigm, conventional grids and microgrids will work in sync complementing each other. <

6February 2015

EditorialEditor-In-Chief

Email: [email protected] Gorstenko

ZEMA Inquiries Bruce Colquhoun. P: 604-790-3299. E: [email protected]

Advertising & Vendor RelationshipsLaura Smyth. P: 604-790-3299. E: [email protected]

Contact DataWatchE: [email protected] Front Desk: 1-866-944-1469 Editorial Department: 778-296-4183 M: ZE PowerGroup Inc. 130-5920 No. 2 Road, Richmond, BC V7C 4R9 To search our archives: www.datawatch.ze.com

Get real-time data updates @zedatawatch

Subscribe on your iPad today

Power

7February 2015

Power

ICE Futures US Lists PJM, MISO, and SPP Power Futures ContractsOn February 16, 2015, the Intercontinental Exchange (ICE) Futures US listed the following new financial power futures:

• PJM AEP Zone Day-Ahead Peak Fixed Price Future• PJM AEP Zone Day-Ahead Off-Peak Fixed Price Future• PJM FE Ohio Day-Ahead Peak Fixed Price Future• PJM FE Ohio Day-Ahead Off-Peak Fixed Price Future• PJM AEP Zone Day-Ahead Peak Daily Fixed Price Future• PJM AEP Zone Day-Ahead Off-Peak Daily Fixed Price Future• PJM FE Ohio Day-Ahead Peak Daily Fixed Price Future• PJM FE Ohio Day-Ahead Off-Peak Daily Fixed Price Future• MISO Texas Hub Day-Ahead Peak Daily Fixed Price Future• MISO Texas Hub Day-Ahead Off-Peak Daily Fixed Price Future• SPP North Hub Day-Ahead Peak Daily Fixed Price Future• SPP North Hub Day-Ahead Off-Peak Daily Fixed Price Future• SPP South Hub Real-Time Peak Daily Fixed Price Future• SPP South Hub Real-Time Off-Peak Daily Fixed Price FutureSee the original announcement.

ZEMA, ZE’s data management solution, collects numerous records from PJM, SPP, and MISO. To learn more, book a free ZEMA demo by visiting http://www.ze.com/book-a-demo/.

The ZEMA graph below shows the day ahead LMP (Locational Marginal Price) for January 1-31, 2015, from PJM and MISO. Texas Hub prices are published by MISO, and Chicago Hub by PJM. High and low values (red points for MISO and yellow points for PJM) are determined if the points fall outside of two standard deviations of each series’ moving average. Moreover, grey crosses denote sliding correlations between the two series. Formulas for moving average, standard deviation, and sliding correlation are easily applied in ZEMA’s Market Analyzer, while graphs can be viewed instantly and customized for visual preference. To learn more, book a complimentary ZEMA demonstration.

launched exchange trading in Nordic power futures on February 16. The next day, it introduced location spreads for further market areas.

In addition, EEX plans to open an office in Oslo shortly in order to support customers on site and to better service the market’s needs for further development. EEX’s presence in the Nordic Market is supported by Geir Reigstad, who is working as a consultant for the exchange.

Concurrently with the Nordic power futures, EEX launched exchange trading for Spain and Switzerland in February.See the original announcement.

EEX Launches Online Shop for Market Data and New SFTP ServerOn February 1, 2015, EEX launched its new online shop for market data and a new sftp server. The following files provided on the new sftp server have been removed from the EEX website as of February 16:

• Phelix_Quarterly.xls• eex_trade_registration_futures_history_2014.csv• spanish_financial_power_futures_history_2014.csv• italian_financial_power_futures_history_2014.csv• ECarbix_history_YYYY.xlsSee the original announcement.

ZEMA collects a range of European power market data, including over 40 records from the EEX. These records include futures price and trading data. To learn more, visit http://www.ze.com/the-zema-solutions/.

8February 2015

Power

EEX Launches Nordic Power FuturesEffective February 16, 2015, the European Energy Exchange (EEX) reinforced its commitment on the Nordic power market with new products and a regional presence. EEX

© Graph created with ZEMA

9February 2015

Power

Italian Borders Market Coupling LaunchesOn February 24, 2015, the Italian Borders Market Coupling successfully launched. From this date onwards, capacity for the Italian-Austrian, Italian-French, and Italian-Slovenian borders will be implicitly allocated through the PCR solution for the day-ahead markets, making those borders part of the MRC.

Three of the five borders of the Italian Borders Market Coupling Project have been coupled with the Multi-Regional Coupling (MRC), thus linking the majority of EU power markets – from Finland to Portugal and Slovenia. The launch of the Italian Borders Market Coupling provides evidence of the flexibility and reliability of the Price Coupling of Regions (PCR) solution.

The day-ahead markets of MRC extended to the Italian Borders Market Coupling covers 20 European countries, accounting for about 2,800 TWh of yearly consumption. The daily average cleared volume over these countries amounts to over 4 TWh, with an average daily value of over €150m.See the original announcement.

Platts to Remove Descriptive Fields in North American Power CSV FilesEffective May 18, 2015, the descriptive fields (Commodity,Region1,Region2,Hub,TOD,Price Tp,GD Id,GD Tkr,Rel Del Pd,Del Pd,Del Yr) in North American power Market Data CSV files delivered on Platts.com (Athena) will be removed.

In June 2014, Platts Reference Standard (PRS) was launched for electric power and natural gas symbols, which provides a standardized set of reference data for each symbol. The reference data is delivered via CSV files on Platts FTP site, and through Platts Market Data Direct Excel plug-in and API.

This will also bring Platts’ North American power Market Data files in line with the standard CSV data files. For all impacted Market Data categories from which the additional descriptive fields will be removed, see page 45 of Market Data User Guide PDF.See the original announcement.

10February 2015

Power

Platts to Discontinue UK High/Low Power AssessmentsEffective May 5, 2015, Platts intends to remove the table named Platts UK Assessments (GTMA, GBP/MWh) from page 9 of European Power Daily. The table displays UK power assessments as a high/low spread.

The discontinuation of the table in European Power Daily will not affect the databasing of UK GTMA power prices. Platts will continue to publish the Platts UK Assessment Midpoints table on page 2 of European Power Daily.

The data series will continue to be published as a high/low range on European Power Alert and will remain available in Market Data category EE. See the original announcement.

APX and Dutch Energy Regulator Sign MOU on REMIT ImplementationOn January 28, 2015, APX announced the signing of a Memorandum of Understanding (MOU) with the Dutch energy regulator Autoriteit Consument & Market (ACM).

Signing of the MOU reaffirms and formalizes the agreements in place between APX and ACM for the mutual work under REMIT Article 13 and 15.

This MOU will enable APX and ACM to detect and investigate potential market manipulation and insider trading. The MOU outlines procedures and practices for the cooperation. It does not replace nor create additional obligations than those arising from REMIT or national electricity regulation. The cooperation will not restrict, extend or alter the existing powers, functions, or duties of APX or ACM.See the original announcement.

Petroleum

11February 2015

PetroleumPlatts to Launch Rotterdam FOB Jet Barge SwapsOn June 1, 2015, Platts intends to launch new assessments for FOB Rotterdam jet barge swaps at 16:30 London time. The proposal is to assess the swaps as differentials to ICE low sulfur gasoil futures three months forward.

Platts would also publish the price in outright terms, as a differential to ICE Brent crude futures (crack), as a spread to CIF NWE jet cargoes and as a spread to FOB ARA diesel barges.See the original announcement.

ZEMA, ZE’s data management solution, collects over 300 Platts records on petroleum and other liquids. To learn more about ZEMA’s vast data library, visit http://www.ze.com/the-zema-solutions/data-coverage/.

Platts to Launch CFR India Petcoke AssessmentsEffective March 11, 2015, Platts will launch two new fuel grade petroleum coke assessments to reflect the value of imports into India’s East and West coasts. The new assessments reflect the value of high-sulfur fuel grade (HSFG) petroleum coke with a sulfur content of 6.5% and a HGI of 40, delivered to India on a 50,000-mt Supramax vessel, in US$/mt, CFR Krishnapatnam (East) and Kandla (West), 30-60 days from date of publication.

Cargoes traded with more prompt or further forward laycans would be normalized to the middle of the assessment period. For assessment purposes, petcoke with 6-8% sulfur and HGI of 38-55 would be considered. See the original announcement.

ZEMA collects Platts petroleum data from all over the world, including 75 reports from the Asia-Pacific region. To learn more about ZEMA’s extensive data reach, book a complimentary demo at http://www.ze.com/book-a-demo/.

Platts to Launch Weekly Turkey Mid-Sulfur Petcoke AssessmentEffective, March 4, 2015, Platts intends to launch a new weekly CIF Turkey mid-sulfur petroleum coke assessment.

The new assessment will take into account petcoke trades done in a forward 30-60-day delivery window. Cargos traded with more prompt or further forward laycans will be normalized to the middle of the assessment period. The assessment will be normalized to the discharge port of Iskenderun, but will take into account the ports of Izmir, Marmara and Samsun.

The range of petcoke specifications for inclusion in the assessment will be: calorific value of 7,000-8,000 kcal/kg NAR, 4-5.5% sulfur content dry basis and Hardgrove Grindability Index of 30-80.

The price assessment will be normalized to reflect the price of mid-sulfur petcoke of 5% sulfur content dry basis and 50 HGI in Supramax 50,000 mt vessels on a 7,500 kcal/kg NAR calorific value basis.See the original announcement.

Petroleum

12February 2015

Platts Introduces Naptha against M3 Waterborne Gasoline AssessmentsEffective February 19, 2015, Platts began assessing standard and heavy naphtha against M3 (11.5 RVP) waterborne gasoline. Bids and offers in the Platts Market on Close assessment process that price against M3 will be normalized back to M4 based on publicly available information that Platts received up until February 18, 2015.See the original announcement.

To learn more about gasoline prices in Europe and the United States, use ZEMA to view records from Platts. To learn more, visit http://www.ze.com/the-zema-solutions/.

The following ZEMA graph represents three alternative tanker routes: TC2 Europe to the US Atlantic coast, TC 5 Ras Tanura to Yokohama, and TD3 Middle Easterm Gulf to Japan. Also included is the Average RBOB for gasoline within the same time periods. From the graph it is easy to see that the shipping lines steadily increased their rates from 2010 onwards. In 2011, we can see rates becoming increasingly competitive, creating a price war, as container lines sought to fill their new ships and defend their market share. From the graph, we can also see the price of gasoline having an impact, likely adding to the shippers’ running costs. To learn more about the ZEMA solution, please book a complimentary demonstration.

Petroleum

© Graph created with ZEMA

Petroleum

13February 2015

Platts Launches Colonial Pipeline Line Space AssessmentsAs of February 2, 2015, Platts has started assessing the value of line space for distillates and gasoline on three major Colonial Pipeline segments between Pasadena, Texas, and Linden, New Jersey.

The assessments reflect a negotiated spot market price in cents/gallon. They reflect the premium or discount paid during the exchange of product at two locations along Colonial’s Line 1 and/or Line 3, as well as Line 2 and/or Line 3.

The assessments are linked with cycle numbers on the Colonial Pipeline schedule.

The 18 new assessments are:

• AAXTA00 – Line space for gasoline on Line 1• AAXTACY – The Colonial cycle number for which Line 1 space is assessed for gasoline • AAXTA03 – The monthly average for line space for gasoline on Line 1• AAXTC00 – Line space for gasoline on Line 1 and Line 3• AAXTCCY – The Colonial cycle number for which Line 1 and Line 3 space are assessed for gasoline • AAXTC03 – The monthly average for line space for gasoline on Line 1 and Line 3• AAXTB00 – Line space for gasoline on Line 3• AAXTBCY – The Colonial cycle number for which Line 3 space is assessed for gasoline • AAXTB03 – The monthly average for line space for gasoline on Line 3• AAXTD00 – Line space for distillates on Line 2• AAXTDCY – The Colonial cycle number for which Line 2 space is assessed for distillates • AAXTD03 – The monthly average for line space for distillates on Line 2• AAXTG00 – Line space for distillates on Line 2 and Line 3• AAXTGCY – The Colonial cycle number for which Line 2 and Line 3 space are assessed for distillates • AAXTG03 – The monthly average for line space for distillates on Line 2 and Line 3• AAXTE00 – Line space for distillates on Line 3• AAXTECY – The Colonial cycle number for which Line 3 space is assessed for distillates • AAXTE03 – The monthly average for line space for distillates on Line 3

The assessments reflect the transfer of a minimum of 25,000 barrels of distillates or gasoline and are not limited to any specific product.

Frozen cycles and spur lines are not part of the assessments.See the original announcement.

Petroleum

Petroleum

14February 2015

Argus Introduces New European Gasoil Bunker AssessmentsEffective March 3, 2015, Argus introduced the following series. These series appear in the DLP files in the DEURO folder of ftp.argusmedia.com.

PA-codeTime Stamp

Price Type

Continuous Forward

Description Category Frequency

PA0011464 6 1, 2 0Gasoil bunker Antwerp

->Products->Gasoil/Diesel/Heating oil->Northwest Europe

Daily

PA0011472 6 1, 2, 6, 7 0Gasoil bunker Rotterdam

->Products->Gasoil/Diesel/Heating oil->Northwest Europe

Daily

See the original announcement.

ZEMA collects a range of Argus petroleum assessment data, including data from the European Crude (Spot Prices) record and the Argus Crude record. To learn more, visit http://www.ze.com/the-zema-solutions/.

Argus Adds New Weekly Snapshot Value for German Diesel BargeOn February 12, 2015, Argus added a new weekly snapshot value for German 10ppm diesel barge NWE. The following code is being added to the DAGM data files in the \DAGM folder of the ftp.argusmedia.com server.

PA-code Time Stamp

Price Type

Continuous Forward

Description Unit Category Frequency

PA5001478 6 8 0

Gasoil diesel 10ppm German NWE barge snapshot

USD/t

->Products-> Gasoil/Diesel/ Heating oil-> Northwest Europe

Weekly

See the original announcement.

Argus Launches New Petcoke AssessmentsOn February 11, 2015, Argus added the following new codes to Energy Argus Petroleum Coke:

PA-codeTime Stamp

Price Type

Description Unit Category Frequency

PA0015716 21 8Petroleum coke fob USWC <2.0% sulphur 45 HGI

USD/t ->Petroleum Coke->USA Weekly

PA0015717 21 8Petroleum coke cfr Turkey 4.5% 70 HGI

USD/t->Petroleum Coke->East Mediterranean

Weekly

PA0015718 21 8Petroleum coke fob Venezuela 4.5% 70 HGI

USD/t->Petroleum Coke-> Latin America

Weekly

Petroleum

Petroleum

15

PA-codeTime Stamp

Price Type

Description Unit Category Frequency

PA0015719 0 1, 2Petroleum coke fob USWC <2.0% sulphur 45 HGI month

USD/t ->Petroleum Coke->USA Monthly

PA0015720 0 1, 2Petroleum coke cfr Turkey 4.5% 70 HGI month

USD/t->Petroleum Coke-> East Mediterranean

Monthly

PA0015721 0 1, 2Petroleum coke fob Venezuela 4.5% 70 HGI month

USD/t->Petroleum Coke-> Latin America

Monthly

PA0015722 21 8

Petroleum coke fob USWC <2.0% sulphur 45 HGI 4 weeks average

USD/t ->Petroleum Coke->USA Weekly

PA0015723 21 8Petroleum coke cfr Turkey 4.5% 70 HGI 4 weeks average

USD/t->Petroleum Coke-> East Mediterranean

Weekly

PA0015724 21 8Petroleum coke fob Venezuela 4.5% 70 HGI 4 weeks average

USD/t->Petroleum Coke-> Latin America

Weekly

See the original announcement.

ZEMA collects over 100 Argus reports regularly, more than 40 of which pertain to petroleum products. To learn more about ZEMA’s vast data coverage, visit http://www.ze.com/the-zema-solutions/data-coverage/.

Argus Adds New Ukrainian Diesel and Gasoline AssessmentsEffective February 9, 2015, Argus introduced new daily assessments in Argus Ukrainian Motor Fuels. The following series will appear in DUMF module and in dumf.csv files in DUMF folder on tp.argusmedia.com server.

PA-code Time Stamp

Price Type

Continuous Forward

Description Differential Basis

Unit Category Frequency

PA0015696 0 1, 2, 6, 7

0

Gasoil die-sel 10 ppm daf Belar-us/Ukraine border (Lithuania)

Diesel NWE barges/cargo

USD/t

->Products-> Gasoil/Diesel/Heating oil->Ukraine

Daily

PA0015697 0 1, 2, 6, 7

0

Gasoil diesel 10 ppm cif Ukrainian ports

Diesel fob Med

USD/t

->Products-> Gasoil/Diesel/Heating oil->Ukraine

Daily

PA0015698 0 1, 2 0

Gasoline A-95 fca North-West Ukraine

- UAH/t ->Products-> Gasoline-> Ukraine

Daily

See the original announcement.

Petroleum

February 2015

Petroleum

16

Petroleum

Argus Introduces New Paraxylene Sinopec AssessmentsEffective February 6, 2015, Argus introduced new series to Argus DeWitt Toluene, Xylenes, and Isomers / PET. This applies to the dtxweekly data file in the DATA/DTXWeekly folder offtp.argusmedia.com.

PA-codeTime Stamp

Price Type

Continuous Forward

Description Unit Category Frequency

PA0015687 0 1, 2 1Paraxylene Sinopec delivered import parity USD/t month

USD/t->Petrochemicals-> Paraxylene-> Asia-Pacific

Weekly

PA0015688 0 1, 2 1Paraxylene Sinopec delivered CNY/t month

CNY/t->Petrochemicals-> Paraxylene-> Asia-Pacific

Weekly

See the original announcement.

ZEMA collects data on a wide range of petroleum products and other liquids from reports such as DeWitt Benzene Daily and DeWitt DTX Weekly. Learn more at http://www.ze.com/the-zema-solutions/.

Argus Adds New Gasoil Bunker CodesOn February 6, 2015, Argus added the following three gasoil bunker codes to Argus Marine Fuels:

PA-codeTime Stamp

Price Type

Description Unit Category Frequency

PA0015700 6 1, 2Gasoil bunker Rotterdam $/mnBtu

USD/mnBtu

->Products-> Gasoil/Diesel/Heating oil->Northwest Europe

Daily

PA0015701

2 1, 2Gasoil bunker Houston $/mnBtu

USD/mnBtu

->Products->Gasoil/Diesel/Heating oil->US Gulf coast

Daily

PA0015702 2 1, 2Gasoil bunker New Orleans $/mnBtu

USD/mnBtu

->Products->Gasoil/Diesel/Heating oil->US Gulf coast

Daily

See the original announcement.

February 2015

Petroleum

17

PetroleumCME to List European and South Korean Trade Month Benzene FuturesOn March 8, 2015, the following trade month Benzene futures will be listed for trading by the Chicago Mercantile Exchange (CME) on CME Globex and clearing submission via CME ClearPort:

Trade Month Benzene Futures

Futures Product NamesFIX/FAST and iLink: tag 1151-Security Group MDP 3.0: tag 6937-Asset

FIX/FAST and iLink: tag 55-Symbol MDP 3.0 tag 1151 - Security Group

European Benzene cif ARA (Argus) Trade Month Futures

BEA JR

Benzene fob South Korea (Argus) Trade Month Futures

BSA JR

See the original announcement.

Using ZEMA’s advanced data collection and analytic capabilities, market participants can easily keep track of the new data that will be generated by CME Globex. To learn more, visit http://www.ze.com/the-zema-solutions /.

CME to Launch Crude Oil and Refined FuturesEffective March 8, 2015, the following crude oil and refined futures will be listed for trading on CME Globex and clearing submission via CME ClearPort:

ProductFIX/FAST and iLink: tag 1151-Security Group MDP 3.0: tag 6937-Asset

FIX/FAST and iLink: tag 55-Symbol MDP 3.0 tag 1151 - Security Group

Futures Product Name tag 1151-SecurityGroup tag 55-Symbol

Mini 3.5% Fuel Oil Barges FOB Rdam (Platts) Crack Spread (100mt) Futures

MFR RF

Mini 1% Fuel oil Cargoes FOB NWE (Platts) Crack Spread (100mt) Futures

MNS RF

Mini Brent Financial Futures MBC PT

Mini Dated Brent (Platts) Financial Futures MDB RF

Mini East-West Fuel Oil Spread (Platts) Futures MEW PT

Mini Singapore Fuel Oil 380cst (Platts) vs. European 3.5% Fuel Oil Barges FOB Rdam (Platts) Futures

MSB RF

Mini 1% Fuel Oil Cargoes CIF NWE(Platts) Futures MFP RF

See the original announcement.

February 2015

Natural Gas

18

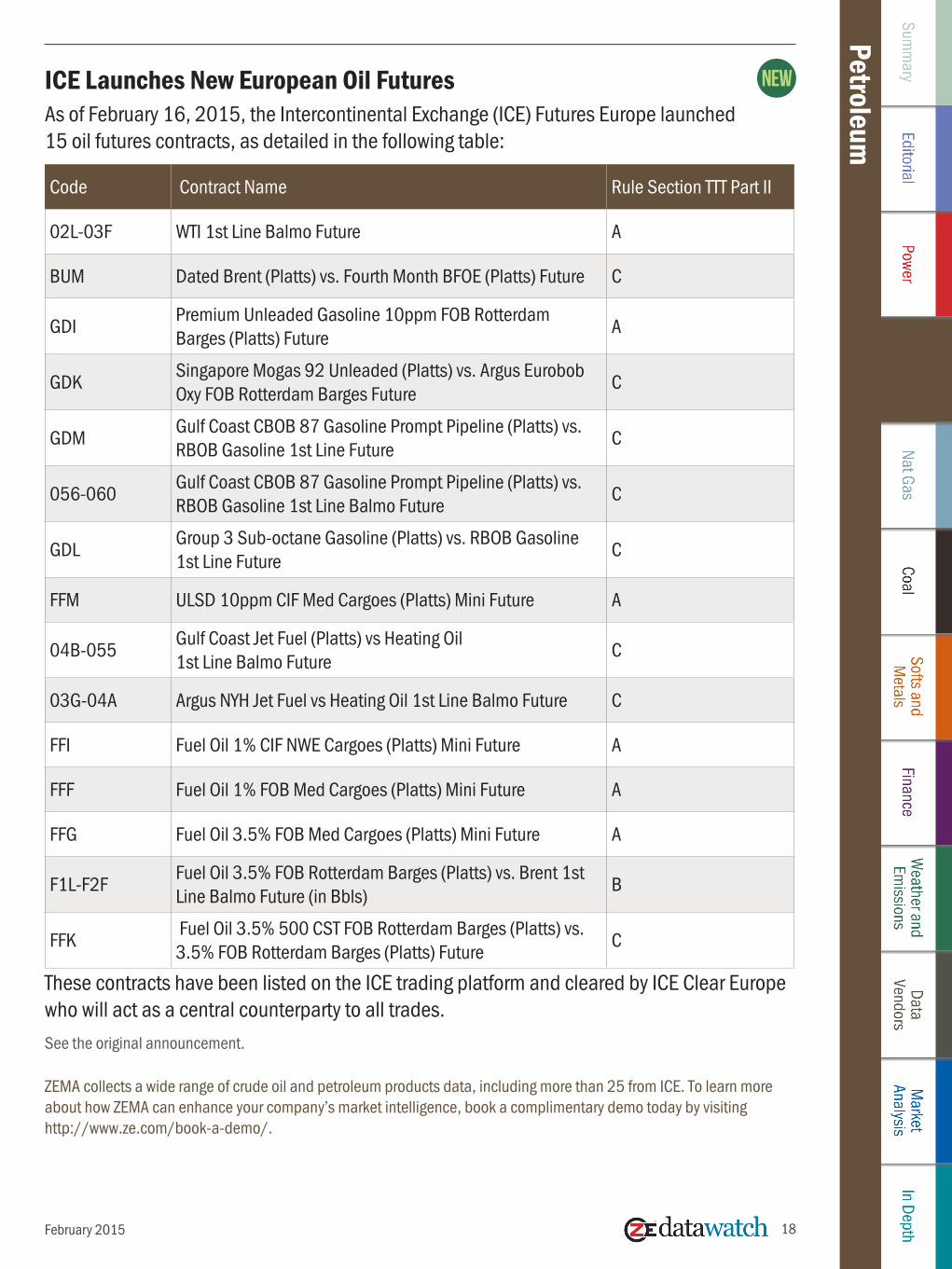

PetroleumICE Launches New European Oil FuturesAs of February 16, 2015, the Intercontinental Exchange (ICE) Futures Europe launched 15 oil futures contracts, as detailed in the following table:

Code Contract Name Rule Section TTT Part II

02L-03F WTI 1st Line Balmo Future A

BUM Dated Brent (Platts) vs. Fourth Month BFOE (Platts) Future C

GDI Premium Unleaded Gasoline 10ppm FOB Rotterdam Barges (Platts) Future

A

GDK Singapore Mogas 92 Unleaded (Platts) vs. Argus Eurobob Oxy FOB Rotterdam Barges Future

C

GDM Gulf Coast CBOB 87 Gasoline Prompt Pipeline (Platts) vs. RBOB Gasoline 1st Line Future

C

056-060 Gulf Coast CBOB 87 Gasoline Prompt Pipeline (Platts) vs. RBOB Gasoline 1st Line Balmo Future

C

GDL Group 3 Sub-octane Gasoline (Platts) vs. RBOB Gasoline 1st Line Future

C

FFM ULSD 10ppm CIF Med Cargoes (Platts) Mini Future A

04B-055 Gulf Coast Jet Fuel (Platts) vs Heating Oil 1st Line Balmo Future

C

03G-04A Argus NYH Jet Fuel vs Heating Oil 1st Line Balmo Future C

FFI Fuel Oil 1% CIF NWE Cargoes (Platts) Mini Future A

FFF Fuel Oil 1% FOB Med Cargoes (Platts) Mini Future A

FFG Fuel Oil 3.5% FOB Med Cargoes (Platts) Mini Future A

F1L-F2F Fuel Oil 3.5% FOB Rotterdam Barges (Platts) vs. Brent 1st Line Balmo Future (in Bbls)

B

FFK Fuel Oil 3.5% 500 CST FOB Rotterdam Barges (Platts) vs. 3.5% FOB Rotterdam Barges (Platts) Future

C

These contracts have been listed on the ICE trading platform and cleared by ICE Clear Europe who will act as a central counterparty to all trades.See the original announcement.

ZEMA collects a wide range of crude oil and petroleum products data, including more than 25 from ICE. To learn more about how ZEMA can enhance your company’s market intelligence, book a complimentary demo today by visiting http://www.ze.com/book-a-demo/.

February 2015

Petroleum

19

Platts to Discontinue European and Mediterranean Low Sulfur 1% Bunker AssessmentsAs of September 1, 2015, Platts will no longer publish its Northwest European, Gibraltar, Algeciras, and Malta low sulfur (1% sulfur) bunker fuel assessments. Platts will continue to assess low sulfur bunker fuel in the ports of Genoa and Piraeus, reflecting the continuation of regional coastal and domestic usage.

In January 2015, low sulfur fuel oil became largely redundant as a bunker fuel. In the wake of the January 1, 2015 implementation of legislation from the International Convention for the Prevention of Pollution from Ships (MARPOL), which further limited the sulfur emissions from ships operating within any Emission Control Area to a maximum of 0.1% from 1% previously, bunker demand for 1% sulfur fuel oil largely disappeared.

Demand for low sulfur bunker fuel has generally been replaced by demand for marine gasoil, or other similar, ultra low sulfur fuels. Pockets of demand for 1% sulfur fuel oil across Europe still exist, though demand is drastically reduced. Platts is maintaining its Genoa and Piraeus low sulfur bunker fuel assessments in order to reflect the pockets of demand specific to the two ports.

Platts will continue to publish assessments for marine gasoil (0.1% sulfur) for all of its existing European and African ports. Platts will also continue to monitor the development of the emerging supply of new ultra low sulfur bunker fuels across Europe and Africa, demand and supply patterns for these fuels, and subscriber demand for new assessments.

Platts low sulfur bunker fuel assessments are currently published in Platts Bunkerwire and on Platts Global Alert. For a complete list of all affected assessments and their PGA codes, please see the table below.

Code Assessment PGA Page Month Code Month PGA Page

AASTY00 Rotterdam LS 1% PGA1850 AASTY03 PGA1861

AASUA00 Antwerp LS 1% PGA1850 AASUA03 PGA1861

AASUM00 Dunkirk LS 1% PGA1850 AASUM03 PGA1861

AASUC00 Hamburg LS 1% PGA1850 AASUC03 PGA1861

AAVVZ00 Gothenburg 1% PGA1870 AAVVZ03 PGA1871

AASUE00 Great Belt LS 1% PGA1870 AASUE03 PGA1871

AASUG00 Gdansk LS 1% PGA1870 AASUG03 PGA1871

AASUI00 St Petersburg LS 1% PGA1870 AASUI03 PGA1871

AAVIW00 Gibraltar LS 1% PGA1860 AAVIW03 PGA1861

AAXCZ00 Algeciras LS 1% PGA1860 AAXCZ03 PGA1861

AARTD00 Malta LS 1% PGA1860 AARTD03 PGA1861See the original announcement.

February 2015

Petroleum

Petroleum

20

Platts to End No. 2 New York Harbor Cargos at London MOCAs of April 1, 2015, Platts will no longer publish its No. 2 gasoil cargo assessment at London MOC, in tandem with the discontinuation of its US Atlantic Coast distillate cargo assessments on the same day.

The proposed change is a result of evolving market conditions and state regulations in the US Northeast distillate markets and a lack of an Atlantic Coast No. 2 cargo assessment after March 2015.

As a result of this change, Platts will no longer publish assessments under database codes AAPYY10 (No. 2 at London 16:30 in cts/gal) and AAPYY00 (No. 2 at London 16:30 in Euro cts/gal).

These assessments can also be found on Platts Global Alert page 1450. Platts will continue to publish its existing New York Harbor gasoline assessment at 16:30 London time. See the original announcement.

Platts Stops Weekly DOP AssessmentOn February 9, 2015, Platts announced a proposal to discontinue its weekly US dioctyl phthalate assessment due to a change in market dynamics.

Liquidity in the US market for DOP has dropped significantly as substitute plasticizers have become more commonplace. These assessments are published on Page PCA161 and are listed under the following codes in the Platts price database: DOP FD US Domestic Weekly, PHARA00; Monthly Average, PHARB03.

These assessments are also published in the Platts Petrochemical Alert. See the original announcement.

Platts Discontinues US Ketones AssessmentsOn Feb 9, 2015, Platts announced its proposal to discontinue all methyl ethyl ketone and methyl isobutyl ketone assessments in the US due to a lack of liquidity in these markets.

Platts intends to end publication of these assessments from September 1, 2015. Affected assessments:

• MEK FOB USG Weekly PHADQ00 PHAYT03 • MEK DER US Domestic Weekly PHADT00 PHAYU03 • MIBK FOB USG Weekly PHADW00 PHAYX03 • MIBK DER US Domestic Weekly PHADZ00 PHAYY03

These assessments can be found on Platts Petrochemical Alert and in the Global Solventswire.See the original announcement.

February 2015

Petroleum

Petroleum

21

Argus Stops Publishing European and Mediterranean Fuel Oil Bunker AssessmentsOn February 27, 2015, Argus discontinued the following series. These series are in the DAMarineF files in the DAMarineF folder of ftp.argusmedia.com.

PA-codeTime Stamp

Price Type

Description Category Frequency

PA0004110 6 1, 2Fuel oil bunker low sulphur 380 cst Antwerp

->Products->Fuel oil->Northwest Europe

Daily

PA0004111 6 1, 2Fuel oil bunker low sulphur 380 cst Rotterdam

->Products->Fuel oil->Northwest Europe

Daily

PA0011459 6 1, 2Fuel oil bunker LS 380 cst Gibraltar

->Products->Fuel oil-> Mediterranean

Daily

PA0011460 6 1, 2Fuel oil bunker LS 380 cst Hamburg

->Products->Fuel oil->Northwest Europe

Daily

PA0011461 6 1, 2Fuel oil bunker LS 380 cst Malta

->Products->Fuel oil-> Mediterranean

Daily

PA0011462 6 1, 2Fuel oil bunker LS 380 cst Piraeus

->Products->Fuel oil-> Mediterranean

Daily

See the original announcement.

Argus Discontinues US Diesel and Fuel Oil AssessmentsEffective February 17, 2015, Argus stopped codes in the Argus US Products publication and data module. For FTP subscribers, these changes apply to data in the dhp .csv files in the DUSPR folder on ftp.argusmedia.com.

PA-codeTime Stamp

Price Type

Description Unit Category Frequency

PA0002192 2 8Diesel 500ppm NYH barge BTU value

USD/mnBtu

->Products->Gasoil/Diesel/Heating oil->US east coast

Daily

PA0002193 2 8Fuel oil No 6 1% NYH BTU value

USD/mnBtu

->Spark spread->North America->New York

Daily

PA0002194 2 8Fuel oil No 6 0.3% high-pour NYH BTU value

USD/mnBtu

->Spark spread->North America->New York

Daily

PA0002195 2 8Spark spread NYH Diesel barge

USD/mnBtu

->Spark spread->North America->New York

Daily

PA0002197 2 8Spark spread NYH Fuel oil No 6 1%

USD/mnBtu

->Spark spread->North America->New York

Daily

PA0002198 2 8Spark spread NYH Fuel oil No 6 0.3% high-pour

USD/mnBtu

->Spark spread->North America->New York

Daily

See the original announcement.

February 2015

Petroleum

Petroleum

22

CME Delists Two Brent Crude Oil CFD Futures ContractsOn February 2, 2015, NYMEX delisted two Brent crude oil CFD futures contracts as set out in the table below. There was no open interest in these contracts.

Product Name Commodity CodeNYMEX Rulebook Chapter Number

Brent CFD: Dated Brent (Platts) vs. Brent Front Month (Platts) Weekly Futures

CFA 1144

Brent CFD: Dated Brent (Platts) vs. Brent Front Month (Platts) Daily Futures

1C 319

As a result of the delisting, information regarding these contracts has been deleted from the respective product chapters, all other references to the contracts, and the terms and conditions contained in the Position Limit, Position Accountability, and Reportable Level Table located in the Interpretations and Special Notices Section of Chapter 5 (Trading Qualifications and Practices) of the NYMEX Rulebook were removed from the Rulebook.See the original announcement.

Platts to Extend Low Sulfur Gasoil Futures CurveEffective June 1, 2015, Platts intends to launch new assessments for ICE low sulfur gasoil futures at 16:30 London time.

Currently, Platts only assesses months one, two, and three. The proposal is to extend the ICE low sulfur gasoil futures assessments to 36 months, 12 quarters, and three years forward. See the original announcement.

Platts Edits European Polymer Contract Price Assessment ParametersEffective February 26, 2015, Platts further defined the parameters reflected in its European polymer contract price assessments. Platts defined a contract price as one negotiated against an annual commitment to supply or procure regular monthly volumes.

Platts may use information on all contractually agreed volumes to form the basis of its assessments, although assessments will be normalized to reflect contractual commitments of 3,000-6,000 mt/year.

The governing factor in the price assessments, however, reflects the negotiated and mutually agreed absolute price.See the original announcement.

February 2015

Petroleum

23February 2015

Petroleum

Platts’ Data Source Changes Petroleum Floor Trading VolumesEffective December 22, 2014, Platts’ NYMEX end of day data provider Commodity Systems Inc. has implemented a change so floor trading volume represents only pit session (RTH: regular trading hours) trading activity. Prior to this date, volume data for floor trading included trading activity from both floor trading and electronic sessions combined. The following are the floor trading contracts affected:

Floor trading contracts Symbol Prefix

NYMEX Light Crude Floor XNCL

NYMEX RBOB Floor XNRB

NYMEX NY ULSD Floor XNHO

The corresponding combined trading contracts:

Floor trading contracts Symbol Prefix

NYMEX Light Crude Combined XNCC

NYMEX RBOB Combined XNRB

NYMEX NY ULSD Combined XNHO

See the original announcement.

Natural GasNatural Gas

24February 2015

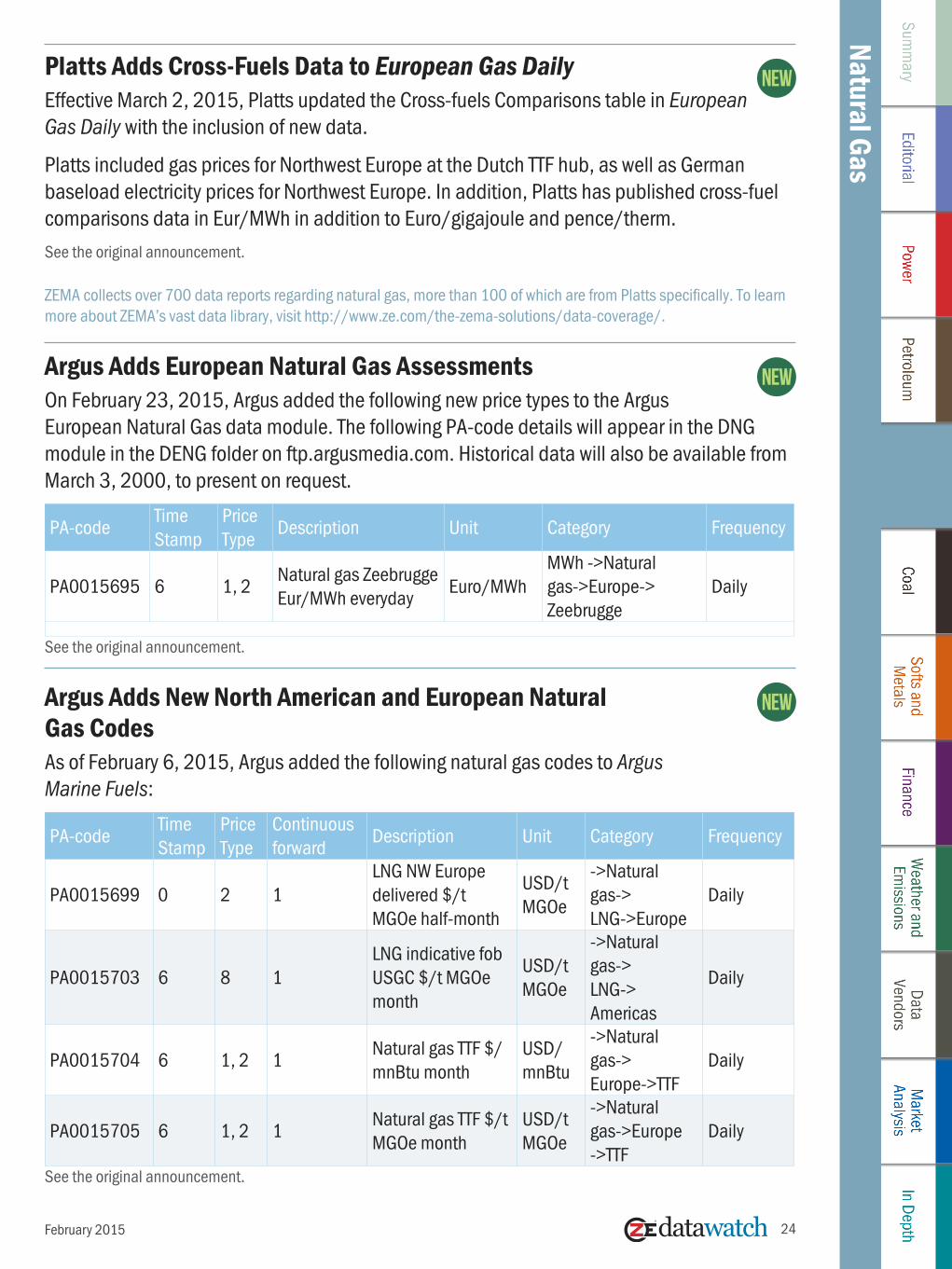

Platts Adds Cross-Fuels Data to European Gas DailyEffective March 2, 2015, Platts updated the Cross-fuels Comparisons table in European Gas Daily with the inclusion of new data.

Platts included gas prices for Northwest Europe at the Dutch TTF hub, as well as German baseload electricity prices for Northwest Europe. In addition, Platts has published cross-fuel comparisons data in Eur/MWh in addition to Euro/gigajoule and pence/therm.See the original announcement.

ZEMA collects over 700 data reports regarding natural gas, more than 100 of which are from Platts specifically. To learn more about ZEMA’s vast data library, visit http://www.ze.com/the-zema-solutions/data-coverage/.

Argus Adds European Natural Gas AssessmentsOn February 23, 2015, Argus added the following new price types to the Argus European Natural Gas data module. The following PA-code details will appear in the DNG module in the DENG folder on ftp.argusmedia.com. Historical data will also be available from March 3, 2000, to present on request.

PA-codeTime Stamp

Price Type

Description Unit Category Frequency

PA0015695 6 1, 2Natural gas Zeebrugge Eur/MWh everyday

Euro/MWhMWh ->Natural gas->Europe-> Zeebrugge

Daily

See the original announcement.

Argus Adds New North American and European Natural Gas CodesAs of February 6, 2015, Argus added the following natural gas codes to Argus Marine Fuels:

PA-codeTime Stamp

Price Type

Continuous forward

Description Unit Category Frequency

PA0015699 0 2 1LNG NW Europe delivered $/t MGOe half-month

USD/t MGOe

->Natural gas-> LNG->Europe

Daily

PA0015703 6 8 1LNG indicative fob USGC $/t MGOe month

USD/t MGOe

->Natural gas-> LNG-> Americas

Daily

PA0015704 6 1, 2 1Natural gas TTF $/mnBtu month

USD/mnBtu

->Natural gas-> Europe->TTF

Daily

PA0015705 6 1, 2 1Natural gas TTF $/t MGOe month

USD/t MGOe

->Natural gas->Europe ->TTF

Daily

See the original announcement.

Natural GasNatural Gas

25

CME Europe Launches Italian Natural Gas FuturesEffective February 1, 2015, the Chicago Mercantile Exchange (CME) Europe listed the following energy futures for trading on CME Globex and clearing submission via CME ClearPort:

ProductFIX/FAST and iLink: tag 1151-Security Group MDP 3.0: tag 6937-Asset

FIX/FAST and iLink: tag 55-SymbolMDP 3.0 tag 1151 - Security Group

Italian PSV Natural Gas (ICIS Heren) Calendar Month Future (Variable Quantity)

IPE JQ

Italian PSV Natural Gas (ICIS Heren) vs. Dutch TTF Natural Gas (ICIS Heren) Calendar Month Spread Future (Variable Quantity)

DPE JQ

These contracts are listed on, and subject to, the rules of UK RIE CME Europe Ltd.See the original announcement.

Using ZEMA’s advanced data collection and analytic capabilities, market participants can easily keep track of the new data that will be generated by CME Globex and CME Europe Ltd. To learn more, visit http://www.ze.com/the-zema-solutions/.

The ZEMA graph shows the Italian natural gas monthly future settlement with monthly shaping average and yearly average for years 2015-2016. The minimum future settlement for the whole period is about 15 Euro/MWh as of April 2015; but the price increases from that point before reaching a maximum of 17.3 Euro/MWh in October 2015. The settlements in 2015 have more fluctuations compared with those in 2016; but overall, the yearly average for the two years remains almost constant (red spots in graph). Analysis like this is easy to customize in ZEMA, due to the solution’s enhanced visualization functionalities. To learn more about the ZEMA solution, please book a complimentary demonstration.

February 2015

© Graph created with ZEMA

Natural GasNatural Gas

26

ICE Futures US Lists Six New Natural Gas FuturesEffective February 16, 2015, the Intercontinental Exchange (ICE) Futures US listed the following natural gas futures contracts:

• Transco Leidy Basis Future• Transco Leidy Swing Future• Transco Leidy Index Future• Tennessee Zone 4 300L Basis Future• Tennessee Zone 4 300L Swing Future• Tennessee Zone 4 300L Index FutureSee the original announcement.

ZEMA collects natural gas records from all over the world and from dozens of different data sources. To receive a complimentary ZEMA demonstration, visit http://www.ze.com/book-a-demo/.

Deutsche Börse Market Data + Services Becomes Exclusive Licensor of PEGASOn February 9, 2015, Deutsche Börse Market Data + Services announced that it has become the exclusive licensor of real-time market data for spot, derivatives, and spread products traded on PEGAS, as of January 1, 2015. PEGAS is the central natural gas trading platform of EEX Group, operated by Powernext.

The PEGAS real-time market data product contains prices of traded within-day, day-ahead, weekend, as well as individual days gas spot contracts. Moreover, it includes prices of traded future gas contracts and prices of traded location spreads.See the original announcement.

Marex Spectron Trades CME Europe TTF and NBP Natural Gas FuturesEffective February 2, 2015, Marex Spectron has executed the first trade of CME Europe’s new monthly Dutch (TTF) and UK (NBP) Natural Gas futures.

The TTF contract was traded for one of Marex Spectron’s major energy clients on the first day of the new products’ availability. On 20 January, Marex Spectron executed the first trade of the CME Europe’s new monthly UK (NBP) Natural Gas future, ending day two of trading in the new contract by arranging three block trades with a total of 75k Therms.

The new contracts are financial and physical cleared products that are available to trade via straight through processing on Marex Spectron’s market venue. They are:

• UK Natural Gas Daily Futures• UK Natural Gas Calendar Month Futures

February 2015

Natural GasNatural Gas

27

• Dutch Natural Gas Daily Futures• Dutch Natural Gas Calendar Month Futures

For all contracts, the front month will be March 2015, and the prompt has been available from February 2, 2015.See the original announcement.

ZEMA regularly collects more than 100 records from the Chicago Mercantile Exchange, several of which are about natural gas futures. Learn more about the ZEMA solution at http://www.ze.com/the-zema-solutions/.

Platts to Discontinue Descriptive Fields in North American Natural Gas CSV FilesEffective May 18, 2015, the descriptive fields (Commodity,Region1,Region2,Hub,TOD,Price Tp,GD Id,GD Tkr,Rel Del Pd,Del Pd,Del Yr) in North American natural gas Market Data CSV files delivered on Platts.com (Athena) will be removed.

This will also bring Platts’ North American natural gas Market Data files in line with the standard CSV data files. For all impacted Market Data categories from which the additional descriptive fields will be removed, see page 45 of Market Data User Guide PDF.See the original announcement.

Argus to Discontinue Propane Swap AssessmentsEffective March 31, 2015, Argus is stopping the following price types (high and low). These will stop for these series, but the midpoints introduced in January 2015 will continue beyond March. These series will be found in the dpgeurope and dpg data file in the \DLPG folder of ftp.argusmedia.com.

PA-codeTime Stamp

Price Type

Continuous Forward

Description Unit Category Frequency

PA0002720 6 1, 21, 2, 3, 4, 5, 6

Propane Swaps NWE month

USD/t->LPG-> Northwest Europe-> Propane

Daily

PA0002721 6 1, 2 1, 2, 3Propane Swaps NWE quarter

USD/t->LPG-> Northwest Europe-> Propane

Daily

PA0002722 6 1, 2 1, 2, 3Propane CP swap month

USD->LPG->Mideast Gulf->Propane

Daily

PA0002723 6 1, 2 1, 2, 3Propane Far East Index swap month

USD->LPG-> Asia-Pacific-> Pro-pane

Daily

See the original announcement.

February 2015

28February 2015

Natural Gas

Argus Discontinues New York Natural Gas AssessmentsAs of February 18, 2015, Argus has stopped the following code in the Argus US Products publication and data module. For FTP subscribers, these changes apply to data in the dhp .csv files in the DUSPR folder on ftp.argusmedia.com.

PA-codeTime Stamp

Price Type

Description Unit Category Frequency

PA0002204 2 8 New York gas (USP)USD/mnBtu

->Spark spread->North America->New York

Daily

PA0002205 2 8Coal New York BTU value (USP)

USD/mnBtu

->Spark spread->North America->New York

Daily

PA0002207 2 8Spark spread New York natural gas (USP)

USD/mnBtu

->Spark spread->North America->New York

Daily

See the original announcement.

Platts’ Data Source Changes Henry Hub Floor Trading VolumesOn December 22, 2014, Platts’ NYMEX end of day data provider Commodity Systems Inc. has implemented a change so floor trading volume represents only pit session trading activity. Prior to this date, volume data for floor trading included trading activity from both floor trading and electronic sessions combined:

Floor trading contract Symbol Prefix

NYMEX Henry Hub Natgas Floor XNNG

Combined trading contract Symbol Prefix

NYMEX Henry Hub Natgas Combined XNNCSee the original announcement.

Coal

29

Coal

February 2015

Platts to Publish CME Group Open Interest for CoalEffective June 26, 2015, Platts will publish the open interest for the front-month CAPP barge, CAPP rail (CSX), PRB 8,800 Btu/lb coal futures contracts as listed by the CME Group, as well as the total CME open interest for each contract and all terms, in the daily OTC Broker Index table in Platts Coal Trader.

The open interest data will lag by one day due to the fact it becomes available each day after Coal Trader’s daily publishing deadline.See the original announcement.

ZEMA regularly collects nearly 150 data reports on coal. For more information, visit http://www.ze.com/the-zema-solutions/.

Platts and Fenwei to Launch CMCI Met Coal Assessment SeriesEffective early April 2015, Platts and Shanxi Fenwei Energy Consulting Co. are proposing to launch the China Metallurgical Coal Index price assessment series, which will initially include five spot metallurgical coal assessments in the domestic Chinese spot market.

The proposed assessments are designed to reflect the daily tradable values of a range of coal specifications in the Chinese domestic spot market. Provisionally, the assessments would include two premium hard coking coal assessments (Liulin No. 4 and Liulin No. 9), a high-vol high-fluidity assessment (North China Fat Coal), a PCI coal assessment (Shanxi PCI), and a semi-soft coking coal assessment (Shandong Semi Soft).

The assessments will be assessed in yuan per metric ton on an ex-washplant, free on rail, and when applicable on a delivered duty paid Tangshan basis.

Platts and Fenwei also propose to assess four domestic logistic routes, including both rail and truck freight from Shanxi to Tangshan and Shandong. Using these new assessments, it will be possible for Platts to analyze the relationship between domestic and seaborne metallurgical coal markets, and Platts may therefore consider the publication of an implied arbitrage calculation.See the original announcement.

30February 2015

CoalPlatts Publishes Front-Month, Front-Quarter Coal AveragesOn February 2, 2015, Platts announced that it will publish a daily average of the front-month and front-quarter price assessments for each of the five over-the-counter coal products it currently assesses in the OTC Broker Index table in Platts Coal Trader.

For example, on March 5 Platts would publish the average of the April daily assessments published from February 26 through March 5. On the same date, Platts would publish the average of the front-quarter (which will be the third calendar quarter) daily assessments published from February 26 to March 5.

The daily front-month and front-quarter averages will show the direction of the underlying prices through the course of the referenced period, providing market participants with more visibility as to the direction of the final monthly settle for both terms.See the original announcement.

ZEMA collects more than 20 different coal records from Platts alone. For a complimentary demo on how ZEMA’s data coverage can be specialized for your company’s needs, visit http://www.ze.com/book-a-demo/.

Argus Discontinues New York BTU Value Coal AssessmentAs of February 18, 2015, Argus has stopped the following code in the Argus US Products publication and data module. For FTP subscribers, these changes apply to data in the dhp .csv files in the DUSPR folder on ftp.argusmedia.com.

PA-codeTime Stamp

Price Type

Continuous Forward

Description Unit Category Frequency

PA0002205 2 8 0Coal New York BTU value (USP)

USD/mnBtu

->Spark spread->North America->New York

Daily

See the original announcement.

Platts to Discontinue Compliance Coal SpreadEffective June 26, 2015, Platts will discontinue listing the CAPP 1% vs. compliance coal spread currently listed in the daily OTC Broker Index table in Platts Coal Trader.

Due to evolving market conditions, there is no longer a premium for low sulfur Central Appalachia thermal coal, as the spread was envisioned to illustrate. Over-the-counter trades for compliance coal have not been reported since February 2012, when the spread last showed a change. The affected code is CTMM001.

Additionally, Platts proposes to stop publishing the second trailing final monthly average for the over-the-counter coal products and the CAPP 1% vs. Compliance Spread listed in the daily OTC Broker Index table in Coal Trader, effective June 26. Platts would like to add in its place content it believes would be more relevant to market participants.See the original announcement.

Softs and Metals

31

Softs and Metals

Platts to Launch Expanded Sugar Futures AssessmentsEffective March 30, 2015, Platts will publish an expanded range of daily assessments for ICE White Sugar Futures (LIFFE 5) and Sugar No. 11 Futures at 16:30 London time.

The new range of assessments will include the first three contracts listed by the exchange for each futures’ contract from the date of publication. This builds upon Platts’ existing front-month contract assessments for both ICE Sugar No. 11 and White Sugar Futures.

Platts would maintain a rolling schedule in line with the ICE expiration schedules for each futures contract. These assessments will appear in a range of Platts sugar reports, and in the

Platts price database. The new symbol codes will be announced at a later date.See the original announcement.

Platts to Decouple Two T2 German Ethanol AssessmentsEffective March 9, 2015, Platts FOB Rotterdam T2 German spec ethanol assessments will include a minimum greenhouse gas saving of 50% when compared with the fossil fuel comparator, as per the European Union’s Fuel Quality Directive calculation.

The fossil fuel comparator and greenhouse gas saving reflected will be per the prevailing implementation of the Fuel Quality Directive in Germany. Currently, the existing FOB Rotterdam T2 German spec assessment is published as fixed at parity to the FOB Rotterdam T2 assessment. Effective March 9, Platts will decouple the existing relationship between the two assessments and establish two independent assessments.

Platts will monitor the activity and development of both markets and continue to review trading activity and assessments for abnormal trading indications. Platts will continue to monitor this activity in light of the change to German domestic biofuel specifications and adapt its methodology as necessary to reflect standard spot market trade flows.

No changes will be made to the Platts FOB Rotterdam T2 assessments. All other specifications will conform with the prevailing renewable energy Directive 2009/28/EC.See the original announcement.

ZEMA’s vast data coverage comprises records on many kinds of agricultural products, including ethanol. To learn more, visit http://www.ze.com/the-zema-solutions/data-coverage/.

SOFTS

February 2015

Softs and Metals

32

Softs and Metals

CME Launches Short-Dated Crop Soybean Meal and Soybean Oil OptionsOn February 22, 2015, the following short-dated crop options were listed for trading on CME Globex, open outcry and clearing submission via CME ClearPort:

Short-Dated New Crop Soybean Meal and Soybean Oil Options

ProductFIX/FAST and iLink: tag 1151-Security Group MDP 3.0: tag 6937-Asset

FIX/FAST and iLink: tag 55-Symbol MDP 3.0 tag 1151 - Security Group (Outrights)

FIX/FAST and iLink: tag 55-Symbol MDP 3.0 tag 1151 - Security Group (UDS)

Short-Dated Options on New Crop Soybean Meal Futures

OMD ML MY

Short-Dated Options on New Crop Soybean Oil Futures

OLD 0O OZ

See the original announcement.

ZEMA can help you keep you up to date on more than 100 regular CME reports, including many on softs. To find out how, book a free demo at http://www.ze.com/book-a-demo/.

February 2015

Softs and Metals

33February 2015

Softs and MetalsCME Europe Lists Fertilizer Cash Settled Futures

On February 2, 2015, CME Europe listed the following fertilizer cash settled futures for trading on CME Globex and clearing submission via CME ClearPort:

ProductFIX/FAST and iLink: tag 1151-Security Group MDP 3.0: tag 6937-Asset

FIX/FAST and iLink: tag 55-Symbol MDP 3.0 tag 1151 - Security Group

Urea (Granular) FOB US Gulf Future FNE FE

UAN FOB NOLA Future FUE FE

DAP FOB NOLA Future FLE FE

DAP FOB Tampa Future FTA FE

Urea (Granular) FOB Egypt Future FEY FE

Urea (Prilled Bulk) FOB Yuzhny Future FKE FE

Urea (Granular) FOB Middle East Future FME FE

Urea (Prilled) FOB China Future FCE FE

These contracts are listed on, and subject to, the rules of UK RIE CME Europe Ltd.See the original announcement.

New MGEX Calendar Spread Options Launched on CME GlobexEffective February 1, 2015, the following options on MGEX futures calendar spreads (CSOs) were listed for trading on CME Globex:

• One consecutive CSO (March 2015 - May 2015)• Two Annual CSOs (September 2015 - September 2016 and December 2015 -

December 2016)• Three non-Consecutive CSOs (March 2015 - July 2015, March 2015 - September 2015,

March 2015 - December 2015)

Upon March expiration, the May Non-Consecutive months will be listed for trading and so on.See the original announcement.

ZEMA collects a wide range of agricultural data, including several reports from MGEX. To learn more about ZEMA’s data coverage, visit http://www.ze.com/the-zema-solutions/data-coverage/.

Softs and Metals

34

Softs and Metals

Marex Spectron Launches Physical Sugar BrokingOn January 5, 2015, Marex Spectron launched a new service providing access to markets for physical sugar. The new service will be offered in conjunction with MB Trading, which will act as agent for Marex Spectron. This is Marex Spectron’s first brokerage service in physical agricultural products.

The new physical broking service is now live and will operate primarily through desks in London and Paris.See the original announcement.

ZEMA currently collects 11 regular data reports on sugar alone. Learn more about ZEMA’s extensive data coverage at http://www.ze.com/the-zema-solutions/data-coverage/.

DCE Lists New Soybean, Corn, Palm Olein, Fiberboard, Blockboard, and Corn Starch ContractsEffective January 19, 2015, the Dalian Commodity Exchange (DCE) has begun trading the following contracts:

• No. 1 Soybeans 1607 Contract• No. 2 Soybeans 1601 Contract, Corn 1601 Contract• Soybean Meal 1601 Contract• Soybean Oil 1601 Contract, LLDPE 1601 Contract• RBD Palm Olein 1601 Contract, Egg 1601 Contract• Egg 1601 Contract• Fiberboard 1601 Contract• Blockboard 1601 Contract• Corn Starch 1601 Contract

See the original announcement.

The ZEMA graph below shows the future contract for corn and soybean in next three years from March 2015 to November 2017 (CME data). The graph displays monthly prices for corn and soybean, which is now trading at the Dalian Commodity Exchange. For the period 2015-2017, we can see upward trend for future contracts of corn, whereas soybean contracts have high volatility in the same period. Analysis like moving average (represented by a line without points for corn and soybean in the graph) helps to remove noise from the random price fluctuations. Easily customizable graphs like this can be built in ZEMA to create simple or complex analyses and make better decisions. To learn more, book a complimentary ZEMA demonstration.

February 2015

Softs and Metals

35February 2015

Softs and Metals

Euronext Extends Milling Wheat Contract to Johannesburg Stock ExchangeOn February 16, 2015, Euronext signed a license agreement with the Johannesburg Stock Exchange (JSE) providing the JSE with the right to list the flagship Milling Wheat contract currently traded on Euronext. The aim of the agreement is to extend access to the global benchmark Milling Wheat contract by broadening its international exposure to a wider audience.

By partnering with the largest exchange in the region, the agreement also extends Euronext’s reach into Africa, which according to International Monetary Fund forecasts, will be the world’s second fastest-growing region next year, expanding 5.75%.

The license agreement signed between the two exchanges is reciprocal, enabling each exchange the right to use the settlement prices and brands for the other’s commodities contracts. JSE will initially list the Euronext Milling Wheat contract, and this agreement can be extended to include its contracts for Rapeseed and Corn.See the original announcement.

© Graph created with ZEMA

36February 2015

Softs and Metals

METALSPlatts to Publish Iron Ore Phosphorus DifferentialEffective April 1, 2015, Platts will begin publishing a daily phosphorus differential used in the normalization process for its iron ore fines assessments. This differential will be reflective of ores within the 60-63.5%-Fe range, in line with the current “per 1% Fe differential.” The differential will be monitored and updated to reflect spot market value.

This differential adjustment used in normalization will be expressed in dollars per dry metric ton for every 0.01 percentage point of phosphorus, up to and including levels of 0.12%. Platts will continue to monitor penalties and premiums for phosphorus above this level and outside of the Fe range and continue to publish this information on a case-by-case basis in market commentaries and news stories.

Platts is proposing to publish this value in the daily iron ore assessment table in SBB Steel Markets Daily on page 3 and on page MW1105 of PMA and to database the value, making it available in data products under the category SI.See the original announcement.

ZEMA collects more than 90 metals records from Platts alone. To gain a wider perspective on the metals market and find out how the ZEMA solution can enhance your company’s business processes, visit http://www.ze.com/the-zema-solutions/.

Argus Launches Gadolinium Oxide AssessmentAs of March 3, 2015, Argus introduced a new Gadolinium oxide assessment to Argus Rare Earths report and associated data feed. The following data series is available in DRareEarths data module in /DRareEarths folder on ftp.argusmedia.com.

PA-code Time Stamp

Price Type

Description Unit Category Frequency

PA0015714 0 1

Gadolinium oxide min 99.999% fob China

USD/t ->Metals - Non-ferrous-> Rare Earths->Asia-Pacific

Daily

PA0015714 0 2

Gadolinium oxide min 99.999% fob China

USD/t ->Metals - Non-ferrous-> Rare Earths->Asia-Pacific

Daily

See the original announcement.

ZEMA Collects more than 25 metals data reports from the Asia region alone. To find out more, book a free demo at http://www.ze.com/book-a-demo/.

37February 2015

Softs and Metals

NYMEX Lists Gold Kilo Futures for Hong Kong DeliveriesEffective January 26, 2015, the New York Mercantile Exchange (NYMEX) listed gold kilo futures to be physically delivered in Hong Kong. The first listed contract month shall be the April 2015 contract. The spot month limit shall be effective at the close of trading on the business day prior to the first day of the delivery month. For example, the spot month limit for the April 2015 contract month shall be effective at the close of trading on March 31, 2015.

Contract Name

Rule Chapter

Commodity Code

Contract Size and Unit

Reporting Level

Spot-Month Limit (In Net Futures Equivalents)

Single Month Account-ability Level

All Month Account- ability Level

Gold Kilo Futures

114 GCK 1 Kilogram Bar

25 6,000 6,000 6,000

The commodity codes are provided for clearing members that file reports pursuant to NYMEX Rule 561.A in a machine-readable format.See the original announcement.

The ZEMA graph below shows average monthly gold prices in years 2012, 2013, and 2014 (LBMA data). The graph clearly demonstrates that the prices have significantly dropped in June 2013 and remained at the low level ever since. Gold prices soared as high as $1,746 USD/toz in October of 2012 and fell as low as $1175 USD/toz in November 2014. NYMEX hopes to complement the existing gold benchmark with its new gold futures contract for the Hong Kong physical gold market. To learn more about the ZEMA solution, book a complimentary demonstration.

© Graph created with ZEMA

38February 2015

Softs and Metals

ICE to Administer the LBMA Gold PriceEffective March 2015, Intercontinental Exchange (ICE) and the London Bullion Market Association (LBMA) have launched the new LBMA Gold Price, which replaces the long established London Gold Fix.

As announced by the LBMA in November 2014, ICE Benchmark Administration (IBA) has officially become the administrator of the new pricing mechanism. As the administrator for the LBMA Gold Price, IBA will transition to a physically settled, electronic and tradable auction, with the ability to participate in three currencies: USD, EUR, and GBP.

Within the process, aggregated gold bids and offers will be updated in real-time with the imbalance calculated and the price updated every 30 seconds. IBA will use ICE’s widely distributed front-end, WebICE, as the technology platform which will allow direct participants, as well as sponsored clients, to manage their orders in the auction in real time via their desktops.See the original announcement.

ZEMA collects more than 200 metals records, several of which regard gold prices. To receive a complimentary ZEMA demonstration, visit http://www.ze.com/book-a-demo/.

Platts Discontinues Platts Tubular Market Data FileEffective January 1, 2015, Platts has discontinued its monthly North American pipe and tube markets data publication, Platts Tubular Market Report data file.

The publication has been discontinued due to the reconfiguration of other Platts publications and data reports that provides subscribers with similar information going forward.

As an alternative, subscribers can receive pipe and tube market data in the Platts Steel Data & Analysis product. Specifically, this data is included in the Imports 1-4 and Exports 1-3 reports.

In addition, pipe and tube data is included in the trend analyzer, also part of a Steel Data & Analysis subscription.See the original announcement.

39February 2015

Softs and Metals

CME Changes FIX Tags for Metals FuturesOn February 23, 2015, CME Group changed the values in the following FIX tags for Metals futures:

• tag 55-Symbol for FIX/FAST, and

• tag 1151-SecurityGroup for MDP 3.0

Product

Product CodeFIX/FAST and iLink: tag 1151- Security Group MDP 3.0: tag 6937-Asset

Current State FIX/FAST and iLink: tag 55-Symbol MDP 3.0 tag 1151 - Security Group

New State FIX/FAST and iLink: tag 55-Symbol MDP 3.0 tag 1151 - Security Group

E-micro Gold futures and calendar spreads

MGC QO GC

miNY Gold futures and calendar spreads

QO QO GC

E-mini Copper futures and calendar spreads

QC QC HG

miNY Silver futures and calendar spreads

QI QI SI

See the original announcement.

LME Extends Publication of Live Forward Price CurvesOn January 20, 2015, The London Metal Exchange (LME) has extended its live forward price curves for each metal as part of its commitment to further enhance the transparency of the price discovery process following last year’s review of the Ring, the Exchange’s open outcry trading platform.

The forward price curves, which were previously published for the Ring’s afternoon “kerb” trading session only, now cover all trading times in the Ring.

In addition to the new price information, the LME is providing extra granularity by publishing monthly prompt dates between three months and one year forward.See the original announcement.

Finance

40

Finance

February 2015

CME Introduces Ratio Calendar Spread for Treasury Bond FuturesOn February 17, 2015, due to unique changes in the deliverable basket affecting the upcoming March-June Treasury Bond (ZB) calendar roll, the Chicago Mercantile Exchange (CME) listed a new reduced-tick ratio calendar spread for trading on CME Globex.

This spread is a reduced tick calendar spread with the usual quarter-32nd tick, but with a leg ratio of 3:2. The details of the spread are included in the Security Definition message as defined below.

Product

FIX/FAST and iLink: tag 1151-Security Group MDP 3.0: tag 6937-Asset

FIX/FAST and iLink: tag 55-Symbol MDP 3.0 tag 1151 - Security Group

Tag 762-Security-SubType

Tag 623- LeqRatioQty

Treasury Bond Reduced-Tick Ratio Calendar Spread

ZBXH5-ZBXM5 ZB RTFront Leg: 3 Back Leg: 2

This spread will not be implied and will not be SLEDS eligible.

The ratio spread is listed alongside the current reduced tick calendar spread. Trade leg assignment and spread pricing differences are outlined in the following scenarios:

• ZBH5 is priced at 150.0 (1500)• ZBM5 is priced at 165.0 (1650)• The Reduced Tick calendar spread ZBH5-ZBM5 trades at -15.0 (-1500) • Front leg – deferred leg • (150.0 – 165.0) = -15.0

Platts to Launch New USD-INR Forex AssessmentOn February 12, 2015, Platts announced that it will be introducing a daily US Dollar-Indian Rupee currency assessment to complement its global sugar pricing coverage.

The assessment would be made basis 16:30 Singapore time, and be used as part of calculations for third-party NCDEX data for sugar prices in India. These assessments would add to Platts’ existing portfolio of currency assessments published to support a range of Platts physical commodity assessments.See the original announcement.

Also on February 12, Platts declared its intent to launch a daily US Dollar-Mexican Peso currency assessment to complement its global sugar pricing coverage.

This assessment would be made basis 14:15 Houston time, and be used as part of calculations for third-party Zafranet data for sugar prices in Mexico.See the original announcement.

Finance

41

Finance• The Reduced-Tick Ratio calendar spread ZBXH5-ZBXM5) trades at 120.0 (120000) • (Front leg*3)-(deferred leg*2) • ((150.0*3)-(165.0*2)) = 120.0See the original announcement.

ZEMA’s sophisticated market data management tools collect hundreds of financial data reports, including reports from CME. To learn how you can begin building your own library of financial data, book a complimentary ZEMA demonstration at http://www.ze.com/book-a-demo/.

CME Globex Lists Second Generation Deliverable Interest Rate Swap FuturesEffective February 8, 2015, the Second-generation 10-Year and 30-Year USD Deliverable Rate Swap futures were listed for trading on CME Globex.

The second-generation 10-Year and 30-Year USD Deliverable Rate Swap futures will be listed for:

• March 2015 quarterly expiration, and

• A different coupon rate than the existing First-generation 10-Year USD Interest Rate Swap and 30-Year USD Interest Rate Swap

ProductFIX/FAST and iLink: tag 1151-Security Group MDP 3.0: tag 6937-Asset

FIX/FAST and iLink: tag 55-Symbol MDP 3.0 tag 1151 - Security Group

Second-generation 30-Year USD Deliverable Rate Swap Futures

B2U ZY

Second-generation 10-Year USD Deliverable Rate Swap Futures

N2U ZN

These contracts were listed with, and subject to, the rules and regulations of CBOT.See the original announcement.

CME Europe Lists Euro and US Dollar Denominated Deliverable Swap FuturesOn January 26, 2015, CME Europe announced that it will list the following Euro and US Dollar Denominated Deliverable swap futures for trading on CME Globex and clearing submission via CME ClearPort for CME Clearing Europe (CMECE), in Q1 2015.

ProductFIX/FAST and iLink: tag 1151-Security Group MDP 3.0: tag 6937-Asset

FIX/FAST and iLink: tag 55-Symbol MDP 3.0 tag 1151 - Security Group

2-Year Deliverable Euro Interest Rate Swap Futures EU2 DS5-Year Deliverable Euro Interest Rate Swap Futures EU5 DS10-Year Deliverable Euro Interest Rate Swap Futures E10 DS2-Year Deliverable US Dollar Interest Rate Swap Futures

DS2 DS

February 2015

Finance

42

ProductFIX/FAST and iLink: tag 1151-Security Group MDP 3.0: tag 6937-Asset

FIX/FAST and iLink: tag 55-Symbol MDP 3.0 tag 1151 - Security Group

5-Year Deliverable US Dollar Interest Rate Swap Futures

DS5 DS

10-Year Deliverable US Dollar Interest Rate Swap Futures

D10 DS

30-Year Deliverable US Dollar Interest Rate Swap Futures

D30 DS