Embed Size (px)

Citation preview

3/1/2017

1

FUNDAMENTAL U.S. TAX CONCEPTS IN INTERNATIONAL TAX

AND ESTATE PLANNING

Richard Andersen, Esq.

Wilmer Cutler Pickering Hale & Dorr LLP

M. Katharine Davidson, Esq.

Henderson, Caverly, Pum & Charney LLP

NYSBA/STEP

13th Annual International Estate Planning Institute

March 23, 2017

1

Agenda

• Basic Concepts and Definitions

• The Federal Wealth Transfer Taxes

• The Federal Income Tax

• State and Local Taxes

2

3/1/2017

2

Basic Concepts and Definitions

• “Taxpayer”

• Which of these is a “taxpayer”?

• A domestic corporation with exclusively U.S. shareholders, managed and operating only here and having only U.S.-situs assets and U.S. source income

• A U.S.-organized partnership

• A foreign grantor trust

• The Government of North Korea

• A foreign corporation with no U.S. shareholders, management, employees, income or assets

3

Which of These is a “Taxpayer”?

• A domestic corporation with exclusively U.S. shareholders, managed and operating only here and having only U.S.-situs assets and U.S. source income … yes

• A U.S.-organized partnership

• A foreign grantor trust

• The Government of North Korea

• A foreign corporation with no U.S. shareholders, management, employees, income or assets

4

3/1/2017

3

Which of These is a “Taxpayer”?

• A domestic corporation with exclusively U.S. shareholders, managed and operating only here and having only U.S.-situs assets and U.S. source income … yes

• A U.S.-organized partnership… yes

• A foreign grantor trust

• The Government of North Korea

• A foreign corporation with no U.S. shareholders, management, employees, income or assets

5

Which of These is a “Taxpayer”?

• A domestic corporation with exclusively U.S. shareholders, managed and operating only here and having only U.S.-situs assets and U.S. source income … yes

• A U.S.-organized partnership… yes

• A foreign grantor trust… yes

• The Government of North Korea

• A foreign corporation with no U.S. shareholders, management, employees, income or assets

6

3/1/2017

4

Which of These is a “Taxpayer”?

• A domestic corporation with exclusively U.S. shareholders, managed and operating only here and having only U.S.-situs assets and U.S. source income … yes

• A U.S.-organized partnership… yes

• A foreign grantor trust… yes

• The Government of North Korea… yes

• A foreign corporation with no U.S. shareholders, management, employees, income or assets

7

Which of These is a “Taxpayer”?

• A domestic corporation with exclusively U.S. shareholders, managed and operating only here and having only U.S.-situs assets and U.S. source income … yes

• A U.S.-organized partnership… yes

• A foreign grantor trust… yes

• The Government of North Korea… yes

• A foreign corporation with no U.S. shareholders, management, employees, income or assets… yes

8

3/1/2017

5

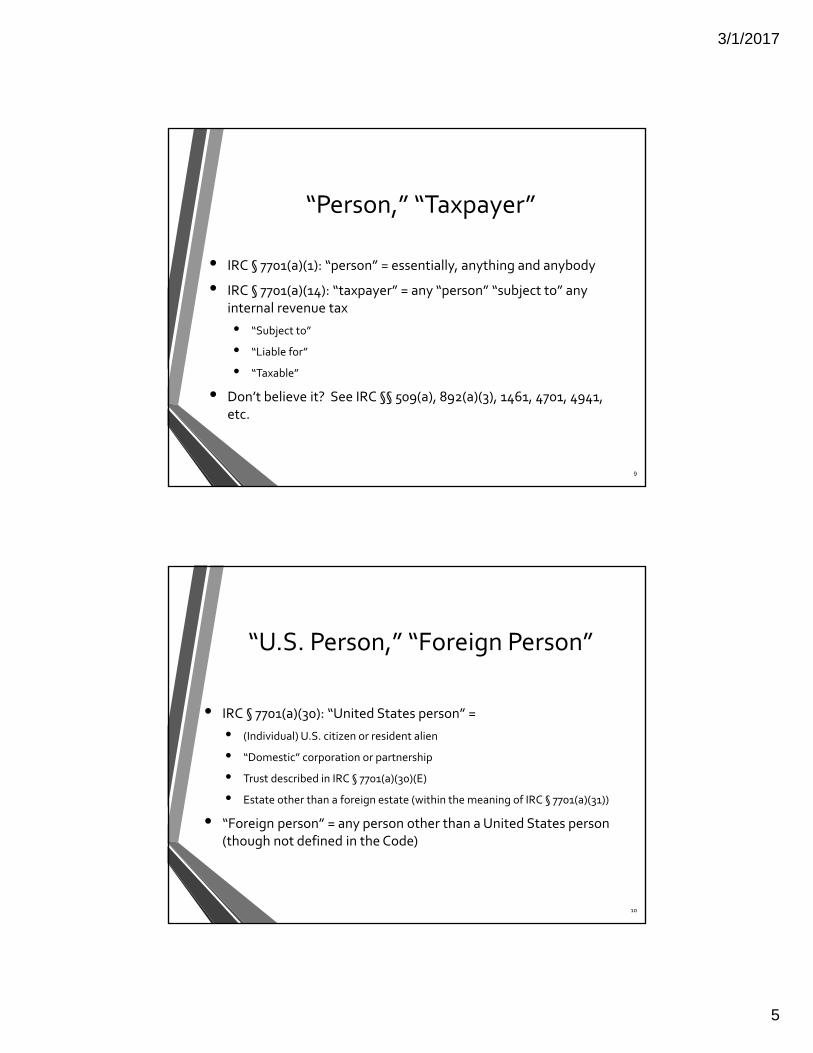

“Person,” “Taxpayer”

• IRC § 7701(a)(1): “person” = essentially, anything and anybody

• IRC § 7701(a)(14): “taxpayer” = any “person” “subject to” any internal revenue tax

• “Subject to”

• “Liable for”

• “Taxable”

• Don’t believe it? See IRC §§ 509(a), 892(a)(3), 1461, 4701, 4941, etc.

9

“U.S. Person,” “Foreign Person”

• IRC § 7701(a)(30): “United States person” =

• (Individual) U.S. citizen or resident alien

• “Domestic” corporation or partnership

• Trust described in IRC § 7701(a)(30)(E)

• Estate other than a foreign estate (within the meaning of IRC § 7701(a)(31))

• “Foreign person” = any person other than a United States person (though not defined in the Code)

10

3/1/2017

6

“U.S. Citizen”

• Determined under federal immigration law

• Several arcane special rules can reverse the normal principles in outlier situations (e.g., birth in the United States does not always confer citizenship)

• Dual citizens are full U.S. citizens for tax purposes

11

“Resident Alien”

• Individual who is not a U.S. citizen and who is not a “nonresident alien”

• The term “nonresident alien” has different meanings for the wealth transfer taxes, on the one hand, and the income tax on the other

• An individual may simultaneously be a resident alien for wealth transfer tax purposes and a nonresident alien for income tax purposes, or vice-versa

• Status may change from year to year

12

3/1/2017

7

Forms of Entity Under the Code

• Corporations

• Partnerships

• Limited liability companies

• Trusts

• Estates

• Outliers

13

“Domestic” Entity (1)

• Corporations, partnerships and limited liability companies are domestic if:

• they were incorporated in the United States or under the laws of any State, and have not redomiciled abroad;

• they are dual resident companies;

• they are “stapled” to a domestic entity; or

• they are successors to a domestic entity by way of inversion

• All others are foreign (locus of management, operations, etc. irrelevant)

14

3/1/2017

8

“Domestic” Entity (2)• Trusts are domestic if:

• A court within the U.S. is able to exercise primary supervision over the administration of the trust, and

• One or more U.S. persons have the authority to control all substantial decisions of the trust

• Estates are domestic unless:

• It is a foreign estate – i.e., an estate, the income of which, from sources without the U.S. which is not effectively connected with the conduct of a trade or business within the U.S., is not includible in gross income under Subtitle A of the Code (Income Taxes)

• Generally for income tax purposes – a foreign estate is that of a nonresident decedent

• All others are foreign15

The Federal Wealth Transfer Taxes• Transfer taxes include:

• Estate Tax

• Gift Tax

• Generation-Skipping Transfer Tax (GST Tax)

• Gifts and Bequests from Covered Expatriates (§2801)

• Basis of Federal Wealth Transfer Taxes:

• Citizenship

• U.S. citizens are taxable on gift, estate and GST transfers on a WORLDWIDE basis

• Residency

• Test for income tax purposes differs from that for transfer tax purposes

• Situs of Assets16

3/1/2017

9

Residency (Domicile)

• Estate, Gift and GST Taxation:• Relevance: Worldwide or Situs Taxation

• Domicile Defined: Acquired by living there, even briefly, with no definite or present intention of leaving U.S.

• Cf. “Residency” for U.S. Income Tax purposes

• How determined: Facts & Circumstances

• Time spent U.S. / abroad

• Size / location / use of homes

• Location of family, friends and contacts

17

Residency (Domicile) (cont’d.)

• Immigration Status

• Est. of Khan

• Rev. Rul. 80-209

• Rev. Rul. 80-263

• Est. of Jack

• A Subjective Test

18

3/1/2017

10

Residency (Domicile) (cont’d.)

• Estate and Gift Tax Treaties

• U.S./U.K. Treaty (Article 4 Fiscal Domicile)

• Available permanent home

• Center of vital interests

• Habitual abode

• Nationality

• Competent Authorities

19

Estate Tax Rules for NRAs

• U.S. Tax on U.S. Situs Assets• Real Property

• Tangible Personal Property located in the U.S.

• Certain Debt Obligations

• Stock in U.S. Corporations

• Certain Intangible Property with U.S. Connection

• Non-U.S. Situs Assets• Stock in Foreign Corporations

• Insurance proceeds on NRA’s life

• Portfolio Debt

• Demand deposits in U.S. Banks

20

3/1/2017

11

Gift Tax Rules for NRAs

• Limited Definition of U.S. Situs Assets

• U.S. Real Property

• Tangible Personal Property located in the U.S.

21

Transfers to Noncitizen Spouses

• Bequests to Noncitizen Spouse

• No Marital Deduction

• But QDOT exception

• Gifts to Noncitizen Spouse

• Annual Exclusion of $149,000 (for 2017)

22

3/1/2017

12

Transfers to Non-Citizen Spouses

• Qualified Domestic Trusts (QDOTs)

• All income to spouse for life

• Only spouse may receive principal distributions

• Taxable, but with hardship exception

• At least one Trustee must be U.S. citizen or domestic corporation

• Must have power to withhold tax on principal distributions

• QDOT election

• QDOT of $2 million or more has additional security requirements

23

Transfers to Non-Citizen Spouses (cont’d)

• Portability

• Generally permits surviving spouse to use most recent deceased spouse’s DSUEA to avoid loss of deceased spouse’s remaining exclusion amount

• Availability depends upon decedent spouse’s citizenship

• Portability election not available to NRA decedent’s estate

• Portability not available to NRA surviving spouse except to extent a treaty applies

• Special rules apply when property passes to a QDOT

24

3/1/2017

13

Transfer Taxes• U.S. Citizen and Domiciled

Aliens

• Estate, Gift and GST taxes

• On Worldwide Transfers

• Current Maximum Rate

• 40%

• Current Exclusion (2017)

• $5.49 million

• Non-Domiciled Aliens• Estate Tax: Only U.S. situs

assets:• $60,000 exemption

• Current maximum tax rate of 40%

• Gift Tax: Only U.S. situs tangible assets:

• Annual exclusion

• No unified credit;

• $149,000 exemption for gifts to non-U.S. citizen spouse

• GST tax generally avoided

25

IRC §2801: New Succession Tax

• Gifts and Bequests Received by U.S. Persons from Covered Expatriates• Tax is on the Recipient

• Taxed at maximum gift or estate tax rate

• Based on FMV in excess of Annual Exclusion Amount ($14,000 for 2017)

• No medical/educational expense exclusions

• No tax on qualifying transfers to spouses/charities

• Tax reduced by any foreign gift/estate taxes on property transfer

• Gifts to domestic or foreign trust electing to be treated as domestic trust immediately taxable

• Distribution from non-electing foreign trusts taxable

• No time limit

26

3/1/2017

14

IRC §2801: New Succession Tax(cont’d)

• Proposed Regulations issued September 2015

• Domestic trusts and electing foreign trusts treated as U.S. persons for purposes of tax

• Tax based on domicile of Expatriate

• Exception for marital deduction includes QDOT transfers to Expatriate

• Expatriate’s general power of appointment that is exercised, released or lapsed that benefits U.S. person is covered• Grant of general power of appointment over property not held in trust

is covered when power is irrevocable and exercisable

• New Form 708 to report the Section 2801 tax has yet to be finalized

27

The Federal Income Tax

• Individuals

• Entities

• Scope of the Tax Base

• U.S. persons

• Foreign persons

• Collection

• Reporting

28

3/1/2017

15

“Nonresident Alien”• Two exclusive statutory categories

• “Green Card” Test

• “Substantial Presence” Test

• General “3-year, 183-Day” Test

• Exempt Days

• “Closer Connection” Exception

• Effects of expatriation

• Effects of income tax treaties

• All other individuals are U.S. persons for federal income tax purposes

29

Foreign Entities

• Corporations

• Partnerships

• Limited liability companies

• Trusts

• Estates

30

3/1/2017

16

Source of Income• Situs of Payor

• Dividends, interest

• Situs of Payee

• Gains from sales of property (important exceptions)

• Situs of Activity

• Services income: place of performance

• Rents: situs of property

• Royalties: territory of use or of right to use

• Some gains from sales of property

• Other rules

31

Income Taxation – Individuals• U.S. Citizens and Residents

• Graduated rates upon the difference between world-wide gross income and allowable deductions

• Nonresident Aliens

• Graduated rates upon the difference between gross income deemed effectively connected to a U.S. trade or business (“ECI”) and allowable, allocable deductions

• Gross flat-rate (30%, subject to income tax treaty reduc-tions) tax on U.S.-source income that is not ECI

• Exemptions

• Effects of income tax treaties

32

3/1/2017

17

Income Taxation – Corporations• Domestic Corporations

• Broadly the same as individuals

• Major differences: losses, capital gains

• Foreign Corporations

• Broadly the same as nonresident aliens

• Major differences: branch profits tax, treaty relief

• Same rules for multi-member LLCs that can, and do, elect/default to non-corporate status

• Single-member LLCs that have non-corporate status are generally disregarded as entities disregarded from its equity owner

33

Income Taxation – Partnerships

• Domestic Partnerships

• Not taxable, but taxpayers; so income is computed at entity level and then passed through to partners

• Foreign Partnerships

• Broadly the same as for domestic partnerships

• Same rules for LLCs that do not (or cannot) elect/default to corporate status

34

3/1/2017

18

Income Taxation – Trusts

• Domestic Non-Grantor Trusts

• A non-grantor trust is a taxable entity: pays income tax at the trust level on any taxable income retained by the trust

• A distribution of income to a beneficiary passes the income to the beneficiary (much like other “pass-through entities”)

• Grantor Trusts

• A grantor trust is treated as “owned” by the grantor and the trust income is taxed directly to the grantors

• Foreign Grantor and Non-Grantor Trusts

35

Classification of Foreign Trusts• A trust is a Foreign Trust unless

• U.S. court has primary supervision over administration (Court Test); AND

• At least one U.S. person has authority to control all “substantial decisions” with no veto power by a non-U.S. person (Control Test)

• Court Test Safe Harbor• The trust instrument does not direct that the trust be administered outside the

U.S.,

• The trust is in fact administered exclusively in the U.S., and

• The trust is not subject to an “automatic migration” provision

• Substantial Decisions• Timing of distributions

• Determining amounts of distributions

• Adding/Removing/Replacing Trustees and Beneficiaries

• Investment decisions (unless U.S. person retains power to hire/fire the investment advisors)

36

3/1/2017

19

Foreign Trusts

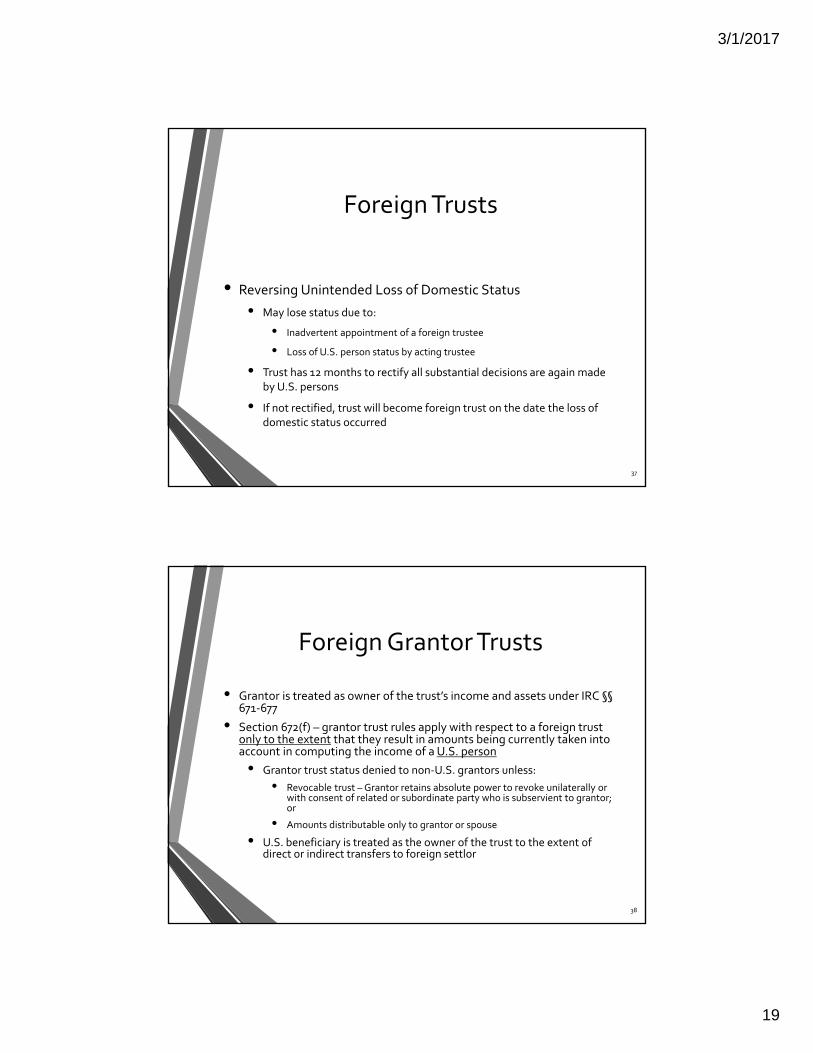

• Reversing Unintended Loss of Domestic Status

• May lose status due to:

• Inadvertent appointment of a foreign trustee

• Loss of U.S. person status by acting trustee

• Trust has 12 months to rectify all substantial decisions are again made by U.S. persons

• If not rectified, trust will become foreign trust on the date the loss of domestic status occurred

37

Foreign Grantor Trusts

• Grantor is treated as owner of the trust’s income and assets under IRC §§671-677

• Section 672(f) – grantor trust rules apply with respect to a foreign trust only to the extent that they result in amounts being currently taken into account in computing the income of a U.S. person• Grantor trust status denied to non-U.S. grantors unless:

• Revocable trust – Grantor retains absolute power to revoke unilaterally or with consent of related or subordinate party who is subservient to grantor; or

• Amounts distributable only to grantor or spouse

• U.S. beneficiary is treated as the owner of the trust to the extent of direct or indirect transfers to foreign settlor

38

3/1/2017

20

Foreign Nongrantor Trusts

• Taxation of U.S. Beneficiaries

• Distributions are taxable up to the trust’s DNI, which includes foreign source income and realized capital gain

• Generally, a distribution in excess of DNI is deemed to come from UNI and is subject to “throwback tax” resulting in:

• Accumulated capital gains are taxed as ordinary income

• A nondeductible interest charge is imposed on the throwback tax under a weighted average method

39

Foreign Trusts with U.S. Grantor• Section 679 – A trust is deemed to be a grantor trust when a U.S.

person transfers assets to a foreign trust with U.S. beneficiaries• Provisions are designed to find trust as having a U.S. beneficiary

• Considers amounts in trust for benefit of a U.S. person even if interest is contingent on a future event

• Any person with discretion to make a distribution from a foreign trust to or for the benefit of any person will cause trust to have a U.S. beneficiary unless a class is defined that does not include a U.S. person

• Any discretion of trustee or protector to distribute or accumulate income for U.S. person deemed to be exercised

• Any agreement or understanding that may result in payments or accumulations to a U.S. person will be considered a term of the trust

• Uncompensated use of trust property (through loan or other use of the trust property) directly or indirectly by a U.S. person will cause the trust to have a U.S. beneficiary

• Conclusive presumption that a foreign trust has a U.S. beneficiary if U.S. beneficiary transfers property (directly or indirectly) to the trust (rebuttable by transferor)

40

3/1/2017

21

Foreign Trusts with U.S. Grantor (cont’d.)

• Use of Trust Property as Distribution• The use of trust property by a U.S. grantor, U.S. beneficiary, or any

related U.S. person is treated as a distribution

• Distribution is for the Fair Market Value of the use of the property

• Does not apply to the extent the trust is paid fair market value “within a reasonable period of time” following the use

• “Within a reasonable period of time” has not been defined

• A subsequent return of the property to the foreign trust will be disregarded for tax purposes

41

Foreign Trusts with U.S. Grantor (cont’d.)

• Reporting Obligations for Foreign Trusts (Form 3520)

• Who has to file?

• U.S. person who creates a foreign trust

• U.S. person who transfers assets to a foreign trust

• U.S. beneficiary who receives a distribution from a foreign trust

• U.S. person treated as owner of a foreign trust

42

3/1/2017

22

Foreign Trusts with U.S. Grantor (cont’d.)

• Annual Reporting (Form 3520)

• Must be filed within 90 days of initial foreign trust formation

• Annual filing of Form 3520 generally due at same time as the person’s U.S. income tax return

• Foreign Trust Annual Reporting (Form 3520-A)

• The foreign trust reports a full and complete accounting of all annual trust activities, trust operations and other relevant information

• Due on 15th day of 3rd month after end of year (March 15 for calendar year foreign trusts)

43

Foreign Trusts with U.S. Grantor (cont’d.)

• Penalties for Failure to Timely File Complete Form 3520:

• Penalty equal to the greater of $10,000 or 35% of the gross reportable amount

• Increased by $10,000 for each 30-day period following notification from the IRS

• 90-day grace period before these additional $10,000 penalties is imposed

• Total penalty assessed may not exceed the gross reportable amount

• Penalties for Failure to Timely File Complete Form 3520-A

• Subject to 5% penalty of gross reportable amount

44

3/1/2017

23

Retention of Nonresident and Non-Domiciliary Status

• Life Insurance

• Mortgage on Real Property

• Foreign Holding Structures

• Partnerships/LLCs

• Residency in Estate/Inheritance/Gift Tax Favorable Jurisdiction

45

Income Taxation – Estates

• Domestic Estates

• An estate is a taxable entity: pays income tax at the estate level on any taxable income retained by the trust

• A distribution of income to a beneficiary passes the income to the beneficiary (much like other “pass-through entities”)

• Foreign Estates

• Generally subject to the income tax rules applicable to NRAs; rules for foreign trusts do not apply

• Only taxable on U.S. source income and ECI

• Payments of FDAP subject to 30% withholding absent treaty benefits

46

3/1/2017

24

Income Taxation – Estates (cont’d)

• Taxation of U.S. Beneficiaries of Foreign Estates

• Taxed on all current income distributions, but amount included in gross income is limited to beneficiary’s share of DNI

• Distributions of foreign source income from foreign estate with UNI are not subject to throwback or accumulation trust rules

• DNI computed in generally the same manner as for a domestic estate, with some exclusions, deductions and exemptions disallowed

• Taxation of Foreign Beneficiaries of a U.S. Estate

• NRA taxed on ECI, FDAP and capital gains on sale or exchange of USRPI

• Tax characterization of distribution carries over to foreign beneficiary

47

State and Local Taxation

• In General

• Inheritance and Gift Taxes

• Income Taxes

48

3/1/2017

25

States with Transfer Taxes

• Fourteen States (Plus District of Columbia) with Estate Tax: • WA, OR, HI, MN, IL, NY, DC, DE, CT, RI, MA, VT, ME, MD*, NJ*

• Six States with Inheritance Tax:• NE, IA, KY, PA, MD*, NJ*

• One State with Gift Tax:• Connecticut

* Maryland and New Jersey have both an Estate Tax and an Inheritance Tax

49

![CT [1642 ed.] t1b - 08 - Tract. De Creatione](https://img.pdfslide.us/doc/110x75/546a6445af795953298b46a1/ct-1642-ed-t1b-08-tract-de-creatione.jpg)

![CT [1642 ed.] t1b - 02 - Q 28, De Relationibus Divinis](https://img.pdfslide.us/doc/110x75/546a6438b4af9f7f2c8b467f/ct-1642-ed-t1b-02-q-28-de-relationibus-divinis.jpg)