Embed Size (px)

Citation preview

Cyprus– An International & Professional Centre

“Cyprus: The Ideal Holding Company Location

Advantages of the Cyprus Tax system”

Kikis Treppides

Managing Director

K. Treppides & Co Ltd

Lithuania, June 2012

2

Cyprus – Facts and Figures

• Member of the European Union since 1 May 2004

• Euro Currency was introduced in Cyprus on 1 January 2008

3

Cyprus Tax Reform

• To conform with European Law and the Acquis Communautaire on Direct and Indirect Taxation

• To comply with the Code of Conduct on Business Taxation and OECD requirements against harmful tax practices.

• To simplify, make more transparent and more effective the whole tax system

4

What is the purpose of an international tax structure?

MAXIMUM

AFTER-TAX RETURN

5

So, what you need is a jurisdiction with …

• Low tax environment for– International holding companies– International trading operations– Cross-border transactions and distributions

• Political, legal and tax systems that are– Stable– Reputable– Sophisticated and experienced

• Supportive Infrastructure– Good communications– Developed business services– Developed professional services

6

Key features of the Cyprus tax system

• The lowest effective tax rate in the European Union

• 10% headline corporate tax rate• Foreign source income generally tax exempt

• Profits on transactions in shares tax-exempt• Generous tax deductibility rules reduces effective

tax rate

7

Key features of the Cyprus tax system

• No withholding taxes on outbound dividends, interest & royalties, irrespective of the country of destination i.e.

• Tax free exit

• EU tax directives apply• Parent / Subsidiary• Interest & Royalties• Re-organisations

• Unilateral credit relief for foreign taxes

8

Key features of the Cyprus tax system

• No CFC (Controlled Foreign Corporation) legislation

• No thin capitalisation rules

• No detailed transfer pricing rules (arm’s length principle only)

• No capital gains tax (except on real estate situated in Cyprus)

• No taxes on entry, reorganizations and exits

9

• No wealth taxes and only minimal stamp & local taxes

• No exchange controls• Most international transactions free of VAT• Low personal tax regime - Top rate 35%

(For foreign staff becoming tax residents of Cyprus as of 01.01.2012 with income over €100.000 maximum tax rate of 17.5%)

• OECD approved / EU compliant system

Key features of the Cyprus tax system

10

• A tax administration that wants to help foreign investors

• Wide network of favorable tax treaties

• OECD approved / EU compliant system

• A tax administration that wants to help foreign investors

• Wide network of favorable tax treaties

Key features of the Cyprus tax system

11

Cyprus Tax Philosophy

The Cyprus Tax System is based:

• On the Tax Residency of the Individual and / or Company.

• The Management and Control of the Company

12

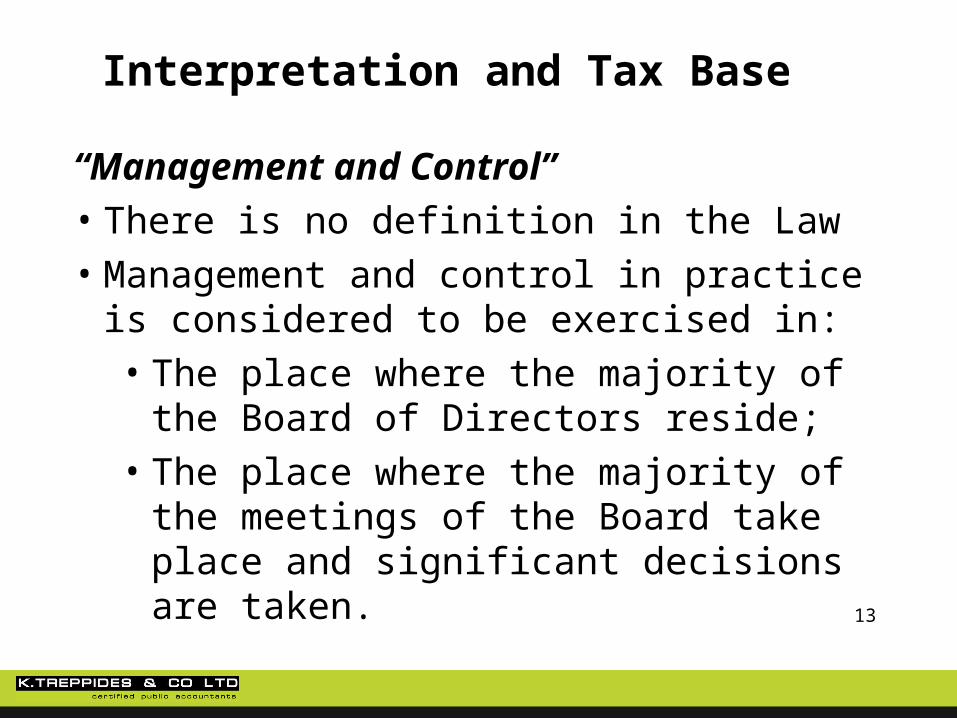

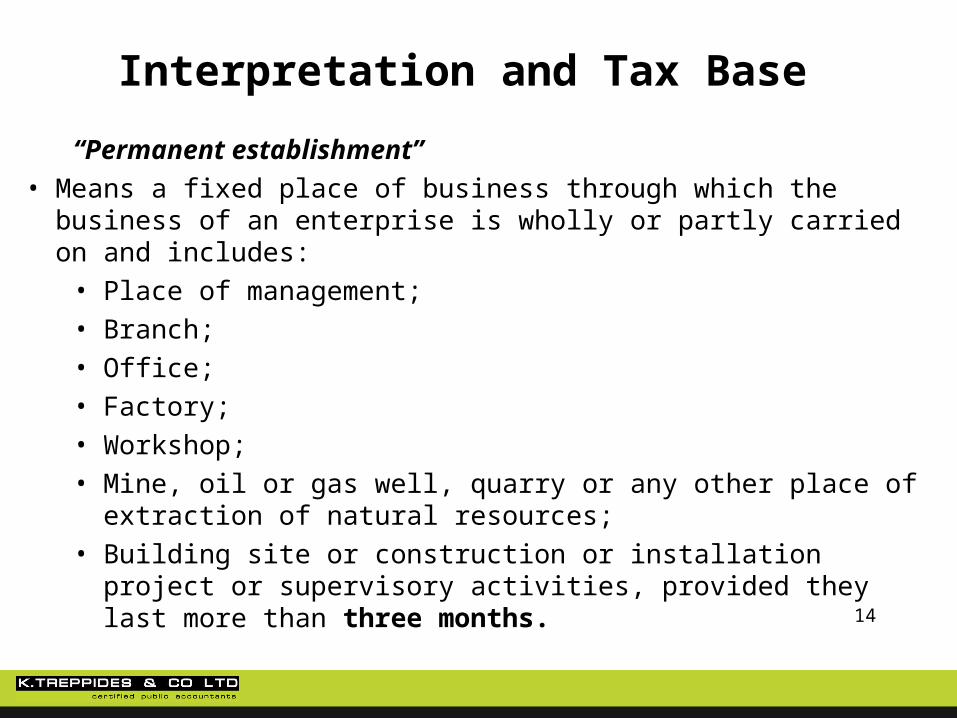

Interpretation and Tax Base

“Resident in the Republic”

• When applied to an individual, means an individual who is present in Cyprus for a period or periods > 183 days in the year of assessment.

• When applied to a company, means a company whose management and control is exercised in Cyprus.

13

“Management and Control”• There is no definition in the Law• Management and control in practice is

considered to be exercised in:• The place where the majority of the Board of

Directors reside;• The place where the majority of the meetings

of the Board take place and significant decisions are taken.

Interpretation and Tax Base

14

“Permanent establishment”• Means a fixed place of business through which the business of an

enterprise is wholly or partly carried on and includes:• Place of management;• Branch;• Office;• Factory;• Workshop;• Mine, oil or gas well, quarry or any other place of extraction of natural

resources;• Building site or construction or installation project or supervisory

activities, provided they last more than three months.

Interpretation and Tax Base

15

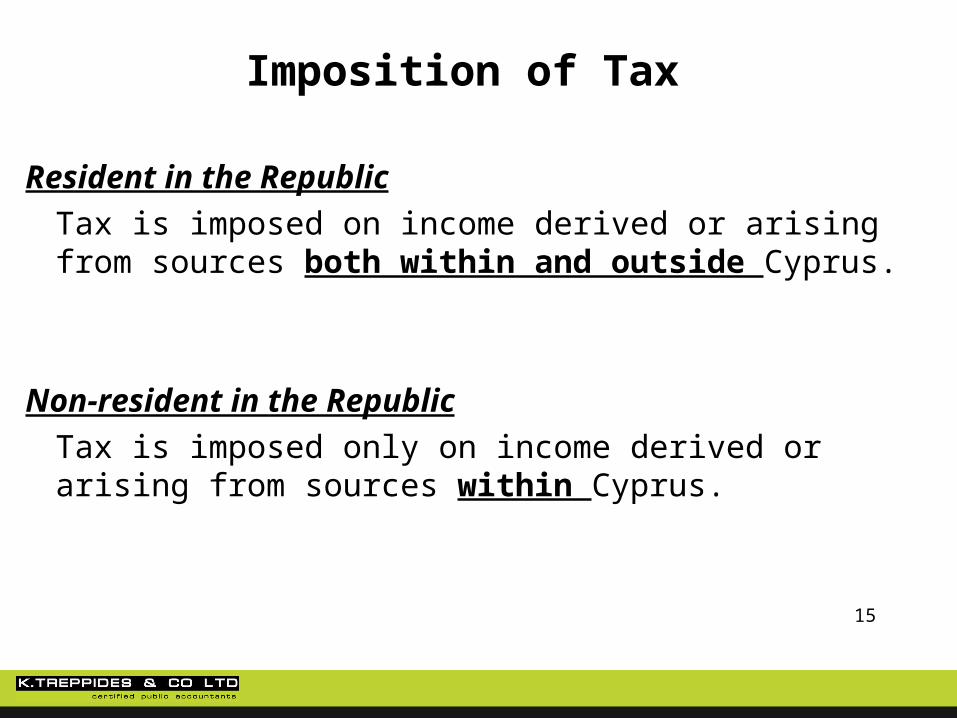

Imposition of Tax

Resident in the Republic

Tax is imposed on income derived or arising from sources both within and outside Cyprus.

Non-resident in the Republic

Tax is imposed only on income derived or arising from sources within Cyprus.

16

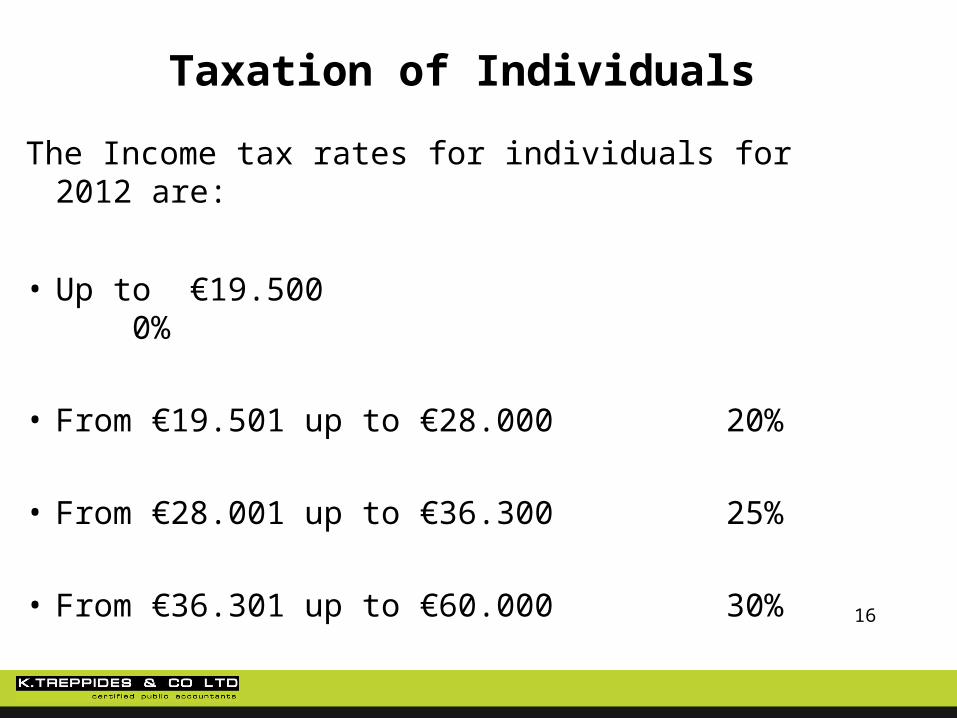

Taxation of Individuals

The Income tax rates for individuals for 2012 are:

• Up to €19.500 0%

• From €19.501 up to €28.000 20%

• From €28.001 up to €36.300 25%

• From €36.301 up to €60.000 30%

• Above €60.000 35%

17

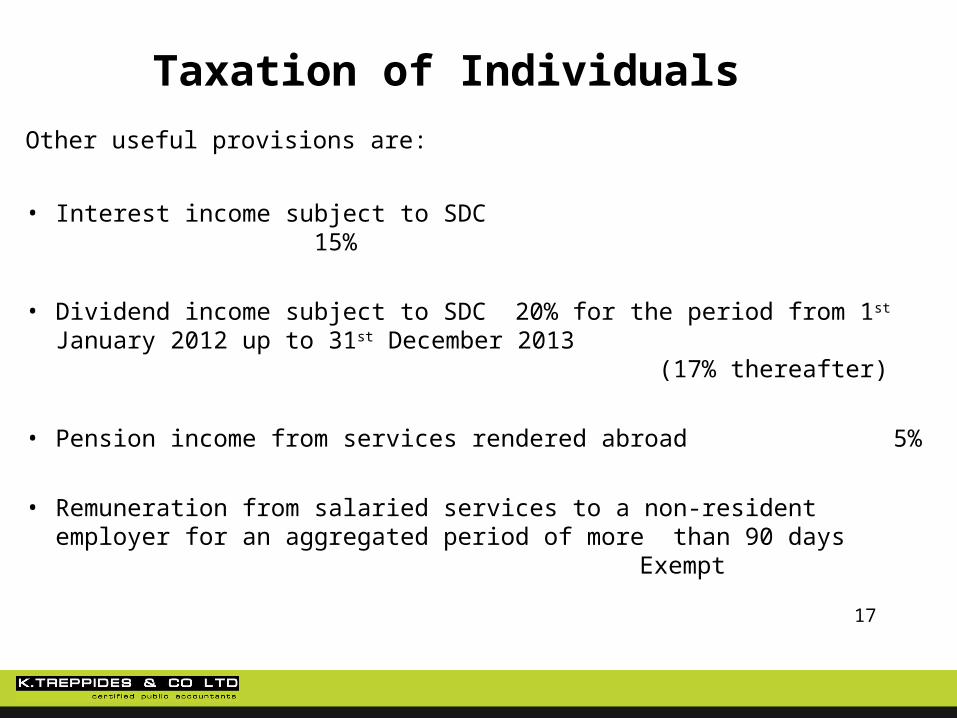

Other useful provisions are:

• Interest income subject to SDC 15%

• Dividend income subject to SDC 20% for the period from 1st January 2012 up to 31st December 2013 (17% thereafter)

• Pension income from services rendered abroad 5%

• Remuneration from salaried services to a non-resident employer for an aggregated period of more than 90 days Exempt

Taxation of Individuals

18

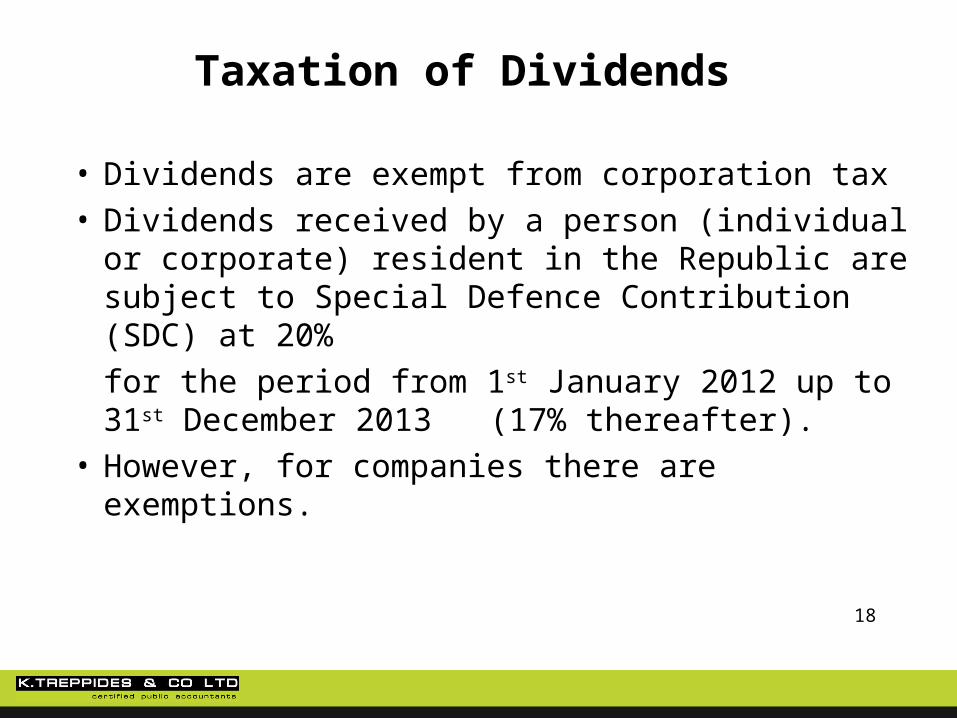

Taxation of Dividends

• Dividends are exempt from corporation tax• Dividends received by a person (individual or corporate)

resident in the Republic are subject to Special Defence Contribution (SDC) at 20%

for the period from 1st January 2012 up to 31st December 2013 (17% thereafter).

• However, for companies there are exemptions.

19

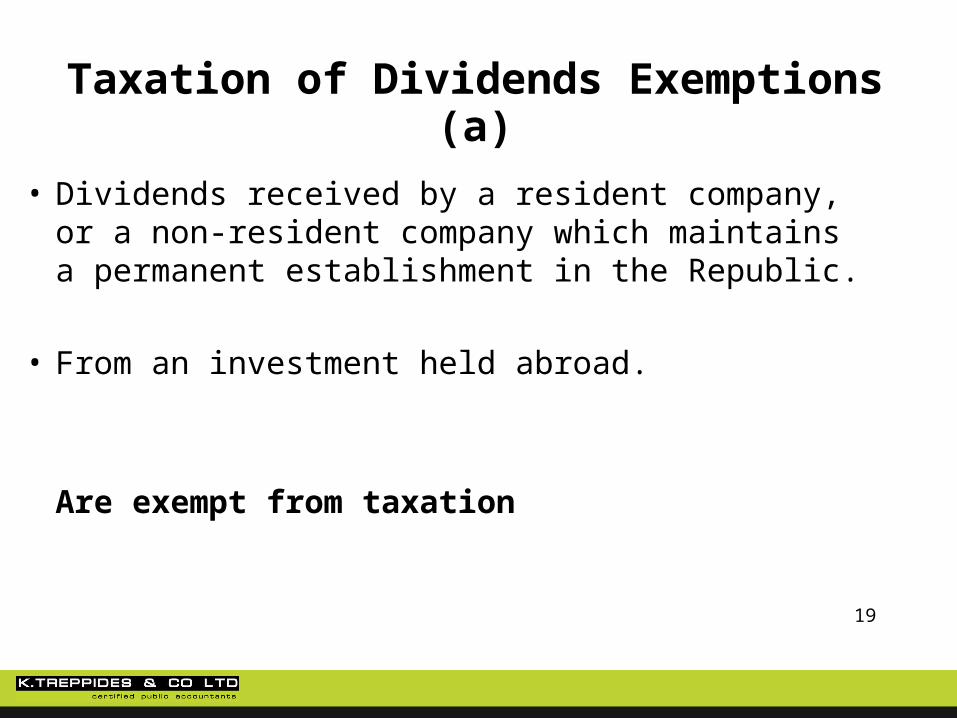

• Dividends received by a resident company, or a non-resident company which maintains a permanent establishment in the Republic.

• From an investment held abroad.

Are exempt from taxation

Taxation of Dividends Exemptions (a)

20

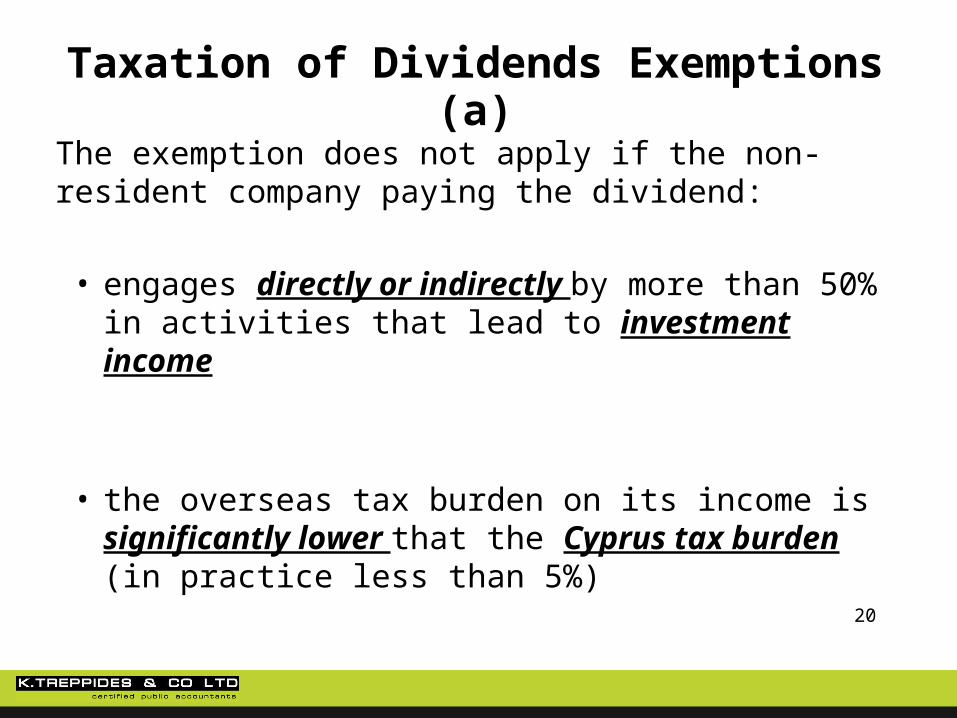

The exemption does not apply if the non-resident company paying the dividend:

• engages directly or indirectly by more than 50% in activities that lead to investment income

• the overseas tax burden on its income is significantly lower that the Cyprus tax burden (in practice less than 5%)

Taxation of Dividends Exemptions (a)

21

• Dividends paid by a resident company to another company, which is also resident in the Republic are exempt from SDC

Taxation of Dividends Exemptions (b)

22

Taxation of Interest

• Interest earned from financing activities is taxed as ordinary business income at a rate of 10%

• If interest does not qualify as business income, then the gross amount of interest received is subject to SDC at a rate of 15%

23

Cyprus: Leading International Shipping Centre

Ranks 3rd top maritime nation in EU27

Top 10 World’s largest shipping management and International ship registries

More than 2100 vessels with 43 million gross tonnage

More than 130 ship owning and ship management related companies with offices in Cyprus, conducting international activities

Deep-sea ports with easy access to Suez

Canal and other major freight routes

Favorable tax regime for ship owning and ship management

24

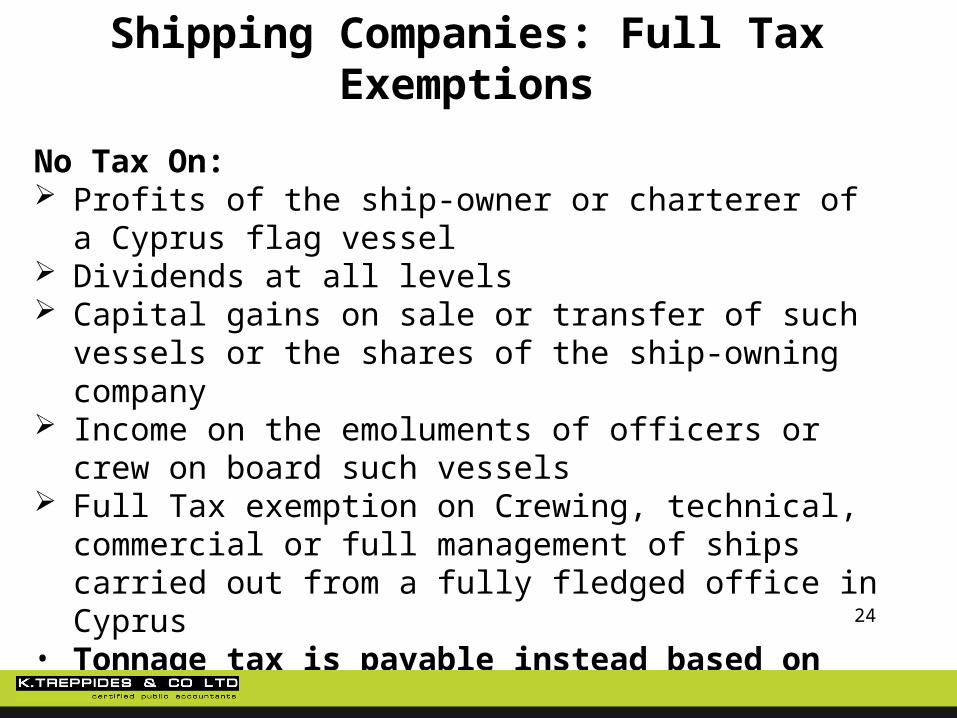

Shipping Companies: Full Tax Exemptions

No Tax On: Profits of the ship-owner or charterer of a Cyprus flag

vessel Dividends at all levels Capital gains on sale or transfer of such vessels or the

shares of the ship-owning company Income on the emoluments of officers or crew on board

such vessels Full Tax exemption on Crewing, technical, commercial or

full management of ships carried out from a fully fledged office in Cyprus

• Tonnage tax is payable instead based on age and tonnage capacity of vessel

25

In Summary

• Modern tax regime acceptable by EU and OECD

• Lowest corporate tax rate in Europe

• Added commercial value and monetary benefits due to ability to register for VAT

• Tax breaks for expatriates

• Offers many opportunities for effective tax planning resulting to an increasing number of Cypriot registered companies

26

Cyprus tax treaties Налоговые соглашения Кипра

• Poland• Qatar• Romania• Russia• San Marino• Serbia

• Norway

• Moldova• Montenegro

• Kyrgyzstan• Lebanon• Malta• Mauritius

• Kuwait

• Ireland• Italy

• United Kingdom• United States • Uzbekistan

• France• Germany• Greece• Hungary• India

• Ukraine• Egypt

• Tajikistan• Thailand

• Czech Republic• Denmark

• Slovenia• South Africa• Sweden• Syria

• Belgium• Bulgaria• Canada• China

• Slovakia• Belarus

• Seychelles• Singapore

• Armenia• Austria

Thank you!

NICOSIA HEAD OFFICETreppides Tower, 9 Kafkasou Str., Aglantzia CY-2112, Nicosia, CyprusP.O. Box 27142, CY-1642, Nicosia, CyprusTel.: +357 (22) 678944, Fax: +357 (22) 679096

E-mail: [email protected] Website: www.treppides.com

LIMASSOL OFFICE12 Arch Makarios III Ave., Kristelina Tower, Mesa Geitonia, 4th floor,Office 401, CY-4000, Limassol , CyprusTel.: +357 (25) 822722, Fax: +357 (25) 822723

Member of EURA AUDIT INTERNATIONAL