Embed Size (px)

Citation preview

Cyclicality Has Not Been Repealed

Chemical Analysts of NYNovember 5, 2003

Dan Smith President and CEO

2

Safe Harbor Language

Statements in this presentation relating to matters that are not historical facts are forward-looking statements. These forward-looking statements are just predictions or expectations and are subject to risks and uncertainties. Actual results could differ materially, based on factors including but not limited to the cyclical nature of the chemical and refining industries; availability, cost and volatility of raw materials and utilities; governmental regulatory actions and political unrest; global economic conditions; industry production capacity and operating rates; the supply/demand balance for Lyondell's and its joint ventures' products; competitive products and pricing pressures; access to capital markets; and technological developments and other risk factors. For more detailed information about the factors that could cause our actual results to differ materially, please refer to Lyondell Chemical Company’s Annual Report on Form 10-K for the year ended December 31, 2002, filed in March 2003, and Lyondell’s Quarterly Report on Form 10-Q, which will be filed in November 2003.

3

You and your peers have raised several questions about the future of the ethylene industry

What will be the impact of future Asian/Middle East supply/demand balances?

– Will US operating rates remain depressed forever?

Are relatively high US polyethylene prices hastening the demise of the industry?

– Will the US become merely an importer of resins and products?

– Will the US lose its entire converter industry?

Do the economics of production allow US producers to survive?

– Has a change in energy costs made the US non-competitive?

4

0

1

2

3

4

5

1986 1989 1992 1995 1998 2001 2004 2007

There is a growing consensus that the global economy is beginning to emerge from a difficult period:

(Percent change in real GDP)Global GDP

Source: Global Insights

5

-8-7-6-5-4-3-2-10123456789

10

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

U.S

. Gro

wth

( Y

r/Y

r %

)

Ind Production GDP

US GDP and Industrial Production

It’s not atypical for industrial production to fall more than GDP but recovery is lagging

Source: Global Insights

6

The US economy should begin to benefit from economic stimulus

Δ GDP

Leads to After

Stimulus Change 1 Year 2 Years Actual Change

Fed Rate Reduction 100 BP 0.6 1.7 150 BP

Real Dollar Decline 10% 0.4 1.6 18%

Income Tax Reduction 1% of GDP 0.4 0.8 3%

Stock Price Increase 20% 0.4 0.8 Flat

Oil Price Decline $10/bbl 0.2 0.4 Up $8

* Source: Fed Reserve, Jan. 1999

7

We believe that global ethylene supply/demand is on a path to a tight balance

175

200

225

250

275

300

Current (2003) 2007 - Base '07 + 2% Growth '07 - 18 Mo Delay

Wo

rld

Eth

yle

ne

Su

pp

ly -

De

ma

nd

(bil

lio

n p

ou

nd

s/y

ea

r)

Effective Capacity Demand

Source: CMAI

8

The companies adding capacity have much at stake at their existing facilities

Company New Capacity* Existing Capacity*

Dow 360 24,970

ExxonMobil 300 18,510

Shell 1,890 14,370

Sabic 2,870 12,100

BP 1,920 10,230

Top 5 Total 7,340 80,180

* MM Lbs/Year per CMAI

Source: CMAI

9

0

20

40

60

80

100

120

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000

2000 GDP/Capita

PE

Co

nsu

mp

tio

n/c

apit

a, lb

s

US

Korea

Taiwan

WE

Singapore

Japan

Thailand

Malaysia

ChinaIndiaIndonesia

The emergence of a middle class increases local demand for plastics

Source: CMAI 2001

10

Even forecasters that have recently developed negative outlooks continue to forecast growth in the US market

Quarterly U.S. Ethylene Demand Vs GDP

4

6

8

10

12

14

16

18

20

3.0 5.0 7.0 9.0 11.0 13.0

GDP - Trillion $ (constant 1996 $'s)

NPRA Quarterly Demand

CMAI Based Forecast

30-Year Trendline

2010

1970

2003

Source: SRI, CMAI, NPRA, US Govn.

Qu

arte

rly

Eth

ylen

e D

eman

d

(B

l. L

bs)

11

When all factors are considered, exporting is not always profitable

Basis: 1 B lbs Producer

Domestic Margin - 17¢ / lb

5% Exports

Export Margin

Export Profit

Neutral Domestic Market Response

¢ / lb $ MM / Yr% Returned

to US Price Impact,

¢ / lb

2 1 12% 0.1

5 2.5 30% 0.26

Source: Lyondell Chemical Company

12

We believe that resin importation growth is a temporary phenomena

0

5

10

15

20

25

30

35

40

HM

W H

DPE

Im

port

ed R

esin

MM

lbs.

0

10

20

30

40

50

60

Spr

ead

cent

s/lb

.

HMW HDPE Imported Resin MM lbs. HMW Price Spread to Feedstock

Source: CMAI

13

Labor costs are the primary driver behind the importation of bags and sheet

0

10

20

30

40

50

60

70

80

U.S. China to U.S. China to U.S. @ equal RM Cost

Bag

Pro

du

ctio

n C

ost

, cen

ts/lb

U.S. Domestic Freight

Ocean Freight

Conversion ex labor

Labor

Raw Material

Source: CMAI & Lyondell

14

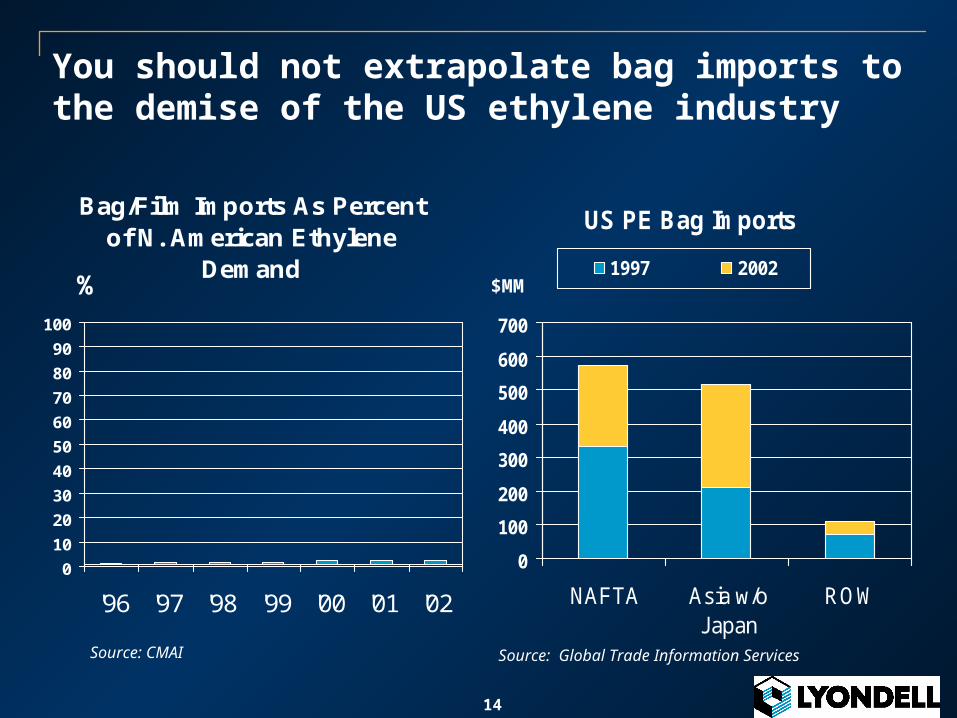

You should not extrapolate bag imports to the demise of the US ethylene industry

Bag/Film Imports As Percent of N. American Ethylene

Demand

0

10

20

30

40

50

60

70

80

90

100

'96 '97 '98 '99 '00 '01 '02

%

US PE Bag Imports

0

100

200

300

400

500

600

700

NAFTA Asia w/oJapan

ROW

1997 2002$MM

Source: Global Trade Information ServicesSource: CMAI

15

Despite the pressure caused by resin prices some converters have maintained a reasonable margin

16

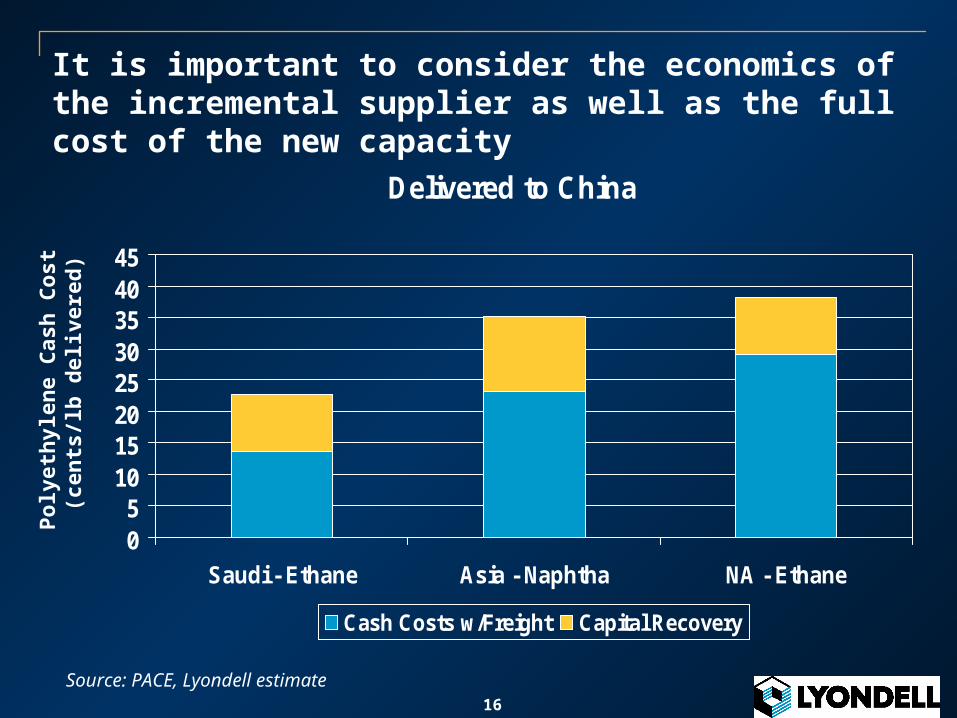

It is important to consider the economics of the incremental supplier as well as the full cost of the new capacity

Delivered to China

05

1015202530354045

Saudi - Ethane Asia - Naphtha NA - Ethane

Cash Costs w/Freight Capital Recovery

Po

lyet

hyl

ene

Cas

h C

ost

(ce

nts

/lb d

eliv

ered

)

Source: PACE, Lyondell estimate

17

Existing US capacity is competitive in its home market – E/P crackers are likely to be the high cost global facilities

Delivered to U.S.

05

1015202530354045

Saudi - Ethane Asia - Naphtha NA - Naphtha NA - Ethane

Cash Costs w/Freight Capital Recovery

Po

lyet

hyl

ene

Cas

h C

ost

(cen

ts/lb

del

iver

ed)

Source: PACE, Lyondell estimate

18

Growing global demand will increasingly be supplied by gas based raw materials

Global Ethylene Supply by Feed Type

0

20

40

60

80

100

120

140

Current (2003) Additions (2008)

Eth

ylen

e S

uppl

y - H

eavy

vs

Ligh

t (b

illio

n po

unds

/ ye

ar)

Heavy Liquid NGL Based

19

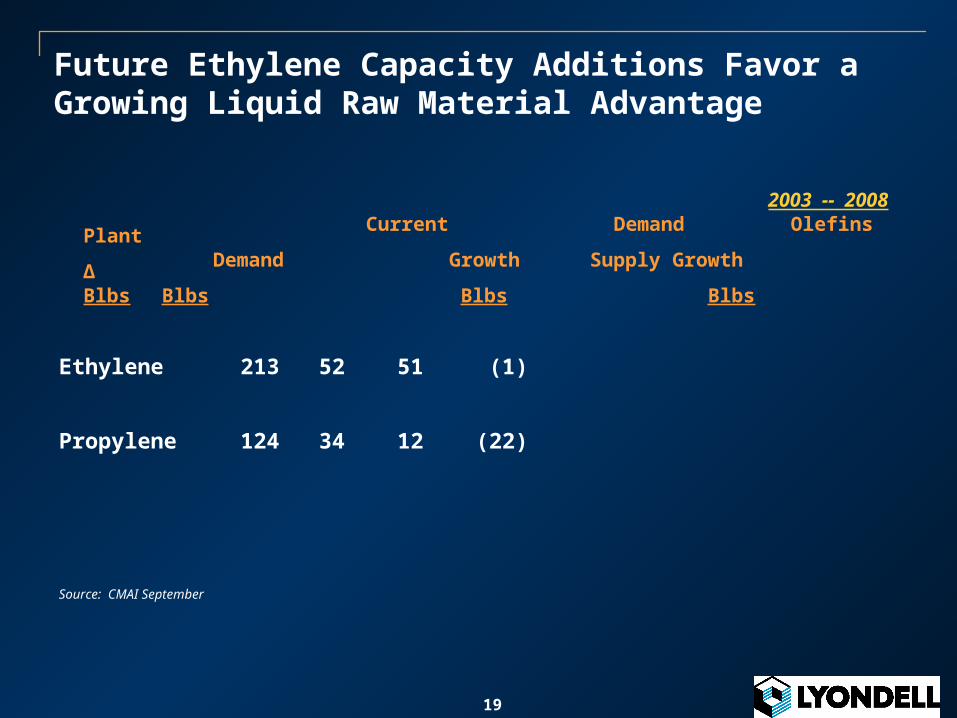

Future Ethylene Capacity Additions Favor a Growing Liquid Raw Material Advantage

2003 -- 2008 Current Demand Olefins Plant

Demand Growth Supply Growth ΔBlbs Blbs Blbs Blbs

Ethylene 213 52 51 (1)

Propylene 124 34 12 (22)

Source: CMAI September

20

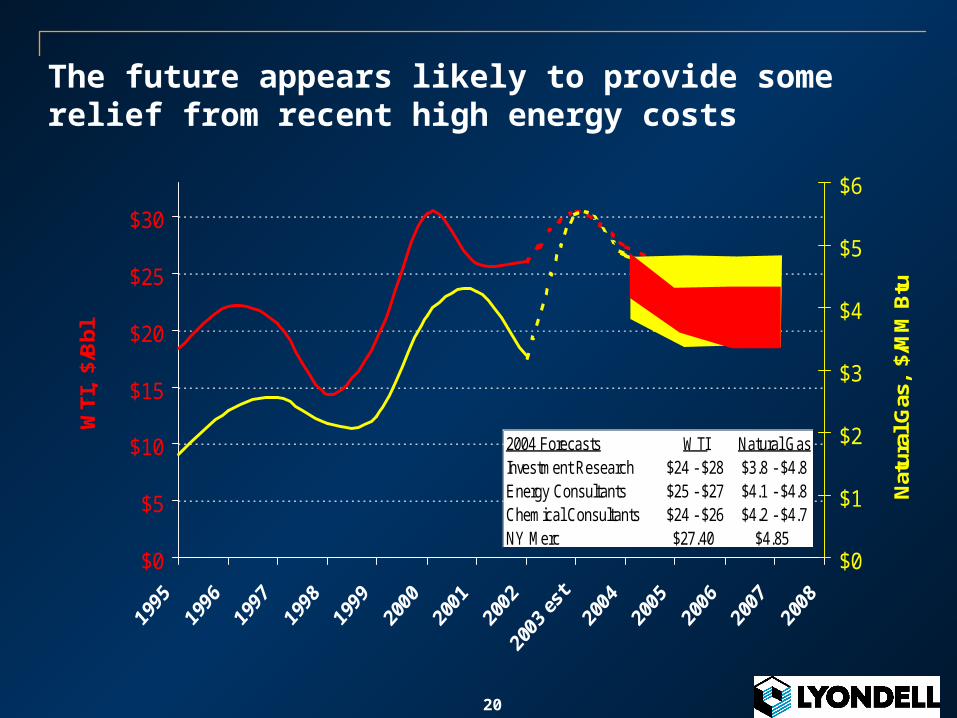

The future appears likely to provide some relief from recent high energy costs

$0

$5

$10

$15

$20

$25

$30

WTI

, $/

Bbl

$0

$1

$2

$3

$4

$5

$6

Nat

ural

Gas

, $/

MM

Btu

2004 Forecasts WTI Natural GasInvestment Research $24 - $28 $3.8 - $4.8Energy Consultants $25 - $27 $4.1 - $4.8Chemical Consultants $24 - $26 $4.2 - $4.7NY Merc $27.40 $4.85

21

It appears that natural gas in the US will be more closely coupled to global energy prices

Oct

Nov

Dec

Jan-03

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Natural Gas & Substitutes Price Trend

$3

$4

$5

$6

$7

$8

$9

Oct

Nov

Dec

Jan-

03

Feb

Mar

Apr

May Jun

Jul

Aug Sep Oct

Nov

Dec

Jan-

04

Feb

Mar

$/M

MBtu

NYMEX

Natural Gas

Source: NYMEX

Distillate

Residual Fuel

22

It appears that natural gas in the US will be more closely coupled to global energy prices

0

2

4

6

8

10

12

14

16

18

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

LNG

Cap

acity

- B

CF/

D

Existing Terminals

Announced North American Growth Actual

ImportsImport Capacity

Source: Platt's Publications

23

This analysis drives our industry view, actions, and strategy

Industry view

– Global and domestic industries will both continue to grow

– Demand will drive increased operating rates and the cycle will turn

– Liquid cracking offers significant leverage and value

– Chasing the incremental export sale generally destroys value

Actions

– Focus on domestic market

– Ethylene expansion must be advantaged and is not a priority

Strategy

– Operationally focus on Operational Excellence

– Financially focus on liquidity and debt reduction

24

We would like to leave you with some other thoughts to consider

Is there evidence that the global demand for plastics is decreasing? Or conversely will global development accelerate its usage?

Is there evidence that new ethylene plants are significantly more efficient than existing plants? Or does the investment in new capital mean they are less cost effective?

Are the middle east countries likely to give away the value of stranded ethane? Or is it more likely to follow the path of crude oil that at one time cost less than $3/bbl?

Will the major oil companies and your banks rush to subject their current investment exposure to excess incremental supply?

Has cyclicality been repealed?