Embed Size (px)

Citation preview

LAG AND DIFFERENCE OPERATORS

• L is an operator such that:

LXt = Xt-1 (16)L2Xt = L (LXt) = Xt-2 (17)LjXt = Xt-j (18)∆Xt= (1-L) Xt = Xt-Xt-1 (19)Xt - Xt-s = (1-Ls) Xt (20)(1-Ls) = ∆s (21)∆s = (1-Ls) = (1-L) (1 + L + … + Ls-1) = ∆ Us-1 (L)

(22)

1980 1985 1990 1995 2000

2000

3000

CEMENT

1980 1985 1990 1995 2000

-.2

0

.2DLCEMENT

1980 1985 1990 1995 2000

-.25

0

.25

.5D12DLCEMENT

1980 1985 1990 1995 2000

-.5

0

.5DD12DLCEMEN

CONCLUSION

• Applying regular and seasonal differences we can remove trend and seasonality.

A FIRST COMMENT ON STATIONARITY

• A time series Zt is stationary if

� E(Zt) = constant = µ� Var(Zt) = constant =γo

� Cov (Zt, Zt+k ) only depends on k = γk

1980 1985 1990 1995 2000

50

200

250

300

350 Cement consumption orginal series

1980 1985 1990 1995 2000

-.3

-.2

-.1

0

.1

.2

.3

.4Cement consumption differencedseries (∆∆∆∆∆∆∆∆12121212log Xt)

Innovations, white noise and random walkInnovations

Time series models

wt = f (past) + atknown at unknown attime t-1 time t-1

We denote,: forecast for wt with information up to t-1

It is a function of the past.

Therefore,

surprise or innovation

1)1(ˆ +−tw

ttt aww += +− 1)1(ˆ

• Up to moment t-1 we have the following information

� Past values of the series: w1, w2, ..., wt-1

� Past innovations: a1, a2, ..., at-1

• According to the information used we can construct two types of time series models:

� wt = f (past history in terms of innovations) + at

– These are called MOVING AVERAGE MODELS (MA)

� wt = f (past history in terms of observed values of the series) + at

– These are called AUTOREGRESSIVE MODELS (AR)

���� White noise time series• The simple time series model will generate a purely random series,

which is denoted as WHITE NOISE and reperesented by at

• A series is white noise if:– cor(at, at-j) = 0 for all , ∀ j ≠0 – Its mean or expected value is constant and equal to zero.

���� Example: The winning numbers of a state lotery.• For many previous records that you know, you dont have any

advantage in forecasting the next winning number.• There is no dependency between future and past numbers.

Properties of white noise series� The order of the observations does not matter.� Being µ = 0, the series is unforecastable.

• Because of property (1) a white noise is in a certain sense the denial of a time series.

0 20 40 60 80 100 120 140 160 180 200

-2

-1

0

1

2

WN

But the white noise is in the base of any time series model...

• Stochastic means that can not be predicted without error, therefore,

wt ≠ f (wt-1, wt-2, ...)

• But,

wt = f (wt-1, wt-2, ...) + an unpredictable component.wt = f (wt-1, wt-2, ...) + white noise.

wt depends on its previous values andis stochastic

���� TIME SERIES MODEL

We consider

wt = f (wt-1, wt-2 , ...) + rt (residuals) (1)

If,

• rt is white noise our model cannot be improved• rt is not white noise:

� is predictable

� we can construct a model for it

� and change (1)

���� Random walk model Efficient markets:

• A huge number of agents having perfect information.

• Therefore they act adapting their behaviours completely to the available information and a price pt results for time tand since there is nothing left to do given the available information this is the price taken for the future.

• But at time (t+1) some unexpected events will occur and agents adapt immediately and in a full way to the new information and a new price will be formed.

pt+1= pt + at

Random walk model

• In this model, the variable pt is not stationary, it is I(1,0), therefore it showslocal oscillations in level and

wt= ∆∆∆∆pt= pt -pt-1 =at

it is unforecastable.

The model pt+1= pt + at+1

is called a RANDOM WALK MODEL.

• In these markets innovations are completely absorbed when they appear and the price changes only depend on contemporaneous innovations, all previous innovations have been absorbed in xt-1

• Changes in prices in efficient markets are unforecastable. Monetary markets, currency markets, etc., are very near to efficiency, therefore the prices in them: interest rates, exchange rates are closed to

xt = xt-1 + at

and the forecasting exercise is too simple

th)t( xx =+ ∀ h

wt is explained as a function of past innovations (a1, a2, ..., at-1)• Moving average model of order 1

wt ==== - θθθθ at-1 + at MA(1)at is a white noise time series with:

Var(at) = σ 2a

���� Moving Average Models (MA)

0 20 40 60 80 100 120 140 160 180 200

-2

-1

0

1

2

MA(1);_-0.5

0 20 40 60 80 100 120 140 160 180 200

-3

-2

-1

0

1

2

3 MA(1);_0.5

Properties: µw = 0 , γo = (1+ θ2) σ 2a

Examples:wt ==== at + 0.5 at-1 wt ==== at - 0.5 at-1

• The innovation at has effect on wt an wt+1 . Let

xt = xt-1 + wt

xt = xt-1 - θat-1 + at

xt-1 = xt-2 - θat-2 + at-1

xt = xt-2 - θat-1+ at - θat-2 + at-1

= xt-2 + at+ (1-θ)at-1 - θat-2 …...

xt = xo + at+ (1-θ)at-1 +(1-θ)at-2 +….

An innovation coming into the system has a permanent effect on the model of magnitud (1-θ) times its value.

• Time dependency in a MA(1) time series.• It is measured by the correlation between wt and wt-j

corr (wt, wt-j), j= 1,2,3..

These are called AUTOCORRELATIONS.

( ) ( )( )t

jttjtt wvar

w,wcovw,wcorr −− =

-1.0

-0.5

0.0

0.5

1.0

1 2 3 4 5 6-1.0

-0.5

0.0

0.5

1.0

1 2 3 4 5 6

Examples:wt ==== at + 0.5 at-1 wt ==== at - 0.5 at-1

Autocorrelations in a MA(1) time series.

• � If θθθθ < 0 ⇒ ρ1 > 0An observation at one side of the mean is inclined to be followed by an observation at the same side of the mean.

• � If θθθθ = 0 ⇒

The resulting series is a white noise.

• � If θθθθ > 0 ⇒ ρ1 < 0The resulting series oscillates more than a white noise

21 1 θ+θ−=ρ

In a MA(1) time series only ρ1 ≠ 0

���� Example:� wt = at + 0.5 at-1 � white noise � wt = at - 0.5 at-1

0 20 40 60 80 100 120 140 160 180 200

-2

-1

0

1

2

WN

0 20 40 60 80 100 120 140 160 180 200

-3

-2

-1

0

1

2

3 MA(1);_0.5

0 20 40 60 80 100 120 140 160 180 200

-2

-1

0

1

2

MA(1);_-0.5

Therefore:• (1) A white noise series is unforecastable.• (2) A MA(1) series can be forecasted one-step ahead whith a

maximun value of R2 < 0.5.

•A mesure of forecastability: R2

we will see that -1< θ <1

)1

12

()(1+

+−=T

T

wVareVarR

)1()1(1 2

2

22

22

θθ

σθσ

+=

+−=R

wt ==== at - θθθθ1 at-1 - θθθθ2 at-2

���� Example: Wt = at - 0.4 at-1 - 0.3 at-2

Moving average model of order 2: MA(2)

0 20 40 60 80 100 120 140 160 180 200

-3

-2

-1

0

1

2

Wt

-1.0

-0.5

0.0

0.5

1.0

1 2 3 4 5 6

FAC

• Only current and 2 past innovations enter in the modelµw = 0 , γo = (1+θ1

2+ θ22) σa

2

• There is a cut in the autocorrelation function after lag 2.

• Just one and two forecasts are different from zerowT+1 ==== aT+1 - θθθθ1 aT - θθθθ2 aT

Persistence of innovations only last 2 periods.Variance of the forecast error increases till var of Wt.

For Xt variance of the forecast error increases without limit.

wt ==== at - θθθθ1 at-1 - θθθθ2 at-2 - … - θθθθq at-q.

• Only current and q previous innovations enter the model

µw = 0 , γo = (1+θ12+…+ θq

2) σa2.

• There is a cut in the autocorrelation function after lag q.• Just one to q steps ahead forecasts are different from zero.• Innovations persist q periods.

• Example: FAC MA(6).

A general moving average model of order q: MA(q)

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

1 2 3 4 5 6 7 8 9 10 11 12

• The autocorrelation function represent dynamics in the time series model.

• The sample counterpart of the autocorrelation function (rk) is the correlogram. It is calculated as:

Autocorrelation Function (FAC) and correlogram

,...2,1k

w

ww

r n

1t

2t

kn

1tktt

k =

⋅

=

∑

∑

=

−

=+

FAC

-1.0

-0.5

0.0

0.5

1.0CORRELOGRAM

-.75

-.5

-.25

0

.25

.5

.75

1

Example : wt ==== at - 0.5at-1

AUTOREGRESSIVE MODELS (AR)

• Dual representation of dynamic models:

MA(q) ⇒ ARAR(p) ⇒ MA

wt = f (past in terms of past w´s) + at

Simplest model: AR(1)

wt = φwt-1 + atknown at unknown attime t-1 time t-1

INNOVATION

wt = 0.5 wt-1 + at

wt-1 = 0.5 wt-2 + at-1

wt = 0.52 wt-2 + 0.5 at-1 + at

wt-2 = 0.5 wt-3 + at-2

wt = 0.53 wt-3 + 0.52 at-2 + 0.5 at-1 + at

...

wt = φφφφwt-1 + at ⇒⇒⇒⇒ wt = φφφφ t wo +(at + φφφφat-1 +…+ φφφφt-1 a1)sequence of INNOVATIONS

An AR model may be represented as an MA model.

MOVING AVERAGE REPRESENTATION OF AN AR(1) PROCESS φ= 0.5

� -1< φφφφ<1• The effect on wt of a very distant

innovation is not exactly 0, but it is negligible.AR(1) may be approximated by MA(q) given to q a sufficient large value.

The autocorrelation will be longer but restricted.

• In MA(q) the innovation at-j , j<q has a free effect given by θj.

• In AR(1) the innovation at-j has a restricted effect to be φj.

INNOVATIONS PERSISTENCE

wt = φφφφ t wo +(at + φφφφat-1 +…+ φφφφt-1 a1)

0 10 20 30 40 50 60 70 80 90 100-.2

.15

-.1

.05

0

.05

.1

.15

Phi=0.3

� φφφφ> 1• From the initial value wo the model

becomes explosive.

• very distant innovations are much more important then recent ones.

• Similary happens with φ<-1.

• Reality does not seem to behave in a permanent explosive way and we reject that |φ |>1.

INNOVATIONS PERSISTENCE

wt = φφφφ t wo +(at + φφφφat-1 +…+ φφφφt-1 a1)

0 10 20 30 40 50 60 70 80 90 100

5

10

15

20

25

30

35 Phi=1.05

� φφφφ= 1• This situation is not explosive.• It is the situation we have considered for

trends characterized by showing local oscilations in level.

INNOVATIONS PERSISTENCE

wt = φφφφ t wo +(at + φφφφat-1 +…+ φφφφt-1 a1)

0 10 20 30 40 50 60 70 80 90 100

.1

.2

.3

.4

.5

.6

.7

.8

.9

1 Phi=1

Now we do not want models for trends, but for deviations from trends, so we restrict theAR(1) model to

|φ |<1-1<φ<1.

An AR(1) model wt = φwt-1 + at

with -1< φ<1 is stationary.

• An MA(1) model may also be represented as an AR modelwt = at - θ at-1

at = wt + θ at-1

at-1 = wt-1 + θ at-2

wt = at + θ (wt-1 + θ at-2 ) =

= at + θwt-1 + θ2 at-2 at-2 = wt-2 + θ at-3

wt = at + θwt-1 + θ2 wt-2 + θ3at-3...wt = at - θθθθ at-1 ⇒⇒⇒⇒ wt = θθθθt ao + at + (θθθθwt-1 + θθθθ2 wt-2 +…+ θθθθt-1 w1 )

ESTIMATION OF INNOVATIONS - Invertibility

We can discuss as in the previous section the effects of the different values for θ.

ESTIMATION OF INNOVATIONS - Invertibility

|θθθθ |> 1

θθθθ = 1

-1 < θθθθ < 1

• From the initial value ao the model becomes explosive.• Very distant observations are much more important than recent

ones• We can not estimate innovations.

• Very distant observations are important .• We can not estimate innovations.

• The effect on wt of a very distant observation in not exactly 0, but it is negligible.

• MA(1) model may be approximated by an AR(p) model with p large enough.

SUMMARY ON ESTATIONARITY AND INVERTIBILITY

• STATIONARITY: old innovations lose their importance as time goesby.

• INVERTIBILITY: old observations of the time series lose their importance as time goes by.

Model Stationarity Invertibility

AR(1) wt= φ wt-1+ at Only if |φ|<1 Always

MA(1) wt= at- θ at-1 Always Only if |θ|<1

STATIONARY: AR(1) MODEL

AR(1)- Model has an infinite moving average - with restricted coefficient which decline to zero. If making ψψψψj = ααααj .

The stationarity condition | φφφφ |<1 can also be expressed as ∑∑∑∑ ψψψψj2 = ∞∞∞∞ .

PROPERTIES:� E(wt) = constant = 0� Var(wt) = γo = σ2 / (1- φ2)� Cov (wt, wt-1 ) = ρk =φk ; ρ1 = φ

wt = φφφφwt-1 + at , | φ |<1

∑∞

=−φ=

0jjt

jt aw

and sowt = at + φwt-1 + φ2 wt-2 + φ3 at-3 +...

THE ACF OF AR(1)

• Only ρρρρ∞∞∞∞ = 0. There is not cutting point.

• But it declines to zero in absolute value.

• Therefore the correlation between wt and wt-H (H large) is not exactly zero but it neglegible: very distant observations have practically no effect at present time.

• The declining to zero depends on | φφφφ | : the higer the value of | φφφφ |the slowest declining.

THE ACF OF AR(1)• Since the correlation between wt and past values (wt-j) could last for

some long time before it becomes negligible.

⇓⇓⇓⇓

The forecast horizon can be large before the forecasts become negligible (zero).

AUTORREGRESIVE MODEL OF ORDER 2 AR(2)

���� Example:(1) Stationary

wt=0.3 wt-1 + 0.4wt-2 + at

0 10 20 30 40 50 60 70 80 90 100

-.2

-.15

-.1

-.05

0

.05

.1

.15

.2

.25 Var1

wt = φ1 wt-1 + φ2 wt-2 + at

The formulation of the dual MA representation is now mathematicallymore complex.

We need to introduce some new concepts.

� Polynomial and lag operators notationthe lag operator -denoted as L- delays one period the variable

L wt = wt-1

L2 wt= L wt-1 = wt-2 .Another way for writing AR or MA models is in terms of the lag operator

wt = φ1 wt-1 + φ1 wt-2 + at

wt = ( φ1 L + φ2 L2 ) wt + at

(1 - φ1 L - φ2 L2 ) wt = at

wt = at - θ at-1 = (1 - θ L ) at .

� Normal equation Z2 = φ1 Z1 + φ2 Z0.

� Roots of the normal equation G1, G2 and denote G the root with largest absolute value.

STATIONARITY AND LARGEST ROOT

• If ||||G|||| <1 the model AR(2) is stationary.

• If ||||G|||| >1 the model AR(2) is explosive.

• If G= 1 the AR(2) model takes the form: (1-L)(1-G2L)Wt=at

(1-L)Wt=G2(1-L)Wt-1+at.

and this model is not stationary but one whith local oscilations in level.

STATIONARITY AND MA REPRESENTATION

where Ψj → 0

and

∑Ψj2 < ∞

1;aw o0j

jtjt =ΨΨ=∑∞

=−

If AR(2) is stationary

Iteratively an AR(2) model can be formulated as an infinite moving average model

AUTOCORRELATION FUNCTION (ACF)• The first values of the ACF depend on the two roots of the normal

equation.• Cases:� G1, G2 real values (as in AR(1) case).

� G1, G2 complex. In this case the ACF will show damped sinusoidal oscillations with period grater then two time units.

An AR(2) with complex roots is a simple model to capture cyclical oscillationin the data.

Real Roots Complex RootsEXAMPLESACF for AR(2)

GENERAL AUTOREGRESSIVE MODEL: AR(p)

• PROPERTIES OF AR(p) MODEL

All the properties are derived mathematically from the normal equation associated to the AR(p) model and its p roots (solutions).

� Normal equation Zp = φ1 Zp-1 + φ2 Zp-2 + … + φp-1 Z + αp

� Roots G1, G2, … ,Gp

� Largest root in absolute value G

wt ==== φφφφ1 wt-1 + φφφφ2 wt-2 + … + φφφφp wt-p + at

STATIONARITY AND LARGEST ROOT

where Ψj → 0

and ∑ Ψj

2 < ∞

1;aw o0j

jtjt =ΨΨ=∑∞

=−

then model AR(p) is stationary

If ||||G|||| <1 the model AR(p) is stationary.If ||||G|||| >1 the model AR(p) is explosive.If G= 1 the AR(p) has local oscillations in level.

Solving the model iteratively in terms of past innovations we obtain anMA(∞).

AUTOCORRELATION FUNCTION (ACF)• The first values of the ACF depend on all the p roots of the normal

equation.But if G is a dominant root - e.g. no other root has an absolute size near |G|-the autocorrelation coefficients.

ρρρρk for k not small.can be approximated by.

ρρρρk ≅≅≅≅ A Gk or G>0 (1)

ρρρρk ≅≅≅≅ ±±±± A |G|k otherwise (2)

where A is a constant.

• The dominant root could be a pair of comple conjugate roots in which case ρk in (2) shows damped sinusoidal oscillation. With period greater than two time units.

PARTIAL AUTOCORRELATION FUNCTION (PACF)• The partial autocorrelacion function is a tool to identify the order of

on AR model.

FAC PACF

FAC and PACF for AR models

���� Example:

• The comparison between on AR(1) and AR(2) shows that, though in both cases each observation is related to the previous ones, the kind of relationship between observations related 2 periods is different.

AR(1): wt-3 → wt-2 → wt-1 → wt

The only relation between wt-2 and wt is through wt-1 .

• Now in the AR(2) the relation between wt-2 and wt is direct and indirect though wt-1

| |AR(2): wt-3 → wt-2 → wt-1 → wt

| |

• The PACF shows the number of direct relations with wt .

DUAL BEHAVIOUR OF ACF AND PACF IN MA AND AR MODELS

ACF PACF

AR(p) long structure cuts at lag p

MA(q) cuts at lag q losg structureFAC PACF

FAC and PACF for MA models

PACFFAC

FAC and PACF for AR models

MIXED AUTOREGRESSIVE-MOVING AVERAGE MODELS

Wt = f(past) + atIN TERMS OF Wt-j ANDIN TERMS OF at-j.

GENERAL FORMULATION: ARMA (p, q)

Wt = φ1Wt-1 + … + φpWt-p - θ1at-1 - … - θqat-q + at

EXAMPLE: ARMA (1,1)Wt = φ1Wt-1 - θ1at-1 + at

THE EXPLOSIVE NATURE OF MODEL ARMA(1, 1) DEPENDS ON AUTOREGRESSIVE PARAMETER φφφφ1111.... IF | φφφφ1| < 1 THE MODEL IS STATIONARY.

THE EXPLOSIVE NATURE OF ARMA(p, q) DEPENDS ON THE AUTOREGRESSIVE PART OF THE MODEL AND THE CONDITON FOR STATIONARITY IS THE SAME THAT IN MODEL AR(p).

PAST INNOVATION

PAST INNOVATION

MIXED AUTOREGRESSIVE-MOVING AVERAGE MODELS

MOVING AVERAGE REPRESENTATION OF ARMA(p, q).

PROCEEDING IN A SIMILAR WAY THAN FOR AN AR MODEL A STATIONARY ARMA (p, q) MODEL CAN BE REPRESENTED BY A MOVING AVERAGE OF INFINITE ORDER WITH DECLINING COEFFICIENTS.

INTEREST OF MODEL ARMA(p, q)• PARSIMONY PRINCIPLE

– A MA(q) model is only valid for variables in which the innovations are fully absorbed after q observations.This could be very restrictive in cases unless q is large.

– An AR(p) model incorporates all previous innovations with restricted coefficients declining to zero. This restriction affect all innovations.Examples: Wt = 0.5 Wt-1 + at

Wt = at + 0.5 at-1 + 0.52 at-2 + …

,...1,0,,5.00

==∑∞

=− jaW

jjt

jt

This could be very restrictive in cases unless p is large.– An ARMA(p, q) model incorporates all previous innovations with restricted

coefficients declining to zero, but in a more flexible way than an AR process.Examples: Wt = 0.5 Wt-1 + 0.2 at-1 +at

Wt = at + 0.7 at-1 + 0.7 · 0.5 at-2 + 0.7 · 0.52at-3 + ...

INTEREST OF MODEL ARMA(p, q)CONCLUSION

• The ARMA(p, q) model can capture longer innovation effects in a less restrictive way with less parameters than MA(q) and AR(p) models.

AGGREGATION AND ARMA MODELS• It can be shown that aggregating MA(q) and AR(p) models one gets an

ARMA model.• Many economic variables: CPI, industrial production, sales in large

firms, etc. are aggregates therefore they can follow an ARMA model.• Also, very often the variables which we observed are an aggregation of

the true variable and a measurement error process.• CONCLUSION: parsimony and aggregation justify that ARMA

models appear in practice.

AUTOCORRELATION FUNCTION• Similar properties to AR(p) model, but with a more flexible declining

behaviour that for models in which q p does not come from the beginning.

≥

STATIONARY AND INVERTIBILITY IN ARMA MODELS

• First let’s recall to the results in AR(p) and MA(q) models.

S t a t io n a r i t y I n v e r t ib i l i t y

A R ( p ) I f l a r g e s t A Rr o o t G h a s |G |< 1

A l w a y s

M A ( q ) A l w a y s I f l a r g e s t M Ar o o t h a s |H |< 1

• These properties remain in ARMA(p,q) MODELS– Stationary: if the largest autoregressive root, G, satisfies |G|<1.– Invertible: If the largest moving average rroot, H satisfies |H|<1.

• Stationary and invertible MA(q), AR(p) or ARMA(p,q) models always have

– (1) An AR representation.– (2) An MA representation.

SEASONAL DEPENDENCY• Time series with monthly or quaterly observations usually show

dependence on previous realizations but also on the ones occurred a year ago.

Dependence on previous months

But also in same month previous years

• Because of this seasonal dependence the ACF of the models may show long temporal dependence that would lead to ARMA models with high values for p and q.

• This will be further simplified with the use of multiplicative models.

Jan. Feb. Mar. Apr. Jun. Jul. Aug.

2000199919981997

*

MAIN POINTS OF THE BOX-JENKINS METHODOLOGY

I. Formulate a theory for a general class of models capable of describing the real times series.

II. Construct a procedure to find for a given time series best model within the general class.

GENERAL CLASS OF MODELS IN B-J METHODOLOGY

• Is the class of ARIMA models with deterministic factor.• In the specification of these models enter different types of

parameters which capture different features of the data.

� A parameter referring if the model is formulated on the original data or on the logarithmic transformation if it shows evolutivity in variance.

SETS OF PARAMETERS IN A ARIMA MODEL

� A set of parameters designed to capture the evolutivity in mean of the data.

EVOLUTIVITY IN TRENDSEASONAL EVOLUTIVITY

These parameters correspond to the number ofregular differencesseasonal differencesoverall constantseasonal dummiesother deterministic factors

� Parameters to capture the time dependency• Having fixed the sets parameters [1] and [2]

the original data can be transformed in stationary data.

• For the stationary data, parameters specifying the ARMA model capture the time dependency.

• Looking at the time dependency appearing in the correlogram we can formulate the main aspects of the time dependency.

� Parameter reflecting the one-step ahead uncertainty

• The only one step ahead factor which is uncertain is at.

• at � Normal (0,σ)

• σ = reflects this uncertainty

EXAMPLE: MODEL 1( ) tt

2221 aXlogLL1 =∆φ−φ−

Stationary transformation:)0,2(Iwxlog tt

2 =∆Systematic growth with no seasonality

[ ] +−+= −−− 2t1t1tt xlogxlogxlogxlog Evolutivity path

+φ+φ −− 2t21t1 ww Oscillations around the evolutivity path

ta Innovations

EXAMPLE: MODEL 2( ) ( )( ) t

ssts

ss aLLXLL θθ −−=∆∆Φ−Φ− 11log1 12

21

Stationary transformation:)0,2(Iwxlog tts =∆∆

Systematic growth and stochastic seasonality

[ ] +−+= −−−− 1stst1tt xlogxlogxlogxlog Evolutivity path

++−−Φ+Φ+ −−+−−−− 1111221 stssstststst aaaww θθθθ Oscillations around the evolutivity path

ta+ Innovations

EXAMPLE: MODEL 3( )

1

1s

t j j tj

x b S t L aθ=

∆ = + −∑

Stationary transformation:∑=

− −−=s

1jjj1ttt tSbxxw

+++= ∑=

∗−

s

1jjj1tt tSbbxx Evolutivity path

1taθ −− + Oscillations around the evolutivity path

ta Innovations

Calculate b= 1/s ∑bj

Define bj*= bj -b and write ( )

11

s

t j j tj

x b b S t L aθ∗

=

∆ = + + −∑

If b is significantly different from zero in model 3 we have systematic growth with a deterministic mean growth (b) and deterministic seasonal factor (bj*). Otherwise model3 only shows local oscillations in level with deterministic seasonality.

PROCEDURE TO FIND THE BEST MODEL FOR A GIVEN TIME SERIES• THREE STAGES:

– INITIAL SPECIFICATION:• Looking at plots of original and differenced data and,• looking at plots of the correlogram and partial correlogram of those time series

(original and differences)• Make an initial specification of the values d, D, p, q, P and Q.

– ESTIMATION:• Given the previous specification estimate the corresponding model.

– DIAGNOSTIC CHECKING:• Apply a battery of tests to the estimation results.• If these tests do not reject the initial model take it as good and use it for

forecasting purposes.• If these tests reject the initial model you will have an indication specifying a

new model. Do it and go to stage (1).Process finishes when at stage (3) you do not reject the model under

consideration.

Determination of evolutivityparameters

• Looking at plots Xt or ∆Xt and log Xt or ∆log Xt

determine in which case the magnitud of the oscillationsare more homogeneous.– If there is not a clear cut consider if the economic phenomenom

can evolve according to proportionality law or not.– In the positive case take the logarithmic transformation.

– In doubt take also the logarithmic transformation.• From now on Xt will represent the data as decided in this

stage.

Determination of parameters for evolutivity in mean(I)

• MAINLY– number of regular differences– number of seasonal differences– constant term– (other deterministic parameters)

• CONSIDER FROM THEORY OR EXPERIENCE the type of evolutivity in the economic phenomenom under study.

Determination of parameters for evolutivity in mean(II)

• EXAMINE the plots and tables of Xt , ∆Xt , ∆sXt ,∆²Xt, and∆∆sXt and decide which one can be taken as stationary:

– constant mean– constant variance– similar dependency along the sample.

• If doubt take the transformations with a small number of differences.• As an auxiliary intrument use correlograms of the corresponding

transformations. The correlograms of the stationary transformation must tend soon to non-significant values.

• These are the series:– Serie 1 � Spanish Cement Consumption

– Serie 2 � Spanish Expenditure in residential building

– Serie 3 � Spanish Non Residential Building

– Serie 4 � Spanish Civil Work

– Serie 5 � Monthly Spanish Consumption of Cement

– Serie 6 � Japanese Cement Consumption

• Now, we are going to see their graphics and correlograms.

Spanish Cement Consumption graphics (Serie 1)

1990 1995 2000

0000

0000

0000 CEM

1990 1995 2000

-.1

0

.1D1LCEM

1990 1995 2000

-.1

0

.1

.2 D4LCEM

1990 1995 2000

-.2

-.1

0

DD4LCEM

Spanish Cement Consumption Correlograms (Serie1)

Correlogram

0 5 10

.25

.5

.75

1LCEM

Correlogram

0 5 10

-.5

0

.5

1D1LCEM

Correlogram

0 5 10

-.5

0

.5

1D4LCEM

Correlogram

0 5 10

-.5

0

.5

1DD4LCEM

Spanish Expenditure in residential building graphics (Serie 2)

1990 1995 2000

0000

0000

RES

1990 1995 2000

-.2

-.1

0

.1

D1LRES

1990 1995 2000

-.1

0

.1

D4LRES

1990 1995 2000

-.1

0

.1

DD4LRES

Spanish Expenditure in residential building correlograms (Serie 2)

Correlogram

0 5 10

-.5

0

.5

1LRES

Correlogram

0 5 10

-.5

0

.5

1D1LRES

Correlogram

0 5 10

-.5

0

.5

1D4LRES

Correlogram

0 5 10

-.5

0

.5

1DD4LRES

Spanish Non Residential Building graphics (Serie 3)

1990 1995 2000

12.6

12.8

13

13.2LNRES

1990 1995 2000

-.2

0

.2 D1LNRES

1990 1995 2000

-.2

0

.2D4LNRES

1990 1995 2000

-.1

0

.1 DD4LNRES

Spanish Non Residential Building correlograms (Serie 3)

Correlogram

0 5 10

-.5

0

.5

1LNRES

Correlogram

0 5 10

-.5

0

.5

1D1LNRES

Correlogram

0 5 10

-.5

0

.5

1D4LNRES

Correlogram

0 5 10

-.5

0

.5

1DD4LNRES

Spanish Civil Work graphics (Serie 4)

1990 1995 2000

e+06

e+06

e+06

e+06OC

1990 1995 2000

-.1

0

.1

.2D1LOC

1990 1995 2000

-.1

0

.1

.2D4LOC

1990 1995 2000

-.1

0

.1DD4LOC

Spanish Civil Work correlograms (Serie 4)

Correlogram

0 5 10

.25

.5

.75

1LOC

Correlogram

0 5 10

-.5

0

.5

1D1LOC

Correlogram

0 5 10

-.5

0

.5

1D4LOC

Correlogram

0 5 10

-.5

0

.5

1DD4LOC

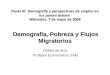

Monthly Spanish Consumption of Cement graphics (Serie 5)

1980 1985 1990 1995 2000

2000

3000

CEMENT

1980 1985 1990 1995 2000

-.2

0

.2DLCEMENT

1980 1985 1990 1995 2000

-.25

0

.25

.5D12DLCEMENT

1980 1985 1990 1995 2000

-.5

0

.5DD12DLCEMEN

Monthly Spanish Consumption of Cement correlograms (Serie 5)

Correlogram

0 5 10 15 20 25

.25

.5

.75

1LCEMENT

Correlogram

0 5 10 15 20 25

-.5

0

.5

1DLCEMENT

Correlogram

0 5 10 15 20 25

-.5

0

.5

1D12DLCEMENT

Correlogram

0 5 10 15 20 25

-.5

0

.5

1DD12DLCEMEN

Japanese Cement Consumption graphics (Serie 6)

60 65 70 75 80 85 90 95 100

-10

0

10

20CEM

60 65 70 75 80 85 90 95 100

0

5

10PIB

60 65 70 75 80 85 90 95 100

-10

0

10

20 CT

Japanese Cement Consumption correlograms (Serie 6)

Correlogram

1 2 3 4 5 6 7 8

.5

1CEM

Correlogram

1 2 3 4 5 6 7 8

.5

1PIB

Correlogram

1 2 3 4 5 6 7 8

.5

1CT

The Stationary Parameters (I)

• Time dependency in stationary data is reflected in:– the correlation parameters (ρ1 , ρ2 ,......) of the

joint pdf f(w1,w2,...,wt) or – the parameters of the conditional mean in the

conditional pdf f(wt/wt-1,wt-2,....)which is the same for every wt by the stationarity property.

The Stationary Parameters (II)

qϑϑϑφφφ ν ,.....,,,,....,, 2121

tststt

ts

st

aawwaLwL

+−=−=−

−− ϑφϑφ

11

1 )1()1(

stst aw −− − ϑφ 11

These parameters are

EXAMPLE

The conditional mean is

Determination of the stationary parameters

• For forecasting purposes what matters is the conditionalmean.

• Procedure:– look at the time dependency in the data by estimating the correlogram and

the partial correlogram.– From these estimations specify an ARMA model.

• Method for initial especification of an ARMA model.– By careful examination of the correlogram and partial correelogram an

expert can propose an ARMA model for the time series in question.– There are also automatic procedures which are quite reliable like TRAMO

or SCA.

Model Users and the specification of ARIMA models

• It is important that they understand well the specification of the evolutivity parameters and it is advisable that they get experience in doing these especifications, because those parameters determine the medium-term forecasts.

• For the stationary parameters it is enough that the user could understand the type of time dependency in the model provided by reliable computer programs.– Long or short dependency– seasonal dependency

Practical rules to determine the orders of an ARMA multiplicative model (I)

�Divide the correlogram and partial correlogram in three parts:– REGULAR CORRELOGRAM: formed by the first

values of the correlogram.– SEASONAL CORRELOGRAM: formed by the values

at seasonal lags.– INTERMEDIATE CORRELOGRAM: formed by the

remaining values

Practical rules to determine the orders of an ARMA multiplicative model (II)

� Remember the properties of the autocorrelation function in MA(q), AR(p) and ARMA(p,q):

P R O C E S S A C F P A C F N O T E

M A ( q ) C u t t in g p o in t a tk = q

N o c u t t in gp o in t

U s e f u l t oc a p t u r e s h o r td e p e n d e n c y

A R ( p ) N o c u t t in g p o in t C u t t in g p o in ta t k = p

U s e f u l t oc a p t u r er e g u la r y

d e c r a s in g lo n gd e p e n d e n c y

A R M A ( p , q ) N o c u t t in g p o in t N o c u t t in gp o in t

U s e f u l t oc a p t u r e

d e c r e a s in glo n g

d e p e n d e n c y .T o a v o id

c o m m o n f a c t o rp r o b le m s d on o t u s e m o r e

Practical rules to determine the orders ofan ARMA multiplicative model (III)

� Take the regular correlogram– Is there a cutting point?

• YES: Look at which lag is the cutting point.Say it occurs at lag q.Then specify an MA(q).

• NOT: Look at the partial correlogramIs there a cutting point?

» YES: Look at which lag is the cutting point.Say it occur at point p.Then specify an AR(p).

» NOT: Specify an ARMA (1,1)

Practical rules to determine the orders ofan ARMA multiplicative model (IV)

� Take the seasonal correlogram– Apply same rules as point 3 and specify on:

– MA(Q) if there is a cutting point in lag Q·S of the correlogram.

– AR(P) if there is not a cutting point in the correlogram and there is one in the partial correlogram at lag P·S.

– For series with long cycles you could specify on AR(2, 1)

Practical rules to determine the orders ofan ARMA multiplicative model (V)

� Take the Intermediate correlogram to confirm previous decisions.– For multiplicative ARMA models the intermediate

autocorrelation function take values as:

where the subscripts mean:(I): intermediate ACF(R): regular ACF(S): seasonal ACF

)()()(·

)(· · S

hSR

KI

KShI

KSh ρρρρ == −+

Practical rules to determine the orders ofan ARMA multiplicative model (VI)

� In applying previous rules you could have reasonable doubts:– make a decision on which could be the

most reasonable values for p, q, P and Q, and

– make a use of all other possibilities. We will consider them at the diagnostic check stage.

ExamplesStationary transformation for Spanish Non Residential

Building correlogram and partial correlogram

ExamplesStationary transformation for Spanish Civil Works

correlogram and partial correlogram

MAIN RESULTS FROM ESTIMATION PROGRAMS

• Estimation of parameters φj , Φh , θj and Θh whith their corresponding variances and correlations between then.

• Estimation of the innovations a

TESTS ON PARAMETER ESTIMATES AND POSSIBLE ALTERNATIVE MODELS

� Apply t-tests to each one of the parameter (τj) to testH0: τj = 0

If t-test less than 2 do not reject H0 and simplify the model eliminating this parameter

� Look at the roots of the MA(q) polynomial

∏=

−=θq

1jjq )LH1()L(

If one Hj is close to one it can be canceled with a difference operator obtaining a simplified model.

∏=

−=φp

1jjp )LG1()L(

� Look at the roots of the AR(p) polynomial

If one Gj is close to unity you could fix it at value one reducing the order of φ(L) to (p-1) and increasing the number of differences to (d+1).

� Look at the correlations between the parameters φj , Φh, θj and ΘhIf you find correlations grater than 0.9 in absolute valueeliminate one of two parameters having large correlation.

MISSPECIFICATION TESTS BASED ON THE ESTIMATED INNOVATIONS

• If the model is correct the innovations should be white noise.

• There we can apply different test to the innovations to ensure that they are white noise.

• If from these tests results that innovations are not white noise the initial model should be modified and the results of the test will give an indication in order to formulate a new specification.

TESTING FOR A ZERO MEAN IN THE INNOVATIONSIf your model does not include a constant, the mean of the

estimared innovations can be significantly different from zero indicating that you need to modify the I(d,m) specification.

Tσσ =ˆ

Test Ho: µ = 0

By a t-test asmeanthisofdeviationstandard

sinnovationestimatedofmean)ˆ(t =µ

2)ˆ( >µtReject Ho if in absolute value.

•If you reject Ho the initial I(d,m) specification is wrong. Consider to:a) apply some segmentationb) increase d by onec) increase m in by one

TESTING FOR CORRELATION BETWEEN THE ESTIMATED INNOVATIONS

by t test.

If you reject Ho for K=1,2,3…s, or 2s your initial model is wrong and you need to modify it.

If the estimated innovations are white noise then their autocorrelations must not be significatly different from zero.

Test Ho: ρa(k) = 0 , ∀ K

Reject Ho and apply (A).

(A) The best way to modify the model is by specifying it according with the doubts that wenote at the specifications stage.

Test Ho: { ρ a(1) , ρa(2) ,.., ρa(s+2) } = 0

By Ljung-Box test (Qs+2)2

2s2sQIf ++ χ>

Even when the initial model has passed the test on the estimation results and on the innovation, still the model can be insatisfactory because that model was just a reasonable choice done at the specification.

• Estimate all the reasonable alternative models including theoriginal model choose the one with less AIC value.

• If you have not douhts about the initial model try alternativesby substituting p by (p+1) ,or q by (q+1) or P by (P+1), or Q by (Q+1). Estimate these alternative including the original model and choose the one with less AIC value.

FORMULATE OF ALTERNATIVE MODELS