Embed Size (px)

Citation preview

#2001-10 June 2001

Current Issues in the Pricing of Telecommunications Services

By

Professor David Gabel, Ph.D. Queens College

AARP is a nonprofit, nonpartisan membership organization for people 50 and over. We provide information and resources; advocate on legislative, consumer, and legal issues; assist members to serve their communities; and offer a wide range of unique benefits, special products, and services for our members. These benefits include AARP Webplace at www.aarp.org, Modern Maturity and My Generation magazines, and the monthly AARP Bulletin. Active in every U.S. state and territory, AARP celebrates the attitude that age isn�t just a number -- it�s about how you live your life.

The Public Policy Institute, formed in 1985, is part of the Public Affairs Group of AARP. One of the missions of the Institute is to foster research and analysis on public policy issues of importance to older Americans. This paper represents part of that effort.

The views expressed herein are for information, debate, and discussion and do not necessarily represent the formal policies of AARP.

Public Policy Institute

D17416. © 2001. AARP. Reprinting with permission only.

AARP 601 E Street, NW, Washington, DC 20049

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 2

Acknowledgments

This paper has benefited greatly from the able assistance of Scott Kennedy, Research Assistant, Queens College. The author and project officer are also grateful for the helpful suggestions provided by Dr. Johannes M. Bauer, Associate Professor in the Department of Telecommunications at Michigan State University; William Gillis, Commissioner, Washington Utilities and Transportation Commission and; Michael Travieso, People�s Counsel, Maryland Office of the People�s Counsel. Within AARP, Susan Weinstock and Coralette Marshall of State Affairs and Jeff Kramer of Federal Affairs provided thoughtful review comments. Special thanks go to Gabriel Montes, AARP Public Policy Institute, for preparing the report for publication.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 3

Table of Contents

Foreword............................................................................................................................. 5

Executive Summary .......................................................................................................... 7 Introduction .............................................................................................................................. 7

Purpose and Methodology .................................................................................................... 7

Principle Findings...................................................................................................................... 8

Conclusion .............................................................................................................................. 10

Introduction...................................................................................................................... 11

I. The Pricing of Telecommunications Services in Competitive Markets ............ 12 The Access Cost Debate ................................................................................................... 12

What Tariffs Indicate About Pricing Under Competition............................................... 14

Retail Services Pricing ...........................................................................................................14

Carrier Access Charges .......................................................................................................17

II. Pricing in Other Network Industries ....................................................................... 21 Cable Telephony in the United Kingdom (UK)................................................................ 21

Relationship Banking .......................................................................................................... 25

The Mobile Phone Market.................................................................................................. 25

Roaming Fees ........................................................................................................................27

Pricing of Access to ATM Networks .................................................................................. 27

III. State Regulatory Responses to Structural Changes: Divestiture vs. The Telecommunications Act of 1996.......................................... 29

IV. Issues Surrounding Basic Local Telephone Service ............................................ 34 Is Basic Local Telephone Service Subsidized?................................................................ 36

Conclusion ....................................................................................................................... 40

Glossary of Terms ............................................................................................................ 41

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 4

Tables and Figures

Table 1: Comparative Vertical Feature Prices and Costs ........................................ 15

Table 2: AT&T of CO: Local Service Offering .............................................................. 16

Table 3: AT&T of CO: Feature Package Options........................................................ 16

Table 4: AT&T, US WEST Switched Access Rates......................................................... 18

Table 5: CLEC Switched Access Rates........................................................................ 18

Table 6: Vertical Feature Prices of Telewest............................................................... 22

Table 7: Total Average Return on Regulated Investment for the 150 Largest Telephone Companies in the US.................................................................. 33

Figure 1: Annual Trend in Basic Local Service Charge 1980-1997 ......................... 30

Figure 2: Comparison of Growth Rates in Minutes of Use ........................................ 31

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 5

Foreword

As telecommunications markets have become increasingly deregulated, a number of economists and telecommunications providers have argued that value-of-service pricing�a type of pricing structure that reflects the presumed value that different classes of customers place on having access to the telephone network�will not be sustainable in a competitive market. They contend that the emergence and continued growth of competitive service providers will force telephone companies to price individual telecommunications services at cost.

Actions by federal regulators indicate that they generally support the proposition that value-of-service pricing is not sustainable in a competitive market because competition inevitably will lead companies to price services at a level that is equal to the marginal cost of production. Last year, in an order intended to smooth the transition to competitive pricing for telecommunications services, the Federal Communications Commission (FCC) changed the manner in which large local telephone companies recover the costs of building and maintaining the local telephone network. In accordance with a plan proposed by a coalition of local and long distance telephone companies, the FCC combined two existing phone bill line item charges, the pre-subscribed interexchange carrier charge (PICC) and the subscriber line charge (SLC) to create one line-item charge on local telephone bills. The industry coalition contends that this restructuring plan establishes a more rational pricing structure for telecommunications services. An end-user charge based on the cost of producing the service is desirable, according to the proponents of this plan, because it allows high-volume toll users to pay less for existing services. They further assert that costs should be recovered in the same manner that they are incurred.

In this paper, Dr. David Gabel of Queens College contends that in unregulated markets prices are not established in the simplistic manner endorsed by the FCC. Instead, unregulated firms establish price structures and levels that reflect the value of using the product. Indeed, many consumer advocates, including AARP, have argued that a subscriber line charge is inconsistent with competitive behavior and harmful to consumers; that is, as a guaranteed revenue stream, the SLC is insulated from competitive pressures, which otherwise could lower or eliminate the price customers pay for access to the telephone network.

One way to evaluate these conflicting views of pricing behavior and consumer welfare in an increasingly competitive telecommunications market is to examine pricing practices and consumer welfare in other, more competitive markets. In this paper, Dr. Gabel pursues such a strategy. He examines the current pricing practices of Competitive Local Exchange Carriers (CLECs), companies in the cable telephony market of the United Kingdom, and firms in the banking and mobile telephone industries in the United States. He also explores some of the arguments that the local telephone companies have made in support of cost-based pricing structures as well as

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 6

how state regulators have reacted to these proposals.

Dr. Gabel�s analysis provides a detailed understanding of the actual pricing behavior of firms in competitive markets and how this behavior affects the ability of consumers to access desired services. Such knowledge is critical to the development of telecommunications policies that will assure all consumers reasonable and affordable access to and the benefits of competitive markets.

Christopher A. Baker Project Officer/Senior Policy Advisor AARP Public Policy Institute

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 7

Executive Summary

Introduction For over two decades, many economists and incumbent telephone companies have criticized the current pricing structure for telecommunications services as inefficient and unsustainable in a competitive market. They have argued that the current system, in which prices for telecommunications services are based on the presumed value customers place on those services (value-of-service pricing) rather than on the cost of providing them, would not be sustainable once competition was introduced into the market. Indeed, despite increased competition in local telecommunications markets, encouraged by the Telecommunications Act of 1996 (TA96), the phone companies have supported the imposition of an increased subscriber line charge via regulation for providing network access. Experience in other deregulated markets, both in the United States and abroad, raises serious questions about the appropriateness of government-mandated access charges and casts doubt on the validity of the phone companies� view that value-of-service pricing is inefficient and unsustainable. In fact, research on pricing strategies indicates that firms rarely set their prices equal to the cost of production. Rather, they seek to differentiate themselves from their competitors by offering services bundled and priced to meet a wide range of consumer needs.1

Purpose and Methodology This report seeks to evaluate claims that value-of-service pricing is inefficient and unsustainable by using a comparative analysis and case study approach to examine the actual pricing behavior of firms in the local telecommunications market and in other, more competitive, networked industries. The first section of the report examines current pricing practices of Competitive Local Exchange Carriers (CLECs). The second section describes and compares the pricing strategies of companies in the cable telephony market of the United Kingdom and the banking and mobile telephone industries in the United States. Section three compares the pricing of telecommunications services following AT&T�s divestiture with pricing decisions made after the passage of TA96. The final section of the report analyzes the contention made by the Incumbent Local Exchange Carriers (ILECs) and their supporters that residential service is a subsidized service whose rates need to be rebalanced upwards in order to 1See, for example, John S. Ying and Theodore E. Keeler, �Pricing in a Deregulated Environment: The Motor Carrier Experience,� Rand Journal of Economics, 22(2) (Summer 1991), pp. 264-273; and Severin Borenstein and Nancy L. Rose, �Competition and Price Dispersion in the U.S. Airline Industry,� Journal of Political Economy 102 (1994): 653- 683. Firms that have never been subject to price regulation, such as online travel agents, also use value-of-service pricing. Clemons, Hann, and Hitt have documented how online travel agents segment customers in order to price discriminate. �The Nature of Competition in Electronic Markets: An Empirical Investigation of Online Travel Agent Offerings,� Eric K. Clemons, Il-Horn Hann, and Lorin M. Hitt, Department of Operations and Information Management, working paper, Wharton School of Business, June 1999. The assertion that price discrimination is found in many industries, not just regulated industries, is consistent with theoretical writings on this topic. As noted by Borenstein and Rose, �[T]heoretical works...indicate...that price discrimination may increase as a market moves from monopoly to imperfect competition.� Id. P.658.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 8

eliminate these subsidies and to recover the cost of providing the service.

Principal Findings The traditional monopoly providers of local telephone service typically price their services based on the customer�s perceived value of the service rather than on the cost of providing that service. However, these companies and many economists have long contended that this pricing structure would not be sustainable in a telecommunications market that was fully open to competition. This paper demonstrates that such a contention is based on an inaccurate or inadequate understanding of the pricing behavior of firms under competitive conditions.

• The Pricing of Telecommunications Services in Competitive Markets The current pricing practices of Competitive Local Exchange Carriers (CLECs) suggest that, contrary to the predictions of economists such as Alfred Kahn, the existence of competition does not drive the price of individual services to cost. Moreover, the data collected for this report show that CLECs are pricing services such as Caller ID and Call Waiting at levels that far exceed their marginal costs. In fact, rather than stimulating a race to the marginal cost of production, local exchange competition has encouraged a complex and rich array of strategic pricing initiatives, such as value-of-service pricing and product bundling, that the CLECs utilize to segment their target markets.

• Pricing in Other Network Industries The cable telephony market in the United Kingdom (UK), the banking and mobile telephone industries in the United States, and the pricing of access to ATM networks provide further illustration that the actual pricing behavior of firms in networked industries is quite different from that predicted by the utility economists. While Kahn and other economists contend that competition drives prices to the cost of providing each service, the data in this report show that companies in these deregulated markets recognize that a firm�s overall profitability is tied to the total profits generated from its customers and not necessarily to the profits created by a particular product or service. In this regard, rival firms respond to competition by lowering or eliminating the price of customer access and then recouping this cost through the provision of multiple products and pricing options. Mobile telephone service providers, for example, often discount or give away the mobile telephone in order to gain network subscribers. With a greater number of subscribers, mobile providers earn more profits from commissions on airtime and increase the value of their network to existing subscribers.

• State Regulatory Responses to Structural Changes: Divestiture vs. The Telecommunications Act of 1996 Following the divestiture of AT&T in 1984 and again after the passage of the Telecommunications Act of 1996, the Incumbent Local Exchange Carriers (ILECs)

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 9

expressed concern that increased competition would lead to significant local exchange bypass�the use of alternative communications facilities or services that circumvent the facilities or services provided by the local telephone company�which would endanger the financial stability of the telephone networks. After AT&T�s divestiture in 1984, state utility commissions acted to address the perceived threat by rebalancing rates�a process in which a commission orders an ILEC to increase local rates and decrease the fees (switched access rates) that long distance companies pay to the ILEC for carrying their customers� calls over the local telephone network. In contrast, state commissions, in general, have not acted to rebalance rates since the passage of TA96.

Several factors may explain this difference in regulatory behavior. Following the enactment of TA96, the ILECs have been hesitant to advocate for rate rebalancing, probably because they believe that such restructuring of rates might bring more competitive entrants into the local market. Moreover, strong ILEC earnings over the past few years and the fact that local exchange rates have been increasing over the past decade while the average economic cost per line has fallen may have convinced state commissions that efforts to rebalance rates are not needed.

• Issues Surrounding Basic Local Telephone Service The ILECs state that the revenue from basic residential telephone service is less than the sum of the cost of access to the local telephone network and the cost of providing local exchange service, which would tend to indicate that a subsidy exists. This comparison is inappropriate as it ignores the fact that the local telephone network, of which the local loop is a part, is a shared facility used in the provision of multiple services, including basic local telephone service, access to toll services, and other telecommunications services. This means that the cost of the loop is a shared cost of all telecommunications services and therefore should not be assigned to one product.

Any serious effort to test the existence of a subsidy to residential customers should follow several important guidelines. First, such an analysis should determine which costs would be avoided if residential service were discontinued and business service were maintained. In this regard, the total incremental cost of residential loops is likely less than the fully allocated cost of all loops. Second, the analysis should take into account that a substantial portion of telecommunications traffic is between business and residential customers and thus the revenue from business services depends, in part, on residential service. An accurate calculation of the revenues associated with residential service requires consideration of this interaction. Finally, because the estimated cost of a loop can vary dramatically depending on the whether reasonable or unreasonable input values are employed, any analysis should ensure that all assumptions regarding the cost-of-money, depreciation lives, and other cost

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 10

inputs are reasonable and accurate.

Conclusion The evolving telecommunications pricing structure has little to do with the positions traditionally advocated by utility economists. They predicted, for example, that competitive entry into the telecommunication�s market would eliminate value-of-service pricing. This has not happened. Instead, in the more mature competitive markets, value-of-service pricing has become more nuanced and complex.

Competition in the telecommunications� markets has caused firms to seek market share, and to differentiate themselves from their competitors, through the introduction of innovative pricing packages offering telecommunications services bundled to suit a diverse range of consumer preferences. Network access is just a part of the bundle. The marketing departments of telecommunications firms understand that consumers want products and services that offer them value. Network access, divorced from network services, has no perceived value. Thus, consumers have no interest in purchasing network access as a stand-alone service.

By advocating for increased subscriber line charges via regulatory fiat, the ILECs and their allies are seeking an outcome that is incompatible with competitive market behavior and which would be detrimental to consumer interests. In the future, policymakers should be focused on adopting the type of pricing structures that are observed in competitive markets. Firms participating in competitive markets do not erect high rate barriers that discourage customers from signing up for service, rather retail prices are established that reflect the value of using the product.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 11

Introduction

Many utility economists and incumbent telephone companies have criticized the current pricing structure for telecommunications services as inefficient and unsustainable in a competitive market. They have long argued that basing prices for telecommunications services on the value customers place on those services (value-of-service pricing), rather than on the cost of providing them, would not be sustainable once competition was introduced into the market. With the passage of the Telecommunications Act of 1996 (TA96), competition in the local telecommunications services market is slowly becoming a reality for more and more local phone customers around the country. Rather than confirming traditional economic arguments, this new competitive reality challenges the criticisms and policy pronouncements of incumbent telephone companies and many utility economists concerning the �inefficiencies� in the pricing of telecommunications services.

This report evaluates these policy pronouncements by examining the pricing behavior of firms in the local telecommunications market and in other, more competitive, networked industries. The first section of the report addresses current pricing practices of Competitive Local Exchange Carriers (CLECs). The second section explores the pricing strategies of companies in the cable telephony market of the United Kingdom and the banking and mobile telephone industries in the United States. Section three compares the pricing of telecommunications services following AT&T�s divestiture with pricing decisions made after the passage of the Telecommunications Act of 1996. The final section of the report evaluates the contention that basic local telephone service is subsidized.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 12

I. The Pricing of Telecommunications Services in Competitive Markets

The Access Cost Debate Proponents of increased charges for local telephone service assert that the fixed costs of customer access to the local network�the cost of providing the loop�should not be recovered through usage charges. Currently, the intrastate and interstate common carrier line charges (CCLC) recover a portion of the loop�s cost through the price of toll services. The CCLC is levied as a per-minute charge on IXCs for the carriage of interexchange traffic over the local network. The purpose of the CCLC is to recover a portion of the loop cost, a cost which is incurred by a local exchange carrier in providing local, toll, and any other switched, voice, data, or broadband service. Because a portion of this cost is recovered from toll service, customer access charges are at levels lower than would otherwise be obtained by recovering the loop cost entirely from those charges. This type of pricing scheme is considered to be inefficient by economists such as Alfred Kahn. These economists believe that the CCLC discourages use of long-distance calling and encourages over-consumption of network access, resulting in inefficient utilization of society�s scarce resources.2 They also believe that, because the cost of the network connection is independent of the volume of calls, it is inefficient to recover any portion of the loop cost in the price of a marginal toll call. Efficiency is a standard that Kahn and other economists adopt for judging the efficacy of a pricing structure. They maintain that society�s welfare is enhanced when economic efficiency is raised.3 They further contend that efficient prices are prices that are set

2See, for example, Alfred Kahn and William Shew, �Current Issues in Telecommunications Regulation: Pricing,� Yale Journal on Regulation 4: 191, 202 (1987); and Alfred Kahn, �The Road to More Intelligent Telephone Pricing,� Yale Journal on Regulation 1: 139, 142-143, 155 (1984); and David L. Kasserman and John W. Mayo, �Cross-Subsidies in Telecommunications: Roadblocks on the Road to More Intelligent Telephone Pricing,� Yale Journal on Regulation 11: 119, 135 (1994). Some of the �economic� arguments for higher customer access charges are unconvincing. For example, Mayo and Kasserman assert that the fixed costs of a firm should be recovered exclusively through a fixed customer charge. When they write �fixed costs, by definition, bear no relationship to the volume of usage,� the logical correlative statement would be neither usage costs nor access costs are fixed costs attributable to providing customer access. Rather than making this statement, they conclude that all fixed costs should be recovered through the price of customer access. Id., p. 124. 3A fundamental tenet of economics is that efficient pricing is obtained by pricing products at the marginal cost-of-production and that society's welfare is maximized when products are priced at this level. In the case of vertical services, such as call waiting, and exchange access pricing the argument goes as follows: If customers are charged more for call waiting, than the cost society incurs in providing the product, the equilibrium level of call waiting output will be less than the amount that maximizes society's welfare. Consumers will purchase call waiting service up to the point that the additional benefit equals the additional cost. If the price for call waiting service is set so that it exceeds the costs that society incurs producing the service, consumers will stop purchasing the service at a level of output where the value to a consumer is less than the cost society incurs in making the service available. Economists believe that society's welfare would be maximized if the level of output is at the point where the value of the last service ordered is equal to the cost society incurs in providing the service. One problem with this standard approach to welfare analysis is that it assumes that a millionaire and a homeless person obtain the same marginal utility from an additional dollar of income. In the telecommunications context, this approach assumes that the social welfare benefits to be gained by reducing the price of vertical features will offset any loss in social welfare caused by customers dropping off the network as a result of increased prices for basic services. An alternative to this approach to measuring social welfare is offered by John Wenders, who suggests measuring the social benefit of different policies by judging them based on an evaluation of individual behavior. Wenders points out that relying on individual decisions, rather than some arbitrary welfare function, is the essence of competitive markets: �But the desirability of the competitive approach is not that it maximizes the sum of the surplus, but that it maximizes individual voluntary exchanges, each of which leave both parties better off.� Wenders, John T., �Two Views of Applied Welfare Analysis: The Case of Local Telephone Service Pricing�, Southern Economic Journal 57 (1989), p. 340.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 13

equal to the marginal cost-of-production and are the inevitable outcome of competition. It is this conviction that motivates their argument that regulators should recover the non-traffic sensitive costs of the local exchange�the customer loop�exclusively through local exchange access rates, regardless of the political unpalatability of this option. These economists assert that as telecommunications markets become increasingly deregulated, competitive pressures will cause the price of exchange access to rise. �The one thing that is certain is that the new regime of competition, on the one hand, and the perpetuation of the old regime of inefficient pricing, on the other, are fundamentally incompatible; one or the other is going to have to give.�4 Kahn, et al., are firmly convinced that competition �...inexorably drives prices to marginal costs [footnote omitted].�5 However, they present little or no evidence to support this proposition.6

The proposition that prices will be driven to marginal cost is only true where certain theoretical conditions hold, conditions rarely observed in actual markets. As is currently illustrated by the pricing of services on the Internet, having a large number of suppliers and customers is not sufficient for eliminating price discrimination and driving all product prices to their respective costs. If, for example, there is a cost associated with searching for price information, we are unlikely to observe a competitive outcome because seeking out the best price may be costly.7 Furthermore, in most markets we observe oligopolistic rather than competitive outcomes. In such markets, firms strategic pricing decisions are much more complex than the simplistic notion of prices being driven towards cost.8

Kahn and others do not account for the fact that �...people do not make purchases by evaluating the products alone but by evaluating the entire purchase opportunity.�9

4Kahn, �More Intelligent Telephone Pricing,�pp. 150, 151 (quote). 5Kasserman, David L. and John W. Mayo, �Cross-Subsidies in Telecommunications: Roadblocks on the Road to More Intelligent Telephone Pricing�, Yale Journal on Regulation 11 (Winter 1994): 137. 6In fact, a recent paper has presented a fairly compelling argument for rejecting this proposition. �The historical evidence shows that, as communication systems have grown and technology has advanced, the balance has moved towards catering to user preferences. The need to extract maximal revenues and to maximize efficiency of the infrastructure have assumed secondary roles�. Therefore, pricing on the basis of marginal costs is becoming untenable, and it becomes necessary to price on the basis of customers� willingness to pay. That calls for quality differentiation and price discrimination approaches such as those of airlines and Coca Cola.� (Source: Odlyzko, Andrew, Internet Pricing and the History of Communications, http://www.research.att.com/~amo, p.5.) 7See, for example, Eric K. Clemons, Il-Horn Hann, and Lorin M. Hitt, �The Nature of Competition in Electronic Markets: An Empirical Investigation of Online Travel Agent Offerings,� Department of Operations and Information Management, working paper, Wharton School of Business, June 1999; Organization for Economic Co-Operation and Development, Electronic Commerce: Prices and Consumer Issues for Three Products: Books, Compact Discs, and Software, DSTI/ICCP/IE(98)4/Final. 8See, for example, Thomas T. Nagle and Reed K. Holden, The Strategy and Tactics of Pricing; A Guide to Profitable Decision Making, Prentice-Hall, Inc., 1987. 9Thomas T. Nagle and Reed K. Holden, The Strategy and Tactics of Pricing; A Guide to Profitable Decision Making, Prentice-Hall, Inc., 1987, p. 168. Southern New England Telephone expressed a similar view to the Connecticut Department of Public Utilities: �competitors will look at the total basket of services a customer buys, not any single service, in making a decision to market to that customer. Put differently, it is the profitability of individual customers, not individual services, that is attractive to competition.� Response of Southern New England Telephone, TE052 Supplemental Response, October 13, 1995, Application of the Southern New England Telephone Company for Financial Review and Proposed Framework for Alternative Regulation, Docket 95-03-01.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 14

Firms recognize this and so take a more nuanced approach to pricing, considering it as much a function of strategic positioning and marketing as it is of cost recovery. Market segmentation through bundled service offerings is evidence of such pricing and marketing strategies. The next sections of the paper will present data illustrating this more nuanced and strategic approach to the pricing of telecommunications products and network access in competitive markets.

What Tariffs Indicate About Pricing Under Competition Kahn has stated that call waiting, caller ID, and other vertical services are �overpriced�, and therefore their rates are economically inefficient.10 Because of the high charges, he maintains that obtaining large contributions from vertical and access services will become �impossible [original emphasis]. So long as competitors can now assemble the network elements necessary to provide such currently overpriced services at cost [original emphasis] ��those inflated prices cannot survive.�11

The following review of various tariff filings indicates that, contrary to the assertions of Kahn and others, value-based prices for vertical features and access charges that recover non-traffic sensitive costs do occur in unregulated telecommunications markets. The entrants pricing decisions illustrate that as in other industries, entry does not drive the price of individual services to cost. These filings also illustrate how firms are strategically bundling services into packaged offerings for their customers.

Retail Services Pricing

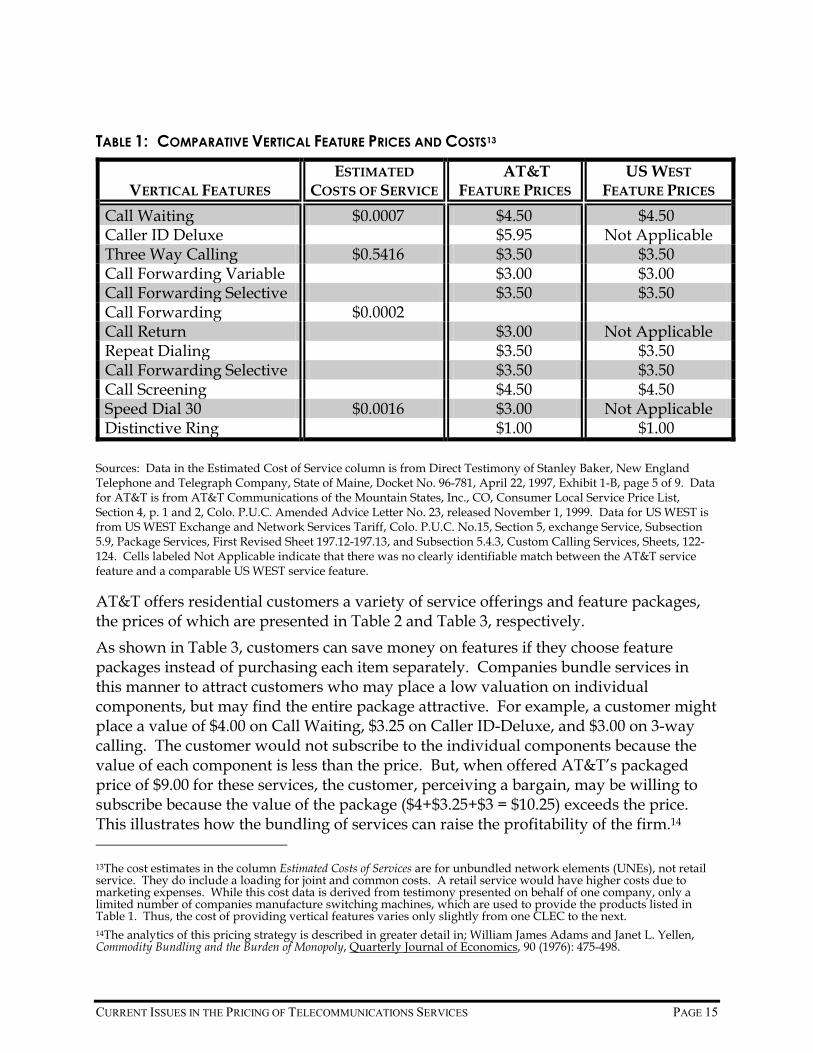

AT&T, operating as AT&T Communications of the Mountain States, Inc., filed a market trial tariff in November 1999 for the introduction of its facilities-based residential local service in the Denver, Colorado area. AT&T filed this tariff as a competitive local exchange carrier (CLEC) and so is not subject to regulation in the Denver market. The data found in Table 1, below, indicates that both US WEST and AT&T charge identical prices for their vertical features, prices well in excess of the incremental costs of providing them. The fact that AT&T, as a new entrant into the Denver residential services market, has chosen vertical feature prices comparable to those charged by US WEST suggests that the presence of a market rival may not drive the prices of these features down to their marginal costs.12

10Kahn, Alfred, Letting Go: Deregulating the Process of Deregulation (East Lansing: Michigan State University Public Utilities Papers, 1998), at 12-14, 115. Mayo and Kasserman have also made the claim that value-of-service pricing is not sustainable under competition. See Kasserman and Mayo, �Telecommunications Cross-Subsides,� pp. 128-29. 11Ibid., p.114 12At this early stage of competition, AT&T�s pricing strategy could be one of umbrella pricing, discussed more fully on page 21, and not reflective of the eventual equilibrium outcome at which these services will be priced. Telecommunications analysts generally reject the umbrella hypothesis and instead forecast a continuation of the current high prices. This is reflected for example, in the Yankee Group�s forecast that �revenues from services like call waiting, caller ID, call forwarding and three-way calling are expected to climb from $6.5 billion in 1998 to approximately $10 billion in 2003�� Joseph Bonocore, Commanding Communications: Navigating Emerging Trends in Telecommunications (New York: John Wiley & Sons, 2001), p.138.

TABLE 1: COMPARATIVE VERTICAL FEATURE PRICES AND COSTS13

Sources: Data in the Estimated Cost of Service column is from Direct Testimony of Stanley Baker, New England Telephone and Telegraph Company, State of Maine, Docket No. 96-781, April 22, 1997, Exhibit 1-B, page 5 of 9. Data for AT&T is from AT&T Communications of the Mountain States, Inc., CO, Consumer Local Service Price List, Section 4, p. 1 and 2, Colo. P.U.C. Amended Advice Letter No. 23, released November 1, 1999. Data for US WEST is from US WEST Exchange and Network Services Tariff, Colo. P.U.C. No.15, Section 5, exchange Service, Subsection 5.9, Package Services, First Revised Sheet 197.12-197.13, and Subsection 5.4.3, Custom Calling Services, Sheets, 122-124. Cells labeled Not Applicable indicate that there was no clearly identifiable match between the AT&T service feature and a comparable US WEST service feature.

VERTICAL FEATURES

ESTIMATED COSTS OF SERVICE

AT&T FEATURE PRICES

US WEST FEATURE PRICES

Call Waiting $0.0007 $4.50 $4.50 Caller ID Deluxe $5.95 Not Applicable Three Way Calling $0.5416 $3.50 $3.50 Call Forwarding Variable $3.00 $3.00 Call Forwarding Selective $3.50 $3.50 Call Forwarding $0.0002 Call Return $3.00 Not Applicable Repeat Dialing $3.50 $3.50 Call Forwarding Selective $3.50 $3.50 Call Screening $4.50 $4.50 Speed Dial 30 $0.0016 $3.00 Not Applicable Distinctive Ring $1.00 $1.00

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 15

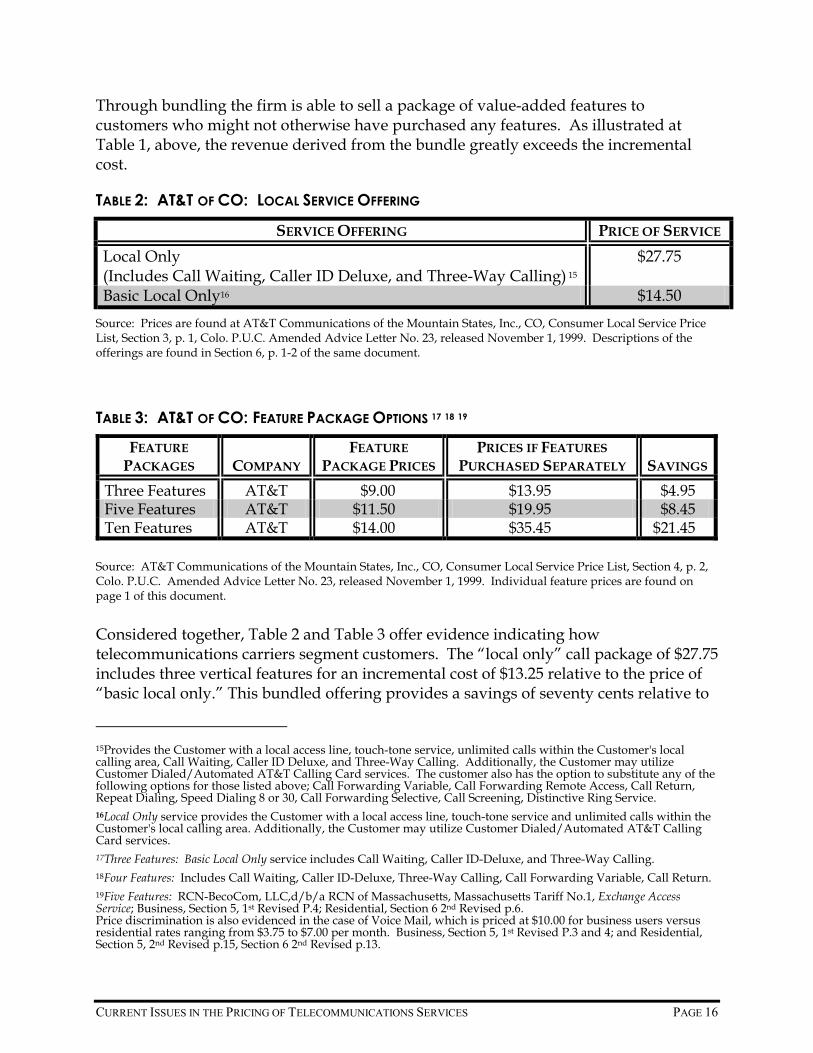

AT&T offers residential customers a variety of service offerings and feature packages, the prices of which are presented in Table 2 and Table 3, respectively. As shown in Table 3, customers can save money on features if they choose feature packages instead of purchasing each item separately. Companies bundle services in this manner to attract customers who may place a low valuation on individual components, but may find the entire package attractive. For example, a customer might place a value of $4.00 on Call Waiting, $3.25 on Caller ID-Deluxe, and $3.00 on 3-way calling. The customer would not subscribe to the individual components because the value of each component is less than the price. But, when offered AT&T�s packaged price of $9.00 for these services, the customer, perceiving a bargain, may be willing to subscribe because the value of the package ($4+$3.25+$3 = $10.25) exceeds the price. This illustrates how the bundling of services can raise the profitability of the firm.14 13The cost estimates in the column Estimated Costs of Services are for unbundled network elements (UNEs), not retail service. They do include a loading for joint and common costs. A retail service would have higher costs due to marketing expenses. While this cost data is derived from testimony presented on behalf of one company, only a limited number of companies manufacture switching machines, which are used to provide the products listed in Table 1. Thus, the cost of providing vertical features varies only slightly from one CLEC to the next. 14The analytics of this pricing strategy is described in greater detail in; William James Adams and Janet L. Yellen, Commodity Bundling and the Burden of Monopoly, Quarterly Journal of Economics, 90 (1976): 475-498.

Through bundling the firm is able to sell a package of value-added features to

customers who might not otherwise have purchased any features. As illustrated at Table 1, above, the revenue derived from the bundle greatly exceeds the incremental cost.TABLE 2: AT&T OF CO: LOCAL SERVICE OFFERING

SERVICE OFFERING PRICE OF SERVICE Local Only (Includes Call Waiting, Caller ID Deluxe, and Three-Way Calling) 15

$27.75

Basic Local Only16 $14.50

Source: Prices are found at AT&T Communications of the Mountain States, Inc., CO, Consumer Local Service Price List, Section 3, p. 1, Colo. P.U.C. Amended Advice Letter No. 23, released November 1, 1999. Descriptions of the offerings are found in Section 6, p. 1-2 of the same document.

TABLE 3: AT&T OF CO: FEATURE PACKAGE OPTIONS 17 18 19

FEATURE PACKAGES

COMPANY

FEATURE PACKAGE PRICES

PRICES IF FEATURES PURCHASED SEPARATELY

SAVINGS

Three Features AT&T $9.00 $13.95 $4.95

Source: AT&T Communications of the Mountain States, Inc., CO, Consumer Local Service Price List, Section 4, p. 2, Colo. P.U.C. Amended Advice Letter No. 23, released November 1, 1999. Individual feature prices are found on page 1 of this document.

Considered together, Table 2 and Table 3 offer evidence indicating how telecommunications carriers segment customers. The �local only� call package of $27.75 includes three vertical features for an incremental cost of $13.25 relative to the price of

Five Features AT&T $11.50 $19.95 $8.45 Ten Features AT&T $14.00 $35.45 $21.45

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 16

�basic local only.� This bundled offering provides a savings of seventy cents relative to

15Provides the Customer with a local access line, touch-tone service, unlimited calls within the Customer's local calling area, Call Waiting, Caller ID Deluxe, and Three-Way Calling. Additionally, the Customer may utilize Customer Dialed/Automated AT&T Calling Card services. The customer also has the option to substitute any of the following options for those listed above; Call Forwarding Variable, Call Forwarding Remote Access, Call Return, Repeat Dialing, Speed Dialing 8 or 30, Call Forwarding Selective, Call Screening, Distinctive Ring Service. 16Local Only service provides the Customer with a local access line, touch-tone service and unlimited calls within the Customer's local calling area. Additionally, the Customer may utilize Customer Dialed/Automated AT&T Calling Card services. 17Three Features: Basic Local Only service includes Call Waiting, Caller ID-Deluxe, and Three-Way Calling. 18Four Features: Includes Call Waiting, Caller ID-Deluxe, Three-Way Calling, Call Forwarding Variable, Call Return. 19Five Features: RCN-BecoCom, LLC,d/b/a RCN of Massachusetts, Massachusetts Tariff No.1, Exchange Access Service; Business, Section 5, 1st Revised P.4; Residential, Section 6 2nd Revised p.6. Price discrimination is also evidenced in the case of Voice Mail, which is priced at $10.00 for business users versus residential rates ranging from $3.75 to $7.00 per month. Business, Section 5, 1st Revised P.3 and 4; and Residential, Section 5, 2nd Revised p.15, Section 6 2nd Revised p.13.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 17

the component prices. The same package of local service plus three features is also sold for $23.50 ($14.50 + $9.00) by combining �basic local only� with the three-feature package option. One can imagine that a supplier might first attempt to sell the three vertical services on a component basis, followed by offerings of �local only,� then finally �basic local only� plus the three feature package option. The sooner the customer says �yes, I want the features,� the higher the profits from the transaction.

Examples of price segmentation may also be found in other tariff filings. For instance, the competitive local exchange carrier RCN has chosen to utilize the competitive pricing strategy known as value-of-service pricing for its Call Waiting service. A business user pays a monthly charge of $4.26 for this service while the price to the residential user is only $2.57 per month. For a business user, being notified of incoming calls while the line is engaged, coupled with the option to put the current caller on hold, so as to take the new call is an important business and client management tool. As such, demand for this service by business users is less price elastic than the demand for this service by residential users and RCN prices the service accordingly.20

Carrier Access Charges

Table 4, which compares AT&T Colorado�s switched access rates to those of US WEST�s indicates that AT&T does not assess a common carrier line charge (CCLC) on interexchange carriers for access to its network. However, AT&T�s rates for switched access (End Office Local Switching21) are high relative to US WEST�s rates. They are very high compared to the Colorado Public Utility Commission approved unbundled network elements (UNE) rates for switched access of $0.00283 for Originating and Terminating Usage.22 In fact, when these rates are compared to the sum of US WEST�s CCLC and End Office Switched Access rates, it becomes obvious that AT&T has merely chosen to offset the lack of revenue from a CCLC by increasing switched access rates. Again, this illustrates that competition does not necessarily drive prices to marginal costs, nor does it prevent firms from assessing access fees for non-member access to their network.

Utility economists have long argued that new entries would drive down the price of the common carrier line charge to the incremental cost of using the loop, which is zero.

20Economists refer to this as �own� price elasticity. That is, the responsiveness of the quantity demanded (or supplied) of a good (or service) to a change in the price of that good (or service). For example, the price elasticity for a service such as Call Waiting is measured by dividing the percentage change in demand for that service, over a specified unit of time, by the percentage change in the price of the service, over the same period of time. Elasticity values between 0 and -1 indicate that demand is inelastic, that is demand is relatively unresponsive to changes in price and values less than, or equal to, -1 indicate that demand is elastic, meaning that demand is very responsive to changes in price. 21An IXC has to pay both the switch and the CCLC access fee as both the loop and the switch are needed for the completion of a call. 22Before the Public Utilities Commission of the State of Colorado, RE: The Investigation and Suspension of Tariff Sheets Filed by US WEST Communications, Inc. with Advice Letter No. 2617, Regarding Tariffs for Interconnection, Local Termination, Unbundling and Resale of Services, Decision No. C97-739, Docket No. 96A-331T, Adopted Date: July 16, 1997, Attachment 4, Page 1 of 4.

This has not occurred. A review of access pricing behavior of select CLECs (see Table 5)

further demonstrates that entrants charge access fees to interexchange carriers. The companies included in this Table constitute only a small fraction of the number of CLECs in operation. However, recent assertions by a prominent CLEC trade organization that its members are charging network access fees comparable to those charged by the ILECs strongly suggests that the access pricing behavior highlighted in Table 5 is indicative of what is occurring throughout the industry.23TABLE 4: AT&T, US WEST SWITCHED ACCESS RATES

Source: Data for AT&T is from AT&T Communications of the Mountain States, Inc., Access Services and Network Interconnection Tariff, Section 17, p.24, Colorado P.U.C. No.2, Issued November 24, 1999. Data for US WEST is from U S WEST Communications, Access Services Tariff, Section 6, Second Revised Sheet 146, Colorado P.U.C. No. 16.

US WEST RATE PER ACCESS MINUTE

AT&T RATE PER ACCESS MINUTE

CCLC Rate Originating $0.012395 No charge Terminating $0.028608 No charge Local End Office Switching Originating $0.015120 $0.044692 Terminating $0.015120 $0.064583 EO Shared Port $0.001300 Total of CCLC and EO Switching Originating $0.028815 $0.044692 Terminating $0.045028 $0.064583

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 18

23See Comments of The Association for Local Telecommunications Services, Before the Federal Communications Commission, In the Matter of Access Charge Reform, CC Docket No. 96-262; Price Cap Performance Review for Local Exchange Carriers, CC Docket No. 94-1, October 29, 1999, p.4. Also, the CLEC RCN notes that �...it is not aware of any instances in which its access charges are significantly different from those charged by the ILEC, Bell Atlantic, when account is taken of all relevant charge components.� Source: Initial Comments of RCN Telecom Services, Inc., Before the Federal Communications Commission, In the Matter of Access Charge Reform, CC Docket No. 96-262., October 29, 1999, p.2. Of late, particularly in relation to the CALLS proposal, the IXCs have made the argument that they must move to Internet-styled �flat-rate� pricing without usage-based access fees or risk loosing market share to Internet-based systems. Given the quality of Internet Telephony, it seems highly unlikely that the IXCs will face real pressure on this front in the near future, at least not for their residential and small business users. For example, one article mentions that �[t]he quality still has a way to go, with the best of conversations resembling a choppy cell-phone call and the worst a wobbly walkie-talkie transmission.� (Source: Romero, Simon, Millions Phoning Online, Finding Price Is Right Even if Quality Isn't, July 6, 2000, http://www.nytimes.com/library/tech/00/07/biztech/articles/06call.html) Until these quality-of-service issues are resolved, I don�t see Internet telephony leading to a decline in the switched minutes of use. It certainly will affect the growth rate, but at this point in time we are not going to see a rapid demise of non-ip telephony.

TABLE 5: CLEC SWITCHED ACCESS RATES

Sources: Bell Atlantic, DTE MA No. 15, Access Service, Section 30, pages 5 and 11; WorldCom Technologies, Inc., MA D.P.U No.3, Section 4, p.1; GST Telecommunications of New Mexico, New Mexico P.R.C. No.3, Original Page No. 38.1; MediaOne Telecommunications of Massachusetts, Inc., MA D.P.U. No.4, Section 3, original page 6, and; RCN-BecoCom, LLC,d/b/a RCN of Massachusetts, Massachusetts Tariff No.1, Exchange Access Service, Section 4, p.1

Alfred Kahn and other economists have stated that �overpriced� vertical services would not survive competitive market pressures.24 As the findings in this report indicate, the actual pricing behavior of entrants in the wireline telecommunications markets does not support such assertions. Tariffs filed by unregulated CLECs plainly show that these firms are pricing enhanced features at premiums well in excess of their

RATES PER ACCESS MINUTE

SWITCHED ACCESS SERVICE

AT&T OF

COLORADO

GST TELECOM

OF NM

BELL ATLANTIC

OF MA

WORLD COMM OF MA

MEDIA ONE OF

MA

RCN OF MA

Carrier Common Line Originating $0.025700 $0.028243 $0.028243 $0.000000 $0.028243 Terminating $0.025700 $0.028243 $0.028243 $0.028243 $0.028243 Local End Office Switching

Originating $0.044692 $0.002797 $0.002797 Terminating $0.064583 $0.003086 $0.003086 Originating (Off-Peak) $0.000314 Terminating (Off-Peak) $0.000346

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 19

marginal costs. In fact, rather than stimulating a down hill race to the marginal cost of production, local exchange competition has stimulated a complex and rich array of strategic pricing initiatives, such as value-of-service pricing and product bundling, that the CLECs utilize to segment their target markets.

As mentioned at the beginning of this section, Kahn et. al. also assert that the charges network operators levy on one another for network access would not survive in a competitive market. Here again the evidence indicates otherwise. While CLECs have the option of charging end-users a high monthly access fee for the local loop, they are choosing not to do so.25 Instead the CLECs are adopting the behavior of the ILECs and

24See, for example, Kahn, Letting Go, p.114. 25Arguably the case might be made that as flat-rate pricing options are introduced for more and more services, this pricing option may have an effect similar to that of high access fees. However, there is a difference between a high access fee and bundling a lot of services for a flat-fee. In the first instance, no service that provides utility is being obtained, only the right to use a network. In the case of bundling, products that provide utility are being obtained. As was discussed earlier in the paper, CLECs and other telecommunication services providers are primarily interested in getting people on the networks so as to sell them services. While flat rate pricing of service bundles could make some bundles unaffordable for some people, there will be enough of a variety of bundled options that customers will not be priced out of network access entirely. They just might not be able to get the level of service offering they desire.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 20

recovering part of the cost of the local loop through the assessment of per minute of use access charges on common carriers wishing to reach customers on their networks. These pricing decisions on the part of unregulated CLECs indicates that the regulatory push to get access charges down to the economic cost of using the traffic sensitive components of the network is not consistent with the behavior of competitive markets.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 21

II. Pricing in Other Network Industries

The cable telephony market in the United Kingdom (UK), the mobile telephone market in the United States, and the pricing of access to ATM networks provide further illustration that the actual pricing behavior of firms in networked industries is quite different from that predicted by the utility economists.

Cable Telephony in the United Kingdom (UK) The CLECs have only been operating in the United States for a few years. Arguably, their pricing strategy merely illustrates umbrella pricing26 by an initial competitor that would end when subsequent entrants emerged and eliminated the profit margins on vertical services. An examination of the local telephone industry in United Kingdom, a more mature, open market, refutes this proposition.

Local telephone competition began in the UK in the early 1990s when entrants constructed networks that were designed to provide both telephone and cable television services. Currently British Telecom (BT), the former government-owned monopoly provider of telecommunications services, accounts for approximately 80 percent of the market27 and about 50 percent of the new connections.28 Given BT�s diminished market share, the low percentage of new connections going to BT, and the number of years that this market has been open to competition, it is reasonable to assume that the current pricing strategy of cable firms offering telephony service is more reflective of long-term equilibrium conditions. As Table 6 indicates, vertical feature prices offered by one of the more established entrants, Telewest, are not close to approaching the marginal cost of production seen in Table 1.

26Umbrella pricing occurs when a new entrant to a market offers a service, or product, that is exactly the same as that offered by the dominant provider of that service, or product, for a price just under that of the dominant provider. The entrants price their products just under the dominant firm price so as to capture market share while maintaining the large margins that the dominant firms pricing still allows it to have. 27It is instructive to note for comparative purposes that the Independent Local Exchange Carriers (ILECs) currently control approximately 97 percent of the local market in the United States. Source: GAO, Development of Competition in Local Markets, GAO/RCED-00-GAO/RCED-00-38, January 2000, P.4. 28OFTEL, Price Control Review: 2nd consultation, A consultative document issued by the Director General of Telecommunications on possible approaches for future retail price and network charge controls, March 2000, ¶2.4.

TABLE 6: VERTICAL FEATURE PRICES OF TELEWEST

Source: Telewest website www.telewest.co.uk.

The case of NTL, currently the UK�s largest cable TV provider (CATV), serves as an illuminating example of the strategies and pricing behaviors actually utilized by firms in competitive telecommunications markets.29 The company�s 10Q filing for the quarter ending September 30, 1999 states the company had 1.7 million customers, approximately 52 percent of which subscribed to both telephony and television services. NTL has high levels of penetration in the UK market. Overall customer penetration rates are 44.7 percent, with telephony penetration at 37.1 percent and CATV penetration at 37.1 percent. The industry average in the United Kingdom is 27 percent for

TELEWEST PRICES IN POUNDS

TELEWEST PRICES IN DOLLARS

Call Waiting £1.00 $1.61 Reminder Call £2.00 $3.22 Call Divert £2.00 $3.22 Voicemail £1.50 $2.42 Call Barring £1.00 $1.61 Speed Dialling £1.00 $1.61 Three-Way Calling £1.00 $1.61 Number Display £1.00 $1.61 Anonymous Caller Rejection £1.50 $2.42 Ring Back When Free £0.40 $0.64

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 22

telephony and 21.8 percent for CATV.30

In a March 31, 1999 report to the U.S. Securities and Exchange Commission, NTL states that �...it has been installing a full-service network capable of providing a high speed, high capacity, two-way voice, data and video communications pathway to the customer. This approach allows the Company to pursue four revenue streams (residential telephony, residential cable television, business telecommunications services and Internet access services) on its network without a significant increase in fixed investment.� NTL believes that this capacity provides it with a competitive advantage in the residential market because it enables the Company to offer integrated telephone, CATV, telecommunications services (including interactive and online services) and multi-product packages designed to encourage customers to subscribe to multiple services.31

29See, U.K. Regulators Raise New Hurdle for NTL�s Cable TV Purchase, TR Daily, November 12, 1999. 30Form 10-Q, United States Security and Exchange Commission, September 30, 1999, Item 2, Management�s Discussion and Analysis of Results of Operations and Financial Condition, p.16. See also, Morgan Stanley Dean Witter, �NTL Inc. (NTLI.O): Leaders in Innovation�, April 9, 1999, European Investment Research. 31NTL 10-k report filed with SEC 3/31/99.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 23

NTL�s strategy has been to �...maximize gross profit contribution per home passed, rather than revenue per customer, by increasing overall penetration of the number of services provided over its network.�32 The Company is pursuing this objective via an intricate and differentiated pricing strategy involving bundled product offerings to encourage subscriptions to multiple services as well as more �a la carte� and transaction-oriented services that increase network utilization.33 Using this strategy NTL offers a bundled package of telephone service, and seven free additional television channels, at the same monthly charge that British Telecommunications (BT) assesses for telephone service alone.34

Judging from a recent report, NTL�s bundling and tie-in strategies appear to be paying off. Churn on its domestic service, the rate at which the company loses customers, is as low as 10 percent,35 telephony margins are up by 10 percent and cable margins are up by 11 percent.36

NTL�s pricing behavior is illustrative of the fact that in more mature, highly competitive markets successful firms develop a rich panoply of pricing strategies designed to further segment their existing and potential customer base so as to better maximize the extraction of customer surplus value. Kahn�s prediction that prices for goods and services will move towards the marginal-cost-of-production in a competitive market does not seem to hold true. Indeed, in a world where platforms are designed to provide multiple products, the notion of prices being driven to the marginal cost of production is increasingly meaningless. The network of a competitive firm like NTL is

32Ibid. 33Ibid. 34Morgan Stanley Dean Witter, Op. Cit. For example a promotion downloaded from www.askntl.com, the NTL web site, on December 13, 1999, contains the following offer. For £9.25 per month, discounted to £4.62 per month till March 2000 if a customer signs up before the end of the year, a customer who signs up on to the NTL cable network will get phone service; BBC1, BBC2, ITV, Channel 4 and Channel 5, plus 7 cable channels including QVC, British Eurosport, BBC News 24, Guest channel, Local channel, TV Travel Shop and BBC Parliament on the TV; and free Internet access, hooked up to TV or PC and metered at only 1p per minute. BT currently charges £9.25 per month for basic phone service only. A recent report by Ovum notes that this practice has also been followed by cable telephony operators in Japan, who have been paralleling Nippon Telephone and Telegraph�s (NTT) tariff structures, and offering more for less. Source: Falshaw, Peter, Jim Holmes, and Daniel Baker, Local Service Competition: Breaking the Bottle Neck, a Report by Ovum Consulting, Ltd., October, 1998, Section D1.4 Segmentation Strategies, p.28. 35For comparison purposes Telewest, the British company mentioned earlier, has a churn rate of around 28 percent. (Source: NTL WILL LAUNCH DIGITAL CABLE, THEN UPGRADE, FT Times article of June 10th, 1999) While in the United States ��analysts confirm that churn rates in the long-distance industry are high, with some estimates indicating that more than 30 percent of mass market customers switched long distance carriers within a twelve month period.� (Source: FCC, CC Docket No. 99-333, In re Applications of SPRINT CORPORATION, Transferor, and MCI WORLDCOM, INC.,Transferee, for Consent to Transfer Control of Corporations Holding Commission Licenses and Authorizations Pursuant to Sections 214 and 310(d) of the Communications Act and Parts 1,21, 24, 25, 63, 73, 78, 90, and 101, November, 17, 1999, at p. 48. 36Ibid. In this report an NTL spokesman, in commenting on the low churn rates, stated that �...services bundled together are the glue that sticks the customer to you.� This is a point that some of the IXCs in the US have appeared to grasp as well. A recent article has noted that in the US long distance market IXCs are scrambling to lock in customers through bundled offerings. The companies have realized that �Bundling is a key to customer retention. Acquiring new customers is a far bigger cost than long-distance transmission.� Source: Brull, Steven V., with Amy Barrett, and Roger Crockett, Why Talk is so Cheap, Business Week, (Sept. 13, 1999) Jeffrey Kagan, a telecommunications analyst, makes the point that many IXCs are choosing to compete on bundles rather than price as there is more perceived value to tying in customers with what are known as �sticky� bundles. Source: AT&T Sees New Rate Plans as Step Toward Integration, TR Daily, August 30, 1999.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 24

designed to provide multiple products. NTL does not attempt to set the price of customer access equal to the marginal cost of providing the entire platform. Rather, it seeks to recover its platform costs through the packaging of multiple products.

The strategy and competitive pricing behavior of NTL are strong indicators of the strategies and pricing behaviors likely to be pursued by Competitive Local Exchange Carriers (CLECs) in the United States. AT&T is a good example. In its effort to enter the local exchange market, AT&T is bundling voice services with data and broadband products, an option made possible by its acquisition of TCI with its 14 million cable subscribers, and by its recently approved merger with MediaOne.37 All early signs indicate that AT&T, like NTL, will offer customers a variety of service packages.38 There are also indications that AT&T will keep customer network access charges low to attract customers to, and keep them on, its networks.39 Local exchange companies are responding to this development by attempting to provide new services, such as interLATA toll and high-speed data access. The local exchange companies have been quite clear that they too intend on packaging voice, toll, and broadband services.40 If the forces of the market place are allowed to prevail, they will preclude the local exchange companies from implementing the high customer access fees long advocated by utility economists.41

37At a news conference announcing the TCI acquisition, AT&T Chairman Michael Armstrong �...trumpeted the idea of creating an all-in-one service as a major reason for the deal, which will create AT&T Consumer Services with a reach into 33 million homes, or one-third of all U.S. households.� Source: Tourtellotte, Bob, Reuters, Los Angeles, July 25, 1998. 38For example, a recent TR Daily article notes the launch of SBC�s �Simple Solutions� offering in two markets AT&T has targeted for its packaged integrated services offering. In comments concerning the offering Roy Caldwell, the President of SBC Operations, stated that �Simple Solutions is a customer-friendly offering�we're giving customers the flexibility to choose from several convenient offerings with compelling prices.� Source: SBC Offers Bundle of Telecom, Entertainment Services, TR Daily, August 24, 1999. 39For example, a CNET news story notes the following: �In what may be a sign of broadband pricing battles to come, Excite@Home's cable partners are offering a limited promotional campaign under which some of them will subsidize the cost of America Online for new users of the high-speed Net-over-cable service.� AT&T Broadband & Internet Services, one of Excite@Home�s partners, initiated this campaign. Source: Excite@Home to Subsidize AOL Members Who Sign Up, Grice, Corey, CNET News.com, July 7, 1999. http://www.news.com/News/Item/0,4,38953,00.html?owv. 40SBC Offers Bundle of Telecom, Entertainment Services, TR Daily, August 24, 1999. 41This is readily apparent in the ISP realm where Michael Duponchel, a director of IBM Europe, has noted that �[t]he shift from access to value-added services is really setting the basis for competition in the ISP business.� Nairn, Geoffrey, ISP Aim to Move up Value Chain with New Services, FT Telcoms Quarterly Review, October 1999, Industry Issues, http://www.ft.com/ftsurveys/sp664a.htm.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 25

Relationship Banking The telecommunications industry is not the only industry generating strategic pricing innovators such as NTL. The banking industry has its innovators as well, and like NTL and its imitators these companies have realized that their ability to survive and grow is dependent on the ��economics of relationships, as opposed to productivity or profitability measured at the level of the product or service��42 For example, Continental Illinois redefined its niche as a set of employees representing a knowledge base about the types of clients the bank wanted to pursue and maintain. In implementing this strategy Continental decided to ��use new products as a way to lock in a �share of mind��to move from simple to complex transactional services, and to provide financial and business advisory services as a means to achieve greater reliance on the bank by the client.�43 This approach called for an emphasis on evaluating product lines in light of the profits generated by the totality of the customer relationships with the bank.

What is known as �relationship management� in the banking world is similar to the bundling and tie-in strategies utilized by innovative telecommunications service providers, such as NTL, to maximize the extraction of customer surplus value. A common strategy banks have adopted as a means of initiating customer relationships is through the underpricing of loans, lowering the cost of access, as it where. Once established, this lending relationship then affords the bank ample opportunity to offer the client additional products and services, such as no fee checking for clients taking out loans of a certain size and able to maintain a specified balance. Banks realize that ��if customers maintain several products and significant balances with a given bank, they will be less likely to switch to a competitor.�44 By locking in their customer base, the bank has the opportunity to extract additional profits from the customer through new product and service offerings.

This example from the banking industry illustrates the fact, as the more savvy network operators have already figured out, that a firm�s overall profitability is tied to the total profits generated from its customers and not necessarily to the profits generated by a particular product, or service.

The Mobile Phone Market The mobile phone market in the US has experienced incredibly rapid growth over the past several years. For example, the number of wireless customers increased from 34 million to 69 million between December 1995 and 1998.45 Part of this growth is

42Calomiris, Charles W., U.S Bank Deregulation in Historical Perspective (Cambridge University Press, 2000), p. 341. 43Ibid. p. 341. 44Ibid. p. 342. 45Trends in Telephone Service, September 1999, Service Industry Analysis Division Common Carrier Bureau Federal Communications Commission, Table 2.1.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 26

attributable to innovations in the pricing of wireless services. In recent years wireless operators have developed a wider variety of innovative, and attractively packaged calling plans. These plans have been increasingly designed with the intention of getting and retaining groups of customers and encouraging them to use more calling minutes. For example, AT&T has come out with its new "AT&T Family Plan" which is intended, among other things, to more fully integrate its wireline and wireless offerings. The plan �allows up to five family members to make unlimited wireless calls to each other and to their landline phone at home, within a defined "family calling area." There's no charge as long as at least one family member subscribes to AT&T's $24.98 plan (covering 60 minutes of calling, $49.99 plan (covering 400 minutes of calling) or $69.99 plan (600 minutes of airtime). The plan links to AT&T's wireline long distance service, which is available at a rate of 7 cents per minute (no monthly fee) to Family Plan customers.�46 Bell Atlantic and Sprint have introduced similar, competing plans.47 This bundling trend is expected to continue as fixed and mobile systems become increasingly integrated.48 The variety and the segmented nature of the calling plan options currently available in the mobile market shows the effect that competition can have on a firm�s pricing strategy. A few years back an Organization for Economic Co-Operation and Development (OECD) report found that when one firm controls the market, it tends to view that market as static; consequently, it does not actively seek new customers or experiment with new pricing plans and products. While the local exchange companies (LECs) have traditionally seen access as a burden associated with providing telephone service, competitive mobile suppliers have lowered the price of access to obtain market share.49 In the mobile market, the handset, the access point to the mobile network, has primarily been seen as a commodity to be heavily discounted, or given away, in order to gain more network subscribers. The mobile operators knew that success in this highly competitive market depended on network size. The more members on the network, the more valuable the network becomes for existing subscribers and the more attractive it becomes for non-network subscribers. The more subscribers to the network, the more profits the company can earn from commissions on airtime.50 The experience of the wireless market further supports the proposition that competition promotes a proliferation of different pricing structures, including those with reduced network member access fees.51 If the market story offered by some utility economists 46AT&T Sees New Rate Plans as Step Toward Integration, TR Daily of 8/30/99. 47Bell Atlantic to Sell New Group Wireless-Calling Plan, Bloomberg Wire Service, October 29, 1999. 48See, for example, Woolf, Peter and David Bhola, Commercial Strategies for Fixed-Mobile Convergence, Analysis Publications, January, 10, 1997. 49OECD, �Mobile Communications: Pricing Strategies and Competition,� 15 May 1995, ¶80-97. 50�Motorola Goes for the Hard Cell,� Business Week, September 23, 1996, p. 39. 51One pricing strategy that is not found in the wireless case is the overt price discrimination between business and residential users in evidence in the wireline arena. However, I would argue that the richness of the bundling options that the wireless providers are offering is indicative of a market segmentation strategy that is more differentiated and nuanced than the traditional business/residential pricing model and which still seeks to price discriminate among customers.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 27

were correct, mobile companies would not give away, or heavily discount, telephones in order to provide customer access.52

Roaming Fees

There is another insight that can be drawn from examining the pricing strategies of wireless providers. Wireless providers charge their end users a roaming fee each time a call is originated outside the carrier�s service territory. In doing so they are not penalizing their users for using the phone outside the territory�they do not have an incentive to do so as the possibility of such a penalty would encourage users to switch to a provider with a larger service territory. Rather, wireless providers charge each other for access to their respective networks and this cost is passed onto subscribers in the form of a roaming fee. This roaming fee illustrates that in unregulated wireless markets, a firm will not give another network provider free access to its network members. If a subscriber needs access to another supplier�s network, they have to pay for the privilege. This roaming charge is the equivalent of the common carrier line charge (CCLC), which is, essentially, a fee that interexchange carriers (IXCs) pay for having access to end users on a LEC network. It is paradoxical that IXCs and LECs have pressured the Federal Communications Commission (FCC) to eliminate the common carrier line charge for wireline service while not freely exercising such an option for their unregulated wireless operations.

Pricing of Access to ATM Networks The history of pricing for access to ATM networks further illustrates that network owners in competitive markets regularly charge non-network members fees for the use of their networks. As described in a series of articles in the New York Times, an intense debate continues over the �foreign� transaction surcharges (FTS) ATM owners assess non-network members for the use of their ATM networks.53 As a result of consumer complaints over these surcharges, some states and municipalities have passed, or are considering passing, legislation banning FTS. ATM owners are starting to fight back. In response to a ban on FTS in Santa Monica, Bank of America and Wells Fargo no longer permit �foreign� transactions at their ATMs. They contend that they should not be expected to provide network services to non-members free of charge. Providing non-members access to their networks involves a cost that the banks assert they should be allowed to recoup.

52The wireless operators recover the cost of providing customer access through usage fees and a fixed monthly fee. The fixed monthly fee typically provides a minimal amount of airtime. The fixed monthly fee also provides a means for recovering a portion of the cost of the mobile set. 53Pollack, Andrew, Debate Intensifies Over ATM Surcharges, New York Times, November 16, 1999; Hershey, Robert D., Jr., Interviewing Donald G. Ogilvie (Executive Vice President of the American Bankers Association) Whose $1 is it, Anyhow? A Defense of an A.T.M. Fee, New York Times, November 14, 1999, NE Section 3, BU 4. Ogilvie likens the argument that banks should not impose surcharges on �foreign� transactions to arguing that a company should not be allowed to charge more for a vending machine drink than a vending machine customer would have to pay for that same drink from a grocery store. We buy a drink at a vending machine, he says, and are willing to pay a premium for doing so, because it is there, cold, when we want it.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 28

Interestingly, banks themselves initially prohibited foreign transaction surcharges. But this prohibition on surcharges was seen by some, particularly smaller banks and retailers, as being anticompetitive in that it prohibited smaller banks and non-financial institutions from entering into the ATM business because they had no way to recoup the costs of the machines. After an intense lobbying effort by these organizations, most of the bans on surcharges for ATM usage were lifted by 1996. In 1997, approximately 123,000 ATMs existed nationwide, now there are about twice that many. The cautionary message behind this historical recounting is that the imposition of particular rate structures by regulatory fiat can limit market competition.54

Levying access charges on non-members for the privilege of network access is a standard business practice; interexchange companies should not be exempt from paying access fees for access to the local network.

The next section addresses the restructuring of telecommunications prices when the market is further opened to competition due to a change in the regulatory rules.

54Pollack, op.cit.

CURRENT ISSUES IN THE PRICING OF TELECOMMUNICATIONS SERVICES PAGE 29

III. State Regulatory Responses to Structural Changes: Divestiture vs. The Telecommunications Act of 1996