Embed Size (px)

Citation preview

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 1/341

L I B R A R Y O FAN D

HISTORY

CURRENCY & BANKING

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 2/341

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 3/341

A

TREATISE

ON

C U R R E N C Y & B A N K IN G

BY

CONDY RAGUET

2nd Edition

[1840]

Reprints of Economic Classics

Augustus M. Kelley Publishers

New York / 1967

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 4/341

First Edition 1839Second Edition 1840

( Philadelphia: Grigg & Elliot, 1840 )

Reprinted 1966 by

Augustus M. Kelley • Publishers

Library of Congress Catalogue Card Number65-26375

P R I N T E D I N T H E U N I T E D S T A T E S O F A M E R I C A

by S E N TR Y P R E S S , N E W Y O R K , N . Y . 1 0 0 1 9

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 5/341

A TREATISE

CURRENCY AND BANKING.

BV

CONDY RAGUET, LL.D.,

MEMBER OF THE AMBRICAN PHILOSOPHICAL SOCIETY; PRE SIDEN T OK TH E CHAMBERO f COMMERCE OF PHILADE LPHIA; LATE CHARGE D'AFFAIRES OF THE UNITED

STATES AT TH E COURT OF BRAZIL, AND AUTHOR OF " THB PRINCIPLES

OF FREE TRA DE ILLUSTRA TED."

" It i9 the interest, of every country that the standard of its money, once set-tled, should be inviolably and immutably kept to perpetuity. For wheneverthat is altered, upon whatever pretence soever, the public will lose by it.

" Men in their bargains contract, not for denominations or sounds, but for theintrinsic value.—LOCKE ON M O N E V .

Second

PHILADELPHIA:

G RIG G Sc E L L I O T , B O O K S E L L E R S , N o . 9 N O A T H F O U R T H S T R E E T ,

1840.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 6/341

Entered, according to act of congress, in the year 1839,

By CONDY RAGUET,

In the office of the clerk of the District Court of the Eastern District

of Pennsylvania.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 7/341

TO

CLEMENT C. BIDDLE, ESQ.

AS AMARK OFRESPECT,

DUE TOAN ENLIGHTENED POLITICAL ECONOMIST, AND

AS ATESTIMONIAL OFAFRIENDSHIP,

COMMENCED IN CHILDHOOD, CONTINUED WITHOUT INTERRUPTION

FOR MORE TH AN FORTY YE AR S, AND STREN GTHE NED BY A H A R -

MONY OF OPINION ONMOST OF THEPOLITICAL SUBJECTS THAT

HAVE OFLATE DIVIDED THEPEOPLE OF THE

UNITED STATES,

AND ESPECIALLY ONTHOSE OF

CURRENCY AND BANKING,

THIS WORK IS,WITH SENTIMENTS OF THE

MOST AFFECTIONATE REGARD,

DEDICATED BY

T H E A U T H O R .

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 8/341

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 9/341

TABLE OF CONTENTS.

BOOK THE FIRST.

O F T HEL A W S W H I C H R E G U L A T E A C U R R E N C Y

C O M P O S E D E N T I R E L Y OFT H E P R E C I O U S ME-

T A L S .

C H A P T E R I . — O f t h e in t r ins ic va lue oft h e p r e c i o u s m e t a l s ,

and of the i r adap ta t ion to thep u r p o s e s of a c i r c u la t in g

m e d i u m , - - - - - - - - - 2

C H A P T E R I I . — O f t h e d i s t r i b u t io n of thep re c io u s me ta l s

t h r o u g h o u t t h e c o m m e r c i a l w o r l d , . . . . 5

C H A P T E R I I I . — O n t h e re la t ive va lue of g o ld a n d s i lve r , - 8

C H A P T E R I V . — O n t h e b a l a n c e of t r a d e , or th e c a u s e s w h i c h

occas ion t h e t r a n s m i s s i o n oft h e prec ious meta ls f rom o n e

c o u n t ry to a n o t h e r , - - - - - - - 1 2C H A P T E R V . — O n t h e p r in c ip l e s of e x c h a n g e , - - - 2 5

C H A P T E R V I . — O n t h e s t e a d i n e s s oft r a d e inc o u n t r i e s e m -

p l o y i n g a me ta l l i c c u r r e n c y , - - - - - - 36

C H A P T E R V I I . — O f thedifferent k inds of d e p re c i a t io n to

w h i c h a me ta l l i c c u r r e n c y is l i a b l e , - - - - 4 2

C H A P T E R V I I I . — O n t h e " c r e d i t s y s t e m , " ort h e influence

of credi t in p r o m o t i n g n a t i o n a l w e a l t h , - - - - 48C H A P T E R I X . — O n the l a w s w h i c h r e g u l a t e the h i r e of

c a p i t a l , a n d ont h e i m p o l i c y of u s u r y l a w s , - - - 53

C H A P T E R X . — E x a m i n a t i o n of the c o mmo n o p in io n re-

s p e c t i n g t h e s i n k i n g of c a p i t a l , - - - - - 58

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 10/341

TABLE OF CONTENTS.

BOOK THE SECOND.

O F T H E L A W S W H I C H R E G U L A T E A M I X E D C U R -

R E N C Y C O M P O S E D O F T H E P R E C I O U S M E T A L S ,

A N D O F P A P E R C O N V E R T I B L E I N T O C O I N O N

D E M A N D .

CHAPTER I.—O f banks of deposite, of banks of discount,

and of banks of circulation, - - - - - - 67

CHAPTER II.— O f the operation of banks of circulation, - 73

CHAPTER III .— O f the principles by wh ich the profits of

ban ks of circulation are determined , - - - - 80

CHAPTER IV.—Of the safest and most profitable mode of

inves ting the capitals of banks of circulation, - - 84

CHAPTER V.—Of the legitimate operations of banks of

circulation, - - - - - - - - - 9 0

CHAPTER VI.—Examination of the common opinion that

banks create capital , - - 9 4

CHAPTER VII.—On the strict convertibility of bank notes

and credits, - - - - - - - - - 100

CHAPTER V III .— O f the various mod es resorted to by som e

bank s to augm ent their dividen ds, - - - - 104

CHAPTER IX .— O f the creation of banks without capitals,

or of fraudulent bank s, - - - - - - 1 1 0

CHAPTER X .— O f the effects of banks dealing in exch ang e, 114

CHAPTER XI.—Examination of the common opinion that

the establishment of banks in the western states upon

eastern cap ital, is beneficial to those sta tes, - - - 124

CHAPTER X II.— O n the circulation of small bank note s, - 127

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 11/341

TABLE OF CONTENTS. vil

BOOK THE THIRD.

O F THE L A W S W H I C H R E G U L A T E A C U R R E N C Y

C O M P O S E D E N T I R E L Y OF I N C O N V E R T I B L E

B A N K P A P E R .

CHAPTER I . — O f the career usually run by b a n k s of circu-

la t ion previou s to a general s toppage of spec ie payments , 134

CHAPTER I I.— O f the fluctuations in the marke t p r ice of

specie and of bi l l s of exchange under an inconvert ible

paper currency , - - - - - - - -140

CHAPTER I II .— O f the t rue character and effects of a gene-

ra l suspension of paymen ts by the b a n k s , and their obli-

gations under it, - - - - - - - - 148

CHAPTER I V . — O f the cr imina l i ty of b a n k s in augmen t ing

their issues after a suspension of p a y m e n t s , - 154

CHAPTER V . — O f the cost to a communi ty , pecunia ry and

mora l , of b a n k s of circula t ion, compared with the bene-

fits derived from them , - - - - - - - 158

CHAPTER V I . — O f the different kinds of deprecia t ion to

w h i c h an inconvert ible paper currency is l iab le , - - 168

BOOK THE FOURTH.

CHAPTER I.—Examination of the question, of what does a

currency consist 1 - - - - - - -173

CHAPTER II.—Examination of the question, of what does a

currency consist! continued, - 177

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 12/341

viii TABLE OF CONTENTS.

CHAPTER III.—On the importance of having uniform peri-

odical statements of the condition of the currency, - 188

CHAPTER IV.—On the impolicy of adhering to our present

mint proportions between gold and silver, - 194

CHAPTER V.—On the superiority of the New York general

banking law, over the present banking system, - - 200

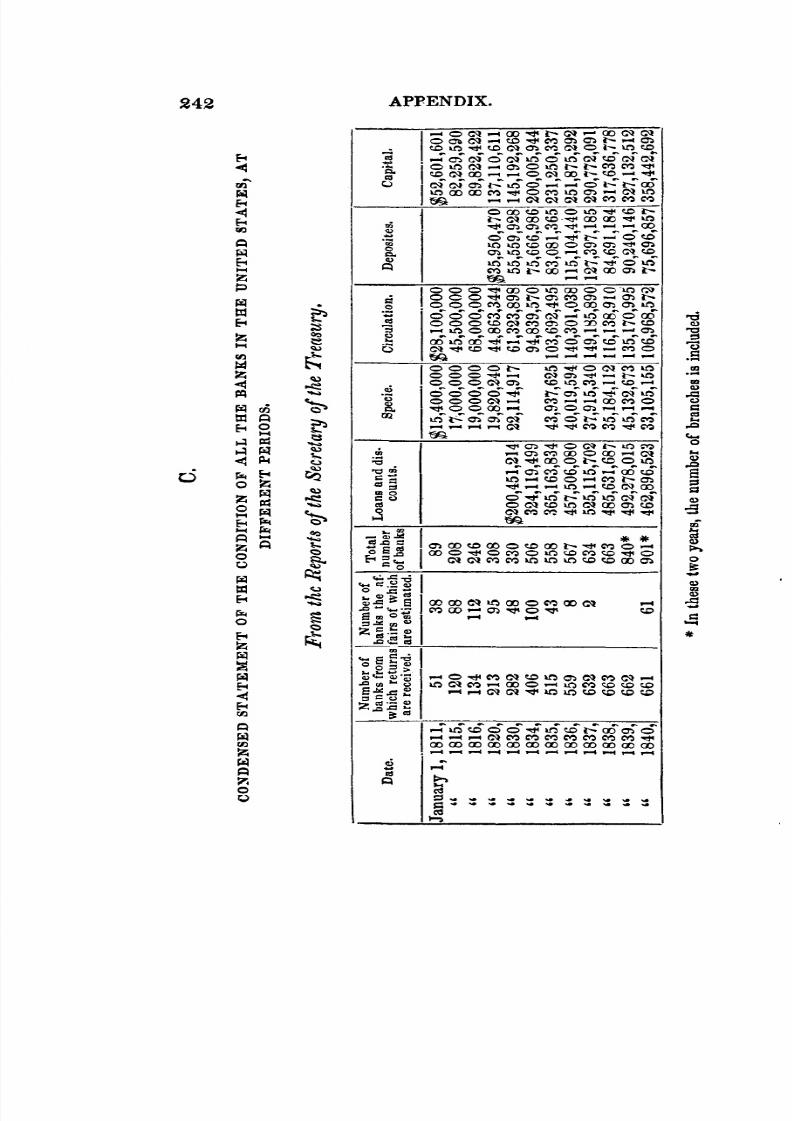

A P P E N D I X .

A.—On therelative value of gold and silver, . . . 207

B.—History of the gold coinage of the United States, - 218

C.—Condensed statement of the condition of all the banks

in the United States, at different periods, - - 242

D.—The New York general banking law, - 243

E.—Letter from theauthor to J. W. Co well, Esq . - - 254

F—Table of imports and exports, from 1789 to 1839, - 258

G.—Essay onunlimited liability, by James Cox, Esq., - 260

H.—Report to the senate of Pennsylvania on the money

crisis of 1818, 289

I.—Prices of state stocks in London at two different pe-

riods, 306

J.—Extract from the annual report of the comptroller of

New York, of January, 1840, upon the general

banking law,with abstracts from tworecents laws, 308

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 13/341

PREFACE.

TH E suspension of specie payments by all the banks

in the United States, south of Ne w E ng lan d, in the

ye ar 1814, and of all, w ith a very few trifling ex ce p-

tions, in the ye ar 1837, ha s strongly impressed the

public mind with the belief that there is something

defective in the present banking system of this conn-try ; and it is not, pe rha ps , ve nturin g too m uch to

assert, that there are now elements at w ork, w hich

will ultimately overthrow the whole fabric, unless

those w ho hav e the pow er to rem edy the evil, shall

introduce the reforms which can alone render a repe-

tition of such a calamity impossible.

It m ust be evident to every obse rvant m ind, tha ta dislike to hea r the truth , w hen opposed to on e's

interests or prejudices, is the principal cause of a

large portion of the mischievous errors which so

generally prevail. M en of education and cap acity,

w ho are best qualified to investigate an d und erstan d

the important principles which belong to the science

of public econom y, are too apt to view them as of

no a ccount, or to despise them w he n they come in

conflict w ith their pu rses, or w ith their political pr o-

motion; and hence that knowledge, which is the most

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 14/341

X PREFACE.

entitled to regard, because most intimately connectedwith the prosperity of a country, is of all others the

m ost neglected. I assert it, an d, in so do ing , I thin k

I do not overestimate its value, that political economy

is the most important of sciences; and if its practical

branches were introduced as a study into all our

colleges and principal schools, it would do more

tow ards ex em pting the country from erroneous anddestructive legislation, than any other study to which

the attention of our youth could be directed.

Of these practical branches, the science of banking

is one, but it is one, to the attainment of a knowledge

of w hich there is no " royal road .7 ' any more tha n

there is to an y other species of learning . H e w ho

w ishes to un der stand it, m ust study and reflect, andthis not with the feelings of a partisan, but in the true

spirit of philosophy, unbiassed by self-interest, or by

any other consideration than a pure love of the truth.

The rapid strides which the banking system has been

making of late in France and other countries of

E ur op e, accomp anied, as i t has been, by indications

of unsoundness, in Belgium and elsewhere, givesjust ground for apprehension, that the same spirit

which has characterised the management of most of

our institutions, as well as those of Great Britain,

producing alternate expansions and contractions of

the curre ncy , to the gre at injury of the pub lic, w ill

also ther e ex tensively pre vail. In such eve nt, the

check to over-issues in this coun try and E ng lan d,w hich now ex ists from the reaction of the m etallic

currencies of continental E ur op e, w ould be greatly

dim inished , and in conseq uence of it, inflations an d

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 15/341

PREFACE. xi

convulsions hitherto unknown in the commercialworld, because extended over a wider field, would

most certainly ov ertak e us all. T h at the interests of

a coun try are best to be prom oted by a stable cur-

rency, precisely as they are by a fixed stan dard of

w eights and m easures, w ill h ardly be d isputed; and

if it can be shown, that a defective, or mismanaged

banking system, produces exactly the same resultsupon the pursuits of industry, and the property of

individua ls, as w ould the decrees of a despot, w ho

should alter, at his plea sure , w ithou t an y previou s

notice, as often as he thought it expedient, the weight

of the po un d, or the leng th of th e yard stick, it is to

be hoped that there is not a patriot in the land, who

w ould hesitate to assist in the entire e radication ofsuch a m onstrous evil. T h a t such is the effect of ou r

present system, as it has been of late conducted, must

be obvious to all who have closely examined its

op erations, and hence the necessity, before it is too

late, of an application of the app rop riate rem ed y.

The author of this treatise in offering it to the

public, ha s no private ends to prom ote. H e has beenfor tw en ty y ears a student of the science w hich he

proposes to discuss, and has during that time in some

reports to the senate of Pennsylvania, and in many

detached publications, presented his views in relation

to currency and banking; and if in the present volume

there should appear here and there an expression

familiar to the reade r from former acq ua intance, hemay be assured that not a phrase has been employed

as original, w hich is not his ow n prop erty. H e

kn ow s that in his opinions respecting the influence

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 16/341

Xii PREFACE.

and operation of ba nk s of circulation, up on the publicprosperity, he differs from some of his personal friends,

and from m an y others engaged in the m anag em ent

of such institutions, for w hose intelligence and pu rity

of character he entertains the highest respect. B ut

the truths of science cann ot be forced to accom m odate

them selves to m an 's imperfection or interests. If

w ha t he advan ces be not such truths , they can beeasily refuted, and he invites the severest criticism to

be applied to his doctrines, in order that their solidity

m ay be tested, and if found to be false or un stab le,

tha t their true cha racter m ay be ex posed . If, on the

other hand, the principles which he asserts, be in

reality, as he honestly believes them to be, incontro-

vertible truths, he will not do any of his readers theinjustice of supp osing, th at the y w ou ld reject them ,

because they are not profitable.

With these preliminary remarks, the author will

briefly state, tha t the plan he h as ad opted , is one w hich

he thinks the best calculated to simplify the subject

to those w ho ha ve no t heretofore m ade it a study .

H e has divided the volum e into four books. T hefirst treats of the laws which regulate a currency

composed entirely of the precious metals; the second,

of those which regulate a currency composed of coin

and convertible paper united; the third, of those

w hich regulate a n inconvertible p ape r curren cy;

w hilst the fourth treats of some miscellaneous m atters,

w hich could not hav e been w ell comprised undereither of the former heads.

In the language and style of the work, the author

ha s sough t rather to rende r his positions intelligible

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 17/341

PREFACE. x i i i

to practical men, than to appear to be scientific, and

hence the read er w ill find some familiar ex pression s,

w hich hav e been purposely adopted, because every

body could understand them.

Jlpril 15, 1S39.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 18/341

x i v PREFACE.

N O T E TO S E C O N D E D I T I O N .

T H E stoppage of specie payments referred to

ab ov e, in 1814, comm enced in Baltimore about the

27th of August, soon after the battle of Bladensburghand the capture of Washington, which events took

place on the 24th of that m onth , and w as followed

by Philadelphia on the 30th, and by N ew York on

the 1st of Se ptem ber. A gene ral resum ption took

place on the 20th of February, 1817.

The second stoppage commenced at New York on

the 10th of M ay , 1837, and w as followed at Ph ila-delphia on the 11th, at Boston and Baltim ore on the

12th, an d in all othe r places in qu ick succession.

Re sum ption took place at N ew Yo rk on the 9th of

M ay . In Boston, Ph ilade lphia , and places further

south it w as delayed until the 13th of A ugu st.

Since the publication of the first edition of this

book, all the banks in the United States, south ofN e w Yo rk, w hich pretended to pay in specie, sus-

pende d pay m ent aga in. Th is even t took place first

in Philadelphia, on the 9th of October, 1839, and

w as follow ed by the rest in rapid succession, leaving

only N ew York and N ew En gland in the enjoyment

of a convertible currency. T his suspension has con-

tinued to this tim e, an d is ex pected to continue until

1841.

June 1, 1840.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 19/341

A TREATISE

ON

CURRENCY AND BANKING

BOOK FIRST.

OF THE LAWS WHICH REGULATE A CURRENCY COM-POSED ENTIRELY OF THE PRECIOUS METALS.

A D A M S M I T H , and other elementary writers on thescience of Political Economy, have shown the princi-ples upon which commodities must have been ex-changed in that rude condition of society which pre-ceded the use of metallic money, and it is not my in-tention to travel over the sam e grou nd, and occupythe attention of the reader in recapitulating detailsw ith w hich he is prob ably alre ady fam iliar. N or isit my intention to give a history of the various inven-tions to facilitate barter, which have been adopted atvarious periods in different countries, such as the useof cattle, cowry shells, tobacco, iron, and some otherobjects, each of w hich has been at some period em -ployed to perform the function of what has been ap-

propriately denominated " a medial co m m od ity/ ' byv/hich the relative value of other things could be deter-m ined . I propose at once to enter upo n the subjectof currency as we find it at the present day in com-m ercial natio ns, and shall first point out the law s by

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 20/341

A TREATISE ON

w hich commerce is carried on in a co untry w he rethere are no bank notes or paper money of any kind,and w he re gold and silver alone constitute the cur-ren cy ; and , as i t w ould be carried on in every cou ntry,if there did not exist paper money.

C H A P T E R I .

OF TH E INTRINSIC VALUE OF TH E PRECIOUS METALS,

AN D OF THE IR AD APTATION TO TH E PURPOSES OF

A CIRCULATING MEDIUM.

G O L D and silver, it is well known, are produced in

va rious pa rts of the glob e, at the cost of labor an dcapital, precisely in the same manner that iron, lead,and other metals are prod uced ; and w ith regard toall the mining countries, they constitute, if not theonly, at least the most inviting product of industry tow hich a portion of the land , labor, an d ca pital, oftheir inha bitan ts can be applied. As pro du cts, the re-fore, of ind ustry, the y possess an intrinsic valu e, likeall other com m odities, dep end ent up on the cost ofproducing them ; that is , upon the am ou nt of the rentpaid to the owner of the land for the privilege ofm ining them , the am oun t paid for the w age s of thelaborers employed in digging and smelting the oreand in refining the m etal, and the am ou nt of the or-dinary profits on capital invested in the enterprise.Were this not the case, it is evident that mines wouldnot be worked, for no proprietor of land or capitalist

would embark in an undertaking that would lead tocertain loss, the object of mining not being to producegold an d silver, bu t to prod uce gold an d silver of avalue greater than that of the capital expended in itsprodu ction. Th is m uch is prem ised, in order that the

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 21/341

CURRENCY AN D BANKING. 3

read er m ay hav e at the outset a clear view of thisfund am ental truth in political econom y, tha t gold andsilver being products of industry, possess a value af

real an d substantial as that w hich belongs to anyother commodities; not indeed founded upon the basisof convention, a s some people ima gine, but upon theirwell known applicability to various purposes of uti-lity and ornament for which no other materials pos-sess equal qualities, and which renders them on thataccount universally sough t for. T he y are thereforenot mere representatives of w ealth as m any personsfancy, but real wealth itself to the full extent of theirvalue.

W h at proportion of the actual value of gold andsilver, as exchangeable for other commodities, is dueto their applicability to objects of utility and orna-ment, and what proportion to their fitness for the pur-

poses of a circulating medium, now that they are ap-plied to that purpose, it would not be easy to deter-mine; nor is it at all necessary to this investigation thatit shou ld be de term ined. It is sufficient for us toknow, that almost every individual who can afford asilver spoon, or a gold watch, or a plated or gilt orna-m en t, w ill ha ve on e; and that if gold and silver w ereto be w holly disused as m oney , they w ould retain a

large share of their present value for the purpose ofbeing converted into plate and other objects of manu-factu re, and in process of tim e, w ould aga in rise to thecost of their production, which would be an indispen-sable requisite to ensu re a future fresh sup ply.

It w ill, per hap s, rem ain for a future d ay to developeall the reasons why gold and silver have become souniversally adopted by all civilised people as the me-dial com m odity, that is, the com modity in ex cha nge

for which any other commodity can almost always bereadily had. Those with w hich w e are already ac-quainted, are the following:—

1. Th eir uniformity of valu e, va ry ing from oneyear to another, and from one period of years to an-

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 22/341

4 A TREATISE ON

othe r, less than jany other kn ow n com m odities, an dtherefore well adapted to be the commodities of con-tracts and obligations payable at a future day.

2. T he universality of this uniformity of va lue , bywhich they serve not only as standards for comparingprices at different per iods of tim e, but prices in diffe-rent countries at the same time.

3. T he ir convenient portab ility, possessing a grea t

value in a small bulk, and yet a bulk not too small forall practical purposes.4. Their divisibility into pieces of any weight, and

of the most ex act qu an tities, and their con vertibilityby fusion back aga in into larger masses w ithout loss.

5. Th eir malleabili ty and toughness, w hich renderthem not liable to break.

6. Their susceptibility of receiving impressions ascoins.

7. Th eir uniformity of physical qu ality, pu re goldor silver being the same at all times and at all places,and thu s unlike most other m etals and com mo ditieswhich have different degrees of excellence.

8. Their capacity of admixture with alloy whichrend ers them as coins less destructible by w ear an dtear, and of their being aga in sepa rated from it w ithvery little loss.

9. Their du rability, not being easily destroyed byfire, and not at all by rust.10. Their clear sound when dropped upon a hard

substance, by w hich they can be know n from basemetals, and be thus distinguished from counterfeits.

11. The ir specific grav ity, w hich differs from th atof other metals of the same bulk, and thus rendersthe detection of counterfeits easy by a practised hand.

T h e beau ty of the m etals adds to their value forpurposes of utility and ornament, but perhaps not totheir value as money; and hence I have not embracedthat quality in the foregoing enumeration.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 23/341

CURRENCY AND BANKING.

CHAPTER II .

OF THE DISTRIBUTION OF THB PRECIOUS METALSTHROUGHOUT THE COMMERCIAL WORLD.

A L L the gold and silver annually produced in the

four qu art ers of the globe, an d not required for con-sumption in manufactures or for currency in the coun-tries w here produc ed, are in the c onstant course of dis-tribution throughout the commercial world in ex-change for commodities which are more desirable tothe producers thau the metals themselves; and w he nthus distributed, they are liable in common with thatportion of the pre-existing mass which retains theform of coin an d bullion, to such further ch ang es of

place as the w an ts and circumstances of each particu-lar coun try m ay require. In these distributions, eachcountry does not equally participate, but each d ra w sto itself that proportion of the whole quantity whichis called for by the extent of its wealth, its population,its commerce, and the state of confidence or creditex isting am ongst its inha bitants . A rich nation, coete-ris parib^s, will require more gold and silver than

a poor one— a large population m ore than a sm allone— a nation carrying on much trade m ore than onew hich carries on little— and a n ation w here confi-dence and credit are circumscribed, more than one inw hich th ey are ex pa nd ed . T he first three of thesepropositions are self-evident. T he fourth needs per-haps some illustration, and as I wish to leave nothingin dispute as I go along, I w ill state m ore plainlyw ha t is mean t by it , w hich is, that in a country w here

no credits or comparatively few are given on the saleof property or merchandise, and where consequentlypayments are made entirely or chiefly in coin on thedelivery of the articles sold, a larger amount of gold-and silver is required, than in another country of equal

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 24/341

6 A TREATISE ON

wealth, population and trade, in which sales are usu-ally or frequently made on credit.

What proportion the supply of the precious metalswhich each country secures to itself as a circulatingmedium bears to its wealth, its population, its trade,or, to the existing state of confidence or credit, itwould not be easy to ascertain: nor is it indeed neces-sary that it should be ascertained, as far as any prac-

tical good can result from the know ledge. Thosewho carry on the operations of trade will take carethat a country has neither too much nor too little ofthem, and it may be assumed as a safe position, thatwhen the precious metals neither flow out from acountry in which there are no gold or silver mines,nor flow into it faster than is incident to her additionalshare of the new annual production of the mines, she

has her exact proportion. These proportions, w henonce attained as nearly as the nature of circumstancesw ill permit, establish w hat may be called the gene-ral level of currencies, and it is to this level, as to aspecies of standard, that reference is made, when wesay that money like w ater w ill find its level. It istrue, that owing to the constant production of themines, w hich may at times occasion unequal distri-butions, or, distributions other than through the ac-

customed channels, as was the case after the revolu-tions in Spanish America took place, which caused tobe sent first to the United States or England, themetals w hich formerly all w ent to Spain, as w ell asto a great variety of other circumstances which dis-turb the currency of particular countries, this levelmay never be a perfect one. It is sufficiently so, how -ever, for all purposes of reasoning upon it, and per-

haps as much so as fully w arrants the figure by whicha fluid-like property is ascribed to the precious metals.The surface of the ocean is never free from undula-tion, and the daily operation of the tides is constantlyinterfering w ith its level, as well as w ilh that of rivers.Moral causes, operating like the physical causes which

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 25/341

C U R R E N C Y A N D B A N K I N G . 1

influence the m ovem ent of the w aters, operate up ongold and silver, in driving them from one place to ano-ther, but it is easily to be seen, that were the extent ofwealth, population, commercial transactions, and con-fidence, in all countries to remain the same for a longperiod together, and were the new productions of them ines to be distributed in d ue proportions, and theold stock in each cou ntry to be diminished by con-

sumption in an equal ratio, gold and silver wouldassume such a uniformity of exchangeable value, asto arriv e at a perfect state of quiescence. Indeed , asit is, gold and silver are of all commodities the leastlikely to be ex po rted from an y cou ntry , ex cept fromthose in which they are produced, and where of con-sequ ence they form a portion of the produce of theland an d labor of the peop le, as iron and lead do in

some other cou ntries; or, from those w hich , in ad di-tion to their supply for the purpose of currency, havepossessed them selves of an am ou nt specifically in-tended for ex portation to countries hav ing produc tsnot procurable by any other means than by purchasew ith gold and silver. * W e m ay therefore conclude,tha t a level do es ex ist, created as w ill be seen he re-after, b y the imp orts and e x ports of commo dities otherthan the precious metals themselves, tow ards w hich

the currencies of all coun tries ha ve a perpe tual ten-dency, and from which, if th.ey do not precisely con-form to it, they do not greatly depart.

* From the period of the Independence of the United Statesup to about the year 1823, nearly all their im ports from Chinaand India were paid for by an exportation of silver dollars,brought into the country in addition to the supply required forthe currency. Since the year mentioned, the chief part of the

China and India cargoes, are paid for by credits or bills onLondon, exports of manufactures, and by coin procured inEurope.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 26/341

8 A TREATISE ON

CHAPTER III .

ON THE RELATIVE VALUE OF GOLD AND SILVER.

G O L D and silver, like all other com m odities, ha veeach their ow n peculiar value founded upon the im-

mutable law of supply and demand, by which al lva lue s are determ ined. T h e scarcity of the one com -pa red w ith tha t of the oth er, in connection w ith thedifference in their respective costs of production, thatis, of the ex pen ses of mining and sm elting the ore, andof refining the m etal, establish betw een them a ve ryw ide difference as reg ard s their relative va lue . A nounce of pu re gold ha s alw ay s been, and prob ablyalw ay s w ill be, w orth more than an ounce of puresilve r. B ut the ratio of this difference, it m ust bemanifest, is not fixed by any law of nature, any moretha n the ratio betw een any tw o other comm odities.Nature does not say, that an ounce of gold shall al-w ay s be w orth so ma ny ounces of si lver, any morethan she says that a pound of copper shall always beworth so many pounds of iron, or a pound of cottonso many pounds of flour, and hence it is clear, that

there is no law of nature applicable to gold and silver,w hich is not equa lly applicable to all other com m odi-ties.

What nature, however, has left undone, man in hislimited w isdom ha s attem pted to accom plish, by theenac tme nt of law s fixing the ratio at w hich gold an dsilver shall be ex cha ng eab le for each other. Th esel a w s , when first enacted,were no doubt founded upon

the observation of the fact, that in the general m ark etof the commercial world, these two metals had, forlong periods to gether, preserved som ething like a fixedproportion, and it w as no doubt conceived, that ch ain-ing them together by statute, w ould preven t themfrom ever separating.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 27/341

CURRENCY AN D BANKING. 9

W e learn from A da m Sm ith,* tha t prior to the dis-covery of the Am erican mines, w hich first b egan toshow its effects som ew here about the y ea r 1570, inthe diminished value of both the precious metals bythe new and annually augmenting supplies whichw ere derived fro n tha t fruitful source , the valu e ofpu re gold to pure silver w as established in the diffe-rent mints of Europe, at proportions varying from

one to ten , to one to tw elve; that is, one ounce of pu regold, w as declared to be the equivalent of ten to tw elv eounces of pu re silver; and in their respective coinagesthese proportions w ere consequently observed. A tabou t the middle of the 17th cen tury, tha t is, ab ou tthe year 1650, the ratio between gold and silver cameto be regu lated in the proportion of one to fourteen,and one to fifteen ounces of silver, no doubt occasionedby the fact, that although both metals had become

mo re ab un da nt in proportion to the dem and , and ha dboth been depreciated below their former va lue, yetsilver had depreciated more than gold, to an ex tentthat had created new proportions in the general m ar-ke t, w hich it w as the design of the n ew law s to followup .

From the period last mentioned, there does not ap-pear to have been any material change in the relative

value of gold and silver in the general market of thetrading world prior to the beginning of the presentce ntu ry , w he n a further depreciation of silver in refe-rence to gold began to show itself, so that by the year1S20, an ounce of gold came to be worth near sixteenounces of silver, of w hich the consequence w as, tha tall the gold coins of the United States, where the mintproportion had been fixed at one to fifteen, were ex-

ported from the cou ntry, to be ex cha nge d for theirproper equivalent.!

* Wealth of Nations, Book I. Chap. x i.| In corroboration of this fact, the following statement of the

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 28/341

10 A TREATISE ON

The author believes that he was one of the first, ifnot the first, writer in this country who called the at-tention of the public to this n ew c han ge , and ap pr e-hensiv e at the time, tha t the legislative folly of attem pt-ing to establish by law what nature herself could notestablish, would be repeated by a new enactment, heurged in D ecember, 1821, upon the late M r. L ow nd es,a representative in congress from South Carolina, andchairman of the committee of finance, the expediencyof abo lishing the coinage of eagles and their fractionalparts , and of substituting in their place new pieces, tow eigh respectively an oun ce, a half ounc e, and a qu ar-ter of an ounce of standa rd gold, un de r the full convic-tion that they would soon be introduced into circula-tion at their proper equivalent, without involving usin the absurdity of hav ing tw o legal tenders.* T h earguments presented to Mr. Lowndes in conversation

w ere at his particular request reduced to w riting, to-gether with answers to two points raised by him, andwere published in the National Gazette of 26th Janu-ar y , 1822. A copy of this pap er w ill be found in theAppendix , marked A.

The death, in the course of the last mentioned year,

coinage of Gold by the mint of the United States, at, and aboutthe period referred to, is adduced.

1 8 1 8 ,

1 8 1 9 ,1 8 2 0 ,

1 8 2 1 ,

1 8 2 2 ,

1 8 2 3 ,1 8 2 4 ,

$242,940,258,615,

1,319,030,189,325,

8 8 , 9 8 0 ,

7 2 , 4 2 5 ,9 3 , 2 0 0 .

This diminution in the coinage of gold after 1820 arose fromthe circumstance that nobody w ished to import gold into the

country to have it coined into eagles at ten dollars each, w henthe gold contained in an eagle was worth more than ten dollars** The ducat of Holland is current all over the continent of

Europe at its fair equivalent. Gold in France circulates at themarket rate of premium, silver being the ordinary currency.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 29/341

CURRENCY AND BANKING. n

of Mr. Lowndes, who was one of the few individualsin con gress w ho ha d studied the subject of the co inag e,appeared to suspend the action of that body in regardto the alteration of the m int regulation s, an d altho ug hseveral propositions w ere at different periods sub se-quently submitted, yet nothing was done until the28th of Jun e, 1834, w hen the law usual ly kno w n asthe gold bill w as passed. A short history of theseproposit ions w as dr aw n up by the auth or in the lastnamed year, and as i t may be of service to those whoha ve a desire to stud y the subject, ex tracts therefromhave been placed in the Appendix marked B.

In connection with this subject, it may not be amissto remark, that the proportion of one to fifteen or six-teen in the relative value of gold to silver, does not byan y m ean s w ar ra nt the inference tha t there is jus t fif-teen or sixteen times as much silver as gold in exis-

tence. A da m Sm ith advan ces conclusive argu m entsto show that the qu an tity of silver at the time he w rotewas far greater than the proportion which it bore togold called for, and indeed any one may be convincedof this fact if he will reflect upon the very small valueof gold com pared w ith silver, tha t is consum ed in plateand ornam ents. T he relative value of no tw o com -modities determines their relative quantities, and it iseasy to be perceive d, tha t if a barsel of flour w erew orth ten dollars, and a bo x of Spanish segars tw en tydollars, it would not necessarily follow that there werein existence only tw ice as m an y barre ls of flour asthere were boxes of segars .

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 30/341

12 A TREA TISE ON

CHAPTER IV.

OF T HE BALANCE O F TRAD E, OR OF TH E CAUSES WH ICHOCCASION T H E TRANSMISSION OF T HE PRECIOUSMETALS FROM ONE COUNTRY TO ANOTHER.

IN a preceding chapter, it w as stated that the pre-cious metals are distributed by the operations of com-merce throughout the trading w orld, in such a w ayas to establish what is called a general level of cur-rencies. I shall now proceed to show the mode byw hich this distribution is accomplished, w hich is ac-cording to the laws of what is termed the balance oftrade.

It must be manifest to every observant mind, that

even under the most perfect level which the curren-cies of all commercial nations can attain, that is, undersuch a state of things as may be imagined where nomotive of profit could lead to the importation or ex-portation of the precious metals, except as relates tothe annual production of the mines, the prices of othercommodities will not be in all countries the same.Were this the case there could be no commerce, for

the only object of commerce is to transport commodi-ties from countries where they can be purchased fora comparatively small quantity of gold and silver; thatis, at a comparatively low price; to other countrieswhere they can be sold for a greater quantity of goldand silver; that is, at a higher price.* Any one can

* The reader will be pleased to keep in mind, that price inpolitical economy is the value of a thing expressed in money

only, and therefore differs from the term value, which expressesthe worth of things as compared with other things than gold andsilver. Th us w e w ould say that five dollars is the price of ahat, where money is to be paid for it, but we would say thatfive pairs of shoes are the value of a hat, if the hat is to be paidfor in that many shoes.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 31/341

CURRENCY AND BANKING. 13

perceive that iron would not be imported into theU nited States from E n gl an d unless it could be soldhere at a higher price than it cost at the place of pro-duction , and th at cotton w ould not be ex po rted from theUnited States to Europe unless it could be sold thereat a higher price than it could be purchased for here.The prices of different articles, it is self-evident, inevery country, are regulated by causes peculiar to

them selves, such as the soil, climate, w ag es of labo r,degree of skill required, extent of population, capital,an d tax ation ; an d this it is w hich sets in mo tion thew hole m achinery of com merce. E v en in the case ofbarter w ith savag e nations, although gold and silverbe absent, yet the trader has reference in his calcula-tions to the metallic stan da rd, in order to enab le himto determ ine h ow m uch he can afford to give of w ha the has to dispose of, in exchange for the commodities

which he is to receive in payment.The foreign commerce of a nation is usually of two

kinds. The Jirst is that w herein the ex port and im-port trade are carried on by the sam e individu al, inthe sam e vessel, and in the prosecution of the sam evo ya ge . Such is the trade of the Un ited States w ithmost parts of the West Indies, South America, Africa,some parts of India, and some other countries. T h e

imports from those regions consist of the articles pur-chased with the proceeds of the outward cargoes, andthis trade is strictly an exchange of equal values, andalthou gh it m ay ex hibit w ha t is called a balan ce oftrade on one side or the other, yet. it calls for no pay-m ent. T he sam e is true of the w hale and other fish-eries, w herein althou gh the am oun t imp orted m ay farexceed in value the amount exported, yet no balanceof trad e is left to be pa id, the difference be ing m ad eup by the value of the labor expended by the crew,of the freight earned by the ship, and by the profits ofthe enterprise.

T h e second trade is that w herein the ex ports andimports are made by different classes of merchants,

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 32/341

14 A TREATISE ON

without any previous consultation or agreement withone another. Such is our trade w ith Great Britainand most of the other maritime nations of E urope.The exporters of cotton, rice, tobacco, flour, and theother commodities which form the bulk of our exportsto Europe, are very rarely the same individuals whoimport the dry goods, hardware, and the infinite vari-ety of other manufactures and productions which con-

stitute the bulk of our imports from Europe. Theformer ship their cargoes to foreign countries, withoutany knowledge of the quantity or value of the com-modities w hich the importing m erchants intend to or-der from abroad, and the latter send their ordersabroad far goods withoi.it any know ledge of the am ountfor w hich the exported cargoes w ill be sold. Theformer class, that is , the exporters, get paid for theircargoes by drawing bills of exchange upon the pro-ceeds in the hands of their foreign correspondents;and the latter class, or the importers, pay for theirgoods by purchasing and remitting these same bills.

Under a course of operations carried on by so manyindependent traders, it would indeed be miraculous ifthe exports and imports should be so exactly equal asto leave no balance one w ay or the other. In truth,experience shows that the exports will sometimes ex-

ceed the imports, and that sometimes the imports willexceed the exports, leaving a balance of trade in theformer case in favor of the country, and in the lattercase against it.

Let us now suppose, that in a given country wherethe currency is at its proper level, where no gold orsilver flow s out or flow s in, and w here consequentlyexchange w ould be at par, an excess of imports should

take place. What w ould be the first effect? Theanswer must be, a demand for more bills of exchangethan are for sale in the market, the effect of which is arise in the rate of exchange above par, which obvi-ously holds out an inducement for the exportation ofcommodities for w hich a sufficient inducement did not

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 33/341

CURRENCY AND BANKING. 1 5

previou sly ex ist. A rise in the exch ang e of one ortwo per cent, may sometimes determine shipments,which without such rise would not have been thoughtof; not that so small a profit w ould of itself induceshipments, but because one or two per cent, added tothe profit which might have been made without suchaddition, would elevate the gain to the height of theaverage mercantile rate of profit requisite to warrant

a shipm ent. A profit in adv anc e is a pow erful stim-ulus to exportation, especially where two thirds orthree fourths of the capital em ployed in the pu rchase ofthe ex ported comm odities can be imm ediately replacedby the sale of a bill of ex cha ng e. T he additional de -m an d , therefore for bills, to assist tow ard s pay ing th ebalance is met, we will suppose, at once by additionalex ports, it sometimes even happ ening that the remit-ting merchant, to save, as it is called, the premium on

bills, becomes himself an exporter.T h u s far it is manifest tha t the balan ce of tra de

occasions no exportation of the precious metals, andtha t conseq uently the gen eral level ef currencies isnot disturbed. B ut it m ay hap pen that the increasedde m an d for expo rtable comm odities arising from theaugmented premium on exchange, may raise theirprice to an extent equal to the rise in the price of bills,

and thus pu t an end to their ex portation, by takinga w a y the additional profit. A new ex pedien t is thenresorted to by capitalists to take advantage of the pre-m ium on ex chan ge, w hich is to obtain a credit ab roadup on w hich they m ay dra w bills, under the calcula-tion that at some future, not very distant period, theyw ill be able to replace the funds a t a low er rate ofex ch an ge , and thereb y realise a profit by the op era-tion. T he transmission, too , of public securities, b an k ,railroad, and canal stocks, and the extension of cre-dits by the consent of the foreign creditors up on allow -ing interest for the extended term, are all well knownlevers in the mechanism of trade, (to say nothing ofba nk rup tcy) , by w hich the tendency of an unfavora-

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 34/341

16 A TREATISE ON

ble balance of trade to cause an ex po rtation of theprecious m etals is frequently n eutralised. B ut it m ayhap pen , ho w eve r, that all these m easures com binedw ill not keep do w n the price of bills of ex cha ng e tothe rate w hich w ill render them more adv antag eou sto rem it than gold or silver. T ha t an ex po rtation ofthe precious m etals w ill then comm ence is quite ap pa -rent, bu t com pared w ith the w hole balance that ma y bed u e, it w ill be ex ceedingly trivial, as I w ill proceedto show.

W e w ill supp ose ten millions of dollars to be thecirculating m edium of the supposed debtor cou ntry,and that that is the amount which is requisite to cir-culate her commodities and to maintain her currencyat an equivalency with the currencies of other coun-tries. No sooner does this quantity become dimi-nished by the ex po rtation of an y pa rt of it , than a

scarc ity of m on ey beg ins to be felt. A scarcity ofmoney invariably occasions a fall in the prices of com-modities, as every body knows, and that fall operatess.s an incentive to exportation, inasmuch as domesticproducts, which were before too high to export , willnow afford a profit. A fall in the price of cotton ofone cent a pound has sometimes occasioned the expor-tation of imm ense qu antities in a short perio d; and it is

very clear that there is a price at which almost anyarticle might be ex ported to adv an tage , and that agra du al diminution of the currency , if continued longen ou gh , w ill even tually establish that price. It is idleto say that possibly the debtor country may not haveon ha nd a sufficiency of pro ducts to discha rge thedeb t, and that therefore she m ust be draine d of herprecious metals to the last dollar. T his can nev er be .If her w eal th or her pow ers of product ion had not

been co m m en sura te to her dem and for foreign com -m odities, she co uld not ha ve had sufficient credit torun deeply into debt. A t all eve nts, she w ould hav eon han d a large portion of the foreign com m oditiesin the purchase of which the debt was incurred, anda scarcity of money might even bring down prices so

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 35/341

CURRENCY AND BANKING. 17

low as to render the exportation of foreign commodities a profitable trad e. It m ight eve n be an object tosend back to the place of production the very commo-dities, the importation of which created the unfavo-rable balance . * It is quite probale that a very sm allreduction of the amount of coin would produce sucha fall in th e prices of com modities as w ould lead totheir exportation to an extent adequate to keep downth e price of bills so as to prev ent an y further ex po r-

tation of the preciou s m etals; bu t if this should not bethe case, and if the scarcity of money should continueto increase, those who had remittances to make wouldeither become ban krup t and m ake no remittances atall, or becom e so e m barra ssed as to default in theirpu nctu ality, e ither of w hich events w ould diminishthe demand for funds abroad, and stop pro lanto theex po rtation of gold and silver, t A nd here it m ay berem arke d by the w ay , that a real scarcity of m oneyis always accompanied by an artificial scarcity whichagg ra va te s the effects of the former. If, for instance,a million of dollars in coin be exported, so as to pro-duce an outcry about scarcity of money, timid peopleand speculators will withhold another million fromcirculation; the former because they are afraid to lendit, and the latter because they expect to profit by for-cing down the prices of property and commodities to

a still low er poin t, the effect of w hich w ould be todiminish the demand for the exportation of coin byreducing the prices of commodities.

B ut indepen dent of the tendency of the causes above

* British goods have frequently been sent back from the Uni-ted States to England, as affording the best market for them,and it is a very common thing for vessels to bring back from

the W est Indies part of their outw ard cargoes, ow ing to theirbeing w orth more at home than they could be sold for abroad.t All the propositions here laid dow n, have recently been

fully established as practical truth s in the United States , andespecially at New York even to the reshipping of British goodsto England.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 36/341

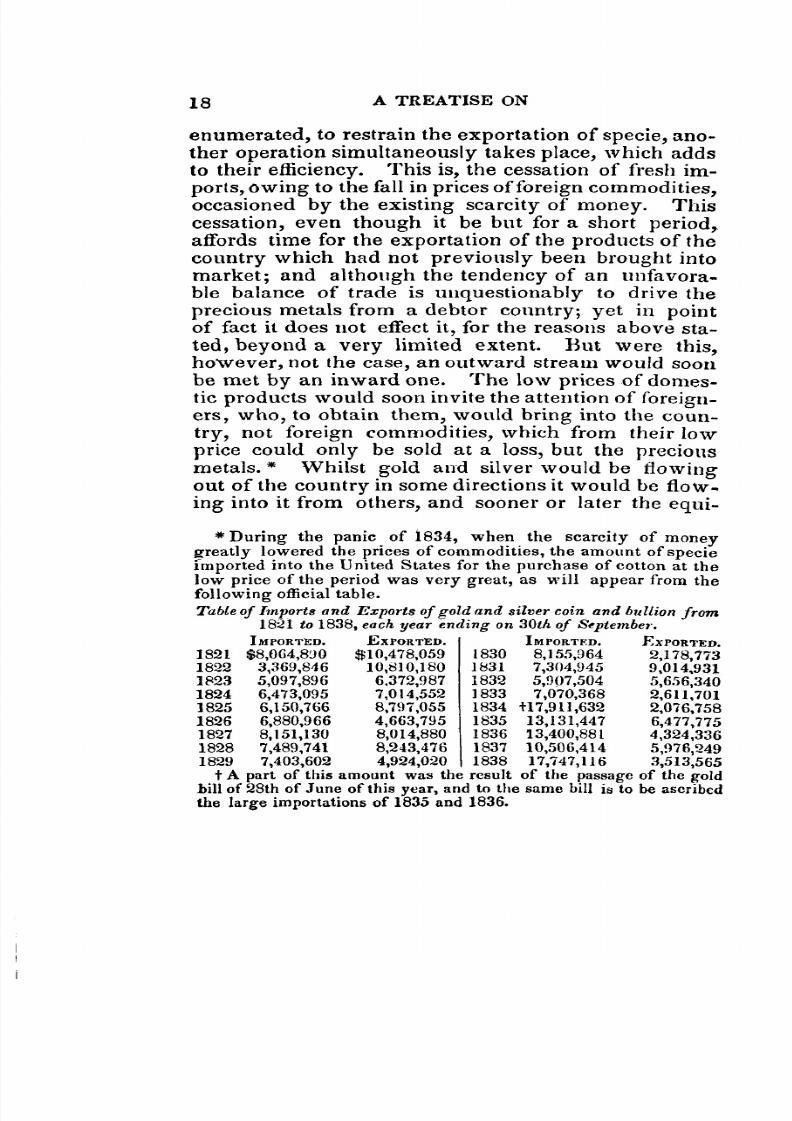

18 A TREATISE ON

enu m erate d, to restrain the ex portation of specie, ano -ther operation simultaneously takes place, which addsto their efficiency. T h is is, the cessation of fresh im -ports, ow ing to the fall in prices of foreign com m oditie s,occasioned by the ex isting scarcity of m oney. T hiscessation, even tho ug h it be but for a short period ,affords time for the ex porta tion of the prod ucts of thecountry which had not previously been brought intom ark et; and although the tendency of an unfavora-

ble balance of trade is unquestionably to drive theprecious m etals from a debto r cou ntry; ye t in pointof fact it does not effect it, for the reasons above sta-ted, beyo nd a very limited ex tent. Bu t w ere this,however, not the case, an outward stream would soonbe m et by an inw ard one. T he low prices of dom es-tic products would soon invite the attention of foreign-ers, who, to obtain them, would bring into the coun-tr y , not foreign com m odities, w hich from their low

price could only be sold a t a loss, bu t th e prec iousm etals. * W hilst gold and silver w ould be flow ingout of the c oun try in some directions it w ould be flow -ing into it from oth ers, an d sooner or later th e eq ui-

* During the panic of 1834, when the scarcity of moneygreatly lowered the prices of commodities, the amount of specieimported into the United States for the purchase of cotton at thelow price of the period w as very great, as w ill appear from thefollowing official table.Table of Imports and Exports of gold and silver coin and bullion from

1821 to 1838, each year ending on 30th of September.

1 8 2 1

1 8 2 2

1 8 2 3

1 8 2 4

1 8 2 5

1 8 2 6

1 8 271 8 2 8

1829

I M P O R T E D .

$8,064,81)0

3,369,8465,097,896

6,473,0956,150,766

6,880,966

8,151,1307,489,741

7,403,602

E X P O R T E D .

S I ,478,059

10,810,180

6,372,987

7,014,5528,797,055

4,663,795

8,014,8808,243,476

4,924,020

1830

1831

1832

1833

1 8 3 4

1835

18361837

1838

I M P O R T E D .

8,155,964

7,304,9455,907,504

7,070,368+17,911,632

13,131,447

13,400,88110,506,414

17,747,116

P^XPORTED.

2,178,773

9 , 0 1 4 , 9 3 1

5 , 6 5 6 , 3 4 0

2 , 6 1 1 ,701

2,076,758

6,477,775

4 , 3 2 4 , 3 3 65 , 97 6 , 2 4 9

3 , 5 1 3 , 5 6 5

t A part of this amount was the result of the passage of the goldhill of 28th of Jun e of this ye ar, and to th e same bill is to be ascribedthe large importations of 1835 and 1836.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 37/341

CURRENCY AND BANKING. 19

l ibrium would be restored, and the double currentarrested.

It may here be remarked, that the accounts currentbetween nations in their commercial dealings, that is,between the individual merchants of one country andthose of anothe r, w hich is the only sense in w hichwe speak of commercial transactions between nations,are not periodically settled like the accounts betweenindividuals of the same country, which are generally

settled by the actua l pay m en t of the balanc e. N a -tional accounts curre nt are nev er settled. T he balancemay be one way to-day and another way to-morrow,an d as there is no gen eral pa y da y, like the first ofJanuary, upon which a general balance is struck,facilities are afforded for w ar ding off such a pressureon the bill ma rke t as w ould ex ist if a pe riodicalpunctuality were rigidly enforced.

Having thus given a detail of the operations whichwould take place under an unfavorable balance oftrade, I will say a few words upon those which wouldoccur und er a favorable balance. An d in doing this,w e w ill take for illustration the sam e coun try tha t w ehave just been considering, and will suppose that anex cess of ex ports should take place. Of such a stateof thin gs, w h a t w ould be the first effect? T he an sw ermust be, a fall in the price of bills of exchange in the

m arket. M ore m oney w ould have to be dra w n forthan the amount required to pay for the imports, andthe competition of the bill drawers might reduce therate of ex chang e d ow n to the point at w hich it w ouldbe more profitable for them to import gold and silverfrom ab roa d, than to dra w bills. Still the q uan titythat would be thus imported, would be comparativelylimited. T h e ve ry ex istence of a foreign balance in

favor of the country, would be proof of the abilityof the nation to consume an additional amount offoreign commodities, and the gain which could bemade by the importing merchants of one or two percent, o n the ex ch ang e, by buy ing bills below par,in

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 38/341

2 0 A TREATISE ON

addition to the usual profits, would invite to more ex-tensive importations. Additional importations w ouldin fact take place, and the supp ly of these new com-modities would be met by a corresponding demand onthe pa rt of those w hose m ean s of' consum ption fromex traordinary crops or ex traord inary profits on theirbusiness, had thus become augmented.

Bu t a fall in the price of bills w ould ha ve a ten -dency to discourage the exports of domestic products,

and this discouragement, in its turn, would have theeffect of raisin g the price of bills by a dim inution ofthe supp ly in the m arket, and thereby of rem ovingthe motive for the importation of the precious metals.The importation of gold and silver, however, shouldit commence, would make money plentier than before,and thus raise the prices of com mo dities, foreign asw ell as dom estic. T his rise in price w ould encouragethe importation of foreign commodities, because tbey

could be sold at an increased profit, w hilst it w oulddiscourage the exportation of domestic products, bywhich means a part of the specie previously importedwould again be exported, in preference to the domes-tic products, w hich could only be procurable at anaug m ented price. It thu s app ear s, that a favorablebalanc e of tra de , althou gh it has a tendency to bringthe precious metals into a country, yet in point of fact

it does not effect it bey ond a limited am ou nt, resem -bling in this particular, the former case of an unfavo-rable balance; two streams might be flowing, one intothe country and one out of it, and sooner or later theequilibrium would be restored, and the level regained.

Thus it would be impossible to retain in any coun-try any more than its true share of the aggregate massof the gold and silver of the trading world, or to ex-clude from it an y portion of that share . N o h um an

contrivance or legislation could possibly effect either,and hence all the efforts which have been made in allpa rts of the w orld to alter w hat the natura l law s ofcomm erce hav e decreed, by prohibiting the ex porta-

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 39/341

CURRENCY AND BANKING. 2 1

tion of the precious metals under heavy penalties, orby attempting to encourage their importation by pro-tective or prohibitory duties on m erchand ise, or. byresorting to any other expedient, have proved utterlyfutile. M on ey , as has been said, like w ater, w ill findits level, and alth ou gh the former like the latter, m ayfor a period be forced into un na tural chann els, the de -viation cannot long continue.

And he re, I w ill take occasion to rem ark , that informing an estimate of the comparative value of theexports and imports of the United States, the customhouse returns, as they appear in their aggregates, arebut imperfect guides to determine the balance oftrad e. T he value of the ex po rts given is their valu eat the time and place of shipment, as furnished by theshipp ers un der o ath , in the form of manifests. T he

va lue of the im ports, is their cost ab roa d, as ascer-tained by the invoices, also furnished un de r oa th,subject to such revision by the custom house apprai-sers as m ay , in case of suspected fraud in the va lua-tion of goods chargeable with ad valorem duties, bedeem ed right and ju st. Th ese foreign invoices em -brac e the cost of the articles, and w hat are called theshipping charg es, that is, the charge s w ithou t thepayment of which they could not be put on shipboard,

but include no frieght, or insurance; and where theyare made out in Brazil, Buenos Ayres or other coun-tries, w here a depreciated paper currency exists, du eallowance is made for the depreciation.

N ow , as cargoes shipped abro ad from the UnitedStates, are burthened with the expenses of freight andinsurance, their value at foreign ports must generallybe augm ented by the am oun t of these expenses and

the profits on the vo ya ge , and consequen tly the nettproceeds of their sales mu st alw ay s furnish' a fundad eq ua te to the purchase of foreign com modities to agrea ter value tha n their cost at hom e. On this ac-count it necessarily follows, that where the trade of acou ntry is profitable, its imp orts will alw ay s exceed itsex po rts, and this too, jus t in the degree tha t it is profi-

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 40/341

22 A TREATISE ON

table, and nothing is clearer than that if the voyageout and home does not give a greater amount of im-portslhan of exports, the trade w ould be abandoned.Of this proposition there can be no dispute, and it isquite probable that an export of a hundred millions ofdollars would purchase abroad as many commoditiesas would show an import on the custom house booksof a hundred and twenty or more millions of dollars,

thus overthrow ing the theory of that class of reasonersw ho maintain that the balance of trade is against acountry when it imports more than it exports, andw ho consequently believe that a "nation is grow ingpoor when she is in reality growing rich.

But to make this matter perfectly plain, I will illus-trate it by a practical case that every body can under-stand.

A merchant in Philadelphia purchases one thou-sand barrels of flour at eight dollars per barrel, andships it to the West Indies. The custom house booksin this case would show an export of eight thousanddollars. On the arrival of the cargo abroad it sellsfor twelve dollars per barrel, and after paying freight,duties, commissions, and all other charges, leaves thenett proceeds ten thousand dollars. This sum isinvested in coffee, and brought home, where it is

entered upon the custom house books as an import ofthat amount. Here, then, w e w ould have an exportof eight thousand dollars and an import of ten thou-sand dollars, showing a clear gain of two thousanddollars, without leaving any balance due one way orthe other. A stronger illustration than this even, is tobe found in the operation of our w haling ships. Avessel with a cargo consisting of nothing but provi-sions sufficient to feed a crew for a voyage, and asmany staves, hoops, and headings, as will make casksenough to hold a cargo of oil, clears out at New Bed-ford for the South seas. The custom house booksshow an export of ten thousand dollars, perhaps, audwhen the ship returns with a cargo of oil, they giveus an import of fifty thousand doflars, thus show ing

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 41/341

CURRENCY AND BANKING. 2 3

what the superficial reasoners above referred to wouldcall a balance of trade again st the coun try of fortythousand d ollars, but w hich is a clear evidence of again to the owners and crew, and consequently to thecountry.

Bu t ev en if the custom h ouse books w ere to fur-nish accu rate statem en ts of the nett proceeds of thesales of the cargoes exported, as well as of the foreign

cost of the hom ew ard cargoes, they w ould not be suf-ficient to enable us to form a correct estimate of thereal balance of trad e. Debits and credits are crea tedin the foreign trade of every cou ntry , w hich nev erap pea r on the custom house books. Specie is im -ported and exported by emigrants and passengers intheir trunks, or secretly shipped by merchants to avoidpenalties or odiu m , or, ex posu re of their ope rations.Goods are sm uggled, and others are purch ased w ithfunds earned by vessels abroad, engaged in the carry-ing trad e, and thereby aug m ent the imp orts, w hilstships are frequently sold ab roa d, and thereb y au g-men t the ex ports. Large am oun ts of property arealso ex ported from some coun tries for w hich no pro -ceeds are to return, or at least, to return at an earlyday, such as happens in the case of foreign subsidies,the m aintena nce of troops and nav ies ab road , the

transmission of revenues to non-resident capitalists,and funds for the expenses of travellers in foreigncou ntries. To these ma y be add ed losses at sea, or byfires abr oa d, the bank rup tcy of the persons to w ho mthe ex ported com mo dities are sold, and investm entsin foreign loans and joint-stock co m pa nie s. In m ostof these cases property of some kind or other is sentabroad which appears on the custom house books

amongst the exports; and, although in many of themthe actual transmission for these specific objects maybe in the form of bills of exchange, yet it is manifest,that these bills could only be dr aw n up on shipm entsof property.

In the foregoing remarks it has been laid down asan axiom, that the price of bills of exchange is deter-

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 42/341

24 A TREATISE ON

m ined by the balance of trad e. Strictly speak ing,ho w ev er, this is not alw ay s the case, for this balanceis liable to be modified by w h at is called the b alanc eof pa ym en ts; and in tru th this latter principle it isw hich.regulates the daily rate of the exch anges. Ifall the merchandise exported and imported was to beimmediately paid for at the time of its changinghands , the balance of trade and the balance of pay-

m ents w ould be identical. B ut, in the intercoursebetween nations we know that this is not always thecase, and that circumstances occur to prevent theim m ediate influence of the balance be tw een im portsand exports from acting directly upon the exchanges.Amongst these circumstances are the following:—

1. Where the imported articles are bought on acredit, and are to be paid for at a distant time, whilstthe exported articles are sold for cash, or vice versa.

2. W he re in the case of both impo rts and ex portsthe sale is on credit, bu t the credits are not of thesame length.

3. W he re the articles shipped abr oad from one ofthe countries should not meet with a ready sale, andshould be kept on han d for a length of time w ithoutbeing drawn upon, whilst on the other side a promptsale is made, and bills drawn for the proceeds.

In either of these cases , the o peration of the balan ceof payments on the exchanges might be such as notonly to neutralise for a time the operation of thebalance of trade , but to turn the ex changes againstthe country w hich had the balance of trade in itsfavo r. A case in point can read ily be referred to.

If an account current were to be made out of thepas t state of debits and credits betw een the Un itedStates and Great Britain, it would no doubt be found,that from the date of planting the first British colonyin this hemisphere, we have owed a balance of tradethat has never been discharged, and w hich at timesmay have amounted to a hundred millions of dollarsor m ore ; and yet, ow ing to the credit tha t has beenex tended to u s, by w hich the pay-d ay has been de-

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 43/341

CURRENCY AND BANKING. 2 5

ferred,the ex chan ge has not alw ays been against us,bu thas , on the co ntra ry, been so controlled by the balanc eof payments as frequently to have been in our favor.*

C H A P T E R V .

ON THE PRINCIPLES OF EXCHANGE.

BILLS of exchange are those commercial instru-ments by which a merchant in one country or placedirects money which is subject to his control inano ther cou ntry or place to be paid over to a thirdpa rty . In the com m ercial transactions of every na -

tion, some of the merchants become indebted to otherm erch ants in foreign coun tries for com m odities pu r-chased there upon credit, whilst some others havefunds in those foreign countries arising from the saleof cargoes disposed of the re. If bills of ex chan ge d idnot ex ist, the debtor class of these m erchan ts w ou ldbe obliged to incur the expense and risk of transport-ing coin or bu llion to foreign cou ntries in discha rgeof their debts, and the creditor class w ould also beobliged to incur the same expense and risk in import-ing coin or bullion in p ay m en t of their cargoes soldabroad. By this double transmission, the m erchan ts,and consequently the nations to which they belonged,w ould be losers to an a m ou nt equ al to. all the ex -penses and risks so incurred, together with intereston their capitals for the time they were out of theirreach . N or could this be avoided unless the im-

porters and exporters were always the same identicalindividuals, in which case the merchandise purchased

* For a table of Imports and Exports of the United Statesfrom 1789 to 1839, see Appendix F.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 44/341

26 A TREATISE ON

abroad would be paid for by the proceeds of them ercha ndise sold. B y the op eration , the n, of billsof exchange, the necessity of this double transmissionis entirely avo ided , and the funds ab ro ad , instead ofbein g sent ho m e, are transferred to those w ho ha vedebts to pay abroad, and who are thus exemptedfrom the expense and risk of sending coin or bullionin payment of their debts.

But this benefit, in which the whole nation partici-

pates , is not limited to the m ere applica tion of fundsin a n y given place to the pa ym en t of a deb t due intha t place. It m atters not w heth er the fund and debtboth stand on the bo oks of m erch ants at the sam eplace, or w hether the debt be due at Man chester andthe fund be at Pa ris. T he m agic po w er of bills ofexchange transfers the payer and receiver both toLondon, the great seat and centre of British and in-

deed of European commercial operations.But the merchants who make remittances of bil lsof exchange to foreign countries, to pay for merchan-dise purch ased the re, do not, it is manifest, proc urethose bills of exch ang e for noth ing. T he y m ust pur-chase them from those who have funds abroad todraw for, and in doing this they will endeavor toproc ure them at as che ap a rate as they can. It is,on the othe r h an d, the interest of those w ho hav e bills

for sale, to secure the highest price for them theycan, and it is this competition between buyer andseller that determines the market price, w hich, l ikethe market price of commodities, must always dependupon the proportion which the supply bears to thede m an d. If bills of ex cha ng e a re scarce, their pricew ill be hig h. If they are plen ty, their price w ill below . Th ere is , how ever, one peculiarity belonging

to a bill of ex ch an ge , w hich is not comm on to a nycom mo dity, and w hich oug ht alw ays to be kept inm ind in discussing th is subject. It is, that if it can-not be sold at a price that will suit its owner, he hasit in his power to avoid the necessity of a sale atgreat loss by importing his funds in coin; and if it

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 45/341

CURRENCY AND BANKING. 27

cann ot be purch ased at a price that w ill suit a p u r-chaser, the latter can avoid the necessity of a disad -van tageo us purchase by ex porting coin in paymentof his de bt. T h e ex istence of this pecu liarity placesa limit upon the fluctuations in the rate of exchange,w hic h cann ot for an y long period tog ethe r fall an dremain below par, or rise and remain above par, to agrea ter ex tent tha n to an am oun t equivalent to theex pe nse of tran sportin g the precious m etals from the

deb tor cou ntry to the creditor cou ntry. Fo r, if am ercha nt ow es a debt abroa d, and cannot procure abill of exchange at an advance above par equal to thefreight, insura nce , com mission, and brok erag e, an dto the value w hich he attaches to that certainty ofpu nctu ality in the fulfilment of his eng age m entabroad, which a set of bills of undoubted credit,sent by two or three different vessels affords, butwhich a shipment of coin cannot always furnish, howsolvent and prompt soever might be the underwritersin settling in case of loss, he w ill un qu estio nablytransmit coin as being the most economical mode ofm akin g a remittance.* An d so, on the other ha nd ,the drawer of a bill, if he cannot sell at a price whichw ill yield him as m uch m oney as the imp ortation ofcoin w ould do, taking into the acc ount, besides th echarges of importation, the interest for the time he

must wait before his money can arrive, and if moneybe scarce, the inconvenience or loss he w ould sustainby the delay , he w ill und oub tedly order his funds tobe shipped to him in coin, as the most ad va nta ge ou smode of getting them into his possession.

Of the correctness of these positions the re ca nn ot

* Specie was shipped from New York to England, at a los s,in October, 1839, in preference to bill3 at par, owing to the ap-

prehended difficulty of getting them discounted under the pres-sure of the London money market. Other shipments w eremade, at the same tim e, of specie, under the impression thatthe Bank of England was about to stop cash payments, in whichevent, the specie would have commanded a premium in London.The cost of freight and insurance on specie from the Un itedState3 to Europe, may be computed at one per cent.

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 46/341

2 8 A TREATISE ON

be a doubt, and w henever the market price of ex-change differs from these rates, it must have its causein one of the following circumstances.

If the exchange be above, it must either be that themerchants who have remittances to make are igno-rant of their business, and therefore pay more for abill than it is worth, or that small profits are notworth their attention, or that there is a penalty or adegree of odium attached to the exportation of coin

which they are not prepared to encounter, or that thepunctuality which is expected of them by their cor-respondents abroad is of a character that w ould notjustify the hazard of a miscarriage by a single ship.

If the exchange be below, it must be because theowner of the funds abroad cannot afford to wait thetime requisite for the transmission of the coin, orbecause in the actual state of the money market,money is worth to him more than the ordinary inter-est, or because there exists a penalty or a degree ofodium attached to the exportation of coin in the coun-try from which his fund is to be drawn.

It must, however, be remarked, that it sometimeshappens that bills are sold below the limits here de-signated in the following cases, viz:

1. Where the commanders of ships of war on for-eign stations have occasion to draw bills upon their

government, at ports of limited trade, or at which thecourse of trade does not call for such bills. I haveknow n a bill on the navy department draw n at aport in South America to be sold at twelve per cent,below the true par.

2. Where masters of vessels and supercargoes, atsuch ports, have not merchandise enough to fill uptheir vessels, and on that account find it for their in-terest to sell bills at a great discount, for the purposeof buying bulky commodities to bring home, andthereby earn a freight more than equivalent to theloss sustained on the bills.

3. Where masters of vessels enter such ports in dis-

7/28/2019 Currency and Banking - Raguet

http://slidepdf.com/reader/full/currency-and-banking-raguet 47/341

CURRENCY AND BANKING. 2 9

tress, and are obliged to draw bills upon their ownersfor necessary repairs.

In w eal thy countr ies , how ever, w here bankers areprep ared w ith large capitals devoted to speculations inbillsof exchange,great fluctuations from the par are notlikely to take place, inasm uch as bills can alw ay s bebought from or sold to them , by allow ing a small profitbeyond the ex penses of expo rting or imp orting coin.T he trade of a banker in E uro pe is to study the ex -chang es not only betw een the place at w hich he residesand all other places, but also between all those placesand each other, by w hich m eans he is generally en-abled, by a combination of operations, by selling billson one place and by bu ying them on anoth er, notonly to raise the fund w ith w hich he d eals, but torealise a p rofit. T h u s, for instance, if he reside a tLondon, and can sell a bill on Hamburgh at half per