Embed Size (px)

Citation preview

The BalTic Sea RegionCultures, Politics, Societies

Editor Witold Maciejewski

The BalTic Sea RegionCultures, Politics, Societies

Editor Witold Maciejewski

A Baltic University Publication

The purpose of this chapter is to identify the role of international trade in the countries and regions covered. The role of economic and political conditions in the creation of the frame-work for international trade is described. Also, some basic statistical figures on the structure of exports and imports are provided.

1. Reasons for foreign trade

There are also other explanations for trade. The concept of intra-industry trade, where countries exchange similar goods, is based on economies of scale in production and larger international co-operation within multinational companies. Some operations are then subcontracted out for countries, which have special advantages concerning some factors of production. Low labour costs are one of the factors that attract labour-intensive industries to move some opera-tions from their homeland to other areas. The practice of Scandinavian companies to move some production of components and semi-final products to the Baltic States, where labour costs are several times lower compared to the homeland of those companies, is one example. Intra-industry trade is part of exports and imports of all countries involved in that division of labour. That type of connection is defined as vertical intra-industry trade.

Another reason for exchange of similar products is related to different tastes and a wide spectrum of consumer preferences. For that reason, the Scandinavian states produce and exchange a wide set of goods that are produced in every country. Examples of this kind of horizontal intra-industry trade are works of art, clothing articles and others.

Economic DEvElopmEntInternational Trade 621

Comparative advantages of production

According to traditional international trade theories, countries differ with respect to the conditions of production, such as weather conditions, amounts of labour, capital and natural resources. This provides each country with a set of comparative advantages. On the basis of these advantages, countries tend to specialise in the production of particular goods and services. Specialisation in production also causes exports of goods and services for which the conditions of the particular country are best, and imports of other products that are more effectively produced in other countries. Traditional trade theories assume that factors of production are immobile and that goods can be freely exchanged across national borders.

49 International Trade Alari Purju

2. Foreign trade policy tools

Although the free trade of goods increases global welfare, individual countries have often intervened against free trade. Countries use several trade policy tools to protect domestic companies from competition of foreign companies. Two classic types of trade barriers are customs tariffs and quantitative restrictions.

Customs tariff is a duty imposed on a product. It may by a fixed duty per unit or an ad valorem duty charged as a percentage of the value of the product. In most cases tariffs are imposed on imports.

Quantitative restrictions such as import quotas restrict the imports of a certain product to a specific volume per year. An example could be quotas for the export of food products to the EU market that EU accession countries have been provided with.

Another type of non-tariff restriction is local content requirement (rules of origin), which determines the share of value added that should be produced in a particular country to make exports acceptable to the other country. In the case of textile and some other products of accession countries, the local content requirement protects the EU from imports from third countries that would otherwise be channelled through accession countries without that requirement.

There are also anti-dumping rules that are targeted to restrict the sale of products with inju-rious price levels. Anti-dumping rules are first of all applied against importers to a particular country or economic area.

Various kinds of export subsidies have been increasingly used in recent years, despite the fact that several international agreements in principle prohibit export subsidies on industrial products. For that reason, most subsidies do not specifically relate to exports but to domestic production. Those subsidies would increase exports, but at the expense of domestic taxpayers, and the welfare effect of export subsidies is negative.

3. Regional integration

The GATT – General Agreement on Tariffs and Trade – signed by 23 countries in 1947, came to pro-vide a framework for post-war trade liberalisation. A new organization, the World Trade Organization (WTO), has been established and the WTO Treaty was signed on 15 April 1994. That treaty includes the GATT Treaty and agreements reached during the latest round of negotiations.

There are several forms of economic integration based on similar rules upon foreign trade. A free trade area consists of a group of countries among which trade takes place freely, i.e. without tariffs or quantitative restrictions. At the same time each country retains its individual tariffs and quantitative import restrictions against countries outside the free trade area. The European Free Trade Association (EFTA) is an example of a free trade area. The EFTA

Economic DEvElopmEntInternational Trade622

Figure 169. Trans-boundary, small-scale trade creates a large market. Building materials ware-house at the Polish-Slovak border. Photo: Alfred F. Majewicz

was established in 1960 by countries staying outside the European Economic Community (EEC) founded by the Rome Treaty in 1958. Later several members of the EFTA joined the European Union (EU). An important free trade area is also the North American Free Trade Area (NAFTA), signed in 1993 and consisting of Canada, the United States and Mexico.

A customs union presents a higher degree of economic integration due to a common for-eign trade policy. The members of a customs union have a common external tariff wall and other common external import restrictions against countries outside of the customs union. The EU is first and foremost a customs union. The tariffs and quantitative restrictions on trade among member countries were banned and after a period of transition a common external tariff wall was set up. The further developments have made the EU a common market also with the free movement of capital and labour in addition the to free movement of goods and services.

There are two types of welfare effects related to joining a customs union. The trade cre-ation effect is due to the volume of new trade created by forming the trade bloc. The trade diversion is the volume of trade diverted from lower cost outside the customs union suppliers to higher cost partners of the customs union suppliers. Whether a customs union is good or bad depends on the difference between its trade creation effect and its trade diversion effect. In the case of the EU, most economists think that its trade creation has outweighed its trade diversion.

4. Foreign trade agreements in the Baltic Region

The foreign trade between the countries located on the shores of the Baltic Sea took place back in historical times. Several cities of the area belonged to the Hanseatic League in the 14th-15th centuries when trade flourished and there were many contacts between the cities.

After the Second World War, the iron curtain divided the area and conditions for for-eign trade were very different. The Scandinavian countries, at different speed, integrated with the Western World. Russia, Belarus and the Baltic States were part of the Soviet Union and participated mainly in the distribution of production between the republics of that state. Poland was a satellite of the former Eastern bloc and this determined the geo-graphical pattern of foreign trade dominated by the Soviet Union and other East European countries.

After the collapse of the Soviet economic system, regained independence of the Baltic States and transition to market economy in Poland, very rapid changes also took place in foreign trade. The transition countries orientated their foreign trade rapidly toward Western Europe, with special emphasis on integration with the EU. Russia also partly deregulated its foreign trade. Belarus remained strictly regulated and oriented on contacts with its Eastern neighbour. The trade with Baltic Region transition economies achieved a larger share also in the trade balance of Scandinavian countries, but those changes were proportionally several times smaller than changes in the trade balances of those countries.

The Baltic Region includes countries with quite different levels of economic development and foreign trade patterns. There are rich Scandinavian countries such as Denmark, Finland and Sweden, transition economies like the Baltic States Estonia, Latvia and Lithuania, and Poland. Also Russia (especially the St-Petersburg area) and Belarus belong to this region. The big differences in welfare and production capacities have a strong impact on foreign trade as well.

The countries differ also in their position in the regional integration process. The three Scandinavian countries are members of the EU, Denmark joined in 1972 and Finland and

Economic DEvElopmEntInternational Trade 623

Sweden as late as 1995. The Baltic States and Poland are accession countries. Poland has had a Free Trade Agreement with the EU in force since 1992 and the European Agreement, which also contains the Free Trade Agreement and regulates its associated member of the EU status, since 1994. Estonia, Latvia and Lithuania have had these agreements in force since 1995 and 1998 respectively. These agreements created free trade between the EU and associated coun-tries of industrial products, while agricultural articles are subject to modest restrictions.

The association countries have also signed free trade agreements between themselves. There is the Baltic Free Trade Agreement between the Baltic States and the Central European Free Trade Agreement between the Czech Republic, Hungary, Poland and Slovakia, the latter agree-ment is known also as the Visegrad agreement after the place where it was concluded.

Twelve countries of the former Soviet Union formed the Commonwealth of Independent States (CIS). The 12 CIS countries signed the Agreement on Creation of a Free Trade Area in 1994. In March 1996, Belarus and Russia, together with Kazakhstan and the Kyrgyz Republic, signed the Customs Union Agreement. Further, the Union of Belarus and Russia was signed in 1997. That agreement sets out, as a long-term goal, the free movement of goods, services, capital and people between the two countries.

All the Scandinavian countries, Estonia, Latvia and Poland are members of the WTO.

5. Geographical and commodity pattern of trade

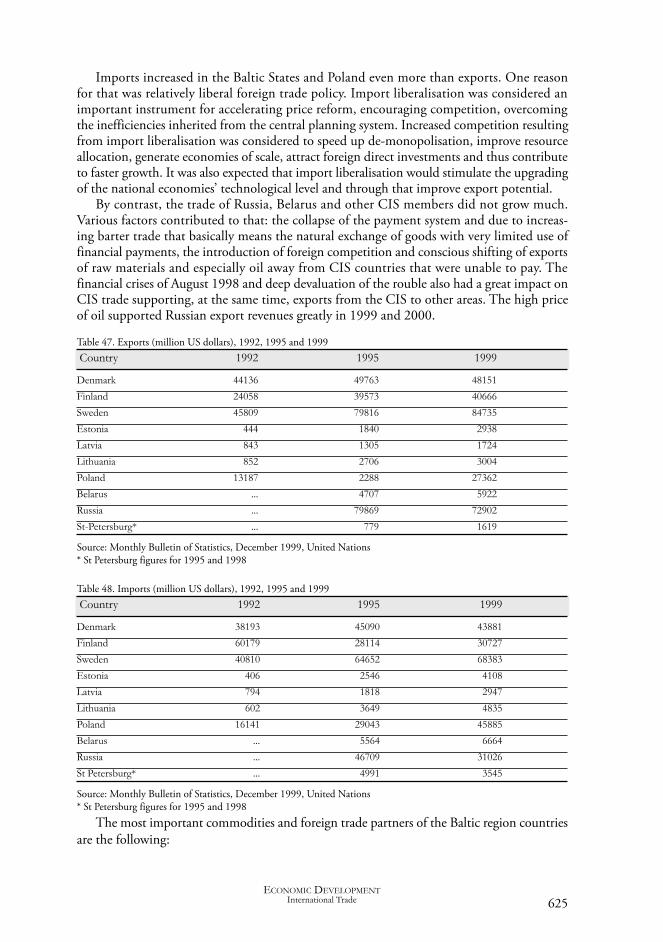

The transition from planned to market economy and liberalisation of foreign trade has also had a strong impact on the geographical and commodity pattern of trade, especially in the former socialist countries. On the basis of the figures in Tables 47 and 48, it is possible to see that values of exports and imports increased in Scandinavian countries modestly and that the foreign trade balance was in surplus, which means that exports exceed imports. The reason for this is strong competitiveness of those countries in world markets of several products such as machinery and equipment, chemical products and some others. Also the geographical trad-ing pattern of Denmark, Finland and Sweden has been quite stable, with the domination of Germany, the United Kingdom and other Scandinavian countries. A new phenomenon of the 1990s was increasing trade with transition economies, particularly with the Baltic States and Poland.

At the same time the Baltic States and Poland had a very great increase in foreign trade flows and rapidly increasing foreign trade deficit. The imports of those states have been dominated by the need for oil and raw materials. As there was a big shortage of consumer goods, the import of those items was important, especially at the beginning of the 1990s when foreign trade was liberalised and convertible currencies were introduced in the Baltic States and the convertibility of the currency was re-established in Poland. The role of machinery and equipment increased rapidly in the middle of the 1990s when, after ownership reform, big structural changes started in transition economies. Foreign direct investments also had a great role in promoting imports of investment goods.

As the export potential of those countries was quite modest, especially during the first half of the 1990s, big foreign trade deficits emerged. That deficit has partly been covered by surplus of services. Another source of financing that deficit was the inflow of foreign capital in the form of share capital and credits to the private sector. Nevertheless, the fast growth of exports has also been characteristic of that group of countries. Exports increased in Poland and Latvia more than twice, in Lithuania more than three times and in Estonia more than six times from 1992 to 1999.

Economic DEvElopmEntInternational Trade624

Imports increased in the Baltic States and Poland even more than exports. One reason for that was relatively liberal foreign trade policy. Import liberalisation was considered an important instrument for accelerating price reform, encouraging competition, overcoming the inefficiencies inherited from the central planning system. Increased competition resulting from import liberalisation was considered to speed up de-monopolisation, improve resource allocation, generate economies of scale, attract foreign direct investments and thus contribute to faster growth. It was also expected that import liberalisation would stimulate the upgrading of the national economies’ technological level and through that improve export potential.

By contrast, the trade of Russia, Belarus and other CIS members did not grow much. Various factors contributed to that: the collapse of the payment system and due to increas-ing barter trade that basically means the natural exchange of goods with very limited use of financial payments, the introduction of foreign competition and conscious shifting of exports of raw materials and especially oil away from CIS countries that were unable to pay. The financial crises of August 1998 and deep devaluation of the rouble also had a great impact on CIS trade supporting, at the same time, exports from the CIS to other areas. The high price of oil supported Russian export revenues greatly in 1999 and 2000.

Table 47. Exports (million US dollars), 1992, 1995 and 1999 Country 1992 1995 1999

Denmark 44136 49763 48151

Finland 24058 39573 40666

Sweden 45809 79816 84735

Estonia 444 1840 2938

Latvia 843 1305 1724

Lithuania 852 2706 3004

Poland 13187 2288 27362

Belarus ... 4707 5922

Russia ... 79869 72902

St-Petersburg* ... 779 1619

Source: Monthly Bulletin of Statistics, December 1999, United Nations* St Petersburg figures for 1995 and 1998

Table 48. Imports (million US dollars), 1992, 1995 and 1999 Country 1992 1995 1999

Denmark 38193 45090 43881

Finland 60179 28114 30727

Sweden 40810 64652 68383

Estonia 406 2546 4108

Latvia 794 1818 2947

Lithuania 602 3649 4835

Poland 16141 29043 45885

Belarus ... 5564 6664

Russia ... 46709 31026

St Petersburg* ... 4991 3545

Source: Monthly Bulletin of Statistics, December 1999, United Nations* St Petersburg figures for 1995 and 1998

The most important commodities and foreign trade partners of the Baltic region countries are the following:

Economic DEvElopmEntInternational Trade 625

Denmark. Denmark is an open economy with the share of exports to GDP at a level of 27-28% in 1990s of merchandise exports. Germany, with 20% of exports and 22% of imports is the most important partner of foreign trade, followed by Sweden with 12% of exports and 12% of imports, United Kingdom with 10% of exports and 8% of imports. The share of Poland was 1.9% of Danish exports and 1.7% of imports, the share of Russia was 1.4% of exports and 0.7% of imports, share of the Baltic States was 1.1% of exports and 0.7% of imports. The share of the EU was 66% of exports and 72% of imports.

The important export articles have been machinery and equipment and food products. Among imported articles, raw materials, consumer goods and machinery and equipment were dominant product groups.

Sweden. Sweden is an open economy with the share of exports to GDP at a level of 33- 35% in the 1990s of merchandise exports. Germany, with 11% of exports and 18% of imports is the most important partner of foreign trade, followed by Norway with 9% of exports and 7% of imports and Denmark with 6% of exports and 6% of imports. The share of Poland was 1.6% of Swedish exports and 1.1% of imports, the share of Russia was 0.9% of exports and 0.6% of imports, share of the Baltic States was 1.1% of exports and 1.4% of imports. The share of the EU was 58% of exports and 70% of imports.

The important export articles have been machinery and equipment with a share of more than half of total exports and wood and articles of wood with 13%. Among imported articles, machinery and equipment also created close to half the imports, fol-lowed by chemicals with 13%.

Finland. Finland is an open economy with the share of exports to GDP at a level of 32- 34% in the 1990s of merchandise exports. Germany, with 12% of exports and 15% of imports is the most important partner of foreign trade, followed by Sweden with 9% of exports and 12% of imports and United Kingdom with 9% of exports and 7% of imports. The share of Poland was 1.8% of Finnish exports and 0.9% of imports, the share of Russia was 4% of exports and 7% of imports, share of the Baltic States was 4.5% of exports and 1.4% of imports. Among the Baltic states, Estonia had the greatest pro-portion, with 3.3% of exports and 1.8% of imports of Finland. The share of the EU was 58% of exports and the same of imports. Among the Scandinavian countries, Finland had the greatest share of trade with countries on the Eastern coast of the Baltic Sea in the 1980s and that tradition has continued partly also through the 1990s.

The important export articles have been machinery and equipment with a share of around 40% of total exports, followed by and pulp and paper articles with 23%. The electrical machinery and equipment related to telecommunications should be underlined as an impor-tant subgroup of machinery and equipment. Raw materials, machinery and equipment and consumer goods made up the lion’s share of imports.

Estonia. Estonia is a very open economy even compared with Scandinavian economies, with the share of exports to GDP at a level of 60-65% in the 1990s of merchandise exports. Finland, with 19% of exports and 23% of imports, is the most important part-ner of foreign trade followed by Sweden with 18% of exports and 9% of imports and Russia with 9% of exports and 13% of imports in 1999. The share of Poland was 0.5% of exports and 1.3% of imports. The share of other Baltic States was 12% of exports and 4% of imports. The share of the EU was 63% of exports and 58% of imports.

Economic DEvElopmEntInternational Trade626

The important export articles have been machinery and equipment with a share of 21% of exports, followed by wood and articles of wood and textile and textile articles. Among imported articles, machinery and equipment also made up the largest proportion.

Latvia. Latvia has a share of exports to GDP at a level of 28-30% in the 1990s of merchandise exports. Germany, with 17% of exports and 15% of imports, is the most important partner of foreign trade, followed by United Kingdom with 16% of exports and 3% of imports and Russia with 7% of exports and 11% of imports in 1999. The share of Poland was 1.8% of exports and 3.5% of imports. The share of other Baltic States was 12% of exports and 13% of imports. The share of the EU was 57% of exports and 53% of imports. There is practically no difference in the proportion of the trade with the EU in total trade in Estonia and Latvia compared to the Scandinavian countries.

The important export articles have been wood and articles of wood and textile and textile articles and machinery. Among imported articles, machinery and equipment also made up the largest proportion.

Lithuania. Lithuania has a share of exports to GDP at a level of 30-35% in the 1990s of mer-chandise exports. Germany, with 16% of exports and 17% of imports, is the most important partner of foreign trade, followed by Russia with 7% of exports and 20% of imports. The share of Poland was 4.5% of exports and 5.7% of imports. The share of Latvia was 11% of exports and 2% of imports, the share of Estonia was 2.6% of exports and 2.7% of imports. The share of the EU was 38% of exports and 50% of imports. Lithuania is more orientated to Central Europe and Poland in comparison with the other Baltic States.

The important export articles have been wood and related articles, textile and textile articles, mineral products and machinery. Among imported articles, mineral products (par-ticularly oil), machinery and equipment also made up the largest proportion.

Belarus. Belarus had an economic policy quite different from the Baltic States. There are still price controls and export permits on a number of goods are required. Belarus has also been quite a closed country with a share of exports to GDP at a level of 20-25% in 1990s of merchandise exports. The CIS trade created 61% of exports and 36% of imports. The most important single foreign trade partner was Russia. The share of the EU was around 8% of exports and imports.

The important export articles have been wood and related articles, textile and textile arti-cles, food products and machinery. Among imported articles, mineral products (particularly oil), machinery and equipment also made up the largest proportion.

Russia. Russia as a big country with a large population and for that reason is also less open than the smaller countries of the region. As Russia has several domestic prices substantially lower than in developed countries (oil and oil products first of all), the export tariff on oil has been used. Some exported products are subject to self-restraints under agreements with the EU and other partners. Temporary price and trade controls were imposed following the August 1998 financial crises. The CIS trade created only 15% of exports and 27% of imports of Russia. The share of the EU was 33% of exports and 37% of imports.

There is a big difference between Russia and other transition economies in terms of the commodity pattern of trade. Russian exports are dominated by raw materials and oil. In 1999, crude oil made up 19%, natural gas 16%, petroleum products 6% and metals 14% of exports.

Economic DEvElopmEntInternational Trade 627

The share of machinery and equipment was 11%. Such an export pattern means great vulner-ability of a country to price and demand changes on the world markets.

From imports, machinery and equipment made up 32% and food products 13%, followed by consumer goods and other industrial commodities.

St Petersburg. St Petersburg used to be historically the Russian window to the Western world. Also nowadays the share of EU exports and imports is higher than average for Russia. Due to closeness to the Scandinavian and Baltic countries, that area has been considered for partnerships in education, culture and tourism. Also in foreign trade con-tacts St Petersburg, as the most important centre of Northwest part of Russia, plays an important role.

6. Perspectives of foreign trade and integration with the EU

If the Baltic States and Poland join the EU, trade policy becomes an EU competence, and all those countries will have to implement the external trade policy of the EU. This will have different influences on enlargement countries. As Estonia currently has practically zero protection, it cannot reap further gains from trade liberalisation. On the other hand, other enlargement countries, which have higher levels of tariffs, will gain from tariff-free trade inside the EU.

EU integration will lead to an increase in the level of protection toward non-EU suppli-ers and, hence, to trade diversion. However, the effect of implementing EU tariffs will be fairly small because the majority of trade will be with EU members and the protection level of the EU is not high in raw materials, which are currently the major import articles from non-EU members.

Joining the EU means also that the enlargement countries have to implement the EU’s anti-dumping and other non-tariff measures. The effects of these measures on the pro-tection level are much more difficult to predict. They may cause trade diversion from Japan, other Asian countries, Russia and Ukraine, with which the EU has higher protec-tive barriers, to more expensive EU importers. It can also cause a rise in import prices of iron and steel if the EU adopts anti-dumping measures against CIS imports.

On the other hand, market access will be much better guaran-

Economic DEvElopmEntInternational Trade628

Figure 170. Gdańsk, one of old trade cities of the BSR. Photo: Katarzyna Skalska

teed by joining the EU, because measures of contingent protection will not be used against imports. In addition, trade with the EU countries will be without tariffs, quantitative restric-tions, and measures having equivalent effect with quantitative restrictions. Various cost-cre-ating barriers will disappear after joining the EU, because national regulations that are not covered by the Association Agreements, and which currently restrict entry into the EU market, will no longer be in effect. EU membership will mean joining the Single Market, which will remove various technical, physical and fiscal barriers to trade. Because the Baltic States and Poland currently conduct close to two-thirds of their total trade with either present EU mem-bers or countries that have applied for membership, the trade creation from improved market access will outweigh the trade diversion from increased protection toward non-EU suppliers. EU membership will give additional advantages by locking in reforms and adding credibility to the government’s liberal policies.

The EU has a Partnership and Co-operation Agreement with members of CIS, i.e. with Russia and Belarus. There is a Northern Dimension agenda, whose one target is to support developments in the Baltic Sea region as well. The Northern Dimension is not a policy of any single EU country but the policy of the entire EU. Functionally, the Northern Dimension contains the northern parts of Europe, Northwest Russia, North Russia and the Baltic States. The Northern Dimension is primarily a long-term process that aims at supporting the acces-sion of the Baltic States into the EU and deepening relations between the EU and Russia. The strategic issues of that policy are energy integration within the northern dimension zone, development of transportation and transport networks, and organising financial sources for the economic development of that area.

Economic DEvElopmEntInternational Trade 629

Figure 171. The role of the Belarusan capital, Minsk, as of a trading centre, is reflected in its name that comes from the verb ‘meniat’, to barter. Photo: BUP archive

Aage, H: 1998a. Institutions and Performance in Transition Economies. Nordic Journal of Political Economy 24 (No. 2, 1998): 125- -144

Aage, H: 1998b. Environmental Transition: A Comparative View. Chap. 1, pp 3-15 in Aage, H. (ed.): Environmental Transition in Nordic and Baltic Countries. Cheltenham: Edward Elgar

Aage, H. (ed.), 1998c: Environmental Transition in Nordic and Baltic Countries. Cheltenham: Edward Elgar 1998

Agenda 2000. Bruxelles: EU-kommissionen, juli 1997

Baldwin, R. E., 1995. The Eastern Enlargement of the European Union. European Economic Review 39 (April 1995, Nos. 3-4) 474-481

Baltic Environmental Forum: 2nd Baltic State of the Environment Report. Riga: Baltic Environmental Forum 2000

Barro, R.J.: 1996. Getting It Right. Markets and Choices in a Free Society. Cambridge, Mass.: The MIT Press

B jörk lund, Ander s e t a l . , 2000, Arbe t s - marknaden, (The Labour Market in Swedish) Stockholm: SNS förlag

Blomström, Magnus, Kokko, Ari & Zejan, Mario 2000. Foreign Direct Investment – Firm and Host Country Strategies, London: Macmillan

Bluffstone, R. (ed.), 1997. Controlling Pollution in Transition Economies. Cheltenham: Edward Elgar

Boeri, T. & Brücker, H.: 2001. The Impact on Eastern Enlargement on Employment and Labour Markets in the EU Member States. Report SOC-97-102454. Bruxelles: EU European Commission (http://www. eu- -oplysningen.dk/euidag/andet/strategisk- rapport)

Boycko M., Shleifer, A. & Vishny, R., 1995: Privatising Russia. Cambridge: MIT Press

Brabant, J.M. van, 1998. Integrating the Transition Economies into the EU Framework – An Overview. Comparative Economic Studies 40 (Fall 1998, No. 3) 1-5

Desai, Padma & Idson, Todd, 2000. Work without Wages. Cambridge, Mass.: The MIT Press

Dunning, John H., 1993. Multinational Enterprises and the Global Economy. Mass: Addison-Wesley

Dunning, John H., 2001. Assessing the Costs and Benefits of Foreign Direct Investment: Some theoretical Issues, in: P. Artisien- -Maksimenko and M. Rojec (eds.): Foreign Investment and Privatization in Eastern Europe- Palgrave

Eamets, Raul, et al., 1999. Background Study on Employment and Labour Market in Lithuania. Working Document, European Training Foundation

EBRD: Transition Report 2000. London: European Bank for Reconstruction and Development 2000

ECE: Economic Survey of Europe 2000 No. 2/3. Gen¯ve: UN Economic Commission for Europe 2000

Economic Policy Initiative, 1998. Mediating the Transition: Labour Markets in Central and Eastern Europe, Forum Report No 4

EU European Commission: Second Report on Economic and Social Cohesion. Comm(2001) 24 final. Bruxelles: EU European Commission 2001. (http://europa.eu.int/eur–lex/en/com/rpt/2001/com2001_0024en03html).

Evidence from the Baltic Republics, Annals of public and cooperative economics, vol. 71, no. 3

Fischer, S. & Sahay, R., 2000. The Transition Economies after Ten Years. NBER Working paper 7664, April 2000

Gregory, P.R. & Stuart, R.C., 1992. Comparative Economic Systems. (4th ed.). Boston: Houghtom Mifflin 1992

Gregory, P.R. & Stuart, R.C.,1989. Comparative Economic Systems. (3rd ed.). Boston: Houghtom Mifflin

Gruzevskis, Boguslavas, et al., 1999. Background Study on Employment and Labour Market in Lithuania, Working Document, European Training Foundation

Economic DEvElopmEntLiterature and References 661

LITERATURE AND REFERENCES

Halsnæs, K., Sørensen, L., 1993. Perspectives o f Re g i ona l Coo rd ina t ed Ene r g y and Environmental Planning. Nordiske Seminar og Arbejdsrapporter (640). Copenhagen: Nordic Council of Ministers

Hay, J.R., Shleifer, A. & Vishny, R.W., 1996. Toward a Theory of Legal Reform. European Economic Review 40 (April 1996, Nos. 3-5) 559-567

Hazans, Mihails, 2001. Wages in Latvia: A Cross-Industry Analysis? Baltic Economic Trends. No 1

Hazley, Colin & Hirvensalo, Inkeri, 1998. Direct Investments to the Baltic Rim Transition Economies: Some Trends, EST, vol. 1998, no. 2, pp 137-157

Hirvensalo, Inkeri, 2000. Foreign Direct Investment around the Baltic Sea – is there policy competi-tion among the countries?, paper presented at the OECD Conference on Fiscal Incentives and Competition for Foreign Direct Investment in the Baltic States, Vilnius, Lithuania, May 30, 2000

Huitfeldt, Henrik, 2001. Active Labour Market Policy in Russia? – An Evaluation of Swedish Technical Assistance to the Russian Employment Service 1997-2000. Sida, Draft, April

IMF (International Monetary Fund): Transition and Policy Issues. Chap. 3, pp 84-137 in World Economic Report May 2001. Washington, D.C.: IMF 2001

Isachsen, A.J., Hamilton, C.B. & Gylfason, T., 1992. Omstilling til marked. Økonomiske utfor-dringer. Oslo: Universitetsforlaget (also pub-lished in Lithuanian and English)

Jensen, Camilla, 2001. Foreign Direct Investment and Technological Change in Polish Manufacturing, Ph.D. Thesis, forthcoming from Odense University Press

Jones D. & Mygind, N., 1999a. The Nature and Determinants of Ownership Changes after Privatisation:Evidence from Estonia, Journal of Comparative Economics, vol 27 no 3, pp 422-441

Jones, D. & Mygind, N., 1999b. Ownership and Productive Efficiency: Evidence from Estonia, in Equality, participation, transition. V. Franicevic & M. Uvalic (eds.), McMillan

Klein, L., et.al.: Novaja ekonomicheskaja politika dlja Rossii (Nezavisimaja Gazeta, 1. July 1996, p 1). Novaja povestka dnja dlja ekonomicheskikh reform v Rossii. Gosudarstvo dolzhno vzjat’ na

sebja osnovnuju rol’ v stabilizatsii pod’ema stra-ny (Nezavisimaja Gazeta, 9. July 2000, p 3)

Kogut , Bruce, 1996. Direct Investment , Experimentation and Corporate Governance in Transition Economies, in: Frydman et al. (eds.): Corporate Governance in Central Europe and Russia – Banks, Funds and Foreign Investors, vol. 1, Budapest: Central European University Press

Koidu, Maria, Kuldkepp, Aiki & Purju, Alari, 1999. Role of Institutional Framework for Trade with the EU. In: Ülo Ennuste and Lisa Wilder (Eds.). Harmonisation with the Western Economies: Estonian Economic Developments and Related Conceptual and Methodological Frameworks. Tallinn: Estonian Institute of Economics at Tallinn Technical University, pp. 91-114

Kołodko, G.W., 2000. From Shock to Therapy. The Political Economy of Postsocialist Transformation. Oxford: Oxford University Press

Krugman, P., 1994. Peddling Prosperity. New York: Norton

Lankes, Hans-Peter & Venables, Anthony, 1996. Foreign Direct Investment in Economic Trans i t ion: The Changing Pattern of Investments, Economics of Transition, vol. 4, pp 331-347.

Lavigne, M., 1998. Conditions for Accession to the EU. Comparative Economic Studies 40 (Fall 1998, No. 3) 38–57

Lipton D. & Sachs, J., 1990. Privatisation in Eastern Europe, The case of Poland, BPEA, 2

Meyer, Klaus E. & Pind, Christina, 1999. FDI growth in the FSU, Economics of Transition, vol. 7, no. 1, pp 201-214

Meyer, Klaus E., 2001a. International Business Research in Transition Economies, in: T. Brewer and A. Rugman, eds: Oxford Handbook of International Business, Oxford: Oxford University Press

Meyer, Klaus E., 2001b. Direct Investment in South-East Asia and Eastern Europe: A Comparative Analysis, in: P. Artisien- -Maksimenko and M. Rojec (eds.): Foreign Investment and Privatization in Eastern Europe, Palgrave

Milgrom, P. & Roberts, J., 1992. Economics, Organization and Management. Englewood Cliffs, N.J.: Prentice-Hall

Mygind, N., 1994. The Economic Transition in the Baltic Countries – Differences and Similarities pp.197-234 in: J.Å. Dellenbrant and O. Nørgaard, The Politics of Transition in the Baltic

Economic DEvElopmEntLiterature and References662

States – Democratization and Economic Reform Policies. Umeˆ University, Research Report No. 2

Mygind, N., 2000. Privatisation, Governance and Restructuring of Enterprises in the Baltics, Working Paper, CCNM/BALT (2000)6, OECD, Paris

Mygind, N., 2001. Enterprise Governance in Transition – a Stakeholder Perspective, forth-coming in Acta Oeconomica, no 3

Nielsen, Jorgen, Ulff-Moller, Madsen, Strojer, Erik & Pedersen, Kurt, 1995. International Economics. The Wealth of Open Nations . Berkshire: McGRAW-HILL Book Company

Nuti D., 1997. Employee Ownership in Polish Privatisations. In: Uvalic and Vaughan- -Whitehead (1997) pp 165-181

Nuti, D.M., 2000. The Costs and Benefits of Europeisation in Central-Eastern Europe before or instead of EMU Membership. Working Paper, London Business School, December 2000

OECD: OECD Environmental Data, Compendium 1999. Paris: OECD

OECD: Environment in the Transition to a Market Economy. Paris: OECD 1999

OECD: Environmental Outlook. Paris: OECD 2001

Oxenstierna, Susanne, 1992. The Labour Market. In: B. Van Arkadie & M. Karlsson (eds) Economic Survey of the Baltic States. London: Pinter Publ. Lim

Oxenstierna, Susanne, 1990. From Labour Shortage to Unemployment? The Soviet Labour Market in the 1980s. Stockholm: Almqvist & Wicksell International

Oxenstierna, Susanne, 1991. Labour Policies in the Baltic Republics, International Labour Review, Vol. 130, No 2

Ponting, C., 1991. A Green History of the World. Harmondsworth: Penguin

Popov, V., 2000. Shock Therapy Versus Gradualism: The End of the Debate (Explaining the Magnitude of Transformational Recession). Comparative Economic Studies 42 (Spring 2000, No. 1) 1-57

Pryor, F.L., 1985. A Guidebook to the Comparative Study of Economic Systems. Englewood Cliffs, NJ: Prentice-Hall

Reddaway, P. & Glinski, D., 2001. The Tragedy of Russian Reform: Market Bolshevism Against Democracy. Washington, D.C.: The United States Institute of Peace Press

Research Report, no. 125, Dept. of Industrial Engineering and Management, Lappeenranta University of Technology, Finland

Rosser, J.B. & Rosser, M.V., 1995. Comparative Economics in a Transforming World Economy. Chicago: Irwin

Schreyer, M., 2001. Financing Enlargement of the European Union, Speech at The London School of Economics, 16 February 2001. (http://www.europa.eu.int (SPEECH/01 /71))

Shleifer, A. & Treisman, D., 2000. Without a Map. Political Tactics and Economic reform in Russia. Cambridge, Mass.: MIT Press

Smith, Kenneth, 2001. Income Distribution in the Baltic States: A Comparison of Soviet and Post Soviet Results, Baltic Economic Trends, No 1

Stiglitz, J.E., 1995. Whither Socialism? Cambridge, Mass.: MIT Press

Sztanderska, Urszula, et al., 1999. Background Study on Employment and Labour Market in Poland. Working Document, European Training Foundation

The NEBI Yearbook 2000. North European and Baltic Sea Integration. Berlin: Springer- -Verlag, 2000

The Transition to a Market Economy. Transformation and Reform in the Baltic States. Ed. By Tarmo Haavisto. Cheltenham: Edward Elgar, 1997

Trapenciere, Ilze et al., 1999. Background Study on Employment and Labour Market in Poland. Working Document, European Training Foundation

UNDP: Human Development Report 1992. Oxford: Oxford University Press 1992

UNCTAD (1997): World Investment Report 1997: Transnational Corporations, Market Structure and Competition Policy, United Nations’ Conference on Trade and Development, New York and Geneva

UNCTAD (2000): World Investment Report 2000: Cross-border Mergers and Acquisition and Development. United Nations Conference on Trade and Development, New York and Geneva

Uvalic, M. & Vaughan-Whitehead, D., 1997. Privatisation Surprises in Transition Economies. Cheltenham: Elgar

Varblane, Urmas, 2000. Foreign Direct Investments in Estonia – Major characteristics, trends and developments in 1993-1999, University of Tartu, Estonia, published under the Phare-ACE research project no. P97-8112-R

Economic DEvElopmEntLiterature and References 663

World Bank (2000): World Development Indicators. The World Bank, Washington

World Bank: World Development Report 1996: From Plan to Market. New York: Oxford University Press 1996

World Resources Institute: World Resources 1992-93. Oxford: Oxford University Press 1993

Zukowska-Gagelmann, 2000. Productivity spill-overs from foreign direct investment in Poland, Economic Systems vol. 24, no. 3, p. 223-25

Economic DEvElopmEntLiterature and References664