Embed Size (px)

Citation preview

CSE GLOBAL LTD CSE GLOBAL LTD

GLOBAL SOLUTIONS PROVIDERCONTROL, TELECOM, ELECTRICAL

MILESTONES MILESTONES

1985 : Commenced operations

1993-1995 : Established presence in Thailand, Malaysia & India

1997 : Management Buy-In

1999 : Initial Public Offering

2000 : Acquired W-Industries (US) and Servelec (UK)

2003 : Acquired Transtel and established presence in Carmen, Doha, Dubai, Tehran, Soku, Muscat, Shanghai, Beijing and Jakarta

2004 : Acquired Uniserve (Australia) & RTUnet (Australia; product business)

BUSINESS OVERVIEW BUSINESS OVERVIEW

Niche global system integrator in Control, Telecommunication andElectrical Systems

- Control Integrated Control System, Safety Systems, Plant ITCompetitor : Honeywell, Emerson Process, Invensys-Foxboro, Yokogawa, ABB, Siemens

- TelecommunicationSatellite and Wireless system, Fiber Optic CommunicationSystem, PABX, Public Address, CCTV etc.Competitor : Alcatel, ABB, Siemens

- ElectricalProtection and Control, High Voltage Electrical SystemsCompetitor : Schweitzer Engineering Lab (SEL), Schneider, Rockwell. ABB

CONTROL CONTROL

- Process Control System- SCADA/Telemetry System- Pipeline Control System- Well Head Control System- Subsea Control System- Chemical Injection System

Integrated Control System

CONTROL CONTROL

Safety System- Emergency Shutdown System- Fire and Gas Detection System- High Integrity Protection System

-Plant Information Systems-Laboratory Information System -Data Reconciliation & Yield Accounting System-Terminal Automatic System

CONTROL CONTROL

Plant IT

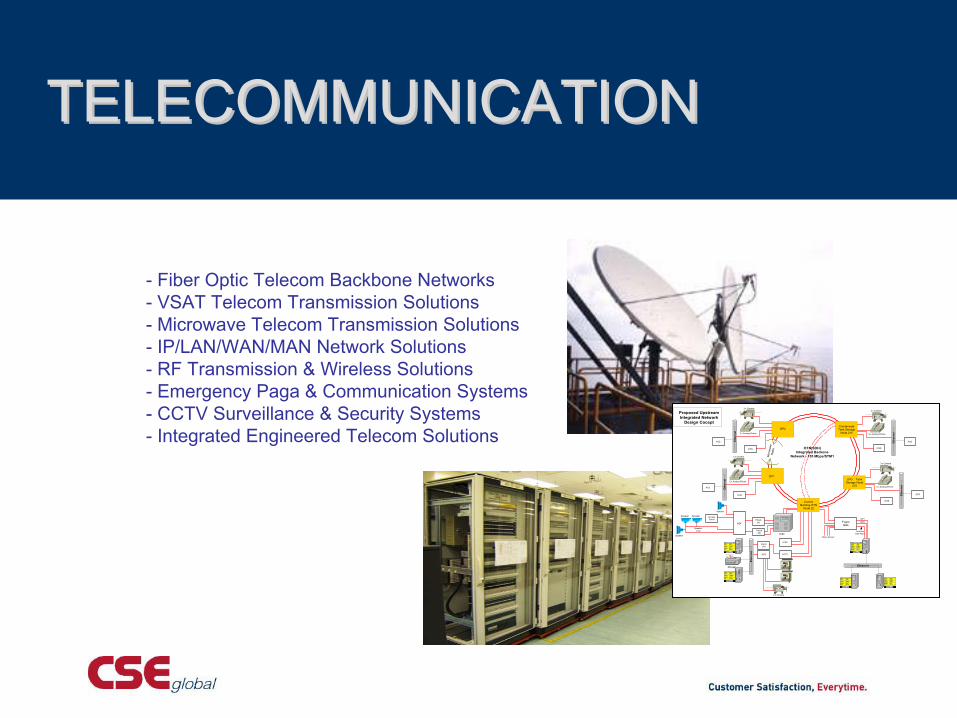

TELECOMMUNICATION TELECOMMUNICATION

- Fiber Optic Telecom Backbone Networks- VSAT Telecom Transmission Solutions- Microwave Telecom Transmission Solutions- IP/LAN/WAN/MAN Network Solutions- RF Transmission & Wireless Solutions- Emergency Paga & Communication Systems- CCTV Surveillance & Security Systems- Integrated Engineered Telecom Solutions Et

hern

et 2 x Analog Phone

3 x Camera

ICSS

ACS Ethe

rnet

ACS

3 x Camera

ICSS

2 x Analog Phone

Ethe

rnet

ACS

Ethe

rnet

Ethernet

Ethe

rnet

2 x Analog Phone

3 x Camera

ICSS

3 x Camera

ICSS

PABX

ICSS

CCTVACS

PAGA(A)

PAGA(B)

Speaker

AlarmUnit

Printer

3 x Camera

FugroGAs

Other Sensor

DP1DP2

OnshoreGas Plant

Proposed UpstreamIntegrated Network

Design Cocept

Monitor

Monitor

MDF

AccessPanel

Speaker

Speaker

Speaker

SpeakerLoop

ACS 2 x Analog Phone

LPG TankStorage Node

215

ControlBuilding OTN

Node 22

DP2

Mic

row

ave

Rad

io

CondensateTank Storage

Node 215

DP1

OTN(SDH)Integrated Backone

Network - 155 Mbps/STM1

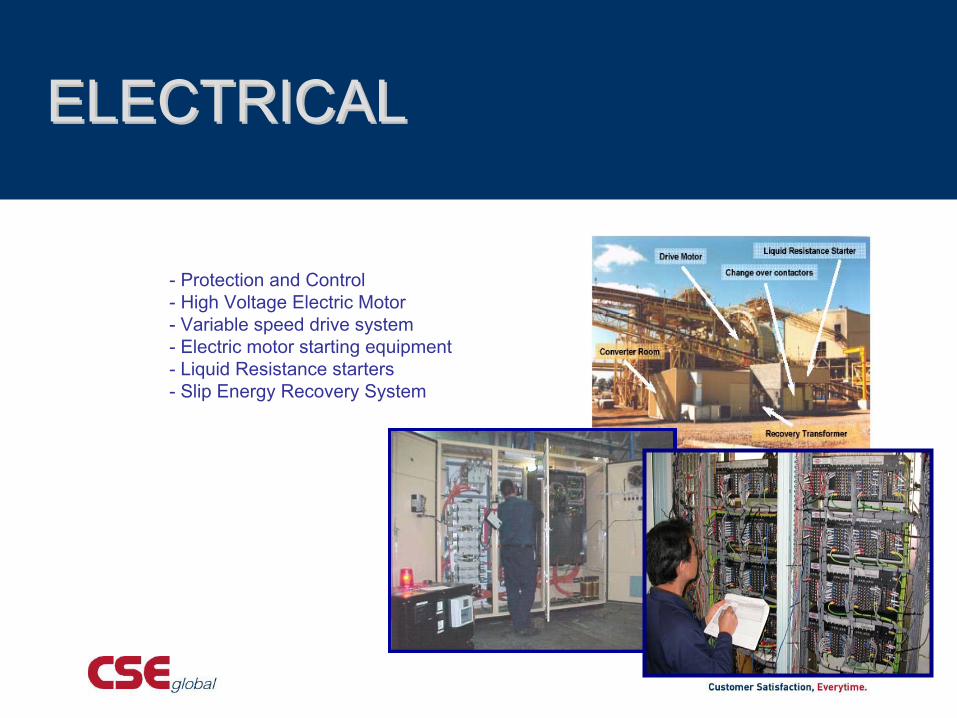

ELECTRICAL ELECTRICAL

- Protection and Control- High Voltage Electric Motor- Variable speed drive system- Electric motor starting equipment- Liquid Resistance starters- Slip Energy Recovery System

BUSINESS OVERVIEW BUSINESS OVERVIEW

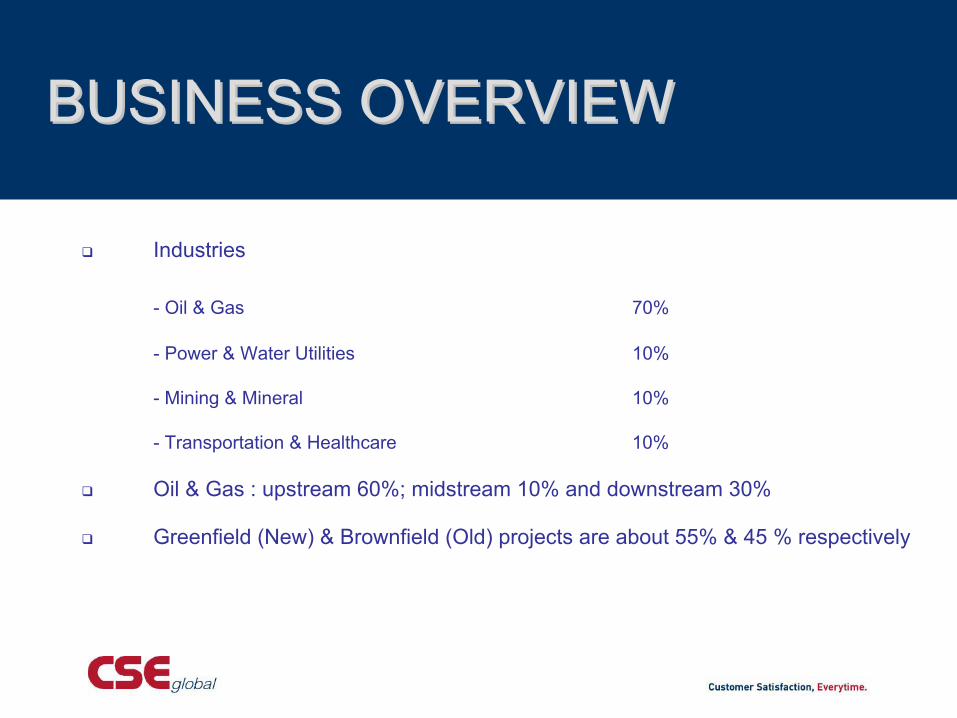

Industries

- Oil & Gas 70%

- Power & Water Utilities 10%

- Mining & Mineral 10%

- Transportation & Healthcare 10%

Oil & Gas : upstream 60%; midstream 10% and downstream 30%

Greenfield (New) & Brownfield (Old) projects are about 55% & 45 % respectively

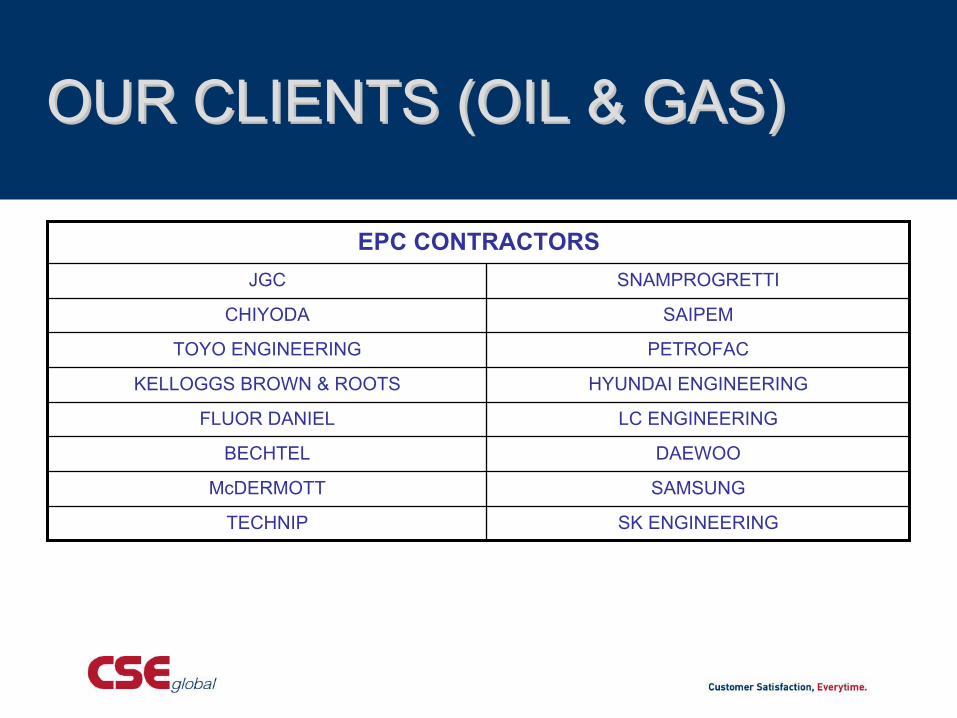

OUR CLIENTS (OIL & GAS) OUR CLIENTS (OIL & GAS)

SK ENGINEERINGTECHNIP

SAMSUNGMcDERMOTT

DAEWOOBECHTEL

LC ENGINEERINGFLUOR DANIEL

HYUNDAI ENGINEERINGKELLOGGS BROWN & ROOTS

PETROFACTOYO ENGINEERING

SAIPEMCHIYODA

SNAMPROGRETTIJGC

EPC CONTRACTORS

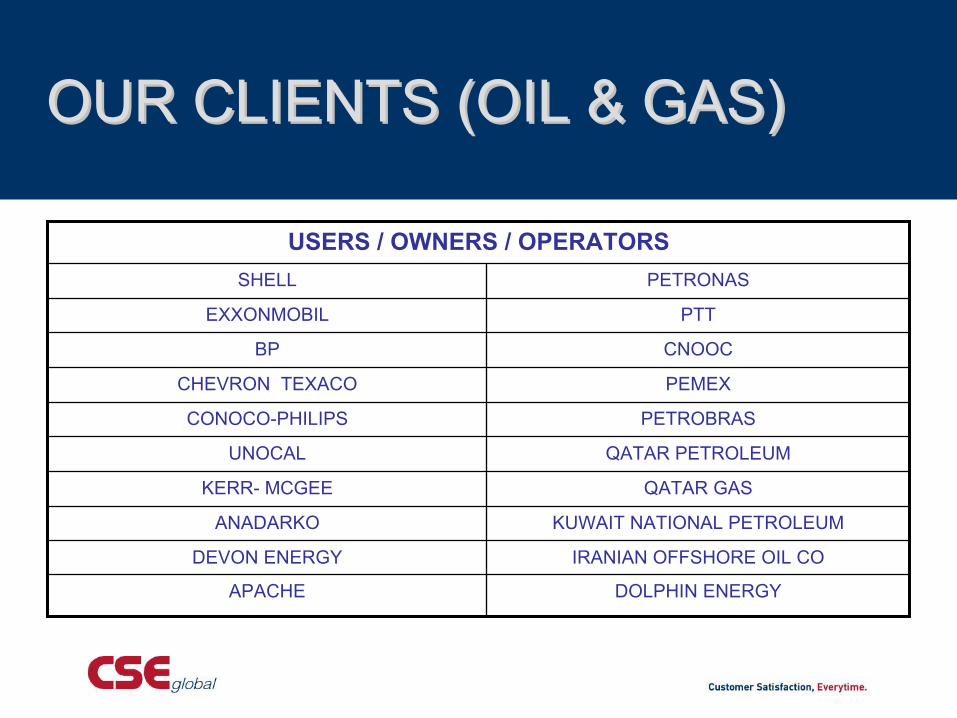

OUR CLIENTS (OIL & GAS) OUR CLIENTS (OIL & GAS)

IRANIAN OFFSHORE OIL CODEVON ENERGY

DOLPHIN ENERGYAPACHE

KUWAIT NATIONAL PETROLEUMANADARKO

QATAR GASKERR- MCGEE

QATAR PETROLEUMUNOCAL

PETROBRASCONOCO-PHILIPS

PEMEXCHEVRON TEXACO

CNOOCBP

PTTEXXONMOBIL

PETRONASSHELL

USERS / OWNERS / OPERATORS

PROJECT EXECUTIONPROJECT EXECUTION

AnalysisPhase

Design &Development

Phase

TestingPhase

SystemImplementation

Phase

SystemWarranty/

MaintenancePhase

ProjectPlanning

Phase

•Contract•TenderSpecifications

•TenderSpecifications

•Functional Specifications

•DesignSpecifications•Test Procedures & Plan•Developed System

•System AcceptanceCertificate•Accepted System•ImplementationPlan

•CommissioningLetter•MaintenanceContract

•ProjectDevelopment &Quality Plan

•FunctionalSpecifications

•Design & ProgramSpecifications•System Test Cases& Results•Test Procedures &Plan•Test Cases•Developed System

•Test Results•AcceptedSystem•SystemAcceptanceCertificate

•Live System•Final Deliverables•Commissioning Letter

•Service Request

The Group currently has 29 offices in 18 countries with about950 employees worldwide

Global Manpower

- Asia Pacific - 300- America - 450- Europe/Middle East/Africa (EMEA) - 200

Singapore business only accounts for about 5% of the group revenue

GLOBAL OPERATIONSGLOBAL OPERATIONS

*

* Branches in Nitra, Prague, Bratislava & Košice

SingaporeBangkokBangalore

Kuala Lumpur

Houston LayfayetteNew OrleansCarmen

Soku

Jakarta

SheffieldNitraTehran

ShanghaiDubai

Beijing

Perth

Brisbane

SydneyMelbourne

Auckland

DohaMuscat

GLOBAL PRESENCEGLOBAL PRESENCE

Beijing Tianjin

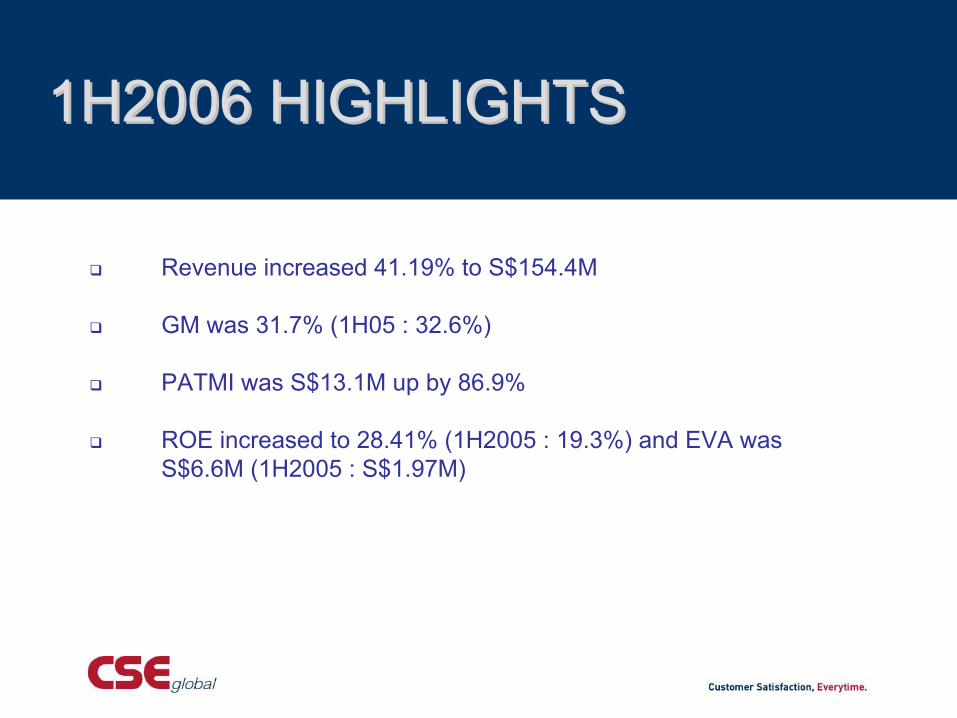

1H2006 HIGHLIGHTS1H2006 HIGHLIGHTS

Revenue increased 41.19% to S$154.4M

GM was 31.7% (1H05 : 32.6%)

PATMI was S$13.1M up by 86.9%

ROE increased to 28.41% (1H2005 : 19.3%) and EVA was S$6.6M (1H2005 : S$1.97M)

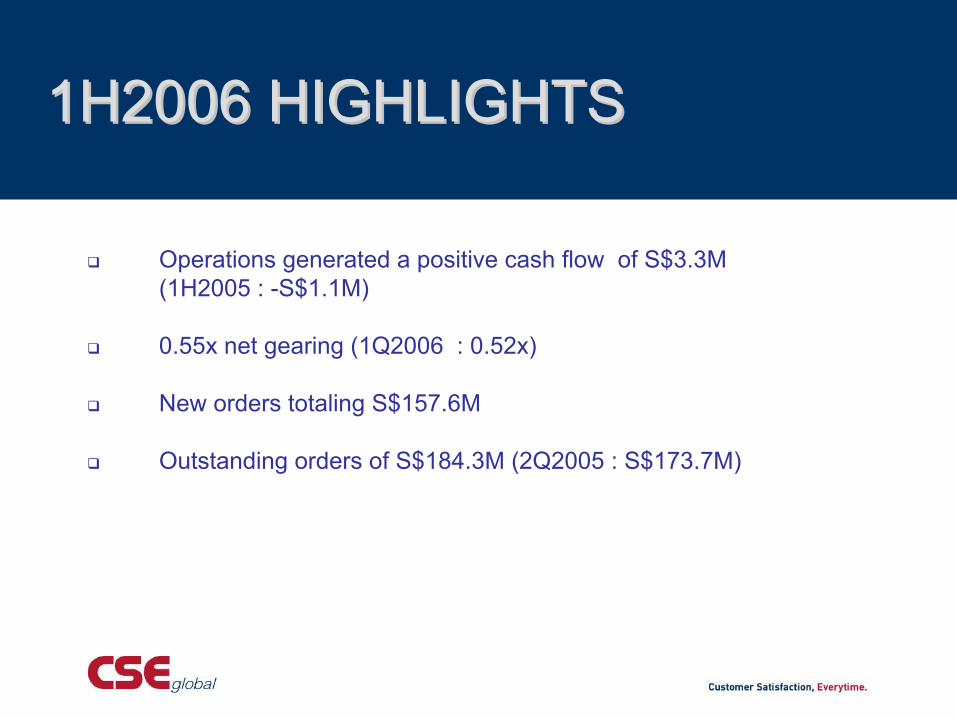

1H2006 HIGHLIGHTS1H2006 HIGHLIGHTS

Operations generated a positive cash flow of S$3.3M (1H2005 : -S$1.1M)

0.55x net gearing (1Q2006 : 0.52x)

New orders totaling S$157.6M

Outstanding orders of S$184.3M (2Q2005 : S$173.7M)

1H2006 GROUP P&L1H2006 GROUP P&L

S$M

2.16.48.5ROS (%)

86.97.013.1PATMI

100.09.118.3PBT

(0.9)32.631.7GM (%)

41.1109.4154.4REVENUE

VARIANCE (%)1H20051H2006

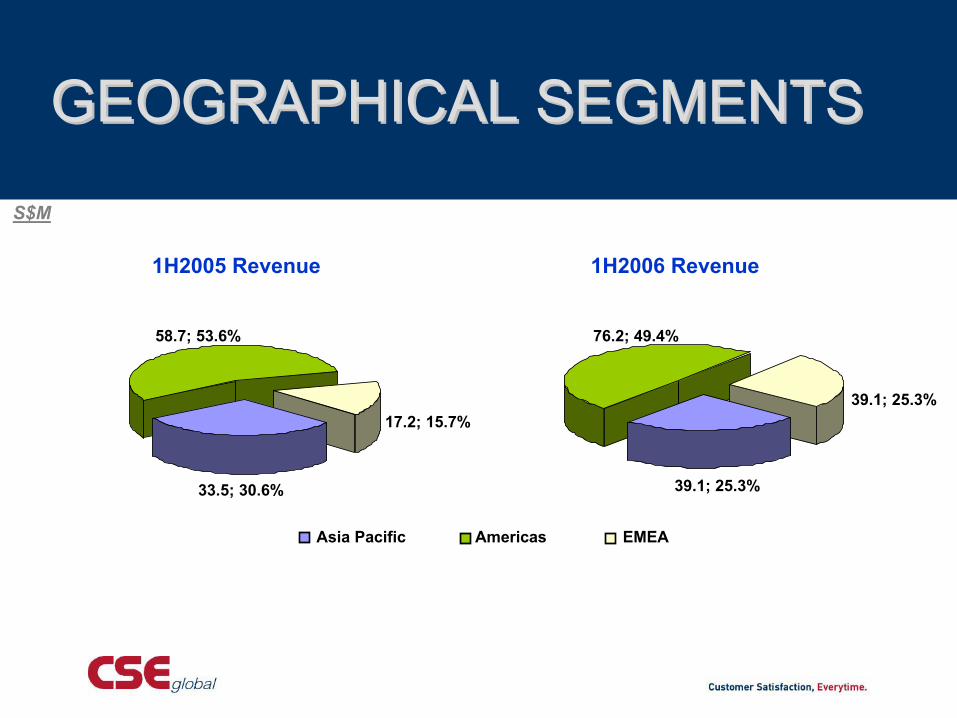

1H2006 Revenue1H2005 Revenue

S$M

Asia Pacific Americas EMEA

GEOGRAPHICAL SEGMENTSGEOGRAPHICAL SEGMENTS

33.5; 30.6%

58.7; 53.6%

17.2; 15.7%

39.1; 25.3%

76.2; 49.4%

39.1; 25.3%

GEOGRAPHICAL SEGMENTSGEOGRAPHICAL SEGMENTS

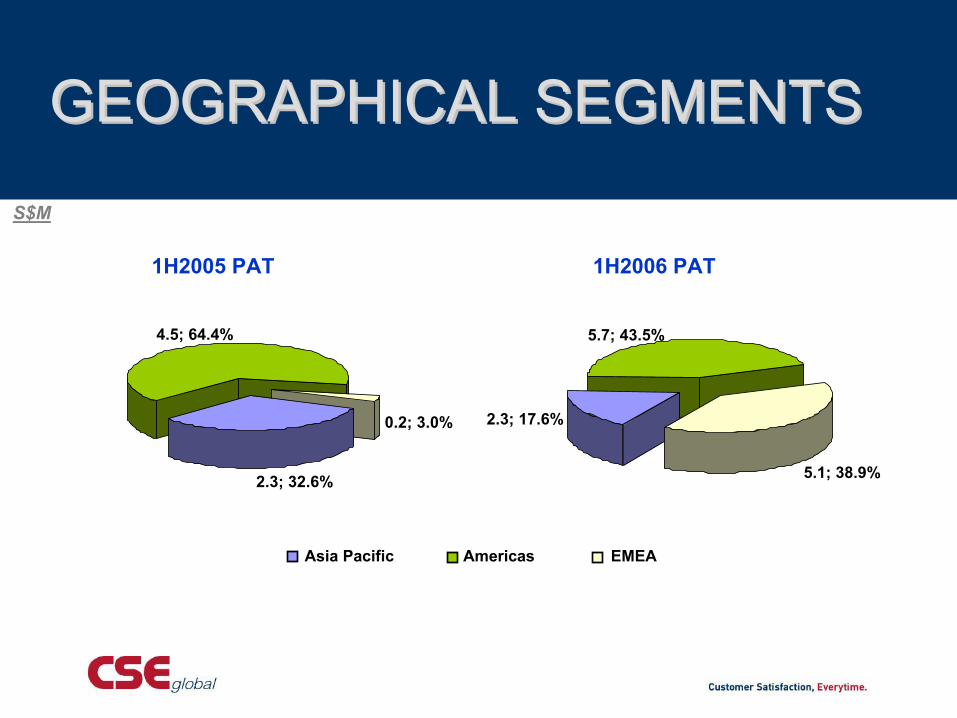

1H2005 PAT

Asia Pacific Americas EMEA

S$M

1H2006 PAT

2.3; 17.6%

5.7; 43.5%

5.1; 38.9%2.3; 32.6%

4.5; 64.4%

0.2; 3.0%

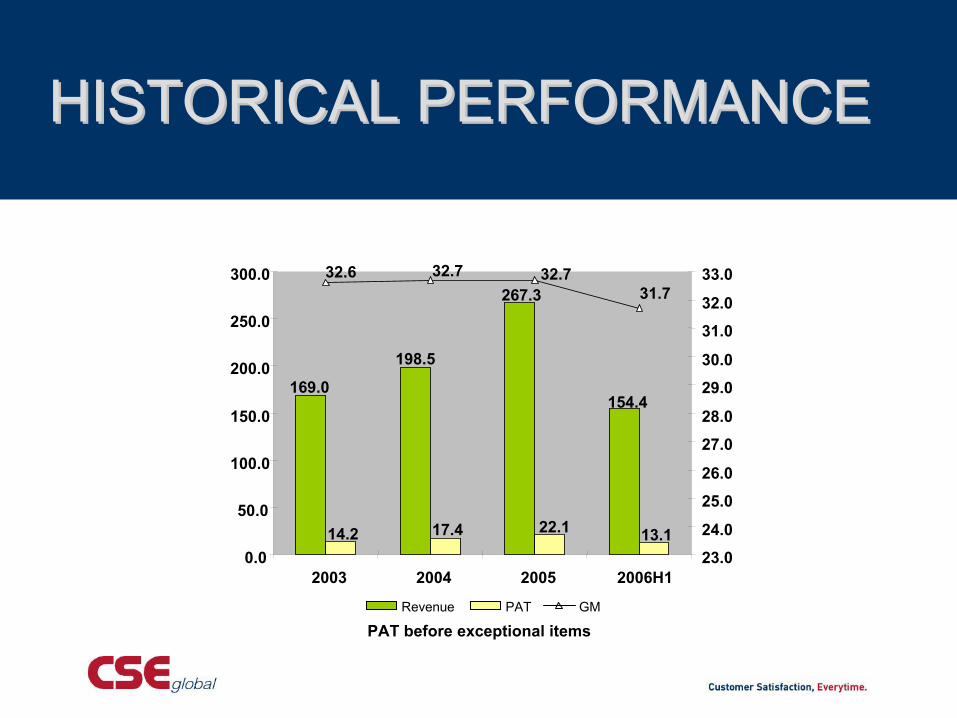

HISTORICAL PERFORMANCEHISTORICAL PERFORMANCE

Revenue PAT GM

PAT before exceptional items

14.2 17.4 22.1 13.1

154.4

198.5

267.3

169.0

31.732.732.732.6

0.0

50.0

100.0

150.0

200.0

250.0

300.0

2003 2004 2005 2006H123.0

24.0

25.0

26.0

27.0

28.0

29.0

30.0

31.0

32.0

33.0

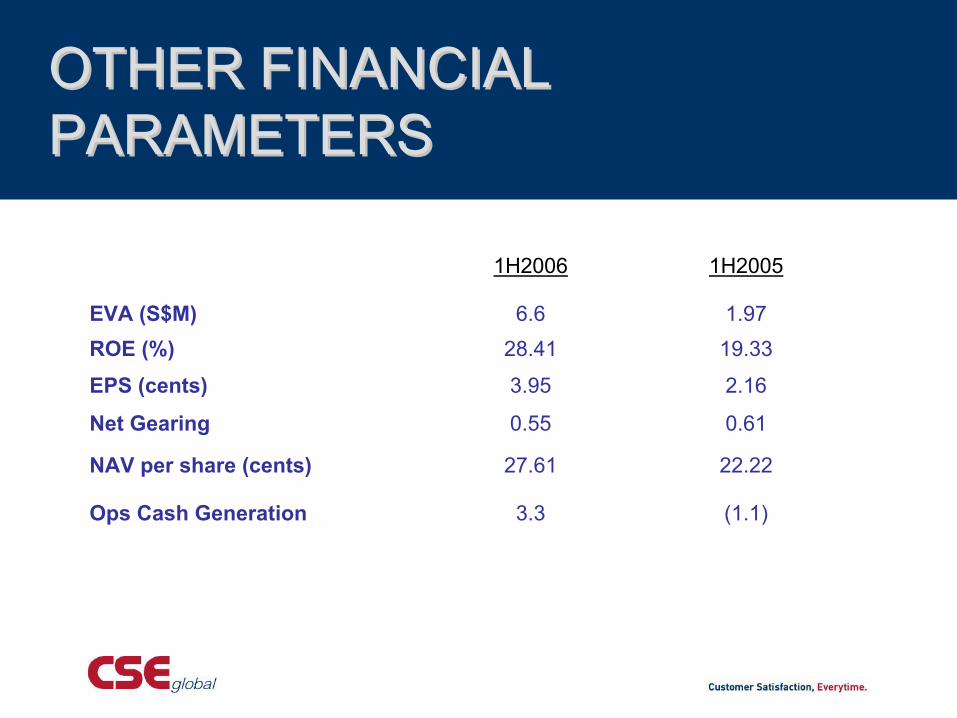

22.2227.61NAV per share (cents)

3.3

0.55

3.95

28.416.6

1H2006

(1.1)

0.61

2.16

19.331.97

1H2005

Ops Cash Generation

Net Gearing

EPS (cents)ROE (%)EVA (S$M)

OTHER FINANCIAL OTHER FINANCIAL PARAMETERSPARAMETERS

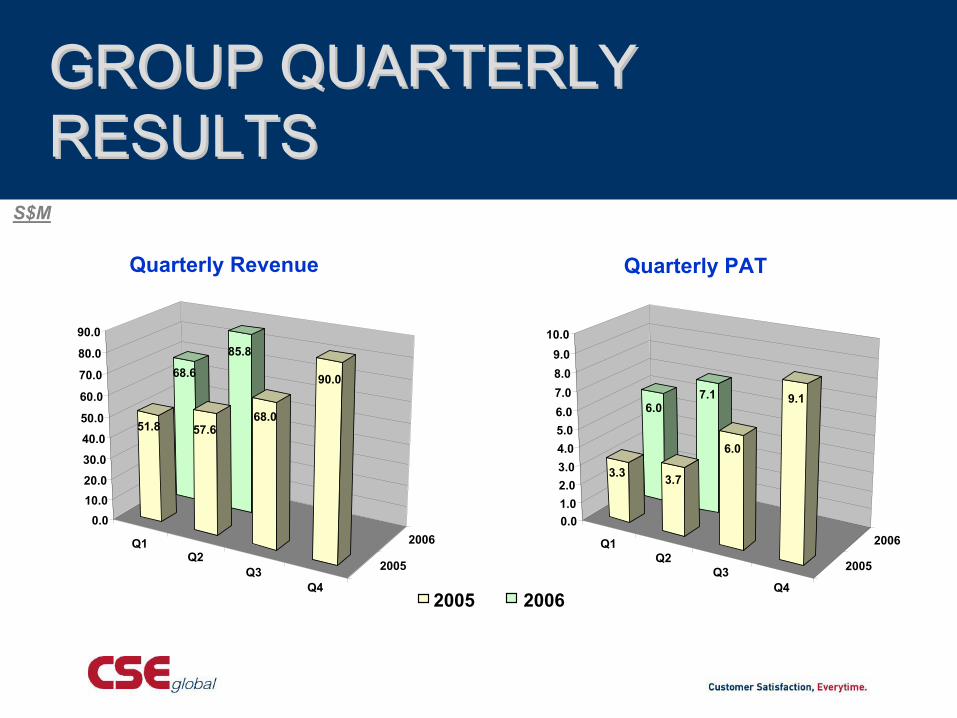

GROUP QUARTERLYGROUP QUARTERLYRESULTS RESULTS

S$M

2005 2006

Quarterly PATQuarterly Revenue

Q1Q2

Q3Q4

2005

2006

68.6

85.8

51.8 57.668.0

90.0

0.010.020.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Q1Q2

Q3Q4

2005

2006

6.07.1

3.3 3.7

6.0

9.1

0.01.02.03.04.05.06.07.08.09.0

10.0

GROUP QUARTERLY GROUP QUARTERLY ORDERSORDERS

S$M

Q4Q1 Q2 Q3

20032004

20052006

36.2

42.1

56.5

50.6

34.8

47.2

71.4

46.6

53.6

143.8

74.8

90.6

70.1

87.5

0

50

100

150

200

250

300

350

400S$M

185.4 200.0

362.8

157.6

FAVORABLE MARKET FAVORABLE MARKET DYNAMICS (OIL & GAS)DYNAMICS (OIL & GAS)

High oil & gas prices and growing world energy demand

Pipeline & Gas Journal 2005 International Pipeline ConstructionSurvey indicated 54,068 miles of oil & gas pipeline underconstruction and planned. Of these, about 80% account forprojects in planned stage and 20% represent pipelines underconstruction

A range of world scale refinery and petrochemical projectscoming to the fore-drive by strong demand, more rigorous products specifications and rising margins

Liquefied Natural Gas (LNG) is expected to play an increasingly importantrole in the global energy markets. The combination of higher natural gasprices, lower LNG costs, rising gas import demand and the desireof gas producer to monitize their gas reserve is setting the stage forincrease in LNG plant projects

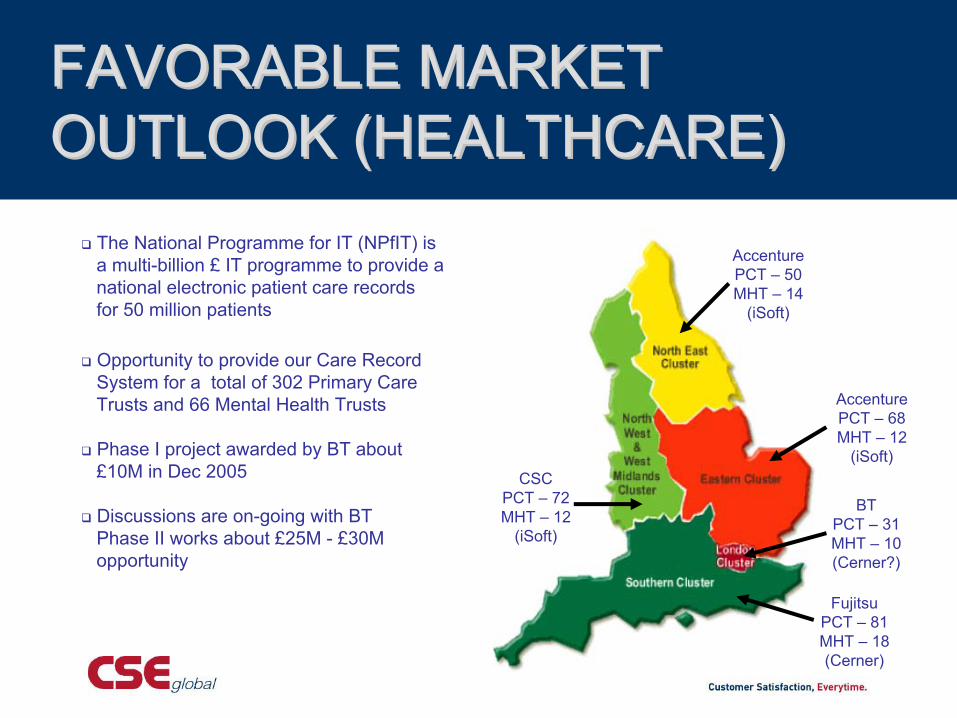

BTPCT – 31MHT – 10(Cerner?)

AccenturePCT – 50MHT – 14

(iSoft)

FujitsuPCT – 81MHT – 18(Cerner)

AccenturePCT – 68MHT – 12

(iSoft)CSC

PCT – 72MHT – 12

(iSoft)

Opportunity to provide our Care Record System for a total of 302 Primary CareTrusts and 66 Mental Health Trusts

Phase I project awarded by BT about£10M in Dec 2005

Discussions are on-going with BTPhase II works about £25M - £30Mopportunity

FAVORABLE MARKET FAVORABLE MARKET OUTLOOK (HEALTHCARE) OUTLOOK (HEALTHCARE)

The National Programme for IT (NPfIT) is a multi-billion £ IT programme to provide a national electronic patient care recordsfor 50 million patients

KEY MESSAGEKEY MESSAGE

Solid earnings and cashflow

Strengthen our global business over years

Operating and capital efficiency

Favorable market dynamic especially in the oil & gas sector

Healthcare business is expected to grow significantly in the next few yearsdue to English NHS’s NPfIT

Orders trends and prospects support another good year ahead

THANK YOUTHANK YOU